Automotive market perspectives Brazil 2014-2018 - … · Current market challenges and counter...

12

Current market challenges and counter strategies - Executive Summary - São Paulo, October 2014 Automotive market perspectives Brazil 2014-2018

Transcript of Automotive market perspectives Brazil 2014-2018 - … · Current market challenges and counter...

Current market challenges and counter strategies - Executive Summary -

São Paulo, October 2014

Automotive market perspectives Brazil 2014-2018

2 SAO-0180-900031-32-76_3_short.pptx

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

3.0

3.5

2.3

3.0

3.5

2.3

2.3

3.0

2.0

1.0

1.5

0.2

0.5

0.1

2.5 2.5

0.9

2.7

7.6

-0.3

5.1

6.1

3.9

3.1

Itaú

Bradesco

Central Bank

Brazilian growth phase

Lower growth

Increased uncertainty

Slowdown of growth

Comments

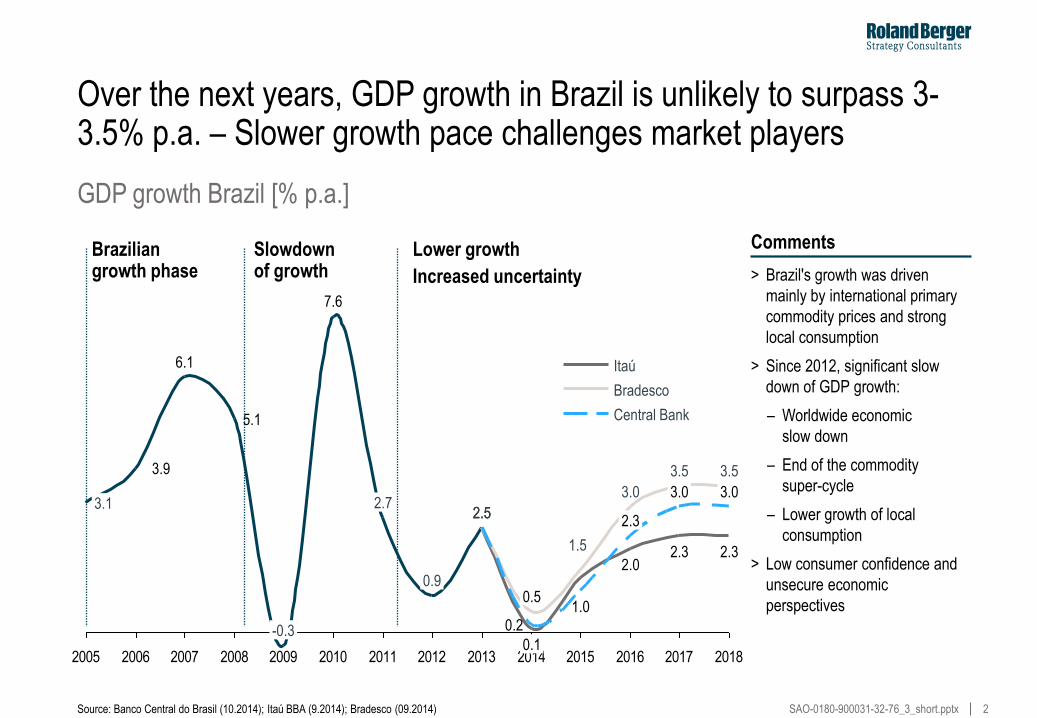

Over the next years, GDP growth in Brazil is unlikely to surpass 3-3.5% p.a. – Slower growth pace challenges market players

Source: Banco Central do Brasil (10.2014); Itaú BBA (9.2014); Bradesco (09.2014)

GDP growth Brazil [% p.a.]

> Brazil's growth was driven

mainly by international primary

commodity prices and strong

local consumption

> Since 2012, significant slow

down of GDP growth:

– Worldwide economic

slow down

– End of the commodity

super-cycle

– Lower growth of local

consumption

> Low consumer confidence and

unsecure economic

perspectives

3 SAO-0180-900031-32-76_3_short.pptx

Based on economic and political scenario, Brazil shows a stable outlook but for the foreseeable future only a limited growth potential

Source: Roland Berger Strategy Consultants

Summary – Strengths and weaknesses of Brazil

Strengths

> Huge domestic market potential with 200 m Brazilians and an increasing middle class

> Government with high interest in Automotive industry - Further protection of the industry very likely

> Overall macroeconomic indicators are stable – Sustained crisis not likely

Weaknesses

> Slow-down of economic growth in the next years due to high dependence on consumption

> Limited competitiveness impacting export capability and raising domestic car prices

> "Custo Brasil" impacting competitiveness and company margins

Implications for the automotive industry

Sustained market protection from the government,

Intact long term growth perspective

Limited growth potential,

2-3 years volume adjustment

4 SAO-0180-900031-32-76_3_short.pptx

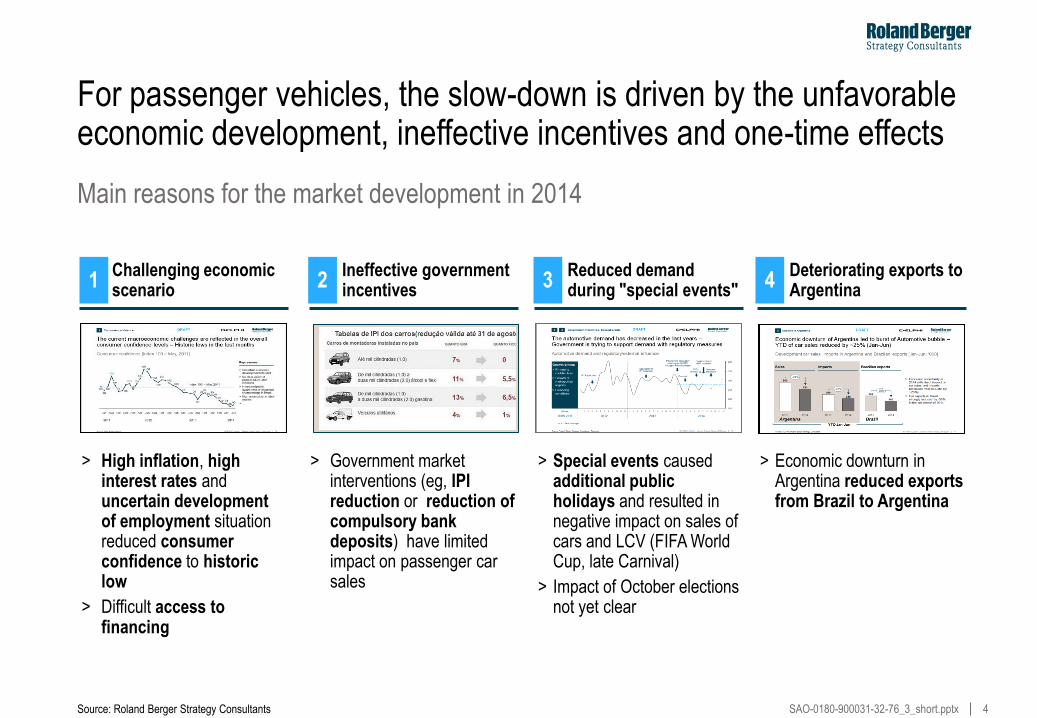

For passenger vehicles, the slow-down is driven by the unfavorable economic development, ineffective incentives and one-time effects

Main reasons for the market development in 2014

Challenging economic scenario 1

Deteriorating exports to Argentina 4

Ineffective government incentives 2

Reduced demand during "special events" 3

Source: Roland Berger Strategy Consultants

> High inflation, high interest rates and uncertain development of employment situation reduced consumer confidence to historic low

> Difficult access to financing

> Government market interventions (eg, IPI reduction or reduction of compulsory bank deposits) have limited impact on passenger car sales

> Special events caused additional public holidays and resulted in negative impact on sales of cars and LCV (FIFA World Cup, late Carnival)

> Impact of October elections not yet clear

> Economic downturn in Argentina reduced exports from Brazil to Argentina

5 SAO-0180-900031-32-76_3_short.pptx

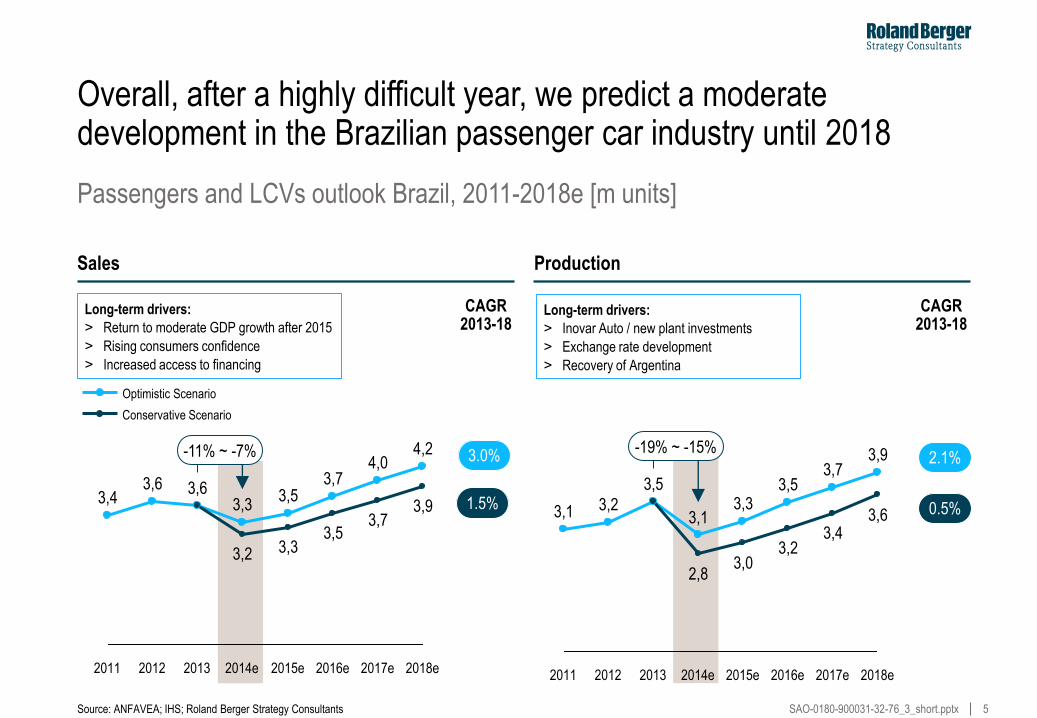

-19% ~ -15%

2018e

3,6

3,9

2017e

3,4

2014e

2,8

3,1

2013

3,5

2012

3,2

2011

3,1

3,0

2015e

3,5

3,2

2016e

3,7

3,3

Overall, after a highly difficult year, we predict a moderate development in the Brazilian passenger car industry until 2018

Passengers and LCVs outlook Brazil, 2011-2018e [m units]

CAGR 2013-18

3.0%

1.5%

Conservative Scenario

Optimistic Scenario

Sales Production

Source: ANFAVEA; IHS; Roland Berger Strategy Consultants

2.1%

0.5%

CAGR 2013-18

3,5

3,7

2015e

3,3

3,5

2014e

3,2

3,3

2013

3,6

2012

3,6

2011

3,4

-11% ~ -7%

2018e

3,9

4,2

2017e

3,7

4,0

2016e

Long-term drivers:

˃ Return to moderate GDP growth after 2015

˃ Rising consumers confidence

˃ Increased access to financing

Long-term drivers:

˃ Inovar Auto / new plant investments

˃ Exchange rate development

˃ Recovery of Argentina

6 SAO-0180-900031-32-76_3_short.pptx

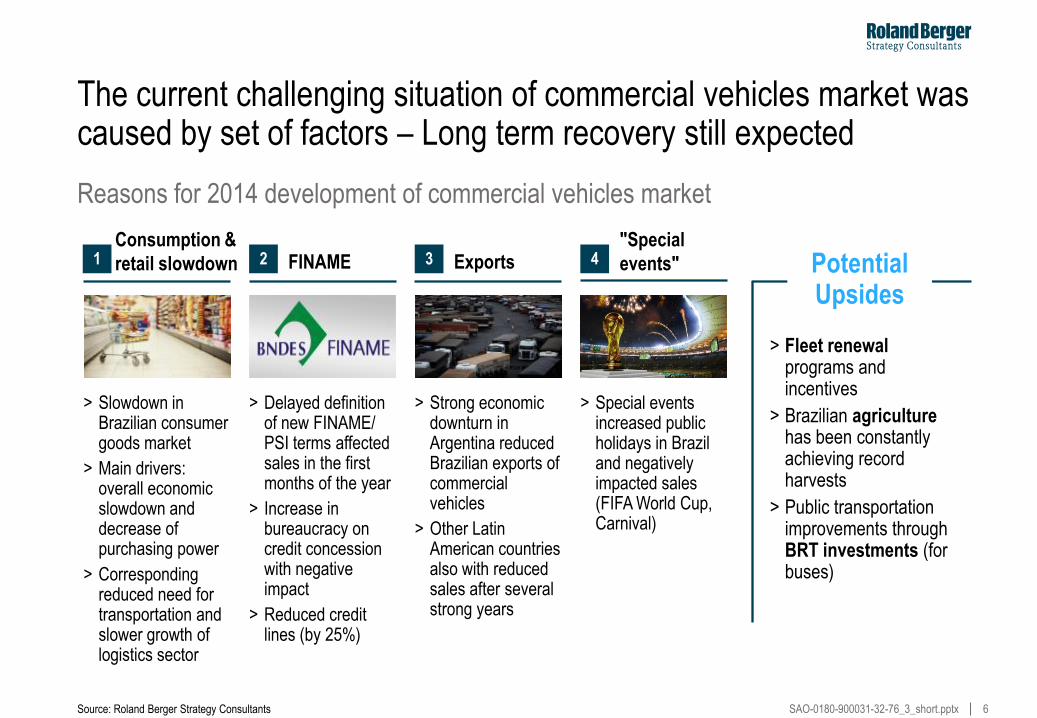

The current challenging situation of commercial vehicles market was caused by set of factors – Long term recovery still expected

Reasons for 2014 development of commercial vehicles market

Consumption &

retail slowdown FINAME Exports "Special

events" Potential Upsides

> Slowdown in Brazilian consumer goods market

> Main drivers: overall economic slowdown and decrease of purchasing power

> Corresponding reduced need for transportation and slower growth of logistics sector

> Delayed definition of new FINAME/ PSI terms affected sales in the first months of the year

> Increase in bureaucracy on credit concession with negative impact

> Reduced credit lines (by 25%)

> Strong economic downturn in Argentina reduced Brazilian exports of commercial vehicles

> Other Latin American countries also with reduced sales after several strong years

> Special events increased public holidays in Brazil and negatively impacted sales (FIFA World Cup, Carnival)

> Fleet renewal programs and incentives

> Brazilian agriculture has been constantly achieving record harvests

> Public transportation improvements through BRT investments (for buses)

1 2 3 4

Source: Roland Berger Strategy Consultants

7 SAO-0180-900031-32-76_3_short.pptx

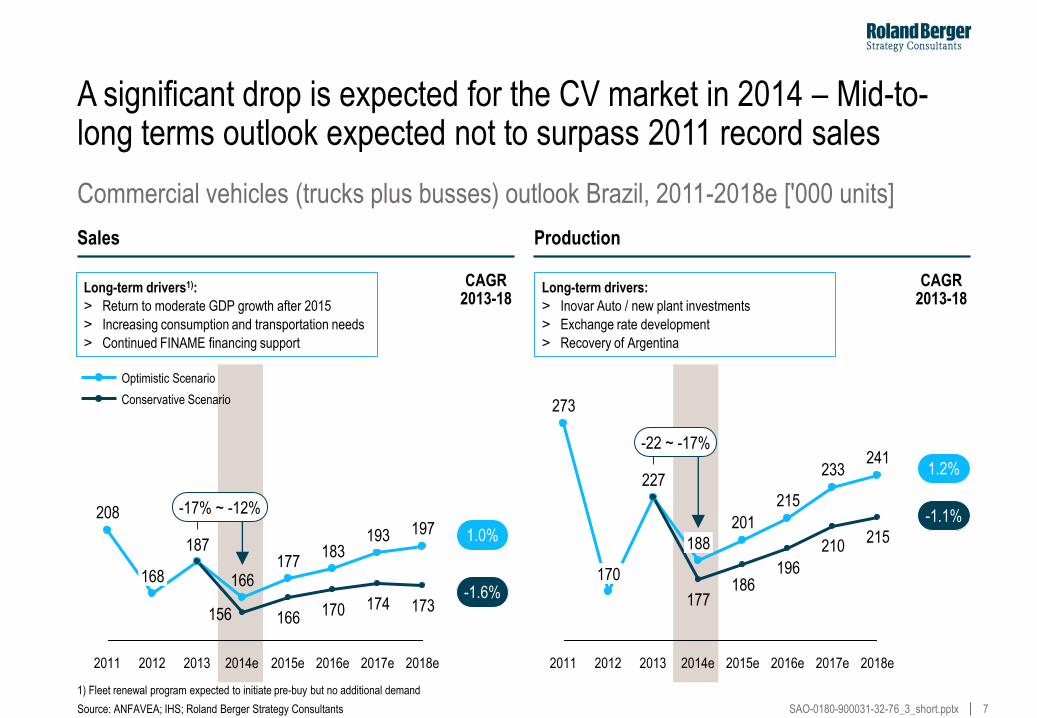

-22 ~ -17%

2018e

215

241

2017e

210

233

2016e

196

215

2015e

186

201

2014e

177

188

2013 2012

170

2011

273

227

A significant drop is expected for the CV market in 2014 – Mid-to-long terms outlook expected not to surpass 2011 record sales

Commercial vehicles (trucks plus busses) outlook Brazil, 2011-2018e ['000 units]

CAGR 2013-18

1.0%

-1.6%

Conservative Scenario

Optimistic Scenario

Sales Production

Source: ANFAVEA; IHS; Roland Berger Strategy Consultants

1.2%

-1.1%

CAGR 2013-18

2018e

-17% ~ -12%

173

197

2017e

174

193

2016e

170

183

2015e

166

177

2014e

156

166

2013 2012

168

2011

208

187

Long-term drivers1):

˃ Return to moderate GDP growth after 2015

˃ Increasing consumption and transportation needs

˃ Continued FINAME financing support

Long-term drivers:

˃ Inovar Auto / new plant investments

˃ Exchange rate development

˃ Recovery of Argentina

1) Fleet renewal program expected to initiate pre-buy but no additional demand

8 SAO-0180-900031-32-76_3_short.pptx

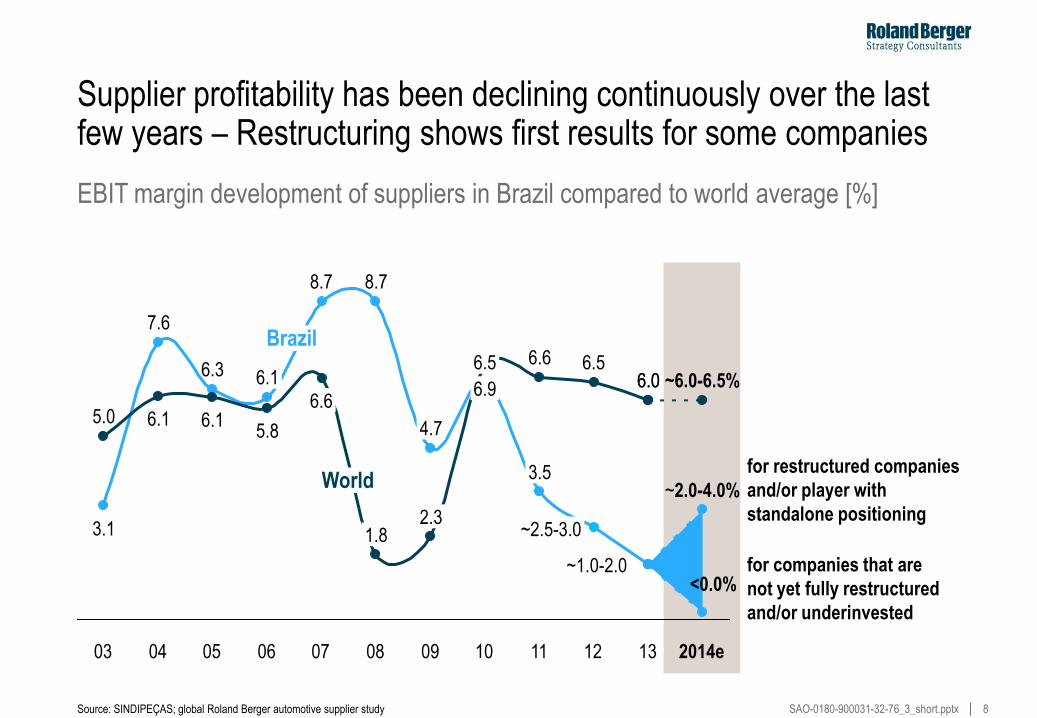

05

6.1

6.3

04

6.1

7.6

03

5.0

3.1

<0.0%

~2.0-4.0%

13

6.0

~1.0-2.0

6.0

12

6.5

~2.5-3.0

11

6.6

3.5

10

~6.0-6.5%

2014e

6.1 6.9

6.5

09

2.3

4.7

08

1.8

8.7

07

6.6

8.7

06

5.8

Supplier profitability has been declining continuously over the last few years – Restructuring shows first results for some companies

Source: SINDIPEÇAS; global Roland Berger automotive supplier study

EBIT margin development of suppliers in Brazil compared to world average [%]

World for restructured companies

and/or player with

standalone positioning

for companies that are

not yet fully restructured

and/or underinvested

Brazil

9 SAO-0180-900031-32-76_3_short.pptx

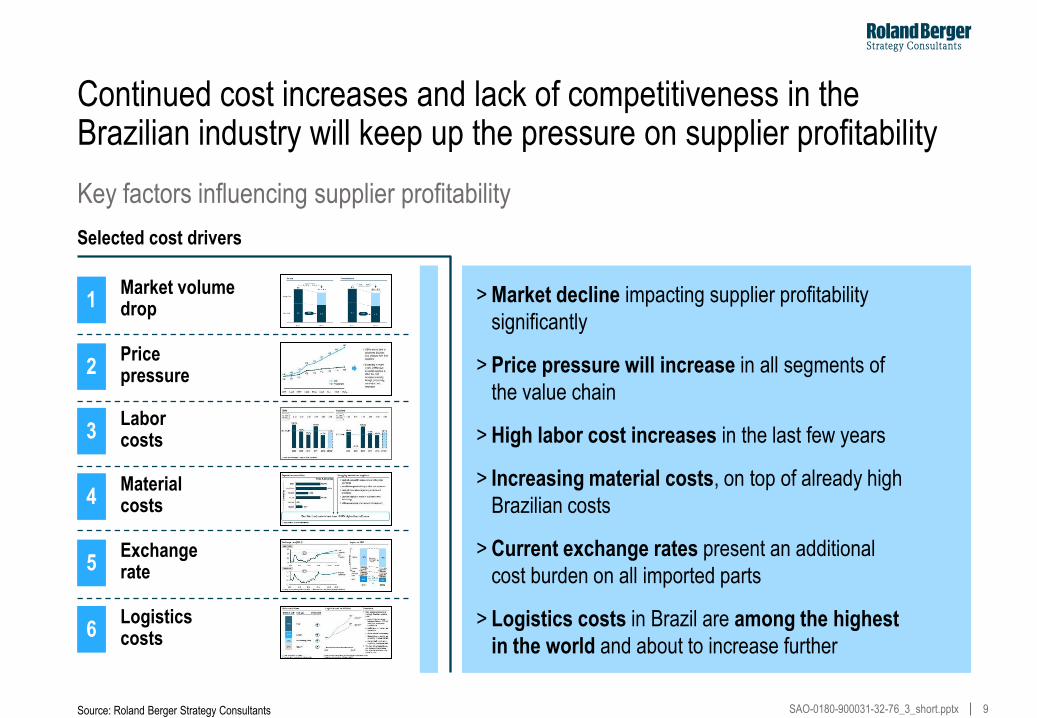

> Market decline impacting supplier profitability

significantly

> Price pressure will increase in all segments of

the value chain

> High labor cost increases in the last few years

> Increasing material costs, on top of already high

Brazilian costs

> Current exchange rates present an additional

cost burden on all imported parts

> Logistics costs in Brazil are among the highest

in the world and about to increase further

Continued cost increases and lack of competitiveness in the Brazilian industry will keep up the pressure on supplier profitability

Key factors influencing supplier profitability

Selected cost drivers

Price pressure 2

Exchange rate 5

Labor costs 3

Material costs 4

Logistics costs 6

Source: Roland Berger Strategy Consultants

Market volume drop 1

10 SAO-0180-900031-32-76_3_short.pptx

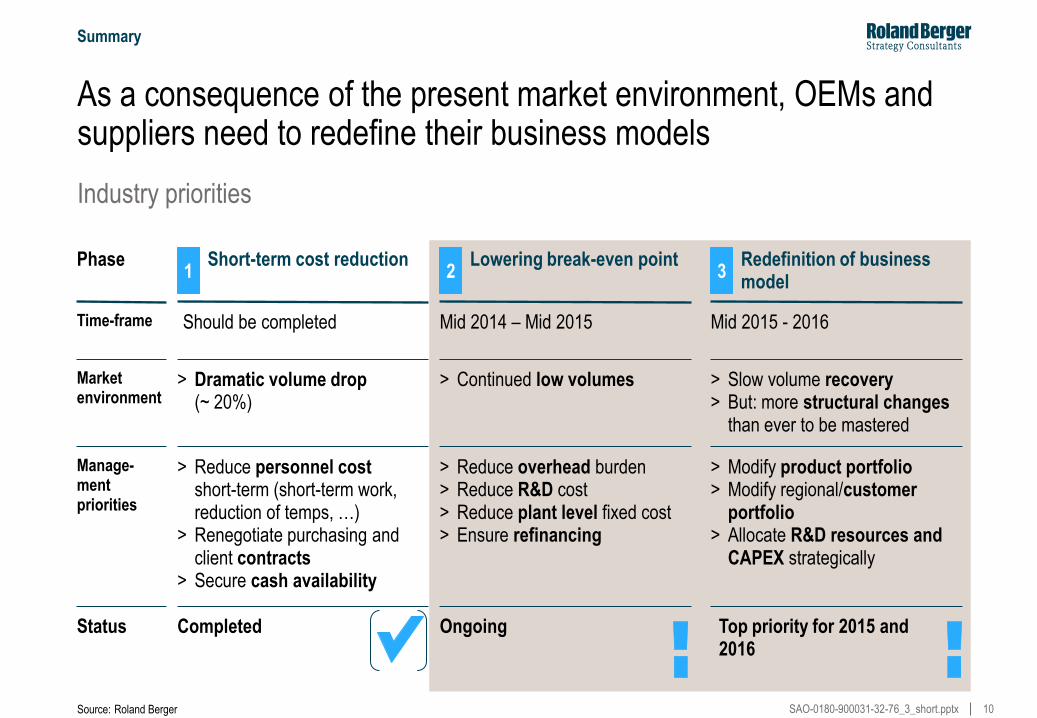

As a consequence of the present market environment, OEMs and suppliers need to redefine their business models

Phase

Status

Redefinition of business model

3 Lowering break-even point

2 Short-term cost reduction

Market environment

> Slow volume recovery > But: more structural changes

than ever to be mastered

> Continued low volumes > Dramatic volume drop (~ 20%)

1

Time-frame Mid 2015 - 2016 Mid 2014 – Mid 2015 Should be completed

Manage-ment priorities

> Modify product portfolio > Modify regional/customer

portfolio > Allocate R&D resources and

CAPEX strategically

> Reduce overhead burden > Reduce R&D cost > Reduce plant level fixed cost > Ensure refinancing

> Reduce personnel cost short-term (short-term work, reduction of temps, …)

> Renegotiate purchasing and client contracts

> Secure cash availability

Top priority for 2015 and 2016

Ongoing Completed

Source: Roland Berger

Industry priorities

Summary

11 SAO-0180-900031-32-76_3_short.pptx

Please contact us for further information

Source: Roland Berger Strategy Consultants

Authors of this study

Stephan Keese

Phone: +55 11 3046 7111

Fax: +55 11 3046 7222

E-mail: [email protected]

Partner São Paulo, Brazil Head of the Automotive Competence Center in South America

Phone: +55 11 3046 7111

Fax: +55 11 3046 7222

E-mail: [email protected]

Martin Bodewig

Principal São Paulo, Brazil Responsible for the Automotive Supplier Cluster in South America

Let's think: act!