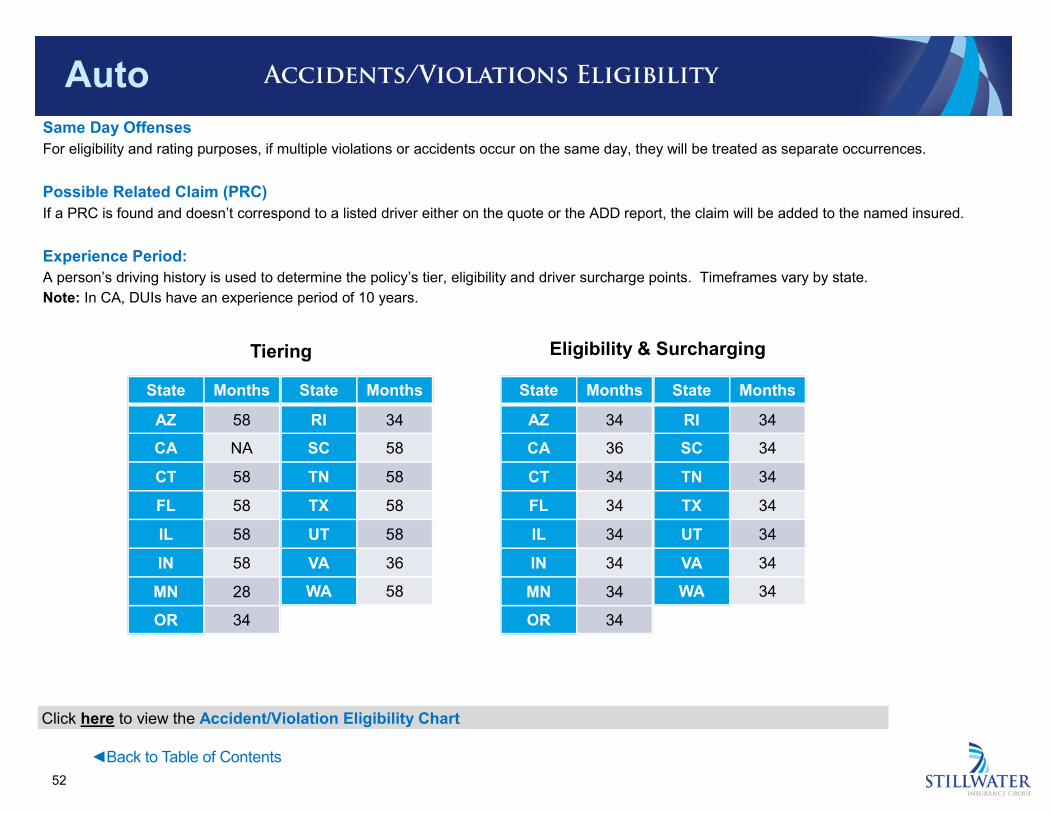

Auto - Stillwater Insurance · PDF fileAuto 2 Expired Drivers LicenseAuto 5.0 Product Guide...

80

Auto Auto Product and Underwriting Guide © 2018 Stillwater Insurance Group All right reserved AM Best Rating of A- (Excellent)

Transcript of Auto - Stillwater Insurance · PDF fileAuto 2 Expired Drivers LicenseAuto 5.0 Product Guide...

Auto

Auto Product and Underwriting Guide

© 2018 Stillwater Insurance Group All right reserved

AM Best Rating of A- (Excellent)

Auto

2

Auto 5.0 Product Guide

Table of Contents

About Stillwater Insurance Auto Program Effective Dates Contact Information Claims Procedure Contact Numbers Letter of Experience Submit Authority Upload Only Non-Bound (Paper) Application Issue Date Backdating Policy Period/Term Report Ordering Rewrites Moratoriums Application Submission FIRST: Quote Questions Submitting Start an Auto Quote Add Quote Reports and Verification Additional Driver Discovery (ADD) Proof of Prior Auto Insurance Policy Questionnaires Renewal Verification Phone Interviews Quality Planning Corp (QPC) File Maintenance & Audit Requirements

Agency Document Requirements UM/UIM Option Form Proof of Not at Fault Personal Injury Protection Different Addresses Driver Exclusion Florida Pre-Inspection Vehicle Inspection Sites (FL only) Photos (Lapse in Coverage) Expired Drivers License Business Use Garaged at School Proof of Marital Status Coverage

Bodily Injury Property Damage Medical Payments Personal Injury Protection (PIP) Uninsured & Underinsured Motorist BI Limits Uninsured & Underinsured Motorist PD Limit

Collision Collision Deductible Waiver Comprehensive Towing and Labor Rental Car Benefit (Transportation Expense) Custom Equipment Coverage Loan Lease Payoff (GAP) Named Non owner or Extended Non Owner Canadian ID Card Limited Coverage in Mexico (CA only) Provisional Instruction Permit Drivers Full Safety Glass Coverage Availability Unacceptable Vehicles Vehicle Eligibility CA Photo/Inspection Req.

Vehicle Use Definitions Pleasure Use Personal/Commute-Work Use Business Use Farm Use Artisan (CA only) Annual Mileage Unacceptable Drivers (Except CA) Prior Insurance Coverage

California Auto Eligibility – Good Driver Program Driver Eligibility Household Members Driver Classification Inexperienced Operator Surcharge Additional (Second) Named Insured Driver Marital Status Permit Holder Driver Status Financial Responsibility SR22 Suspension & Failure to Appear Driver Exclusions Non-Related Roommates Out-of-State Driver’s Licenses Rated Drivers (CA Only) Non Rated Drivers Unacceptable Policies Car Sharing Ride Sharing Florida-specific Rules

Accidents/Violations Eligibility Same Day - Concurrent Offenses Possible Related Claim (PRC) Experience Period Driving Record Minor Violations Speeding Major Violations Alcohol related Violations Accidents Comprehensive Losses Glass Claims Towing Claims Commercial Convictions

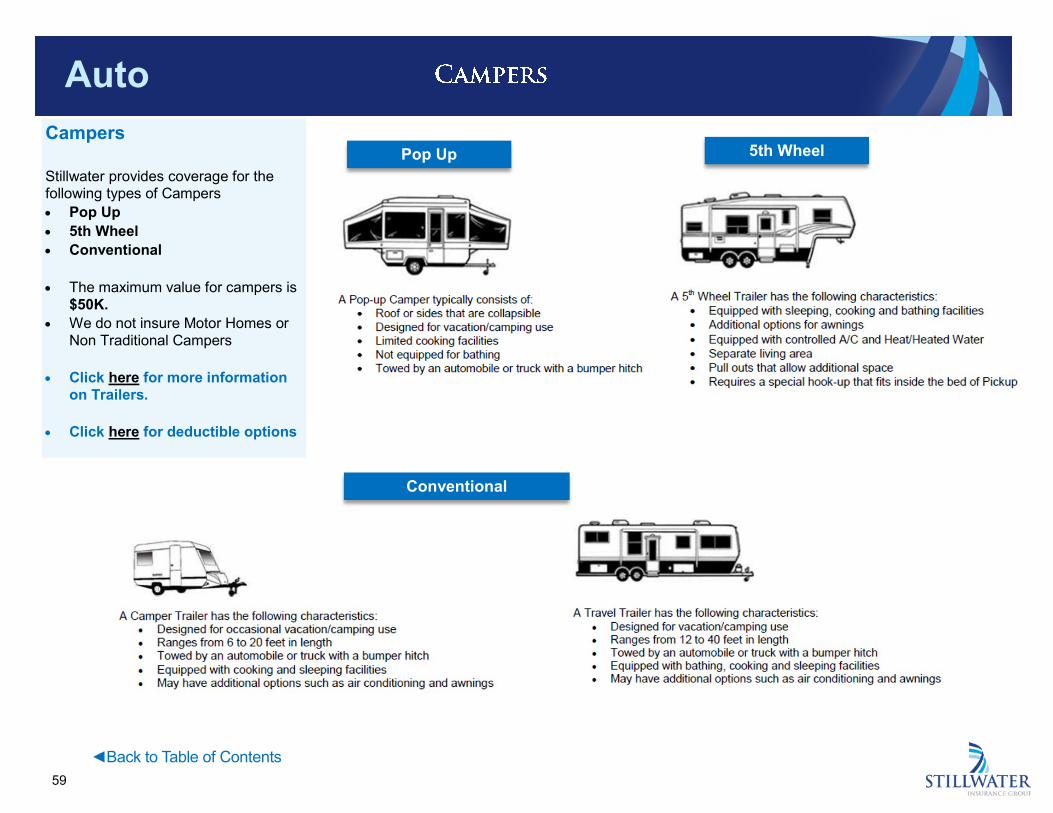

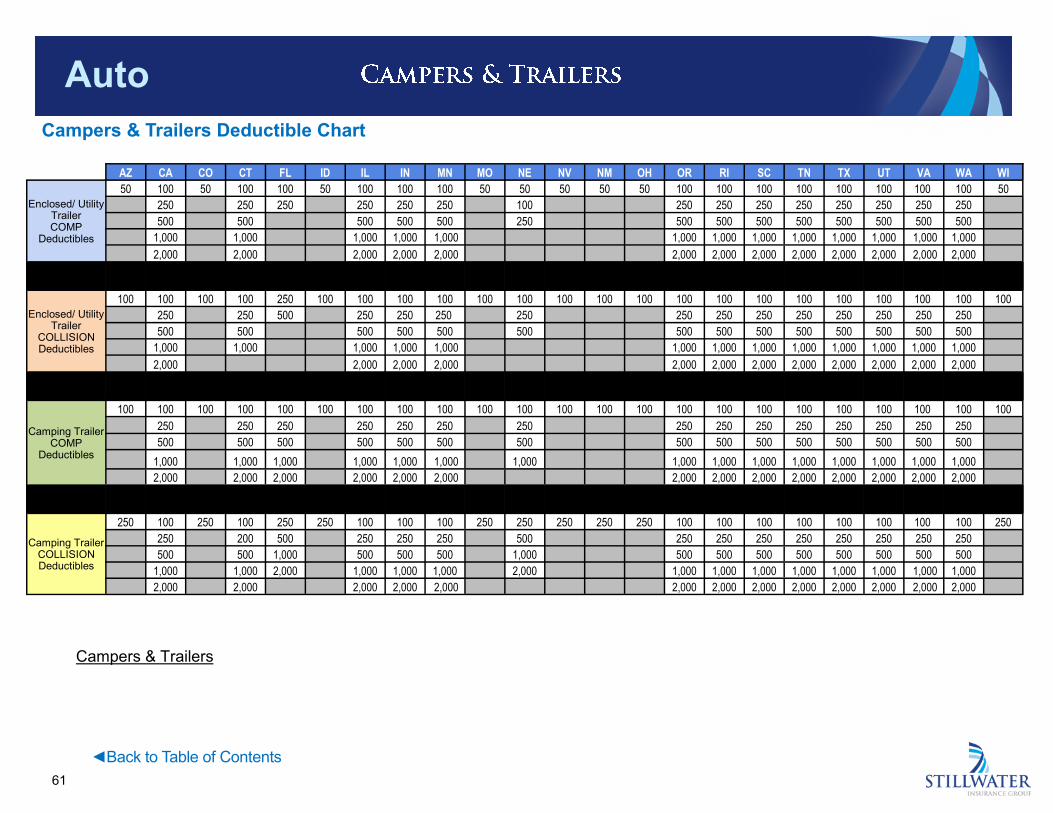

Campers & Trailers Campers Trailers Camper & Trailers Deductible Chart Discounts Accident Free Advance Quote Anti-Lock Brakes Anti-Theft Device Coverage Defensive Driver/Accident Prevention Course Distant Student Driver Training Employee Good Driver Good Student Homeownership Hybrid Vehicle Mature Driver Multi-Car Multi-Policy Paid in Full Paperless Passive Restraint Renewal Violation Free Discount Availability Processing Endorsements How to Make Policy Changes Number of Vehicles on a Policy Cancellation Reinstatements Returned Premium Payments Pay Plans and Installment Fees EFT Refunds Policy Fees Comparative Raters Frequently Asked Questions

Auto

3

Companies and Copyrights

Copyright © 2018 Stillwater Insurance Group all rights reserved. Stillwater Insurance Group, the Stillwater Group logo,

Stillwater Insurance Services, Inc. and the Stillwater Insurance Services, Inc. logo are registered trademarks of Duval Holdings, Inc.

Stillwater Insurance Group consists of the following companies:

• Stillwater Insurance Company

• Stillwater Property and Casualty Insurance Company

• Stillwater Insurance Services, Inc.

Stillwater Insurance Group is AM Best rated A-Excellent.

◄Back to Table of Contents ◄Back to Table of Contents

Auto

4

State Company Company number

Rate Book Code

New Business Date

Renewal Business Date Rater

AZ Stillwater Insurance Company (SIC) 20 N17 10/6/17 11/12/17 Auto 5.0

CA Stillwater Insurance Company (SIC) 20 817 5/3/18 5/3/18 Auto 5.0

CO Stillwater Property and Casualty Insurance Company (SPC) 21 HLR 9/30/16 11/6/16 Legacy

CT Stillwater Insurance Company (SIC) 20 916 9/1/16 9/1/16 Auto 5.0

FL Stillwater Insurance Company (SIC) 20 12T 1/13/17 2/20/17 Auto 5.0

ID Stillwater Insurance Company (SIC) 20 O17 9/15/17 10/22/17 Auto 5.0

IL Stillwater Insurance Company (SIC) 20 916 8/5/16 9/11/16 Auto 5.0

IN Stillwater Property and Casualty Insurance Company (SPC) 21 12T 1/13/17 2/20/17 Auto 5.0

MN Stillwater Insurance Company (SIC) 20 O17 2/16/18 2/16/18 Auto 5.0

MO Stillwater Insurance Company (SIC) 20 HLR 10/8/16 11/14/16 Legacy

NE Stillwater Insurance Company (SIC) 20 617 4/28/17 6/4/17 Legacy

NV Stillwater Insurance Company (SIC) 20 HLR 9/30/16 11/6/16 Legacy

NM Stillwater Property and Casualty Insurance Company (SPC) 21 HLR 11/18/16 12/25/16 Legacy

OH Stillwater Insurance Company (SIC) 20 D15 11/20/15 12/27/15 Legacy

OR Stillwater Property and Casualty Insurance Company (SPC) 21 717 8/11/17 9/17/17 Auto 5.0

RI Stillwater Property and Casualty Insurance Company (SPC) 21 717 6/9/17 7/16/17 Auto 5.0

SC Stillwater Insurance Company (SIC) 20 D17 4/13/18 5/20/18 Auto 5.0

TN Stillwater Property and Casualty Insurance Company (SPC) 21 317 2/3/17 3/12/17 Auto 5.0

TX Stillwater Insurance Company (SIC) 20 917 10/6/17 11/12/17 Auto 5.0

UT Stillwater Insurance Company (SIC) 20 915 10/1/16 10/1/16 Auto 5.0

VA Stillwater Insurance Company (SIC) 20 317 11/17/17 11/17/17 Auto 5.0

WA Stillwater Property and Casualty Insurance Company (SPC) 21 717 3/2/18 4/8/18 Auto 5.0

WI Stillwater Property and Casualty Insurance Company (SPC) 21 HLR 9/30/16 11/6/16 Legacy

◄Back to Table of Contents ◄Back to Table of Contents

Auto

5

Company Website

www.stillwater.com

Underwriting & Submissions

Phone: 1-800-849-6140

Fax: 1-866-699-1936

Email: [email protected]

Service Hours

Customer Service Representatives are available to meet your ser-

vice needs and for technical assistance:

Monday - Friday 8:00am - 9:00pm Eastern

Saturday 8:00am – 3:00pm Eastern

Service & Endorsements

Phone: 1-800-849-6140

Fax: 1-866-877-6355

Email: [email protected] Evidence of Insurance Requests for Evidence of Insurance can be emailed to: [email protected] or faxed to 1-888-333-2490

Mailing Address

Stillwater Insurance Group

P.O. Box 45126

Jacksonville, FL 32232-5126

Physical Address (for Overnight deliveries)

Stillwater Insurance Group

4905 Belfort Rd, STE 110

Jacksonville, FL 32256

Claims

Toll Free: 1-800-220-1351

Fax Number: 1-800-491-7683 or 1-402-242-4872

Email: [email protected]

Claims Mailing Address

Stillwater Insurance Group

12500 I Street, STE 100

Omaha, NE 68137

◄Back to Table of Contents ◄Back to Table of Contents

Auto

6

Claims Procedures

All claims are to be reported to Stillwater Claims Service immediately.

For fast claims service and to completely eliminate your time involvement in processing claims forms, please instruct your insureds and claimants to call our

claims department directly. This procedure will eliminate non-productive time and give the company the opportunity to give both your client and claimants

immediate direct claim service.

General Information:

• Please remember that you have no claims settlement authority. Please refer all claims to our claims department.

• The toll free line is (800)220-1351.

• The toll free number is answered by Stillwater staff during the following hours:

— Monday - Friday from 8:00am - 8:00pm Eastern

— Saturday from 8:00am - 6:00pm Eastern

After these hours a service called Lynx Services LLC answers the 800 line and can take a first notice of loss. They can take the initial claims info,

but cannot verify coverage. Lynx Services LLC is available 24/7.

• If there is a genuine and severe emergency or very severe loss the Lynx Services rep can in most cases get a Stillwater adjuster in touch with the client.

• We offer a translation service where English is a second language. The service handles dozens of languages including Hmong, Farsi, Punjabi,

Mandarin, Cantonese and Vietnamese.

◄Back to Table of Contents ◄Back to Table of Contents

Auto

7

Claims Contact Numbers: • Phone (800) 220-1351

• Fax (402) 351-2650 or 1-800-491-7683

• Email: [email protected]

Letter of Experience Stillwater Insurance is able to provide a letter that shows the insured’s Loss History while insured with Stillwater Insurance Group.

Please send a request to: [email protected] or via fax: 1-800-491-7683

• Please include the policy number

• Please allow 24 – 48 hours to process the request.

• Upon completion the Letter of Experience will be emailed.

• If the LOE needs to be forwarded to additional parties, please include that contact information in your email.

◄Back to Table of Contents ◄Back to Table of Contents

Auto

8

Upload Only You must upload all Stillwater policies through our quoting system, FIRST. We will not pay commission on paper applications. Non-Bound (Paper) Applications In Connecticut, an exception to uploading policies through FIRST is made when requesting Uninsured Motorist Bodily Injury limits higher than listed on our quoting system. In these situations, we require a paper application to be submitted to Underwriting for review. The application review may take up to 30 days from the receipt of the application. For consideration, the paper application must include the following – • A printout of the complete ACORD Application signed by the customer • Photos for all vehicles – 2 photos from opposite corners • Motor Vehicle Reports (MVRs) and Comprehensive Loss Underwriting Exchange (CLUE) reports • Any other applicable completed forms such as Driver Exclusion and Physician’s Opinion forms

Issue Date Policies can be issued a maximum of 90 days in the future. Backdating 1. We do NOT allow back dating of policies. 2. If an exception or a correction is needed, please contact Underwriting. 3. A statement of no losses is required. 4. Requests greater than 7 days will require a manager/supervisor’s approval. 5. A request greater than 30 days requires VP approval. 6. A cancellation request greater than 60 days requires VP approval.

◄Back to Table of Contents ◄Back to Table of Contents

Auto

9

Policy Period/Term Policies are issued and renewed with 6-month terms. Report Ordering While Stillwater does not bill agents for reports, it is something we monitor closely. Rewrites Policies need to be rewritten when there is a lapse in coverage greater than 30 days due to expiration or cancellation. Before submitting a rewritten policy, an override must be requested to allow a driver on a 2nd policy. Any remaining or waived balance on the previous policy must be received before an override is allowed. Please contact customer service to request an override. Note: Rewritten policies are not eligible for the Advance Quote discount (where applicable). Moratoriums • Submit authority may be suspended for new business or increased coverage endorsements during periods of imminent danger from natural disasters, or

when the National Weather Service has issued a severe weather warning.

• The types of natural disasters include but, are not limited to, Earthquake, Earth movement (landslide, mudslide, sinkhole, etc.), Wild Fire, Hurricane,

Tropical Storm, Tornado, and Flood.

• We reserve the right to suspend submission authority as we deem fit, and as allowed by state regulations and emergency orders.

• In the event of such suspension, we will issue a moratorium on FIRST. During moratoriums, no new business or increased coverage

endorsements may be submitted.

◄Back to Table of Contents ◄Back to Table of Contents

Auto

10

Application Submission

FIRST is a real-time Quoting and Underwriting system designed to assist our Producers in quoting and issuing insurance policies. This system provides an

easy way of doing business by indicating whether the risk is eligible and if so, allows the Producer to issue the policy instantly.

FIRST: Quote Questions

Responses to the various questions during the quote process will advise of underwriting eligibility conflicts. The producer does NOT have the authority to sub-

mit coverage for any vehicle exhibiting a conflict with one or more of the characteristics shown in our Underwriting Guidelines.

However, the Company may be contacted for prior approval regarding acceptability. Policy submission is subject to acceptance of the risk based on the Com-

pany Exposure Management Plan. All such requests should be emailed to [email protected] for consideration.

Submitting

Policies are only valid if they are issued on FIRST with a policy number. WE do NOT provide the Producer submission authority except through FIRST.

Click below for information on starting a Quote on FIRST:

◄Back to Table of Contents ◄Back to Table of Contents

Start an Auto Quote

Auto

11

◄Back to Table of Contents ◄Back to Table of Contents

Auto

12

Add Quote

"Add Quote" should be used when you start a quote for another line of business, like Auto. This will give you the option to pre-populate the new quote with the basic info from the HO or Dwelling quote. It also links the quotes and policies so that discounts can be applied and maintained. In addition, it makes servicing and supporting the quotes and policies easier.

◄Back to Table of Contents ◄Back to Table of Contents

Auto

13

Verification

As a part of new business process FIRST will order third-party data reports.

MVRs, CLUE, ADD (Additional Driver Discovery), & insurance bureau scores (if applicable).

Other forms may be applicable to the risk and may be requested.

Additional Driver Discovery (ADD)

Please verify the relationship between the insured and the driver(s) listed on the Additional Driver Discovery (ADD) report. Also tell us if they are a

member of the insured’s household. If they are not a household resident, please advise if there is regular access to drive the insured’s vehicle(s).

Prior Auto Insurance Proof

Any of these items must include the named insured and most recent term with expiration date and previous liability limits.

• Declarations page;

• Cancellation notice;

• Nonrenewal notice;

• Print-out from an agency management system.

The named insured on the new Stillwater policy must be the named insured on the prior policy or a listed driver on the prior policy.

Identification (ID) cards will be considered at minimum limits if the liability limits are not displayed.

Anything sent in other than what is stated above will cause the policy to be re-rated without prior insurance.

Documentation of an acceptable reason for not having prior insurance may also be considered on an exception basis.

◄Back to Table of Contents ◄Back to Table of Contents

Click Next for additional Verification guidelines: Next

Auto

14

Policy Questionnaires

The company may mail a new business or renewal questionnaire to the policyholder. Typically a timely response is required to enable the continuation or renewal of the policy. Some risks may require additional forms to be submitted: Example: If a previously unlisted driver is excluded from the policy, a signed driver exclusion form will be required* To avoid notice, potential changes, or possible cancellation of a policy, please fax required forms and/or information with your original submission to: (866) 699-1936, or email to [email protected]. If applicable forms are not signed and submitted, or requested information is not provided to us within 7 business days of notice, we will adjust and rerate the policy accordingly or possibly cancel the policy if it is no longer eligible for our program.

*Please print application forms from the “Application Forms” link under Quick Links in the right margin of any auto quote. Forms are also available on the “Policy Forms” menu from the Client List screen on FIRST.

◄Back to Table of Contents ◄Back to Table of Contents

Click Next for additional Verification guidelines: Next

Auto

15

Renewal Verification

Phone Interviews

The company may periodically contact the policyholder to conduct a phone interview.

Quality Planning Corporation (QPC)

QPC is a nationally recognized company based in San Francisco that is part of ISO (Insurance Services Office - a leading source of information and

databases related to Property & Casualty business.) QPC performs renewal underwriting questionnaires for many top-flight companies in CA and

across the nation and we have engaged them to help verify and correct basic risk and rating data on our auto renewals. The process is as follows:

• QPC mails letters asking policyholders to confirm rating information within 14-21 days.

• We are manually entering a note on the AS400 to indicate this. In due course this note will be added automatically. It will say the following or

something similar: QPC CA AUTO QUESTIONNAIRE MAILED.

There are two letters:

1. One letter with a website address to allow an on-line response on policies (with the PIN provided in the letter) where we are only pursuing a

potential annual mileage disparity.

2. One without the website address on policies where we might be pursuing something else/additional (e.g. potential missing driver).

• They are asked to call QPC toll free at (866)-634-4830 for English and (855)-571-9775 for Spanish between 6am-8pm PST (Mon-Fri) and

6am -2pm PST (Sat). Or they can log-on to stillwater.autopolicyupdate.com

• The calls are answered by a team in Canada. These are highly professional call-center staff who are very well scripted in how to handle

and help callers. Although the CSRs are in Canada, the data is all securely maintained on the QPC servers in San Francisco.

• QPC may send a follow-up letter or make outbound calls to selected policy policyholders who did not respond to the letter.

• QPC transmits the acquired data to us.

• We enter the updated information in the green screens and send the renewal offer.

◄Back to Table of Contents ◄Back to Table of Contents

Auto

16

Document Send to Company

Retain in Agency File Requirement

Application X Completed and signed by named insured(s) and agent

UM Selection Rejection X X Completed and signed by named insured(s). Send to company if UM is waived or reduced

PIP Selection rejection X X Completed and signed by named insured(s). Send to company if PIP is waived.

Discounts X X Documents to support good student, distant student, affinity/group program and defensive driving programs

EFT X Signed electronic funds transfer (EFT) form

Credit Card X Signed credit card authorization

Not At-Fault Accident X X Letter of Experience - Proof to support an at-fault accident was not at fault

Driver Exclusion X X Signed exclusion form listing all persons excluded from coverage

Proof of special equipment X X If custom equipment is purchased

Proof of Prior X X Required if information is missing or incorrect on current carrier report

Photos and Inspections X X As required by state (CA, FL)

Physician’s Opinion Form X X Required for drivers 75 years of age or over

File Maintenance and Audit Requirements You are required to maintain relevant documentation for a period of seven years after the policy expiration plus the additional statutory requirements for record retention after the policy is non-renewed or cancelled.

◄Back to Table of Contents ◄Back to Table of Contents

Auto

17

REQUIRED FORMS

Uninsured/Underinsured Motorist Option Form The UMBI form or waiver must be signed when deleting UMBI coverage, when UMBI is less than the BI limit, and when the non-stacked option is purchased in FL. The UMPD form or waiver must be signed when deleting UMPD coverage. If the signed UM/UIM Option form is not provided, we will add coverage and/or raise the limits. For UM changes in CT legacy (SPC), please send a request to [email protected], the form requirements are handled manually.

Proof of Not At-fault (NAF) Accident Please provide proof in the form of either a letter of experience from the prior carrier or a police report with accident details stating that the insured was not at fault. If proof is not received, the accident will be rated as an at fault accident.

Personal Injury Protection (PIP) Selection (only applicable in FL, MN, OR, TX, and WA) In applicable states, the PIP Selection form must be completed, signed, and included with your submission. Different Addresses If the mailing address is different than the garaging address, please provide the reason why they are different. If this critical underwriting information is not received, the policy will be canceled for underwriting reasons.

Driver Exclusion Please provide the signed and completed Driver Exclusion form. Failure to return this required form will result in the cancellation of the policy. Please click here for more information on Driver Exclusions.

Click Next for additional required Document Requirements:

◄Back to Table of Contents ◄Back to Table of Contents

Next

Auto

18

REQUIRED FORMS continued….

Florida Pre-Inspection Inspection will be waived if any of the conditions below are met:

1) If the vehicle garaging address is not in the following counties: Duval, Palm Beach, Broward, Dade, Orange, Hillsborough, and Pinellas.

2) If the vehicle is a new purchase or new lease from a licensed motor vehicle dealer or leasing company.

a. Note: Proof required:

i. Bill of sale, buyer’s order, or lease agreement that contains full description of motor vehicle or;

ii. Copy of the title or registration that shows transfer of ownership from dealer or leasing company to the customer and copy of the window sticker.

3) If the policyholder has been insured for two or more years without interruption on a private passenger automobile policy where physical damage was

provided.

4) If the vehicle is 10 or more years old as determined by

a. (Current Year – Model Year) e.g. 2016 – 2006 = 10, so 2006 vehicles or older are waived for inspection in 2016.

5) If the policy is a renewal or part of an agency book transfer and the policy does not have a change in vehicles or coverages.

6) If the authorized inspection service has no facility within 10 miles of the vehicle’s garaging location.

At new business, the inspection form must be completed and sent to Stillwater within 7 days of the policy effective date. For mid-term changes, the form must

be completed and sent in within 7 days of the effective date of the change.

Vehicle Inspection Sites (FL Only)

If the agency is unable to conduct the inspection, agents can send customers that require a vehicle inspection to Carco inspection sites. To find the Carco pre-

inspection site that is nearest to the policyholder, visit Carco’s website.

http://www.carcogroup.com/vehicle_inspections.php

The agent or customer can input their zip code at the bottom.

Or call Carco at 1-888-242-1200.

◄Back to Table of Contents ◄Back to Table of Contents

Auto

19

REQUIRED FORMS continued….

Photos (Lapse in Coverage) If physical damage coverage is requested on a vehicle where there is a lapse in coverage, then two photos of the vehicle must accompany the application. Please provide us with at least two photos of the vehicle that clearly show all four sides. If the photos are not provided, the policy will be cancelled for underwriting reasons. Expired Driver’s License If it has been noted that a driver has an expired license, please provide us with a copy of his/her renewed driver’s license or a letter from the DMV stating that his/her license has been renewed. If documentation is not provided, this policy will be cancelled for underwriting reasons.

Business Use If the policy has been rated with a Business Use vehicle and it’s noted the insured is a self-employed, please specify how the vehicle is being used and confirm that the vehicles insured under this policy are not being used in the course of the insured’s employment.

Garaged at School If a vehicle is listed as garaged at school, please provide the school’s address. If this critical underwriting information is not received, the policy will be canceled for underwriting reasons. Students away at school with a vehicle, in or out of the state and not located in Michigan can be considered.

Proof of Marital Status if Spouse/Partner is Excluded Please provide proof in the form of a photocopy of the marriage license/certificate or a photocopy of the most recent tax filing. Please click here for more information on Marital Status. **Not Required in California

◄Back to Table of Contents ◄Back to Table of Contents

Auto

20

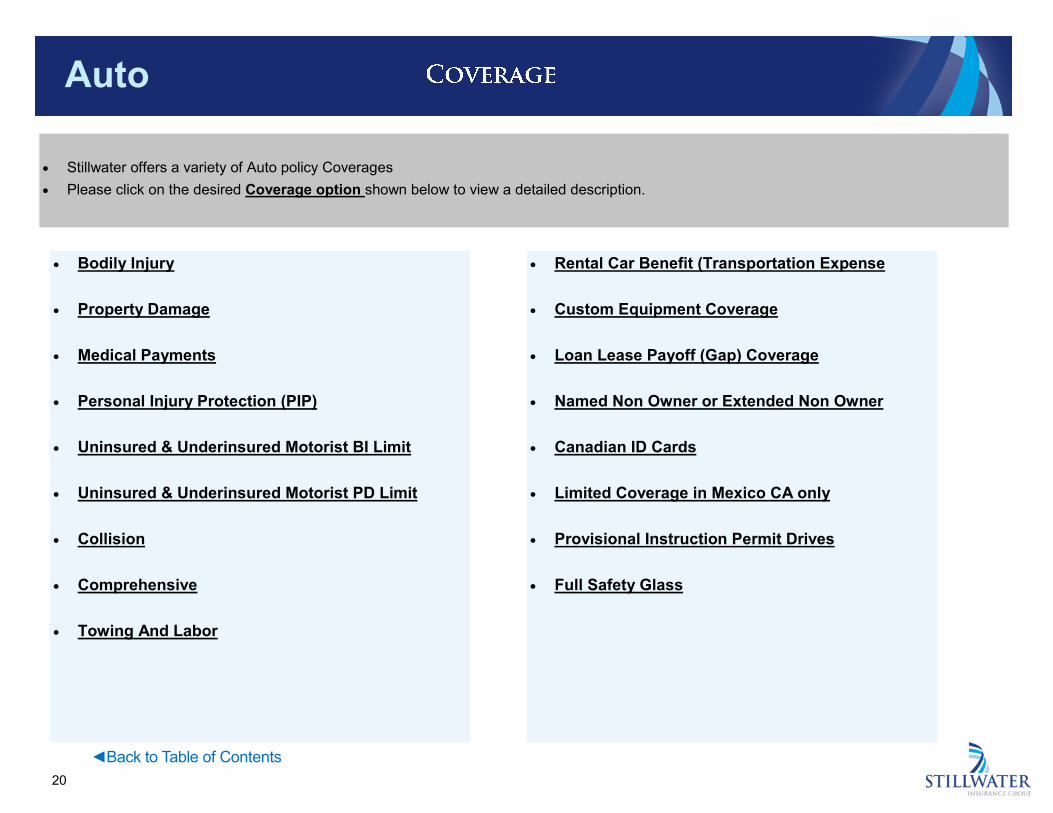

• Stillwater offers a variety of Auto policy Coverages

• Please click on the desired Coverage option shown below to view a detailed description.

• Bodily Injury

• Property Damage

• Medical Payments

• Personal Injury Protection (PIP)

• Uninsured & Underinsured Motorist BI Limit

• Uninsured & Underinsured Motorist PD Limit

• Collision

• Comprehensive

• Towing And Labor

• Rental Car Benefit (Transportation Expense

• Custom Equipment Coverage

• Loan Lease Payoff (Gap) Coverage

• Named Non Owner or Extended Non Owner

• Canadian ID Cards

• Limited Coverage in Mexico CA only

• Provisional Instruction Permit Drives

• Full Safety Glass

◄Back to Table of Contents ◄Back to Table of Contents

Auto

21

Bodily Injury – Limits must be equal to or higher than the minimum financial responsibility limits required by law. All vehicles on the policy insured for liability coverages must carry the same liability limits

Property Damage – Limits must be equal to or higher than the minimum financial responsibility limits required by law. All vehicles on the policy insured for liability coverages must carry the same liability limits

Medical Payments Limits – Medical Payments limits apply to each person, for each accident. If selected, all vehicles on the policy must carry the same medical limits.

Personal Injury Protection – Personal Injury Protection (PIP) limits apply for each accident. If selected, all vehicles on the policy must carry the same PIP limits. In states where PIP and Medical Payments are offered, PIP cannot be purchased if Medical Payments is selected.

Uninsured and Underinsured Motorist BI Limits – This coverage is required under all vehicle liability policies insuring the owner of a motor vehicle, unless rejected by your customer. If this coverage is purchased on one vehicle on a policy, it must be purchased on all vehicles on the policy insured for liability coverages. Note: This coverage cannot be rejected in Oregon or Illinois.

Click on the Coverage to view limits and availability by state:

◄Back to Table of Contents ◄Back to Table of Contents

◄Back to Coverage Menu ◄Back to Coverage Menu

Auto

22

◄Back to Table of Contents

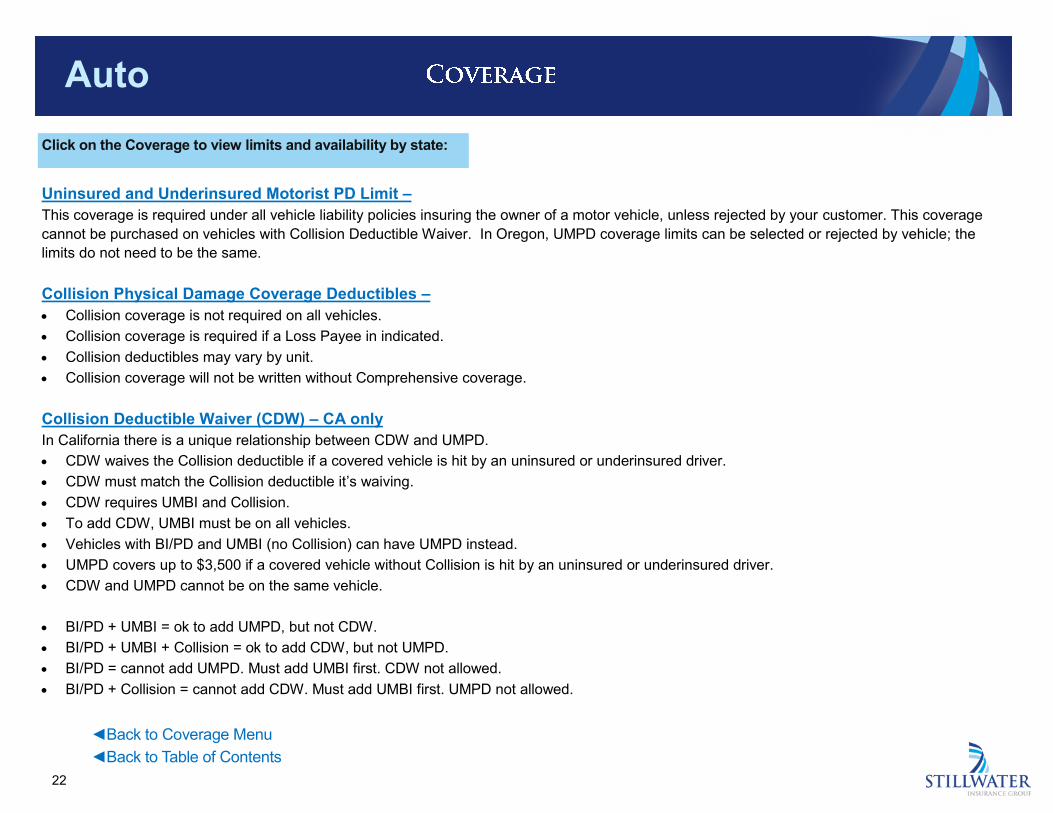

Uninsured and Underinsured Motorist PD Limit –

This coverage is required under all vehicle liability policies insuring the owner of a motor vehicle, unless rejected by your customer. This coverage

cannot be purchased on vehicles with Collision Deductible Waiver. In Oregon, UMPD coverage limits can be selected or rejected by vehicle; the

limits do not need to be the same.

Collision Physical Damage Coverage Deductibles –

• Collision coverage is not required on all vehicles.

• Collision coverage is required if a Loss Payee in indicated.

• Collision deductibles may vary by unit.

• Collision coverage will not be written without Comprehensive coverage.

Collision Deductible Waiver (CDW) – CA only

In California there is a unique relationship between CDW and UMPD.

• CDW waives the Collision deductible if a covered vehicle is hit by an uninsured or underinsured driver.

• CDW must match the Collision deductible it’s waiving.

• CDW requires UMBI and Collision.

• To add CDW, UMBI must be on all vehicles.

• Vehicles with BI/PD and UMBI (no Collision) can have UMPD instead.

• UMPD covers up to $3,500 if a covered vehicle without Collision is hit by an uninsured or underinsured driver.

• CDW and UMPD cannot be on the same vehicle.

• BI/PD + UMBI = ok to add UMPD, but not CDW.

• BI/PD + UMBI + Collision = ok to add CDW, but not UMPD.

• BI/PD = cannot add UMPD. Must add UMBI first. CDW not allowed.

• BI/PD + Collision = cannot add CDW. Must add UMBI first. UMPD not allowed.

◄Back to Coverage Menu

◄Back to Table of Contents

◄Back to Coverage Menu

Click on the Coverage to view limits and availability by state:

Auto

23

◄Back to Table of Contents

◄Back to Coverage Menu

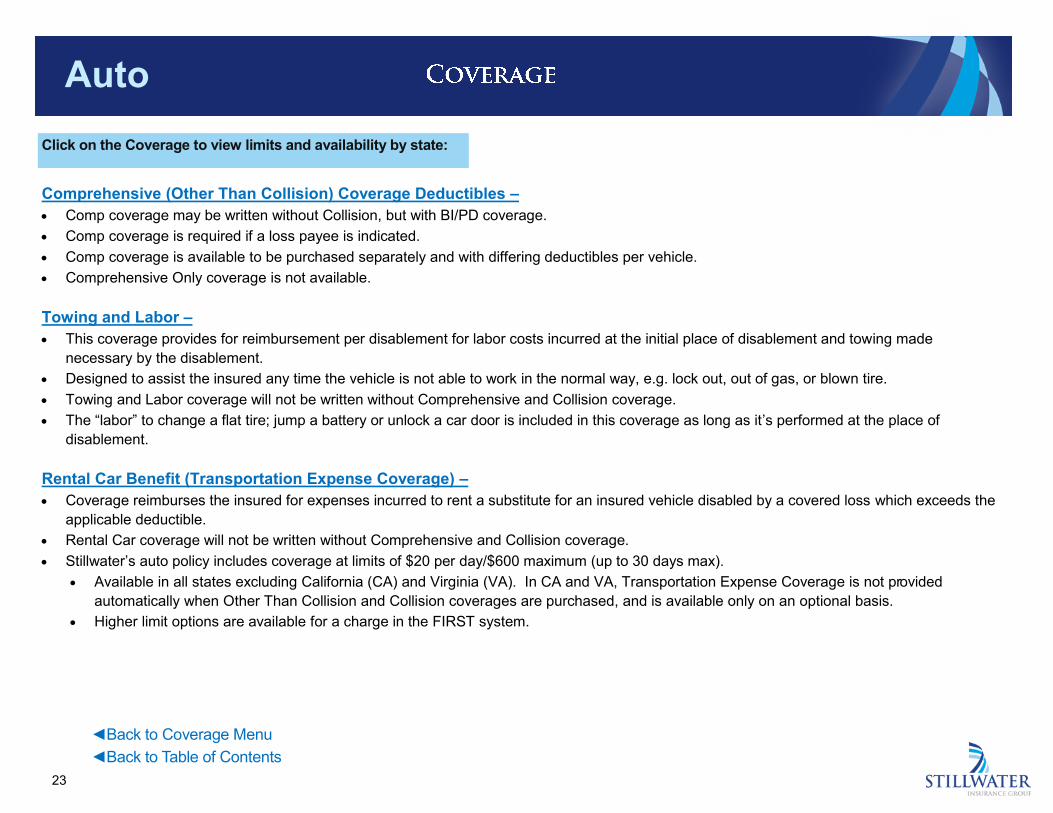

Comprehensive (Other Than Collision) Coverage Deductibles –

• Comp coverage may be written without Collision, but with BI/PD coverage.

• Comp coverage is required if a loss payee is indicated.

• Comp coverage is available to be purchased separately and with differing deductibles per vehicle.

• Comprehensive Only coverage is not available.

Towing and Labor –

• This coverage provides for reimbursement per disablement for labor costs incurred at the initial place of disablement and towing made

necessary by the disablement.

• Designed to assist the insured any time the vehicle is not able to work in the normal way, e.g. lock out, out of gas, or blown tire.

• Towing and Labor coverage will not be written without Comprehensive and Collision coverage.

• The “labor” to change a flat tire; jump a battery or unlock a car door is included in this coverage as long as it’s performed at the place of

disablement.

Rental Car Benefit (Transportation Expense Coverage) –

• Coverage reimburses the insured for expenses incurred to rent a substitute for an insured vehicle disabled by a covered loss which exceeds the

applicable deductible.

• Rental Car coverage will not be written without Comprehensive and Collision coverage.

• Stillwater’s auto policy includes coverage at limits of $20 per day/$600 maximum (up to 30 days max).

• Available in all states excluding California (CA) and Virginia (VA). In CA and VA, Transportation Expense Coverage is not provided

automatically when Other Than Collision and Collision coverages are purchased, and is available only on an optional basis.

• Higher limit options are available for a charge in the FIRST system.

◄Back to Table of Contents

◄Back to Coverage Menu

Click on the Coverage to view limits and availability by state:

Auto

24

◄Back to Table of Contents

◄Back to Coverage Menu

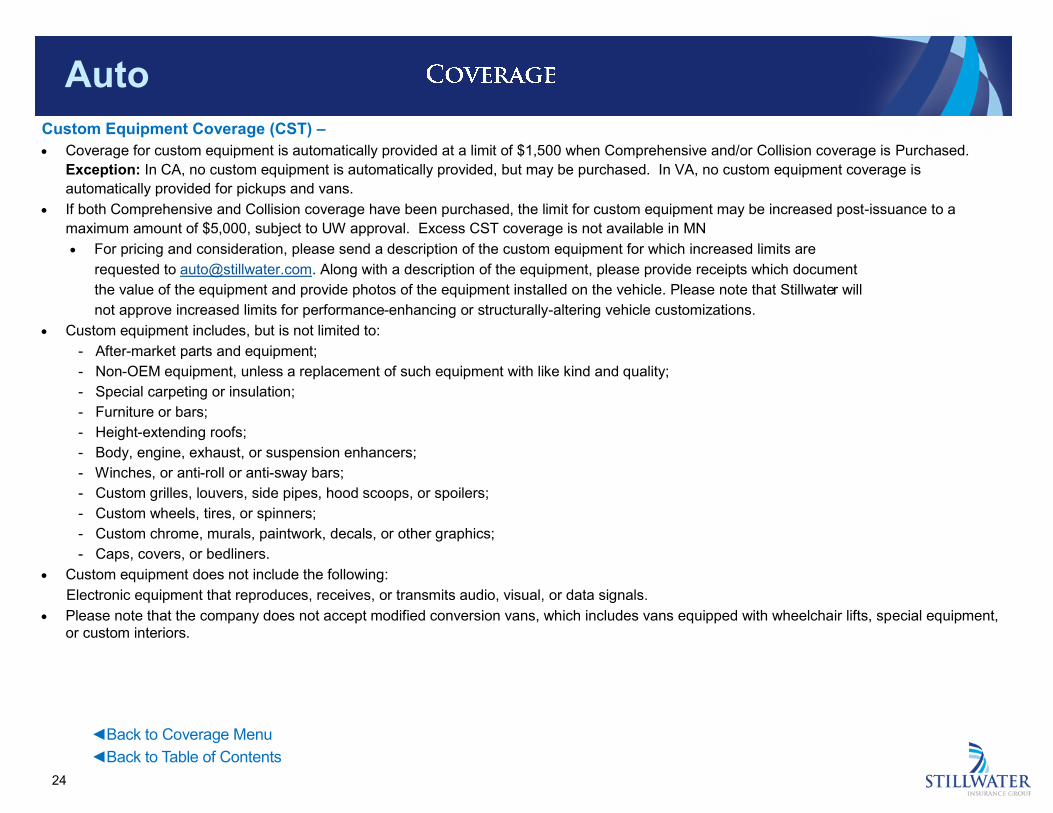

Custom Equipment Coverage (CST) –

• Coverage for custom equipment is automatically provided at a limit of $1,500 when Comprehensive and/or Collision coverage is Purchased.

Exception: In CA, no custom equipment is automatically provided, but may be purchased. In VA, no custom equipment coverage is

automatically provided for pickups and vans.

• If both Comprehensive and Collision coverage have been purchased, the limit for custom equipment may be increased post-issuance to a

maximum amount of $5,000, subject to UW approval. Excess CST coverage is not available in MN

• For pricing and consideration, please send a description of the custom equipment for which increased limits are

requested to [email protected]. Along with a description of the equipment, please provide receipts which document

the value of the equipment and provide photos of the equipment installed on the vehicle. Please note that Stillwater will

not approve increased limits for performance-enhancing or structurally-altering vehicle customizations.

• Custom equipment includes, but is not limited to:

- After-market parts and equipment;

- Non-OEM equipment, unless a replacement of such equipment with like kind and quality;

- Special carpeting or insulation;

- Furniture or bars;

- Height-extending roofs;

- Body, engine, exhaust, or suspension enhancers;

- Winches, or anti-roll or anti-sway bars;

- Custom grilles, louvers, side pipes, hood scoops, or spoilers;

- Custom wheels, tires, or spinners;

- Custom chrome, murals, paintwork, decals, or other graphics;

- Caps, covers, or bedliners.

• Custom equipment does not include the following:

Electronic equipment that reproduces, receives, or transmits audio, visual, or data signals.

• Please note that the company does not accept modified conversion vans, which includes vans equipped with wheelchair lifts, special equipment,

or custom interiors.

◄Back to Table of Contents

◄Back to Coverage Menu

Auto

25

Loan Lease Payoff (Gap) Coverage –

• This is for new vehicles (previously unregistered) within 60 days of lease or purchase. Exception: If a private passenger auto, pickup or van was

previously afforded this coverage with another carrier and otherwise meets the eligibility requirements of this rule, then coverage may be

afforded. Please provide proof to [email protected] for consideration.

• If an owned automobile sustains a total loss, the Company will pay, in addition to any amounts otherwise payable under Part III –

Physical Damage, the difference between:

• The actual cash value of the owned automobile at the time of the total loss reduced by the applicable deductible, in any, shown on the

declarations and by its salvage value if the insured retains the salvage; and

• Any greater amount the owner of the owned automobile is legally obligated to pay under a written loan or lease agreement to which the

owned automobile is subject at the time of the total loss, reduced by

• Any unpaid finance charges or refunds due to the owner for such charges;

• excess mileage charges or charges for wear and tear; charges for extended warranties or refunds due to the owner for extended warranties;

charges for credit insurance or refunds due to the owner for credit insurance;

• past due payments and charges for past due payments; or collection or repossession expenses.

◄Back to Table of Contents

◄Back to Coverage Menu

◄Back to Table of Contents

◄Back to Coverage Menu

Auto

26

Named Non-owner or Extended Non-owner Policies

Stillwater does not offer non-owner or extended non-owner coverage

Canadian Insurance Card

1. Car insurance in Canada is mandatory, regardless of whether you’re driving your personal vehicle or renting one.

2. In most cases, coverage is provided if you drive into Canada.

3. If a Canadian Insurance Card is needed, please a request to [email protected].

4. Please allow 3-5 business days.

Limited Coverage in Mexico (CA policies only)

Limited Coverage is available on California policies only based on the following guidelines:

Policy Period, Territory: This insurance applies only to loss to a motor vehicle insured hereunder and accidents which occur during the policy period

in the United States of America, its territories or possessions, or Canada, or while such vehicle is being transported between ports thereof. This

insurance also applies under Parts II and III to such accidents and loss in Mexico within 50 miles of the United States boundary. Loss in Mexico

under Part III shall be determined upon the basis of cost at the nearest United States point.

If such a loss occurs in any referenced state or jurisdiction other than where your owned automobile is principally garaged, coverage will apply as

follows:

1. If the state or jurisdiction has:

a) A financial responsibility or similar law specifying limits of liability for bodily injury and property damage (Part I) higher than the limit shown in

the declarations, your policy will provide the higher specified limit.

b) A compulsory insurance or similar law requiring a non resident to maintain insurance whenever the non resident uses a vehicle in that state

or jurisdiction, your policy will provide at least the required amounts and types of coverage.

2. No one will be entitled to duplicate payments for the same elements of loss.

WARNING

Unless you have automobile insurance written by a Mexican insurance company, you may spend many hours or days in jail, if you have an accident in Mexico. Insurance coverage should be secured from a company licensed under the laws of Mexico to write such insurance in order to avoid complications and some other penalties possible under the laws of Mexico, including the possible impoundment of your automobile.

◄Back to Table of Contents

◄Back to Coverage Menu

◄Back to Table of Contents

◄Back to Coverage Menu

Auto

27

◄Back to Table of Contents

◄Back to Coverage Menu

Provisional Instruction Permit Drivers –

• The purpose of this endorsement is to offer a facility to families whose children under age 16 who have a permit and not a full license. Drivers

who are not resident children of the named insured and spouse do not qualify. The permit holder is eligible to drive his/her parent’s vehicles

insured on the Stillwater policy, with no increase in premium until they reach 16 years of age. As soon as the permit holder attains age 16 or is

licensed (whichever occurs sooner) he/she will be added to the policy as a driver and the appropriate premium will be charged. Driving

experience credit begins once they are rated as a driver.

• The Provisional Instruction Permit Driver form must be completed. Failure to do so will result in an endorsement to add the permit holder as a

rated driver. Please be sure to indicate whether you are adding a permit driver or a rated driver.

• All normal underwriting criteria apply to the permit holder. Misrepresentation of warranty questions may lead to a declination to add the driver and

possibly to rescission.

Full Safety Glass Coverage –

• This coverage provides for repair or replacement of damaged safety glass with no deductible.

• This coverage is available for additional premium. Comprehensive coverage is required.

• Available in AZ, CT, ID, IL, IN, MN, OR, RI, TN, TX, UT, VA, and WA. In FL, it is included as part of Comprehensive coverage without additional

premium. In SC, it is a separate coverage and is automatically added when Comprehensive coverage is afforded.

◄Back to Table of Contents

◄Back to Coverage Menu

Auto

28

◄Back to Table of Contents

◄Back to Coverage Menu

AZ CA CO CT FL* ID IL IN MN MO NE NV NM OH OR RI TN TX UT VA WA WI SC

BI 15/30 15/30 25/50 20/40 10/20 25/50 25/50 25/50 30/60 25/50 25/50 25/50 25/50 15/30 25/50 25/50 25/50 30/60 25/65 25/50 25/50 25/50 25/50

20/40 25/50 50/100 25/50 15/30 50/100 50/100 50/100 50/100 50/100 50/100 50/100 50/100 20/40 50/100 50/100 50/100 50/100 50/100 50/100 50/100 50/100 50/100

25/50 50/100 100/300 50/100 20/40 100/300 100/300 100/300 100/300 100/300 100/300 100/300 100/300 25/50 100/300 100/300 100/300 100/300 100/300 100/300 100/300 100/300 100/300

50/100 100/300 250/500 100/300 25/50 250/500 250/500 250/500 250/500 250/500 250/500 250/500 250/500 50/100 250/500 250/500 250/500 250/500 250/500 250/500 250/500 150/300 250/500

100/300 250/500 250/500 50/100 100/300 250/500

250/500 100/300 250/500

250/500

PD 5 5 15 10 10 15 20 10 10 10 25 10 10 10 20 25 15 25 15 20 10 10 25

10 10 25 15 15 25 25 25 25 15 50 15 15 15 25 50 25 50 25 25 25 15 50

15 15 50 25 25 50 50 50 50 25 100 25 25 25 50 100 50 100 50 50 50 25 100

25 25 100 50 50 100 100 100 100 50 50 50 50 100 100 100 100 100 50

50 50 100 100 100 100 100 100 100

100 100

MP MP MP MP MP MP MP MP MP PIP MP MP MP MP MP PIP MP MP MP PIP MP PIP MP MP

PIP 500 500 5,000 500 5,000 500 500 1,000 Stacked 500 500 500 500 500 15 2,000 500 500 0 1,000 10 1,000 500

1,000 1,000 10,000 1,000 10,000 1,000 1,000 2,000 Non- 1,000 1,000 1,000 1,000 1,000 25 5,000 1,000 1,000 2,000 35 2,000 1,000

2,000 2,000 25,000 2,000 2,000 2,000 5,000 Stacked 2,000 2,000 2,000 2,000 2,000 50 10,000 2,000 2,500 5,000 5,000 2,000

5,000 3,000 5,000 5,000 5,000 10,000 Ded. 5,000 5,000 5,000 5,000 5,000 5,000 5,000 10,000 10,000 5,000

10,000 4,000 10,000 PIP 10,000 10,000 25,000 0 10,000 10,000 10,000 10,000 10,000 10,000 10,000 10,000

5,000 Basic $200 PIP

RepBen 250 Wk Loss 2,500

5,000 500 Wk Loss 5,000

10,000 1,000 Excl. 10,000

*In Florida, the max BI limits available are 100/300 for policies with more than 2 vehicles. This rule only applies to policies originally quoted on or

after 2/10/17

◄Back to Table of Contents

◄Back to Coverage Menu

Auto

29

◄Back to Table of Contents

◄Back to Coverage Menu

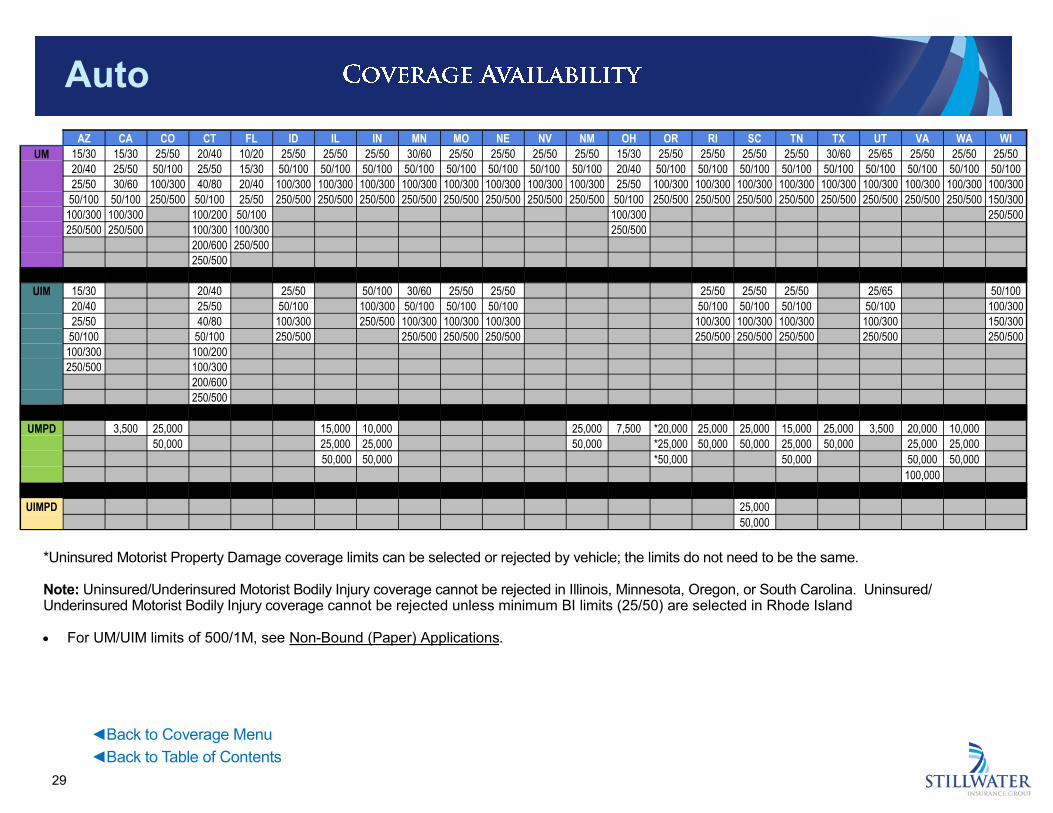

AZ CA CO CT FL ID IL IN MN MO NE NV NM OH OR RI TN TX UT VA WA WI SC

UM 15/30 15/30 25/50 20/40 10/20 25/50 25/50 25/50 30/60 25/50 25/50 25/50 25/50 15/30 25/50 25/50 25/50 30/60 25/65 25/50 25/50 25/50 25/50

20/40 25/50 50/100 25/50 15/30 50/100 50/100 50/100 50/100 50/100 50/100 50/100 50/100 20/40 50/100 50/100 50/100 50/100 50/100 50/100 50/100 50/100 50/100

25/50 30/60 100/300 40/80 20/40 100/300 100/300 100/300 100/300 100/300 100/300 100/300 100/300 25/50 100/300 100/300 100/300 100/300 100/300 100/300 100/300 100/300 100/300

50/100 50/100 250/500 50/100 25/50 250/500 250/500 250/500 250/500 250/500 250/500 250/500 250/500 50/100 250/500 250/500 250/500 250/500 250/500 250/500 250/500 150/300 250/500

100/300 100/300 100/200 50/100 100/300 250/500

250/500 250/500 100/300 100/300 250/500

200/600 250/500

250/500

UIM 15/30 20/40 25/50 50/100 30/60 25/50 25/50 25/50 25/50 25/65 50/100 25/50

20/40 25/50 50/100 100/300 50/100 50/100 50/100 50/100 50/100 50/100 100/300 50/100

25/50 40/80 100/300 250/500 100/300 100/300 100/300 100/300 100/300 100/300 150/300 100/300

50/100 50/100 250/500 250/500 250/500 250/500 250/500 250/500 250/500 250/500 250/500

100/300 100/200

250/500 100/300

200/600

250/500

UMPD 3,500 25,000 15,000 10,000 25,000 7,500 *20,000 25,000 15,000 25,000 3,500 20,000 10,000 25,000

50,000 25,000 25,000 50,000 *25,000 50,000 25,000 50,000 25,000 25,000 50,000

50,000 50,000 *50,000 50,000 50,000 50,000

100,000

UIMPD 25,000

50,000

*Uninsured Motorist Property Damage coverage limits can be selected or rejected by vehicle; the limits do not need to be the same. Note: Uninsured/Underinsured Motorist Bodily Injury coverage cannot be rejected in Illinois, Minnesota, Oregon, or South Carolina. Uninsured/Underinsured Motorist Bodily Injury coverage cannot be rejected unless minimum BI limits (25/50) are selected in Rhode Island • For UM/UIM limits of 500/1M, see Non-Bound (Paper) Applications.

◄Back to Table of Contents

◄Back to Coverage Menu

Auto

30

◄Back to Table of Contents

◄Back to Coverage Menu

AZ CA CO CT FL ID IL IN MN MO NE NV NM OH OR RI TN TX UT VA WA WI SC

COMP 100 100 100 100 100 100 100 100 100 100 100 100 100 100 100 100 100 250 100 100 100 100 100

Ded. 200 200 200 200 200 200 250 250 250 200 200 200 200 200 250 250 250 500 250 200 250 200 250

250 250 250 250 250 250 500 500 500 250 250 250 250 250 500 500 500 1,000 500 250 500 250 500

500 500 500 500 500 500 1,000 750 750 500 500 500 500 500 1,000 750 750 1,500 750 500 1,000 500 750

1,000 1,000 1,000 1,000 1,000 1,000 1,500 1,000 1,000 1,000 1,000 1,000 1,000 1,000 2,000 1,000 1,000 2,000 1,000 1,000 2,000 1,000 1,000

2,000 2,000 2,000 2,000 1,500 1,500 1,500 1,500 1,500 1,500

2,500 2,000 2,000 2,000 2,000 2,000 2,000

COLL 250 250 200 200 200 200 250 250 250 250 250 250 250 250 250 250 250 250 250 250 250 250 250

Ded. 500 500 250 250 250 250 500 500 500 500 500 500 500 500 500 500 500 500 500 500 500 500 500

1,000 1,000 500 500 500 500 1,000 750 750 1,000 1,000 1,000 1,000 1,000 1,000 750 750 1,000 750 1,000 1,000 1,000 750

2,000 1,000 1,000 1,000 1,000 1,500 1,000 1,000 2,000 1,000 1,000 1,500 1,000 2,000 2,000 1,000

2,500 2,000 2,000 1,500 1,500 1,500 2,000 2,000 1,500 1,500

2,000 2,000 2,000 2,000 2,000

TOW 75 75 25 75 75 25 75 75 75 25 25 25 25 25 75 75 75 75 75 75 75 25 75

100 100 50 100 100 50 100 100 100 50 50 50 50 50 100 100 100 100 100 100 100 50 100

200 200 75 200 200 75 200 200 200 75 75 75 75 75 200 200 200 200 200 200 200 75 200

RNL* 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600 20/600

30/900 30/900 30/900 30/900 30/900 30/900 30/900 30/900 30/900 30/900 30/900 30/900 30/900 30/900 30/900 30/900 30/900 30/900 30/900 30/900 25/750 30/900 30/900

40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 40/1,200 35/1,050 40/1,200 40/1,200

50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500 50/1,500

70/2,100 75/2,250

75/2,250

100/3,000

*Rental (RNL) limits are listed as daily limit/maximum limit. Note: When Stillwater provides coverage for the same loss on both the home and auto policies, only one deductible (whichever is higher) will be

applied.

◄Back to Table of Contents

◄Back to Coverage Menu

Auto

31

◄Back to Table of Contents

1. Vehicles with a principal out-of-state garaging location

2. Vehicles used for;

• Delivering goods

• Racing or off road;

• Emergency Service; or

• Snowplowing

• Hire, lease, rental or transportation of passengers (including

Transportation Network Companies & ride-sharing services);

3. Artisan or Business Use:

• Travel to more than 2 job sites a day

• Driven by employees

• Not owned by the named insured or spouse

• Carries supplies

• Signage on vehicle

Any of the following Vehicles:

4. Not registered for street use;

5. That require a state or federal motor carrier permit to operate;

6. Motorhomes

7. Modified conversion vans

8. Equipped with cooking equipment or a bathroom

9. Rebuilt or structurally altered;

10. Modified for speed or performance

11. Used as a primary residence;

12. Commercial type such as step, panel and cutaway vans; flatbed,

stake beds and dump trucks

13. GVWR greater than 10,000 lbs.

14. Original Cost New greater than $125,000

15. Titled or owned/leased by a partnership or corporation,

16. Previously totaled, salvaged or reconstructed

17. High performance, Gray market, Exotic or limited production.

18. Aluminum or Titanium panel

19. Golf Carts, GEMs or Low Speed Vehicle

20. Incomplete vehicles

21. Vehicle with less than 4 wheels

22. Self-driving / Autonomous vehicles

23. Vehicles with a principal out-of-state garaging location in Michigan

or any county in which we do not accept personal auto insurance

applications.

◄Back to Table of Contents

Auto

32

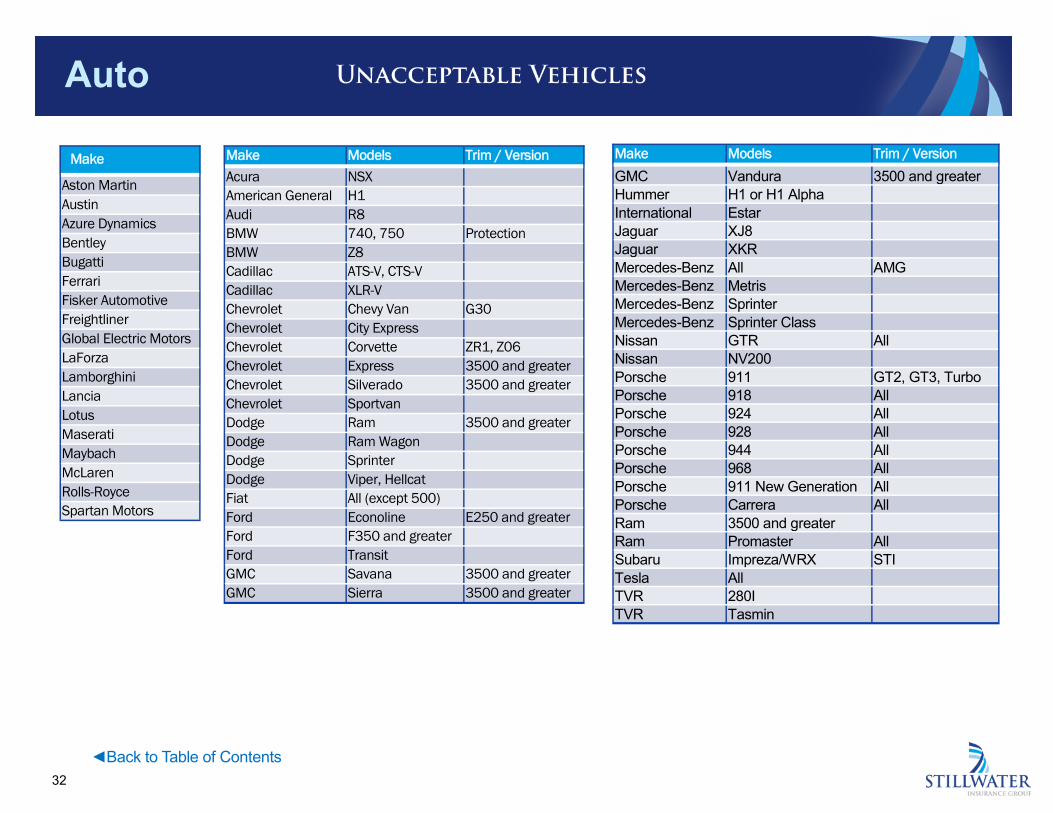

Make Aston Martin Austin Azure Dynamics Bentley Bugatti Ferrari Fisker Automotive Freightliner Global Electric Motors LaForza Lamborghini Lancia Lotus Maserati Maybach McLaren Rolls-Royce Spartan Motors

Make Models Trim / Version Acura NSX

American General H1

Audi R8

BMW 740, 750 Protection

BMW Z8

Cadillac ATS-V, CTS-V

Cadillac XLR-V

Chevrolet Chevy Van G30

Chevrolet City Express

Chevrolet Corvette ZR1, Z06

Chevrolet Express 3500 and greater

Chevrolet Silverado 3500 and greater

Chevrolet Sportvan

Dodge Ram 3500 and greater

Dodge Ram Wagon

Dodge Sprinter

Dodge Viper, Hellcat

Fiat All (except 500)

Ford Econoline E250 and greater

Ford F350 and greater

Ford Transit

GMC Savana 3500 and greater

GMC Sierra 3500 and greater

Make Models Trim / Version GMC Vandura 3500 and greater

Hummer H1 or H1 Alpha

International Estar

Jaguar XJ8

Jaguar XKR

Mercedes-Benz All AMG

Mercedes-Benz Metris

Mercedes-Benz Sprinter

Mercedes-Benz Sprinter Class

Nissan GTR All

Nissan NV200

Porsche 911 GT2, GT3, Turbo

Porsche 918 All

Porsche 924 All

Porsche 928 All

Porsche 944 All

Porsche 968 All

Porsche 911 New Generation All

Porsche Carrera All

Ram 3500 and greater

Ram Promaster All

Subaru Impreza/WRX STI

Tesla All

TVR 280I

TVR Tasmin

◄Back to Table of Contents ◄Back to Table of Contents

Auto

33

Prohibited

1. Any vehicle which is not a passenger car or truck is prohibited.

2. Any vehicles over 10,000 pounds GVWR, over 10,000 pounds shipping weight, or over $150,000 base MSRP

3. Certain high-performance and exotic vehicles are prohibited/referred on a case-by-case basis.

4. If the company is required to accept the vehicle under state law, coverage will be limited to liability only.

Model Year

The model year is determined by the vehicle’s original manufacturer.

Pre-1981 vehicles

1. Liability coverage may be purchased.

2. Comprehensive and Collision coverage is also available on multi-car policies where at least one other vehicle carries liability coverage.

3. The company does not offer “Agreed Value” coverage, widely regarded as the best protection for collector or classic cars.

4. The company uses the “Average Retail Value” per NADA Guides (www.nadaguides.com) for all vehicles manufactured prior to 1981.

5. The value of the vehicle may be written up to the “Average Retail Value” value not to exceed $10,000.

6. If a total loss occurs, the company will only pay the lesser value (either the actual cash value or the value entered) – minus the deductible.

◄Back to Table of Contents ◄Back to Table of Contents

Auto

34

Referred

Due to the uniqueness of certain vehicles, the following criteria will require underwriting approval prior to purchasing the policy.

1. Any vehicles which are indicated to be a Cargo Van/Passenger Van greater than 6,000 pounds GVWR.

2. Any vehicle with a base model and/or trim options between $125,000 and $150,000 base MSRP

Trucks and Vans

Certain trucks and vans are unacceptable unless approved by underwriting prior to issuance. If a possible commercial vehicle or any other referred

vehicle is not approved by UW prior to binding, the policy may be subject to cancellation.

Please send the following information to [email protected] for consideration.

• Information regarding occupation/usage

• Photos showing all 4 sides of the vehicle

• A signed commercial use exclusion form except VA (list under quick links)

◄Back to Table of Contents ◄Back to Table of Contents

Auto

35

◄Back to Table of Contents

Photo/Inspection Requirements (CA Only) 1) When Physical Damage coverage is included on a policy any pre-existing damage should be noted and kept with the application information.

2) The Agent is responsible for taking two photos per inspection from each opposite corner of the vehicle. Please retain the photos in your agency

files for audit and claim purposes. Additional Inspections may be requested at the company’s discretion.

3) Photos are required on all vehicles that are requesting physical damage coverage with the following exceptions:

4) Vehicles that are new and unused and purchased or leased from a dealer within the last 7 days

5) Additional or replacement vehicles will not require photos if the applicant has been continuously insured for the previous 12 months.

6) The named insured can provide proof of 6 months prior physical damage coverage without a lapse from an admitted California insurer, or provide

a copy of an inspection report completed on the vehicle within the last 12 months. Previously completed inspection reports should be retained in

your agency files.

7) If the named insured lives 45 miles or more from the agency’s office or if the drive to the office is more than 45 minutes, we will waive the

inspection requirement.

8) If a vehicle is listed in the makes and models on the Unacceptable Vehicles section or has a symbol assignment of 999, photo documentation

must be submitted with the application and is not eligible for waiver.

9) For Age of Vehicle, calculate based on October 1 of the current year

Please note: Submission of fictitious pictures by a producer or customer will be considered misrepresentation on the policy and is a

violation of the producer agreement

◄Back to Table of Contents

Auto

36

◄Back to Table of Contents

Pleasure Use

Vehicles not used for business or other purposes or not used for commuting to work or school. Typically used for “excess” or “unassigned” vehicles

and for retired drivers.

Personal/Commute-Work Use

The regular non-business use of a personal vehicle, including commuting to or from work or school.

Note: A vehicle used for driving to or from school is considered as used for driving to or from work.

Business Use:

The following are examples of some but not all types of eligible business use:

• Vehicles owned or leased by the applicant and used in their business or occupation, such as consultants and business contractors;

• Vehicles used by sales reps, such as realtors, insurance agents, manufacturer and company reps, and home-based sales, such as Avon, Mary

Kay and Tupperware;

• Vehicles used by professionals whose duties include travel to hospitals, clinics, courthouses, job sites or client homes, such as doctors, attor-

neys, architects, accountants, financial advisors, engineers and clergy;

• Vehicles used in a business for occasional errands

Ineligible Business Use

The following are examples of some but not all types of ineligible business use:

• vehicles used for transportation of passengers, such as: taxis or limousines;

• vehicles used for retail or wholesale delivery, such as: pizza, flowers, newspapers, mail, etc.

Farm Use

The vehicle is principally garaged on a farm or ranch and is not primarily used in going to or from work other than farming or ranching and is not used in any occupation other than farming or ranching.

Click Next for additional Vehicle Use Definitions: Next

◄Back to Table of Contents

Auto

37

◄Back to Table of Contents

Artisan (CA only)

The following are examples of some but not all types of eligible artisan use:

• self employed without employee (no self-employed nor a franchisee with employees)

• vehicle operated only by insured and listed family members

• vehicle visits (on average) no more than 3 job sites per day and is driven within a radius of 100 miles

• vehicle does not display special permanently installed equipment or signage - racks and mounted tool chests are not allowed

• vehicle does not carry equipment in excess of 500 lbs. and does not tow a trailer, nor have a flatbed or custom truck body

• vehicle is not a Heavy Duty type with a load capacity greater than 2,000 lbs.

• gross vehicle weight does not exceed 10,000 lbs.

• not used for transportation of material or supplies to the job site

Corporations, partnerships, and trusts cannot be listed as a named insured, second named insured or an additional insured, but may be

listed as an additional interest.

Annual Mileage (CA only)

The pre-approved minimum Annual Mileage in CA is 7,000. You must provide proof of Annual Mileage when selecting less than 7,000 miles.

◄Back to Table of Contents

Auto

38

◄Back to Table of Contents

1. Without a current, valid US driver’s license (We do not accept

foreign & international driver’s licenses)

2. Foreign nationals not having a verifiable U.S. driver’s license for 3

years.

3. Without a valid motor vehicle report or with an unverifiable driving

record; except when newly licensed

4. Without a specific, in-state garaging address;

5. Who are not permanent residents of the state seven months out of

year;

6. With permanently suspended or revoked licenses;

7. Under the minimum age for state licensing; (*Learners Permit is

Acceptable)

8. Who have been convicted of insurance fraud;

9. Employed in illegal enterprises and occupations;

10. Employed in occupations involving the use of an insured vehicle by

nonresident, non-dependent operators

11. Who have had a policy cancelled by us for loss experience or

misrepresentation

12. Youthful driver (under 21 years old) as a primary name insured.

(Not applicable in South Carolina)

13. With less than 3 years U.S. Driving experience, unless a newly

licensed U.S. driver residing in the same household where at least

one other rated driver has 3 or more years of U.S. driving

experience. We accept driving experience only from actual U.S.

states, not U.S. Territories such as Puerto Rico or Guam.

14. With less than 3 years since license reinstatement

15. Principal Operator(s) under 21 years of age unless they are part of

a family account insured by Stillwater with at least one adult

operator that is greater than or equal to 21 years or older. (Not

applicable in Oregon – OAR 836-0081-0010(1)(a))

16. Risks canceled, non-renewed or declined by Stillwater or any other

carrier. If there are exceptional circumstances, contact Customer

Service. (Not applicable in Oregon - OAR 836-0081-0010(1)(k))

17. With lapse in coverage 30 days or more. (Not applicable in

Oregon - OAR 836-0081-0010(1)(m))

18. 75 years or older without a physician’s opinion form. (Physician

signature not required in South Carolina)

19. Drivers that require a Financial Responsibility Filing (SR-22) at new

business, unless required by state law.

Note: MVRs are only available for display to internal staff.

◄Back to Table of Contents

*Exception — The rules above apply in all states except California. For California Auto Driver Eligibility, please see

the next pages for California Good Driver Program rules.

Auto

39

◄Back to Table of Contents ◄Back to Table of Contents

Prior Insurance Coverage—Does Not Include California

In Connecticut, Idaho, Indiana, Oregon, Rhode Island, and Texas, if there is a lapse in insurance coverage greater than 30 days, the policy requires a

PRE underwriting review.

Requests for review can be sent to [email protected].

Please include the quote number and supporting documentation, if available.

Acceptable reasons for a lapse greater than 30 days are:

• Military deployment

• Did not own a vehicle

• Did not operate a vehicle

• Company car

• Incarcerated

• Not required in the previous state of residence

• Out of the country

• Physically impaired or ill

• Covered by a self-indemnity bond.

The named insured or spouse that was not required to have insurance must take reasonable steps to obtain insurance within 15 days following the

expiration of such reason. The policy may be cancelled if appropriate proof is not provided.

In all other states:

The risk is only acceptable if the lapse is due to a Company car or Military deployment.

Auto

40

◄Back to Table of Contents

California Good Driver

All insured drivers must be CA Good Drivers. Exception: Unmarried, resident children who otherwise qualify, but have less than 3 years license

experience, and are listed on the parents’ application.

To qualify as a Good Driver, a driver must meet the following requirements:

1. The driver must have been continuously licensed to drive a motor vehicle for the preceding three years with a valid U.S. or Canadian license

(Applicant must provide Canadian MVR). If licensed less than three years in California, provide the out of state license number in order to

prove at least 3 years of license experience. (A suspended or revoked driver’s license within the past 3 years will disqualify a driver for the

Good Driver discount. An expired license will not.) Drivers with foreign driving experience will be considered to be Good Drivers if they

provide:

a. A written statement stating they had continuous licensing experience and qualifying driving records during the 36-month experience

period; AND

b. Proof that during the 18 months prior to the application effective date they have been continuously licensed to drive a motor vehicle

in the United States or Canada.

2. During the previous 3 years (or 18 months for foreign drivers per 1. b. above), the driver has not had:

• More than one violation point count; or

• An at fault accident which resulted in bodily injury or death;

• or More than one at fault accident, involving property damage only; or

• A combination of incidents that results in more than one violation point count being assessed (for example, one moving violation

and one at fault accident involving property damage only); or

• A two-point conviction.

3. A driver that has been convicted of the violations listed below will not qualify within 10 years of the violation date.

• Vehicle Code Sections 23140, 23152, 23153 and out of state codes 17, 18, A1 and A2 (DUI’s), a felony violation of Section 23550

or 23566, or former Section 23175

• Penal Code Section 191.5, or Subdivision (a) of Section 192.5 (Manslaughter)

If a driver with a violation attends traffic school, we will reorder the person’s MVR. If the incident has been removed by the DMV, the policy will be rerated at the next renewal. Please send proof and requests to [email protected].

Click Next for additional info on Driver Eligibility: Next

◄Back to Table of Contents

Auto

41

◄Back to Table of Contents

Unacceptable Risks:

License Related:

Insured and Spouse with less than 3 years continuous license

experience

− Only unmarried resident children may have less than 3 years

license experience

Violation / Accident Related:

Any of these incidents in 10 years

Alcohol / Drug Related

Vehicular Homicide

Any of these Violations in the past 3 years:

License

At-Fault: Bodily Injury or Death

Driving Under Suspension

Racing

Speeding Over 100 MPH

Other Major Violation

Leaving Scene of an Accident

Fleeing, Eluding, Disobeying Police

Careless or Improper Operation

Reckless Driving

More than 1 of these Violations/Accidents in the past 3 years:

Greater than 1 point Cumulative

At-Fault: $1000 or more

Speeding

Other Moving Violation

Traffic Signal, Sign or Marking

Failure to Signal

Failure to Yield or Stop

Following Too Close

Improper Passing, Lane Change, Turning

Improper Use of Lights

Passing a School Bus

Commercial Conviction (CA Only)

◄Back to Table of Contents

Click Next for additional info on Driver Eligibility: Next

Auto

42

◄Back to Table of Contents

Household Members

Click here for more information on Driver Exclusions & Non Rated Driver guidelines.

The entire household should be insured on a single policy. All household members who are of eligible driving or permit age must be rated or

excluded, with the exception of those under age 16 who currently have a permit.

Resident means anyone residing in the same household except:

• an individual in active military service with the armed forces of the United States of America shall not be considered a resident in the household

unless such individual customarily operates the vehicle;

• a youthful operator who is a resident student without a car at a school, college or educational institution over 100 road miles from the place of

principal garaging of the vehicle shall be considered a resident in the household but the vehicle shall be eligible for the distant student discount.

All household residents above the legal driving age and any other person that regularly or frequently drives a covered vehicle must be disclosed on

the application.

Drivers must be rated or excluded (where allowed). Drivers are individuals that are currently licensed or were previously licensed. (For example:

Revoked or suspended license).

Driver Classification

Drivers are classified by age, sex and marital status.

Age means the age of the driver as of the term effective date.

Inexperienced Operator Surcharge

Applies to any newly licensed driver regardless of age, who does not have three years driving experience in the United States. We must be able to

obtain the Motor Vehicle Record to verify the driving experience.

Additional (Second) Named Insured

Two named insureds may be listed on a policy. A second named insured can be designated by putting a check mark in the additional named insured field in our quoting system. The designated individual will be shown as a secondary named insured on the declaration page. The second named insured does not have to be the named insured’s spouse.

Click Next for additional info on Driver Eligibility: Next

◄Back to Table of Contents

Auto

43

◄Back to Table of Contents

Click Next for additional info on Driver Eligibility: Next

Driver Marital Status

Only those drivers who are married or in a civil union will be classified as married. Drivers who are single, widowed, legally separated or divorced

will be classified as single.

• Married means an operator who meets the local statutory definition of married.*

• Domestic Partners means same-sex couples and, sometimes, opposite-sex couples status recognized by the state.*

• * The spouse must be listed on the policy as a rated driver or excluded with proof of marriage for the insured to be considered married for the

purpose of rating. All drivers not qualifying under the definition above will be rated as single.

• If the named insured or the named insured’s spouse is list only or excluded, we will rate the rated spouse as single unless proof of marriage or

domestic partnership is provided.

Permit Holder

Youthful operators under the age of 16 that hold a learner’s permit can be added to the policy at no charge. When a youthful driver turns 16,

Stillwater will automatically add the youthful driver to the policy.

Driver Status

Drivers with a suspended, revoked, or canceled license are not eligible.

Financial Responsibility Filings (SR-22)

Individuals requiring a filing must be rated and cannot be excluded or list only

The name of the filing must appear exactly as it reads on the driver’s license

Filings are not available for a driver with an unverifiable driving record

If we are unable to verify the driver record or a driver requiring a filing, the policy is subject to cancellation

Individuals requiring a filing should contact our Underwriting department prior to purchasing the policy.

◄Back to Table of Contents

Auto

44

◄Back to Table of Contents

Suspension & Failure To Appear (FTA)

We do not accept risks with suspensions in the last 5 years due to any vehicular-related reason, including FTA's (either open or closed). If there is

any non-vehicular suspension, do not enter this on FIRST. Instead, note the reasons or explanation in the Underwriting screen.

Driver Exclusions

Except for the state specifically noted below (ID, OR, RI, UT, VA, MN, and WI), we require all licensed drivers in the household to be either rated

or excluded on our policy. We verify members of the household by using third-party reports. Please review additional driver report (ADD) for

potential additional drivers and if not a member of the household or regular drivers of the insured vehicle provide information about this in the

Submission Remarks section on FIRST.

• rate them on the policy, or-

• exclude them from the policy. Exclusions MUST be signed by the named insured and faxed into us with the submission of the

application.

• Tell us about status of the potential other drivers (including those that show up on the ADD report) in relation to the household (Example: “Joe

Smith does not reside in the household”). This also includes youthful operators who are resident students at a school, college or educational

institution located more than 100 road miles from the principal garaging address on the policy and who are without a car at a school. However,

the operator shall be eligible for the Distant Student discount.

In Idaho, exclusions do not apply to liability coverage, therefore, we apply a driver exclusion surcharge to the policy. The BI/PD limits are 25/50/15 for excluded drivers.

In Oregon, exclusions are only recognized for the following reasons, reference OR statute 742.450 for full details:

• driver has a suspended or revoked license,

• there is a financial burden in excess of $1,000,

• the vehicle is high performance or

• driver exceeds eligible points.

Driver Exclusions continued on the next page.

◄Back to Table of Contents

Auto

45

◄Back to Table of Contents

Driver Exclusions (continued)

In Rhode Island, Family Members, this includes any family member, relative, or non-relative that share the same street address, may not be

excluded from coverage and are required to be rated. All Family Members that are household residents or any Family Member that may operate

any insured vehicle on this policy must be added as a rated driver to the policy.

In Utah, the Utah Motor Vehicle Financial Responsibility Law under 41-12A-301 requires:

• All drivers must maintain liability limits greater than or equal to 25/65/15.

• All excluded drivers must either have their driver’s license denied, revoked, or suspended.

• If the driver’s license is valid, the excluded driver must provide proof of other auto insurance to be excluded.

• In addition, Stillwater requires that form SP1891 04 17 UT SIC must be signed by the Named insured and all excluded drivers. In Virginia and Minnesota, drivers who are not or have never been licensed are not allowed to be added. Such drivers are ineligible at new business and will prompt UW action if added midterm.

Exception: Drivers age 18 or younger may be added as non-rated operators if they have never been licensed (no learner’s permit and no full driver’s license) and are being listed on their parent or guardian’s policy. As long as they continue to be listed on their parent or guardian’s policy and remain unlicensed, they will be allowed to continue as non-rated operators after age 18. Please keep in mind that these non-rated individuals must have been added before age 19 in order for this exception to apply. Once they obtain a learner’s permit or become fully licensed, they will be changed to a rated operator.

Driver exclusions are not allowed in MN, VA, and WI

Non-Relative Roommates

In Exclusion States – Either Rate or Exclude.

In Non-Exclusion States – Either Rate or Remove (not rated). To be eligible to remove a licensed, non-relative roommate, send proof of coverage through a Dec page or ID card for that driver to [email protected]. If a licensed, non-relative roommate doesn’t have proof of their own insurance coverage and they have a license, they will be added as a rated driver on the policy.

◄Back to Table of Contents

Auto

46

◄Back to Table of Contents

Out-of-State Driver’s Licenses

• The company requires all drivers on the policy to have an in-state driver’s license.

• Individuals that have recently moved into the state, a new in-state license is required within 45 days.

If not received within 45 days, the policy will be cancelled.

A copy of the driver’s license along with the policy number should be sent to [email protected].

Rated Drivers (CA & VA)

CA does not use the average driver class factor. CA automatically assigns the Highest Rated Driver to the Highest Rated Vehicle.

VA assigns the Highest Rated Driver to the Highest Rated Vehicle for surcharging violation points.

Non Rated Drivers

Persons of driving age in the household who will not be permitted to drive any of the insured’s vehicles.

Examples of acceptable non-rated driver reasons are:

1. Any spouse or eligible age adult resident who has never had a license;

2. Any resident youthful operator with a valid learners permit if under the age of 16;

3. An individual in active military service with the armed forces of the United States of America unless such individual customarily operates a

covered vehicle.

Oregon exception: Non-Rated Drivers

In Oregon, if an individual within the household has other insurance and the insured would like them to be listed but not rated:

1. Submit proof of the other insurance.

2. We'll scan/attach/document the policy accordingly

3. The operator/household must meet our underwriting guidelines for the entire policy to qualify.

◄Back to Table of Contents

Click Next for additional info on Driver Eligibility: Next

Auto

47

◄Back to Table of Contents

Unacceptable Policies:

1. Two or more personal auto insurance policies issued by Stillwater for same household.

Exceptions (No exceptions in Florida):

• Children who own their own vehicle or the parent’s policy is with Stillwater.

• Unrelated resident/roommates

• Policies with vehicles garaged at two different addresses and drivers in two different households

2. Policies with only pre-1981 vehicles. All policies must have at least one vehicle from model year 1981 or newer. (Not applicable in South

Carolina)

3. Policies with all vehicles intended for business use. At least one vehicle on each policy must be intended for personal use.

4. Additionally, risks may be considered for coverage provided they do not exceed the accident, convictions or claim criteria on the following page.

5. Vehicles with a principal out-of-state garaging location in Michigan or any county in which we do not accept personal auto insurance

applications.

Car Sharing

Car Sharing is unacceptable. Car sharing is a car rental where people rent cars for short periods of time, often by the hour. They are attractive to

customers who make only occasional use of a vehicle, as well as others who would like occasional access to a vehicle of a different type than they

use day-to-day. Some car sharing operations supply a fleet of vehicles such as Car2Go, City CarShare, Enterprise CarShare, and Zipcar, while

others use their members’ cars or peer-to-peer rentals such as Turo and Getaround.

Ride Sharing

Ride Sharing is unacceptable. A transportation network company (TNC) is a company that uses an online-enabled platform to connect passengers

with drivers using their personal, non-commercial, vehicles. Examples include Lyft, Uber X, Sidecar, Wingz, Summon and Haxi.

Florida-specific Rules:

1. No policy may have more than 4 vehicles listed.

2. Policies with more than 2 vehicles listed may only have maximum Bodily Injury (BI) limits of 100/300.

3. These rules only apply to FL policies originally quoted on or after 2/10/2017.

Click here to view the Accident/Violation Eligibility Chart

◄Back to Table of Contents

Auto

48

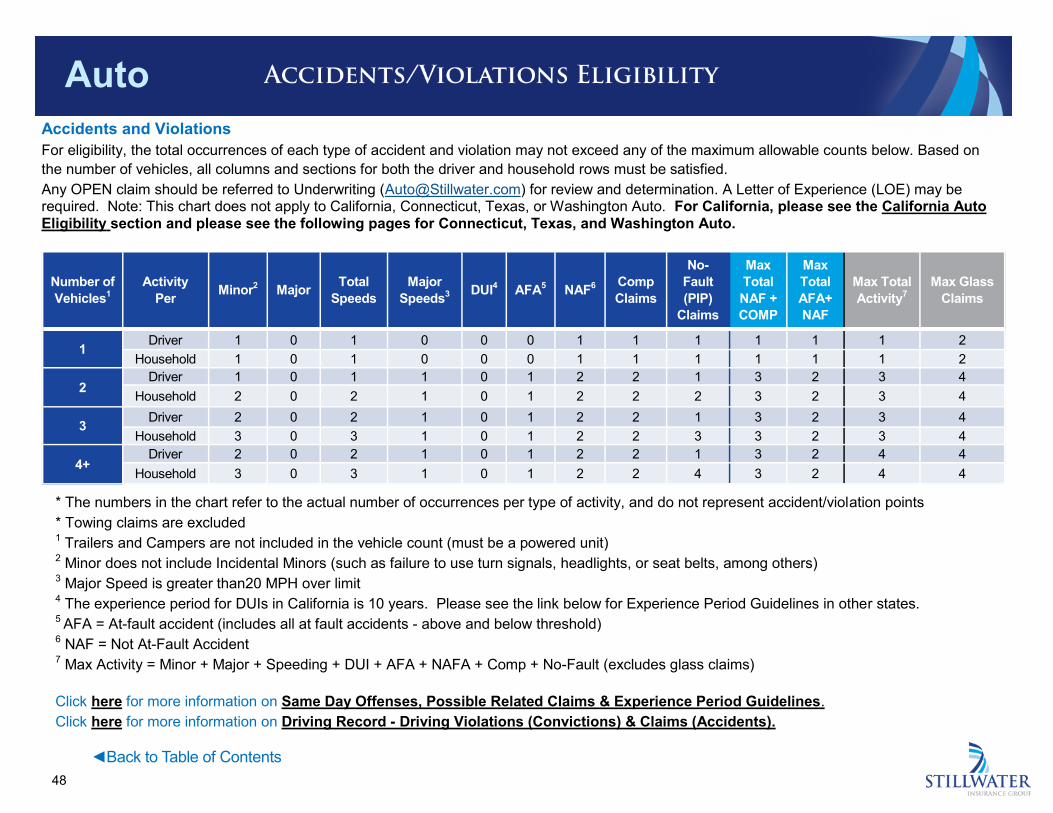

◄Back to Table of Contents

Number of

Vehicles1

Activity Per Minor

2 Major Total

Speeds Major

Speeds3 DUI

4 AFA5 NAF

6 Comp

Claims

No-

Fault

(PIP)

Claims

Max

Total

NAF +

COMP

Max

Total AFA+

NAF

Max Total

Activity7

Max Glass

Claims

1 Driver 1 0 1 0 0 0 1 1 1 1 1 1 2

Household 1 0 1 0 0 0 1 1 1 1 1 1 2

2 Driver 1 0 1 1 0 1 2 2 1 3 2 3 4

Household 2 0 2 1 0 1 2 2 2 3 2 3 4

3 Driver 2 0 2 1 0 1 2 2 1 3 2 3 4

Household 3 0 3 1 0 1 2 2 3 3 2 3 4

4+ Driver 2 0 2 1 0 1 2 2 1 3 2 4 4

Household 3 0 3 1 0 1 2 2 4 3 2 4 4

Accidents and Violations

For eligibility, the total occurrences of each type of accident and violation may not exceed any of the maximum allowable counts below. Based on