Asian Palm Oil Producers Foray into Frontier African Markets · · 2017-01-24• Asia’s major...

15

Copyright 2013 Sustainalytics - All rights reserved • Asia’s major palm oil producers are making large-scale land acquisitions in several west and central African countries. In the context of fledgling governance mechanisms, disregard for community rights and increasing scrutiny from civil society organizations, these land deals often court controversy and increase the reputational and financial risk exposure of companies. • Investors must consider companies’ previous track records and impacts, exposure to human rights risks faced in new frontier markets, and their degree of preparedness to avoid and mitigate these risks. This may reduce reputational risks but along with financially material risks that result from slower than anticipated growth via African concessions. • This Insight assesses six of the leading Asian palm oil producers’ overall vulnerability to community relations or human rights risks involving land acquisition and production in Africa (see Appendix I). Although most of these companies are members of the Roundtable on Sustainable Palm Oil (RSPO), their degree of compliance with its provisions on community engagement and free, prior and informed consent (FPIC) 1 is questionable. In general, the companies assessed in this Insight fall short of demonstrating best practice regarding community engagement and respect for human rights. While palm oil is touted for its high yields, historically low pricing and nutritional benefits, oil palm plantations face considerable scrutiny for their adverse social and environmental impacts. Such impacts include deforestation, the destruction of areas with high conservation value such as peatland (using indiscriminate clearing methods such as slash-and-burn), greenhouse-gas emissions, biodiversity loss, as well as water and soil contamination from herbicide and pesticide use. The negative social impacts of oil palm plantations include illegal and inequitable land acquisition, destruction of culturally significant lands during plantation development, loss of livelihoods for local communities, poor living conditions for smallholder farmers and surrounding communities, poor working conditions, and disregard for diverse indigenous cultures. Until recently, criticism and public scrutiny of corporations involved in palm oil production have focused on global food manufacturers. For example, a high-profile Greenpeace campaign against Nestlé called on the company to cease procuring palm oil from Indonesia-based Sinar Mas (an affiliate of Golden Agri- Resources ), one of the largest palm oil producers, citing the company’s implication in the destruction of Asian Palm Oil Producers Foray into Frontier African Markets Jennifer Penikett & Jungho Park January 2013

Transcript of Asian Palm Oil Producers Foray into Frontier African Markets · · 2017-01-24• Asia’s major...

ESG Ins ight ASIA — January 2013 1

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

ESG Insight

ASIA

• Asia’s major palm oil producers are making large-scale land acquisitions in several west and central African countries. In the context of fledgling governance mechanisms, disregard for community rights and increasing scrutiny from civil society organizations, these land deals often court controversy and increase the reputational and financial risk exposure of companies.

• Investors must consider companies’ previous track records and impacts, exposure to human rights risks faced in new frontier markets, and their degree of preparedness to avoid and mitigate these risks. This may reduce reputational risks but along with financially material risks that result from slower than anticipated growth via African concessions.

• This Insight assesses six of the leading Asian palm oil producers’ overall vulnerability to community relations or human rights risks involving land acquisition and production in Africa (see Appendix I). Although most of these companies are members of the Roundtable on Sustainable Palm Oil (RSPO), their degree of compliance with its provisions on community engagement and free, prior and informed consent (FPIC)1 is questionable. In general, the companies assessed in this Insight fall short of demonstrating best practice regarding community engagement and respect for human rights.

While palm oil is touted for its high yields, historically low pricing and nutritional benefits, oil palm plantations face considerable scrutiny for their adverse social and environmental impacts. Such impacts include deforestation, the destruction of areas with high conservation value such as peatland (using indiscriminate clearing methods such as slash-and-burn), greenhouse-gas emissions, biodiversity loss, as well as water and soil contamination from herbicide and pesticide use. The negative social impacts of oil palm plantations include illegal and inequitable land acquisition, destruction of culturally significant lands during plantation development, loss of livelihoods for local communities, poor living conditions for smallholder farmers and surrounding communities, poor working conditions, and disregard for diverse indigenous cultures.

Until recently, criticism and public scrutiny of corporations involved in palm oil production have focused on global food manufacturers. For example, a high-profile Greenpeace campaign against Nestlé called on the company to cease procuring palm oil from Indonesia-based Sinar Mas (an affiliate of Golden Agri-Resources), one of the largest palm oil producers, citing the company’s implication in the destruction of

Asian Palm Oil Producers Foray into Frontier African Markets

Jennifer Penikett & Jungho Park

January 2013

ESG Ins ight ASIA — January 2013 2

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

orangutan-inhabited Indonesian rainforests.2 However, stakeholder scrutiny is now beginning to directly target palm oil producers themselves, the majority of which are headquartered in emerging markets such as Malaysia and Indonesia.3 Many of these palm oil producers are making a foray into Africa, prompted, in part, by a shortage of suitable land in their domestic markets and increasingly stringent environmental standards and regulatory restrictions. Some of these producers have already established a foothold in Africa, whereas others cite plans to do so.

Despite the low costs of land, expansion into Africa often comes with a reputational cost. Many companies face allegations of unfair land acquisition (sometimes referred to as “land grabbing”), characterised by inadequate company engagement with affected communities on development plans and failure to solicit the FPIC of affected indigenous peoples. FPIC and community engagement have become a major point of contention among companies and civil society organisations and, as such, represent a key focus area for the RSPO Principles and Criteria (P&C) Review discussions to be held in January 2013.

While reputational risks for companies and their investors are obvious, they can be accompanied by weaker investor returns, and in some cases, the erosion of value. The inability to attain a social license to operate in these new markets can delay or even derail existing plans and future expansion prospects. Moreover, in certain cases the absence of broad-based community support for projects exacerbates a company’s dependence on the continuity of a specific regime; as such, the risk of political change can severely jeopardize long-term project viability.

This Insight assesses the major palm oil producers that have initiated expansions into Africa, evaluating their preparedness to effectively address the rights and interests of local communities and their track records in the region to date. Each of these companies has been or will be exposed to human rights risks via their palm oil production in African markets.

Palm oil fruit

ESG Ins ight ASIA — January 2013 3

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Sustainalytics’ assessment of the relative risk that companies face when expanding oil palm operations to Africa are set out in the table below. A full assessment of one company has been included in Appendix I. For a similar assessment of other companies, please contact the authors or email [email protected].

CompanyLevel Assessment

Sime Darby Berhad

High

Highest exposure to contentious land acquisitions in Liberia via a USD 2.1 billion investment in 220,000 hectares (ha). Community opposition has hampered the company’s ambitious expansion plans. However, recent changes including greater management oversight and local community engagement suggest a partly mitigated risk outlook.

Golden Agri-Resources Ltd (GAR)

High

High exposure via its significant investments in Liberian oil palm plantations. Given that GAR does not have any direct operations in Africa, its risk exposure is deemed lower (220,000 ha through the Verdant Fund, which owns Golden Veroleum [Liberia]), yet its degree of accountability on the ground may also be constrained. GAR has also established community engagement policies that address FPIC, which are reportedly applicable to companies it is invested in regardless of management control. Additionally, approximately 16% of the company’s total planted area is RSPO certified.

Wilmar International Limited

High

High exposure to contentious land acquisitions in Nigeria and Uganda. While Wilmar has management systems in place, its oversight of the sustainability of its African operations is lacking and the company has been accused of not recognising community rights in Nigeria and Uganda. Approximately 48% of its oil palm plantations are RSPO certified.

Bakrie Sumatera Plantations (BSP)

Moderate

Moderate exposure to contentious land acquisitions. BSP’s operations in Africa are limited to 4,000 ha, yet through affiliate companies it intends to focus expansion on Liberia and Ivory Coast, two countries with recent exposure to political unrest. The company fails to disclose community engagement and FPIC policies and programmes, suggesting an inadequate level of preparedness.

Olam International Limited

Moderate

Moderate exposure to contentious land acquisitions. Olam is involved in oil palm plantations in Gabon, which may be considered a less risky African country to invest in as it is not mired with political instability, and given its intention to become the first sustainable palm oil producer in Africa by 2017. The company has relatively strong community engagement programmes and management systems that are backed by risk prevention measures; however, Olam is a relatively new RSPO member, and as of January 2013 does not have any certified palm oil plantations.

Felda Global Ventures Holdings Berhad (FGVH)

Low

Low exposure to contentious land acquisitions in Africa as the company does not yet operate there. The combination of its stated African expansion plans, spotty track record of community engagement in its native markets, and the lack of policies and systems that are applied to its companies that manage plantations in Asia, however, bode poorly for its community relations in Africa.

Risk assessment of involvement in contentious land acquisitions in Africa

ESG Ins ight ASIA — January 2013 4

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Drivers for African ExpansionPalm oil is the world’s most widely used vegetable oil – a trend that is expected to persist as population growth, changing dietary trends and its application in several other industries continue to boost demand. Its more recent use as a biofuel has generated competing demands to supply the transportation sector, triggering price increases. As of 2010, palm oil demand totaled nearly 50 million tonnes4 and, according to the UN Food and Agriculture Organisation (FAO), this demand is expected to reach 77 million tonnes by 2050.5 To date, the largest markets for palm oil are India and China, followed closely by the EU. The U.S. Department of Agriculture estimates that in 2012-13, India will import 7.7 million tonnes, which is equivalent to approximately 19 per cent of the world’s total, followed by 16 per cent in China and 13.5 per cent in the EU.6 While domestic palm oil consumption in Africa is approximately 5.4 million tonnes, the FAO projects a doubling and tripling of this demand by 2030 and 2050, respectively.7

In order to meet this increasing global demand, major palm oil producers are expanding production capacity into west and central Africa to supplement output from existing plantations in Indonesia and Malaysia. Several African countries, including Nigeria, Ghana, Ivory Coast, the Democratic Republic of Congo, Liberia, Cameroon, and Uganda are best suited for oil palm plantations due to their favourable soil and climatic conditions. Other push factors for diversification in African markets include competition for land for biofuel production and increasing regulatory restrictions on obtaining new concessions in domestic markets. Compounding the continent’s own rapid growth potential, Africa is deemed attractive due to its proximity to key EU markets, not to mention, the considerable efforts made by a number of African regimes to secure business by offering long-term concessions at low costs.

Large Scale Land Acquisition: Risk and ImpactGiven long-standing concerns about the adverse social and environmental impact of palm oil production in Southeast Asia, the World Wildlife Fund (WWF) established the RSPO in 2004 as a global multi-stakeholder roundtable to improve the sustainability of palm-related operations. The RSPO Principles & Criteria (see Appendix II) provide guidelines on how companies should respect the rights of local communities and indigenous peoples and address their concerns regarding the impact of plantations on their traditional lands. In accordance with FPIC, companies’ disclosure of engagement with indigenous

Uganda Nigeria Liberia Gabon Cameroon Cote d’Ivoire Ghana Mozambique Oil palm

plantation (ha)

Wilmar 50,000 planted; 32,000 planned

FGVH (FELDA) -

Olam 100,000Sime Darby 220,000

GAR 220,000BSP 4,000

Summary table indicating African countries where Asian palm oil producers have exposure to plantations8

Planted palm plantation Planned palm plantationOther crops including rubber, rice, sugar, cotton, timber

ESG Ins ight ASIA — January 2013 5

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

people should include detailed information on environmental and social impact assessments, land acquisitions, compensation and benefits, grievance mechanisms and conflict resolution.9 Ultimately, FPIC allows indigenous peoples to either accept or reject proposals to have land or natural resources developed. For further information on FPIC, see Sustainalytics’ October 2011 report, License to Operate: Indigenous Relations and Free Prior and Informed Consent in the Mining Industry.

While RSPO’s guidance and stance has led to some progress, effective enforcement on the ground has been a challenge. The RSPO has begun a Principles and Criteria Review with the next discussions slated for January 2013.

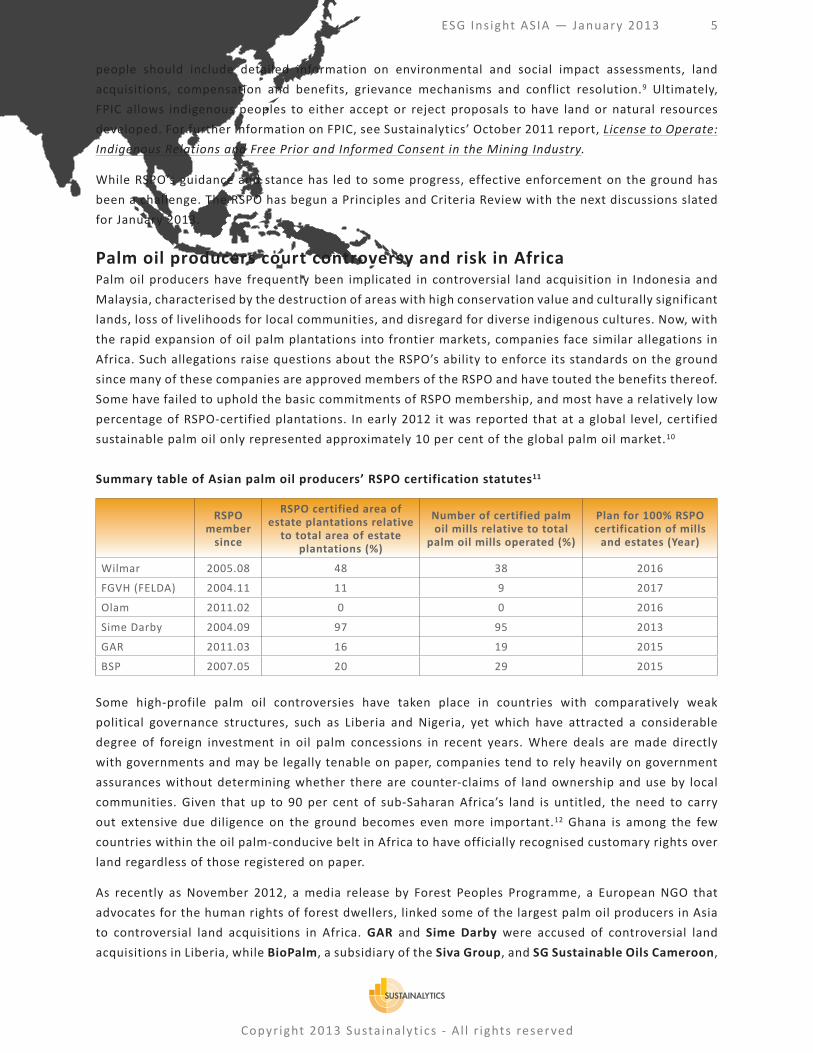

Palm oil producers court controversy and risk in AfricaPalm oil producers have frequently been implicated in controversial land acquisition in Indonesia and Malaysia, characterised by the destruction of areas with high conservation value and culturally significant lands, loss of livelihoods for local communities, and disregard for diverse indigenous cultures. Now, with the rapid expansion of oil palm plantations into frontier markets, companies face similar allegations in Africa. Such allegations raise questions about the RSPO’s ability to enforce its standards on the ground since many of these companies are approved members of the RSPO and have touted the benefits thereof. Some have failed to uphold the basic commitments of RSPO membership, and most have a relatively low percentage of RSPO-certified plantations. In early 2012 it was reported that at a global level, certified sustainable palm oil only represented approximately 10 per cent of the global palm oil market.10

Summary table of Asian palm oil producers’ RSPO certification statutes11

Some high-profile palm oil controversies have taken place in countries with comparatively weak political governance structures, such as Liberia and Nigeria, yet which have attracted a considerable degree of foreign investment in oil palm concessions in recent years. Where deals are made directly with governments and may be legally tenable on paper, companies tend to rely heavily on government assurances without determining whether there are counter-claims of land ownership and use by local communities. Given that up to 90 per cent of sub-Saharan Africa’s land is untitled, the need to carry out extensive due diligence on the ground becomes even more important.12 Ghana is among the few countries within the oil palm-conducive belt in Africa to have officially recognised customary rights over land regardless of those registered on paper.

As recently as November 2012, a media release by Forest Peoples Programme, a European NGO that advocates for the human rights of forest dwellers, linked some of the largest palm oil producers in Asia to controversial land acquisitions in Africa. GAR and Sime Darby were accused of controversial land acquisitions in Liberia, while BioPalm, a subsidiary of the Siva Group, and SG Sustainable Oils Cameroon,

RSPO member

since

RSPO certified area of estate plantations relative

to total area of estate plantations (%)

Number of certified palm oil mills relative to total

palm oil mills operated (%)

Plan for 100% RSPO certification of mills

and estates (Year)

Wilmar 2005.08 48 38 2016

FGVH (FELDA) 2004.11 11 9 2017

Olam 2011.02 0 0 2016

Sime Darby 2004.09 97 95 2013

GAR 2011.03 16 19 2015

BSP 2007.05 20 29 2015

ESG Ins ight ASIA — January 2013 6

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

owned by U.S. company Herakles Farms, were accused of contentious land acquisition in Cameroon.13 BioPalm reportedly had not consulted a local pygmy tribe when it began planning its operations in Cameroon and has faced strong opposition. Nigerian NGOs and local community leaders have also filed a formal complaint with the RSPO to halt Wilmar’s palm oil expansion in Cross River State in Nigeria, claiming that the company had not recognised the full extent of FPIC for local communities at its Ibiae Estate. Wilmar’s acquisitions in Uganda were also called into question in April 2012. In September 2012, a Gabonese NGO launched a campaign to collect signatures to stop Olam’s acquisition of what it claims was ancestral land in Gabon.

GAR, Sime Darby, Wilmar, and Olam (along with FGVH and BSP) are all active members of the RSPO, which suggests that the Roundtable may not be able to effectively police and enforce its standards. The extent to which the RSPO’s P&C will be amended and implemented, and how membership activity will be monitored, will be critical to addressing the social impact of the palm oil industry, alongside its environmental impact.

Poor community relations not only damage company reputations (in the wake of increased scrutiny from civil society) but also jeopardize a company’s social licence to operate. The FAO’s director general was recently quoted as saying that only 10 to 15 per cent of the land acquired in Africa (not limited to palm oil) over the past five years was actually being developed. While some of this may owe to the fact that land banks have been purchased for future use, it also points to obstacles companies have faced and deals falling through in some cases.

Effective engagements with communities in these new markets are critical to soliciting a social license to operate. Risks that stem from political regime changes may also be counterbalanced by community support, whereas in cases where a license to operate is almost entirely determined by political support, subsequent regime changes can severely impair long-term project viability.

Case study: Lessons for Sime Darby in Liberia In 2009, Malaysia-based Sime Darby signed a 63-year agreement with the Government of Liberia to develop 220,000 hectares (ha)

of land for palm oil and rubber cultivation. In October 2011, the Forest Peoples Programme lodged a complaint with the RSPO against

the company, accusing it of illegally confiscating land from local farmers in violation of the RSPO P&C.14 Subsequently, a report

released by Columbia University’s Center for International Conflict Resolution (CICR) in January 2012 claimed that indigenous tribes

affected by the company’s operations in Liberia were not given the opportunity to grant their FPIC.15 Described by the CICR as “the

most controversial concessionaire presently operating in Liberia,” Sime Darby’s operations have received negative media attention

and local community opposition. The CICR raised concerns about escalating social conflict due to the lack of consultation and the loss

of livelihoods for local communities as a result of large-scale land acquisition for its plantations. Moreover, some experts pointed out

that, given the length of the leases, communities would effectively be giving up their land for entire generations.

Community resistance has made operations very difficult and according to a report by The Financial Times, Sime Darby was well

behind schedule with only 3,200 ha under cultivation as of August 2012 — far from its anticipated expansion of 30,000 ha in that time,

based on projections of 10,000 ha per year.16

There are indications, however, that the company is accepting responsibility for its actions and establishing better mechanisms to

communicate with local communities. In November 2012, Sime Darby agreed to compensate affected communities in Cape Mount

County (one of the four Liberian counties in which the company operates) through the creation of a fund. As such, for the next 60

years it has committed to compensate local communities for the destruction of community farmlands, cash crops, and shrines. It will

also provide food donations and scholarships to the affected communities.17 (As per Appendix 1, contact Sustainalytics for further

assessment of Sime Darby’s performance relative to its industry peers).

ESG Ins ight ASIA — January 2013 7

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Mitigating Risk and Promoting Best PracticeThere is no single solution to mitigating the risks associated with expanding palm oil production into African markets, as each case introduces a unique set of challenges. However, investors can assess palm oil companies based on measures taken (some of which are already propagated by the RSPO) to mitigate risks and foster best practice. As noted, RSPO membership represents a valuable first step, yet it does not negate the need for company-specific policies and programmes addressing human rights of indigenous and marginalised peoples. In order to mitigate the operational, financial and reputational risks of being linked to environmentally and/or socially controversial land acquisition practices, investors should also look for company management systems for community engagement, which meet or exceed local regulatory requirements.

Key aspects on which companies may be assessed for risk avoidance and mitigation are discussed below:

Policies on human rights and FPIC: It is considered best practice for companies to develop policies and programmes that address human rights and the rights of indigenous people, community engagement programmes, and robust social and environmental impact assessments. A formal policy on human rights should clearly define how a company deals with human rights issues within its sphere of influence. Furthermore, the policy should specify how the company views its role in countries with a record of frequent human rights abuses. Best practice entails making a formal commitment to adhere to the UN Guiding Principles on Business and Human Rights, developed by John Ruggie in June 2011, which outline corporations’ responsibility to protect, respect and remedy human rights in volatile regimes.18 Additionally, for companies that are involved in agricultural operations in countries where there are indigenous groups, policies should commit to: respect their unique livelihoods, culture and land rights; seek effective representation and informed participation of all related indigenous peoples; report on progress on a periodic basis; and ultimately adhere to the principles of FPIC.

Company standards for environmental and social impact assessments: Companies should commit to conducting environmental and social impact assessments for new projects with considerable impacts, including oil palm planting and processing facilities. The impact assessments are meant to inform all interested parties about project impacts. Identifying High Conservation Value areas (HCVs) in the projected land for oil palm plantations and protecting the HCVs may reduce potential conflicts with environmental NGOs and local communities.19 Further, given that FPIC auditors can have differing standards, companies should develop and disclose their own FPIC manuals that form the basis of such assessments.

Consultative community engagement programmes: Community engagement programmes are important management tools, particularly for companies operating in regions where the legal framework or enforcement mechanisms are considered weak. Strong community consultation systems should include detailed guidelines outlining a formal system for identifying stakeholders of interest, taking into account groups that may not have equal representation at a local government level (i.e., minorities, elderly, or women). Programmes must include mechanisms for early consultation, prior to any development, and consultation throughout the entire life cycle of the project. In order to conduct sound community engagement programmes, companies should first compile socio-economic data to understand the needs of local communities. Ideally, a company should also provide sufficient training to community members in all aspects of palm oil production and a formal community complaints and grievance mechanism should be implemented.

ESG Ins ight ASIA — January 2013 8

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

It is imperative that community engagement programmes are based on long-term dialogue that treats consultation and negotiation as an iterative process.

Provisions for early community consultations should be implemented regardless of whether a legally binding land agreement only requires government approval. Even in cases where land is granted by the government, a company should carry out an independent assessment to ensure that the terms of the agreement meet an acceptable and inviolable company standard.

Long-term compensation: Compensation should factor in long-term loss of livelihood, not only for communities that claim customary rights, but for any that earn a livelihood from working the land. Compensation should include long-term job creation for impacted parties and compensation payments staggered over time. Once the consent of indigenous communities is obtained, the company should articulate, clarify and commit to the condition in which land will be returned, to whom it will be returned and under which terms it will be returned.

Reporting on implementation of commitments: Companies should be open to third-party scrutiny of their claims and approaches at the time of land acquisition and beyond. They should also periodically report on the progress of implementation and have such disclosure vetted by an independent agency.

Implications for InvestorsLarge-scale land acquisitions in Africa will be subject to increased stakeholder scrutiny as communication channels improve across the region, heightening the reputational risks faced by companies and their shareholders.

In the meantime, operational risks will persist in the form of project delays or derailment and a loss of a company’s social license to operate. Weak or tenuous relations between palm oil producers and local communities may exacerbate the long-term operational risks faced by investments in some African countries. In such contexts, these investments are subject to volatility surrounding regime changes, which can present material risks.

Setting up oil palm plantations is capital-intensive, requiring high initial investments for land acquisition, clearing, infrastructure, construction of production facilities, and other related expenditures. On average, a 30-month no-return period should be anticipated between initial planting and the first harvest.20 Any operational setbacks and delays at the oil palm plantation development stage can extend the already lengthy no-return period.

Collaboration: Various tools and opportunities for investor collaboration on palm oil include the following:

• WWF has developed a Palm Oil Financing Handbook,21 formulated based on RSPO standards, to help investors and financial institutions draft and implement responsible palm oil investment policies.

• The UN PRI Working Group on Sustainable Palm Oil comprises approximately 25 global investors with an aim to provide a unified investor voice in support of sustainable palm oil and engage with companies in support of more sustainable practices.22

• Investors may join the RSPO as members. Moreover, two seats (12.5 per cent representation) on the RSPO Executive Board are designated for investors and lenders.

ESG Ins ight ASIA — January 2013 9

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Policy development: Some commercial banks and investors have sharpened their minimum standards and risk assessment frameworks for oil palm plantations or companies involved in the palm oil value chain. These may be positioned as stand-alone policies or part of broader policy commitments related to sustainable development. Few mainstream investors have stand-alone investment policies specifically concerning palm oil.23 Although heavily reliant on RSPO guidelines and membership, BNP Paribas has a standalone corporate social responsibility policy on the palm oil sector that also extends to its asset management business.24 Policies developed by asset managers can more explicitly focus on community relations and human rights concerns in the context of land acquisition and development in markets with weak governance structures.

Integration and engagement: Investors can integrate the vulnerability assessment featured in this Insight into their own decision-making processes. They can also become better informed through dialogue with companies around the points identified below. While this Insight has highlighted African land acquisitions, it is important to note that palm oil producers, and other agricultural commodity producers, are exposed to similar risks in other regions as well.

Points for discussion

Policies and programmes

• Does the company have a human rights policy in place that addresses community engagement, and more explicitly FPIC, and that is applied to all plantations regardless of local regulatory requirements?

• Does the company have a formal community engagement programme with clear grievance mechanisms?

Oil palm plantation in Indonesia, North Sumatra

ESG Ins ight ASIA — January 2013 10

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Land acquisition

• When looking to invest in land, does the company effectively engage with all stakeholders, including traditionally disadvantaged groups (i.e., indigenous peoples, minorities, elderly, women)?

• Does the company prepare and/or collect socio-economic data on local communities before commencing approval procedures and/or environmental and social impact assessments (ESIA)?

• Does the company routinely communicate with internal and external stakeholders on FPIC, human rights, and community engagement?

• Does the company have experienced in-house facilitators who can conduct FPIC procedures and/or ESIA? If not, how does the company select and appoint on-the-ground facilitators who are experts on the affected regions?

Compensation and reclamation

• Does the company have programmes to address environmental degradation? If land is “leased” from a community, what standards are in place regarding its condition upon return to the community? What binding commitments does the company make to ensure that fair reclamation has taken place?

• What is the company’s stance on long-term compensation versus one-time handouts?• Does the company consult with an affected community about compensation and benefits for

mutually agreeable results?

Transparency

• Does the company disclose agreements that it has in place with local communities and/or indigenous peoples?

• Does the company assess and articulate to its shareholders the risks posed to investments from local community opposition?

• If the company is an RSPO member, does it provide annual communications on progress and the percentage of RSPO-certified sites and the percentage of certified sustainable palm oil? If not, when does the company plan to sign on as an RSPO member?

ESG Ins ight ASIA — January 2013 11

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Appendix ICompany Assessments25

Sample information for Olam International Limited (OLAM: Singapore)

Assessment: Moderate

As a relatively more seasoned African investor through its involvement in other agricultural commodities, Olam has certain advantages in this region. Moreover, while there have been some claims that the company has violated local communities’ rights, there are also reports by the Forest Peoples Programme suggesting that Olam has made tangible commitments to the sustainability of its oil palm plantations, backed up by management systems and risk prevention measures.

Exposure

Olam’s palm business is largely focused on upstream and end markets in Africa. Olam Palm is establishing palm plantations in Gabon over two phases. The company has partnered with the Government of the Republic of Gabon in a 70/30 joint venture to develop 100,000 ha of palm plantations out of a total 300,000 ha land concession. The company states that as of January 2013, 7,134 ha near Kango and 20,360 ha near Mouila have been identified as suitable for planting. Olam states that upon successful completion of the first phase of 50,000 ha, 30,000 ha of oil palm will be developed under out-growers to enable communities to benefit economically from oil palm development. While land-use planning and unclear demarcations of agricultural land are intrinsic problems that the Gabon government faces, that can slow development, it has a stated ambition to become the first sustainable palm oil producer in Africa by 2017. As such, the Gabonese government may represent a more supportive business partner for oil palm projects than some of its neighbouring countries.

Preparedness (based on programmes, policies and management systems)

Olam is a relatively new RSPO member, yet has its own Palm Sustainability Policy, which states that it engages transparently with communities to ensure FPIC of local communities and stakeholders and respect of customary rights before beginning developments. Its land management procedures require that while its ESIAs comply with national requirements, they must also adhere to International Finance Corporation (IFC) standards, which include considerations for FPIC. Additionally, the company states that it continues to engage with communities long after development has begun through regular meetings with affected communities and inviting community representatives to palm plantations.

The company’s decision to not plant 27,890 ha of an approximately 50,000 ha concession in Gabon for the preservation of High Conservation Value areas, community use areas and riparian buffers, including 950 ha reserved for subsistence farming as per community engagement, is noteworthy. It suggests that its risk mitigation efforts have included avoiding development on the basis of its impact assessments.

Track record

Brainforest, a Gabonese organisation, targeted the company for violating communities’ rights including destruction of ancestral lands. The organisation claims that the Gabonese government is granting large scale land concessions to the company, without consideration of community engagement and the right to FPIC. Avaaz, a global advocacy organisation, reports plans to collect signatures to prevent the company’s land acquisitions in that country.

Questions for engagement

Do Olam’s policies on sustainable palm oil also apply to its joint ventures? If so, is this contractually obligated and what monitoring systems does it have in place?

Does the company have a plan to disclose its overall FPIC processes and results?

Research for other companies covered in this report can be obtained from Sustainalytics upon written request:

[email protected](+65) 62 24 07 66

ESG Ins ight ASIA — January 2013 12

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Appendix II

Principle 1: Commitment to Transparency

Criterion 1.1 Oil palm growers and millers provide adequate information to other stakeholders on environmental, social and legal issues relevant to RSPO Criteria, in appropriate languages and forms to allow for effective participation in decision making.

Criterion 1.2 Management documents are publicly available, except where prevented by commercial confidentiality or where disclosure of information would result in negative environmental or social outcomes.

Principle 2: Compliance with applicable laws and regulations

Criterion 2.1 There is compliance with all applicable local, national and ratified international laws and regulations.

Criterion 2.2 The right to use the land can be demonstrated, and is not legitimately contested by local communities with demonstrable rights.

Criterion 2.3 Use of the land for oil palm does not diminish the legal rights, or customary rights, of other users, without their free, prior and informed consent.

Principle 6: Responsible consideration of employees and of individuals and communities affected by growers and mills

Criterion 6.1 Aspects of plantation and mill management, including replanting, that have social impacts are identified in a participatory way, and plans to mitigate the negative impacts and promote the positive ones are made, implemented and monitored, to demonstrate continuous improvement.

Criterion 6.2 There are open and transparent methods for communication and consultation between growers and/or millers, local communities and other affected or interested parties.

Criterion 6.3 There is a mutually agreed and documented system for dealing with complaints and grievances, which is implemented and accepted by all parties.

Criterion 6.4 Any negotiations concerning compensation for loss of legal or customary rights are dealt with through a documented system that enables indigenous peoples, local communities and other stakeholders to express their views through their own representative institutions.

Principle 7: Responsible development of new plantings

Criterion 7.1 A comprehensive and participatory independent social and environmental impact assessment is undertaken prior to establishing new plantings or operations, or expanding existing ones, and the results incorporated into planning, management and operations.

Criterion 7.5 No new plantings are established on local peoples’ land without free, prior and informed consent, through a documented system that enables indigenous peoples, local communities and other stakeholders to express their views through their own representative institutions.

Criterion 7.6 Local people are compensated for any agreed land acquisitions and relinquishment of rights, subject to their free, prior and informed consent and negotiated agreements.

Roundtable on Sustainable Palm Oil, Principles and Criteria relating to community engagement and FPIC26

ESG Ins ight ASIA — January 2013 13

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Endnotes1 Free, prior, and informed consent is a principle set out in the UN Declaration of the Rights of Indigenous Peoples and adopted by the RSPO. It has also been

adopted as a best practice in corporate social responsibil ity by extractive industries. Source: Forest Peoples Programme, “Free, Prior and Informed Consent and the Roundtable on Sustainable Palm Oil: A Guide for Companies,” October 2008.

2 Greenpeace, “Ask Nestlé to give rainforests a break,” http://www.greenpeace.org /international/en/campaigns/climate-change/kitkat/ (accessed 30 November 2012).

3 Forest Peoples Programme. “Free Prior and Informed Consent and the RSPO.” http://www.forestpeoples.org /sites/fpp/fi les/publication/2012/10/rspofpic23oct12.pdf (accessed 30 November 2012).

4 WWF, “ The Journey Towards Sustainable Palm Oil: How Your Company Can Get Started,” 2012; http://awsassets.panda.org /downloads/wwf_palmoil_

brochure_china_webversion.pdf (accessed 03 December 2012).

5 Food and Agriculture Organization, “World agriculture: towards 2030/2050, Prospects for food, nutrition, agriculture and major commodity groups, Interim report,” http://www.fao.org /fi leadmin/user_upload/esag /docs/Interim_report_AT2050web.pdf (accessed 03 December 2012).

6 United States Department of Agriculture, Foreign Agriculture Services, “Oilseeds: World Markets and Trade,” Circular Series FOP 11-12, November 2012: Table 11. http://www.fas.usda.gov/psdonline/circulars/oilseeds.pdf (accessed 29 November 2012).

7 Index Mundi, “Palm Oil Domestic Consumption by Country in 1000 MT,” http://www.indexmundi.com/agriculture/?commodity=palm-oil&graph=domestic-consumption (accessed 07 December 2012).

8 This table highlights known oil palm plantations in key African markets based on available information. Its validity is challenged by inadequate company disclosures and potential inaccuracies in media reports. There are other African countries such as Sierra Leone, Democratic Republic of Congo, and Ethiopia, where governments have awarded concessions for at least 1.5 mill ion ha of land to commercial oil palm plantations; however, these lands have not been awarded to Asian palm oil producers mentioned above to date.

9 Irene Sosa, “License to Operate: Indigenous Relations and Free Prior and Informed Consent in the Mining Industry,” October 2011, http://www.sustainalytics.com/sites/default/fi les/indigenouspeople_fpic_final.pdf (accessed 12 December 2012).

10 WWF, “Profitabil ity and Sustainabil ity in Palm Oil Production: Analysis of Incremental Financial Costs and Benefits of RSPO Compliance,” March 2012, http://awsassets.panda.org /downloads/profitabil ity_and_sustainabil ity_in_palm_oil_production__update_.pdf (accessed 11 November 2012).

11 The RSPO-related data are derived from individual companies’ RSPO annual communication of progress 2011-2012 report (http://www.rspo.org /en/members_search).

12 The Guardian, “How African governments allow farmers to be pushed off their land,” www.guardian.co.uk/global-development/poverty-matters/2012/mar/02/african-governments-land-deals (accessed 06 December 2012).

13 Forest Peoples Programme, “New oil palm land grabs exposed: Asian palm oil companies run into trouble in Africa,” http://www.forestpeoples.org /topics/palm-oil-rspo/news/2012/11/press-release-new-oil-palm-land-grabs-exposed-asian-palm-oil-compa (accessed 30 November 2012).

14 Forest People Programmes website, www.forestpeoples.org (accessed 12 December 2012).

15 Columbia University – School of International and Public Affairs, Center for International Conflict Resolution, “Smell-No-Taste: The Social Impact of Foreign Direct Investment in Liberia,” January 2012. http://www.cicr-columbia.org /wp-content/uploads/2012/01/Smell-No-Taste.pdf (accessed 02 January 2013).

16 Financial Times, “Palm oil: Companies have trouble securing land,” www.ft.com/intl/cms/s/0/6d679244-f8f0-11e1-b4ba-00144feabdc0.html (accessed 11 December 2012).Sime Darby, “Sime Darby To Set Roots In Liberia,” www.simedarby.com/Sime_Darby_To_Set_Roots_In_Liberia.aspx (accessed 11 December 2012).

17 All Africa, “Liberia: Sime Darby agrees to pay U.S. one mill ion,” allafrica.com/stories/201211281265.html (accessed 29 November 2012).

18 United Nations Human Rights, Office of the High Commissioner, “Guiding Principles on Business and Human Rights: Implementing the United Nations ‘Protect, Respect and Remedy’ Framework,” June 2011 http://www.ohchr.org /Documents/Publications/GuidingPrinciplesBusinessHR_EN.pdf (accessed 06 December 2012).

19 Six types of HCVs are developed by the Forest Stewardship Council for certif ication of forest ecosystems; however, certif ication is now applied to assessments of other ecosystems including fundamental areas to meet local communities’ basic needs and critical areas to local communities’ traditional cultural identities. Source: http://ic.fsc.org /high-conservation-values-and-biodiversity-identification-management-and-monitoring.213.htm (accessed 11 December 2012).

20 The Malaysian Palm Oil Board, “Malaysian Palm Oil Industry,” http://www.palmoilworld.org /about_malaysian-industry.html (accessed 27 November 2012).RSPO, “Fact sheet: Palm oil,” http://www.rspo.org /fi les/pdf/Factsheet-RSPO-AboutPalmOil.pdf (accessed 27 November 2012).

21 WWF, “ The Palm Oil Financing Handbook: Practical guidance on responsible financing and investing in the palm oil sector,” 2008. http://wwf.panda.org /what_we_do/footprint/agriculture/palm_oil/solutions/responsible_financing / (accessed 15 January 2013).

22 As part of the UNPRI’s priority collaborative engagements, the Investor Working on Sustainable Palm Oil engages with global buyers of palm oil to encourage them to set commitments and deadlines for purchasing sustainable palm oil. Source: http://www.unpri.org /areas-of-work/collaborations/priority-collaborative-engagements/ (accessed 15 January 2013).

23 WWF, “Palm Oil Investor Review: Investor Guidance on Palm Oil,” 2012, http://www.rspo.org /fi le/Palm%20Oil%20Investor%20Review%20Web%20Version.pdf (accessed 15 January 2013).

24 BNP Paribas, “Corporate Social Responsibil ity Sector Policy – Palm Oil,” http://compresse.bnpparibas.com/applis/wCorporate/wCorporate.nsf/docsByCode/LDIO-8CJESM/$FILE/Politique%20Sectorielle%20Huile%20de%20palme.pdf (accessed 15 January 2013).

ESG Ins ight ASIA — January 2013 14

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

25 Company assessments are based on disclosures made by companies, media reports and NGO/civil society reports. Sources include company annual reports, sustainabil ity reports, corporate websites, civi l society reports and websites, and media sources. Disclosures on land bank and plantation acquisitions and plans are often opaque, and controversial cases tend to draw polarized views from companies and civil groups, respectively. As such, all of the companies were contacted directly for feedback. As of 11 January 2013, Felda Global Ventures Holdings, Olam International, Sime Darby, Golden Agri-Resources, and Wilmar International responded and their responses were factored into Sustainalytics’ assessments.

26 Selected principles included in this table are those which relate to community engagement and FPIC. Roundtable on Sustainable Palm Oil, “RSPO Principles and Criteria for Sustainable Palm Oil Production; Including Indicators and Guidance,” October 2007. http://www.rspo.org /fi les/resource_centre/RSPO%20Principles%20&%20Criteria%20Document.pdf (accessed 30 November 2012).

Contact InformationFor more information on any of the contents of this report please feel free to contact the authors. For more information about Sustainalytics’ products and services please email

[email protected] or visit our website www.sustainalytics.com.

Jennifer PenikettAssociate Analyst, Research [email protected]

Jung-Ho ParkAnalyst, Research [email protected]

ESG Ins ight ASIA — January 2013 15

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Amsterdam | Bogotá | Boston | Brussels | Bucharest | Copenhagen | Frankfurt | London | Madrid | Paris | San Francisco |Singapore | Timisoara | Toronto

Copyright ©2013 Sustainalytics. All rights reserved. No part of this report may be reproduced in any manner without the expressed written consent of Sustainalytics.

This report was drafted in accordance with the agreed work to be performed and reflects the situation as on the date of the report. The information on which this report is based has – fully or partially – been derived from third parties and is therefore subject to continuous modification. Sustainalytics observes the greatest possible care in using information and drafting reports but cannot guarantee that the report is accurate and/or complete. Sustainalytics will not accept any liability for damage arising from the use of this report, other than liability for direct damage in cases of an intentional act or omission or gross negligence on the part of Sustainalytics.

Sustainalytics will not accept any form of liability for the substance of the reports, notifications or communications drafted by Sustainalytics vis-à-vis any legal entities and/or natural persons other than its direct principal who have taken cognisance of such reports, notifications or communications in any way.

Sustainalyticswww.sustainalytics.com

For general enquiries:[email protected](+65) 6224 0766