Autopistas de Puerto Rico y - Electronic Municipal Market ...

19

pwc Autopistas de Puerto Rico y Compania, S.E. Reports and Financial Statements December 31, 2011 and 2010

Transcript of Autopistas de Puerto Rico y - Electronic Municipal Market ...

pwc

Autopistas de Puerto Rico y Compania, S.E. Reports and Financial Statements December 31, 2011 and 2010

pwc

Report of Independent Auditors

To the Partners of Autopistas de Puerto Rico y Campania. S.E.

In our opinion, the accompanying balance sheets and the related statements of operations. of changes in partners' deficit, and of cash flows present fairly, in all material respects, the financial position of Autopistas de Puerto Rico y Campania, S.E. (the "Partnership") at December 31 , 2011 and 2010, and the results of its operations and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America. These financial statements are the responsibility of the Partnership's management Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these statements in accordance with auditing standards generally accepted in the United States of America. Those standards requite that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that OUt audits provide a reasonable basis for our opinion.

Our audits were conducted for the purpose of forming an opinion on the basic financial statements taken as a whole. The accompanying schedule of changes in sinking funds held by trustee is presented for purposes of additional analysis and is not a required part of the basic financial statements. Such information has been subjected to the auditing procedures applied in the aud its of the basic financial statements and, in our opinion, is fairly stated in all material respects in relation to the basic financial statements taken as a whole.

Apnl 3D, 2012

CERTIFIED PUBLIC ACCOUNTANTS (OF PUERTO RICO) I.lcell$e No. 216 Expires Uec. 1 2013 Stamp E24871 of the P .R. Society of Ce~ PLlblic Acc.ounlants has been affixed 10 the file copy of this repcn

I'ric~wat~rhoUSeC(Xl/K'rs 1.1,P,:!..54 MU/lm~ Rivera, BBVA 7i)wcr, Suite 9Of), Sall ./uolI, PR 00918 T' (787) 7,S·l g090 , F: (; 10171 766 /094 . www.pwc.com/us

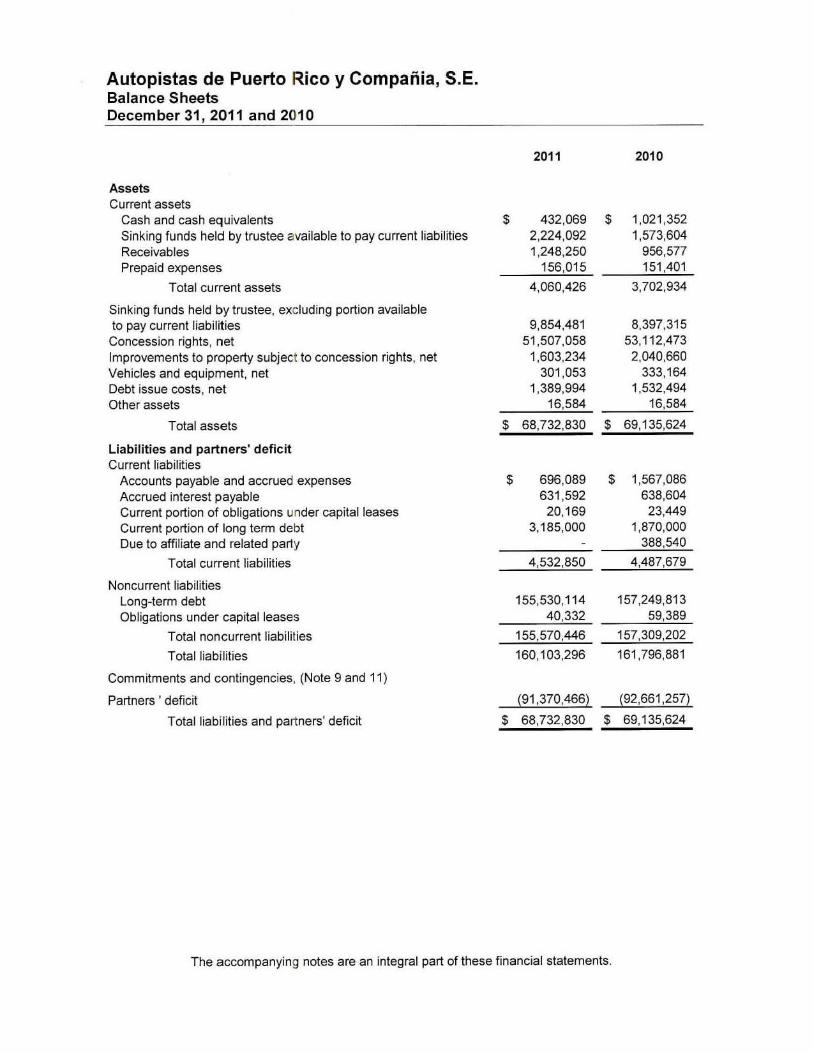

Autopistas de Puerto Rico y Compania, S.E. Balance Sheets December 31, 2011 and 2010

2011 2010

Assets Current assets

Cash and cash equivalents $ 432 ,069 $ 1,021,352 Sinking funds held by trustee available to pay current liabilities 2 ,224 ,092 1,573,604 Receivables 1,248,250 956,577 Prepaid expenses 156,015 151,401

Total current assets 4,060,426 3,702 ,934

Sinking funds held by trustee, excluding portion available to pay current liabilities 9,854,481 8,397 ,315

Concession rights , net 51.507,058 53,112,473

Improvements to property subject to concession rights , net 1,603,234 2,040,660 Vehicles and equipment , net 301,053 333,164 Debt issue costs, net 1,389,994 1,532,494

Other assets 16,584 16,584

Total assets $ 68,732 ,830 $ 69,135,624

Liabili ties and partners' deficit Current liabilities

Accounts payable and accrued expenses $ 696 ,089 $ 1,567,086

Accrued interest payable 631 ,592 638,604

Current portion of obligations under capital leases 20,169 23 ,449 Current portion of long term debt 3,185,000 1,870,000

Due to affil iate and related par1y 388,540

Total current liabilities 4,532,850 4,487 ,679

Noncurrent liabilities Long-term debt 155,530,114 157,249,813

Obligations under capital leases 40,332 59,389

Total noncurrent liabilities 155,570,446 157,309,202

Totalliabflilies 160,103,296 161,796,881

Commitments and contingencies, (Note 9 and 11 )

Partners' deficit (91 ,370,466) (92,661 ,257)

Total liabilities and partners' deficit $ 68,732 ,830 $ 69,135,624

The accompanying notes are an integral part of these financial statements.

Autopistas de Puerto Rico y Compania, S.E. Statements of Operations Year Ended December 31 , 201 1 and 2010

2011 2010

Revenues ToU revenue, net $ 18.145.890 $ 18.365.309

Operati ng expenses Depreciation and amortization 2.137,083 2,196,027 Salaries and employee benefits 1.233.576 1,671 ,988 Outside services 2,358,126 1,617,860 Insurance 370,033 404,747 Maintenance and utilities 310,229 326,11 3 Other operating and administrative expenses 754,806 1,480,970

Total operating expenses 7,163,853 7,697,705

Operating income 10,982,037 10,667,604

Other income (expense) Interest expense (9,234,215) (9,216,329) Interest income 1,833 2,245 Other income 541 ,136

Tolal olher expense, net (8,691 ,246) (9,214 ,084)

Net income $ 2,290,791 $ 1,453.520

The accompanying notes are an integral part of Ihese financial statements.

Autopistas de Puerto Rico y Compania, S.E. Statement of Changes in Partners' Deficit Year Ended December 31 , 2011 and 2010

Supra and Company, S.E.

Balance at December 31 , 2009 S (23.543.356)

Transfer of interest between Partners 23 .543.356 Stock-based compensation Net income

Balance at December 31 , 2010 Partner distribution Net income

Balance at December 31 , 2011 5

Abertis Infraestructuras,

SA

$ (70.629.635) $

(23.543 .356) 58 ,214

1,453,520

(92,661,257) (1,000,000) 2,290,791

$ (91 ,370,466) $

The accompanying notes are an integral part of these financial statements.

Tota l Partners'

Deficit

(94.172.991)

58,214 1.453,520

(92,661,257) (1,000,000) 2,290,791

(91,370,466)

Autopistas de Puerto Rico y Compania, S.E. Statements of Cash Flows Year Ended December 31 , 2011 and 2010

2011 2010

Cash flows from operating activities Net income Adjustments to reconcile net income to net cash provided by operating activities

Depreciation and amortization Amortization of debt issue costs Siock-based compensation Accretion of interest Interest earned on sinking funds held by trustee loss on disposal of fixed assets Changes in operating assets and liabilities that increase (decrease) cash

Receivables Prepaid expenses Book overdraft Accounts payable, accrued expenses and accrued interest payable Due to affiliate and related party Deferred revenue

Total adjustments

Net cash provided by operating activities

Cash flows from investing activities Deposits to sinking funds held by trustee Withdrawals from sinking funds held by trustee Capital expenditures

Net cash used in investing activities

Cash flows from financing activ ities Distributions to partners Repayments of long-term debt Obligations under capital leases Repayments of obligations under capital leases Repayments of cash advances from partners

Net cash used in financing activities

Net increase (decrease) in cash and cash equivalents Cash and cash equivalents at beginning of year

Cash and cash equivalents at end of year

$ 2 ,290,791

2.137.083 142,500

1,465,301 (1 .133)

(291,673) (4,614)

(878.009) (388.540)

2,180 ,915

4,471,706

(17.437,236) 15,330,715

(62,131)

(2 ,168,652)

(1.000,000) (1 ,870 .000)

(22 ,337)

(2.892,337)

(589,283) 1,021 ,352

$ 432 ,069

The accompanying notes are an integral part of these financial statements.

$ 1,453,520

2,196,285 144,871

58 ,214 1,381 ,569

(893) 20,175

(81.735) 58,361

(29,687) 899 .236

(153,689) (129,821)

4,362,886

5,816,406

(17,829.516) 13,959.669

(211.652)

(4.081.499)

(990.000) 89,126

(70,321 ) (13,376)

(984,571)

750 .336 271 ,016

S 1,021,352

Autopistas de Puerto Rico y Compaiiia, S.E. Notes to Financial Statements December 31,2011 and 2010

1. Organization

Autopistas de Puerto Rico y Campania, S.E. ("Autopistas· or the ·Partnership"), is a special partnership organized on March 20, 1991 , under the laws of the Commonwealth of Puerto Rico, for the purpose of designing, financing, constructing, operating. and maintaining toll roads, bridges , highways, or other public works under an administrative concession, lease, franchise, or similar arrangement with the Commonwealth of Puerto Rico.

From inception through February 23, 1994, Autopistas was engaged in the design and supervision of the construction of the Teodoro Moscoso Bridge Expressway (the "Facility"). On April 1. 1992, initial financing was provided by the Puerto Rico Highway and Transportation Authority (the "Authority") (an instrumentality of the Commonwealth of Puerto Rico) by lending the proceeds from the issuance of bonds aggregating approximately $116,753,000 to Autopistas through a loan agreement. On October 22, 2003, the Authority issued and sold the Special Facility Revenue Refunding Bonds, 2003 Series A (Teodoro Moscoso Bridge) (the "2003 Bonds") amounting to $153,222,270. The proceeds from the sale of the 2003 Bonds were loaned by the Authority to Autopistas through a loan agreement for the purpose of defeasing previous bonds (see Note 7). Since February 23, 1994, Autopistas has operated the Facil ity in accordance with the concession agreement as amended in September 3, 2009 and discussed in Note 6. The operation of the Facility is the only business activity Autopistas had for the years ended December 31 , 2011 and 2010.

The partners of Autopistas are Abertis Infraestructuras, SA ('Abertis"), a company organized under the laws of Spain, which has a 99.9% interest in Autopistas, and Autopistas Corporation, a Puerto Rico corporation wholly-owned by Abertis , which acts as Autopistas' managing partner and owns the remaining interest in the Partnership.

On March 19, 2010, Abertis acquired the 24.99% interest in the Partnership previously held by Supra and Company, S.E. ("Supra").

2. Summary of Significant Accounting Polic ies

Use of Estimates The preparation of the financial statements requires management to make a number of estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates.

Cash and Cash Equivalents Cash and cash equivalents include cash on hand, time and certificate of deposits with maturities of three months or less. At December 31, 2011 and 2010, Autopistas had time deposits of $8,989 and $8.999, and certificates of deposit of $141,110 and $140,689, respectively.

Vehicles and Equipment, Net Vehicles and computer, office, and maintenance equipment are carried at cost less accumulated depreciation. Depreciation is provided using the straight-line method over the estimated useful lives of the related assets. Useful lives range from one to ten years , The balance is net of accumulated depreciation of $492,978 and $416.194 in 2011 and 2010. respectively. Maintenance and repairs are charged to expense as incurred.

1

Autopistas de Puerto Rico y Compaiiia, S.E. Notes to Financial Statements December 31 , 2011 and 2010

Concession Rights Concession rights consist of costs incurred in the development of the Facility, including design, construction, net construction period interest. other financing costs . and other costs associated with the Facility prior to commencement of operations on February 23, 1994. These costs, aggregating approximately $104,234,000 are being amortized using the straight-line method commencing on February 23, 1994 over the remaining term of concession agreement further described in Note 6. The balance is net of accumulated amortization of $52,727,638 and $51 .122,224 at December 31 , 2011 and 2010, respectively.

Improvements to Proper1y Subject to Concession Rights Improvements to property subject to concession rights represent the cost of improvements to the Facility, which are stated at cost , and are being amortized over a period of 10 years using the straight-line method. The balance is net of accumulated amortization of $2,189,982 and $1 ,735,098 in 2011 and 2010, respectively.

Sinking Funds Held by Trustee As the ultimate recipient of the proceeds from the Authority's bond issuance and pursuant to a loan agreement (see Note 7), Autopistas is required to remit all collections from the operation of the Facility to a trustee. Funds held by the trustee , invested principally in short-term certificates of deposit and fixed income governmental securities funds, are used to service Autopistas ' debt with the Authority, maintain certain required reserves, and pay for the operating expenses of the Facility. Investments held by the trustee are carried at cost, which approximates fair market value .

Impairment or Disposal of Long-lived Assets Autopistas reviews long-lived assets for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable . Recoverability of assets to be held and used is measured by a comparison of the carrying amount of an asset to future net cash flows expected to be generated by the asset. If the carrying amount of an asset exceeds its estimated future cash flows, an impairment charge is recognized by the amount by wh ich the carrying amount of the asset exceeds the fair value of the asset. Assets to be disposed of are reported at the lower of the carrying amount or fair value less costs to sell.

Toll Revenue Toll revenue is accounted for using the accrual basis of accounting based on usage of the Facility and established rates.

Autopistas has an agreement with the Authority for the electronic toll collection system -Autoexpreso". Under this agreement, Autopistas receives the Autoexpreso toll revenue net of a 5% commission , for administrative charges, from the Authority based on daily receipts of Autoexpreso users. Revenues from Autoexpreso are presented net of this commission . For the year ended at December 31 , 2011 and 2010 commissions kept by the Authority related to Autoexpreso amounted to $482,595 and $406,823, respectively.

Debt Issue Costs Debt issue costs consist of costs incurred as a result of the refinancing of debt, which occurred in October 22, 2003 (see Note 7). These costs are being amortized using a method that approximates the interest method over the life of the debt issue. The balance is net of accumulated amortization of $1 ,177,792 and $1 ,035,291 at December 31 , 2011 and 2010, respectively.

2

Autopistas de Puerto Rico y Compania, S.E. Notes to Financial Statements December 31,2011 and 2010

Income Taxes Autopistas is not taxable for Puerto Rico income tax purposes pursuant to the special partnersh ip election submitted to and approved by the Department of the Treasury of Puerto Rico. Instead, the partners report their distributive share in the profits and losses in their income tax return.

3. Receivables

Receivables at December 31 , 2011 and 2010 consist of the following :

Toll usage Other

Total

201 1 2010

$ 1,238,178 $ 945.981 10,072 10,596

$ 1,248,250 ..::$_...;9",5",6,;:.57",7_

4. Related·Party Transactions

5.

During the year ended December 31, 2011 and 2010, certain partners and affiliates charged approximately $1 ,340,000 and $243,000, respectively, for management and administrative services. Amounts due for these services at December 31 , 2011 and 2010 aggregating $0 and $200,000, net of a receivable amount of $0 and $19,320, respectively. are expected to be settled in the normal course of business.

Additionally, the Partnership had a balance due to a related party (by common management) related to promotional expenses paid on their behalf. Amounts due were $244.991 at December 31 , 2010. net of receivables of $37.131 . In 2011 the balance was paid .

On 2011 and 2010 the Partnership has an irrevocable standby letter of credit in the amount of $8 million in connection with the funding of the reserve requirement provided by the 2003 Bonds (Notes 5 and 7 ). As of December 31 . 2011 and 2010 this letter was secured by Banco Santander SA Madrid . At December 31 , 2011 and 2010, no balance was outstanding .

Sinking Funds Held by Trustee

Sinking funds held by trustee at December 31,2011 and 201 0 consist of the following :

201 1 2010

Company Reserve Fund $ 11 ,987 $ 11.986 Reserve Fund 2,500,798 2.500,528 Bond Service Fund 1.327.262 779,250 General Fund 7,233,1 19 5.002.148 Renewal and Replacement Fund 378,160 228.127 Revenue Fund 627,247 1,448,880

Total 12,078,573 9,970,919

Less amount to be used to settle current accrued interest payable and current prinCipal balance (2,224.092) (1,573 ,604)

Noncurrent sink ing funds held by trustee $ 9,854,481 $ 8.397.315

3

Autopistas de Puerto Rico y Compaiiia, S.E. Notes to Financial Statements December 31 , 2011 and 2010

All moneys held in the sinking funds are invested in U.S. treasury noles, bearing interest at 0.01 % at December 31, 2011 and 2010.

On October 1, 2003. the Authority and Banco Popular de Puerto Rico (the "Trustee") entered into a trust agreement (the "Trust") whereby the duty of the Trustee is , on or before the lasl day of each month, to withdraw from the Revenue Fund an amount equal to the sum of all moneys then held to the credit of the Revenue Fund, transfer to Autopislas a sum equal to the amount of current expenses set forth in the annual budget for the next month, and deposit the remainder of the sum to the credit of the following funds in the following order: Bond Service Fund, Redemption Fund, Reserve Fund, Renewal and Replacement Fund, and the General Fund.

The funds comprising the sinking funds held by the Trustee for the 2003 Bonds were created for the following purposes:

Company Reserve Fund The Company Reserve Fund represents a special fund created and designated by the provisions of Section 509(b) of the Trust. The moneys in the Company Reserve Fund shall be held by the Trustee and shall not be subject to any security interest, lien, and charge in favor of the holders of the 2003 Bonds, the Trustee, or the Authority. The moneys held to the credit of the Company.

Reserve Fund shall not be available to pay any amounts payable in connection with the operation of the Facility, make any deposits to the various funds or to pay the principal of or interest or premium, if any, on the 2003 Bonds.

Autopistas shall have the right, subject to satisfaction of its prior obligations under the loan agreement, to deposit moneys to the credit of the Company Reserve Fund from its own funds or from funds available for distribution to its partners . Unless and until such time, as the balance then to credit of the Reserve Fund is less than $4 million the Trustee is hereby authorized and directed to follow the written instructions of Autopistas regarding application of moneys then to the credit of the Company Reserve Fund, including instructions to the Trustee to transfer all or any part of the monies then to the credit of the Company Reserve Fund to Autopistas or to the Reserve Fund and in such latter case to reduce the stated amount, in whole or in part, of any reserve account letter of credit or reserve account Insu rance policy, to the extent that after any such transfer and reduction, the balance to the credit of the Reserve Fund shall not be less than S4 million. Upon the balance in the Reserve Fund falling (and for so long as such balance shall remain) below $4 million, the Trustee shall withdraw from the Company Reserve Fund and deposit to the credit of the Reserve Fund such amount thereof (or the entire balance of the Company Reserve Fund if less than the required amount) as may be required to make the amount then to the credit of the Reserve Fund equal $4 million.

Reserve Fund The Reserve Fund receives from the Revenue Fund amounts required to maintain the stipulated reserve requirement of $8 million. Initially, the Reserve Fund was funded with an irrevocable standby letter of credit of 58 million issued by Banco Santander de Puerto Rico with an initial term of five years. On October 2009 this letter of credit was amended to extend the credit expiration date for one additional year, to reduce the amount to $5.5 million dollars , to redefine the term ' applicable interest rate' and to modify the letter of credit fees. On 2010 the letter of credit was amended to increase the amount to $0 million , the original letter expired on October 2011 but it was extended to October 29, 2012 and it is secured by Banco Santander SA Madrid. Since the letter of credit is not designed to guarantee payment of the entire principal of and interest on the 2003 Bonds as it becomes due, but is being used solely as a mechanism to initially fund the

4

Autopistas de Puerto Rico y Compaiiia, S.E. Notes to Financial Statements December 31 , 2011 and 2010

Reserve Fund, the leiter of credit does nol provide for automatic reinstatement of amounts drawn thereunder. Funds are to be used to supplement the Bond Service Fund, the Redemption Fund, and the General Fund when requ ired . Any excess over the stipulated reserve requirement shall be transferred to the Revenue Fund to the extent that after any such transfer the balance of the Reserve Fund shall nol be less than $4 million.

If a deficiency in the Reserve Fund occurs, the Trust requires the Trustee to deposit in the Reserve Fund any revenue available, after payment of budgeted current expenses and the required deposits to the Bond Service Fund and the Redemption Fund have been made, and if such available revenue shall be insufficient, to transfer to the Reserve Fund any moneys then to the credit of the General Fund in amounts necessary to cure such deficiency. Failure by Autopistas to restore the balance of the Reserve Fund to an amount at least equal to $4 million within 30 days after such balance has been reduced to an amount below $4 million constitutes an event of default under the loan (see Note 7) and, consequently, under the Trust.

Under the Trust, the Trustee must draw the fu ll amount of any such Reserve Fund letler of credit or financial guaranty insurance policy on the 30th day prior to its expiration in the event that such letler of credit or financial guaranty insurance policy is not extended or replaced with cash . Investment obligations, or a successor letter of credit or financial guaranty insurance policy from an entity with a long-term debt rating in one of the three highest rating categories (without regard to any gradations with in any such categories) from a nationally recognized securities ratings organization at least 30 days before its expiration . In addition , the Trustee must draw the full amount of any such Reserve Fund letter of credit or financial guaranty insurance policy immediately upon its receipt of notice from the issuer of such letter of credit or financial guaranty insurance policy that such letter of credit or financial guaranty insurance policy will be terminated as a result of a default by the partners of Autopistas (which are the entities responsible for reimbursing the issuer of the letler or financial guaranty insurance policy for any drawings made thereunder) under the related reimbursement or similar agreement.

In the event that the concession agreement is terminated, Autopistas may be entitled to withdraw some or all of the money deposited in the Reserve Fund. Upon such withdrawal, the AuthOrity will be required to replenish the Reserve Fund to the required $8 million level within 12 months (in equal quarterly installmenls) after the Authority assumes Autopistas' obligation to pay the 2003 Bonds. In the event that Ihe concession agreement is terminated prior to the fifth anniversary of the date of issuance of the 2003 Bonds for any reason, Autopistas will be entitled to withdraw all funds in the Reserve Fund, up to the reserve requirement. In the event that the concession agreement is terminated on or after the frfth anniversary of the dale of issuance of the 2003 Bonds, Autopistas will be entitled to withdraw (i) all the funds in the Reserve Fund, if the concession agreement is term inated by Autopistas as a result of a default by the Authority, or (ii) atlthe funds in the Reserve Fund in excess of $4 million if the concession agreement is terminated as a result of the exercise by Autopistas of its termination option. If the concession agreement is term inated by the Authority as a result of a default by Autopistas, Autopistas will not be entitled to withdraw any of the funds in the Reserve Fund.

Bond Service Fund The Bond Service Fund receives from the Revenue Fund an amount equal to the interest becoming due and payable on the interest payment date, and one-twelfth of the amount of principal of the serial bonds becoming due and payable within the ensuing 12 months. As of December 31, 2011 and 2010, there was $1 ,327,262 and $779,250, respectively, deposited in the Bond Service Fund.

5

Autopistas de Puerto Rico y Compaiiia, S.E. Notes to Financial Statements December 31 , 2011 and 2010

General Fund The General Fund receives from the Revenue Fund any amount remaining after meeting the requirements of the Bond Service Fund, the Redemption Fund, the Reserve Fund, and the Renewal and Replacement Fund and transfers to Autopistas any amount required to pay current expenses in excess of the annual budget. The General Fund shall be used to supplement the Reserve Fund, as required, and subject to certain financial parameters, to pay partner distributions.

Renewal and Replacement Fund The Renewal and Replacement Fund receives from the Revenue Fund an amount, which shall make total deposits for each six-month period ending June 30 and December 31 equal to $75,000, or such greater amount as Autopistas may determine.

Redemption Fund The Redemption Fund receives from the Revenue Fund an amount equal to one-twelfth of the principal on the term bonds becoming due and payable within the ensuing 12 months. As of December 31, 2011 and 2010, there were no moneys deposited in the Redemption Fund.

Revenue Fund The Revenue Fund receives all revenue derived from the operation of the Facility and transfers at month-end the cash to meet the requirements of all other funds.

6. Concession Agreement

General Autopistas and the Authority entered into a concession agreement (the ·Concession"), which granted Autopistas the right to design, construct, operate, maintain, and manage the Facility, as well as to charge tolls for the use of the Facility. The Concession is for an original term of 35 years , scheduled to expire on April 3, 2027. On September 9, 2009, the Concession Agreement was amended extending the term from 35 to 52 years; the agreement will now expire on February 22, 2044, unless earlier terminated as provided therein .

Distributions to Partners The partners are entitled to receive any balance held in the General Fund after the end of every fiscal year as defined (July 1 through June 30), if the sum of net revenue (as defined by the Concession) and the beginning of year balance of the General Fund is greater than 110% of the aggregate principal and interest requirements for the year. Under the terms of the Trust, this amount can be transferred, at the written direction of Autopistas, to the credit of the Autopistas' Reserve Fund . As a result of the amendment of September 9, 2009 to the Concession Agreement, Autopistas shall pay 5% of toll revenues, as defined, to the Authority until February 22, 2027, and commencing on February 23, 2027 and through the end of the term, 61 .5% of toll revenues.

Prior to the amendment of September 9, 2009 to the Concession Agreement, the partners were entitled to receive any balance held in the General Fund after the end of every fiscal year as defined (July 1 through June 30), if the sum of net revenue (as defined by the Concession) and the beginning of year balance of the General Fund was greater than 110% of the aggregate principal and interest requirements for the year. Under the terms of the Trust, this amount could be transferred, at the written direction of Autopistas, to the credit of the Autopistas' Reserve Fund. This distribution would continue until the base return on partners ' capital (as defined) reached 19%, after income or withhold ing taxes payable by such partners , calculated from the date of contribution. tn any fisca l year that the base return on partners ' capital was reached by any partner, any excess revenue was shared by such partner with the Authority in the proportion of

6

Autopistas de Puerto Rico y Campania, S.E. Notes to Financial Statements December 31, 2011 and 2010

60% for the Authority and 40% for the partner until such time as the internal rale of return on partners' capital was equal to 22% nel, after income or withholding taxes payable by such partners, and thereafter in the proportion of 85% for the Authority and 15% for such partners.

On March 2011 . the Partnership and the Authority signed an amendment to the Concession Agreement The Authority agreed to compensate the Partnership with sixty percent of the amounts payable to the Authority for amounts attributable to 2010, 2011 and 2012. The Authority has requested in exchange that the loll rates be maintained at the current levels until December 31 , 2012. In 2010 the amount payable to the Authorny was reduced by approximately $541 ,000, the amount is reflected in 201 1 as other income.

During the year ended December 31 , 2011 , gross distributions to the partner amounted to $1 ,000,000. No distributions were made in 2010.

Termination Should Autopistas opt to tenninate the Concession, as stipulated in the Concession, it would surrender all of its rights in the Facility in exchange for the release from all of its obligations related to the financing of the Facility.

Should Autopistas be obligated to tenninate the Concession because of its failure to cure an insufficiency for the payment of the 2003 Bonds, the Authority will be automatically and irrevocably obligated to acquire the Concession in exchange for the assumption by the Authority of aU of the payment obligations of Autopistas.

7. Long.Term Debt

On April 1 , 1992, Autopistas and the Authority entered into an agreement (the "l oan") whereby the proceeds from certain bonds issued by the Authority, aggregating to approximately $116,753,000, were lent to Autopistas for the purpose of developing the Faci lity . Autopistas was obligated to repay the loan in amount& that would be sufficient to pay principal and interest becoming due and payable on the bonds, as well as amounts required to effect mandatory redemption of the bonds, when applicable. For that purpose all revenue derived from the operations of the Facility were deposned with the trustee in the Revenue Fund.

On October 22, 2003, the Authority issued and sold the 2003 Bonds amounting to $153,222,270. The 2003 Bonds were issued as serial bonds, tenn bonds, and capital appreciation bonds. The proceeds from the sale of the 2003 Bonds were loaned by the Authority to Autopistas through a loan Agreement (the loan) and used to refund the Authority's Special Facility Revenue Bonds, 1992 Series A, B, and C (San Jose lagoon Bridge Project) (the ·1992 Bonds"), and to pay the costs of issuance of the 2003 Bonds. The net proceeds from the sale of the 2003 Bonds were deposited with the trustee of the 1992 Bonds (Banco Santander de Puerto Rico) and invested in government securities to be used to redeem the 1992 Bonds. As a result, the 1992 Bonds were defeased for purposes of the trust agreement under which they were issued and the provisions of such trust agreement ceased to be in effect . The 1992 Bonds that are future income growth securities or capital appreciation bonds are not redeemable prior to maturity and will be paid at their respective maturities.

On October 1, 2003, and as part of the refunding of the 1992 Bonds, the Authority, Banco Santander de Puerto Rico, and Autopistas entered into an escrow deposit agreement to create an irrevocable trust fund , where the net proceeds from the sale of the 2003 Bonds and a payment of $1 ,022,552 by Autopislas were to be deposited in the fonn of government obligations thai would

7

Autopistas de Puerto Rico y Campania, S.E. Notes to Financial Statements December 31 , 2011 and 2010

produce investment income and earnings at such times and in such amounts thai will be sufficient to pay when due, whether al maturity or upon the redemption thereof, all of the principal of and redemption premium and interest on the 1992 Bonds that are capital appreciation bonds.

Autopistas is obligated to repay the Loan in amounts thai will be sufficient to pay principal and interest becoming due and payable on the 2003 Bonds, as well as amounts required to effect mandatory redemption of the bonds, when applicable . For that purpose all revenue derived from the operations of the Fac!lity continues to be deposited with the Trustee in the Revenue Fund. Pursuant to the loan, Aulopistas covenants that it will at all times fix, revise, charge and collect rates , rentals, fees, tol1s, and other charges for the use or services of the bridge sufficient to pay current expenses, to make the required deposits to the sinking fund and the Renewal and Replacement Fund established under the Trust, and to restore the Reserve Fund established under the New Trust to the required level (see Note 5) . If in any fiscal year the net revenue is not sufficient to satisfy this toll covenant, Autopistas is required to employ a firm of traffic engineers to recommend revisions to the toll schedule and the annual budget to provide sufficient net revenue to pay debt service on the 2003 Bonds, make the required deposits to the Renewal and Replacement Fund, and restore the Reserve Fund, to the required level.

8

Autopistas de Puerto Rico y Compania, S.E. Notes to Financia l Statements December 31, 2011 and 2010

Following is a description of the outstanding bonds underlying the Loan at December 31 :

2011 Interest Interest Payment

Description Amount Rate Date Maturity

Monthly, first day of each month commencing

Serial bonds $ 7,765,000 4.50% - 5,00% December 1, 2003 2012 through 2013 Monthly, first day of each month commencing

Term bonds 125,670,000 5.55% - 5.85% December " 2003 201 41hrough 2027 Capital appreciation bonds 51,285,000 5.90%·6.15% Maturity 2021 through 2026

Total debt 184,720,000

Less unacaeted discount on capital appreciation bonds (25,874,259) Less original issue d iscount (130,627) Less current portion {3,185,OOOl

long - term debt $1 55,530,114

2010 Interest Interest Payment

Description Amou nt Rate Data Maturi~

Monthly, first day of each month commencing

Serial bonds $ 9,635,000 4.50%·5.00% December 1, 2003 2011 through 2013 Monthly, firs t day of each month commencing

Tem bonds 125,670,000 5.55%· 5.85% December 1, 2003 201 4 through 2027 Capital appreciation bonds 51 ,285.000 5.90%·6.1 5% Maturity 2021 through 2026

Total debt 186.590,000

Less unaccreted discount on capital appreciation bonds (27,335,481 ) Less original issue discount (134,706) Less current port ion 11.870.000)

Long · term debt $ 157,249,813

Contractual sinking fund requirements of the bonds (excluding the effects of mandatory redemption, if applicable) for the next five years and thereafter are as follows:

Year ending Oecember 31 , Principal Interest Total

2012 $ 3,185,000 $ 7.579.102 $ 10.764,1 02 2013 4.580,000 7,427,815 12.007.815 2014 5,275.000 7,198,81 5 12,473,815 2015 6.280,000 6.906.052 13,186.052 2016 7,195,000 6.557.512 13,752,512 Thereafter 158.205.000 39.951 ,371 198,156.371

Total $184,720,000 $ 75,620,667 $ 260.340,667

9

Autopistas de Puerto Rico y Compania, S.E. Notes to Financial Statements December 31 , 2011 and 2010

The interest on the serial bonds and the term bonds are payable monthly on the first day of each month, beginning on December 1, 2003. Discount on the Capital Appreciation Bonds will be accreted every six months, on each January 1 and July 1, and the interest will be payable as part of their accreted value upon maturity or earlier payment in full. Interest is accrued from the date of issuance of the 2003 Bonds on the basis of a 360-day year consisting of twelve 30-day months.

The 2003 Bonds that mature after July 1. 2011 may be redeemed at the option of Autopistas in whole at any time not earl ier than October 1, 2011 , or in part on any interest payment dale not earlier than October 1, 2011, at the following prices (expressed as a percentage of the principal amount of the 2003 Bonds to be redeemed) plus accrued interest to the redemption date:

Redemption Period

October 1, 2011 through September 30, 2012 October 1, 2012 through September 30, 2013 October 1, 2013 and thereafter

Redemption Price

101% 100-112%

100%

tn addition , under certain conditions, the 2003 Bonds are subject to mandatory redemption, at the principal amount of the 2003 Bonds to be redeemed , plus any accrued interest to the redemption date, without premium. A portion of the term bonds due on July " 2018, July 1, 2020 and March " 2027, could be redeemed to the extent of their respective amortization requirements on each July " commencing on July 1, 2014, 2019, 2021 and 2026, respectively, at a redemption price equal to the principal amount of the 2003 Bonds to be redeemed plus accrued interest 10 the redemption date, without premium. The obligations of Aulopistas under the loan are secured by toll revenue, but are not secured by a lien on the Facility or on any other property of Autopistas.

The failure of Autopistas to pay the amounts required with respect to principal and interest on the 2003 bonds, when due and payable amon9 other things, constitutes an event of default under the loan Agreement. In such event, and provided the default is notified, the Authority could declare all unpaid amounts under the loan due and payable. II is the opinion of management of Aulopistas that the projected 2012 operating revenue and sinking funds held by the Trustee will be sufficient to pay the Facility's operating expenses and scheduled loan and interest payments for 2012.

The Concession was amended on October 30, 2003, so as to provide an initial five-year holiday in the funding of the required $8 million balance in the Reserve Fund applicable 10 the 2003 Bonds and the substitution of such required depos it by an irrevocable standby letter of credit provided by the partners of Autopistas . Additionally, the partners of Autopistas received a cred it of $4 million to the capital of Aulopistas for purposes of calculating the future distributions of available excess cash flows.

8. Cash Flows Information

During the year ended December 31 , 2011 and 2010, Autopislas made interest payments of approximately $7,628,190 and $7,684,000, respectively.

10

Autopistas de Puerto Rico y Compaiiia, S.E. Notes to Financial Statements December 31 , 2011 and 2010

9. Commitments and Contingencies

On October 1, 2003, and as part of the refunding of the 1992 Bonds. the Authority, Banco Santander de Puerto Rico, and Autopislas entered into an escrow deposit agreement to create irrevocable trust fund, where the net proceeds from the sale of the 2003 Bonds and a payment of $1,022,552 by Autopistas were to be deposited in the form of government obligations that would produce investment income and earnings at such times and in such amounts that will be sufficient to pay when due, whether at maturity or upon Ihe redemption thereof, all of the principal of and redemption premium and interest on the 1992 Bonds thai are capital appreciation bonds. Section 2.02 of this agreement stipulates that if the amounts deposited in the escrow fund from the maturing government obligations acquired with the initial deposit are insufficient to make the payments of principal, redemption premium. and interest as these become due, Autopistas. prior to the Authority becoming obligated, should deposit into the escrow fund the amount of any deficiency immediately upon notice from the escrow agent. During 20OS, Banco Santander Puerto Rico Trust Department was sold to Banco Popu lar Puerto Rico. which was the named successor under the same conditions described above.

Pursuant to the requirements of ASC 460 Guarantees, amount to be recorded as a liability should be the equivalent of the fair value of the estimated cash flows to be paid multiplied by the estimated probability of having to make the payment. In view of the quality of the financial instruments deposited in escrow the probability of having to honor the guarantee is estimated to be insignificant.

The maximum amount of undiscounted payments Autopistas would have to make in the event of a deficiency in the e~crow fund upon redemption of the 1992 Bonds is the full outstanding balance of such bonds plus all estimated interest and redemption premium amounting to approximately $21 million. At December 31 , 2011 and 2010. the trust had investments with a par value of $21 and $29 million (market value of $21 and $30 million) for the payment of the outstanding principal and interest due on the 1992 Bonds.

In 1991 , Autopistas was awarded the right to enter into a concession agreement with the Authority for the final design, construction. and operation of Highway 66 (the Project) . The Authority canceled negotiations for the execution of the concession agreement in February 1997. As a result, in March 12. 1997, Autopistas filed a lawsuit against the Authority claiming damages in the amount of $200 million. The case was settled during 2009. As part of the settlement, the parties agreed to amend the Concession Agreement to extend the term to 50 years and Autopistas agree to pay to the Authority 5% of the toll revenues, as defined. until 2027 and 61 .5% thereafter until the end of the Concession.

The legal costs and expenses generated from the Highway 66 legal case were assumed by the then Autopistas partners (Abertis and Supra).

11

Autopistas de Puerto Rico y Compania, S.E. Notes to Financial Statements December 31, 2011 and 2010

10. Reti rement Plan

Autopistas has a defined contribution plan (165(e) Plan). Eligible employees are allowed to contribute up to 10% of eligible eamings subject to a maximum provided by law. The Partnership matches 100% of the first 8% of the eligible pay contributed by a participant. Tolal contributions made by the Partnership for the year ended December 31 , 2011 and 2010 amounted to approximately $59,000 and $S9,000, respectively_

11. Lease

Autopistas has capital leases for certain vehicles. Future minimum lease payments under noncancelable capital leases are as follows:

Year ending December 31,

2012 S 24,016 2013 25,785 2014 17,190

Total minimum lease payments 66.991

Less amount representing interest (6.4901

Obligation under capital leases 60,501

less current port ion (20.1691

S 40,332

12. Significant Concentration of Risk

The Partnership places its cash with financial institutions located in Puerto Rico. The Partnership monitors the credit quality of the financial institutions and does nol anticipate their nonperformance.

13. Subsequent Events

Events and transactions from January I, 2012 through April 30 , 201 2. the date the financial statements were available to be issued, have been evaluated by management. Management has determined that there were no other material subsequent events thai would require adjustment to or disclosure in the Partnership's financial statements through April 30. 2012.

12

Autopistas de Puerto Rico y Compania, S.E. Schedule of Changes in Sinking Funds Held by Trustee December 31 , 2011 and 2010 Schedule

Renewal and Bond Company Replacement Service Redemption Reserve Reserve Revenue General

Fund Fund Fund Fund Fund Fund Fund Total

Balance at December 31 , 2009 • 220,453 $ 412,520 • S 2,500,204 $ 11.984 S 1,501 ,383 S 1,453,635 S 6,100,179

AddrtionS Cash from Oper31iOfls 17,829,516 17,829,516 Interest earned 32 63 324 , 9' 3&l 893

Deductions Payment of Interest (7,687,796) (7,687 ,796) Payment of principal (990,000) (990,000) Distribution 10 partners Withdrawals 10 fund maintenance actlv~ies (1 42,358) (1 42,358)

Cash advances for operating costs (5,130,000) (5,130.000) Trustee fees (9,515) (9,515)

Transfers 150,000 9 ,044,463 p2 ,742,596~ 3,548,1 33

Balance at Decem ber 31, 2010 228,127 779,250 2,500,528 11,986 1,448,880 5,002,148 9,970,919

Additions Cash from operations 17,437,236 17,437,236 lnleres! earned 33 95 '68 60 675 1,132

Deductions Payment rA interest (7,628,190) (7,628,190) Payment of principal (1 ,870,000) (I,870,000) Distribution to partners (1 ,000,000) (I,OOO,OOO) Withdrawals to fund maintenance activities

Cash advances for operaling costs (4,827,926) (4,827,926) Trustee fees , (4,600) (4,598)

Transfers 150,000 10,046,107 (1 3,426,4031 3,230,296

Balance at Decem ber 31, 2011 • 378,160 $ 1,327,262 • $ 2,500,798 • 11 ,987 • 627,247 $ 7,233,119 $ 12,078,573

13