Asian insuranceAsian insurance - Actuaries Institute · KSJ &AD Fire ndai n gbu n Re IAG S UN Q...

34

Asian insurance Asian insurance What do investors think of insurance companies? Scott Russell, FIAA Head of Financials Research, Asia Macquarie Capital Securities Limited 1 Harbour View Street Central Hong Kong 1 Harbour View Street, Central, Hong Kong +852-3922 3567 [email protected] November 2015 In preparing this research, we did not take into account the investment objectives, financial situation and particular needs of the reader. Before making an investment decision on the basis of this research, the reader needs to consider, with or without the assistance of an adviser, whether the advice is appropriate in light of their particular investment needs, objectives and financial circumstances. Please see disclaimer.

Transcript of Asian insuranceAsian insurance - Actuaries Institute · KSJ &AD Fire ndai n gbu n Re IAG S UN Q...

Asian insuranceAsian insuranceWhat do investors think of insurance companies?

Scott Russell, FIAAHead of Financials Research, Asia

Macquarie Capital Securities Limited1 Harbour View Street Central Hong Kong1 Harbour View Street, Central, Hong Kong

+852-3922 [email protected]

November 2015

In preparing this research, we did not take into account the investment objectives, financial situation and particular needs of the reader. Before making an investment decision on the basis of this research, the reader needs to consider, with or without the assistance of an adviser, whether the advice is appropriate in light of their particular investment needs, objectives and financial circumstances. Please see disclaimer.

Agendag

1. Overview

2. Quantitative factors

3. Qualitative factors

4. Putting it together

5. Summary

2

Investor conundrums Asia offers some of the most and least attractive insurance markets globally

Which countries offer the best/worst investment opportunities?

Life or Non-life?

Growth or value? What holding period?

What changes will regulators and Government make?What changes will regulators and Government make?

Where are stock markets, FX rates and interest rates going?

What is the right price to buy/sell?

3

Agendag

1. Overview

2. Quantitative factors

3. Qualitative factors

4. Putting it together

5. Summary

4

Quantitative factors Market share, scale and volume growth Distribution channel trends Persistency Margins Returns on capital Returns on capital Solvency Leverage Asset allocation & investment returns EV composition & trends Volatilityy Sensitivity to external factors Valuation

5

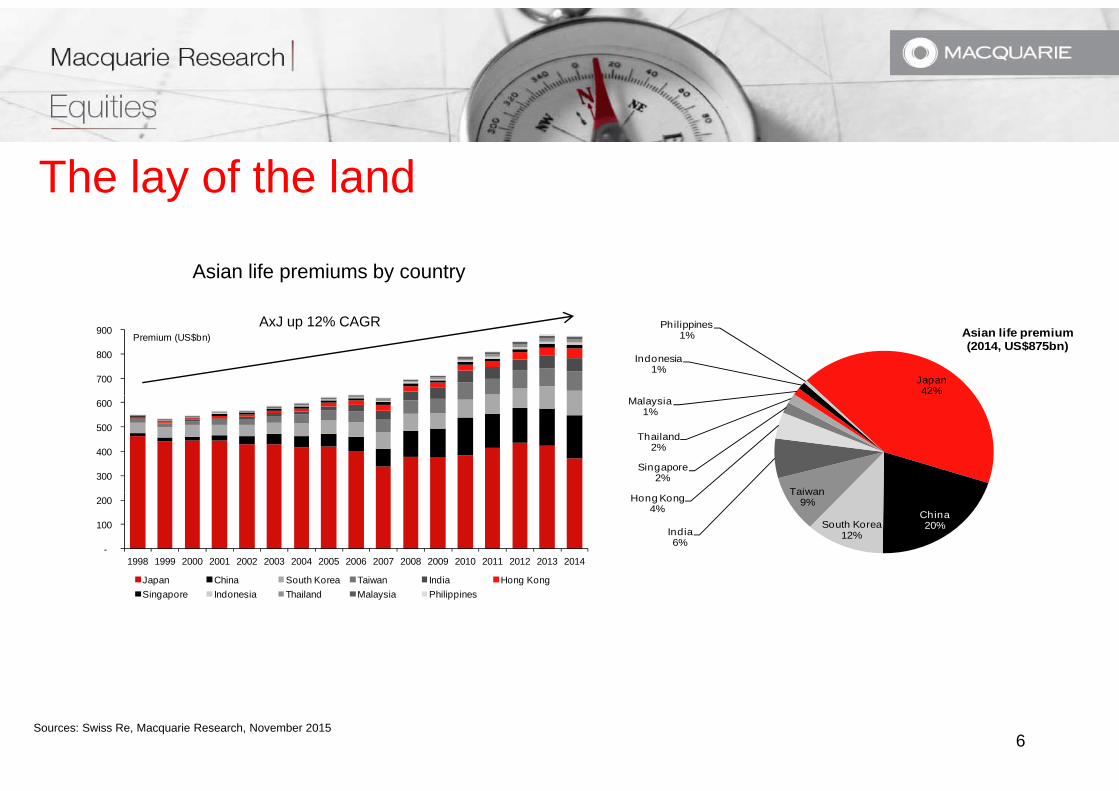

The lay of the landy

Asian life premiums by country

700

800

900 Premium (US$bn)

Japan42%

Indonesia1%

Philippines1% Asian life premium

(2014, US$875bn)

AxJ up 12% CAGR

300

400

500

600

Taiwan

Singapore2%

Thailand2%

Malaysia1%

-

100

200

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Japan China South Korea Taiwan India Hong Kong

China20%South Korea

12%

Taiwan9%

India6%

Hong Kong4%

Singapore Indonesia Thailand Malaysia Philippines

Sources: Swiss Re, Macquarie Research, November 20156

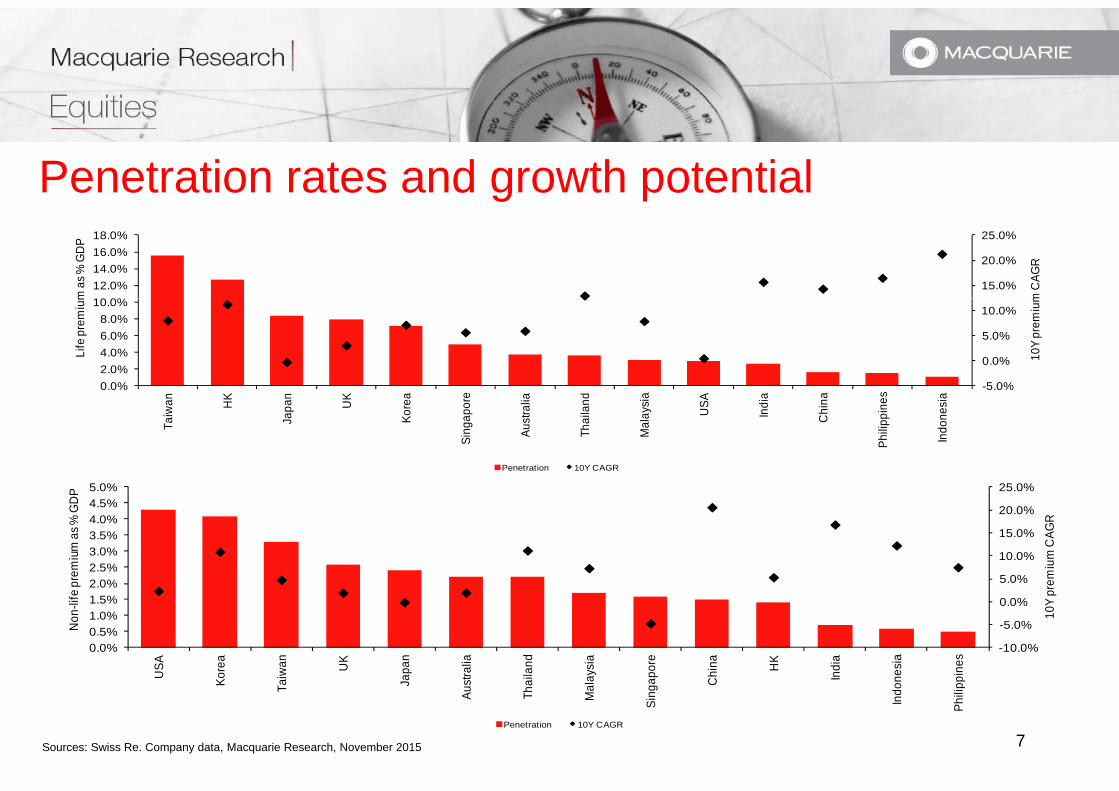

Penetration rates and growth potentialg

15.0%

20.0%

25.0%

10 0%12.0%14.0%16.0%18.0%

m C

AGR

m a

s % G

DP

-5.0%

0.0%

5.0%

10.0%

0.0%2.0%4.0%6.0%8.0%

10.0%

n K n K a e a d a A a a s a

10Y

prem

ium

Life

pre

miu

m

Taiw

an HK

Japa

n

UK

Kore

a

Sing

apor

e

Aust

ralia

Thai

land

Mal

aysi

a

USA

Indi

a

Chi

na

Phili

ppin

es

Indo

nesi

a

Penetration 10Y CAGR

25.0%5.0%P

5.0%

10.0%

15.0%

20.0%

2.0%2.5%3.0%3.5%4.0%4.5%

rem

ium

CAG

R

prem

ium

as %

GD

P

-10.0%

-5.0%

0.0%

0.0%0.5%1.0%1.5%

USA

Kore

a

Taiw

an UK

Japa

n

stra

lia

aila

nd

alay

sia

gapo

re

Chi

na HK

Indi

a

ones

ia

ppin

es

10Y

p

Non

-life

Sources: Swiss Re. Company data, Macquarie Research, November 2015

T Au Th Ma

Sing Indo

Phili

p

Penetration 10Y CAGR

7

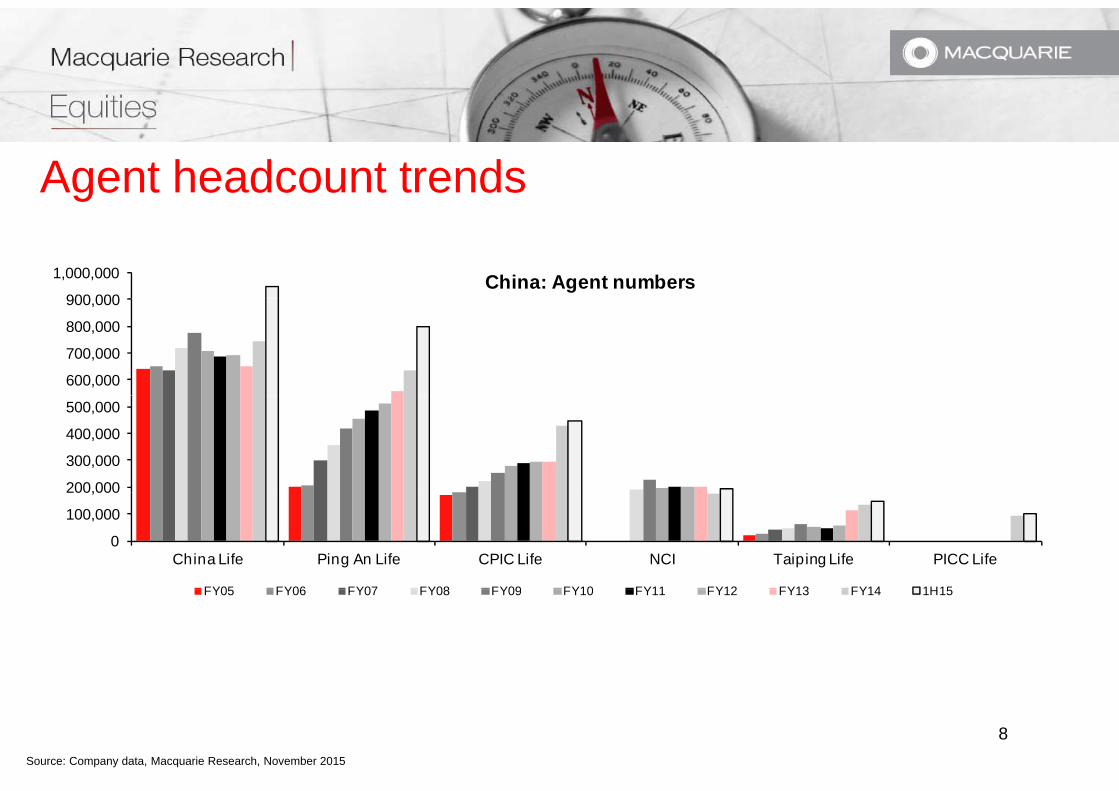

Agent headcount trendsg

900 000

1,000,000 China: Agent numbers

600,000

700,000

800,000

900,000

200,000

300,000

400,000

500,000

0

100,000

200,000

China Life Ping An Life CPIC Life NCI Taiping Life PICC Life

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 1H15FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 1H15

Source: Company data, Macquarie Research, November 2015

8

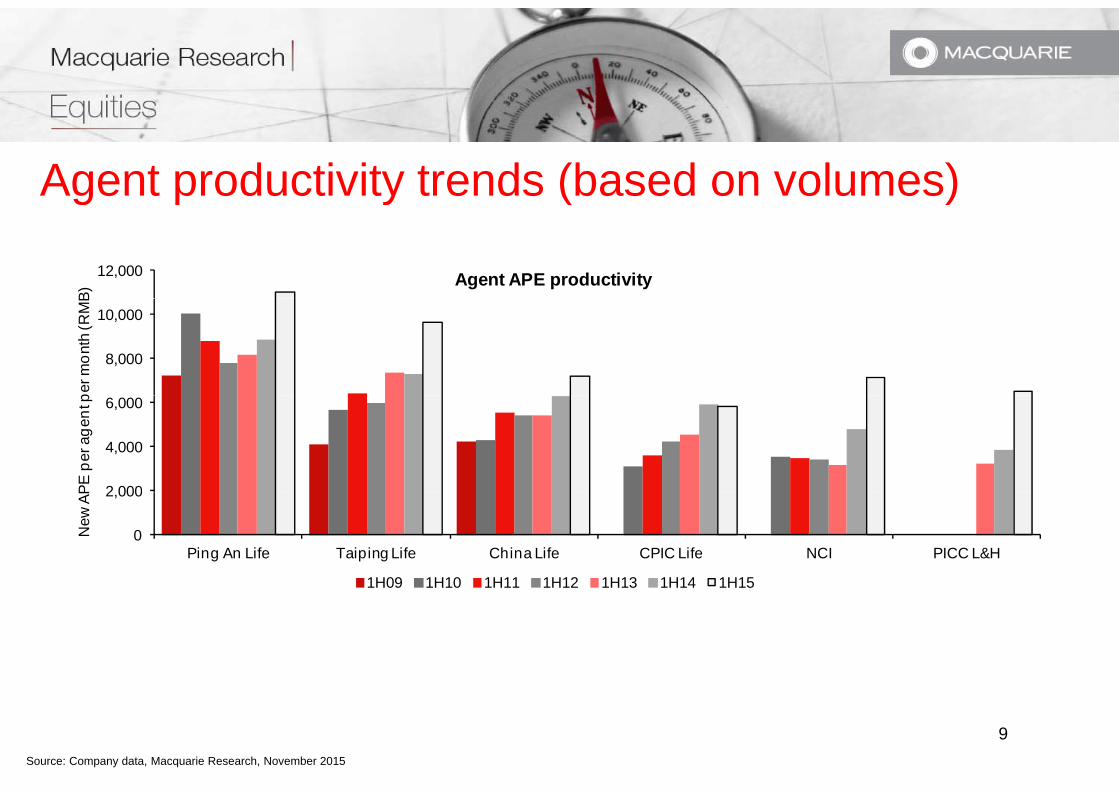

Agent productivity trends (based on volumes)g p y ( )

12,000

B)

Agent APE productivity

8,000

10,000

per m

onth

(RM

B

2 000

4,000

6,000

PE p

er a

gent

p

0

2,000

Ping An Life Taiping Life China Life CPIC Life NCI PICC L&H

New

AP

1H09 1H10 1H11 1H12 1H13 1H14 1H15

Source: Company data, Macquarie Research, November 2015

9

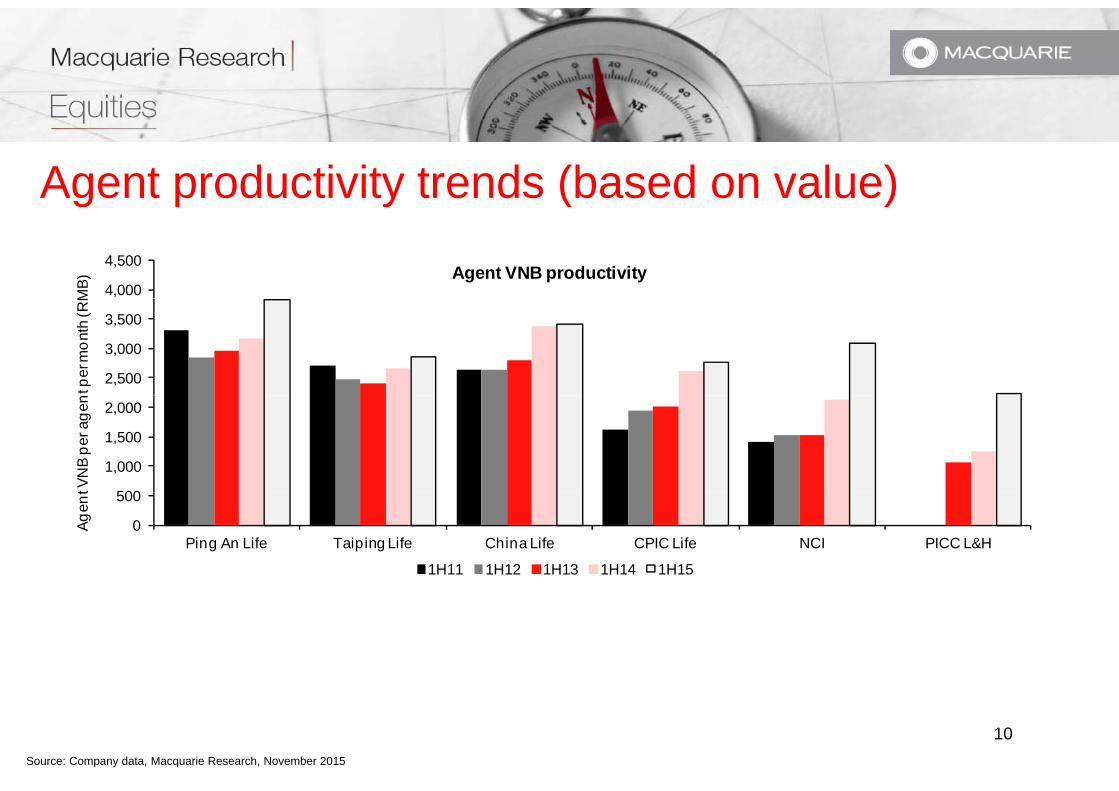

Agent productivity trends (based on value)g p y ( )

4,000

4,500

MB)

Agent VNB productivity

2,500

3,000

3,500

t per

mon

th (R

M

500

1,000

1,500

2,000

t VN

B pe

r age

n

0

500

Ping An Life Taiping Life China Life CPIC Life NCI PICC L&H

Agen

t

1H11 1H12 1H13 1H14 1H15

Source: Company data, Macquarie Research, November 2015

10

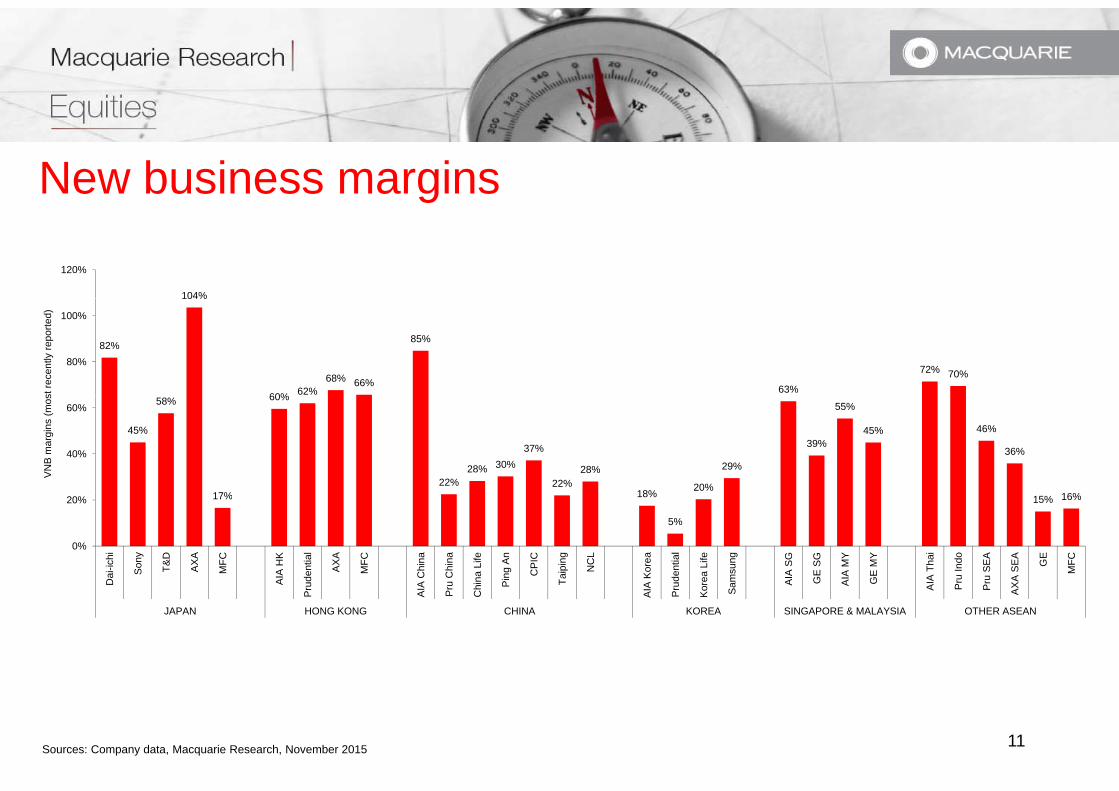

New business marginsg

104%

120%

82%

104%

60% 62%68% 66%

85%

63%

72% 70%80%

100%

st re

cent

ly re

porte

d)

45%

58%

17%

60%

22%28% 30%

37%

22%28%

18% 20%

29%

39%

55%

45% 46%

36%40%

60%

VN

B m

argi

ns (m

os

17% 18%

5%

15% 16%

0%

20%

Dai

-ichi

Son

y

T&D

AX

A

MFC

AIA

HK

rude

ntia

l

AX

A

MFC

IA C

hina

ru C

hina

hina

Life

Pin

g A

n

CP

IC

Taip

ing

NC

L

A K

orea

rude

ntia

l

orea

Life

Sam

sung

AIA

SG

GE

SG

AIA

MY

GE

MY

AIA

Tha

i

Pru

Indo

Pru

SE

A

AX

A S

EA

GE

MFC

Pr

AI Pr

Ch

AI Pr

Ko S A P P A

JAPAN HONG KONG CHINA KOREA SINGAPORE & MALAYSIA OTHER ASEAN

Sources: Company data, Macquarie Research, November 2015 11

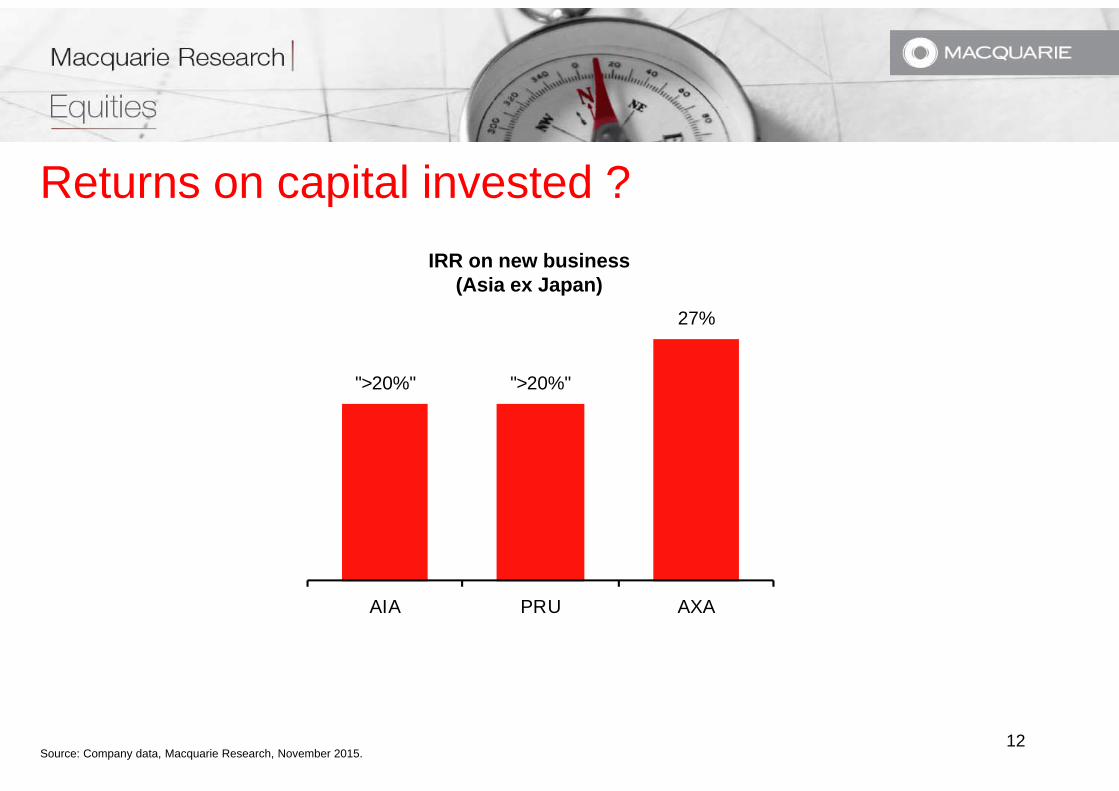

Returns on capital invested ?pIRR on new business

(Asia ex Japan)

">20%" ">20%"

27%

AIA PRU AXA

Source: Company data, Macquarie Research, November 2015. 12

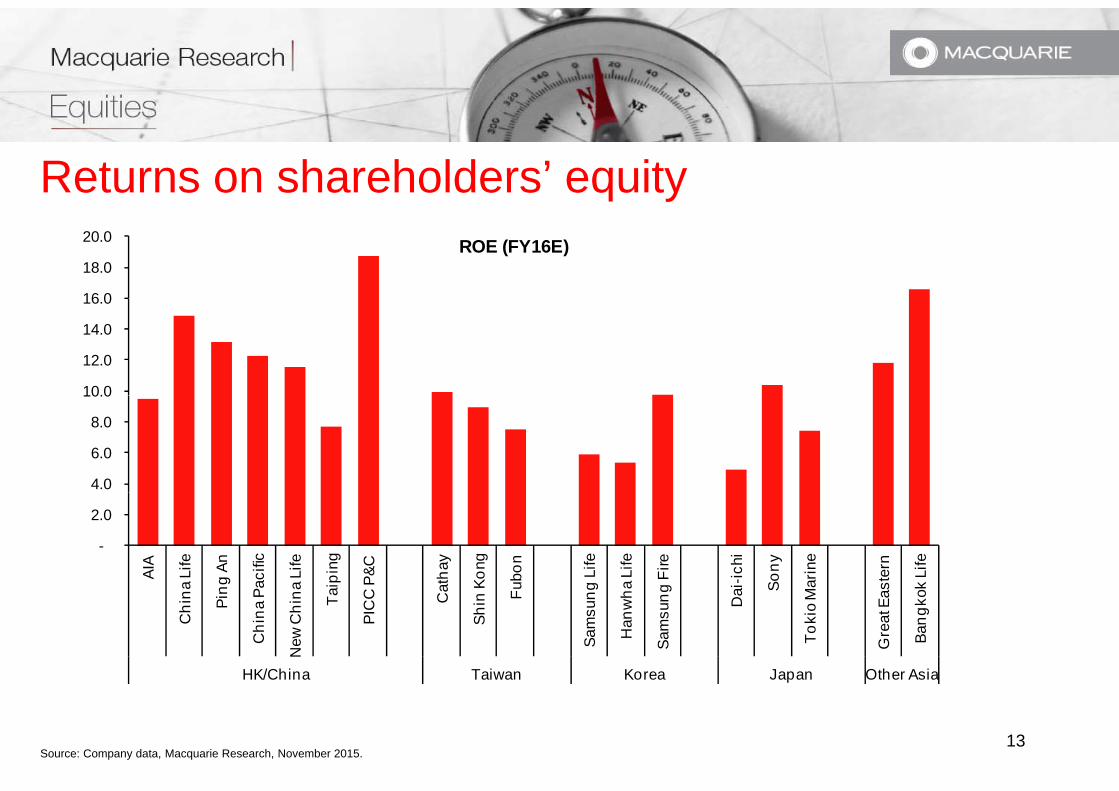

Returns on shareholders’ equityy

16 0

18.0

20.0 ROE (FY16E)

10.0

12.0

14.0

16.0

4.0

6.0

8.0

10.0

-

2.0

AIA

a Li

fe

ng A

n

Paci

fic

a Li

fe

aipi

ng

C P

&C

atha

y

Kong

ubon

g Li

fe

a Li

fe

g Fi

re

ai-ic

hi

Sony

Mar

ine

ster

n

k Li

fe

Chi

n Pin

Chi

na P

New

Chi

na Ta

PIC

C Ca

Shin

F

Sam

sun g

Han

wh

Sam

sung Da S

Toki

o M

Gre

at E

as

Bang

ko

HK/China Taiwan Korea Japan Other Asia

Source: Company data, Macquarie Research, November 2015. 13

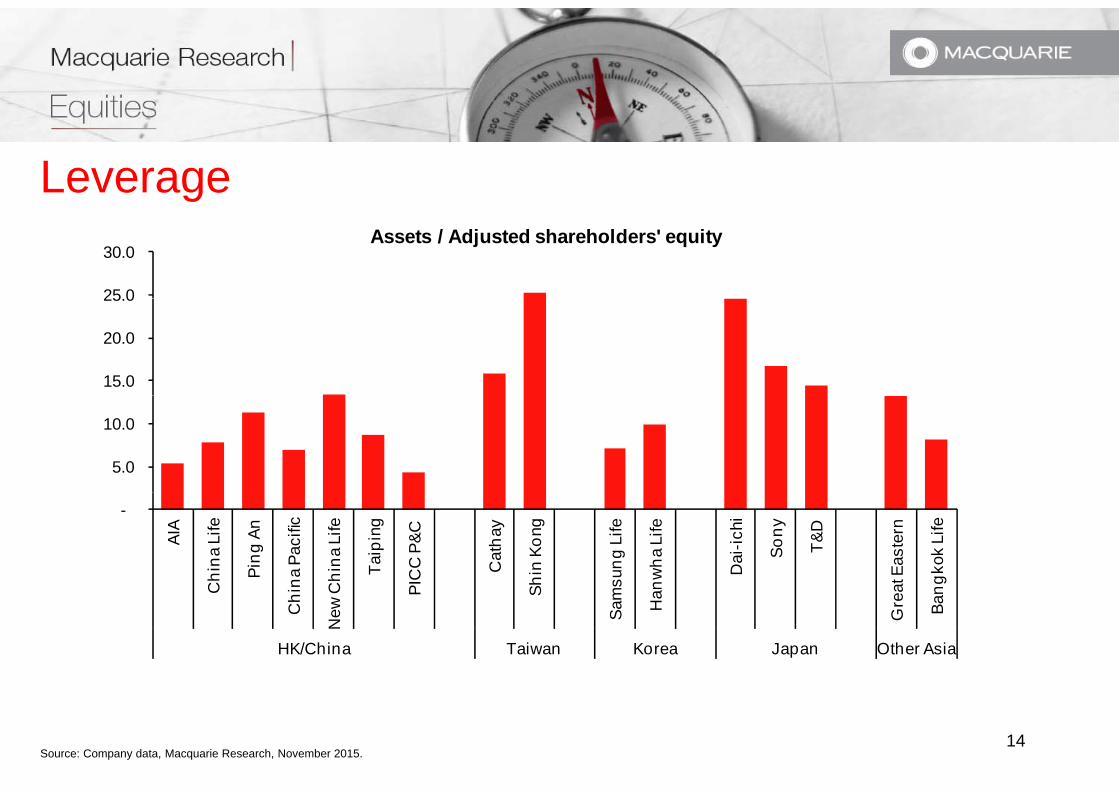

Leverageg

25 0

30.0 Assets / Adjusted shareholders' equity

15.0

20.0

25.0

5.0

10.0

-

AIA

Chi

na L

ife

Ping

An

na P

acifi

c

Chi

na L

ife

Taip

ing

PIC

C P

&C

Cat

hay

Shin

Kon

g

msu

ng L

ife

nwha

Life

Dai

-ichi

Sony

T&D

at E

aste

rn

ngko

k Li

fe

C

Chi

New

C P S

Sam Ha

Gre

a

Ban

HK/China Taiwan Korea Japan Other Asia

Source: Company data, Macquarie Research, November 2015. 14

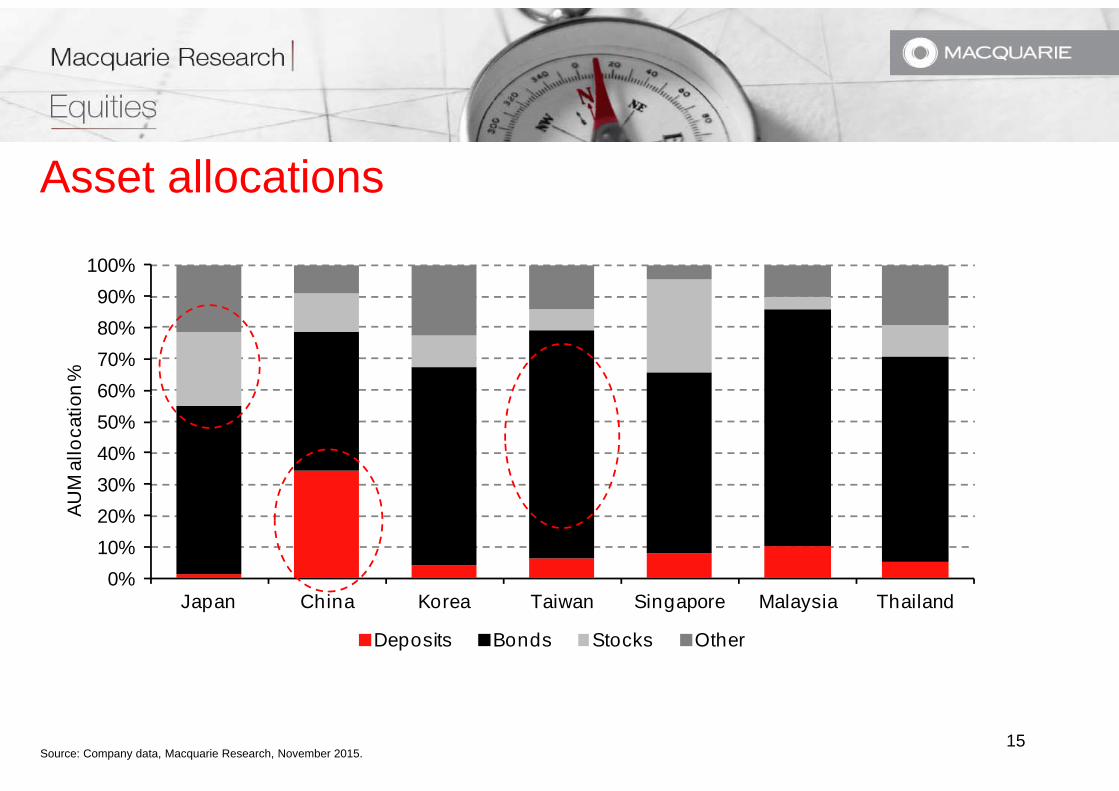

Asset allocations

90%100%

60%70%80%90%

n %

30%40%50%60%

UM

allo

catio

0%10%20%AU

Japan China Korea Taiwan Singapore Malaysia Thailand

Deposits Bonds Stocks Other

Source: Company data, Macquarie Research, November 2015. 15

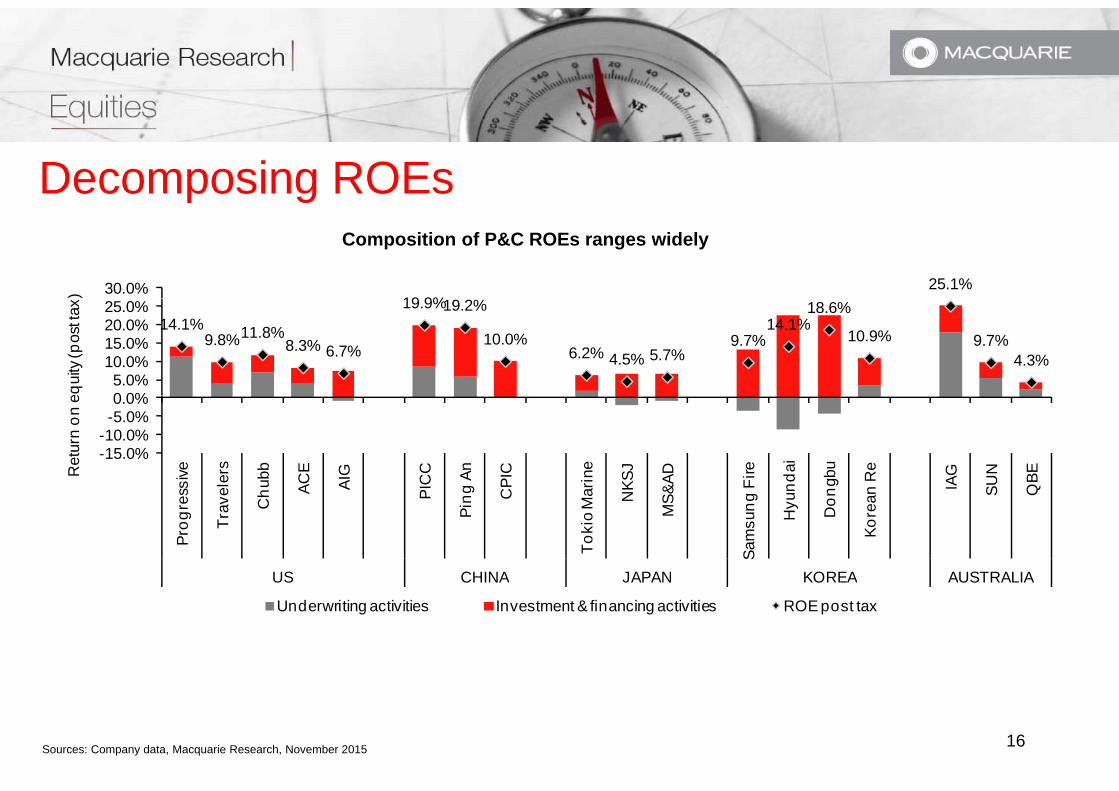

Decomposing ROEsp gComposition of P&C ROEs ranges widely

19 9%25.1%30.0%)

14.1%9.8%11.8%

8.3% 6.7%

19.9%19.2%

10.0%6.2% 4.5% 5.7%

9.7%14.1%

18.6%

10.9% 9.7%4.3%

0 0%5.0%

10.0%15.0%20.0%25.0%

equi

ty (p

ost t

ax

-15.0%-10.0%-5.0%0.0%

ssive

eler

s

hubb

ACE

AIG

PIC

C

g An

CPI

C

arin

e

NKS

J

&AD

Fire

ndai

ngbu

n R

e

IAG

SUN

QBER

etur

n on

e

Prog

res

Trav

e

Ch A P

Ping C

Toki

o M

a N

MS&

Sam

sung Hyu Do n

Kore

an S Q

US CHINA JAPAN KOREA AUSTRALIA

Underwriting activities Investment & financing activities ROE post tax

Sources: Company data, Macquarie Research, November 2015 16

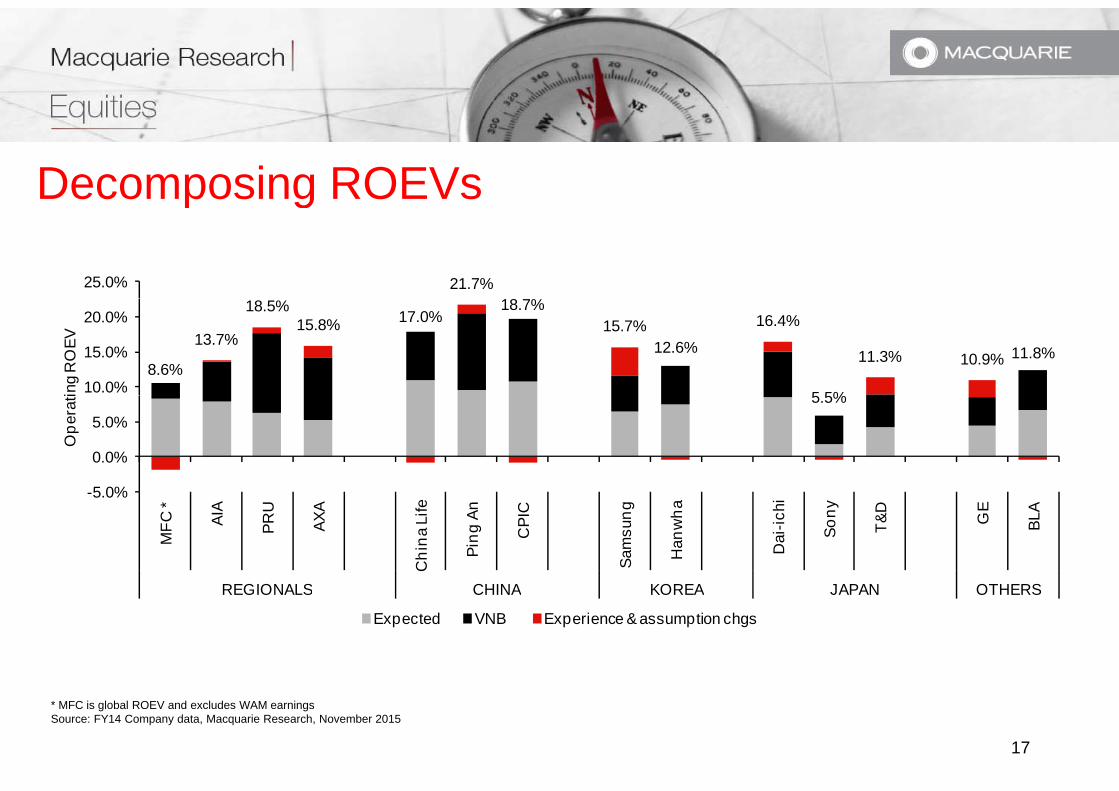

Decomposing ROEVsp g

21.7%%

25.0%

8.6%

13.7%

18.5%15.8% 17.0%

18.7%15.7%

12.6%

16.4%

5 5%

11.3% 10.9% 11.8%

10.0%

15.0%

20.0%

ing

RO

EV

5.5%

5 0%

0.0%

5.0%

Ope

rati

-5.0%

MFC

*

AIA

PRU

AXA

Chi

na L

ife

Ping

An

CPI

C

Sam

sung

Han

wha

Dai

-ichi

Sony

T&D

GE

BLA

REGIONALS CHINA KOREA JAPAN OTHERSREGIONALS CHINA KOREA JAPAN OTHERS

Expected VNB Experience & assumption chgs

* MFC is global ROEV and excludes WAM earningsSource: FY14 Company data, Macquarie Research, November 2015

17

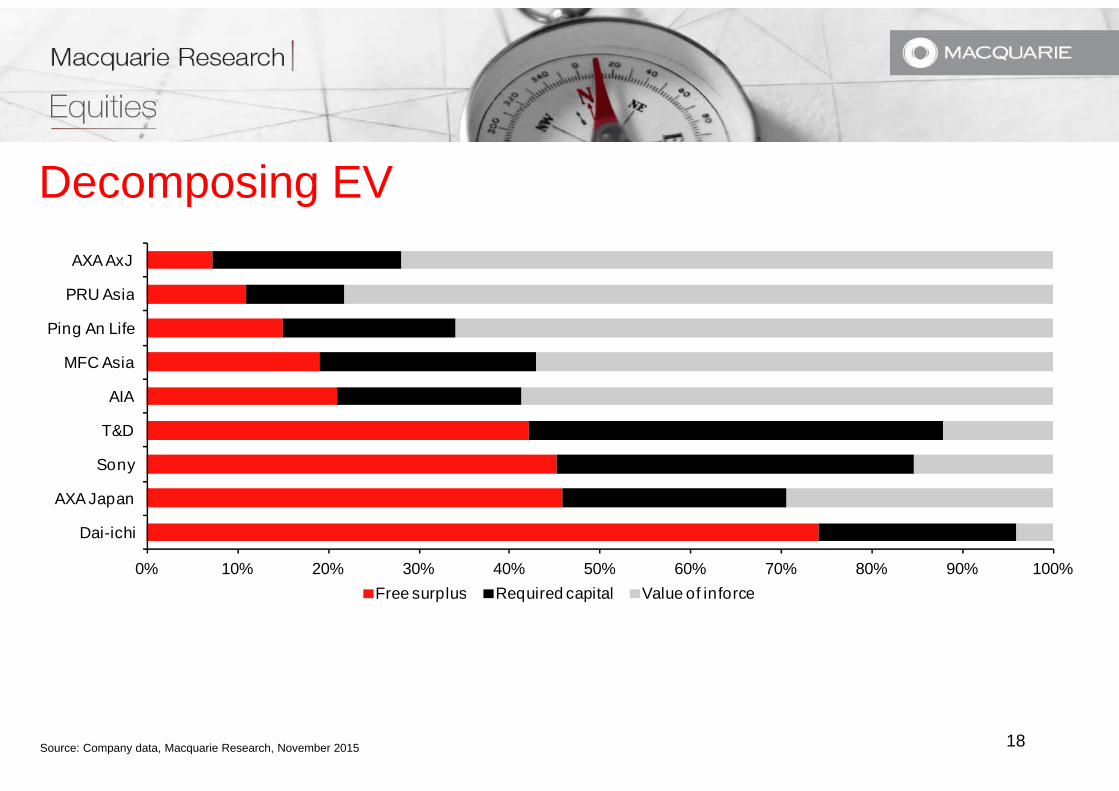

Decomposing EVp g

PRU Asia

AXA AxJ

AIA

MFC Asia

Ping An Life

PRU Asia

Sony

T&D

AIA

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Dai-ichi

AXA Japan

F l R i d it l V l f i fFree surplus Required capital Value of inforce

Source: Company data, Macquarie Research, November 2015 18

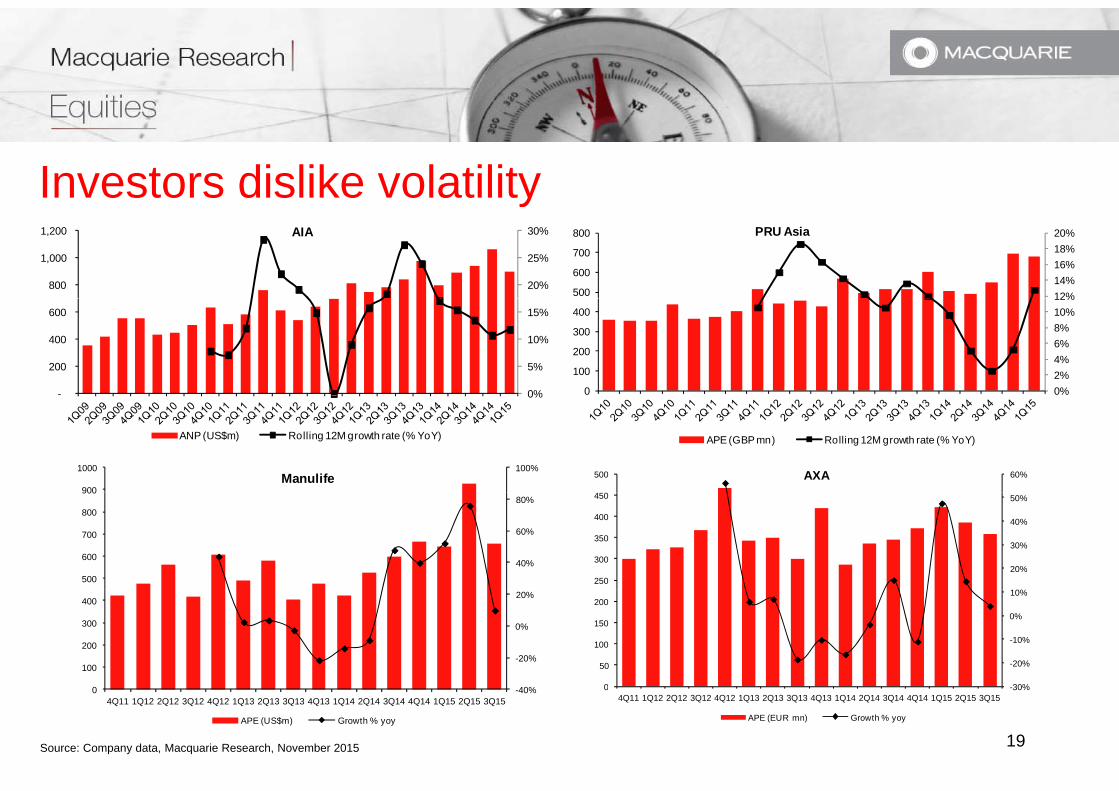

Investors dislike volatilityy

20%

25%

30%

800

1,000

1,200 AIA

12%14%16%18%20%

500

600

700

800 PRU Asia

0%

5%

10%

15%

-

200

400

600

0%2%4%6%8%10%12%

0

100

200

300

400

0%

ANP (US$m) Rolling 12M growth rate (% YoY) APE (GBP mn) Rolling 12M growth rate (% YoY)

100%

900

1000Manulife 60%500 AXA

40%

60%

80%

500

600

700

800

900

20%

30%

40%

50%

250

300

350

400

450

-20%

0%

20%

100

200

300

400

30%

-20%

-10%

0%

10%

0

50

100

150

200

Source: Company data, Macquarie Research, November 2015 19

-40%04Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15

APE (US$m) Growth % yoy

-30%04Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15

APE (EUR mn) Growth % yoy

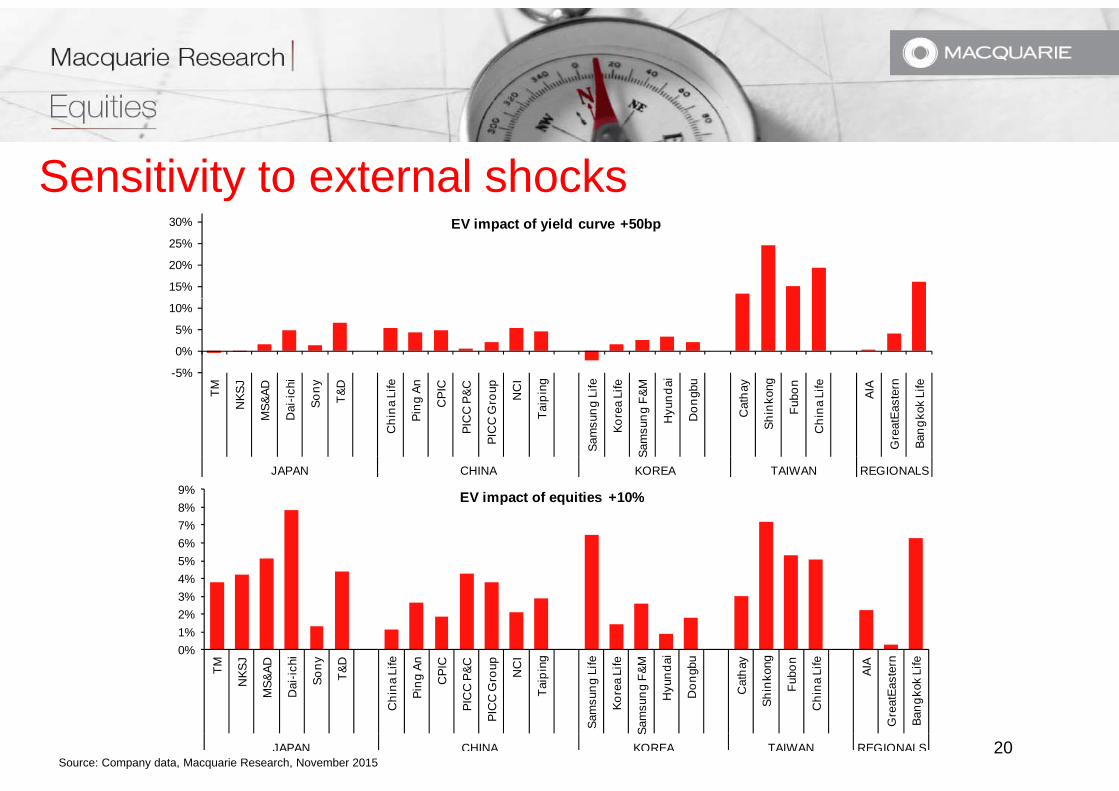

Sensitivity to external shocks

15%

20%

25%

30% EV impact of yield curve +50bp

-5%

0%

5%

10%

TM KSJ

AD chi

ony

&D Life An PIC

&C oup

NC

I

ing

Life

Life &M da

i

gbu

hay

ong

bon

Life

AIA ern

Life

9% EV i t f iti 10%

T

NK

MS&

A

Dai

-i So T

Chi

na L

Ping

CP

PIC

C P

&

PIC

C G

ro N

Taip

Sam

sung

L

Kore

a L

Sam

sung

F&

Hyu

n

Don

g

Cat

h

Shin

ko

Fub

Chi

na L A

Gre

atEa

st

Bang

kok

L

JAPAN CHINA KOREA TAIWAN REGIONALS

4%5%6%7%8%9% EV impact of equities +10%

0%1%2%3%

TM

NKS

J

S&AD

ai-ic

hi

Sony

T&D

na L

ife

ng A

n

CPI

C

C P

&C

Gro

up NC

I

aipi

ng

g Li

fe

ea L

ife

g F&

M

unda

i

ongb

u

atha

y

nkon

g

Fubo

n

na L

ife AIA

aste

rn

ok L

ife

Source: Company data, Macquarie Research, November 201520

MS

Da

Chi

n Pin

PIC

C

PIC

C G Ta

Sam

sun

Kore

Sam

sung Hy Do C

Shi n F

Chi

n

Gre

atEa

Bang

ko

JAPAN CHINA KOREA TAIWAN REGIONALS

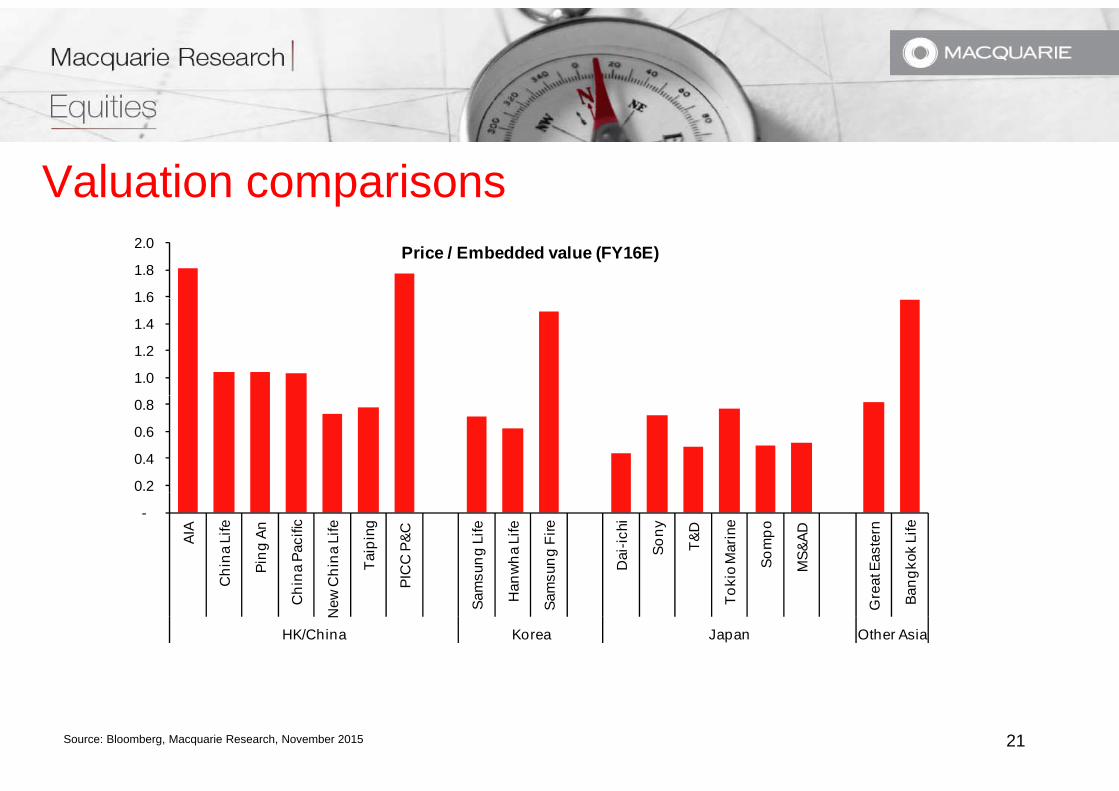

Valuation comparisonsp

1 6

1.8

2.0 Price / Embedded value (FY16E)

1.0

1.2

1.4

1.6

0.2

0.4

0.6

0.8

-

AIA

Chi

na L

ife

Ping

An

hina

Pac

ific

Chi

na L

ife

Taip

ing

PIC

C P

&C

msu

ng L

ife

anw

ha L

ife

msu

ng F

ire

Dai

-ichi

Sony

T&D

okio

Mar

ine

Som

po

MS&

AD

eat E

aste

rn

angk

ok L

ife

Ch

New

Sam Ha

Sam

To Gre Ba

HK/China Korea Japan Other Asia

Source: Bloomberg, Macquarie Research, November 2015 21

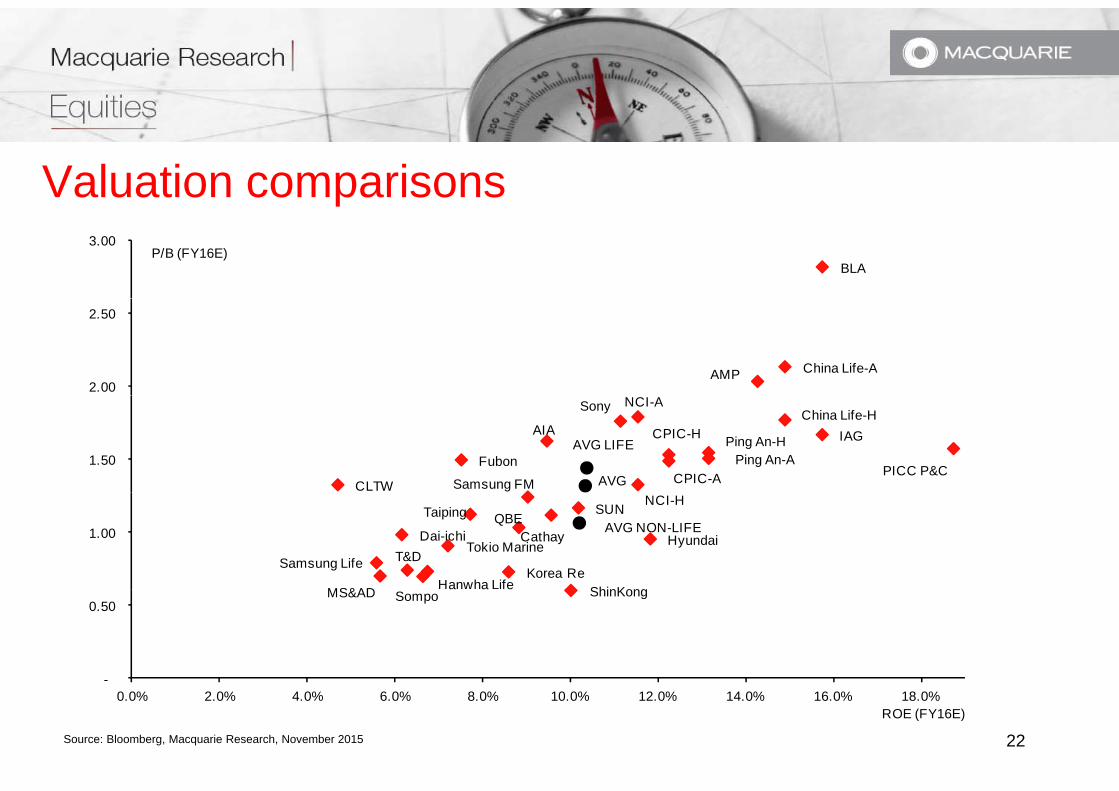

Valuation comparisonspBLA

3.00 P/B (FY16E)

China Life-AAMP2.00

2.50

China Life-H

Ping An-HCPIC-HAIA

Ping An-ACPIC-A

NCI-A

Fubon

CLTW

Sony

AVG LIFE

PICC P&CSamsung FM

IAG

AVG1.50

NCI-HTaiping

ShinKong

Cathay

Hanwha LifeSamsung Life

Dai-ichiT&D

Hyundai

Korea Re

Tokio Marine

MS&AD

QBESUN

AVG NON-LIFE1.00

ShinKonga a eMS&AD Sompo

-

0.50

Source: Bloomberg, Macquarie Research, November 2015 22

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0%ROE (FY16E)

Agendag

1. Overview

2. Quantitative factors

3. Qualitative factors

4. Putting it together

5. Summary

23

Qualitative factors Business quality Management qualityg q y Corporate governance Corporate transparency Regulatory direction Regulatory direction Thematics

24

Business quality is subjectiveq y j Product mix Agent productivityAgent productivity Policy term & typical persistency Premium payment terms Margins Margins IRR

25

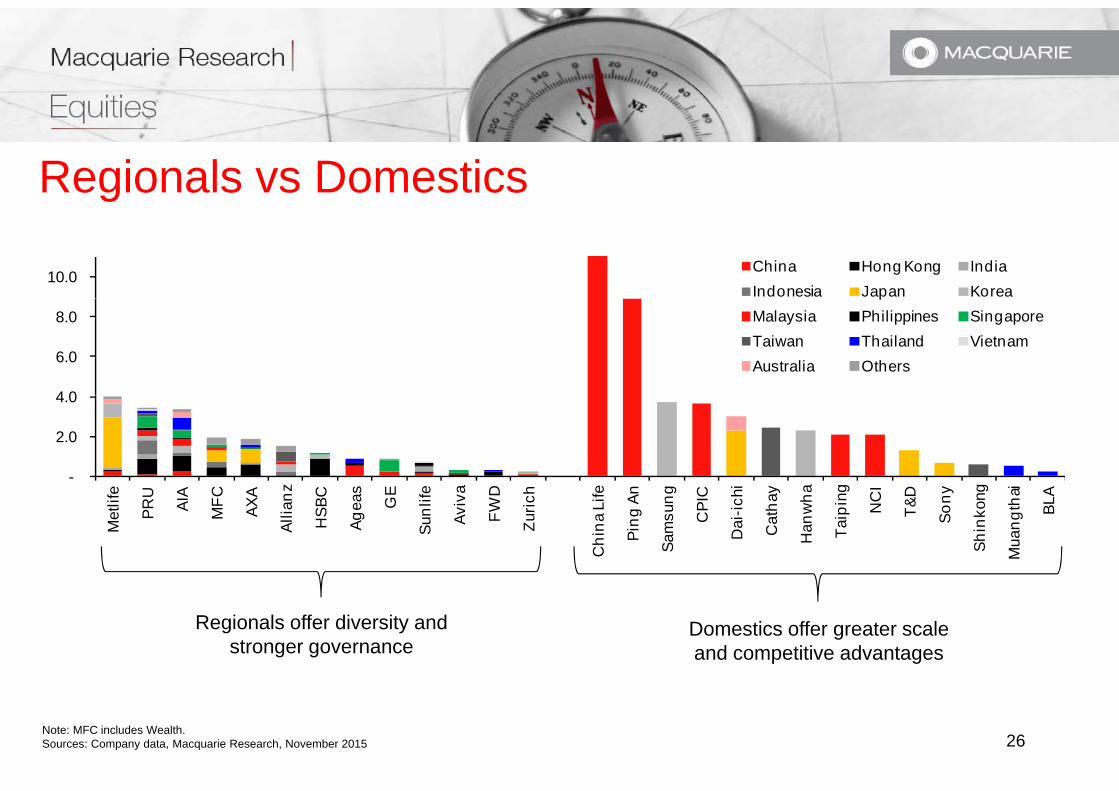

Regionals vs Domesticsg

10.0 China Hong Kong IndiaIndonesia Japan Korea

4 0

6.0

8.0 p

Malaysia Philippines SingaporeTaiwan Thailand VietnamAustralia Others

-

2.0

4.0

e U A C A z C s E e a D h e n g C hi y a g CI D y g ai A

Met

life

PRU

AIA

MFC AX

A

Allia

n

HSB

C

Agea

s

GE

Sunl

ife

Aviv

a

FWD

Zuric

h

Chi

na L

ife

Ping

An

Sam

sung

CPI

C

Dai

-ich

Cat

hay

Han

wh

Taip

in NC

T&D

Sony

Shin

kon

Mua

ngth

a

BLA

Regionals offer diversity and stronger governance

Domestics offer greater scale and competitive advantages

Note: MFC includes Wealth.Sources: Company data, Macquarie Research, November 2015 26

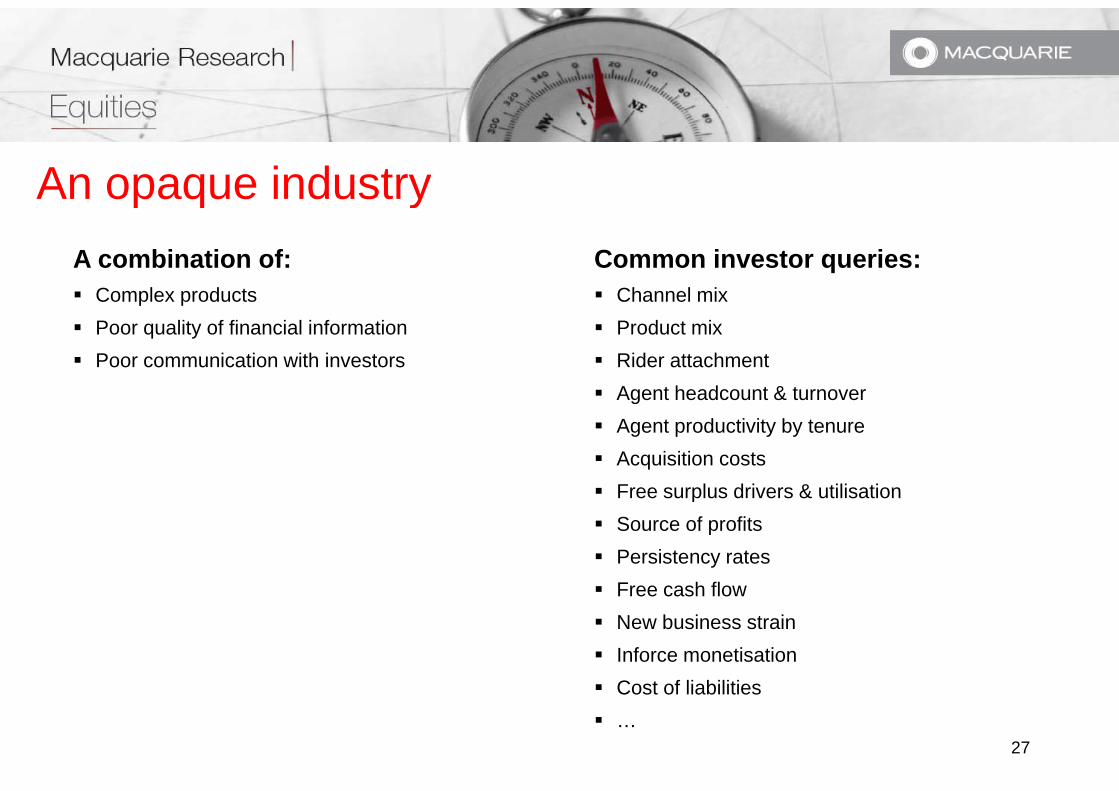

An opaque industryp q yA combination of: Complex products

Common investor queries: Channel mixComplex products

Poor quality of financial information Poor communication with investors

Channel mix Product mix Rider attachment Agent headcount & turnover Agent headcount & turnover Agent productivity by tenure Acquisition costs Free surplus drivers & utilisation Free surplus drivers & utilisation Source of profits Persistency rates Free cash flow Free cash flow New business strain Inforce monetisation Cost of liabilities

27

Cost of liabilities …

Regulatory directiong yO

LDER

S

OLD

ERS

OLI

CYH

O

HA

REH

O

PO SH

28

Thematics

What long-term themes will drive the market?

Demographics Government policy & reformsGovernment policy & reforms New market opportunities Agent professionalism

P t ti b k t Penetrating bank customers Technology & the internet Recruitment

29

Agendag

1. Overview

2. Quantitative factors

3. Qualitative factors

4. Putting it together

5. Summary

30

Investor conundrums Asia offers some of the most and least attractive insurance markets globally

Which countries offer the best/worst investment opportunities?

Life or Non-life?

Growth or value? What holding period?

What changes will regulators and Government make?What changes will regulators and Government make?

Where are stock markets, FX rates and interest rates going?

What is the right price to buy/sell?

31

Which markets do investors like?Views by market, in order of preference:

China: Underdeveloped, savings-focused market with strong demographics, regulation and margins. Indonesia: Strong growth supported by favourable demographics & a lack of personal safety nets Indonesia: Strong growth supported by favourable demographics & a lack of personal safety nets. Hong Kong: One of the more profitable life markets in the world, with growth supported by mainland ties. Philippines: Similar dynamics to Indonesia on a smaller scale, and earlier in its development. Thailand: Excellent demographics will support growth albeit increasingly into lower margin bancassurance Thailand: Excellent demographics will support growth, albeit increasingly into lower-margin bancassurance. Singapore: Recent regulatory trends have been favourable for both volumes & margins, but we see this

reversing. Malaysia: Penetration opportunity remains elusive regulation turning more consumeristMalaysia: Penetration opportunity remains elusive, regulation turning more consumerist. India: Long-term potential is enormous, but regulatory and grassroots development has been poor. Japan: A highly competitive market in structural decline, pressured further by low & falling investment yields. Korea: Very little sales growth opportunity onerous regulation legacy drag albeit resilient balance sheetsKorea: Very little sales growth opportunity, onerous regulation, legacy drag, albeit resilient balance sheets. Taiwan: We have concerns for earnings & asset quality, interest sensitivity, capital adequacy and FX risks.

32

Investor (mis)perceptions( )p p• Ageing population is good for life insurers

• Protection products are high quality. Savings products are low quality

• Bancassurance is largely deposit replacement

• Wealth management is low margin

• The internet will eventually disrupt traditional insurance modelsThe internet will eventually disrupt traditional insurance models

• Japan is saturated and therefore offers no growth

• IFRS earnings & capital suffer from rising interest rates

&C• Emerging P&C markets are usually irrational

33

In summaryy

34