August 30, 2015 - Amazon Simple Storage Service · Last Tuesday, the PBoC injected ... currency for...

7

August 30, 2015 Greetings, It’s possible that China is not ready for free markets. The first sign was in the first half of 2015 when regulators let Chinese stocks soar, fueled by hugely speculative investments and a surge in margin trading. Then, after the bubble popped, policymakers cobbled together a haphazard rescue package that ultimately failed to support the market. The currency “devaluation” was an attempt to appease the IMF and also jumpstart the country’s stagnant manufacturing industry. But allowing CNY to drop a mere 3% before resuming intervention will not spark economic activity. Most alarming was the PBoC’s inability to lower money market rates last week while the local stock market dropped 10% in one session. Last Tuesday, the PBoC injected 150bn CNY into the banking system through reverse repos. On the same day, 120bn CNY worth of repos matured – making the net injection 30bn CNY. It’s often overlooked, but the PBoC doesn’t actually intervene in FX markets. Instead, it instructs state-backed banks to intervene on its behalf. The same day, Chinese banks sold ~$15bn USD/CNY to protect the exchange rate. However, that soaked up another 96bn CNY ($15bn*6.4) of capital from the system. At the end of the day, the PBoC actually tightened liquidity by 66bn CNY.

Transcript of August 30, 2015 - Amazon Simple Storage Service · Last Tuesday, the PBoC injected ... currency for...

August 30, 2015

Greetings,

It’s possible that China is not ready for free markets. The first sign was in the first half of 2015

when regulators let Chinese stocks soar, fueled by hugely speculative investments and a surge in margin

trading. Then, after the bubble popped, policymakers cobbled together a haphazard rescue package that

ultimately failed to support the market. The currency “devaluation” was an attempt to appease the IMF

and also jumpstart the country’s stagnant manufacturing industry. But allowing CNY to drop a mere 3%

before resuming intervention will not spark economic activity.

Most alarming was the PBoC’s inability to lower money market rates last week while the local

stock market dropped 10% in one session. Last Tuesday, the PBoC injected 150bn CNY into the banking

system through reverse repos. On the same day, 120bn CNY worth of repos matured – making the net

injection 30bn CNY. It’s often overlooked, but the PBoC doesn’t actually intervene in FX markets. Instead,

it instructs state-backed banks to intervene on its behalf. The same day, Chinese banks sold ~$15bn

USD/CNY to protect the exchange rate. However, that soaked up another 96bn CNY ($15bn*6.4) of capital

from the system. At the end of the day, the PBoC actually tightened liquidity by 66bn CNY.

The tightening of liquidity served to push up repo-rates, which is exactly what the market didn’t

need. By Wednesday, the PBoC had figured this out and dropped the hammer with a 25bps interest rate

cut combined with a RRR reduction. This was effective in dropping repo rates, but their inability to

manipulate a state-controlled market in a time of panic feeds the narrative that China is not ready for the

major leagues.

Cup & Handle subscribers have known for a while that, more than anything, China needs lower

real interest rates. Even now, after five policy rate cuts, real rates are only back to 2012 levels when GDP

was running above +8% Y/Y. They’ll need to drop a lot further for the domestic economy to generate any

momentum, but, at the same time, policymakers don’t want to add to an enormous debt burden. It will be

a very tricky balancing act, and the release valve could be a much weaker CNY.

The market has its eyes squarely fixed on China now, and developments in the Middle Kingdom

will be the key factor in the future direction of asset prices. The first snapshot of economic data for

August was ugly. The preliminary Caixin manufacturing PMI was 47.1, well below expectations. Investors

will now turn their attention to US non-farm payrolls on Friday before we see China’s exports, CPI and

lending data next week. More than anything Chinese policymakers need to show the market that they

have a handle on things. The explosion in Tianjin and subsequent lack of response did nothing to soothe

concerns. Premier Li Keqiang is already thought to be on the hot seat, and if things don’t settle down

President Xi will name other scapegoats.

The Cup & Handle Fund is up around 7.0% YTD, and +27% Y/Y. The portfolio was up huge last

Monday, but gave back some gains during the subsequent rally. I’ve adjusted the portfolio slightly, but the

fundamental thesis hasn’t changed much. Expect big gains later this year. Without being redundant, the

last two monthly letters have been home runs. If you’d like to start receiving these letters click here.

Today’s letter will cover several topics, including:

China

US

Europe

Chart of the Week

As always, if you have any questions or comments or just want to vent, please send me an email at

Until next time, tread lightly out there,

Michael Lingenheld Managing Editor – Cup & Handle Macro

We’re going to try a slightly different format this week; maybe we’ll stick with it, maybe we won’t.

With macro back in vogue it seems like the right time to give an update of where the big 3 economies (US,

Europe and China (above)) stand, and where they could be headed.

US

The United States is still far and away the world’s strongest economy. The most recent GDP

reading, for 2Q, came in at +3.7% Q/Q on Thursday, which not only beat expectations but jumped from

the 1Q reading of +2.3% Q/Q – although weak 1Q figures can be attributed to bad weather. Despite

lackluster wage growth, the job market looks pretty healthy. Initial jobless claims are at their lowest

levels in history, the unemployment rate is near 5%, and consumer sentiment is the strongest it’s been

since 2007.

You’ll notice that all of those metrics are backward looking. Markets are forwarding looking, which

is why US assets stumbled recently. Oil staged a big rally towards the end of last week, but it’s still down

55% Y/Y. This weighs on inflation expectations and hurts growth. Earlier this year, the Fed was

predicting +4.1% GDP growth in 2015; now that forecast is +2.6%. Some of the more timely indicators

are starting to show weakness. The Empire Manufacturing Survey declined -14.2 in August, indicating

ISM should fall below 50 in the coming months – signaling outright contraction.

Economists need to abandon this theory that lower gasoline prices boost consumption. I know

academics can point to studies showing some causality, but there’s no way to make money using that

assumption. Data from Visa and MasterCard have shown that consumers are using their gas savings to

pay down debt and save, not consume. The chart above shows that gasoline and retail sales actually have

pretty decent correlation, and I wouldn’t be surprised to see Y/Y retail sales dip below 0% before year

end. On Tuesday morning, Canada will release 2Q GDP figures. I’ve mentioned this several times already,

but if that reading comes in below zero on a Q/Q basis, it would be the second consecutive decline.

Historically, the US has never avoided a recession when that occurs.

And, of course, there’s the Federal Reserve. NY Fed President Dudley gave a speech on Wednesday

making it clear the Fed has its eyes on China. A September hike seems unlikely, although strong non-farm

payroll figures for August could change that equation. At least some of the rally in stocks the past few

days can be attributed to the anticipation of QE4 – a view supported by Larry Summers and Ray Dalio.

That leaves the Fed in a tricky spot, where a September hike would destroy stocks and no action might

still bring down the market. Overall, stocks could muddle through over the next six months as weak

growth increases the odds of stimulus, but the attractive risk/reward bets all seem skewed towards the

downside – both in terms of growth and asset prices.

Europe

Just think, two months ago markets were hyperventilating over the potential exit of Greece from

the Eurozone. Nothing has changed since. Greece got a loan but it’s still a third world country. Prime

Minister Tsiparas resigned two weeks ago and called for new elections (again), but Greece is nothing

more than a precedent-setter for countries like Spain and Italy with unresolvable structural issues.

Elsewhere, economic conditions are rather non-descript. The Eurozone, led by Germany, posted

solid PMI figures for August around 53. EUR is the new JPY in the sense that it’s become a funding

currency for carry trades. The unwinding of those positions, combined with the EU’s current account

surplus sent EUR higher during last week’s chaos. It’s hard to imagine EUR will stray too far from the

price of oil, although the correlation has broken down materially this month.

The stronger EUR might hurt Europe’s export competitiveness marginally, but it’s still down 15%

Y/Y. However, any further strength will make the ECB nervous. They’re already committed to QE through

September 2016. I’m willing to bet that it extends beyond that date, but it’s too soon to tell. During last

week’s meltdown, ECB member Praet said the central bank was “ready to expand or extend its QE

program if needed.” Europe’s main problem right now (besides Russia) is not monetary policy, but rather

a humanitarian crisis brewing across the continent.

Migrants are fleeing the Middle East and North Africa in droves, headed for Europe. More than

100,000 migrants reached the EU in July – the most on record. Germany alone is expected to take in more

than 700,000 asylum seekers this year. Many of these people are Muslim and the locals aren’t exactly

keen on welcoming them into the community, especially after the Charlie Hebdo attack and the foiled

terrorist shooting on a French train last week.

Predictably, radical political groups are enjoying a huge resurgence in support. France’s right-

wing National Front just kicked out its founder, Jean-Marie Le Pen, for playing down the Holocaust. His

daughter, Marie Le Pen, is the party’s current leader and contender for the 2017 Presidential election.

When asked in June for her solution to the migrant crisis, Le Pen said, "We must send them back to their

own countries." In Germany, migrant shelters are being burned by Neo-Nazi’s. The Freedom Party, in

Austria, where 70 migrants were found dead in a truck last week, has support from 29% of the

population for its hostile views towards immigrants.

Alternatively, the left-wing radicals in Spain and Greece are looking to turn back austerity and

stick it to Germany. Syriza is already took power in Greece, and Podemos is looking to join a coalition

government in Spanish elections this November. The problem is that trading politics is very difficult, and

Europe doesn’t appear to have many opportunities in either direction.

EU bank stocks look cheap on a long-term chart, but they’re trading at those levels for a reason –

notably their enormous derivative obligations. Interest rates aren’t going anywhere, which should keep

margins tight for banks. Honestly, the best opportunities might be outside the Eurozone in Switzerland,

where negative interest rates are proving effective in weakening CHF. Swiss CPI in July was -1.3% Y/Y

and many expect the SNB to step up the stimulus effort soon. Look for EUR/CHF to trade back to the level

of its floor over time.

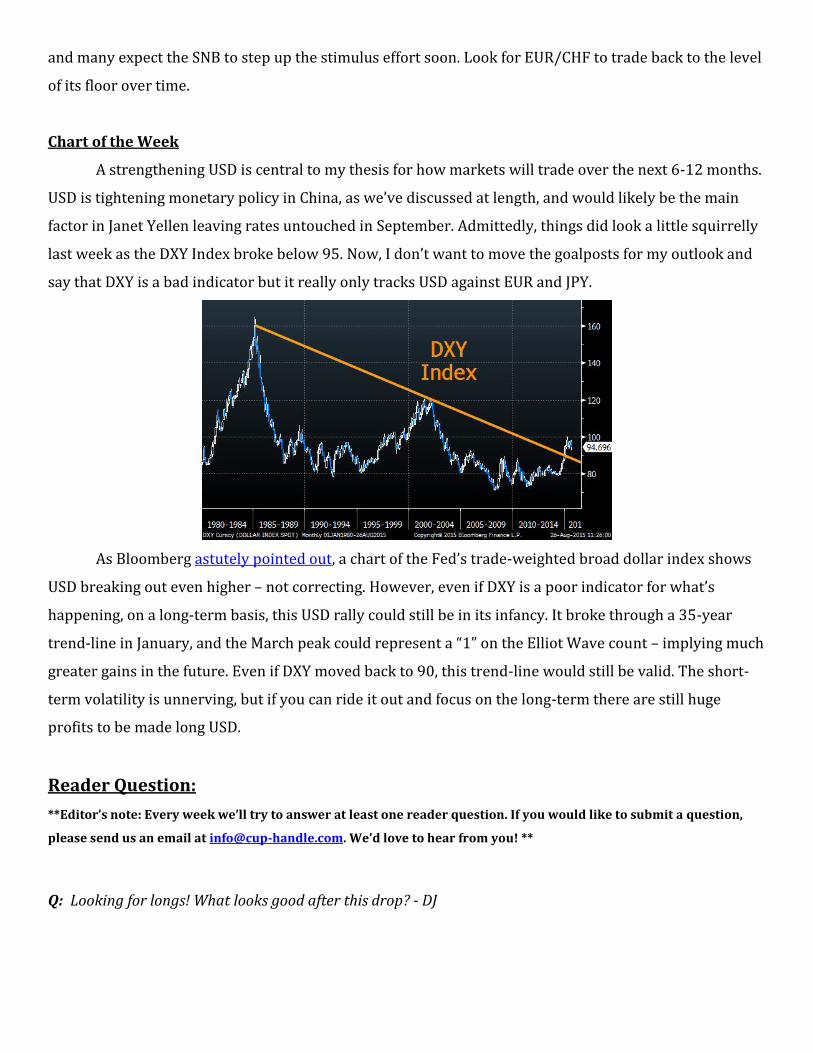

Chart of the Week

A strengthening USD is central to my thesis for how markets will trade over the next 6-12 months.

USD is tightening monetary policy in China, as we’ve discussed at length, and would likely be the main

factor in Janet Yellen leaving rates untouched in September. Admittedly, things did look a little squirrelly

last week as the DXY Index broke below 95. Now, I don’t want to move the goalposts for my outlook and

say that DXY is a bad indicator but it really only tracks USD against EUR and JPY.

As Bloomberg astutely pointed out, a chart of the Fed’s trade-weighted broad dollar index shows

USD breaking out even higher – not correcting. However, even if DXY is a poor indicator for what’s

happening, on a long-term basis, this USD rally could still be in its infancy. It broke through a 35-year

trend-line in January, and the March peak could represent a “1” on the Elliot Wave count – implying much

greater gains in the future. Even if DXY moved back to 90, this trend-line would still be valid. The short-

term volatility is unnerving, but if you can ride it out and focus on the long-term there are still huge

profits to be made long USD.

Reader Question:

**Editor’s note: Every week we’ll try to answer at least one reader question. If you would like to submit a question,

please send us an email at [email protected]. We’d love to hear from you! **

Q: Looking for longs! What looks good after this drop? - DJ

A: I’m still relatively pessimistic about the broader outlook, but the most intriguing long on my radar is

EWZ - Brazil ETF. I haven't had a position the whole time, but I've been very bearish Brazil since back in

2012. However, there's already a lot of bad news priced in. Rates are already the highest in the world,

meaning there’s capacity to stimulate. Also, Brazil’s President, Dilma Rouseff, could get tossed out of

office, which should ultimately be bullish. If China fires up their stimulus machine, which they'll probably

be forced to, Brazil could really benefit a lot.

That’s all. See you next week!

For any questions or comments, please email us at: [email protected] Please visit our website. Follow us on Twitter: @cuphandlemacro

Disclaimer: None of the information contained in this publication constitutes a recommendation that any particular investment, security, portfolio,

transaction or investment strategy is suitable for any specific person. This publication may contain news, information, speculation, rumors, opinions and/or commentary. Cup & Handle Macro Research, LLC (“C&H”), is not permitted to offer personalized trading or investment advice to subscribers. C&H is not a broker/dealer, an exchange or a futures commission merchant and is not subject to regulation by the U.S. Securities and Exchange Commission, the U.S. Commodity Futures Trading Commission or any similar regulatory authority in connection with its activities. C&H does not act as an investment adviser or a commodity trading advisor and does not provide any investment advice or commodity trading advice. The information, statements, views and opinions included in this publication are based on sources (both internal and external) considered to be reliable, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness, including without limitation, any implied warranties of merchantability, fitness for use for a particular purpose, accuracy or non-infringement. Use of any information obtained from or through this publication is entirely at your own risk. C&H does not routinely moderate, screen or edit any third party content. Such information, statements, views and opinions are expressed as of the date of publication, are subject to change without further notice and do not constitute a solicitation for the purchase or sale of any investment referenced in the publication. SUBSCRIBERS SHOULD VERIFY ALL CLAIMS AND DO THEIR OWN RESEARCH BEFORE INVESTING IN ANY INVESTMENTS REFERENCED IN THIS PUBLICATION. INVESTING IN SECURITIES, PRECIOUS METALS, AND OTHER INVESTMENTS, SUCH AS OPTIONS AND FUTURES, IS SPECULATIVE AND CARRIES A HIGH DEGREE OF RISK. SUBSCRIBERS MAY LOSE MONEY TRADING AND/OR INVESTING IN ANY SUCH INVESTMENTS. ALL USERS OF THIS PUBLICATION ACKNOWLEDGE AND AGREE THAT NO PERSON OR ENTITY INVOLVED IN THE PUBLICATION OF THIS PUBLICATION SHALL HAVE ANY LIABILITY FOR ANY LOSS OR DAMAGES, INCLUDING WITHOUT LIMITATION, CLAIMS FOR LOSS OF MONEY, ERRORS, DEFAMATION OR OTHER EXPENSES, RELATING TO ANY PLACEMENT OF CONTENT IN THIS PUBLICATION, OR ANY RELIANCE ON ANY INFORMATION CONTAINED HEREIN, OR THROUGH ANY LINKS CONTAINED IN THIS PUBLICATION OR THE SITE. Employees and/or affiliates of C&H may give advice and take action with respect to clients and/or investments that differs from the information, statements, views and opinions included in this publication. Nothing herein or in the subscription agreement shall limit or restrict the right of employees or affiliates of C&H to perform investment management, advisory or other services for any persons or entities. In addition, nothing herein or in the subscription agreement shall limit or restrict employees or affiliates of C&H from buying, selling or trading securities or other investments for their personal or other related accounts, or for the accounts of their clients. Employees or affiliates of C&H may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. C&H shall have no obligation whatsoever to recommend securities or investments in this publication as a result of its employees’ or affiliates’ investment activities for their own accounts or for any other accounts. This publication is proprietary and intended solely for the use of its subscribers, and is protected by domestic and international copyright laws. No license is granted to any subscriber, except for the subscriber’s personal use. No part of this publication or its contents may be copied, downloaded, stored, further transmitted, or otherwise reproduced, transferred, or used, in any form or by any means, except as expressly permitted under the subscription agreement or with the prior written permission of C&H. Any further disclosure or use, distribution, dissemination or copying of this publication, or any portion hereof, is strictly prohibited. There is no guarantee that this site will operate in an uninterrupted or error-free manner or is free of viruses or other harmful components. This publication assumes no responsibility for any omission, interruption, deletion, defect, delay in operation or transmission, communications line failure, theft or destruction or unauthorized access to, or alteration hereof. The publication is not responsible for any technical malfunction or other problems of any computer, telephone or other equipment, or software occurring for any reason, including but not limited to, technical problems or traffic congestion on the Internet or at any site or with respect to this publication or combination thereof, including injury or damage to any person’s computer, mobile phone, or other hardware or software, related to or resulting from using or downloading any content hereof.