Asset & Financial Management Strategies & Plans 11 October ...

56

Asset & Financial Management Strategies & Plans 11 October 2018 Annexure 7 - C1 - October 2018

Transcript of Asset & Financial Management Strategies & Plans 11 October ...

Asset & Financial Management Strategies & Plans

11 October 2018

Annexure 7 - C1 - October 2018

Annexure 7 - C1 - October 2018

Asset & Financial Management Strategies & Plans – October 2018 Page 1

Contents

Introduction ............................................................................................................................................................... 1

Executive Summary ................................................................................................................................................. 2

PART 1

Long-Term Financial Management Strategy Plan & Policies .................................................................... 3

1 Strategic Plan ............................................................................................................................................... 3

2 Annual Plan ................................................................................................................................................... 4

3 Interpretation .............................................................................................................................................. 5

4 Classes of Assets ......................................................................................................................................... 5

5 Long-Term Financial Management Plan ............................................................................................. 7

6 Financial Management Strategy ........................................................................................................ 23

PART 2

Long Term Asset Management Strategies Plans & Policies ................................................................... 30

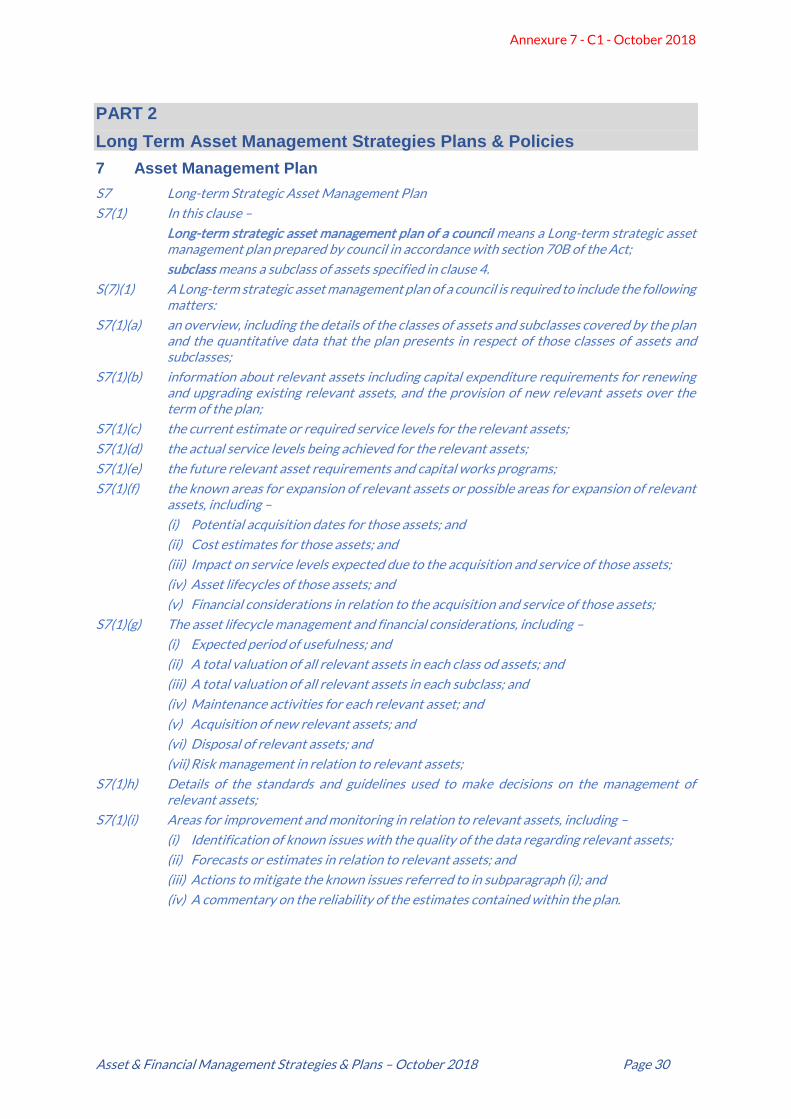

7 Asset Management Plan ....................................................................................................................... 30

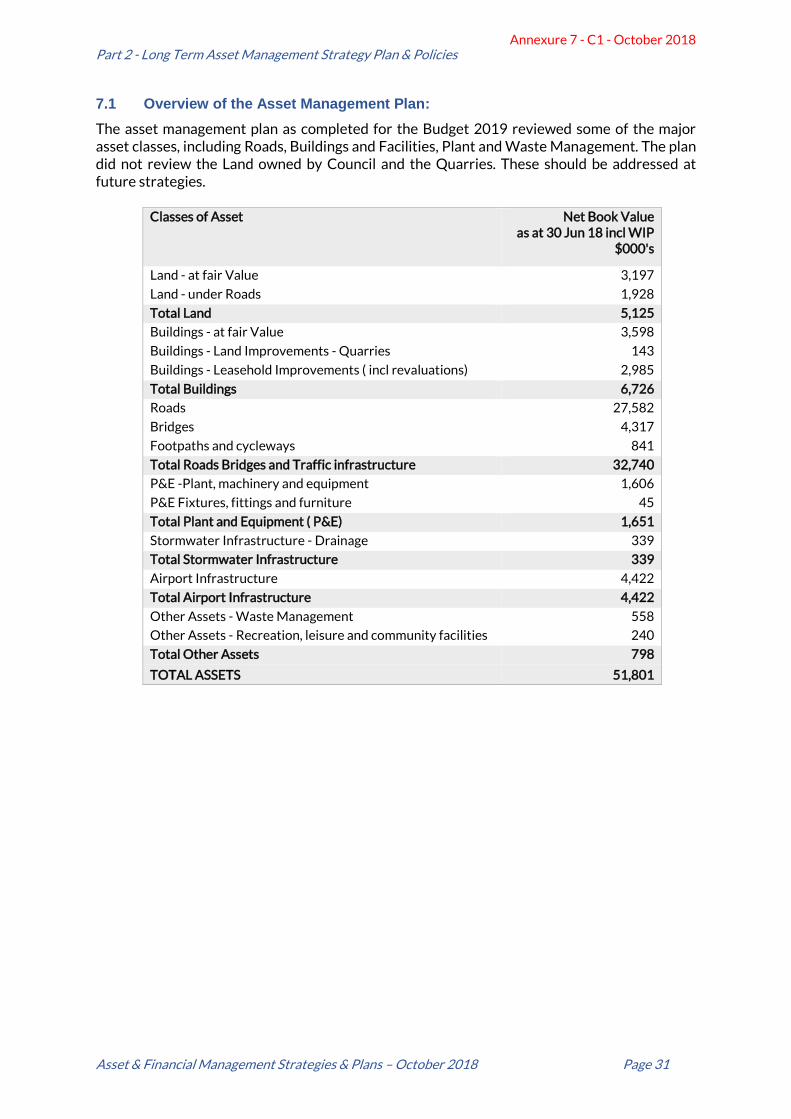

7.1 Overview of the Asset Management Plan: ............................................................................ 31

7.2 Roads .................................................................................................................................................. 33

7.3 Buildings & Facilities ..................................................................................................................... 34

7.4 Waste Management Program .................................................................................................... 35

7.5 Plant and Machinery ..................................................................................................................... 37

7.6 Land – Council owned Land ........................................................................................................ 37

7.7 Airport Infrastructure ................................................................................................................... 37

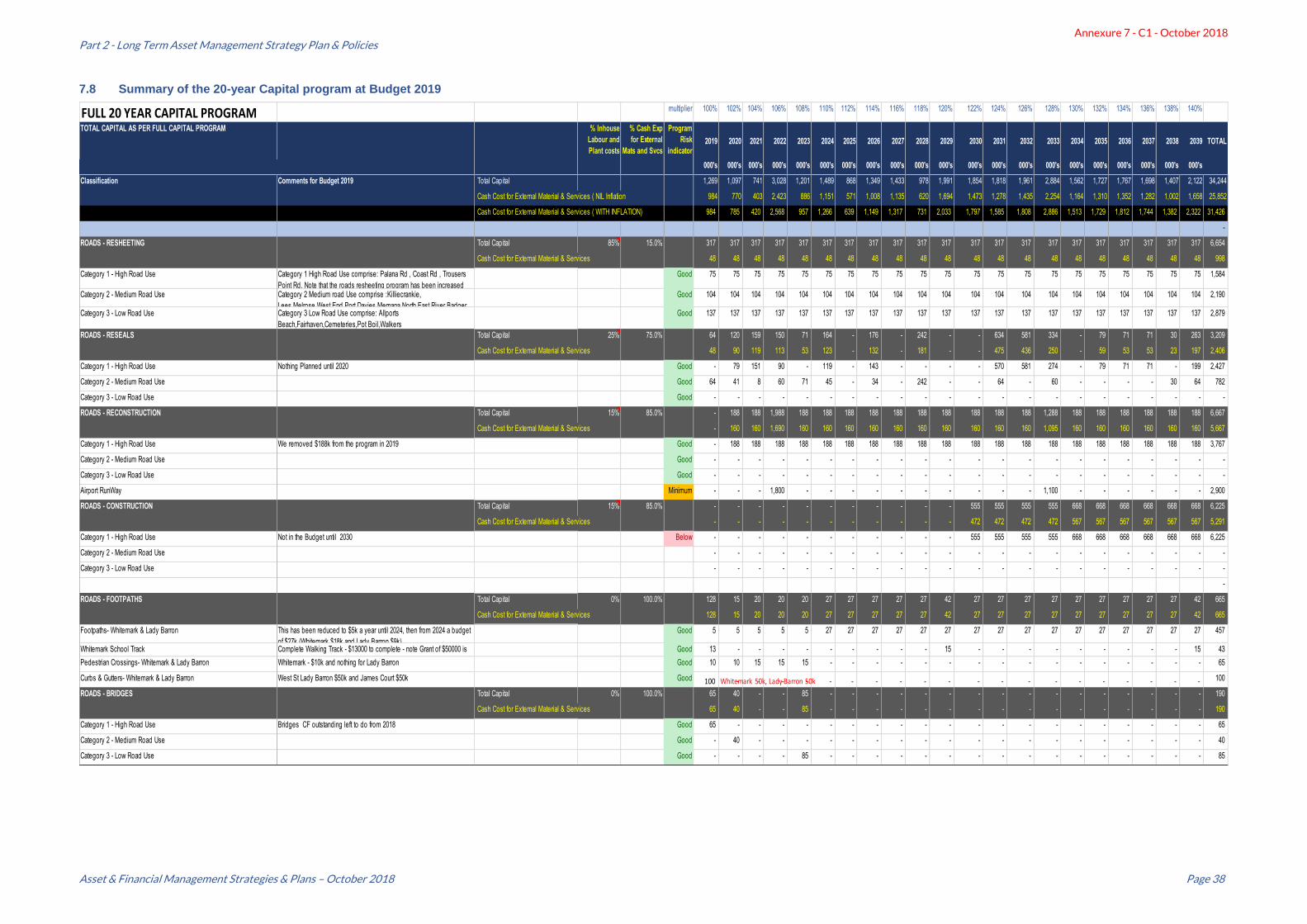

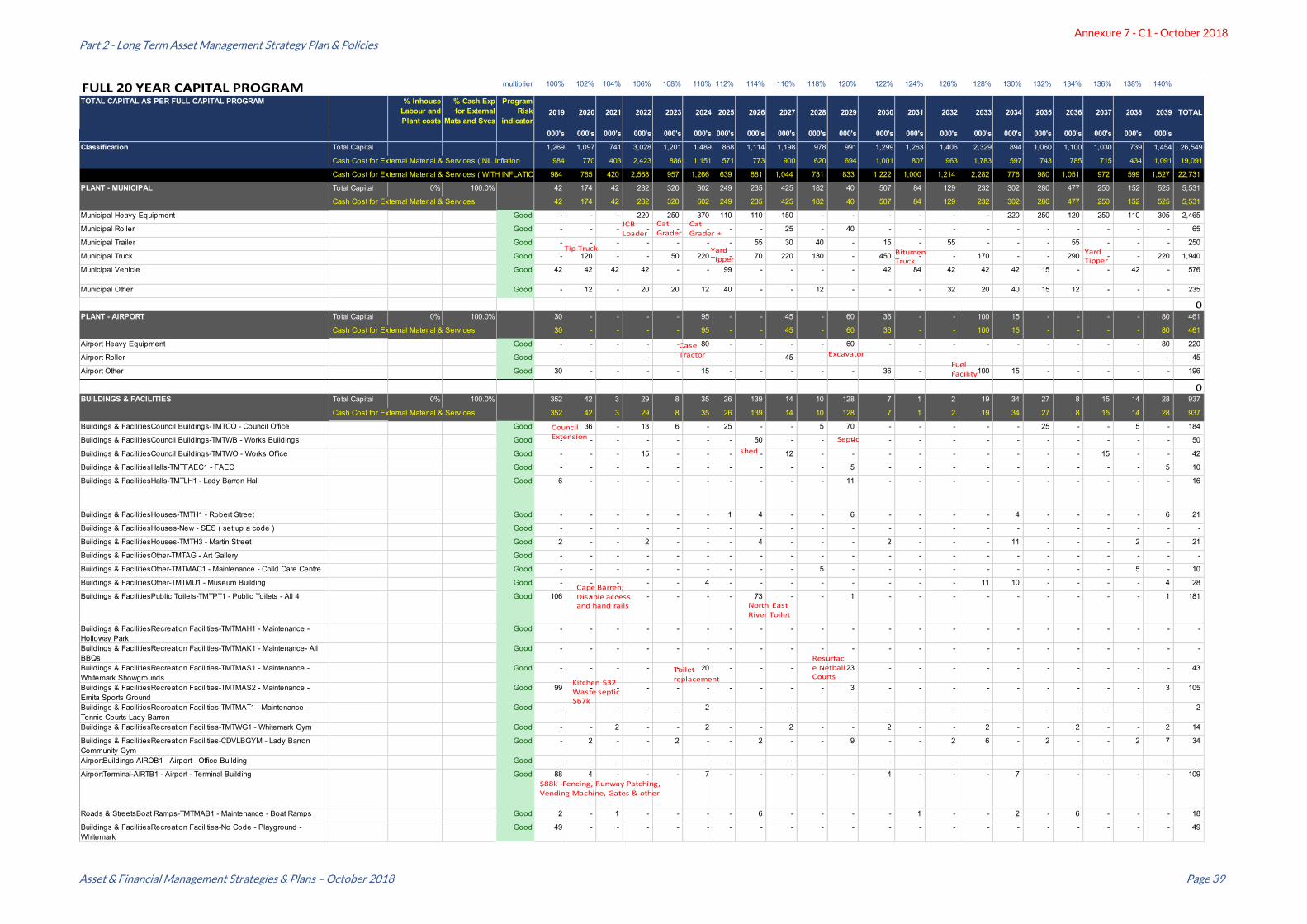

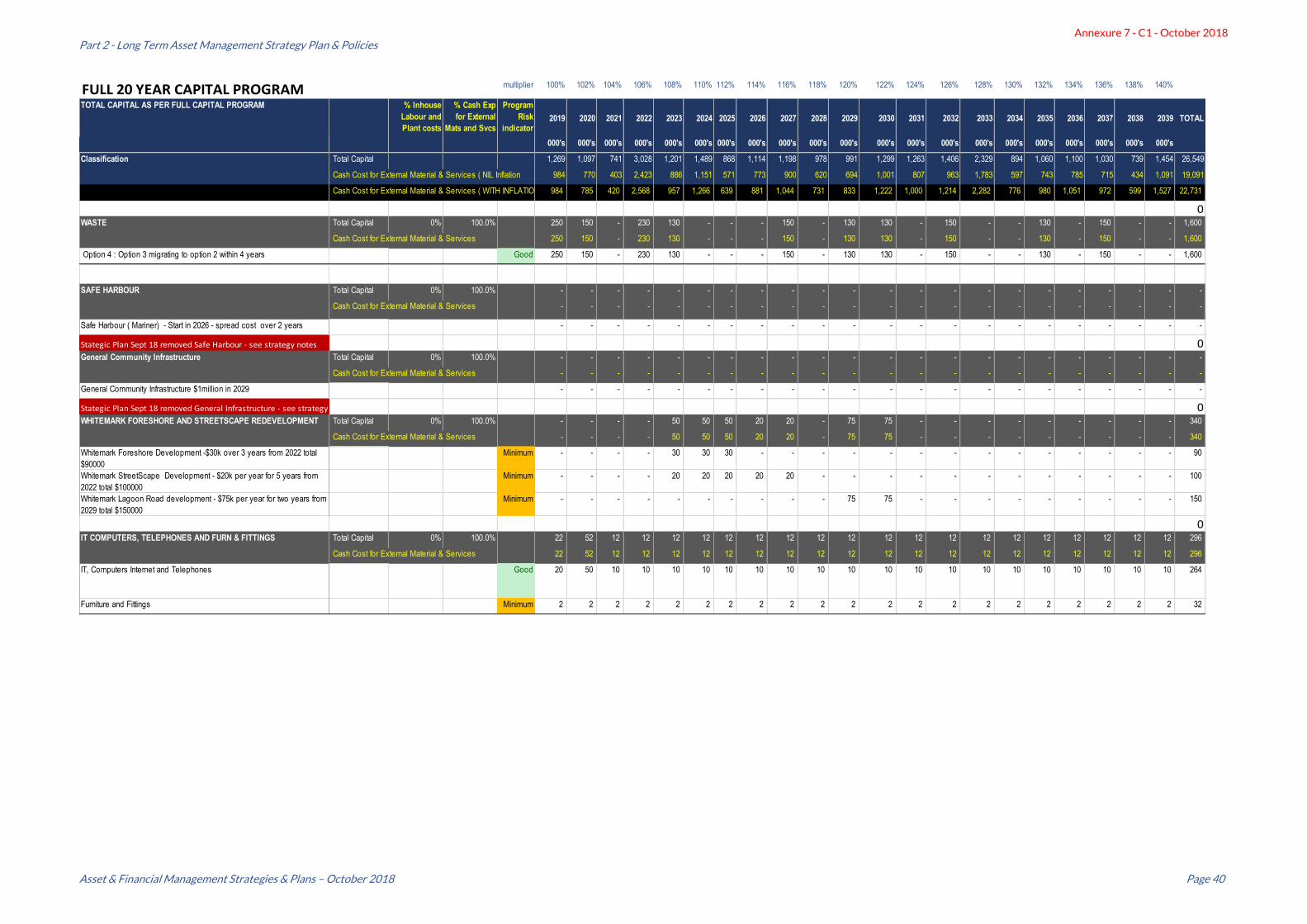

7.8 Summary of the 20-year Capital program at Budget 2019 ............................................. 38

8 Asset Management Policy .................................................................................................................... 41

8.1 Principles ........................................................................................................................................... 41

8.2 Accounting Policies for Property Plant and Infrastructure: ............................................ 43

9 Asset Management Strategy ............................................................................................................... 46

PART 3

Budget 2019 Commentary in Context to the Long-Term Financial & Asset Management Strategies ................................................................................................................................................................. 47

10 2019 Budget & Rating Commentary ............................................................................................ 47

10.1 Background ...................................................................................................................................... 47

10.2 Current Situation............................................................................................................................ 50

10.3 Budget 19 Documents: ................................................................................................................. 51

References ............................................................................................................................................................... 52

Annexure 7 - C1 - October 2018

Asset & Financial Management Strategies & Plans – October 2018 Page 1

Introduction

Under the Local Government Act 1993, Councils have a range of functions and powers including but not limited to the following: S20(1) (a) to provide for the health, safety and welfare of the community (b) to represent and promote the interests of the community (c) to provide for peace, order and good government of the municipal area In terms of achieving these and other objectives, Council is required to develop a range of strategic and operational plans that underpin the operations of the Council the importance of which should not be underestimated.

S68 Strategic Plan Section 1 S70 Long Term Financial Management Plan Section 5 S70A Financial Management Strategies Section 6 S70B Long-term Strategic Asset Management Plan Section 7 S70C Asset Management Policies Section 8 S70D Asset Management Strategies Section 9 S71 Annual Plan Section 1 S82 Estimate (Budget & Rating Strategy Section 3

This document assists in setting the framework for the Budget Estimates of Council’s revenue and expenditure, and aims to explain the rationale, context and overall operational philosophy underpinning Flinders Council’s plans and strategies. It provides analysis of past operations and future predictions leading to the eventual adoption of future budgets and annual business plans. The document has been prepared in three (3) basic parts as follows:

PART1 Long Term Financial Management Strategy Plan & Policies

PART 2 Long Term Asset Management Strategies Plans & Policies

PART 3 Budget Commentary in Context to the Long Term Financial & Asset Management Strategies

The Format of this document has been also prepared to highlight the “legislative” the provisions of the Local Government Act 1993 as expressed through the Local Government (Content and Strategies Order) 2014. Each Section of these orders corresponds to the relevant heading within the document. The applicable requirements under the Order are shown in Blue Text, with the strategy outputs

is in black text.

Annexure 7 - C1 - October 2018

Asset & Financial Management Strategies & Plans – October 2018 Page 2

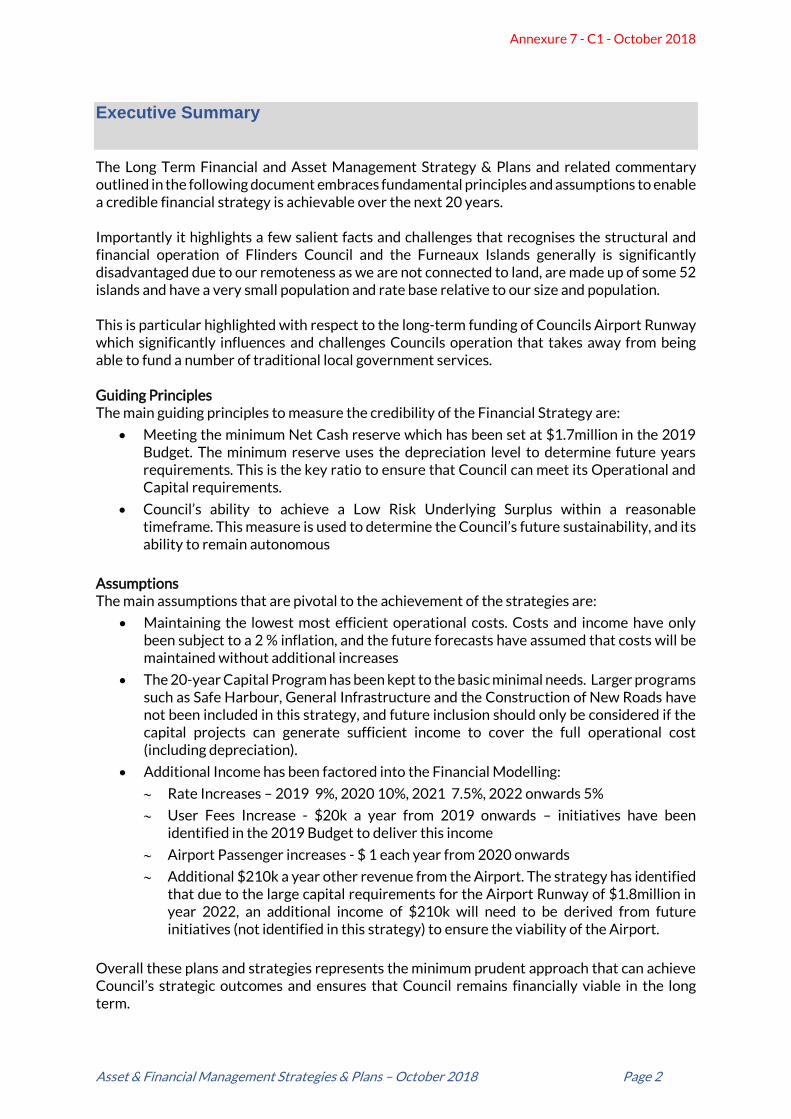

Executive Summary

The Long Term Financial and Asset Management Strategy & Plans and related commentary outlined in the following document embraces fundamental principles and assumptions to enable a credible financial strategy is achievable over the next 20 years. Importantly it highlights a few salient facts and challenges that recognises the structural and financial operation of Flinders Council and the Furneaux Islands generally is significantly disadvantaged due to our remoteness as we are not connected to land, are made up of some 52 islands and have a very small population and rate base relative to our size and population. This is particular highlighted with respect to the long-term funding of Councils Airport Runway which significantly influences and challenges Councils operation that takes away from being able to fund a number of traditional local government services. Guiding Principles The main guiding principles to measure the credibility of the Financial Strategy are:

• Meeting the minimum Net Cash reserve which has been set at $1.7million in the 2019 Budget. The minimum reserve uses the depreciation level to determine future years requirements. This is the key ratio to ensure that Council can meet its Operational and Capital requirements.

• Council’s ability to achieve a Low Risk Underlying Surplus within a reasonable timeframe. This measure is used to determine the Council’s future sustainability, and its ability to remain autonomous

Assumptions The main assumptions that are pivotal to the achievement of the strategies are:

• Maintaining the lowest most efficient operational costs. Costs and income have only been subject to a 2 % inflation, and the future forecasts have assumed that costs will be maintained without additional increases

• The 20-year Capital Program has been kept to the basic minimal needs. Larger programs such as Safe Harbour, General Infrastructure and the Construction of New Roads have not been included in this strategy, and future inclusion should only be considered if the capital projects can generate sufficient income to cover the full operational cost (including depreciation).

• Additional Income has been factored into the Financial Modelling:

Rate Increases – 2019 9%, 2020 10%, 2021 7.5%, 2022 onwards 5%

User Fees Increase - $20k a year from 2019 onwards – initiatives have been identified in the 2019 Budget to deliver this income

Airport Passenger increases - $ 1 each year from 2020 onwards

Additional $210k a year other revenue from the Airport. The strategy has identified that due to the large capital requirements for the Airport Runway of $1.8million in year 2022, an additional income of $210k will need to be derived from future initiatives (not identified in this strategy) to ensure the viability of the Airport.

Overall these plans and strategies represents the minimum prudent approach that can achieve Council’s strategic outcomes and ensures that Council remains financially viable in the long term.

Annexure 7 - C1 - October 2018

Asset & Financial Management Strategies & Plans – October 2018 Page 3

PART 1

Long-Term Financial Management Strategy Plan & Policies

1 Strategic Plan

Council’s Strategic Plan was adopted following public consultation in September 2015. Under the Act it needs to be reviewed at least every 4 years, however, a Council may decide if it wishes, to adopt a rolling review. The next review is due early 2019, following the 2018 October council elections. Council has identified 5 main Strategic Priorities:

1 Population growth – focusing on strategies, projects and policy initiatives that support the community, assist in the economic development and address investment attraction.

2 Development of Infrastructure and services – placed base approach to planning and delivery to ensure community and environmental values are maintained.

(A place-based approach targets an entire community and aims to address issues that exist at the neighbourhood level, such as poor housing, social isolation, poor or fragmented service provision that leads to gaps or duplication of effort and limited economic opportunities. Several recent authors have recommended that “sense of place” should become an important concept in our evaluation of environmental policies.)

3 Improve access and connectivity – work with service providers and other relevant stakeholders to improve security and reliability of access and connectivity in a cost-effective manner.

4 Developing a strategic, efficient and effective organisation – to have the ability to respond to risks and opportunities.

5 Liveability – to protect, improve and promote the safety, creativity, health and wellbeing of the Islands’ communities.

The above Strategic Objectives encompasses the Council’s overarching philosophy which is Community Building and the improvement of infrastructure. As evidenced by the following extract, the nature of Council’s Strategic Plan is not dissimilar to most Councils who all focus on community building. An Extract from the Northern Tasmanian Council Shared Services Study – Final Report July 2017: Seven Strategic priorities have been identified in the northern council’s Strategic Plans in terms of commonality. The main strategic priority that appears in each council’s strategic plan is community building. Community building in the sense of creating a community that is liveable and engaging. The second most common priority is infrastructure in terms of improvement and upgrades for various purposes such as public transport or industry etc. Environment planning is the next most common priority of the councils. Environment planning includes environment conservation, adopting sustainable practices in service delivery and the mitigating effect of climate change”

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 4

2 Annual Plan

Each year Council adopts a range of actions through its Annual Plan, which identifies the way Council endeavours to meet the goals and objectives as determined by the Strategic Plan. Every formal report to Council references elements of the Council’s Strategic Plan which includes these goals and objectives. Progress reports on the delivery of the Strategic Plan will through the business plan be submitted to Council on a Quarterly basis as well as annually through the Annual report. There has been a change in the role of local government (of which Flinders is a part), that indicates a leaning towards community building and the general support of local organisations. This can be evidenced by the recent acceleration in upgrades and improvements in a range of activities such as upgrades of the Flinders Arts and Entertainment Centre, Lady Barron Hall, Emita Hall, art gallery, playgrounds, new and improved toilet and BBQ facilities, community gyms, youth development programs and the Furneaux Islands Festival. Due to the positive response from the community regarding the Council’s support within the community services sector, the current level of performance and support as articulated through Council’s Annual Plan Actions should be at least retained at current levels in the short term and further encourage an increase in community participation. As a small community, with a limited resource base, Council’s leadership in this area is pivotal. (Note the Full Annual Plan for Budget 2019 is not included in this document.)

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 5

3 Interpretation

The following legislative aspects associated with the are to be considered within the Local Government (Content and Strategies Order) 2014

S3(1) In this Order:

AASB 101 means the AASB 101 – Presentation of Financial Statements

(a) Published by the Australian Accounting Standards Board, as appointed by the Financial Reporting Council of the Commonwealth; and

(b) As amended or substituted from time to time;

Act means the local Government Act 1993;

comprehensive income has the same meaning as other comprehensive income in the AASB 101,

comprehensive result has the same meaning as total comprehensive income in the AASB 101;

relevant asset means an asset within a class of assets specified in clause 4

underlying surplus or deficit means an amount that is the recurrent income (not including income received specifically for new or upgraded assets, physical resources received free of charge or other income of a capital nature) of a council for a financial year less the recurrent expenses of the council for the financial year.

The Comprehensive Income and result includes asset revaluations/revaluation adjustments, and profit from the sale of assets. The Budget 2019 has $30k in for the Income of Sale of assets, but in future years there is no prediction for sale of assets and revaluations, as this area is too unpredictable. S3(2) The Acts Interpretation Act 1931 applies to the interpretation of this order as if it were by-

laws.

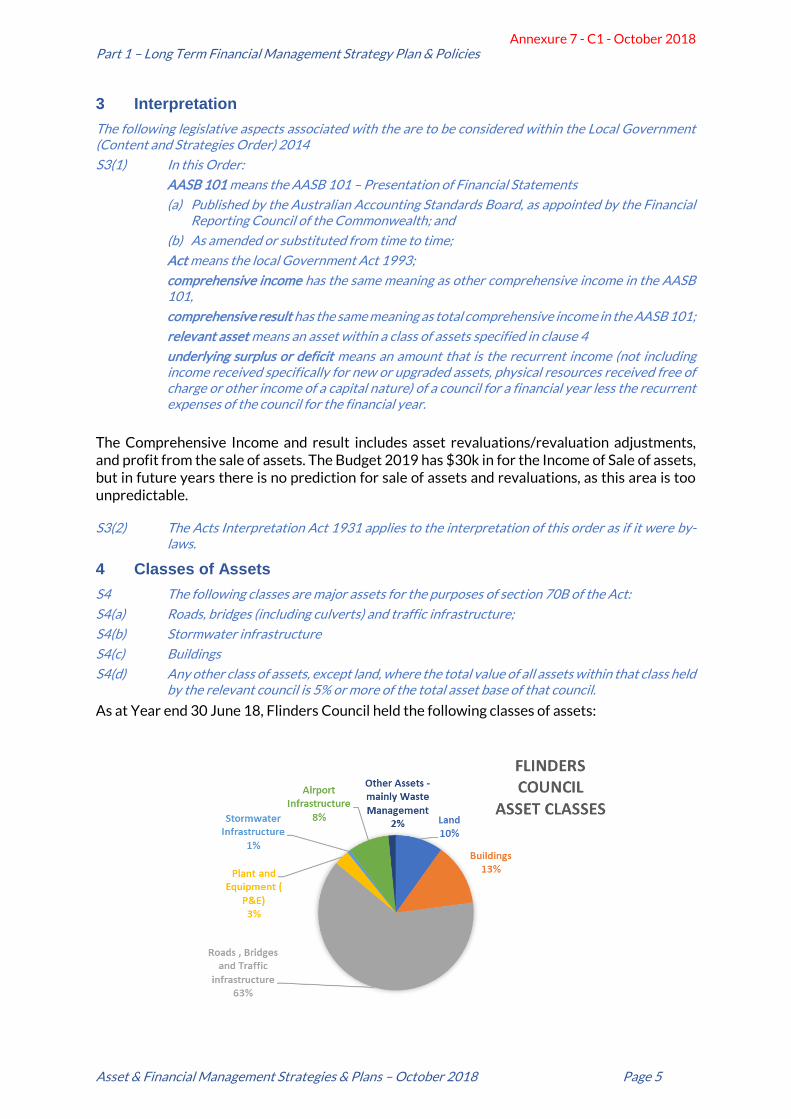

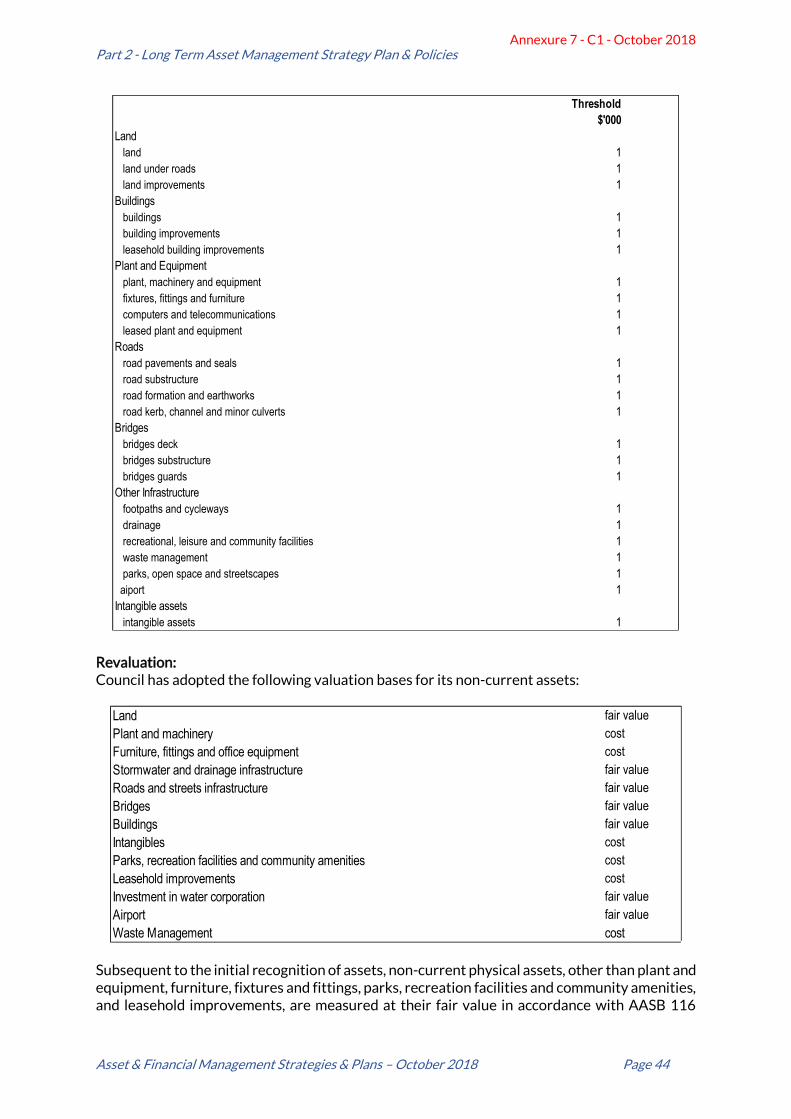

4 Classes of Assets

S4 The following classes are major assets for the purposes of section 70B of the Act:

S4(a) Roads, bridges (including culverts) and traffic infrastructure;

S4(b) Stormwater infrastructure

S4(c) Buildings

S4(d) Any other class of assets, except land, where the total value of all assets within that class held by the relevant council is 5% or more of the total asset base of that council.

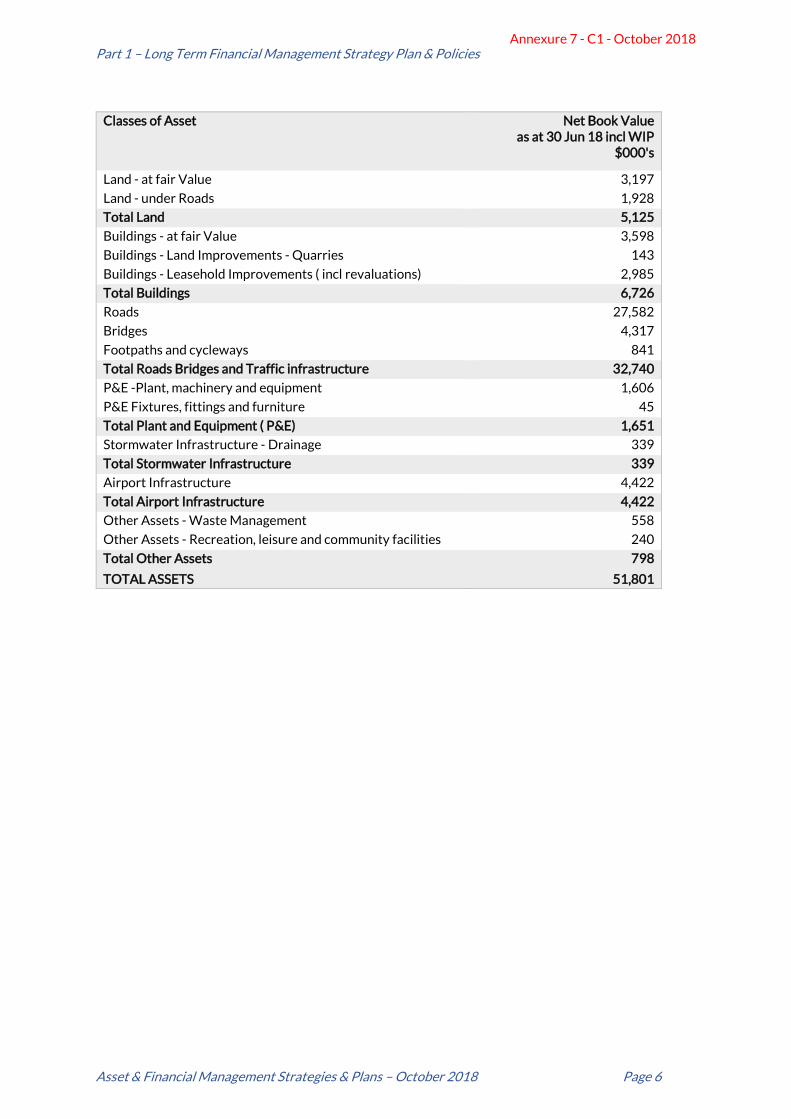

As at Year end 30 June 18, Flinders Council held the following classes of assets:

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 6

Classes of Asset Net Book Value

as at 30 Jun 18 incl WIP $000's

Land - at fair Value 3,197

Land - under Roads 1,928

Total Land 5,125

Buildings - at fair Value 3,598

Buildings - Land Improvements - Quarries 143

Buildings - Leasehold Improvements ( incl revaluations) 2,985

Total Buildings 6,726

Roads 27,582

Bridges 4,317

Footpaths and cycleways 841

Total Roads Bridges and Traffic infrastructure 32,740

P&E -Plant, machinery and equipment 1,606

P&E Fixtures, fittings and furniture 45

Total Plant and Equipment ( P&E) 1,651

Stormwater Infrastructure - Drainage 339

Total Stormwater Infrastructure 339

Airport Infrastructure 4,422

Total Airport Infrastructure 4,422

Other Assets - Waste Management 558

Other Assets - Recreation, leisure and community facilities 240

Total Other Assets 798

TOTAL ASSETS 51,801

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 7

5 Long-Term Financial Management Plan

S5(1) In this clause – long-term financial management plan of a council, means a long-term financial management plan prepared by the council in accordance with section 70 of the Act.

S5(2) A long-term financial management plan of a council is required to include the following matters:

S5(2)(a) The estimated revenues and expenses for each financial year of the plan, including the revenues and expenses in relation to each of the following matters:

(i) all capital works;

(ii) all capital expenditure;

(iii) all asset management requirements identified as required under clause 7(2)(b) in the long-term strategic asset management plan;

The Long-term Financial plan has been divided into three segments:

• Total Council Income and Expenditure 20-year forecast

• Airport Income and Expenditure 20-year forecast

• Municipal Income and Expenditure 20-year forecast

The Long-Term Financial Plan was prepared in conjunction with and as part of preparing the 2018/19 Budget. Significant work has been undertaken in preparing a Long-Term Asset Management Plan (Section 7), which plays a significant part of the Long-Term Financial Plan and provides a framework to enable an assessment of the Councils revenue resources and assists the Council to plan and fund operational and capital expenditures. The Act requirements as indicated in blue text, is the framework for the long-term financial management plan. The current long-term financial strategy, though not fully complete as required under the relevant Ministerial Orders, nevertheless, provides a sound way forward as it highlights how Council’s cash position is to be managed and identifies the challenges to meet future sustainability. Each section has been reviewed, and where an area has not been addressed by this report, it has been noted. This section has been completed. Reservation however is made on the term “all capital works and expenditure” in so far as the work carried out has sought to review to the best of our ability the main categories, and though significant work has been undertaken, there may be areas that we have not identified.

S5(2)(b) For each financial year of the plan, a statement of comprehensive income, including estimates of –

(i) Recurrent revenue; and

(ii) Recurrent expenses; and

(iii) Underlying surplus or deficit; and

(iv) Net surplus or net deficit; and

(v) Comprehensive result;

The Flinders Council Long-term Financial plan has included recurrent revenue and recurrent expenses. The underlying surplus or deficit and comprehensive result has been calculated for the Budget 2019 and requires detailed forecasting of the depreciation to enable forecasting the underlying surplus or deficit, and comprehensive result for the years beyond 2019. This section is completed as fpllows:

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 8

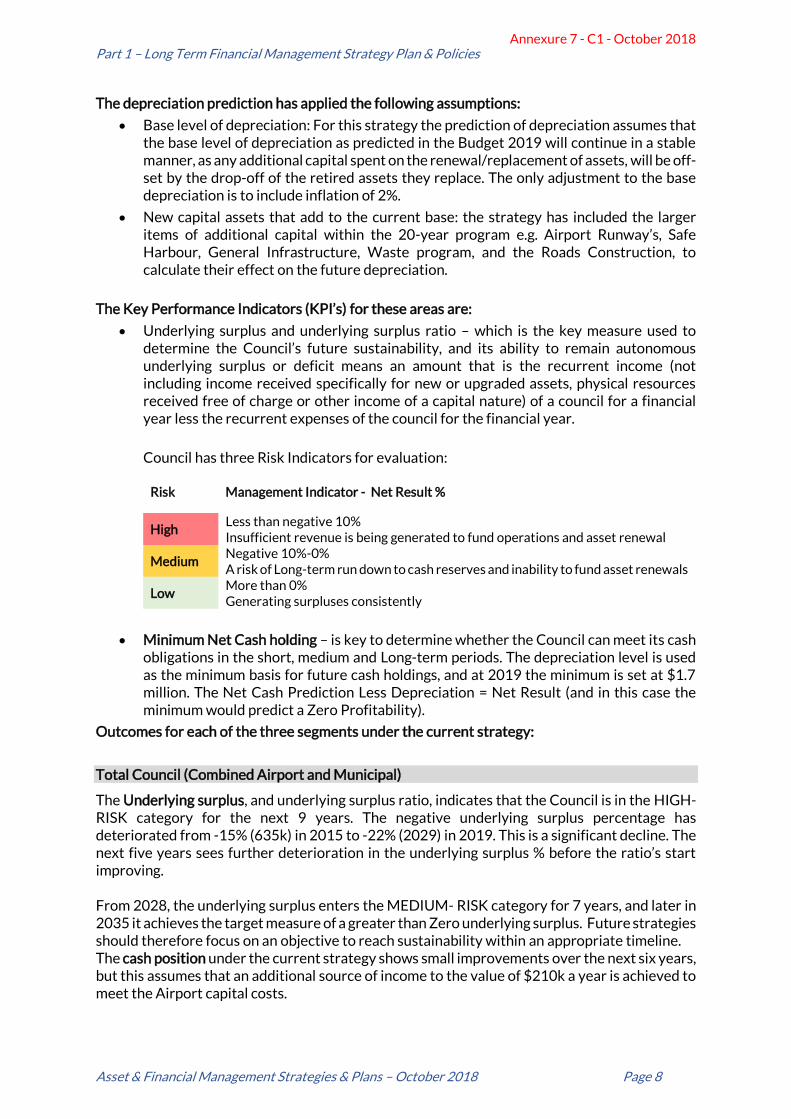

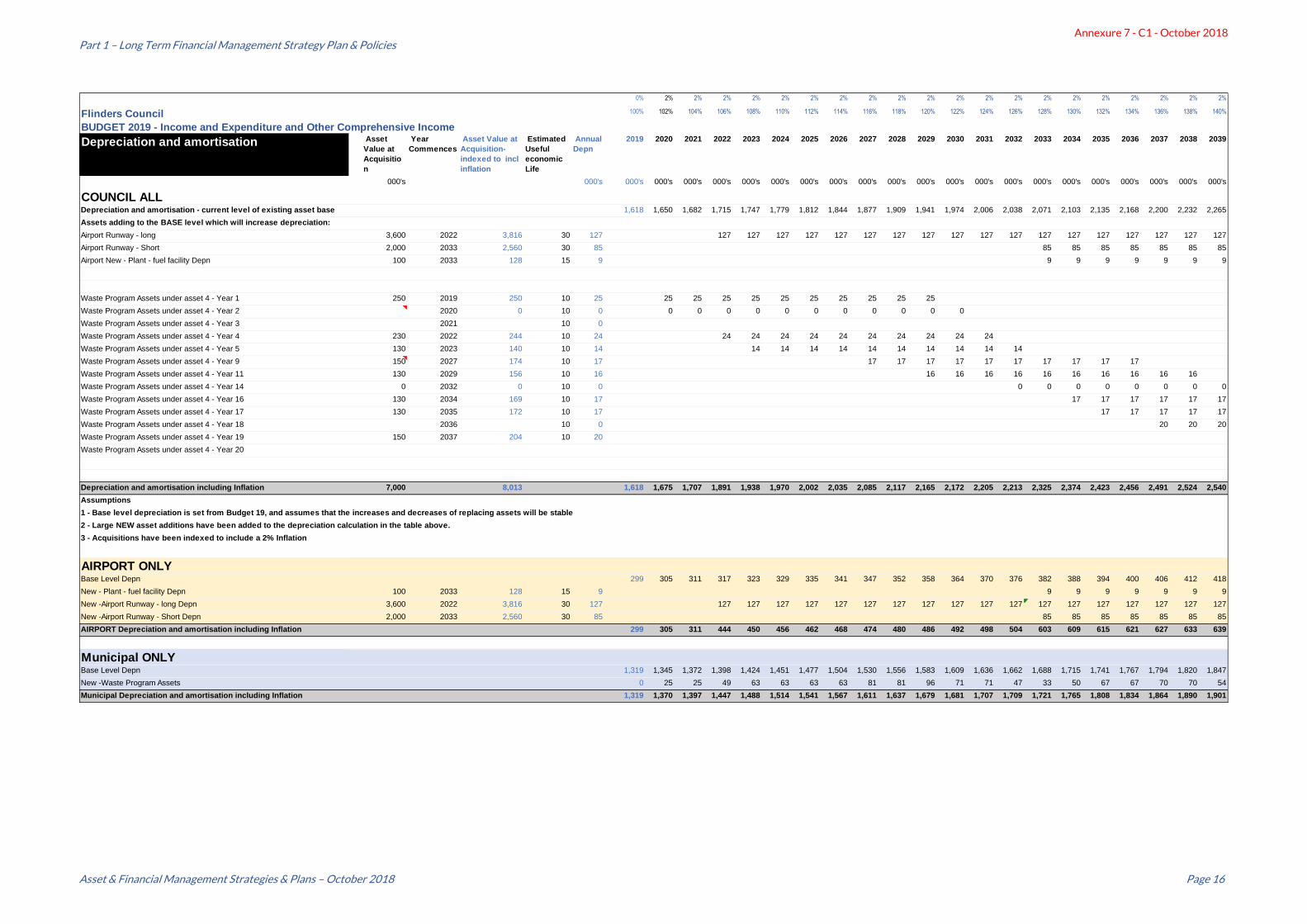

The depreciation prediction has applied the following assumptions:

• Base level of depreciation: For this strategy the prediction of depreciation assumes that the base level of depreciation as predicted in the Budget 2019 will continue in a stable manner, as any additional capital spent on the renewal/replacement of assets, will be off-set by the drop-off of the retired assets they replace. The only adjustment to the base depreciation is to include inflation of 2%.

• New capital assets that add to the current base: the strategy has included the larger items of additional capital within the 20-year program e.g. Airport Runway’s, Safe Harbour, General Infrastructure, Waste program, and the Roads Construction, to calculate their effect on the future depreciation.

The Key Performance Indicators (KPI’s) for these areas are:

• Underlying surplus and underlying surplus ratio – which is the key measure used to determine the Council’s future sustainability, and its ability to remain autonomous underlying surplus or deficit means an amount that is the recurrent income (not including income received specifically for new or upgraded assets, physical resources received free of charge or other income of a capital nature) of a council for a financial year less the recurrent expenses of the council for the financial year.

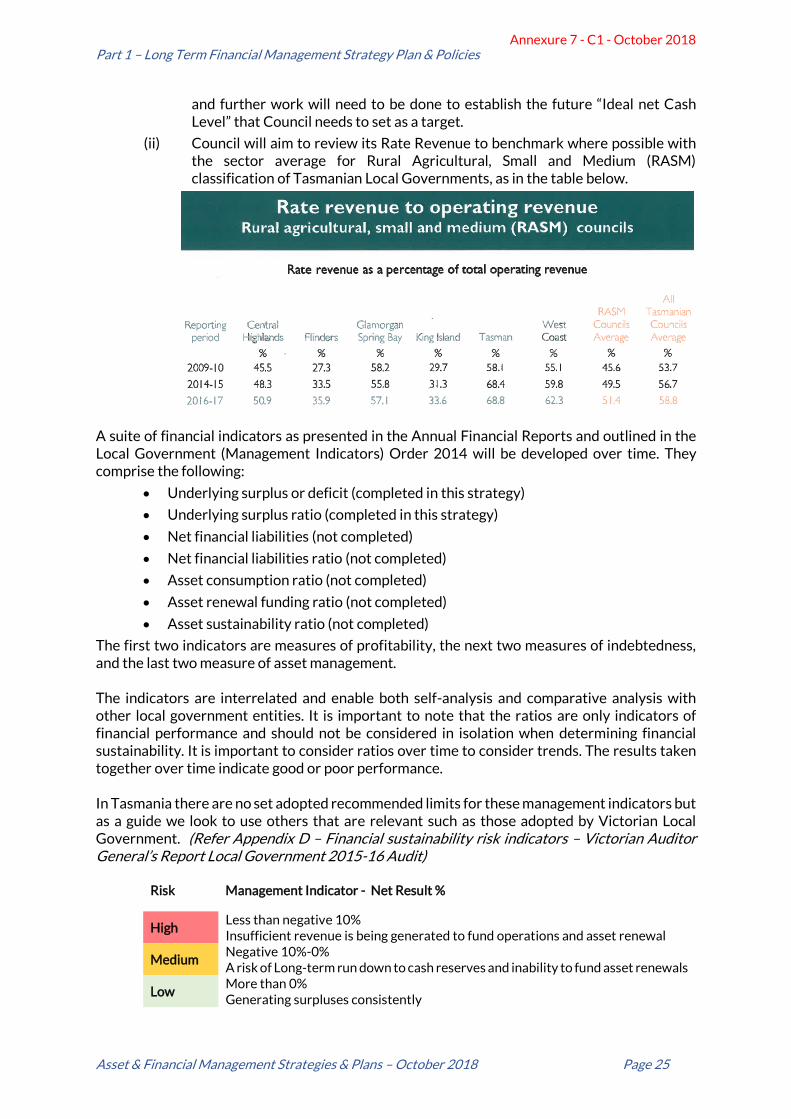

Council has three Risk Indicators for evaluation:

Risk Management Indicator - Net Result %

High Less than negative 10% Insufficient revenue is being generated to fund operations and asset renewal

Medium Negative 10%-0% A risk of Long-term run down to cash reserves and inability to fund asset renewals

Low More than 0% Generating surpluses consistently

• Minimum Net Cash holding – is key to determine whether the Council can meet its cash obligations in the short, medium and Long-term periods. The depreciation level is used as the minimum basis for future cash holdings, and at 2019 the minimum is set at $1.7 million. The Net Cash Prediction Less Depreciation = Net Result (and in this case the minimum would predict a Zero Profitability).

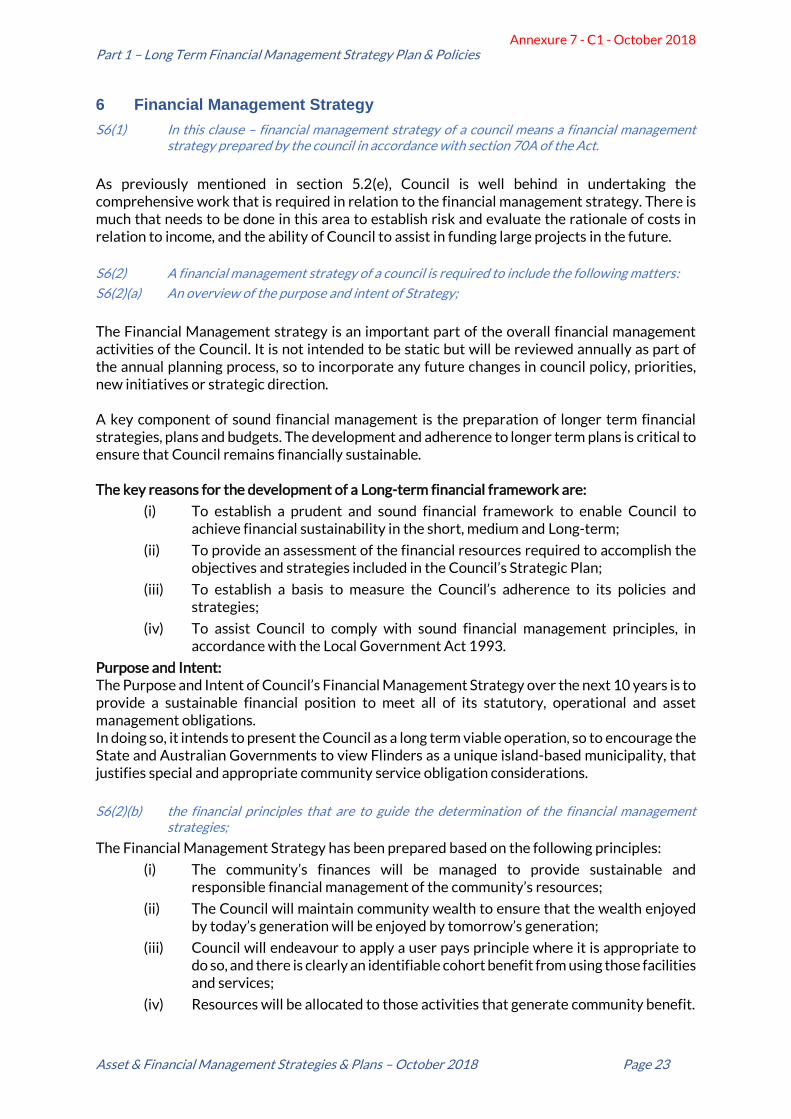

Outcomes for each of the three segments under the current strategy:

Total Council (Combined Airport and Municipal)

The Underlying surplus, and underlying surplus ratio, indicates that the Council is in the HIGH-RISK category for the next 9 years. The negative underlying surplus percentage has deteriorated from -15% (635k) in 2015 to -22% (2029) in 2019. This is a significant decline. The next five years sees further deterioration in the underlying surplus % before the ratio’s start improving. From 2028, the underlying surplus enters the MEDIUM- RISK category for 7 years, and later in 2035 it achieves the target measure of a greater than Zero underlying surplus. Future strategies should therefore focus on an objective to reach sustainability within an appropriate timeline. The cash position under the current strategy shows small improvements over the next six years, but this assumes that an additional source of income to the value of $210k a year is achieved to meet the Airport capital costs.

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 9

The main factors contributing to the inability to improve the underlying surplus within a short timeframe lies with these issues:

• Small Revenue base: The Council has a small revenue base and therefore a small recurrent income, but high operational costs (high recurrent expenditure) which leaves insufficient funds to manage the extensive capital program.

• Large asset carrying level: Though Flinders is a small council, it has a very large asset carrying level of $52 million. The Rates Revenue (1.7million in 2019) in ratio to the Asset Carrying is only 3%. To improve this ratio the rates income needs to significantly increase and the asset carrying needs to reduce (or a bit of both). But the current strategy as it stands aims to increase its asset base within the next 20 years and by 2039 the new carrying level is predicted to be $76 million, with an annual rates income of 2.5 million, resulting in a Rates to Asset Holding Ratio of 3%. The ratio indicates that there is some improvements over the 20-year period.

• Evaluation of Capital needs should be based on Asset Value and the Councils ability to fund future operational and capital replacements: When evaluating additional capital needs, the asset carrying level is not based on the Council’s cash contribution to the asset, but on the value of the asset at the time of acquisition. For example, the Airport Runway has a $1.8 million cost to be incurred by council (as a grant is predicted to be provided for the other $1.8 million), but the value of the asset to be maintained and replaced in future is valued at $3.6 million. As such if the useful life of the asset is 30 years, then the Council needs to ensure that there is an additional $127k cash set aside each year for a period of 30 years, to provide for replacing/renewing that asset. This is what the depreciation fund is measuring.

Based on this principle, as the Council are already struggling to meet its basic capital requirements to maintain the $52 million asset base, any new capital therefore creates an additional burden and exacerbates the problem.

Asset additions removed from the current strategic plan. The Strategic Long- Term Asset Management Plan removed the following assets from the plan in the draft version 2, as the asset additions were too large for the forecast revenue base.

Safe Harbour Project $5.5 million

General Infrastructure $1.0 million

Road Construction (3km a year) $6.2 million

The above projects will need to be considered in future strategies. The Council’s ability to fund such large projects has not been identified in this strategy, and future inclusion should only be considered if the capital projects can generate sufficient income to cover both the ongoing operational costs, including the depreciation fund.

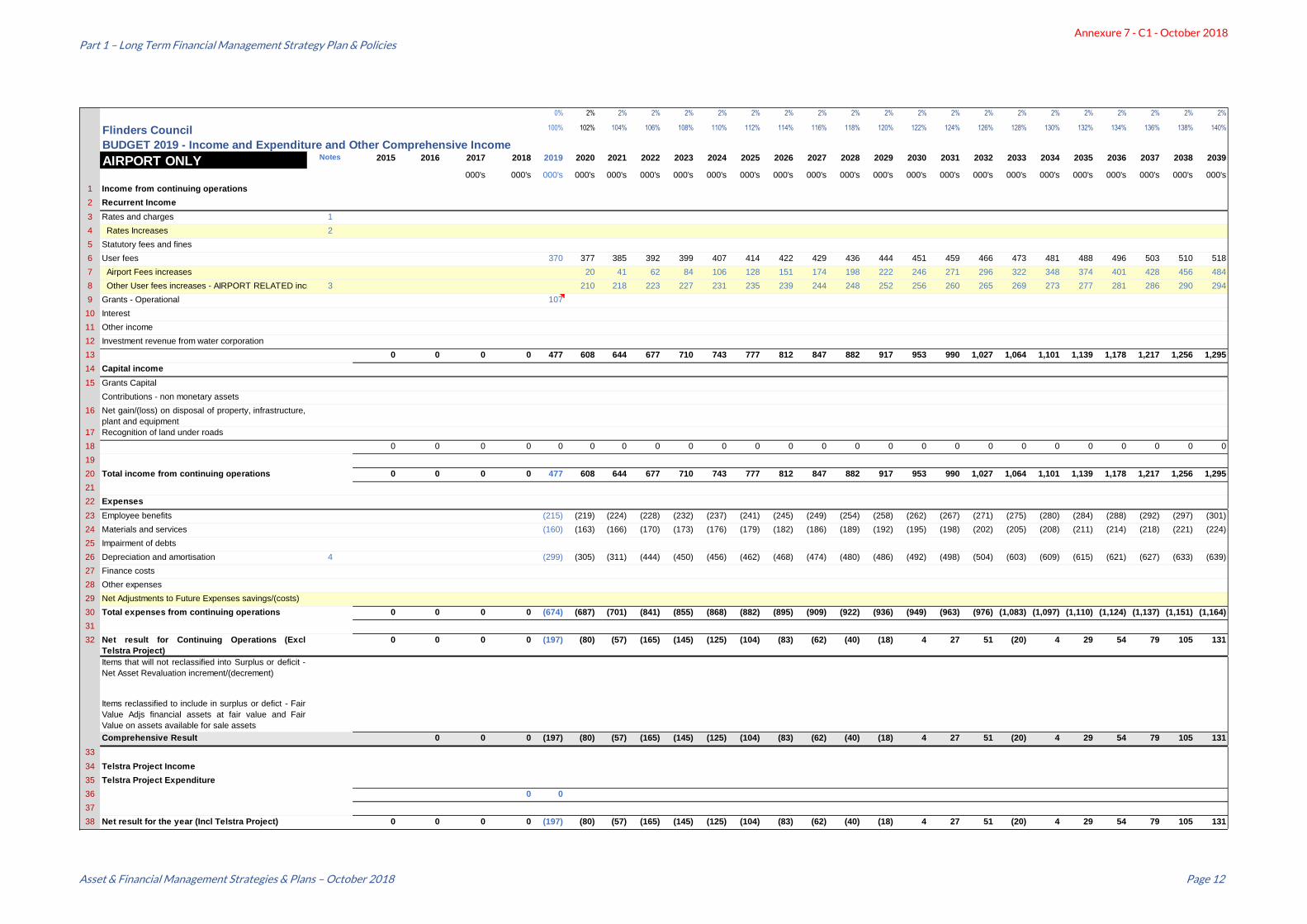

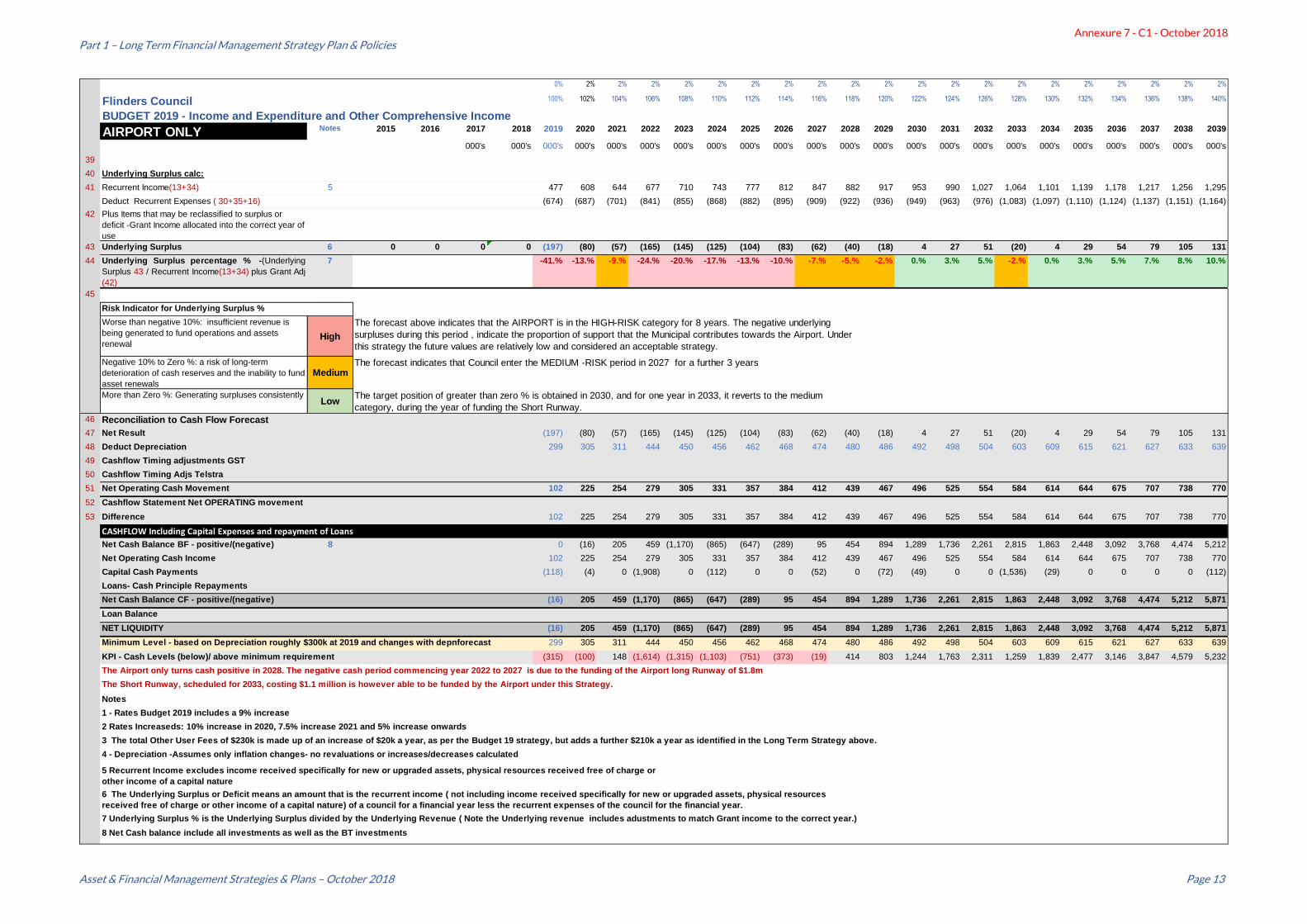

Airport

The Airport underlying surplus remains in the HIGH-RISK category for the first 8 years, and then enters the MEDIUM – RISK period for in 2017 for a further 3 years. The strategy achieves the targeted LOW-RISK under-lying surplus in 2030. The important point to note here is that the future sustainability of the airport and positive outlook presented in this strategy is hinged on the ability to achieve an additional $210k a year of Airport Income to cover the Airport Runway Capital costs. The strategy has not reviewed or identified the future possible sources of income that represent the $210k.

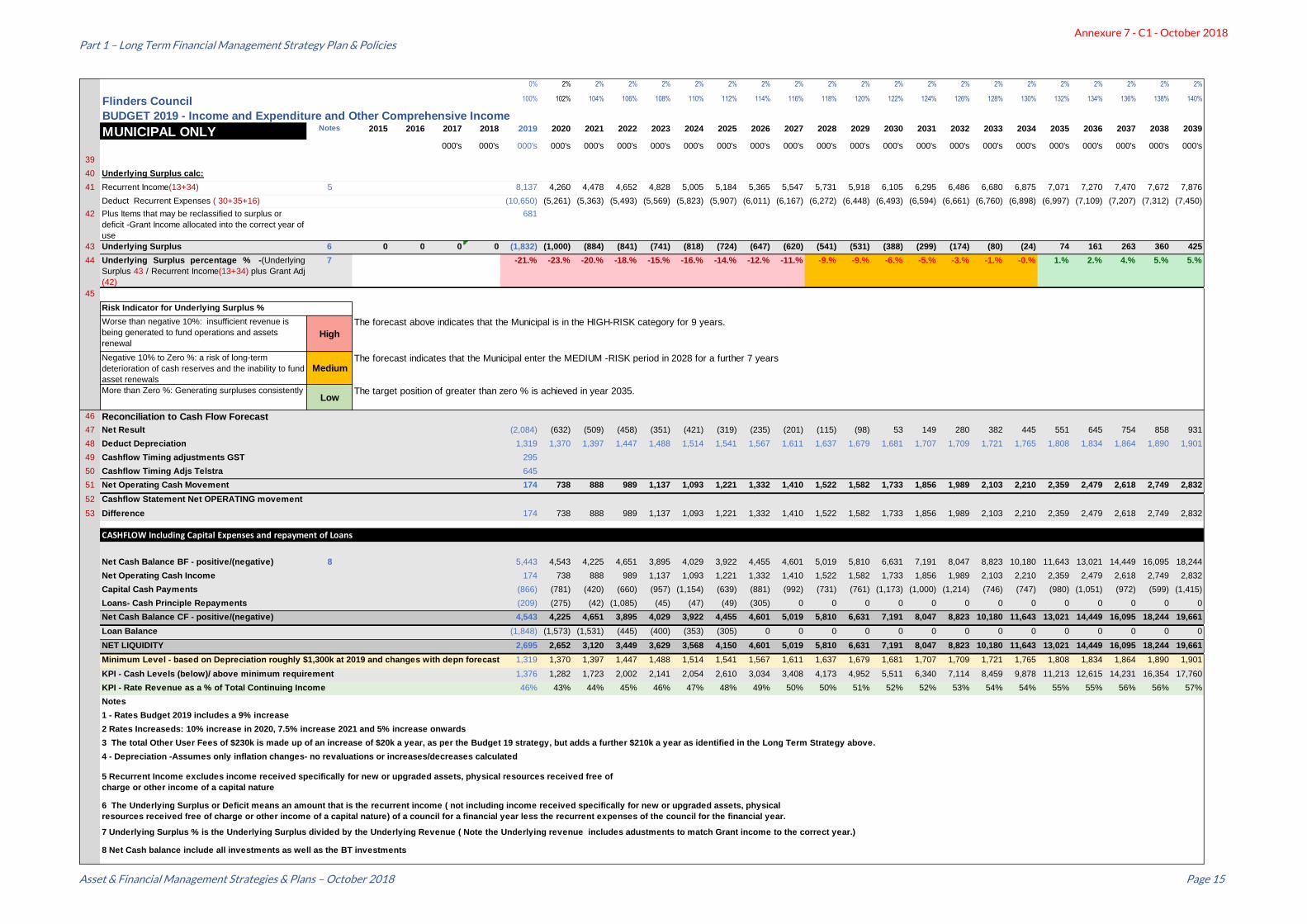

Municipal

The Municipal is in the HIGH-RISK category for 9 years, before entering the MEDIUM- RISK period in 2028 for a further 7 years. The targeted LOW-RISK status is reached very late in 2035.

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 10

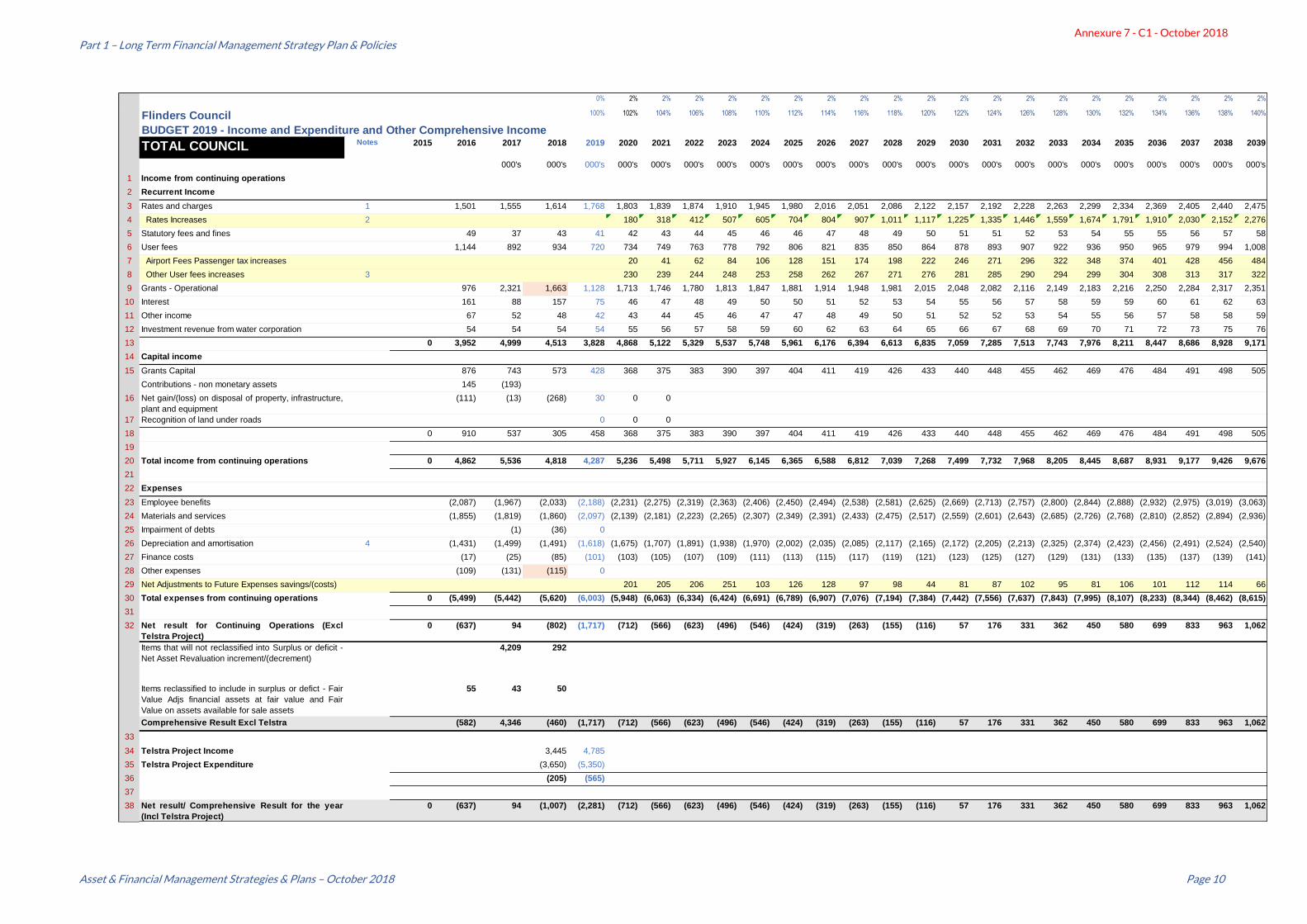

0% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2%

Flinders Council 100% 102% 104% 106% 108% 110% 112% 114% 116% 118% 120% 122% 124% 126% 128% 130% 132% 134% 136% 138% 140%

BUDGET 2019 - Income and Expenditure and Other Comprehensive Income

TOTAL COUNCIL Notes 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039

000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's

1 Income from continuing operations

2 Recurrent Income

3 Rates and charges 1 1,501 1,555 1,614 1,768 1,803 1,839 1,874 1,910 1,945 1,980 2,016 2,051 2,086 2,122 2,157 2,192 2,228 2,263 2,299 2,334 2,369 2,405 2,440 2,475

4 Rates Increases 2 180 318 412 507 605 704 804 907 1,011 1,117 1,225 1,335 1,446 1,559 1,674 1,791 1,910 2,030 2,152 2,276

5 Statutory fees and fines 49 37 43 41 42 43 44 45 46 46 47 48 49 50 51 51 52 53 54 55 55 56 57 58

6 User fees 1,144 892 934 720 734 749 763 778 792 806 821 835 850 864 878 893 907 922 936 950 965 979 994 1,008

7 Airport Fees Passenger tax increases 20 41 62 84 106 128 151 174 198 222 246 271 296 322 348 374 401 428 456 484

8 Other User fees increases 3 230 239 244 248 253 258 262 267 271 276 281 285 290 294 299 304 308 313 317 322

9 Grants - Operational 976 2,321 1,663 1,128 1,713 1,746 1,780 1,813 1,847 1,881 1,914 1,948 1,981 2,015 2,048 2,082 2,116 2,149 2,183 2,216 2,250 2,284 2,317 2,351

10 Interest 161 88 157 75 46 47 48 49 50 50 51 52 53 54 55 56 57 58 59 59 60 61 62 63

11 Other income 67 52 48 42 43 44 45 46 47 47 48 49 50 51 52 52 53 54 55 56 57 58 58 59

12 Investment revenue from water corporation 54 54 54 54 55 56 57 58 59 60 62 63 64 65 66 67 68 69 70 71 72 73 75 76

13 0 3,952 4,999 4,513 3,828 4,868 5,122 5,329 5,537 5,748 5,961 6,176 6,394 6,613 6,835 7,059 7,285 7,513 7,743 7,976 8,211 8,447 8,686 8,928 9,171

14 Capital income

15 Grants Capital 876 743 573 428 368 375 383 390 397 404 411 419 426 433 440 448 455 462 469 476 484 491 498 505

Contributions - non monetary assets 145 (193)

16 Net gain/(loss) on disposal of property, infrastructure,

plant and equipment

(111) (13) (268) 30 0 0

17 Recognition of land under roads 0 0 0

18 0 910 537 305 458 368 375 383 390 397 404 411 419 426 433 440 448 455 462 469 476 484 491 498 505

19

20 Total income from continuing operations 0 4,862 5,536 4,818 4,287 5,236 5,498 5,711 5,927 6,145 6,365 6,588 6,812 7,039 7,268 7,499 7,732 7,968 8,205 8,445 8,687 8,931 9,177 9,426 9,676

21

22 Expenses

23 Employee benefits (2,087) (1,967) (2,033) (2,188) (2,231) (2,275) (2,319) (2,363) (2,406) (2,450) (2,494) (2,538) (2,581) (2,625) (2,669) (2,713) (2,757) (2,800) (2,844) (2,888) (2,932) (2,975) (3,019) (3,063)

24 Materials and services (1,855) (1,819) (1,860) (2,097) (2,139) (2,181) (2,223) (2,265) (2,307) (2,349) (2,391) (2,433) (2,475) (2,517) (2,559) (2,601) (2,643) (2,685) (2,726) (2,768) (2,810) (2,852) (2,894) (2,936)

25 Impairment of debts (1) (36) 0

26 Depreciation and amortisation 4 (1,431) (1,499) (1,491) (1,618) (1,675) (1,707) (1,891) (1,938) (1,970) (2,002) (2,035) (2,085) (2,117) (2,165) (2,172) (2,205) (2,213) (2,325) (2,374) (2,423) (2,456) (2,491) (2,524) (2,540)

27 Finance costs (17) (25) (85) (101) (103) (105) (107) (109) (111) (113) (115) (117) (119) (121) (123) (125) (127) (129) (131) (133) (135) (137) (139) (141)

28 Other expenses (109) (131) (115) 0

29 Net Adjustments to Future Expenses savings/(costs) 201 205 206 251 103 126 128 97 98 44 81 87 102 95 81 106 101 112 114 66

30 Total expenses from continuing operations 0 (5,499) (5,442) (5,620) (6,003) (5,948) (6,063) (6,334) (6,424) (6,691) (6,789) (6,907) (7,076) (7,194) (7,384) (7,442) (7,556) (7,637) (7,843) (7,995) (8,107) (8,233) (8,344) (8,462) (8,615)

31

32 Net result for Continuing Operations (Excl

Telstra Project)

0 (637) 94 (802) (1,717) (712) (566) (623) (496) (546) (424) (319) (263) (155) (116) 57 176 331 362 450 580 699 833 963 1,062

Items that will not reclassified into Surplus or deficit -

Net Asset Revaluation increment/(decrement)

4,209 292

Items reclassified to include in surplus or defict - Fair

Value Adjs financial assets at fair value and Fair

Value on assets available for sale assets

55 43 50

Comprehensive Result Excl Telstra (582) 4,346 (460) (1,717) (712) (566) (623) (496) (546) (424) (319) (263) (155) (116) 57 176 331 362 450 580 699 833 963 1,062

33

34 Telstra Project Income 3,445 4,785

35 Telstra Project Expenditure (3,650) (5,350)

36 (205) (565)

37

38 Net result/ Comprehensive Result for the year

(Incl Telstra Project)

0 (637) 94 (1,007) (2,281) (712) (566) (623) (496) (546) (424) (319) (263) (155) (116) 57 176 331 362 450 580 699 833 963 1,062

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 11

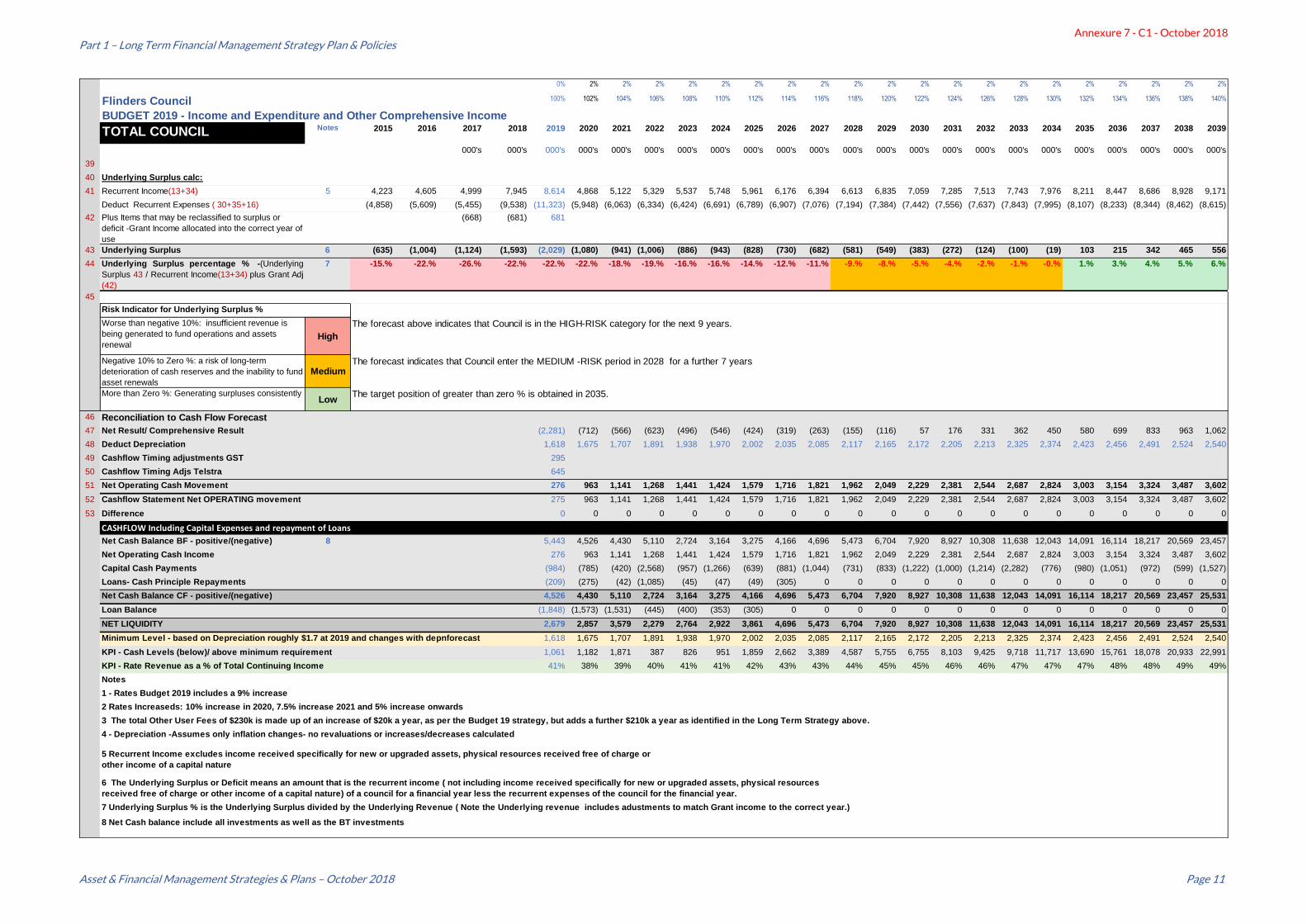

0% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2%

Flinders Council 100% 102% 104% 106% 108% 110% 112% 114% 116% 118% 120% 122% 124% 126% 128% 130% 132% 134% 136% 138% 140%

BUDGET 2019 - Income and Expenditure and Other Comprehensive Income

TOTAL COUNCIL Notes 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039

000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's

39

40 Underlying Surplus calc:

41 Recurrent Income(13+34) 5 4,223 4,605 4,999 7,945 8,614 4,868 5,122 5,329 5,537 5,748 5,961 6,176 6,394 6,613 6,835 7,059 7,285 7,513 7,743 7,976 8,211 8,447 8,686 8,928 9,171

Deduct Recurrent Expenses ( 30+35+16) (4,858) (5,609) (5,455) (9,538) (11,323) (5,948) (6,063) (6,334) (6,424) (6,691) (6,789) (6,907) (7,076) (7,194) (7,384) (7,442) (7,556) (7,637) (7,843) (7,995) (8,107) (8,233) (8,344) (8,462) (8,615)

42 Plus Items that may be reclassified to surplus or

deficit -Grant Income allocated into the correct year of

use

(668) (681) 681

43 Underlying Surplus 6 (635) (1,004) (1,124) (1,593) (2,029) (1,080) (941) (1,006) (886) (943) (828) (730) (682) (581) (549) (383) (272) (124) (100) (19) 103 215 342 465 556

44 Underlying Surplus percentage % -(Underlying

Surplus 43 / Recurrent Income(13+34) plus Grant Adj

(42)

7 -15.% -22.% -26.% -22.% -22.% -22.% -18.% -19.% -16.% -16.% -14.% -12.% -11.% -9.% -8.% -5.% -4.% -2.% -1.% -0.% 1.% 3.% 4.% 5.% 6.%

45

Risk Indicator for Underlying Surplus %

Worse than negative 10%: insufficient revenue is

being generated to fund operations and assets

renewalHigh

Negative 10% to Zero %: a risk of long-term

deterioration of cash reserves and the inability to fund

asset renewals

Medium

More than Zero %: Generating surpluses consistentlyLow

46 Reconciliation to Cash Flow Forecast

47 Net Result/ Comprehensive Result (2,281) (712) (566) (623) (496) (546) (424) (319) (263) (155) (116) 57 176 331 362 450 580 699 833 963 1,062

48 Deduct Depreciation 1,618 1,675 1,707 1,891 1,938 1,970 2,002 2,035 2,085 2,117 2,165 2,172 2,205 2,213 2,325 2,374 2,423 2,456 2,491 2,524 2,540

49 Cashflow Timing adjustments GST 295

50 Cashflow Timing Adjs Telstra 645

51 Net Operating Cash Movement 276 963 1,141 1,268 1,441 1,424 1,579 1,716 1,821 1,962 2,049 2,229 2,381 2,544 2,687 2,824 3,003 3,154 3,324 3,487 3,602

52 Cashflow Statement Net OPERATING movement 275 963 1,141 1,268 1,441 1,424 1,579 1,716 1,821 1,962 2,049 2,229 2,381 2,544 2,687 2,824 3,003 3,154 3,324 3,487 3,602

53 Difference 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

CASHFLOW Including Capital Expenses and repayment of Loans

Net Cash Balance BF - positive/(negative) 8 5,443 4,526 4,430 5,110 2,724 3,164 3,275 4,166 4,696 5,473 6,704 7,920 8,927 10,308 11,638 12,043 14,091 16,114 18,217 20,569 23,457

Net Operating Cash Income 276 963 1,141 1,268 1,441 1,424 1,579 1,716 1,821 1,962 2,049 2,229 2,381 2,544 2,687 2,824 3,003 3,154 3,324 3,487 3,602

Capital Cash Payments (984) (785) (420) (2,568) (957) (1,266) (639) (881) (1,044) (731) (833) (1,222) (1,000) (1,214) (2,282) (776) (980) (1,051) (972) (599) (1,527)

Loans- Cash Principle Repayments (209) (275) (42) (1,085) (45) (47) (49) (305) 0 0 0 0 0 0 0 0 0 0 0 0 0

Net Cash Balance CF - positive/(negative) 4,526 4,430 5,110 2,724 3,164 3,275 4,166 4,696 5,473 6,704 7,920 8,927 10,308 11,638 12,043 14,091 16,114 18,217 20,569 23,457 25,531

Loan Balance (1,848) (1,573) (1,531) (445) (400) (353) (305) 0 0 0 0 0 0 0 0 0 0 0 0 0 0

NET LIQUIDITY 2,679 2,857 3,579 2,279 2,764 2,922 3,861 4,696 5,473 6,704 7,920 8,927 10,308 11,638 12,043 14,091 16,114 18,217 20,569 23,457 25,531

Minimum Level - based on Depreciation roughly $1.7 at 2019 and changes with depnforecast 1,618 1,675 1,707 1,891 1,938 1,970 2,002 2,035 2,085 2,117 2,165 2,172 2,205 2,213 2,325 2,374 2,423 2,456 2,491 2,524 2,540

KPI - Cash Levels (below)/ above minimum requirement 1,061 1,182 1,871 387 826 951 1,859 2,662 3,389 4,587 5,755 6,755 8,103 9,425 9,718 11,717 13,690 15,761 18,078 20,933 22,991

KPI - Rate Revenue as a % of Total Continuing Income 41% 38% 39% 40% 41% 41% 42% 43% 43% 44% 45% 45% 46% 46% 47% 47% 47% 48% 48% 49% 49%

Notes

3 The total Other User Fees of $230k is made up of an increase of $20k a year, as per the Budget 19 strategy, but adds a further $210k a year as identified in the Long Term Strategy above.

7 Underlying Surplus % is the Underlying Surplus divided by the Underlying Revenue ( Note the Underlying revenue includes adustments to match Grant income to the correct year.)

8 Net Cash balance include all investments as well as the BT investments

The forecast above indicates that Council is in the HIGH-RISK category for the next 9 years.

The forecast indicates that Council enter the MEDIUM -RISK period in 2028 for a further 7 years

The target position of greater than zero % is obtained in 2035.

1 - Rates Budget 2019 includes a 9% increase

2 Rates Increaseds: 10% increase in 2020, 7.5% increase 2021 and 5% increase onwards

4 - Depreciation -Assumes only inflation changes- no revaluations or increases/decreases calculated

5 Recurrent Income excludes income received specifically for new or upgraded assets, physical resources received free of charge or

other income of a capital nature

6 The Underlying Surplus or Deficit means an amount that is the recurrent income ( not including income received specifically for new or upgraded assets, physical resources

received free of charge or other income of a capital nature) of a council for a financial year less the recurrent expenses of the council for the financial year.

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 12

0% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2%

Flinders Council 100% 102% 104% 106% 108% 110% 112% 114% 116% 118% 120% 122% 124% 126% 128% 130% 132% 134% 136% 138% 140%

BUDGET 2019 - Income and Expenditure and Other Comprehensive Income

AIRPORT ONLY Notes 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039

000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's

1 Income from continuing operations

2 Recurrent Income

3 Rates and charges 1

4 Rates Increases 2

5 Statutory fees and fines

6 User fees 370 377 385 392 399 407 414 422 429 436 444 451 459 466 473 481 488 496 503 510 518

7 Airport Fees increases 20 41 62 84 106 128 151 174 198 222 246 271 296 322 348 374 401 428 456 484

8 Other User fees increases - AIRPORT RELATED increases3 210 218 223 227 231 235 239 244 248 252 256 260 265 269 273 277 281 286 290 294

9 Grants - Operational 107

10 Interest

11 Other income

12 Investment revenue from water corporation

13 0 0 0 0 477 608 644 677 710 743 777 812 847 882 917 953 990 1,027 1,064 1,101 1,139 1,178 1,217 1,256 1,295

14 Capital income

15 Grants Capital

Contributions - non monetary assets

16 Net gain/(loss) on disposal of property, infrastructure,

plant and equipment

17 Recognition of land under roads

18 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

19

20 Total income from continuing operations 0 0 0 0 477 608 644 677 710 743 777 812 847 882 917 953 990 1,027 1,064 1,101 1,139 1,178 1,217 1,256 1,295

21

22 Expenses

23 Employee benefits (215) (219) (224) (228) (232) (237) (241) (245) (249) (254) (258) (262) (267) (271) (275) (280) (284) (288) (292) (297) (301)

24 Materials and services (160) (163) (166) (170) (173) (176) (179) (182) (186) (189) (192) (195) (198) (202) (205) (208) (211) (214) (218) (221) (224)

25 Impairment of debts

26 Depreciation and amortisation 4 (299) (305) (311) (444) (450) (456) (462) (468) (474) (480) (486) (492) (498) (504) (603) (609) (615) (621) (627) (633) (639)

27 Finance costs

28 Other expenses

29 Net Adjustments to Future Expenses savings/(costs)

30 Total expenses from continuing operations 0 0 0 0 (674) (687) (701) (841) (855) (868) (882) (895) (909) (922) (936) (949) (963) (976) (1,083) (1,097) (1,110) (1,124) (1,137) (1,151) (1,164)

31

32 Net result for Continuing Operations (Excl

Telstra Project)

0 0 0 0 (197) (80) (57) (165) (145) (125) (104) (83) (62) (40) (18) 4 27 51 (20) 4 29 54 79 105 131

Items that will not reclassified into Surplus or deficit -

Net Asset Revaluation increment/(decrement)

Items reclassified to include in surplus or defict - Fair

Value Adjs financial assets at fair value and Fair

Value on assets available for sale assets

Comprehensive Result 0 0 0 (197) (80) (57) (165) (145) (125) (104) (83) (62) (40) (18) 4 27 51 (20) 4 29 54 79 105 131

33

34 Telstra Project Income

35 Telstra Project Expenditure

36 0 0

37

38 Net result for the year (Incl Telstra Project) 0 0 0 0 (197) (80) (57) (165) (145) (125) (104) (83) (62) (40) (18) 4 27 51 (20) 4 29 54 79 105 131

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 13

0% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2%

Flinders Council 100% 102% 104% 106% 108% 110% 112% 114% 116% 118% 120% 122% 124% 126% 128% 130% 132% 134% 136% 138% 140%

BUDGET 2019 - Income and Expenditure and Other Comprehensive Income

AIRPORT ONLY Notes 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039

000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's

39

40 Underlying Surplus calc:

41 Recurrent Income(13+34) 5 477 608 644 677 710 743 777 812 847 882 917 953 990 1,027 1,064 1,101 1,139 1,178 1,217 1,256 1,295

Deduct Recurrent Expenses ( 30+35+16) (674) (687) (701) (841) (855) (868) (882) (895) (909) (922) (936) (949) (963) (976) (1,083) (1,097) (1,110) (1,124) (1,137) (1,151) (1,164)

42 Plus Items that may be reclassified to surplus or

deficit -Grant Income allocated into the correct year of

use

43 Underlying Surplus 6 0 0 0 0 (197) (80) (57) (165) (145) (125) (104) (83) (62) (40) (18) 4 27 51 (20) 4 29 54 79 105 131

44 Underlying Surplus percentage % -(Underlying

Surplus 43 / Recurrent Income(13+34) plus Grant Adj

(42)

7 -41.% -13.% -9.% -24.% -20.% -17.% -13.% -10.% -7.% -5.% -2.% 0.% 3.% 5.% -2.% 0.% 3.% 5.% 7.% 8.% 10.%

45

Risk Indicator for Underlying Surplus %

Worse than negative 10%: insufficient revenue is

being generated to fund operations and assets

renewalHigh

Negative 10% to Zero %: a risk of long-term

deterioration of cash reserves and the inability to fund

asset renewals

Medium

More than Zero %: Generating surpluses consistentlyLow

46 Reconciliation to Cash Flow Forecast

47 Net Result (197) (80) (57) (165) (145) (125) (104) (83) (62) (40) (18) 4 27 51 (20) 4 29 54 79 105 131

48 Deduct Depreciation 299 305 311 444 450 456 462 468 474 480 486 492 498 504 603 609 615 621 627 633 639

49 Cashflow Timing adjustments GST

50 Cashflow Timing Adjs Telstra

51 Net Operating Cash Movement 102 225 254 279 305 331 357 384 412 439 467 496 525 554 584 614 644 675 707 738 770

52 Cashflow Statement Net OPERATING movement

53 Difference 102 225 254 279 305 331 357 384 412 439 467 496 525 554 584 614 644 675 707 738 770

CASHFLOW Including Capital Expenses and repayment of Loans

Net Cash Balance BF - positive/(negative) 8 0 (16) 205 459 (1,170) (865) (647) (289) 95 454 894 1,289 1,736 2,261 2,815 1,863 2,448 3,092 3,768 4,474 5,212

Net Operating Cash Income 102 225 254 279 305 331 357 384 412 439 467 496 525 554 584 614 644 675 707 738 770

Capital Cash Payments (118) (4) 0 (1,908) 0 (112) 0 0 (52) 0 (72) (49) 0 0 (1,536) (29) 0 0 0 0 (112)

Loans- Cash Principle Repayments

Net Cash Balance CF - positive/(negative) (16) 205 459 (1,170) (865) (647) (289) 95 454 894 1,289 1,736 2,261 2,815 1,863 2,448 3,092 3,768 4,474 5,212 5,871

Loan Balance

NET LIQUIDITY (16) 205 459 (1,170) (865) (647) (289) 95 454 894 1,289 1,736 2,261 2,815 1,863 2,448 3,092 3,768 4,474 5,212 5,871

Minimum Level - based on Depreciation roughly $300k at 2019 and changes with depnforecast 299 305 311 444 450 456 462 468 474 480 486 492 498 504 603 609 615 621 627 633 639

KPI - Cash Levels (below)/ above minimum requirement (315) (100) 148 (1,614) (1,315) (1,103) (751) (373) (19) 414 803 1,244 1,763 2,311 1,259 1,839 2,477 3,146 3,847 4,579 5,232

The Airport only turns cash positive in 2028. The negative cash period commencing year 2022 to 2027 is due to the funding of the Airport long Runway of $1.8m

The Short Runway, scheduled for 2033, costing $1.1 million is however able to be funded by the Airport under this Strategy.

Notes

3 The total Other User Fees of $230k is made up of an increase of $20k a year, as per the Budget 19 strategy, but adds a further $210k a year as identified in the Long Term Strategy above.

7 Underlying Surplus % is the Underlying Surplus divided by the Underlying Revenue ( Note the Underlying revenue includes adustments to match Grant income to the correct year.)

1 - Rates Budget 2019 includes a 9% increase

2 Rates Increaseds: 10% increase in 2020, 7.5% increase 2021 and 5% increase onwards

8 Net Cash balance include all investments as well as the BT investments

4 - Depreciation -Assumes only inflation changes- no revaluations or increases/decreases calculated

The forecast above indicates that the AIRPORT is in the HIGH-RISK category for 8 years. The negative underlying

surpluses during this period , indicate the proportion of support that the Municipal contributes towards the Airport. Under

this strategy the future values are relatively low and considered an acceptable strategy.

The forecast indicates that Council enter the MEDIUM -RISK period in 2027 for a further 3 years

The target position of greater than zero % is obtained in 2030, and for one year in 2033, it reverts to the medium

category, during the year of funding the Short Runway.

5 Recurrent Income excludes income received specifically for new or upgraded assets, physical resources received free of charge or

other income of a capital nature

6 The Underlying Surplus or Deficit means an amount that is the recurrent income ( not including income received specifically for new or upgraded assets, physical resources

received free of charge or other income of a capital nature) of a council for a financial year less the recurrent expenses of the council for the financial year.

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 14

0% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2%

Flinders Council 100% 102% 104% 106% 108% 110% 112% 114% 116% 118% 120% 122% 124% 126% 128% 130% 132% 134% 136% 138% 140%

BUDGET 2019 - Income and Expenditure and Other Comprehensive Income

MUNICIPAL ONLY Notes 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039

000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's

1 Income from continuing operations

2 Recurrent Income

3 Rates and charges 1 1,768 1,803 1,839 1,874 1,910 1,945 1,980 2,016 2,051 2,086 2,122 2,157 2,192 2,228 2,263 2,299 2,334 2,369 2,405 2,440 2,475

4 Rates Increases 2 0 180 318 412 507 605 704 804 907 1,011 1,117 1,225 1,335 1,446 1,559 1,674 1,791 1,910 2,030 2,152 2,276

5 Statutory fees and fines 41 42 43 44 45 46 46 47 48 49 50 51 51 52 53 54 55 55 56 57 58

6 User fees 350 357 364 371 378 385 392 399 406 413 420 427 434 441 448 455 462 469 476 483 490

7 Airport Fees increases 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

8 Other User fees increases 3 0 20 21 21 22 22 22 23 23 24 24 24 25 25 26 26 26 27 27 28 28

9 Grants - Operational 1,021 1,713 1,746 1,780 1,813 1,847 1,881 1,914 1,948 1,981 2,015 2,048 2,082 2,116 2,149 2,183 2,216 2,250 2,284 2,317 2,351

10 Interest 75 46 47 48 49 50 50 51 52 53 54 55 56 57 58 59 59 60 61 62 63

11 Other income 42 43 44 45 46 47 47 48 49 50 51 52 52 53 54 55 56 57 58 58 59

12 Investment revenue from water corporation 54 55 56 57 58 59 60 62 63 64 65 66 67 68 69 70 71 72 73 75 76

13 0 0 0 0 3,352 4,260 4,478 4,652 4,828 5,005 5,184 5,365 5,547 5,731 5,918 6,105 6,295 6,486 6,680 6,875 7,071 7,270 7,470 7,672 7,876

14 Capital income

15 Grants Capital 428 368 375 383 390 397 404 411 419 426 433 440 448 455 462 469 476 484 491 498 505

Contributions - non monetary assets 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

16 Net gain/(loss) on disposal of property, infrastructure,

plant and equipment

30 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

17 Recognition of land under roads 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

18 0 0 0 0 458 368 375 383 390 397 404 411 419 426 433 440 448 455 462 469 476 484 491 498 505

19

20 Total income from continuing operations 0 0 0 0 3,810 4,629 4,854 5,035 5,217 5,402 5,588 5,776 5,966 6,157 6,351 6,546 6,743 6,941 7,142 7,344 7,548 7,753 7,961 8,170 8,381

21

22 Expenses

23 Employee benefits (1,973) (2,012) (2,052) (2,091) (2,131) (2,170) (2,209) (2,249) (2,288) (2,328) (2,367) (2,407) (2,446) (2,486) (2,525) (2,565) (2,604) (2,643) (2,683) (2,722) (2,762)

24 Materials and services (1,937) (1,976) (2,015) (2,054) (2,092) (2,131) (2,170) (2,209) (2,247) (2,286) (2,325) (2,364) (2,402) (2,441) (2,480) (2,518) (2,557) (2,596) (2,635) (2,673) (2,712)

25 Impairment of debts 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

26 Depreciation and amortisation 4 (1,319) (1,370) (1,397) (1,447) (1,488) (1,514) (1,541) (1,567) (1,611) (1,637) (1,679) (1,681) (1,707) (1,709) (1,721) (1,765) (1,808) (1,834) (1,864) (1,890) (1,901)

27 Finance costs (101) (103) (105) (107) (109) (111) (113) (115) (117) (119) (121) (123) (125) (127) (129) (131) (133) (135) (137) (139) (141)

28 Other expenses 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

29 Net Adjustments to Future Expenses savings/(costs) 0 201 205 206 251 103 126 128 97 98 44 81 87 102 95 81 106 101 112 114 66

30 Total expenses from continuing operations 0 0 0 0 (5,330) (5,261) (5,363) (5,493) (5,569) (5,823) (5,907) (6,011) (6,167) (6,272) (6,448) (6,493) (6,594) (6,661) (6,760) (6,898) (6,997) (7,109) (7,207) (7,312) (7,450)

31

32 Net result for Continuing Operations (Excl

Telstra Project)

0 0 0 0 (1,520) (632) (509) (458) (351) (421) (319) (235) (201) (115) (98) 53 149 280 382 445 551 645 754 858 931

Items that will not reclassified into Surplus or deficit -

Net Asset Revaluation increment /(decrement)

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Items reclassified to include in surplus or defict - Fair

Value Adjs financial assets at fair value and Fair

Value on assets available for sale assets

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Comprehensive Result 0 0 0 (1,520) (632) (509) (458) (351) (421) (319) (235) (201) (115) (98) 53 149 280 382 445 551 645 754 858 931

33 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

34 Telstra Project Income 4,785 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

35 Telstra Project Expenditure (5,350) 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

36 0 (565)

37

38 Net result for the year (Incl Telstra Project) 0 0 0 0 (2,084) (632) (509) (458) (351) (421) (319) (235) (201) (115) (98) 53 149 280 382 445 551 645 754 858 931

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 15

0% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2%

Flinders Council 100% 102% 104% 106% 108% 110% 112% 114% 116% 118% 120% 122% 124% 126% 128% 130% 132% 134% 136% 138% 140%

BUDGET 2019 - Income and Expenditure and Other Comprehensive Income

MUNICIPAL ONLY Notes 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039

000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's

39

40 Underlying Surplus calc:

41 Recurrent Income(13+34) 5 8,137 4,260 4,478 4,652 4,828 5,005 5,184 5,365 5,547 5,731 5,918 6,105 6,295 6,486 6,680 6,875 7,071 7,270 7,470 7,672 7,876

Deduct Recurrent Expenses ( 30+35+16) (10,650) (5,261) (5,363) (5,493) (5,569) (5,823) (5,907) (6,011) (6,167) (6,272) (6,448) (6,493) (6,594) (6,661) (6,760) (6,898) (6,997) (7,109) (7,207) (7,312) (7,450)

42 Plus Items that may be reclassified to surplus or

deficit -Grant Income allocated into the correct year of

use

681

43 Underlying Surplus 6 0 0 0 0 (1,832) (1,000) (884) (841) (741) (818) (724) (647) (620) (541) (531) (388) (299) (174) (80) (24) 74 161 263 360 425

44 Underlying Surplus percentage % -(Underlying

Surplus 43 / Recurrent Income(13+34) plus Grant Adj

(42)

7 -21.% -23.% -20.% -18.% -15.% -16.% -14.% -12.% -11.% -9.% -9.% -6.% -5.% -3.% -1.% -0.% 1.% 2.% 4.% 5.% 5.%

45

Risk Indicator for Underlying Surplus %

Worse than negative 10%: insufficient revenue is

being generated to fund operations and assets

renewalHigh

Negative 10% to Zero %: a risk of long-term

deterioration of cash reserves and the inability to fund

asset renewals

Medium

More than Zero %: Generating surpluses consistentlyLow

46 Reconciliation to Cash Flow Forecast

47 Net Result (2,084) (632) (509) (458) (351) (421) (319) (235) (201) (115) (98) 53 149 280 382 445 551 645 754 858 931

48 Deduct Depreciation 1,319 1,370 1,397 1,447 1,488 1,514 1,541 1,567 1,611 1,637 1,679 1,681 1,707 1,709 1,721 1,765 1,808 1,834 1,864 1,890 1,901

49 Cashflow Timing adjustments GST 295

50 Cashflow Timing Adjs Telstra 645

51 Net Operating Cash Movement 174 738 888 989 1,137 1,093 1,221 1,332 1,410 1,522 1,582 1,733 1,856 1,989 2,103 2,210 2,359 2,479 2,618 2,749 2,832

52 Cashflow Statement Net OPERATING movement

53 Difference 174 738 888 989 1,137 1,093 1,221 1,332 1,410 1,522 1,582 1,733 1,856 1,989 2,103 2,210 2,359 2,479 2,618 2,749 2,832

CASHFLOW Including Capital Expenses and repayment of Loans

Net Cash Balance BF - positive/(negative) 8 5,443 4,543 4,225 4,651 3,895 4,029 3,922 4,455 4,601 5,019 5,810 6,631 7,191 8,047 8,823 10,180 11,643 13,021 14,449 16,095 18,244

Net Operating Cash Income 174 738 888 989 1,137 1,093 1,221 1,332 1,410 1,522 1,582 1,733 1,856 1,989 2,103 2,210 2,359 2,479 2,618 2,749 2,832

Capital Cash Payments (866) (781) (420) (660) (957) (1,154) (639) (881) (992) (731) (761) (1,173) (1,000) (1,214) (746) (747) (980) (1,051) (972) (599) (1,415)

Loans- Cash Principle Repayments (209) (275) (42) (1,085) (45) (47) (49) (305) 0 0 0 0 0 0 0 0 0 0 0 0 0

Net Cash Balance CF - positive/(negative) 4,543 4,225 4,651 3,895 4,029 3,922 4,455 4,601 5,019 5,810 6,631 7,191 8,047 8,823 10,180 11,643 13,021 14,449 16,095 18,244 19,661

Loan Balance (1,848) (1,573) (1,531) (445) (400) (353) (305) 0 0 0 0 0 0 0 0 0 0 0 0 0 0

NET LIQUIDITY 2,695 2,652 3,120 3,449 3,629 3,568 4,150 4,601 5,019 5,810 6,631 7,191 8,047 8,823 10,180 11,643 13,021 14,449 16,095 18,244 19,661

Minimum Level - based on Depreciation roughly $1,300k at 2019 and changes with depn forecast 1,319 1,370 1,397 1,447 1,488 1,514 1,541 1,567 1,611 1,637 1,679 1,681 1,707 1,709 1,721 1,765 1,808 1,834 1,864 1,890 1,901

KPI - Cash Levels (below)/ above minimum requirement 1,376 1,282 1,723 2,002 2,141 2,054 2,610 3,034 3,408 4,173 4,952 5,511 6,340 7,114 8,459 9,878 11,213 12,615 14,231 16,354 17,760

KPI - Rate Revenue as a % of Total Continuing Income 46% 43% 44% 45% 46% 47% 48% 49% 50% 50% 51% 52% 52% 53% 54% 54% 55% 55% 56% 56% 57%

Notes

3 The total Other User Fees of $230k is made up of an increase of $20k a year, as per the Budget 19 strategy, but adds a further $210k a year as identified in the Long Term Strategy above.

7 Underlying Surplus % is the Underlying Surplus divided by the Underlying Revenue ( Note the Underlying revenue includes adustments to match Grant income to the correct year.)

8 Net Cash balance include all investments as well as the BT investments

1 - Rates Budget 2019 includes a 9% increase

2 Rates Increaseds: 10% increase in 2020, 7.5% increase 2021 and 5% increase onwards

4 - Depreciation -Assumes only inflation changes- no revaluations or increases/decreases calculated

5 Recurrent Income excludes income received specifically for new or upgraded assets, physical resources received free of

charge or other income of a capital nature

The forecast above indicates that the Municipal is in the HIGH-RISK category for 9 years.

The forecast indicates that the Municipal enter the MEDIUM -RISK period in 2028 for a further 7 years

The target position of greater than zero % is achieved in year 2035.

6 The Underlying Surplus or Deficit means an amount that is the recurrent income ( not including income received specifically for new or upgraded assets, physical

resources received free of charge or other income of a capital nature) of a council for a financial year less the recurrent expenses of the council for the financial year.

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 16

0% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2%

Flinders Council 100% 102% 104% 106% 108% 110% 112% 114% 116% 118% 120% 122% 124% 126% 128% 130% 132% 134% 136% 138% 140%

BUDGET 2019 - Income and Expenditure and Other Comprehensive Income

Depreciation and amortisation Asset

Value at

Acquisitio

n

Year

Commences

Asset Value at

Acquisition-

indexed to incl

inflation

Estimated

Useful

economic

Life

Annual

Depn

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039

000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's 000's

COUNCIL ALLDepreciation and amortisation - current level of existing asset base 1,618 1,650 1,682 1,715 1,747 1,779 1,812 1,844 1,877 1,909 1,941 1,974 2,006 2,038 2,071 2,103 2,135 2,168 2,200 2,232 2,265

Assets adding to the BASE level which will increase depreciation:

Airport Runway - long 3,600 2022 3,816 30 127 127 127 127 127 127 127 127 127 127 127 127 127 127 127 127 127 127 127

Airport Runway - Short 2,000 2033 2,560 30 85 85 85 85 85 85 85 85

Airport New - Plant - fuel facility Depn 100 2033 128 15 9 9 9 9 9 9 9 9

Waste Program Assets under asset 4 - Year 1 250 2019 250 10 25 25 25 25 25 25 25 25 25 25 25

Waste Program Assets under asset 4 - Year 2 2020 0 10 0 0 0 0 0 0 0 0 0 0 0 0

Waste Program Assets under asset 4 - Year 3 2021 10 0

Waste Program Assets under asset 4 - Year 4 230 2022 244 10 24 24 24 24 24 24 24 24 24 24 24

Waste Program Assets under asset 4 - Year 5 130 2023 140 10 14 14 14 14 14 14 14 14 14 14 14

Waste Program Assets under asset 4 - Year 9 150 2027 174 10 17 17 17 17 17 17 17 17 17 17 17

Waste Program Assets under asset 4 - Year 11 130 2029 156 10 16 16 16 16 16 16 16 16 16 16 16

Waste Program Assets under asset 4 - Year 14 0 2032 0 10 0 0 0 0 0 0 0 0 0

Waste Program Assets under asset 4 - Year 16 130 2034 169 10 17 17 17 17 17 17 17

Waste Program Assets under asset 4 - Year 17 130 2035 172 10 17 17 17 17 17 17

Waste Program Assets under asset 4 - Year 18 2036 10 0 20 20 20

Waste Program Assets under asset 4 - Year 19 150 2037 204 10 20

Waste Program Assets under asset 4 - Year 20

Depreciation and amortisation including Inflation 7,000 8,013 1,618 1,675 1,707 1,891 1,938 1,970 2,002 2,035 2,085 2,117 2,165 2,172 2,205 2,213 2,325 2,374 2,423 2,456 2,491 2,524 2,540

Assumptions

1 - Base level depreciation is set from Budget 19, and assumes that the increases and decreases of replacing assets will be stable

2 - Large NEW asset additions have been added to the depreciation calculation in the table above.

3 - Acquisitions have been indexed to include a 2% Inflation

AIRPORT ONLYBase Level Depn 299 305 311 317 323 329 335 341 347 352 358 364 370 376 382 388 394 400 406 412 418

New - Plant - fuel facility Depn 100 2033 128 15 9 9 9 9 9 9 9 9

New -Airport Runway - long Depn 3,600 2022 3,816 30 127 127 127 127 127 127 127 127 127 127 127 127 127 127 127 127 127 127 127

New -Airport Runway - Short Depn 2,000 2033 2,560 30 85 85 85 85 85 85 85 85

AIRPORT Depreciation and amortisation including Inflation 299 305 311 444 450 456 462 468 474 480 486 492 498 504 603 609 615 621 627 633 639

Municipal ONLYBase Level Depn 1,319 1,345 1,372 1,398 1,424 1,451 1,477 1,504 1,530 1,556 1,583 1,609 1,636 1,662 1,688 1,715 1,741 1,767 1,794 1,820 1,847

New -Waste Program Assets 0 25 25 49 63 63 63 63 81 81 96 71 71 47 33 50 67 67 70 70 54

Municipal Depreciation and amortisation including Inflation 1,319 1,370 1,397 1,447 1,488 1,514 1,541 1,567 1,611 1,637 1,679 1,681 1,707 1,709 1,721 1,765 1,808 1,834 1,864 1,890 1,901

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 17

S5(c) For each financial year of the plan, a statement of financial position including estimates of –

(i) Current and non-current assets; and

(ii) Current and non-current liabilities; and

(iii) Net assets; and

(iv) Equity, including reserves;

This section has not been completed. The work required in this area will be developed in future Strategic modelling, however, due to the nature of the work undertaken by the Council, this area is a low risk impact area, as the dynamics of the income and expenditure should not present any major fluctuations in future levels of current and non-current assets and liabilities i.e. for example Debtors, creditors, Inventory holdings, Capital works in progress.

S5(d) For each financial year of the plan, a cashflow statement, including estimates of

(i) Receipts, payments, dividends and net cash from operational activities, financial activities including loan borrowings, and investment activities; and

(ii) Net increases or decreases in cash held; and

(iii) Cash and cash equivalents held at the beginning of the period; and

(iv) Cash and cash equivalents held at the end of the period

This section has been completed as per the following Long-term Cashflow forecast for Budget 2019

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 18

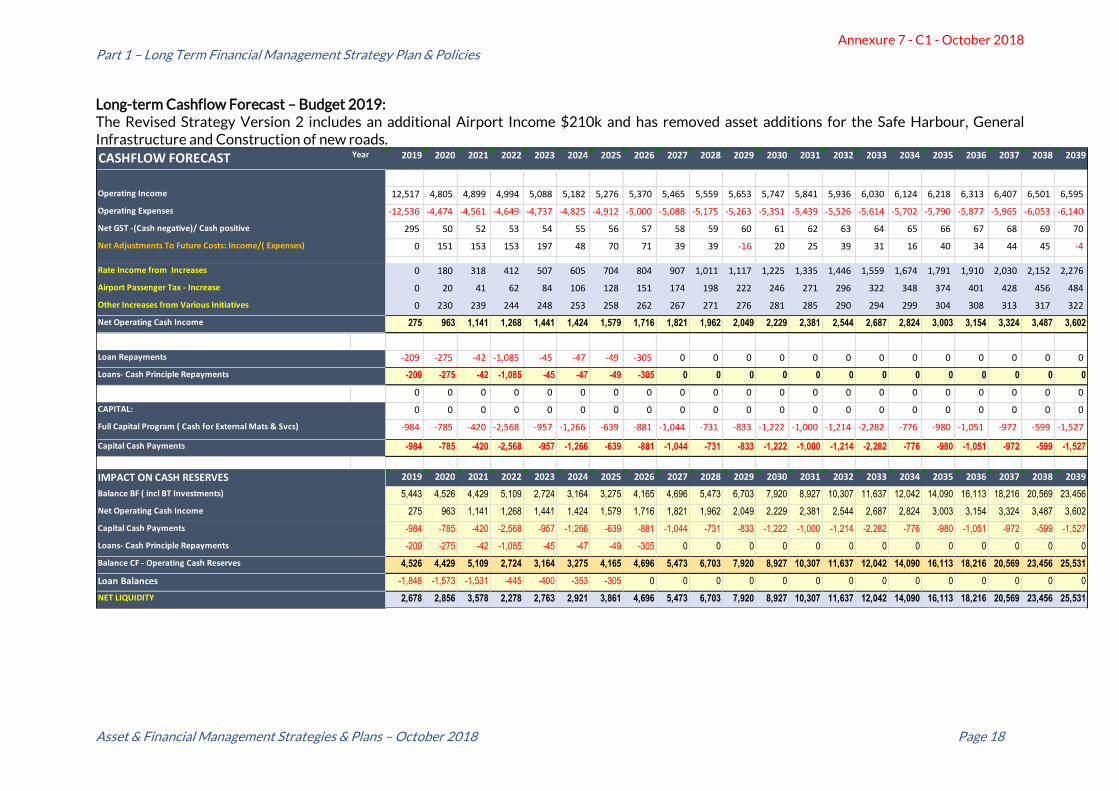

Long-term Cashflow Forecast – Budget 2019: The Revised Strategy Version 2 includes an additional Airport Income $210k and has removed asset additions for the Safe Harbour, General Infrastructure and Construction of new roads.

CASHFLOW FORECAST Year 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039

Operating Income 12,517 4,805 4,899 4,994 5,088 5,182 5,276 5,370 5,465 5,559 5,653 5,747 5,841 5,936 6,030 6,124 6,218 6,313 6,407 6,501 6,595

Operating Expenses -12,536 -4,474 -4,561 -4,649 -4,737 -4,825 -4,912 -5,000 -5,088 -5,175 -5,263 -5,351 -5,439 -5,526 -5,614 -5,702 -5,790 -5,877 -5,965 -6,053 -6,140

Net GST -(Cash negative)/ Cash positive 295 50 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70

Net Adjustments To Future Costs: Income/( Expenses) 0 151 153 153 197 48 70 71 39 39 -16 20 25 39 31 16 40 34 44 45 -4

Rate Income from Increases 0 180 318 412 507 605 704 804 907 1,011 1,117 1,225 1,335 1,446 1,559 1,674 1,791 1,910 2,030 2,152 2,276

Airport Passenger Tax - Increase 0 20 41 62 84 106 128 151 174 198 222 246 271 296 322 348 374 401 428 456 484

Other Increases from Various Initiatives 0 230 239 244 248 253 258 262 267 271 276 281 285 290 294 299 304 308 313 317 322

Net Operating Cash Income 275 963 1,141 1,268 1,441 1,424 1,579 1,716 1,821 1,962 2,049 2,229 2,381 2,544 2,687 2,824 3,003 3,154 3,324 3,487 3,602

Loan Repayments -209 -275 -42 -1,085 -45 -47 -49 -305 0 0 0 0 0 0 0 0 0 0 0 0 0

Loans- Cash Principle Repayments -209 -275 -42 -1,085 -45 -47 -49 -305 0 0 0 0 0 0 0 0 0 0 0 0 0

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

CAPITAL: 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Full Capital Program ( Cash for External Mats & Svcs) -984 -785 -420 -2,568 -957 -1,266 -639 -881 -1,044 -731 -833 -1,222 -1,000 -1,214 -2,282 -776 -980 -1,051 -972 -599 -1,527

Capital Cash Payments -984 -785 -420 -2,568 -957 -1,266 -639 -881 -1,044 -731 -833 -1,222 -1,000 -1,214 -2,282 -776 -980 -1,051 -972 -599 -1,527

IMPACT ON CASH RESERVES 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039

Balance BF ( incl BT Investments) 5,443 4,526 4,429 5,109 2,724 3,164 3,275 4,165 4,696 5,473 6,703 7,920 8,927 10,307 11,637 12,042 14,090 16,113 18,216 20,569 23,456

Net Operating Cash Income 275 963 1,141 1,268 1,441 1,424 1,579 1,716 1,821 1,962 2,049 2,229 2,381 2,544 2,687 2,824 3,003 3,154 3,324 3,487 3,602

Capital Cash Payments -984 -785 -420 -2,568 -957 -1,266 -639 -881 -1,044 -731 -833 -1,222 -1,000 -1,214 -2,282 -776 -980 -1,051 -972 -599 -1,527

Loans- Cash Principle Repayments -209 -275 -42 -1,085 -45 -47 -49 -305 0 0 0 0 0 0 0 0 0 0 0 0 0

Balance CF - Operating Cash Reserves 4,526 4,429 5,109 2,724 3,164 3,275 4,165 4,696 5,473 6,703 7,920 8,927 10,307 11,637 12,042 14,090 16,113 18,216 20,569 23,456 25,531

Loan Balances -1,848 -1,573 -1,531 -445 -400 -353 -305 0 0 0 0 0 0 0 0 0 0 0 0 0 0

NET LIQUIDITY 2,678 2,856 3,578 2,278 2,763 2,921 3,861 4,696 5,473 6,703 7,920 8,927 10,307 11,637 12,042 14,090 16,113 18,216 20,569 23,456 25,531

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 19

S5(2)(e) A description of the financial management strategies to be adopted by the council, including financial targets and their rationale;

Council is well behind in undertaking the comprehensive work that is required in relation to the financial management strategies. There is much that needs to be done in this area to establish risk and evaluate the rationale of costs in relation to income, and the ability of Council to assist in funding large projects in the future.

From the work performed in section 5.2, it is clear from the presented strategy that the Council currently does not have the ability to fund large projects.

The 2019 Budget and future projections have taken a step forward to begin to identify some of the financial targets. These include setting a minimum net cash reserve base at $1.7million, as well as an in-depth examination of the capital program which affects the cash output.

The predictions of the underlying surplus indicate the future sustainability of the Council, to assist in decision making, and the current strategy does not reflect a positive outlook.

S5(2)(f) A comparison of projected financial performance against targets (determined by the council) for financial indicators, including those indicators specified in an order made under section 84(2A) of the ACT for each financial year included in the Long-term financial plan;

This section has not been fully completed as we are yet to determine the range of key performance indicators that are relevant to improve Council’s decision making. We have however identified the following KPI’s:

KPI – minimum cash holding $1.7 million:

As a critical measure to base the financial cashflow forecast, and to provide sound decision making, the minimum cash holding KPI has been set at $1.7 million dollars. This is the minimum cash level that reaches a base of zero net profitability, after we include depreciation. Depreciation is estimated to be $1.6 million in the 2019 Budget.

KPI – Ideal Net Cash Level:

Although the graph below has identified a measure to restore Net Cash levels to the 2015 position, Council has indicated that this level is not necessarily the ideal level that Council should strive to attain. The calculation behind this KPI will need to be explored, reviewed and agreed upon in future strategic work. At present this has not been set, however its measure is not as important to target, because the basic measure of a LOW-RISK underlying surplus is the ultimate measure for future sustainability, and through achieving the underlying surplus ratio, the Ideal cash level would most likely become evident.

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 20

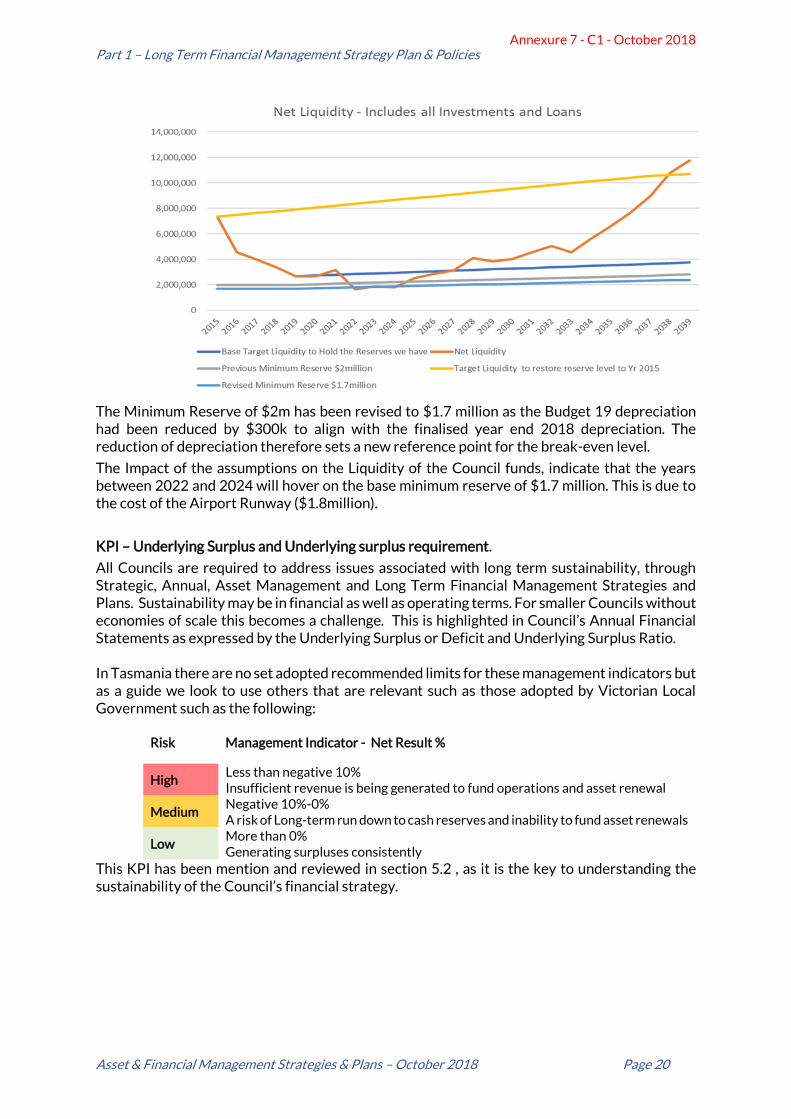

The Minimum Reserve of $2m has been revised to $1.7 million as the Budget 19 depreciation had been reduced by $300k to align with the finalised year end 2018 depreciation. The reduction of depreciation therefore sets a new reference point for the break-even level.

The Impact of the assumptions on the Liquidity of the Council funds, indicate that the years between 2022 and 2024 will hover on the base minimum reserve of $1.7 million. This is due to the cost of the Airport Runway ($1.8million).

KPI – Underlying Surplus and Underlying surplus requirement.

All Councils are required to address issues associated with long term sustainability, through Strategic, Annual, Asset Management and Long Term Financial Management Strategies and Plans. Sustainability may be in financial as well as operating terms. For smaller Councils without economies of scale this becomes a challenge. This is highlighted in Council’s Annual Financial Statements as expressed by the Underlying Surplus or Deficit and Underlying Surplus Ratio. In Tasmania there are no set adopted recommended limits for these management indicators but as a guide we look to use others that are relevant such as those adopted by Victorian Local Government such as the following:

Risk Management Indicator - Net Result %

High Less than negative 10% Insufficient revenue is being generated to fund operations and asset renewal

Medium Negative 10%-0% A risk of Long-term run down to cash reserves and inability to fund asset renewals

Low More than 0% Generating surpluses consistently

This KPI has been mention and reviewed in section 5.2 , as it is the key to understanding the sustainability of the Council’s financial strategy.

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 21

S(5)(2)(g) All assumptions used in the development of the estimates referred to in paragraphs (a), (b), (c), and (d).

Assumptions for the Long-term financial plan:

Estimated Revenues:

• Projected revenues Include a 2% inflationary rate;

• Rateable income applies 9% increase in 2019, 10% increase in 2020, 7.5% increase in 2021 and 5% increase in the years beyond to 2039;

• Airport Passenger Service Charges, applies an Increase $9 to $12 passenger tax in 2019, and thereafter a $1 increase each year over the next twenty years;

• User fees and Charges includes a $20,000 increase in Budget 2019 from various identified initiatives, but no further increases have been included in the years beyond;

• Grant Income (Operational and Capital), includes only known Grant Income in the 2019 Budget, and the years beyond 2019 recognise only the sustainable (and assumed ongoing) grants such as FAGS grant and Roads to recovery Grants;

• Grant Interest income from loan closures have been included in the projected income.

• Net GST on operational income and expenditure has been assumed to be flat at $50k a year positive and therefore does not affect the fluctuations of cash in the projections.

Estimated Expenditure – Operational:

• Projected operational expenditure Includes a 2% inflationary rate;

• One-off costs identified in 2019 have been removed from the ongoing cost projection;

• Telstra one-off costs in 2019 do not continue into the future projections.

• Additional costs have been included in the projection where increases have been identified for example the Waste Management program cost increases.

• Repairs and maintenance for the buildings section has had a full review after site visits and evaluation of each building/facility in order to predict more accurately the ongoing repairs and maintenance for this section.

Capital Expenditure:

• The Capital works program has reviewed and analysed the requirements of each class of assets in detail. It uses estimated assumptions to identify the forecasted capital replacement timescales, and though a logical approach has been employed for each category, a full asset review has not been performed to solidify the assumptions made.

• Projected capital expenditure Includes a 2% inflationary rate;

• Roads, Bridges and Traffic infrastructure includes sufficient expenditure to meet the Roads to Recovery Grant criteria over the next 5 years. It does however exclude any construction of roads until 2029 due to cash constraints;

• Plant and Equipment has had a full review and most assets have been scheduled into the program in the recommended time frame except for two large plant purchases which were pushed forward by one year, to balance cash levels;

• Building upgrades have been scheduled in the Budget 2019 program as most of the building works either have grant income attached to them and are carry overs from 2018. The period beyond 2019 has minimal capital allocated for the building upgrades;

• All other minor asset classes have been reviewed and included in the capital program.

Annexure 7 - C1 - October 2018

Part 1 – Long Term Financial Management Strategy Plan & Policies

Asset & Financial Management Strategies & Plans – October 2018 Page 22

• The Airport Runway upgrade assumes a 50% grant income will be achieved, leaving $1.8million cost to be incurred by the Council.

• The Safe Harbour capital project assumes half a million cost will be incurred by the Council and the remainder $5 million of cost is funded through grants.

Loans and Borrowings.

• The Cash projection assumes that all loans will be repaid, and no additional loans taken out in the 20-year plan.

• The principles underlying borrowings has been identified later in point 6.2 (d).

• The Net Cash position, to be used for cashflow projections is $5.6 million total investments and cash holdings less $2 million in loans.

S5(3) For the purposes of subclause (2)(d)(i), the estimates are to include separate estimates in respect of renewal, upgrade and new capital expenditure in relation to the activities to in that clause.

The detailed workings of the Capital/ Asset Program have identified future requirements under the classifications of ‘renewal, upgrade/capital replacement, and new capital. Although the Budget 2019 documentation has not shown the capital programs in these classifications, the detailed work has this level of depth.

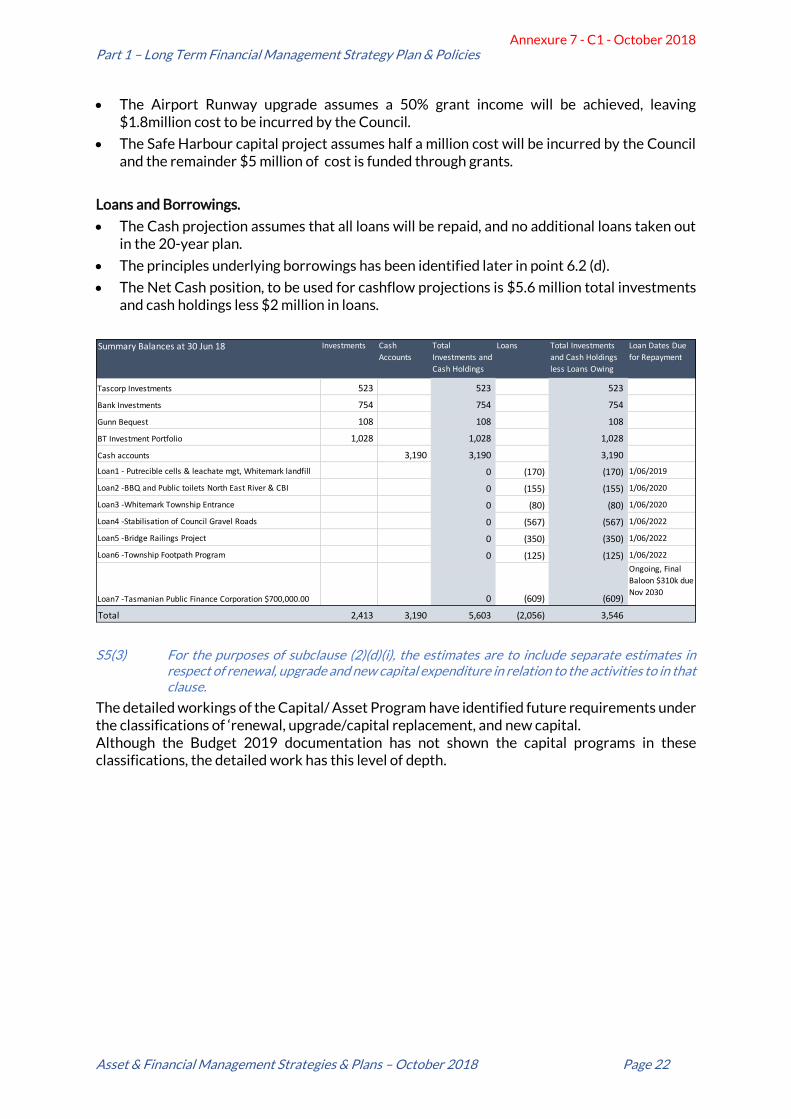

Summary Balances at 30 Jun 18 Investments Cash

Accounts

Total

Investments and

Cash Holdings

Loans Total Investments

and Cash Holdings

less Loans Owing

Loan Dates Due

for Repayment

Tascorp Investments 523 523 523

Bank Investments 754 754 754

Gunn Bequest 108 108 108

BT Investment Portfolio 1,028 1,028 1,028

Cash accounts 3,190 3,190 3,190