Aura Light BLV GE Lighting NARVA OSRAM GmbH Philips Lighting Havells Sylvania WEEE – Producer’s...

32

Aura Light • BLV • GE Lighting • NARVA • OSRAM GmbH • Philips Lighting • Havells Sylvania WEEE – Producer’s Experience in Europe Christoph von Rautenfeld OSRAM

-

Upload

daniel-marshall -

Category

Documents

-

view

225 -

download

0

Transcript of Aura Light BLV GE Lighting NARVA OSRAM GmbH Philips Lighting Havells Sylvania WEEE – Producer’s...

Aura Light • BLV • GE Lighting • NARVA • OSRAM GmbH • Philips Lighting • Havells Sylvania

WEEE – Producer’s Experience in Europe

Christoph von RautenfeldOSRAM

Page 2

Agenda

Introduction ELC – the organization and people involved

Specialty of lighting for EPR/WEEE

The Situation in EU History of the directive in EU

Reaction of the lighting industry

Organizational model ELC

Operational Costs Overview

(Current) issues in Europe

Key Learnings from EU

Page 3

Introduction: Contacts

Christoph v. Rautenfeld, OSRAM CFO of OSRAM in Brazil

4 years working on WEEE in EU

Since July 2007 responsible for WEEE/EPR GlobalPhone: +55 11 3684 7471

Mobile: +49 170 636 8755 / +55 11 8196 5043

eMail: [email protected]

Page 4

Introduction:Who are we?

ELC represents the leading lamp manufacturers in Europe

95% of total European production

50 000 employees in Europe

€6 billion European Turnover

We are an international non profit-making association under Belgian law

with a secretariat in Brussels

We are a flexible, light & efficient decision-making lobby organisation to

promote efficient lighting practice for the advancement of human

comfort, health and safety

We were created in 1985

Page 5

Introduction: Which companies?

Havells Sylvania

Page 6

Specialty of lighting:Lamps are different with regard to WEEE

The collection and recycling of Lamps is considerably different from all other WEEE products due to:

Fragility Hazardous waste regulation Low weight High volume over 700 million (WEEE relevant) lamps per year put

on the EU market No material value after recycling

Also due to these characteristics collection and recycling costs are significant in relation to product prices.

Lamps are one of the few components separately included in WEEE legislation in Europe

Lamps are different, and require specific WEEE solutions

Page 7

45ct

10ct

3ct

COGS

Sellingothers

1) Average calculation for FL

Specialty of lighting:High Costs Involved

Example Cost Structure1

WasteFee2 30ct

2) European average

Drastic impact from WEEE Fee For most products exceeding all

individual cost blocks (selling, material, personnel etc)

Impact for lighting industry in Europe: approx. 180’ mio. EUR p.a.Excluding company provisions for WEEE obligation

(Initial waste fee was more in the range of 0,60 EUR!)

Page 8

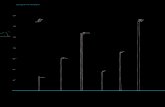

0%

20%

40%

60%

80%T

V

DV

D

Vac

uu

mC

lean

er

Sh

aver

Co

ffee

mak

er

Mic

row

ave

Was

her

Dis

hw

ash

er

Dry

er

Fre

ezer

/F

rid

ge FL

CF

L-I

CF

L-n

I

HID

Eo

L-F

ee

( %

of

Co

st P

rice

)

Situation Netherlands after 3 yrs

Best case estimation

Specialty of lighting:High Costs Involved

Page 9

The Situation in EU:History of the directive

WEEE Directive in place since February 2003WEEE = Waste Electric and Electronical Equipment

The directive just gave a framework – each member state was supposed to transpose it into national law

Roll out process took way longer than foreseen in the time planning of EU (e.g. target was 02/2005 – Italy started in 11/2007)

Legal environment is scattered due to country specific transposition of the law, even though there is a directive as basis you can not speak of a European model!

The non uniformity causes high compliance costs and market disturbance

Page 10

The Situation in EU:Reaction of the lighting industry

The impact for the European lamp industry had been estimated at 180 mio EUR

ELC started (too late) Europe wide project activities

A core team consisting out of experts from all ELC members had been set-up

During the past four years more than 27 collective lamps schemes have been set-up by the member companies and the core team

Page 11

The Situation in EU:ELC organizational model

The Working Principles of a „CRSO“

Page 12

A level playing field for (collective) schemes that will

Fulfill the full legal responsibility in a financially sustainable way

Reach current and future targets

Develops Eco-efficient solutions as to successfully integrate financial concerns of its participants and the environmental goals

Provide a sustainable infrastructure for collection and recycling

Ensure a level playing field

Guarantee confidentiality of market data

Inform all stakeholders adequately

ELC preferred WEEE solutions

Page 13

CRSO

CRSO = Collection and Recycling Support Organization Organizations (legal entities or associations) set-up and owned by lamp industry Open to all producers – not limited to the shareholders Equal conditions for all customers (called “participants” or “members”) Non for profit and tax exempted

What is done by a lamp collective scheme? Customize logistics concept for country specific aspects To ensure quality and cost it has been proven successful to invest into

lighting specific collection containers Ensure an utmost efficient cooperation of logistics and recycling

providers. Transportation and recycling are outsourced to third parties:

For Europe Recycling itself has proven not be a key success factor – techniques are simple and either widely available or easily to being acquired

Page 14

CRSO: main operational flows

CRSO

End User

Municipalities

Prof. Collection Site

Retail Transporter Recycler

Government

Producer

Product Flow

Financial FlowStakeholder

Page 15

Clear Responsibilities of each Stakeholder required

Producers: Support the setup of CRSOs, transfer waste fee

Consumers: Return of end-of-life products, payment of compliance costs/fee

Distribution: Take back end-of-life products

Municipalities: Provide municipal collection sites

Recyclers: Comply with recycling requirements

CRSO: Organize efficient and sustainable processes, inform stakeholders

Governments: Define stakeholder responsibilities, ensure level playing field

NGO’s: Increase awareness

Page 16

CRSO

Waste Fee set by the collective scheme: Flat = all lamp types have the same fee For all participants same level Based on units (reporting of weight offers too much leeway for un-

compliant behavior)

Utmost highest transparency Visible invoicing to the customer

Page 17

CRSO

Pay as you go Collective schemes have been set up as “pay as you go” models Current periods costs from collection & recycling are allocation to the

units sold in the current period Financing done based on market share

Calculations need to be based on a target collection rate of 90% to 100%, if not:

Limited motivation to increase collection ratesSchemes start to compete only for lower fees instead of competing for an increase of collection rates Fee would be fluctuating and market acceptance would be lowSchemes need to build up a reserve for the full obligation they take over

Page 18

Operational Cost Overview:Different Fee Scenarios

in EUR cent Min1 Max2 Estimated situation in a

mature

market3

Logistics 6,0 19,3 7,5Recycling 3,8 19,0 3,5Communication/Awareness 8,9 12,4 1,5Overhead4

0,2 38,0 0,2Fee: 12,7

1) Best sustainable cost2) Max cost witH level playing field3) Estimated cost for collective scheme> 5 years operational experience, country with proper stakeholder def.

Page 19

Issues with the European implementation

National issues – Slovakia: Multiple competing schemes for lamps No clearing mechanism between schemes / no legal collection

obligation Target of ELC system was to build up logistics infrastructure and

raise collection rates (Long-term target > 80%) Driven by the founding importers the competing schemes lowered

their fees drastically Sustainable fee would be 0,30 EUR - competing schemes

charging 0,03 EUR Despite OSRAM and Philips all other members have left for cost

reasons Competing schemes do not collect and therefore have low/zero

costs

Page 20

Issues with the European implementation

National issues – Bulgaria: Producers (= importers to Bulgaria) can choose between a

state tax on import and the fulfillment of their WEEE obligation

A sustainable fee in Bulgaria would be three times as high as the state tax

State tax not used for proper collection and recycling

Producers not able to organize a sustainable scheme

Page 21

Issues with the European implementation

National issues – Austria: Producers can not take their responsibility

Only legal entities with local invoicing in Austria accepted as producer

Big end users buying across the border can escape as their obligation is not regulated properly

Page 22

Issues with the European implementation

National issues – UK: Clearing mechanism drives up the price and leave parts of

the country without collection

Different rules for household and professional

40 uncontrolled, competing schemes for lamps

No financial certainty that future lamps can be financed

Page 23

General learning

Financing Market share vs. share in products returning

Visible Fee

Keep it simple Do not differentiate legal responsibility for the same product

over sub categorize causes complexity (tubular, compact, sodium etc)

Definition of weight needs to be controllable and auditable

Keep it level (no market disturbance Definition of Producer same in in one economic union

Accreditation of schemes : to ensure eco efficiency and fair competition.

Allocation between schemes: to ensure competition is not on limiting collection

Guarantees: to keep financing for future obligations

Key Learnings from EU

Page 24

General Learning from EU

Non uniform implementation is the major cause of increase of integral compliance costs not the actual technical cost of logistics and recycling:

Non uniform legislation increases cost for compliance

Protectionist legislation

Legislation that triggers provisions without bringing security to society.

Defining the responsibility of the producer is not sufficient. The roles of all Stakeholders need to be defined e.g. Producers, other sellers, government, End user, government, Waste operators/recyclers

Specific legislation per WEEE product category is needed. Lamps are very sensitive with regard to financing and awareness because expense is high and they can be easily alternatively discarded

Page 25

In Europe two schemes are applied: Currently applied is Market-share (with a visible fee). Payment is on product

put on the market. This proofed to be a simple and controllable auditable way to finance

In legislation but not duly implemented is payment on the basis of waste returning (IPR). This is advocated to drive product design This is causing major provisions for stock listed companies

2005… 2010 2011 2012 20132009

IPR

Market share

Sample Life cycle product

Financing: Market share vs share in products returning

Page 26

IPR a financial driver to design for better recycling? NO

The financial driver does not exist Commonly required Payback times in the electronics industry for

investments are short: max 2-3 years Products sold now will return on average in 6-10 years Highly unlikely that design projects will start due to financial

incentive aimed at ease of recycling Statement: No producer has made significant costly changes for

recycling. Examples are anecdotic!

Financing: Individual Prod. Resp. (IPR)?

Page 27

IPR a financial driver to design for better recycling? NO

Changes in design are immediately made so as to Comply with legal requirements on material or energy use Appeal to customers (marketing) Build a sustainable image

Not all Producers under WEEE have an impact on design Only manufacturers have an impact on the design of the product,

not importers, in many cases also not private brand owners

Eco-design should be regulated in Energy Using Products (EUP) or in Restriction on Hazardous Substances (RoHS) legislation

Financing: Individual Prod. Resp.?

Page 28

IPR a financial driver for increased separate collection rates? NO

IPR may rather lead to decreased separate collection rates due to the incentive for Producers to minimize collection (and as such costs)

IPR will increase the risk for externalization of costs, e.g. orphan waste (which can never be fully avoided)

IPR requires brand specific separate collection, leading to increased costs for C&R and inconveniences due to the need for a multitude to collection and sorting capabilities

IPR is only possible if the EEE can be tracked and traced on a Producer individual level from the cradle to the grave (marking not sufficient, esp. not for small items on which no details can be put)

IPR will decrease the ability of various stakeholders (a.o. Govt.) to monitor and control the objectives of the WEEE Directive

IPR does not ensure increased collection rates

Financing: Individual Prod. Resp.?

Page 29

Financing: Visible Fee

A visible fee

Builds ongoing consumer awareness. Awareness is the key for efficient take back. A visible fee is the strongest communication tool available. Specifically needed for products that can be easily alternatively disposed

and have a significant cost for collection and recycling related to product price

Increases transparency: Effective tool against free riders

Allows payback after proven export

Page 30

Keep it simple

Differentiated legal responsibility for the same product between use in household and professional has caused a un-level playing field and un-clarity for users

over sub categorize causes complexity (tubular, compact, sodium etc) for reporting purposes only causes un-needed costs without benefits

Definition of weight needs to be controllable and auditable: For lamps due to large variance only pieces or pieces times average weight allow for a auditable financing scheme

Page 31

Keep it level (no market disturbance)

Definition of Producer same in in one economic union Needs to cover: producer, reseller, re-branding, end-users

Accreditation of schemes : to ensure eco efficiency and fair competition.

Strict accreditation needed to limit start-up of unsustainable set ups

Schemes can not be for profit. All funds need to allocated for collection and recycling

Guarantees: to keep financing for future obligations

Allocation between schemes: to ensure competition is not on limiting collection.

Page 32

Thank you for your attention!

Christoph v. Rautenfeld, OSRAM Phone: +55 11 3684 7471

Mobile: +55 11 8196 5043

eMail: [email protected]