Assessment procedure in Income- types of assessments …

37

Transcript of Assessment procedure in Income- types of assessments …

• Assessment procedure in Income-tax Act, 1961 (‘the Act’) [different

types of assessments under the Act]

• Compulsory faceless Assessments (from 13th August 2020) onwards

• Procedural aspects

• Appeals under the Act

2CA. BHUVANESH KANKANI29-08-2020

1. Summary Assessment (i.e. u/s 143(1) of the Act)

2. Scrutiny Assessment (i.e. u/s 143(3) of the Act)

3. Best Judgement Assessment (i.e. u/s 144 of the Act)

4. Re-assessment (i.e. u/s 147 of the Act)

5. Assessments for Search Matters u/s 153A/153C of the Act

3CA. BHUVANESH KANKANI29-08-2020

• It is a type of assessment carried out without any human intervention done by

centralized processing center (CPC)

• The information submitted by the assessee in his return of income is cross-

checked against the information that the income tax department has access

to

• In case ay addition is proposed it is mandatory to provide opportunity of being

heard

• Its an appealable order.

4CA. BHUVANESH KANKANI29-08-2020

• Done where return is furnished either (u/s 139 or 142(1) of the Act)

• Here, unlike summary assessment, information / evidences are called for by

he Assessing officer

• After hearing such evidences assessment is completed of total income or loss.

• Appealable Order

5CA. BHUVANESH KANKANI29-08-2020

• Done where Assessee,

• has not furnished return u/s 139(1) or 142(1) of the Act or

• has not complied the requirements of notice u/s 142(1) of the Act (i.e. filing of return,

providing books of accounts or information)

• has not complied with direction u/s 142(2A) of the Act i.e. Departmental Audit

• has not provided information as called vide notice u/s 143(2) of the Act

• Assessment to be completed on the basis of material available on record.

• Show cause notice is required to be issued for completing assessment u/s 144.

• Appealable order

6CA. BHUVANESH KANKANI29-08-2020

• Done where,

• Assessee’s Income has escaped assessment and

• Assessing officer has ‘Reasons to believe’ that particular income has escaped from

assessment

• Case can be reopened for last 4 years (in case income escaped is Rs.1 Lac or

more then 6 years and in case of foreign assets its 16 years)

• Before issuing notice of reopening (u/s 148 of the Act) the AO has to record

‘Reasons to Believe’ for reopening

7CA. BHUVANESH KANKANI29-08-2020

• In case where search action is conducted Assessments are completed in

altogether different sections i.e. u/s 153A

• Whereas, u/s 153C in case of another person, the information or valuables of

whom are found during search

• Search cases are Centralized (i.e. assessments done by AO’s of Central

Circles)

8CA. BHUVANESH KANKANI29-08-2020

• Apart from summary assessment all other assessments were generally

conducted by personal appearance.

• However, from 2017 E-assessment era was started wherein replies and

information were required to be submitted online. But, it was not Face less.

• All the assessments were carried by jurisdictional Assessing officer.

9CA. BHUVANESH KANKANI29-08-2020

• E-assessments was already in function

• On 13th August 2020 vide order F No. 187/3/2020-ITA-I Government of India

Announce mandatory completion of all the assessment on Faceless basis (i.e.

to be passed by National E-Assessment Center) except,

• Cases assigned to Central charges

• Cases assigned to International tax charges (F No. 187/3/2020-ITA-I)

10CA. BHUVANESH KANKANI29-08-2020

• Through Finance Act 2018, Section 143 was amended to insert three new sub-

sections (3A), (3B) and (3C).

• Section 143(3A) provides that CG may make scheme by notification in official gazette.

• 143(3B) enabled govt. to apply provisions of IT act, with such exception, adaptations and

modifications as may be specified to give effect to scheme prescribed u/s 143(3A).

• 143(3C) provides that every notification issued under subsection 3A and 3B be laid before

each of parliament as soon as issued

11CA. BHUVANESH KANKANI29-08-2020

The Hon’ble FM, in her Budget Speech on 5th July 2019 announced:

✓Faceless assessment in electronic mode

✓With no human interface

✓Notices to be issued electronically by a Central cell

✓Cases to be allocated to Assessment Units in a random manner

✓Central Cell to be the single point of contact between taxpayer and the

Department

12CA. BHUVANESH KANKANI29-08-2020

13CA. BHUVANESH KANKANI29-08-2020

Title Notification No. Date

CBDT notifies Income Tax E-assessment Scheme, 2019

Notification No. 61/2019-Income Tax

12/09/2019

Directions for giving effect to Income Tax E-assessment Scheme, 2019

Notification No. 62/2019-Income Tax

12/09/2019

On 12th September 2019 notifications were issued by CBDT regarding e-assessment scheme

2019, which was to be launched in phased manner.

Faceless Assessment Scheme inaugurated as Phase 1 on 7th Oct 2019 with 58,320 assigned

cases

14CA. BHUVANESH KANKANI29-08-2020

Title Notification No. Remark

Amendment to originally Notified Scheme (61/2019)

Notification No. 60/2020 – Income Tax

dated 13th August 2020

- Procedures are

detailed further

- has widened the scope

- Shifted from E-

assessment to faceless

Assessment

Amendment to Directions for giving effect to Income Tax E-assessment Scheme, 2019 (62/2019)

Notification No. 61/2020 – Income Tax

dated 13th August 2020

15CA. BHUVANESH KANKANI29-08-2020

Regional e-Assessment Centre (ReAC) under PCIT

National e-Assessment Centre

(NeAC)

Assessment Unit (AU)

Verification Unit (VU)

4Technical Unit (TU)

Review Unit (RU)

Taxpayer

✓ No Human interface

✓ Dynamic Jurisdiction

✓ Team Based Working

✓ Functional Specialisation

A. Existing Cases where the notice under section 143(2) was issued by NeAC (including notice u/s148);

B. Cases where returns of Income are filed (including u/s 148) and case already selected forScrutiny by issuing notice u/s 143(2)

C. Cases where notices under section 142(1) has been issued and no return has been furnished

D. Cased where the assessee has not furnished return of income under section 148(1) and anotice under section 142(1) calling for information has been issued

In cases (B, C and D) NeAC shall intimate the Assessee that assessment in their case will becompleted under Faceless Scheme.

16CA. BHUVANESH KANKANI29-08-2020

• Specify format, mode, procedure and processes after approval from Board

• Send all notices/communication electronically

• Assessee may reply to notice u/s 143(2) within 15 days.

• Assign cases to AU in any ReAC through automated allocation system

• On a request for verification by an AU allocate case to verification units

(ReAC) through automated allocation system.

• Provide Technical Inputs through TU including Issues such as Legal, Technical,

Data Analytics, Forensic Accounting forensic, information technology,

valuation and audit

17CA. BHUVANESH KANKANI29-08-2020

• Inform AU if Assessee fails to comply with a notice

• Select Draft Assessment Order (DAO) for review & allocate to review unit through

automated allocation system

• Where RU suggests modification allocate case to an AU other than original AU

through automated allocation system

• Providing opportunity to taxpayer in case of any order prejudicial to Assessee before

finalising assessment order

• Finalize assessment orders (including refund amount)

• Transfer all electronic records to jurisdictional AO for post assessment work

• Transfer Cases to Jurisdictional AO after Approval from Board

18CA. BHUVANESH KANKANI29-08-2020

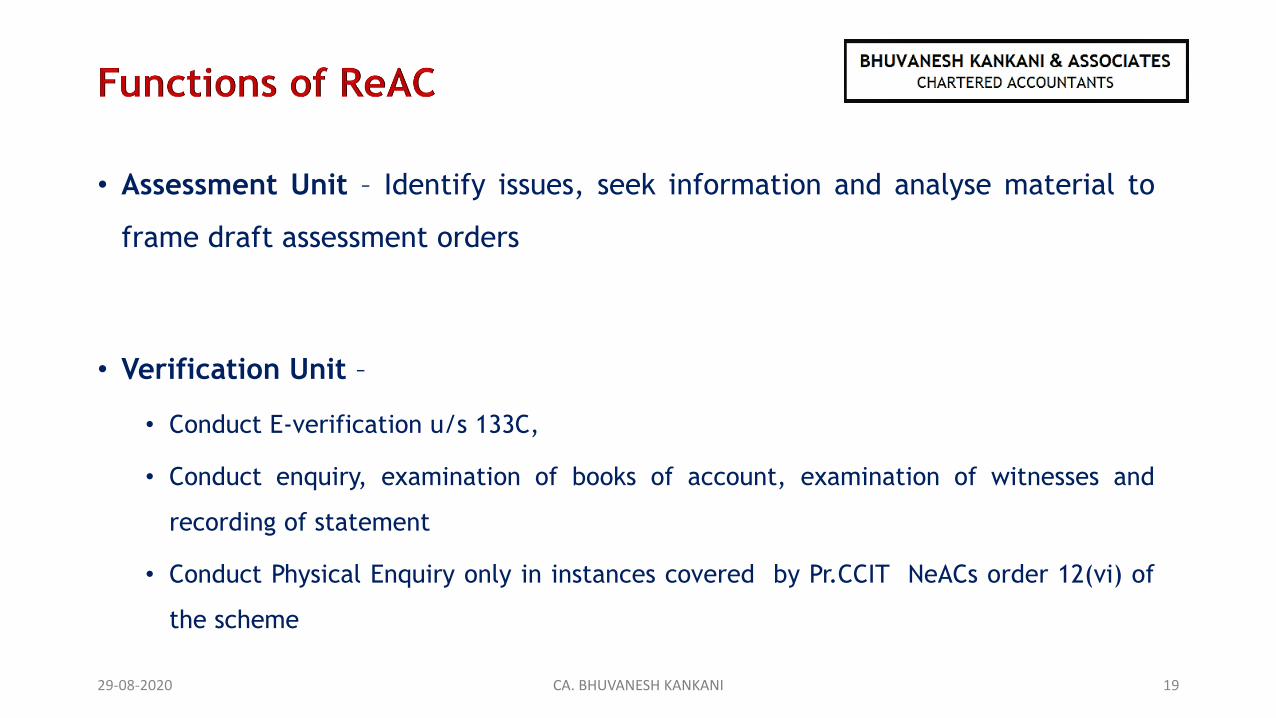

• Assessment Unit – Identify issues, seek information and analyse material to

frame draft assessment orders

• Verification Unit –

• Conduct E-verification u/s 133C,

• Conduct enquiry, examination of books of account, examination of witnesses and

recording of statement

• Conduct Physical Enquiry only in instances covered by Pr.CCIT NeACs order 12(vi) of

the scheme

19CA. BHUVANESH KANKANI29-08-2020

• Review Unit – Review of Draft Assessment Order –checking whether material

evidence brought on record, points of facts and law incorporated in DAO,

application of judicial decisions considered, arithmetic correctness etc.

• Technical Unit - Provide Technical Inputs through TU including Issues such as

Legal, Technical, Data Analytics, Forensic Accounting forensic, information

technology, valuation and audit

20CA. BHUVANESH KANKANI29-08-2020

• In assigned cases, AU, may make a request to NeAC for

• obtaining further information, documents or evidence from the assessee or any other

person,

• conducting of enquiry or verification by VU

• seeking technical assistance from the TU

• where a request has been made by the AU, the NeAC shall issue ‘appropriate notice or

requisition’ to the assessee or any other person for obtaining the information,

• the assessee or any other person, shall file his response to above within the specified/

extended time (adjournment)

• Request for verification or technical support shall be assigned by the NEAC to a VU/ TU through

automated allocation system(AES);

• NeAC shall send Verification/ Technical report received from the VU /TU, to the concerned AU

21CA. BHUVANESH KANKANI29-08-2020

• In all Cases the AU after taking into account relevant material available on the record shallprepare a Draft Assessment Order (DAO) either accepting the return or modifying the incomeor sum payable, (Also providing details of the penalty proceedings to be initiated therein, ifany )

• Send DAO to the National e-assessment Centre;

• NeAC may select the case for review through Risk Management Strategy using AutomaticExamination tool (AET)

• NeAC may

• In case no review suggested and no modification in income or sum payable done; NeAC tofinalise Assessment order, (along with Penalty Notice (if any), Demand Notice mentioningdemand or refund due)

• In case no review suggested and modification in income or sum payable proposed, the SCNshall accompany DAO and NeAC to provide an opportunity to show cause as to why theassessment should not be completed as per the DAO or

• In Case of Review assign the DAO to an RU through an automated allocation system, forconducting review

22CA. BHUVANESH KANKANI29-08-2020

• Review Unit may either concur with DAO or suggest modification

• In case it concurs with AU either

• order will be finalized: where no modification to income is proposed or

• Issue SCN along with DAO, in case DAO has proposal for modification to income.

• In case RU suggests modification to DAO, case shall be re-assigned to fresh AU;

• The new AU shall consider the suggestions made and submit fresh DAO to NeAC.

• NeAC shall again either pass order or issue SCN

• Where no response to SCN within allowed time, the assessment shall be finalized as per DAO.

• Response to SCN shall be forwarded to the AU to prepare revised DAO and send it to NeAC.

• In case of no modification by AU, NeAC shall pass & serve order. Whereas, if modification withreference to revised DAO; another SCN to be issued

23CA. BHUVANESH KANKANI29-08-2020

• Non-compliance to appropriate notice or requisition, notice u/s 142(1) or directions

u/s 142(2A)

• NeAC shall serve notice under section 144 giving an opportunity to show-cause, why

best judgment order should not be passed

• Assessee has to respond within time specified or seek extension.

• In case Assessee fails to respond NeAC to intimate the failure to the AU

• The AU shall, prepare DAO to the best of its judgment, either accepting or modifying

the income or sum payable, and send DAO to the NeAC a

• The DAO shall be examined under RMS as in the case of other orders as mentioned

above 24CA. BHUVANESH KANKANI29-08-2020

• In case an SCN along with DAO is issued , the assessee or AR may request for personal hearing

• CCIT (ReAC) of the concerned Unit may approve the request for personal hearing only if

covered by the circumstances to be specified under clause (vib) of Paragraph 12 of the

Scheme by Pr.CCIT NeAC after approval from CBDT

• The personal hearing exclusively through Video Conference (‘VC’) specified by Board.

• Any examination, recording of statement (except in case of survey) shall be conducted by VC.

• Board has to establish suitable facility of video conferencing (at such locations) so that

Assessee or his AR is denied the benefit.

25CA. BHUVANESH KANKANI29-08-2020

• By the NeAC by affixing its digital signature;

• the Assessee or any other person, by

• affixing his digital signature if required under the Rules to furnish return

of income under digital signature,

• in any other case by affixing his digital signature or under electronic

verification code; (EVC)

26CA. BHUVANESH KANKANI29-08-2020

• To be specified by Pr.CCIT (NeAC), with the prior approval of the CBDT Forlaying out

• circumstances where exclusive electronic communication to Assessee orhis AR as required in provisions of sub-paragraph (1) of paragraph 8 of thesaid Scheme ( SO.3264) shall not apply.

• circumstances in which personal hearing through Video Conference in sub-paragraph (3) of paragraph (11) of the said Scheme (SO.3264) shall beapproved shall be approved;

• Transfer of a Case to Jurisdictional AO

● If considered necessary at any stage of assessment

● By Pr. CCIT, NeAC With prior approval of Board

27CA. BHUVANESH KANKANI29-08-2020

• To Assessee:

a. Placing a copy on registered account or

b. Sending email on registered email id of assessee or his AR or

c. Uploading a copy on Assessee’s Mobile APP

And Sending real time alert (on registered Mobile Number or Email or Mobile App)

• To other person by sending email on registered Email Id.

28CA. BHUVANESH KANKANI29-08-2020

• Registered Email Id

a. Available in registered account

b. Available in last ITR or

c. Available in PAN database or

d. Available in Aadhar Database or

e. In case of company, email id available with MCA or

f. Any other ID made available by the assessee

• Registered Mobile No: refers to mobile number of Assessee of his AR appearing in user

profile in Registered Account

29CA. BHUVANESH KANKANI29-08-2020

30CA. BHUVANESH KANKANI29-08-2020

Present Assessment System Faceless Assessment System

1. Case Selection througha) Systemb) Manualc) Tax evasion information

1. No discretion to any officer in selection2. No Selection except through system red alerts3. No Selection other than information-based2.

1. Cases were permanentlyassigned to a territorialjurisdiction

1. Automated random allocation of cases2. Dynamic jurisdiction to any faceless team anywhere

in the country – 95 AUs, 35 VUs, 20 RUs and 4TUs

1. Issue of notices bothmanually and on System

1. No discretion in issue of notices2. System generated notices triggered by alert3. Notices without DIN are invalid4. Notices to be issued electronically and centrally from

the NEAC Delhi.5. The NeAC is the single point of faceless contact

between the taxpayer and the Department.

31CA. BHUVANESH KANKANI29-08-2020

Present Assessment System Faceless Assessment System

1. During scrutiny proceedings

multiple physical meetings

with officers

2. Long waiting time before

meeting the officers

1. No physical meetings with any officer

2. No officer will call you to office

3. No more waiting outside the office

4. Officer identity to remain unknown

5. Assessments in electronic mode

1. Wide discretion with officers

leads to subjective approach

and varying interpretations

1. No discretion with any individual officer. Team based

assessment

2. Draft in one city, review in another city, finalization in

third city

3. Objective, Fair and just order

1. No Draft Assessment order

(except in DRP matters)

1. Before finalization of assessment against the assessee

SCN along with Draft Assessment order has to be

issued

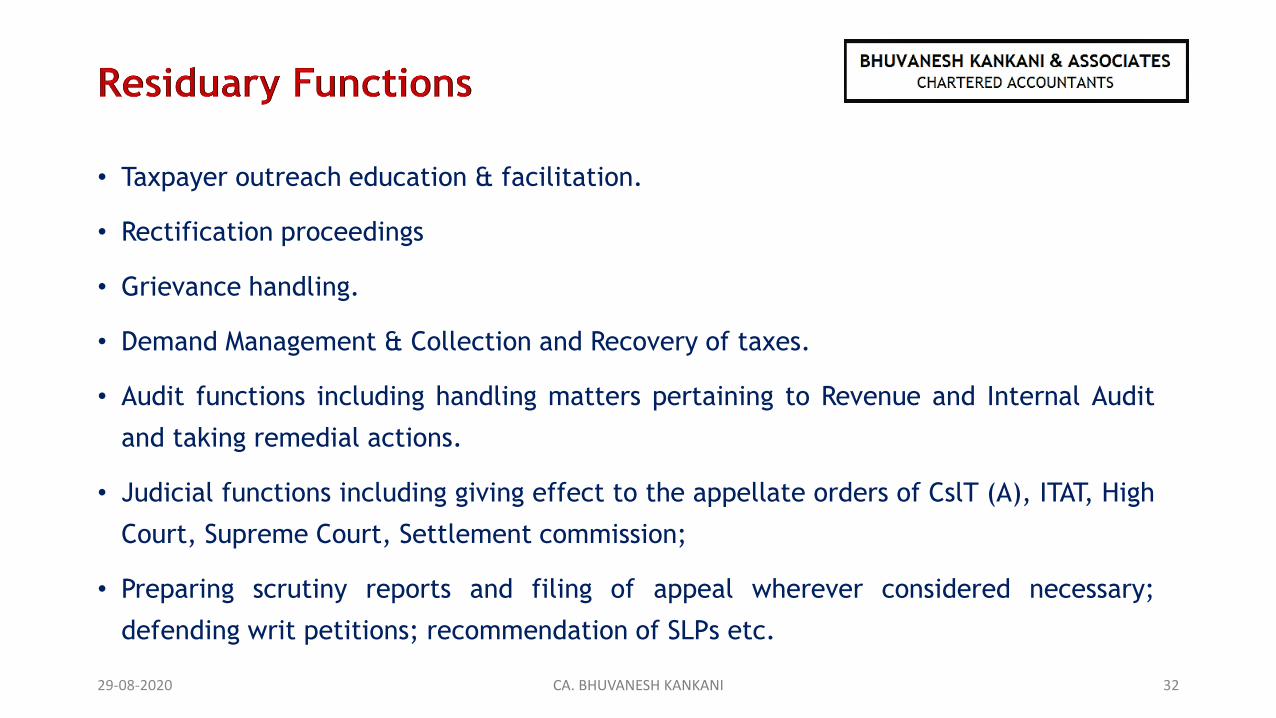

• Taxpayer outreach education & facilitation.

• Rectification proceedings

• Grievance handling.

• Demand Management & Collection and Recovery of taxes.

• Audit functions including handling matters pertaining to Revenue and Internal Audit

and taking remedial actions.

• Judicial functions including giving effect to the appellate orders of CslT (A), ITAT, High

Court, Supreme Court, Settlement commission;

• Preparing scrutiny reports and filing of appeal wherever considered necessary;

defending writ petitions; recommendation of SLPs etc.

32CA. BHUVANESH KANKANI29-08-2020

• Statutory powers under section 263 / 264 of the IT Act, 1961.

• Prosecution and compounding proceedings and related court matters.

• Administrative, HRD and cadre control matters including related court

matters.

• Custody and management of Case records.

• Management and control of infrastructure

• All the above Functions have to be done in Faceless Manner through ITBA

Portal

33CA. BHUVANESH KANKANI29-08-2020

• Orders passed by the NeAC are appealable before Commissioner of Income-tax

(Appeals)- Jurisdictional (to be filed within 30 days of receipt of Assessment

order) [section 246A of the Act].

• Further, in case Assessee is aggrieved by order of CIT(A) then he can prefer

further appeal before Income-tax Appellate Tribunal within 60 days of receipt

of CIT(A) order [Section 253 of the Act]

• Order of ITAT are appealable before HC and thereafter before SC.

34CA. BHUVANESH KANKANI29-08-2020

Questions

35CA. BHUVANESH KANKANI29-08-2020

36

Thank You

Presentation is meant only for private circulation.

PuneOffice No.121, Poornima Towers, Shankar Seth Road,

Near Swargate, Pune – 411 037, IndiaTel: +91 9421847944

E-mail: [email protected]

CA. BHUVANESH KANKANI29-08-2020

Disclaimer

37

All the information in this document are personal views of Author and are for illustrative

purposes only and should not be regarded or relied upon as legal advice by Bhuvanesh

Kankani and Associates. The information contained in herein is of a general nature and is not

intended to address the circumstances of any particular individual or entity. Although we

endeavor to provide accurate and timely information, there can be no guarantee that such

information is accurate as of the date it is received or that it will continue to be accurate in

the future. No one should act on such information without appropriate professional advice.