Attention Discrimination in Retail Lending

30

Attention Discrimination in Retail Lending January 7, 2021 Bo Huang, Jiacui Li, Tse-Chun Lin, Mingzhu Tai, Yiyuan Zhou 1 Abstract Using proprietary retail loan screening data, we document that loan officers exhibit “attention discrimina- tion”. That is, discrimination happens at the earlier stage of information acquisition: loan officers exert less effort reviewing ex-ante unfavorable applicants and reject them at a higher rate. Further, when loan officers face stronger attention constraints when burdened by more applications, the degree of discrimination increases. This magnitude is significant: approval rate for the ex-ante disadvantaged applicants drops from 19.0% to 7.5% when officers are in the top decile of busyness. Overall, the results show that attention con- straints magnify discrimination. This has important implications on the strategy to reduce discrimination of decision makers. Keyword: attention allocation, attention constraint, statistical discrimination JEL Classification: D83, D91, G21 1 Introduction Since the seminal works of Phelps (1972) and Arrow (1972), it has been a crucial concern that decision makers may engage in statistical discrimination – that is, they rely on group attributes such as ethnicity or gender to make decisions when individual-level information is not available. This concern has been widely voiced in many contexts including decision making by judges in trials, recruitment by employers, voting in elections, college admission decisions, and so on. 2 In statistical discrimination, decision makers exhibit discrimination 1 Huang ([email protected]): School of Finance at Remin University of China. Li ([email protected]): David Eccles School of Business at University of Utah. Lin, Tai, and Zhou ([email protected], [email protected], [email protected]): School of Economics and Finance at University of Hong Kong. 2 Time Magazine (2002) cites a study that shows recruiters spend an average of six seconds on each resume. The Chronicle of Higher Education (2017) report that admission officers at the University of Pennsylvania spend four minutes on each initial read of each college application. 1

Transcript of Attention Discrimination in Retail Lending

Attention Discrimination in Retail Lending

January 7, 2021

Bo Huang, Jiacui Li, Tse-Chun Lin, Mingzhu Tai, Yiyuan Zhou1

Abstract

Using proprietary retail loan screening data, we document that loan officers exhibit “attention discrimina-

tion”. That is, discrimination happens at the earlier stage of information acquisition: loan officers exert

less effort reviewing ex-ante unfavorable applicants and reject them at a higher rate. Further, when loan

officers face stronger attention constraints when burdened by more applications, the degree of discrimination

increases. This magnitude is significant: approval rate for the ex-ante disadvantaged applicants drops from

19.0% to 7.5% when officers are in the top decile of busyness. Overall, the results show that attention con-

straints magnify discrimination. This has important implications on the strategy to reduce discrimination

of decision makers.

Keyword: attention allocation, attention constraint, statistical discrimination

JEL Classification: D83, D91, G21

1 Introduction

Since the seminal works of Phelps (1972) and Arrow (1972), it has been a crucial concern that decision makers

may engage in statistical discrimination – that is, they rely on group attributes such as ethnicity or gender

to make decisions when individual-level information is not available. This concern has been widely voiced in

many contexts including decision making by judges in trials, recruitment by employers, voting in elections,

college admission decisions, and so on.2 In statistical discrimination, decision makers exhibit discrimination

1Huang ([email protected]): School of Finance at Remin University of China. Li ([email protected]): DavidEccles School of Business at University of Utah. Lin, Tai, and Zhou ([email protected], [email protected], [email protected]):School of Economics and Finance at University of Hong Kong.

2Time Magazine (2002) cites a study that shows recruiters spend an average of six seconds on each resume. The Chronicleof Higher Education (2017) report that admission officers at the University of Pennsylvania spend four minutes on each initialread of each college application.

1

2

at the decision stage. However, when under attention constraints, they may also discriminate early on in

the information acquisition stage and pay less attention to the ex-ante disadvantaged groups. In a “cherry-

picking” situation where the default action without sufficient information is to reject, this discriminatory

attention allocation decision will magnify the role of pre-existing priors or preferences. (Bartos, Bauer,

Chytilova, and Matejka, 2016) call this mechanism “attention discrimination”.

The attention discrimination mechanism can be easily understood through an example. Consider the case

when referees are time-constrained in reviewing economics papers. When given infinite time, there are many

things referees can do to improve her judgement on the submissions such as scrutinizing each table, doing

thorough literature searches, and performing replications (which happens in some NBER discussions). That

is clearly unrealistic as referees face time constraints – they need to attend to their own work and life as well.

When faced with stronger time-constraints, referees may use their priors to guide how much effort to put in

each review. Such priors can include whether the referee personally finds the claims plausible, whether the

submission is written by well-established researchers and has been presented in notable conferences, etc. If a

paper scores negatively on all of these fronts – that is, it comes from an ex-ante disadvantaged group – then

the referee may decide to spend less effort scrutinizing the paper and hand out a quick rejection. Further,

the more time constrained is the reviewer, the more likely she will engage in such attention discrimination.

Even though attention discrimination is a natural phenomenon that may be reasonably expected to occur

in many decision making contexts, it is difficult to study empirically in real world application decision

processes.3 As noted by Gabaix (2019), “measuring attention is ... a hard task – we still have only a limited

number of papers that measure attention in field settings.” Further, to test the role of inattention, one also

needs plausibly exogenous shocks to attention constraints which is often lacking in field data. This paper

fills this gap by documenting attention discrimination using a large, detailed retail loan screening data set

from one of the largest Chinese banks. To the best of our knowledge, we are the first to document attention

discrimination using large-scale field data.

Our data contains the complete proprietary records of 92 officers deciding whether to approve approximately

146,000 retail loan applications over the span of a year (April 2013 to April 2014). We observe the screening

process in detail: for each application, we can trace which officer is it assigned to, what time is it assigned,

whether loan officers have conducted further due diligence, and when is the decision made. Loan officers do

face time constraints: the median review time on each application is only 18 minutes which includes both

reviewing and sometimes making further phone calls for due diligence. Because we observe all application

assignment and decision times, we also can measure how busy is each officer at a given time as a proxy for

the strength of attention constraints.

In our empirical exercise, we start by documenting the connection between attention allocation and approval

rate. Applications that receiver less attention – measured using less time spent in reviews or shorter officer-

written comments – are more likely to be rejected. The median time spent on eventually approved application

is 28 minutes but only 13 minutes – less than half – on rejected applications. 27% of rejections are reviewed

for less than 5 minutes before being rejected. Similarly, officers wrote a median of 57 Chinese characters of

comments on approved applications while only 6 characters on rejected applications.

3The seminal paper on attention discrimination, Bartos et al. (2016), ran field experiments through email advertisements inrental and labor markets.

3

Second, we find evidence that officers use simple signals to allocate their attention. In our data, some ap-

plicants are able to obtain official certificates for their income, employment, housing property, etc. Those

who can obtain such certificates often work for the public sector or larger companies, have more stable

employment, and have better credit history. Those who cannot obtain these certificates are ex-ante disad-

vantaged. Loan officers appear to make use of these in allocating attention. While many applicants with

such certificates are also not approved, they are usually rejected after longer review time and further due

diligence efforts by the officers. In contrast, the disadvantaged group without certificates are more likely to

be rejected after only a few minutes and without further due diligence.

To examine whether inattention exacerbates discrimination, we exploit variation in loan officer busyness,

measured by the number of decisions made by each officer on each day. We argue that officers are more

inattentive on busier days. Because an officer can endogenously choose to work faster or slower, her actual

busyness is endogenous, we also instrument this busyness measure using the number of applications assigned

to the officer on that day and the previous three days. As most officers strive to make decisions on most

assigned applications within a few days, this turns out to be a strong instrument and a good predictor of

actual busyness. Because the assignments are made by a central dispatcher algorithm that officers have no

control over, this is an arguably exogenous source of variation in busyness.

As predicted by the attention discrimination mechanism, when loan officers are busier (more inattentive),

they discriminate more against the disadvantaged group with fewer certificates. That is, those applications

are rejected with higher probability while the advantaged group is not effected (or even slightly positively

affected). This finding holds when we sort on within officer busyness and thus is not driven by officer-

specific preferences. The result is also robust to different definitions of ex-ante disadvantage and different

instruments for busyness. The degree of attention-based discrimination is economically significant. If an ex-

ante disadvantaged application happens to be decided upon when an officer is in the top decile of busyness,

the approval rate is only 7.5% as compared to 19.0% when in the bottom decile of busyness. That is, the

approval rate declines by more than half.

One may worry that our results are driven by endogenous changes in application quality on busy versus non-

busy days. Specifically, this alternative explanation requires that the true application quality gap between

the advantaged and disadvantaged groups increases when officers are busier. We alleviate this concern in two

steps. First, since we observe almost all of the application information, we can verify that all credit-relevant

application observables are balanced across busy versus non-busy periods. We also control for all relevant

observables in all our results. However, there remains the possibility that there are time-varying differences

in unobservables. To help alleviate this concern, we then construct a leave-one-out instrument using the

number of applications from other parts of the country that are assigned to the same loan officer. The idea

is as follows. The loan officers we observe work at the bank headquarter and screen applications from all

across the country. If a large number of applications from area A makes the loan officer busy, it can affect

her decision making on applications from area B. In this case, the quality of loans from area B is independent

to the application volume from area A that drives the busyness of the loan officer (after controlling for the

application volume in the local area). All our results are also robust to using this instrument.

We want to emphasize that attention discrimination behavior of loan officers may be either rational or behav-

ioral. From the rational perspective, attention discrimination can be understood as optimal behavior subject

4

to attention constraints. Because loan officers only approve a small fraction of applications, when busy, their

time is better spent on the learning about applicants from the “good groups” with higher average credit

quality. From the behavioral perspective, Kahneman (2011) argues that people are more likely to engage

in time-saving “System 1” heuristics when under time constraint. However, regardless of the interpretation,

the outcome is the same: inattention exacerbates discrimination.

This paper has two main contributions. First, we show that discrimination can happen early on in the

attention-allocation stage, in addition to the later decision-making stage. Second, our results indicate that

inattention magnifies discrimination. This has important implications for the staffing of decision making

institutions such as courts, the United States Patent and Trademark Office, college admission offices, and

so on. Conventionally, to combat discrimination, these institutions emphasize the use of anti-discrimination

training in order to help decision makers self-reflect and guard against their unconscious biases. However, our

findings indicate that discrimination may be an unavoidable consequence of attention constraints. Therefore,

these decision making institutions can alleviate discrimination simply by not being short-staffed.4

Discrimination in lending (e.g. Bartlett, Morse, Stanton, and Wallace (2019); Fuster, Goldsmith-Pinkham,

Ramadorai, and Walther (2020)) is considered a serious threat to fairness. In response to this, regulators

in the U.S. and around the world created various anti-discrimination legislation to combat discrimination

in financial practices. For example, The Equal Credit Opportunity Act (ECOA) prohibits creditors from

discriminating against credit applicants on the basis of race, color, religion, national origin, sex, marital

status, and age.5

This paper is closely related to the the seminal work of Bartos et al. (2016) that proposed the idea of

discrimination. Using a slightly different theoretical setting, Davies, Van Wesep, and Waters (2019) also

show that biases in decision-making can be magnified by endogenous information acquisition. This paper

is also related to studies on individual decision making behaviors in the credit market. For example, (?)

document that using soft information in lending decisions leads to worse loan quality when loan officers

are busy, and (Gao, Karolyi, and Pacelli, 2018) show that distracted loan officers are deficient in screening,

pricing, and monitoring. In addition, (Liao, Wang, Xiang, Yan, and Yang, 2020) find that individuals only

partially account for important credit information when making lending decisions under time pressure. Our

paper augments these studies by providing both theoretical foundations and empirical evidence for the role

of attention allocation in amplifying discrimination using step-by-step loan screening records.

The paper is organized as follows. Section 2 describes the data and relevant institutional details on the loan

screening process. Section 3 provides evidence that loan officer attention allocation matters for the eventual

decision. Section 4 shows that officers discriminate more when busier, and Section 5 concludes.

2 Data and Institutional Background

In this section, we describe the data and provide background information on the retail loan screening process.

4Many have argued that these institutions are short-staffed. For instance, Frakes and Wasserman (2017) argue that the U.S.patent office is short-staffed and that leads to the granting of invalid patents.

5See https://www.govinfo.gov/content/pkg/USCODE-2011-title15/html/USCODE-2011-title15-chap41-subchapIV.htm formore details.

5

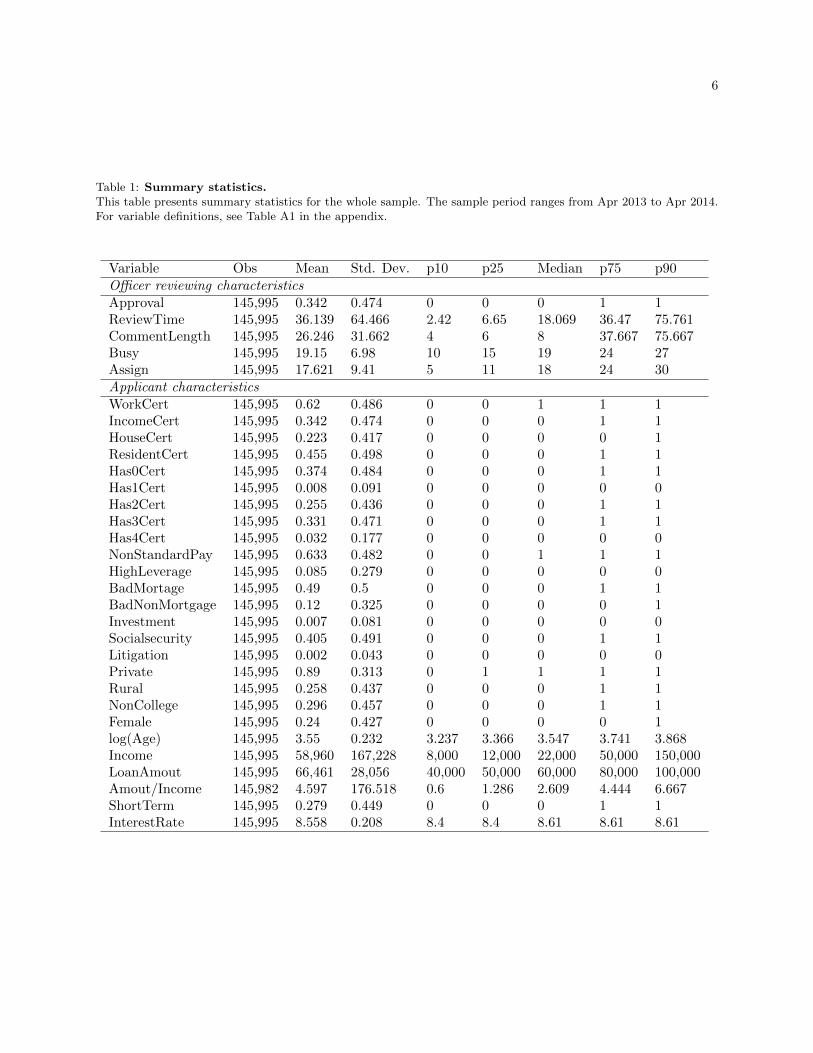

The data we obtained is the complete internal records of loan screening from one of the largest Chinese

banks. The loan products are similar to standard regular retail financing in many markets, such as unsecured

personal term loans or secured home equity loans in the US. The data covers approximately 146,000 retail

loan applications screened by 92 officers over the course of April 2013 to April 2014. The median (mean)

loan amount is 60,000 (66,461) Chinese RMB which converts to 9,787 (10,841) US dollars. This is higher

than the Chinese GDP per capita of 7,073 USD in 2013. The average annual interest rate is 8.56% and

there are two possible maturities, with 28% of applications of 12 month maturity and the rest for 36 month

maturity. 34% of applications are approved and the rest are rejected. Summary statistics are presented in

Table 1.

2.1 The loan application screening process

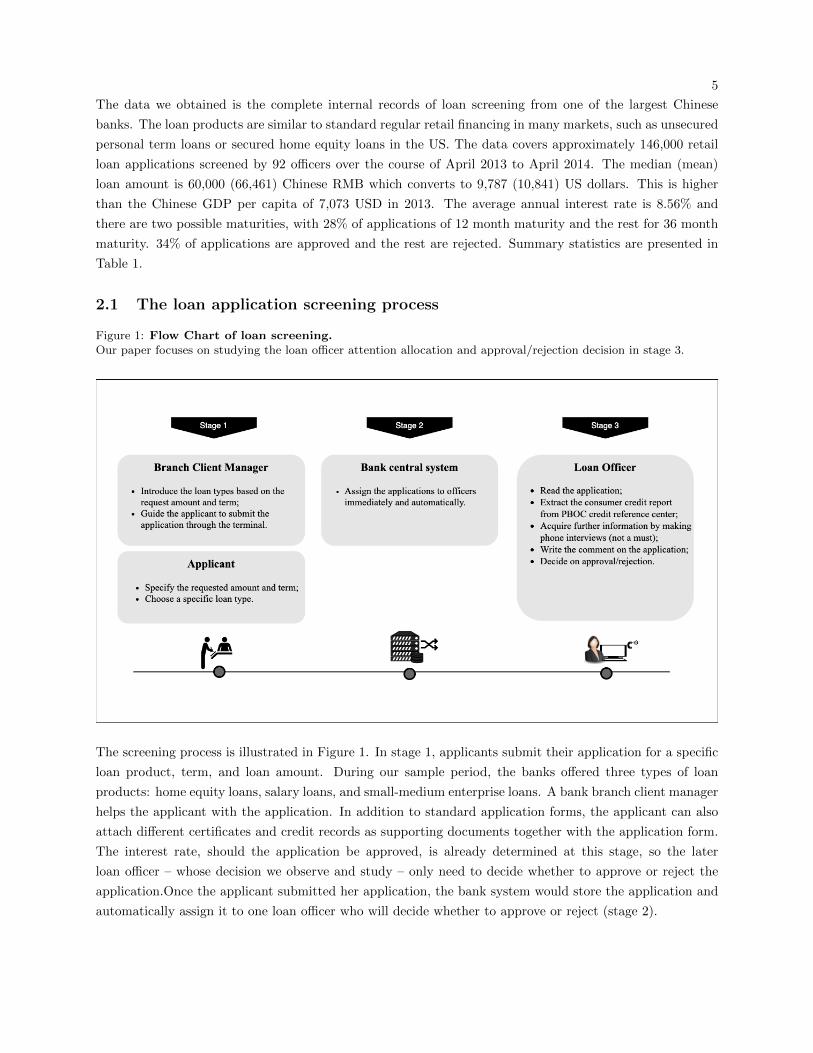

Figure 1: Flow Chart of loan screening.Our paper focuses on studying the loan officer attention allocation and approval/rejection decision in stage 3.

The screening process is illustrated in Figure 1. In stage 1, applicants submit their application for a specific

loan product, term, and loan amount. During our sample period, the banks offered three types of loan

products: home equity loans, salary loans, and small-medium enterprise loans. A bank branch client manager

helps the applicant with the application. In addition to standard application forms, the applicant can also

attach different certificates and credit records as supporting documents together with the application form.

The interest rate, should the application be approved, is already determined at this stage, so the later

loan officer – whose decision we observe and study – only need to decide whether to approve or reject the

application.Once the applicant submitted her application, the bank system would store the application and

automatically assign it to one loan officer who will decide whether to approve or reject (stage 2).

6

Table 1: Summary statistics.This table presents summary statistics for the whole sample. The sample period ranges from Apr 2013 to Apr 2014.For variable definitions, see Table A1 in the appendix.

Variable Obs Mean Std. Dev. p10 p25 Median p75 p90Officer reviewing characteristicsApproval 145,995 0.342 0.474 0 0 0 1 1ReviewTime 145,995 36.139 64.466 2.42 6.65 18.069 36.47 75.761CommentLength 145,995 26.246 31.662 4 6 8 37.667 75.667Busy 145,995 19.15 6.98 10 15 19 24 27Assign 145,995 17.621 9.41 5 11 18 24 30Applicant characteristicsWorkCert 145,995 0.62 0.486 0 0 1 1 1IncomeCert 145,995 0.342 0.474 0 0 0 1 1HouseCert 145,995 0.223 0.417 0 0 0 0 1ResidentCert 145,995 0.455 0.498 0 0 0 1 1Has0Cert 145,995 0.374 0.484 0 0 0 1 1Has1Cert 145,995 0.008 0.091 0 0 0 0 0Has2Cert 145,995 0.255 0.436 0 0 0 1 1Has3Cert 145,995 0.331 0.471 0 0 0 1 1Has4Cert 145,995 0.032 0.177 0 0 0 0 0NonStandardPay 145,995 0.633 0.482 0 0 1 1 1HighLeverage 145,995 0.085 0.279 0 0 0 0 0BadMortage 145,995 0.49 0.5 0 0 0 1 1BadNonMortgage 145,995 0.12 0.325 0 0 0 0 1Investment 145,995 0.007 0.081 0 0 0 0 0Socialsecurity 145,995 0.405 0.491 0 0 0 1 1Litigation 145,995 0.002 0.043 0 0 0 0 0Private 145,995 0.89 0.313 0 1 1 1 1Rural 145,995 0.258 0.437 0 0 0 1 1NonCollege 145,995 0.296 0.457 0 0 0 1 1Female 145,995 0.24 0.427 0 0 0 0 1log(Age) 145,995 3.55 0.232 3.237 3.366 3.547 3.741 3.868Income 145,995 58,960 167,228 8,000 12,000 22,000 50,000 150,000LoanAmout 145,995 66,461 28,056 40,000 50,000 60,000 80,000 100,000Amout/Income 145,982 4.597 176.518 0.6 1.286 2.609 4.444 6.667ShortTerm 145,995 0.279 0.449 0 0 0 1 1InterestRate 145,995 8.558 0.208 8.4 8.4 8.61 8.61 8.61

7

In stage 3, the loan officer can access the submitted application forms, all the supporting materials, and

a consumer credit report from the Chinese central bank’s credit reference center. The loan officers have

a number of levers they can pull to acquire information. They can screen the consumer credit report to

acquire demographic information (such as individual’s identification information, marital status, education

background, and working status), credit payment information (such as the detailed credit history on personal

loans, credit cards, mortgage loans, guarantee and other credit accounts), or seek other public records

obtained from public administration authorities (such as past civil or criminal records of the applicants ).

They can also call the applicant, the applicant’s employer and contacts, or anyone else they deem relevant.

The officers can also write internal comments on each application detailing their information acquisition and

rationale for the decision.

Our data contains detailed records of the application assignment in stage 2 and the loan officer decision in

stage 3, as well as all the submitted application information. Because our data ends in April 2014, vast

majority of approved loans have not yet matured so we do not observe the eventual default rate. Therefore,

we focus our attention on studying the approval/rejection decision of the loan officer. Having access to these

details allows us to peer into the often black box loan screening process.

3 Disadvantaged applications are at higher risk of attention dis-

crimination

We start by demonstrating that lower officer attention tends to lead to rejections. We then note that the

group of applicants without official certificates for their income, property, etc. are ex-ante disadvantaged.

Finally, we show that officers tend to be particularly inattentive to the disadvantaged group, often rejecting

those applications without extensive review or due diligence.

3.1 Attention is necessary for obtaining approval

An important premise of the attention discrimination mechanism is that, if an officer pays less attention to

an applicant, the default outcome is more likely a rejection. The reasoning is simple: the risk of accepting

unscrutinized applications is too high. This can be shown in a quick back-of-envelope exercise. Consider a

random loan application. The average interest rate in our sample is 8.6%. Even if the bank’s cost of capital

is the risk-free rate of 3.25% in our sample period, this means the bank can only make a cost-adjusted

annual return of 5.35% if the applicant does not default. In contrast, if the application defaults, assuming

a 40% recovery rate, the bank stands to loose 60%. Therefore, as long as the expected default rate of all

applications is higher than 3.25%3.25%+60% ≈ 5%, the default loan officer action without sufficient information

acquisition should be rejection.

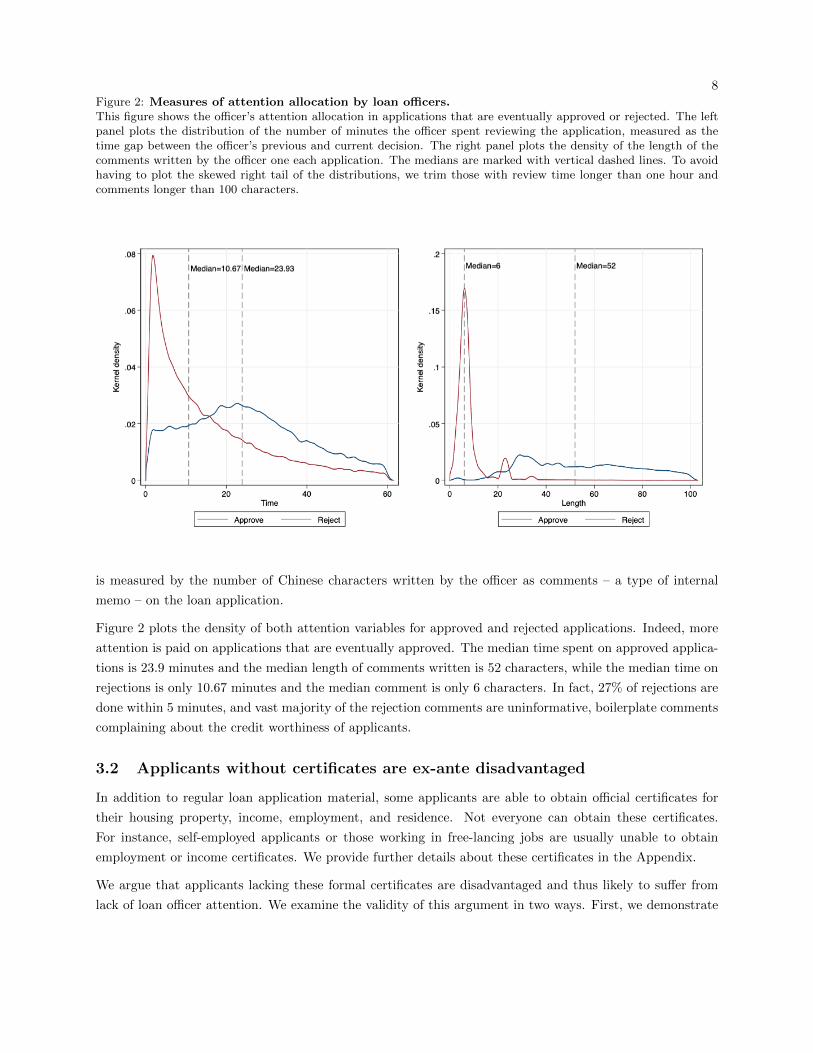

We now examine whether attention appears to be associated with approval by using direct proxies of officer

attention. As noted by the survey paper of Gabaix (2019), it is hard to measure attention in field settings.

Luckily, with the complete administrative records of the internal loan screening process, we can construct

two reasonable proxies: the time spent on each application and the amount of comments written. The

former is measured as the number of minutes elapsed since the previous to the current decision. The latter

8Figure 2: Measures of attention allocation by loan officers.This figure shows the officer’s attention allocation in applications that are eventually approved or rejected. The leftpanel plots the distribution of the number of minutes the officer spent reviewing the application, measured as thetime gap between the officer’s previous and current decision. The right panel plots the density of the length of thecomments written by the officer one each application. The medians are marked with vertical dashed lines. To avoidhaving to plot the skewed right tail of the distributions, we trim those with review time longer than one hour andcomments longer than 100 characters.

is measured by the number of Chinese characters written by the officer as comments – a type of internal

memo – on the loan application.

Figure 2 plots the density of both attention variables for approved and rejected applications. Indeed, more

attention is paid on applications that are eventually approved. The median time spent on approved applica-

tions is 23.9 minutes and the median length of comments written is 52 characters, while the median time on

rejections is only 10.67 minutes and the median comment is only 6 characters. In fact, 27% of rejections are

done within 5 minutes, and vast majority of the rejection comments are uninformative, boilerplate comments

complaining about the credit worthiness of applicants.

3.2 Applicants without certificates are ex-ante disadvantaged

In addition to regular loan application material, some applicants are able to obtain official certificates for

their housing property, income, employment, and residence. Not everyone can obtain these certificates.

For instance, self-employed applicants or those working in free-lancing jobs are usually unable to obtain

employment or income certificates. We provide further details about these certificates in the Appendix.

We argue that applicants lacking these formal certificates are disadvantaged and thus likely to suffer from

lack of loan officer attention. We examine the validity of this argument in two ways. First, we demonstrate

9

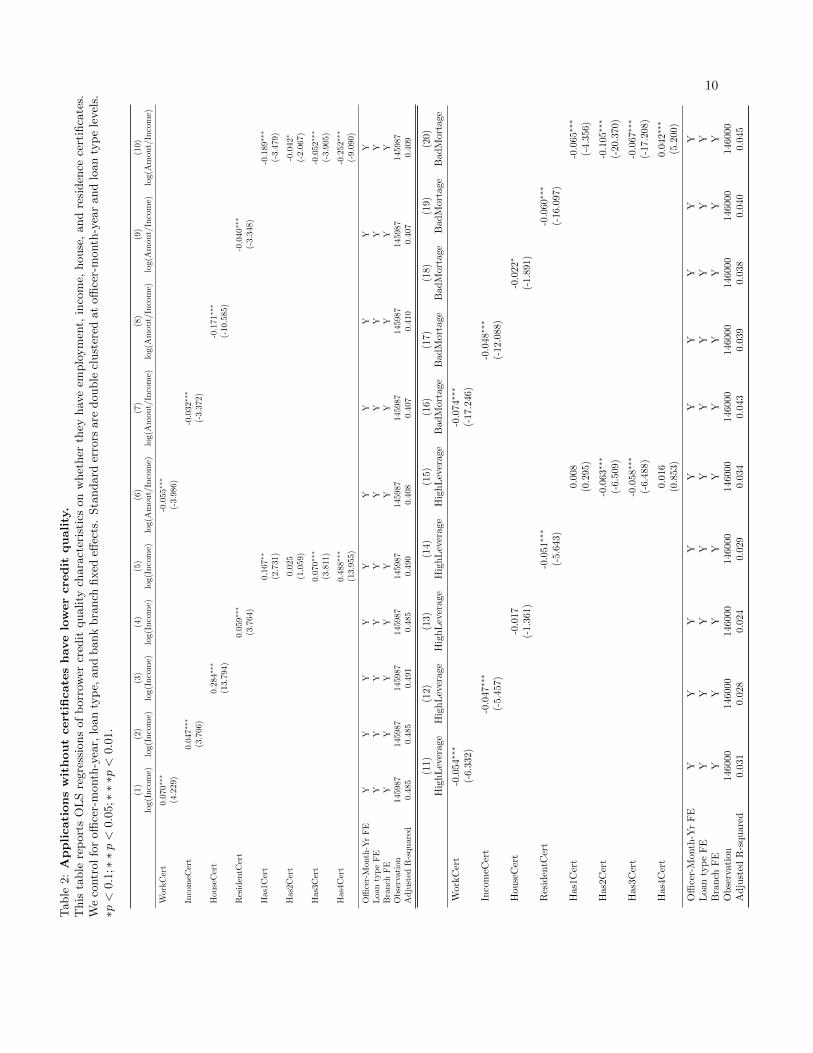

that these applicants indeed have lower income and worse credit-related attributes. This is shown by the

regression results in Table 2. Applicants with certificates tend to have higher income, lower loan-to-income

ratio, lower ex-ante leverage, and lower chance of having bad mortgages payment histories. The relationship

is also monotone in the number of certificates that each applicant has as shown in columns 5, 10, 15, and 20.

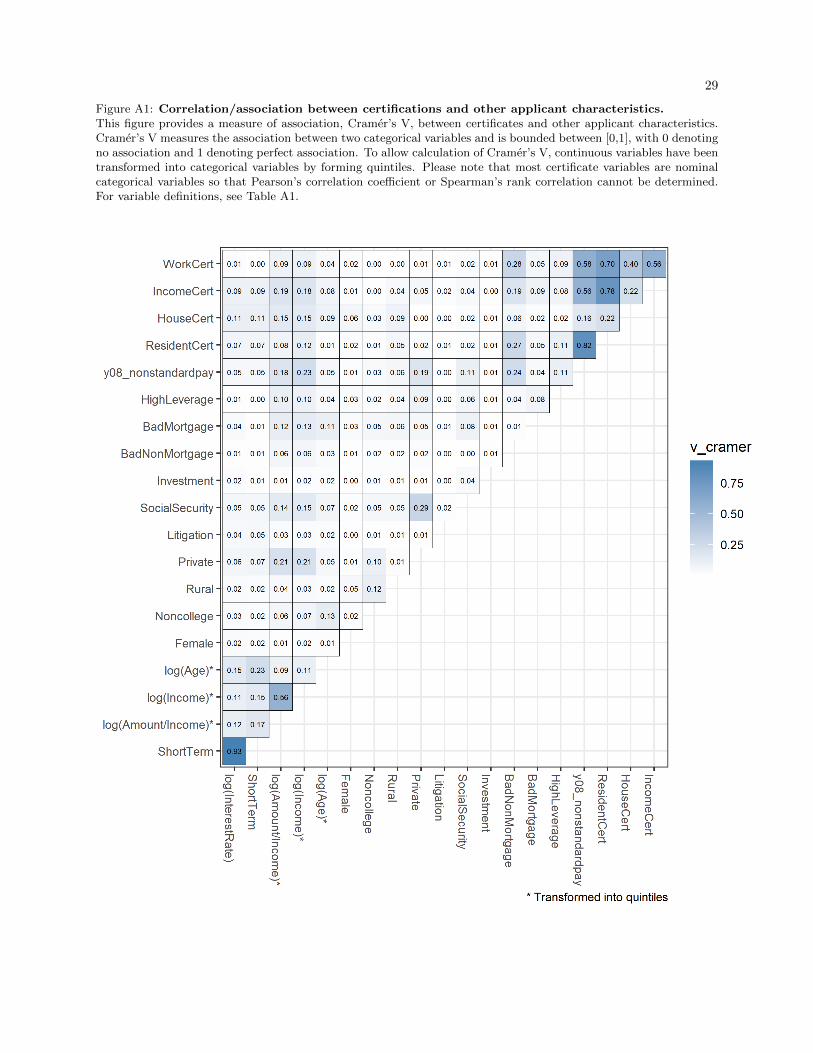

Even though the certificates are correlated with loan characteristics, they clearly do not subsume the in-

formation in other characteristics as the association is not too high. This is shown in Figure ?? in the

Appendix.

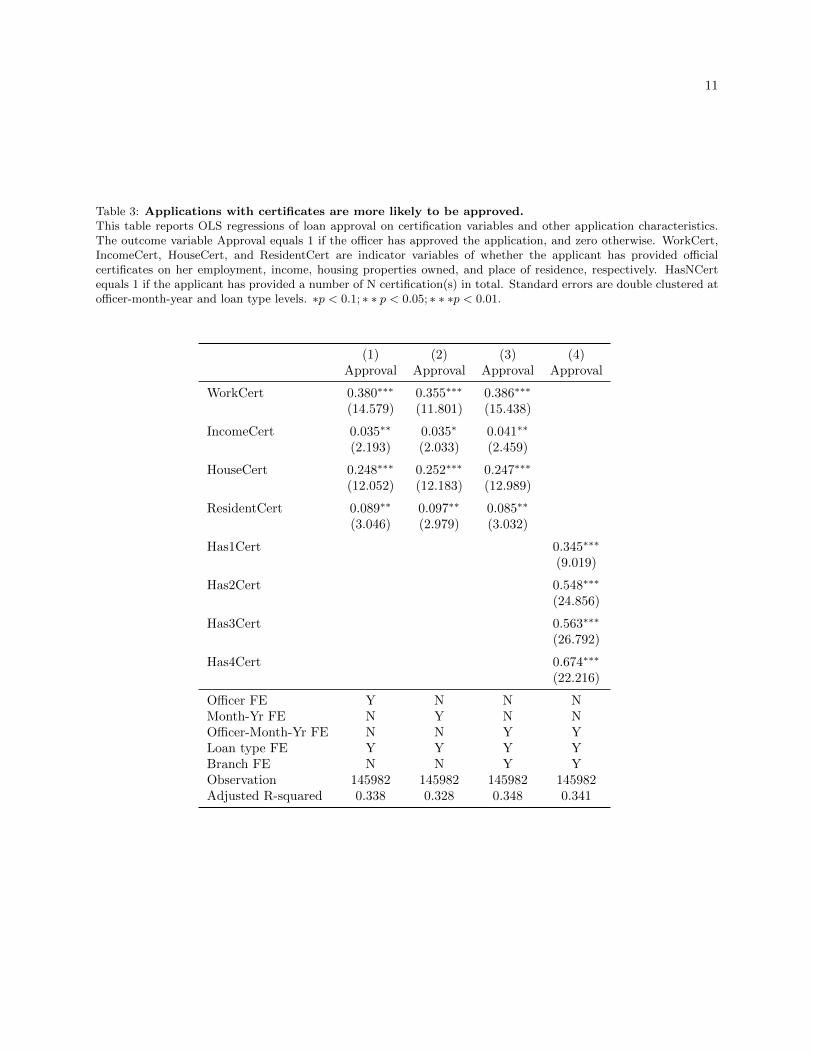

Second, we verify that applicants with more certificates are much more likely to have their loan application

approved. This is shown in Table 3. After controlling for a host of application-level observables, we find

that applicants with certificates are much more likely to be approved. In the main specification in column

3, we control for loan type, bank branch, and officer-year-month fixed effects. Columns 1 and 2 show that

the result is not sensitive to the choice of which fixed effects to include. Column 4 shows that approval rate

is increasing in the number of certificates that the applicant has.

3.3 Do officers use certificates to guide their attention allocation?

The discussion so far suggests that officers, when facing time constraints, may simply use the existence or lack

of certificates to guide their attention allocation across applications assigned to them. If so, we would expect

that applications with fewer or no certificates are more at risk of fast rejection without careful scrutiny.

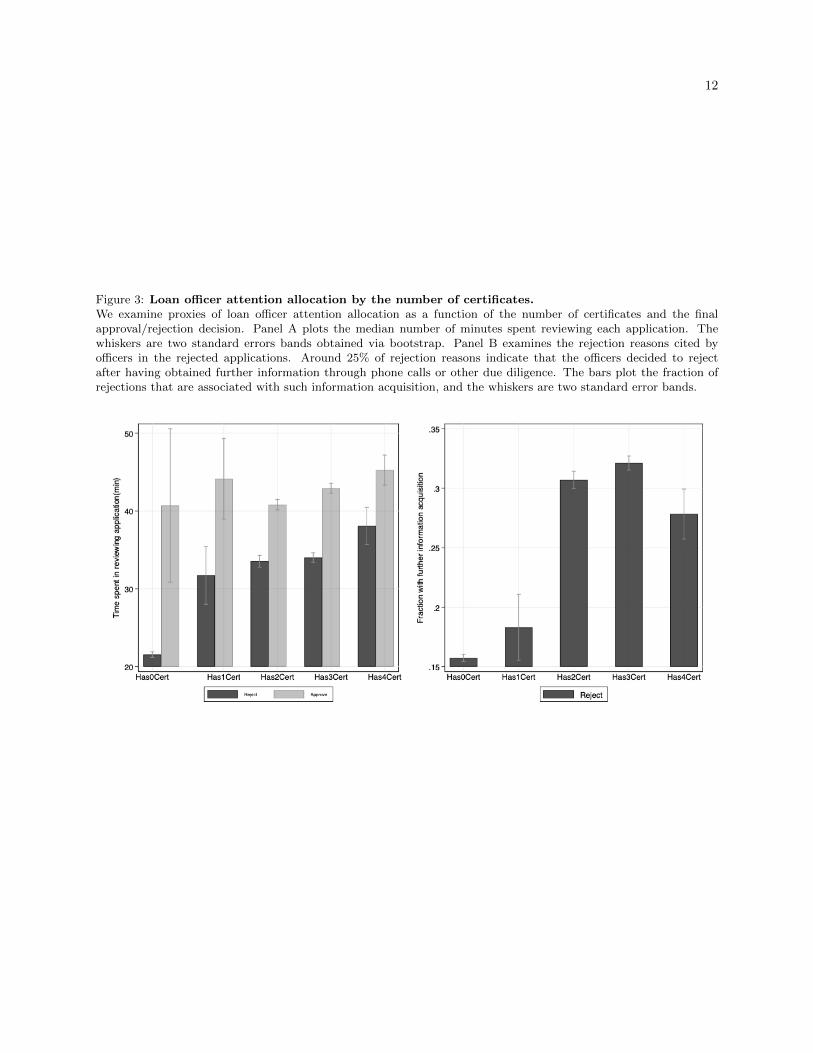

We indeed find evidence that officers use certificates to guide their attention allocation. Panel A of Figure 3

plots the median review time by officers for approved or rejected applications by the number of certificates.

The whiskers are two standard error bands.6 While the time spent on approved applications has little

dependence on the number of certificates, there is large difference in the time spent on rejected applications.

Officers only spend a median of 8.3 minutes before rejecting those without certificates but 21.7 minutes on

those with four certificates. This suggests that applications with no certificates are at high risk of being

rejected without careful review.

We also examine officer attention using what they cite as the reason for rejection. In the bank we study,

officers are asked to select from a list of standardized rejection reasons. While most cited rejection reasons

are boilerplate such as “bad credit quality”, “leverage is too high”, or even “other”, approximately 25%

of the rejection reasons indicate that the officer only rejected after having spent further effort acquiring

information by calling the applicant, contacting references, etc. We take the latter rejection reasons as an

indicator that the officer has attempted further due diligence. Indeed, officers spend a median of 20.7 minutes

when their rejection reasons indicate further due diligence and only 9.9 minutes when not. A list of most

common rejection reasons are listed in Table A2 in the appendix.

Panel B of Figure 3 plots the fraction of rejections with information acquisition. While this is admittedly a

noisy measure, the results show that applications with no certificates are more likely rejected without further

attempts of information acquisition by the officer. This is also consistent with the finding in Panel A which

indicates that such applications tend to be rejected rather quickly.

6We plot median instead of mean because the review time is heavily right skewed, but the results based on means arequalitatively similar.

10

Table

2:

Applicati

ons

wit

hout

cert

ificate

shave

low

er

cre

dit

quality

.T

his

table

rep

ort

sO

LS

regre

ssio

ns

of

borr

ower

cred

itquality

chara

cter

isti

cson

whet

her

they

hav

eem

plo

ym

ent,

inco

me,

house

,and

resi

den

cece

rtifi

cate

s.W

eco

ntr

ol

for

offi

cer-

month

-yea

r,lo

an

typ

e,and

bank

bra

nch

fixed

effec

ts.

Sta

ndard

erro

rsare

double

clust

ered

at

offi

cer-

month

-yea

rand

loan

typ

ele

vel

s.∗p

<0.1

;∗∗p<

0.0

5;∗

∗∗p

<0.0

1.

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

log(I

nco

me)

log(I

nco

me)

log(I

nco

me)

log(I

nco

me)

log(I

nco

me)

log(A

mou

t/In

com

e)lo

g(A

mout/

Inco

me)

log(

Am

ou

t/In

com

e)lo

g(A

mou

t/In

com

e)lo

g(A

mou

t/In

com

e)

Wor

kC

ert

0.070

∗∗∗

-0.0

55∗∗

∗

(4.2

29)

(-3.

986)

Inco

meC

ert

0.0

47∗∗

∗-0

.032

∗∗∗

(3.7

06)

(-3.3

72)

Hou

seC

ert

0.28

4∗∗

∗-0

.171∗

∗∗

(13.7

94)

(-10

.585)

Res

iden

tCer

t0.0

59∗∗

∗-0

.040

∗∗∗

(3.7

64)

(-3.3

48)

Has

1C

ert

0.1

67∗

∗-0

.189

∗∗∗

(2.7

31)

(-3.4

79)

Has

2Cer

t0.0

25

-0.0

42∗

(1.0

59)

(-2.0

67)

Has

3Cer

t0.0

70∗∗

∗-0

.052

∗∗∗

(3.8

11)

(-3.9

05)

Has

4Cer

t0.4

88∗∗

∗-0

.252

∗∗∗

(13.9

55)

(-9.0

90)

Offi

cer-

Mon

th-Y

rF

EY

YY

YY

YY

YY

YL

oan

typ

eF

EY

YY

YY

YY

YY

YB

ran

chF

EY

YY

YY

YY

YY

YO

bse

rvat

ion

1459

87145

987

1459

87145987

145987

145

987

145

987

1459

87

1459

87

14598

7A

dju

sted

R-s

qu

are

d0.

485

0.485

0.49

10.4

85

0.4

90

0.40

80.

407

0.4

10

0.407

0.4

09

(11)

(12)

(13)

(14)

(15)

(16)

(17)

(18)

(19)

(20)

Hig

hL

ever

age

Hig

hL

ever

age

Hig

hL

ever

age

Hig

hL

ever

age

Hig

hL

ever

age

Bad

Mort

age

Bad

Mort

age

Bad

Mor

tage

Bad

Mor

tage

Bad

Mort

age

Wor

kC

ert

-0.0

54∗∗

∗-0

.074∗∗

∗

(-6.

332)

(-17.2

46)

Inco

meC

ert

-0.0

47∗∗

∗-0

.048

∗∗∗

(-5.

457)

(-12

.088

)

Hou

seC

ert

-0.0

17

-0.0

22∗

(-1.3

61)

(-1.8

91)

Res

iden

tCer

t-0

.051

∗∗∗

-0.0

60∗

∗∗

(-5.6

43)

(-16.

097

)

Has

1Cer

t0.0

08

-0.0

65∗∗

∗

(0.2

95)

(-4.

356)

Has

2Cer

t-0

.063∗∗

∗-0

.105∗

∗∗

(-6.5

09)

(-20.

370)

Has

3Cer

t-0

.058∗∗

∗-0

.067∗

∗∗

(-6.4

88)

(-17.

208)

Has

4Cer

t0.0

16

0.0

42∗∗

∗

(0.8

53)

(5.2

00)

Offi

cer-

Mon

th-Y

rF

EY

YY

YY

YY

YY

YL

oan

typ

eF

EY

YY

YY

YY

YY

YB

ran

chF

EY

YY

YY

YY

YY

YO

bse

rvat

ion

1460

00146

000

1460

00

146

000

146000

146000

1460

0014

600

014

600

0146

000

Ad

just

edR

-squ

ared

0.03

10.

028

0.0

24

0.02

90.0

34

0.0

43

0.0

390.

038

0.04

00.0

45

11

Table 3: Applications with certificates are more likely to be approved.This table reports OLS regressions of loan approval on certification variables and other application characteristics.The outcome variable Approval equals 1 if the officer has approved the application, and zero otherwise. WorkCert,IncomeCert, HouseCert, and ResidentCert are indicator variables of whether the applicant has provided officialcertificates on her employment, income, housing properties owned, and place of residence, respectively. HasNCertequals 1 if the applicant has provided a number of N certification(s) in total. Standard errors are double clustered atofficer-month-year and loan type levels. ∗p < 0.1; ∗ ∗ p < 0.05; ∗ ∗ ∗p < 0.01.

(1) (2) (3) (4)Approval Approval Approval Approval

WorkCert 0.380∗∗∗ 0.355∗∗∗ 0.386∗∗∗

(14.579) (11.801) (15.438)

IncomeCert 0.035∗∗ 0.035∗ 0.041∗∗

(2.193) (2.033) (2.459)

HouseCert 0.248∗∗∗ 0.252∗∗∗ 0.247∗∗∗

(12.052) (12.183) (12.989)

ResidentCert 0.089∗∗ 0.097∗∗ 0.085∗∗

(3.046) (2.979) (3.032)

Has1Cert 0.345∗∗∗

(9.019)

Has2Cert 0.548∗∗∗

(24.856)

Has3Cert 0.563∗∗∗

(26.792)

Has4Cert 0.674∗∗∗

(22.216)

Officer FE Y N N NMonth-Yr FE N Y N NOfficer-Month-Yr FE N N Y YLoan type FE Y Y Y YBranch FE N N Y YObservation 145982 145982 145982 145982Adjusted R-squared 0.338 0.328 0.348 0.341

12

Figure 3: Loan officer attention allocation by the number of certificates.We examine proxies of loan officer attention allocation as a function of the number of certificates and the finalapproval/rejection decision. Panel A plots the median number of minutes spent reviewing each application. Thewhiskers are two standard errors bands obtained via bootstrap. Panel B examines the rejection reasons cited byofficers in the rejected applications. Around 25% of rejection reasons indicate that the officers decided to rejectafter having obtained further information through phone calls or other due diligence. The bars plot the fraction ofrejections that are associated with such information acquisition, and the whiskers are two standard error bands.

13

4 Do officers discriminate more when they are busier?

We now test the key prediction of attention discrimination: do officers discriminate more when they are

busier?

4.1 Measuring officer busyness

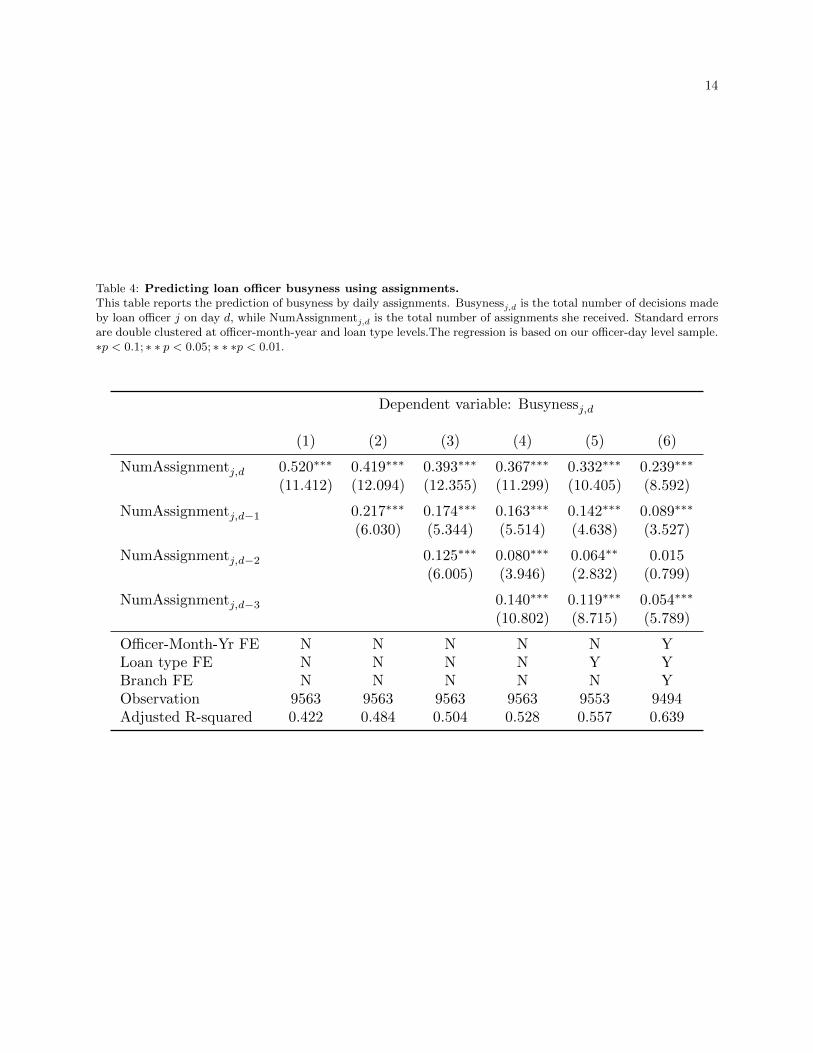

We use several measures of officer busyness. First, we define busynessj,d as the number of decisions made

by officer j on day d. There is ample variation of busyness within officer. On average, an officer handles 24

loans in a top quintile busyness day and only 15 applications in a bottom quintile busyness day.

One obvious worry is that the actual number of decisions made by an officer is endogenous. For instance,

suppose applications with certain characteristics take longer to process, then the busyness of officer will

become negatively correlated with that characteristic. There is some evidence of such correlations in Panel

A of Table 5. Officers can also choose to work faster or slower based on their personal preferences.

Therefore, we want a cleaner measure of busyness that officers do not have control over. To do this, we

instrument the actual busyness using the number of applications assigned:

Busynessj,d = a+ b0 ·NumAssignmentj,d + b1 ·NumAssignmentj,d−1 + b2 ·NumAssignmentj,d−2 (1)

+ b3 ·NumAssignmentj,d−3 + Controls + εj,d (2)

We use up to 3 lagged work days because while some applications are not immediately decided, most

applications are decided within a few days of assignment. The results of this regression is shown in Table 4.

While our data provider does not disclose how exactly the assignment algorithm assign applications to

officers, we are informed that officers themselves have no influence on this assignment process. Thus, the

number of assignments is exogenous from the officer’s point of view. In Panel B of Table 5, we verify that

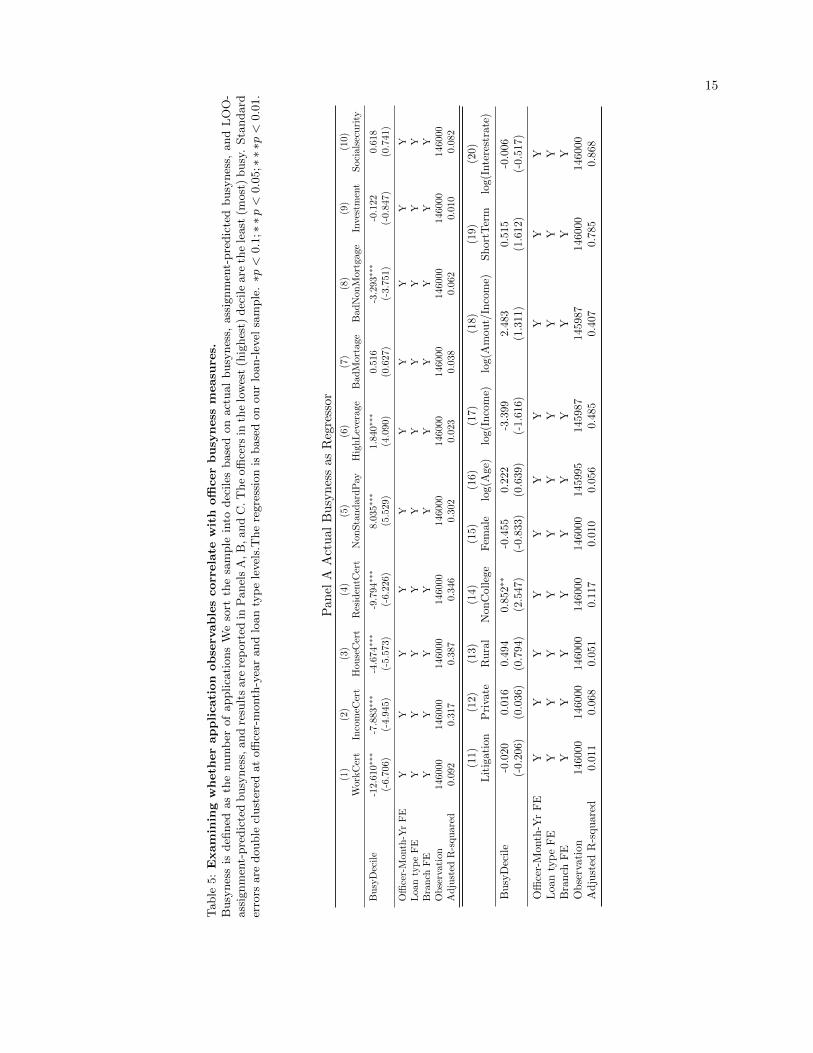

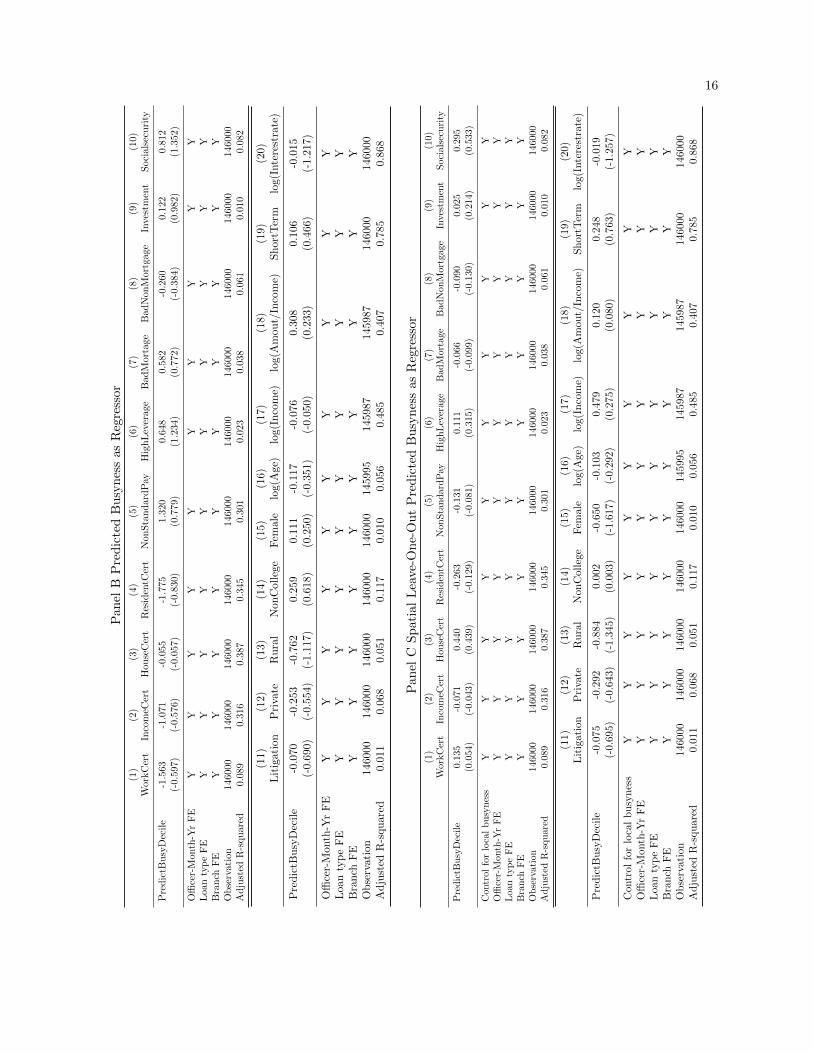

the predicted busyness measure is uncorrelated with all main observable loan characteristics.

Finally, one can also worry about correlation between unobservables and the number of assignments. To

partially address this concern, we also construct a loan-level leave-one-out instrument using the number of

applications from other parts of the country that are assigned to the same loan officer. The idea is that loan

officers at the headquarter office process loan applications from all across the country, and if a large number

of applications from area A makes the loan officer busy, it can affect her decision making on applications

from area B. In this case, the quality of loans from area B is independent to the application volume from

area A that drives the busyness of the loan officer (after controlling for the application volume in the local

area).7

4.2 Does discrimination increase when loan officer are busier?

We now examine whether loan officers discriminate more based on the certificates when busy.

7Panel C of Table 5 verifies that this measure is also not correlated with loan observables.

14

Table 4: Predicting loan officer busyness using assignments.This table reports the prediction of busyness by daily assignments. Busynessj,d is the total number of decisions madeby loan officer j on day d, while NumAssignmentj,d is the total number of assignments she received. Standard errorsare double clustered at officer-month-year and loan type levels.The regression is based on our officer-day level sample.∗p < 0.1; ∗ ∗ p < 0.05; ∗ ∗ ∗p < 0.01.

Dependent variable: Busynessj,d

(1) (2) (3) (4) (5) (6)

NumAssignmentj,d 0.520∗∗∗ 0.419∗∗∗ 0.393∗∗∗ 0.367∗∗∗ 0.332∗∗∗ 0.239∗∗∗

(11.412) (12.094) (12.355) (11.299) (10.405) (8.592)

NumAssignmentj,d−1 0.217∗∗∗ 0.174∗∗∗ 0.163∗∗∗ 0.142∗∗∗ 0.089∗∗∗

(6.030) (5.344) (5.514) (4.638) (3.527)

NumAssignmentj,d−2 0.125∗∗∗ 0.080∗∗∗ 0.064∗∗ 0.015(6.005) (3.946) (2.832) (0.799)

NumAssignmentj,d−3 0.140∗∗∗ 0.119∗∗∗ 0.054∗∗∗

(10.802) (8.715) (5.789)

Officer-Month-Yr FE N N N N N YLoan type FE N N N N Y YBranch FE N N N N N YObservation 9563 9563 9563 9563 9553 9494Adjusted R-squared 0.422 0.484 0.504 0.528 0.557 0.639

15

Table

5:

Exam

inin

gw

heth

er

applicati

on

obse

rvable

scorr

ela

tew

ith

offi

cer

busy

ness

measu

res.

Busy

nes

sis

defi

ned

as

the

num

ber

of

applica

tions

We

sort

the

sam

ple

into

dec

iles

base

don

act

ual

busy

nes

s,ass

ignm

ent-

pre

dic

ted

busy

nes

s,and

LO

O-

ass

ignm

ent-

pre

dic

ted

busy

nes

s,and

resu

lts

are

rep

ort

edin

Panel

sA

,B

,and

C.T

he

offi

cers

inth

elo

wes

t(h

ighes

t)dec

ile

are

the

least

(most

)busy

.Sta

ndard

erro

rsare

double

clust

ered

at

offi

cer-

month

-yea

rand

loan

typ

ele

vel

s.T

he

regre

ssio

nis

base

don

our

loan-l

evel

sam

ple

.∗p

<0.1

;∗∗p<

0.0

5;∗

∗∗p

<0.0

1.

Pan

elA

Act

ual

Bu

syn

ess

as

Reg

ress

or

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Wor

kC

ert

Inco

meC

ert

Hou

seC

ert

Res

iden

tCer

tN

onSta

ndar

dP

ayH

igh

Lev

erag

eB

adM

orta

ge

BadN

onM

ort

gage

Inves

tmen

tS

oci

als

ecu

rity

Busy

Dec

ile

-12.

610∗

∗∗-7

.883

∗∗∗

-4.6

74∗∗

∗-9

.794

∗∗∗

8.03

5∗∗

∗1.

840∗

∗∗0.

516

-3.2

93∗∗

∗-0

.122

0.6

18

(-6.

706)

(-4.

945)

(-5.

573)

(-6.

226)

(5.5

29)

(4.0

90)

(0.6

27)

(-3.7

51)

(-0.8

47)

(0.7

41)

Offi

cer-

Mon

th-Y

rF

EY

YY

YY

YY

YY

YL

oan

typ

eF

EY

YY

YY

YY

YY

YB

ranch

FE

YY

YY

YY

YY

YY

Obse

rvat

ion

1460

0014

6000

1460

0014

600

014

6000

1460

0014

6000

146000

146000

146000

Adju

sted

R-s

quar

ed0.

092

0.31

70.

387

0.34

60.

302

0.023

0.03

80.0

62

0.0

10

0.0

82

(11)

(12)

(13)

(14)

(15)

(16)

(17)

(18)

(19)

(20)

Lit

igat

ion

Pri

vate

Rura

lN

on

Coll

ege

Fem

ale

log(A

ge)

log(I

nco

me)

log(

Am

ou

t/In

com

e)S

hort

Ter

mlo

g(In

tere

stra

te)

Bu

syD

ecil

e-0

.020

0.01

60.

494

0.8

52∗∗

-0.4

55

0.2

22-3

.399

2.483

0.515

-0.0

06

(-0.

206)

(0.0

36)

(0.7

94)

(2.5

47)

(-0.8

33)

(0.6

39)

(-1.6

16)

(1.3

11)

(1.6

12)

(-0.5

17)

Offi

cer-

Mon

th-Y

rF

EY

YY

YY

YY

YY

YL

oan

typ

eF

EY

YY

YY

YY

YY

YB

ran

chF

EY

YY

YY

YY

YY

YO

bse

rvat

ion

1460

0014

6000

146000

146000

146000

145995

145

987

1459

8714

6000

146

000

Ad

just

edR

-squ

ared

0.01

10.

068

0.051

0.1

170.

010

0.0

56

0.485

0.407

0.7

850.8

68

16

Pan

elB

Pre

dic

ted

Bu

syn

ess

as

Reg

ress

or

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Wor

kC

ert

Inco

meC

ert

Hou

seC

ert

Res

iden

tCer

tN

onS

tan

dar

dP

ayH

igh

Lev

erag

eB

adM

ort

age

Bad

Non

Mort

gage

Inve

stm

ent

Soci

als

ecu

rity

Pre

dic

tBu

syD

ecil

e-1

.563

-1.0

71-0

.055

-1.7

75

1.32

00.6

48

0.58

2-0

.260

0.1

22

0.8

12

(-0.

597)

(-0.

576)

(-0.

057)

(-0.

830)

(0.7

79)

(1.2

34)

(0.7

72)

(-0.3

84)

(0.9

82)

(1.3

52)

Offi

cer-

Mon

th-Y

rF

EY

YY

YY

YY

YY

YL

oan

typ

eF

EY

YY

YY

YY

YY

YB

ran

chF

EY

YY

YY

YY

YY

YO

bse

rvat

ion

1460

0014

6000

1460

00

146

000

1460

0014

6000

146

000

146000

146000

146000

Ad

just

edR

-squ

ared

0.08

90.

316

0.38

70.3

450.

301

0.023

0.0

380.0

61

0.0

10

0.0

82

(11)

(12)

(13)

(14)

(15)

(16)

(17)

(18)

(19)

(20)

Lit

igat

ion

Pri

vate

Rura

lN

on

Coll

ege

Fem

ale

log(A

ge)

log(I

nco

me)

log(A

mou

t/In

com

e)S

hort

Ter

mlo

g(I

nte

rest

rate

)

Pre

dic

tBu

syD

ecil

e-0

.070

-0.2

53-0

.762

0.2

59

0.1

11

-0.1

17

-0.0

76

0.3

08

0.1

06

-0.0

15

(-0.

690)

(-0.

554)

(-1.

117)

(0.6

18)

(0.2

50)

(-0.3

51)

(-0.0

50)

(0.2

33)

(0.4

66)

(-1.2

17)

Offi

cer-

Mon

th-Y

rF

EY

YY

YY

YY

YY

YL

oan

typ

eF

EY

YY

YY

YY

YY

YB

ran

chF

EY

YY

YY

YY

YY

YO

bse

rvat

ion

1460

0014

6000

14600

01460

00

1460

00

145995

14598

714598

7146000

146000

Ad

just

edR

-squ

ared

0.01

10.

068

0.0

510.1

17

0.0

10

0.0

56

0.4

85

0.407

0.7

85

0.8

68

Pan

elC

Sp

ati

al

Lea

ve-

On

e-O

ut

Pre

dic

ted

Bu

syn

ess

as

Reg

ress

or

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Wor

kC

ert

Inco

meC

ert

Hou

seC

ert

Res

iden

tCer

tN

onSta

ndard

Pay

Hig

hL

ever

age

Bad

Mort

age

BadN

onM

ort

gage

Inve

stm

ent

Soci

als

ecuri

ty

Pre

dic

tBusy

Dec

ile

0.13

5-0

.071

0.440

-0.2

63-0

.131

0.11

1-0

.066

-0.0

90

0.0

25

0.2

95

(0.0

54)

(-0.

043)

(0.4

39)

(-0.

129)

(-0.

081)

(0.3

15)

(-0.0

99)

(-0.1

30)

(0.2

14)

(0.5

33)

Con

trol

for

loca

lbusy

nes

sY

YY

YY

YY

YY

YO

ffice

r-M

onth

-Yr

FE

YY

YY

YY

YY

YY

Loa

nty

pe

FE

YY

YY

YY

YY

YY

Bra

nch

FE

YY

YY

YY

YY

YY

Obse

rvat

ion

1460

0014

6000

1460

00

1460

0014

600

014

6000

1460

00146000

146000

146000

Adju

sted

R-s

quar

ed0.

089

0.31

60.

387

0.34

50.

301

0.02

30.0

38

0.0

61

0.0

10

0.0

82

(11)

(12)

(13)

(14)

(15)

(16)

(17)

(18)

(19)

(20)

Lit

igat

ion

Pri

vate

Rura

lN

on

Coll

ege

Fem

ale

log(

Age

)lo

g(I

nco

me)

log(A

mou

t/In

com

e)S

hor

tTer

mlo

g(In

tere

stra

te)

Pre

dic

tBu

syD

ecil

e-0

.075

-0.2

92

-0.8

840.

002

-0.6

50-0

.103

0.47

90.

120

0.248

-0.0

19(-

0.69

5)(-

0.64

3)

(-1.3

45)

(0.0

03)

(-1.

617)

(-0.2

92)

(0.2

75)

(0.0

80)

(0.7

63)

(-1.

257)

Con

trol

for

loca

lb

usy

nes

sY

YY

YY

YY

YY

YO

ffice

r-M

onth

-Yr

FE

YY

YY

YY

YY

YY

Loa

nty

pe

FE

YY

YY

YY

YY

YY

Bra

nch

FE

YY

YY

YY

YY

YY

Ob

serv

atio

n14

6000

1460

00

14600

0146

000

14600

0145

995

145

987

1459

8714

6000

1460

00

Ad

just

edR

-squ

ared

0.01

10.

068

0.0

510.1

170.

010

0.05

60.4

85

0.40

70.

785

0.8

68

17

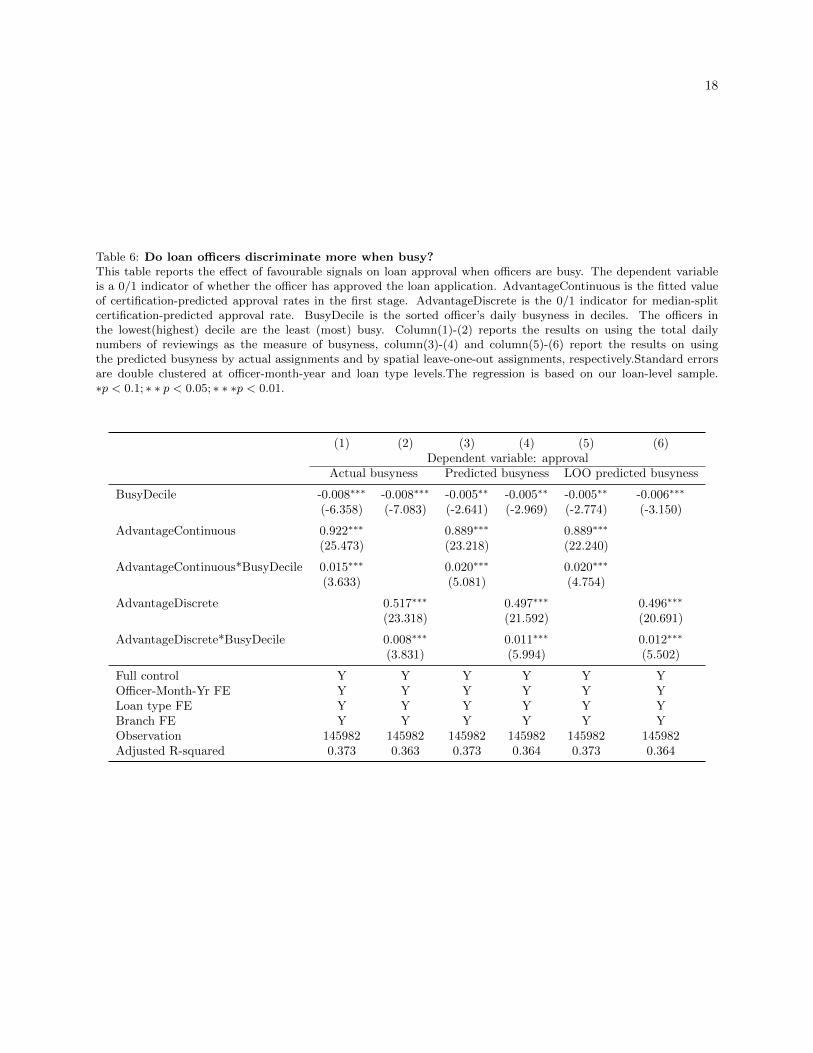

To capture the extent to which the four certificates collectively affect loan officer decisions, we construct a

single-dimension measure that reflect the applicant’s ex-ante advantageousness perceived by the loan officer

based on the existence of those four certificates. This measure is estimated by regressing the actual approval

outcome on the four certificate indicators and then computing the predicted value of the outcome. The

estimation is shown in Table 3. We call the certificates-predicted approval rate, which is continuous, as

AdvantageContinuous. For simplicity of plotting, we also split applications into halves by this measure and

create an indicator variable AdvantageDiscrete which equals 1 for applications in the top 50% of Advantage-

Continuous.

To exploit variation in busyness, we split the sample into deciles based on the three busyness measures.

We then estimate the impact of being in the ex-ante advantaged group on approval rate interacted with

busyness. Table 6 reports the results. As predicted, when officers are busier, their decision depends more

heavily on whether the application is from the more ex-ante advantage group. Regardless of the busyness

measure used, the coefficient of approval rate on AdvantageDiscrete increases by 8% to 12% when busyness

goes from the lowest to the highest decile (columns 2, 4, and 6). This effect is economically large as the

overall approval rate is only 34%.

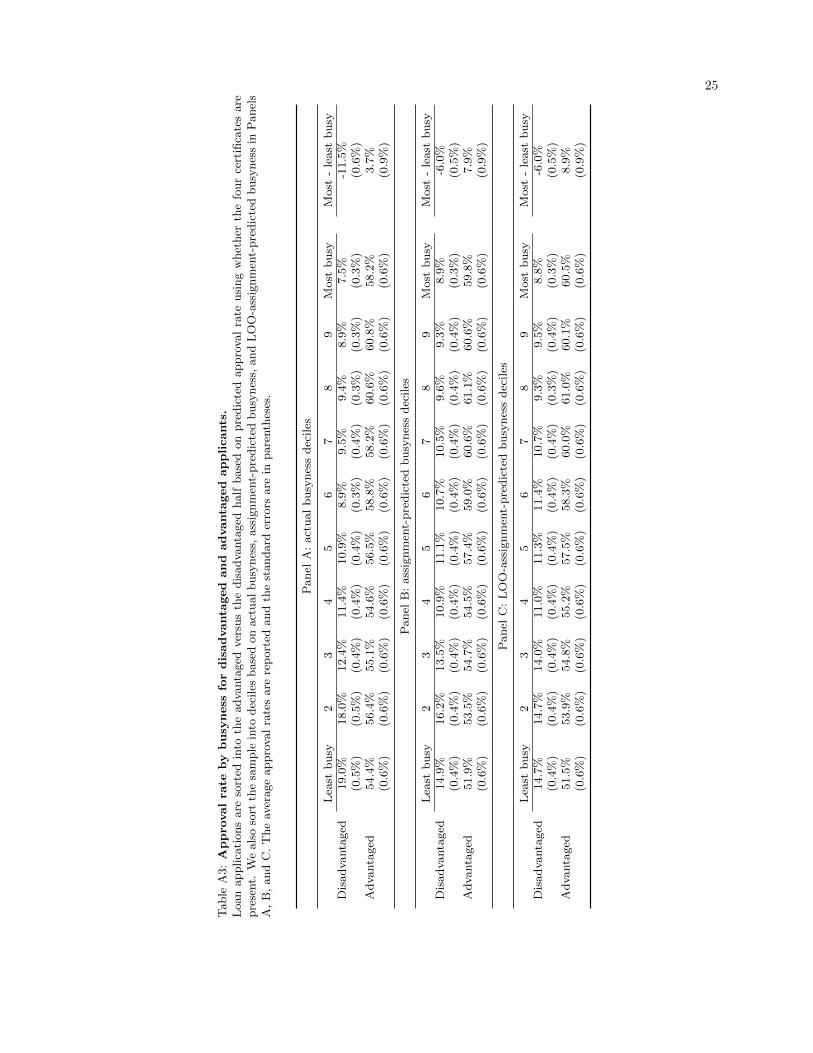

How large are the effects? To get an intuitive sense, Figure 4 plots the average approval rate of advantaged

and disadvantaged applicants in the ten deciles of busyness. The disadvantaged group has an approval rate

of 14.7% to 19.0% in the least busy decile but that declines to around half – 7.5% to 8.9% – in the most busy

decile. In contrast, the advantaged group enjoys some increase in approval rate. The numbers are reported

in Table A3 in the appendix.

In an ideal world, applications should only be judged based on their creditworthiness. However, in our

sample, the actual outcome also depends on the extraneous factor of whether the officer happens to be busy

or not when processing the application.

4.3 Robustness

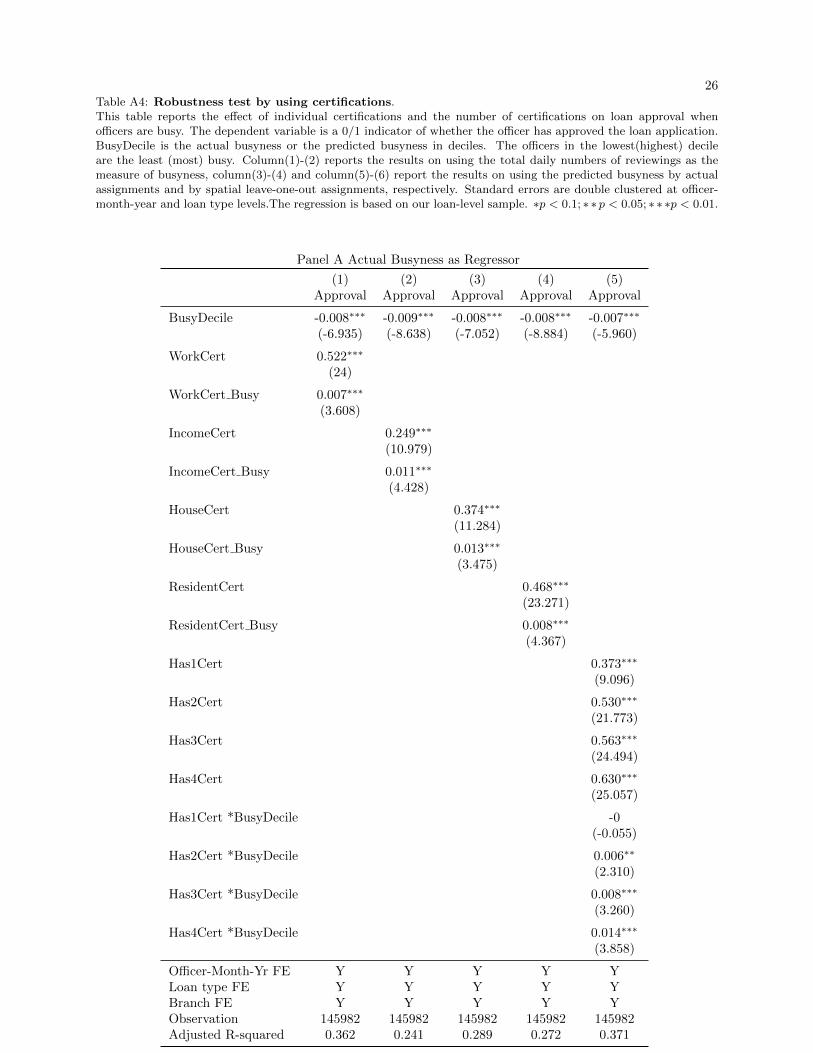

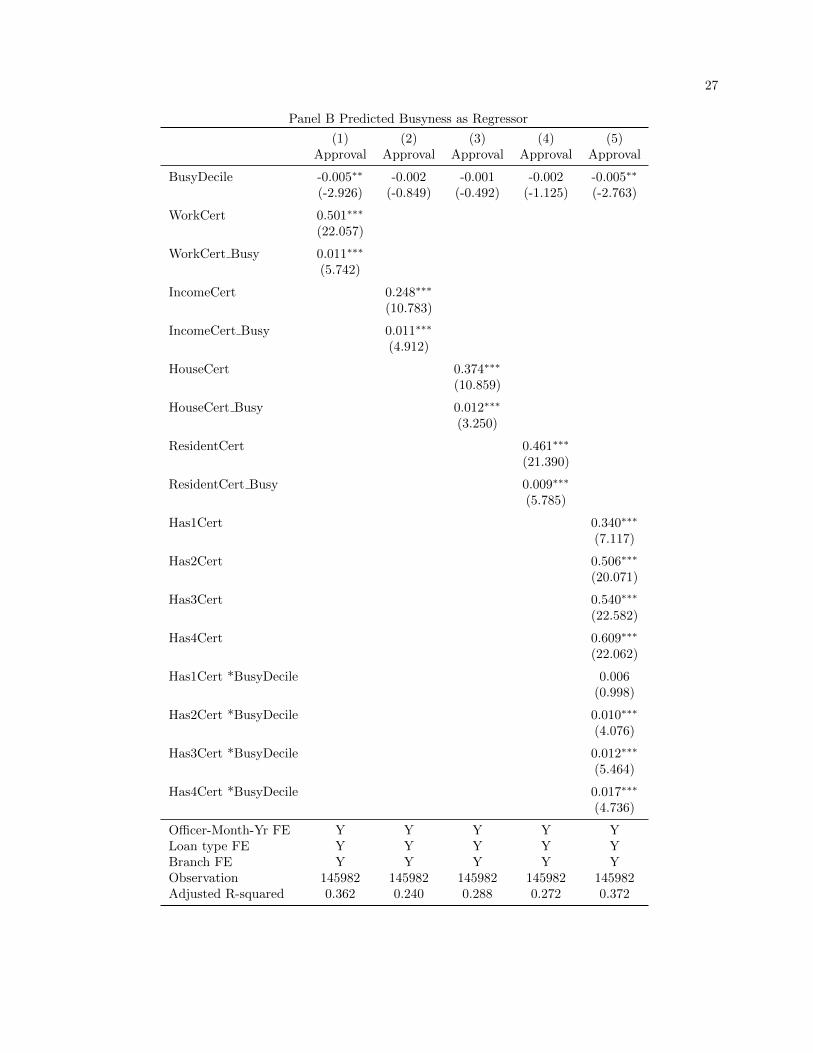

One may be concerned that our results depend on the specific way we define advantage and disadvantage ap-

plicants. We now verify that the result also holds when we separately examining each of the four certificates,

as shown in Table A4. To conserve space, we only report results using the LOO-assignment-predicted-

busyness as the results using the other two measures, reported in the appendix, are similar. For each of the

four certificates, their impact on approval rate increases when the loan officer is busier. Further, column 5

shows that the interaction effect increases with the number of certificates.

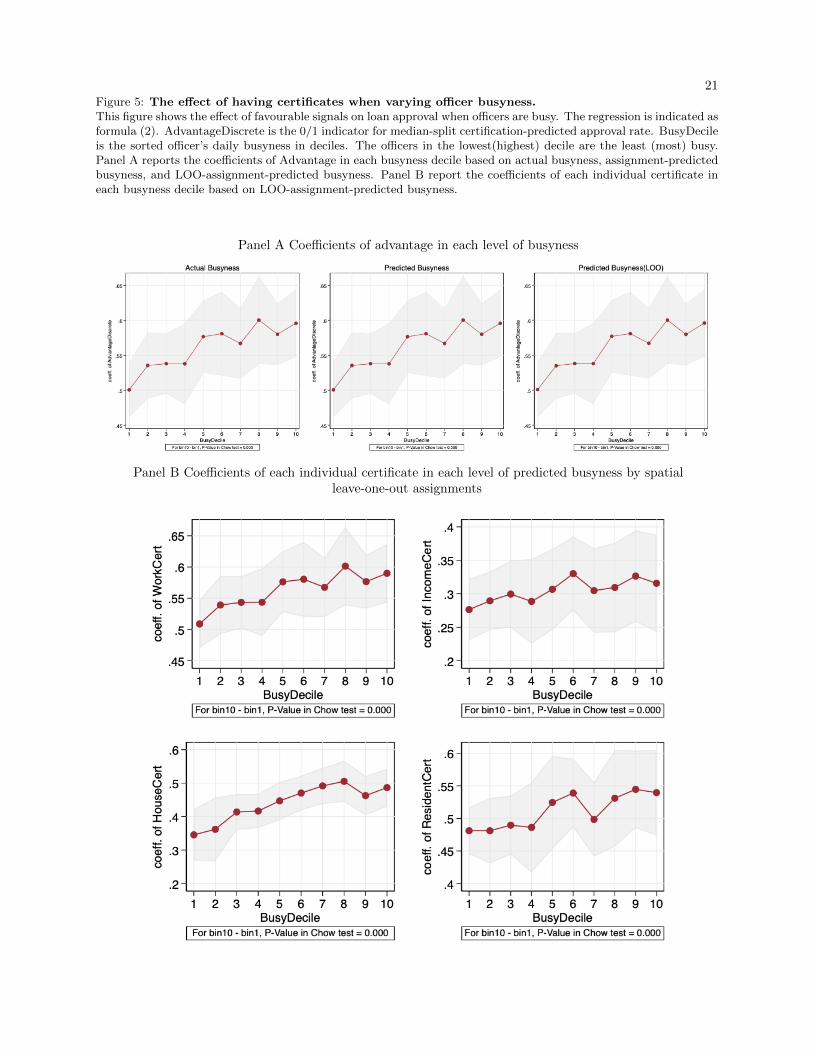

The effect is also relatively monotone in the degree of busyness. To test this, we replace the busyness Decile

in the earlier regression by indicators:

Approvali = a+

10∑k=1

bk ·AdvantageDiscrete · Ibusyness decile k + Controlsi + εi

and plot the coefficients {b1, ..., b10} in Panel A of Figure 5 with two standard error bands. For the lowest

busyness decile, the advantaged applications are accepted with approximately 50% higher probability, a

18

Table 6: Do loan officers discriminate more when busy?This table reports the effect of favourable signals on loan approval when officers are busy. The dependent variableis a 0/1 indicator of whether the officer has approved the loan application. AdvantageContinuous is the fitted valueof certification-predicted approval rates in the first stage. AdvantageDiscrete is the 0/1 indicator for median-splitcertification-predicted approval rate. BusyDecile is the sorted officer’s daily busyness in deciles. The officers inthe lowest(highest) decile are the least (most) busy. Column(1)-(2) reports the results on using the total dailynumbers of reviewings as the measure of busyness, column(3)-(4) and column(5)-(6) report the results on usingthe predicted busyness by actual assignments and by spatial leave-one-out assignments, respectively.Standard errorsare double clustered at officer-month-year and loan type levels.The regression is based on our loan-level sample.∗p < 0.1; ∗ ∗ p < 0.05; ∗ ∗ ∗p < 0.01.

(1) (2) (3) (4) (5) (6)Dependent variable: approval

Actual busyness Predicted busyness LOO predicted busyness

BusyDecile -0.008∗∗∗ -0.008∗∗∗ -0.005∗∗ -0.005∗∗ -0.005∗∗ -0.006∗∗∗

(-6.358) (-7.083) (-2.641) (-2.969) (-2.774) (-3.150)

AdvantageContinuous 0.922∗∗∗ 0.889∗∗∗ 0.889∗∗∗

(25.473) (23.218) (22.240)

AdvantageContinuous*BusyDecile 0.015∗∗∗ 0.020∗∗∗ 0.020∗∗∗

(3.633) (5.081) (4.754)

AdvantageDiscrete 0.517∗∗∗ 0.497∗∗∗ 0.496∗∗∗

(23.318) (21.592) (20.691)

AdvantageDiscrete*BusyDecile 0.008∗∗∗ 0.011∗∗∗ 0.012∗∗∗

(3.831) (5.994) (5.502)

Full control Y Y Y Y Y YOfficer-Month-Yr FE Y Y Y Y Y YLoan type FE Y Y Y Y Y YBranch FE Y Y Y Y Y YObservation 145982 145982 145982 145982 145982 145982Adjusted R-squared 0.373 0.363 0.373 0.364 0.373 0.364

19

Figure 4: Approval rate by busyness for disadvantaged and advantaged applicants.Loan applications are sorted into the advantaged versus the disadvantaged half based on predicted approval rate usingwhether the four certificates are present. We also sort the sample into deciles based on actual busyness, assignment-predicted busyness, and LOO-assignment-predicted busyness in Panels A, B, and C.

(a) Sorting on actual busyness (b) Sorting on predicted busyness

(c) Sorting on LOO-predicted busyness

20

number that increases to around 60% in the top busyness decile regardless of the busyness measure used.

In Panel B, we repeat the same exercise by only each of the four individual certificates and the results are

qualitatively similar. To conserve space, in Panel B, we only report results using the LOO busyness measure

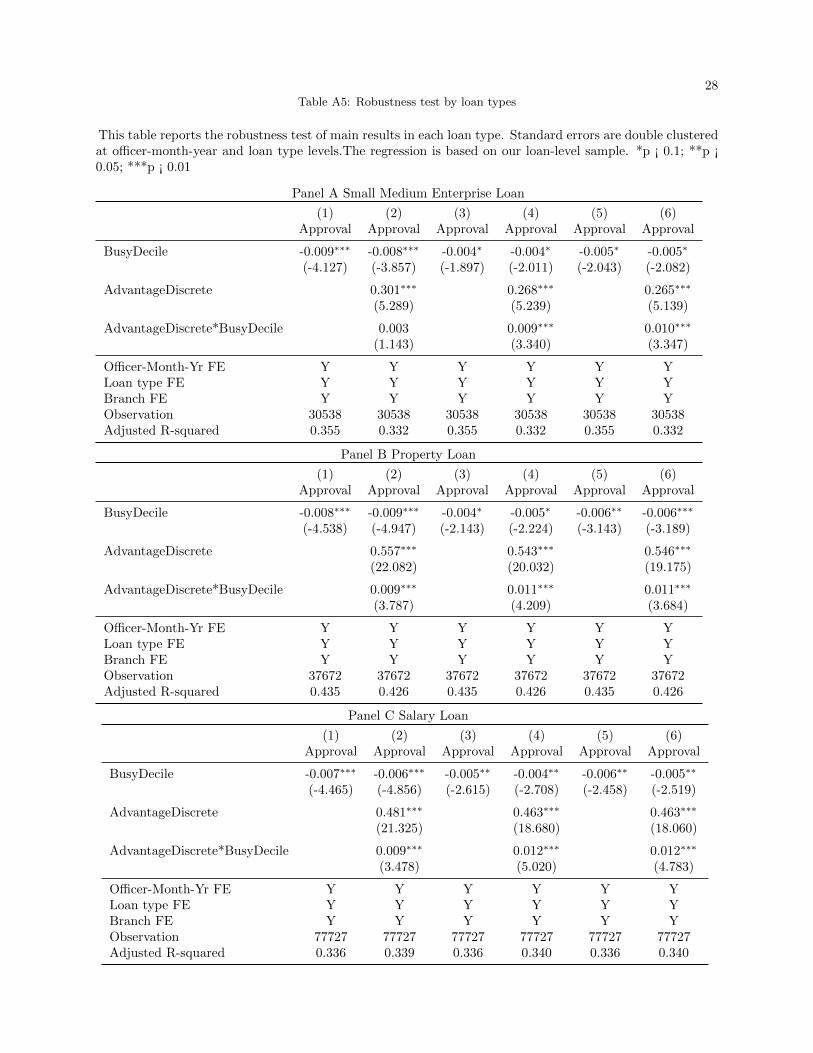

and report the qualitatively similar results using other busyness measures in the appendix. Finally, in Table

A5, we also verify that our findings are robust in each of the three types of loans.

5 Conclusion

Traditionally, researchers focus on preference-based and statistical-discrimination of decision makers. In this

paper, we call attention to “attention discrimination”. That is, when acting under attention constraints,

decision makers may choose to pay less attention to ex-ante disadvantaged applicants and exert less effort

acquiring information about them. In settings where the default action is to reject, this leads to higher

rejection rates for those disadvantaged applicants.

This paper is the first to document attention discrimination in large-scale field data. Using the proprietary

retail loan screening records of a large Chinese bank, we show that loan officers allocate less attention to

reviewing applicants who cannot obtain official certificates for their income, property, etc. Those disadvan-

taged applicants are much more likely to be summarily rejected only after a few minutes of review. Further,

when loan officers are busy and overwhelmed by workload, such discrimination increases. The effect is

economically significant: if a disadvantaged application is processed when officers are in the top decile of

busyness, its approval probability shrinks from 19% to 7.5% – a three-fifths reduction.

Our findings have important implications for designing policies to combat discrimination. Since discrimina-

tion is the unintentional byproduct of busyness, it is important for the decision makers to not be overwhelmed

by workload. Unfortunately, this is often the case for court judges, USPTO patent examiners, etc. Then

more these institutions are short-staffed, the more it may be unavoidable for them to exhibit discriminatory

propensities.

21Figure 5: The effect of having certificates when varying officer busyness.This figure shows the effect of favourable signals on loan approval when officers are busy. The regression is indicated asformula (2). AdvantageDiscrete is the 0/1 indicator for median-split certification-predicted approval rate. BusyDecileis the sorted officer’s daily busyness in deciles. The officers in the lowest(highest) decile are the least (most) busy.Panel A reports the coefficients of Advantage in each busyness decile based on actual busyness, assignment-predictedbusyness, and LOO-assignment-predicted busyness. Panel B report the coefficients of each individual certificate ineach busyness decile based on LOO-assignment-predicted busyness.

Panel A Coefficients of advantage in each level of busyness

Panel B Coefficients of each individual certificate in each level of predicted busyness by spatialleave-one-out assignments

22

References

Arrow, Kenneth J, 1972, Models of job discrimination, Racial discrimination in economic life 83.

Bartlett, Robert, Adair Morse, Richard Stanton, and Nancy Wallace, 2019, Consumer-lending discrimination

in the fintech era, Technical report, National Bureau of Economic Research.

Bartos, Vojtech, Michal Bauer, Julie Chytilova, and Filip Matejka, 2016, Attention discrimination: Theory

and field experiments with monitoring information acquisition, American Economic Review 106, 1437–75.

Davies, Shaun, Edward Dickersin Van Wesep, and Brian Waters, 2019, On the magnification of small biases

in decision-making, Available at SSRN 3407651 .

Frakes, Michael D, and Melissa F Wasserman, 2017, Is the time allocated to review patent applications induc-

ing examiners to grant invalid patents? evidence from microlevel application data, Review of Economics

and Statistics 99, 550–563.

Fuster, Andreas, Paul Goldsmith-Pinkham, Tarun Ramadorai, and Ansgar Walther, 2020, Predictably un-

equal? the effects of machine learning on credit markets .

Gabaix, Xavier, 2019, Behavioral inattention, Handbook of Behavioral Economics: Applications and Foun-

dations 1 2, 261–343.

Gao, Janet, Stephen A Karolyi, and Joseph Pacelli, 2018, Screening and monitoring by inattentive corporate

loan officers, Technical report, Working Paper.

Kahneman, Daniel, 2011, Thinking, fast and slow (Macmillan).

Liao, Li, Zhengwei Wang, Jia Xiang, Hongjun Yan, and Jun Yang, 2020, User interface and firsthand

experience in retail investing, The Review of Financial Studies .

Phelps, Edmund S, 1972, The statistical theory of racism and sexism, The american economic review 62,

659–661.

The Chronicle of Higher Education, 2017, Working smarter, not harder, in admissions, Online article by

Eric Hoover (March 12, 2017) .

Time Magazine, 2002, How to make your resume last longer than 6 seconds, Online article by Josh Sanburn

(April 13, 2012) .

23

APPENDIX

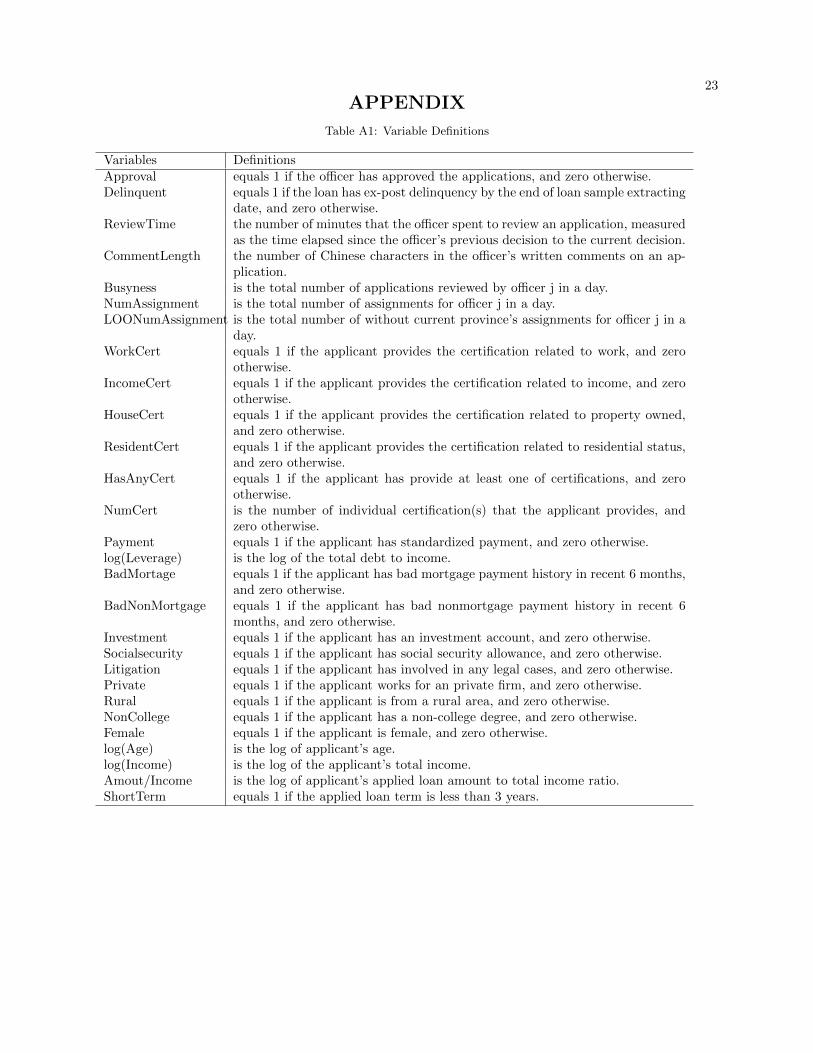

Table A1: Variable Definitions

Variables DefinitionsApproval equals 1 if the officer has approved the applications, and zero otherwise.Delinquent equals 1 if the loan has ex-post delinquency by the end of loan sample extracting

date, and zero otherwise.ReviewTime the number of minutes that the officer spent to review an application, measured

as the time elapsed since the officer’s previous decision to the current decision.CommentLength the number of Chinese characters in the officer’s written comments on an ap-

plication.Busyness is the total number of applications reviewed by officer j in a day.NumAssignment is the total number of assignments for officer j in a day.LOONumAssignment is the total number of without current province’s assignments for officer j in a

day.WorkCert equals 1 if the applicant provides the certification related to work, and zero

otherwise.IncomeCert equals 1 if the applicant provides the certification related to income, and zero

otherwise.HouseCert equals 1 if the applicant provides the certification related to property owned,

and zero otherwise.ResidentCert equals 1 if the applicant provides the certification related to residential status,

and zero otherwise.HasAnyCert equals 1 if the applicant has provide at least one of certifications, and zero

otherwise.NumCert is the number of individual certification(s) that the applicant provides, and

zero otherwise.Payment equals 1 if the applicant has standardized payment, and zero otherwise.log(Leverage) is the log of the total debt to income.BadMortage equals 1 if the applicant has bad mortgage payment history in recent 6 months,

and zero otherwise.BadNonMortgage equals 1 if the applicant has bad nonmortgage payment history in recent 6

months, and zero otherwise.Investment equals 1 if the applicant has an investment account, and zero otherwise.Socialsecurity equals 1 if the applicant has social security allowance, and zero otherwise.Litigation equals 1 if the applicant has involved in any legal cases, and zero otherwise.Private equals 1 if the applicant works for an private firm, and zero otherwise.Rural equals 1 if the applicant is from a rural area, and zero otherwise.NonCollege equals 1 if the applicant has a non-college degree, and zero otherwise.Female equals 1 if the applicant is female, and zero otherwise.log(Age) is the log of applicant’s age.log(Income) is the log of the applicant’s total income.Amout/Income is the log of applicant’s applied loan amount to total income ratio.ShortTerm equals 1 if the applied loan term is less than 3 years.

24

Table A2: Top ten cited rejection reasons with or without information acquisition.Officers are asked to select from a list of rejection reasons when rejecting an application. We manually separatethem into two categories. The first category (Panel A) suggests that the officer has performed further informationacquisition such as by calling the applicant, his employer, his reference contracts, or contacted third parties. Thesecond category (Panel B) are the rest that do not indicate further information acquisition. We list the top tenreasons in each category. The last column is the median number of minutes spent by officers when citing theserejection reasons.

Panel A: rejection reasons with information acquisition

Rank Cited rejection reasons Obs Fraction Review time (min)

1 Called and found discrepancies 13,402 54.8% 24.02 Employer phone number does not exist 3,254 13.3% 16.43 Cannot reach employer by phone 2,753 11.2% 10.14 Employer said that applicant does not work there 1,537 6.3% 14.45 Provided reference contact information is fake 1,420 5.8% 26.06 References cannot be reached 573 2.3% 12.57 Cannot verify employment information 487 2.0% 19.08 Found issues when contacting third party information provider 461 1.9% 18.29 Applicant or references do not cooperate with due diligence 169 0.7% 20.510 Found negative in further investigation 158 0.6% 27.1Other reasons 262 1.1% 18.7

Panel B: rejection reasons without information acquisition

Rank Cited rejection reasons Obs Fraction Review time (min)

1 Leverage is too high 19,430 27.1% 12.12 Negative credit card history 7,920 11.1% 4.43 Lacking useful credit history 7,334 10.2% 4.74 Other reasons 4,524 6.3% 14.95 Overall too risky 3,124 4.4% 15.26 Negative loan repayment history 2,759 3.9% 4.67 Negative credit card history per the PBOC 2,216 3.1% 6.38 Too many credit requests 1,672 2.3% 4.69 Employment is unstable 1,183 1.7% 16.510 Lacking work or business operation history 1,123 1.6% 14.4Other reasons 20,283 28.3% 12.8

25

Table

A3:

Appro

val

rate

by

busy

ness

for

dis

advanta

ged

and

advanta

ged

applicants

.L

oan

applica

tions

are

sort

edin

toth

eadva

nta

ged

ver

sus

the

dis

adva

nta

ged

half

base

don

pre

dic

ted

appro

val

rate

usi

ng

whet

her

the

four

cert

ifica

tes

are

pre

sent.

We

als

oso

rtth

esa

mple

into

dec

iles

base

don

act

ual

busy

nes

s,ass

ignm

ent-

pre

dic

ted

busy

nes

s,and

LO

O-a

ssig

nm

ent-

pre

dic

ted

busy

nes

sin

Panel

sA

,B

,and

C.

The

aver

age

appro

val

rate

sare

rep

ort

edand

the

standard

erro

rsare

inpare

nth

eses

.

Pan

elA

:act

ual

bu

syn

ess

dec

iles

Lea

stb

usy

23

45

67

89

Most

bu

syM

ost

-le

ast

bu

syD

isad

vanta

ged

19.0

%18.0

%12.4

%11.4

%10.9

%8.9

%9.5

%9.4

%8.9

%7.5

%-1

1.5

%(0

.5%

)(0

.5%

)(0

.4%

)(0

.4%

)(0

.4%

)(0

.3%

)(0

.4%

)(0

.3%

)(0

.3%

)(0

.3%

)(0

.6%

)A

dvanta

ged

54.4

%56.4

%55.1

%54.6

%56.5

%58.8

%58.2

%60.6

%60.8

%58.2

%3.7

%(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.9%

)

Pan

elB

:ass

ign

men

t-p

red

icte

db

usy

nes

sd

eciles

Lea

stb

usy

23

45

67

89

Most

bu

syM

ost

-le

ast

bu

syD

isad

vanta

ged

14.9

%16.2

%13.5

%10.9

%11.1

%10.7

%10.5

%9.6

%9.3

%8.9

%-6

.0%

(0.4

%)

(0.4

%)

(0.4

%)

(0.4

%)

(0.4

%)

(0.4

%)

(0.4

%)

(0.4

%)

(0.4

%)

(0.3

%)

(0.5

%)

Ad

vanta

ged

51.9

%53.5

%54.7

%54.5

%57.4

%59.0

%60.6

%61.1

%60.6

%59.8

%7.9

%(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.9%

)

Pan

elC

:L

OO

-ass

ign

men

t-p

red

icte

db

usy

nes

sd

eciles

Lea

stb

usy

23

45

67

89

Most

bu

syM

ost

-le

ast

bu

syD

isad

vanta

ged

14.7

%14.7

%14.0

%11.0

%11.3

%11.4

%10.7

%9.3

%9.5

%8.8

%-6

.0%

(0.4

%)

(0.4

%)

(0.4

%)

(0.4

%)

(0.4

%)

(0.4

%)

(0.4

%)

(0.3

%)

(0.4

%)

(0.3

%)

(0.5

%)

Ad

vanta

ged

51.5

%53.9

%54.8

%55.2

%57.5

%58.3

%60.0

%61.0

%60.1

%60.5

%8.9

%(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.6%

)(0

.9%

)

26Table A4: Robustness test by using certifications.This table reports the effect of individual certifications and the number of certifications on loan approval whenofficers are busy. The dependent variable is a 0/1 indicator of whether the officer has approved the loan application.BusyDecile is the actual busyness or the predicted busyness in deciles. The officers in the lowest(highest) decileare the least (most) busy. Column(1)-(2) reports the results on using the total daily numbers of reviewings as themeasure of busyness, column(3)-(4) and column(5)-(6) report the results on using the predicted busyness by actualassignments and by spatial leave-one-out assignments, respectively. Standard errors are double clustered at officer-month-year and loan type levels.The regression is based on our loan-level sample. ∗p < 0.1; ∗∗p < 0.05; ∗∗∗p < 0.01.

Panel A Actual Busyness as Regressor

(1) (2) (3) (4) (5)Approval Approval Approval Approval Approval

BusyDecile -0.008∗∗∗ -0.009∗∗∗ -0.008∗∗∗ -0.008∗∗∗ -0.007∗∗∗

(-6.935) (-8.638) (-7.052) (-8.884) (-5.960)

WorkCert 0.522∗∗∗

(24)

WorkCert Busy 0.007∗∗∗

(3.608)

IncomeCert 0.249∗∗∗

(10.979)

IncomeCert Busy 0.011∗∗∗

(4.428)

HouseCert 0.374∗∗∗

(11.284)

HouseCert Busy 0.013∗∗∗

(3.475)

ResidentCert 0.468∗∗∗

(23.271)

ResidentCert Busy 0.008∗∗∗

(4.367)

Has1Cert 0.373∗∗∗

(9.096)

Has2Cert 0.530∗∗∗

(21.773)

Has3Cert 0.563∗∗∗

(24.494)

Has4Cert 0.630∗∗∗

(25.057)

Has1Cert *BusyDecile -0(-0.055)

Has2Cert *BusyDecile 0.006∗∗

(2.310)

Has3Cert *BusyDecile 0.008∗∗∗

(3.260)

Has4Cert *BusyDecile 0.014∗∗∗

(3.858)

Officer-Month-Yr FE Y Y Y Y YLoan type FE Y Y Y Y YBranch FE Y Y Y Y YObservation 145982 145982 145982 145982 145982Adjusted R-squared 0.362 0.241 0.289 0.272 0.371

27

Panel B Predicted Busyness as Regressor

(1) (2) (3) (4) (5)Approval Approval Approval Approval Approval

BusyDecile -0.005∗∗ -0.002 -0.001 -0.002 -0.005∗∗

(-2.926) (-0.849) (-0.492) (-1.125) (-2.763)

WorkCert 0.501∗∗∗

(22.057)

WorkCert Busy 0.011∗∗∗

(5.742)

IncomeCert 0.248∗∗∗

(10.783)

IncomeCert Busy 0.011∗∗∗

(4.912)

HouseCert 0.374∗∗∗

(10.859)

HouseCert Busy 0.012∗∗∗

(3.250)

ResidentCert 0.461∗∗∗

(21.390)

ResidentCert Busy 0.009∗∗∗

(5.785)

Has1Cert 0.340∗∗∗

(7.117)

Has2Cert 0.506∗∗∗

(20.071)

Has3Cert 0.540∗∗∗

(22.582)

Has4Cert 0.609∗∗∗

(22.062)

Has1Cert *BusyDecile 0.006(0.998)

Has2Cert *BusyDecile 0.010∗∗∗

(4.076)

Has3Cert *BusyDecile 0.012∗∗∗

(5.464)

Has4Cert *BusyDecile 0.017∗∗∗

(4.736)

Officer-Month-Yr FE Y Y Y Y YLoan type FE Y Y Y Y YBranch FE Y Y Y Y YObservation 145982 145982 145982 145982 145982Adjusted R-squared 0.362 0.240 0.288 0.272 0.372

28Table A5: Robustness test by loan types

This table reports the robustness test of main results in each loan type. Standard errors are double clusteredat officer-month-year and loan type levels.The regression is based on our loan-level sample. *p ¡ 0.1; **p ¡0.05; ***p ¡ 0.01

Panel A Small Medium Enterprise Loan

(1) (2) (3) (4) (5) (6)Approval Approval Approval Approval Approval Approval

BusyDecile -0.009∗∗∗ -0.008∗∗∗ -0.004∗ -0.004∗ -0.005∗ -0.005∗

(-4.127) (-3.857) (-1.897) (-2.011) (-2.043) (-2.082)

AdvantageDiscrete 0.301∗∗∗ 0.268∗∗∗ 0.265∗∗∗

(5.289) (5.239) (5.139)

AdvantageDiscrete*BusyDecile 0.003 0.009∗∗∗ 0.010∗∗∗

(1.143) (3.340) (3.347)

Officer-Month-Yr FE Y Y Y Y Y YLoan type FE Y Y Y Y Y YBranch FE Y Y Y Y Y YObservation 30538 30538 30538 30538 30538 30538Adjusted R-squared 0.355 0.332 0.355 0.332 0.355 0.332

Panel B Property Loan

(1) (2) (3) (4) (5) (6)Approval Approval Approval Approval Approval Approval

BusyDecile -0.008∗∗∗ -0.009∗∗∗ -0.004∗ -0.005∗ -0.006∗∗ -0.006∗∗∗

(-4.538) (-4.947) (-2.143) (-2.224) (-3.143) (-3.189)

AdvantageDiscrete 0.557∗∗∗ 0.543∗∗∗ 0.546∗∗∗

(22.082) (20.032) (19.175)

AdvantageDiscrete*BusyDecile 0.009∗∗∗ 0.011∗∗∗ 0.011∗∗∗