Assign AMB204 - Intern. Financial Mangmt - M.ombe

23

Amity Campus Uttar Pradesh India 201303 ASSIGNMENTS PROGRAM: MBA IB SEMESTER-II Subject Name : International Financial Management Study COUNTRY : Mozambique Roll Number (Reg.No. ) : IB01272014-2016033 Student Name :Marciano da Piedade Isaque Alexandre Ombe INSTRUCTIONS a) Students are required to submit all three assignment sets. ASSIGNMENT DETAILS MARKS Assignment A Five Subjective Questions 10 Assignment B Three Subjective Questions + Case Study 10 Assignment C Objective or one line Questions 10 b) Total weightage given to these assignments is 30%. OR 30 Marks c) All assignments are to be completed as typed in word/pdf. d) All questions are required to be attempted. e) All the three assignments are to be completed by due dates and need to be submitted for evaluation by Amity University. f) The students have to attached a scan signature in the form. Signature : Date : 13-JUN-2015_________ ( √ ) Tick mark in front of the assignments submitted Assignment ‘A’ √ Assignment ‘B’ √ Assignment ‘C’ √

-

Upload

marciano-ombe -

Category

Documents

-

view

214 -

download

0

Transcript of Assign AMB204 - Intern. Financial Mangmt - M.ombe

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 1/23

Amity Campus

Uttar Pradesh

India 201303

ASSIGNMENTSPROGRAM: MBA IB

SEMESTER-II

Subject Name : International Financial Management

Study COUNTRY : Mozambique

Roll Number (Reg.No.) : IB01272014-2016033Student Name :Marciano da Piedade Isaque Alexandre

Ombe

INSTRUCTIONS

a) Students are required to submit all three assignment sets.

ASSIGNMENT DETAILS MARKS

Assignment A Five Subjective Questions 10

Assignment B Three Subjective Questions + Case Study 10

Assignment C Objective or one line Questions 10

b) Total weightage given to these assignments is 30%. OR 30 Marks

c) All assignments are to be completed as typed in word/pdf.

d) All questions are required to be attempted.

e) All the three assignments are to be completed by due dates and need to be submitted

for evaluation by Amity University.

f) The students have to attached a scan signature in the form.

Signature :

Date : ________________________13-JUN-2015_________

( √ ) Tick mark in front of the assignments submitted

Assignment

‘A’ √ Assignment ‘B’ √ Assignment ‘C’ √

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 2/23

International Financial Management

Assignment – A

Ques 1. What is the need of International Financial Management? List outthe difference between domestic Finance & International Finance.

Answer:

As a business grows, so does their awareness of opportunities available in foreign

market. Initially, they may merely attempt to export a product to a particular country or

import supplies from a foreign manufacturer. An understanding of International

Financial Management is crucial to not only the large MNCs with numerous foreign

subsidiaries, but also to the small business engaged in Exporting or Importing.

International business is even important to companies that have no intention of

engaging in International Business. What companies need to know is how their foreign

competition will be affected by movements in Exchange Rates, Foreign Interest rates,

Labour Costs, and Inflation. Such economic characteristics can have an effect on foreign

competitors’ cost of production and pricing policy. MNCs may have significant foreign

operation driving a high percentage of their sales overseas. The financial managers of

such MNCs must understand the complexities of international finance so that they can

make sound financial and investment decision. In simple words, international financial

management is defined as: –

“Managing working capital, financing the business, assessing control of foreign Exchange

and political risks and evaluating foreign direct Investment."

List of differences between domestic finance and international finance are –

1) The worldwide scale of operations makes the information requirements greater

in case of international finance.

2) The Communications, planning, control and coordination needs are also greater.

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 3/23

3) Different currencies are involved and their relationships change with changing

economic, financial and political developments.

4) The cultural, social and political factors are different in various countries of the

world; adoption to their different environments requires that firms have

different rules for different parts of their operation.

5) The problems of measurement of performances are complicated by the different

circumstances of individual foreign subsidiaries.

6) The terms and conditions of finances and its availability are subject to

continuous change, presenting new opportunities and risks.

7) The proper balance between centralization and decentralization of strategies,

policies and operation is more difficult to achieve in international operation.

Ques 2. i) An investor has two options to choose from:a) $ 7000 after 1 year b)$ 10000 after 3years.Assuming the discount rate of9% which alternative he should opt for?

Answer:

A BFV = $7,000

Discount rate = 9%

Time = 1yr

PV = FV/(1+i)n

PV =$7,000/(1+9/100)1

= $7,000(0.9174)

= $6,422

FV = $10,000

Discount rate = 9%

Time = 3yrs

PV = FV/(1+i)n

= $10,000/(1+9/100)3

= $10,000(0.7722)

= $7,722

The investor should take on $7000 after one year because it needs minimal initial capital

of $6,422 compared to $10,000 after three years which needs $7,722.

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 4/23

ii) A person would need USD 5000, 6 years from now. How much

should he deposit each year in his bank account, if yearly interest rate is 10%?

Answer:

Using the formula FVAn = A((1+K)n – 1)/k

The valve (amount to be deposited every yr)

A = FVAnK / ((1+K)n—1)

K = 10/100 =0.1

N = 6yrs

FVA6 = $5,000

A = ?

A = FVAn / (1+K)n –1)/ K

= $5,000 / 7.71561

= $648.037

The person should deposite $648.037 every

year.

(1+K) = 1+0.1 =1.1

(1+K) = (1.1)6 = 1.771561

1+K)n –1 = 0.771561

(1+K)n –1)/ K = 7.71561

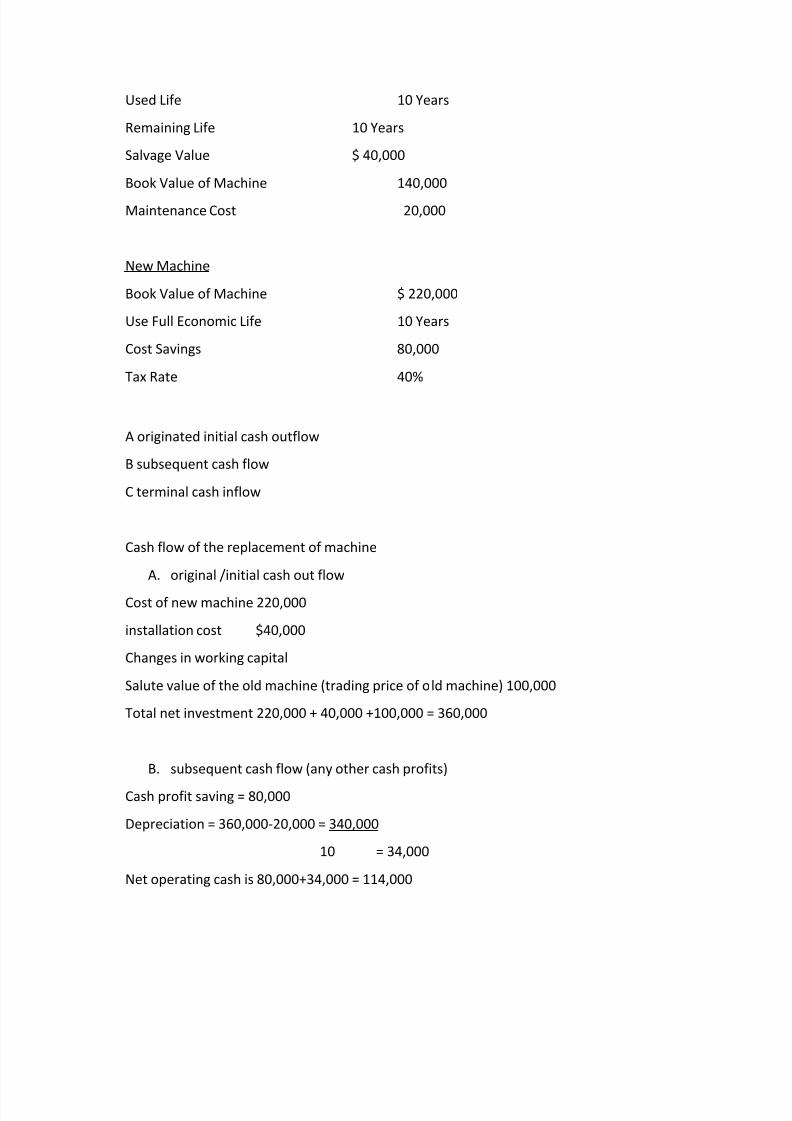

Ques3. Zain corporation ltd is trying to decide on replacement decision ofits current manually operated machine with a fully automatic version. Theexisting machine was purchased ten years ago. It has a book value of $140000 and remaining life of 10 years salvage value $40000. The machinehas recently begun causing problems with breakdown and its costing thecompany $ 20000 per year in maintenance expenses. The company hadbeen offered $ 100000 for the old machinery as a trade-in on the automaticmodel which has a deliver price of $ 220000. It is expected to have a tenyear life & a salvage value of $ 20000. The new machine will requireinstallation modifications costing $ 40000 to the existing facilities, but it isestimated to have cost savings in materials of $ 80000 per year.Maintenance costs are included in the purchase contract and are borne bymachine manufacturer. The tax rate is 40 % .Find out the relevant cashflows

Answer:

Old Machine:

Economic Life of Machine: 20 Years

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 5/23

Used Life 10 Years

Remaining Life 10 Years

Salvage Value $ 40,000

Book Value of Machine 140,000

Maintenance Cost 20,000

New Machine

Book Value of Machine $ 220,000

Use Full Economic Life 10 Years

Cost Savings 80,000

Tax Rate 40%

A originated initial cash outflow

B subsequent cash flow

C terminal cash inflow

Cash flow of the replacement of machine

A. original /initial cash out flow

Cost of new machine 220,000

installation cost $40,000

Changes in working capital

Salute value of the old machine (trading price of old machine) 100,000

Total net investment 220,000 + 40,000 +100,000 = 360,000

B. subsequent cash flow (any other cash profits)

Cash profit saving = 80,000

Depreciation = 360,000-20,000 = 340,000

10 = 34,000

Net operating cash is 80,000+34,000 = 114,000

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 6/23

C. terminal cash flows

Salvage value of machine (10yrs) 20,000

Ques 4.

a) You have a choice of accepting either of two

Calculate the payback period and give your opinion that which project isbetter.

Answer:

Years (I) Cash flows($

US)

Cumulative

($US)

Year (II) Cash flows

($US)

Cumulative

($US)

0 -24500 (q) 0 -28,000(q)

1 6,000 6,000 1 11,000 11,000

2 6,000 12,000 2 9,000 20,000

3 6,000 18,000 3(p) 7,000 27,000®

4(p) 6,000 24,000® 4 5,000 32,000

5 6,000 30,000 5 3,000 35,000

Payback period for alternative (I) = 4 + (24500—24000)/6000

= 4 + 0.0833

= 4.0833 years

Cash flows

YearAlternative I (in

USD)Alternative II

( in USD)

1 6000 11000

2 6000 9000

3 6000 70004 6000 5000

5 6000 3000

lump sum amountat the time

zero(outflows) 24500 28000

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 7/23

Payback period for alternative (II) = 3 + (28000—27000)/ 5000

= 3 + 0.2

= 3.2 years.

Since the payback period is shorter for Alternative II, it can be considered is better.

b) Why is the consideration of time important in financial decision making?How can time be adjusted?

Answer:

Most financial decisions, such as the purchase of assets or procurement of funds, affect

the firm’s cash flows in different time periods. Cash flows occurring in different time

periods are not comparable. Hence, it is required to adjust cash flows for their

differences in timing and risk. The value of cash flows to a common time point should be

calculated. To maximize of owner’s equity, it’s extremely vital to consider the timing and

risk of cash flows. The choice of the risk adjusted discount rate (interest rate) is

important for calculating the present value of cash flows. For instance, if time

preference rate is 10 percent, it implies that an investor can accept receiving USD 100 if

he is offered USD 110 after one year. USD 110 is the future value of USD 100 today at

10% interest rate. Thus, the individual is indifferent between USD 100 and USD 110 a

year from now as he/she considers these two amounts equivalent in value. You can also

say that USD 100 today is the present value of USD 110 after a year at 10% interest rate.

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 8/23

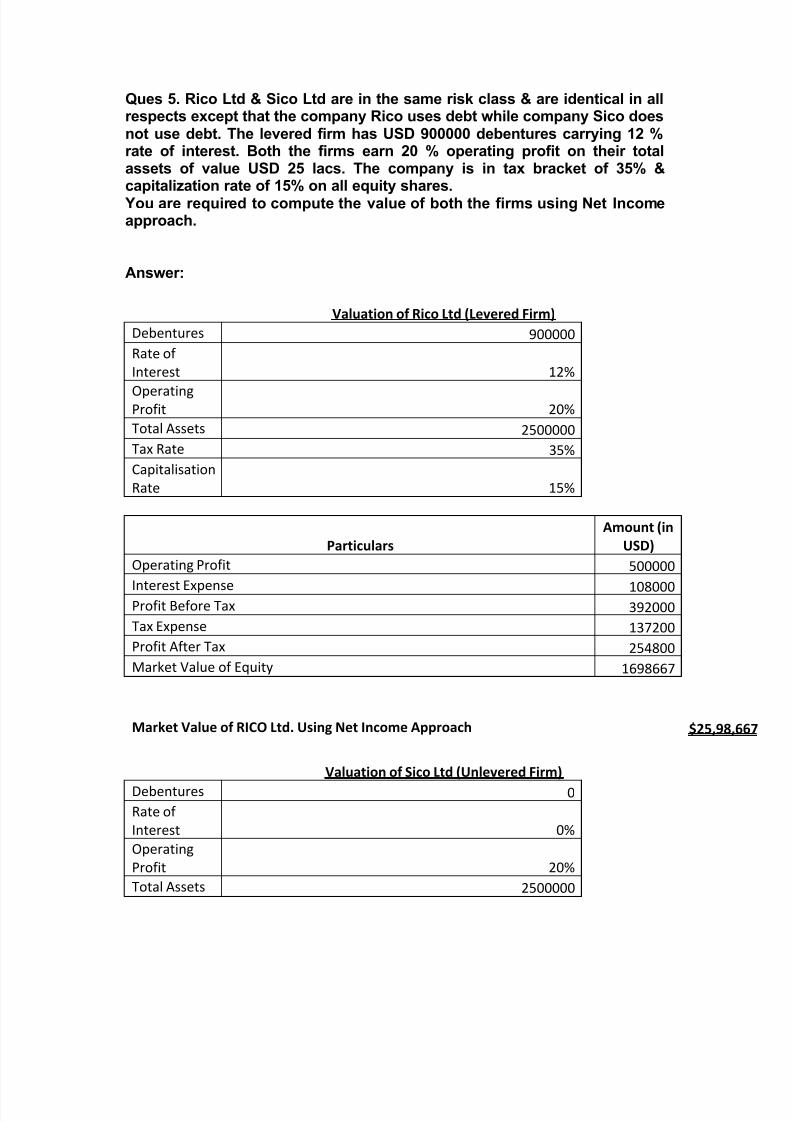

Ques 5. Rico Ltd & Sico Ltd are in the same risk class & are identical in allrespects except that the company Rico uses debt while company Sico doesnot use debt. The levered firm has USD 900000 debentures carrying 12 %rate of interest. Both the firms earn 20 % operating profit on their totalassets of value USD 25 lacs. The company is in tax bracket of 35% &

capitalization rate of 15% on all equity shares. You are required to compute the value of both the firms using Net Incomeapproach.

Answer:

Valuation of Rico Ltd (Levered Firm)

Debentures 900000

Rate of

Interest 12%

Operating

Profit 20%

Total Assets 2500000

Tax Rate 35%

Capitalisation

Rate 15%

Particulars

Amount (in

USD)

Operating Profit 500000

Interest Expense 108000

Profit Before Tax 392000

Tax Expense 137200

Profit After Tax 254800

Market Value of Equity 1698667

Market Value of RICO Ltd. Using Net Income Approach $25,98,

Valuation of Sico Ltd (Unlevered Firm)Debentures 0

Rate of

Interest 0%

Operating

Profit 20%

Total Assets 2500000

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 9/23

Tax Rate 35%

Capitalisation

Rate 15%

Particulars

Amount (in

USD)

Operating Profit 500000

Interest Expense 0

Profit Before Tax 500000

Tax Expense 175000

Profit After Tax 325000

Market Value of Equity 2166667

Market Value of SICO Ltd. Using Net Income Approach $21,66,

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 10/23

Assignment – BQues 1.

i) What are the factors affecting the capital structure of the

company?

Answer:

Internal factors

Cost of Capital: The process of raising the funds involves some cost. While planning the

capital structure, it should be ensured that the use of the capital should be capable of

earning the revenue enough to meet the cost of capital. It should be noted here that the

borrowed funds are cheaper than the equity funds so far as the cost of capital is

concerned. This is because of two reasons. The interest rates (i.e. the form of return on

the borrowed capital) are usually less than the dividend rates (i.e. the form of return on

the equity capital) and the interest paid on borrowed capital is an allowable expenditure

for income tax purposes while the dividends are the appropriate out of the profits.

Risk Factor : While planning the capital structure, the risk factor consideration inevitably

comes into picture. If the company raises the capital by way of borrowed capital, it

accepts the risk in two ways. Firstly, the company has to maintain the commitment of

payment of the interest as well as the installments of the borrowed capital, at a

specified rate and at a predefined time, irrespective of the fact whether there are

profits or losses. Secondly, the borrowed capital is usually the secured capital. If the

company fails to meet its contractual obligations, the lenders of the borrowed capital

may enforce the sale of assets offered to them as security. Hence the risk on the part of

the company is more for debt compared to equity.

Control Factor : While planning the capital structure and more particularly while raising

additional funds, the control factor plays an important role, especially in case of closely

held private limited companies. If the company decides to raise the long term funds by

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 11/23

issuing further equity shares or preference shares, it dilutes the controlling interest of

the present shareholders / owners, as the equity shareholders enjoy absolute voting

rights and preference share holders enjoy limited voting rights. The control factor

usually does not come into the picture in case of borrowed capital unless the lender of

the long term funds, i.e. Banks or financial institutions, stipulate the appointment of

nominee directors on the Board of Directors of the company.

Constitution of Company : While deciding about the capital structure, the constitution of

the company plays an important role. In case of private limited company, the control

factor may be more important while in case of public limited company, cost factor may

be more important.

Characteristics of Company : Characteristics of the company, in terms of size, age and

credit standing play very important role in deciding capital structure. Very small

companies and the companies in their early stages of life have to depend more on the

equity capital, as they have limited bargaining capacity, they can’t tap various sources of

raising the funds and they do not enjoy the confidence of the investors.

Similarly, the companies having good credit standing in the market, may be in theposition to get the funds from the sources of their choice. But this choice may not be

available to the companies having poor credit standing.

Stability of Earnings: lf the sales and earnings of the company are not likely to be stable

enough over a period of time and are likely to be subject to wide fluctuation, the risk

factor plays more important role and the company may not be able to have more

borrowed capital in its capital structure as it carries more risk. However, if the earningsand sales of the company are fairly constant and stable over the period of time, it may

afford to take the risk, where the cost factor or control factor may play important role.

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 12/23

Attitude of the Management : lf the attitude of the management is too conservative; the

control factor may play an important role in capital structure decision. If the policy of

the management is liberal, the cost factor may get more importance.

Objects of Capital Structure Planning: While planning the capital structure, the following

objects of the capital structure planning come into play.

To maximize the earning per share of the company,

To issue the transferable securities and this can be ensured by listing the

securities on the stock exchange.

To issue the further securities in such a way that the value of shareholding of the

present owners is not affected.

External Factors

General Economic Conditions: While planning the capital structure, the general

economic conditions should be considered. If the economy is in the state of depression,

preference will be given to equity form of capital as it will be involving less amount of

risk. But it may not be possible always as the investors may not be willing to take the

risk. Under such circumstances, the company may be required to go in for borrowedcapital. If the capital market is in boom and the interest rates are likely to decline in

further, equity form of capital may be considered immediately, leaving the borrowed

form of capital to be tapped in future. It may also be possible to raise more equity

capital in boom as the investors may be ready to take risk and to invest.

Level of Interest Rates: If funds are available in the capital market, only at the higher

rates of the interest, the raising of capital in the form of borrowed capital may be

delayed till the interest rates become favorable.

Policy of Lending Institutions: If the policy of term lending institutions is rigid and harsh,

it will be advisable not to go in for borrowed capital, but the equity capital form should

be tapped.

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 13/23

Taxation Policy : Taxation policy of the Government has to be viewed from the angles of

both corporate taxation and as well as individual taxation. The return on borrowed

capital i.e. interest is an allowable deduction for income tax purposes while computing

taxable income of the company, while return on equity capital i.e. dividend is not

considered like that as it is the appropriation out of the taxable profits. As far as

individual taxation is concerned, both interest as well as dividend will be taxable in the

hands of lender of the capital subject to specified deductions available for the purposes.

Statutory Restrictions: The statutory restrictions prescribed by the Government and

various statutes are required to be taken into consideration before the capital structure

is planned. The company has to decide the capital structure within the overall

framework prescribed by the Government and various statutes.

ii) The company raised preference share capital of $ 100000 by theissue of 10% preference share of $ 10 each. The floatation cost is1%. Find out the cost of preference share capital issued at i) 10%premium ii) 10% discount

Answer:

Calculation of Cost of Preference Share Capital

Particulars Amount

Preference Share Capital $1,00,000

Value Per Share 10

Rate of Dividend on Preference Share 10%

Floatation Cost 1%

Prefence Dividend Per Year $10,000

Cost of Preference Share if issued at 10% Premium

No. of Preference Shares Issued 10000

Price per share @ 10% Premium $11

Cash inflow by issuing shares $1,10,000

Less: Floatation Cost $1,000

Net Proceeds by issuing Preference Capital $1,09,000

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 14/23

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 15/23

Debt 5% 400000 380000

Calculation of Book Value weights to determine the WACC

Types of Capital Specific Cost Book Value (in $) WeightsE F G H

Preference Capital 8% 100000 0.0769

Equity Capital*

13%

(600000+200000)=80000

0 0.6154

Debt 5% 400000 0.3077

*Equity Capital = Retained earnings + Surplus & Reserve + Paid Up Capital

Weighted Average Cost of Capital using Book Value = 0.0769*8 + 0.6154*13 +

0.3077*5

= 10.15%

b) Market value weights.

Answer:

Calculation of Market Value weights to determine the WACC

Types of Capital Specific Cost Market Value (in $)

Preference Capital 8% 110000 0.0651

Equity Capital 1* 13% 1200000 0.7101

Debt 5% 380000 0.2249

1* Equity Capital = Retained earnings + Surplus & Reserve + Paid Up Capital

Weighted Average Cost of Capital using Market Value 10.88%

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 16/23

How are they different? Can you think of a situation where the WACCwould be the same using either of the weights?

Answer:

Calculation of Weighted Average Cost of Capital using market value weights is differentfrom using book value weights. Since, we know that there is always a difference in the

book value of the equity compared to its market value, which leads to different

Weighted Average Cost of Capital.

WACC using either of the weights could be same only if the market value and the book

value are same. It means that there is no difference in the market value of the Equity,

Preference Capital & Debt compared to its book value.

Ques 3 Calculate the degree of operating leverage (DOL), degree offinancial leverage (DFL), degree of combined leverage (DCL), for thefollowing firms:

Firm AFirm

B Firm COutput(units) 90000 35000 200000

Fixed Costs (USD) 10000 16000 2000Variable cost per

unit 0.2 1.5 0.02Interest onborrowed funds 4000 8000 -Selling price per

unit 0.6 5 0.1

Answer:

Particulars Firm A Firm B Firm C

Output 90000 35000 200000

Selling Price Per Unit 0.6 5 0.1

Sales 54000 175000 20000

Fixed Cost 10000 16000 2000

Variable Cost 0.2 1.5 0.02

Interest on Borrowed Funds 4000 8000 0

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 17/23

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 18/23

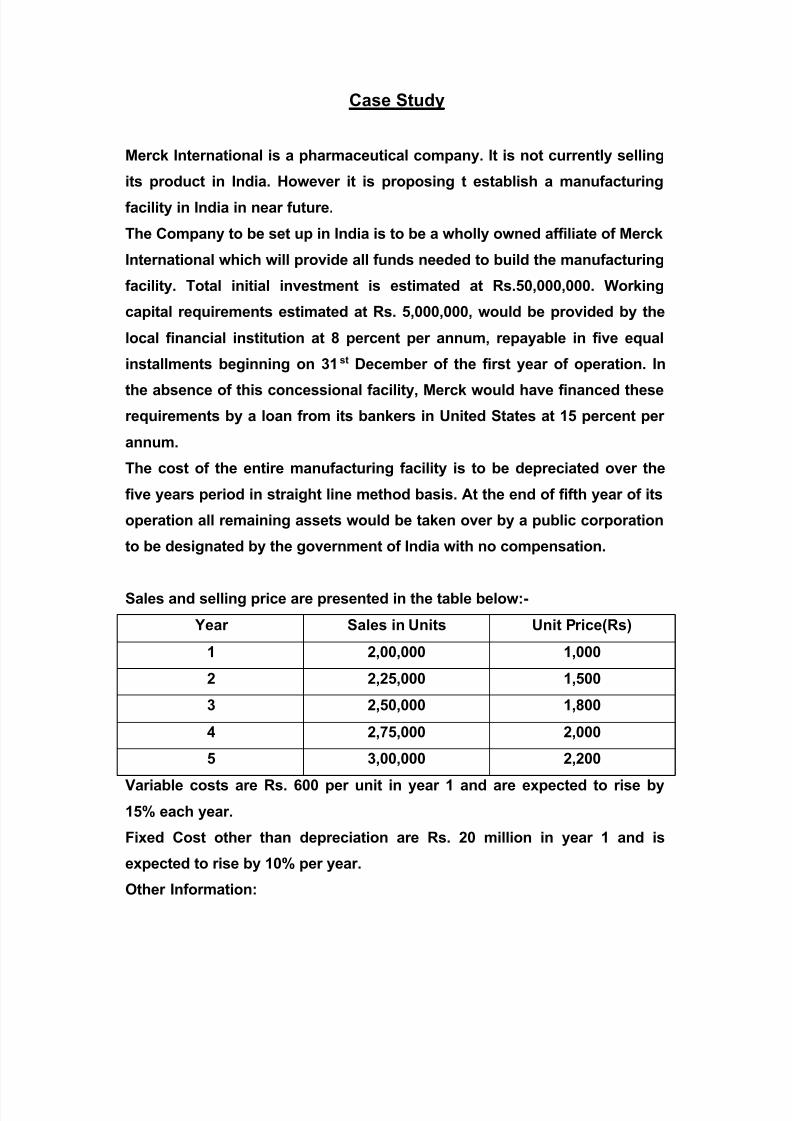

Case Study

Merck International is a pharmaceutical company. It is not currently selling

its product in India. However it is proposing t establish a manufacturing

facility in India in near future.

The Company to be set up in India is to be a wholly owned affiliate of Merck

International which will provide all funds needed to build the manufacturing

facility. Total initial investment is estimated at Rs.50,000,000. Working

capital requirements estimated at Rs. 5,000,000, would be provided by the

local financial institution at 8 percent per annum, repayable in five equal

installments beginning on 31st December of the first year of operation. In

the absence of this concessional facility, Merck would have financed these

requirements by a loan from its bankers in United States at 15 percent per

annum.

The cost of the entire manufacturing facility is to be depreciated over the

five years period in straight line method basis. At the end of fifth year of its

operation all remaining assets would be taken over by a public corporation

to be designated by the government of India with no compensation.

Sales and selling price are presented in the table below:-

Year Sales in Units Unit Price(Rs)

1 2,00,000 1,000

2 2,25,000 1,500

3 2,50,000 1,800

4 2,75,000 2,000

5 3,00,000 2,200

Variable costs are Rs. 600 per unit in year 1 and are expected to rise by

15% each year.

Fixed Cost other than depreciation are Rs. 20 million in year 1 and is

expected to rise by 10% per year.

Other Information:

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 19/23

All profit after tax realized by the affiliate are transferable to the parent

company at the end of each year. Depreciation funds are to be blocked

until the end of year 5. These funds may be invested in local money market

instruments, fetching a tax-free return of 15%. When the operating assets

are turned over a local corporation, the balance of these funds including

interest may be repatriated.

The income tax rate in India is 48% but there are no with holding tax on

transfer of dividends. Dividends received by Merck International in the

United states would be subject to 50% tax.

Merck International uses a 20% weighted average cost of capital for

evaluating domestic projects similar to the ones planned in India. For

Foreign projects in developing countries a 6% political premium is added.

Calculate the NPV and IRR for the project from the standpoint of the parent

company. What are your recommendations for the proposal?

Answer:

Total initial investment Rs.50, 000,000 Merck International

Working capital (India) Rs.50, 000,000 by commercial institution in India @ 8% loan

per annum which is payable in 5 equal investments beginning 31st December of the first

year of operation.

OR form USA @ 15% interests.

Depreciation for 5 years @ straight line method basis

After 5 years nationalizing of the project in India with no compensation and all the

remaining assets will be taken.

Year Sales Unit Unit price

1 200,000 1,000

2 22,5000 1,500

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 20/23

3 250,000 1,800

4 275,000 2,000

5 300,000 2,2000

Profits after = Transferred to USA

Depreciation is to be blocked till end of year 5

Provision for depreciation to be terminated in local money market @ tax free return

15%

WACC (in USA) =20%

WACC (foreign project) = 6%+20=political premium

IRR=TIV=TBi) R 50,000,000

ii) WC=5,000,0000(8% per interest)

FV=PV (1+r) n

FV=5,000,000(1.08)5

FV=7,346,640.384

WC=7,346,640

So annual installment =1,469,328Total initial investment =55M

Year Sales in Units Price Sales revenue Available Cost

1 200,000 1,000 200,000,000 120,000,000

2 225,000 1,500 337,500,000 155,250,000

3 250,000 1,800 450,000,000 198,375,000

4 275,000 2,000 550,000,000 250,944,375

5 300,000 22,000 660,000,000 314,821,110

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 21/23

Fixed Costs Earnings throughout the year

20,000,000 60,000,000

22,000,000 160,250,000

24,200,000 22,7425,00026,620,000 272,435,625

29,282,000 315,998,000

Manufacturing facility=50,000,000

Depreciation =value of manufacturing facility

No of years

50 = 10M

Accumulated value of depreciation =A ((1+K) n-1)

K

=10((1+15%)5-1)

0.15

At the end of 5 years Depreciation interest = 67423812.5

Year Earning Depreciation 48% Indian

taxation

Net earning Merk international

net earnings

1 60,000,000 10M 24M 26M 13M

2 160,250,000 10M (72.12) 78.13M 39.065M

3 227,425,000 15M (104.364) 113.061M 56.5305M

4 272,435,625 15M (125.9691) 136.466552M 68.23326

5 315,898,000 10M (146.83104) 159.0669M 79.53M+67.4233/2

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 22/23

79.5M+33.712M

113.212M

Discounting factor Present value Initial investment

1/1.26)5 4.0935M -45.906

1/1.26)4 15.5M -30..4065

1/1.26)3 28.26M -2.1465

1/1.26)2 42.979M -40.823

1/1.26)1 89.874M

Net present value=180.7065M

28.26M+42.979M/2=35.6195

IRR=35.6195/180.7055

0.1971135

IRR=19.71%

8/18/2019 Assign AMB204 - Intern. Financial Mangmt - M.ombe

http://slidepdf.com/reader/full/assign-amb204-intern-financial-mangmt-mombe 23/23

Assignment – C

1: B

2 :B

3: D

4: A

5: D

6: D

7: C

8: C

9: A

10: A

11: B

12: A

13: B

14:D

15: I

16: 1V

17: II

18: II

19: IV

20: I

21: I

22: I

23: I

24: II

25: IV

26: II

27: IV

28: I

29: III

30: II

31: I

32: II

33: I

34: II

35: II

36: I

37: I

38: I

39: II

40: II