Assessment of the Farmers’ and Fishermen’s Pension … · CTC Ceylon Tobacco Company DO...

60

Research Studies: Demographic Transition and Pension Series No. 2 August 2003 Vindya Eriyagama Ravi P. Rannan-Eliya INSTITUTE OF POLICY STUDIES 99, St. Michael’s Road, Colombo 3, Sri Lanka. Assessment of the Farmers’ and Fishermen’s Pension and Social Security Benefit Scheme

Transcript of Assessment of the Farmers’ and Fishermen’s Pension … · CTC Ceylon Tobacco Company DO...

Research Studies: Demographic Transition and Pension Series No. 2

August 2003

Vindya Eriyagama

Ravi P. Rannan-Eliya

INSTITUTE OF POLICY STUDIES 99, St. Michael’s Road, Colombo 3, Sri Lanka.

Assessment of the Farmers’ andFishermen’s Pension and SocialSecurity Benefit Scheme

ContentsContents ...................................................................................................................................... iTable of Tables .......................................................................................................................... iiiAcronyms .................................................................................................................................. ivForward ...................................................................................................................................... vAcknowledgement ..................................................................................................................... viExecutive Summary .................................................................................................................... 11. Establishment and Organization of the Farmers and Fishermen’s Pension

Schemes ................................................................................................................................ 31.1 Establishment and Enabling Legislation .......................................................................... 3

Farmers’ pension and social security benefit scheme act ............................................... 3Fishermen’s pension and social security benefit scheme act .......................................... 3Agricultural and Agrarian Insurance Board .................................................................... 3

1.2 Organization and Structure of Agricultural and Agrarian Insurance Board ...................... 4Board of directors .......................................................................................................... 4Functions of the board ................................................................................................... 4Specific functions of the board in relation to the pension and socialsecurity benefit schemes for farmers and fishermen ....................................................... 4Advisory committees ..................................................................................................... 5Administrative structure of AAIB .................................................................................... 6

2. Farmers’ Pension and Social Security Benefit Scheme .......................................................... 82.1 Origin and Objectives .................................................................................................... 82.2 Administration and Staffing ............................................................................................ 82.3 Eligibility and Enrolment ................................................................................................ 8

Eligibility ....................................................................................................................... 8Enrolment process ......................................................................................................... 9

2.4 Contributions ............................................................................................................... 10Regular payment basis ................................................................................................. 10Discount payment basis ............................................................................................... 11Record keeping ............................................................................................................ 11

2.5 Pension and Social Security Benefits ............................................................................ 13Standard pension entitlement ...................................................................................... 13Reduced pension entitlement ...................................................................................... 13Survivor benefits .......................................................................................................... 13Social security benefits ................................................................................................ 14

2.6 Exit Procedures ............................................................................................................ 182.7 Enrolment and Coverage .............................................................................................. 18

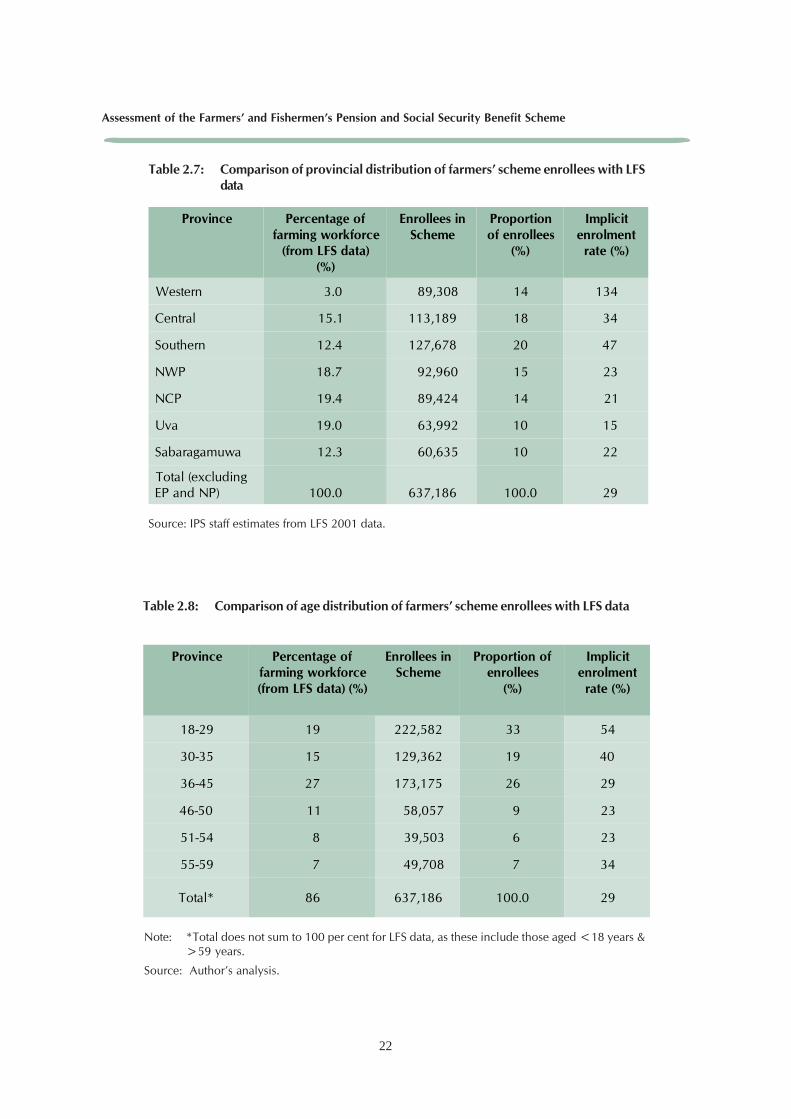

Availability of data ...................................................................................................... 18Enrolment .................................................................................................................... 18Geographical distribution ............................................................................................ 20Age distribution ........................................................................................................... 20Gender distribution ...................................................................................................... 20Default rate ................................................................................................................. 20

i

2.8 Financial Operations .................................................................................................... 23

Financial record keeping ............................................................................................. 23

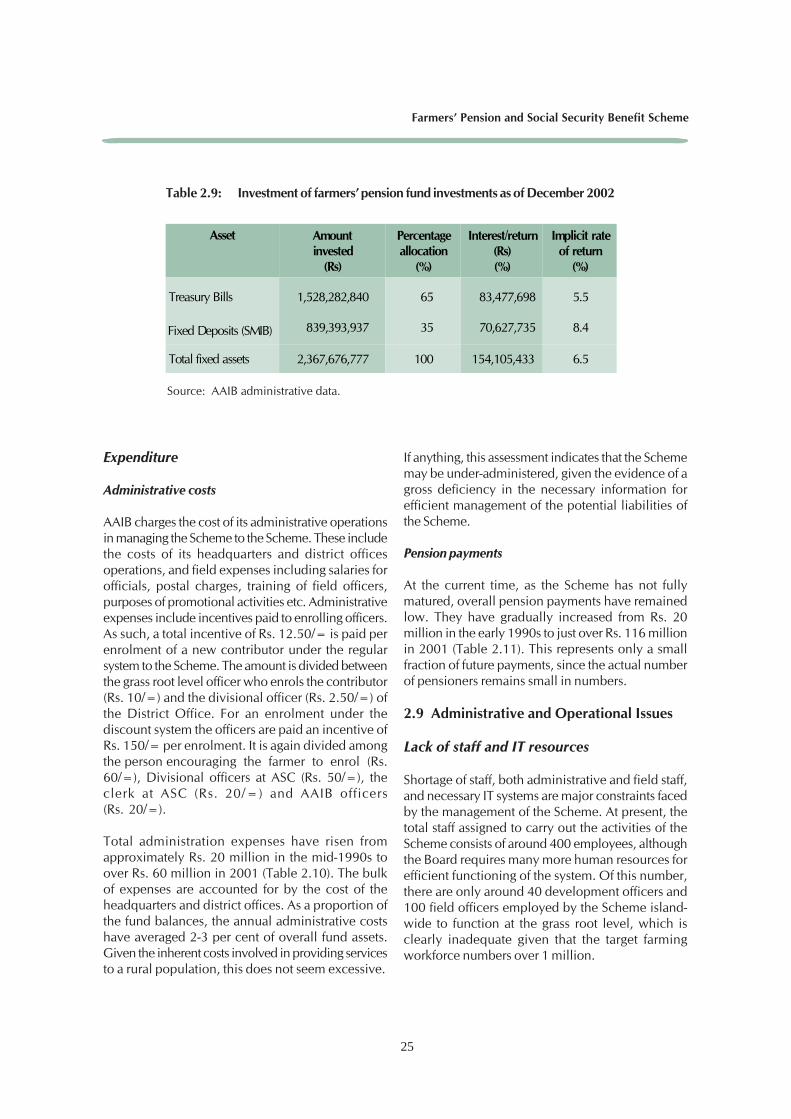

Income ........................................................................................................................ 24Expenditure .................................................................................................................. 25

2.9 Administrative and Operational Issues ......................................................................... 25Lack of staff and IT resources ....................................................................................... 25Updating and maintenance of individual accounts ...................................................... 27Default ........................................................................................................................ 28Promotional activities .................................................................................................. 30

3. Fishermen’s Pension and Social Security Benefit Scheme.................................................. 313.1 Origin and Objectives ................................................................................................. 313.2 Administration and Staffing ......................................................................................... 313.3 Eligibility and Enrolment ............................................................................................. 32

Eligibility ..................................................................................................................... 32Enrolment process ....................................................................................................... 32

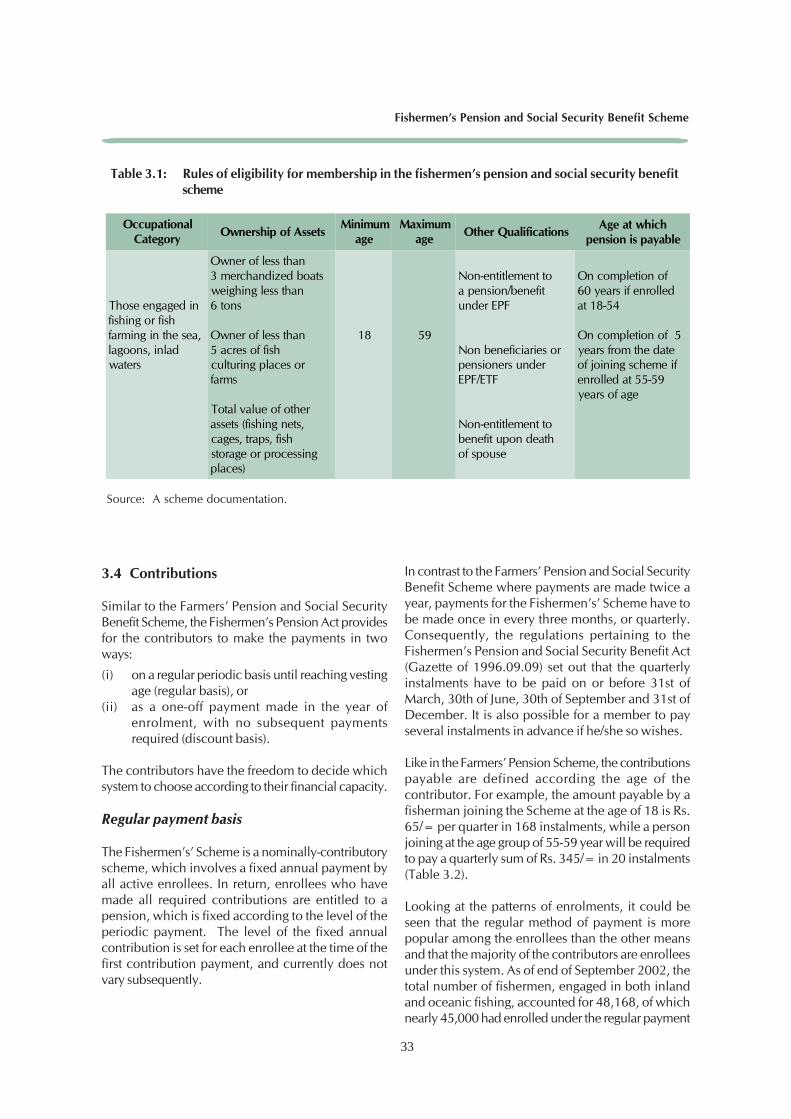

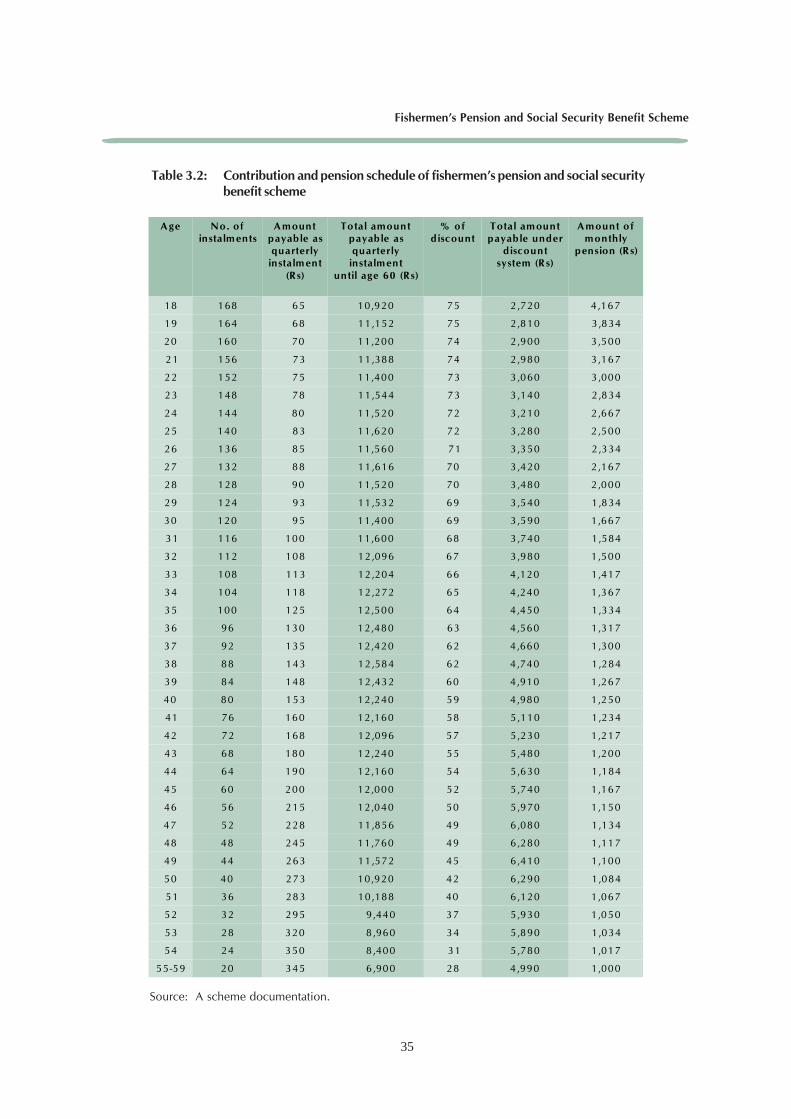

3.4 Contributions .............................................................................................................. 33Regular payment basis ................................................................................................ 33Discount payment basis .............................................................................................. 34Record keeping ........................................................................................................... 34

3.5 Pension and Social Security Benefits ........................................................................... 34Standard pension entitlement ..................................................................................... 36Survivor benefits ......................................................................................................... 36Social security benefit ................................................................................................. 36

3.6 Default Rate ................................................................................................................ 40Financial Performance of the Scheme ......................................................................... 41

3.7 Enrolment and Coverage ............................................................................................. 42Availability of data ...................................................................................................... 42Coverage .................................................................................................................... 42Age and gender distribution ........................................................................................ 42Geographic distribution .............................................................................................. 42

3.8 Administrative and Operational Issues ........................................................................ 44Lack of staff ................................................................................................................. 44Promotional and enrolment activities ......................................................................... 44Commitment of officers ............................................................................................... 44Default rate ................................................................................................................. 44Updating of accounts .................................................................................................. 45Financial constraints ................................................................................................... 45

4. Assessment of Ability of Schemes to Provide Social Security ............................................ 464.1 Adequacy of Retirement Income in Farmers’ and Fishermen’s Pension

Schemes ...................................................................................................................... 464.2 Financial Self-sufficiency of the Farmers’ and Fishermen’s Pension

Schemes ...................................................................................................................... 485. Recommendations ............................................................................................................. 51

Bibliography ............................................................................................................................. 52

ii

iii

Tables

Table 2.1: Rules of eligibility for membership in the farmers’ pension and

social security benefit scheme ................................................................................ 9

Table 2.2: Contribution and pension schedule of farmers’ pension and social security

benefit scheme..................................................................................................... 12

Table 2.3: Number of pensioners and amount paid as pension ............................................. 14

Table 2.4: Gratuities payable under disablement benefit, farmers’ scheme ........................... 16

Table 2.5: Enrolments in farmers’ pension scheme ............................................................... 19

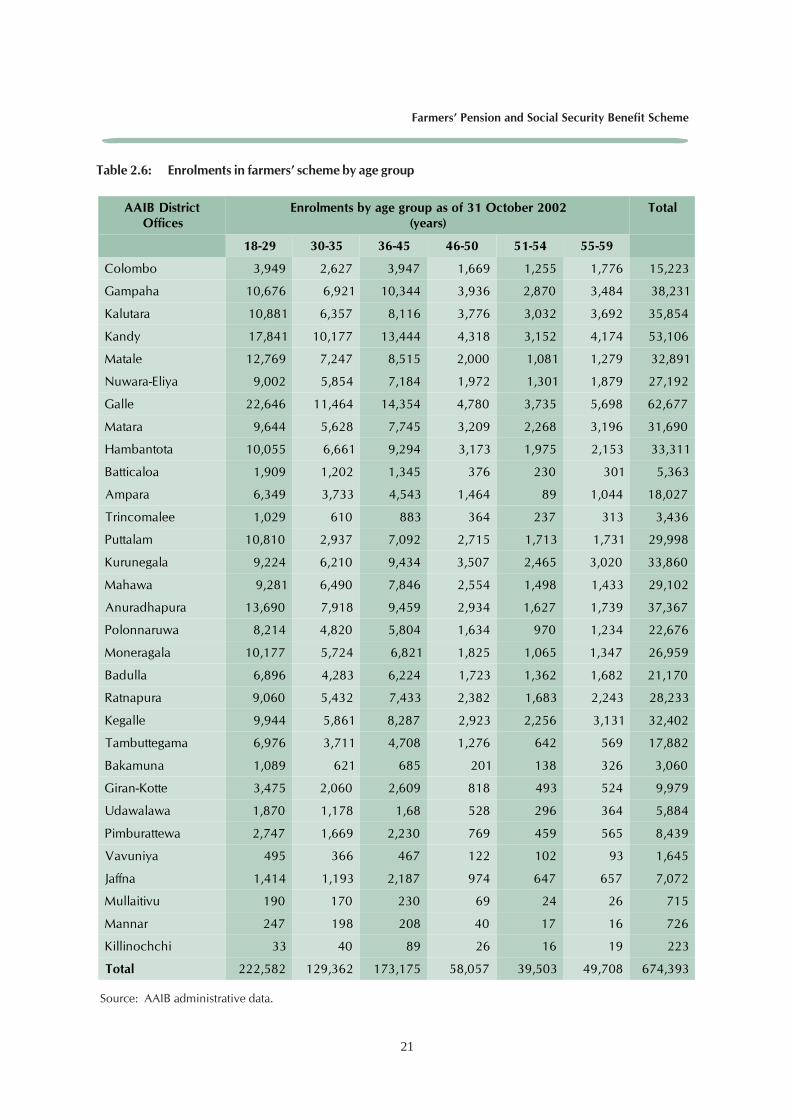

Table 2.6: Enrolments in farmers’ scheme by age group ....................................................... 21

Table 2.7: Comparison of provincial distribution of farmers’ scheme enrollees with

LFS data ............................................................................................................... 22

Table 2.8: Comparison of age distribution of farmers’ scheme enrollees with

LFS data ............................................................................................................... 22

Table 2.9: Investment of farmers’ pension fund investments as of December

2002 .................................................................................................................... 25

Table 2.10: Administration expenses of farmers’ pension scheme,

1996-2001 (Rupees) ............................................................................................. 26

Table 2.11: Pension expenditures of farmers’ pension scheme, 1996-2001 (Rupees) .............. 26

Table 3.1: Rules of eligibility for membership in the fishermen’s pension and

social security benefit scheme .............................................................................. 33

Table 3.2: Contribution and pension schedule of fishermen’s pension and social

security benefit scheme ....................................................................................... 35

Table 3.3: Gratuities payable under disablement benefit, fishermen’s scheme ...................... 37

Table 3.4: Trends in enrolment and pensioners, fishermen’s scheme, 1991-2002 ................. 37

Table 3.5: Enrolment by age ................................................................................................. 43

Table 3.6: Provincial distribution of enrollees in fishermen’s scheme ................................... 43

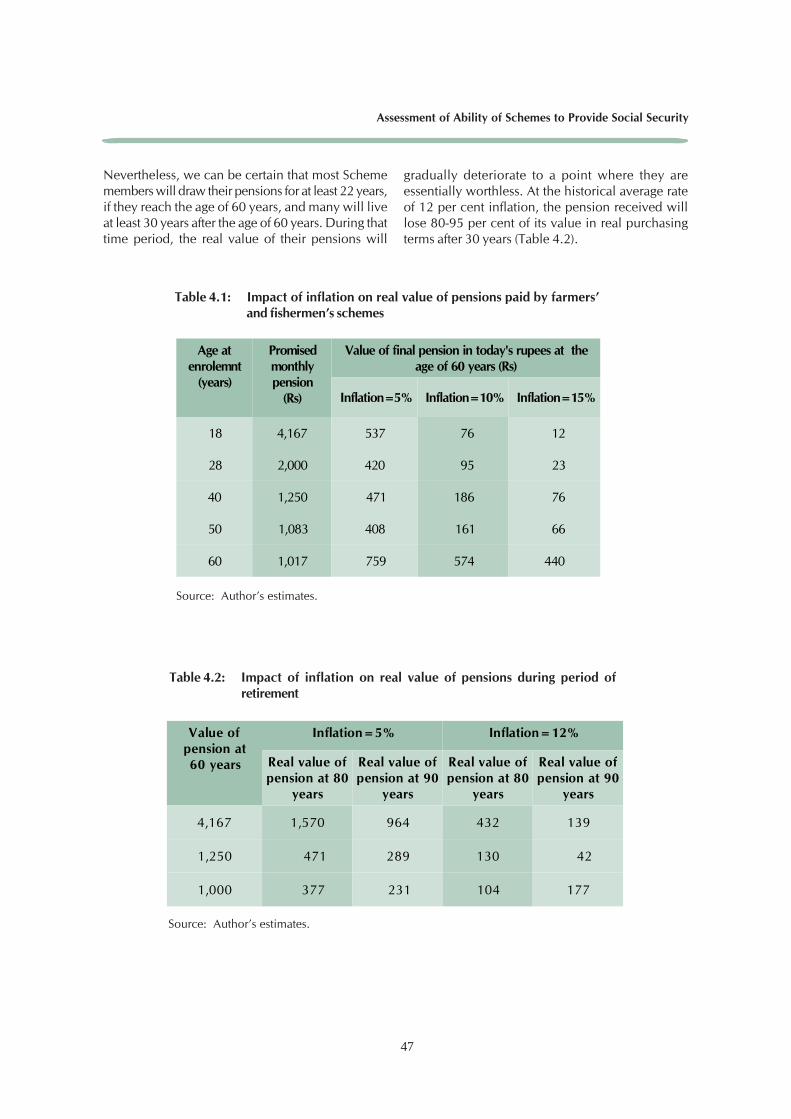

Table 4.1: Impact of inflation on real value of pensions paid by farmers’ and

fishermen’s schemes ............................................................................................ 47

Table 4.2: Impact of inflation on real value of pensions during period of

retirement ............................................................................................................ 47

Table 4.3: Mean gross interest rates on investments of farmers’ pension

fund, 1987-2002 .................................................................................................. 49

Table 4.4: Estimated liability per member under investment return ...................................... 50

Figures

Figure 1.1: Organization Chart of the Agricultural and Agrarian Insurance Board .................... 7

Acronyms

AAIB Agricultural and Agrarian Insurance BoardAD Assistant DirectorASC Agrarian Services CentreCSPS Civil Servants Pension SchemeCTC Ceylon Tobacco CompanyDO Development OfficerDS Divisional SecretariatEP Eastern ProvinceEPF Employees’ Provident FundETF Employees’ Trust FundFI Fisheries InspectorFO Field OfficerGS Grama SevakaLFS Labour Force SurveyNCP North Central ProvinceNGO Non Government OrganizationsNP Northern ProvinceNWP North Western ProvinceSMIB State Mortgage and Investment Bank

iv

v

FOREWORD

EXTENSION OF SOCIAL SECURITY COVERAGE TO THE EXCLUDED

Only one in five people in the world has adequate social security coverage: yet social security is a basicneed and a basic human right. Its fulfilment would contribute to the promotion of decent work and to thereduction of poverty. As a result of discussion during the International Labour Conference in June 2001,an international tripartite consensus emerged which urged member states to give priority to this issue andthe ILO was called upon to launch a global campaign on extension of coverage, The Director General ofthe ILO formally launched the Global Campaign on Social Security and Coverage for All at the InternationalLabour Conference in Geneva in June 2003.

The overall objective of the campaign is to extend social security to the excluded through the mobilisationof key actors at the national and international levels. The process relies heavily on social dialogue and oninnovative approaches to meeting social protection needs. Technical cooperation projects in manydeveloping countries will be an important instrument in this process and, in as many countries as possible,an action plan for extension will be formulated based on a diagnosis of social security needs and weaknesses.Financial support was secured from the Government of the Netherlands for a technical cooperation projectto be executed from early 2002 in three developing countries - Sri Lanka Honduras and Mali.

In Sri Lanka, a national diagnosis of social security provisions and needs in Sri Lanka has been completedand a report is being prepared which will assess the existing system as a basis for formulating a nationalaction plan. This diagnosis is based on a series of special studies of existing schemes and information onbackground issues.

This report is concerned with assessing the effectiveness of the special contributory scheme which seeksto provide social security for farmers and fishermen.

Clive Bailey Claudia CoenjaertsSocial Security Policy and Development Branch Director, ILOILO Geneva Colombo

Acknowledgement

This study was conducted as part of the IPS Health Policy Programme’s core research effort into theeconomic and social impacts of demographic ageing. The authors wish to express their sincere thanks tothe staff of the Agricultural and Agrarian Insurance Board for the valuable information provided by themon the Farmers’ and Fishermen’s Pension and Social Security Benefit Schemes. Mention must be made ofMr. L. R. B. Dissanayake, Chairman of Agricultural and Agrarian Insurance Board for his valuable insightand support in facilitating the study. Special acknowledgement should be also made to Mr. U. R.Chandradasa, Acting Director, Farmers’ Pension and Social Security Benefit Scheme and Mr. S. M. A. W.K. Manchanayake, Deputy Director, Fishermen’s Pension and Social Security Benefit Scheme for extendingtheir immense support in providing us with vital information and statistics on the two schemes. Mr. R. B.Wijekoon, Deputy Director, Actuarial, Research and Marketing and Mr. D. Manathunga, Deputy Director,Finance of the AAIB also provided much assistance in obtaining information and data on the two schemesfor which the authors are very grateful.

The authors are thankful to Ms Chantal Samarasinghe, Research Assistant, IPS Health Policy Programmefor providing valuable assistance with data collection. The authors also wish to thank the other staff of theInstitute of Policy Studies Health Policy Programme for extending their assistance in various activitiesrelated to the study, and to Nirosha Gaminiratne for helpful comments and corrections to the text.

Desktop and graphical layout of the final publication was carried out by Ms. Sharmini de Silva underthe guidance of Ms. Manu Tissera-Gunasekara of the IPS Publications Unit, and final editing by Mr. D. D.M. Waidyasekera. Finally the authors wish to express their appreciation to the International LabourOrganization (ILO) for funding this study and the printing of this publication.

vi

1

Executive Summary

Farmers and fishermen comprise 25-30 per cent and 1 per cent of the workforce in Sri Lanka, orapproximately 2.0-2.4 million and 0.1 million respectively. Most are self-employed, with income in bothoccupations usually seasonal and subject to many factors beyond their control. Both occupations involvehard physical work, and many continue working beyond the age of 60 years. The Farmers’ and Fishermen’sPension and Social Security Benefit Schemes were established by successive acts of legislation in 1987and 1990. The objectives were to provide a minimum level of social security and provision in old age forworkers, who had no access to other formal schemes. Both Schemes are administered by the Agriculturaland Agrarian Insurance Board (AAIB), with overall supervision provided by the Ministers in charge ofAgriculture and the Department of Fisheries.

The Farmers’ Pension Scheme targets farmers whose main source of income is agriculture includinglivestock farming, with some exclusions such as owning more than certain stipulated limits for landownership, or being covered or eligible for enrolment in EPF or any other pension scheme. The Fishermen’sScheme targets fishermen. Both schemes restrict enrolment to those aged between 18-59 years.

In both Schemes, contributions are fixed-level payments which do not change once set, according to theage at enrolment, and must be made twice yearly in the Farmers’ Scheme, and quarterly in the Fishermen’sScheme. They range from Rs. 260/= per year if enrolling at age 18 to Rs. 1,380/= per year if enrolling atage 59. To receive the final benefits, members make all contributions, although considerable leeway isprovided for defaulters to make good their payment history. Members must maintain contributions up tothe age of 60 years, when they are entitled to receive a pension, unless they enrol between the ages of 55and 59 when the vesting period is 5 years.

The major benefit in both Schemes is the pension, in addition to which some disability benefits such asgratuity and disability pensions are provided. The pension is a monthly payment, the level of which isfixed at the time of enrolment. According to the schedules in both Schemes, the earlier the age ofenrolment, the lower the fixed-level contributions, and the higher the ultimate pensions. In the Farmers’Scheme, the fixed level pension varies from Rs. 1,000/= per month to Rs. 4,167/= per month. For theFishermen’s Scheme, it varies from Rs. 1,000/= per month to Rs. 4,167/= per month. There is a survivorbenefit in that both pensions are payable to surviving spouses till their death. The contribution scheduleshave not been changed in either scheme since inception, but the pension schedules have been revisedby raising the minimum pension benefit repeatedly to a minimum of Rs. 1,000/= per month currently.

Contribution collection is decentralized, and has in part been delegated to other government agencies,including the Postal Department. Both schemes mainly rely on field officers from the AAIB or from thesupporting government departments to collect contributions. Collected contributions are paid into separatepension and social security funds maintained by AAIB. Most funds are invested in deposits at state banksor in Treasury Bills, with the AAIB required to follow the advice of the Finance Minister in makinginvestments. Both Schemes charge their administrative costs to the gross investment returns achieved.Net returns on investment after these administrative charges are similar to the gross return on members’accounts paid by EPF. The government made capital commitments at inception to both schemes to aidtheir financial sustainability, but only one third of these were actually paid, and the government hasadvised both schemes not to expect further funding.

Member records are maintained mostly on a manual and decentralized basis. The Farmers’ Scheme inparticular lacks an efficient information system, and is not in a position to monitor defaults in a timelymanner. In addition, the lack of computerized information systems ensures that both schemes lack readyaccess to detailed information on the profile and payment histories of members, and thus cannot efficiently

2

monitor risks and potential liabilities of the Scheme. Work is ongoing to computerize the Farmers’ Scheme,but funding appears insufficient for the scale of the task. Additional improvements are also required in thehandling of contribution collections, as significant delays in receipt of funds by AAIB have been noted.

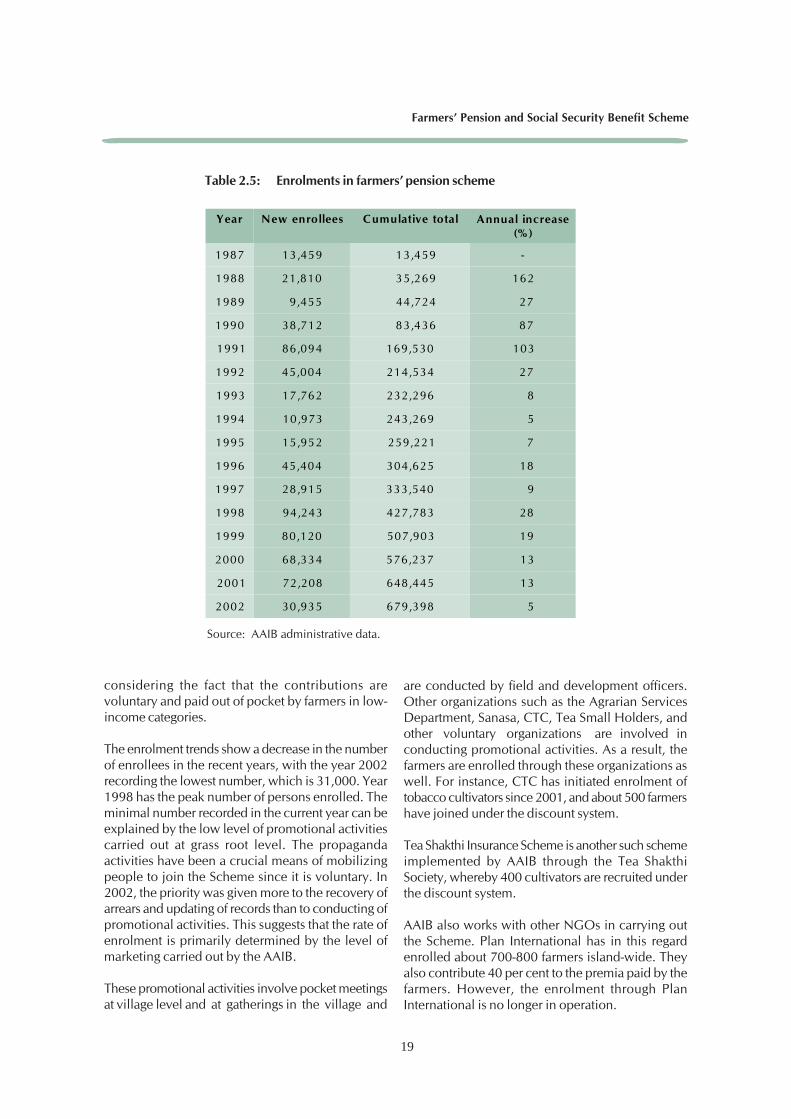

The Farmers’ Scheme has enrolled 675,000 members out of an AAIB-estimated eligible 1.2 million farmers(56 per cent coverage), and the Fishermen’s Scheme has enrolled 48,000 out of an estimated eligible115,000 population (42 per cent coverage). This is substantial, but excludes half the agricultural andfishing workforce. Coverage appears to be quite variable across the country and in the less developedprovinces much lower. In addition, approximately 30-40 per cent of members in both schemes may havedefaulted.

The Schemes have two major deficiencies. First, neither Scheme will provide adequate replacementincome for most members, as the pensions being provided are too low, and in addition are not inflationprotected. The major reasons for the low replacement level are the low contribution amounts and theshort vesting period. Second, at current contribution levels and given likely increases in life expectancy,there will be insufficient funds to honour pension commitments made to existing members. There is anestimated funding gap of at least a billion rupees in current rupees, based on current enrolments.

To address these issues, the following are recommended as near term improvements:

(i) As policy, the contribution schedules should be automatically adjusted whenever the pensionschedules are revised. Changes in the two should be actuarially-linked

(ii) The contribution period should be extended in a flexible manner beyond age 60, for those who wishto extend their contributions, in return for an actuarially-fair increase in pension entitlements

(iii) Work to computerize the information systems in both schemes should be reviewed and acceleratedin order to provide better information for future management

In the longer term, the following more substantial changes to both schemes should be given seriousconsideration in order to provide the relevant workers with substantive income replacement during oldage:

(i) The government will need to honour its explicit pension guarantee that it has provided to currentmembers by providing substantial future subsidies, and needs to recognize that extending socialsecurity to these workers in the long-term will require significant tax-funding

(ii) A shift to providing inflation-indexed pensions. This may require reducing the initial pension paid,and will necessitate establishing capacity for detailed actuarial and economic analysis

(iii) Replacement of the current fixed contribution and pension schedules with a more flexible formulathat permits greater flexibility in contributions, sets pensions individually according to life-timecontributions, and allows for some redistribution between higher income and lower incomecontributors

(iv) An increase in the average number of years that members pay contributions for, in return for higherpension benefits

(v) The minimum and average level of contributions should be increased substantially. However, inorder to maintain or improve coverage to the poorer workers, an explicit government subsidy will benecessary

(vi) Alternative mechanisms for funding the administrative operations should be explored to identifyoptions which involve less trade-off with the investment returns of the pension funds and whichwould enable more substantial modernization of the administrative operations. One option is tofund all administrative costs from an annual government contribution, which would also yield moreaccountability

3

Establishment and Organization of the Farmers and Fishermen’s Pension Schemes

1. Establishment and Organization of theFarmers’ and Fishermen’s PensionSchemes

1.1 Establishment and Enabling Legislation

The established pension and old-age securityarrangements in Sri Lanka, which are the Civil ServantsPension Scheme (CSPS), Employees’ Provident Fund(EPF), Employees’ Trust Fund (ETF) and privateprovident funds in the mercantile sector, are restrictedto the formal sector work-force. The Government ofSri Lanka established three major schemes in the 1980sand 1990s to cover segments of the work-force noteligible for participation in these existingarrangements, namely the Farmers’ Pension and SocialSecurity Benefit Scheme, Fishermen’s Pension andSocial Security Benefit Scheme and the Pension andSocial Security Benefit Scheme for the Self-EmployedPersons. The three schemes are voluntary, nominally-contributory schemes, which are explicitly targetedat the relevant occupational groups. Both Schemeswere established and are governed by legislation.

Farmers’ pension and social security benefitscheme act

The Farmers’ Pension and Social Security BenefitScheme was established via legislation by theGovernment of Sri Lanka through the Farmers’ Pensionand Social Security Benefit Scheme Act, No. 12 of1987. It was principally targeted at the approximately2 million persons estimated to be directly or indirectlyengaged in agriculture, of which the majority arepeasant farmers who operate on a subsistence levelworking hard in youth through to late in life. It wasrecognized that the lack of provision of social securityoften rendered them helpless, and therefore that themajority were left without any resources to fall backon in old age (Perera, 1989). Mostly, they have reliedon family support and state welfare for their needswhen in old age. The Scheme has to date enrolledover 600,000 persons.

Fishermen’s pension and social security benefitscheme act

The Fishermen’s’ Pension and Social Security BenefitScheme was established via legislation by theGovernment of Sri Lanka through the Fishermen’s’Pension and Social Security Benefit Scheme Act, No.

23 of 1990. The Scheme is targeted at the fishingwork-force, which is estimated by the Agriculturaland Agrarian Insurance Board (AAIB) to numberapproximately 115,000. The Scheme has enrollednearly 50,000 persons to date. The fishing work-force,in a similar manner to the agricultural work-force,are subject to considerable insecurity and uncertaintyin their income, as well as numerous occupationalhazards. The specific objectives of the Scheme arestated to be:

• To provide social security to fishermen during oldage or disability and to their families given therisky nature of their occupation

• To provide relief to dependents of fishermen upondeath

• To encourage fishermen to continue in theiroccupation which is necessary for the developmentof the fisheries industry

• To attract young persons to the fishing industry• To promote the habit of saving and thrift among

fishermen

In both Schemes, the enacting legislation has beenaccompanied by administrative regulations issued viaGovernment Gazette, in accordance with the primarylegislation.

Agricultural and Agrarian Insurance Board

The Agricultural and Agrarian Insurance Board (AAIB)is the authorized body assigned with the tasks ofimplementing and managing both Farmers’ andFishermen’s Pension and Social Security BenefitSchemes. The AAIB was established in the form of astatutory organization under the Agricultural InsuranceLaw, No. 27 of 1973, thereby repealing theAgricultural Insurance Scheme introduced under theCrop Insurance Act in 1961. The formation of thisnew organization was with the specific objective ofmaking the Agricultural Insurance Scheme into a moreeffective and fruitful body. Accordingly, the Boardwas initially entrusted with the key responsibility ofimplementing an extensive insurance scheme for thebenefit of small-scale paddy cultivators and livestockfarmers with a view to providing a better and moremeaningful service to the farmer community. Inaddition, undertaking research that is necessary forthe promotion and development of such agriculturalinsurance is another function assigned to the Boardunder the Agricultural Insurance Law.

Later, with the setting up of the Farmers’ andFishermen’s Pension and Social Security Benefit

4

Assessment of the Farmers’ and Fishermen’s Pension and Social Security Benefit Scheme

Schemes in 1987 and 1990 respectively, the functionsof the AAIB has expanded, since the task ofadministration, operation and implementation ofthese two Schemes are also assigned to the AAIB. Atits inception, the organization was known as theAgricultural Insurance Board, which has beensubsequently changed to Agricultural and AgrarianInsurance Board following an amendment to theAgricultural Insurance Law brought forth in 1999(Agricultural and Agrarian Insurance Act. No 20,1999).

1.2 Organization and Structure of theAgricultural and Agrarian InsuranceBoard

The AAIB is governed by its enabling legislation,which specifies its structure and authority.

Board of directors

As specified in Section 3 of the Agricultural andAgrarian Insurance Act No. 20 of 1999, the Boardconsists of seven members appointed to hold officefor a period of 3 years. Of the Board members, theChairman and the representative from the NationalLevel Farmer Organization are appointed entirely bythe Minister, while the other members who constitutethe Board of Directors are appointed ex-officio. TheBoard is vested with the powers of making rules withregard to the administration of the Board and overallimplementation and management of the activitiescarried out by AAIB. The Board of Directors isspecified as follows:

(i) The Chairman to be appointed by the Minister(ii) The Secretary to the Ministry of Finance or an

officer of the Ministry of Finance nominated bythe Minister of Finance

(iii) The Secretary to the Ministry of Agriculture or anominee of the Minister of Agriculture

(iv) The Secretary to the Ministry of Fisheries or hisnominee

(v) The Secretary to the Ministry of Livestock or asnominated by the Minister of Livestock

(vi) The Chief Executive of a licensed CommercialBank within the meaning of the Banking Act(Act No. 30 of 1988) nominated by the Ministeror his nominee (Central Bank)

(vii) The nominee of a National Level FarmerOrganization recognized by the Government

Functions of the board

According to the Agricultural and Agrarian InsuranceBoard Act, the Board is expected to carry out severalfunctions and duties which include:

(i) Establishment and operation of a widespreadinsurance scheme for the benefit of theagriculturists in respect of crops, which includeplantation crops, medicinal plants, fisheries,forestry and livestock, with the intention ofproviding stability to agriculturists andpromoting agricultural production, andproviding indemnity against losses

(ii) Establishment and operation of an insurancescheme for agriculturists with regard toagricultural equipment and implements andother movable and immovable property ofagriculturists

(iii) Establishment and operation of an insurancescheme for agriculturists in respect of storageand preservation of agricultural, horticultural andforest produce and the products of medicinalplants

(iv) Establishment and operation of medical benefitsand social security schemes for the benefit ofthe agriculturists, which are namely, the Farmers’and Fishermen’s Pension and Social SecurityBenefit Schemes

Specific functions of the board in relation tothe pension and social security benefit schemesfor farmers and fishermen

In addition to the functions, responsibilities andpowers conferred on it by the Agricultural andAgrarian Insurance Board Act, the Board is empoweredto carry out certain specific tasks in respect to theabove Schemes, as specified in Section 11 of theFarmers’ Pension and Social Security Benefit Act No.12 of 1987, and in Section 13 of the Fishermen’sPension and Social Security Benefit Act No. 23 of1990. Accordingly, as the authorized agent inmanaging the two Schemes, the AAIB is expected toand has the authority to:

(i) Make rules in respect of the administrative affairsof the Board with regard to the two Schemes

(ii) Refer to the Advisory Committee for advice onany matter pertaining to the Schemes

(iii) Maintain the required actuarial, financial andoperational reports in respect of the Schemes

(iv) Monitor, evaluate and review the Schemes andeffect changes in the operational rules wherenecessary and where it is empowered to do so

5

Establishment and Organization of the Farmers and Fishermen’s Pension Schemes

(v) Determine the award to be made to anycontributor in terms of the policy issued to him/her

(vi) Employ officers, servants and other employeesas are necessary for the efficient managementof the Schemes

(vii) Do all other things which in the opinion of theBoard are necessary to facilitate the operationand management of the Schemes

Advisory committees

Apart from the special powers and functions above,both Farmers’ and Fishermen’s Pension and SocialSecurity Benefit Scheme Acts also provide for theappointment of an Advisory Committee for each ofthe Schemes. As such, two separate AdvisoryCommittees are in operation. Their purpose is toprovide the Board with necessary advice pertainingto the two Schemes, when and where it is required.The Committees of both Farmers’ and Fishermen’sPension and Social Security Benefit Schemes thusformed each comprise a total of 12 members, with 6ex-officio members and 6 nominated members whoare appointed to hold office for a period of 3 years.The Chairman of the Agricultural and AgrarianInsurance Board also acts as the Chairman of the twoAdvisory Committees. The Committees generally meetonce a month to discuss and advise the Board onmatters related to the Schemes.

Both Acts, under Section 22, also permit the AdvisoryCommittees to exercise certain powers in this regard.Accordingly, their statutory function is to advise theBoard on matters relevant to the management,operation and implementation of the two Schemesas may be requested by the Board. The Committeesare also empowered to advise the Board with regardto making rules of the Board, and to formulate policiesfor the efficient management, operation andimplementation of the Schemes. In addition, theirfunctions also involve those such as reviewing theactivities of the Board in view of the management,operation and implementation of the two Schemes,as well as providing advice and makingrecommendations to the relevant Minister in thisregard.

As mentioned above, the Advisory Committee forthe Farmers’ Scheme consists of 6 ex- officio membersand 6 nominated members. The ex-officio memberscomprise:

(i) The Chairman of the AAIB who is also theChairman of the Advisory Committee

(ii) The Director of Pensions or his representative(iii) The Commissioner of Agrarian Services or his

representative(iv) The Chief Actuary of the Insurance Corporation

of Sri Lanka or his representative(v) The Superintendent of the Department of the

Employees’ Provident Fund of the Central Bankof Sri Lanka or his representative

(vi) The Commissioner of Labour or hisrepresentative

The nominated members comprise:

(i) One member nominated by the Minister inconsultation with the Minister in charge of thesubject of Agricultural Development andResearch

(ii) One member nominated by the Minister fromthe General Treasury in consultation with theMinister in charge of the subject of Finance

(iii) Three members nominated by the Minister fromthe Agricultural and Agrarian Insurance Boardin consultation with the Minister in charge ofthe subject of Agricultural Insurance

(iv) One member nominated by the Minister fromamong persons with a wide knowledge andexperience in social security benefit schemes.

The Advisory Committee for the Fishermen’s Schemeconsists of 6 ex- officio members and 6 nominatedmembers, in a similar manner to the AdvisoryCommittee for the Farmers’ Scheme. The ex-officiomembers comprise:

(i) The Chairman of the AAIB who acts as theChairman of the Advisory Committee

(ii) The Director of Fisheries or his representative(iii) The Director of Pensions or his representative(iv) The Chief Actuary of the Insurance Corporation

of Sri Lanka or his representative(v) The Superintendent of the Department of the

Employees’ Provident Fund of the Central Bankof Sri Lanka or his representative

(vi) The Commissioner of Labour or hisrepresentative

The nominated members comprise:

(i) Two members nominated by the Minister fromthe Ministry in his charge

(ii) One member nominated by the Minister fromthe General Treasury in consultation with theMinister in charge of the subject of Finance

6

Assessment of the Farmers’ and Fishermen’s Pension and Social Security Benefit Scheme

(iii) Two members nominated by the Minister fromthe Agricultural and Agrarian Insurance Boardin consultation with the Minister in charge ofthe subject of Agricultural Insurance

(iv) One member nominated by the Minister fromamong persons with a wide knowledge andexperience in social security benefit schemes

It can be observed both from the original intent ofthe legislation and their operation in practice, thatboth Advisory Committees serve as the main sourceof technical input for the overall strategicmanagement of the Schemes. However, it is observedthat much of this input requires actuarial expertise,which is scarce within Sri Lanka generally.

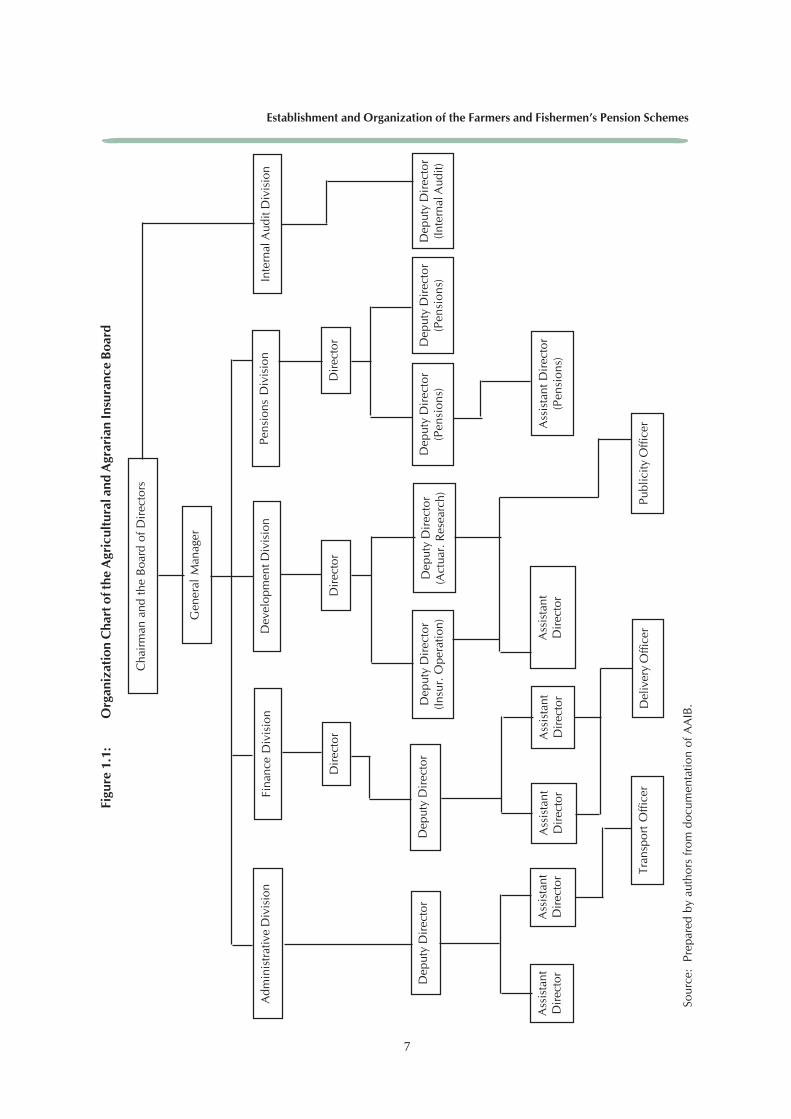

Administrative structure of AAIB

From its commencement, the administrative structureof the Board has consisted of several divisions. Until1997, these comprised:

(i) Administrative Division(ii) Finance Division(iii) Actuarial and Research Division(iv) Insurance Operations Division(v) Livestock Division(vi) Publicity and Training Division(vii) Internal Audit Division(viii) Farmers’ Pensions Division(ix) Fishermen’s Pensions Division

However, this structure has been transformed as aresult of a complete structural re-organization thatwas effected in the year 1997. Consequently, theInsurance Operations Division, the Actuarial andResearch Division and the Livestock InsuranceDivision have been brought under the DevelopmentDivision. Duties, such as implementing andmaintaining the crop and Livestock insurance schemesisland-wide, and handling operational and researchactivities have been put in charge of this division. Atthe same time, the Farmers’ Pension and SocialSecurity Benefit Scheme and the Fishermen’s Pensionand Social Security Benefit Scheme were re-structured,and placed under a merged Pensions Division. Theactivities involving those such as updating andmaintenance of applications and individual accountsof the members of the Schemes, payment of pensions,disability benefits and death gratuities are carried outby the Pensions Division accordingly. Presently, theadministrative structure of the Agricultural andAgrarian Insurance Board comprises five maindivisions:

(i) Administrative Division(ii) Finance Division(iii) Development Division(iv) Pensions Division(v) Internal Audit Division

7

Establishment and Organization of the Farmers and Fishermen’s Pension SchemesFi

gure

1.1

:

O

rgan

izat

ion

Cha

rt o

f the

Agr

icul

tura

l and

Agr

aria

n In

sura

nce

Boa

rd

Sour

ce:

Prep

ared

by

auth

ors

from

doc

umen

tatio

n of

AA

IB.

Cha

irm

an a

nd th

e B

oard

of D

irec

tors

Gen

eral

Man

ager

Inte

rnal

Aud

it D

ivis

ion

Pens

ions

Div

isio

nD

evel

opm

ent D

ivis

ion

Fina

nce

Div

isio

nA

dmin

istr

ativ

e D

ivis

ion

Dep

uty

Dir

ecto

r

Ass

ista

ntD

irec

tor

Ass

ista

ntD

irec

tor Tr

ansp

ort

Offi

cer

Dir

ecto

r

Dep

uty

Dir

ecto

r

Ass

ista

ntD

irec

tor

Ass

ista

ntD

irec

tor

Del

iver

y O

ffice

r

Dir

ecto

r

Dep

uty

Dir

ecto

r(In

sur.

Ope

ratio

n)D

eput

y D

irec

tor

(Act

uar.

Res

earc

h)

Ass

ista

ntD

irec

tor

Publ

icity

Offi

cer

Dep

uty

Dir

ecto

r(P

ensi

ons)

Dep

uty

Dir

ecto

r(P

ensi

ons)

Dir

ecto

r

Dep

uty

Dir

ecto

r(In

tern

al A

udit)

Ass

ista

nt D

irec

tor

(Pen

sion

s)

8

Assessment of the Farmers’ and Fishermen’s Pension and Social Security Benefit Scheme

2. Farmers’ Pension and Social SecurityBenefit Scheme

2.1 Origin and Objectives

The Farmers’ Pension and Social Security BenefitScheme was established in 1987 by Act of ParliamentNo.12 of 1987, and is administered by the Agriculturaland Agrarian Insurance Board. The AAIB estimatesthe farmer community in Sri Lanka to number nearly2 million, of which approximately 10-12 lakhs offarmers are estimated to be eligible for the Scheme,that is, those who are thought to be having thequalifications required for membership. Of thisnumber, more than half, or 675,000 of farmers haveenrolled in the Scheme up to now, whilst the actualnumber of contributors is approximately 4 lakhs.According to its corporate plan for 2002 the AAIBintends to expand the coverage up to 1 million withinthe next 5 years (2002-2007). The current number ofenrolments is seen by it as a satisfactory figure, whenconsidering the fact that the contributions arevoluntary and paid out of pocket by farmers in low-income categories. The Scheme also indirectly seeksto encourage saving habits of the farmers.

2.2 Administration and Staffing

The Farmers’ Scheme is administered and managedby the AAIB. The AAIB is located in Colombo andcarries out activities at District level by way of Districtoffices established in each District. The district officesare headed by Assistant Directors and support staff,consisting of both clerical and field staff. The fieldstaff is made up of Development Officers (DO) andField Officers (FO), who function at grass root level.These officers are assigned different Divisions underDivisional Secretariats (DS). The Development Officersare graduates, whilst the Field Officers are recruitedfrom persons who have passed the Advanced LevelExamination. Currently, there are around 40Development Officers and 100 Field Officersemployed island-wide. Their primary function is topromote the Scheme at village level and enrol farmersto the Scheme.

In addition to the DOs and FOs, who form part ofthe District Office cadre of the AAIB, the promotionaland enrolment activities are also carried out throughthe Agrarian Services Centres (ASC). In each ASC,there are Govi Sevana Niyamakas and AgriculturalResearch and Production Assistants, representing each

Grama Sevaka (GS) Division. Their duties involvedoing AAIB related work, which primarily is topromote activities related to the Scheme throughvillage level meetings etc. The number of officersemployed depends on the number of Grama SevakaDivisions. In the case of Mahaweli Divisions, theactivities are carried out through Divisional Offices.

2.3 Eligibility and Enrolment

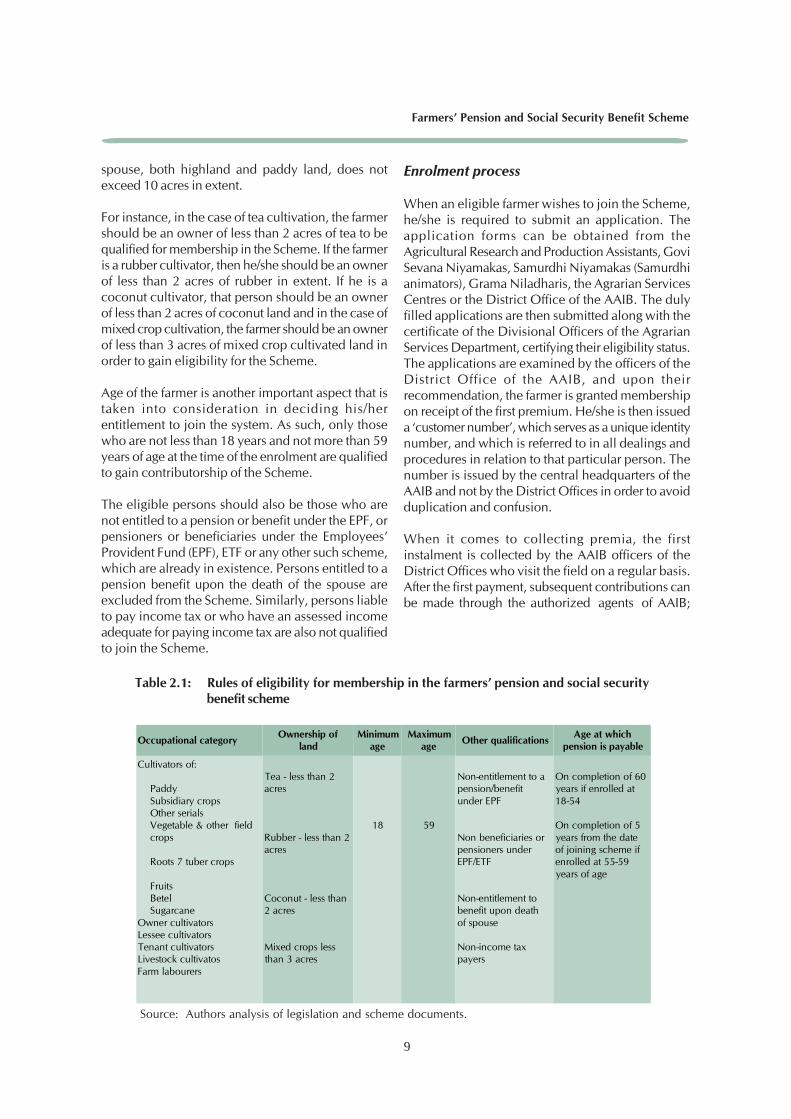

Eligibility

The Scheme targets farmers who are Sri Lankan citizens,both male and female, and whose main source ofsubsistence is agriculture. Not all farmers however,are eligible to join the Scheme, as members arerequired to fulfil certain additional qualifications. Theeligibility criteria are primarily based on the types ofcrop cultivated, the amount of cultivable land ownedor cultivated, age, and non-entitlement to otherbenefit schemes. The additional eligibility criteria arespecified not in the enacting legislation, but insubsequent gazetted regulations.

The primary qualification for a person to be eligiblefor gaining membership of the Scheme is that he/sheshould be a cultivator, whether as owner, lessee ortenant-cultivators. Accordingly, as specified in theregulations (No. 452/12; Gazette 7 of May 1987),farmers engaged in the cultivation of the followingcrops are qualified to join the Scheme; these includefarmers engaged in paddy cultivation, cultivation ofother cereals, subsidiary crop cultivation, vegetablesand cultivation of other field crops, cultivators ofroots and tuber crops, fruits, betel and sugar cane.Those cultivating on the authority of the owner andcertified as farmers by an authorized officer underthe Agrarian Services Act, No. 58 of 1979, the LandDevelopment Ordinance (Chapter 464), or the CrownLands Ordinance (Chapter 454) are also entitled tojoin the Scheme. Apart from these categories, it wasalso opened to persons engaged in livestock farmingwhose main livelihood is animal husbandry, and farmlabourers employed in agricultural crop cultivationor dealing with livestock production with effect fromSeptember 1998 under the new regulations publishedin the Gazette No.522/6 of 7 September 1988.

It is compulsory that the extent of cultivable landowned either by an owner cultivator or by his familydoes not exceed 10 acres in extent in order to beentitled to join the Scheme. It is also required thatthe land cultivated, including those cultivated by the

9

Farmers’ Pension and Social Security Benefit Scheme

spouse, both highland and paddy land, does notexceed 10 acres in extent.

For instance, in the case of tea cultivation, the farmershould be an owner of less than 2 acres of tea to bequalified for membership in the Scheme. If the farmeris a rubber cultivator, then he/she should be an ownerof less than 2 acres of rubber in extent. If he is acoconut cultivator, that person should be an ownerof less than 2 acres of coconut land and in the case ofmixed crop cultivation, the farmer should be an ownerof less than 3 acres of mixed crop cultivated land inorder to gain eligibility for the Scheme.

Age of the farmer is another important aspect that istaken into consideration in deciding his/herentitlement to join the system. As such, only thosewho are not less than 18 years and not more than 59years of age at the time of the enrolment are qualifiedto gain contributorship of the Scheme.

The eligible persons should also be those who arenot entitled to a pension or benefit under the EPF, orpensioners or beneficiaries under the Employees’Provident Fund (EPF), ETF or any other such scheme,which are already in existence. Persons entitled to apension benefit upon the death of the spouse areexcluded from the Scheme. Similarly, persons liableto pay income tax or who have an assessed incomeadequate for paying income tax are also not qualifiedto join the Scheme.

Enrolment process

When an eligible farmer wishes to join the Scheme,he/she is required to submit an application. Theapplication forms can be obtained from theAgricultural Research and Production Assistants, GoviSevana Niyamakas, Samurdhi Niyamakas (Samurdhianimators), Grama Niladharis, the Agrarian ServicesCentres or the District Office of the AAIB. The dulyfilled applications are then submitted along with thecertificate of the Divisional Officers of the AgrarianServices Department, certifying their eligibility status.The applications are examined by the officers of theDistrict Office of the AAIB, and upon theirrecommendation, the farmer is granted membershipon receipt of the first premium. He/she is then issueda ‘customer number’, which serves as a unique identitynumber, and which is referred to in all dealings andprocedures in relation to that particular person. Thenumber is issued by the central headquarters of theAAIB and not by the District Offices in order to avoidduplication and confusion.

When it comes to collecting premia, the firstinstalment is collected by the AAIB officers of theDistrict Offices who visit the field on a regular basis.After the first payment, subsequent contributions canbe made through the authorized agents of AAIB;

Occupational categoryOwnership of

landMinimum

ageMaximum

ageOther qualifications

Age at whichpension is payable

Cultivators of:

Paddy Subsidiary crops Other serials Vegetable & other field crops

Roots 7 tuber crops

Fruits Betel SugarcaneOwner cultivatorsLessee cultivatorsTenant cultivatorsLivestock cultivatosFarm labourers

Tea - less than 2acres

Rubber - less than 2acres

Coconut - less than2 acres

Mixed crops lessthan 3 acres

18 59

Non-entitlement to apension/benefitunder EPF

Non beneficiaries orpensioners underEPF/ETF

Non-entitlement tobenefit upon deathof spouse

Non-income taxpayers

On completion of 60years if enrolled at18-54

On completion of 5years from the dateof joining scheme ifenrolled at 55-59years of age

Table 2.1: Rules of eligibility for membership in the farmers’ pension and social securitybenefit scheme

Source: Authors analysis of legislation and scheme documents.

10

Assessment of the Farmers’ and Fishermen’s Pension and Social Security Benefit Scheme

Cooperative Rural Banks, Agrarian Services Centresin the case of the North Western and Centralprovinces, Cooperative Societies, and through thePeoples’ Bank if the farmers are from the Mahawelisystems.

The procedure of collecting second and successivepremia in the case of the North Western and CentralProvinces through officers of the Agrarian ServicesCentres was launched recently as a new measure,since mid-2002. This is as a part of a pilot projectcarried out by the AAIB to examine the possibilityof collecting instalments through Agrarian ServicesCentres, taking into account the limited AAIB staffavailable and the vast number of areas they arerequired to cover on visits to collect instalments.The pilot project was launched in April 2002 and isongoing. Under the customary arrangements for thecollection of instalments, an AAIB officer issometimes required to cover as many as 10 Divisions.The situation causes inconvenience for both farmersand the officers, on the one hand since the farmersare sometimes unable to meet the officers, as theofficers are often too busy and on the other hand,the officers are unable to meet the farmers on theirvisits. This delays payments and contributes toinefficiency. So far, it is reported by AAIB that thepilot project has proved to be a successful modusoperandi in the attempt to decentralize the premiacollection, which the AAIB intends to expand island-wide. However, the Agrarian Services Centres wouldonly be expected to collect the second and successivepremia, while the first premium would still becollected by the AAIB officers operating throughDistrict Offices.

2.4 Contributions

The rate of contributions is specified by governmentgazette, and may be amended in the same manner.These essentially specify one schedule of standardpayments, which varies according to the age of theenrollee at enrolment, frequency of payment andwhether payment is periodic or one-off. There is novariation in the payment schedule or benefitsavailable to those enrollees who wish to pay morethan the stipulated amount. A notable feature is thatthe schedule of contributions has not been variedsince the inception of the Scheme in 1987.

Once enrolled, the farmer has the choice of payingthe contributions either:

(i) on a regular periodic basis until reaching vestingage (regular basis), or

(ii) as a one-off payment made in the year ofenrolment, with no subsequent payments required(discount basis)

The amount to be contributed and the number ofinstalments are determined according to the age of thecontributor at enrolment.

Regular payment basis

The Farmers’ Scheme is a nominally contributoryScheme, which involves a fixed payment each year byall active enrollees. In return, enrollees who have madeall required contributions are entitled to a pension,which is fixed according to the level of the periodicpayment. The level of the fixed annual contributionis set for each enrollee at the time of the firstcontribution payment, and currently does not varysubsequently.

The standard contribution schedule involves fixedannual or semi-annual payments from the time ofenrolment to the age of eligibility for a pension. Themajority of the members are enrolled on this basis,which amounts to nearly 6 lakhs in number, of which,the actual number of active members under this systemis estimated to be around half of the total numberenrolled currently.

The regular payment system was designed to take intoaccount the fluctuating income of agriculturists withthe seasonal cultivation of Yala and Maha, duringwhich period the prime harvests are reaped and themain income received. Contributors make the annualpayment in the form of two instalments during theyear, and these have to be continued till the age ofsixty. Accordingly, the contributions in the MahaSeason have to be made before 1st of April, and theinstalments for the Yala Season should be paid before1st of October. It is also possible for any farmer to payseveral instalments together at one time, although thisis not compulsory.

The contributions are fixed amounts, the level of whichare based on the age at which the contributor enrols.The fixed amount does not change once the contributorenrols. The older the contributor at the time ofenrolment, the higher the periodic payment is, but theultimate pension payable is also reduced. Table 2.1gives the rate of contribution payments and associatedpension payments.

11

Farmers’ Pension and Social Security Benefit Scheme

For instance, a person who obtains membership atthe age of 18 years has to make a total deposit of Rs.10,920/= in 84 instalments of Rs. 130/= eachbiannually. But a person who joins the Scheme at theage of 54 will have to pay a half-yearly instalment ofRs. 700/= in 12 instalments to be eligible for fullbenefits of the Scheme. The total sum of money thatperson is required to pay will be Rs. 8,400/=.

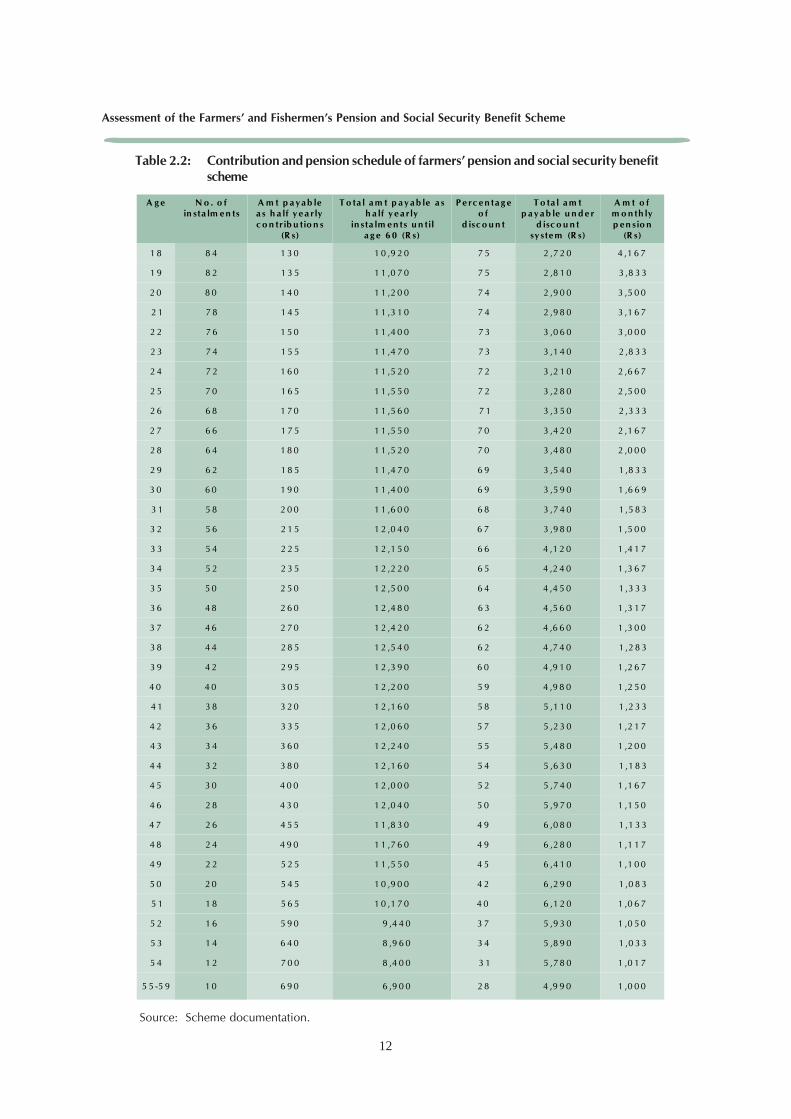

Discount payment basis

Enrollees have the option of making their life-timecontribution in the first year, instead of making regularperiodic payments. If they choose this option, theyare given a discount on the nominal total payment,which can be as much as 75 per cent. As at end of2002, the total number of farmers enrolled on thediscount payment basis remained around 73,000 ofwhich, around 12,000 members have left the Schemeas a result of disability, death and entitlement topension on completion of 60 years of age.

Under the discount system, a contributor has twooptions for making payments:

(i) In the form of an outright deposit of the fulldiscounted sum

(ii) In the form of two or four instalments over aperiod of 12 months

From its inception up to 1999, the Scheme allowedpayments under the discount system only in the formof lump sum contributions. The second option wasintroduced only recently.

Table 2.2 shows the required contributions under thediscount basis compared with the standard paymentschedule. The discounts potentially available on anominal basis are substantial. For example, if a farmerjoins the Scheme at the age of 18, then he/she has tomake a total contribution of Rs. 10,920/=in 84instalments under the regular system at Rs. 130/= ona half yearly basis before he/she becomes entitled todraw a monthly pension on reaching the age of 60years. Instead, if he chooses to pay on the discountbasis, it is possible for him/her to make an outrightpayment of Rs. 2,720/=, which is only 25 per centof the total contribution and obtain complete pensionrights.

However, AAIB reports that this method of paymentis less popular among farmers due to the fact thatmany are incapable of paying bigger amounts due tofinancial constraints. Accordingly, taking into account

these financial difficulties faced by farmers and uponrequests by them, AAIB introduced two other systemsof payments so as to facilitate and encourage lumpsum contributions since 1999. Under these twosystems, a farmer can make the lump sum contributionin two or four instalments within a period of one year.The number enrolled under these two paymentmethods, that is, those paying lump sum in instalments,does not exceed 10,000 in number with 15 per cent ofdefaulters.

Record keeping

Upon payment of the first premium, the contributorsunder the regular payment system and thosecontributing on the divided discount basis are issueda passbook, which they are required to produce whenmaking successive payments. The passbook isimportant as a record of each payment is kept in it,and as the contributor is required to hand it over tothe AAIB on reaching the age of 60 years, when he/she is entitled to draw the pension. The records ofpayments are also kept in the District Office of theAAIB, with a copy being made to the central office.In the event of a lost passbook, a contributor couldobtain a new one by paying an amount of Rs. 25/=.However, no such passbook is issued to farmers whoprefer to obtain the contributorship by making a singlelump sum payment on the discount basis, as it is notnecessary, since the money is paid outright.

Apart from the passbook, every farmer enrolled in thesystem is issued with a policy specifying the termsand conditions of the policy, benefits he/she is entitledto and the contributions to be made by him/her. Thepolicy may be terminated by the AAIB in the instanceof incorrect or untrue information or statementsprovided in the application for enrolment, andwithholding of information. Failure to make duepayments and cessation of qualifications required tojoin the Scheme may also be reasons to end the policyissued to a particular farmer. In addition, a specialdiscount certificate is issued to those who contributeunder the lump sum basis.

In practice, implementation of this system suffers froma number of shortcomings. According to a surveyconducted by the AAIB island-wide in 2002, it wasfound that a significant number of farmers enrolled inthe Scheme are still without the policy or the discountcertificate guaranteed by the AAIB even 15 years afterits inception.

12

Assessment of the Farmers’ and Fishermen’s Pension and Social Security Benefit Scheme

Table 2.2: Contribution and pension schedule of farmers’ pension and social security benefitscheme

Source: Scheme documentation.

A g e N o . o fin sta lm e n ts

A m t p a ya b lea s h a lf y e a rlyc o n tr ib u tio n s

(R s)

T o ta l a m t p a y a b le a sh a lf y e a rly

in sta lm e n ts u n tila g e 6 0 (R s)

P e rc e n ta g eo f

d isc o u n t

T o ta l a m tp a y a b le u n d e r

d isc o u n tsy ste m (R s)

A m t o fm o n th lyp en sio n

(R s)

1 8 8 4 1 3 0 1 0 ,9 2 0 7 5 2 ,7 2 0 4 ,1 6 7

1 9 8 2 1 3 5 1 1 ,0 7 0 7 5 2 ,8 1 0 3 ,8 3 3

2 0 8 0 1 4 0 1 1 ,2 0 0 7 4 2 ,9 0 0 3 ,5 0 0

2 1 7 8 1 4 5 1 1 ,3 1 0 7 4 2 ,9 8 0 3 ,1 6 7

2 2 7 6 1 5 0 1 1 ,4 0 0 7 3 3 ,0 6 0 3 ,0 0 0

2 3 7 4 1 5 5 1 1 ,4 7 0 7 3 3 ,1 4 0 2 ,8 3 3

2 4 7 2 1 6 0 1 1 ,5 2 0 7 2 3 ,2 1 0 2 ,6 6 7

2 5 7 0 1 6 5 1 1 ,5 5 0 7 2 3 ,2 8 0 2 ,5 0 0

2 6 6 8 1 7 0 1 1 ,5 6 0 7 1 3 ,3 5 0 2 ,3 3 3

2 7 6 6 1 7 5 1 1 ,5 5 0 7 0 3 ,4 2 0 2 ,1 6 7

2 8 6 4 1 8 0 1 1 ,5 2 0 7 0 3 ,4 8 0 2 ,0 0 0

2 9 6 2 1 8 5 1 1 ,4 7 0 6 9 3 ,5 4 0 1 ,8 3 3

3 0 6 0 1 9 0 1 1 ,4 0 0 6 9 3 ,5 9 0 1 ,6 6 9

3 1 5 8 2 0 0 1 1 ,6 0 0 6 8 3 ,7 4 0 1 ,5 8 3

3 2 5 6 2 1 5 1 2 ,0 4 0 6 7 3 ,9 8 0 1 ,5 0 0

3 3 5 4 2 2 5 1 2 ,1 5 0 6 6 4 ,1 2 0 1 ,4 1 7

3 4 5 2 2 3 5 1 2 ,2 2 0 6 5 4 ,2 4 0 1 ,3 6 7

3 5 5 0 2 5 0 1 2 ,5 0 0 6 4 4 ,4 5 0 1 ,3 3 3

3 6 4 8 2 6 0 1 2 ,4 8 0 6 3 4 ,5 6 0 1 ,3 1 7

3 7 4 6 2 7 0 1 2 ,4 2 0 6 2 4 ,6 6 0 1 ,3 0 0

3 8 4 4 2 8 5 1 2 ,5 4 0 6 2 4 ,7 4 0 1 ,2 8 3

3 9 4 2 2 9 5 1 2 ,3 9 0 6 0 4 ,9 1 0 1 ,2 6 7

4 0 4 0 3 0 5 1 2 ,2 0 0 5 9 4 ,9 8 0 1 ,2 5 0

4 1 3 8 3 2 0 1 2 ,1 6 0 5 8 5 ,1 1 0 1 ,2 3 3

4 2 3 6 3 3 5 1 2 ,0 6 0 5 7 5 ,2 3 0 1 ,2 1 7

4 3 3 4 3 6 0 1 2 ,2 4 0 5 5 5 ,4 8 0 1 ,2 0 0

4 4 3 2 3 8 0 1 2 ,1 6 0 5 4 5 ,6 3 0 1 ,1 8 3

4 5 3 0 4 0 0 1 2 ,0 0 0 5 2 5 ,7 4 0 1 ,1 6 7

4 6 2 8 4 3 0 1 2 ,0 4 0 5 0 5 ,9 7 0 1 ,1 5 0

4 7 2 6 4 5 5 1 1 ,8 3 0 4 9 6 ,0 8 0 1 ,1 3 3

4 8 2 4 4 9 0 1 1 ,7 6 0 4 9 6 ,2 8 0 1 ,1 1 7

4 9 2 2 5 2 5 1 1 ,5 5 0 4 5 6 ,4 1 0 1 ,1 0 0

5 0 2 0 5 4 5 1 0 ,9 0 0 4 2 6 ,2 9 0 1 ,0 8 3

5 1 1 8 5 6 5 1 0 ,1 7 0 4 0 6 ,1 2 0 1 ,0 6 7

5 2 1 6 5 9 0 9 ,4 4 0 3 7 5 ,9 3 0 1 ,0 5 0

5 3 1 4 6 4 0 8 ,9 6 0 3 4 5 ,8 9 0 1 ,0 3 3

5 4 1 2 7 0 0 8 ,4 0 0 3 1 5 ,7 8 0 1 ,0 1 7

5 5 -5 9 1 0 6 9 0 6 ,9 0 0 2 8 4 ,9 9 0 1 ,0 0 0

13

Farmers’ Pension and Social Security Benefit Scheme

The survey was carried out island-wide from April toJune 2002, covering all districts with a total sampleof 276,039 farmers, which was 42 per cent of thetotal number of enrollees at the time (657,860). Ofthis sample, 69,106 (25 per cent of the sample) hadnot been issued with policies, while another 20,478(7.4 per cent) had not obtained the discount certificateat the time of the survey. However, in recent effortsto minimize this backlog, the AAIB has succeededin resolving the problem to a large extent.

2.5 Pension and Social Security Benefits

The Farmers’ Pension and Social Security BenefitScheme consists of two components:

(i) A pension scheme(ii) A social security benefit scheme.

The pension scheme aims at providing old age incomesecurity, while the primary objective of the socialsecurity benefit component is to provide groupinsurance in event of trouble, so as to help themmaintain life in normal conditions.

Standard pension entitlement

Under the pension scheme, the contributors areentitled to a monthly pension on completion of 60years of age, which is paid until death. However, afarmer joining the scheme at 55-59 will be entitledto a pension only upon paying the entire contributionas prescribed and on completion of 5 years from thedate of joining the Scheme. By the end of 2002, thenumber of farmers receiving the benefit of a pensionamounted to 14,271, showing a steady increase inthe number of pensioners since the beginning ofpension payment in 1992, with only 567 of farmersdrawing a pension in that year. No enrollees hadbeen eligible prior to 1992, as none had completedthe necessary vesting period of 5 years.

Presently, the pension entitlement ranges from aminimum of Rs. 1,000/= up to Rs. 4,166/= amonth, depending on the age of contributor at thetime of enrolment, and the contributions to be paidaccording to age.

At the commencement of the Scheme the minimumpension was set as Rs. 200/=, but the maximumpension has not been changed from Rs. 4,166/= permonth. The change was effected via two successivegazette amendments to the Scheme’s regulations. Thefirst gazette amendment increased the minimum

pension to Rs. 500/= per month. Later it was againincreased to Rs. 1,000/= in 1995. This was as partof a restructuring process of the Scheme, which waslaunched during this year under the guidance andadvice of the Minister of Agriculture, Land andForestry, with a view to providing better pensionbenefits and agricultural insurance. Accordingly,during the year 1995, a number of changes wereintroduced to the Farmers’ Pension and Social SecurityBenefit Scheme in accordance with prescriptions andrecommendations made by a Special Committeeappointed by the Minister to consider the possibilityof expanding the Scheme. Among these changes werethe steps taken to increase the minimum monthlypension up to Rs. 1,000/= which has been in effectsince then.

It is critical to note that the increase in the minimumpension payment, which also involved compressingthe schedule of pension entitlements by age, wasnot accompanied by any change in the contributionschedule. In effect, these changes have resulted inunfunded increases in the liabilities of the Scheme.AAIB officials are aware of the financial implicationsof the changes, but the changes must be seen as policydecisions made at the political level.

Reduced pension entitlement

A farmer is entitled to a full pension only uponpayment of all the contributions. However, if thetotal of half-yearly instalments paid is at least 75 percent of the total amount required to have been paid,then he/she is eligible for a reduced pension. In theevent that the total amount of contributions made isless than 75 per cent but more than 10 per cent, thecontributor has the opportunity of reclaiming themoney, but only upon expiry of the period for payingcontributions. As such, a contributor can obtain arefund of the entire amount of net contributions he/she had made along with interest on reaching theage of 60 years. If a particular contributor has failedto pay at least 10 per cent of the required amount ofcontributions, no refund of money is possible, inwhich case the money remains in the fund.

Survivor benefits

Originally, the Farmers’ Pension and Social SecurityBenefit Act also made provisions for the spouse of adeceased contributor after his/her pension becomesdue, to be entitled to the balance payment thatremained after deducting what is paid as pension.That is, if the deceased contributor, after his/her

14

Assessment of the Farmers’ and Fishermen’s Pension and Social Security Benefit Scheme

pension becomes due, has not drawn at least thetotal amount of his/her net contributions and theinterest thereon as a periodical pension, then thebalance lying to his/her credit excluding theGovernment subsidy can be claimed by his/her legalheir within a period of 1 year. However, if thedeceased pensioner had already drawn an amountequivalent to the sum of his net contributions andthe interest while alive, the surviving heir will notbe entitled to any payment since there is no balancelying in his/her credit.

Changes that were introduced in 1995 brought forthan important amendment in this regard, whereby aBoard decision was made to pay the full pension tothe heir of the deceased instead of the balancepayment, if there is any, but only till the deceasedreaches the age of 80 years. There is no difference inthe pension which is passed on to the survivingspouse from the pension received by the pensionerwhile alive, and there is no necessity for him/her topay an extra contribution to be eligible for this benefit.

Source: AAIB administration data.

This decision to pay the pension to the heir till up tothe year the deceased completes 80 years is primarilyafter considering the cost of pension payments. Thepension is calculated for 20 years from age of 60after reviewing actuarial evaluations and financialviability of the fund in payment of pensions. Already

if the pensioner continues to live after completion of80 years of age, the pension paid to him/her is paidfrom the share of the government subsidy in reality.Under these circumstances, the continuation of thepayment of pension afterwards to the spouse will bean additional cost, since he/she may not be acontributor, and since the money will have to bedrawn from the government subsidy.

Social security benefits

In addition to provision of a pension at the age of 60years, the Farmers’ Scheme provides a number of otherinsurance benefits. These consist of:

(i) Disability benefit(ii) Disablement gratuity(iii) Death gratuity

These benefits are paid out of a separate social securitybenefit fund, which receives Rs. 60/= per yeardeducted from each contributor’s periodiccontributions. Apart from this fixed amount ofRs.5/= per month deducted from the contributions,the members are not required to make any extrapayment to be entitled to these benefits. The Schemeis organized nominally as a collective insurance fund.As of end of 2002, the Scheme had paid out Rs.21,404,000/= as disability benefits for 887 disabledmembers either partially or permanently.

At the inception of the Scheme, the benefits providedunder this system comprised only a disablementgratuity, a death gratuity and a life insurancecoverage. Subsequently, an advance payment in theevent of death and an increase in the amount paidunder the life insurance coverage (up to Rs.25,000/=) have been made available to the memberssince 1995.

When the Scheme first came into force in 1987, theRegulation to the Act published in the Gazette(Gazette No. 452/12 of May 7, 1987) provided onlythe contributors between the age group of 18-54 yearsto be entitled for the benefits granted by the socialsecurity scheme (Regulation 20). As a result, farmersjoining the Scheme at the age group of 55-59 werenot eligible for the benefits under this regulation.However this regulation was amended by anotherGazette notification (Gazette No. 522/6 of September7, 1988) thereby enabling those contributors who arebetween the age group of 55-59 also to benefit fromthe social security benefits.

Year No. of pensioners Rs. paid as pension

1992 567 1,711,500

1993 1,137 6,598,702

1994 1,546 14,570,491

1995 2,177 27,763,881

1996 3,643 59,135,217

1997 4,758 109,813,301

1998 5,566 172,405,250

1999 6,712 246,604,072

2000 7,967 335,189,272

2001 10,366 116,202,030

2002 14,271 679,073,598

Table 2.3: Number of pensioners and amountpaid as pension

15

Farmers’ Pension and Social Security Benefit Scheme

Disablement benefit

The disablement benefit provided is of two types. Itconsists of:

(i) a permanent and partial disablement benefit,and

(ii) a permanent and total disablement benefit

(i) Permanent and partial disablement benefit

The permanent and partial disablement benefit is paidto a member if he/she suffers the following losses asa result of accident or sickness:

• Loss of sight in one eye• Loss or permanent disability of one hand• Loss of one leg or permanent disability in one leg

In the event that a contributor suffers above losses,two options are provided to him/her. It is eitherpossible for him/her to claim a disablement gratuityand leave the Scheme or to continue to remain in theScheme if he/she so wishes. If the contributor takesthe first option available to him/her, he/she can claima permanent and partial disablement benefit up toRs. 25,000/= depending on the age. The disablementbenefit paid in this instance consists of the totalamount of disablement gratuity specified accordingto the age, the net contributions he/she has made tothe Scheme and the nominal interest accrued. Underthis provision, the contributor can claim the gratuityonly once on the occurrence of the above losses.

If the contributor chooses to remain in the Schemeeven after being rendered disabled, he/she has theoption to do so without further contributing to theScheme provided that he/she does not draw thedisablement gratuity otherwise due to him/her underthe first option. In the instance, where he/she opts toremain in the Scheme, he/she is entitled to receivean allowance (pension) when it becomes due at age60. The contributors, who choose this option, thenare required to appeal to the Board with a request toconsider payment of such an allowance. Once suchan appeal is made, the Board would grant permissionenabling the contributor to further remain in theScheme without any more contributions and to receivea pension when it becomes due on reaching the ageof 60 until death. The allowance depends on the ageand the total amount due to the person up to then.The contributor has the full freedom to decide betweenthe two options.

(ii) Permanent and total disablement benefit

When a member of the Scheme is rendered disabledpermanently and totally, he/she is entitled tosomewhat similar benefits available to permanentlyand partially disabled contributors. A contributorwould be deemed as permanently and totally disabledif he/she suffers the following damages as a result ofaccident or sickness:

• Loss of both hands or permanent disability of bothhands

• Loss of both legs or permanent disability of bothlegs

• Loss of sight in both eyes• Loss of one hand or permanent disability of one

hand and loss of one leg or permanent disabilityof one leg

• Loss of a leg or permanent disability of one legand loss of vision in one eye

• Loss of one hand or permanent disability of onehand and loss of vision in one eye

• Complete paralysis from the neck downwards

As in the case of the permanent and partial disability,the contributors, who are disabled permanently andtotally, are also given the same options. As such,they have the option to either remain in the Schemeor obtain the lump sum disablement gratuity availableto them and drop out of the Scheme.

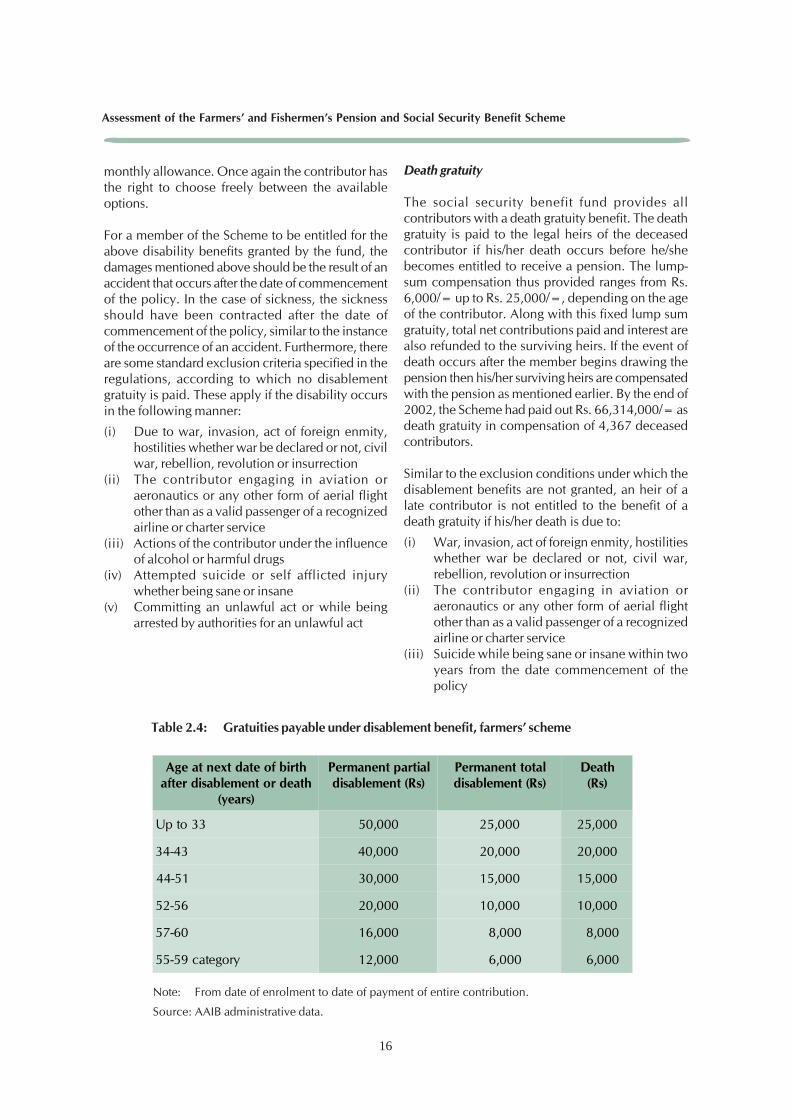

If a particular contributor chooses to claim the gratuityhe can claim a gratuity up to Rs. 50,000/=, plus thenet contributions paid to date and the interestnominally accrued. The compensation provided forthis category is higher than what is given to thepermanently and partially disabled members as seenin Table 2.4. As in the previous instance, the gratuityis payable only once on the occurrence of the damagesspecified above.

If the contributor prefers to remain in the Schemeinstead of claiming the gratuity due to him, he/shecould receive a monthly disablement allowancewithout making further contributions. The allowanceis paid from the date of disablement until death. Theallowance due to the person is calculated taking intoconsideration the amount of contributions he/she hadmade up to the time of disablement and the age ofthe contributor. As in the above case, if thecontributor chooses to remain in the Scheme he/shemust appeal to the Board to pay him/her a monthlyallowance, after which the Board can permit him tocontinue to stay in the Scheme and receive the

16

Assessment of the Farmers’ and Fishermen’s Pension and Social Security Benefit Scheme

monthly allowance. Once again the contributor hasthe right to choose freely between the availableoptions.

For a member of the Scheme to be entitled for theabove disability benefits granted by the fund, thedamages mentioned above should be the result of anaccident that occurs after the date of commencementof the policy. In the case of sickness, the sicknessshould have been contracted after the date ofcommencement of the policy, similar to the instanceof the occurrence of an accident. Furthermore, thereare some standard exclusion criteria specified in theregulations, according to which no disablementgratuity is paid. These apply if the disability occursin the following manner:

(i) Due to war, invasion, act of foreign enmity,hostilities whether war be declared or not, civilwar, rebellion, revolution or insurrection