Auditing When You Don't Have an Internal Auditor

40

AUDITING WHEN YOU DON’T HAVE AN INTERNAL AUDITOR AASBO Annual Conference and Exposition July 21, 2016 Jennifer Shields, Heinfeld, Meech & Co., P.C. Sara Kirk, Heinfeld, Meech & Co., P.C. Lizette Huie, Sahuarita Unified School District

-

Upload

diane-bradley -

Category

Government & Nonprofit

-

view

101 -

download

1

Transcript of Auditing When You Don't Have an Internal Auditor

AUDITING WHEN YOU DON’T HAVE AN

INTERNAL AUDITORAASBO Annual Conference and Exposition

July 21, 2016

Jennifer Shields, Heinfeld, Meech & Co., P.C. Sara Kirk, Heinfeld, Meech & Co., P.C.

Lizette Huie, Sahuarita Unified School District

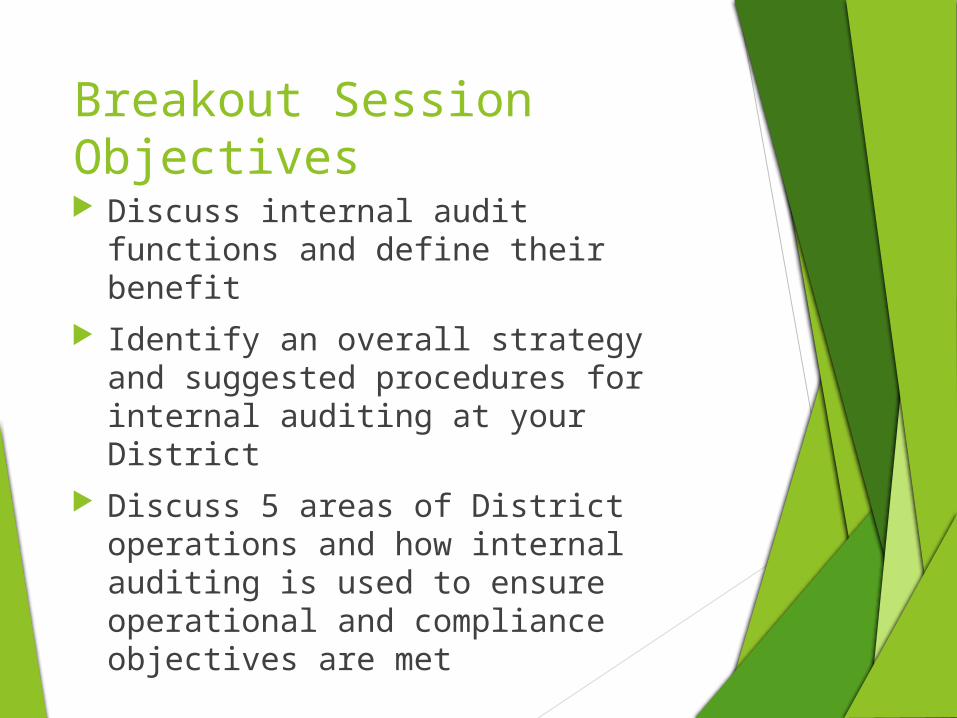

Breakout Session Objectives Discuss internal audit functions and

define their benefit Identify an overall strategy and

suggested procedures for internal auditing at your District

Discuss 5 areas of District operations and how internal auditing is used to ensure operational and compliance objectives are met

What is internal auditing?

Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization's operations. It helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes. Internal auditing is a catalyst for improving an organization's governance, risk management and management controls by providing insight and recommendations based on analyses and assessments of data and business processes.

We already have an auditor!Internal Auditor Evaluate and

improve the effectiveness of control processes

Provide assurances to management and help carry out objectives

Assist management in fulfilling duties

External Auditor Add credibility and

reliability to financial reports

Test compliance Report to State and

Federal Agencies

Benefits of Internal Auditing

Test procedures, verify consistent and effective

Verify compliance

Cross train employees

Identify issues early, reduce risk

Detect fraud

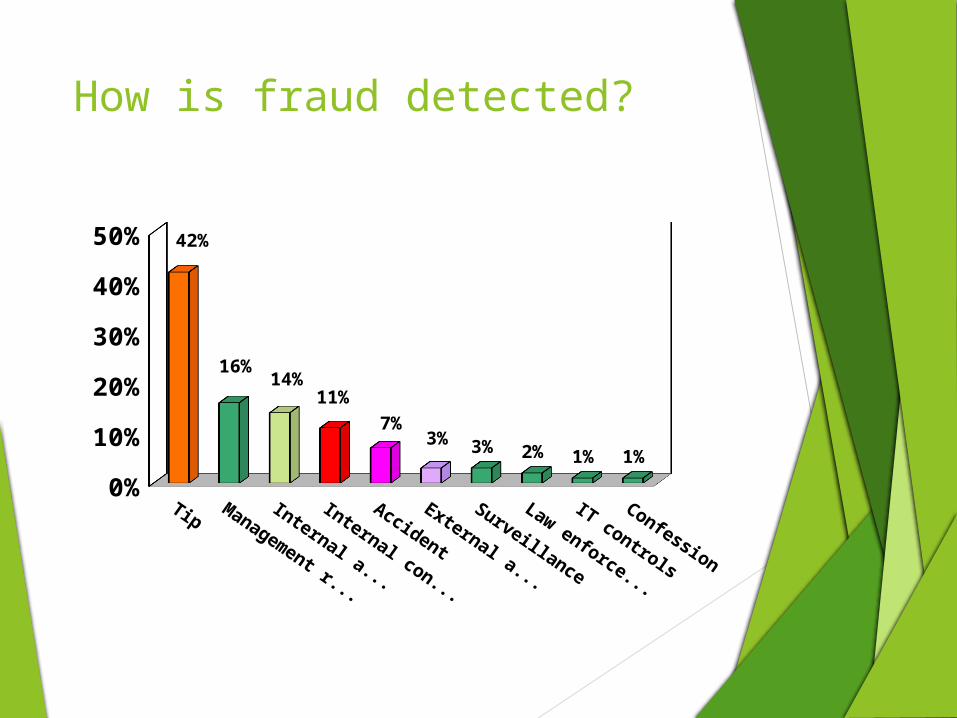

How is fraud detected?

Tip Management re...

Internal audit

Internal controls

Accident

External audit

Surveillance

Law enforce...

IT controls

Confession

0%

10%

20%

30%

40%

50% 42%

16%14%

11%7%

3% 3% 2% 1% 1%

Who Can Perform Internal Auditing Procedures at Your District?

Payroll clerks

Accounts payable clerks

Attendance clerks/School secretaries

Other district office or school

site staffAnyone!

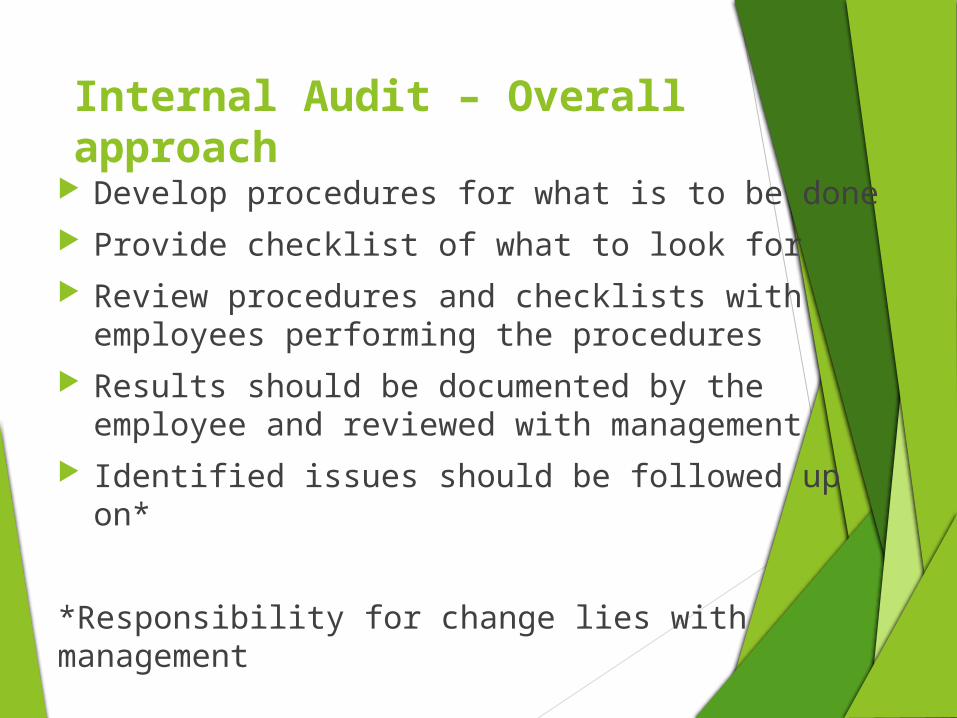

Internal Audit – Overall approach

Develop procedures for what is to be done Provide checklist of what to look for Review procedures and checklists with employees

performing the procedures Results should be documented by the employee

and reviewed with management Identified issues should be followed up on*

*Responsibility for change lies with management

What types of audit procedures are there?

Analytical Inquiry

Inspection of records

Observation

Recalculation and

reperformance

Implementing an Internal Audit Program at Your District

Evaluate your staff: Existing workloads / re-organization Strengths/weaknesses Cross training efforts & succession planning

Meet with staff: Discuss & establish clear expectations Explain the audit requirements and emphasize the

importance of internal auditing practices Check for understanding

Implementing an Internal Audit Program at Your District

Self Audits Encourage the opportunity to conduct staff self

audits.

Assign peer audits/reviews Explain benefits of cross training and succession

planning to help relieve pressure or impression of employee scrutiny.

Significant operational areas/Risk areas

Student

attendance

Cash handling

- Student activities/Auxilia

ry operatio

ns

Accounts

payable/PurchasingPayrollGener

al Ledger

Student attendance

Internal Audit – Student attendance– Suggested Procedures

Select

• Select an entry or withdrawal transaction from the SMS

Verify

• Verify supported by an enrollment form or Official Notice of Pupil Withdrawal

Internal Audit – Student attendance– Suggested Procedures

Select •Select a student with a partial day absence reported for a day from a state report

Verify •Recalculate the amount prorated and reported for accuracy

Internal Audit – Student attendance

Sahuarita Unified School District

Finding the right staff Work ethic & pride in work Attention to detail

SRMS Technician Implementation of the internal audit Sample audits at every school regularly Site visits On going training

Internal Audit – Student attendance Sahuarita Unified School District

•Prior Year Findings•Internal Controls

Focused Review

•Staff Meetings•Discussions for solutions

Teamwork Efforts

•Set clear & focused expectations for upcoming year.•Review changes / new regulations

Set Clear Expectations

Internal Audit – Student attendance

Sahuarita Unified School District

Attendance external audit comparison results: 2013 – 11 of 23 Attendance Audit Findings 2014 – 6 of 22 Attendance Audit Findings 2015 – 2 of 22 Attendance Audit Findings

Cash handling

Internal Audit – Cash Handling – Suggested Procedures

Select

• Select a deposit from banking records or the accounting records (GL)

Verify

• Verify deposit supported by deposit slip, cash collection report containing reconciliation of items sold to cash collected as applicable

Internal Audit – Cash Handling – Suggested Procedures

Cash collection Deposit

Recording in accounting

records Reconciliation

VERIFY SEGREGATION OF DUTIES PERIODICALLY

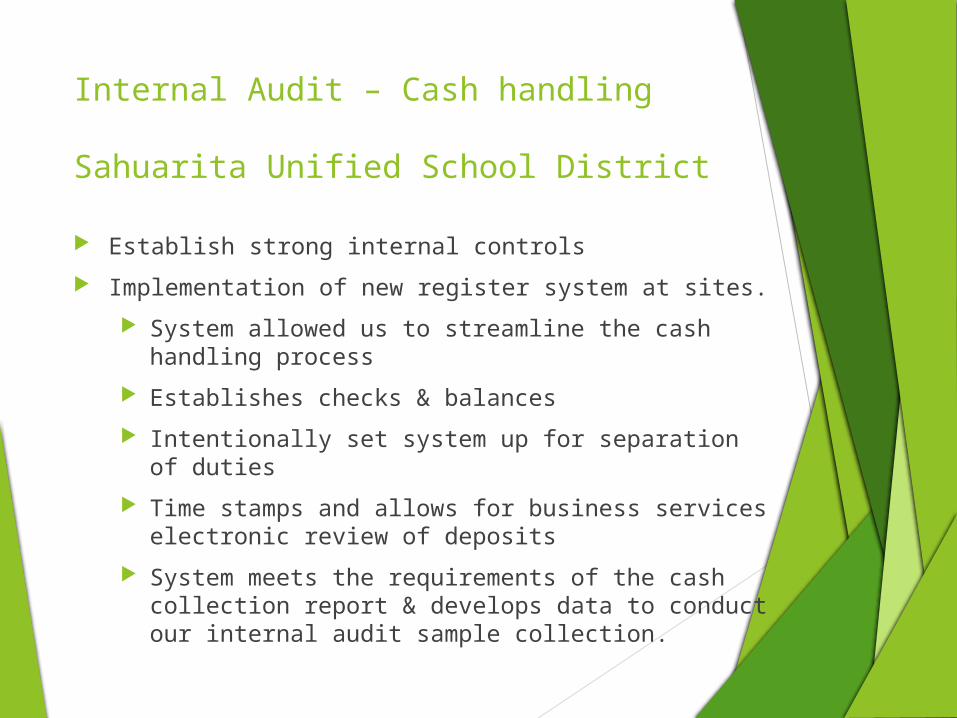

Internal Audit – Cash handling

Sahuarita Unified School District Establish strong internal controls Implementation of new register system at sites.

System allowed us to streamline the cash handling process

Establishes checks & balances Intentionally set system up for separation of duties Time stamps and allows for business services

electronic review of deposits System meets the requirements of the cash

collection report & develops data to conduct our internal audit sample collection.

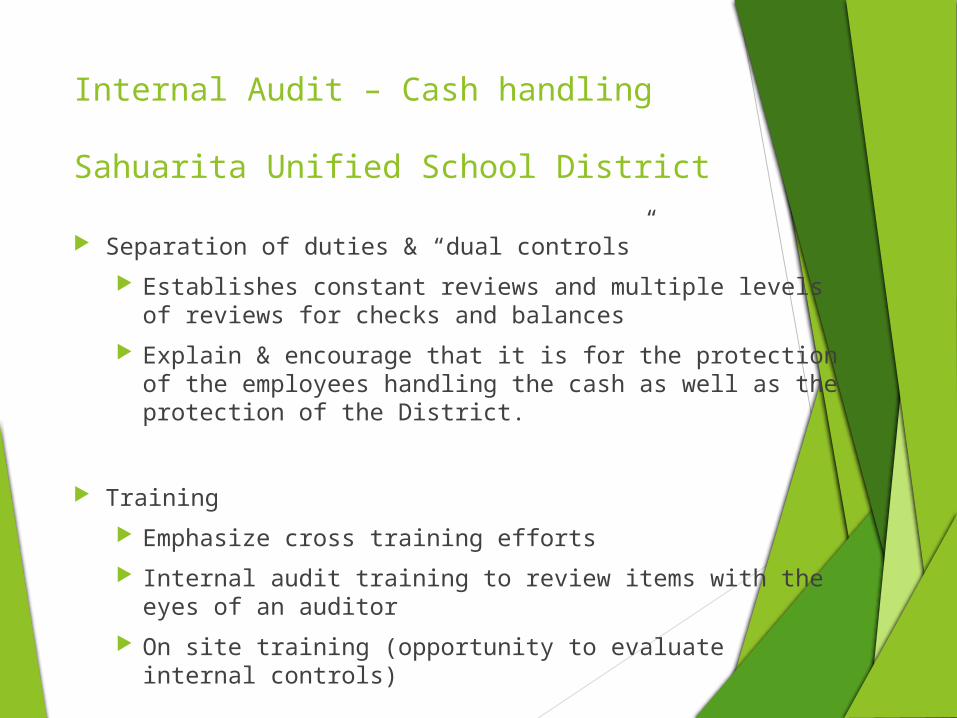

Internal Audit – Cash handling

Sahuarita Unified School District Separation of duties & “dual controls”

Establishes constant reviews and multiple levels of reviews for checks and balances

Explain & encourage that it is for the protection of the employees handling the cash as well as the protection of the District.

Training Emphasize cross training efforts Internal audit training to review items with the eyes of an

auditor On site training (opportunity to evaluate internal controls)

Internal Audit – Cash handling

Sahuarita Unified School District

2013: Timely Deposits 5 of 5 Audit Findings

Student Activities 4 of 5 Tax Credit

2014 – Timely Deposits 2 of 5 Student

Activities 0 of 5 Tax Credit

2015: None 0 of 10 Tax

Credits/SA & Aux!

Accounts payable/Purchasing

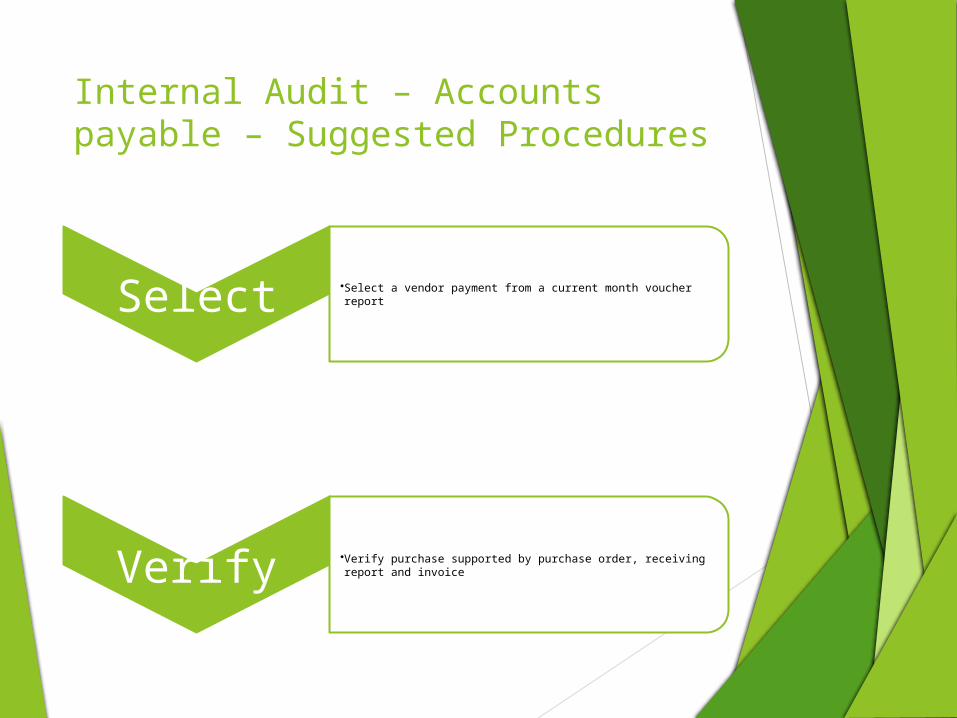

Internal Audit – Accounts payable – Suggested Procedures

Select •Select a vendor payment from a current month voucher report

Verify •Verify purchase supported by purchase order, receiving report and invoice

Internal Audit – Accounts payable – Suggested Procedures

Verify an approved PO was in place prior to the order or receipt of goods

and servicesVerify goods or services were

received prior to payment

Review account coding

Spot check payments made from federal

funds for allowability

Verify invoice checked for clerical

accuracy

Internal Audit - Purchasing

Vendor Totals Report

Cumulative Purchases

Quote Threshold

Bid Threshold

Completed Files

Internal Audit – Purchasing – Suggested Procedures

Ensure procurement rules were followed

as applicableReview procurement

file for required documentation

Review invoices against contract for alignment of

contract terms and pricing

Internal Audit – Accounts payable & Purchasing

Sahuarita Unified School District

Account responsibility rotations Semester or quarterly account rotations

Self audits & peer audits Utilize our financial system to collect data

Perform internal audits as part of job requirements Utilize the compliance questionnaire as a

checklist.

Internal Audit – Accounts payable & Purchasing

Sahuarita Unified School District

Audit Finding Results: 2013 – Credit Card

Policies/Transactions & TC purchases

2014 – Credit Card Policies/Transactions

2015 – Zero AP/Purchasing findings!

Payroll

Internal Audit – Payroll – Suggested Procedures

Recalculate hourly payroll/OT pay

Spot checks of employees paid from federal programs for allowability

Verify register review

Review employee files for required documents

Verify start and end dates for new and terminated employees

Internal Audit – Payroll

Sahuarita Unified School District

Routine audit checks regularly Director of Business Services

Self & Peer Internal Audit Utilize our financial system to collect data Use opportunity for peer audit to benefit

cross training Established procedures, expectations,

internal controls.

Internal Audit – Payroll

Sahuarita Unified School District

Audit Finding Results:

2013 - None

2014 – 1 Compensated Absences

2015 – None

General ledger

Internal Audit – General Ledger – Suggested Procedures

Review chart of accounts for account code strings

that do not conform to the District’s Chart of Accounts

Negative assets, liabilities, revenues (with the exception of interest) or expenditures?

High level analysis of revenue and expenditure items

Verify adjusting journal entries are reviewed

and approved

Internal Audit – General ledger

Sahuarita Unified School District Consistent & timely reconciliation efforts

Ensure deadlines are met for compliance Utilize Calendar of Events (USFR)

Separation of Duties Review & approval of JE’s both written and

electronically

Staff evaluation & reorganization – Strength & weaknesses (Fixed Assets)

Internal Audit – General ledger

Sahuarita Unified School District

Audit Finding Results:

2013 – Fixed asset findings

2014 – Fixed asset findings & reconciliations

2015 – None

Questions? Thank you for attending!