Assessing Market Potential of NFC for Mobile Payments in 2012 From Swiping to Waving

37

ASSESSING MARKET POTENTIAL OF NFC FOR MOBILE PAYMENTS IN 2012: FROM SWIPING TO WAVING September 2011

-

Upload

vousfaitechier -

Category

Documents

-

view

14 -

download

0

Transcript of Assessing Market Potential of NFC for Mobile Payments in 2012 From Swiping to Waving

ASSESSING MARKET POTENTIAL OF NFC FOR MOBILE PAYMENTS IN 2012: FROM SWIPING TO WAVING

September 2011

INTRODUCTION

NEAR FIELD COMMUNICATIONS (NFC)

MOBILE PHONES AS THE DIGITAL WALLET

CRITICAL SUCCESS FACTORS

MARKETS READY FOR NFC MOBILE

PAYMENT 2012

© Euromonitor International PASSPORT 3 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

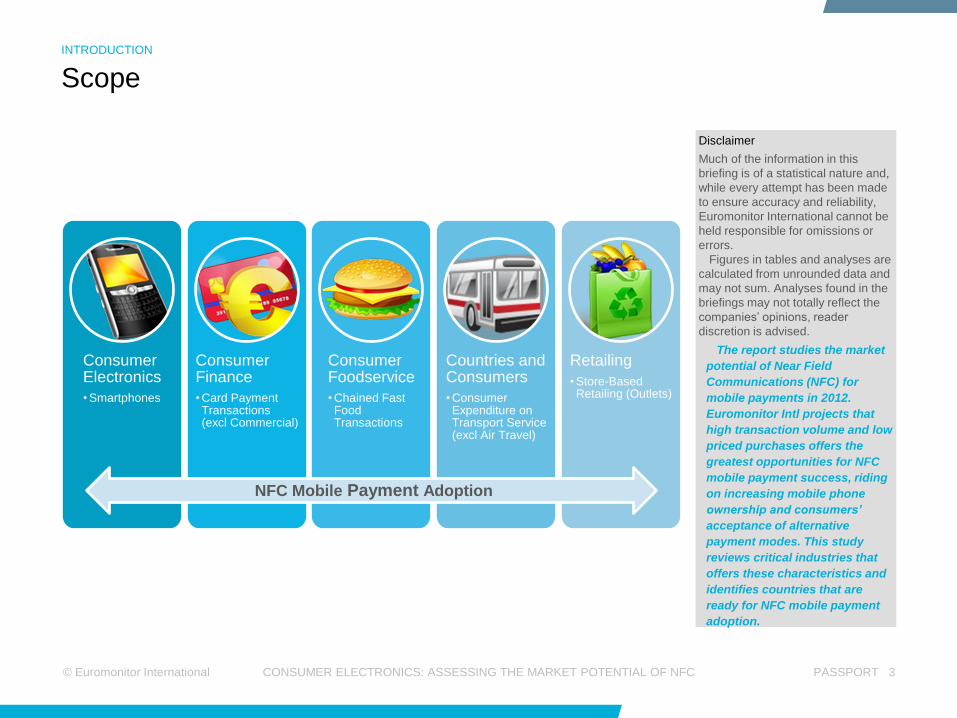

Disclaimer

Much of the information in this

briefing is of a statistical nature and,

while every attempt has been made

to ensure accuracy and reliability,

Euromonitor International cannot be

held responsible for omissions or

errors.

Figures in tables and analyses are

calculated from unrounded data and

may not sum. Analyses found in the

briefings may not totally reflect the

companies‘ opinions, reader

discretion is advised.

The report studies the market

potential of Near Field

Communications (NFC) for

mobile payments in 2012.

Euromonitor Intl projects that

high transaction volume and low

priced purchases offers the

greatest opportunities for NFC

mobile payment success, riding

on increasing mobile phone

ownership and consumers’

acceptance of alternative

payment modes. This study

reviews critical industries that

offers these characteristics and

identifies countries that are

ready for NFC mobile payment

adoption.

Scope

INTRODUCTION

Consumer Electronics

• Smartphones

Consumer Finance

• Card Payment Transactions (excl Commercial)

Consumer Foodservice

• Chained Fast Food Transactions

Countries and Consumers

• Consumer Expenditure on Transport Service (excl Air Travel)

Retailing

• Store-Based Retailing (Outlets)

NFC Mobile Payment Adoption

© Euromonitor International PASSPORT 4 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

The core objective of this report is to review the potential for the mobile phone to become the new digital

wallet through the adoption of Near Field Communications (NFC) in 2012.

NFC is a secure, short-range radio technology, which enables communication between a reader and a

NFC tag when placed close to one another. This in turns, allows for simplified and time-efficient

transactions, data exchange and connections.

The following industries have been selected as case studies due to their inherent characteristics that befits

NFC usage:

Consumer Electronics

Consumer Finance

Consumer Foodservice

Countries and Consumers

Retailing

For NFC mobile payments to potentially succeed, Euromonitor International projects that high transaction

volume, low value purchases inherent in the above industries offers the highest potential for mass NFC

mobile payment adoption. Other success factors includes the widening ownership of mobile phones, the

presence of built-up Infrastructure such as the number of retail outlets and consumer behavior towards the

usage of card payments vs alterative payment modes.

In addition, this report examines all the critical success variables and identifies countries with the highest

potential for NFC mobile payment adoption in 2012.

Objectives

INTRODUCTION

© Euromonitor International PASSPORT 5 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Key findings

INTRODUCTION

Government-backed

initiatives key to success

A top-down push from the government, especially for public transport systems,

holds the key to the potential success of NFC mobile payments.

Company-backed initiatives

limited in impact

Consumers are generally not keen to have different versions of mobile

payments for different products/services/companies, as they typically

encounter inter-operability difficulties and are confusing in application.

High volume, low value

transactions

High volume, low value transactions such as those apparent in fast food

services and public transportation offer the highest potential for mobile

payments.

Consumers eager for

mobile payment

Interestingly, consumers in developing markets are more receptive to and

eager to adopt mobile payments than consumers from developed markets,

due to a lack of existing payment options.

Implementation not costly Cost of implementation lies largely in the installation of payment terminals for

retailers, since consumers can convert their existing mobile phones to be

NFC-enabled at a minimal additional cost.

Lack of common standard The lack of an industry-wide standard will be a major growth obstacle if

consumers are unable to enjoy a seamless usage experience.

Security concerns must be

addressed

Consumers are skeptical of alternative payment options and are concerned

with theft and fraud. Putting into place security safety measures and frequent

consumer education programmes will be critical to the success of mobile

payments.

INTRODUCTION

NEAR FIELD COMMUNICATIONS (NFC)

MOBILE PHONES AS THE DIGITAL WALLET

CRITICAL SUCCESS FACTORS

MARKETS READY FOR NFC MOBILE

PAYMENT 2012

© Euromonitor International PASSPORT 7 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Payment

For mobile payments as a replacement for

credit/prepaid cards and to store credit/bank

information.

Ticketing

To purchase and add stored value to the tickets to

access transportation gates and gain event entry.

Sharing

To aid the transfer of documents and content

across electronic devices.

Service initiation

To activate a service on another device, which

allows for data transfer, to gain access to websites

and discounts on smart posters, amongst others.

Pairing

To establish Bluetooth connection by bringing

devices to ―NFC hotspots‖, by configuring networks

automatically between a pair of Wi-Fi devices.

NFC technology can be used for a wide variety of applications, especially in high volume and low value

transactions. This includes the use of NFC;

NFC and the Ecosystem

NEAR FIELD COMMUNICATIONS (NFC)

NFC Ecosystem

Payment

Ticketing

Sharing Service Initiation

Pairing

© Euromonitor International PASSPORT 8 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Globally, consumers are well acquainted with the use of cards for payments, which often offers point

rewards for usage. Typically, cards are used for big ticket purchases while low priced transactions are

currently paid for in cash. Hence, NFC mobile payment offers as an attractive cashless alternative.

A significant advantage of NFC mobile payment over cash and card payment is the speed of transaction.

Consumers just tap or wave the NFC mobile gadget and payments will be transferred instantly.

For mass adoption, high transactional volume will be crucial to make up for the low priced purchases.

Train station and retail points, as detailed in the below chart, are just two examples that showcases the

high potential usage of NFC mobile payment due to the high volume, low priced transactions for train

commuters and shoppers respectively.

Train Station

Gantry entry

Payment

Vehicle

Driver licence

Payment

Office

Enter/exit office

Exchange business cards

Computer login

Retail

Payment

Loyalty points

Discount coupons

NFC Mobile payment application

NEAR FIELD COMMUNICATIONS (NFC)

PASSPORT 9

NFC trials have been undergoing in many

countries for some time now, by both

governments and private sectors. However,

actual country-wide implementation has been

limited, due to low consumer acceptance, cost

of nationwide implementation and technology

sophistication limitations.

Case studies: Actual implementation still low

NEAR FIELD COMMUNICATIONS (NFC)

PASSPORT 10

Transport operators and authorities are

cooperating to create a national ticketing system,

by combining Touch&Travel and HandyTicket.

Touch&Travel is a mobile ticketing scheme

initiated in 2008 and which has expanded to a

Touch&Travel iPhone app in January 2011.

There are plans to implement the NFC software

into the Android operating system, which will

accelerate NFC penetration on mobile phones.

HandyTicket works similar to Touch&Travel.

China Unicom launched a commercial NFC service

in Beijing, following extensive field testing in the

Chinese capital and in the cities of Shanghai,

Guangzhou and Chongqing.

Commuters can use their mobile phones to make

payments on public transport services and at more

than 2,000 other businesses.

Users can continue using their current mobile

phones, with just the need of upgrading to a new

subscriber identification module (SIM) card with the

NFC module integrated.

Australian bank ANZ completed a mobile wallet

service trial in April 2011. This system requires

consumers to use an iPhone case that contains an

NFC-enabled microSD (secure digital) card.

As reported, 90% of the participants in the trial

found that the technology either met or exceeded

their expectations and needs. However, ANZ Bank

preferred the NFC functionality to be embedded in

the mobile phones rather than the external case

that had to be used during the trial.

Mobile operator Orange and Barclays Bank jointly

launched NFC mobile payment services in May

2011. Presently, it only works with the 2G

Samsung S5230.

Payments are limited to purchase below £15 while

the service is available at more than 50,000 stores.

Participating merchants include high transacting

food operators such as McDonald‘s and Subway.

Australia - Retailing UK - Retailing

China - Transportation Germany - Transportation

Case studies: NFC trials and implementations

NEAR FIELD COMMUNICATIONS (NFC)

PASSPORT 11

Fans of music band Faithless tested the NFC

system, which allows them to exchange contacts

and interact with one another via Facebook.

Held during the PIAS Nites festival in March 2011,

fans were given NFC tagged cards and they could

post on Facebook pictures taken in NFC-enabled

photobooths.

This system also offers the fans access to games,

contests and digital media.

Finnish start-up company, 6Starz, unveiled a new

social networking service, based on NFC and

Quick Response code, with the latter allowing for

convenience-oriented applications.

Customers can check in and make friend

connections by touching two NFC phones together

as well as make mobile coupon claims.

Pilot testing of 6Starz service continues to run, with

results expected in the last quarter of 2011.

Google Wallet and Google Offers was launched in

May 2011, with more than 300,000 merchants

country-wide such as Macy‘s and Dairy Queen

providing tap-and-pay terminals.

This system also allows consumers to store all

their credit card details and to receive information

of their current location, such as F&B promotions.

Google Wallet expects up to one-third of the retail

stores in the country to provide NFC mobile

payment services in the next one year of launch.

Think&Go NFC system allows consumers to enjoy

interactive shopping. Mobile services include

instant access to product information, personalised

marketing advice and couponing. Shoppers will

also be alerted to products, according to

purchasing habits, needs and allergies.

Retailers, such as Carrefour and Casino, can

collect shoppers‘ information and analyse detailed

consumer activity to develop retailing strategies.

US - Retailing France - Retailing

Finland - Social Networking/Foodservice Belgium - Music/Networking

Case studies: NFC trials and implementations

NEAR FIELD COMMUNICATIONS (NFC)

© Euromonitor International PASSPORT 12 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Based on the earlier review of NFC trials and

implementations, three key elements that must exist

for NFC mobile payment to take off are:

NFC enabled smartphones

Mobile phone manufacturers are generally

reluctant to implement NFC functionality as it

increases handset costs and consumers‘ lament of

a lack of a good range of NFC enabled

smartphones.

As a vicious cycle, the limited consumer usage is

also a key factor in not offering NFC functionality.

Retailers providing NFC mobile payment terminals

Retailers typically cited a lack of consumer demand

for not readily providing NFC terminals.

NFC payment option also competes with the in-

house store cards offered by established retailers

such as Isetan, which gives the latter access to

shopper details and purchasing habits.

Consumers‘ confidence in NFC mobile payment

Consumers‘ ready acceptance of a new payment

mode, with concerns of security well addressed.

Section summary

Currently, NFC mobile payment is caught in a

situation where all parties – consumers, retailers

and manufacturers – are waiting for each other to

bolster the technology adoption and application.

Despite this stalemate, the general consensus is

when, rather than if, NFC payment will take off.

The following slides underpins the importance of

mobile phones and identify critical success factors

that address the concerns and actions of

manufacturers, retailers and consumers in 2012.

The waiting game: Manufacturers, retailers and consumers

NEAR FIELD COMMUNICATIONS (NFC)

NFC enabled smartphones

Retailers’

acceptance

Consumer usage

INTRODUCTION

NEAR FIELD COMMUNICATIONS (NFC)

MOBILE PHONES AS THE DIGITAL WALLET

CRITICAL SUCCESS FACTORS

MARKETS READY FOR NFC MOBILE

PAYMENT 2012

© Euromonitor International PASSPORT 14 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Having identified the key parameters that must

exist for NFC mobile payments to successful take

off, we now explore how and why mobile phones

can become the new digital wallet. This implies that

consumers can leave their homes with basically

nothing but just their mobile phones in hand.

A quick review of the compelling statistics in

Euromonitor‘s various researched industries,

captured on the right, paints a rosy picture for the

growth and penetration of NFC mobile payments.

Specifically in the following slide, we will be

exploring how mobile phones are evolving to be

the one most critical consumer electronics item of

ownership and where penetration of mobile phone

subscriptions in less developed pockets are

robustly gaining momentum, if not, already on par

with developed markets.

Over the 5 year period of 2011-2015, smartphones

will become the top product choice for new

purchases (as opposed to feature phones) and

increase its percentage contribution significantly as

a total of mobile phone sales globally.

75% of the world‘s population will possess mobile phone subscriptions in 2012

28% the world‘s population will have a credit card in 2012

1,502 million new mobile phones sales in 2012

Key consumer statistics

MOBILE PHONES AS THE DIGITAL WALLET

© Euromonitor International PASSPORT 15 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Key Point: Globally, mobile phones have emerged

as the most important electronic product of

ownership, with mobile phone subscriptions in

developing markets such as Brazil being on a par

with, if not higher, than developed Western Europe.

Especially in developing markets, the first time a

consumer accesses the internet could be via a

mobile phone rather than a computer.

Mobile phones an integral part of consumer lifestyles

MOBILE PHONES AS THE DIGITAL WALLET

Mobile Phone Subscriptions (Per capita) 2010/2015

2010 2015

Eastern Europe 1.4 1.5

Western Europe 1.2 1.3

Australasia 1.1 1.2

Latin America 1.0 1.0

North America 1.0 1.0

Asia Pacific 0.6 0.7

Middle East and Africa 0.6 0.7 0

450,000

900,000

1,350,000

1,800,000

2011 2012 2013 2014 2015

Global Retail Volume 2011-2015 (‗000)

Smartphones Feature Phones

Global Retail Volume 2012

Smartphones

Feature Phones

© Euromonitor International PASSPORT 16 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Beyond mobile phone ownership, an online poll by Accenture shows that consumers in developing markets

such as India and China are more receptive to mobile payments than consumers in developed markets,

such as in Europe and the US.

Mobile payment gaining acceptance in developing markets

MOBILE PHONES AS THE DIGITAL WALLET

China

Yes

No

India Brazil

US and Europe Japan South Korea

Source: Accenture online poll of consumers indicating if they favour using mobile phones for most payments

© Euromonitor International PASSPORT 17 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

0% 25% 50% 75% 100%

Germany

Japan

South Korea

France

UK

US

Brazil

China

India

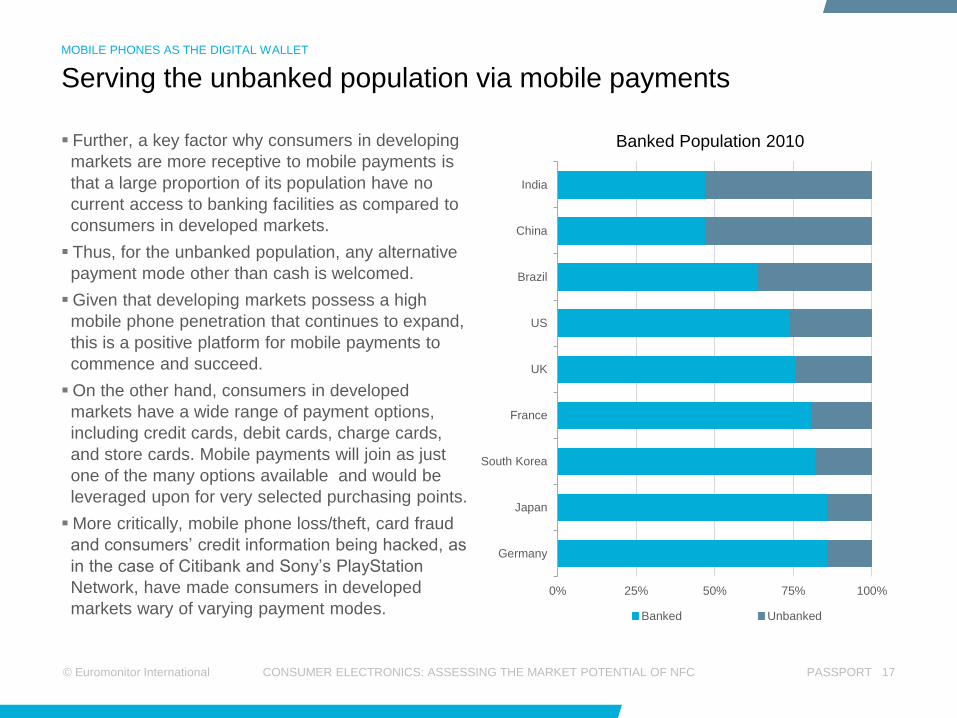

Banked Population 2010

Banked Unbanked

Further, a key factor why consumers in developing

markets are more receptive to mobile payments is

that a large proportion of its population have no

current access to banking facilities as compared to

consumers in developed markets.

Thus, for the unbanked population, any alternative

payment mode other than cash is welcomed.

Given that developing markets possess a high

mobile phone penetration that continues to expand,

this is a positive platform for mobile payments to

commence and succeed.

On the other hand, consumers in developed

markets have a wide range of payment options,

including credit cards, debit cards, charge cards,

and store cards. Mobile payments will join as just

one of the many options available and would be

leveraged upon for very selected purchasing points.

More critically, mobile phone loss/theft, card fraud

and consumers‘ credit information being hacked, as

in the case of Citibank and Sony‘s PlayStation

Network, have made consumers in developed

markets wary of varying payment modes.

Serving the unbanked population via mobile payments

MOBILE PHONES AS THE DIGITAL WALLET

INTRODUCTION

NEAR FIELD COMMUNICATIONS (NFC)

MOBILE PHONES AS THE DIGITAL WALLET

CRITICAL SUCCESS FACTORS

MARKETS READY FOR NFC MOBILE

PAYMENT 2012

© Euromonitor International PASSPORT 19 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

The opportunity for wide-spread NFC mobile payment

adoption lies in its offer of convenience and time efficiencies

in payment transfer.

For many individuals, mobile phone is the most important

item to have on hand when out of home. Accordingly, the

growth vision for NFC mobile payment is for individuals to

just bring their NFC embedded mobile phones when out,

negating the need to bring along one‘s wallet or to wait in

slow moving queues.

In this and the subsequent slides, Euromonitor International

identifies industries like fast food and public transport that

can capitalize on the convenience factor of NFC mobile

payment by converting cash payments for high volume, low

value transactions into mere waves.

Importantly, factors like the availability of smartphones,

number of retail outlets and cash payment transactions will

be thoroughly discussed while identifying potential countries

ready for NFC mobile payment adoption.

In addition, accompanying analysis will draw attention to

the trends and developments on selected countries for each

industry, with an emphasis on developing markets, rather

than advanced markets like the US and UK.

Critical success factors

CRITICAL SUCCESS FACTORS

Consumers using NFC payment

Chained fast food transactions

Expenditure on land transport

Retailers‘ acceptance of NFC payment

Number of retail outlets

Card payment transactions

NFC enabled smartphones

Smartphones sales

© Euromonitor International PASSPORT 20 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

The availability of smartphones will spur the adoption of NFC mobile

payments and Euromonitor International‘s projection of the top 15

markets for smartphone sales in 2012 draws to attention the strong

presence of developing countries in this list.

A critical catalyst for the penetration of smartphones in China stems

from the Chinese government's effort to consolidate mobile network

operators (MNOs), which sees them investing in 3G infrastructure and

improving coverage, rather than price-cutting each other.

AT&T‘s acquisition of its rival T-Mobile will trigger a 4G price war with

Verizon and Sprint, propelling smartphone sales in the US.

Brazil and Mexico‘s strong smartphones sales is due to the countries'

reviving economic growth and improving income levels, smartphone

deals targeted at low-income consumers and growing mobile internet.

India‘s strong local mobile phone manufacturers such as Micromax and

Spice and having the world‘s lowest call rates are incentives to launch

smartphones to increase hardware sales and data revenue.

Russia‘s Yota is the sole 4G network provider and MNOs will work with

Yota to avoid costly duplication of infrastructure investment. Consumers

will benefit from faster 4G service access and lower data prices.

Saudi Arabia‘s position is driven by its affluent citizens and a large

number of foreign workers working in the gulf nation while a third of the

Filipino population is below 14 years and rapidly acquiring smartphones.

Smartphones ownership 2012

CRITICAL SUCCESS FACTORS

Top 15 Markets

Rank Country

1 China

2 US

3 UK

4 France

5 Brazil

6 South Korea

7 Germany

8 India

9 Italy

10 Spain

11 Canada

12 Russia

13 Saudi Arabia

14 Philippines

15 Mexico

© Euromonitor International PASSPORT 21 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Smartphones ownership 2012

CRITICAL SUCCESS FACTORS

(‗000 units)

>80,000

10,000-80,000

5,000-9,000

© Euromonitor International PASSPORT 22 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Land transport expenses, in both developed and developing countries,

will continue to account for a good portion of one‘s dispensable income

and offers good prospect for NFC mobile payment adoption

Rail continues to be the preferred transport mode within and between

EU countries such as France and Germany, with high speed trains

hugely popular amongst both tourists and business travellers.

An established and extensive land transport network in Japan and South

Korea means that land travel remains a comfortable and efficient option.

Top of the list, China‘s high spend growth and ranking is due to the

government‘s focus on rail and road development to reduce economic

hours lost due to traffic congestion and to allow for fast and affordable

means of travel between Chinese cities.

While domestic air travel in Brazil is gaining popularity due to poor road

conditions and safety issues, spend remains highest on land transport.

On the other hand, Mexico will have the highest land spend growth as

commuters are switching back to trains and buses due to rising airfares.

Other developing countries that make up the top 15 list such as India

has a huge low-income population who extensively use its government-

owned transport network, despite poor road/rail quality.

While not a common feature in top lists, the Algerian government‘s

commitment of a US$9.6b budget to develop its land transport network

to stimulate economic growth will push the country into the top 15.

Consumer expenditure on land transport 2012

CRITICAL SUCCESS FACTORS

Top 15 Markets

Rank Country

1 China

2 France

3 Brazil

4 Mexico

5 Japan

6 US

7 Germany

8 India

9 UK

10 Russia

11 Italy

12 Algeria

13 South Korea

14 Netherlands

15 Spain

© Euromonitor International PASSPORT 23 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Consumer expenditure on land transport 2012

CRITICAL SUCCESS FACTORS

(US$ million, fixed ex-rate)

>50,000

20,000-49,000

10,000-19,000

© Euromonitor International PASSPORT 24 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

The prevalence and usage of cards in payments will compete with NFC

mobile payments, especially with the offer of loyalty programs and reward

points. The top 15 list tracks card usage trends and popularity.

Post economic recession, US consumers have shifted to a ―buy now, pay

now‖ mentality over the ―buy now, pay later‖ mentality and favour debit

cards. This is also to avoid hefty interest and late credit charges.

On the other hand, in the UK, charge cards are still preferred to credit

cards but increased usage in personal cards may be attributed to

purchases by small companies and self-employed entrepreneurs.

The Dutch have abolished extra charges on small transactions, driving

debit card usage over cash payments. In addition, cash withdrawals and

retail transactions on cards are free of charge within the Eurozone.

Lower-income earners in Brazil are fuelling card payment growth, aided by

rising wages and government social programmes despite the risk of lower-

income families defaulting on payments. In Turkey, credit card usage

remains very strong as card users enjoy huge discounts up to 20%, free

instalments and valet services etc.

Credit card ownership remains relatively low in China, with the market

dominated by the Government‘s China Union Pay, a debit card system.

The increased costs of ATM cash withdrawal and discounts offered by

retailers are driving card transactions in Argentina. The government is also

looking have the unbanked population to have accounts and debit cards.

Card payment transactions 2012

CRITICAL SUCCESS FACTORS

Top 15 Markets

Rank Country

1 US

2 Brazil

3 South Korea

4 China

5 France

6 UK

7 Canada

8 Japan

9 Hong Kong, China

10 Turkey

11 Russia

12 Netherlands

13 Australia

14 Argentina

15 Taiwan

© Euromonitor International PASSPORT 25 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Card payment transactions 2012

CRITICAL SUCCESS FACTORS

(US$ million, fixed ex-rate)

>1,500,000

500,000-1,500,000

120,000-490,000

© Euromonitor International PASSPORT 26 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

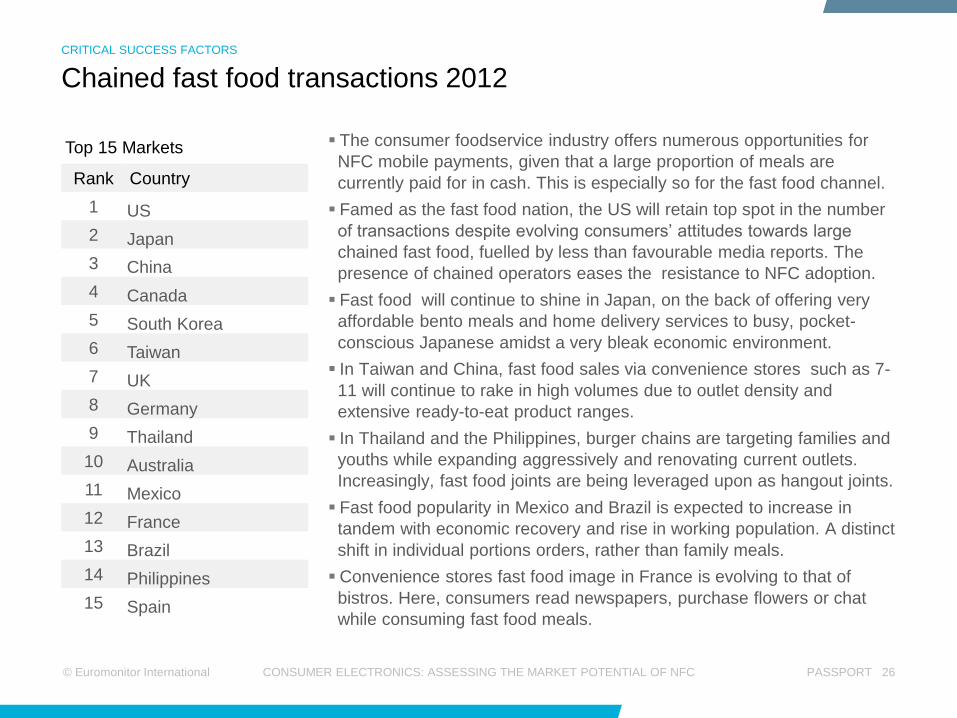

The consumer foodservice industry offers numerous opportunities for

NFC mobile payments, given that a large proportion of meals are

currently paid for in cash. This is especially so for the fast food channel.

Famed as the fast food nation, the US will retain top spot in the number

of transactions despite evolving consumers‘ attitudes towards large

chained fast food, fuelled by less than favourable media reports. The

presence of chained operators eases the resistance to NFC adoption.

Fast food will continue to shine in Japan, on the back of offering very

affordable bento meals and home delivery services to busy, pocket-

conscious Japanese amidst a very bleak economic environment.

In Taiwan and China, fast food sales via convenience stores such as 7-

11 will continue to rake in high volumes due to outlet density and

extensive ready-to-eat product ranges.

In Thailand and the Philippines, burger chains are targeting families and

youths while expanding aggressively and renovating current outlets.

Increasingly, fast food joints are being leveraged upon as hangout joints.

Fast food popularity in Mexico and Brazil is expected to increase in

tandem with economic recovery and rise in working population. A distinct

shift in individual portions orders, rather than family meals.

Convenience stores fast food image in France is evolving to that of

bistros. Here, consumers read newspapers, purchase flowers or chat

while consuming fast food meals.

Chained fast food transactions 2012

CRITICAL SUCCESS FACTORS

Top 15 Markets

Rank Country

1 US

2 Japan

3 China

4 Canada

5 South Korea

6 Taiwan

7 UK

8 Germany

9 Thailand

10 Australia

11 Mexico

12 France

13 Brazil

14 Philippines

15 Spain

© Euromonitor International PASSPORT 27 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Chained fast food transactions 2012

CRITICAL SUCCESS FACTORS

(‗000 transactions)

>20,000,000

1,000,000-20,000,000

450,000-900,000

© Euromonitor International PASSPORT 28 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

The absolute number of retail points defines the universe for NFC

mobile payment opportunities. Given their tremendous physical spread,

developing markets feature strongly in this top 15 list.

In Indonesia and India, shopping malls are rapidly increasing, driven by

a growing urban population who enjoy congregate in shopping malls as

meeting points and to shop /dine in air-conditioned comfort.

Egyptians aged under 24 years account for 55% of the domestic

population. Being more westernised and liberal as compared to the older

generation, these consumers view shopping /dining as a form of

socialisation and entertainment.

In Brazil, heightened retailing competition has resulted in mergers and

acquisitions, with more retailing outfits being set up in the Northeast.

While the retailing scene in Philippines will see expanded number of

shopping malls nationally, Thailand continues to grow as non-store

retailers such as Avon increase their visibility in store-based retail

channels, unaffected by its unstable political climate.

The retail scene in Pakistan remains highly fragmented, with large retail

stores found largely in the major cities such as Lahore and fuelling

growth, even as the risk of inflation escalation remains high.

Grocery retailers Coop and CONAD continued to fight for retail

leadership while foreign retailers are moving into the Italian market,

opening more outlets.

Store-based retailing 2012

CRITICAL SUCCESS FACTORS

Top 15 Markets

Rank Country

1 India

2 China

3 Indonesia

4 Egypt

5 Brazil

6 Mexico

7 Iran

8 US

9 Thailand

10 Philippines

11 Japan

12 Italy

13 Turkey

14 Pakistan

15 Spain

© Euromonitor International PASSPORT 29 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Store-based retailing 2012

CRITICAL SUCCESS FACTORS

(‗000 outlets)

>5,000

1,000-5,000

500-900

INTRODUCTION

NEAR FIELD COMMUNICATIONS (NFC)

MOBILE PHONES AS THE DIGITAL WALLET

CRITICAL SUCCESS FACTORS

MARKETS READY FOR NFC MOBILE

PAYMENT 2012

© Euromonitor International PASSPORT 31 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

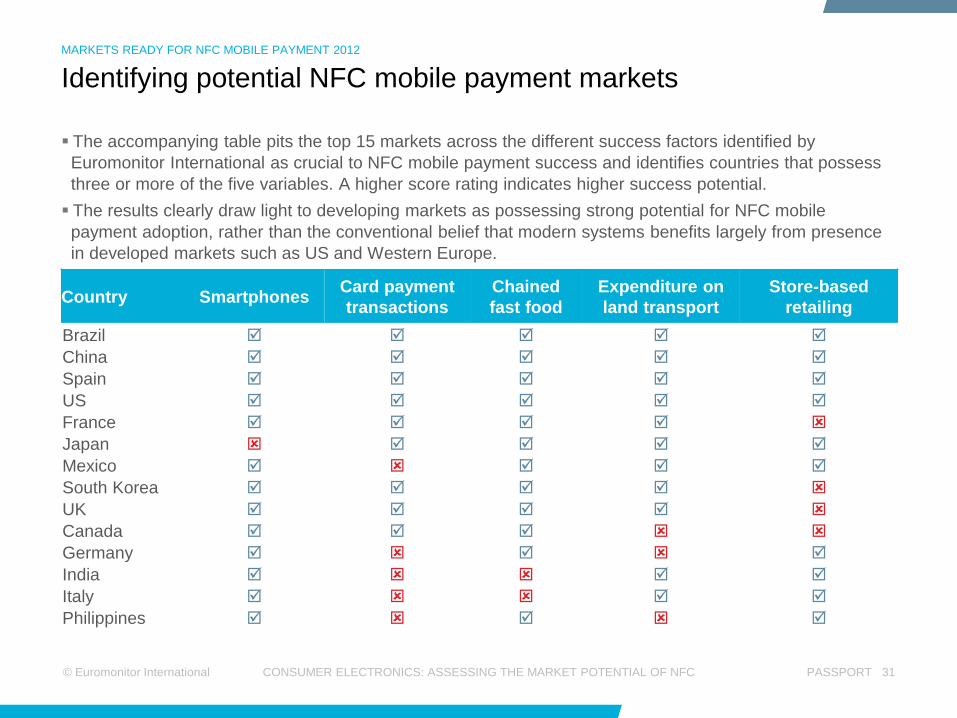

Identifying potential NFC mobile payment markets

MARKETS READY FOR NFC MOBILE PAYMENT 2012

The accompanying table pits the top 15 markets across the different success factors identified by

Euromonitor International as crucial to NFC mobile payment success and identifies countries that possess

three or more of the five variables. A higher score rating indicates higher success potential.

The results clearly draw light to developing markets as possessing strong potential for NFC mobile

payment adoption, rather than the conventional belief that modern systems benefits largely from presence

in developed markets such as US and Western Europe.

Country Smartphones Card payment

transactions

Chained

fast food

Expenditure on

land transport

Store-based

retailing

Brazil

China

Spain

US

France

Japan

Mexico

South Korea

UK

Canada

Germany

India

Italy

Philippines

© Euromonitor International PASSPORT 32 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Potential markets for NFC mobile payments 2012

MARKETS READY FOR NFC MOBILE PAYMENT 2012

High potential market

Good market

Ready market

© Euromonitor International PASSPORT 33 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

WIN

NE

RS

L

OS

ER

S

With the proliferation of smartphones and SIM card with NFC tag

embedded, existing mobile phones can be used for NFC mobile

payments.

The transaction cost of NFC payment is lower than credit cards,

which will encourage retailers to set up NFC payment option.

With local governments pushing for NFC as alternative payment

option and its implementation on public transport, the sheer volume

of transactions will trigger uptake by other merchants.

The unique selling point of NFC mobile payments is to enable a

seamless user experience for consumers. The absence of industry-

wide conformity to a common standard in terms of technical

infrastructure for NFC presents an obstacle for mass adoption.

Consumers are concerned about security as electronic fraud

becomes increasingly prevalent. Consumer education programs are

critical in allaying these fears.

Small retailers are not keen on electronic payments as the

transaction costs are seen as additional costs when compared to

cash..

From swiping to waving: Challenges ahead

MARKETS READY FOR NFC MOBILE PAYMENT 2012

Low start-up cost

Economies of scale

Inter-operability

Consumers’ concern and

retailer distrust

© Euromonitor International PASSPORT 34 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Euromonitor International‘s final country ranking list of NFC mobile payment ready markets offers a

dynamic mix of both developed markets such as the US, Germany, Japan, Spain and the UK, alongside

developing ones such as Brazil, China, India and Mexico.

Developed markets offer ready and established public transportation systems, strong financial institutions

and necessary technical expertise for successful, end-to-end implementation. The presence of chained

operators with presence across numerous countries also eases the adoption process as they are

constantly on the lookout for means to increase/expedite transacting volumes and grow revenues.

Developing markets, on the other hand, offer large population numbers who are keen to try out new

technologies, aside from cash payments. The low penetration of card payments with minimum income

qualification works to the advantage for NFC mobile payment adoption, by reducing the number of payment

mode options.

NFC enabled mobile phones offers usage beyond payments, including that of access to discount coupons,

user identification (eg. driver licence), access transport ticketing and more — enabling their device to act as

a wallet replacement. NFC functionality can also replace existing store loyalty cards and help retailers

identify its customers purchasing behaviors.

While obstacles such as technology advancements, cost of implementation, consumer acceptance and

retailer attitude have significant impact on the successful rollout of mobile payments, these identified

countries possess the underlying fundamentals for successful implementation of nationwide mobile

payment sooner rather than later. While the demand and market potential for NFC mobile payments is

clearly strong, the onus is to convert feasibility studies into actual, cost effective implementation.

Summing up

MARKETS READY FOR NFC MOBILE PAYMENT 2012

© Euromonitor International PASSPORT 35 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

2010 figures are provisional and based on part-year estimates.

Volume data are given in ‗000 units, unless otherwise stated.

Historic value data are given in US$ year-on-year exchange rates, unless otherwise stated.

The forecast period under review subsumes the years 2010 through to 2015, inclusive.

Forecast value data are given in constant US$ terms using fixed 2010 exchange rates, unless otherwise

stated.

Definitions for industry-specific and other terminology/abbreviations used in this report:

Consumer Electronics

Smartphones

Any device capable of voice communication over a cellular network. A smartphone must have an

identifiable operating system, allows installation of software applications (apps) and screen size of less

than 5‖

Consumer Finance

Card Payment Transactions (excl Commercial)

Includes debit, credit, charge, store and prepaid transactions)

Consumer Foodservice

Fast Food

Fast food outlets are typically distinguished by the following characteristics: a standardised and

restricted menu; food for immediate consumption; tight individual portion control on all ingredients and

on the finished product; individual packaging of each item; a young and unskilled labour force; counter

service

Data parameters and report definitions

MARKETS READY FOR NFC MOBILE PAYMENT 2012

© Euromonitor International PASSPORT 36 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

Retailing

Store-Based Retailing

Store-based retailing is the aggregation of grocery retailers and non-grocery retailers. Sales of new and

used goods to the general public for personal or household consumption from retail outlets or market

stalls

Countries and Consumers

Consumer Expenditure on Transport

Expenditure on purchase of cars, motorcycles and other vehicles, operation of personal transport

equipment and transport services

Data parameters and report definitions (2)

MARKETS READY FOR NFC MOBILE PAYMENT 2012

© Euromonitor International PASSPORT 37 CONSUMER ELECTRONICS: ASSESSING THE MARKET POTENTIAL OF NFC

This research from Euromonitor International is part of a global

strategic intelligence system which offers a complete picture of

the commercial environment. Also available from Euromonitor

International:

Global Briefings

Timely, relevant insight published every month on the state of the

market , emerging trends and pressing industry issues.

Interactive Statistical Database

Complete market analysis at a levels of detail beyond any other

source. Market sizes, market shares, distribution channels and

forecasts.

Strategy Briefings

Executive debate on the global trends changing the consumer markets

of the future.

Global Company Profiles

The competitive positioning and strategic direction of leading

companies including uniquely sector-specific sales and share data.

Country Market Insight Reports

The key drivers influencing the industry in each country;

comprehensive coverage of supply-side and demand trends and how

they shape the future outlook.

Learn More

To find out more about

Euromonitor International's

complete range of business

intelligence on industries,

countries and consumers please

visit www.euromonitor.com or

contact your local Euromonitor

International office:

London +44 (0)20 7251 8024

Chicago +1 312 922 1115

Singapore +65 6429 0590

Shanghai +86 21 6372 6288

Vilnius +370 5 243 1577

Dubai +971 4 372 4363

Cape Town +27 21 552 0037

Santiago +56 2 915 7200

Sydney +61 2 9275 8869

Tokyo +81 3-5403-4790

Bangalore +91 80 49040500

Experience more...

![PM [D03] What is there waving?](https://static.fdocuments.in/doc/165x107/58d08e341a28ab012d8b6eb5/pm-d03-what-is-there-waving.jpg)