ASSOCIATION OF DEVELOPMENT FOR ECONOMIC SOCIAL HELP … · WASO Credit Rating Company (BO) Ltd....

14

WASO Credit Rating Company (BD) Limited Promoting Global Risk Management Practices at National Level ASSOCIATION OF DEVELOPMENT FOR ECONOMIC & SOCIAL HELP (ADESH) Credit Rating Report

Transcript of ASSOCIATION OF DEVELOPMENT FOR ECONOMIC SOCIAL HELP … · WASO Credit Rating Company (BO) Ltd....

WASO Credit Rating Company (BD) Limited Promoting Global Risk Management Practices at National Level

ASSOCIATION OF DEVELOPMENT FOR

ECONOMIC & SOCIAL HELP (ADESH)

Credit Rating Report

Page 1

Abdul '.Vadud FIES, MBA l'.1anasing 01ractor

· :..so Crcd: R~ 19 C-:r.-::a~:1 51:1) Ltd.

WCRCL also viewed the organization with "Stable" outlook and believes that ADESH will be able to maintain its good fundamentals in the foreseeable future.

The long term rating implies that the MFI rated in this category is subject to medium credit risk. It is considered medium grade and as such may possess certain speculative characteristics. The obligor currently has the capacity to meet its financial commitment on the obligation; however, it faces major ongoing uncertainties which could lead to the obliger's inadequate capacity to meet its financial commitment on the obligation.

The above ratings have been assigned based on the fundamentals of the organization which include long track record of operation, good baking relationship, diversified loan portfolio, moderate spread between cost and benefit of fund, and net surplus from operation. However, the above factors are constrained lack of geographical diversification, stagnant savings, lower loan loss provision expenses, highly levered organization, and poor risk coverage ratio.

Methodology: Corporate raring methodology published on the WCRa webs/re or www.wasocredltratinq.com

Financial Based on- Audired Financial Staremenrs up re 30 June 2018.

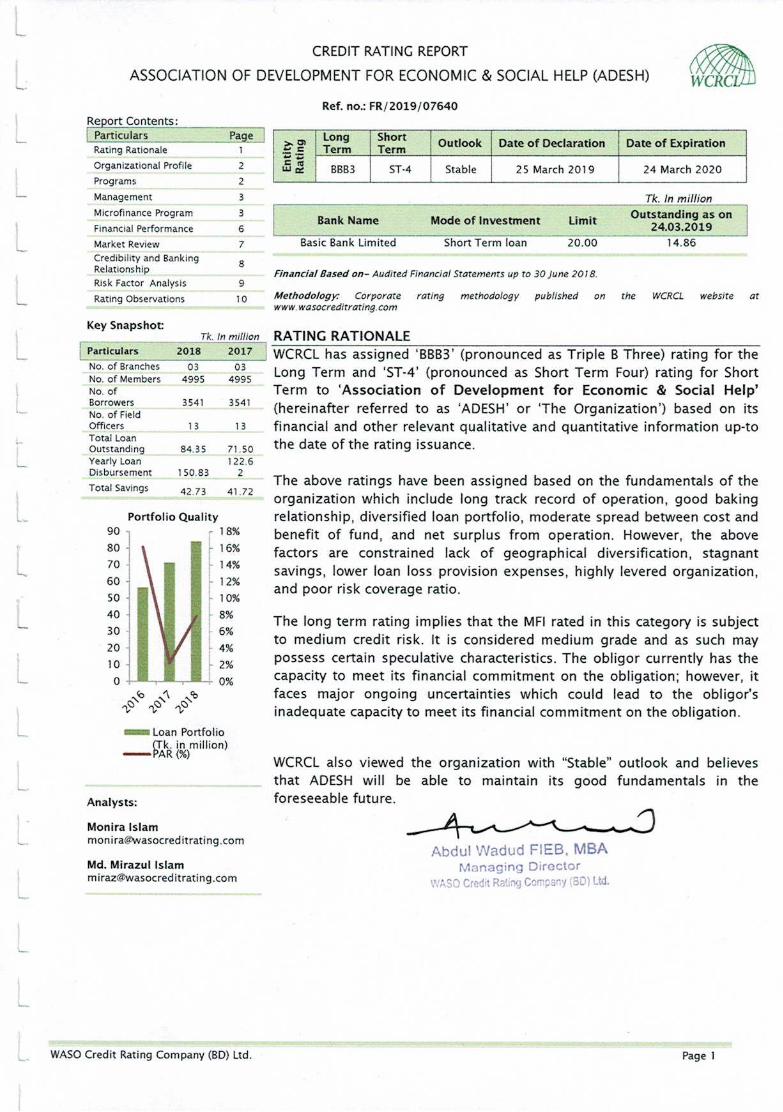

14.86 20.00 Short Term loan Basic Bank Limited

limit Mode of Investment Outstanding as on 24.03.2019 Bank Name

Tk. In million

>.OI long Short Outlook Date of Declaration Date of Expiration .... c Term Term -- c fa 8883 ST-4 Stable 25 March 2019 24 March 2020 Wa:

Ref. no.: FR/2019/07640

WASO Credit Rating Company (SD) Ltd.

Md. Mirazul Islam [email protected]

Monira Islam [email protected]

Analysts:

- Loan Portfolio (Tk. in million)

-PAR(%)

~ 10%

8% 6% 4% 2%

~--- ................... 0%

~~ 1· 40 30 20

I 0 1 0

Portfolio Quality 90 ., ~ 18% 80 ~ ~ 16% 70 14%

~ 12%

41.72

·-

L

......

Re2ort Contents: I Particulars Pa~

Rating Rationale 1

Organizational Profile 2 Programs 2

Management 3 Mlcrofinance Program 3 Financial Performance 6 Market Review 7 Credibility and Banking

8 Relationship Rlsk Factor Analysis 9 Rating Observations 10

Key Snapshot: _____ rk ..... _,.1n_m_,.11_11o"'"'n_, RATING RATIONALE

[Pa~rs 201s 2017 I WCRCL has assigned 'BBB3' (pronounced as Triple B Three) rating for the ~:: :~~;:~e~~ 4~!5 4~!s Long Term and 'ST-4' (pronounced as Short Term Four) rating for Short No. of Term to 'Association of Development for Economic & Social Help' ~~r~7;~1d 3541 3541 (hereinafter referred to as 'ADESH' or 'The Organization') based on its Officers i s 13 financial and other relevant qualitative and quantitative information up-to Total Loan outstanding 84.35 71.50 the date of the rating issuance. Yearly Loan 122.6 Disbursement 1 50.83 2 Total Savings 42 73

CREDIT RATING REPORT

ASSOCIATION OF DEVELOPMENT FOR ECONOMIC & SOCIAL HELP (ADESH)

Page 2 WASO Credit Rating Company (BO) Ltd.

Executive Committee (EC) This is the second layer of the management and is involved with carrying on the strategies and decisions taken by the GC. By the .A-7/

The GC is involved with electing the executive committee of the organization. This committee is also involved with approving the annual works, amending the organizational constitution, approving the annual budgets, formulating future work strategies, and all other relevant decision making.

CC consists of 31 members, who combined takes strategic decisions

General Committee (GC) The supreme authority of ADESH is its Governing Committee. The GC of the organization is comprised of 31 (Thirty one) members all of whom are from different professions. The professions of the members are mainly private jobs, teacher, social activists, and business.

The management team of Association of Development for Economic & Social Help (ADESH) is divided into two committees, which are: the

Two layers of management General Committee (GC) and the Executive Committee (EC). General Committee is the highest authoritative body of the organization. The GC is supported by the Executive Committee, which is involved with executing all the decisions and strategies taken by the GC.

MANAGEMENT

The head office of the organization is located at House-'PRIYA', 5/2, Block-C, Anandapur City lane, Savar, Dhaka-I 340. The organization operates in seven unions of Savar Upazila under Dhaka District.

The organization is managed by two layers of management. The top layer is the General Committee that consists of 31 (Thirty one) members. All the members of the committee are well educated and are from different professions. This committee is engaged in formulating different policies for the organization. On the other hand, this committee is supported by the second layer of management, the Executive Committee (EC). This committee carries out all the decisions and strategies formulated by the GC.

ADESH visualize its organized women groups to actively participate in the micro-finance activities and take loan at a reasonable interest to invest in any financially sound and profitable enterprise to change their social and economic life.

Association of Development for Economic & Social Help (hereinafter referred to as 'ADESH' or 'The Organization') is a local non government, non-political, voluntary organization, which is involved with development of socio-economic condition of the peoples of Savar,

Operational since 1988 Dhaka. The organization was established on 16 December 1988. The organization got registered with NGO Affairs on 03 February 1992 with registration number of DSS/FDO-R-595. Subsequently, the organization got registered with Registered with the Directorate of Social welfare Services on 03 March 1991 with registration number DH-02552. Since 2007, the organization has been registered with Microcredit Regulatory Authority (MRA) under registration number of 00091- 00396-00079. ADESH has a vision to poverty eradication of the distressed and exploited people, especially the women is the vision of ADESH micro finance program with ultimate goal to empower them in socio-economic life.

ORGANIZATIONAL PROFILE

CREDIT RATING REPORT ~ ASSOCIATION OF DEVELOPMENT FOR ECONOMIC & SOCIAL HELP Wc~f!/ffJ

(AD ESH)

Page 3 WASO Credit Rating Company (BO) ltd. L

As on 30 June 2018, the organization had 3 branches and total 4,995 members. The number of members are stable during the year. The number of borrowers, on the other hand, on that point-in-time was 3,541, which was stable from the preceding year. Total number of staffs employed has also been stable gradually over the years. Similarly, total savings increasing by 2.43% to Tk. 42.73 million. Although loan disbursement during the year increased by 23.01%, the loan outstanding at the end of the year increased by 1 7 .98% and stood at TK. 84.35 million. Apart from these, during 201 S to 2018, the average loan size and the average savings increased by 2.43% and 21.33% per year. This indicates the organization is disbursing credit more from other sources than savings of the members.

Decreasing average savings and increasing average loan

size

Type Loan Loan Interest Repayment Tenure Amount Rate Fr uenc

Micro credit I year 20,000 to 27% Weekly/Monthly 75,000

Housing 3 Years 35,000- S.5% Monthly 70,000

Two loan products

Program Evaluation Perfect Development Foundation (ADESH) launched its microfinance program in 2007. The main purpose of this program has its successful story in Bangladesh and ADESH is no less than that, ADESH has successful launched its micro finance program since last 7 years and acquired experience to gear it further among the targeted women to eradicate poverty. ADESH's microftnance program has two loan products. most of which has loan tenure of 1-3 years and weekly and monthly repayment frequency. However, these may vary from product to product. The loan size also varies across the loan type.

L

I Name Desi2nation Age Education I Dr. Benoy Goswami Chairperson 61 HSC Papri Gain Vice Chairperson 51 HSC Md. Chowdhury Miah General Secretary 73 BCom Rebecca Adhikary Asst. General Secretary 58 SSC Stanley Sitangshu Karmokar Treasurer 55 MSS Kalpana Das General Member SB HSC Fatema Haque General Member 41 MSS Sipra Adhikary General Member 39 SSC Md. Shahjahan Bhuiyan General Member 56 M.Ed.

MICROFINANCE PROGRAM L

Currently, Or. Benoy Goswami (age: 61 years) is the Chairperson of the Executive Committee. Papri Gain is the Vice-chairperson of the organization. The General Secretary of the committee is Md. Chowdhury Miah, Rebecca Adhikary is the Assistant General Secretary, Stanley Sitangshu Karmokar is the Treasurer of the executive committees. Kalpana Das, Fatema Haque, Sipra Adhikari, and Md. Shahjahan Bhuiyan are the General members of the executive committee in the organization. The list of the EC is presented below:

CREDIT RATING REPORT ~ ASSOCIATION OF DEVELOPMENT FOR ECONOMIC & SOCIAL HELP W'c"i.f!ll]

(AD ESH) constitution of the organization, the EC should have seven members in it. There should be one Chairperson, one Vice-chairperson, one Executive Director, one Treasurer, and three Executive Members.

Page 4 WASO Credit Rating Company (BO) Ltd.

During 2018, the organization experienced significant growth of 1 7.98% in the PAR compared to growth in the total loan outstanding amount of Tk. 84.35 million. This reflects that although the organization disbursed higher amount of loan during the year, the overall quality and recover of the loans has moderate. ~

PAR grew at significantly PAR 1 ·30 days 0.16 0.19 0.06 0.09 rate than loan portfolio PAR 31-180 days 0.74 0.87 0.45 0.64

PAR 181 ·365 days 0.62 0.73 0.26 0.36 PAR> 365 days 0.61 0.72 0.70 0.99 Total 2.12 2.51 1.48 2.07

Loan 2018 2017

Classification Value I % of Loan Value I %of Loan

Outstandina OutstandinQ

ADESH has adequate portfolio risk coverage with loan loss provision fund of Tk. 2.35 million.

Aging schedule of loan portfolio of ADESH depicts that at the end of 2018, 2.51% of the loan portfolio's repayment was not regular where 0.72% of the portfolio's repayment was outstanding for more than 365 days. This was only 0.99% during the year preceding. Total value of the portfolio at risk is about Tk. 2.12 million, which was only Tk. 2.07 million in 2017.

Quality of the portfolio deteriorated significantly for

increase in PAR

Quality of the Portfolio Non-government organizations whose loan is typically not backed by bankable collateral the quality of the portfolio is absolutely crucial. The most widely used measure of portfolio quality is Portfolio at Risk (PAR), which measures the portion of the loan portfolio contaminated by arrears as a percentage of the total portfolio.

25.56 52.31 26.41

96.18 3.82 100.00

68.77 2.73 71.50

17.71 24.77 17.98

95.96 4.04 100.00

Micro credit 80.94 Housing 3.40 Total 84.3S

2018 2017 Particulars Tk. in I Total I Growth Tk. in j Total j Growth

million (%) (%) million (%) (%)

Loan portfolio Analysis Total loan outstanding of the organization as on 30 June 2018 was Tk. 84.35 million. The main concentration of the loans was on microcredit loan. About 95.96% of total loan outstanding is composed of micro credit loan as on the year end of 2018. This percentage was about 96.18% in 2017. The total loan outstanding experienced about 17.98% growth in that year, which was mainly supported by micro credit and housing loan etc.

Diversified loan portfolio, with concentration on the

micro credit-based loan

.._

I Particulars 2018 2017 2016 201s I No. of Branches 3 3 1 1

L No. of Members 4.995 4,995 4.139 4,720 No. of Borrowers 3,541 3,541 2,946 3,365

No. of Field Officers 13 13 1 3 13

Total Loan Outstanding (Tk. In million) 84.35 71.50 56.56 48.10

Yearly Loan Disbursement (Tk. In million) l 50.83 122.62 95.04 85.85

Total Savings (Tk. In million) 42.73 41.72 34.39 31.90

Average Loan Outstanding 23.820 20.191 l 5,973 13.583 Average Savings 12.069 11.783 9,712 9,008

CREDIT RATING REPORT ~ ASSOCIATION OF DEVELOPMENT FOR ECONOMIC & SOCIAL HELP \Vc3{8'Lfl)

(AD ESH)

Page 5 WASO Credit Rating Company (BO) Ltd.

Capitalization and Funding Mix ADESH's microfinance program was mainly funded by Members' Savings, which contributed about 3.97% of total funding mix. This is followed by 27.34% from bank loans, 23.90% from Capital Fund, and 6.09% by fund liabilities. During 2018 capital fund increased by 3.97% mainly because of lower expenses incurred. Total fund of the organization during 2018 grew marginally. ,,J><1I

I Particulars 2018 2017 2016 2015 Capital/Asset Ratio(%) 23.79 28.34 29.70 30.79 Debt to Equity Ratio (Times) 1.42 0.72 0.61 0.56 Deposits to Loans (%) 50.67 58.36 60.80 66.32 Deposits to Assets (%) 42.47 51.36 52.19 51.99 Loan Portfolio to Assets (%} 83.82 88.00 85.84 78.39

ADESH generally would be able to access commercial sources of funds and therefore achieve moderate Debt than other MFls. ADESH is approaching its borrowing limits in order to expand its credit growth, as the Capital/ Asset ratio stood at 18.21 %. The rest of the portion is financed through either borrowing or collecting deposits from members, both of which are treated as debts. Through rapid increases in debt funding would put pressure on ADESH's margin. In 2018, debt to-equity ratio of ADESH increased marginally; whereas, deposit-to loans ratio remained stable after declining in the preceding year. Deposits, on the other hand, has a significant contribution in the assets of the organization, about 23.79%, which has increased marginally in 2018 after sharp decline in 2017.

-

I Particulars 2018 2017 2016 2015 Provision Expense Ratio o.ss 0.71 0.97 2.82 Loan Loss Reserve Ratio 2.79 3.29 4.94 5.81 Risk Coverage Ratio 35.65 146.37 30.56 41.84

L

Provision Expense Ratio gives an indication of the expense incurred by ADESH to anticipate future loan losses. The provision expenses ratio decreased by 1.19 percentage point (PP) in 2018 from 201 S due to deterioration of the portfolio quality. The loan loss reserve ratio reflects accumulated provision expense, which increased by 0.45 PP and stood at 2.50%, indicating that the overall provisioning of the organization has improved over the year. However, the organization did not keep any provision against the portfolio at risk (PAR) before 2018. As a result, the related ratios could not be calculated for those periods. Additionally, the organization kept about 30.00% reserve compared to its PAR. The Risk Coverage Ratio is calculated by dividing loan loss reserves by the outstanding balance on arrears over 1 day. This measure shows that in 2018 it was 35.65% of the Portfolio at Risk is covered by actual loan loss reserves. Although this ratio is complies with Microcredit Regulatory Authority (MRA), significant change in the PAR can jeopardize the reserve situation.

Less than 100% in Risk Coverage Ratio

I Particulars 2018 2017 2016 2015 Loan Outstanding (Tk. in Mil} 84.35 71.SO 56.56 48.10 PAR (Tk. in Mil) 212 1.48 t.n 1.79 Loan Portfolio Growth (%) 17.98 26.41 17.60 NIA

PAR Amount's Growth (%) 43.33 -14.06 --4.05 NIA

CREDIT RATING REPORT ~ ASSOCIATION OF DEVELOPMENT FOR ECONOMIC & SOCIAL HELP VfCt..e!}lJ

(AD ESH)

Page 6 WASO Credit Rating Company (BO) Ltd.

I Particulars 2018 2017 2016 2015 I Profitability & Efficiency Portfolio Yield (%) 25.99 25.30 23.80 7.99 Return on Assets (ROA) (%) 1.68 4.15 0.94 (14. 75) Operating Expense Ratio (%) 24.19 20.49 23.19 46.03 Fund Cost Cost of Savings (%) 4.27 4.01 3.99 6.83 Cost of Borrowings (%) 10.51 7.79 7.11 10.11 Avg. Cost of Savings & Sorrowing (%) 6.60 5.04 4.78 7.65 Capitalization

~ Borrowed Fund to Equity (Times) 1.42 0.72 0.61 0.56

Financial Indicators At the end of 2018, portfolio yield increased by 0.69 percentage point to 25.99% and ROA increased to 1.68% from 4.15%. In 2018, operating expense ratio that indicates efficiency of the organization, increased by 3.07 percentage point mainly because rapid increase in the operational scope. The cost of saving, on the other hand, has declined marginally by 6.60 percentage points.

Portfolio Yield of 25.99% Cost of savings of 4.27%

Cost of borrowing of I 0. 51 %

Tk. in mlflion

Particulars 2018 2017

Amount Growth Amount Growth Fund Based Income (a) 20.53 24.6% 16.48 29.5%

Interest income on loan 20.25 25.0% 16.20 30.1% Interest income on bank deposit 0.28 -0.8% 0.28 4.6%

Interest & Finance Charges (b) 4.45 69.2% 2.63 24.1% On Borrowings 2.65 139.4% 1.11 38.4% On Deposits 1.80 18.2% 1.53 15.5%

Net Interest Income (a-b) 16.07 16.1% 13.85 30.6% Fee Based & Other Income (c ) 0.02 113.2% 0.01 -75.4% Total Income (a+c):d 20.54 24.6% 16.49 29.3% Gross Surplus (d-b) 16.09 16.1% 13.86 30.3% Expenses 13.97 39.3% 10.03 5.5%

Personnel Expenses 7.73 11. 9% 6.91 8.7% Administrative & Other Expenses 6.23 99.9% 3.12 · 1.1%

Provision For Loan Loss 0.43 -6.4% 0.46 -9.5% Net Surplus 1.69 -49.7% 3.37 445.1%

Increased Net surplus In 2018, fund based income increased significantly, by about 20.53% and net interest income increased by 20.25% due to significant increase in Interest expense on borrowing. As a result, Gross Surplus of the program also increased by 16.09%. However, because of increase in administrative expenses and Provision for Loan Loss, the Net Surplus decreased by 49.70% compared to previous year (2017). The Net Surplus stood at Tk. 1.69 million in 2018 from Tk. 3.37 million in 2017.

Financial Performance

2018 2017 Particulars Tk.in I Total I Growth Tk. in] Total J Growth

million (%) (%) million (%) (%) Capital Fund 23.94 23.90 3.97 23.03 28.34 17.64 Long Term 33.48 33.43 102.96 16.49 20.30 38.26 liabilities /loan

L Fund Liabilities 6.10 6.09 93.58 3.1 5 3.88 (17.81) Bank Loan 27.38 27.34 105.18 13.35 16.43 64.78

Members' Savings 42.73 42.67 2.43 41.72 51.36 21.33

Total 100.15 100.00 23.28 81.24 100.0 23.30 0

CREDIT RATING REPORT ~ ASSOCIATION OF DEVELOPMENT FOR ECONOMIC & SOCIAL HELP W(;1ke?JD

(AD ESH)

Page 7 WASO Credit Rating Company (BO) Ltd.

This sector has created direct job opportunities for over 111 ,800 people; 80% of them are male and 20% are female. At the end of June 2011, the sector had outstanding loans of Tk. 173.8 billion disbursed to 20.7 million borrowers, and had accumulated Tk. 63.3 billion as savings from around 26.1 0 million clients - over 93% of them are women - through more than 18,000 branches, by 576 NGO-MFls licensed by MRA. ,,kV

Range of No.of Loan %of Loan Total Savings %of categories Outstanding Borrowers Mfls Tk. in Million Outstanding (Tk. in Million) Savings

UptolOOO 171 1.360.52 0.49 513.77 0.46

Very Small 1001 ·2000 180 2.091.50 0.75 892.14 0.81 2001-6000 126 4.253.28 1.54 2045.84 1.81 6001·10000 47 4,036.20 1.50 1479.99 1.35

Small 10001·50000 108 31,079.80 11.28 11 523.93 10.01 Medium 50001·100000 19 16,624.95 5.72 6178.50 5.4 7

._ Large 100001 · 1 000000 23 78.108.25 28.19 31054.00 27.49

Very Large 1000001 and 2 140,463.05 50.52 59303.88 52.50 Above Total 676 278,017.SS 100.00 112,992.0S 100.00

In the microfinance sector total loan outstanding is around Tk. 278 billion {including Grammen Bank) and savings is about Tk. 299 billion. The total clients of this sector is 3 5 million that accelerates overall economic development process of the country. Credit services of this sector can be categorized into six broad groups: i) general microcredit for small-scale self employment based activities, ii) microenterprise loans, iii) loans for ultra poor, iv) agricultural loans, v) seasonal loans, and vi) loans for disaster management. Loan amounts up to BOT 50,000 are generally considered as microcredit; loans above this amount are considered as microenterprise loans.

Bangladesh's microfinance sector shows strong resilience and continues to contribute towards enhancement of macroeconomic growth. Bangladesh microfinance sector is now matured and its assets constituted around 3% of GDP in 2011. Total outstanding loan of this sector increased by around 20.0% from Tk. 145.0 billion in June 2010 to Tk. 173.8 billion in June 2011 disbursed among 20.7 million poor people.

The top three MFls contribute 54% of total loan outstanding as well as savings of the microfinance sector in Bangladesh. Two of the largest MFls, viz .• BRAC & ASA, are each serving over five million borrowers. There are a few more developing fast. On the other hand the smallest 428 NGO-MFls have contributed only 4 percent of total loan outstanding and 5 percent of total savings. Institutional concentration ratio is highly skewed in favor of large MFls: just 22 institutions are in control of 76 percent of the market share while three largest organizations have control of over 50 percent in terms of both clients and total financial portfolios.

L

Microcredit programs in Bangladesh are implemented by non government organizations (NGOs), Grameen Bank, state-owned commercial banks, private commercial banks, and specialized programs of some ministries of Bangladesh government.

CREDIT RA TING REPORT ~ ASSOCIATION OF DEVELOPMENT FOR ECONOMIC & SOCIAL HELP \ifc~f!ljj)

(AD ESH)

Page 10 WA50 Credit Rating Company (BO) ltd.

Oise/aimer: lnformarlon used herein was obtained from sources believed to be accurate and reliable. However. WCRCL does not guarantee the accuracy, adequacy or completeness of any lnformarlon and Is nor responsible for any errors or omissions or for the results obtained from the use of such information. The rating is an opinion on credit qual/ty only and Is not a recommendatton to buy or sell any securities or to finance In a projea. A/I rlghrs of rhls report are reserved by WCRCL The contents may be used by the news media and researchers wnn due acknowledgement.

END OF THE REPORT

Business Potentials • New market exploration • Introducing new loan products • Availability of lower cost funds

CREDIT RATING REPORT ~ ASSOCIATION OF DEVELOPMENT FOR ECONOMIC & SOCIAL HELP W'c"A_81/J

(AD ESH)

L

Page 11 WASO Credit Rating Company (BO) Ltd.

A short-term obligation rated ' Short Term - 6' is in payment default or jeopardized through bankruptcy petition of similar action.

A short-term obligation rated ' Short Term - 5' is currently vulnerable to nonpayment and is dependent upon favorable business. financial, and economic conditions for the obligor to meet Its financial commitment on the obligation.

A short-term obligation rated ' Short Term - 4' is regarded as having some speculative characteristics. The obligor currently has the capacity to meet its financial commitment on the obligation; however, it may face uncertainties which could lead to the obligor's inadequate capacity to meet its financial commitment on the obligation.

Issuer/Issue rated "Short Term - r has an acceptable ability to repay short term debt obligations from internal sources. However, it is expected to rely on external sources of committed financing due to downturn in economic or industry circumstances.

Issuer/Issue rated "Short Term - r has a strong ability to repay short term debt obligations. It is likely to meet their obligations over the coming 12 months through internal resources but may rely on external sources of committed financing.

ST-6 L.

ST-5

ST-4

... .... 0 s: V'I

! ns

8. .... 0 u

ST-3

ST-2 "' QI ;: 0 C')

! J C') c :u 0::: E .... QI I-

Issuer/Issue rated "Short Term - 1- has a superior ability to repay short term debt obligations. It is ST-1 most likely to have the capacity to meet their obligations over the coming 1 2 months through

internal resources without relying on external sources of committed financing.

Indicates that the issuer/Issue is in default, is technically or actually in bankruptcy.

Default Grade

Issuer/Issue rated C is the lowest rated class of bonds and typically in default with little prospect of recovery of principal and interest.

Issuer/Issue rated CC is highly speculative and likely or very near in default, with some prospect of recovery of principal and interest .

Issuer/Issue rated CCC is judged to be of poor standing and subject to very high credit risk.

Risky Grade

Issuer/Issue rated Bis considered speculative and subject to high credit risk.

Issuer/Issue rated BB is judged to have speculative elements and subject to substantial credit risk.

Speculative Grade

Issuer/Issue rated BBB is subject to medium credit risk. And considered medium grade and as such may possess certain speculative characteristics.

Issuer/Issue rated AAA is judged to be of the highest quality with minimal credit risk.

Issuer/Issue rated AA is judged to be of very high quality and subject to very low credit risk.

Issuer/Issue rated A is an upper medium grade and subject to low credit risk.

Investment Grade L AAA

AAl, AA2, AA3

Al, A2, A3

"' 8881, 8882, QI ;: 8883 0 Cl QI ... ta u Cl 881,882,883 c :u 0::: Bl,82,83 E .... QI I- Cl c CCCI, CCC2, 0

-I CCC3 ! ta ....

~ 8. CCl, CC2, CC3 .... 0 u

L c

D

WCRCL RATING SCALE FOR CORPORATE

RATING SCALE & DEFINITION

CREDIT RATING REPORT ~ ASSOCIATION OF DEVELOPMENT FOR ECONOMIC & SOCIAL HELP \ifc'}fBZtlJ

(AD ESH)

L

(2) We have complied with all the requirements, policy and procedures of these rules as prescribed by the Securities and Exchange Commission vide No. SEC/CMRRCD/2001- 27 /01 /Admin/01-41 dated November 17,2009 in respect of this rating

~

(1) We, WASO Credit Rating Company (BO) Ltd (WCRCL), as well as the analysts of the rating has examined, prepared, finalized and issued this report without compromising with the matters of our conflict of interest, if there be any; And

We, WASO Credit Rating Company (BO) Ltd (WCRCL), While assigning this rating to the "Association of Development for Economic & Social Help (ADESH)" hereby solemnly declare that:

DISCLOSURE AS PER RULE 8 (b) of SEC NOT/FICA TION NOVEMBER 17, 2009

L..

Pantha Plaza {4'h Floor), 68, West Panthapath, Kalabagan, Dhaka-1205, Bangladesh. Tel: 88-02-8126452, 9146329, 9111330

E-mail: [email protected] wasocreditrati ng@gmai I .com

Web: www.wasocreditrating.com