ASSOCHAM– Overview of TDS Provisions Niranjan Govindekar Associate Director October 2010.

31

ASSOCHAM– Overview of TDS Provisions Niranjan Govindekar Associate Director www.pwc.com October 2010

-

Upload

kelvin-henwood -

Category

Documents

-

view

226 -

download

1

Transcript of ASSOCHAM– Overview of TDS Provisions Niranjan Govindekar Associate Director October 2010.

ASSOCHAM– Overview of TDS Provisions

Niranjan Govindekar Associate Director

www.pwc.com

October 2010

PwC

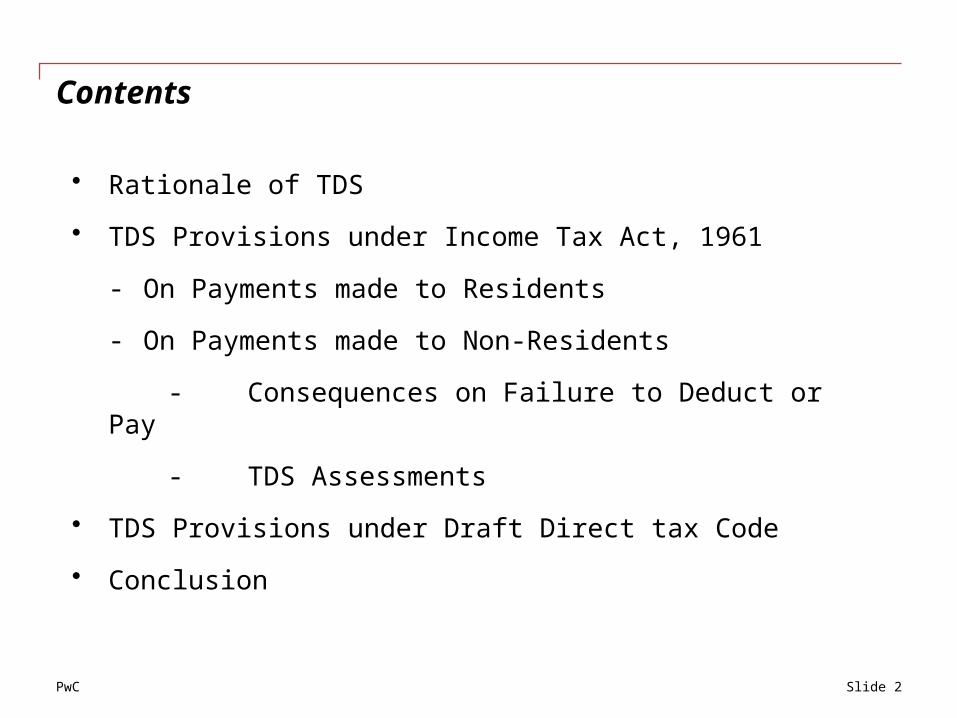

Contents

• Rationale of TDS

• TDS Provisions under Income Tax Act, 1961

- On Payments made to Residents

- On Payments made to Non-Residents

- Consequences on Failure to Deduct or Pay

- TDS Assessments

• TDS Provisions under Draft Direct tax Code

• Conclusion

Slide 2

PwC

Rationale of TDS…

Slide 3

• Ensure regular flow of funds for the Government

• Early collection of the revenue by the government

• Helps in widening the tax base

• Reporting of correct income

• Check tax evasion

• Cheapest mode of collection and recovery of tax

Why TDS?

• Tax deduction liability is a vicarious liability and the principal liability is of the person who is taxable in respect of such income

• TDS provision, of late are increasingly used the world over to collect taxes with least effort on the part of governments. India is no exception.

• Robust growth in TDS collection during last 5 Year

PwC

TDS Provisions under IT Act

Slide 4

PwC

TDS Provisions on payments to Residents…Section &Nature Rate of TDS Exemption

Company

Individuals/ HUF

Any other person

192 - Salaries • Tax is deducted at the average rate of income tax computed on the basis of rate in force for the financial year

• Entertainment allowance (for government employees)

• Professional tax• Deduction under section

80C &80CCC• Deduction under section

80D• Medical treatment of

handicapped section 80DD• Basic Slab exemption

193 - Interest on Securities 10% 10% 10% • Amount not exceeding Rs. 2500 applicable only in case payee is an individual & the interest is payable on listed debentures

• Interest payable on certain specified government securities or on listed security which is in dematerialised form, etc.

194 - Dividend 10% 10% 10% • Exemption in case shares are beneficially owned by government, RBI, LIC, general insurance Slide 5

PwC

TDS Provisions on payments to Residents…

Section &Nature Rate of TDS Exemption

Company Individuals/ HUF

Any other person

194 A – Interest other than interest on securities

10% 10% 10% • Amount not exceeding Rs. 5000 and in case of banking company or cooperative society engaged in banking, amount not exceeding Rs. 10,000.

194C – Payment to Contractors & sub-

contractors

2% 1% 2% • W.e.f 1st July,2010; contract payment not exceeding Rs 30000 single contract or aggregate Rs. 75000 during financial year

• W.e.f 1st October, 2009; payment to transport operators (if PAN is furnished)

• Payment exclusively for personal purposes of Individuals and HUF

• Contract for sale of goods

194D – Insurance Commission

10% 10% 10% • Amount not exceeding Rs. 20,000 (w.e.f 1st July 2010)

Slide 6

PwC

…TDS Provisions on payments to Residents…Section & Nature Rate of TDS Exemption

Company Individuals/ HUF

Any other person

194H - Commission or Brokerage

10% 10% 10% • Aggregate payment during the Financial Year does not exceed Rs 5,000 ( w.e.f 1st July 2010)

• Turnover commission payable by RBI to Agency Banks

• Payments of brokerage on purchase and sale of securities

• Not being Insurance commission

194I- Rent Machinery/ equipment

Rent on land/ building/ furniture

2%

10%

2%

10%

2%

10%

• When aggregate payments to the payee during a financial year does not exceed Rs 1,80,000( w.e.f 1st July 2010 )

194J – Fees for professional and

technical services

10% 10% 10% • Payment exclusively for personal purposes of Individuals and HUF

• Aggregate payments during a financial year does not exceed Rs 30,000(w.e.f 1st July 2010)

Slide 7

PwC

Issues – Payments made to Residents…

• Interest other than interest on securities u/s 194

- When loans and repayments relating to directors are routed through the company? CIT vs. Century Building Industries (P.) Ltd. (293 ITR 194) (SC)

- Whether deduction should be on gross interest or net interest? CIT vs. S.K. Sundararamier & Sons (240 ITR 740) (Mad.)

- Whether payment under hire purchase agreement will atrract TDS under 194A? Instruction no.1425, dated 16.11.1981

• Contractors u/s 194C

- Whether both oral and written contracts covered? Circular No.93 dated 26-9-1972

- Whether contracts for rendering Professional services covered?

Chamber of Income Tax Consultants v CBDT [209 ITR 660 (Bom)]

- Whether supply of printed Labels covered? BDA Ltd V ITO(TDS) (2006) 281 ITR 99 (BOM)/ Circular 715/ August 1995

- Outsourcing of fabrication and manufacturing? CBDT Circular No. 681, 715 and 13/2006

Slide 8

PwC

…Issues – Payments made to Residents

• Rent u/s 194I

- Whether tax is deductible on non refundable deposit? CIT vs Reebok India Co (2007) (291 ITR 455) (Del)/ Circular 718/ August 1995

- Whether limit of Rs 120,000 pa applies separately for each co-owner? Circular No 715 dated August 8, 1995

- Rented space sublet for putting up hoardings? Circular 715 dated 08/08/1995 (Q.no.5)

- Tax credit in case of advance rent- Circular no. 5/2001 dated. March 2, 2001

• Professional/ Technical fees u/s 194J

- Whether tax deductible from payment of use of standard facility?

Skycell Communications Ltd V DCIT [251 ITR 53] (Mad)

- Whether TDS on payment of advertising, broadcasting, telecasting contract is covered by under section 194J?

CBDT Circular No. 715 dated August 8, 1995 (Q.no. 4)

- Commission for non-executive directors- whether covered under section 192 or section 194J or section 194H?

- Whether TDS is deducted on the gross amount, including service tax? CBDT Circular No. 715 dated August 8, 1995

Slide 9

PwC

TDS provisions on payments to Non -Residents…

Slide 10

• Section 195 of the Act cast obligation on payer to deduct tax at

source on making payment to Non-residents

• Objective of TDS on payments made to Non-Residents (Circular No. 152 dated 27.11.1974):

- Tax is collected at the earliest point of time;

- No difficulty in collection of tax at the time of assessment;

- To avoid loss of revenue as the non resident may sometimes

have

no assets in India from which subsequent recovery can be made.

PwC

…TDS provisions on payments to Non -Residents…

Slide 11

• Salient Features:

- Payment by ‘any person’ (includes non-residents and foreign companies)

- Payments to non-residents (having presence in India or not)

- Any Sum chargeable to tax (other than salary)

- Deduction at the time of credit or payment, whichever is earlier

• Exception to Government, Public Sector Banks and PFI – on payment basis.

- Deduction at the rates in force

• Circular no. 728 dated 30.10.1995

- Payment made by Non-resident to Resident covered

• Circular no. 726 dated 18.10.1995

- Payment made by Non-Resident to Non-Resident covered if transaction is India Centric

PwC

…TDS provisions on payments to Non -Residents

Slide 12

• Obligation cast on Payer

- Determine the characterisation of income & its taxability under the Act

- Evaluation of applicable tax treaty

- Get appropriate documentation from payee to grant him treaty benefits.

- Knowledge of recent judicial precedents

- Meet Deadlines for withholding taxes and timely deposit of taxes so withheld

PwC

Issues – Applicability…

Slide 13

Sr. No. Applicability of Section 195 Case laws/ Circulars

1. TDS whether deductible from:- Gross sum, or- Only income embedded

• Transmission Corporation of A.P. LTD vs. CIT (239 ITR 587) (SC)

• To be effected on net paymentsRaymonds Ltd. vs. DCIT (86 ITD 791) (Mum)

2. Payment made in Kind • Kanchanganga Sea Foods Ltd (265 ITR 644)

3. No obligation to deduct tax where income is not chargeable to tax in India

• GE India Technology Centre Pvt. Ltd (2010-TII-07-SC-INTL)

4. Payment by an Indian Branch of a Foreign Co. to its overseas Head Office

• Circular 649/ 31.03.1993 & 740/17.04.1996

• ABN Amro Bank NV (2005) 97ITD 89(SB)• Dresdner Bank (105 TTJ 149) (Mum.)

PwC

…Issues – Applicability…

Slide 14

Sr. No. Applicability of Section 195 Case laws/ Circulars

5. Payment by Resident to an Indian Branch of a Foreign Bank

Circular 20/ 3.08.1961

6. Payment by branch of an Indian Company located offshore to offshore branch of an Indian Bank will not attract TDS liability as payment is made by resident to resident.

7. Reimbursement of Expenses - Mere reimbursement of expenses (out of pocket

expenses)

- No income embedded in such pure reimbursement duly supported by necessary documents

- Cost of Services is charged and recovered by way of reimbursement, even without profit element

• Clifford Chance UK vs. DCIT (82 ITD 106) (Mum.)

Contrary views• Hindalco Industries Ltd. vs. ACIT (94 ITD 242) (Mum.)

• Mahindra & Mahindra Ltd. vs DCIT (2005/SOT 896) (Mum.)

• ACIT vs. Arthur Anderson & Co. (5 SOT 393) (Mum.)

PwC

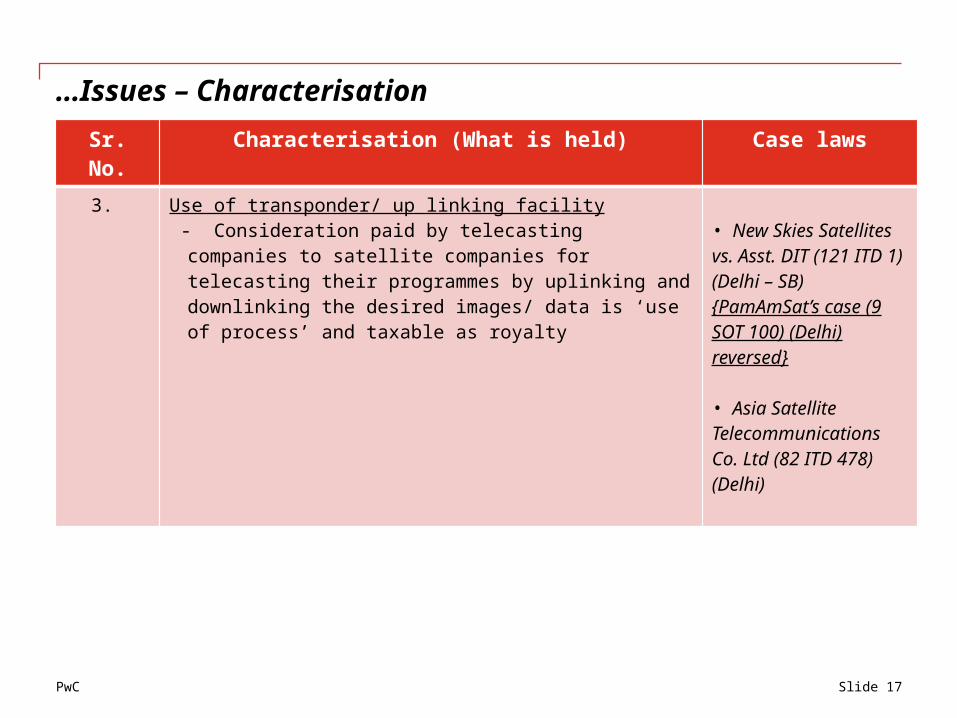

Issues – Characterisation…

Slide 15

Sr. No. Characterisation (What is held) Case laws

1. Software Payments - Copyrighted article partake character of sale of goods

and hence no royalty

- Passing on a right to use and facilitating the use of product for which the owner has a copyright is not the samething as transferring or assigning the rights in relation to copyright

- Mere Connectivity charges is not royalty or FTS

• Sonata Information Technology Ltd vs. Add. CIT (103 ITD 324) (Bang.)

• AAR ruling in case of Geoquest Systems BV (6 taxmann.com 95) 2010 (New Delhi)

• AAR ruling in case of Dassault Systems (322 ITR 125) (2010)

• Skycell Communications Ltd vs. DCIT (251 ITR 53) (Mad.)

PwC

…Issues – Characterisation

Slide 16

Sr. No. Characterisation (What is held) Case laws

2. Design/Drawing - Outright purchase of Design and Drawing is not

royalty but capital gain

- Drawing forming part of composite contract for supply of machinery payment is not royalty

- Payment for providing design documentation as part of the agreement for erecting plant, amounts to payment for information concerning Industrial, Commercial, Scientific experience and hence royalty

Davy Ashmore India Ltd (190 ITR 626)(Cal.)

Neyveli Lignite Corp (243 ITR 459) (Che.)

Munak Galva Sheeta Ltd (35 ITD 304) (Delhi)

PwC

…Issues – Characterisation

Slide 17

Sr. No. Characterisation (What is held) Case laws

3. Use of transponder/ up linking facility - Consideration paid by telecasting companies to

satellite companies for telecasting their programmes by uplinking and downlinking the desired images/ data is ‘use of process’ and taxable as royalty

• New Skies Satellites vs. Asst. DIT (121 ITD 1) (Delhi – SB){PamAmSat’s case (9 SOT 100) (Delhi) reversed}

• Asia Satellite Telecommunications Co. Ltd (82 ITD 478) (Delhi)

PwC

…Issues – Characterisation

Slide 18

Sr. No. Characterisation (What is held) Case laws

4. Consideration for Analysis, Testing, Certifying/Rating - Payment for installation and commissioning services

associated with installation of satellite network communication system including rendering project management and engineering support services and factory acceptance test services. Held, since it did not ‘make available’ technical expertise & knowledge, no FIS

- Payment to Non-resident credit rating agency for providing commercial information is not FIS.

- Payment of fees to undertake and provide technical services for upgradation of National Highway including preparation of detailed project report. Held, when payment is only where technical or consultancy service consists of development and transfer of technical plan or design, no make available required and hence taxable as FIS

• Dy. DIT vs. Scientific Atlanta (33 SOT 220) (Mum.)

• ICICI Bank Ltd. vs. DCIT (20 SOT 453) (Mum.)Contrary viewEssar Oil Ltd. vs. CIT (4 SOT 161) (Mum.)

• SNC- Lavalin International Inc vs. DDIT (26 SOT 155) (Delhi)

PwC

Application by Payer u/s 195(2) by payee u/s 195(3)

Slide 19

Application by Payer

• Deals with a scenario where payer makes an application for an order

- Transmission Corporation of A.P. Ltd (239 ITR 587) (SC)

• No prescribed format for an application

Application by Payee

• Payee can make an application for a certificate

• Application can be made in prescribed format:

- Form No. 15C in the Case of Banking Company

- Form No. 15D in any other case

• Condition for issue of Certificate under section 195(3) of the Act (Rule 29B)

• Validity of Certificate

PwC

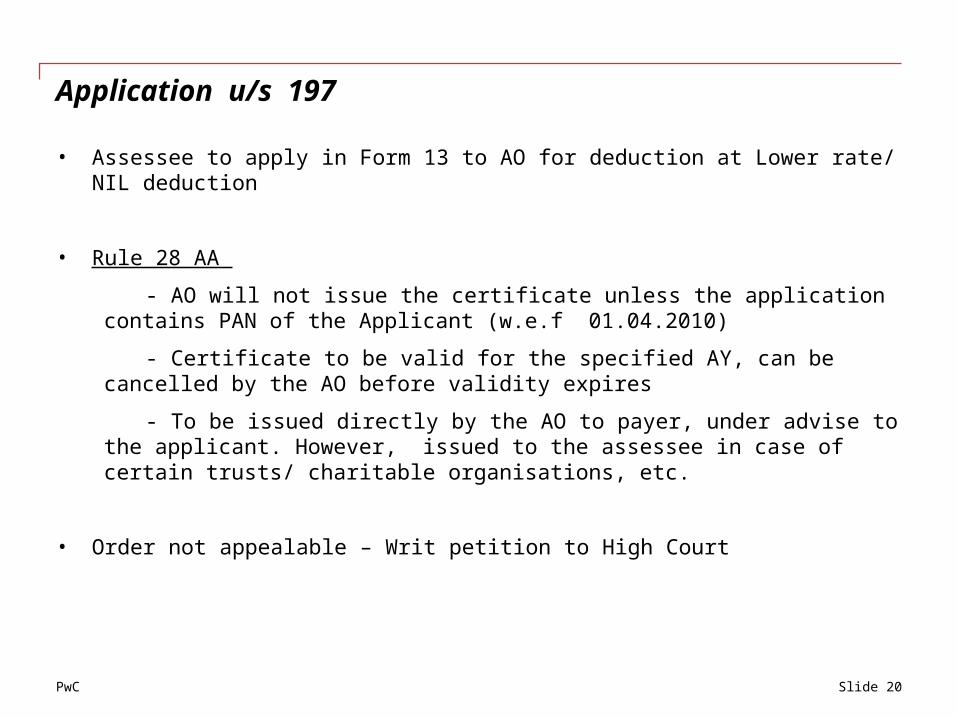

Application u/s 197

Slide 20

• Assessee to apply in Form 13 to AO for deduction at Lower rate/ NIL deduction

• Rule 28 AA

- AO will not issue the certificate unless the application contains PAN of the Applicant (w.e.f 01.04.2010)

- Certificate to be valid for the specified AY, can be cancelled by the AO before validity expires

- To be issued directly by the AO to payer, under advise to the applicant. However, issued to the assessee in case of certain trusts/ charitable organisations, etc.

• Order not appealable – Writ petition to High Court

PwC

Section 206 AA - On payments to Non-Residents

Slide 21

• Non – Obstante Clause

• Payee to furnish his PAN to Payer (if tax is deductible under Chapter XVII

B) – failing which tax shall be deducted at the highest of the following

rates:

- Rate specified in the relevant provision

- Rate in force

- Rate of 20%

• Issue :

Whether Section 206AA overrides the Tax Treaty Provisions?

PwC

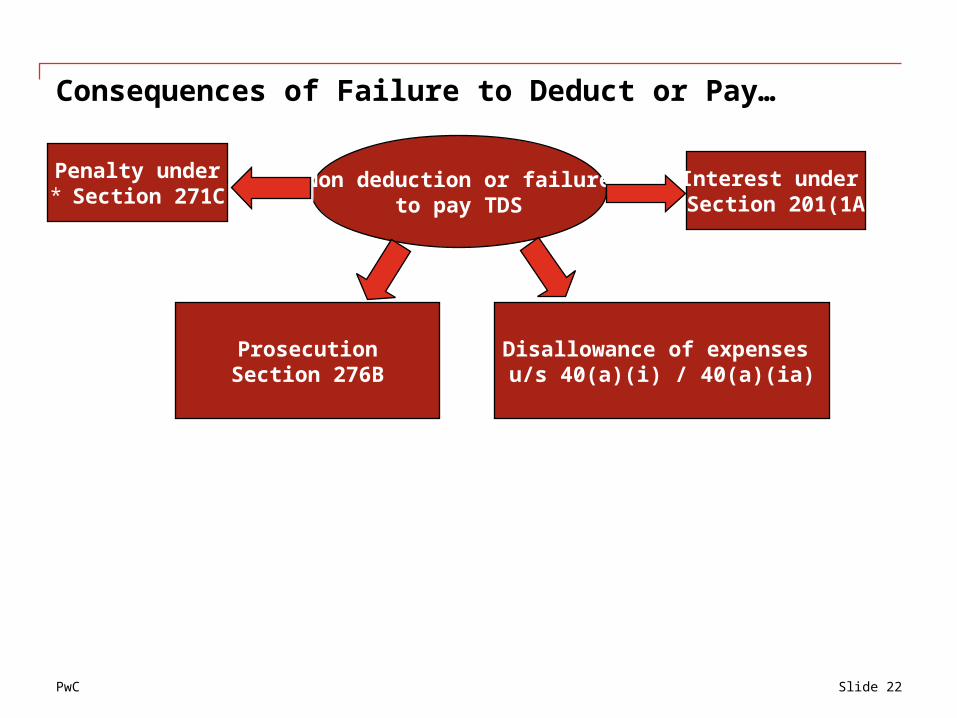

Consequences of Failure to Deduct or Pay…

Slide 22

Non deduction or failureto pay TDS

Non deduction or failureto pay TDS

Interest under Section 201(1A)Interest under

Section 201(1A)

ProsecutionSection 276BProsecutionSection 276B

Penalty under* Section 271CPenalty under

* Section 271C

Disallowance of expenses u/s 40(a)(i) / 40(a)(ia)

Disallowance of expenses u/s 40(a)(i) / 40(a)(ia)

PwC

…Consequences of Failure to Deduct or Pay…

Slide 23

• Section 40(a)(i)/(ia)

• Section 2011. Person deemed as “Assessee in Default”

2. Mandatory Interest (1% for every month/ part of month for the period of delay in deduction and 1.5% for every month/ part of month for the period of delay in credit to government)

3. Tax deducted and not paid shall be a charge on the assets of the person so defaulting

Payments to Disallowance

Non-Residents [section 40(a)(i)]

Tax has not been deducted or after deduction, has not been paid during the PY or before the time limit under Rule 30

Residents [section 40(a)(ia)] No disallowance if tax deducted at any time during the PY deposited on or before the due date of filing of the tax return (retrospective w.e.f FY 2009-10)

PwC

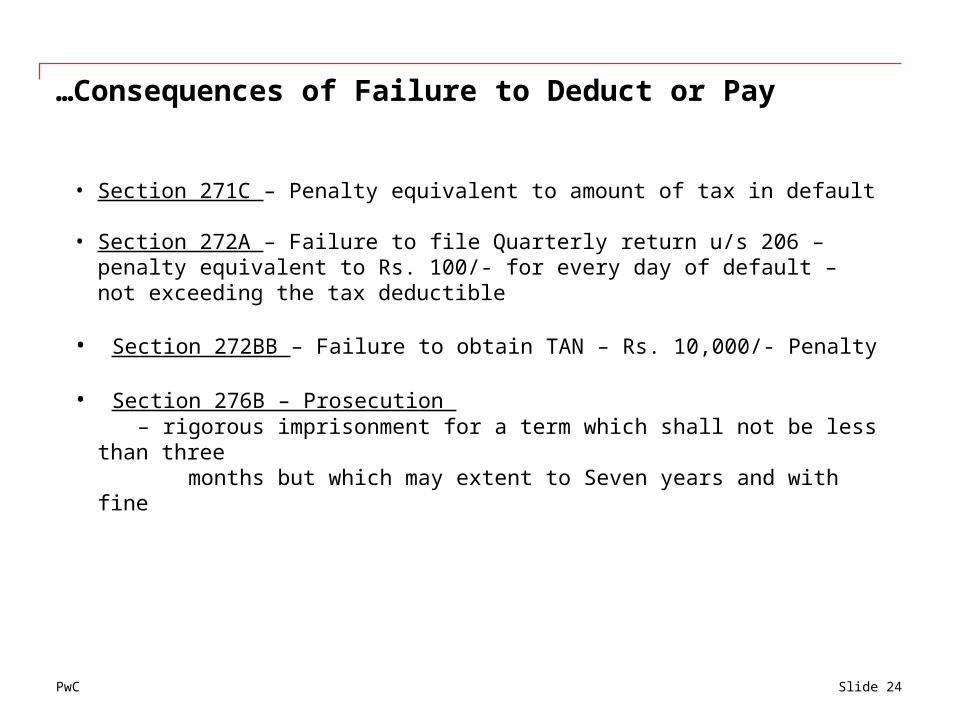

…Consequences of Failure to Deduct or Pay

Slide 24

• Section 271C – Penalty equivalent to amount of tax in default

• Section 272A – Failure to file Quarterly return u/s 206 – penalty equivalent to Rs. 100/- for every day of default – not exceeding the tax deductible

• Section 272BB – Failure to obtain TAN – Rs. 10,000/- Penalty

• Section 276B – Prosecution – rigorous imprisonment for a term which shall not be less than three months but which may extent to Seven years and with fine

PwC

TDS Assessments

Slide 25

• TDS assessment u/s 201 and 201A of the Act.

• Time Limit for completion of assessment in respect of payments to residents (w.e.f 01.04.2010)

- 2 years from the end of FY in which TDS statement is filed - 4 years from the end of FY in which payment is made or credit is

given, in any other case

• No Time Limit for completion of assessment in case payment is made to Non-Residents

• Orders passed are appealable

PwC

TDS Provisions under Draft Direct Tax Code

Slide 26

PwC

TDS Provisions under Draft DTC

Slide 27

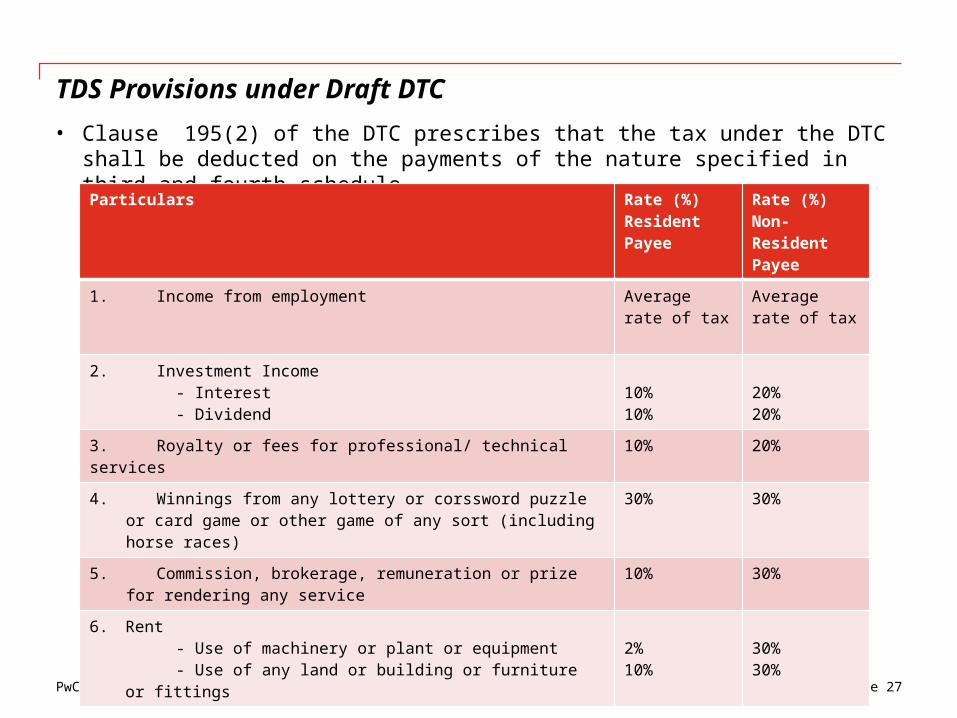

• Clause 195(2) of the DTC prescribes that the tax under the DTC shall be deducted on the payments of the nature specified in third and fourth schedule.Particulars Rate (%)

Resident Payee

Rate (%)Non-Resident Payee

1. Income from employment Average rate of tax

Average rate of tax

2. Investment Income - Interest - Dividend

10%10%

20%20%

3. Royalty or fees for professional/ technical services 10% 20%

4. Winnings from any lottery or corssword puzzle or card game or other game of any sort (including horse races)

30% 30%

5. Commission, brokerage, remuneration or prize for rendering any service

10% 30%

6. Rent - Use of machinery or plant or equipment - Use of any land or building or furniture or fittings

2%10%

30%30%

PwC

TDS Provisions under Draft DTC

Slide 28

• Failure to furnish PAN continues to result in deduction of tax at a higher rate of 20%

• Tax Officers authorized to issue certificates for deduction of tax at Nil/Lower rate

• Central Government to notify instances wherein payer is required to report payments made without deduction of tax.

Particulars Rate (%) Resident Payee

Rate (%)Non-Resident Payee

7. Payment of compensation on compulsory acquisition of immoveable property other than agricultural land

10% 30%

8. Payment to Contractors 2% 30%

PwC

Glossary

• IT Act Indian Income-tax Act, 1961• TDS Tax Deducted at Source• WHT Withholding Tax• DTC Draft Direct Tax Code • PAN Permanent Account Number• PFI Public Financial Institution• AO Assessing Officer• AY Assessment Year• PY Previous Year• SB Special Bench

Slide 29

PwC

Disclaimer

Our presentation is based on the facts and assumptions stated above. Any inaccuracy therein could have a material impact on our recommendations or conclusions and should therefore be intimated to us immediately.

Our presentation is based on the law as of date. Tax laws are subject to changes from time to time and as such any changes may affect the advice contained in our presentation. We have no responsibility to update our advice for events and circumstances occurring after the date of this presentation, unless specifically requested by you.

Further, tax advice is a matter of interpretation of law and is based on our experience with the tax authorities. Accordingly, it cannot be said with certainty that the presentation expressed above would be accepted by the tax authorities.

We do not, in giving this presentation, accept or assume responsibility for any other purpose or to any other person to whom this presentation is shown or in whose hands it may come unless expressly agreed by us in writing.

Slide 30

Thank You

© 2010 PricewaterhouseCoopers. All rights reserved. “PricewaterhouseCoopers” refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity.

![ASSOCHAM-Companies Bill Web[1]](https://static.fdocuments.in/doc/165x107/577cc3531a28aba71195ae50/assocham-companies-bill-web1.jpg)