Asset Allocation Fund · Central Depository Company of Pakistan Limited, Chief Financial Officer...

33

Condensed Interim Financial Information for the Nine Months & Quarter Ended March 31, 2017 Asset Allocation Fund

Transcript of Asset Allocation Fund · Central Depository Company of Pakistan Limited, Chief Financial Officer...

Condensed Interim Financial Information for theNine Months & Quarter EndedMarch 31, 2017

Asset Allocation Fund

Fund Information

Mission Statement

Report of the Directors of the Management Company

Condensed Interim Statement of Assets and Liabilities

Condensed Interim Income Statement

Condensed Interim Distribution Statement

Condensed Interim Cash Flow Statement

Condensed Interim Statement of Movement in Unit Holders’ Fund

Notes to the Condensed Interim Financial Information

04

05

06

10

11

12

13

14

15

31

Deloitte Yousuf Adil, Chartered Accountants

JS Bank Limited

Faysal Asset Management Limited

Mr. Nauman Ansari, ChairmanMr. Osman Khan, DirectorSyed Ibad-Ur-Rehman Chishti, DirectorMr. Mohammad Zahid Ahmed, DirectorMr. Razi-Ur-Rahman Khan, Director/CEO

Mr. Naved Hanif

Mr. Osman Khan, ChairmanSyed Ibad-ur-Rehman Chisti, Member

Central Depository Company of Pakistan Limited,

Chief Financial Officerand Company Secretary of theManagement Company

Mr. Osman Khan, ChairmanSyed Ibad-Ur-Rehman Chishti, MemberMr. Razi-Ur-Rahman Khan, Member

HR Comittee

Quarter Ended March 31

2017 2016

32.88(1.88)

31.00-

31.0080.53

42.53

(5.87)

36.66

-

36.66

65.63

Nine Months Ended

March 312017 2016

34.07 (7.64)

26.43-

26.4380.53

(35.02)

(19.35)

(54.37)

-

(54.37)

65.63

Quarter Ended March 31

2017 2016

32.88(1.88)

31.00-

31.0080.53

42.53

(5.87)

36.66

-

36.66

65.63

Nine Months Ended

March 312017 2016

34.07 (7.64)

26.43-

26.4380.53

(35.02)

(19.35)

(54.37)

-

(54.37)

65.63

Current account deficit increased to $ 5.5 billion in Jul-Feb FY17, which was largely due to a sizable increase in imports of capital goods, along with delayed receipts of Coalition Support Fund (CSF). The rise in overall import payments was mainly driven by increased purchases and higher prices of fuel. However, there was significant increase in capital goods imports, which will lead the economy to a higher growth path.

Till March 31 2017, Pakistan’s total liquid foreign exchange reserves amounted to $21.550 billion for the period ended March 31, 2017. Forex reserves held by the State Bank of Pakistan (SBP) stood at $16.466 billion, while the net foreign exchange reserves held by commercial banks equaled at $5.084 billion. However, the external front constraints pose immense risk to country’s long term sustainable growth evident from the monthly import bill that crossed $5 billion for the first time in March, which took the nine-month trade deficit to $23.4 billion – also a new record. The gap between imports and exports stood at $23.38 billion in the July-March period of current fiscal year, which was 38.8% or $6.53 billion more than the comparative period of previous year. The main reason behind the ballooning deficit was constant double-digit growth in imports and contraction in exports. The nine-month trade gap was $2.9 billion more than the fiscal year’s annual deficit target of $20.5 billion, set by the Ministry of Finance. Exports fell 3.1% to only $15.1 billion during July-March 2016-17, which were $478 million less than the shipments made in the comparative period of last year. Imports, however, increased 18.7% to $38.5 billion in the same period. In absolute terms, the import bill was $6.6 billion higher than the previous year.

Remittances play a major role in stabilizing Pakistan’s external sector, as they make up almost half the import bill and cover the deficit in the trade of goods account. Nevertheless, in recent times, they have come under pressure due to global economic slowdown on the back of low crude oil prices. Overseas Pakistani workers sent remittances amounting to $1.69 billion in March, an increase of 19% from February when it stood at $1.42 billion. However, cumulatively, the figure fails to convey the whole picture as remittances during the first nine months (July-March) of the current fiscal year declined to $14.06 billion from $14.39 billion in the same period of previous fiscal year – a fall of 2.29%.

Analysts have warned that the country’s foreign reserves might deplete fast in the coming months unless its policymakers take serious steps in increasing exports on sustainable basis. However, the SBP is confident that the country faces no immediate threat from the slowdown in remittances and it is in a much better position to repay debts in the next four to five years.

All in all, Pakistan has entered into a new era of development whereby overseas investors have acknowledged it as land of unlimited opportunities offering investment friendly environment in diverse sectors as prided by board of Investment (BOI) achieving $ 1.3 billion foreign investment target set for first three quarters of current fiscal year. Consequently, despite constraints on country’s balance of payments position, improvements in investors’ confidence as reflected in an uptick in private sector credit, especially for fixed investment purposes; foreign interests in Pakistani companies; and increased production of consumer durables are indeed laudable. Similarly, a surge in import of machinery and raw materials also points to a robust industrial activity and buildup of future productive capacity. The fact that Pakistan is growing and enjoys the trust of the lender agencies will go on to act as a catalyst in redoubling its successes in the years to come.

The Board of Directors of the Faysal Asset Management Limited, the management company of the Faysal Asset Allocation Fund (FAAF), is pleased to present the un-audited condensed interim financial information of FAAF for the nine months and quarter ended March 31, 2017.

FINANCIAL HIGHLIGHTS

ECONOMIC REVIEW:

Pakistan's economy is out of the woods. It is now on a winning streak. Irrespective of inherent weaknesses, its private and public sectors have made great strides. Our country’s economy has strengthened following successful completion of its three-year program with International Monetary Fund (IMF) where the economy is expected to grow by 5% over the next two years because of China Pakistan Economic Corridor (CPEC) projects as infrastructure gaps may reduce through increased investment in transportation and power. This is quite a healthy trend, keeping in view the economic turmoil on an international stage since 2008. In terms of purchasing power, Pakistan's economy is ranked 24th in the world. Its 200 million population, with an enterprising youth, are the decisive factors for social mobility, growth and productivity. At the macro-economic level, Pakistan has made immense progress irrespective of bottlenecks. Inflow of capital in the last few years has helped in the development of infrastructure, especially in the sectors of health, education and civic amenities.

Average CPI-based inflation in three quarters of the current fiscal year (July-March) increased 4.01% compared to 2.64% the same period of previous year reflecting higher domestic demand and increase in global commodity prices. The large scale manufacturing (LSM) sector continues to grow at 3.5% with increase in production of cement, steel, pharmaceuticals, automobiles, paper & board and electronics.

FBR had collected PKR 2258 billion during July-March of the current fiscal year. the FBR is facing shortfall due to the pro growth incentives offered to various sectors of the economy particularly exports and agriculture; major item of revenue gap amounting to PKR 100 billion was due to not passing the full impact of the POL prices to the common man. Pakistan has also revised the budget deficit target to 4.1% of the GDP from budgetary estimates of 3.8% of the GDP due to lower tax collection and soaring expenditures.

Total Income / (loss)

Operating Expenses

Profit / (loss) Before Tax

Taxation

Profit/ (loss) After Tax

NAV per unit (Rs. Per unit)

Quarter Ended March 31

2017 2016

32.88(1.88)

31.00-

31.0080.53

42.53

(5.87)

36.66

-

36.66

65.63

Nine Months Ended

March 312017 2016

34.07 (7.64)

26.43-

26.4380.53

(35.02)

(19.35)

(54.37)

-

(54.37)

65.63

EQUITY REVIEW

Equity Market ended the nine months period of FY17 at 48,155.93 levels remarkably returning 27.45% in 9MFY17, while KMI 30 generated a staggering return of 24%.

The month of March’17 however, persisted on dull note as the index remained almost flat compared to previous month’s closing level as PSX 100 index slipped 0.78% MoM to take CYTD return to merely 0.73%.

In the nine months of FY17 (July-March 2016-17), foreign investors have sold stocks worth $483 mn. Foreign selling was majorly absorbed by mutual funds which cumulatively bought $419 mn worth shares in those eight months.

In this depressing scenario, mutual funds have come to the rescue that have scaled up PSX by 27% in 9MFYTD (till March 31, 2017), which is reasonably healthy as index is trajecting upward with a huge arbitrage standing in view of upcoming MSCI EM inclusion due next month.

During the 3rd quarter 2017 (January 2017- March 2017) foreigners & local banks were net sellers of US$163.3mn/US$66.9mn, while local mutual funds and insurance companies were net buyers of US$111.1mn/US$35.7mn. Average volume/value surged 154%/132% partially due to low base effect of last year, as volumes were thin due to low oil prices & a global equities sell-off.

During the period ended on March 31 2017, Automobile Assemblers, Chemicals, Engineering, Oil & Gas Marketing, Paper & Board, Refinery, and Transport sectors performed better than the market while, Fertilizer, Oil & Gas Exploration, Power Generation & Distribution sectors lagged behind. Healthy earnings announcements and improving future outlook amid strong volumetric growth and robust profit margins resulted in the out-performance of the Automobile & Assembler sector. Gas distribution companies led the upside of OMC sector amid improving earnings outlook. Investors accumulated position in Paper & Board sector on the back of better than expected corporate results by a select company and improving earnings outlook considering likely imposition of anti-dumping duty on imports. We attribute the abysmal performance of the Fertilizer sector to the weak global price outlook of urea amid supply glut. Owing to un-impressive earnings announcements and lower than expected payouts the Power Generation & Distribution sector failed to draw investors’ interest. Driven by renewed fall in the global oil prices, the Oil & Gas Exploration sector depicted subdued performance.

All in all, positivity on the market direction cannot be ruled out as future events (results, upcoming upgrade, Budget) may help the market shade off its underperformance. PSX stake sale & MSCI EM-upgrade’s bullish sentiments are likely to be checked by political & regulatory uncertainty along with a prelude to MSCI flows in the form of foreign funds rebalancing new FTSE scrips between themselves overseas.

Going forward, we still see substantial upside potential for equities driven by reasonable valuations as captured in forward P/E multiples of 10.4x; benign near-term inflation and interest rates; improving macro-economic outlook; buoyant business and consumer

sentiment; and expectation of healthy foreign inflows from funds tracking MSCI EM Index. That said, we may see bouts of volatility amid domestic political liquidity and global policy uncertainty. Investors are advised to stay the course unfazed by the confusing headlines, keeping long-term objective in mind.

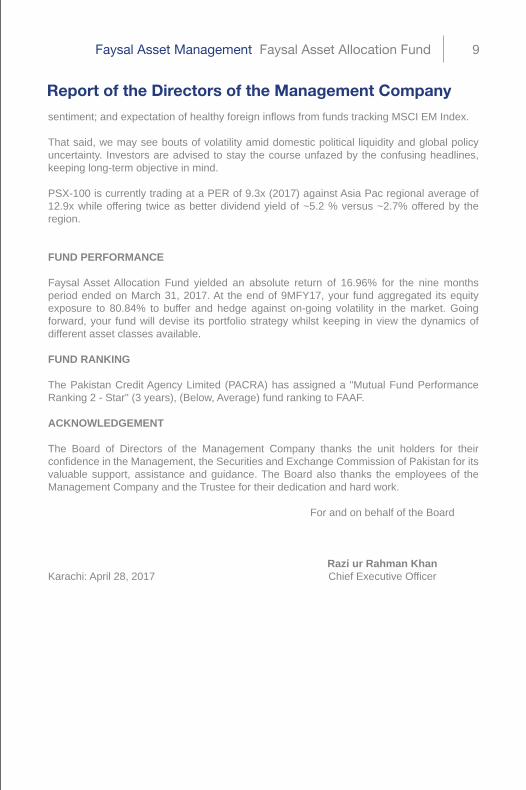

PSX-100 is currently trading at a PER of 9.3x (2017) against Asia Pac regional average of 12.9x while offering twice as better dividend yield of ~5.2 % versus ~2.7% offered by the region.

FUND PERFORMANCE

Faysal Asset Allocation Fund yielded an absolute return of 16.96% for the nine months period ended on March 31, 2017. At the end of 9MFY17, your fund aggregated its equity exposure to 80.84% to buffer and hedge against on-going volatility in the market. Going forward, your fund will devise its portfolio strategy whilst keeping in view the dynamics of different asset classes available.

FUND RANKING

The Pakistan Credit Agency Limited (PACRA) has assigned a "Mutual Fund Performance Ranking 2 - Star" (3 years), (Below, Average) fund ranking to FAAF.

ACKNOWLEDGEMENT

The Board of Directors of the Management Company thanks the unit holders for their confidence in the Management, the Securities and Exchange Commission of Pakistan for its valuable support, assistance and guidance. The Board also thanks the employees of the Management Company and the Trustee for their dedication and hard work.

For and on behalf of the Board

Razi ur Rahman KhanKarachi: April 28, 2017 Chief Executive Officer

Current account deficit increased to $ 5.5 billion in Jul-Feb FY17, which was largely due to a sizable increase in imports of capital goods, along with delayed receipts of Coalition Support Fund (CSF). The rise in overall import payments was mainly driven by increased purchases and higher prices of fuel. However, there was significant increase in capital goods imports, which will lead the economy to a higher growth path.

Till March 31 2017, Pakistan’s total liquid foreign exchange reserves amounted to $21.550 billion for the period ended March 31, 2017. Forex reserves held by the State Bank of Pakistan (SBP) stood at $16.466 billion, while the net foreign exchange reserves held by commercial banks equaled at $5.084 billion. However, the external front constraints pose immense risk to country’s long term sustainable growth evident from the monthly import bill that crossed $5 billion for the first time in March, which took the nine-month trade deficit to $23.4 billion – also a new record. The gap between imports and exports stood at $23.38 billion in the July-March period of current fiscal year, which was 38.8% or $6.53 billion more than the comparative period of previous year. The main reason behind the ballooning deficit was constant double-digit growth in imports and contraction in exports. The nine-month trade gap was $2.9 billion more than the fiscal year’s annual deficit target of $20.5 billion, set by the Ministry of Finance. Exports fell 3.1% to only $15.1 billion during July-March 2016-17, which were $478 million less than the shipments made in the comparative period of last year. Imports, however, increased 18.7% to $38.5 billion in the same period. In absolute terms, the import bill was $6.6 billion higher than the previous year.

Remittances play a major role in stabilizing Pakistan’s external sector, as they make up almost half the import bill and cover the deficit in the trade of goods account. Nevertheless, in recent times, they have come under pressure due to global economic slowdown on the back of low crude oil prices. Overseas Pakistani workers sent remittances amounting to $1.69 billion in March, an increase of 19% from February when it stood at $1.42 billion. However, cumulatively, the figure fails to convey the whole picture as remittances during the first nine months (July-March) of the current fiscal year declined to $14.06 billion from $14.39 billion in the same period of previous fiscal year – a fall of 2.29%.

Analysts have warned that the country’s foreign reserves might deplete fast in the coming months unless its policymakers take serious steps in increasing exports on sustainable basis. However, the SBP is confident that the country faces no immediate threat from the slowdown in remittances and it is in a much better position to repay debts in the next four to five years.

All in all, Pakistan has entered into a new era of development whereby overseas investors have acknowledged it as land of unlimited opportunities offering investment friendly environment in diverse sectors as prided by board of Investment (BOI) achieving $ 1.3 billion foreign investment target set for first three quarters of current fiscal year. Consequently, despite constraints on country’s balance of payments position, improvements in investors’ confidence as reflected in an uptick in private sector credit, especially for fixed investment purposes; foreign interests in Pakistani companies; and increased production of consumer durables are indeed laudable. Similarly, a surge in import of machinery and raw materials also points to a robust industrial activity and buildup of future productive capacity. The fact that Pakistan is growing and enjoys the trust of the lender agencies will go on to act as a catalyst in redoubling its successes in the years to come.

The Board of Directors of the Faysal Asset Management Limited, the management company of the Faysal Asset Allocation Fund (FAAF), is pleased to present the un-audited condensed interim financial information of FAAF for the nine months and quarter ended March 31, 2017.

FINANCIAL HIGHLIGHTS

ECONOMIC REVIEW:

Pakistan's economy is out of the woods. It is now on a winning streak. Irrespective of inherent weaknesses, its private and public sectors have made great strides. Our country’s economy has strengthened following successful completion of its three-year program with International Monetary Fund (IMF) where the economy is expected to grow by 5% over the next two years because of China Pakistan Economic Corridor (CPEC) projects as infrastructure gaps may reduce through increased investment in transportation and power. This is quite a healthy trend, keeping in view the economic turmoil on an international stage since 2008. In terms of purchasing power, Pakistan's economy is ranked 24th in the world. Its 200 million population, with an enterprising youth, are the decisive factors for social mobility, growth and productivity. At the macro-economic level, Pakistan has made immense progress irrespective of bottlenecks. Inflow of capital in the last few years has helped in the development of infrastructure, especially in the sectors of health, education and civic amenities.

Average CPI-based inflation in three quarters of the current fiscal year (July-March) increased 4.01% compared to 2.64% the same period of previous year reflecting higher domestic demand and increase in global commodity prices. The large scale manufacturing (LSM) sector continues to grow at 3.5% with increase in production of cement, steel, pharmaceuticals, automobiles, paper & board and electronics.

FBR had collected PKR 2258 billion during July-March of the current fiscal year. the FBR is facing shortfall due to the pro growth incentives offered to various sectors of the economy particularly exports and agriculture; major item of revenue gap amounting to PKR 100 billion was due to not passing the full impact of the POL prices to the common man. Pakistan has also revised the budget deficit target to 4.1% of the GDP from budgetary estimates of 3.8% of the GDP due to lower tax collection and soaring expenditures.

EQUITY REVIEW

Equity Market ended the nine months period of FY17 at 48,155.93 levels remarkably returning 27.45% in 9MFY17, while KMI 30 generated a staggering return of 24%.

The month of March’17 however, persisted on dull note as the index remained almost flat compared to previous month’s closing level as PSX 100 index slipped 0.78% MoM to take CYTD return to merely 0.73%.

In the nine months of FY17 (July-March 2016-17), foreign investors have sold stocks worth $483 mn. Foreign selling was majorly absorbed by mutual funds which cumulatively bought $419 mn worth shares in those eight months.

In this depressing scenario, mutual funds have come to the rescue that have scaled up PSX by 27% in 9MFYTD (till March 31, 2017), which is reasonably healthy as index is trajecting upward with a huge arbitrage standing in view of upcoming MSCI EM inclusion due next month.

During the 3rd quarter 2017 (January 2017- March 2017) foreigners & local banks were net sellers of US$163.3mn/US$66.9mn, while local mutual funds and insurance companies were net buyers of US$111.1mn/US$35.7mn. Average volume/value surged 154%/132% partially due to low base effect of last year, as volumes were thin due to low oil prices & a global equities sell-off.

During the period ended on March 31 2017, Automobile Assemblers, Chemicals, Engineering, Oil & Gas Marketing, Paper & Board, Refinery, and Transport sectors performed better than the market while, Fertilizer, Oil & Gas Exploration, Power Generation & Distribution sectors lagged behind. Healthy earnings announcements and improving future outlook amid strong volumetric growth and robust profit margins resulted in the out-performance of the Automobile & Assembler sector. Gas distribution companies led the upside of OMC sector amid improving earnings outlook. Investors accumulated position in Paper & Board sector on the back of better than expected corporate results by a select company and improving earnings outlook considering likely imposition of anti-dumping duty on imports. We attribute the abysmal performance of the Fertilizer sector to the weak global price outlook of urea amid supply glut. Owing to un-impressive earnings announcements and lower than expected payouts the Power Generation & Distribution sector failed to draw investors’ interest. Driven by renewed fall in the global oil prices, the Oil & Gas Exploration sector depicted subdued performance.

All in all, positivity on the market direction cannot be ruled out as future events (results, upcoming upgrade, Budget) may help the market shade off its underperformance. PSX stake sale & MSCI EM-upgrade’s bullish sentiments are likely to be checked by political & regulatory uncertainty along with a prelude to MSCI flows in the form of foreign funds rebalancing new FTSE scrips between themselves overseas.

Going forward, we still see substantial upside potential for equities driven by reasonable valuations as captured in forward P/E multiples of 10.4x; benign near-term inflation and interest rates; improving macro-economic outlook; buoyant business and consumer

sentiment; and expectation of healthy foreign inflows from funds tracking MSCI EM Index. That said, we may see bouts of volatility amid domestic political liquidity and global policy uncertainty. Investors are advised to stay the course unfazed by the confusing headlines, keeping long-term objective in mind.

PSX-100 is currently trading at a PER of 9.3x (2017) against Asia Pac regional average of 12.9x while offering twice as better dividend yield of ~5.2 % versus ~2.7% offered by the region.

FUND PERFORMANCE

Faysal Asset Allocation Fund yielded an absolute return of 16.96% for the nine months period ended on March 31, 2017. At the end of 9MFY17, your fund aggregated its equity exposure to 80.84% to buffer and hedge against on-going volatility in the market. Going forward, your fund will devise its portfolio strategy whilst keeping in view the dynamics of different asset classes available.

FUND RANKING

The Pakistan Credit Agency Limited (PACRA) has assigned a "Mutual Fund Performance Ranking 2 - Star" (3 years), (Below, Average) fund ranking to FAAF.

ACKNOWLEDGEMENT

The Board of Directors of the Management Company thanks the unit holders for their confidence in the Management, the Securities and Exchange Commission of Pakistan for its valuable support, assistance and guidance. The Board also thanks the employees of the Management Company and the Trustee for their dedication and hard work.

For and on behalf of the Board

Razi ur Rahman KhanKarachi: April 28, 2017 Chief Executive Officer

Current account deficit increased to $ 5.5 billion in Jul-Feb FY17, which was largely due to a sizable increase in imports of capital goods, along with delayed receipts of Coalition Support Fund (CSF). The rise in overall import payments was mainly driven by increased purchases and higher prices of fuel. However, there was significant increase in capital goods imports, which will lead the economy to a higher growth path.

Till March 31 2017, Pakistan’s total liquid foreign exchange reserves amounted to $21.550 billion for the period ended March 31, 2017. Forex reserves held by the State Bank of Pakistan (SBP) stood at $16.466 billion, while the net foreign exchange reserves held by commercial banks equaled at $5.084 billion. However, the external front constraints pose immense risk to country’s long term sustainable growth evident from the monthly import bill that crossed $5 billion for the first time in March, which took the nine-month trade deficit to $23.4 billion – also a new record. The gap between imports and exports stood at $23.38 billion in the July-March period of current fiscal year, which was 38.8% or $6.53 billion more than the comparative period of previous year. The main reason behind the ballooning deficit was constant double-digit growth in imports and contraction in exports. The nine-month trade gap was $2.9 billion more than the fiscal year’s annual deficit target of $20.5 billion, set by the Ministry of Finance. Exports fell 3.1% to only $15.1 billion during July-March 2016-17, which were $478 million less than the shipments made in the comparative period of last year. Imports, however, increased 18.7% to $38.5 billion in the same period. In absolute terms, the import bill was $6.6 billion higher than the previous year.

Remittances play a major role in stabilizing Pakistan’s external sector, as they make up almost half the import bill and cover the deficit in the trade of goods account. Nevertheless, in recent times, they have come under pressure due to global economic slowdown on the back of low crude oil prices. Overseas Pakistani workers sent remittances amounting to $1.69 billion in March, an increase of 19% from February when it stood at $1.42 billion. However, cumulatively, the figure fails to convey the whole picture as remittances during the first nine months (July-March) of the current fiscal year declined to $14.06 billion from $14.39 billion in the same period of previous fiscal year – a fall of 2.29%.

Analysts have warned that the country’s foreign reserves might deplete fast in the coming months unless its policymakers take serious steps in increasing exports on sustainable basis. However, the SBP is confident that the country faces no immediate threat from the slowdown in remittances and it is in a much better position to repay debts in the next four to five years.

All in all, Pakistan has entered into a new era of development whereby overseas investors have acknowledged it as land of unlimited opportunities offering investment friendly environment in diverse sectors as prided by board of Investment (BOI) achieving $ 1.3 billion foreign investment target set for first three quarters of current fiscal year. Consequently, despite constraints on country’s balance of payments position, improvements in investors’ confidence as reflected in an uptick in private sector credit, especially for fixed investment purposes; foreign interests in Pakistani companies; and increased production of consumer durables are indeed laudable. Similarly, a surge in import of machinery and raw materials also points to a robust industrial activity and buildup of future productive capacity. The fact that Pakistan is growing and enjoys the trust of the lender agencies will go on to act as a catalyst in redoubling its successes in the years to come.

The Board of Directors of the Faysal Asset Management Limited, the management company of the Faysal Asset Allocation Fund (FAAF), is pleased to present the un-audited condensed interim financial information of FAAF for the nine months and quarter ended March 31, 2017.

FINANCIAL HIGHLIGHTS

ECONOMIC REVIEW:

Pakistan's economy is out of the woods. It is now on a winning streak. Irrespective of inherent weaknesses, its private and public sectors have made great strides. Our country’s economy has strengthened following successful completion of its three-year program with International Monetary Fund (IMF) where the economy is expected to grow by 5% over the next two years because of China Pakistan Economic Corridor (CPEC) projects as infrastructure gaps may reduce through increased investment in transportation and power. This is quite a healthy trend, keeping in view the economic turmoil on an international stage since 2008. In terms of purchasing power, Pakistan's economy is ranked 24th in the world. Its 200 million population, with an enterprising youth, are the decisive factors for social mobility, growth and productivity. At the macro-economic level, Pakistan has made immense progress irrespective of bottlenecks. Inflow of capital in the last few years has helped in the development of infrastructure, especially in the sectors of health, education and civic amenities.

Average CPI-based inflation in three quarters of the current fiscal year (July-March) increased 4.01% compared to 2.64% the same period of previous year reflecting higher domestic demand and increase in global commodity prices. The large scale manufacturing (LSM) sector continues to grow at 3.5% with increase in production of cement, steel, pharmaceuticals, automobiles, paper & board and electronics.

FBR had collected PKR 2258 billion during July-March of the current fiscal year. the FBR is facing shortfall due to the pro growth incentives offered to various sectors of the economy particularly exports and agriculture; major item of revenue gap amounting to PKR 100 billion was due to not passing the full impact of the POL prices to the common man. Pakistan has also revised the budget deficit target to 4.1% of the GDP from budgetary estimates of 3.8% of the GDP due to lower tax collection and soaring expenditures.

8

EQUITY REVIEW

Equity Market ended the nine months period of FY17 at 48,155.93 levels remarkably returning 27.45% in 9MFY17, while KMI 30 generated a staggering return of 24%.

The month of March’17 however, persisted on dull note as the index remained almost flat compared to previous month’s closing level as PSX 100 index slipped 0.78% MoM to take CYTD return to merely 0.73%.

In the nine months of FY17 (July-March 2016-17), foreign investors have sold stocks worth $483 mn. Foreign selling was majorly absorbed by mutual funds which cumulatively bought $419 mn worth shares in those eight months.

In this depressing scenario, mutual funds have come to the rescue that have scaled up PSX by 27% in 9MFYTD (till March 31, 2017), which is reasonably healthy as index is trajecting upward with a huge arbitrage standing in view of upcoming MSCI EM inclusion due next month.

During the 3rd quarter 2017 (January 2017- March 2017) foreigners & local banks were net sellers of US$163.3mn/US$66.9mn, while local mutual funds and insurance companies were net buyers of US$111.1mn/US$35.7mn. Average volume/value surged 154%/132% partially due to low base effect of last year, as volumes were thin due to low oil prices & a global equities sell-off.

During the period ended on March 31 2017, Automobile Assemblers, Chemicals, Engineering, Oil & Gas Marketing, Paper & Board, Refinery, and Transport sectors performed better than the market while, Fertilizer, Oil & Gas Exploration, Power Generation & Distribution sectors lagged behind. Healthy earnings announcements and improving future outlook amid strong volumetric growth and robust profit margins resulted in the out-performance of the Automobile & Assembler sector. Gas distribution companies led the upside of OMC sector amid improving earnings outlook. Investors accumulated position in Paper & Board sector on the back of better than expected corporate results by a select company and improving earnings outlook considering likely imposition of anti-dumping duty on imports. We attribute the abysmal performance of the Fertilizer sector to the weak global price outlook of urea amid supply glut. Owing to un-impressive earnings announcements and lower than expected payouts the Power Generation & Distribution sector failed to draw investors’ interest. Driven by renewed fall in the global oil prices, the Oil & Gas Exploration sector depicted subdued performance.

All in all, positivity on the market direction cannot be ruled out as future events (results, upcoming upgrade, Budget) may help the market shade off its underperformance. PSX stake sale & MSCI EM-upgrade’s bullish sentiments are likely to be checked by political & regulatory uncertainty along with a prelude to MSCI flows in the form of foreign funds rebalancing new FTSE scrips between themselves overseas.

Going forward, we still see substantial upside potential for equities driven by reasonable valuations as captured in forward P/E multiples of 10.4x; benign near-term inflation and interest rates; improving macro-economic outlook; buoyant business and consumer

sentiment; and expectation of healthy foreign inflows from funds tracking MSCI EM Index. That said, we may see bouts of volatility amid domestic political liquidity and global policy uncertainty. Investors are advised to stay the course unfazed by the confusing headlines, keeping long-term objective in mind.

PSX-100 is currently trading at a PER of 9.3x (2017) against Asia Pac regional average of 12.9x while offering twice as better dividend yield of ~5.2 % versus ~2.7% offered by the region.

FUND PERFORMANCE

Faysal Asset Allocation Fund yielded an absolute return of 16.96% for the nine months period ended on March 31, 2017. At the end of 9MFY17, your fund aggregated its equity exposure to 80.84% to buffer and hedge against on-going volatility in the market. Going forward, your fund will devise its portfolio strategy whilst keeping in view the dynamics of different asset classes available.

FUND RANKING

The Pakistan Credit Agency Limited (PACRA) has assigned a "Mutual Fund Performance Ranking 2 - Star" (3 years), (Below, Average) fund ranking to FAAF.

ACKNOWLEDGEMENT

The Board of Directors of the Management Company thanks the unit holders for their confidence in the Management, the Securities and Exchange Commission of Pakistan for its valuable support, assistance and guidance. The Board also thanks the employees of the Management Company and the Trustee for their dedication and hard work.

For and on behalf of the Board

Razi ur Rahman KhanKarachi: April 28, 2017 Chief Executive Officer

Current account deficit increased to $ 5.5 billion in Jul-Feb FY17, which was largely due to a sizable increase in imports of capital goods, along with delayed receipts of Coalition Support Fund (CSF). The rise in overall import payments was mainly driven by increased purchases and higher prices of fuel. However, there was significant increase in capital goods imports, which will lead the economy to a higher growth path.

Till March 31 2017, Pakistan’s total liquid foreign exchange reserves amounted to $21.550 billion for the period ended March 31, 2017. Forex reserves held by the State Bank of Pakistan (SBP) stood at $16.466 billion, while the net foreign exchange reserves held by commercial banks equaled at $5.084 billion. However, the external front constraints pose immense risk to country’s long term sustainable growth evident from the monthly import bill that crossed $5 billion for the first time in March, which took the nine-month trade deficit to $23.4 billion – also a new record. The gap between imports and exports stood at $23.38 billion in the July-March period of current fiscal year, which was 38.8% or $6.53 billion more than the comparative period of previous year. The main reason behind the ballooning deficit was constant double-digit growth in imports and contraction in exports. The nine-month trade gap was $2.9 billion more than the fiscal year’s annual deficit target of $20.5 billion, set by the Ministry of Finance. Exports fell 3.1% to only $15.1 billion during July-March 2016-17, which were $478 million less than the shipments made in the comparative period of last year. Imports, however, increased 18.7% to $38.5 billion in the same period. In absolute terms, the import bill was $6.6 billion higher than the previous year.

Remittances play a major role in stabilizing Pakistan’s external sector, as they make up almost half the import bill and cover the deficit in the trade of goods account. Nevertheless, in recent times, they have come under pressure due to global economic slowdown on the back of low crude oil prices. Overseas Pakistani workers sent remittances amounting to $1.69 billion in March, an increase of 19% from February when it stood at $1.42 billion. However, cumulatively, the figure fails to convey the whole picture as remittances during the first nine months (July-March) of the current fiscal year declined to $14.06 billion from $14.39 billion in the same period of previous fiscal year – a fall of 2.29%.

Analysts have warned that the country’s foreign reserves might deplete fast in the coming months unless its policymakers take serious steps in increasing exports on sustainable basis. However, the SBP is confident that the country faces no immediate threat from the slowdown in remittances and it is in a much better position to repay debts in the next four to five years.

All in all, Pakistan has entered into a new era of development whereby overseas investors have acknowledged it as land of unlimited opportunities offering investment friendly environment in diverse sectors as prided by board of Investment (BOI) achieving $ 1.3 billion foreign investment target set for first three quarters of current fiscal year. Consequently, despite constraints on country’s balance of payments position, improvements in investors’ confidence as reflected in an uptick in private sector credit, especially for fixed investment purposes; foreign interests in Pakistani companies; and increased production of consumer durables are indeed laudable. Similarly, a surge in import of machinery and raw materials also points to a robust industrial activity and buildup of future productive capacity. The fact that Pakistan is growing and enjoys the trust of the lender agencies will go on to act as a catalyst in redoubling its successes in the years to come.

The Board of Directors of the Faysal Asset Management Limited, the management company of the Faysal Asset Allocation Fund (FAAF), is pleased to present the un-audited condensed interim financial information of FAAF for the nine months and quarter ended March 31, 2017.

FINANCIAL HIGHLIGHTS

ECONOMIC REVIEW:

Pakistan's economy is out of the woods. It is now on a winning streak. Irrespective of inherent weaknesses, its private and public sectors have made great strides. Our country’s economy has strengthened following successful completion of its three-year program with International Monetary Fund (IMF) where the economy is expected to grow by 5% over the next two years because of China Pakistan Economic Corridor (CPEC) projects as infrastructure gaps may reduce through increased investment in transportation and power. This is quite a healthy trend, keeping in view the economic turmoil on an international stage since 2008. In terms of purchasing power, Pakistan's economy is ranked 24th in the world. Its 200 million population, with an enterprising youth, are the decisive factors for social mobility, growth and productivity. At the macro-economic level, Pakistan has made immense progress irrespective of bottlenecks. Inflow of capital in the last few years has helped in the development of infrastructure, especially in the sectors of health, education and civic amenities.

Average CPI-based inflation in three quarters of the current fiscal year (July-March) increased 4.01% compared to 2.64% the same period of previous year reflecting higher domestic demand and increase in global commodity prices. The large scale manufacturing (LSM) sector continues to grow at 3.5% with increase in production of cement, steel, pharmaceuticals, automobiles, paper & board and electronics.

FBR had collected PKR 2258 billion during July-March of the current fiscal year. the FBR is facing shortfall due to the pro growth incentives offered to various sectors of the economy particularly exports and agriculture; major item of revenue gap amounting to PKR 100 billion was due to not passing the full impact of the POL prices to the common man. Pakistan has also revised the budget deficit target to 4.1% of the GDP from budgetary estimates of 3.8% of the GDP due to lower tax collection and soaring expenditures.

EQUITY REVIEW

Equity Market ended the nine months period of FY17 at 48,155.93 levels remarkably returning 27.45% in 9MFY17, while KMI 30 generated a staggering return of 24%.

The month of March’17 however, persisted on dull note as the index remained almost flat compared to previous month’s closing level as PSX 100 index slipped 0.78% MoM to take CYTD return to merely 0.73%.

In the nine months of FY17 (July-March 2016-17), foreign investors have sold stocks worth $483 mn. Foreign selling was majorly absorbed by mutual funds which cumulatively bought $419 mn worth shares in those eight months.

In this depressing scenario, mutual funds have come to the rescue that have scaled up PSX by 27% in 9MFYTD (till March 31, 2017), which is reasonably healthy as index is trajecting upward with a huge arbitrage standing in view of upcoming MSCI EM inclusion due next month.

During the 3rd quarter 2017 (January 2017- March 2017) foreigners & local banks were net sellers of US$163.3mn/US$66.9mn, while local mutual funds and insurance companies were net buyers of US$111.1mn/US$35.7mn. Average volume/value surged 154%/132% partially due to low base effect of last year, as volumes were thin due to low oil prices & a global equities sell-off.

During the period ended on March 31 2017, Automobile Assemblers, Chemicals, Engineering, Oil & Gas Marketing, Paper & Board, Refinery, and Transport sectors performed better than the market while, Fertilizer, Oil & Gas Exploration, Power Generation & Distribution sectors lagged behind. Healthy earnings announcements and improving future outlook amid strong volumetric growth and robust profit margins resulted in the out-performance of the Automobile & Assembler sector. Gas distribution companies led the upside of OMC sector amid improving earnings outlook. Investors accumulated position in Paper & Board sector on the back of better than expected corporate results by a select company and improving earnings outlook considering likely imposition of anti-dumping duty on imports. We attribute the abysmal performance of the Fertilizer sector to the weak global price outlook of urea amid supply glut. Owing to un-impressive earnings announcements and lower than expected payouts the Power Generation & Distribution sector failed to draw investors’ interest. Driven by renewed fall in the global oil prices, the Oil & Gas Exploration sector depicted subdued performance.

All in all, positivity on the market direction cannot be ruled out as future events (results, upcoming upgrade, Budget) may help the market shade off its underperformance. PSX stake sale & MSCI EM-upgrade’s bullish sentiments are likely to be checked by political & regulatory uncertainty along with a prelude to MSCI flows in the form of foreign funds rebalancing new FTSE scrips between themselves overseas.

Going forward, we still see substantial upside potential for equities driven by reasonable valuations as captured in forward P/E multiples of 10.4x; benign near-term inflation and interest rates; improving macro-economic outlook; buoyant business and consumer

9

sentiment; and expectation of healthy foreign inflows from funds tracking MSCI EM Index. That said, we may see bouts of volatility amid domestic political liquidity and global policy uncertainty. Investors are advised to stay the course unfazed by the confusing headlines, keeping long-term objective in mind.

PSX-100 is currently trading at a PER of 9.3x (2017) against Asia Pac regional average of 12.9x while offering twice as better dividend yield of ~5.2 % versus ~2.7% offered by the region.

FUND PERFORMANCE

Faysal Asset Allocation Fund yielded an absolute return of 16.96% for the nine months period ended on March 31, 2017. At the end of 9MFY17, your fund aggregated its equity exposure to 80.84% to buffer and hedge against on-going volatility in the market. Going forward, your fund will devise its portfolio strategy whilst keeping in view the dynamics of different asset classes available.

FUND RANKING

The Pakistan Credit Agency Limited (PACRA) has assigned a "Mutual Fund Performance Ranking 2 - Star" (3 years), (Below, Average) fund ranking to FAAF.

ACKNOWLEDGEMENT

The Board of Directors of the Management Company thanks the unit holders for their confidence in the Management, the Securities and Exchange Commission of Pakistan for its valuable support, assistance and guidance. The Board also thanks the employees of the Management Company and the Trustee for their dedication and hard work.

For and on behalf of the Board

Razi ur Rahman KhanKarachi: April 28, 2017 Chief Executive Officer

10

Condensed Interim Statement of Assets and LiabilitiesAs at March 31, 2017

(Un- Audited) (Audited)March 31, June 30,

2017 2016Note

Assets

Bank balances 4 27,747,461 347,436,656 Investments 5 155,098,908 488,081,582 Prepayments, deposits and other receivables 4,462,318 16,312,114 Receivable against sale of investments 4,605,226 - Total assets 191,913,913 851,830,352

Liabilities

Payable to the Management Company 581,270 912,126 Remuneration payable to the Trustee 67,181 148,215 Payable against redemption of units - 59,840,000 Accrued and other liabilities 6 6,856,116 11,910,259 Payable against purchase of investments 2,457,025 40,220,505 Total liabilities 9,961,592 113,031,105

Net assets 181,952,321 738,799,247

Unit holders’ fund (as per the statement attached) 181,952,321 738,799,247

Contingencies and Commitments 7

Number of units in issue 2,259,527 10,731,241

Net asset value per unit 80.53 68.85

The annexed notes from 1 to 15 form an integral part of this condensed interim financial information.

For Faysal Asset Management Limited(Management Company)

FAYSAL ASSET ALLOCATION FUNDCONDENSED INTERIM STATEMENT OF ASSETS AND LIABILITIES

AS AT MARCH 31, 2017

-------------- (Rupees) --------------

--------- (Number of units) ---------

-------------- (Rupees) --------------

____________________ ___________________ ___________________Chief Executive Officer Director Director

11

Condensed Interim Income StatementFOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

March 31, March 31, March 31, March 31,2017 2016 2017 2016

NoteIncome

Income from Margin Trading System (MTS) - 1,502,390 - - Dividend income on investment classified

as at fair value through profit or loss' - held-for-trading 3,645,050 4,884,000 2,129,050 1,432,891 Income from participation in purchase of shares - 2,000,000 - 2,000,000 Return on bank balances 3,345,206 5,641,516 1,631,597 4,028,463 Net gain / (loss) on investments classified as 'at fair value

- Net capital gain / (loss) on sale of investments 61,219,428 (12,854,821) 27,089,077 4,891,399 - Net unrealised (loss) / gain on revaluation of investments (53,131) (37,393,153) 9,543,501 27,108,003

61,166,297 (50,247,974) 36,632,578 31,999,402

Total income / (loss) 68,156,553 (36,220,068) 40,393,225 39,460,756

Expenses

Remuneration of the Management Company 4,612,691 9,597,544 1,976,238 3,162,456 Reimbursement of expenses to Management Company 215,672 - 83,849 - Provision for individual taxes & duties 6.2 - 1,750,590 - 578,903 Sales tax on management fee 599,650 1,343,657 256,911 442,743 Remuneration of the Trustee 621,800 959,816 353,876 316,265 Sales tax on Trustee fee 80,833 134,374 46,004 43,686 Brokerage charges 2,187,289 2,947,864 789,033 429,648 Bank charges 56,605 63,938 39,362 20,350 Auditors' remuneration 444,016 480,455 320,950 218,794 SECP non refundable annual fee 219,459 454,465 94,226 148,974 Fees and subscriptions 127,135 117,214 84,034 41,825 Settlement charges, federal excise duty and capital value tax 1,083,845 1,353,960 496,641 410,855 Printing and other expenses 164,907 147,532 115,483 29,417 Reversal against provision of Worker's Welfare Fund 6.1 (3,314,208) - (3,314,208) 29,417 Provision for Sindh Workers' Welfare Fund 6.1 539,399 - 539,399 -

Total expenses 7,639,093 19,351,409 1,881,798 5,873,333

Net income / (loss) from operating activities 60,517,460 (55,571,477) 38,511,427 33,587,423

Element of (loss) / income and capital gains / (losses) includedin prices of units sold less those in units redeemed - net (34,086,880) 1,199,332 (7,511,747) 3,064,747

Net income / (loss) for the period before taxation 26,430,580 (54,372,145) 30,999,680 36,652,170

Taxation 8 - - - -

Net income / (loss) for the period after taxation 26,430,580 (54,372,145) 30,999,680 36,652,170

Other comprehensive income for the period - - - -

Total comprehensive income / (loss) for the period 26,430,580 (54,372,145) 30,999,680 36,652,170

Earnings per unit 9

The annexed notes from 1 to 15 form an integral part of this condensed interim financial information.

through profit or loss'-held for trading:

For Faysal Asset Management Limited(Management Company)

FAYSAL ASSET ALLOCATION FUNDCONDENSED INTERIM INCOME STATEMENT

FOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

Nine months ended Quarter ended

------------ (Rupees) ------------ ------------ (Rupees) ------------

____________________ ___________________ ___________________Chief Executive Officer Director Director

12

Condensed Interim Distribution StatementFOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

March 31, March 31,2017 2016

Accumulated loss brought forward [includes unrealised loss on investments of Rs. 50,300,274(2015: unrealised gain of Rs. 7,411,743)] (178,167,320) (159,427,430)

Net income / (loss) for the period after taxation 26,430,580 (54,372,145)

Accumulated loss carried forward (151,736,740) (213,799,575) [includes unrealised loss on investments of Rs. 743,448(2016 : unrealised loss of Rs 31,057,027)]

The annexed notes from 1 to 15 form an integral part of this condensed interim financial information.

(Management Company)

FAYSAL ASSET ALLOCATION FUNDCONDENSED INTERIM DISTRIBUTION STATEMENT

FOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

Nine months ended

-------------- (Rupees) --------------

For Faysal Asset Management Limited

____________________ ___________________ ___________________Chief Executive Officer Director Director

13

Condensed Interim Cash Flow StatementFOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

March 31, March 31,2017 2016

NoteCASH FLOWS FROM OPERATING ACTIVITIESNet income / (loss) for the period before taxation 26,430,580 (54,372,145)

Adjustments for non-cash and other items:Income on Margin Trading System (MTS) - (1,502,390) Dividend income on investment classified as

'at fair value through profit or loss' - held-for-trading (3,645,050) (4,884,000) Return on bank balances (3,345,206) (5,641,516) Net (gain) / loss on investments classified as

'at fair value through profit or loss'-held for trading:- Net capital (gain) / loss on sale of investments (61,219,428) 12,854,821 - Net unrealised loss on revaluation of investments 53,131 37,393,153

Element of loss / (income) and capital losses / (gains) included in prices of units sold less those in units redeemed - net 34,086,880 (1,199,332)

(7,639,093) (17,351,409) Increase / (decrease) in assetsPrepayments, deposits and other receivables 10,515,627 (502,109)

(Decrease) /increase in liabilitiesPayable to the Management Company (330,856) 511,012 Remuneration payable to the Trustee (81,034) 62,191 Contingencies and Commitments (59,840,000) - Accrued and other liabilities (5,054,143) (527,896)

(65,306,033) 45,307 (62,429,499) (17,808,211)

Proceeds from sale of investments 1,624,270,538 1,448,616,576 Proceeds from redemption of preference shares - 3,771,510 Payments made against purchase of investments (1,272,490,273) (1,768,128,781) Receipts against Margin Trading System (MTS) - 76,585,764 Income received on Margin Trading System (MTS) - 1,569,042 Markup received on preference shares - 97,441 Dividend received 4,014,000 4,097,735 Return received on bank balances 4,310,425 5,664,063 Net cash generated from / (used in) operating activities 297,675,191 (245,534,861)

CASH FLOWS FROM FINANCING ACTIVITIESAmounts received against issue of units 677,022,289 771,488,335 Payments made against redemption of units (1,294,386,675) (584,664,647) Net cash (used in) / generated from financing activities (617,364,386) 186,823,688

Net decrease in cash and cash equivalents during the period (319,689,195) (58,711,173) Cash and cash equivalents at the beginning of the period 347,436,656 207,426,860

Cash and cash equivalents at the end of the period 4 27,747,461 148,715,687

The annexed notes from 1 to 15 form an integral part of this condensed interim financial information.

For Faysal Asset Management Limited(Management Company)

FAYSAL ASSET ALLOCATION FUNDCONDENSED INTERIM CASH FLOW STATEMENT

FOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

Nine months ended

-------------- (Rupees) --------------

____________________ ___________________ ___________________Chief Executive Officer Director Director

14

Condensed Interim Statement of Movement in Unit Holders’ Fund FOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

March 31, March 31,2017 2016

Net asset value per unit at the beginning of the period 68.85 70.59

Net asset value per unit at the end of the period 80.53 65.63

Net assets at the beginning of the period 738,799,247 587,687,268

Amounts received on issue of units * 677,022,289 771,488,335

Amounts paid on redemption of units ** (1,294,386,675) (584,664,647)

(617,364,386) 186,823,688 Element of loss / (income) and capital losses / (gains) included

in prices of units sold less those in units redeemed - net 34,086,880 (1,199,332)

Net capital gain / (loss) on sale of investments 61,219,428 (12,854,821)Net unrealised lesson revaluation (53,131) (37,393,153) Other net loss for the period (34,735,717) (4,124,171) Total comprehensive income / (loss) for the period 26,430,580 (54,372,145)

Net assets at the end of the period 181,952,321 718,939,479

* Number of units issued (including Nil bonus units issued during the periods ended March 31, 2017 and March 31, 2016) 9,228,000 11,258,033

** Number of units redeemed 17,699,714 8,628,259

The annexed notes from 1 to 15 form an integral part of this condensed interim financial information.

For Faysal Asset Management Limited(Management Company)

FAYSAL ASSET ALLOCATION FUNDCONDENSED INTERIM STATEMENT OF MOVEMENT IN UNIT HOLDERS' FUNDFOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

Nine months ended

--------- (Rupees) ----------

-------- (Number of units) --------

____________________ ___________________ ___________________Chief Executive Officer Director Director

15

Notes to the Condensed Interim Financial Information FOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

1. LEGAL STATUS AND NATURE OF BUSINESS

The policy of the Fund is to invest in a mix of equity securities, fixed income and money market instruments.

2. BASIS OF PREPARATION

The disclosures made in this interim financial information have, however, been limited based on the requirements of the International Accounting Standard 34 - Interim Financial Reporting.

The condensed interim financial information is presented in Pakistani Rupees which is the Fund's functional andpresentation currency.

The Pakistan Credit Rating Agency Limited (PACRA) has assigned a "long term rating 2-Stars" to Faysal AssetAllocation Fund as of December 07, 2016.

JCR - VIS has awarded an "AM3++" asset manager rating to the Management Company as of May 04, 2016.

This condensed interim financial information has been prepared in accordance with the requirements of InternationalAccounting Standard 34: ‘Interim Financial Reporting’, the Trust Deed, the NBFC Rules, Non-Banking FinanceCompanies and Notified Entities Regulations, 2008 (NBFC Regulations) and directives issued by SECP. In case where the requirements differ, the requirements of the Trust Deed, the NBFC Rules, the NBFC Regulations or the directivesissued by the SECP shall prevail.

This condensed interim financial information does not include all the information and disclosures required in the annualfinancial statements, and should be read in conjunction with the annual financial statements of the Fund for the yearended June 30, 2016.

The Fund is categorised as an "Asset Allocation Scheme" as per the circular 07 of 2009 issued by SECP.

FAYSAL ASSET ALLOCATION FUNDNOTES TO THE CONDENSED INTERIM FINANCIAL INFORMATIONFOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

Faysal Asset Allocation Fund (the Fund) has been established under the Non-Banking Finance Companies(Establishment and Regulation) Rules, 2003 (the NBFC Rules) and has been authorised as a unit trust scheme by theSecurities and Exchange Commission of Pakistan (SECP) on September 21, 2005. It has been constituted under aTrust Deed, dated January 31, 2006, between AMZ Asset Management Limited (former Management Company) andCentral Depository Company of Pakistan Limited (CDC) as the Trustee till February 24, 2010 and thereafter betweenFaysal Asset Management Limited (the Management Company), a company incorporated under the CompaniesOrdinance, 1984 and CDC as the Trustee, also a company incorporated under the Companies Ordinance, 1984.

The Fund is an open-end asset allocation fund and is listed on the Pakistan Stock Exchange Limited (formerly LahoreStock Exchange Limited). Units are offered for public subscription on a continuous basis and the units are transferableand can be redeemed by surrendering them to the Fund.

Notes to the Condensed Interim Financial Information FOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

3. ACCOUNTING POLICIES,ESTIMATES AND RISK MANAGEMENT PRINCIPLES

3.1 New / Revised Standards, Interpretations and Amendments

IFRS 11 - Joint Arrangements (Revised 2011)-Investments in Associates and Joint VenturesIFRS 12 - Disclosure of Interests in Other EntitiesIAS 1 - Presentation of Financial Statements - Disclosure Initiative (Amendment)IAS 28 - Investment in Associates

3.2

(Un-Audited) (Audited)March 31, June 30,

2017 2016

Note

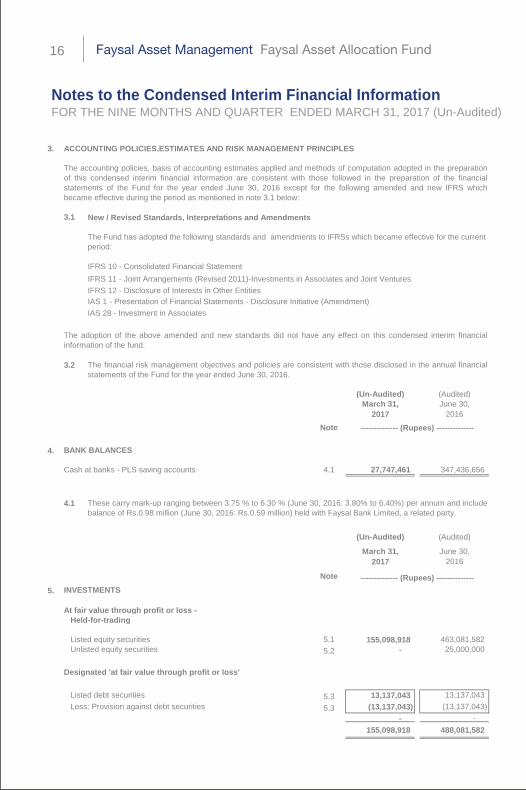

4. BANK BALANCES

Cash at banks - PLS saving accounts 4.1 27,747,461 347,436,656

4.1

(Un-Audited) (Audited)

March 31, June 30,2017 2016

Note

5. INVESTMENTS

At fair value through profit or loss -Held-for-trading

Listed equity securities 5.1 155,098,918 463,081,582 Unlisted equity securities 5.2 - 25,000,000

Designated 'at fair value through profit or loss'

Listed debt securities 5.3 13,137,043 13,137,043 Less: Provision against debt securities 5.3 (13,137,043) (13,137,043)

- - 155,098,918 488,081,582

The accounting policies, basis of accounting estimates applied and methods of computation adopted in the preparationof this condensed interim financial information are consistent with those followed in the preparation of the financialstatements of the Fund for the year ended June 30, 2016 except for the following amended and new IFRS whichbecame effective during the period as mentioned in note 3.1 below:

These carry mark-up ranging between 3.75 % to 6.30 % (June 30, 2016: 3.80% to 6.40%) per annum and includebalance of Rs.0.98 million (June 30, 2016: Rs.0.59 million) held with Faysal Bank Limited, a related party.

-------------- (Rupees) --------------

The Fund has adopted the following standards and amendments to IFRSs which became effective for the current period:

IFRS 10 - Consolidated Financial Statement

The adoption of the above amended and new standards did not have any effect on this condensed interim financialinformation of the fund.

The financial risk management objectives and policies are consistent with those disclosed in the annual financialstatements of the Fund for the year ended June 30, 2016.

-------------- (Rupees) --------------

16

17

Notes to the Condensed Interim Financial Information FOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

5.1

List

ed e

quity

sec

uriti

es -

held

for t

radi

ng

As

at J

uly

01, 2

016

Pur

chas

ed

durin

g th

e pe

riod

Tra

nsfe

rred

fr

om

unlis

ted

secu

ritie

s

Bon

us /

right

sh

ares

re

ceiv

ed

durin

g th

e pe

riod

Dis

pose

d of

f dur

ing

the

perio

d

As

at

Mar

ch 3

1,

2017

Car

ryin

g Va

lue

as a

t M

arch

31,

201

7

Mar

ket V

alue

as

at M

arch

31,

20

17

Net

ass

ets

Tota

l in

vest

men

ts

Inve

stee

co

mpa

ny

paid

-up

capi

tal

* O

rdin

ary

shar

es h

avin

g a

face

val

ue o

f Rs.

10 e

ach

unle

ss s

tate

d ot

herw

ise.

OIL

& G

AS E

XPLO

RAT

ION

CO

MPA

NIE

SO

il an

d G

as D

evel

opm

ent C

ompa

ny L

imite

d-

84

7,40

0

-

847,

400

-

-

-

-

-

-

P

akis

tan

Oilf

ield

s Li

mite

d50

,000

20

,000

-

69,5

00

50

0

264,

438

222,

525

0.15

%0.

14%

-

M

ari P

etro

leum

Com

pany

Lim

ited

6,20

0

57

,770

-

60,9

70

3,

000

4,08

4,00

2

4,56

1,41

0

3.14

%2.

94%

-

4,

348,

439

4,

783,

935

3.

29%

3.08

%0.

00%

OIL

AN

D G

AS M

ARK

ETIN

G C

OM

PAN

IES

Pak

ista

n S

tate

Oil

Com

pany

Lim

ited

22,4

00

75,0

00

-

97

,400

-

-

-

-

-

-

H

asco

l Pet

role

um L

imite

d5.

1.1

-

70,0

00

-

50

,000

20,0

00

6,98

2,30

4

5,99

8,00

0

4.13

%3.

87%

0.02

%A

ttock

Pet

role

um L

imite

d-

10

,000

-

10,0

00

-

-

-

-

-

-

Atto

ck R

efin

ery

Lim

ited

-

5,00

0

-

-

5,

000

2,30

5,00

0

2,24

4,05

0

1.55

%1.

45%

0.01

%N

atio

nal R

efin

ery

Lim

ited

-

1,35

0

-

-

1,

350

985,

082

962,

485

0.66

%0.

62%

-

10

,272

,386

9,20

4,53

5

6.34

%5.

94%

0.03

%R

EFIN

ERY

Pak

ista

n R

efin

ery

Lim

ited

250,

000

1,

200,

000

-

1,45

0,00

0

-

-

-

-

-

-

-

-

PO

WER

GEN

ERAT

ION

AN

D D

ISTR

IBU

TIO

NK

-Ele

ctric

Lim

ited

-

800,

000

-

50

0,00

0

30

0,00

0

2,

450,

000

2,

454,

000

1.

69%

1.58

%0.

03%

Kot

Add

u P

ower

Com

pany

Ltd

-

100,

000

-

15

,000

85,0

00

7,01

2,24

9

6,81

7,85

0

4.70

%4.

40%

0.01

%N

isha

t Pow

er L

imite

d-

35

,000

-

-

35

,000

2,

244,

990

1,

786,

750

1.

23%

1.15

%0.

01%

Hub

Pow

er C

ompa

ny L

td-

60

,000

-

10,0

00

50

,000

6,

726,

090

6,

553,

000

4.

52%

4.23

%-

18,4

33,3

29

17

,611

,600

12

.14%

11.3

6%0.

05%

CO

MM

ERC

IAL

BAN

KS

Hab

ib B

ank

Lim

ited

25,0

00

95,6

00

-

11

4,60

0

6,

000

1,68

7,44

0

1,61

7,66

0

1.11

%1.

04%

-

M

CB

Ban

k Li

mite

d-

58

,600

-

58,6

00

-

-

-

-

-

-

Uni

ted

Ban

k Li

mite

d50

,000

82

,900

-

122,

900

10,0

00

2,42

4,09

6

2,27

6,30

0

1.57

%1.

47%

-

N

atio

nal B

ank

of P

akis

tan

-

50,0

00

-

50

,000

-

-

-

-

-

-

B

ank

Alfa

lah

Lim

ited

-

100,

000

-

50

,000

50,0

00

1,87

5,50

0

1,80

7,00

0

1.25

%1.

17%

-

S

umm

it B

ank

Lim

ited

-

425,

000

-

-

425,

000

1,79

2,40

0

1,84

0,25

0

1.27

%1.

19%

0.02

%7,

779,

436

7,

541,

210

5.

20%

4.87

%0.

02%

FER

TILI

ZER

Fauj

i Fer

tiliz

er B

in Q

asim

Lim

ited

130,

500

10

0,00

0

-

230,

500

-

-

-

-

-

-

E

ngro

Cor

pora

tion

Lim

ited

25,0

00

196,

000

-

20

1,00

0

20

,000

7,

389,

921

7,

360,

400

5.

07%

4.75

%-

Eng

ro F

ertil

izer

s Li

mit e

d5.

1.1

-

1,10

5,00

0

-

1,

016,

500

88

,500

6,

160,

158

5,

545,

410

3.

82%

3.58

%0.

01%

Fauj

i Fer

tiliz

er C

ompa

ny L

imite

d-

65

,000

-

65,0

00

-

-

-

-

-

-

Daw

ood

Her

cule

s C

orpo

ratio

n Li

mite

d-

16

0,00

0

-

160,

000

-

-

-

-

-

-

E

ngro

Pol

ymer

& C

hem

ical

s Lt

d-

15

0,00

0

-

50,0

00

10

0,00

0

2,

517,

390

2,

528,

000

1.

74%

1.63

%0.

02%

16,0

67,4

68

15

,433

,810

10

.63%

9.96

%0.

03%

-----

Inve

stm

ent a

s %

of -

----

Nam

e of

the

Inve

stee

Com

pany

Not

e

------

------

------

------

---- N

umbe

r of s

hare

s ---

------

------

------

------

-- --

------

-- R

upee

s ---

------

-

Notes to the Condensed Interim Financial Information FOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

18

As

at J

uly

01, 2

016

Pur

chas

ed

durin

g th

e pe

riod

Tra

nsfe

rred

fr

om

unlis

ted

secu

ritie

s

Bon

us /

right

sh

ares

re

ceiv

ed

durin

g th

e pe

riod

Dis

pose

d of

f dur

ing

the

perio

d

As

at

Mar

ch 3

1,

2017

Car

ryin

g Va

lue

as a

t M

arch

31,

201

7

Mar

ket V

alue

as

at M

arch

31,

20

17

Net

ass

ets

Tota

l in

vest

men

ts

Inve

stee

co

mpa

ny

paid

-up

capi

tal

-----

Inve

stm

ent a

s %

of -

----

Nam

e of

the

Inve

stee

Com

pany

Not

e

------

------

------

------

---- N

umbe

r of s

hare

s ---

------

------

------

------

-- --

------

-- R

upee

s ---

------

-

CH

EMIC

ALS

ICI P

akis

tan

Lim

ited

63,5

00

27,5

00

-

85

,000

6,00

0

6,

572,

922

6,

695,

160

4.

61%

4.32

%0.

01%

6,57

2,92

2

6,69

5,16

0

4.61

%4.

32%

0.01

%C

EMEN

TD

.G.K

han

Cem

ent C

ompa

ny L

imite

d-

13

5,00

0

-

110,

000

25,0

00

5,72

5,43

5

5,81

0,00

0

4.00

%3.

75%

0.01

%M

aple

Lea

f Cem

ent F

acto

ry L

imite

d46

,500

10

0,00

0

-

146,

500

-

-

-

-

-

-

K

ohat

Cem

ent C

ompa

ny L

imite

d-

60

,000

-

35,0

00

25

,000

6,

799,

650

6,

584,

750

4.

54%

4.25

%0.

02%

Pio

neer

Cem

ent L

imite

d-

55

,500

-

20,5

00

35

,000

4,

863,

898

5,

005,

000

3.

45%

3.23

%0.

02%

Che

rat C

emen

t Com

pany

Lim

ited

-

300,

000

-

27

5,00

0

25

,000

4,

464,

774

4,

780,

250

3.

29%

3.08

%0.

01%

Luck

y C

emen

t Lim

ited

-

55,0

00

-

51

,000

4,00

0

3,

457,

842

3,

349,

560

2.

31%

2.16

%-

Dew

an C

emen

t Lim

ited

-

25,0

00

-

25

,000

-

-

-

-

-

-

25

,311

,599

25,5

29,5

60

17.5

9%16

.47%

0.06

%FO

OD

& P

ERSO

NAL

CAR

E PR

OD

UC

TSFa

uji F

oods

Lim

ited

(Non

-Vot

ing)

(for

mer

ly No

on P

akist

an L

imite

d)13

2,70

0

250,

500

-

35

3,20

0

30

,000

2,

564,

451

3,

078,

300

2.

12%

1.98

%0.

15%

Fauj

i Foo

ds L

imite

d37

5,00

0

100,

000

-

45

0,00

0

25

,000

2,

737,

970

2,

764,

750

1.

91%

1.78

%-

Eng

ro F

oods

Lim

ited

-

225,

000

-

20

0,00

0

25

,000

4,

412,

444

4,

061,

000

2.

80%

2.62

%-

9,71

4,86

5

9,90

4,05

0

6.83

%6.

38%

0.15

%TE

XTIL

E C

OM

POSI

TEN

isha

t Mill

s Li

mite

d38

9,00

0

50,0

00

-

42

4,00

0

15

,000

2,

387,

451

2,

478,

000

1.

71%

1.60

%-

Gad

oon

Text

ile M

ills

Ltd

-

8,00

0

-

-

8,

000

2,10

6,54

0

1,91

2,00

0

1.32

%1.

23%

0.03

%N

isha

t (C

huni

an) L

imite

d-

80

,000

-

70,0

00

10

,000

63

1,46

0

60

5,70

0

0.

42%

0.39

%-

5,12

5,45

1

4,99

5,70

0

3.45

%3.

22%

0.03

%AU

TOM

OB

ILE

ASSE

MB

LER

Pak

Suz

uki M

otor

Com

pany

Lim

ited

51,9

00

5,00

0

-

51,9

00

5,

000

3,54

0,99

8

3,09

9,85

0

2.14

%2.

00%

0.01

%In

dus

Mot

or C

ompa

ny L

imite

d-

6,

000

-

3,

000

3,

000

4,85

0,84

0

4,77

4,68

0

3.29

%3.

08%

-

D

ewan

Far

ooqu

e M

otor

s Li

mite

d-

55

2,00

0

-

552,

000

-

-

-

-

-

-

A

tlas

Hon

da L

td-

3,

000

-

1,

850

1,

150

858,

204

864,

708

0.60

%0.

56%

-

M

illat

Tra

ctor

s Li

mite

d11

0,00

0

-

-

11

0,00

0

-

-

-

-

-

-

9,25

0,04

2

8,73

9,23

8

6.03

%5.

64%

0.01

%O

IL A

ND

GAS

MAR

KET

ING

CO

MPA

NIE

SS

ui N

orth

ern

Gas

Pip

elin

es L

imite

d-

4,

063,

000

-

3,97

3,00

0

90,0

00

10,9

98,5

92

12

,849

,300

8.

85%

8.28

%0.

01%

Sui

Sou

ther

n G

as C

ompa

ny L

imite

d2,

686,

000

690,

000

-

3,

376,

000

-

-

-

-

-

-

10,9

98,5

92

12

,849

,300

8.

85%

8.28

%0.

01%

TRAN

SPO

RT

Pak

ista

n In

tern

atio

nal A

irlin

es C

orpo

rtatio

n Li

mite

d-

20

0,00

0

-

200,

000

-

-

-

-

-

-

P

akis

tan

Nat

iona

l Shi

ppin

g C

orpo

ratio

n-

20

0,00

0

-

200,

000

-

-

-

-

-

-

-

-

-

-

-

Notes to the Condensed Interim Financial Information FOR THE NINE MONTHS AND QUARTER ENDED MARCH 31, 2017 (Un-Audited)

19

As

at J

uly

01, 2

016

Pur

chas