AstraZeneca Q4 and Full Year 2014 Results...3 Q4 and Full Year 2014 Results Marc Dunoyer Finance...

44

AstraZeneca Q4 and Full Year 2014 Results

Transcript of AstraZeneca Q4 and Full Year 2014 Results...3 Q4 and Full Year 2014 Results Marc Dunoyer Finance...

AstraZeneca Q4 and Full Year 2014 Results

2

Cautionary statement regarding forward-looking statements In order, among other things, to utilise the 'safe harbour' provisions of the US Private Securities Litigation Reform Act 1995, we are providing the following cautionary statement: This presentation contains certain forward-looking statements with respect to the operations, performance and financial condition of the Group. Although we believe our expectations are based on reasonable assumptions, any forward-looking statements, by their very nature, involve risks and uncertainties and may be influenced by factors that could cause actual outcomes and results to be materially different from those predicted. The forward-looking statements reflect knowledge and information available at the date of preparation of this presentation and AstraZeneca undertakes no obligation to update these forward-looking statements. We identify the forward-looking statements by using the words 'anticipates', 'believes', 'expects', 'intends' and similar expressions in such statements. Important factors that could cause actual results to differ materially from those contained in forward-looking statements, certain of which are beyond our control, include, among other things: the loss or expiration of patents, marketing exclusivity or trade marks, or the risk of failure to obtain patent protection; the risk of substantial adverse litigation/government investigation claims and insufficient insurance coverage; exchange rate fluctuations; the risk that R&D will not yield new products that achieve commercial success; the risk that strategic alliances and acquisitions will be unsuccessful; the impact of competition, price controls and price reductions; taxation risks; the risk of substantial product liability claims; the impact of any failure by third parties to supply materials or services; the risk of failure to manage a crisis; the risk of delay to new product launches; the difficulties of obtaining and maintaining regulatory approvals for products; the risk of failure to observe ongoing regulatory oversight; the risk that new products do not perform as we expect; the risk of environmental liabilities; the risks associated with conducting business in emerging markets; the risk of reputational damage; the risk of product counterfeiting; the risk of failure to successfully implement planned cost reduction measures through productivity initiatives and restructuring programmes; the risk that regulatory approval processes for biosimilars could have an adverse effect on future commercial prospects; and the impact of increasing implementation and enforcement of more stringent anti-bribery and anti-corruption legislation. Nothing in this presentation should be construed as a profit forecast.

3

Q4 and Full Year 2014 Results

Marc Dunoyer Finance

Pascal Soriot Overview

Pascal Soriot Closing

Luke Miels Growth platforms

Briggs Morrison Pipeline

• Q4 2014: 4th consecutive quarter of revenue growth; $6,683m, +2% (+3% excl. effect of US Branded Pharma Fee) • FY 2014: Growth platforms +15%; 53% of total revenue:

• Brilinta: +70% • Diabetes: +139% • Respiratory: +10% • Emerging Markets: +12%; China +22% • Japan: -3%

4

2014: Continued strategic progress

Growth rates at constant exchange rates (CER)

• Since Q3 2014: • Duaklir Genuair: Approval EU; lesinurad: Regulatory submission US, EU; brodalumab: Positive Phase IIIs • Saxa/dapa: Regulatory submission US; Brilinta: Positive PEGASUS Phase III • Lynparza: Approval US, EU; Iressa: Regulatory submission US • Moventig: Approval EU

Returning to growth

Achieving scientific leadership

5

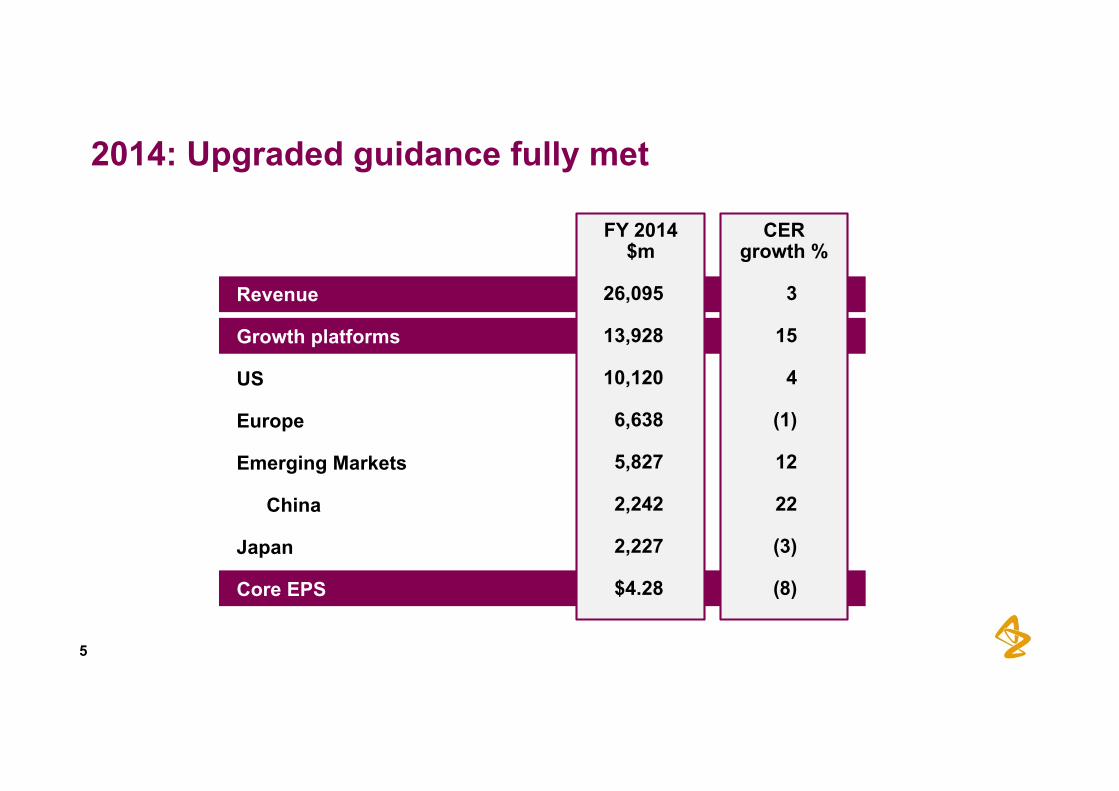

2014: Upgraded guidance fully met

Revenue Growth platforms

US Europe Emerging Markets

China Japan Core EPS

CER growth %

3

15

4

(1)

12

22

(3)

(8)

FY 2014 $m

26,095

13,928

10,120

6,638

5,827

2,242

2,227

$4.28

6

Strategic priorities

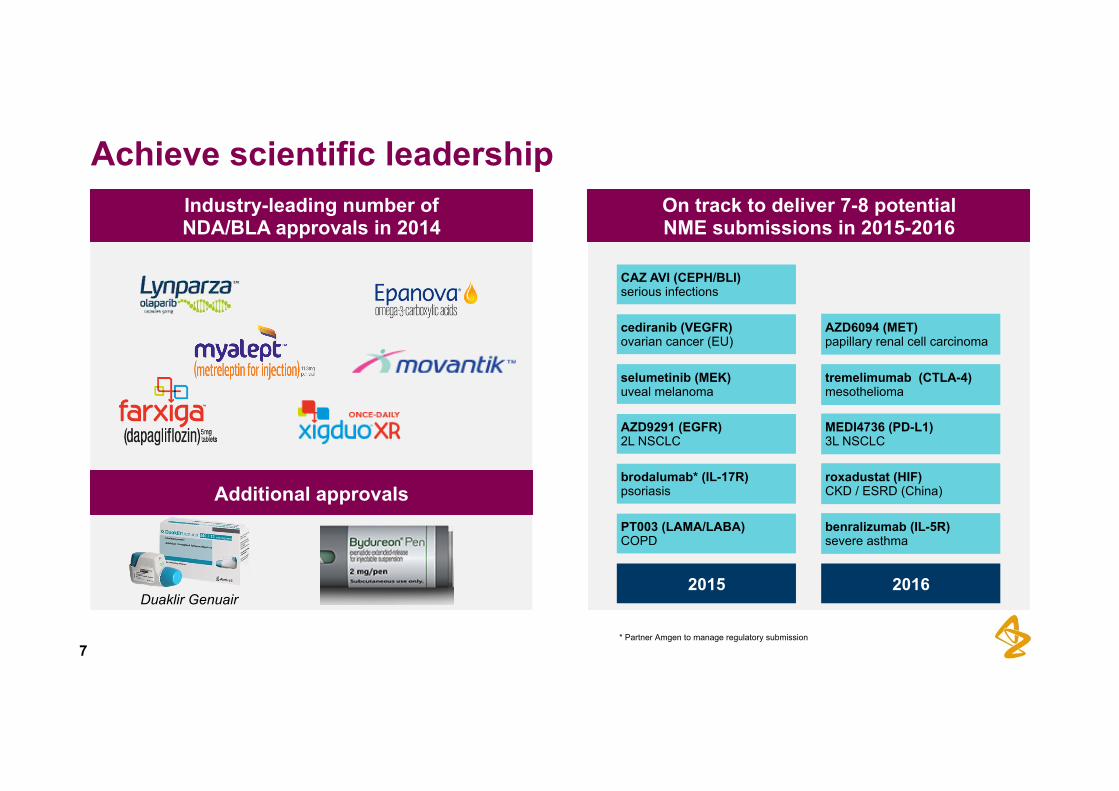

Achieve scientific leadership

1 Return to growth

2 Be a great place to work

3

7

Achieve scientific leadership

* Partner Amgen to manage regulatory submission

Industry-leading number of NDA/BLA approvals in 2014

On track to deliver 7-8 potential NME submissions in 2015-2016

Additional approvals

Duaklir Genuair

CAZ AVI (CEPH/BLI) serious infections

2015

PT003 (LAMA/LABA) COPD

brodalumab* (IL-17R) psoriasis

AZD9291 (EGFR) 2L NSCLC

selumetinib (MEK) uveal melanoma

cediranib (VEGFR) ovarian cancer (EU)

2016

roxadustat (HIF) CKD / ESRD (China)

benralizumab (IL-5R) severe asthma

AZD6094 (MET) papillary renal cell carcinoma

tremelimumab (CTLA-4) mesothelioma

MEDI4736 (PD-L1) 3L NSCLC

8

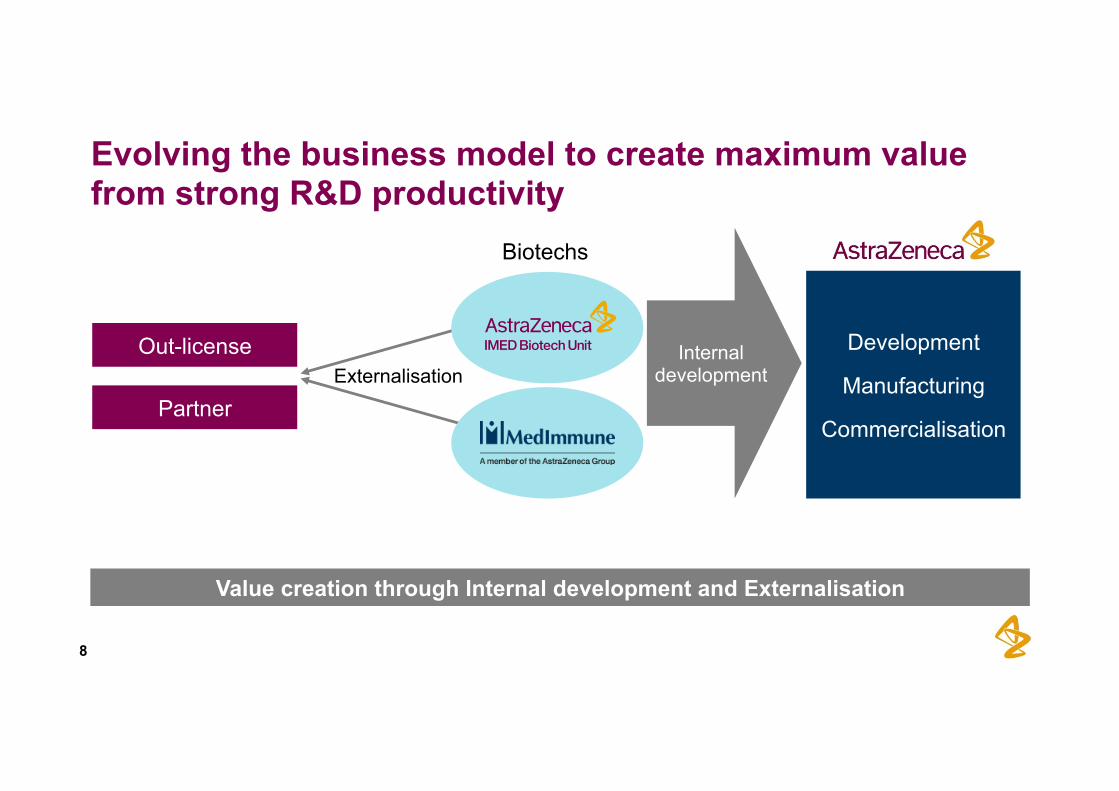

Evolving the business model to create maximum value from strong R&D productivity

Value creation through Internal development and Externalisation

Externalisation

Biotechs

Development

Manufacturing

Commercialisation

Out-license

Partner

Internal development

9

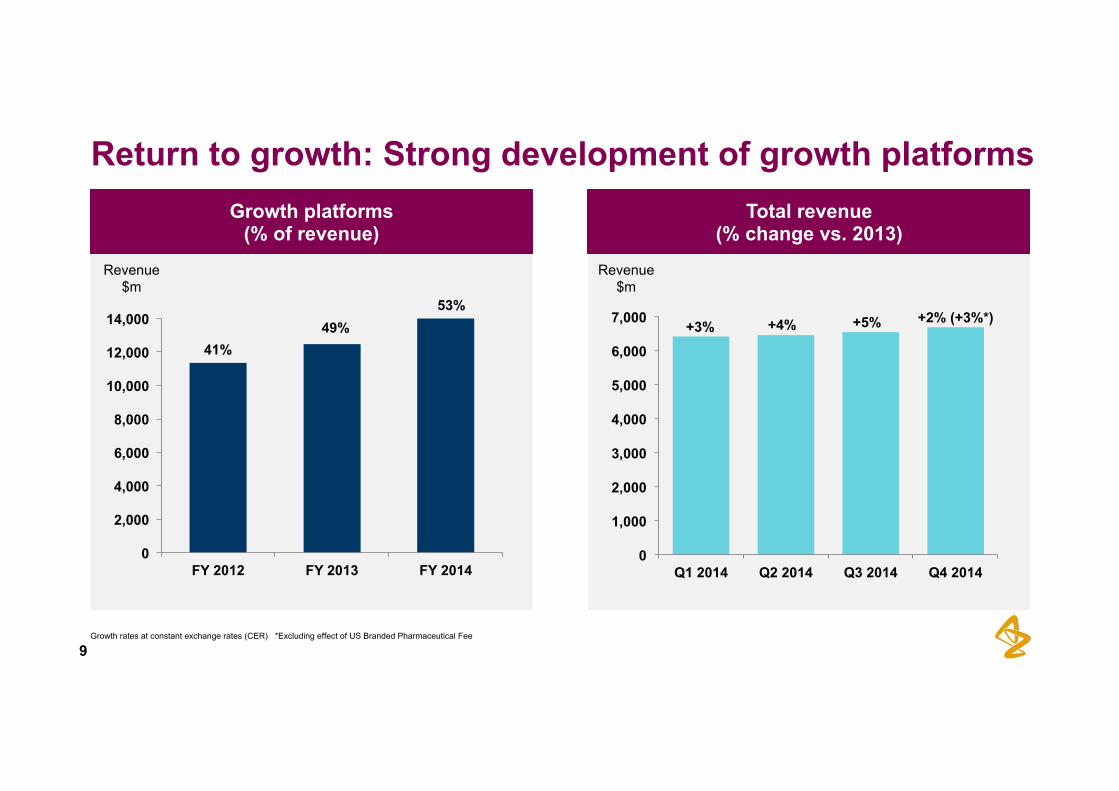

Return to growth: Strong development of growth platforms

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Q1 2014 Q2 2014 Q3 2014 Q4 2014

Revenue $m

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY 2012 FY 2013 FY 2014

41% 49%

Revenue $m

Growth platforms (% of revenue)

Total revenue (% change vs. 2013)

+3% +4% +5% +2% (+3%*) 53%

Growth rates at constant exchange rates (CER) *Excluding effect of US Branded Pharmaceutical Fee

Growth platforms

Luke Miels, EVP Global Portfolio & Product Strategy

11

Growth platforms: Strong delivery

$1,870m 139% Diabetes

$5,063m 10% Respiratory

$5,827m 12% Emerging Markets

$2,227m -3%* Japan

FY 2014 Growth

$476m 70% Brilinta

Oncology emerging as sixth growth platform

*Including impact from mandated price cuts Growth rates at constant exchange rates (CER)

12

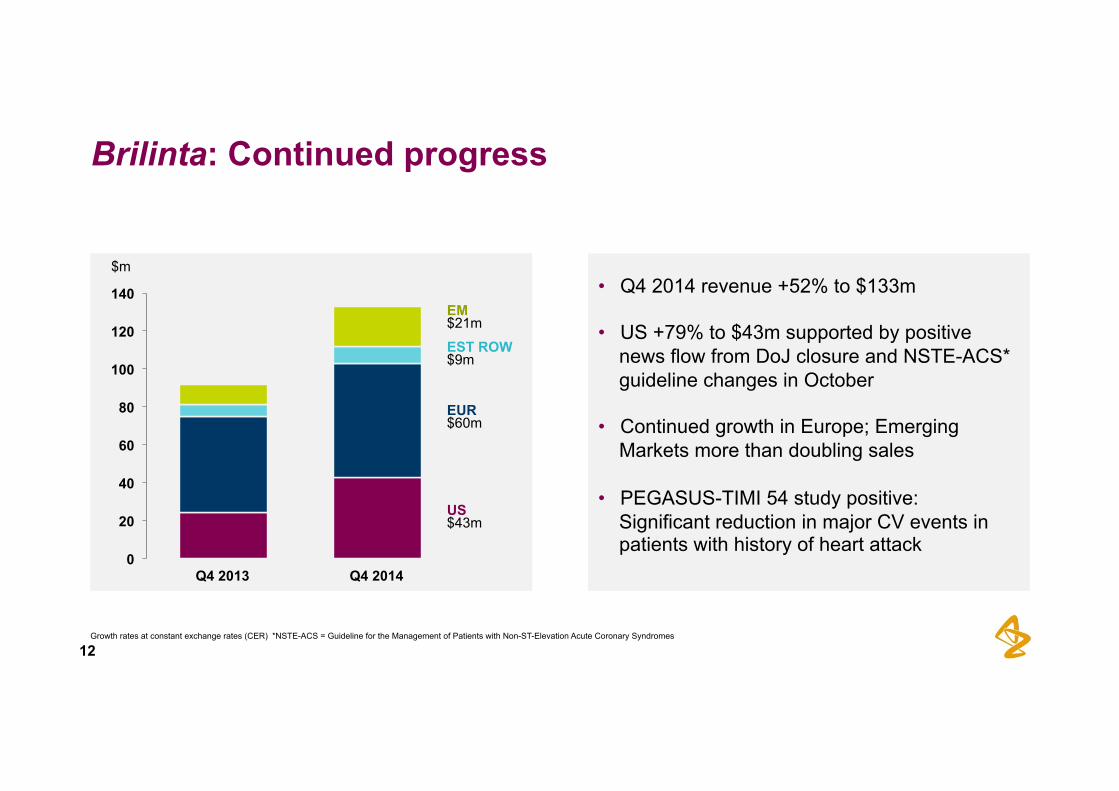

Brilinta: Continued progress

• Q4 2014 revenue +52% to $133m • US +79% to $43m supported by positive

news flow from DoJ closure and NSTE-ACS* guideline changes in October

• Continued growth in Europe; Emerging

Markets more than doubling sales • PEGASUS-TIMI 54 study positive:

Significant reduction in major CV events in patients with history of heart attack

0

20

40

60

80

100

120

140

Q4 2013

$m

Q4 2014

US $43m

EUR $60m

EST ROW $9m

EM $21m

*NSTE-ACS = Guideline for the Management of Patients with Non-ST-Elevation Acute Coronary Syndromes Growth rates at constant exchange rates (CER)

US hospital units purchased US oral anti-platelet class market shares (new-to-brand prescriptions NBRx)

Closure of DoJ Investigation

13

Brilinta: Steady increase in US

Source: IMS Health DDD (Defined Daily Dose) weekly (MMT: 4 week rolling average) through w/e Jan 9, 2015 Source: IMS Health NPA Weekly through w/e Jan 16, 2015

49,960

40,314

0

10,000

20,000

30,000

40,000

50,000

60,000

3-Ja

n-14

24-J

an-1

4

14-F

eb-1

4

7-M

ar-1

4

28-M

ar-1

4

18-A

pr-1

4

9-M

ay-1

4

30-M

ay-1

4

20-J

un-1

4

11-J

ul-1

4

1-A

ug-1

4

22-A

ug-1

4

12-S

ep-1

4

3-O

ct-1

4

24-O

ct-1

4

14-N

ov-1

4

5-D

ec-1

4

26-D

ec-1

4

Brilinta Competitor

7.57% 8.07%

0%

5%

10%

15%

05-J

ul-1

3 05

-Aug

-13

05-S

ep-1

3 05

-Oct

-13

05-N

ov-1

3 05

-Dec

-13

05-J

an-1

4 05

-Feb

-14

05-M

ar-1

4 05

-Apr

-14

05-M

ay-1

4 05

-Jun

-14

05-J

ul-1

4 05

-Aug

-14

05-S

ep-1

4 05

-Oct

-14

05-N

ov-1

4 05

-Dec

-14

05-J

an-1

5

2013 2014

Brilinta Competitor

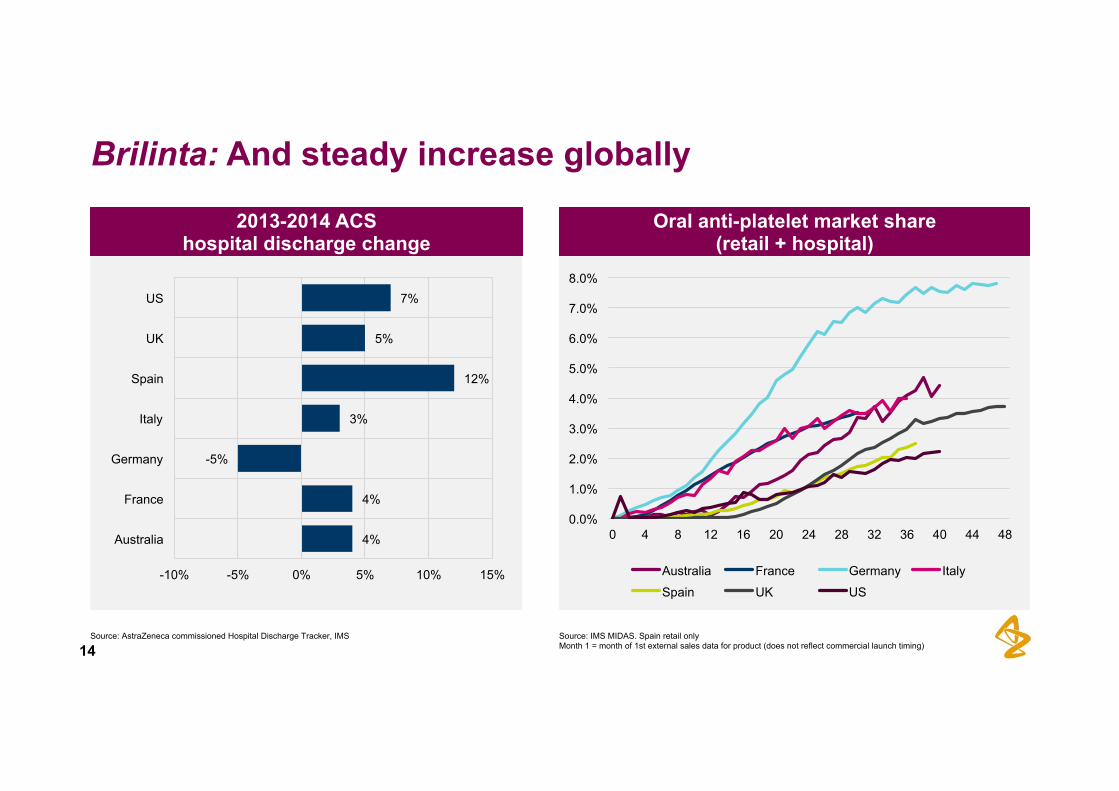

Oral anti-platelet market share (retail + hospital)

2013-2014 ACS hospital discharge change

14

Brilinta: And steady increase globally

4%

4%

-5%

3%

12%

5%

7%

-10% -5% 0% 5% 10% 15%

Australia

France

Germany

Italy

Spain

UK

US

Source: AstraZeneca commissioned Hospital Discharge Tracker, IMS Source: IMS MIDAS. Spain retail only Month 1 = month of 1st external sales data for product (does not reflect commercial launch timing)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0 4 8 12 16 20 24 28 32 36 40 44 48

Australia France Germany Italy

Spain UK US

15

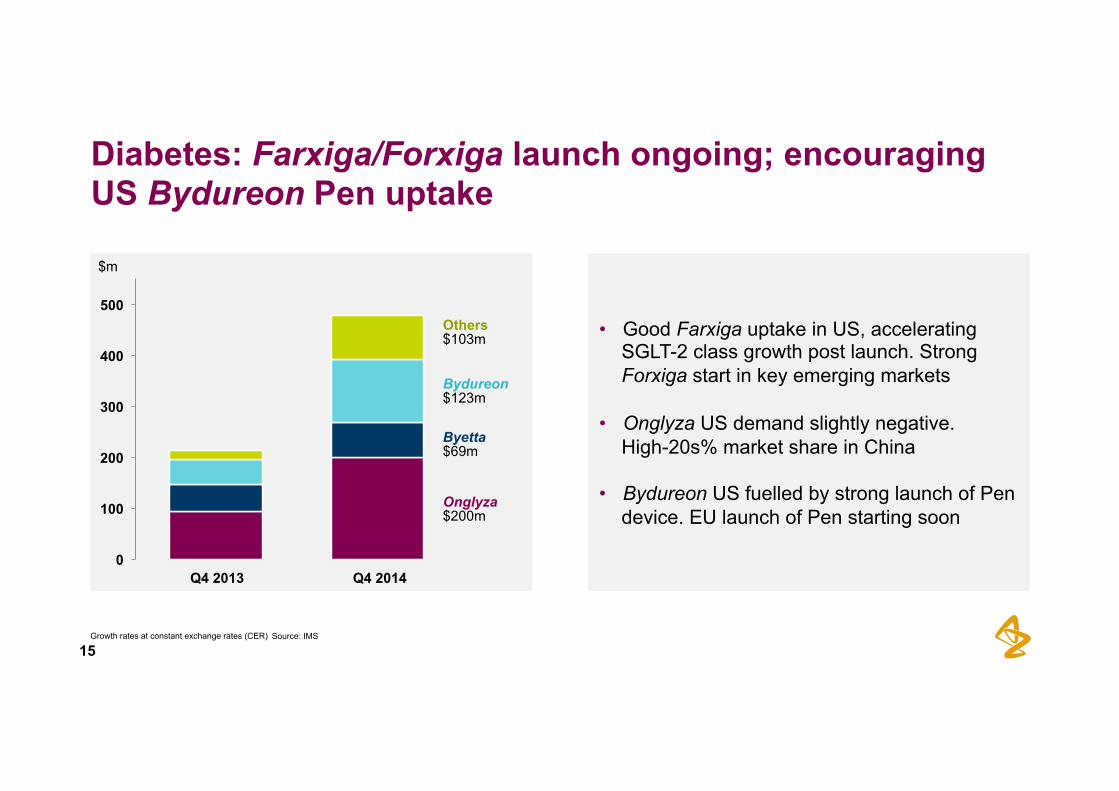

Diabetes: Farxiga/Forxiga launch ongoing; encouraging US Bydureon Pen uptake

• Good Farxiga uptake in US, accelerating SGLT-2 class growth post launch. Strong Forxiga start in key emerging markets

• Onglyza US demand slightly negative.

High-20s% market share in China • Bydureon US fuelled by strong launch of Pen

device. EU launch of Pen starting soon

0

100

200

300

400

500

Source: IMS

Q4 2013 Q4 2014

$m

Bydureon $123m

Others $103m

Onglyza $200m

Byetta $69m

Growth rates at constant exchange rates (CER)

US Farxiga volume (weekly prescriptions)

US SGLT-2 market (new monthly prescriptions NRx)

16

Farxiga: Continued US uptake; SGLT-2 market acceleration post launch

Source: TRx and NRX-NPA+7 (Retail, Mail & LTC), NBRx- IMS APLD (Retail and Mail) and IMS Health NPA, weekly through Jan 16, 2015. Monthly data through December, 2014

27,039

10,560

4,317

0

5,000

10,000

15,000

20,000

25,000

30,000

07-F

eb-1

4

28-F

eb-1

4

21-M

ar-1

4

11-A

pr-1

4

02-M

ay-1

4

23-M

ay-1

4

13-J

un-1

4

04-J

ul-1

4

25-J

ul-1

4

15-A

ug-1

4

05-S

ep-1

4

26-S

ep-1

4

17-O

ct-1

4

07-N

ov-1

4

28-N

ov-1

4

19-D

ec-1

4

09-J

an-1

5

TRx NRx NBRx

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

Apr

-13

May

-13

Jun-

13

Jul-1

3 A

ug-1

3 S

ep-1

3 O

ct-1

3 N

ov-1

3 D

ec-1

3 Ja

n-14

Fe

b-14

M

ar-1

4 A

pr-1

4 M

ay-1

4 Ju

n-14

Ju

l-14

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Farxiga launch – driving class growth

Farxiga/Forxiga launch uptake among innovative oral anti-diabetic medicines (SGLT-2 + DPP4)

M10 M20 M14 M18 M17 M16 M15 M9 M19 M7 M6 M5 M4 M8 M2 M1 M13 M12 M11 M3

Gulf Philippines South Korea Chile

Sweden Norway Argentina

Australia Mexico

UK Brazil

Germany USA

Source: IMS Midas Nov 2014 17

Forxiga: Strong start in key international markets

13 12 11 10

9 8 7 6 5 4 3 2 1 0

Mar

ket s

hare

day

s on

ther

apy

US Bydureon family share in GLP-1 market US Bydureon family (new monthly prescriptions NRx)

18

Bydureon: Strong US uptake of new Pen; EU launch next

20.7%

20.9%

33.0%

0%

5%

10%

15%

20%

25%

30%

35%

40%

May

-13

Jun-

13

Jul-1

3 A

ug-1

3 S

ep-1

3 O

ct-1

3 N

ov-1

3 D

ec-1

3 Ja

n-14

Fe

b-14

M

ar-1

4 A

pr-1

4 M

ay-1

4 Ju

n-14

Ju

l-14

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

TRx NRx NBRx

Chg Pen Launch

Chg vs Sep

Chg Vs Dec ‘13

TRx 0.9% 0.5% 3.5%

NRx 2.2% 1.0% 4.1%

NBRx 9.5% 3.7% 8.5%

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Bydureon Tray Bydureon Pen

Source: TRx and NRX-NPA+ (Retail, Mail & LTC), NBRx- IMS APLD (Retail & Mail Combined) Dec

19

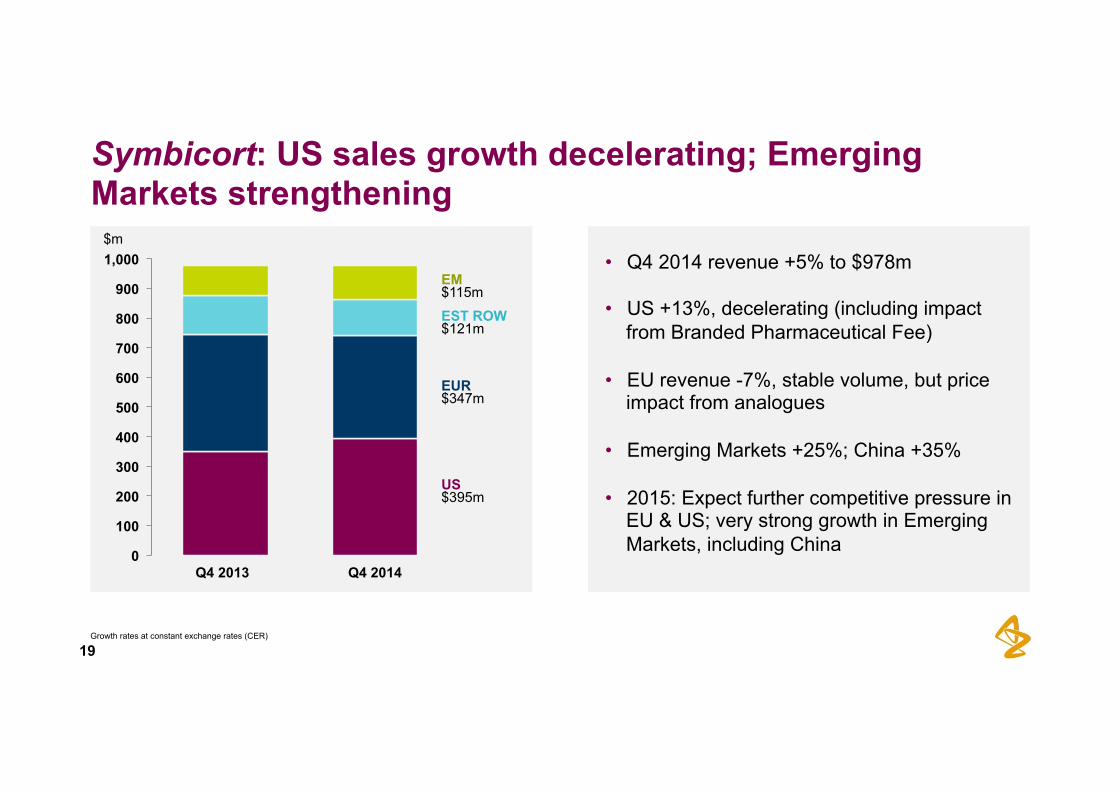

Symbicort: US sales growth decelerating; Emerging Markets strengthening

• Q4 2014 revenue +5% to $978m • US +13%, decelerating (including impact

from Branded Pharmaceutical Fee) • EU revenue -7%, stable volume, but price

impact from analogues • Emerging Markets +25%; China +35% • 2015: Expect further competitive pressure in

EU & US; very strong growth in Emerging Markets, including China

0

100

200

300

400

500

600

700

800

900

1,000

Q4 2013 Q4 2014

$m

EUR $347m

US $395m

EST ROW $121m

EM $115m

Growth rates at constant exchange rates (CER)

Emerging Markets: Continued strong growth

Q4 14

12%

Q3 14

9%

Q2 14

5%

Q1 14

5%

Q4 13

0%

Q3 13

2%

Q2 13

10%

Q1 13

3%

Q4 12

2%

Q3 12

1%

Q2 12

-2%

Q1 12

-3%

China

EMs outside China

Q4 14

19%

Q3 14

21%

Q2 14

23%

Q1 14

22%

Q4 13

21%

Q3 13

13%

Q2 13

21%

Q1 13

21%

Q4 12

20%

Q3 12

23%

Q2 12

12%

Q1 12

13%

+4% +8% -1%

20

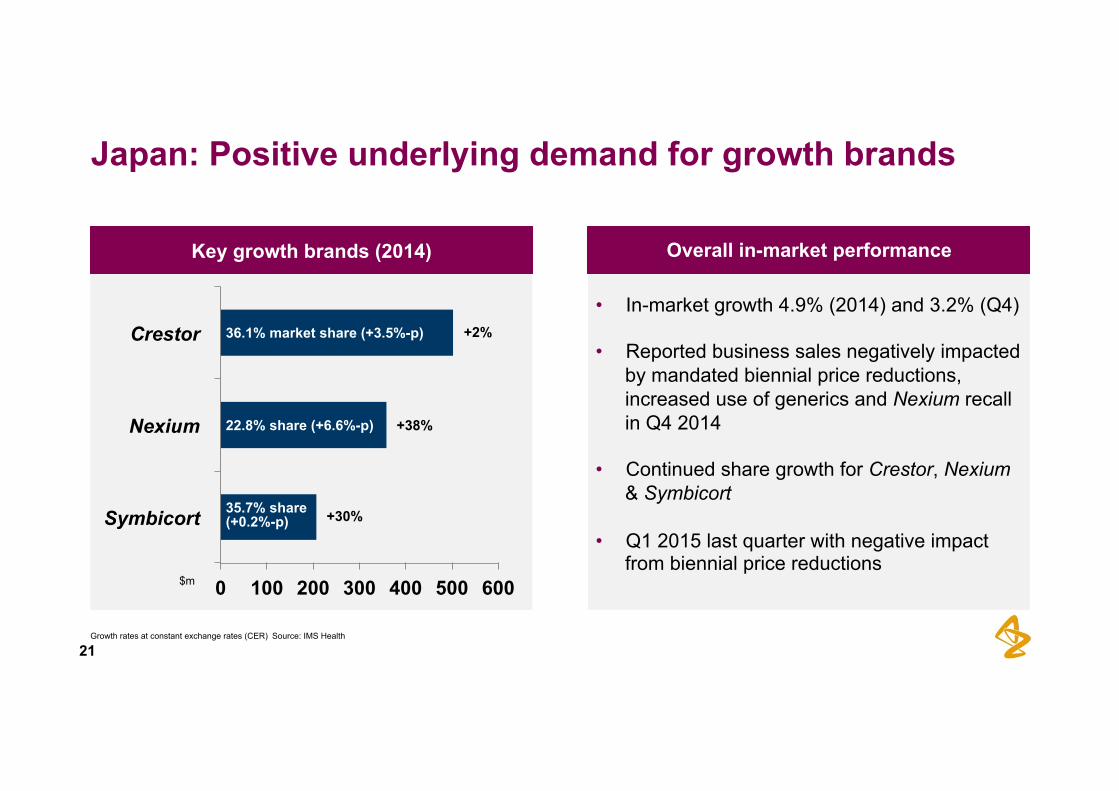

Growth rates at constant exchange rates (CER)

Key growth brands (2014)

• In-market growth 4.9% (2014) and 3.2% (Q4) • Reported business sales negatively impacted

by mandated biennial price reductions, increased use of generics and Nexium recall in Q4 2014

• Continued share growth for Crestor, Nexium

& Symbicort

• Q1 2015 last quarter with negative impact from biennial price reductions

Overall in-market performance

Japan: Positive underlying demand for growth brands

Source: IMS Health

$m 0 100 200 300 400 500 600

Symbicort

Nexium

Crestor 36.1% market share (+3.5%-p)

22.8% share (+6.6%-p)

35.7% share (+0.2%-p)

+2%

+38%

+30%

21

BRCA-mutated advanced ovarian cancer • US & EU (France 1st) launch in

December 2014 • Rapid uptake due to bolus of patients

awaiting treatment

Opioid-induced constipation • US launch expected H1 2015

following recent de-scheduling determination

• EU launch expected H2 2015

Launch products

22

Chronic obstructive pulmonary disease (COPD) • EU launch underway

Duaklir

Finance

Marc Dunoyer, Chief Financial Officer

• Profit & loss redeployment

• Balance sheet flexibility

• Create long-term shareholder value

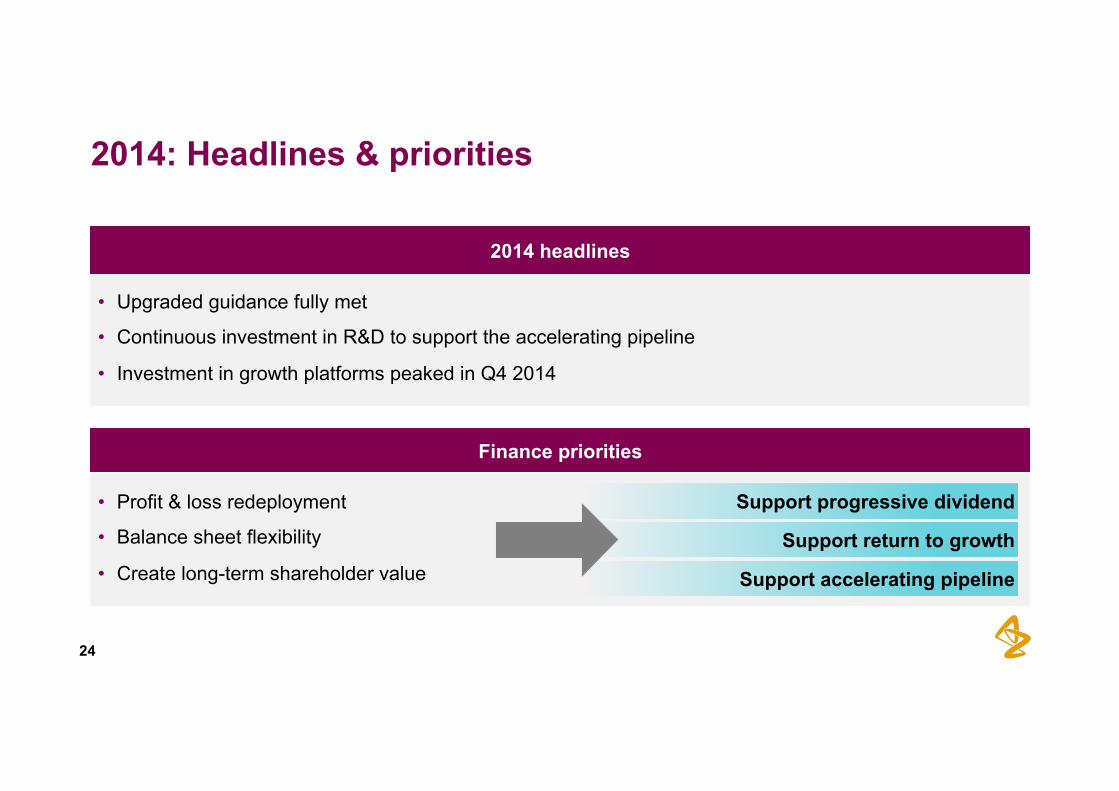

2014: Headlines & priorities

• Upgraded guidance fully met

• Continuous investment in R&D to support the accelerating pipeline

• Investment in growth platforms peaked in Q4 2014

Finance priorities

2014 headlines

Support progressive dividend

Support return to growth

Support accelerating pipeline

24

Has supported increased investment in: • Growth platforms, including Emerging Markets build-up • Unprecedented # of on-going/upcoming launches

2012 2014

$m

2012 2014

$m

Total IT costs Total facilities costs

-11% -8%

Profit & loss: Redeployment Core SG&A

68% 76%

32% 24%

2012 2014

G&A

SM&M

Structural change in SG&A due to redeployment of resources From fixed to more variable costs

Examples

25 SM&M: Sales, Marketing & Medical

Strategic flexibility to support progressive dividend, return to growth and accelerating pipeline

26

87

69

45

2012 2014

Cash conversion cycle (days) Debt & cash • Continue to target a strong, investment-grade

credit rating • Moody’s: A2 Stable outlook • Standard & Poor’s: AA- Negative outlook

• November 2014: 0.875% EUR 2021 medium-term notes (€750m); oversubscribed 4 times

• Cash and cash equivalents end-2014 $6.4bn • Net debt $3.2bn

Cash conversion calculated as DSO + DIO - DPO at the end of the year (in days) as a function of net sales

Balance sheet: Flexibility

Peer average

Q4 2014 considerations

Q4 2014 $m

Q4 2013 $m

CER Growth

% Factors

Revenue 6,683 6,844 2 +3% excluding US Branded Pharmaceutical Fee

Core R&D (1,360) (1,205) 17

Core SG&A (2,953) (2,483) 23

Core Operating Profit

1,184 1,983 (33)

27

R&D investment

• Pipeline progression/acceleration, e.g.: • Oncology immuno & small molecules • RIA biologics pipeline • Brilinta PARTHENON costs peaked

SG&A • Growth platforms; incl. Diabetes

integration • On-going launches

– Farxiga/Forxiga (US, EU, EMs), Bydureon Pen (US)

• Pre-launch activities – Lynparza – Movantik/Moventig

• Almirall integration Opportunistic investment in Q4 2014

28

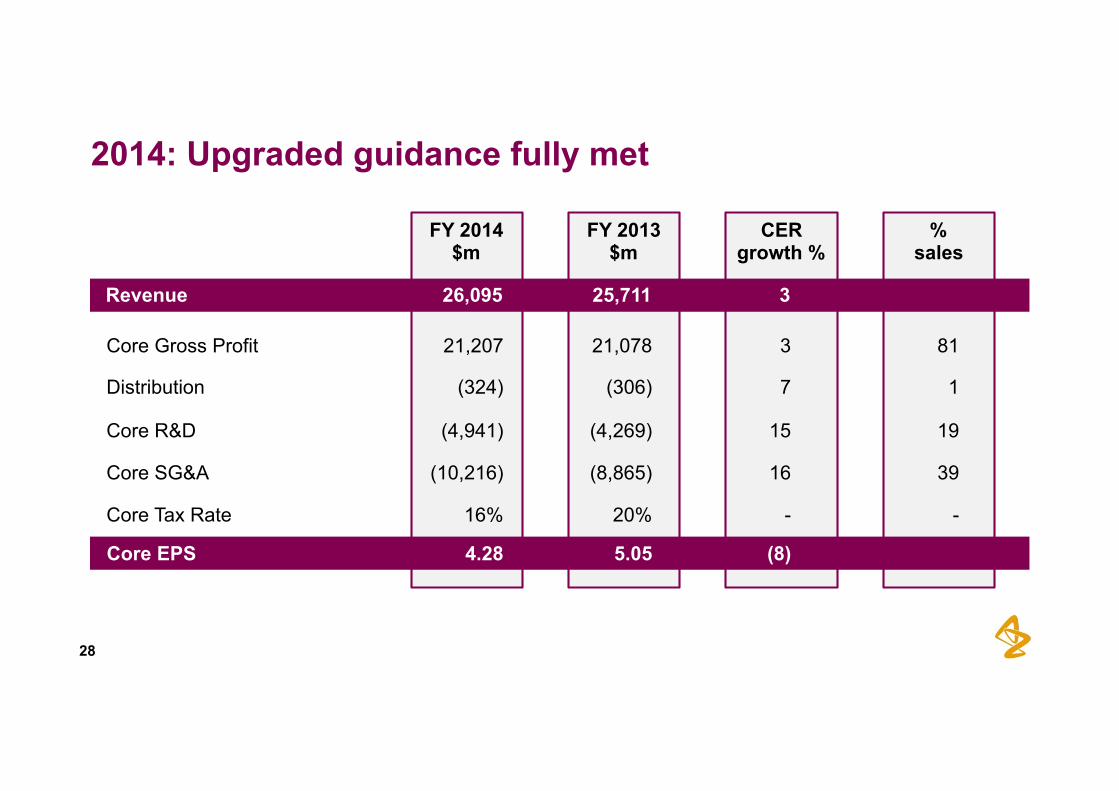

2014: Upgraded guidance fully met

Revenue 26,095 25,711 3

FY 2014 $m

CER growth %

% sales

Core Gross Profit 21,207 21,078 3 81

Distribution (324) (306) 7 1

Core R&D (4,941) (4,269) 15 19

Core SG&A (10,216) (8,865) 16 39

Core Tax Rate 16% 20% - -

FY 2013 $m

Core EPS 4.28 5.05 (8)

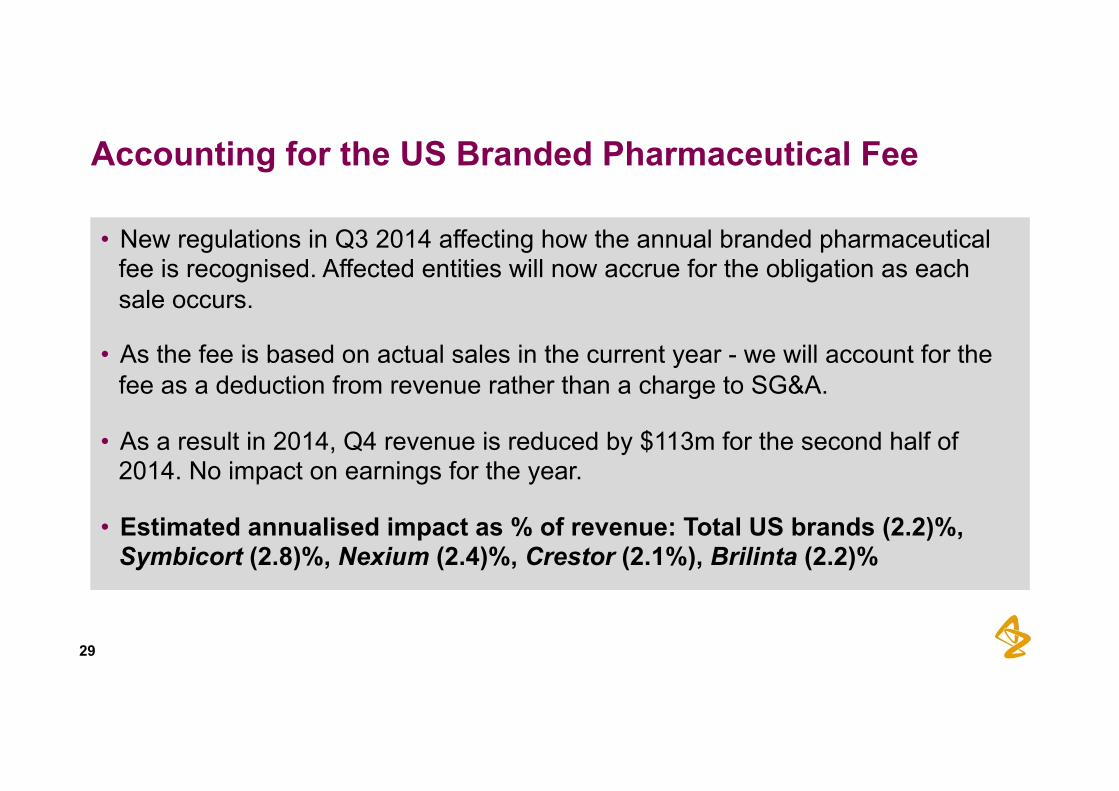

Accounting for the US Branded Pharmaceutical Fee

• New regulations in Q3 2014 affecting how the annual branded pharmaceutical fee is recognised. Affected entities will now accrue for the obligation as each sale occurs.

• As the fee is based on actual sales in the current year - we will account for the fee as a deduction from revenue rather than a charge to SG&A.

• As a result in 2014, Q4 revenue is reduced by $113m for the second half of 2014. No impact on earnings for the year.

• Estimated annualised impact as % of revenue: Total US brands (2.2)%, Symbicort (2.8)%, Nexium (2.4)%, Crestor (2.1%), Brilinta (2.2)%

29

30

2015 guidance

Sales revenue1

Core EPS

Decline by mid single-digit percent

Increase by low single-digit percent

Constant exchange rates

1 Assumes imminent launch of a Nexium generic in the US market

31

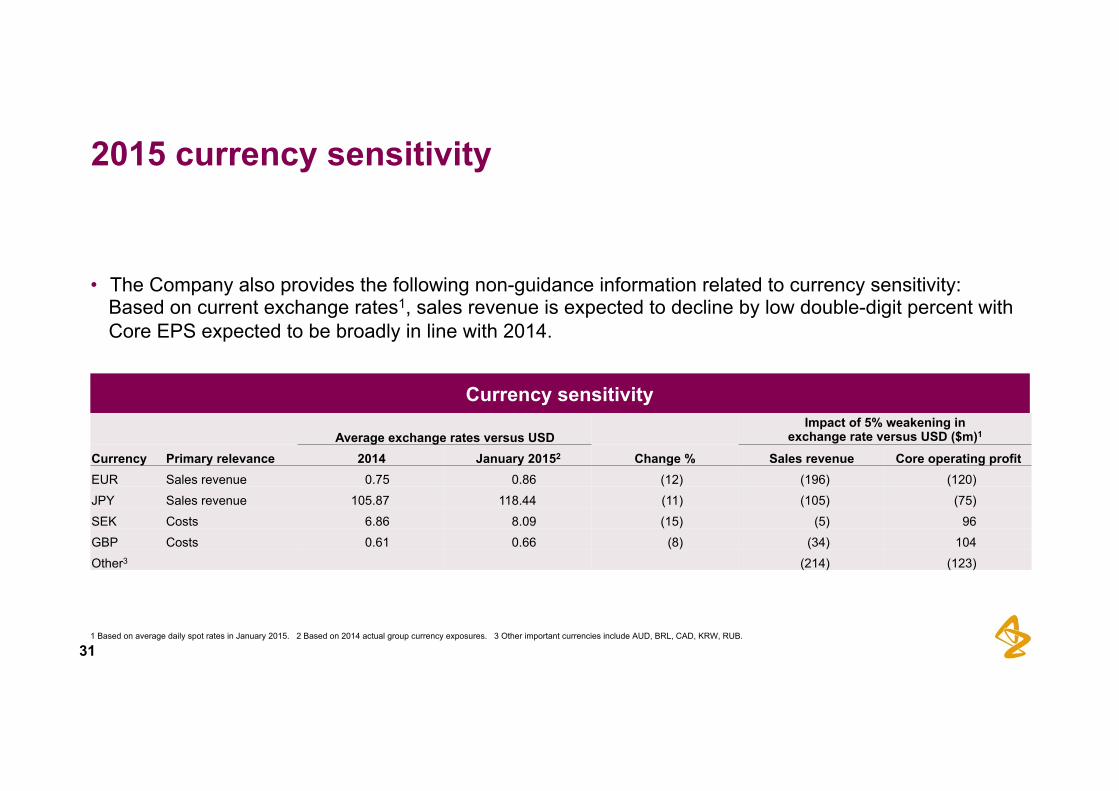

2015 currency sensitivity

• The Company also provides the following non-guidance information related to currency sensitivity: Based on current exchange rates1, sales revenue is expected to decline by low double-digit percent with Core EPS expected to be broadly in line with 2014.

Currency sensitivity

Average exchange rates versus USD Impact of 5% weakening in

exchange rate versus USD ($m)1

Currency Primary relevance 2014 January 20152 Change % Sales revenue Core operating profit EUR Sales revenue 0.75 0.86 (12) (196) (120) JPY Sales revenue 105.87 118.44 (11) (105) (75) SEK Costs 6.86 8.09 (15) (5) 96 GBP Costs 0.61 0.66 (8) (34) 104 Other3 (214) (123)

1 Based on average daily spot rates in January 2015. 2 Based on 2014 actual group currency exposures. 3 Other important currencies include AUD, BRL, CAD, KRW, RUB.

NGM

Pearl Triple combination LABA/LAMA/ICS

Respiratory

• Strengthened diabetes portfolio and commitment to main therapeutic areas

• Myalept divestment reinforced focus on main strategic priorities; allows for redeployment of resources

• Strengthened inhaled portfolio in asthma and COPD

• SNG001: Novel, inhaled interferon beta in clinical development for severe asthma

• Strategic partnerships / acquisitions strengthened Oncology portfolio, particularly immuno-oncology-combination therapies, novel predictive biomarkers

32

2014: Targeted business development in main areas

Respiratory, Inflammation & Autoimmunity

Cardiovascular & Metabolic Disease Oncology

33

Respiratory: Actavis deal strengthens franchise

• Strategic deal to add US rights to Europe & ROW aclidinium franchise acquired from Almirall in 2014, including Tudorza (LAMA) and Pressair DPI device

• Augments the Respiratory franchise with Actavis product, Daliresp (oral PDE4 inhibitor for COPD)

• Access to on-market revenues, near-term growth and future potential of LAMA combination products

• Targeted investment in main therapy area: $600m initial consideration and low single-digit royalties above a certain revenue threshold

• Additional $100m payment regarding the settlement of a number of contractual consents and approvals

Increases focus on the Respiratory growth platform

Expands geographic presence

Broadens product and device offering

Pipeline

Briggs Morrison, EVP Global Medicines Development

Improve the lives of 200 million patients…one patient at a time

Outstanding year • Industry-leading 6 NDA/BLA approvals • Excellent pipeline progress • Focusing R&D spend on main therapeutic

areas

2014: An outstanding year

35

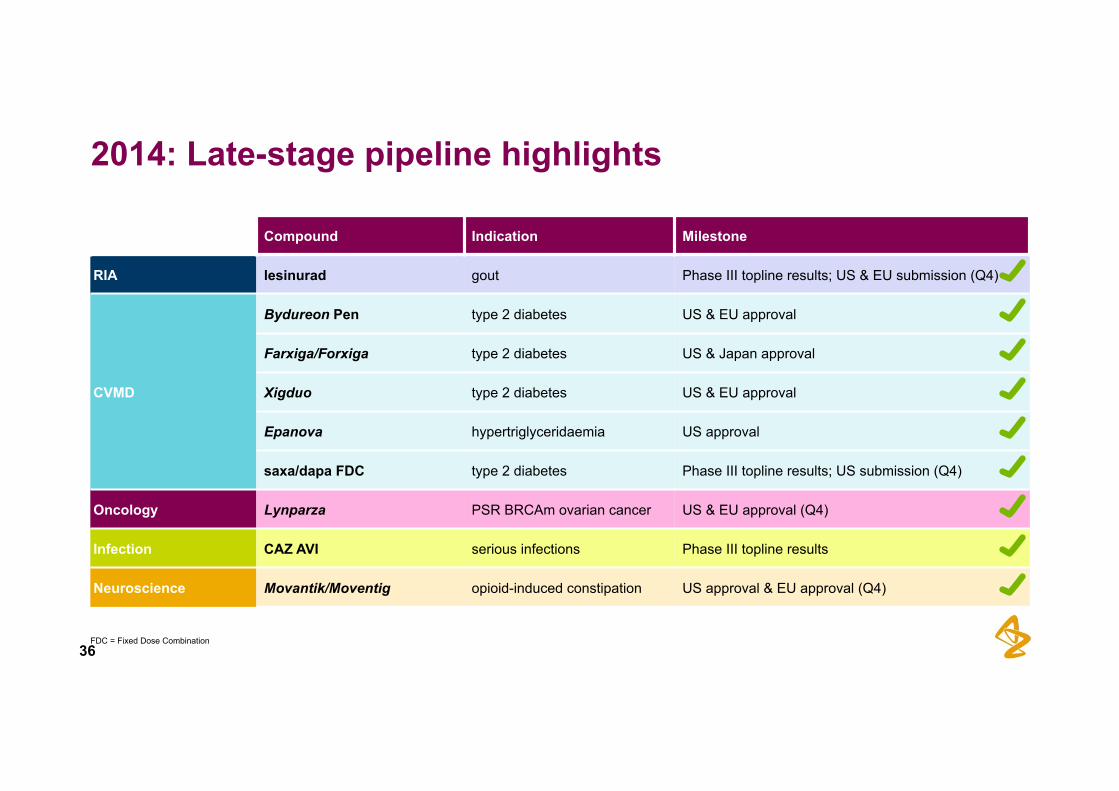

2014: Late-stage pipeline highlights

Compound Indication Milestone

RIA lesinurad gout Phase III topline results; US & EU submission (Q4)

CVMD

Bydureon Pen type 2 diabetes US & EU approval

Farxiga/Forxiga type 2 diabetes US & Japan approval

Xigduo type 2 diabetes US & EU approval

Epanova hypertriglyceridaemia US approval

saxa/dapa FDC type 2 diabetes Phase III topline results; US submission (Q4)

Oncology Lynparza PSR BRCAm ovarian cancer US & EU approval (Q4)

Infection CAZ AVI serious infections Phase III topline results

Neuroscience Movantik/Moventig opioid-induced constipation US approval & EU approval (Q4)

36 FDC = Fixed Dose Combination

37

Recent highlights: Respiratory, Inflammation & Autoimmunity (RIA)

Sifalimumab (Phase IIb in lupus/SLE)

• Key endpoints met

Mavrilimumab (Phase IIb rheumatoid arthritis) • Key endpoints met; no apparent safety signals

Lesinurad (Phase III gout)

• Key endpoints met; comparable AE profile in lesinurad 200mg + allopurinol vs. allopurinol alone

• Regulatory submissions US, EU (accepted)

• First Phase III trial for the treatment of mild asthma

• Potential for improved disease control with flexible as-needed regimen as compared to rescue inhaler

ACR (November 2014) Symbicort SYGMA study started

38

Recent highlights: Cardiovascular & Metabolic Disease (CVMD)

Saxa/dapa • Regulatory submission: US Q4 2014, EU expected

Q2 2015

Farxiga/Forxiga for Type 1 diabetes

• Phase III programme initiated Q4 2014

Epanova

• STRENGTH long-term outcomes trial initiated Q4 2014

• PEGASUS: Statistically significant reduction in major CV events in patients with history of heart attack

• Expect presentation at ACC in March 2015

• Ongoing PARTHENON programme - SOCRATES (ischaemic stroke/TIA), EUCLID (PAD), THEMIS (CAD & T2D)

• One CV outcomes study each year 2015-2017

Diabetes Brilinta

39

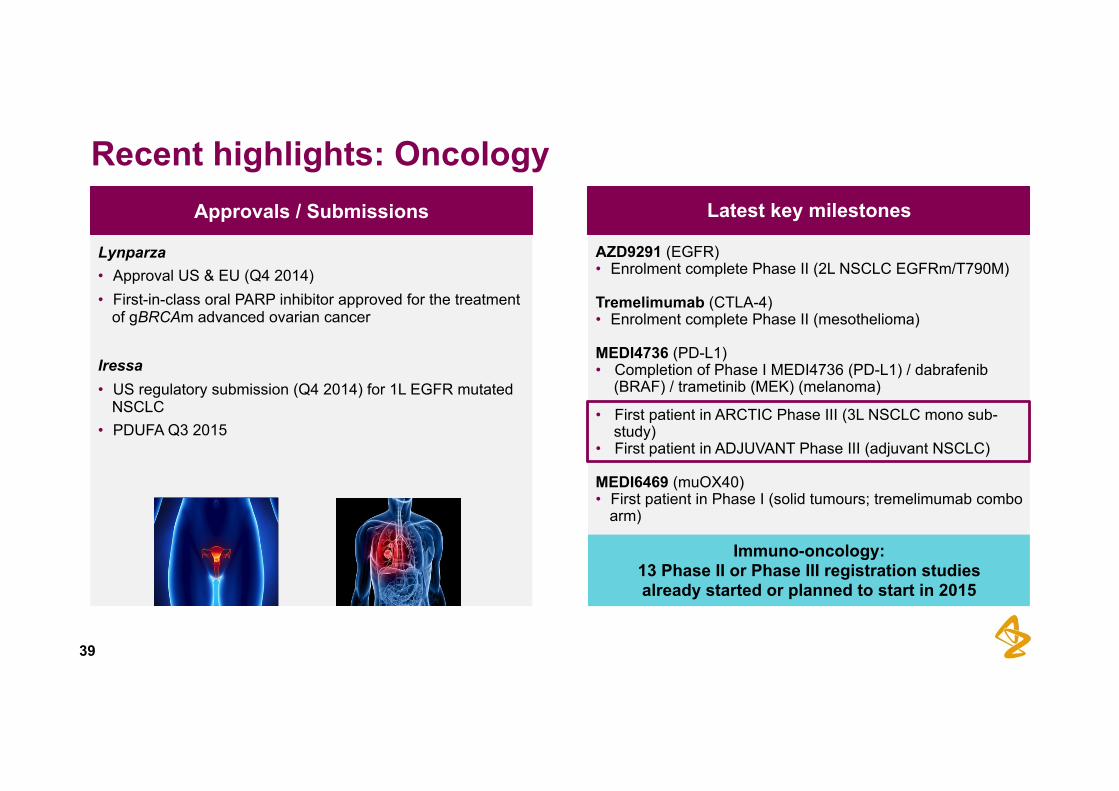

Recent highlights: Oncology

Lynparza • Approval US & EU (Q4 2014) • First-in-class oral PARP inhibitor approved for the treatment

of gBRCAm advanced ovarian cancer Iressa • US regulatory submission (Q4 2014) for 1L EGFR mutated

NSCLC • PDUFA Q3 2015

AZD9291 (EGFR) • Enrolment complete Phase II (2L NSCLC EGFRm/T790M) Tremelimumab (CTLA-4) • Enrolment complete Phase II (mesothelioma) MEDI4736 (PD-L1) • Completion of Phase I MEDI4736 (PD-L1) / dabrafenib

(BRAF) / trametinib (MEK) (melanoma) • First patient in ARCTIC Phase III (3L NSCLC mono sub-

study) • First patient in ADJUVANT Phase III (adjuvant NSCLC) MEDI6469 (muOX40) • First patient in Phase I (solid tumours; tremelimumab combo

arm)

Approvals / Submissions Latest key milestones

Immuno-oncology: 13 Phase II or Phase III registration studies already started or planned to start in 2015

Late-stage pipeline: Key news flow through 2015 Compound Indication Potential milestone

RIA

brodalumab1 psoriasis Regulatory submission

PT003 (LAMA/LABA) COPD Phase III results & regulatory submission

anifrolumab lupus/SLE Phase II presentation

lesinurad gout Regulatory submission

CVMD Brilinta prior MI (PEGASUS) Phase III results

saxa/dapa FDC type 2 diabetes Regulatory submission

Oncology

Lynparza PSR BRCAm ovarian cancer Approval Phase III topline results (SOLO-2)

AZD9291 2nd line NSCLC Regulatory submission

MEDI4736 (PD-L1) 3rd line NSCLC Phase II/potential registration topline results

MEDI4736 (PD-L1) / tremelimumab NSCLC Phase I presentation (ASCO)

cediranib ovarian cancer Further analysis (ICON6); EU regulatory submission

selumetinib uveal melanoma Phase III results & regulatory submission

Neuroscience Movantik/Moventig opioid-induced constipation EU approval, US de-scheduling US launch

40

New2

1 Partner Amgen to manage regulatory submission 2 New disclosure since Investor Day November 2014

(US)

41

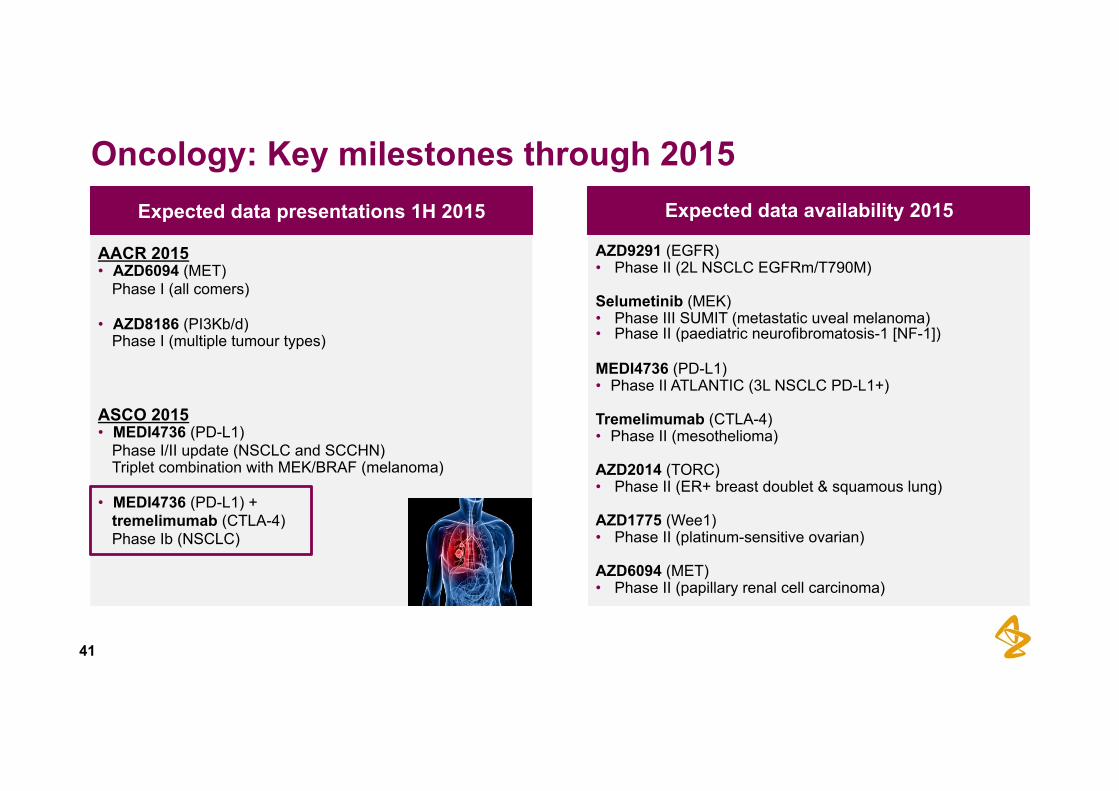

Oncology: Key milestones through 2015

AACR 2015 • AZD6094 (MET)

Phase I (all comers) • AZD8186 (PI3Kb/d)

Phase I (multiple tumour types) ASCO 2015 • MEDI4736 (PD-L1)

Phase I/II update (NSCLC and SCCHN) Triplet combination with MEK/BRAF (melanoma)

• MEDI4736 (PD-L1) +

tremelimumab (CTLA-4) Phase Ib (NSCLC)

AZD9291 (EGFR) • Phase II (2L NSCLC EGFRm/T790M) Selumetinib (MEK) • Phase III SUMIT (metastatic uveal melanoma) • Phase II (paediatric neurofibromatosis-1 [NF-1]) MEDI4736 (PD-L1) • Phase II ATLANTIC (3L NSCLC PD-L1+) Tremelimumab (CTLA-4) • Phase II (mesothelioma) AZD2014 (TORC) • Phase II (ER+ breast doublet & squamous lung) AZD1775 (Wee1) • Phase II (platinum-sensitive ovarian) AZD6094 (MET) • Phase II (papillary renal cell carcinoma)

Expected data presentations 1H 2015 Expected data availability 2015

Closing

Pascal Soriot, Chief Executive Officer

43

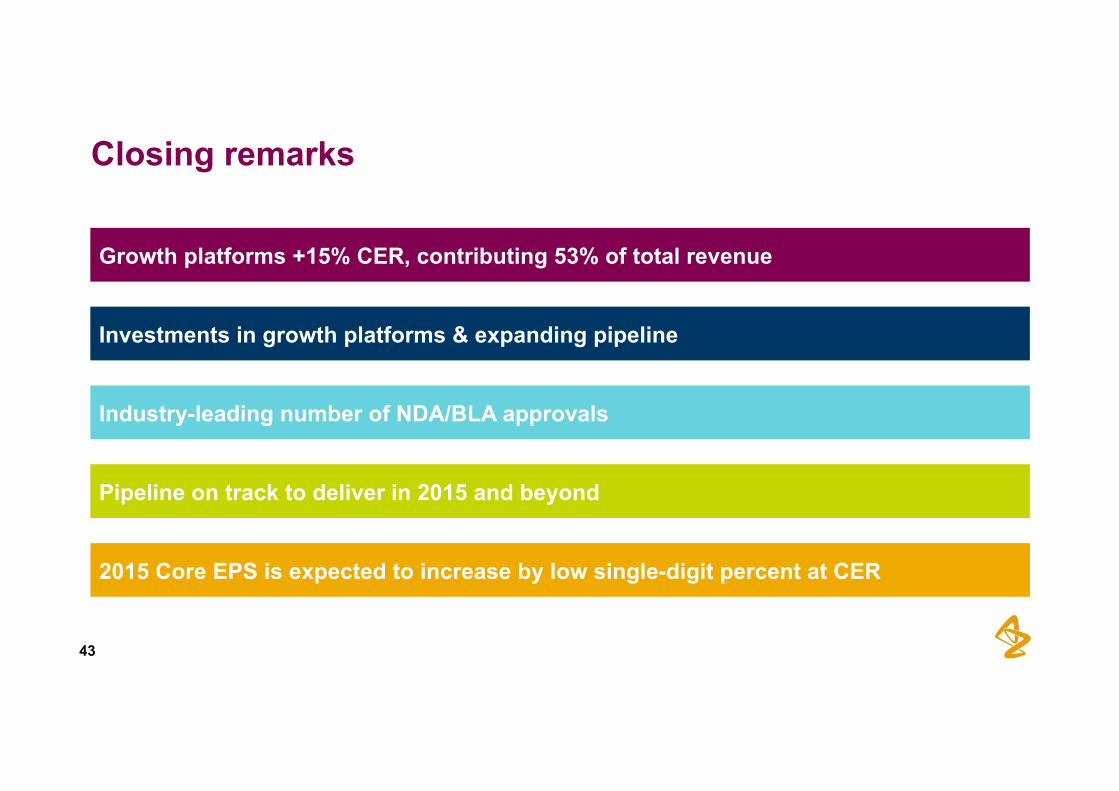

Closing remarks

Growth platforms +15% CER, contributing 53% of total revenue

Investments in growth platforms & expanding pipeline

Industry-leading number of NDA/BLA approvals

Pipeline on track to deliver in 2015 and beyond

2015 Core EPS is expected to increase by low single-digit percent at CER

Q&A

Pascal Soriot, Chief Executive Officer Marc Dunoyer, Chief Financial Officer Briggs Morrison, EVP Global Medicines Development Luke Miels, EVP Global Portfolio & Product Strategy