AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT The Australian Government Bond Market Peter McCray Deputy...

34

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT The Australian Government Bond Market Peter McCray Deputy Chief Executive Officer

-

date post

19-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT The Australian Government Bond Market Peter McCray Deputy...

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

The Australian Government Bond Market

Peter McCrayDeputy Chief Executive Officer

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Introduction

• Australia today enjoys well-developed financial markets across all major product lines– a result of a longstanding pursuit of market-

based policies– a concerted program of financial sector

deregulation and reform

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Introduction

• Three broad areas to cover:– Australia’s financial markets today,

emphasising the current government bond market

– snapshot of pre-deregulation market environment

– operational and infrastructure reforms that have underpinned development of today’s government bond market

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Australian Government Bond Market

• Domestic government bonds are the most liquid segment of the Australian market

– corporate outstandings now comparable

– secondary market turnover in government sector far greater

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Australian Government Bond Market

• Boosting liquidity in the physical market are:

– deep and liquid derivatives market for fixed interest products

– consolidation of Australian government bonds into benchmark lines

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Government Bond Market - Looking Back Twenty Years

• Australia’s financial system was heavily regulated up until the early 1980s:

– fixed exchange rate / exchange controls

– regulated interest rates and lending in the banking sector

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Government Bond Market - Looking Back Twenty Years

– fixed price ‘tap’ system for issuance

– unclear separation between monetary policy and debt management

– domestic investor base

• Australia’s government bond market reflected this regulated environment:

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Government Bond Market - Looking Back Twenty Years

– ‘buy and hold’ market - little secondary market activity

– no derivatives markets

– ‘captive market’ arrangements

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Development of Government Bond Market

• The broad context:– removal of exchange controls and floating of

Australian dollar– removal of regulated interest rates and other

controls; introduction of foreign bank competition

– separation of Debt Management and Monetary Policy

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Development of Government Bond Market

• ‘Operational’ reforms

– issuer behaviour– primary issuance mechanism– captive market arrangements– issuer support of bond secondary market and

derivatives markets

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Development of Government Bond Market

• ‘Infrastructure’ reforms

– clear separation of debt management and monetary policy responsibilities

– clearing and settlement systems– regulatory framework

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Operational Reforms - Issuer Behaviour

• Requirement to act responsibly– perceptions of market integrity– maintain a high reputation for financial

management competency– transparent and predictable debt management

activities– maintain regular and open communication with

markets• but not totally mechanical in approach

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Operational Reforms - Issuance Mechanism

• A market-based issuance mechanism to replace the tap system– auction approach– ‘dealer panel’ arrangement

• Bond auctions introduced in August 1982

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Operational Reforms - Issuance Mechanism

• An auction mechanism not always the most appropriate approach, at least initially– nature of investor base– stage of market development

• Australia has used other mechanisms to introduce new debt instruments– dealer panels & underwriting syndicates– cost an important consideration

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Operational Reforms - Captive Investors

• Captive investor arrangements influenced the bond market until the early to mid 1980s

– prudential aspect

– guaranteed a growing demand for government bonds

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Operational Reforms - Captive Investors

• But ultimately a costly and inefficient approach

– removes an important fiscal discipline

– distorts flow of investment funds

– inhibits secondary market development

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Operational Reforms - Secondary Market Development

• Most potent influence on liquidity is the volume of new issuance and bond outstandings

– ultimately beyond the control of the government debt manager

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Operational Reforms - Secondary Market Development

• Meet investors demands

• Encourage specialist market makers

• Direct secondary market participation

• Short-selling of government bonds permitted

• Encourage liquid and efficient repo and derivatives markets

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Infrastructure Reforms - Separation from Monetary Policy• Move to bond auctions and floating

exchange rate permitted independent monetary and debt policies

• Separation of responsibilities between the RBA and AOFM– Transactions based on a commercial arms

length basis

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Infrastructure Reforms - Clearing & Settlement Systems

• Reliable and timely clearing, transfer of ownership and settlement arrangements are essential

– electronic transfer and settlement system for government securities (RITS)

– Real Time Gross Settlement (RTGS)

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Infrastructure Reforms - Clearing & Settlement Systems

• Desirable features of robust clearing and settlement infrastructure – clear, unambiguous regulations– a sound legal basis– sound risk management procedures– well established contingency arrangements– explicit identification of government regulator

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Infrastructure Reforms - Regulatory Framework

• A well-functioning debt market requires a regulatory system which:– prescribes a level playing field– clearly defines property rights– has transparent information flow– a capable and appropriately empowered

prudential authority

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Conclusion

• A review of Australia’s experience suggests a number of strategies to promote bond markets

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Conclusion

• Issuers must act responsibly

• Issuance arrangements need to take account of market development

• Captive investor arrangements are not recommended

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Conclusion

• Markets require a steady supply of new securities to sustain liquidity

• Authorities can support secondary market activity

• Clear separation of debt management and monetary policy is essential

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Conclusion

• Reliable and timely clearing and settlement arrangements are essential

• A prudential/regulatory regime to provide legal certainty and a level playing field– flexible enough to adapt to a dynamic market

environment

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Conclusion

• Ultimately, need an economic case for intermediaries and investors to participate in the government bond market

– Strength of Australian markets reflects their local financing role in the Australia economy and investors desire to be part of this economy

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

Domestic Bonds Outstanding

Bond Market Turnover(daily average)

0

20

40

60

80

100

120

90/1 91/2 92/3 93/4 94/5 95/6 96/7 97/8 98/9

$ billions

Australian Government

State Government

Non-Government

0

1

2

3

4

5

90/1 91/2 92/3 93/4 94/5 95/6 96/7 97/8 98/9

Australian Government

State Government

Non-Government

$ billions

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

0

1

2

3

4

5

6

7

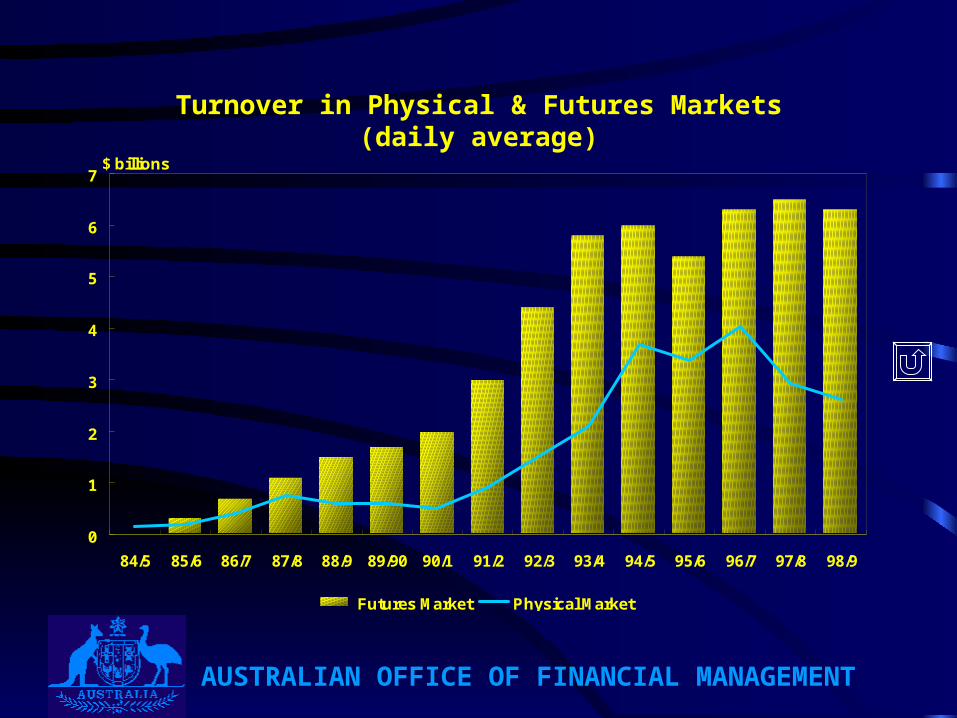

84/5 85/6 86/7 87/8 88/9 89/90 90/1 91/2 92/3 93/4 94/5 95/6 96/7 97/8 98/9

Futures Market Physical Market

$ billions

Turnover in Physical & Futures Markets(daily average)

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

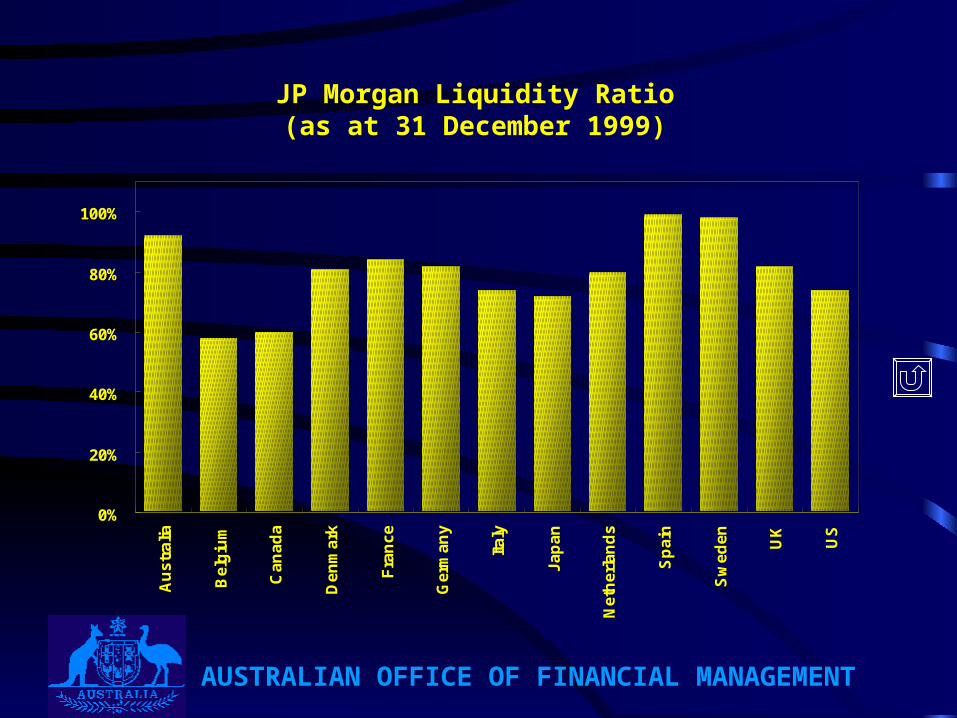

0%

20%

40%

60%

80%

100%

Au

str

alia

Be

lgiu

m

Ca

na

da

De

nm

ark

Fra

nc

e

Ge

rma

ny

Ita

ly

Ja

pa

n

Ne

the

rla

nd

s

Sp

ain

Sw

ed

en

UK

US

JP Morgan Liquidity Ratio(as at 31 December 1999)

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

0

20

40

60

80

100

84/5 85/6 86/7 87/8 88/9 89/90 90/1 91/2 92/3 93/4 94/5 95/6 96/7 97/8 98/9

0

1

2

3

4

5

6

7

Bonds Outstanding (LHS) Turnover (RHS)

$ billions$ billions

Daily Average Turnover Versus Bonds Outstanding

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

0

1

2

3

4

5

6

7

7% A

pr

00

13%

Ju

l 00

8.75

% J

an

01

12%

No

v 01

9.75

% M

ar

02

10%

Oct

02

9.5%

Au

g 0

3

9% S

ep

04

7.5%

Ju

l 05

10%

Fe

b 0

6

6.75

% N

ov

06

10%

Oct

07

8.75

% A

ug

08

7.5%

Se

p 0

9

5.75

% J

un

11

$ billions

Benchmark Bond Issues(as at 24 March 2000)

AUSTRALIAN OFFICE OF FINANCIAL MANAGEMENT

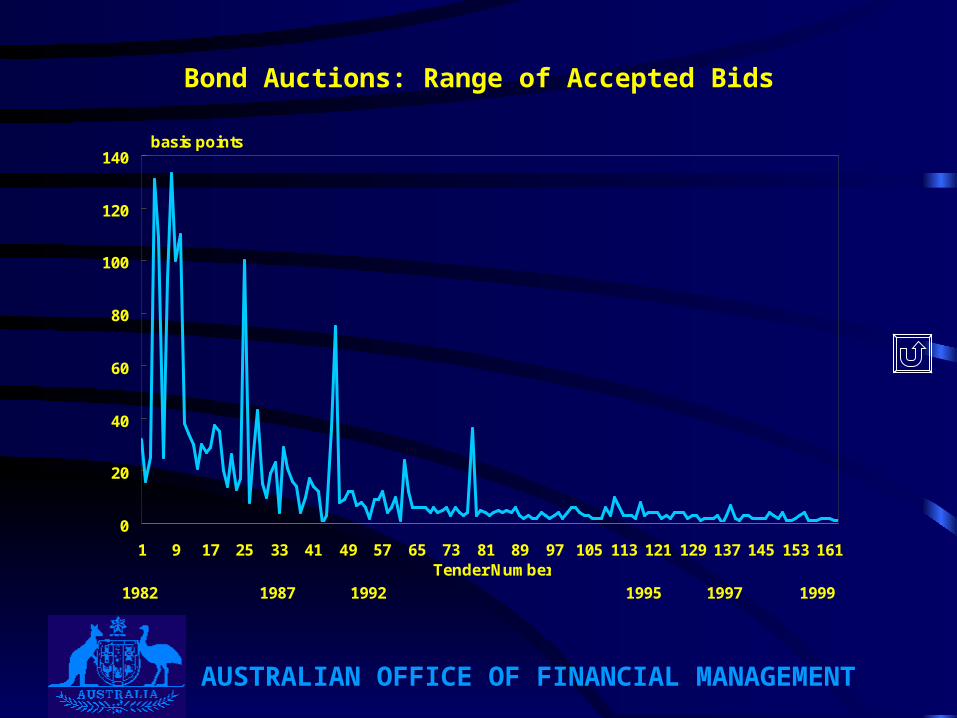

Bond Auctions: Range of Accepted Bids

0

20

40

60

80

100

120

140

1 9 17 25 33 41 49 57 65 73 81 89 97 105 113 121 129 137 145 153 161

basis points

Tender Number

1982 1987 1992 1997 19991995