Τax Alert

7

August 2011 Tax Alert Athens, Greece New Law 4002/2011 “Amendments of the pension legislation of the public sector - Regulations for the development and fiscal restructuring – Issues within the competence of the Ministries of Finance, Culture and Tourism and Labor and Social Security” L.4002/2011 which has been recently voted by the Greek Parliament contains the following main tax provisions: Settlement of tax liabilities towards the State under favorable terms Taxpayers are granted the possibility to settle their tax liabilities towards the State under favorable terms as far as the imposition of penalties is concerned. The specific terms of this regulation can be summarized as follows: Application scope The settlement is effected by virtue of the filing of tax returns by 30 September 2011 and by virtue of the payment of the tax due under favorable terms as concerns the imposition of penalties. In specific: • Individuals and legal entities liable for income tax that have not filed a tax return or have filed an inaccurate tax return can file by 30th September 2011 initial or supplementary returns for income earned up to and including financial year 2010 without the imposition of surcharges or penalties. The filing of the tax return mentioned above has as a consequence the non imposition of the penalty of exhaustive taxation at 50%, which is applicable in case in view of prospective real estate property transfers the tax payers proceed to the late filing of tax returns for the taxation of income from rental property or from free concession of use • Taxpayers liable for the following categories of taxes can file - by 30th September 2011 and with favorable terms in relation to the imposition of surcharges (please see below) - late tax returns, the filing deadline of which has expired by the time of the introduction of the present law (i.e. 14th July 2011): L. 4002/2011 • Regulates the settlement of tax liabilities under favorable terms • Extends the application of tax settlement law 3888/2010 to a larger number of entrepreneurs • Extends for another year the statute of limitation of the State that expires on 31.12.2011 • Abolishes voluntary motive compliance provisions in the framework of regular or provisional tax audit

-

Upload

artion-conferences-events -

Category

Documents

-

view

212 -

download

0

description

Law4002/2011

Transcript of Τax Alert

August 2011

Tax AlertAthens, Greece

New Law 4002/2011

“Amendments of the pension legislation of the public sector - Regulations for the development and fiscal restructuring – Issues within the competence of the Ministries of Finance, Culture and Tourism and Labor and Social Security” L.4002/2011 which has been recently voted by the Greek Parliament contains the following main tax provisions:

Settlement of tax liabilities towards the State under favorable termsTaxpayers are granted the possibility to settle their tax liabilities towards the State under favorable terms as far as the imposition of penalties is concerned. The specific terms of this regulation can be summarized as follows:

Application scopeThe settlement is effected by virtue of the filing of tax returns by 30 September 2011 and by virtue of the payment of the tax due under favorable terms as concerns the imposition of penalties. In specific:

• Individuals and legal entities liable for income tax that have not filed a tax return or have filed an inaccurate tax return can file by 30th September 2011 initial or supplementary returns for income earned up to and including financial year 2010 without the imposition of surcharges or penalties. The filing of the tax return mentioned above has as a consequence the non imposition of the penalty of exhaustive taxation at 50%, which is applicable in case in view of prospective real estate property transfers the tax payers proceed to the late filing of tax returns for the taxation of income from rental property or from free concession of use

• Taxpayers liable for the following categories of taxes can file - by 30th September 2011 and with favorable terms in relation to the imposition of surcharges (please see below) - late tax returns, the filing deadline of which has expired by the time of the introduction of the present law (i.e. 14th July 2011):

L. 4002/2011

• Regulates the settlement of tax liabilities under favorable terms

• Extends the application of tax settlement law 3888/2010 to a larger number of entrepreneurs

• Extends for another year the statute of limitation of the State that expires on 31.12.2011

• Abolishes voluntary motive compliance provisions in the framework of regular or provisional tax audit

2 Tax Alert August 2011

a. VAT, in relation to:

− initial or amending, periodical, extraordinary or clearance VAT returns and stock returns,

− extraordinary tax returns for the payment to the State of VAT that has been unduly refunded to farmers,

− EC Listings in relation to intracommunity receipt/provision of services and acquisition/sale of goods,

− Intrastat returns.

b. Exhaustive taxation of income arising from real estate, from securities, from the transfer of business/shares/royalties, etc., from indemnity paid upon termination of employment relationship, etc.

c. Capital gains taxation from the revaluation of real estate property.

d. Turnover tax, premium tax, mobile phone subscribers’ duty and prepaid phone duty.

e. Stamp duty (with the exception of bills of exchange and promissory notes).

f. Taxes withheld or pre-paid in relation to all kind of fees, remunerations and indemnities.

g. Contributions to the Organization of Greek Agricultural Insurance (EL.G.A).

h. Capital concentration tax and special banking services tax.

i. Real estate transfer tax/automatic capital gain tax/transaction duty, inheritance/donation/parental grant or dowry tax & legal entities special real estate duty and real estate tax.

j. Any other tax, duty, contribution or withholding that is not stated above, with the exception of vehicle circulation duties.

Settlement under favorable terms

• In case of income tax:

1. Legal entities should pay the tax due in three (3) equal monthly installments, the first of which upon filing of the tax return and the remaining two up until the last working day of the two subsequent months.

2. Individuals should pay the tax due by the last working day of the month that follows the tax assessment date.

3. The filing of initial or supplementary returns will be effected without the imposition of any surcharges or fines.

• In case of the other taxes:

1. The tax should be paid either lump sum or in six (6) equal monthly installments, the first of which upon filing of the returns and each of the following installments by the last working day of the respective subsequent months. The amount of each installment cannot be less than three hundred (300) Euros, except for the last installment.

2. If the tax is paid lump sum, no surcharge is due,

3. If the tax is paid in installments, surcharges are due as follows:

− 10% in cases that the tax liability arose by December 31, 2009

− 3% in cases the tax liability arose as from January 1, 2010 onwards and the deadline for filing the return had expired by the introduction of the present law (i.e. by 14th July 2011).

In case no tax is due, no fine is imposed.

3Tax Alert August 2011

Exemptions• The following cases are excluded from the relevant provisions and are not subject to the

settlement:

− Cases where, by the time the present law enters into force, the tax assessment notes have been issued and registered in the respective conveyance registers.

− Wealth tax and property statement (E9) cases.

− Tax returns that are filed with reservation.

− Income tax returns declaring losses.

− Cases for which the process of issuance and serving of tax assessment notes has not been completed by the date of publication of the present law provided that the books and records have been judged by the respective committee of the Ministry of Finance as insufficient/inaccurate or provided that the deadline for the filing of administrative recourses has elapsed. Cases pending before the respective committee of the Ministry of Finance are also exempt.

− The submission of periodical VAT returns that relate to tax periods as from 1.1.2011 and onwards.

− Cases of entities for the audit of which Special Tax Audit Teams have been formed.

Settlement deadline• Tax payers liable for income tax as well as for the other taxes mentioned above can file

the relevant tax returns by 30th September 2011.

• By exception, tax payers that have been selected for temporary or regular tax audits by the date of publication of the new law (22nd August 2011) and who have been served with a respective written invitation to that end, can file the abovementioned returns within a deadline of ten (10) days as from the service of the said invitation and no later than by the end of the second month following the publication of the new law, i.e. no later than 31st October 2011.

Extension of application of the provisions of Law 3888/2010 (tax settlement of tax cases) to a larger number of entrepreneursThe new law grants the possibility to a larger number of entrepreneurs to be subject to the provisions of Law 3888/2010 regarding the tax settlement of years up to and including 31.12.2009 in relation both to tax unaudited years and to tax audited years which are pending before the administrative courts.

In specific:

• There is an increase of the limit of gross revenues from € 20 million to € 40 million (or the equivalent amount in drachmas) above which each unaudited year or case and all subsequent years are not subject to the tax settlement.

• For the calculation of the tax due, as gross revenues are considered: a) in the case of agricultural associations the 20% of the declared gross revenues and b) in all other cases the declared gross revenues after the deduction of revenues from the sale and lease back of own fixed equipment.

• The following cases (that were exempt by Law 3888/2010) become now subject to the tax settlement: cases of enterprises listed in the Athens Stock Exchange and cases of individual entrepreneurs who are subject to real estate taxation.

4 Tax Alert August 2011

• A deadline of five (5) days as from the serving of the relevant tax settlement Clearance Note is introduced, within which the tax payer must accept the tax settlement Clearance Note which is issued by the Greek tax office so that the tax settlement becomes effective before the start of the audit. The respective tax settlement Clearance Note can also be submitted to the tax office by the taxpayer by 31st October 2011.

• A decision of the Minister of Finance may regulate the procedure for the assessment of the taxes due, the payment terms, as well as any issues concerning the application of the relevant provisions.

Based on the above, the Law 3888/2010 on tax settlement is in force as follows:

With respect to all “pending years” up to December 31, 2009, an entrepreneur may choose to “close” them by accepting to pay for each pending year or case the tax amount calculated based on a specific formula provided for by the law. “Pending” are the years which are unaudited by the tax authorities or for which there is pending litigation before the tax courts.

Application scope• Pending years are defined as those for which up to the date of enactment of the law:

− A tax audit has not started or, if started, has not finished;

− A Tax Assessment Sheet or Findings Report has been issued but is not yet finalized;

− Are pending before either the First Instance Court or the Court of Appeal and, in the latter case, they have not been heard before the Court;

− Have already been audited but supplementary Tax Assessment Sheets have been issued or fines of Greek Tax Code of Books and Records have been imposed based on complementary data up to 31.8.2010, which either have not yet been finalized or are pending before the tax courts and have not been heard before the Court of Appeal.

• Cases which have been settled without audit by virtue of the provisions of articles 13-17 L.3296/2004 (“self-settlement”) and have been selected for audit but the latter has not started or, if started, has not finished, are also subject to the provisions of this law. For fiscal years 2008 and 2009, the settlement of these cases is possible provided that the ½ of the settlement tax, as defined below, is paid.

ExemptionsThe following cases are not subject to settlement:

• Those for which an income tax return has not been filed up to 31.08.2010 in respect of any unaudited fiscal year and all subsequent fiscal years;

• Those of the farmers of special regime;

• Those concerning fiscal years in which an entity’s gross revenues exceeded € 40 million and all subsequent fiscal years;

• Those for which supplementary returns have been filed under article 6 para.2 L.2753/1999 (i.e. in case the gross revenues of legal entities for VAT purposes are bigger than the ones declared for income tax purposes);

• Those concerning shipping taxation, real estate taxation, real estate transfer taxation and inheritance and gifts taxation;

• Those for which a special tax audit is conducted or refer to non-profit organizations;

• Those concerning fiscal years for which it derives without any doubt from a tax audit report or any official documentation violation of the Greek Tax Code of Books and Records due to issuance of false tax records and all the subsequent fiscal years.

5Tax Alert August 2011

Terms and consequences• It is possible to settle some of the unaudited fiscal years insofar as the first in line

unaudited fiscal year is settled together with its subsequent fiscal years.

• With the settlement of the unaudited years it is also possible to settle any pending provisional Tax Assessment Sheets and pending fine assessments.

• The settlement is effected through the payment of the total tax liability calculated in the relevant clearance note, without possibility of offsetting or deducting the income tax assessed based on the respective tax returns.

Calculation of settlement tax• The income tax is calculated as follows:

− The declared gross revenues are multiplied by 2% and the resulting figure is further multiplied with a specific coefficient, depending on the declared gross revenues, as follows:

Gross revenues Coefficient

Up to € 150,000 1

€ 150,001 - € 300,000 1.05

€ 300,001 – € 600,000 1.10

€ 600,001 – € 1,200,000 1.15

€ 1,200,001 – € 3,000,000 1.20

€ 3,000,001 – € 6,000,000 1.25

€ 6,000,001 and above 1.30

− The amount extracted from such calculations is subject to tax at a rate of 20%, except for SAs (AE) and Limited Liability Companies (ΕΠΕ) which are taxed at a rate of 25%.

• In case of non submission of the annual (clearance) VAT return, the above tax is further increased by 10% (and by at least € 200), whereas in case of specified infringements of the Greek Tax Code of Books and Records by 20%, 40% or 60% depending on the case. Special provisions apply in case of non declared revenues.

• The amount of tax due may not in any case be lower than:

− € 300 for entrepreneurs that are not liable to maintain accounting books or that maintain purchases only accounting books,

− € 500 (€ 700 for freelancers), for entrepreneurs maintaining revenue – expenses accounting books,

− € 700 (€ 1,000 for freelancers), for entrepreneurs maintaining double entry accounting books.

− Entrepreneurs who have received false or fictitious invoices or who have issued fictitious invoices may also settle the cases concerned by declaring such invoices to the tax authorities and paying income tax at 55% (for SAs and EPEs), or 40% (for all other entrepreneurs) on the invoice value (net from VAT). This applies to all entrepreneurs irrespective of turnover and whether they are listed on the Athens Stock Exchange or not.

6 Tax Alert August 2011

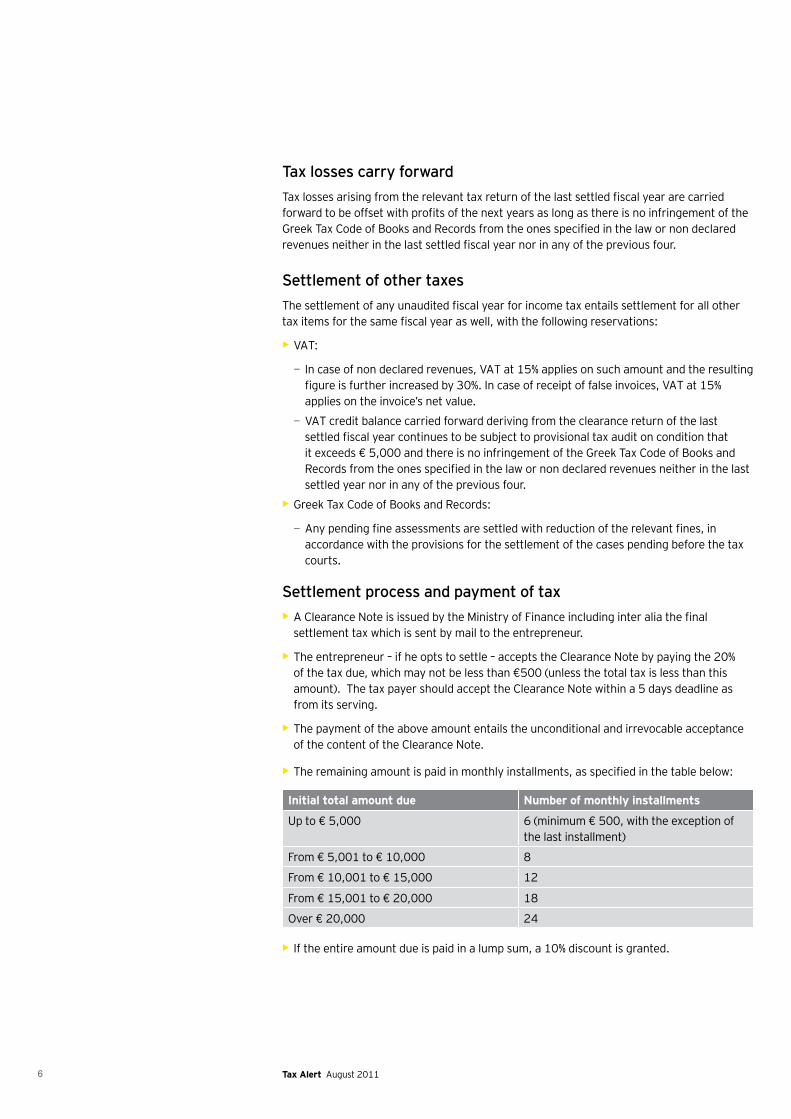

Tax losses carry forwardTax losses arising from the relevant tax return of the last settled fiscal year are carried forward to be offset with profits of the next years as long as there is no infringement of the Greek Tax Code of Books and Records from the ones specified in the law or non declared revenues neither in the last settled fiscal year nor in any of the previous four.

Settlement of other taxesThe settlement of any unaudited fiscal year for income tax entails settlement for all other tax items for the same fiscal year as well, with the following reservations:

• VAT:

− In case of non declared revenues, VAT at 15% applies on such amount and the resulting figure is further increased by 30%. In case of receipt of false invoices, VAT at 15% applies on the invoice’s net value.

− VAT credit balance carried forward deriving from the clearance return of the last settled fiscal year continues to be subject to provisional tax audit on condition that it exceeds € 5,000 and there is no infringement of the Greek Tax Code of Books and Records from the ones specified in the law or non declared revenues neither in the last settled year nor in any of the previous four.

• Greek Tax Code of Books and Records:

− Any pending fine assessments are settled with reduction of the relevant fines, in accordance with the provisions for the settlement of the cases pending before the tax courts.

Settlement process and payment of tax• A Clearance Note is issued by the Ministry of Finance including inter alia the final

settlement tax which is sent by mail to the entrepreneur.

• The entrepreneur – if he opts to settle – accepts the Clearance Note by paying the 20% of the tax due, which may not be less than €500 (unless the total tax is less than this amount). The tax payer should accept the Clearance Note within a 5 days deadline as from its serving.

• The payment of the above amount entails the unconditional and irrevocable acceptance of the content of the Clearance Note.

• The remaining amount is paid in monthly installments, as specified in the table below:

Initial total amount due Number of monthly installments

Up to € 5,000 6 (minimum € 500, with the exception of the last installment)

From € 5,001 to € 10,000 8

From € 10,001 to € 15,000 12

From € 15,001 to € 20,000 18

Over € 20,000 24

• If the entire amount due is paid in a lump sum, a 10% discount is granted.

7Tax Alert August 2011

Settlement of pending litigation irrespective of turnover• Special provisions apply for the settlement of the cases that are pending before the

tax courts, with reduction or deletion of the additional taxes and surcharges or fines depending on the litigation status of each case and the content of the First Instance Court’s decision (where applicable).

• Specifically cases that have not been yet heard to the First Instance Court may be settled with deletion of the surcharges and reduction to 1/5 of any fines.

Extension of the statute of limitationThe statute of limitation, after which the State’s right to impose taxes or fines expires, currently 31.12.2011, is extended up to 31.12.2012.

Abolishment of voluntary compliance motives As from 1st September 2011 the provisions regarding the granting of motives for the voluntary compliance are being abolished. According to the said abolished provisions, the tax payer that had been selected for provisional or regular tax audit could file initial or supplementary returns regarding income tax, VAT or other taxes, duties and contributions, with a reduction to ½ of the surcharges for the filing of late tax returns.

Ernst & Young

Assurance | Tax | Transactions | Advisory

© 2011 Ernst & Young All Rights Reserved.

This document contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

About Ernst & Young Ernst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 141,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com.

About Ernst & Young’s Tax services Your business will only achieve its true potential if you build it on strong foundations and grow it in a sustainable way. At Ernst & Young, we believe that managing your tax obligations responsibly and proactively can make a critical difference. So our 25,000 talented tax professionals in over 135 countries give you technical knowledge, business experience, consistent methodologies and an unwavering commitment to quality service — wherever you are and whatever tax services you need. It’s how Ernst & Young makes a difference.

For more information, please contact: Stefanos Mitsios Head of Tax, Ernst & Young Greece Tel.: +30 210 288 6363