Asset liability management-in_the_indian_banks_issues_and_implications

Upload

jingli-liCategory

view

232download

2description

Asset-liability Management for Golden Gate Bank Annuity

Jingli Li (661138638)

Executive Summery

By using the expected value with respect to one unit risk (the ratio of expected return/standard deviation), I find out that among the 4-year bonds and 5-year bonds the top four bonds with high ratio are Morgan Stanley D W DISC SRMTNS with price 106.25, GE CAPITAL INTERNOTES with price 113.19, GE CAPITAL INTERNOTES with price 113.95, and Federal Home Loan with price 112.22.

After the optimal portfolio selection, I obtain three different portfolios. After duration analysis, and gap analysis, I decide to use 1113200 Morgan Stanley D W DISC SRMTNS with price 106.25 to meet the obligation at the end of year 4 and 1620785 Federal Home Loan Banks with price 112.22 to meet the obligation at the end of year 5. Approximately, the asset portfolio is consisted of 40% investment into Morgan Stanley bonds and 60% investment into Federal Home Loan Banks bonds. In addition, in stress testing, my portfolio also stands well.

Then I did the Credit Risk analysis of this portfolio. Below is the credit VaR for my portfolio:

One-Year Credit VaR 335835929.364

Two-Year Credit VaR 326646641.862

Three-Year Credit VaR 315119923.219

Four-Year Credit VaR 27262885.79

Five-Year Credit VaR

However, I should notice that, even with my optimal portfolio, the probability that I can meet the liability requirements at both 4th year and 5th year is only about 47.8%, and the probability that I could not meet the obligation requirements at both 4th year and 5th year is as large as 44.4%. Therefore, my suggestion is, in order to meet the liability requirement from the annuities, I need to increase the size of our assets.

Project background

Janet Beach, head of an Asset-Liability Management group, faces a task to deal with the asset-liability management for JH Financial Services. She is required to design an investment strategy that will better match the distribution of the liabilities and assets. I am assigned to work on this project in Janet’s group.

The portfolio of annuities has a net accrued premium of $ 300 million, which will be covered by the pool of 24 bonds with a 4-year or 5-year maturity. The annual yield of these annuities will be tracked by a bond index, normally distributed with an expected annual yield of 3.5% and an annual standard deviation of 2%. Benefits payment for the annuities will be paid respectively 40% at the end of 4th year, and the rest will be paid at the end of 5th year.

Assumption

Before presenting the detailed analysis, I summarize the assumptions stated in this report.

First, in the section of annuity liabilities analysis, the annuity liabilities grow at the simple interest rate each year. The rest unpaid liability at the end of 4th year will grow at the fifth year growth rate.

Second, in the section of corporate bonds selection, the coupons are paid annually at the end of November; Accrued coupon payments appreciate at an annual 1 year T-Bill rate of 0.8%; Bonds belong to the senior secured seniority class for recovery rates calculation; 5 year bonds can be sold in the 4 th year; the bond’s default only appear the end of maturity

Third, in the section of bonds return and standard deviation calculation, the default for bonds is assumed to happen at the end of maturity. And, it is assumed to ignore the bond’s grade change among periods for convenient.

Fourth, in the section of asset-liability analysis, the cumulative gap will be calculated by the sum of single period gap from 2017 and 2018. Considering the 1-year T-Bill rate is 0.8%, I decide that the time value will be ignored when the gap from 2017 is added into the gap 2018.

Fifth, in the appendix, the amount of bonds and the portion of bonds are rounded to the integer. So, the rounding error may appear. But, the amount caused by such error is much small compared with total investment. So, I decide to ignore it.

Analysis of Annuity Liabilities

According to the case, the information of annuity liabilities is summarized in table 1:

Table 1 Summary of annuity liabilitiesCurrent Portfolio (Millions) $300Payment at year 4 40%Growth rate (Expected Value) 0.05Margin 0.015Standard Deviation 0.02

I use excel to simulate liability of each year by using NORMINV to generate 1000 results. And then I get the Net Worth and Payments at the end of year 4 and year 5. Please see the results in Appendix Annuity Liabilities.

Bonds Selection

1) Basic idea

Basically there are three kinds of bonds:

A. 4 year bonds at year 4 plus accrued coupons

B. 5 year bonds at year 4 plus accrued coupons

C. 5 year bonds at year 5 plus accrued coupons

I think that bonds in class A and class B can be used to match liabilities in year 4, and bonds in class C can only be used to match liabilities in year 5. On the bond selection criteria, the basic idea is to select the bonds with the top four high expected bond return respect to one unit risk. So next, the calculation of bonds expected values and standard deviations will be discussed further in this report.

2) 4-year Transition Matrix

First of all, in order to calculate the net worth of the bond at the end of year 4 and year 5, I need to calculate the 4-year debt migration Matrix. Since I already have the 1-year Matrix, I can easily get the 4-year one by matrix computation, or the Excel function MMULT. Please see the 4-year Migration Matrix in Appendix 2-year, 3- year, 4-year and 5-year Transition Matrix.

3) The valuation process of bonds

a) 4-year bond at the end of year 4The way I calculate the value of 4-year bond at the end of year 4 is straightforward. Take the 4 Year Bond “MORGAN STANLEY D W DISC SRMTNS” as an example.

Table 2 4 Year Bond MORGAN STANLEY D W DISC SRMTNSCoupon 6.875% Principle($) 100

Default Probability 0.44% 1-year T-Bill 0.80%Recovery Rate 53.8%

Year CF At the year 41 $6.88 $7.042 $6.88 $6.993 $6.88 $6.934 $106.64 $106.64

Sum - 127.60

In table 2, at the end of year 4, if the bond does not default, the cash flow from the bond would be $100 (principle) + $6.88 (interest payment for year 4); if it defaults, the recovery rate is 53.8%. So the expected cash flow would be: $106.64 and this is also the market value of the bond at the end of year 4.

If I consider the coupon payments at previous years as cash assets, as I discussed earlier in this report, then the total assets payment at the end of year 4 will be $127.60

b) 5-year bond at the end of year 5Likewise, using the same approach, I can calculate the value of the 5-year bond at the end of year 5. Take the 5 Year Bond “FEDERAL HOME LOAN BANKS” as an example:

Table 3 5 Year Bond FEDERAL HOME LOAN BANKSCoupon 3.75% Principle($) 100

Default Probability 0.04% 1-year T-Bill 0.80%Recovery Rate 53.8%

Year CF At the year 41 $6.88 $7.042 $6.88 $6.993 $6.88 $6.934 $106.64 $106.64

Sum - 127.60

c) 5-year bond at the end of year 4In order to meet the premium payment, I might need to sell some of the 5-year bonds at the end of year 4. So it is necessary for us to calculate the value of the 5-year bonds at the year of 4.

By calculating the probabilities and price at each possibly bond classes, I can get the expected value of the bond at the end of year 4. Take the Take the 5 Year Bond “GE CAPITAL INTERNOTES” as an example: In table 4.1, it shows that the change of bond grade affect the expected value at the end of year 4.

Table 4.1 5 Year Bond GE CAPITAL INTERNOTESCoupon 5.00%

Principle($)

100

Price $116.01r(4,5) CF(5) Price(4) Coupon(4) Prob. Weighted Price

AAA 6.30% 105.00 98.78 5.00 2.13% 2.21AA 6.35% 105.00 98.73 5.00 68.71% 71.28A 6.50% 105.00 98.59 5.00 23.74% 24.59

BBB 6.78% 105.00 98.33 5.00 3.93% 4.07BB 8.75% 105.00 96.55 5.00 0.70% 0.71B 10.00% 105.00 95.45 5.00 0.59% 0.59

CCC/C 12.00% 105.00 93.75 5.00 0.08% 0.08D 53.80 0.00 0.11% 0.06

Expected value at the end of year 4 103.59

Considering the previous coupons, the total value can be summarized in the table 4.2:

Table 4.2 5 Year Bond GE CAPITAL INTERNOTESCoupon 5.00% Principle($) 100

1-year T-Bill 0.80% Recovery Rate 53.8%Year CF FV

1 $5.00 $5.122 $5.00 $5.083 $5.00 $5.044 $103.59 $103.59

Sum $118.83

In table 5.1, the GE bond’s return is calculated by using the expected value of the bond from table 4.1 and table 4.2 and the price of the bond. Like, ($118.83-$116.01)/ 116.01= 0.02433, (namely, 2.433%)

The standard deviation of the GE bond is just the standard deviation of the return of the bond. According to, at the end of year 4, the GE bond will suffer the change of grade from AA to AAA, AA to A, AA to BBB, AA to BB, AA to B, AA to CCC/C, or AA to D or keep the original grade AA, the standard deviation of GE bond can be calculated. Take one grade change as an example. The standard deviation from AA to AAA can be calculated as {[($103.78+$5.12+$5.08+$5.04)/116.01-1]-2.433}^2*2.13%= 5.52728E-08; Similarly, the standard deviation for the rest can be calculated in the same way.

About the bonds sold at maturity, the standard deviation can be calculated as above. Table 5.2, 5.3 and 5.4 show the different return under expected value, no-default value and default value of the bond MORGAN STANLEY D W DISC SRMTNS.

Table 5.2 Expected Value of MORGAN STANLEY D W DISC SRMTNSCoupon 6.88% Price $106.25

1-year T-Bill 0.80% YTM 5.167%Year CF FV Return

1 $6.88 $7.04 20.09%2 $6.88 $6.993 $6.88 $6.934 $106.64 $106.64

Net Value $127.60

Table 5.3 Non- default Value of MORGAN STANLEY D W DISC SRMTNSCoupon 6.88% Price $106.25

1-year T-Bill 0.80% YTM 5.167%Year CF FV Return

1 $6.88 $7.04 20.31%2 $6.88 $6.993 $6.88 $6.934 $106.88 $106.88

Net Value $127.83

Table 5.4 Default Value of MORGAN STANLEY D W DISC SRMTNSCoupon 6.88% Price $106.251-year T-Bill 0.80% YTM 5.167%Year CF FV Return1 $6.88 $7.04 -29.64%2 $6.88 $6.993 $6.88 $6.934 $53.80 $53.80Net Value $74.76

The standard deviation for bond MORGAN STANLEY D W DISC SRMTNS is 3.29%.

4) Bonds valuation and standard deviation

For now I have all the value and standard deviations for all the bonds. Please see the results in Appendix Bonds’ return & STD at Year 4, and Bonds’ return & STD at Year 5.

5) The selection of bonds

Based on the results in Appendix, I summarize the ratio of bond’s expected return to its standard deviation into a new table and put it into the appendix called ratio summary. According to the summary, the top four bonds with high expected return respect to unit risk both in above three categories are MORGAN STANLEY D W DISC SRMTNS with price $106.25, GE CAPITAL INTERNOTES with price $113.95, GE CAPITAL INTERNOTES with price $113.19, and FEDERAL HOME LOAN BANKS with price $112.22. Next, the amounts of bonds and name of bonds will be selected by using excel solver function after the asset distribution generated.

Allocation of Assets

After choosing the above four bonds invested in assets management, I need to decide how much I am going to allocate into each bond. In order to optimal the asset-liability structure, I first need to figure out the distribution of assets and liabilities. Because the assets and liabilities have totally different distributions, I decide to use simulation method to project the asset-liability structure, and then assess the characteristic of the structure.

About the distribution of assets, 1000 random numbers between 0 and 1 are first generated. According to the random numbers and the default probability for a bond from the debt migration matrix, the distribution of four bonds can be generated separately. In addition, as I discussed before, the growth of the liabilities follows a normal distribution with the mean of 3.5% (5% growth of bond index our annuity follows minus 1.5% commissions) and the standard deviation of 1.5%.

Thus, I could form the asset-liability distributions at the end of year 4 and year 5. The table below is an abstract of our simulation.

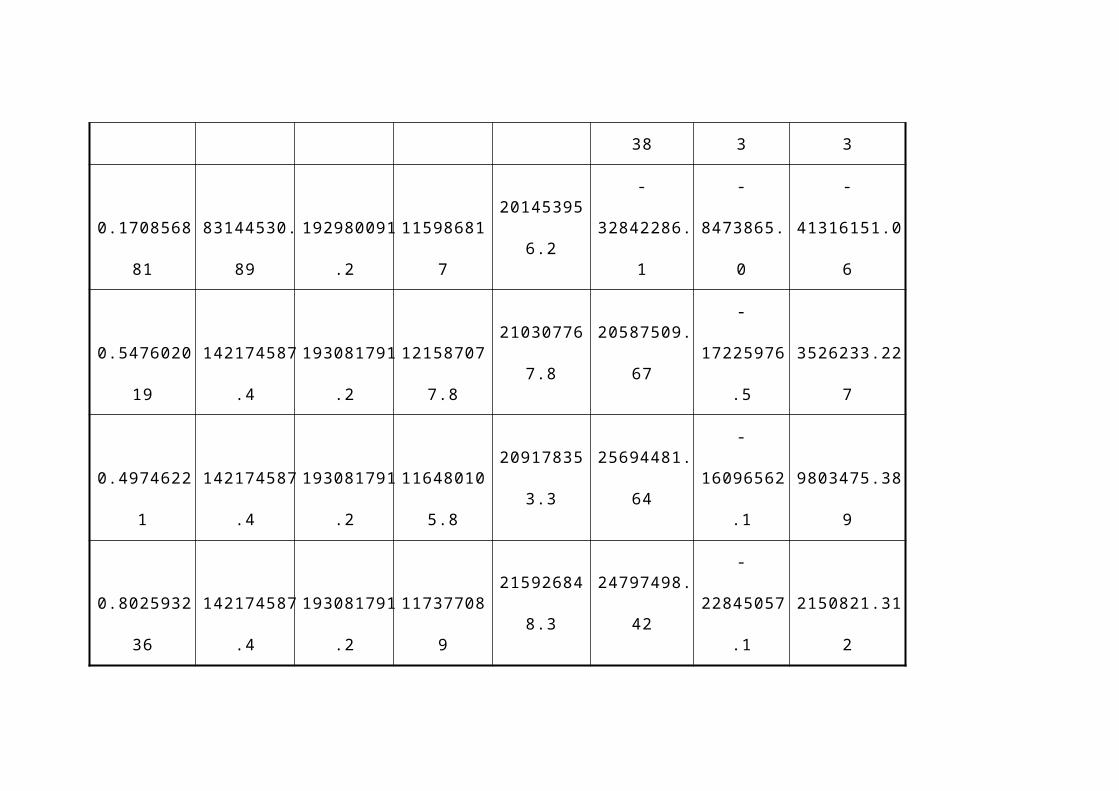

Table 6 Abstract of Asset-Liability Distributions and Gap Analysis

RandomPortfolio

Value 2017Portfolio

Value 2018Liability

Value 2017Liability

Value 2018Gap (1) Gap (2)

Cumulative Gap

0.945003538 142174587.4 193081791.2 115336392.4 221882189.2 26838194.99 -28800397.9 -1747497.3640.810190378 142174587.4 193081791.2 110665133.8 216202225.7 31509453.58 -23120434.4 8641094.7650.136738857 83144530.89 192980091.2 120256095.3 200006204.5 -37111564.38 -7026113.3 -44137677.630.170856881 83144530.89 192980091.2 115986817 201453956.2 -32842286.1 -8473865.0 -41316151.060.547602019 142174587.4 193081791.2 121587077.8 210307767.8 20587509.67 -17225976.5 3526233.2270.49746221 142174587.4 193081791.2 116480105.8 209178353.3 25694481.64 -16096562.1 9803475.3890.802593236 142174587.4 193081791.2 117377089 215926848.3 24797498.42 -22845057.1 2150821.312

First I choose a random number from 0 to 1. Then treating the random number as the cumulative probability and implying it into the distributions of asset payments, I can obtain the value of asset portfolio at the end of year 4 and at the end of year 5 correspondingly. In addition, I also use the projected payment obligations simulated from first year to the fifth year at random growth rate in the annuity liability section. Here are several gaps I need to pay attention to. Gap (1) is the difference between the total assets value and the payment liabilities (40% of the total liabilities) at the end of year 4. Gap (2) is the difference between the total assets value and the total liabilities at the end of year 5. The last column, the cumulative gap is the cumulative gap of year 4 and year 5, equal to the sum of Gap (2) and Gap (3). I simulate for 1,000 times and summarize the mean and standard deviation of each column. (The table is in the appendix called asset- liability analysis)

Next, I need to choose an optimal object (via solver of Excel). According to my analysis, the best asset-liability management should maximize the net worth of my portfolio, which could be reflected by the gap of each year. The conditions used in solver function include: the amount of four bonds are larger than or equal to zero; optimal portfolio is 100% investment into four bonds; and both the mean of 2017 gap and cumulative gap are required to be larger than zero. I decide to choose the third condition because I think that it is important to first satisfy the debtors in 2017 and then use the extra money from gap in 2017 and asset matured at the end of 2018 to pay for the liability in 2018 as much as possible. All portfolios are listed in table 7. One of objectives I try is to minimize the standard deviation of 2017 gap. The generated portfolio has the drawbacks: although it control the standard deviation in 2017 gap, that at the end of year 5 and cumulative gap are not optimized, with one large positive

and one large negative. As manager, I do not want to see such a misbalance between these two years. Thus, I directly exclude this portfolio and consider the other portfolios.

There are three optimal portfolios:

One is 41% investment into Morgan Stanley bonds and 59% investment into Federal Loan bonds. This portfolio could maximize the gap at the end of year 5, maximize the gap at the end of year 4 and guarantee the gap at the end of year 4 is not less than zero, as well as minimize the standard deviation of the gap at the end of year 5.

One is 40% investment into Morgan Stanley and 60% investment into Federal Loan bonds. This portfolio could minimize the standard deviation of the cumulative gap.

One is 48% investment into Morgan Stanley bonds and 52% investment into Federal Loan bonds. This portfolio could maximize the gap at the end of year 4.

Therefore, I need to analyze these three portfolios further and choose a better one.

Table 7 Summary of Optimal Portfolio with Gap Analysis4y Gap 5y Gap Cumulative Gap

MS (%)GE1(%)

GE2(%)

FL(%) Mean SD Mean SD Mean SD

Maximize Cumulative Gap 41.00 0 0 59.00 1.51115E-08 29752946.09 -18001822.07 12174685.93 -17884653.05 27983397.42Minimize SD of Cumulative Gap 40.00 0 0 60.00 -9.98137E-07 29752946.09 -18001822.07 12174685.93 -17884653.05 27983397.42Maximize 5y Gap (4y Gap > 0) 41.00 0 0 59.00 1.51115E-08 29752946.09 -18001822.07 12174685.93 -17884653.05 27983397.42Maximize 4y Gap (5y Gap > 0) 48.00 0 0 52.00 19855393.82 34776529.24 -39416799.6 11107442.13 -19337880.31 32088880.78

Minimize SD of 4y (4y Gap > 0) 1.00 0 0 0 177067847.9 74789418.97 -208978381.1 8006447.51 -30493990.41 69143487.3Minimize SD of 5y (5y Gap > 0) 41.00 0 0 59.00 1.51115E-08 29752946.09 -18001822.07 12174685.93 -17884653.05 27983397.42

Note: “MS” is MORGAN STANLEY D W DISC SRMTNS bond with price $106.25; “GE1” is GE CAPITAL INTERNOTES with price $113.95; “GE2” is GE CAPITAL INTERNOTES with price $113.19, “FL” is FEDERAL HOME LOAN BANKS with price $112.22

In the appendix portfolio selection and gap analysis, all my works are showed.

Duration Analysis:

Next, I examine the duration of the asset-liability structure to determine whether these two portfolios could react well to the change of interest rate. The table below shows the calculation procedure of the duration. Again, I use the simulation method to project the duration for 1,000 times, and then summarize the mean and standard deviation of the duration. In the appendix duration analysis, all results are listed

Table 8.1 Abstract of Duration Analysis for 41% into Morgan Stanley bonds and 59% into Federal Loan bonds

Liability at 4y Liability at 5y Duration of LiabilityAsset Portfolio at

4yAsset Portfolio at

5yDuration of A

115336392.4 221882189.2 4.657977351 142302419.2 192958362.5 4.575547076110665133.8 216202225.7 4.661437184 142302419.2 192958362.5 4.575547076120256095.3 200006204.5 4.624507489 83219287.66 192958362.5 4.698674793115986817 201453956.2 4.634619032 83219287.66 192958362.5 4.698674793

121587077.8 210307767.8 4.633657831 142302419.2 192958362.5 4.575547076116480105.8 209178353.3 4.642324335 142302419.2 192958362.5 4.575547076

Mean 4.644450036 Mean 4.628874624STD 0.012392465 STD 0.061086619

Note: I assume that the payment liabilities and assets only occur at the end of year 4 and the end of year 5.

Thus:DurationL(¿ A )=4∗L4+5∗L5

L4+L5

Table 8.2 Abstract of Duration Analysis for 40% into Morgan Stanley bonds and 60% into Federal Loan bonds

Liability at 4y Liability at 5y Duration of LiabilityAsset Portfolio at

4yAsset Portfolio at

5yDuration of A

115336392.4 221882189.2 4.657977351 142302419.3 192958362.5 4.575547072110665133.8 216202225.7 4.661437184 142302419.1 192958362.5 4.575547071120256095.3 200006204.5 4.624507489 83219287.61 192958362.4 4.698674794115986817 201453956.2 4.634619032 83219287.60 192958362.5 4.698674793

121587077.8 210307767.8 4.633657831 142302419.1 192958362.2 4.575547079116480105.8 209178353.3 4.642324335 142302419.1 192958362.3 4.575547072

Mean 4.644450036 Mean 4.628874532STD 0.012392465 STD 0.061086634

Table 8.1 Abstract of Duration Analysis for 48% into Morgan Stanley bonds and 52% into Federal Loan bonds

Liability at 4y Liability at 5yDuration of

LiabilityAsset Portfolio at

4yAsset Portfolio at

5yDuration of A

115336392.4 221882189.2 4.657977351 166815804.6 171323778.4 4.506665848110665133.8 216202225.7 4.661437184 166815804.6 171323778.4 4.506665848120256095.3 200006204.5 4.624507489 97554858.9 171323778.4 4.637178841115986817 201453956.2 4.634619032 97554858.9 171323778.4 4.637178841

121587077.8 210307767.8 4.633657831 166815804.6 171323778.4 4.506665848116480105.8 209178353.3 4.642324335 166815804.6 171323778.4 4.506665848

Mean 4.644450036 Mean 4.56319367STD 0.012392465 STD 0.064749136

The durations of liabilities are rounded to about 4.64. The durations of assets of the former portfolio are rounded to 4.62, 4.62, and 4.56, while the standard deviations are rounded to 0.061, 0.061 and 0.064. The differences are not significant. The duration gaps of assets and liabilities in these portfolios are small, meaning that when the interest rate change, the change in the value of assets and liabilities can offset with each other to a great extent. Thus, these three portfolios both perform well from the view of duration.

Gap Analysis:

I look further into the gap of these three portfolios. I count the number of simulations when gaps of both years are larger than zero and that when gaps of both years are less than zero.

Below is an abstract table of the calculation for the portfolio with 41% investment into Morgan Stanley Bonds and 59% investment into Federal Loan Bonds.

Table 9.1 Abstract of Gap Analysis for 41% investment into Morgan Stanley Bonds and 59% investment into Federal Loan Bonds

Gap at 4y Gap at 5y Cumulative Gap Number of both Gap larger than 0

Number of both Gap less than 0

26966026.75 -28923826.6 -1742071.66 0 031637285.34 -23243863.2 8646520.469 1 0-37036807.62 -7047842.0 -44084649.58 0 1-32767529.33 -8495593.7 -41263123.01 0 120715341.44 -17349405.2 3531658.931 1 025822313.4 -16219990.8 9808901.093 1 024925330.18 -22968485.8 2156247.017 1 0-25586540.82 -12433339.1 -38019879.9 0 1-31932491.3 -6091278.5 -38023769.78 0 1-30884812.03 -6760299.2 -37645111.19 0 130188152.4 -15112841.6 15316816.04 1 0

-31233070.68 -76305347.9 -107538418.6 0 1Sum 473 444

Implementing the same process for other portfolios, I can reach to the result that:

Table 9.2 Abstract of Gap Analysis for 40% investment into Morgan Stanley Bonds and 60% investment into Federal Loan Bonds

Gap at 4y Gap at 5y Cumulative GapNumber of both Gap

larger than 0Number of both Gap less than 0

26966026.75 -28923826.6 -1742071.66 1 031637285.34 -23243863.2 8646520.469 1 0-37036807.62 -7047842.0 -44084649.58 0 1-32767529.33 -8495593.7 -41263123.01 0 120715341.44 -17349405.2 3531658.931 1 025822313.4 -16219990.8 9808901.093 1 024925330.18 -22968485.8 2156247.017 1 0-25586540.82 -12433339.1 -38019879.9 0 1-31932491.3 -6091278.5 -38023769.78 0 1-30884812.03 -6760299.2 -37645111.19 0 130188152.4 -15112841.6 15316816.04 1 0

-31233070.68 -76305347.9 -107538418.6 0 1Sum 476 444

Table 9.3 Abstract of Gap Analysis for 48% investment into Morgan Stanley Bonds and 52% investment into Federal Loan Bonds

Gap at 4y Gap at 5y Cumulative GapNumber of both Gap

larger than 0Number of both Gap less than 0

51479412.12 -50558410.8 1332836.635 1 056150670.71 -44878447.3 11721428.76 1 0-22701236.38 -28682426.1 -51383662.5 0 1-18431958.09 -30130177.8 -48562135.92 0 145228726.8 -38983989.4 6606567.226 1 050335698.77 -37854575.0 12883809.39 1 049438715.54 -44603070.0 5231155.311 1 0-11250969.58 -34067923.2 -45318892.82 0 1-17596920.06 -27725862.6 -45322782.69 0 1-16549240.79 -28394883.3 -44944124.1 0 154701537.76 -36747425.7 18391724.34 1 0-16897499.44 -88862858.5 -105760357.9 0 1

Sum 469 444

Under the second portfolio, the number of simulations when both gaps are larger than zero is higher than that under the first portfolio. Also, the number of simulations when both gaps are less than zero is same. Thus, I can conclude that, the second portfolio outperforms the first one and the third one in increasing the probability of achieving positive gaps in both years and in decreasing the probability of achieving negative gaps in both years. So from this point of view, it's better to choose the second one as the optimal portfolio.

Stress Testing

T-Bill rate decreases to 0.4%

When T-Bill rate decrease to 0.4%, our every year cumulative coupon will decrease, I calculated the cumulative coupon and the results are summarized into the appendix stress testing.

Considering the cumulative coupon changes, my total value of the asset every year will also change, by calculating, I get the result as follows:

4 year Gap 5 year Gap Cumulative GapMean STD Mean STD Mean STD

Portfolio-10.23103E-07 2989946.09 -19801822.07 11174685.93

-18103653.05

27983405.42

Compared to original state, I find that gap changed very slightly due to the value of both asset and liability changed small. My portfolio still matches asset-liability well.

Credit VaR Analysis

Next, I do the credit assessment for the portfolio. I decide to use Credit VaR approach to assess the portfolio at each year. I generate the Debt Migration Matrix and the forward yield curve for each time period, and then evaluate our portfolio. Assuming the credit migration for these two bonds are independence, by calculating the expected value of the portfolio at each year and the change of the portfolio value in the worst scenario at 99% confidential level, I can have the Credit VaR for this portfolio at 99% confidential level. The calculation process is presented into the appendix called Credit VaR.

Table 10 Summary of Credit VaR for 40% investment into Morgan Stanley Bonds and 60% investment into Federal Loan Bonds

One-Year Credit VaR 335835929.364

Two-Year Credit VaR 326646641.862

Three-Year Credit VaR 315119923.219

Four-Year Credit VaR 27262885.79

Five-Year Credit VaR

Conclusion

I choose two bonds, Morgan Stanley and Federal Home loan, to invest in, with 40% into Morgan Stanley and 60% into Federal Home loan. And I also do gap analysis, duration analysis and Credit VaR analysis for this portfolio. I should notice that, even with our optimal portfolio, the probability that I can meet the liability requirements at both 4th year and 5th year is only about 47.8%, and the probability that I could not meet the obligation requirements at both 4th year and 5th year is as large as 44.4%. Therefore, my suggestion is, in order to meet the liability requirement from the annuities, I need to increase the size of our assets.

Appendix

Additional review of annuity products:1. Conception:In the United States an annuity is created as a contract between an insured party, usually an individual, and a life

insurance company. Under this situation, an insured party make a lump-sum payment or a series of payment and a life insurance company agrees to make periodic payments distributed to the insured party over time.

Annuity contract traditionally provides a guaranteed distribution of income beginning immediately or at some future time, such as via fixed payments. The formula of the present value of annuity which has n year maturity is presented below:

P=A×( 1i− 1

i (1+i )n)

P presents present value of annuity, and A presents annuity, and i presents rate of return.

2. Variable annuity and Fixed annuityVariable annuity:During the accumulation period, you can choose to allocate your purchase payments from among a number of

investment options. The amount of money you have allocated to each mutual fund investment option will be determined depending on the fund's performance.

Fixed annuity:Insurance company makes fixed payments to the annuitant in term of the contract over the annuitant’s lifetime.

3. Immediate annuityA common use for an immediate annuity might be to provide a pension income. In the U.S., the tax treatment of a

non-qualified immediate annuity is that every payment is a combination of a return of principal (this part is not taxed) and income (this part is taxed not with capital gain rates but with ordinary income rates). The formula of the current value of immediate annuity which has n year maturity is presented below:

P=A(1−(1+i )−(n−1 ))

1+i

4. PerpetuitiesA perpetuity is an annuity which has infinite maturity and a stream of cash payments that continues forever. There

are few actual perpetuities in existence, for example, scholarship. The conception of perpetuity is closely linked to terminal value and terminal growth rate in valuation. The formula of the current value of perpetuities which has n year maturity is presented below:

P= Ai

5. Deferred annuityDeferred annuity is a type of annuity contract which delays payments of income, installments or a lump sum until

the investor chooses to receive them. Two main phases associated with deferred annuity. The one is the savings phase in which you invest money into the account and the other one is the income phase in which the plan is converted into an annuity. A deferred annuity can be either variable or fixed. The formula of the present value of perpetuities which has n year maturity is presented below:

P= Ai×(1− 1

(1+i )n)× 1

(1+i)m

n presents annuity maturity and m presents deferred maturity.

Formula sheet

1. Liability: Payment at the end of year 4: 300* 10^6*(1+r1)*(1+r2)*(1+r3)*(1+r4)*0.4Payment at the end of year 5: 300* 10^6*(1+r1)*(1+r2)*(1+r3)*(1+r4)*0.6*(1+r5)

r1, r2,r3,r4,r5 represents the random numbers generated by using rand() in excel

2. PV=∑i=1

n cf (i)(1+r)i

+ FV(1+r )n

STD (stated in the report with example) Expected Value (stated in the report with example) Expected Return (stated in the report with example)

3. Forward Rate= j−i√ (1+r ( j ))j

¿¿¿ ¿

Appendix1. Annuity Liabilities Total Sample :1000;

2. Transition Matrix2-year, 3-year, 4-year, and 5-year

3 Bond Return and STD at year 4

4. Bond return and STD at year 5

5-ratio summaryRatio= expected return / standard deviation

6 Asset Liability Analyses(Total Sample: 1000)

7. Portfolio selection and gap analysis(The excel sheet for gap analysis is combined with the portfolio selection)Obj: maximize the mean of gap in 2018

Obj: maximize the mean of gap in 2017

Obj: maximize the mean of cumulative gap

Obj: minimize the STD of gap in 2018

Obj: minimize the STD of gap in 2017

Obj: minimize the STD of cumulative gap

8. Duration analysisLiability

Asset

9 stress testing

10. Credit Var