August 7, 2015 Daehaeng Kim, IMF, Belgrade Office · 2015-17 (rightsizing via attrition and...

26

August 7, 2015 Daehaeng Kim, IMF, Belgrade Office

Transcript of August 7, 2015 Daehaeng Kim, IMF, Belgrade Office · 2015-17 (rightsizing via attrition and...

August 7, 2015

Daehaeng Kim, IMF, Belgrade Office

Context Fiscal imbalances have been piling up since 2008/9 Attempts to stop the growing public debt proved

ineffective: e.g., 2009 and 2011 SBA, and stopgap measures in 2013/14

3-year IMF precautionary SBA approved in February 2015, with three main objectives: Address macroeconomic imbalances and vulnerabilities, most

notably by placing public debt on a sustainable path Bolster resilience of the financial sector and improve its

intermediation function necessary to support growth Improve competitiveness and reduce key growth bottlenecks

through vigorous implementation of comprehensive structural and SOE reforms

What do we learn from Serbia’s fiscal reforms? Focusing fiscal issues in Serbia, the presentation offers

a real example to illustrate:

What caused the growing fiscal imbalances

How policy was designed to address the root causes of the imbalances

How the policy has been implemented

And what kind of risks and challenges the policy implementation faces

Outline Part 1. Fiscal Developments Since 2008/9

Part 2. Causes of Fiscal Imbalances

Part 3. Fiscal Program Objectives And Policy Design

Part 4. Progress So Far And Challenges Ahead

Part 1. Fiscal Developments Since 2008/9

High deficit and growing debt GG deficit increased

from 2½ percent of GDP in 2008 to over 7 percent in 2012, and remained high until 2014.

Public sector debt grew from 32½ percent of GDP in 2008 to 72½ percent in 2014.

30.0

35.0

40.0

45.0

50.0

55.0

60.0

65.0

70.0

75.0

-8.0

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

2007 2008 2009 2010 2011 2012 2013 2014

(in percent of GDP)

Generalgovernment balance

Public debt, rhs

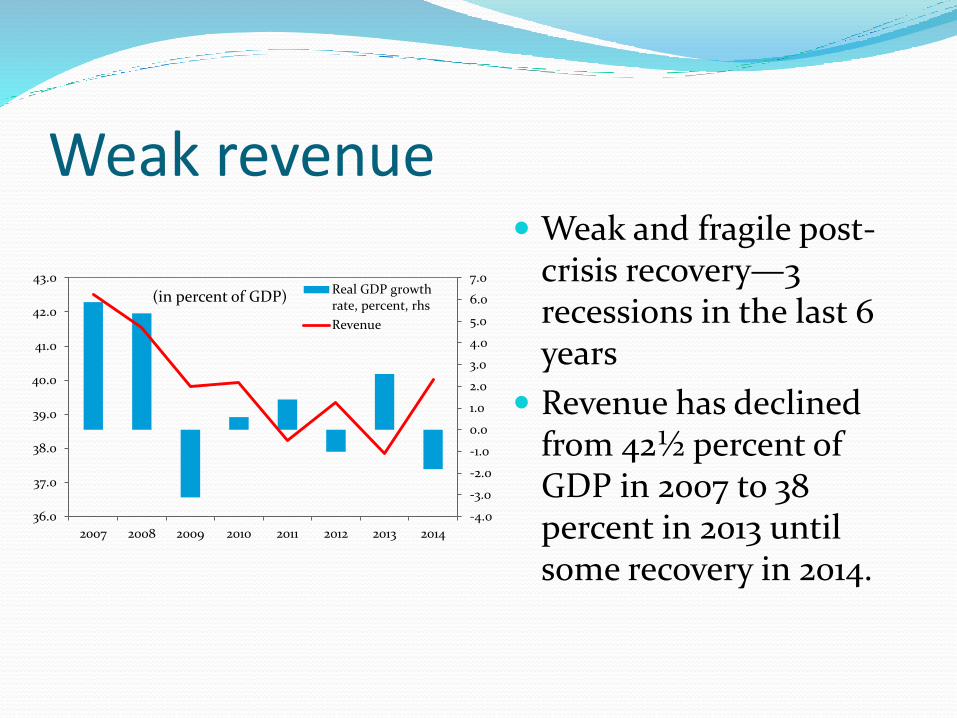

Weak revenue Weak and fragile post-

crisis recovery—3 recessions in the last 6 years

Revenue has declined from 42½ percent of GDP in 2007 to 38 percent in 2013 until some recovery in 2014.

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

36.0

37.0

38.0

39.0

40.0

41.0

42.0

43.0

2007 2008 2009 2010 2011 2012 2013 2014

(in percent of GDP)Real GDP growthrate, percent, rhs

Revenue

High entitlement spending Expenditure has

increased despite consolidation efforts in 2011 and 13.

Entitlement spending—GG wage bills, pension, and subsidies—has grown from 24 percent of GDP in 2007 to 27¼ percent in 2014.

21.0

22.0

23.0

24.0

25.0

26.0

27.0

28.0

29.0

42.0

42.5

43.0

43.5

44.0

44.5

45.0

45.5

46.0

46.5

47.0

2007 2008 2009 2010 2011 2012 2013 2014

(in percent of GDP)Wage, pension,subsidies

Expenditure

Decomposition of debt growth Growing guarantees and

materialization of contingent liabilities (i.e., amortization of called guarantees + bank bailout cost) account for 20 percent of debt increase in the last 4 years.

Exchange rate depreciation also increased debt burden significantly.

8.0

28.4

51.9

11.7

Contribution to the change in public debt: 2011-14

Guaranteed debt

Exchange ratedepreciation

Budget deficit net ofmaterializatin ofcontingent liabilities

Materialization ofcontingent liabilities

Part 2. Causes of Fiscal Imbalances

Stagnant growth and weak labor market performance

3 recessions in the last 6 years

Unemployment remains very high, while employment has been declining

Total population is 7.2 million, but formal employment is 1.7 million, equal to the number of pensioners

0 0.5 1 1.5 2 2.5 3

Total employment

Formal employment

Public sector employment

Pensioners(In millions)

60

70

80

90

100

110

120

10

12

14

16

18

20

22

24

26

28

30

2008 2009 2010 2011 2012 2013 2014

Total employment ('08=100, rhs)

Unemployment rate (in percent)

Formal employment ('08=100, rhs)

Weak revenue collection Share of indirect tax—VAT

and Excise—is relatively high (about 45 percent of tax revenues), reflecting the labor market situation

Growing grey economy and declining tax efficiency until 2014

VAT efficiency weakening: Effect of the rate hike in September 2012 (18 to 20%) was limited

65

70

75

80

85

90

9

9.5

10

10.5

11

11.5

2007 2008 2009 2010 2011 2012 2013 2014

VAT Efficiency, rhs

VAT in percent of GDP

Weak control over GG wage bill High GG wage bill

High inefficiency in some sectors

High wage rate compared to the private sector

Weak control and high wage drift until 2013

Number of workers

Overly complex and fragmented wage system

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2007 2008 2009 2010 2011 2012 2013 2014

Average monthly gross wage (RSD)Public sector

Private sector

Public Sector Wage System

Job titles 2,200

Elements of pay 71

Base salaries 5

Job coefficients 900

Laws that regulate renumeration 19

Pension dilemma—neither considered enough nor affordable

Unfavorable population age profile Social expectations:

High replacement ratio: 70 percent, but about €200 per month on average

Generous early retirement: statutory vs. effective retirement age (Man: 63 vs. 60) before the reform

Internationally high pension spending

Growing share of the population stays outside the system—risk to future social protection spending

0

20

40

60

80

100

120

IRL

JPN

NZ

L

GB

R

US

A

HR

V

CA

N

SW

E

DE

U

ES

T

FR

A

NO

R

BE

L

CH

E

CZ

E

FIN

PR

T

SR

B

SV

K

ES

P

SV

N

DN

K

AU

T

TU

R

LU

X

NL

D

HU

N

GR

C

Net replacement rate of a standard pensioner, 2011

0

2

4

6

8

10

12

14

16

18

20

IRL

LV

A

GB

R

SV

K

NL

D

NO

R

BG

R

LU

X

RO

U

CZ

E

LT

U

DN

K

MK

D

CH

E

ES

P

ES

T

SW

E

BE

L

SV

N

HR

V

FIN

DE

U

HU

N

MN

E

PO

L

GR

C

PR

T

FR

A

AU

T

SR

B

ITA

UK

R

Public pension expenditure (in percent of GDP), 2010

Inefficient state aid and drain on the budget

Lack of transparency and weak governance

State aid for employment Railways: budget subsidies =

total wage bill Large loss-making

companies—direct or indirect support

Weak financial control and payment discipline State guarantees for liquidity

loans with little prospect for repayment

Arrears to utility companies

Bank bailout cost

0

100

200

300

400

500

600

700

800

Amortization of activatedguarantees

Bank recap and arrearsclearance

Millions of euros, cumulative during 2012-14

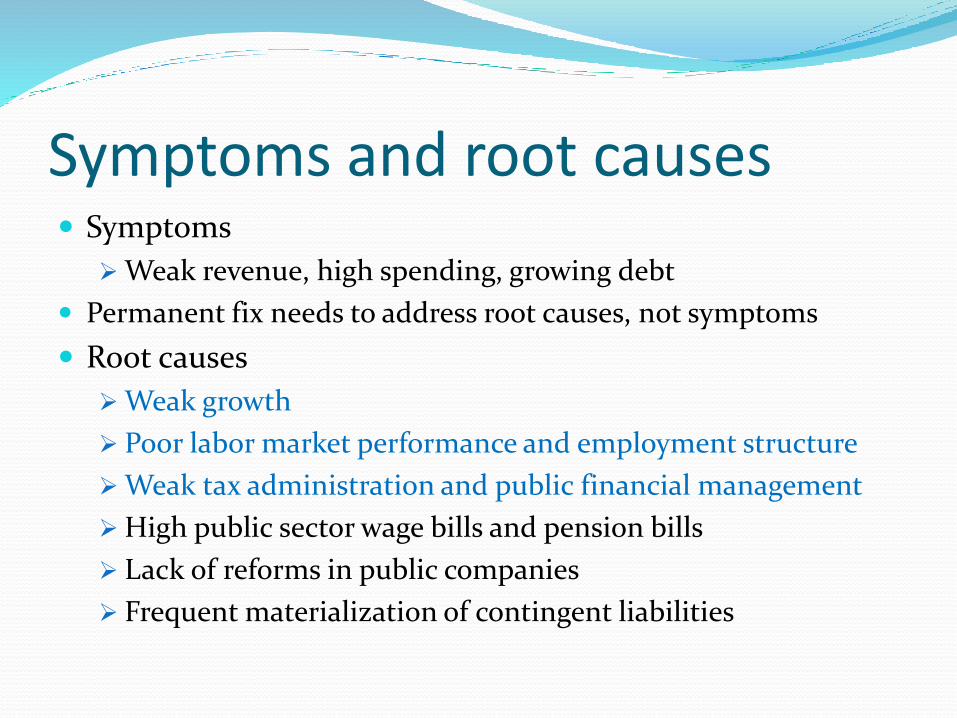

Symptoms and root causes Symptoms

Weak revenue, high spending, growing debt

Permanent fix needs to address root causes, not symptoms

Root causes

Weak growth

Poor labor market performance and employment structure

Weak tax administration and public financial management

High public sector wage bills and pension bills

Lack of reforms in public companies

Frequent materialization of contingent liabilities

Part 3. Fiscal Program Objectives and Policy Design

Fiscal objectives Reverse the rise in public debt by

2017 and put it on a downward path thereafter (chart)

3-year fiscal adjustment, amounting to 4¾ percent of GDP (3½ percent of GDP in structural terms) Productive spending should be

protected The savings from the

consolidation measures should be lasting

Strike balance between credibility and growth impact Slightly over 50 percent of the

adjustment takes place in 2015

40.0

50.0

60.0

70.0

80.0

90.0

100.0

-14.0

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2012 2013 2014 2015 2016 2017 2018 2019 2020

Public debt, rhs

General government balance

projection

Policy measures: before program Key structural reforms and consolidation measure in the

summer 2014

Labor law amendments

Raise the threshold for automatic extension of collective agreement

Clarify the cases for dismissal

Rationalize severance compensation

Extend the maximum length of temporary contracts

Parametric pension reforms

Gradually raise the statutory retirement age for women

Introduce early retirement penalty

10 percent wage cut and 22/25 percent pension cut

Program measures Limited room for tax rate hikes

Focus on containing entitlement spending (2/3) and state aid (1/3) In addition to wage and pension cuts

Wage and pension indexation freeze—until their GDP shares reach 7 and 11 percent of GDP, respectively

Reduction of employment cost by 5 percent each in 2015-17 (rightsizing via attrition and targeted separation)

Reduction of state aid to public companies, underpinned by SOE reforms

No guarantee for liquidity loans

Structural fiscal reforms Structural reforms needed to support the fiscal consolidation

and/or mitigate fiscal risks Rightsizing to increase the efficiency of the general government,

while reducing the cost, via its organizational and functional restructuring

Wage system reform to bring the wage system under control Reforms to improve fiscal transparency, which is the first step for

better accountability; better monitoring and control of fiscal risks Introduction of 3-year expenditure ceiling Clarification of the coverage of the general government Improvement of the reliability and coverage of public sector

employment registry Strengthening of SOE financial monitoring function of MOF Enhancement of the payment discipline between public sector entities

Tax administration reform to improve collection without rate hike

SOE reforms Subsidies to large SOEs have been a drain to the budget,

and fiscal risks from them are significant

SOE reforms, via privatization and/or restructuring, agreed to improve the financial viability of large SOEs and thus contain fiscal risks from them

Railways—unbundling and financial restructuring

Electricity Producer (EPS) —recorporatization and financial restructuring, including electricity price increases

Srbijagas—financial restructuring

Large steel and chemical companies—seeking privatization, assurance of no state aid and no accumulation of arrears

Growth enhancing measures To mitigate the short-term impact of the fiscal

retrenchment, and establish foundation for sustained growth:Reforms to promote investment

Construction permit and land development law

Land ownership conversion law

Investment law

WB-supported privatization

EBRD Investment Climate and Governance Initiatives

Rebalancing policy mix toward monetary easing

NPL resolutions to support credit growth

Part 4. Progress So Far and Challenges Ahead

First Review The First Review was

completed on June 26

Performance Criteria met with good margins

Structural benchmarks were met with some delays

Sovereign Credit Default Swap is falling

Exchange rate stabilized

0

50

100

150

200

250

300

350

400

450

500

Jan-14 Jul-14 Jan-15

Sovereign CDS SpreadsBulgariaCroatiaRomaniaSerbia

114

115

116

117

118

119

120

121

122

123

124

125

RSD/EUR

Challenges ahead Structural reforms

Will reforms stick?

Or will this effort be another band aid?

Sustained consolidation is key for 2016-17

Wage and pension indexation freeze until their GDP shares reach 7 and 11 percent, respectively

General government rightsizing

Return of sustainable high growth and improved tax collection will be strong tail wind for debt reduction