Copyright © 2014 Pearson Education Chapter 6 Audit Responsibilities and Objectives.

Upload

evelyn-crossCategory

view

222download

2

Auditing 81.3550Auditing 81.3550

Responsibilities & Objectives

Chapter 5

Responsibilities & Objectives

Chapter 5

HighlightsHighlights

• Audit Objectives – the specifics

• Management & Auditor Responsibilities

• Audit Approach

• Assertions, Objectives Transactions, & Ending Balances

• The Audit Process

• Audit Objectives – the specifics

• Management & Auditor Responsibilities

• Audit Approach

• Assertions, Objectives Transactions, & Ending Balances

• The Audit Process

Audit ObjectivesAudit Objectives

• To express an opinion on the F/S that they present fairly in all material respects in accordance with GAAP

• Accumulate evidence to enable auditor to express an opinion

• Need to ensure complete and verifiable evidence incase called upon to the defend quality of audit and/or opinion

• To express an opinion on the F/S that they present fairly in all material respects in accordance with GAAP

• Accumulate evidence to enable auditor to express an opinion

• Need to ensure complete and verifiable evidence incase called upon to the defend quality of audit and/or opinion

Management’s ResponsibilityManagement’s Responsibility

• What exactly are management responsibilities when it comes to the F/S?– Maintaining adequate Internal Controls

– Fair representations

– Setting/adopting sound accounting policies

– F/S preparation including notes

• Management has the most intimate knowledge of the business, transactions, as well as the ultimate level of control

• What exactly are management responsibilities when it comes to the F/S?– Maintaining adequate Internal Controls

– Fair representations

– Setting/adopting sound accounting policies

– F/S preparation including notes

• Management has the most intimate knowledge of the business, transactions, as well as the ultimate level of control

Auditor’s ResponsibilitiesAuditor’s Responsibilities• Performs audit meeting GAAS and GAAP

requirements• Including:

– Maintaining “professional skepticism”– Using professional judgment– Adequate planning and gathering of evidence

• Not responsible to uncover fraud but must act on fraud if it is discovered during the audit

• May include expanding testing to determine if an unintentional error vs. fraudulent behaviour

• Performs audit meeting GAAS and GAAP requirements

• Including:– Maintaining “professional skepticism”– Using professional judgment– Adequate planning and gathering of evidence

• Not responsible to uncover fraud but must act on fraud if it is discovered during the audit

• May include expanding testing to determine if an unintentional error vs. fraudulent behaviour

General Fraud & The AuditGeneral Fraud & The Audit

• Fraud Fraud – is criminal deception intended to benefit the deceiver most often financially

• Estimated 75% of Fraud goes undetected• when performing the audit need to think about the

likelihood of fraud and the type in a particular area• GONE Theory – essential ingredients for fraud to occur

– G – Greed– O – Opportunity– N – Need (motivation)– E - Exposure

• Fraud Fraud – is criminal deception intended to benefit the deceiver most often financially

• Estimated 75% of Fraud goes undetected• when performing the audit need to think about the

likelihood of fraud and the type in a particular area• GONE Theory – essential ingredients for fraud to occur

– G – Greed– O – Opportunity– N – Need (motivation)– E - Exposure

Fraud & The AuditFraud & The Audit• Employee Fraud• Chances fraud is committed by an employee (in Canada)

4 out of 5 times (Report on Business Magazine)• Most common theft of assets• Management Fraud – often more difficulty to uncover

due to increased level of opportunity, and increased level of sophistication in covering up the fraud

• Typical frauds involve share price manipulation, related party transactions, expense related and kickbacks

• Employee Fraud• Chances fraud is committed by an employee (in Canada)

4 out of 5 times (Report on Business Magazine)• Most common theft of assets• Management Fraud – often more difficulty to uncover

due to increased level of opportunity, and increased level of sophistication in covering up the fraud

• Typical frauds involve share price manipulation, related party transactions, expense related and kickbacks

Fraud & The AuditFraud & The Audit

• Computer Fraud - basically fraud with assistance from a(n) computer(s) often involves using software

• Examples include: obtaining customer information, theft of credit card numbers, identity theft, redirecting/manipulation of automatic payroll/payments

• Computer Fraud - basically fraud with assistance from a(n) computer(s) often involves using software

• Examples include: obtaining customer information, theft of credit card numbers, identity theft, redirecting/manipulation of automatic payroll/payments

Illegal ActsIllegal Acts

• Defn: a violation of a domestic of foreign statutory law or government regulation attributable to the entity under audit, or to management or employees acting on the entity's behalf. (Section 5136)

• Defn: a violation of a domestic of foreign statutory law or government regulation attributable to the entity under audit, or to management or employees acting on the entity's behalf. (Section 5136)

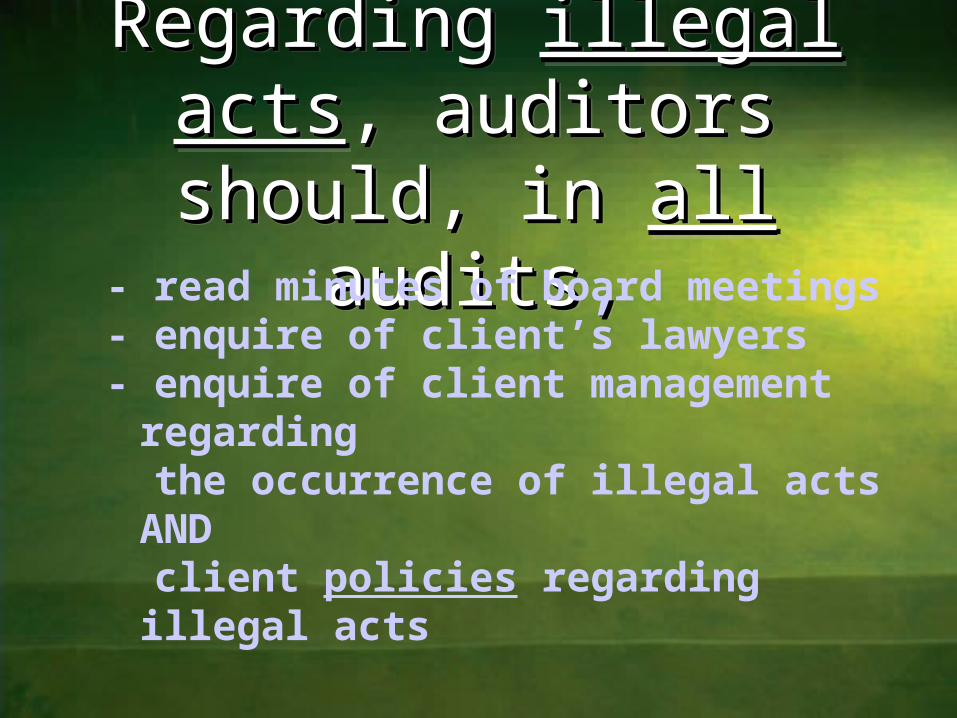

Regarding Regarding illegal actsillegal acts, , auditors should, in auditors should, in allall audits audits,,

Regarding Regarding illegal actsillegal acts, , auditors should, in auditors should, in allall audits audits,,

- read minutes of board meetings- enquire of client’s lawyers- enquire of client management

regarding the occurrence of illegal acts AND client policies regarding illegal acts

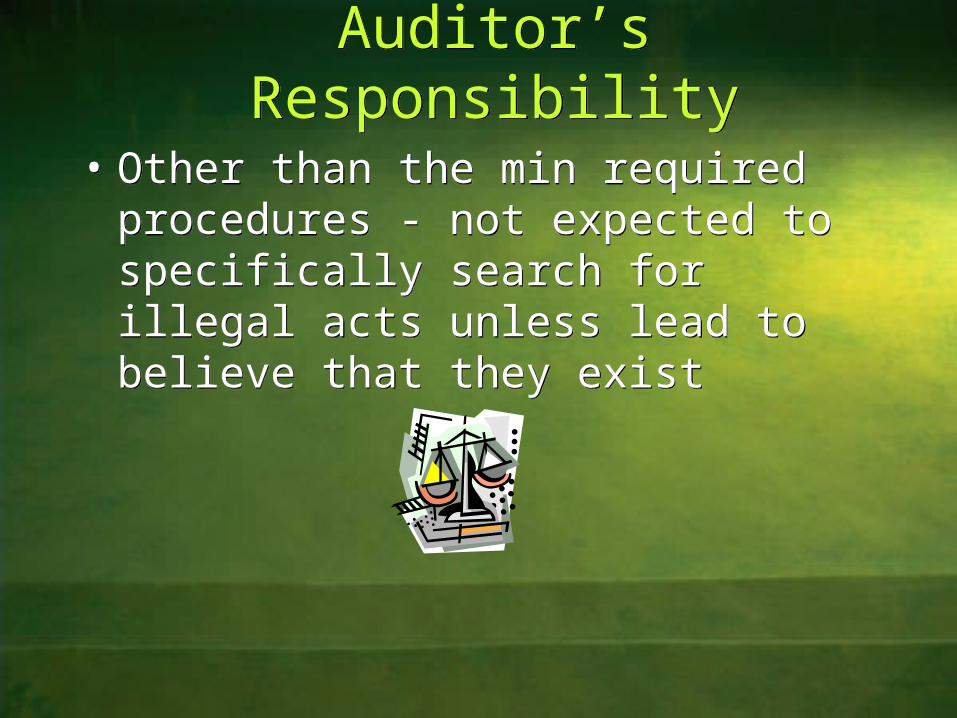

Auditor’s ResponsibilityAuditor’s Responsibility

• Other than the min required procedures - not expected to specifically search for illegal acts unless lead to believe that they exist

• Other than the min required procedures - not expected to specifically search for illegal acts unless lead to believe that they exist

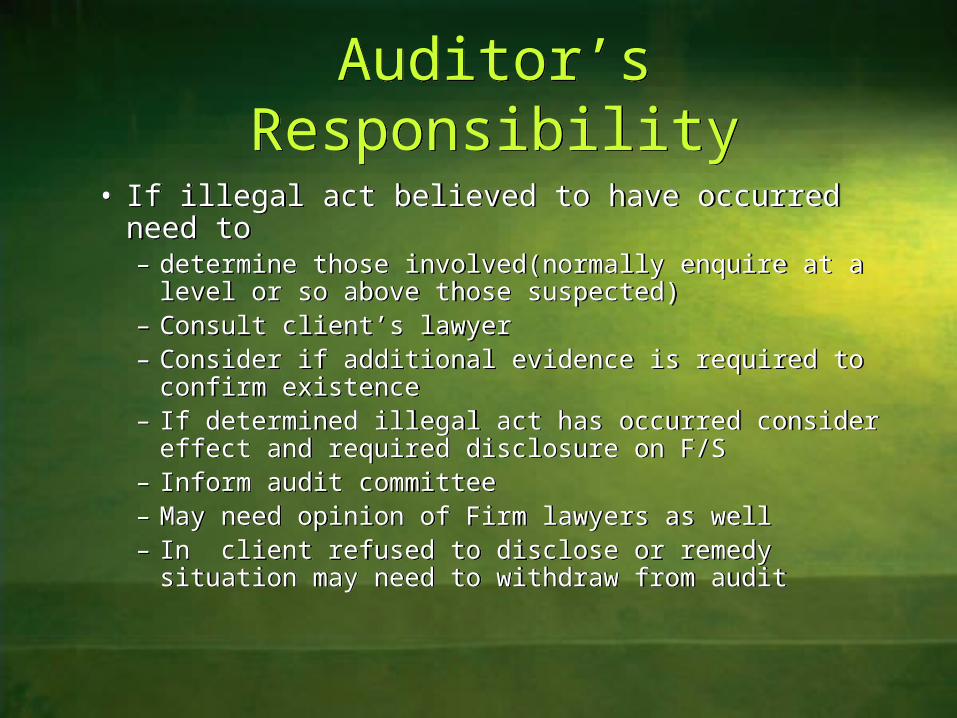

Auditor’s ResponsibilityAuditor’s Responsibility

• If illegal act believed to have occurred need to– determine those involved(normally enquire at a level or so

above those suspected)– Consult client’s lawyer– Consider if additional evidence is required to confirm

existence– If determined illegal act has occurred consider effect and

required disclosure on F/S– Inform audit committee – May need opinion of Firm lawyers as well– In client refused to disclose or remedy situation may need to

withdraw from audit

• If illegal act believed to have occurred need to– determine those involved(normally enquire at a level or so

above those suspected)– Consult client’s lawyer– Consider if additional evidence is required to confirm

existence– If determined illegal act has occurred consider effect and

required disclosure on F/S– Inform audit committee – May need opinion of Firm lawyers as well– In client refused to disclose or remedy situation may need to

withdraw from audit

5 -44Copyright 2003 Pearson Education Canada Inc.

EE

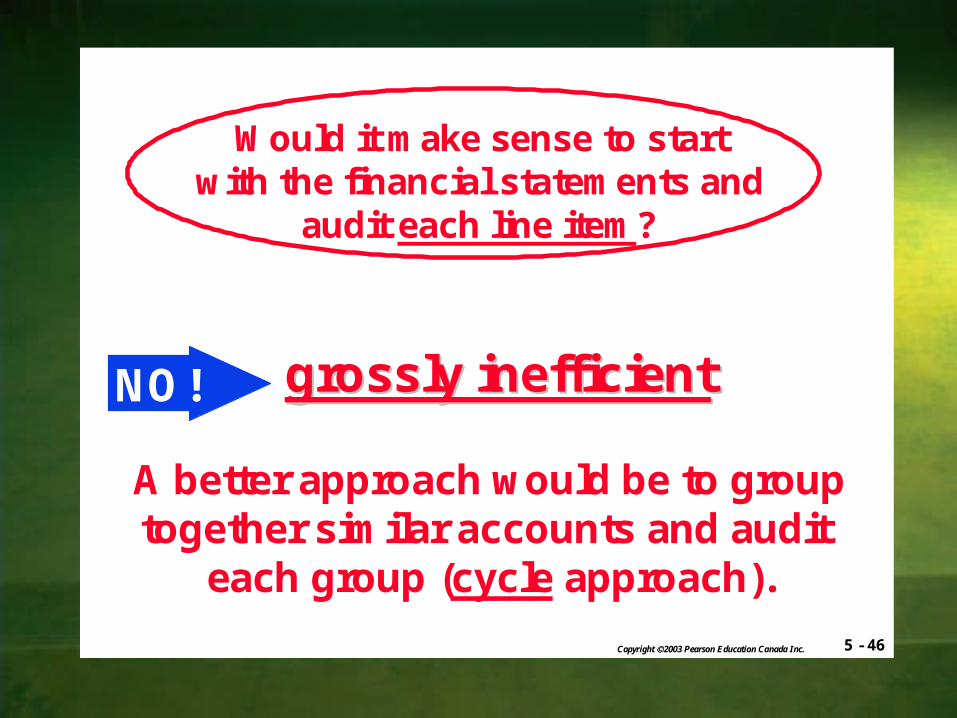

Inan auditengagement,where doesthe auditorstart?

TTNN

CCLLII

5 - 46Copyright 2003 Pearson Education Canada Inc.

A better approach would be to grouptogether similar accounts and audit

each group (cycle approach).

NO! grossly inefficientgrossly inefficient

Would it make sense to startwith the financial statements and

audit each line item?

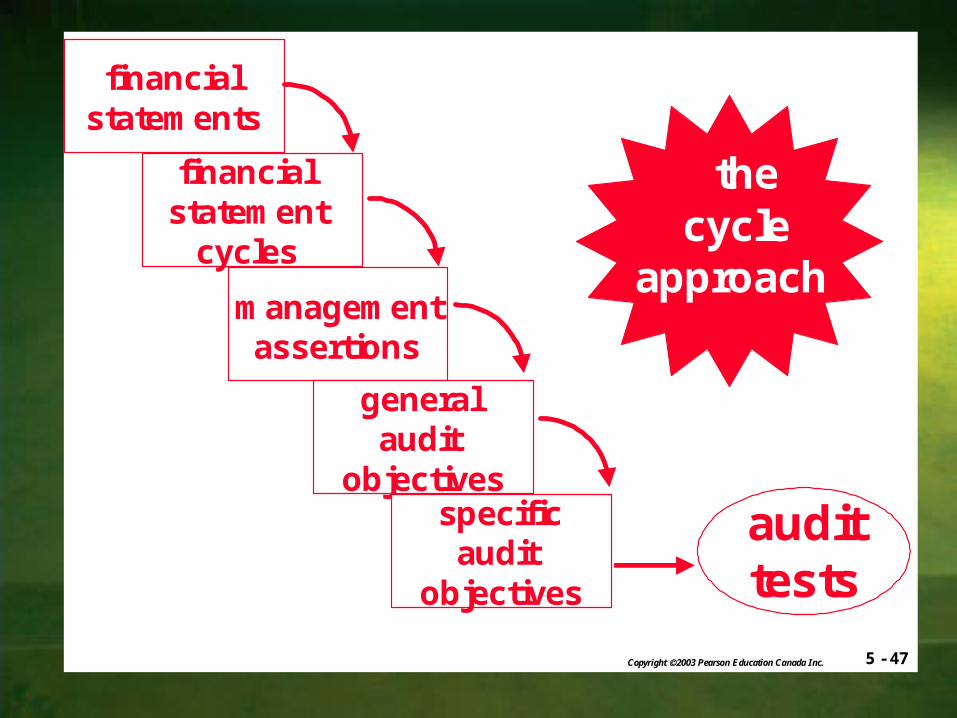

5 - 47Copyright 2003 Pearson Education Canada Inc.

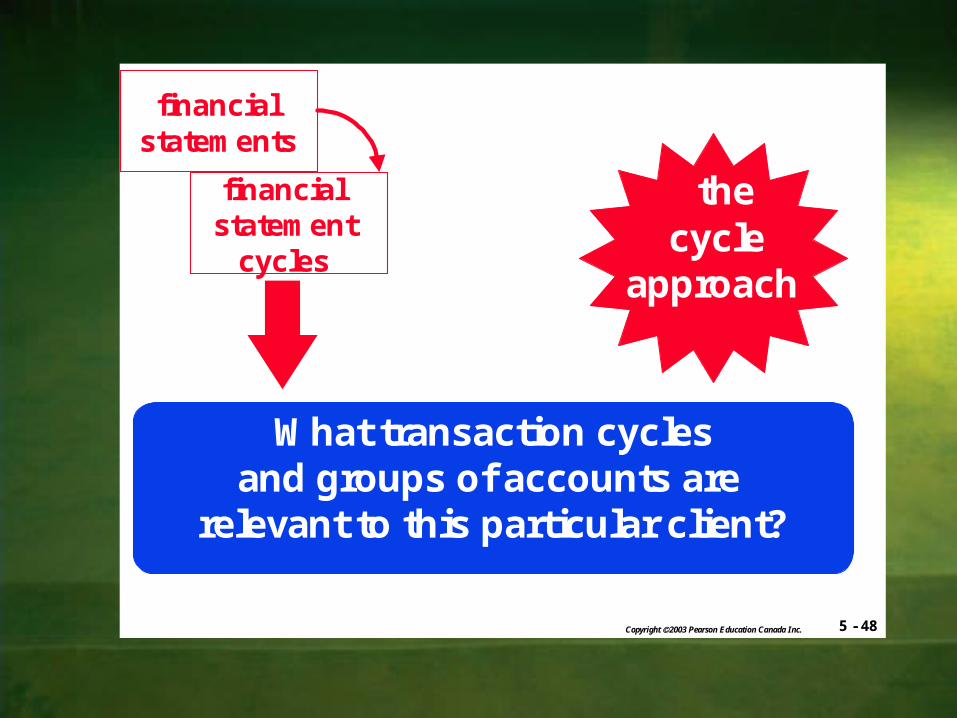

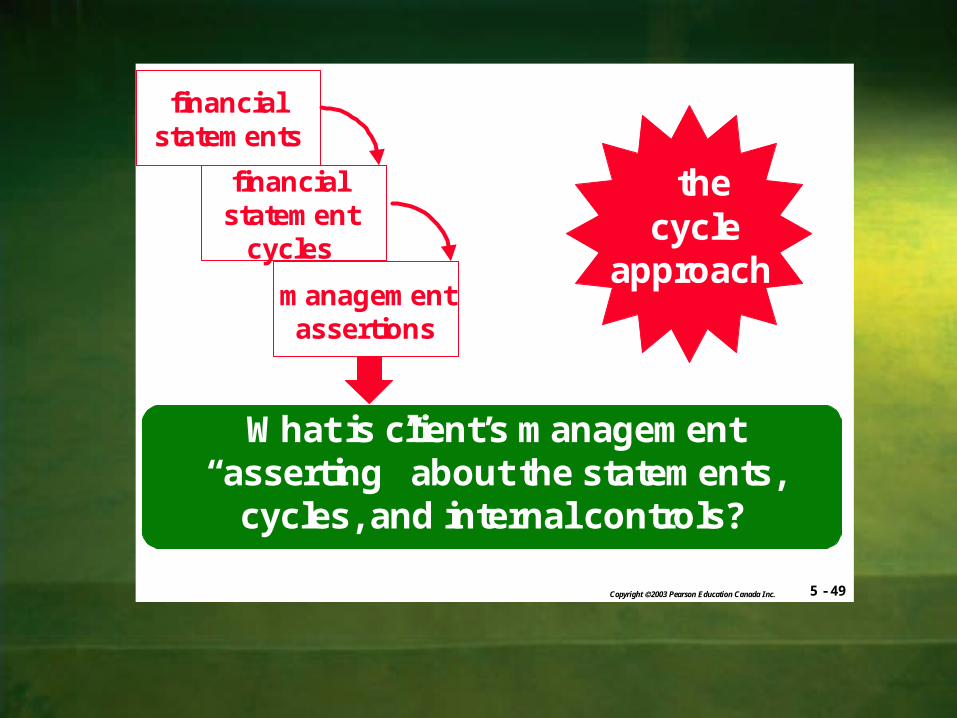

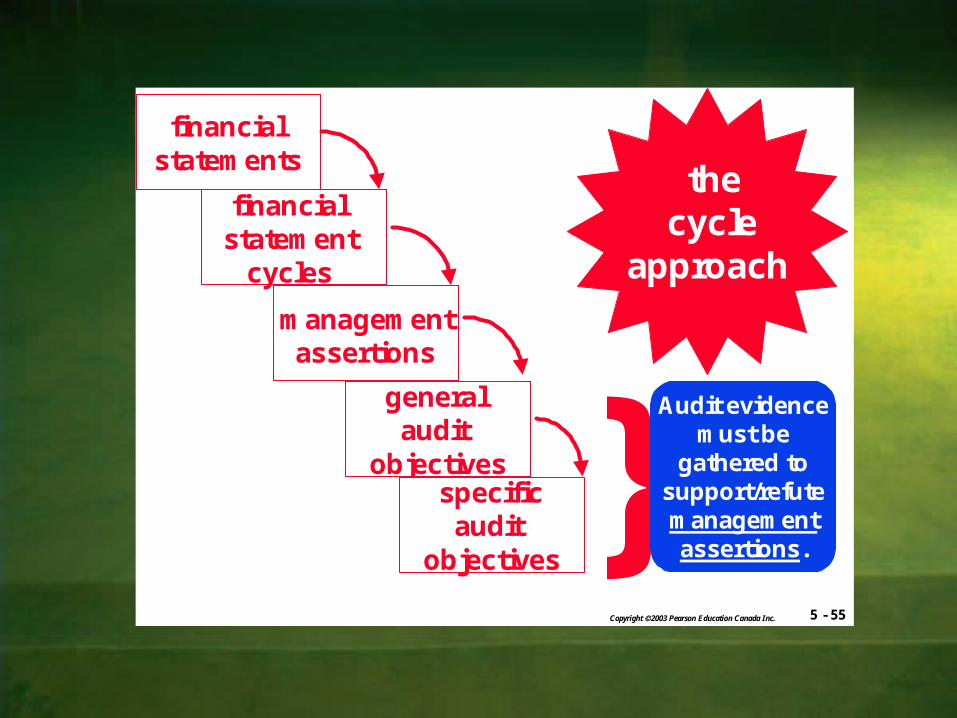

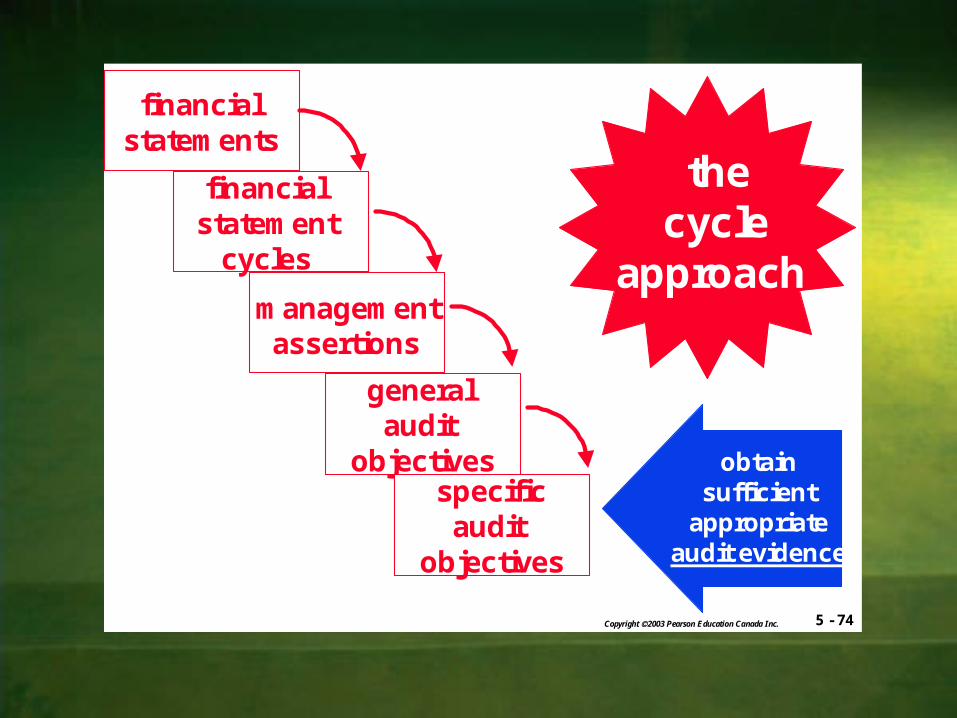

financial statements

financialstatement

cycles

managementassertions

generalaudit

objectivesspecificaudit

objectives

thecycle

approach

audittests

5 - 48Copyright 2003 Pearson Education Canada Inc.

financial statements

financialstatement

cycles

thecycle

approach

What transaction cyclesand groups of accounts are

relevant to this particular client?

5 - 49Copyright 2003 Pearson Education Canada Inc.

financial statements

financialstatement

cycles

managementassertions

thecycle

approach

What is client’s management“asserting” about the statements,

cycles, and internal controls?

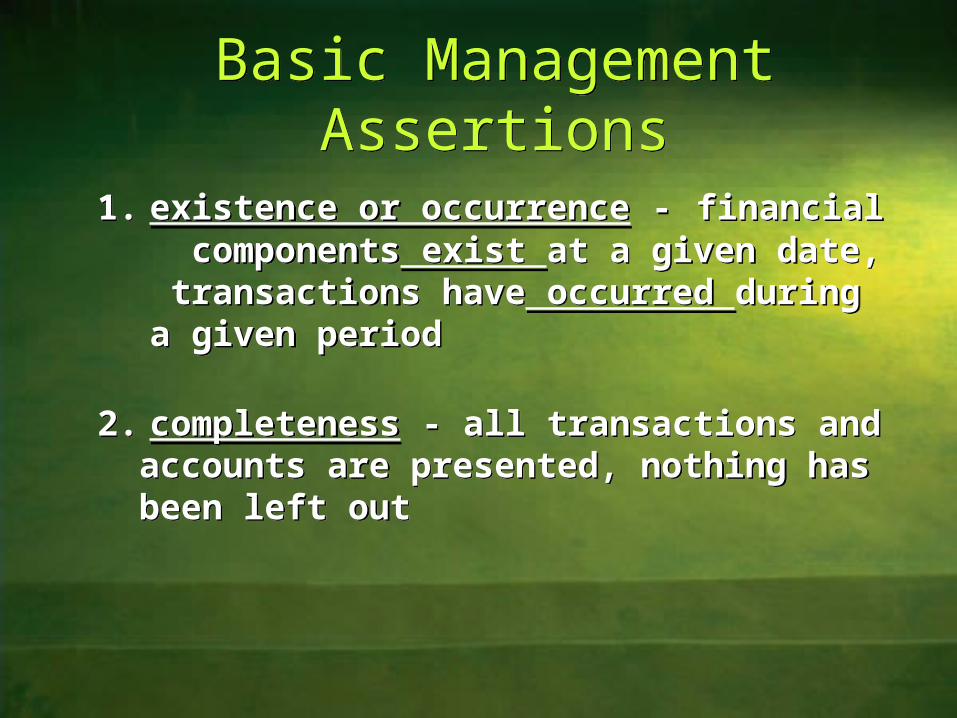

Basic Management AssertionsBasic Management Assertions

1. existence or occurrence - financial components exist at a given date, transactions have occurred during a given period

2. completeness - all transactions and accounts are presented, nothing has been left out

1. existence or occurrence - financial components exist at a given date, transactions have occurred during a given period

2. completeness - all transactions and accounts are presented, nothing has been left out

Basic Management AssertionsBasic Management Assertions

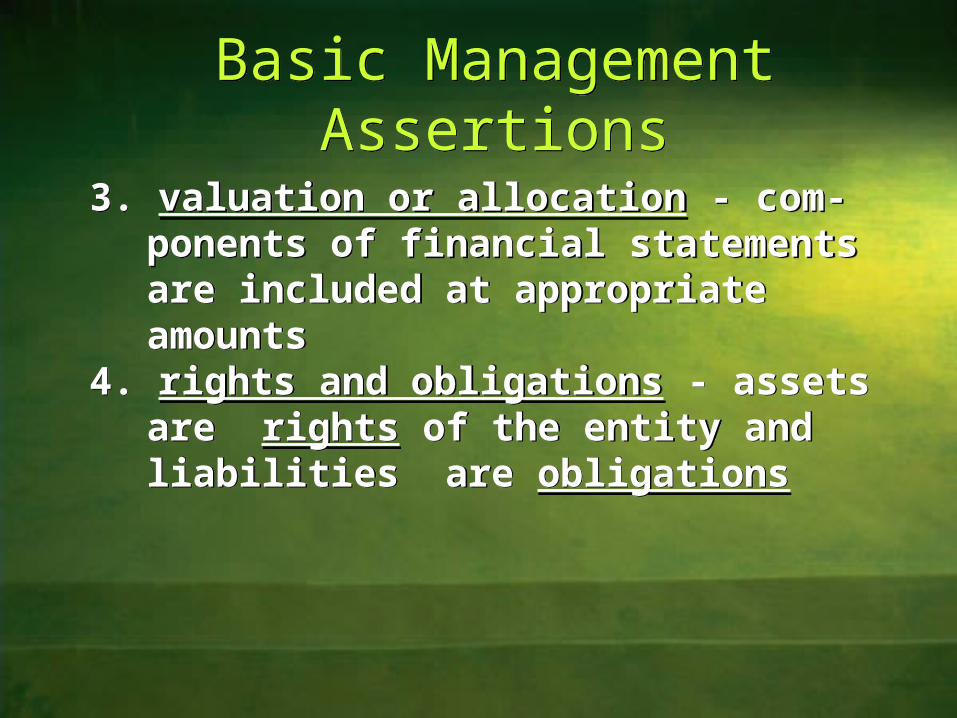

3. valuation or allocation - com- ponents of financial statements are included at appropriate amounts 4. rights and obligations - assets are

rights of the entity and liabilities are obligations

3. valuation or allocation - com- ponents of financial statements are included at appropriate amounts 4. rights and obligations - assets are

rights of the entity and liabilities are obligations

Basic Management AssertionsBasic Management Assertions

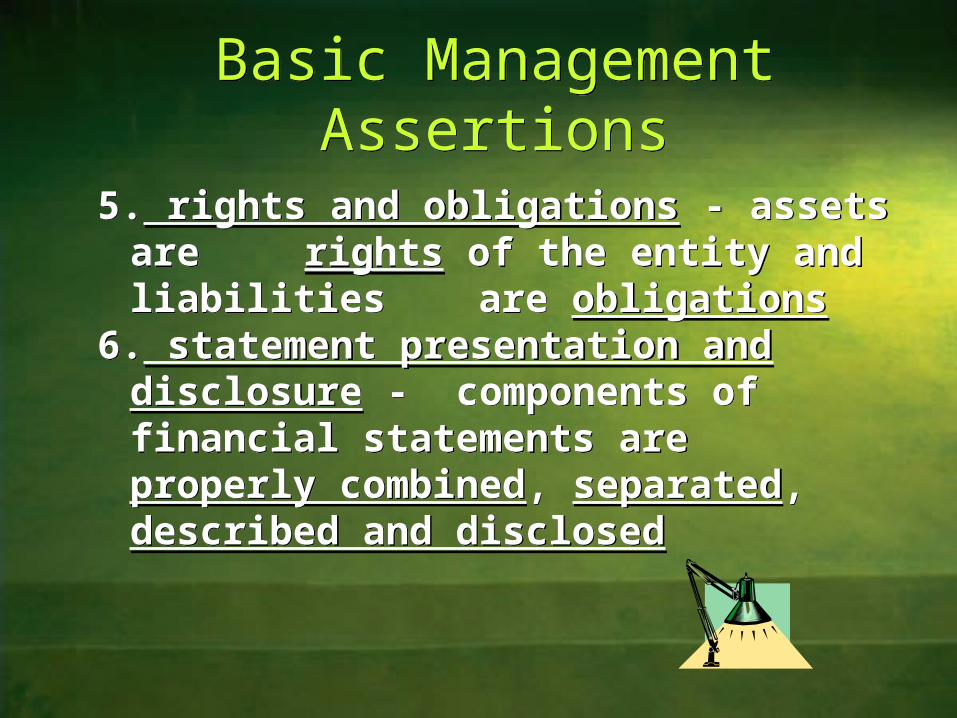

5. rights and obligations - assets are rights of the entity and liabilities

are obligations6. statement presentation and

disclosure - components of financial statements are properly combined, separated, described and disclosed

5. rights and obligations - assets are rights of the entity and liabilities

are obligations6. statement presentation and

disclosure - components of financial statements are properly combined, separated, described and disclosed

5 - 55Copyright 2003 Pearson Education Canada Inc.

}

financial statements

financialstatement

cycles

managementassertions

generalaudit

objectives

thecycle

approach

Audit evidence must be

gathered to support/refute management assertions.

specificaudit

objectives

5 - 56Copyright 2003 Pearson Education Canada Inc.

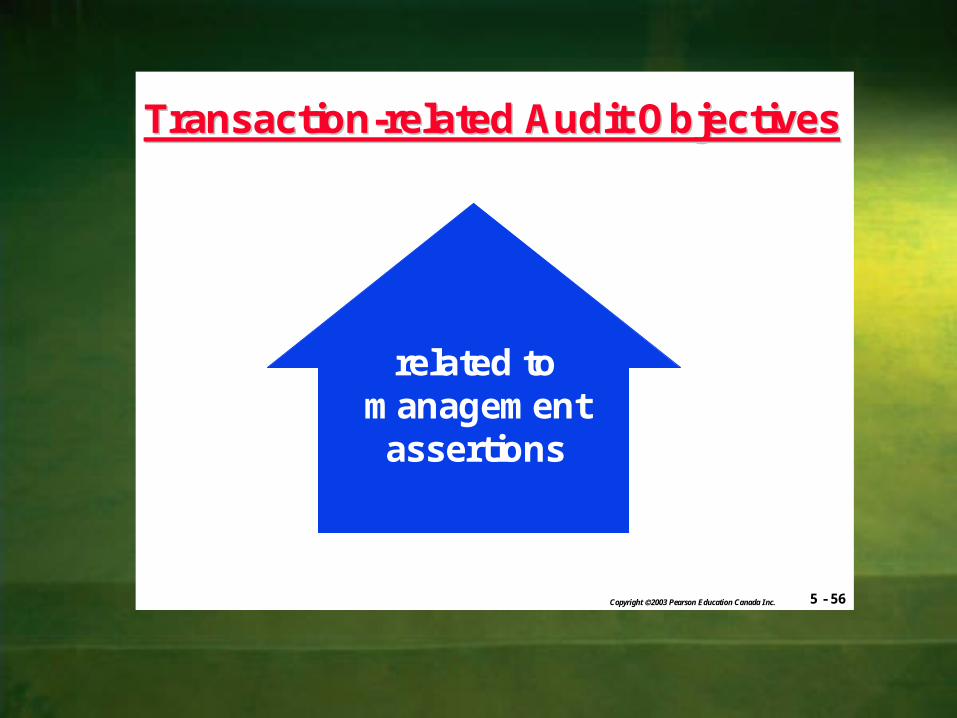

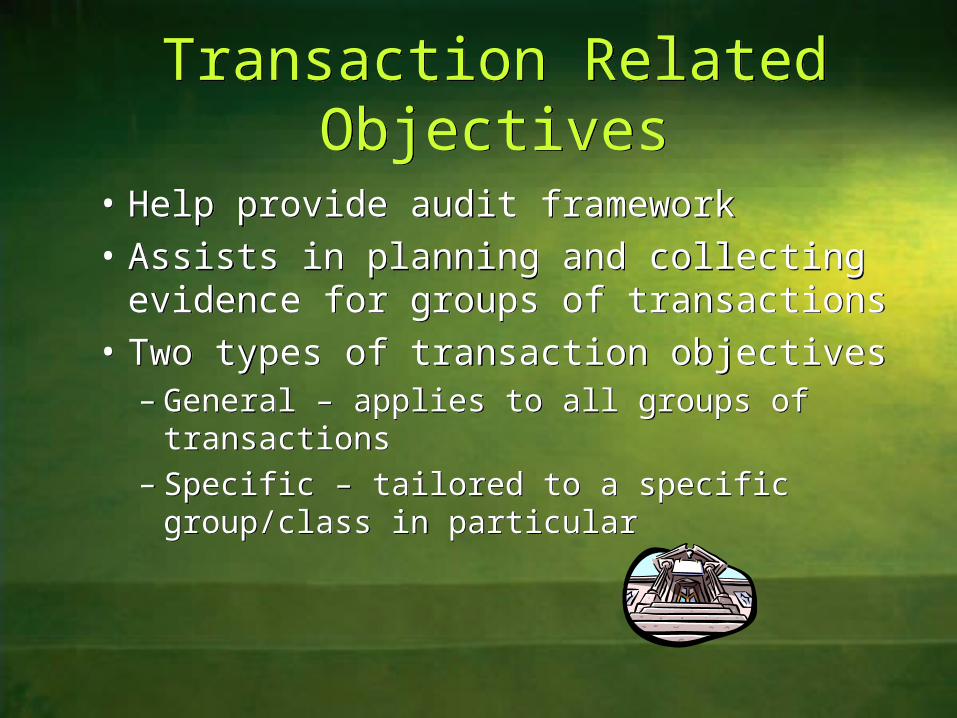

TransactionTransaction--related Audit Objectivesrelated Audit Objectives

related tomanagement

assertions

Transaction Related ObjectivesTransaction Related Objectives

• Help provide audit framework

• Assists in planning and collecting evidence for groups of transactions

• Two types of transaction objectives – General – applies to all groups of transactions– Specific – tailored to a specific group/class in

particular

• Help provide audit framework

• Assists in planning and collecting evidence for groups of transactions

• Two types of transaction objectives – General – applies to all groups of transactions– Specific – tailored to a specific group/class in

particular

5 - 57Copyright 2003 Pearson Education Canada Inc.

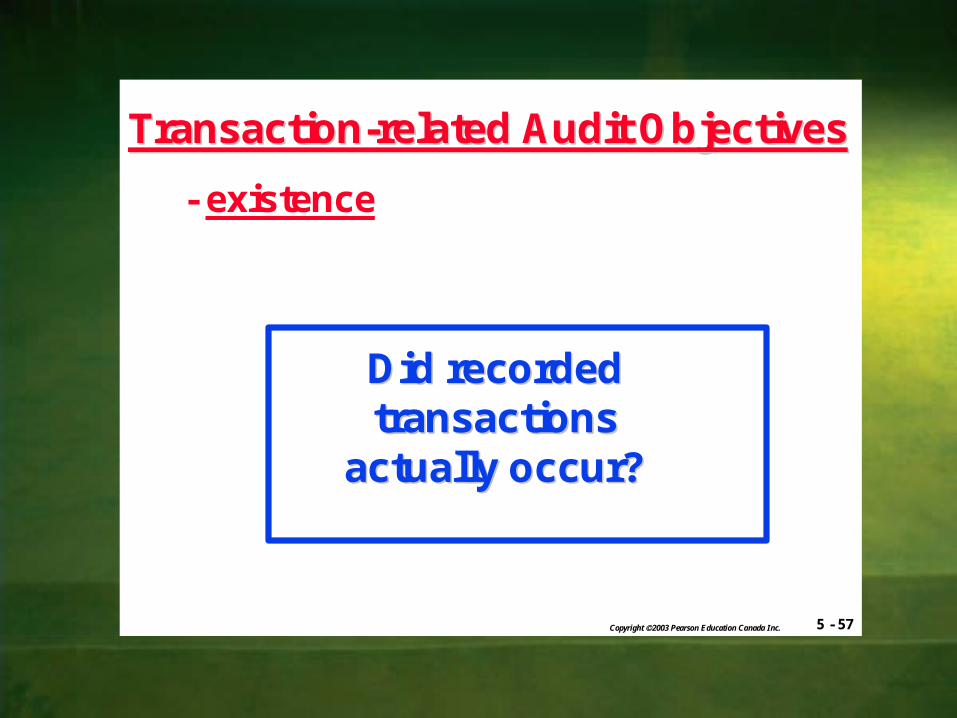

TransactionTransaction--related Audit Objectivesrelated Audit Objectives

- existence

Did recordedDid recordedtransactionstransactions

actually occur?actually occur?

5 - 58Copyright 2003 Pearson Education Canada Inc.

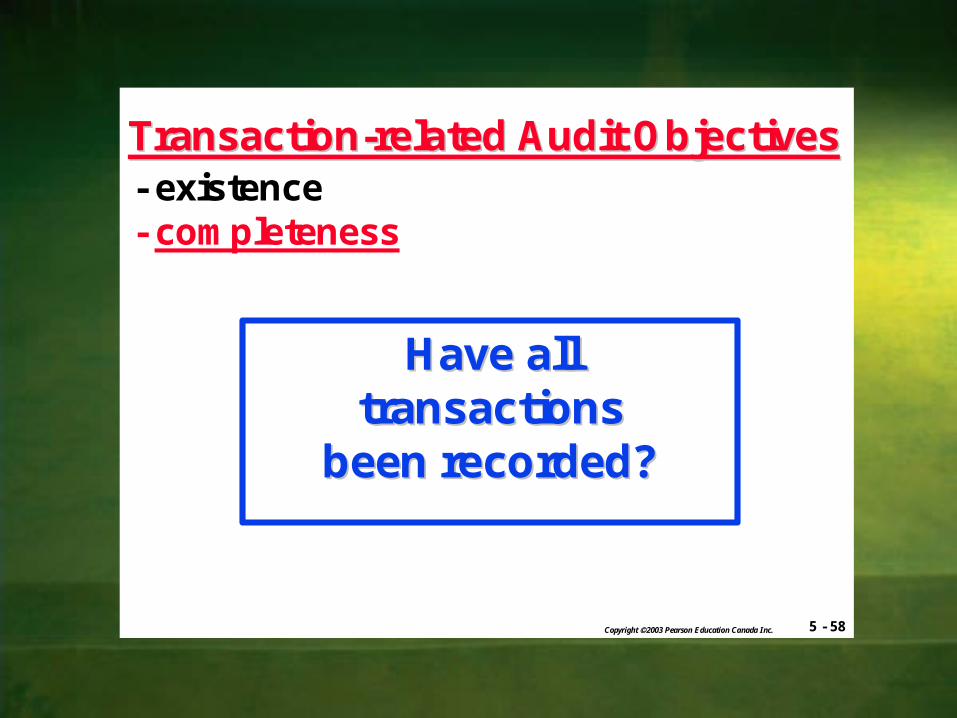

TransactionTransaction--related Audit Objectivesrelated Audit Objectives- existence- completeness

Have allHave alltransactionstransactions

been recorded?been recorded?

5 - 59Copyright 2003 Pearson Education Canada Inc.

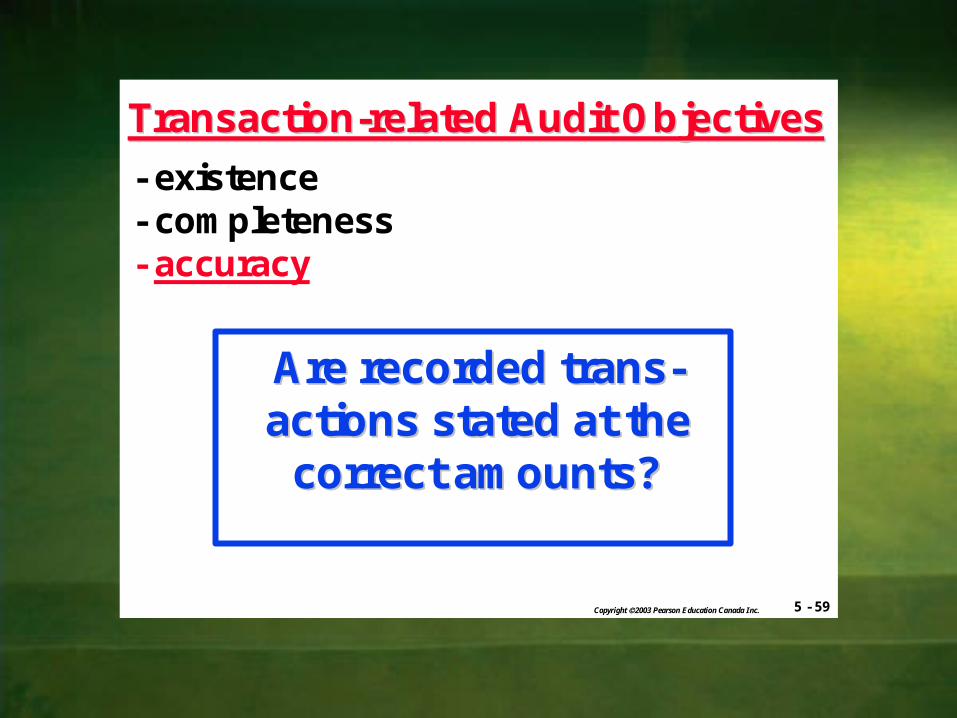

TransactionTransaction--related Audit Objectivesrelated Audit Objectives

- existence- completeness- accuracy

Are recorded transAre recorded trans--actions stated at theactions stated at the

correct amounts?correct amounts?

5 - 60Copyright 2003 Pearson Education Canada Inc.

TransactionTransaction--related Audit Objectivesrelated Audit Objectives- existence- completeness- accuracy- classification

Are transactionsAre transactionsproperlyproperly

classified?classified?

5 - 61Copyright 2003 Pearson Education Canada Inc.

TransactionTransaction--related Audit Objectivesrelated Audit Objectives- existence- completeness- accuracy- classification- timing

Are transactionsAre transactionsrecorded on therecorded on thecorrect dates?correct dates?

5 - 62Copyright 2003 Pearson Education Canada Inc.

TransactionTransaction--related Audit Objectivesrelated Audit Objectives- existence- completeness- accuracy- classification- timing- posting and

summarization

Are recorded Are recorded transactionstransactions

properly included properly included in the accountingin the accounting

records and records and correctly correctly

summarized?summarized?

5 - 63Copyright 2003 Pearson Education Canada Inc.

BalanceBalance--related Audit Objectivesrelated Audit Objectives

alsorelated to

managementassertions

• Instead of examining groups/classes (i.e. sales transactions etc.) of transactions now looking at balances (i.e. ending balances on the balance sheet and income statement)

• Instead of examining groups/classes (i.e. sales transactions etc.) of transactions now looking at balances (i.e. ending balances on the balance sheet and income statement)

Balance Related ObjectivesBalance Related Objectives

5 - 64Copyright 2003 Pearson Education Canada Inc.

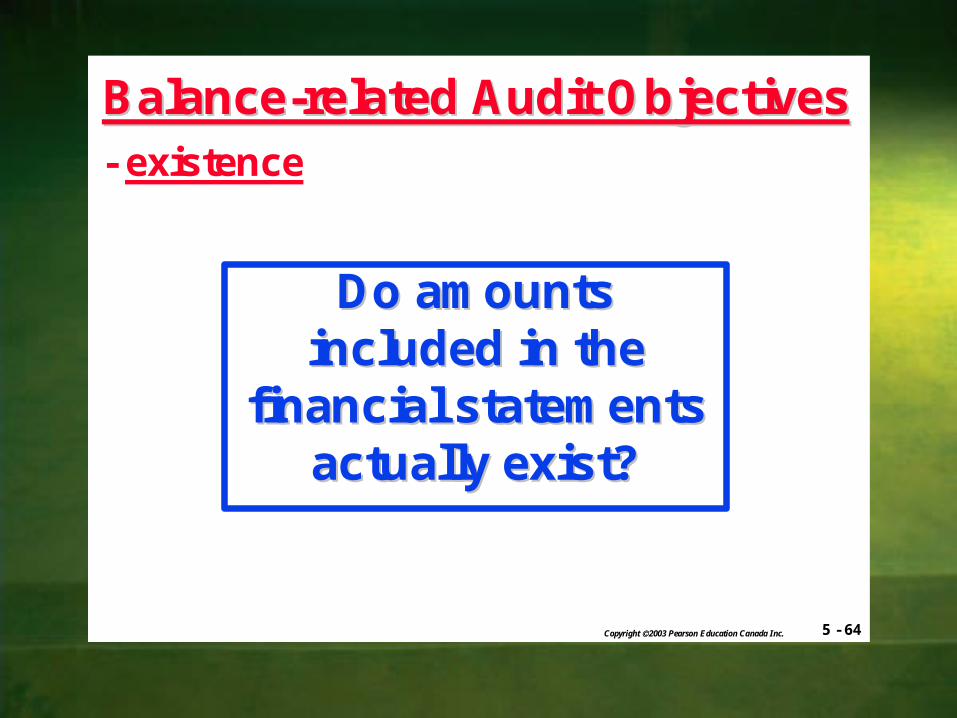

BalanceBalance--related Audit Objectivesrelated Audit Objectives- existence

Do amountsDo amountsincluded in theincluded in the

financial statementsfinancial statementsactually exist?actually exist?

5 - 65Copyright 2003 Pearson Education Canada Inc.

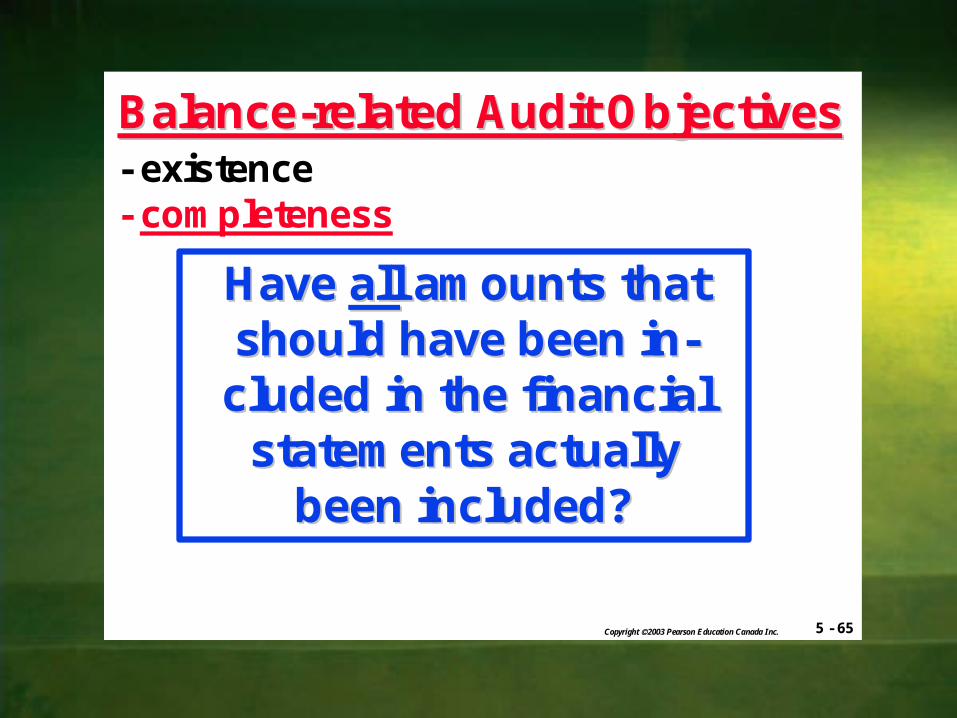

BalanceBalance--related Audit Objectivesrelated Audit Objectives- existence- completeness

Have Have allall amounts thatamounts thatshould have been inshould have been in--

cludedcluded in the financialin the financialstatements actuallystatements actually

been included?been included?

5 - 66Copyright 2003 Pearson Education Canada Inc.

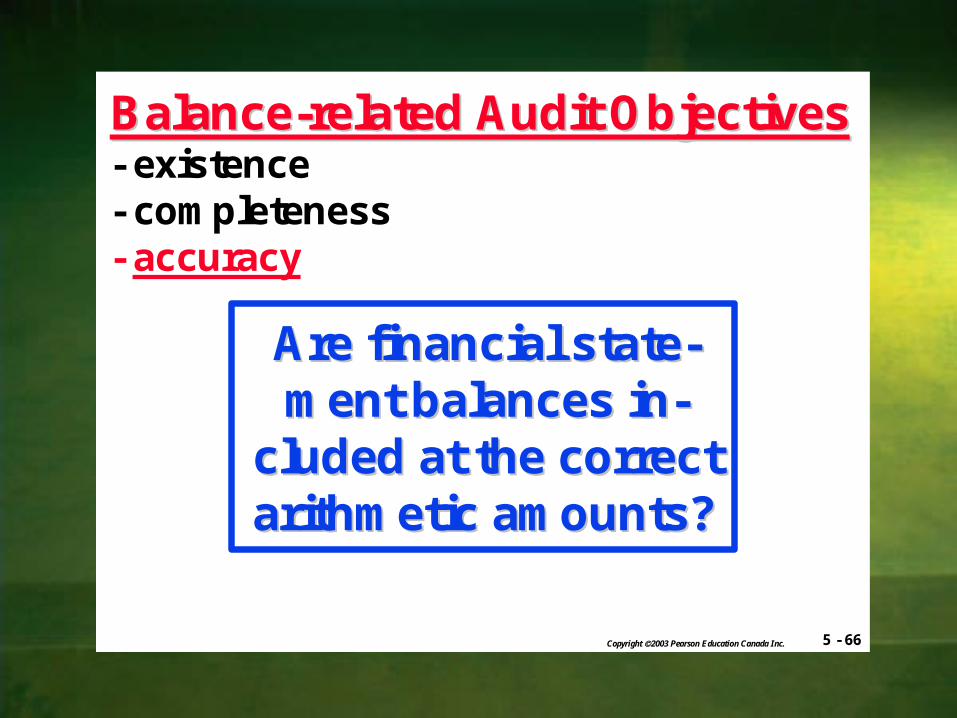

Are financial stateAre financial state--mentment balances inbalances in--

cludedcluded at the correctat the correctarithmetic amounts?arithmetic amounts?

BalanceBalance--related Audit Objectivesrelated Audit Objectives- existence- completeness- accuracy

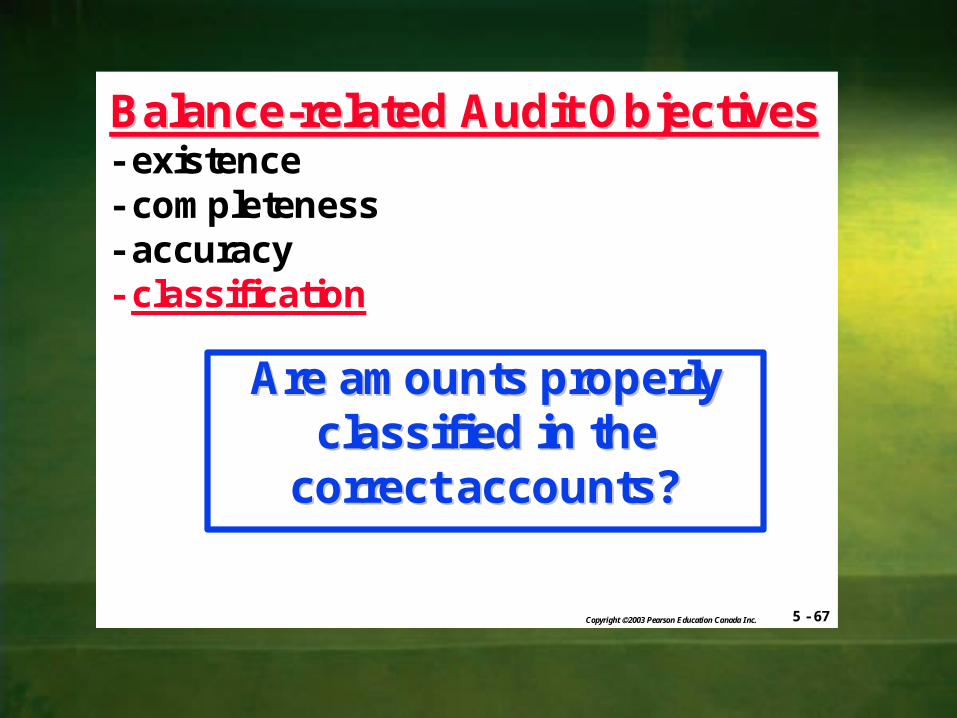

5 - 67Copyright 2003 Pearson Education Canada Inc.

Are amounts properlyAre amounts properlyclassified in theclassified in the

correct accounts?correct accounts?

BalanceBalance--related Audit Objectivesrelated Audit Objectives- existence- completeness- accuracy- classification

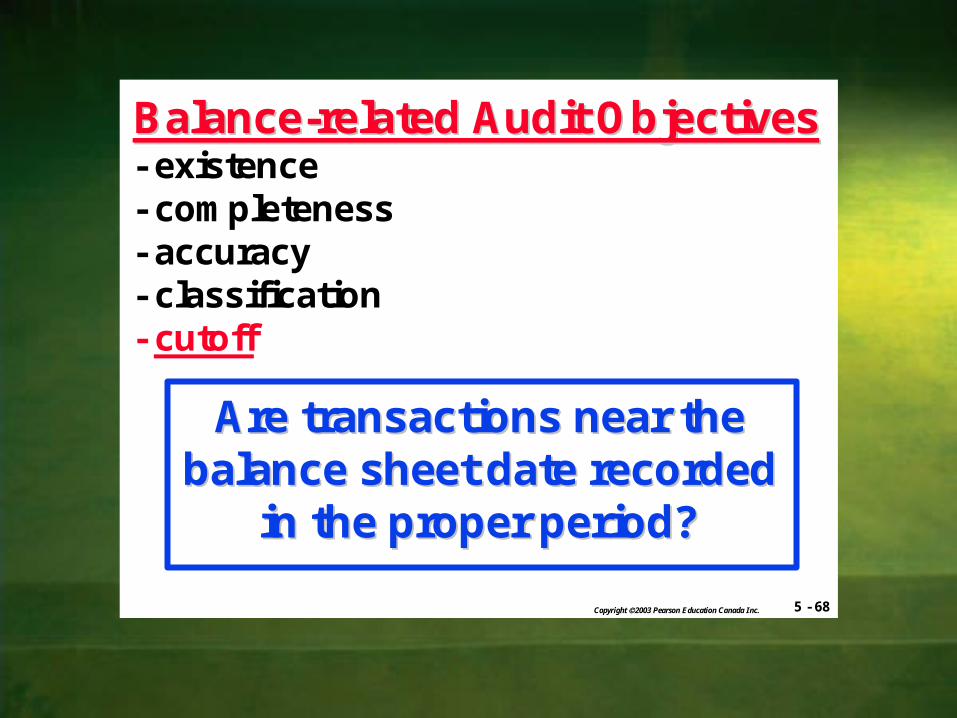

5 - 68Copyright 2003 Pearson Education Canada Inc.

Are transactions near theAre transactions near thebalance sheet date recordedbalance sheet date recorded

in the proper period?in the proper period?

BalanceBalance--related Audit Objectivesrelated Audit Objectives- existence- completeness- accuracy- classification- cutoff

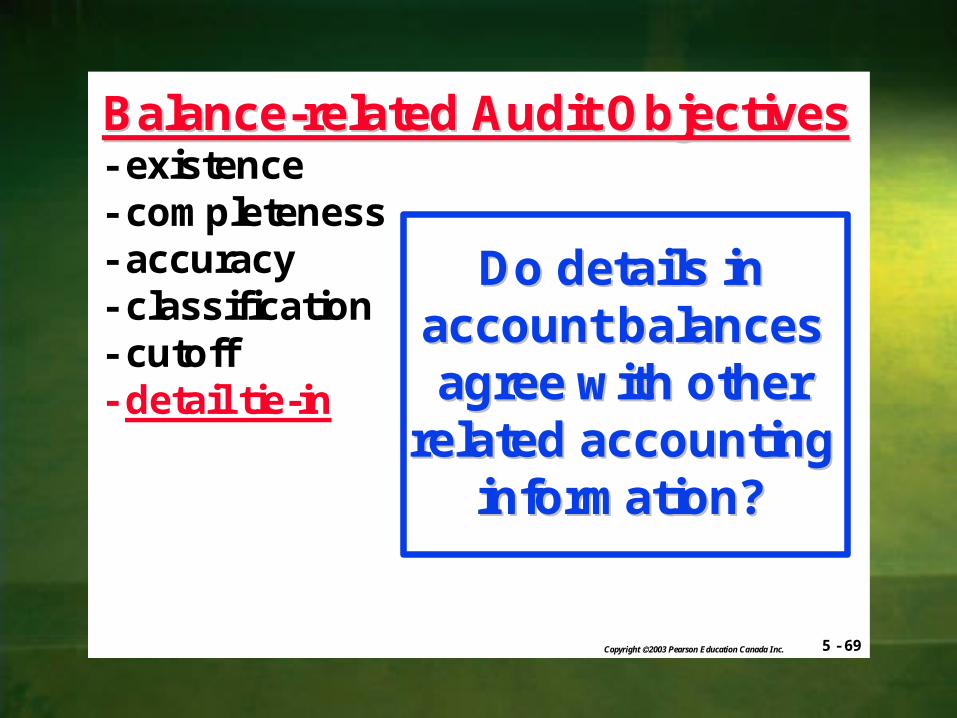

5 - 69Copyright 2003 Pearson Education Canada Inc.

Do details in Do details in account balances account balances agree with other agree with other

related accounting related accounting information?information?

BalanceBalance--related Audit Objectivesrelated Audit Objectives- existence- completeness- accuracy- classification- cutoff- detail tie-in

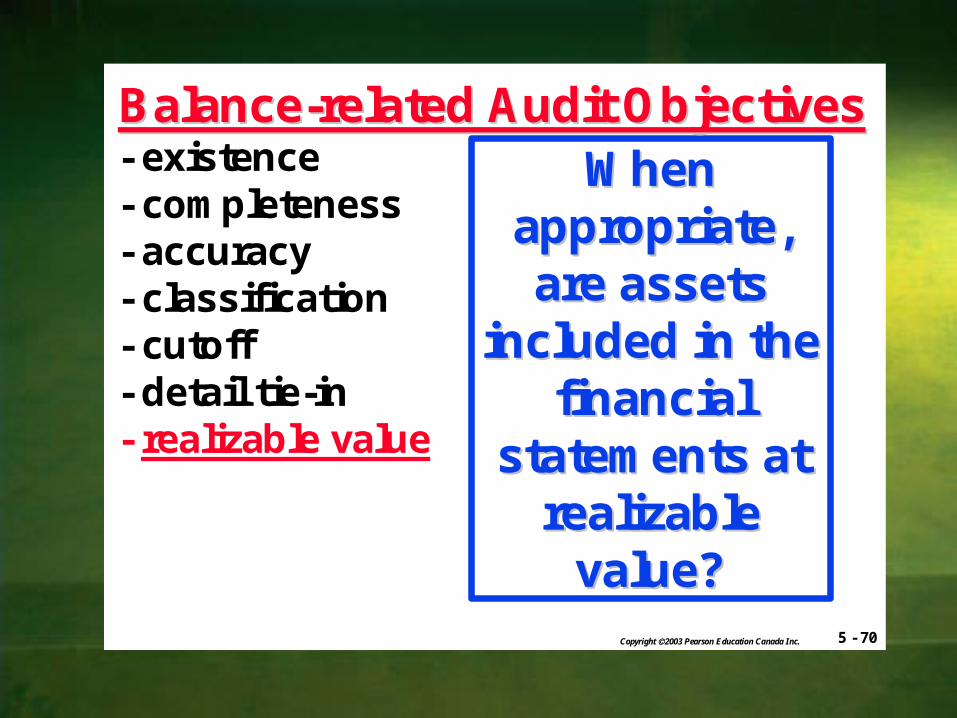

5 - 70Copyright 2003 Pearson Education Canada Inc.

When When appropriate, appropriate, are assets are assets

included in the included in the financial financial

statements at statements at realizable realizable

value?value?

BalanceBalance--related Audit Objectivesrelated Audit Objectives- existence- completeness- accuracy- classification- cutoff- detail tie-in- realizable value

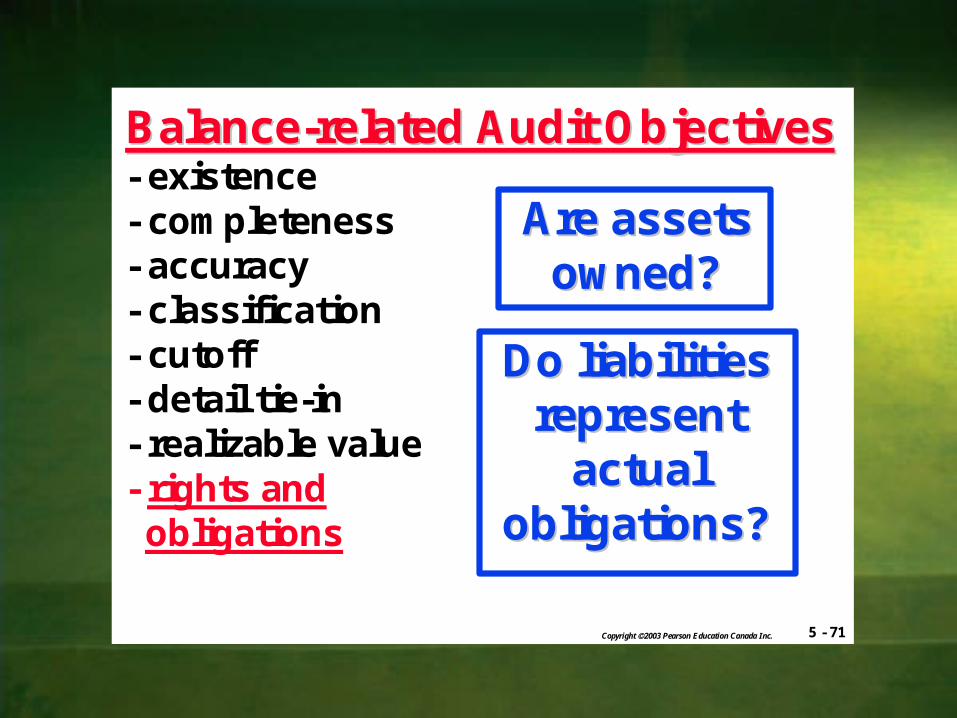

5 - 71Copyright 2003 Pearson Education Canada Inc.

BalanceBalance--related Audit Objectivesrelated Audit Objectives- existence- completeness- accuracy- classification- cutoff- detail tie-in- realizable value- rights and

obligations

Do liabilities Do liabilities represent represent

actual actual obligations?obligations?

Are assets Are assets owned?owned?

5 - 72Copyright 2003 Pearson Education Canada Inc.

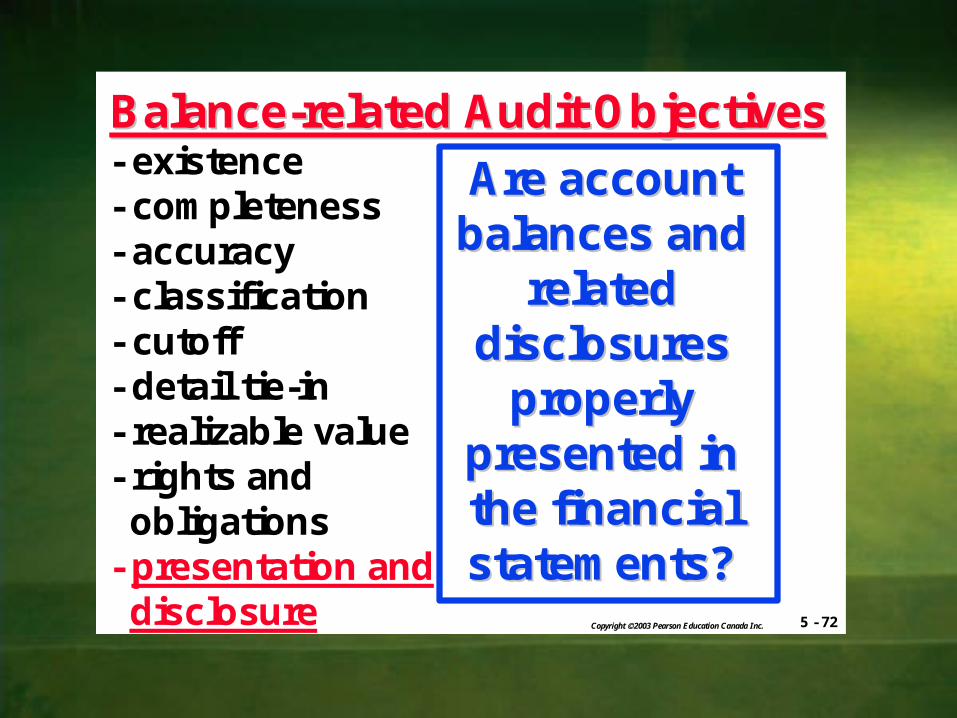

BalanceBalance--related Audit Objectivesrelated Audit Objectives- existence- completeness- accuracy- classification- cutoff- detail tie-in- realizable value- rights and

obligations- presentation and

disclosure

Are account Are account balances and balances and

related related disclosures disclosures

properly properly presented in presented in the financial the financial statements?statements?

5 - 74Copyright 2003 Pearson Education Canada Inc.

financial statements

financialstatement

cycles

managementassertions

generalaudit

objectivesspecificaudit

objectives

thecycle

approach

obtain sufficient

appropriate audit evidence

5 - 75Copyright 2003 Pearson Education Canada Inc.

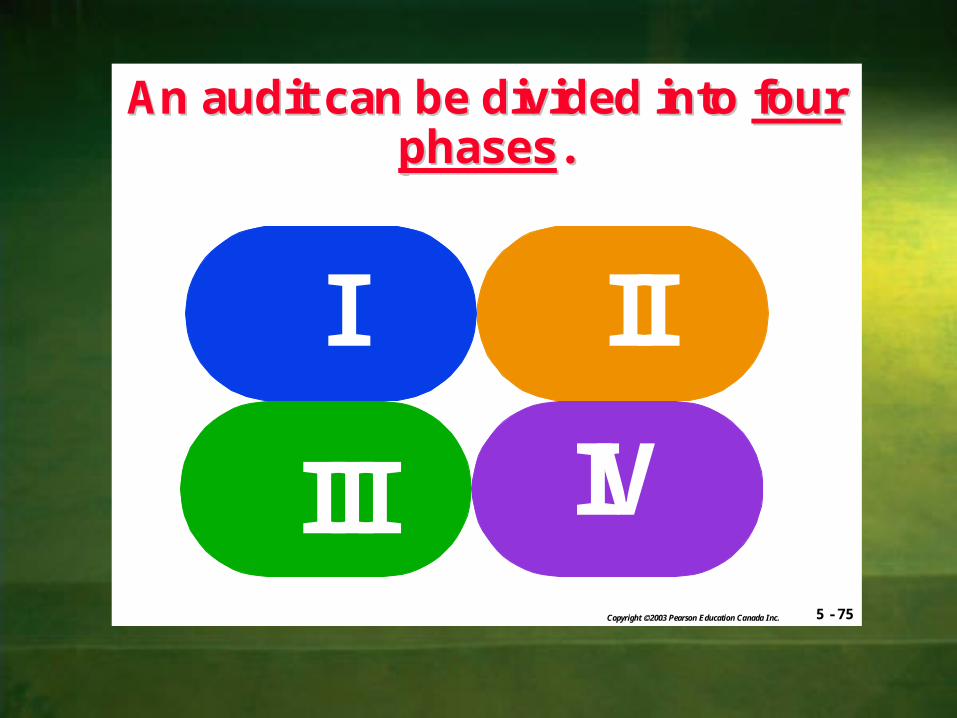

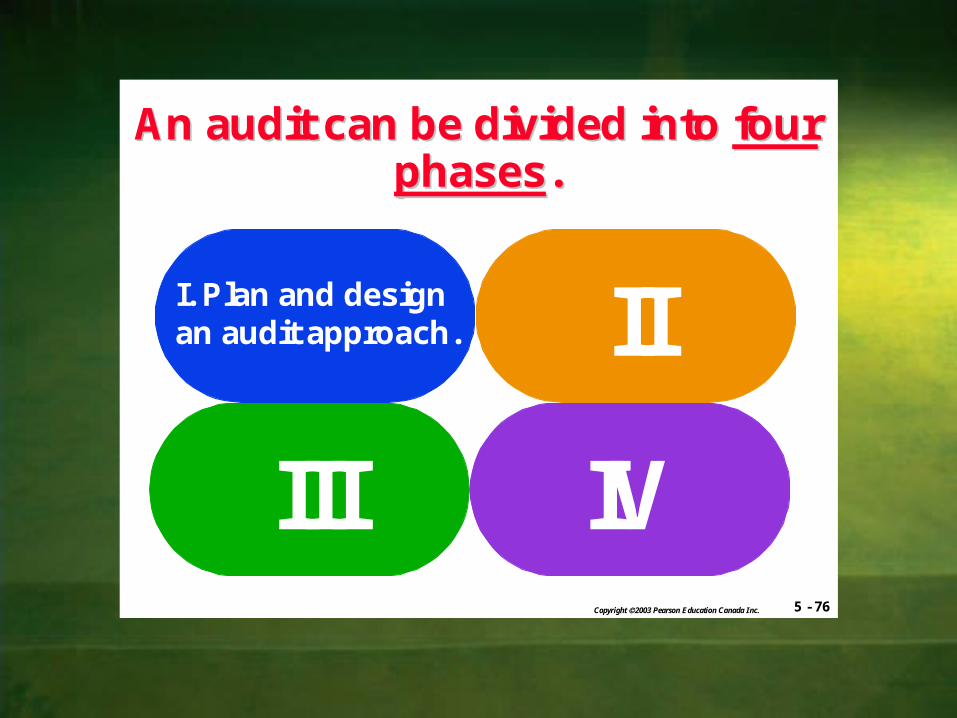

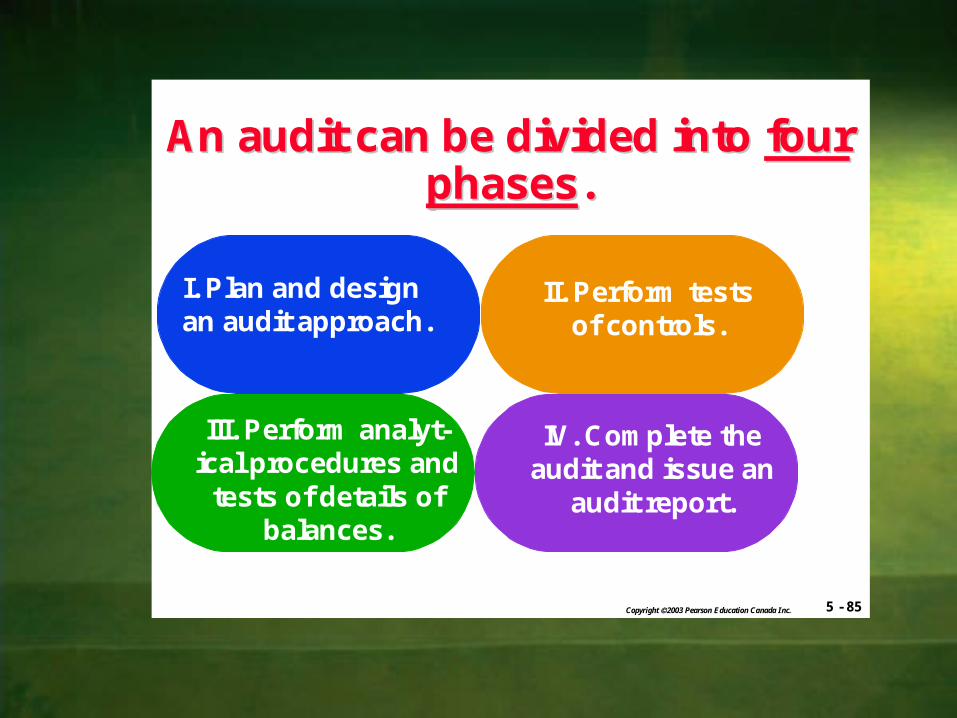

An audit can be divided into An audit can be divided into four four phasesphases..

I II

III IV

5 - 76Copyright 2003 Pearson Education Canada Inc.

An audit can be divided into An audit can be divided into four four phasesphases..

II

III IV

I. Plan and designan audit approach.

5 - 79Copyright 2003 Pearson Education Canada Inc.

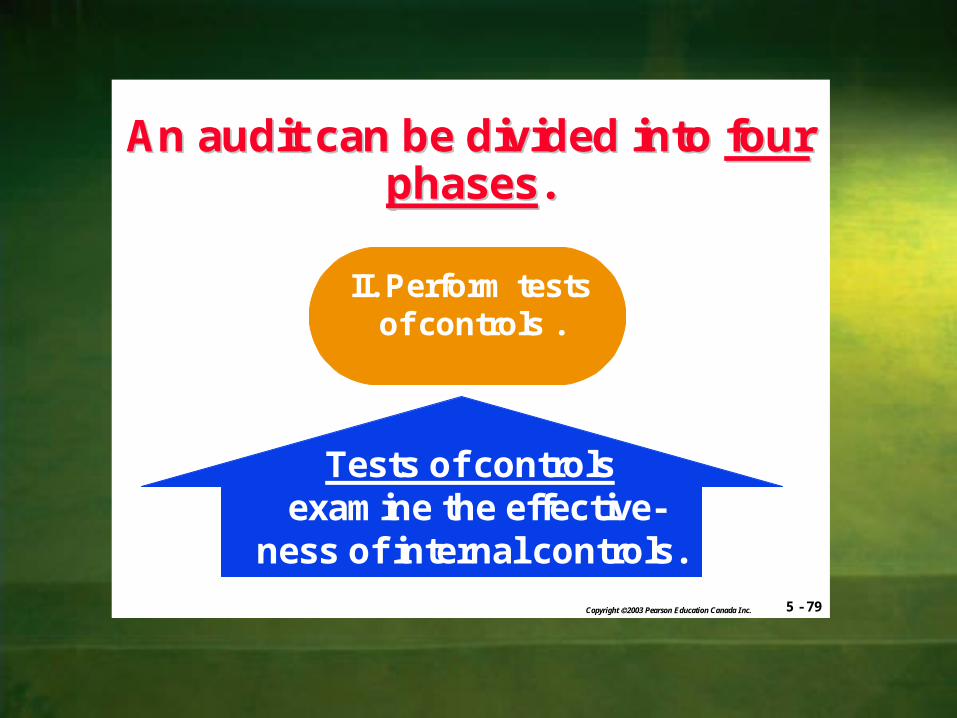

An audit can be divided into An audit can be divided into four four phasesphases..

II. Perform testsof controls .

Tests of controlsexamine the effective-

ness of internal controls.

5 - 82Copyright 2003 Pearson Education Canada Inc.

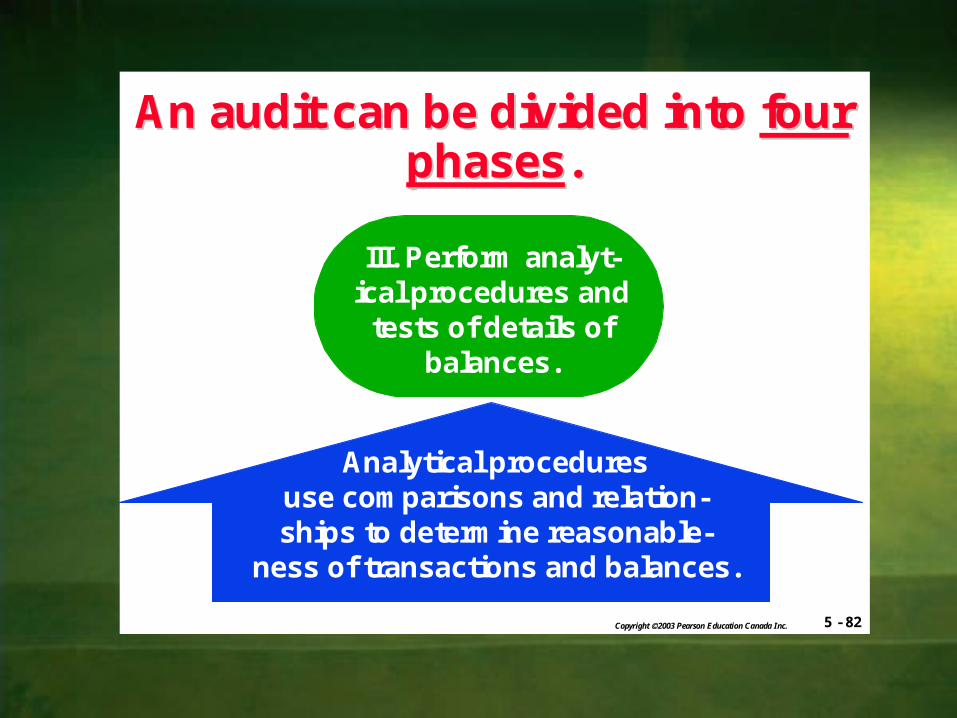

An audit can be divided into An audit can be divided into four four phasesphases..

III. Perform analyt-ical procedures and

tests of details ofbalances.

Analytical proceduresuse comparisons and relation-ships to determine reasonable-

ness of transactions and balances.

5 - 84Copyright 2003 Pearson Education Canada Inc.

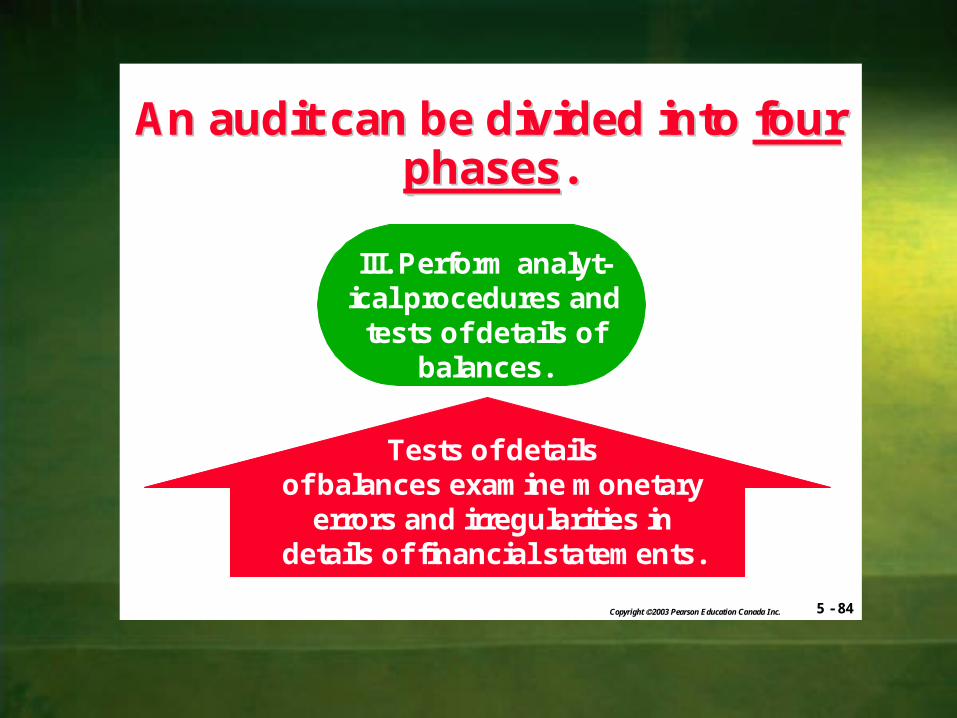

An audit can be divided into An audit can be divided into four four phasesphases..

III. Perform analyt-ical procedures and

tests of details ofbalances.

Tests of detailsof balances examine monetary

errors and irregularities indetails of financial statements.

5 - 85Copyright 2003 Pearson Education Canada Inc.

An audit can be divided into An audit can be divided into four four phasesphases..

I. Plan and designan audit approach.

II. Perform testsof controls.

III. Perform analyt-ical procedures and

tests of details ofbalances.

IV. Complete theaudit and issue an

audit report.