AutoServ_Opportunities in the Indian Automotive Aftermarket Final

13

This report is furnished to the recipient for information purposes only. Each recipient should conduct their own investigation and analysis of any such information contained in this report. No recipient is entitled to rely on the work of McKinsey & Company, Inc. contained in this report for any purpose. McKinsey & Company, Inc. makes no representations or warranties regarding the accuracy or completeness of such information and expressly disclaims any and all liabilities based on such information or on omissions therefrom. The recipient must not reproduce, disclose or distribute the information contained herein without the express prior written consent of McKinsey & Company, Inc. Opportunities in the Indian automotive aftermarket Prepared for Auto Serve 2010, a conference on improving the productivity in the automotive aftermarket organised by the Confederation of Indian Industry Chennai, November 19 th , 2010

Transcript of AutoServ_Opportunities in the Indian Automotive Aftermarket Final

This report is furnished to the recipient for information purposes only. Each recipient should conduct their own investigation and analysis of any such information contained in this report. No recipient is entitled to rely on the work of McKinsey & Company, Inc. contained in this report for any purpose. McKinsey & Company, Inc. makes no representations or warranties regarding the accuracy or completeness of such information and expressly disclaims any and all liabilities based on such information or on omissions therefrom. The recipient must not reproduce, disclose or distribute the information contained herein without the express prior written consent of McKinsey & Company, Inc.

Opportunities in the Indian automotive aftermarket

Prepared for Auto Serve 2010, a conference on improving the productivity in the automotive aftermarket organised by the Confederation of Indian Industry

Chennai, November 19th, 2010

This report is furnished to the recipient for information purposes only. Each recipient should conduct their own investigation and analysis of any such information contained in this report. No recipient is entitled to rely on the work of McKinsey & Company, Inc. contained in this report for any purpose. McKinsey & Company, Inc. makes no representations or warranties regarding the accuracy or completeness of such information and expressly disclaims any and all liabilities based on such information or on omissions therefrom. The recipient must not reproduce, disclose or distribute the information contained herein without the express prior written consent of McKinsey & Company, Inc.

McKinsey & Company | 1

Executive Summary

The automotive aftermarket for parts in India is a large and growing market that spans manufacturers, distributors, retailers, service providers and garages. Currently worth INR 19,000 crore to INR 24,000 crore1, the market has been growing at 11 per cent, and is estimated to reach INR 39,000 crore to INR 44,000 crore by 2015. This growth will primarily be fuelled by the increasing number of vehicles on the road, as well as the aggressive expansion of independent and foreign players. While current margins for the industry remain attractive, players across the value chain may see margins reducing to the lower levels observed in developed economies. Therefore, to sustain profitability, it is imperative that players evaluate additional ways of capturing value, including expanding service networks, developing branded generic parts, forward integrating and building scale. Looking ahead, revenue pools remain large across the value chain, hence if players are able to pursue appropriate strategies, significant profits can be made in this sector.

THE INDIAN MARKET IS LARGE AND HAS SCOPE FOR FURTHER GROWTH

The Indian automotive aftermarket has been growing at a steady pace and is expected to expand rapidly over the next five years. The total size of this sector is currently estimated at USD 5 billion to USD 6 billion, while the global market is worth USD 490 billion to USD 540 billion.

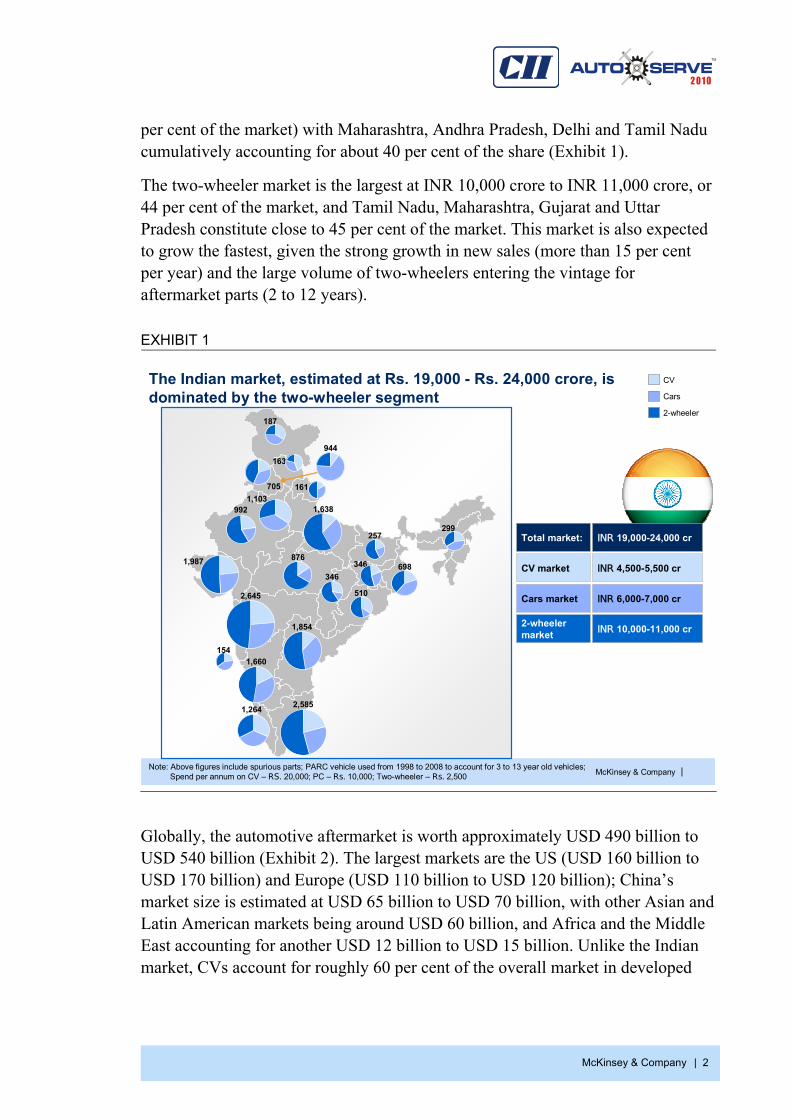

Growing market offers significant potential The Indian market is valued at INR 19,000 crore to INR 24,000 crore, of which roughly 30 per cent comprises spurious parts. Commercial vehicles (CV), which include multi-axle vehicles, light commercial vehicles (LCVs), buses and trailers account for roughly 22 per cent of this market (INR 4,500 crore to INR 5,500 crore), with Maharashtra, Tamil Nadu, Gujarat and Kerala accounting for over 40 per cent. The car market is estimated at INR 6,000 crore to INR 7,000 crore (34

1 Excludes services, which is estimated to be in the range of an additional Rs. 8,000 – Rs. 12,000 crore

McKinsey & Company | 2

per cent of the market) with Maharashtra, Andhra Pradesh, Delhi and Tamil Nadu cumulatively accounting for about 40 per cent of the share (Exhibit 1).

The two-wheeler market is the largest at INR 10,000 crore to INR 11,000 crore, or 44 per cent of the market, and Tamil Nadu, Maharashtra, Gujarat and Uttar Pradesh constitute close to 45 per cent of the market. This market is also expected to grow the fastest, given the strong growth in new sales (more than 15 per cent per year) and the large volume of two-wheelers entering the vintage for aftermarket parts (2 to 12 years).

EXHIBIT 1

McKinsey & Company |

The Indian market, estimated at Rs. 19,000 - Rs. 24,000 crore, is dominated by the two-wheeler segment

Note: Above figures include spurious parts; PARC vehicle used from 1998 to 2008 to account for 3 to 13 year old vehicles; Spend per annum on CV – RS. 20,000; PC – Rs. 10,000; Two-wheeler – Rs. 2,500

299

1,987

187

1,660

1,264

992

2,585

1,638

1,854

2,645

876

705

944

346346 698

510

257

161

163

154

CV

Cars

2-wheeler

Total market:

CV market

Cars market

2-wheeler market

INR 19,000-24,000 cr

INR 4,500-5,500 cr

INR 6,000-7,000 cr

INR 10,000-11,000 cr

1,103

Globally, the automotive aftermarket is worth approximately USD 490 billion to USD 540 billion (Exhibit 2). The largest markets are the US (USD 160 billion to USD 170 billion) and Europe (USD 110 billion to USD 120 billion); China’s market size is estimated at USD 65 billion to USD 70 billion, with other Asian and Latin American markets being around USD 60 billion, and Africa and the Middle East accounting for another USD 12 billion to USD 15 billion. Unlike the Indian market, CVs account for roughly 60 per cent of the overall market in developed

McKinsey & Company | 3

countries. The global off-road equipment market, which includes construction equipment such as cranes and rollers, as well as tractors, is roughly USD 11 billion to USD 15 billion.

EXHIBIT 2

McKinsey & Company |

The global aftermarket across CV, passenger cars and off-road is estimated at USD 490-510 billion

SOURCE: Datamonitor; AAIA Factbook; DAT; ZDK; IFA Nürtingen; AAI Factbook; US Dept. of Energy; McKinsey team; The Freedonia Group; McKinsey team analysis

USD billion, 2008

Total market: USD 490-540 billion

Total… … …

CV PC Off-road

US: 160 - 170 EU: 110 - 120

India: 5 - 6

UK: 23 - 28

MEA: 12 - 15

110 50 5

15 10 1

LatAM: 60 - 70

60 1.5

13 1

65 45 4

1 4 .5

China: 65 - 70

32 35 2

Rest of Asia: 50 - 6050 2.5

Note: CV and passenger car breakup not available for Africa/ME, South East Asia and S. America; India and China PC includes 2 Wheelers

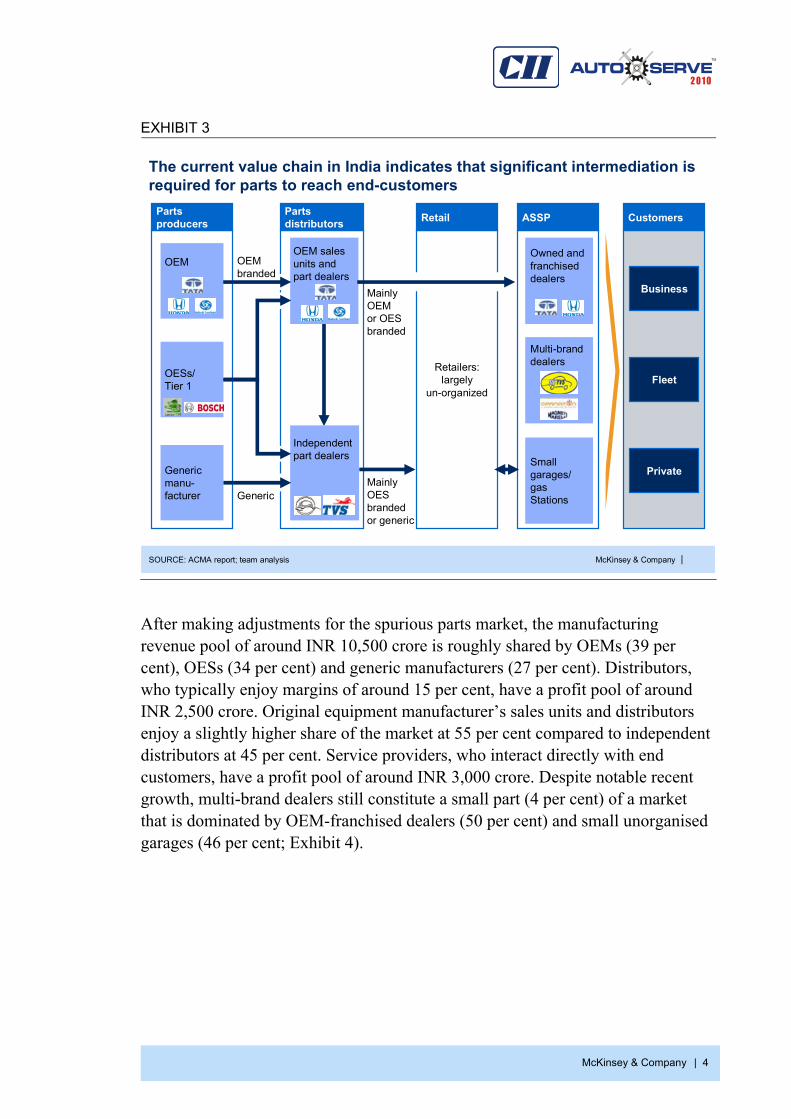

Current market structure is fragmented The value chain in India remains highly fragmented and there is a significant level of intermediation required for parts to reach end customers. The production of parts is split between original equipment manufacturers (OEM), original equipment suppliers (OES) and generic manufacturers. While OEM’s may rely on their own distribution networks, with parts being sold through directly-owned or franchised dealers, the independent channel has grown in significance in recent times. Original equipment suppliers have the advantage of being able to both directly supply OEMs, as well as go through independent distributors (Exhibit 3).

McKinsey & Company | 4

EXHIBIT 3

McKinsey & Company |

The current value chain in India indicates that significant intermediation is required for parts to reach end-customers

SOURCE: ACMA report; team analysis

Business

Fleet

Private

Generic

Mainly OEM or OES branded

Mainly OES branded or generic

Small garages/ gasStations

Retailers:largely

un-organized

Owned and franchised dealers

Multi-brand dealers

OEM sales units and part dealers

Independent part dealers

Genericmanu-facturer

OESs/Tier 1

OEM

Parts producers

Parts distributors Retail ASSP Customers

OEMbranded

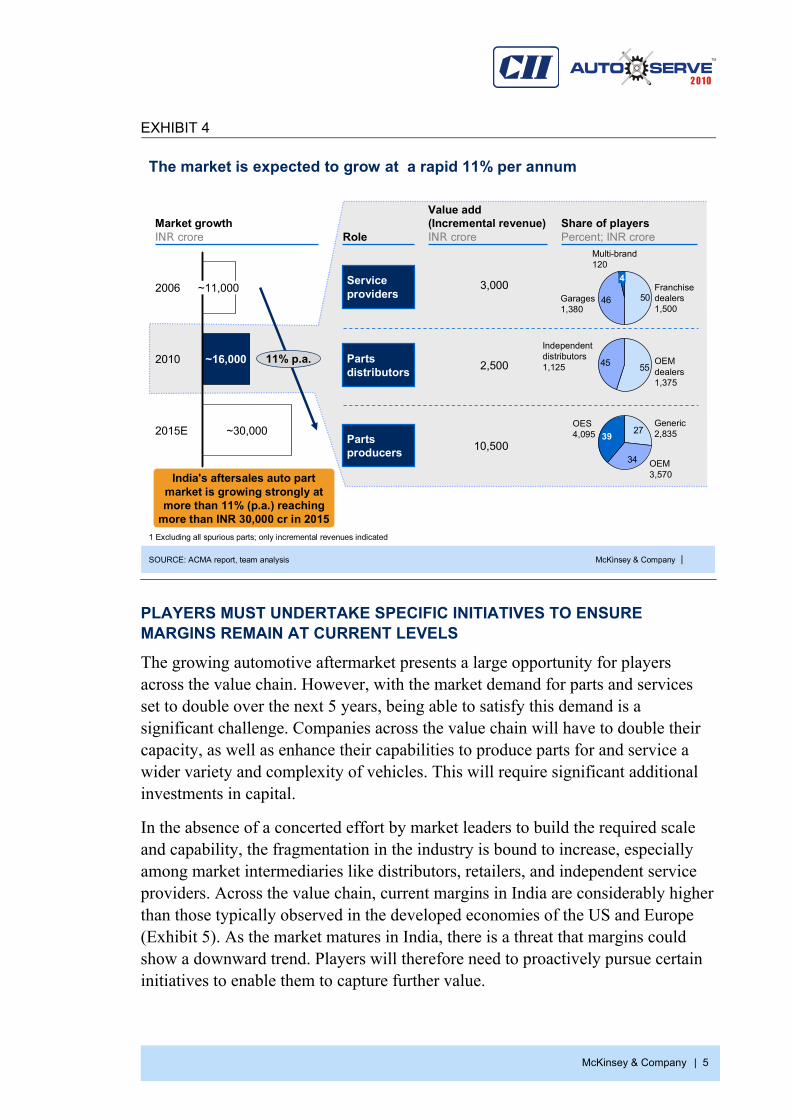

After making adjustments for the spurious parts market, the manufacturing revenue pool of around INR 10,500 crore is roughly shared by OEMs (39 per cent), OESs (34 per cent) and generic manufacturers (27 per cent). Distributors, who typically enjoy margins of around 15 per cent, have a profit pool of around INR 2,500 crore. Original equipment manufacturer’s sales units and distributors enjoy a slightly higher share of the market at 55 per cent compared to independent distributors at 45 per cent. Service providers, who interact directly with end customers, have a profit pool of around INR 3,000 crore. Despite notable recent growth, multi-brand dealers still constitute a small part (4 per cent) of a market that is dominated by OEM-franchised dealers (50 per cent) and small unorganised garages (46 per cent; Exhibit 4).

McKinsey & Company | 5

EXHIBIT 4

McKinsey & Company |

The market is expected to grow at a rapid 11% per annum

SOURCE: ACMA report, team analysis

1 Excluding all spurious parts; only incremental revenues indicated

Share of playersPercent; INR crore

Value add (Incremental revenue)INR croreRole

India's aftersales auto part market is growing strongly at more than 11% (p.a.) reaching

more than INR 30,000 cr in 2015

Market growthINR crore

11% p.a.

2015E ~30,000

2010 ~16,000

2006 ~11,000Service providers

Parts distributors

Parts producers

3,000

2,500

10,500

46 50

Multi-brand120

4

Garages1,380

Franchise dealers1,500

45 55

Independent distributors1,125

OEM dealers1,375

34

27OES4,095 39

OEM 3,570

Generic 2,835

PLAYERS MUST UNDERTAKE SPECIFIC INITIATIVES TO ENSURE MARGINS REMAIN AT CURRENT LEVELS

The growing automotive aftermarket presents a large opportunity for players across the value chain. However, with the market demand for parts and services set to double over the next 5 years, being able to satisfy this demand is a significant challenge. Companies across the value chain will have to double their capacity, as well as enhance their capabilities to produce parts for and service a wider variety and complexity of vehicles. This will require significant additional investments in capital.

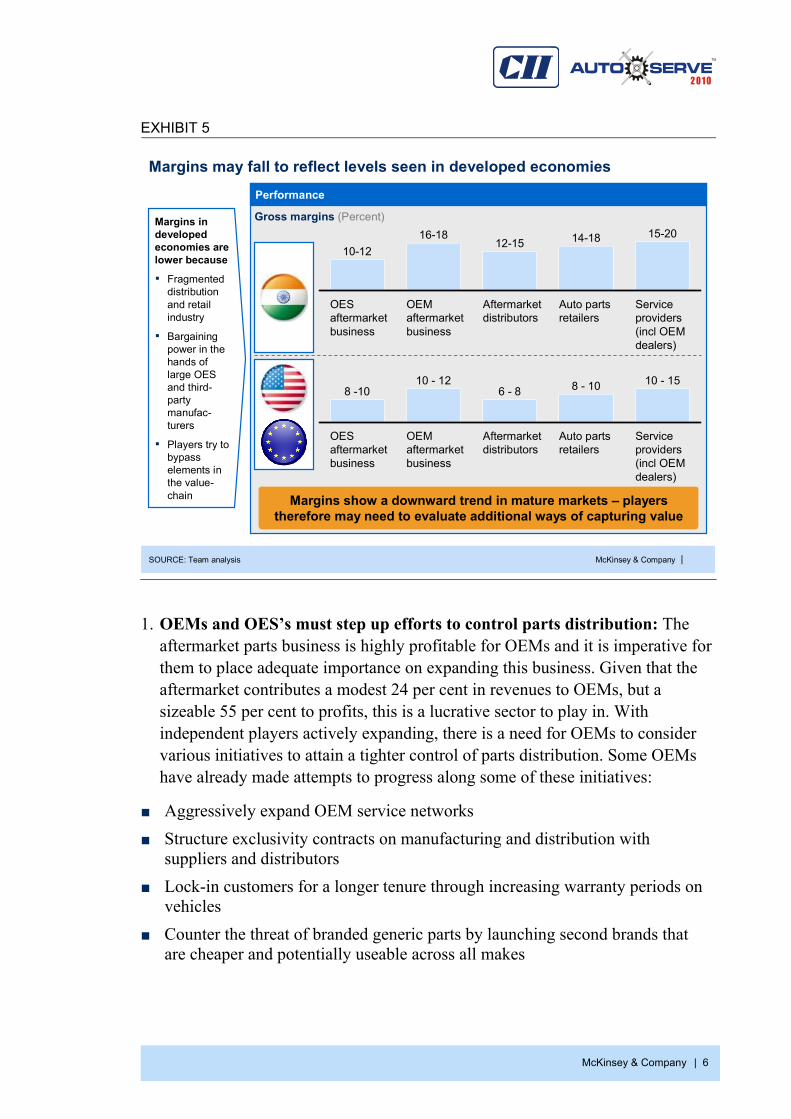

In the absence of a concerted effort by market leaders to build the required scale and capability, the fragmentation in the industry is bound to increase, especially among market intermediaries like distributors, retailers, and independent service providers. Across the value chain, current margins in India are considerably higher than those typically observed in the developed economies of the US and Europe (Exhibit 5). As the market matures in India, there is a threat that margins could show a downward trend. Players will therefore need to proactively pursue certain initiatives to enable them to capture further value.

McKinsey & Company | 6

EXHIBIT 5

McKinsey & Company |

Margins may fall to reflect levels seen in developed economies

Margins in developed economies are lower because

▪ Fragmented distribution and retail industry

▪ Bargaining power in the hands of large OESand third-party manufac-turers

▪ Players try to bypass elements in the value-chain

Performance

Gross margins (Percent)

Service providers(incl OEM dealers)

15-20

Auto partsretailers

14-18

Aftermarket distributors

12-15

OEM aftermarket business

16-18

OESaftermarket business

10-12

Service providers(incl OEM dealers)

10 - 15

Auto partsretailers

8 - 10

Aftermarket distributors

6 - 8

OEM aftermarket business

10 - 12

OESaftermarket business

8 -10

Margins show a downward trend in mature markets – players therefore may need to evaluate additional ways of capturing value

SOURCE: Team analysis

1. OEMs and OES’s must step up efforts to control parts distribution: The aftermarket parts business is highly profitable for OEMs and it is imperative for them to place adequate importance on expanding this business. Given that the aftermarket contributes a modest 24 per cent in revenues to OEMs, but a sizeable 55 per cent to profits, this is a lucrative sector to play in. With independent players actively expanding, there is a need for OEMs to consider various initiatives to attain a tighter control of parts distribution. Some OEMs have already made attempts to progress along some of these initiatives:

■ Aggressively expand OEM service networks ■ Structure exclusivity contracts on manufacturing and distribution with

suppliers and distributors ■ Lock-in customers for a longer tenure through increasing warranty periods on

vehicles ■ Counter the threat of branded generic parts by launching second brands that

are cheaper and potentially useable across all makes

McKinsey & Company | 7

■ Create awareness through promotions on the use of original spare parts, and tie up with insurance providers, to ensure higher off-take of original spares.

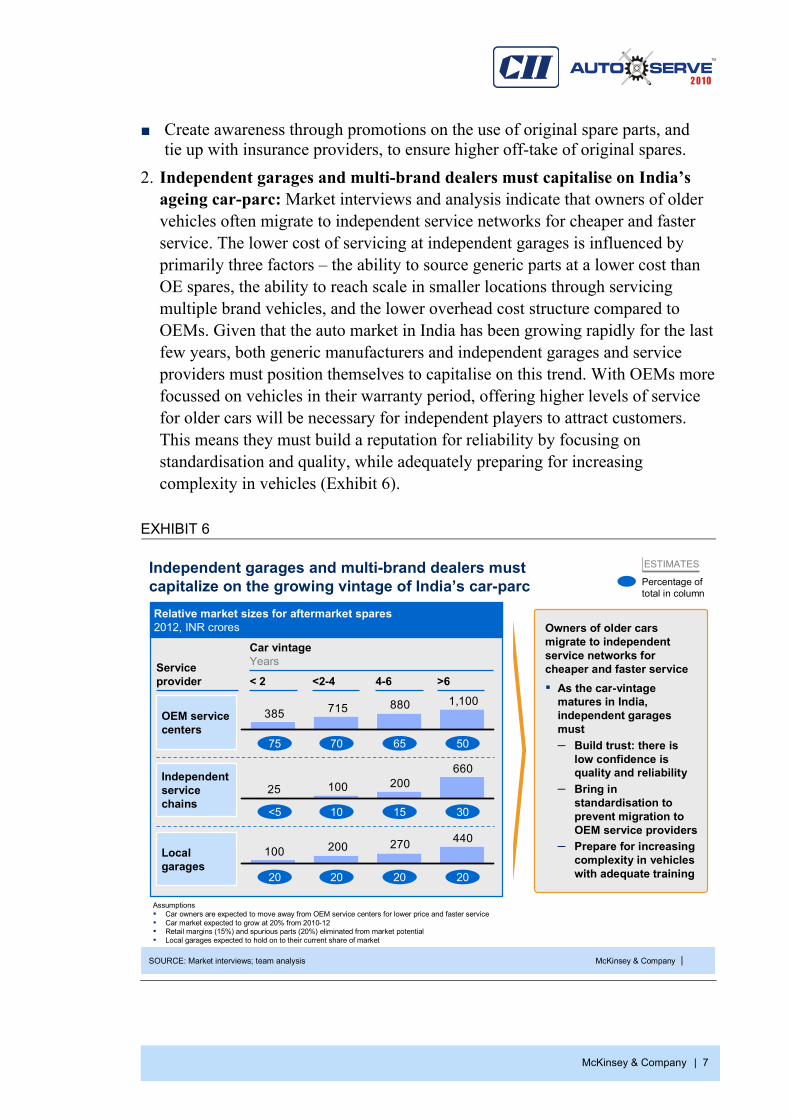

2. Independent garages and multi-brand dealers must capitalise on India’s ageing car-parc: Market interviews and analysis indicate that owners of older vehicles often migrate to independent service networks for cheaper and faster service. The lower cost of servicing at independent garages is influenced by primarily three factors – the ability to source generic parts at a lower cost than OE spares, the ability to reach scale in smaller locations through servicing multiple brand vehicles, and the lower overhead cost structure compared to OEMs. Given that the auto market in India has been growing rapidly for the last few years, both generic manufacturers and independent garages and service providers must position themselves to capitalise on this trend. With OEMs more focussed on vehicles in their warranty period, offering higher levels of service for older cars will be necessary for independent players to attract customers. This means they must build a reputation for reliability by focusing on standardisation and quality, while adequately preparing for increasing complexity in vehicles (Exhibit 6).

EXHIBIT 6

McKinsey & Company |

Independent garages and multi-brand dealers must capitalize on the growing vintage of India’s car-parc

SOURCE: Market interviews; team analysis

Owners of older cars migrate to independent service networks for cheaper and faster service▪ As the car-vintage

matures in India, independent garages must– Build trust: there is

low confidence is quality and reliability

– Bring in standardisation to prevent migration to OEM service providers

– Prepare for increasing complexity in vehicles with adequate training

ESTIMATES

Percentage of total in column

Relative market sizes for aftermarket spares2012, INR crores

Assumptions▪ Car owners are expected to move away from OEM service centers for lower price and faster service▪ Car market expected to grow at 20% from 2010-12▪ Retail margins (15%) and spurious parts (20%) eliminated from market potential▪ Local garages expected to hold on to their current share of market

OEM service centers

Independent service chains

Service provider

Car vintageYears

<2-4 4-6

Local garages

1,100880715385

66020010025

440270200100

75 70 65 50

<5 10 15 30

20 20 20 20

>6< 2

McKinsey & Company | 8

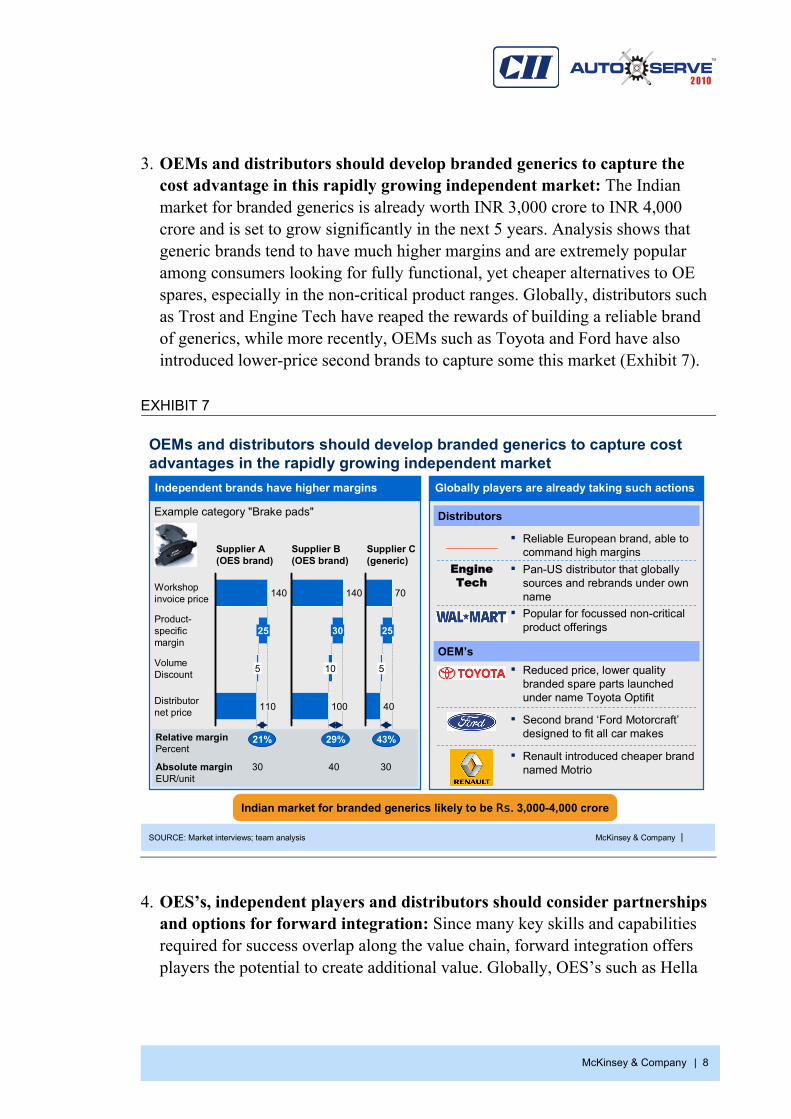

3. OEMs and distributors should develop branded generics to capture the cost advantage in this rapidly growing independent market: The Indian market for branded generics is already worth INR 3,000 crore to INR 4,000 crore and is set to grow significantly in the next 5 years. Analysis shows that generic brands tend to have much higher margins and are extremely popular among consumers looking for fully functional, yet cheaper alternatives to OE spares, especially in the non-critical product ranges. Globally, distributors such as Trost and Engine Tech have reaped the rewards of building a reliable brand of generics, while more recently, OEMs such as Toyota and Ford have also introduced lower-price second brands to capture some this market (Exhibit 7).

EXHIBIT 7

McKinsey & Company |

OEMs and distributors should develop branded generics to capture cost advantages in the rapidly growing independent market

Distributors

OEM’s

▪ Reliable European brand, able to command high margins

Engine Tech

▪ Pan-US distributor that globally sources and rebrands under own name

▪ Popular for focussed non-critical product offerings

▪ Reduced price, lower quality branded spare parts launched under name Toyota Optifit

▪ Second brand ‘Ford Motorcraft’designed to fit all car makes

▪ Renault introduced cheaper brand named Motrio

Indian market for branded generics likely to be Rs. 3,000-4,000 crore

Example category "Brake pads"

Supplier A(OES brand)

Supplier B (OES brand)

Relative marginPercent

Absolute marginEUR/unit

110Distributor net price

Volume Discount 5

Product-specificmargin

25

Workshop invoice price 140

21%

100

10

30

140

29%

30 30

Supplier C (generic)

40

40

5

25

70

43%

SOURCE: Market interviews; team analysis

Independent brands have higher margins Globally players are already taking such actions

4. OES’s, independent players and distributors should consider partnerships and options for forward integration: Since many key skills and capabilities required for success overlap along the value chain, forward integration offers players the potential to create additional value. Globally, OES’s such as Hella

McKinsey & Company | 9

(direct distribution through Hella Logistics Center) and Bosch (Bosch Car Service, 1a Autoservice) have successfully acted as parts distributors and even service providers. In India too, Bosch has successfully built an extensive distribution network. Independent parts distributors must also actively look for opportunities to act as service providers and retailers. Such a move will allow distributors to increase their bargaining power since they can provide suppliers with a ready market for their parts. Most American distributors already have retail arms, while many European distributors such as Stahlgruber and Europart partner with retail outlets such as Meisterhaft and AC Autocheck. In India, TVS distribution has already made efforts to forward integrate through PartSmart and MyTVS. Forward integration may be crucial going forward as it enables market leaders to tap into additional revenue sources, as well as build significant entry barriers for new competition.

5. Independent distributors should consider building scale, expanding globally and sourcing from low-cost countries: While global trends and the complex nature of the Indian market indicate independent distributors are going to remain valuable components of the value chain , it is imperative that they build scale in order to counter the threat of exclusivity from OEMs, OESs and the risk of displacement by logistics providers. Furthermore, distributors will need to build scale by building large own-brand portfolios, sourcing from other low-cost countries, and looking for opportunities to expand internationally. Globally, distributors have been trying to achieve relevant scale, with the top 10 distributors both in the US and Europe having a minimum of around USD 200 million in revenues. The recent spurt in merger and acquisitions (M&A) activities among distributors in these geographies are also markers to their attempts to gain significance through scale.

SIGNIFICANT PROFITS CAN BE MADE IF PLAYERS ALONG THE VALUE CHAIN ADOPT THE APPROPRIATE STRATEGIES

Several favourable trends will positively impact the Indian automotive aftermarket in the years ahead. However, all players remain susceptible to certain risks and so will need to focus on implementing key imperatives in order to enjoy high margins and growing profits.

While increasing customer affluence and an already well-established network give OEMs a sound starting position, they must continue to create barriers to entry for independent players by expanding networks, demanding exclusivity and increasing warranty periods. Similarly, despite the unique position of OESs that enables them to ride off the success of both OEMs and independent distributors, it is vital they

McKinsey & Company | 10

seize opportunities to forward integrate along the value chain. The growing number of parts suitable for manufacturing by generic players and the increasing vehicle parc (especially in rural India) puts generic manufacturers and independent garages in a very attractive position. However, the focus must increasingly shift towards quality and reliability as customer expectations grow. Independent distributors, a vital element in the value chain, also face threats from OESs and must therefore look to build scale through forward integration, creation of generic brands and global sourcing.

□ □ □

The Indian automotive aftermarket is at an inflection point – vehicle parc is increasing, parts are getting more complex, customers are more price sensitive, and global suppliers are expanding their sourcing and distribution presence in India. Scaling up capacity to service the growing demand will be a challenge for Indian companies across the value chain, especially with margins likely to come under pressure. Overall, the industry revenue pools will significantly increase, and players who adapt their business models to the changing scenario, are likely to emerge as winners.

Umang Dua Ramesh Mangaleswaran Consultant, McKinsey & Company Director, McKinsey & Company Ananth Narayanan Srivatsan Sridhar Partner, McKinsey & Company Engagement Manager, McKinsey & Company