Asian Banker - Core Banking Replacement

173

w w w . t h e a s i a n b a n k e r . c o m Management Report: Roadmap to Successful Core Banking System Replacement Critical Success Factor s and Best Practices

Transcript of Asian Banker - Core Banking Replacement

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 1/173

w w w . t h e a s i a n b a n k e r . c o m

Management Report:

Roadmap to SuccessfulCore Banking System Replacement

Critical Success Factor s and Best Practices

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 2/173

Neeti Aggarwal, CFA

Published September 2006©2006 The Asian Banker

Management Report:

Roadmap to Successful

Core Banking System ReplacementCritical Success Factors and Best Practices

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 3/173

IMPORTANT NOTICE Although the author and publisher have tried to provide information

as accurately as possible, they accept no responsibility for any loss,

injury or inconveniences suffered by any person using this document.

The author and publisher have taken all reasonable care to ensure

the data and information in this report is accurate and presents a fair

representation of the subject matter.

First Publication: 15 September 2006

ISBN: 981-05-6643-3

© 2006 The Asian Banker. All rights reserved

The Asian Banker, incorporated in Singapore as T.A.B. International Pte Ltd, claims all rights as owner of

intellectual property in this report. No part of this document may be reproduced, stored in a retrieval system or

transmitted in any form by any means, electronic, mechanical, photocopying, recording or otherwise, without

the written permission of the publisher and the copyright owner.

PORTANT NOTICE

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 4/173

ABOUT THE ASIAN BANKER Asia’s financial service landscape is undergoing tremendous change and evolution.Liberalisation, consolidation and rapid technological advances have opened uptremendous opportunities for financial institutions and, it is vital for banks to benchmarkthemselves against their competitors and to keep abreast of global developments.

Decision-makers need accurate, incisive, timely and continuous information to bring theirorganisation to the next level, meet competitive challenges successfully and managetheir own future. The Asian Banker has long recognised the importance of information asa strategic management and decision-making tool and is positioned to provide banks and

partner organisations useful, crucial and timely business intelligence.

The Asian Banker achieves this through three synergistic services:

As ian Banker Research: current , cont inuous and in-depth research on bestpractices and market developments and trends

Proprietary & generic research services

Subscription-based research support services for different programs

As ian Banker Publicat ions: incisive news and in formation on transformationalissues

The Asian Banker Journal

Asian Banker E-newsletters on different segments in the financial services industrysuch as operations & technology, wealth management, CRM, retail distribution and

payment systems amongst others Annual Publication: The CEO Collection; The Asian Banker 300 Banks Ranking

Special Reports on M&A; Internet Banking; Payments Systems; Retail Banking;CRM; Risk Management; Wealth Management and Operations & Technology

As ian Banker Forums: exc lusive gather ing of industry leaders and sen ior dec is ionmakers to network and exchange information

Annual Major Conferences

The Asian Banker Summit

The Future of Banking in China

Asia Pacific Heads of Retail Banking Annual Meeting

China International Risk Convention (CIRC)

Roundtable Series / Consultative Forums

Wealth Management Advisory Forum

Consumer Credit Advisory Forum

Risk Advisory Forum

Industry Briefings

Contact:

THE ASIAN BANKER

10 Hoe Chiang Road#14-06 Keppel Tower Singapore 0899315Tel: (65) 6236 6500Fax: (65) 6236 6530http://www.theasianbanker.com

•

•

•

•

•

•

•

•

•

ABOUT THE ASIAN BANKER

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 5/173

ACKNOWLEDGEMENTWe would like to convey our sincere thanks to Mr Hubert Knapp for sparing his

valuable time and providing us with important insights into core banking systems for

the preparation of this report.

Mr Knapp is one of our International Resource Directors. He is currently a Managing

Partner in Immacon Pte Ltd and holds a dual responsibility as Executive Partner in

Motif Technologies Bangkok.

Mr Knapp has 25 years of experience in the financial services industry. He specialises

in core banking enabled change, business transformation, credit risk management

and strategy development. His career in banking and consulting covers assignments

in Germany, United Kingdom, Switzerland, Turkey, Nepal, Sri Lanka, ASEAN and

many other parts of the world.

He has managed retail and wholesale banking operations for major global banks

in Europe and Asia. After his stint as Deputy General Manager of a joint-venture

merchant bank in Indonesia, his interest turned to financial services consulting. His

consulting assignments constitute a highly diversified portfolio that includes some of

the largest commercial banks in Asia.

CKNOWLEDGEMENT

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 6/173

Core BankingTransformationCritical Success Factors and Best Practices

Table of Contents

1. Core Banking Trends in Asia Pacific

Market Trends

1.1 Prominent recent deals in the region

1.2 Geographic dispersion of deals in recent years and 2006

estimates

1.3 Activity within countries and their vendor preferences

1.4 Estimates of system and software spending in Asia

Pacific

Technical Trends

1.5 Evolution and convergence of core banking systems

1.6 Technology integration in Asian countries

1.7 Trends in platform usage among Asian countries

1.8 Trends in deployment approach

2. Bankers’ Perception Survey on Core Banking System

Selection

2.1 Survey results on key reasons for replacement

2.2 Survey results on factors considered in system selection

2.3 UNIX versus mainframe – survey results on

considerations in system selection

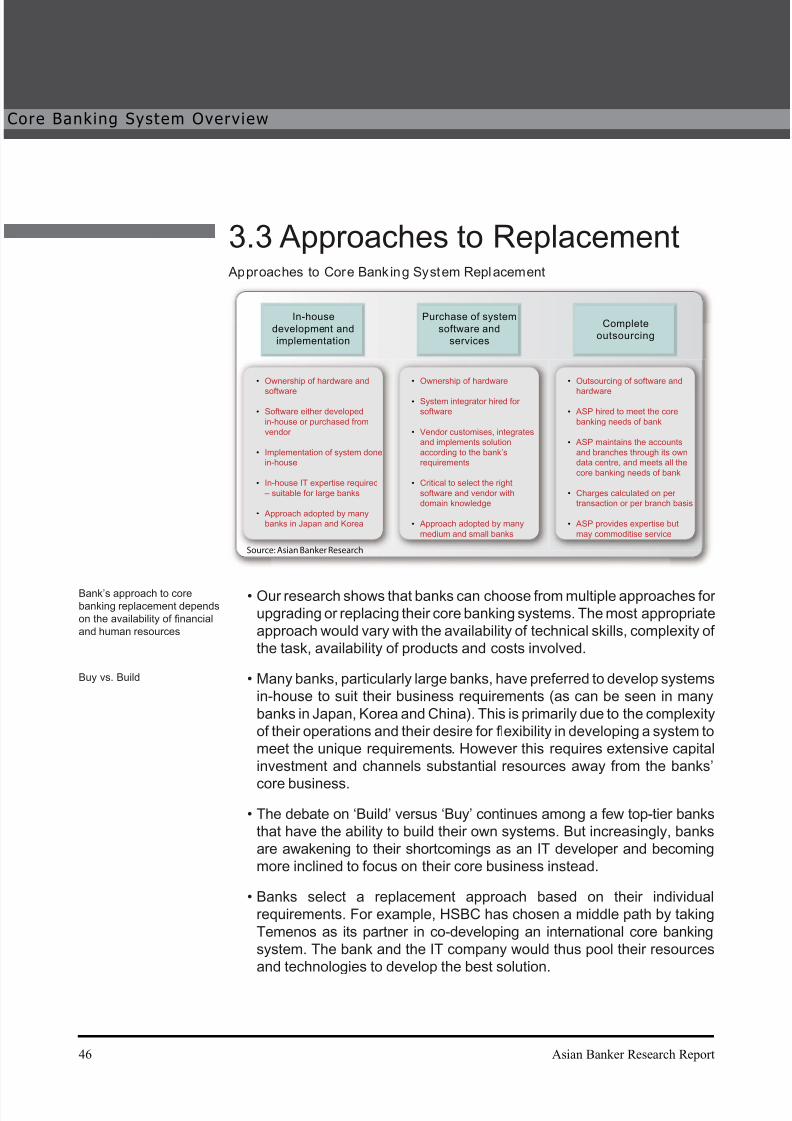

3. Core Banking System – An Overview

3.1 Core banking system – an introduction and definition

3.1.1 Definition of core banking system

3.1.2 What to expect in core banking replacement

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 7/173

3.1.3 Rationale for front-end systems replacement

3.2 Overview of the core banking system replacement

project

3.3 Approaches to replacement

4. Phases of Core Banking Replacement and Critical

Considerations

4.1 Phases of core banking replacement – an overview

4.2 Timeline of replacement project stages

4.3 Phase 1 – Business justification and blueprint

4.3.1 Developing business objectives

4.3.2 Delta methodology – assessing future requirements

4.4 Phase 2 – Selection

4.4.1 Reasons for replacement

4.4.2 Considerations in determining selection criteria

4.4.3 Key considerations in vendor selection

4.4.4 The right architecture and platform

4.4.5 Selection process

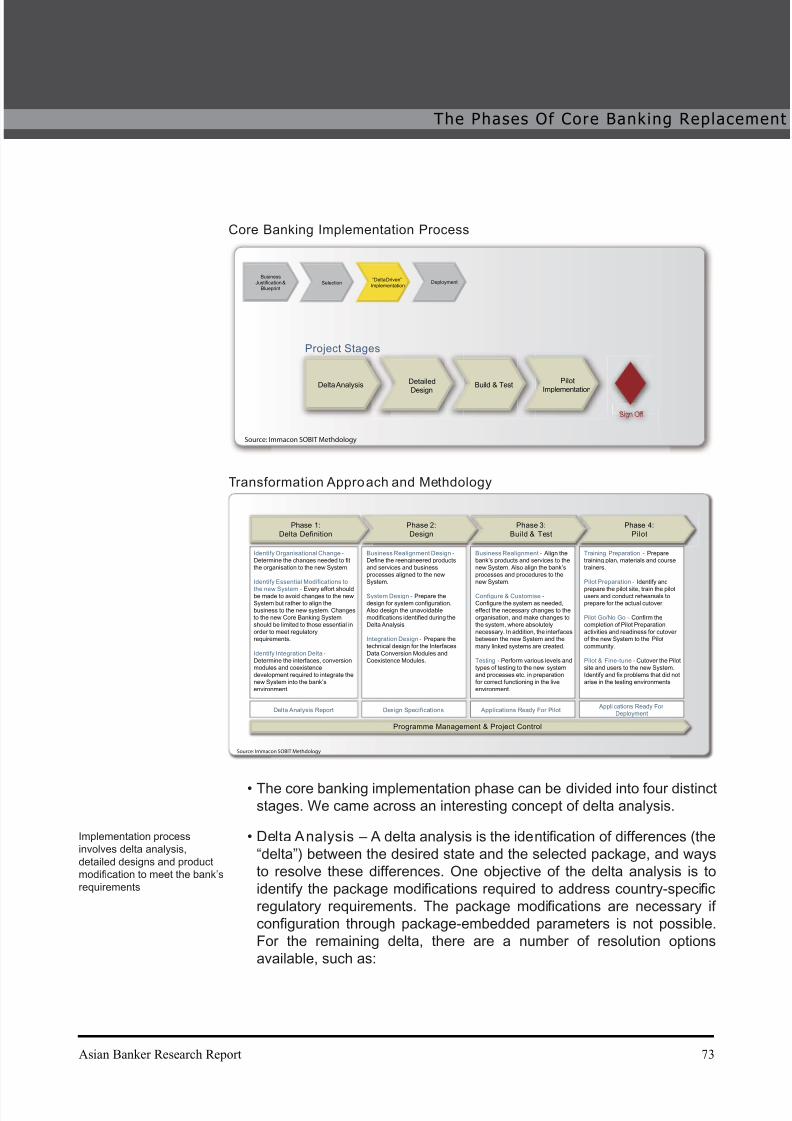

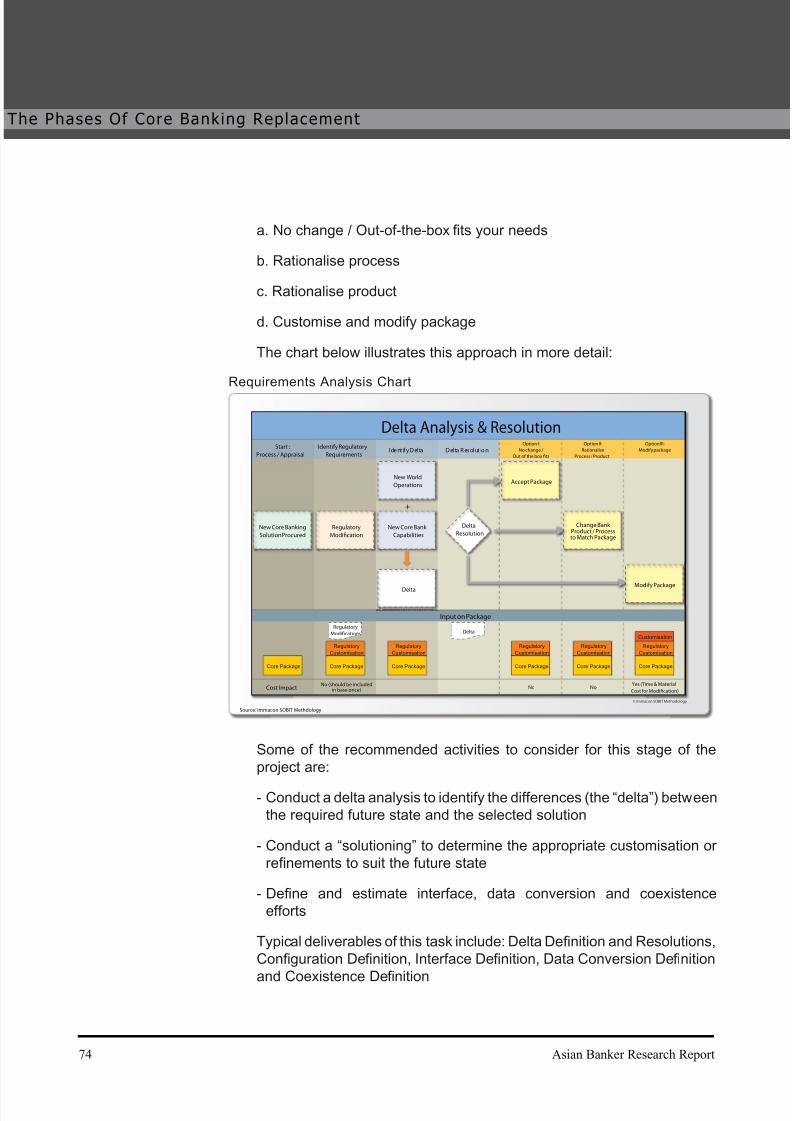

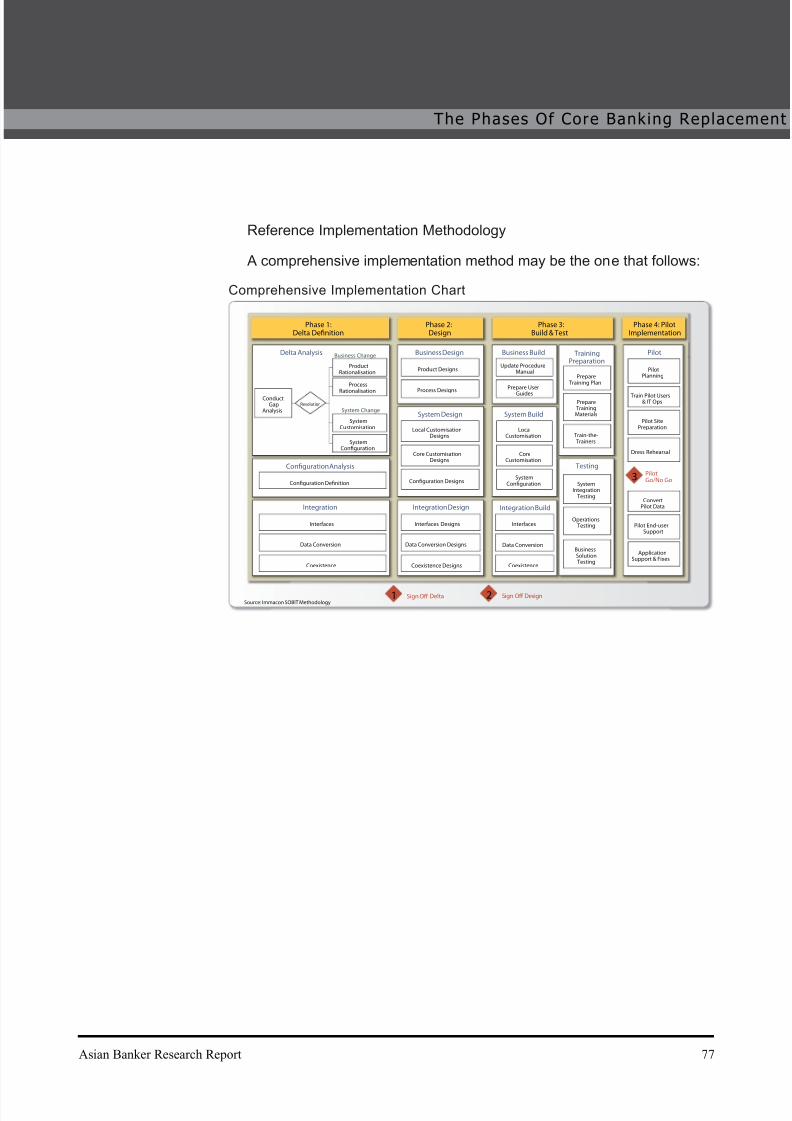

4.5 Phase 3 – Implementation

4.5.1 Key challenges and critical success factors

4.5.2 Implementation process

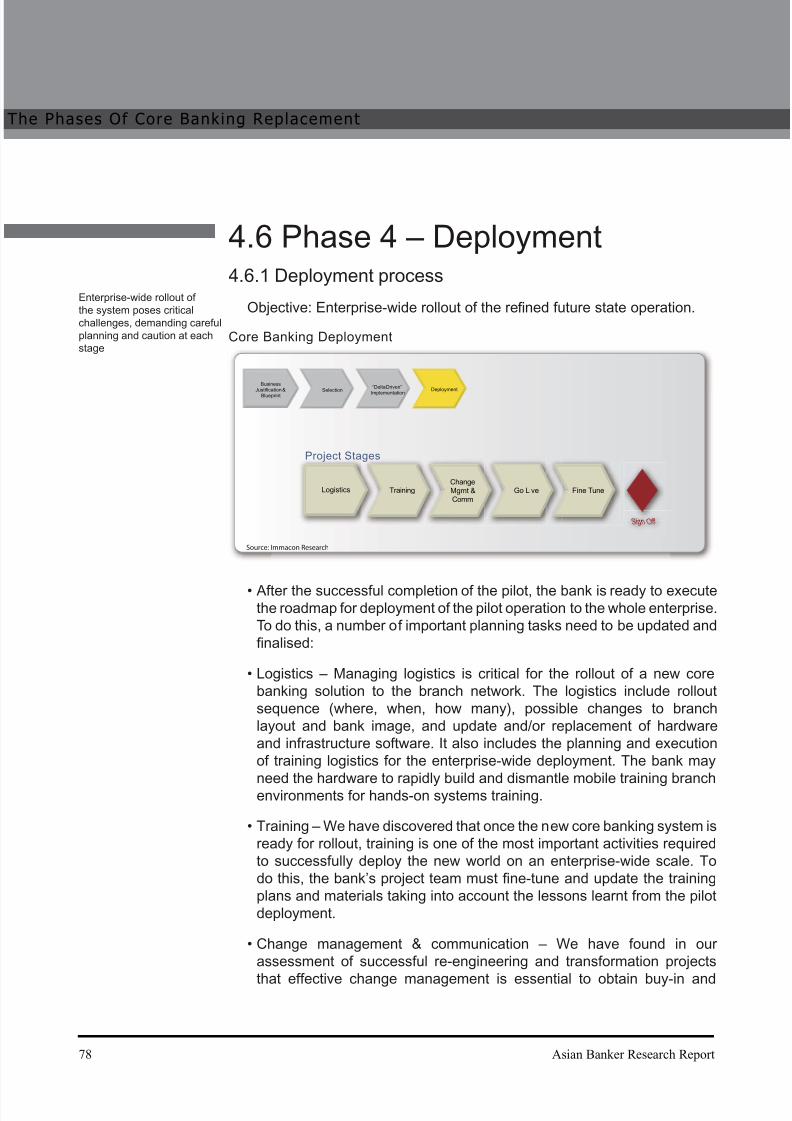

4.6 Phase 4 – Deployment

4.6.1 Deployment process

4.6.2 Deployment approaches

4.7 Risk mitigation

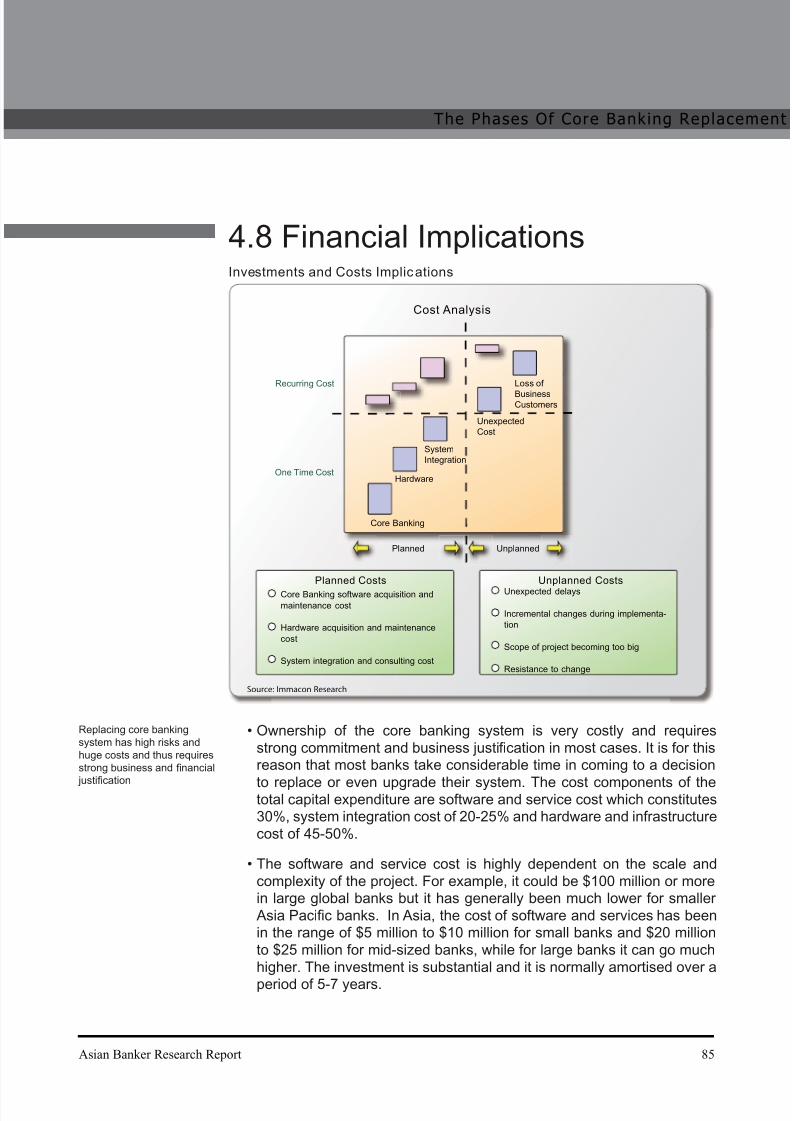

4.8 Financial implications

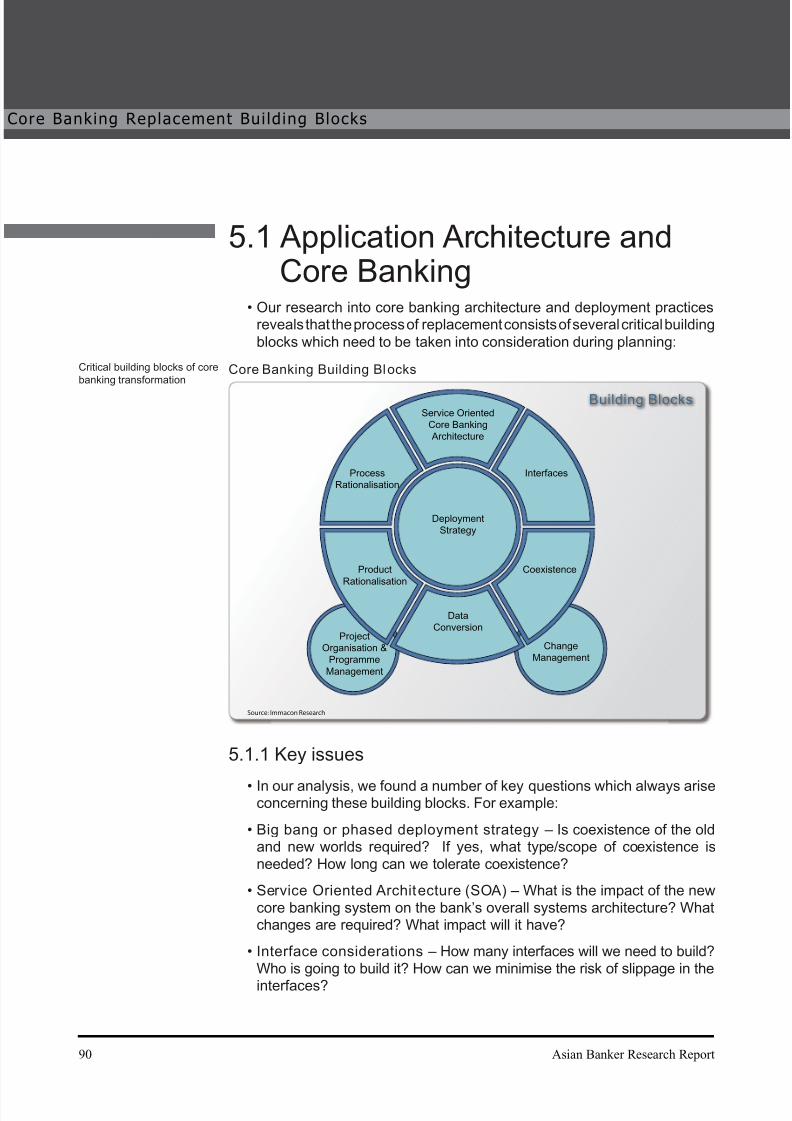

5. Core Banking Replacement Building Blocks

5.1 Application architecture and core banking

5.1.1 Key issues

5.1.2 Deployment strategy

5.2 Service oriented architecture

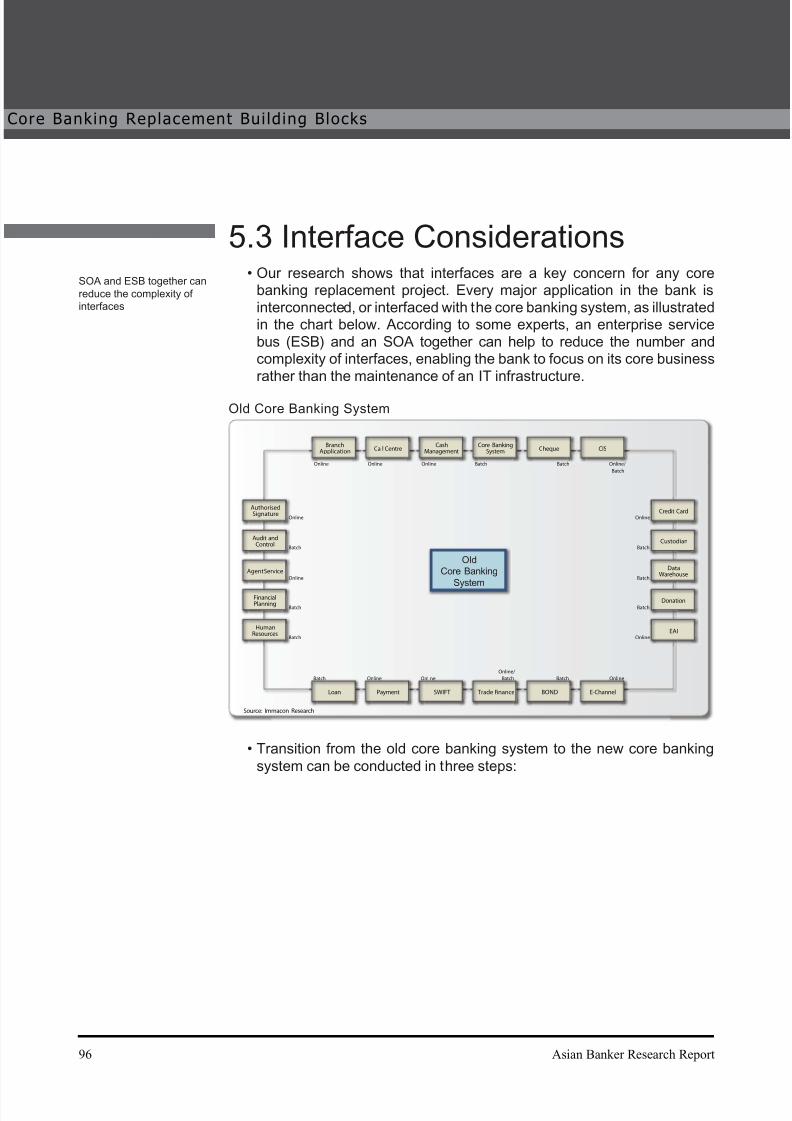

5.3 Interface considerations

5.4 Coexistence

ble of Con tents

2 Asian Banker Research Report

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 8/173

Table of Con tents

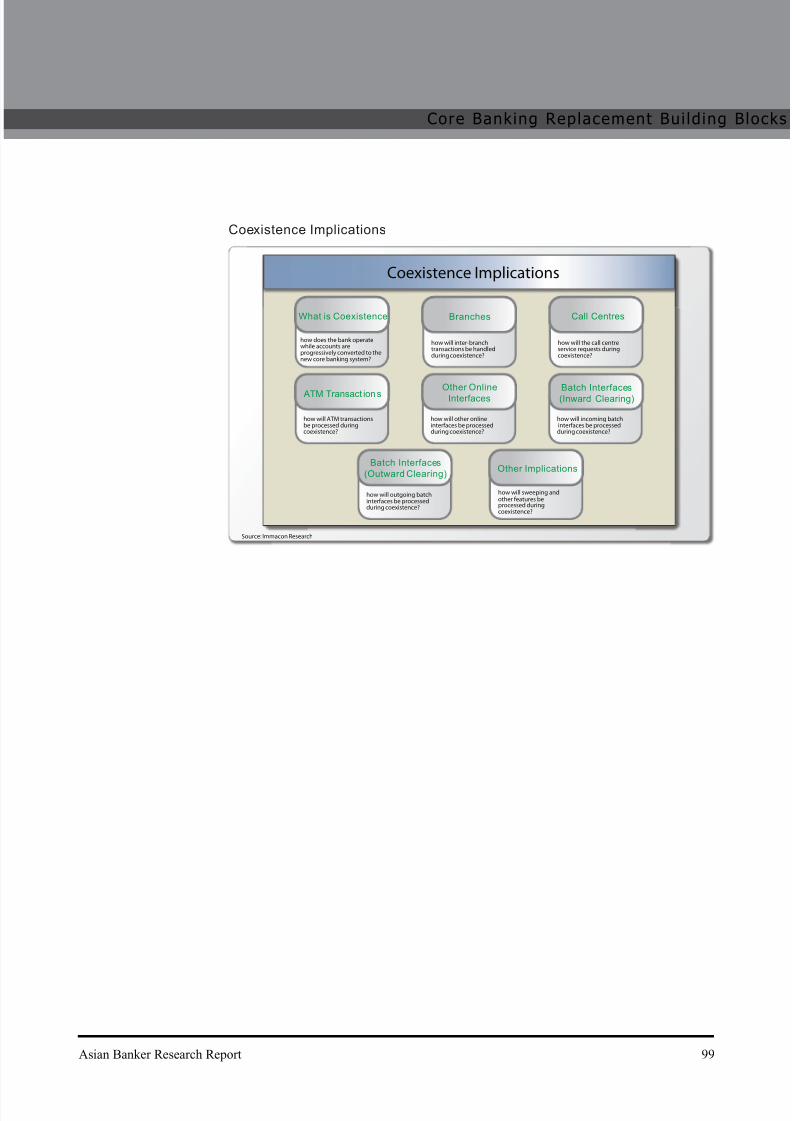

5.4.1 Branches

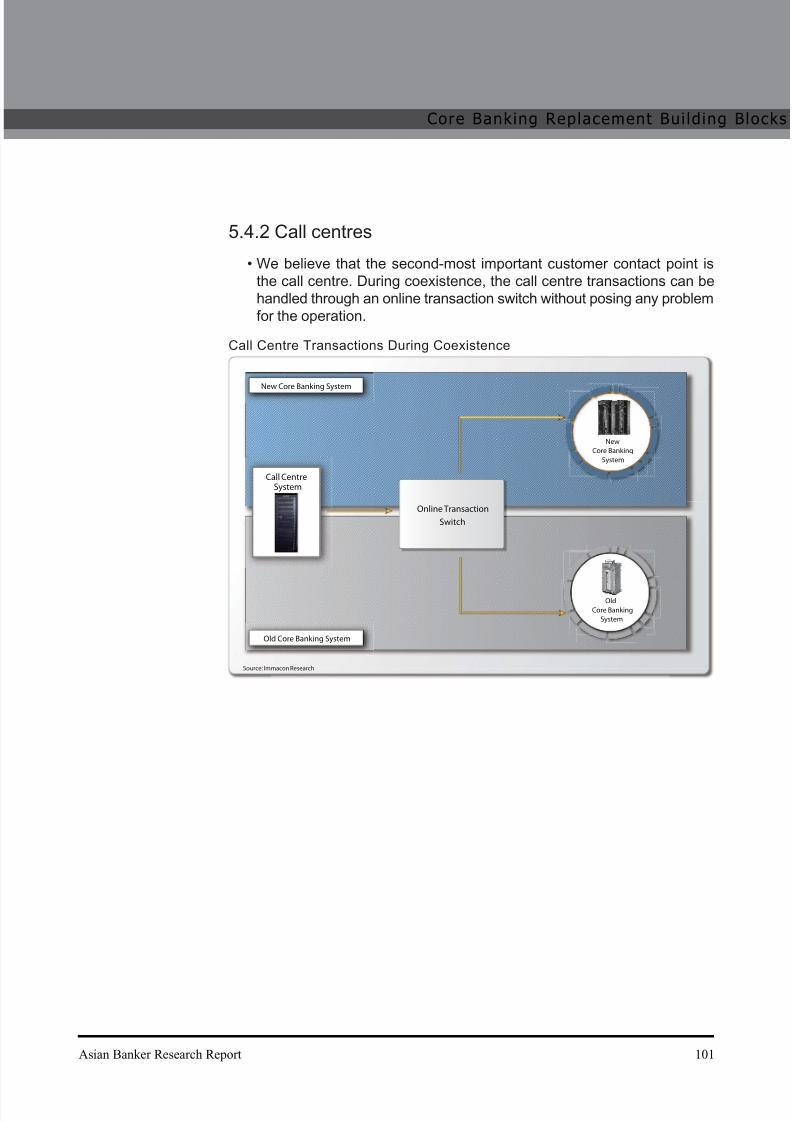

5.4.2 Call centres

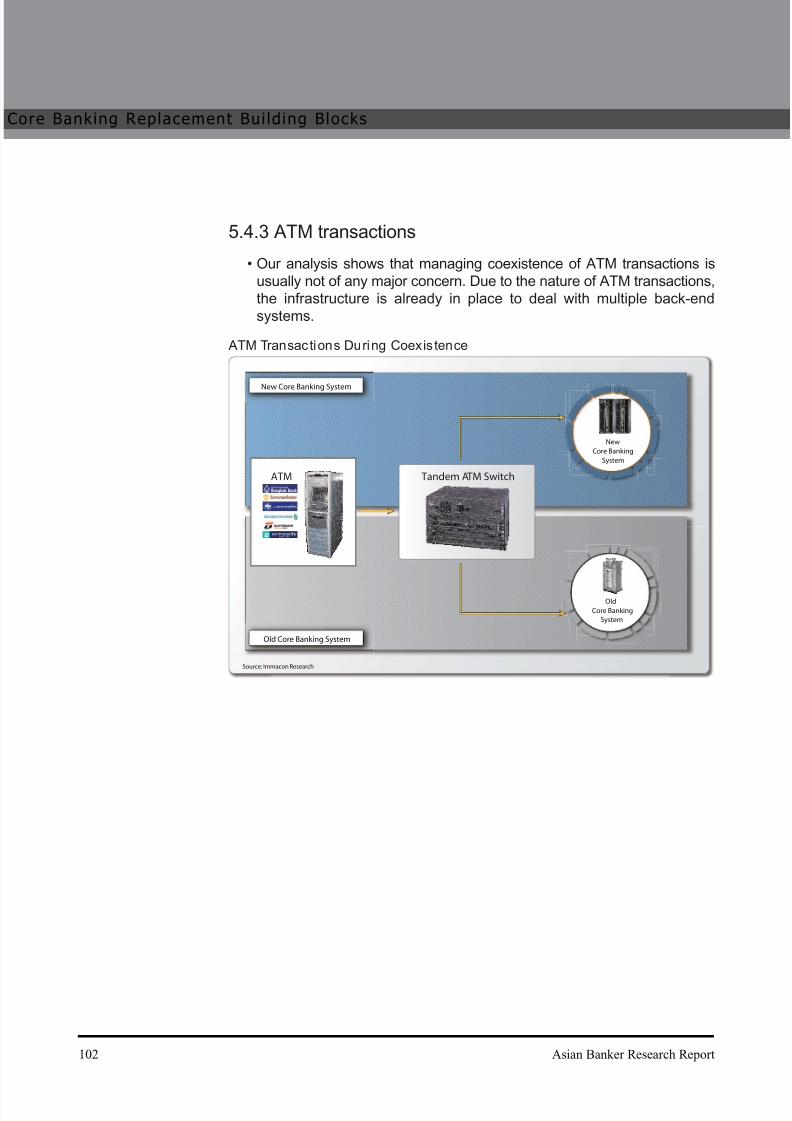

5.4.3 ATM transactions

5.4.4 Other online interfaces

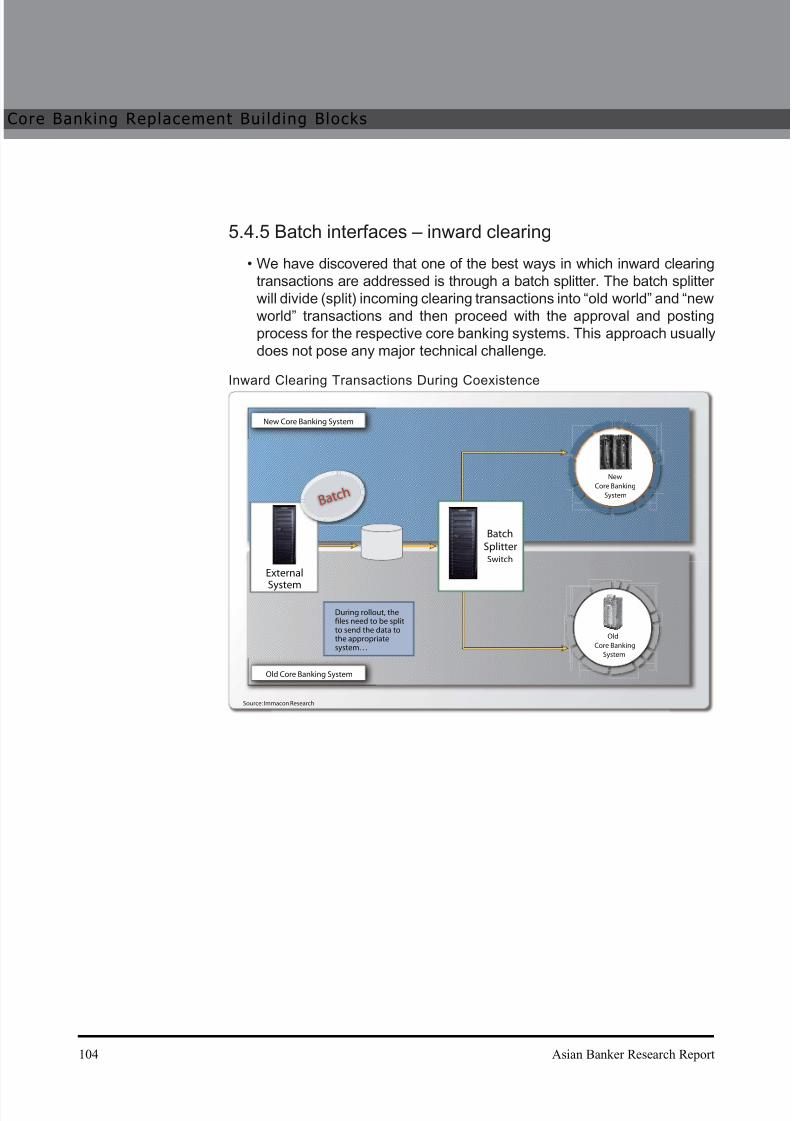

5.4.5 Batch interfaces – inward clearing

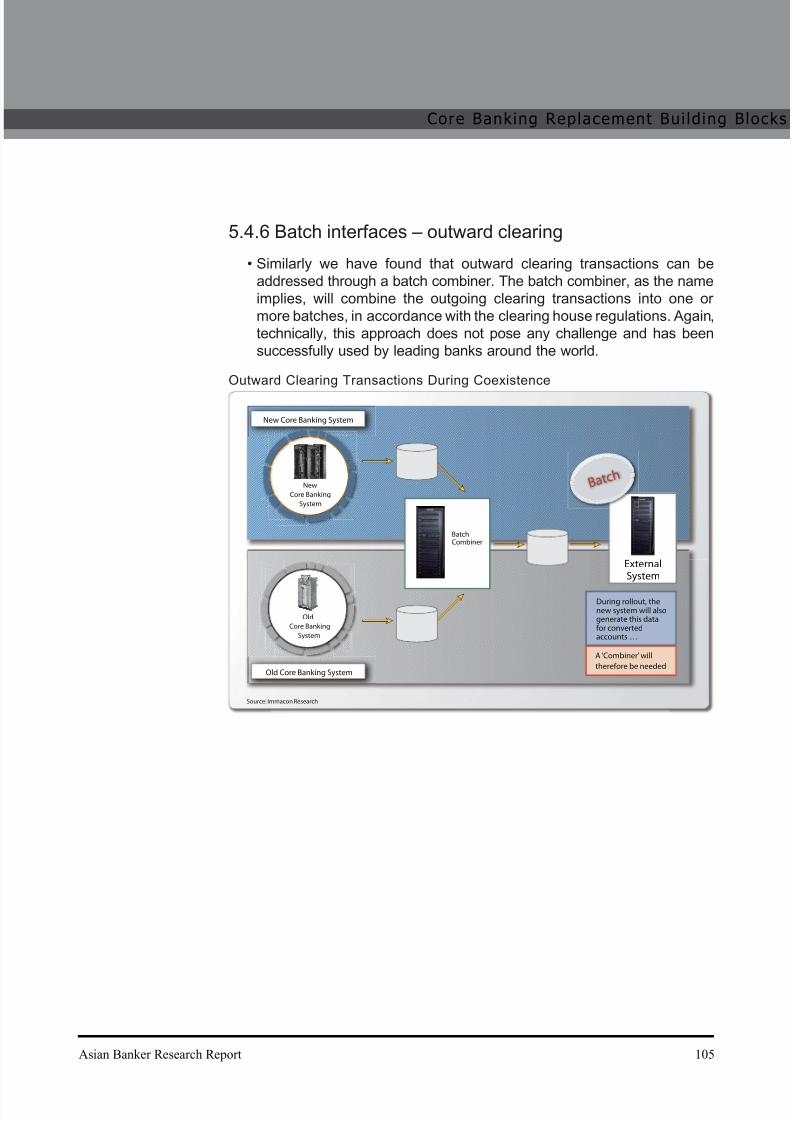

5.4.6 Batch interfaces – outward clearing

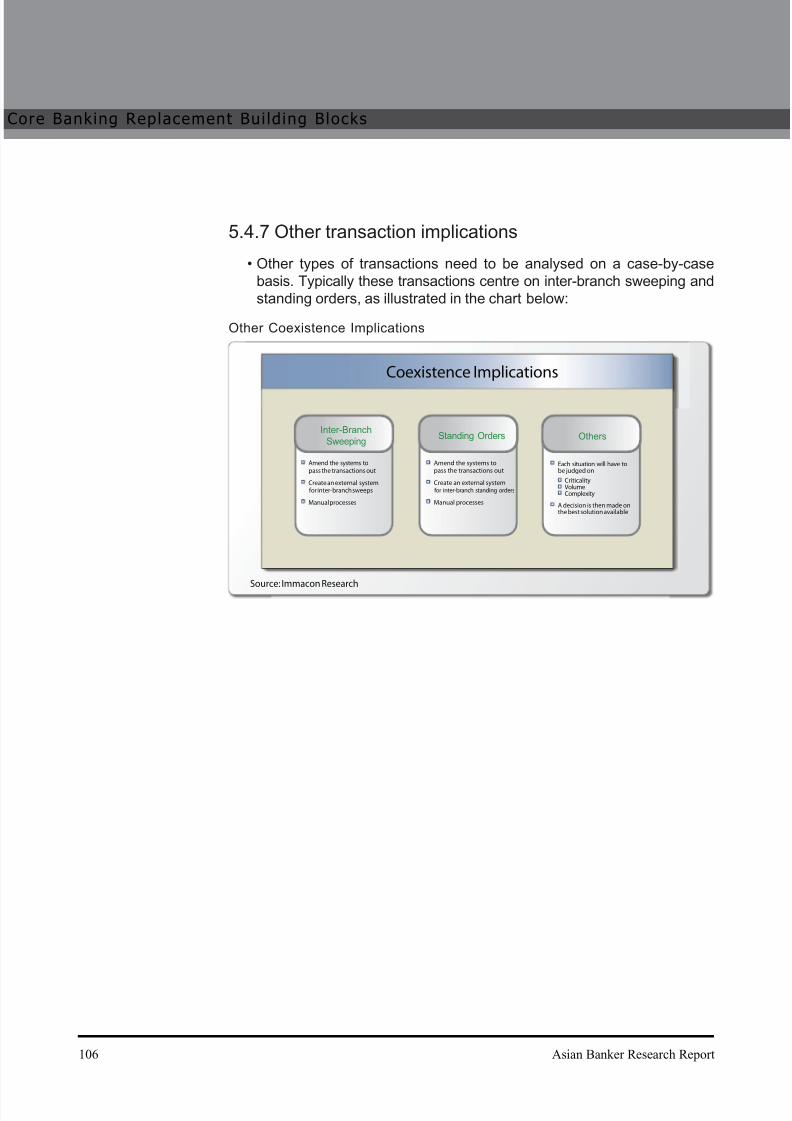

5.4.7 Other transaction implications

5.5 Data conversion and data cleansing5.6 Product rationalisation

5.7 Process rationalisation

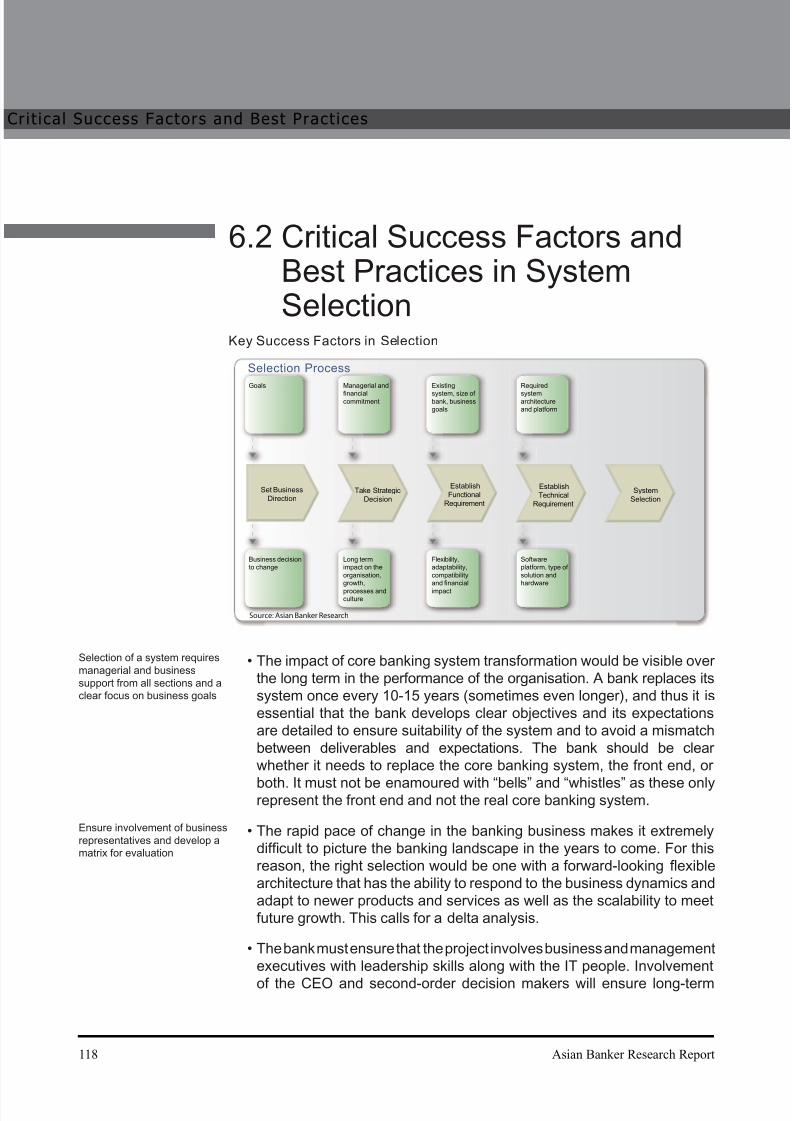

6. Critical Success Factors and Best Practices

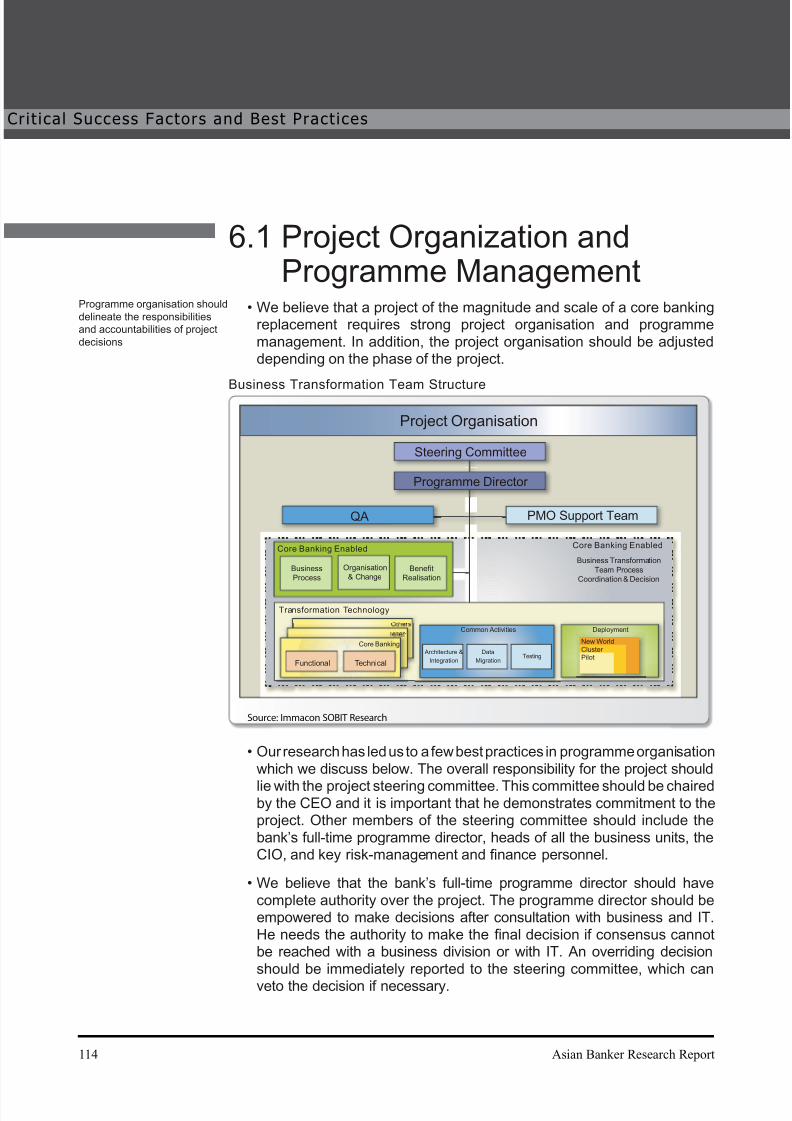

6.1 Project organisation and programme management

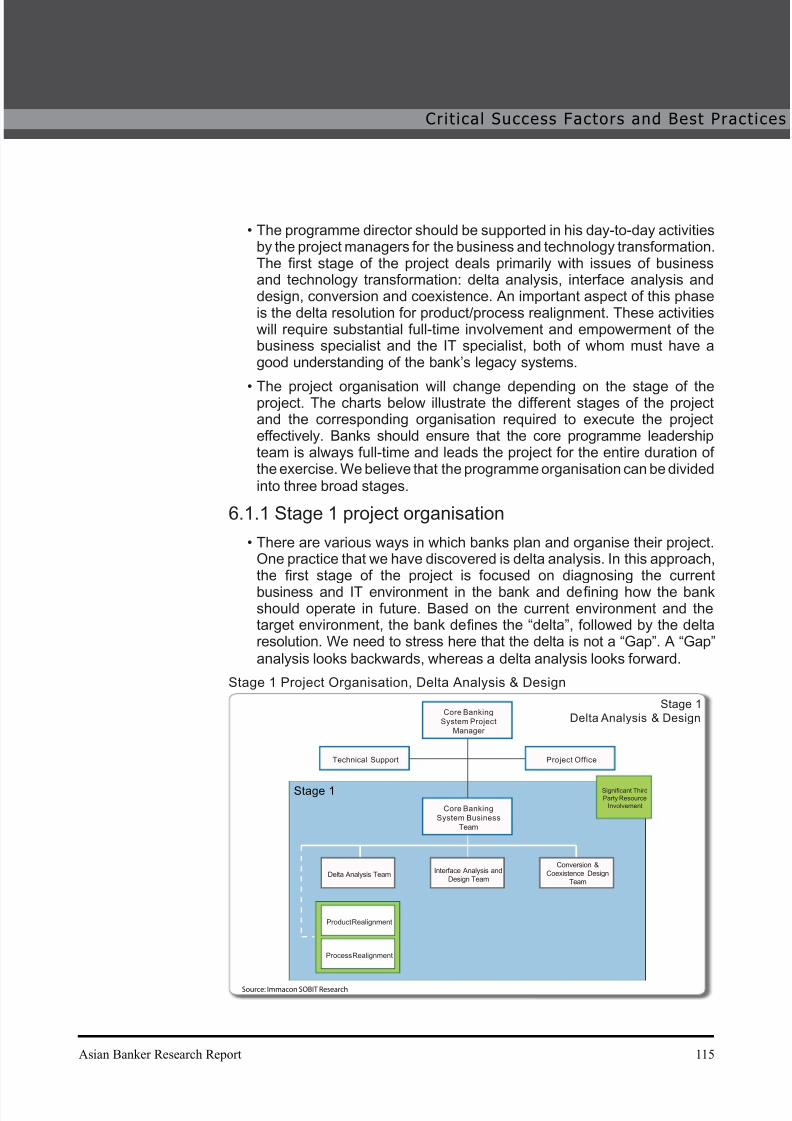

6.1.1 Stage 1 project organisation

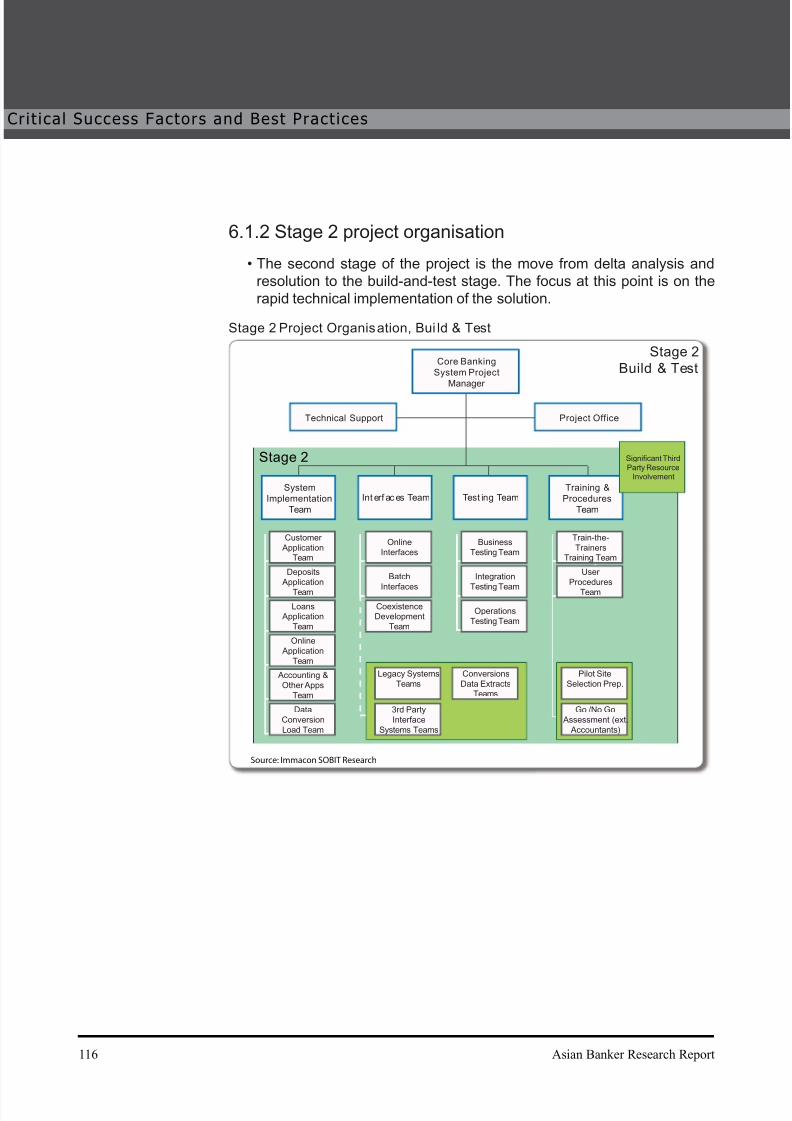

6.1.2 Stage 2 project organisation

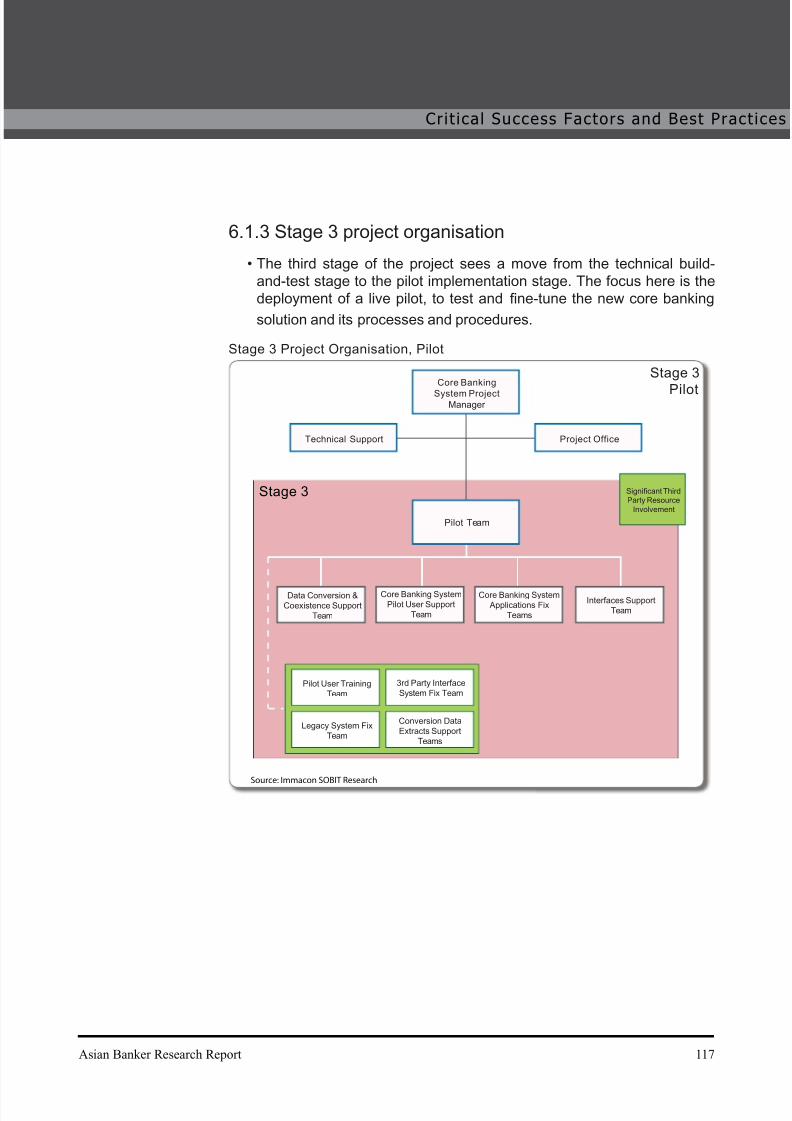

6.1.3 Stage 3 project organisation

6.2 Critical success factors and best practices in system

selection

6.3 Critical success factors and best practices in vendor

selection

6.4 Best practices for vendors (for successful

implementation)

7. Unique Core Banking Replacement Considerations

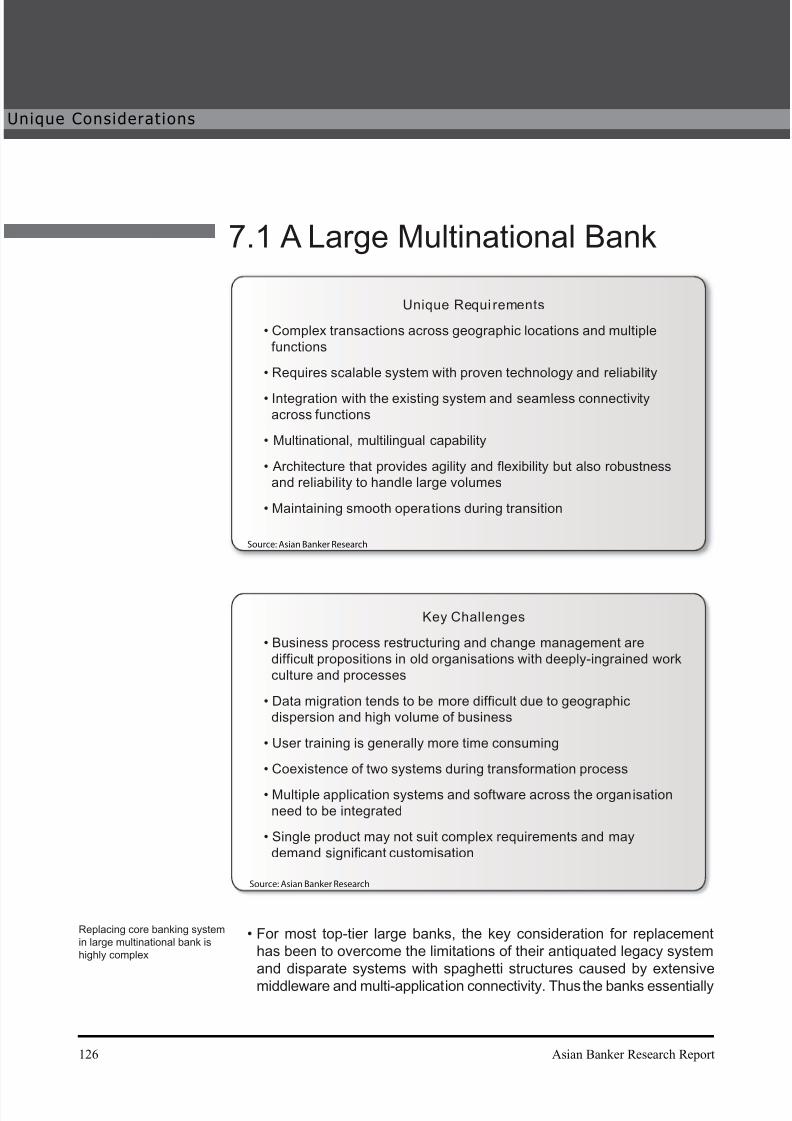

7.1 A large multinational bank

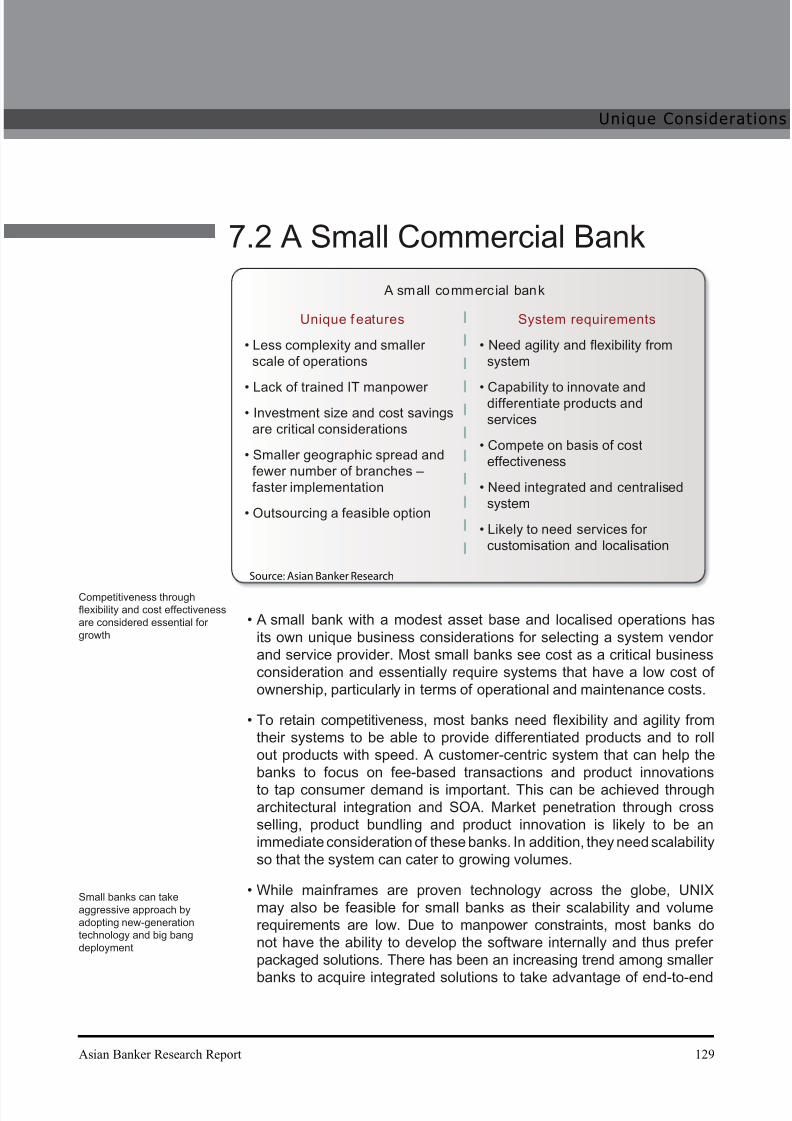

7.2 A small commercial bank

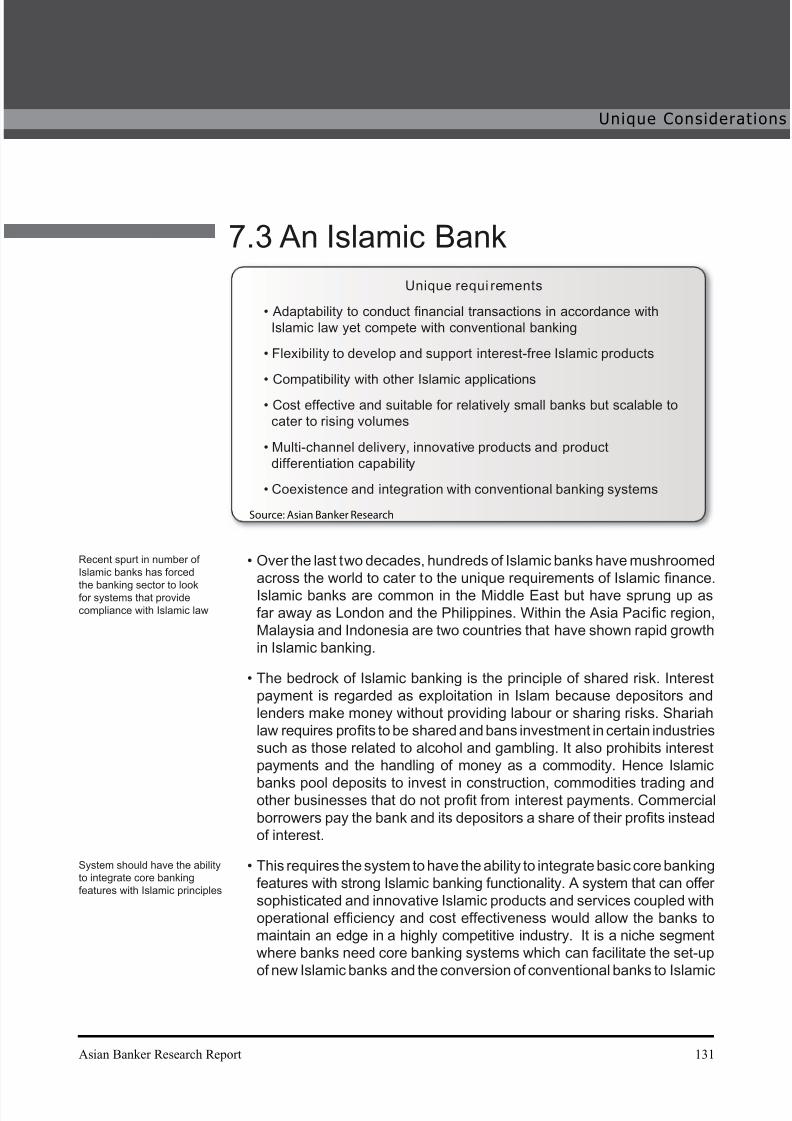

7.3 An Islamic bank

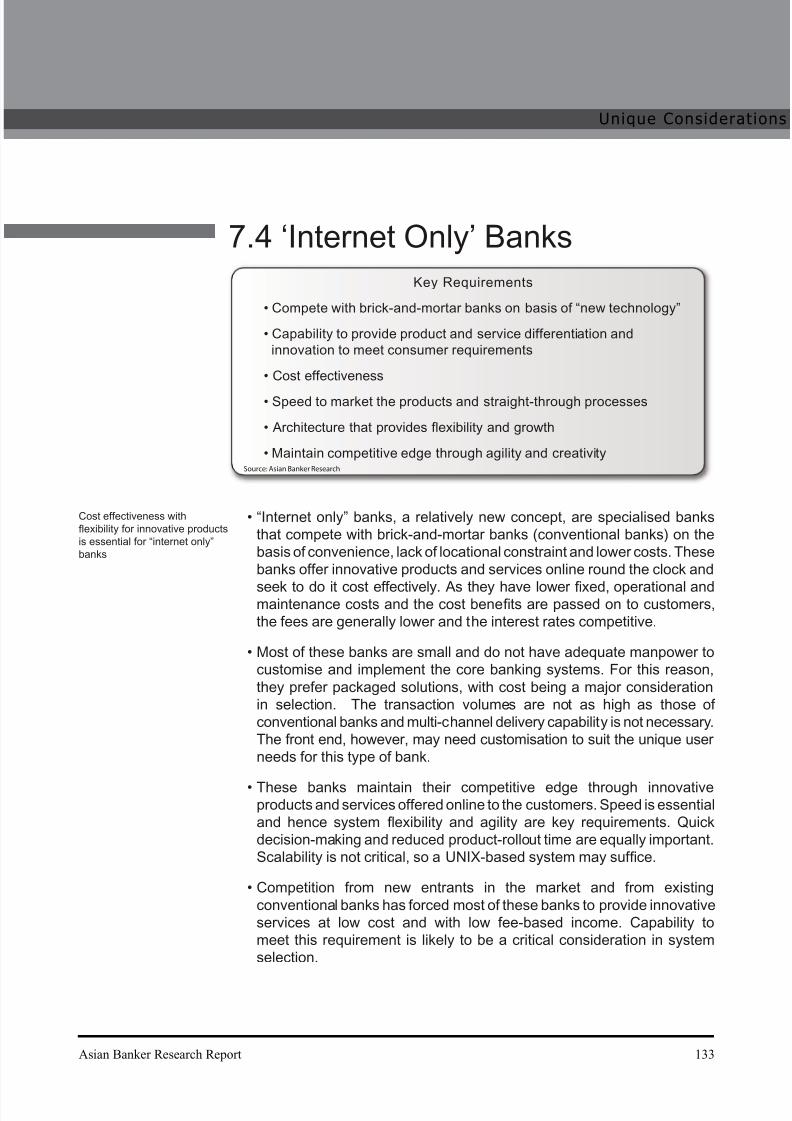

7.4 “Internet only” banks

7.5 Mergers and acquisitions of banks

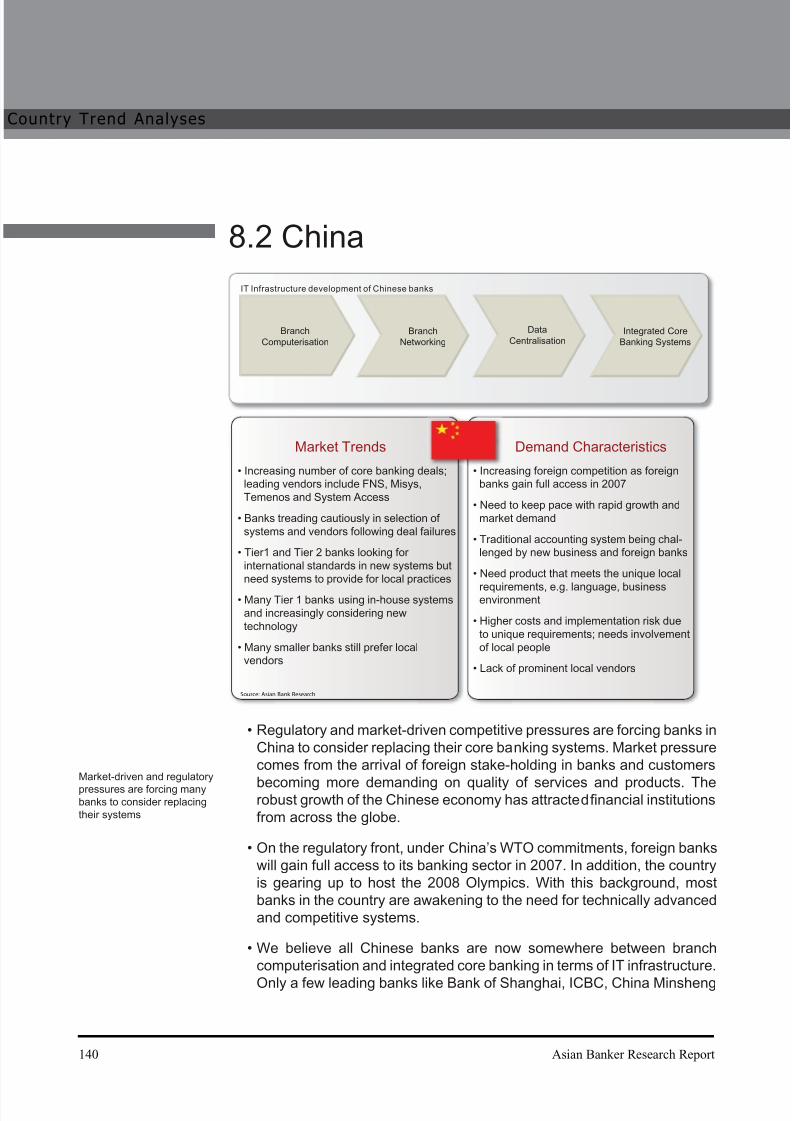

8. Country Trend Analyses

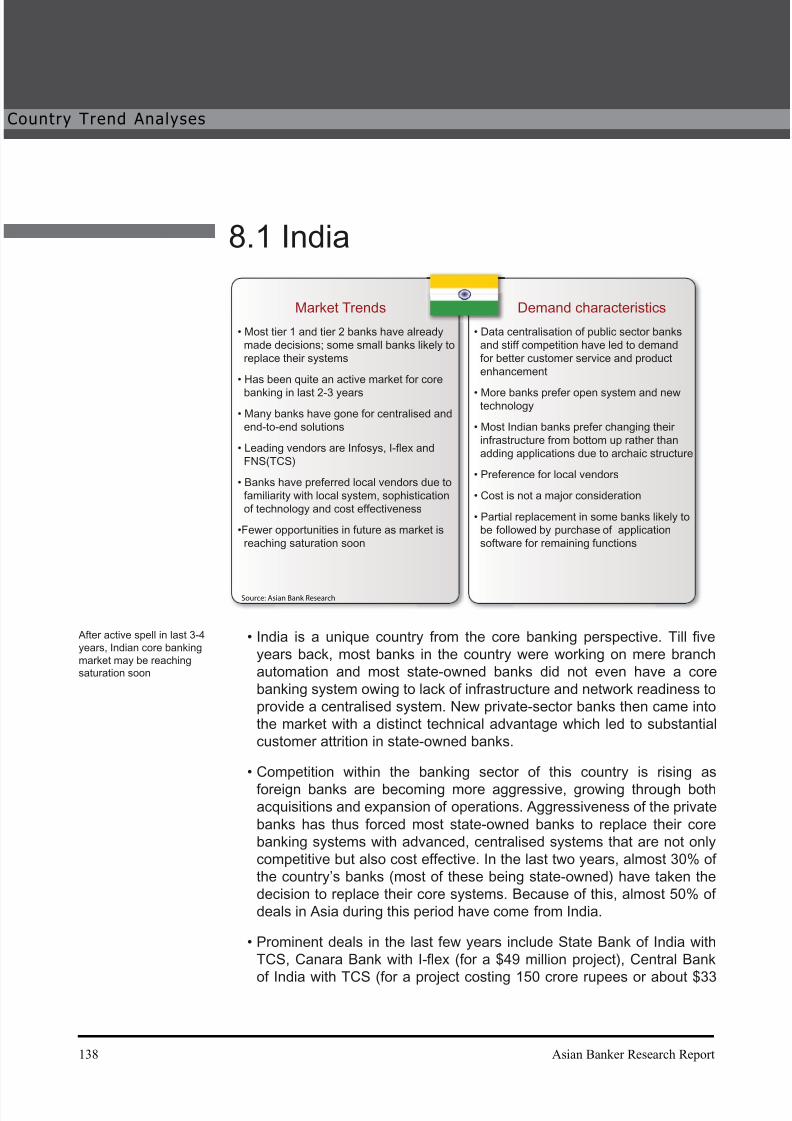

8.1 India

8.2 China

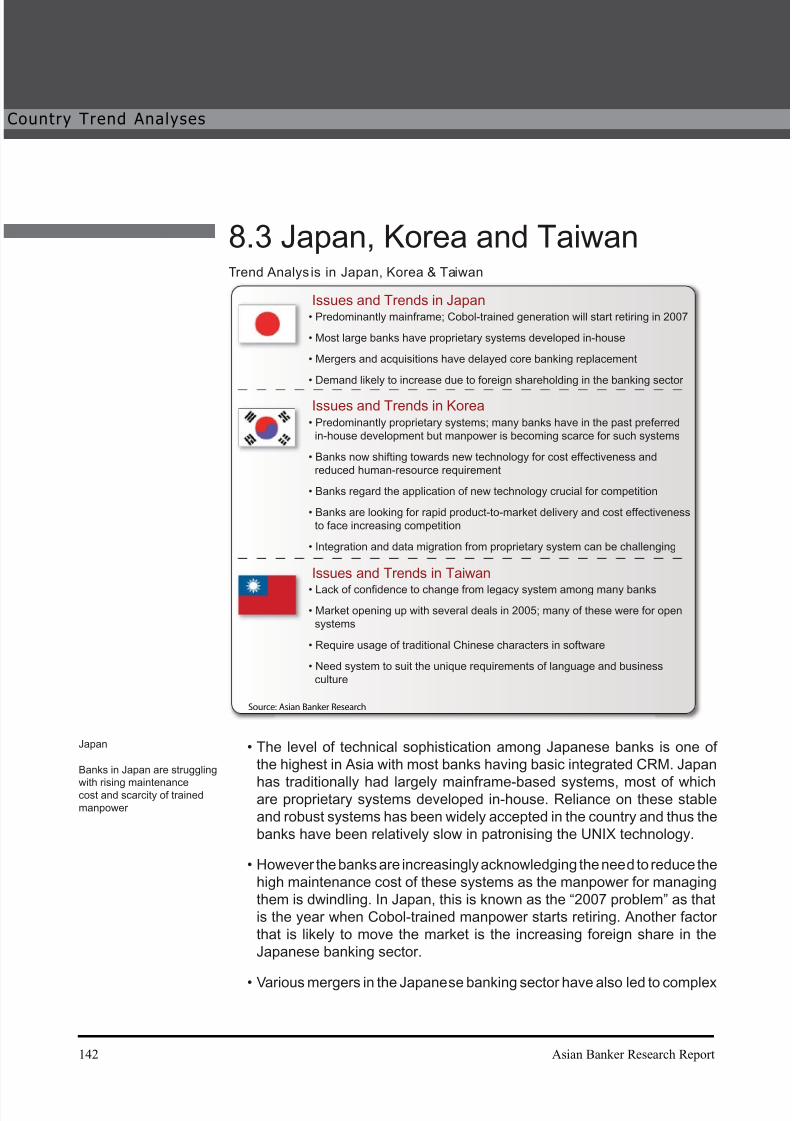

8.3 Japan, Korea and Taiwan

Asian Banker Research Report 3

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 9/173

8.4 South East Asia – Indonesia, Malaysia, Thailand and

Singapore

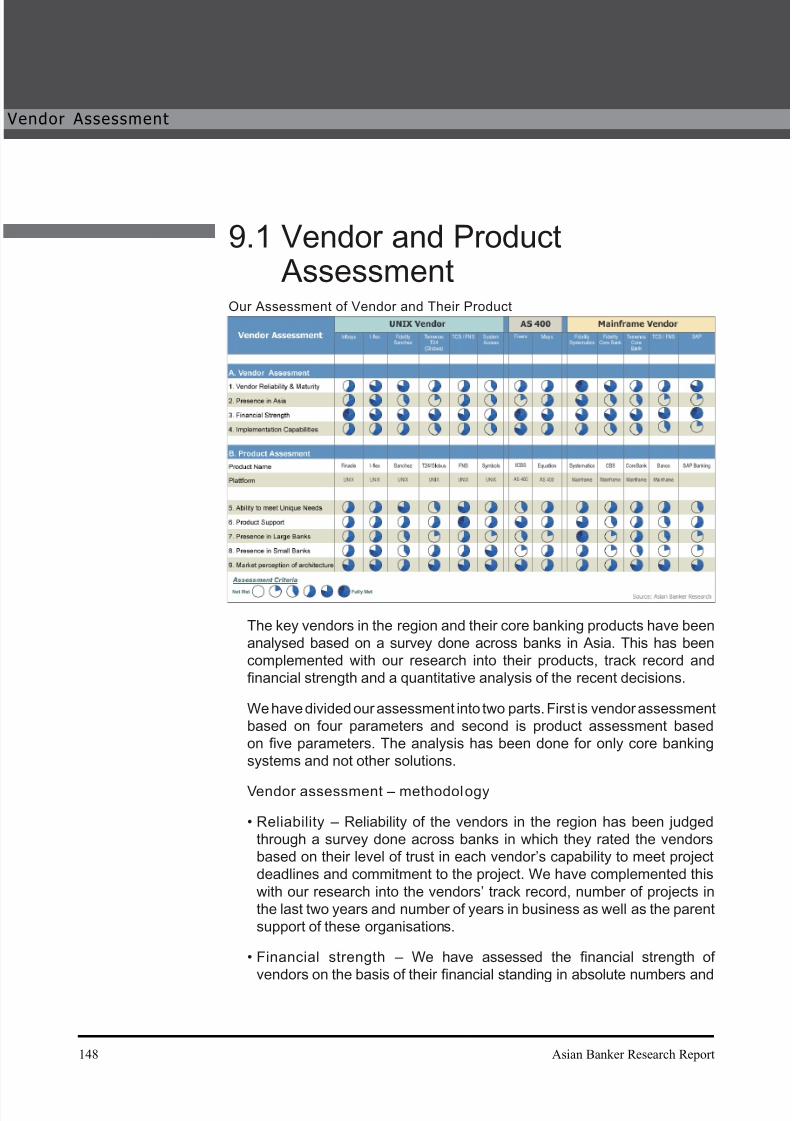

9. Vendor Assessment

9.1 Vendor and product assessment

9.2 Market positioning

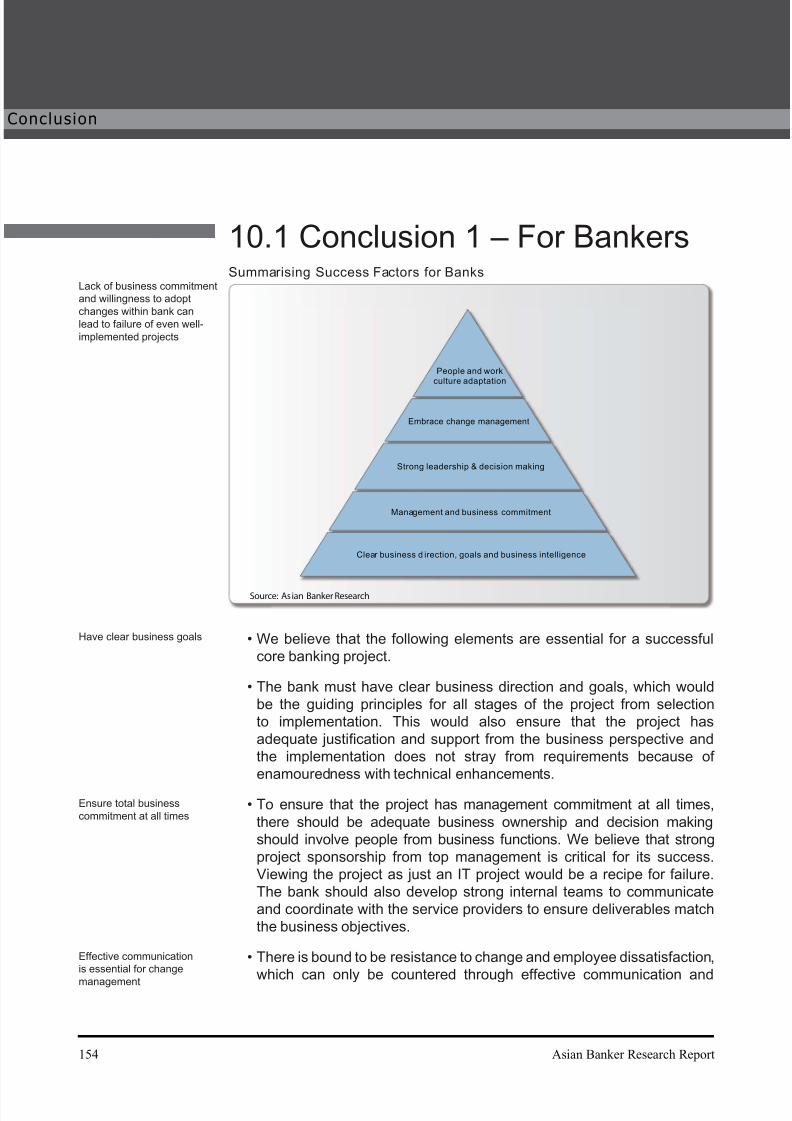

10. Conclusions10.1 Conclusion 1 – for bankers

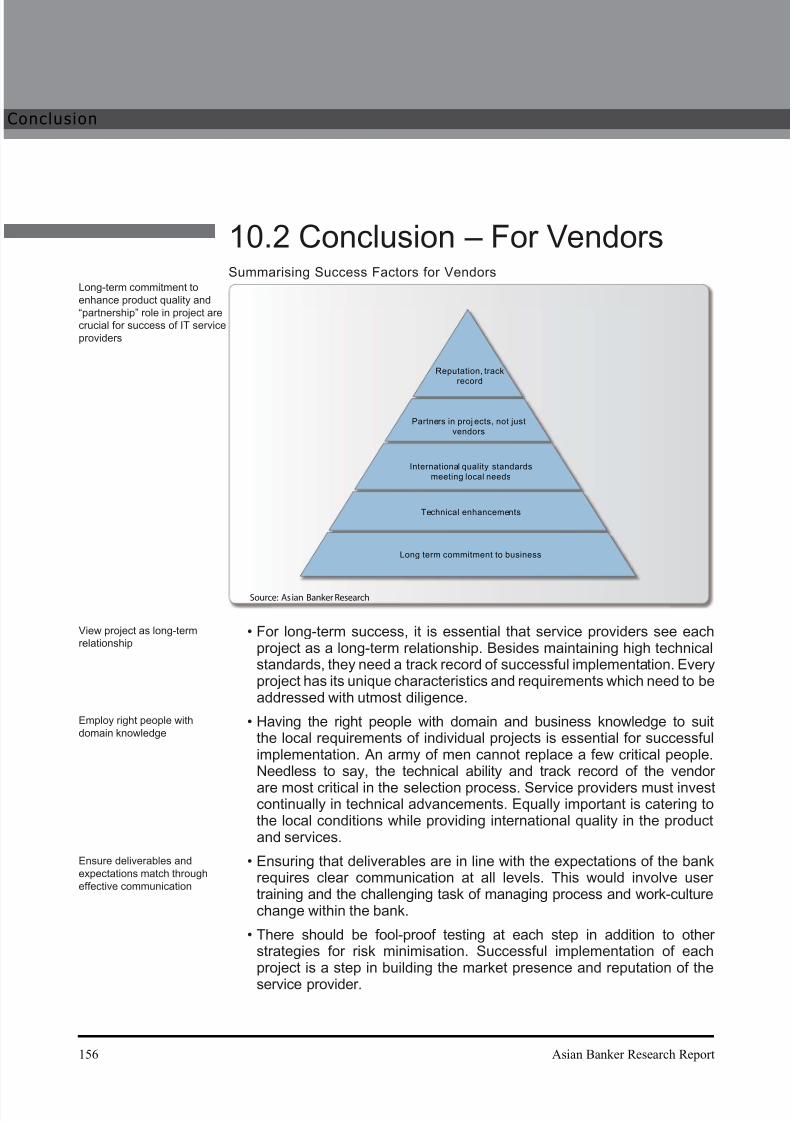

10.2 Conclusion 2 – for vendors

A1. Appendix I – Case Studies

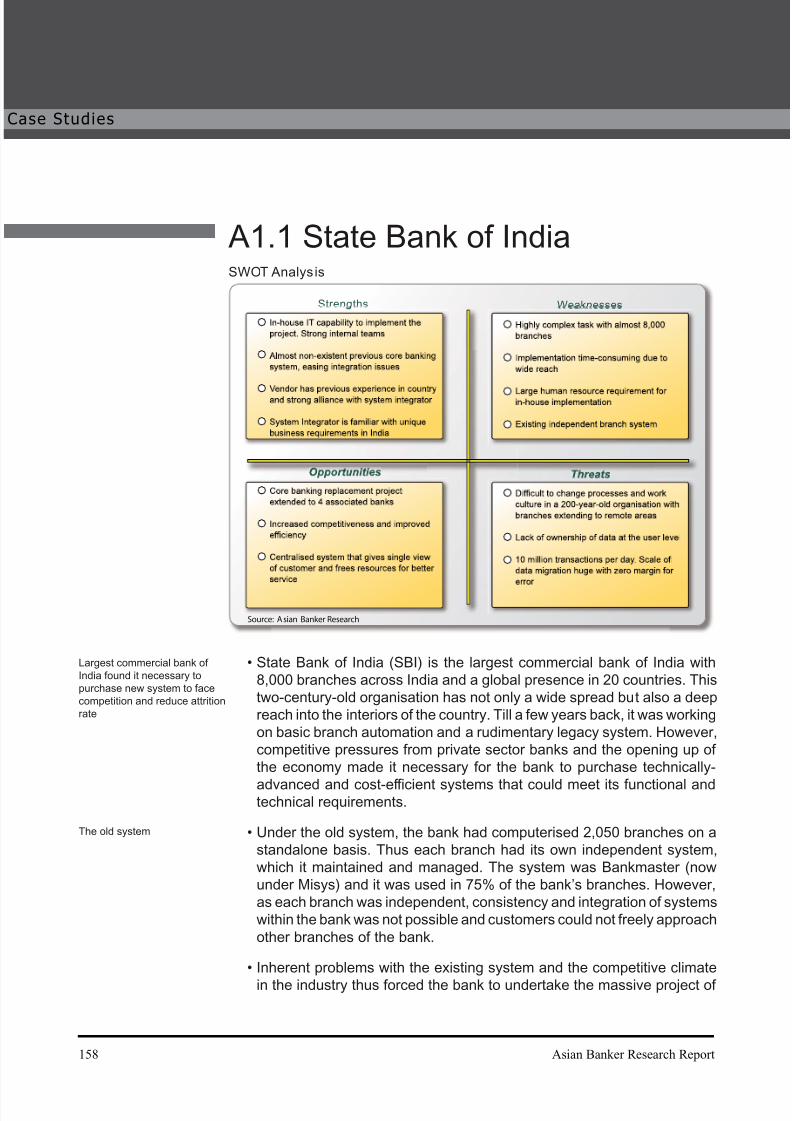

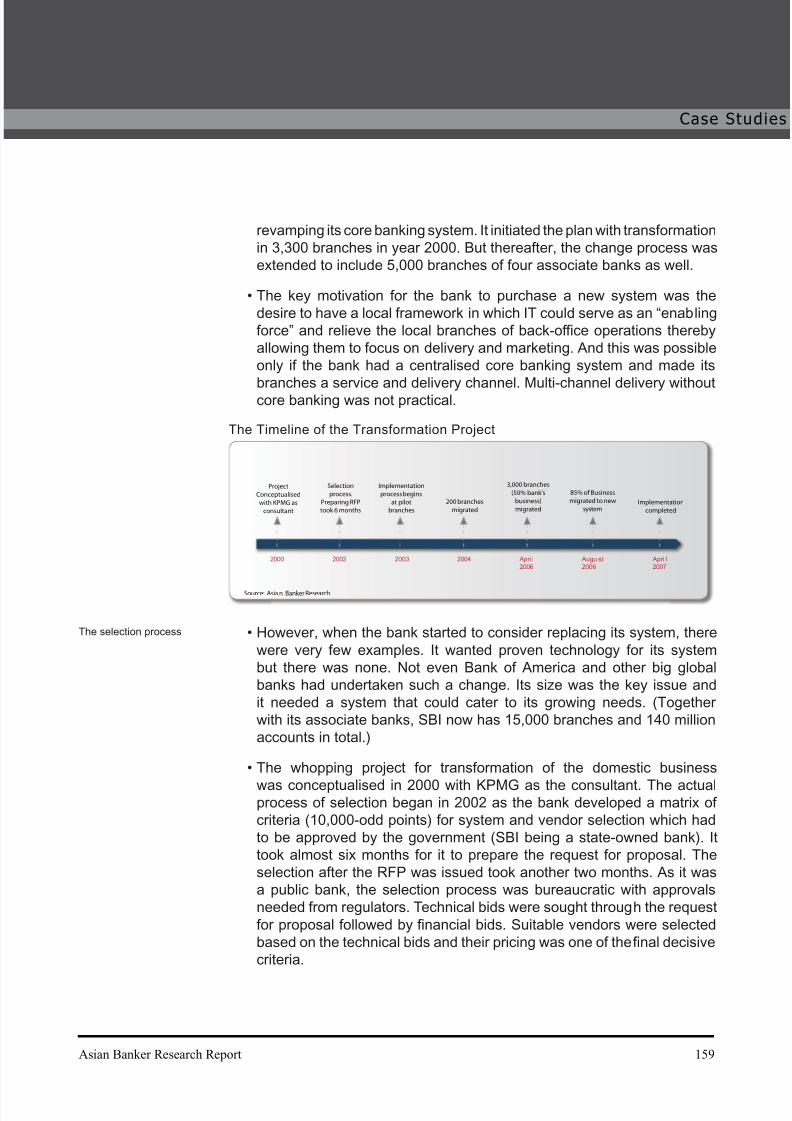

A1.1. State bank of India

A1.2 Union bank of Philippines

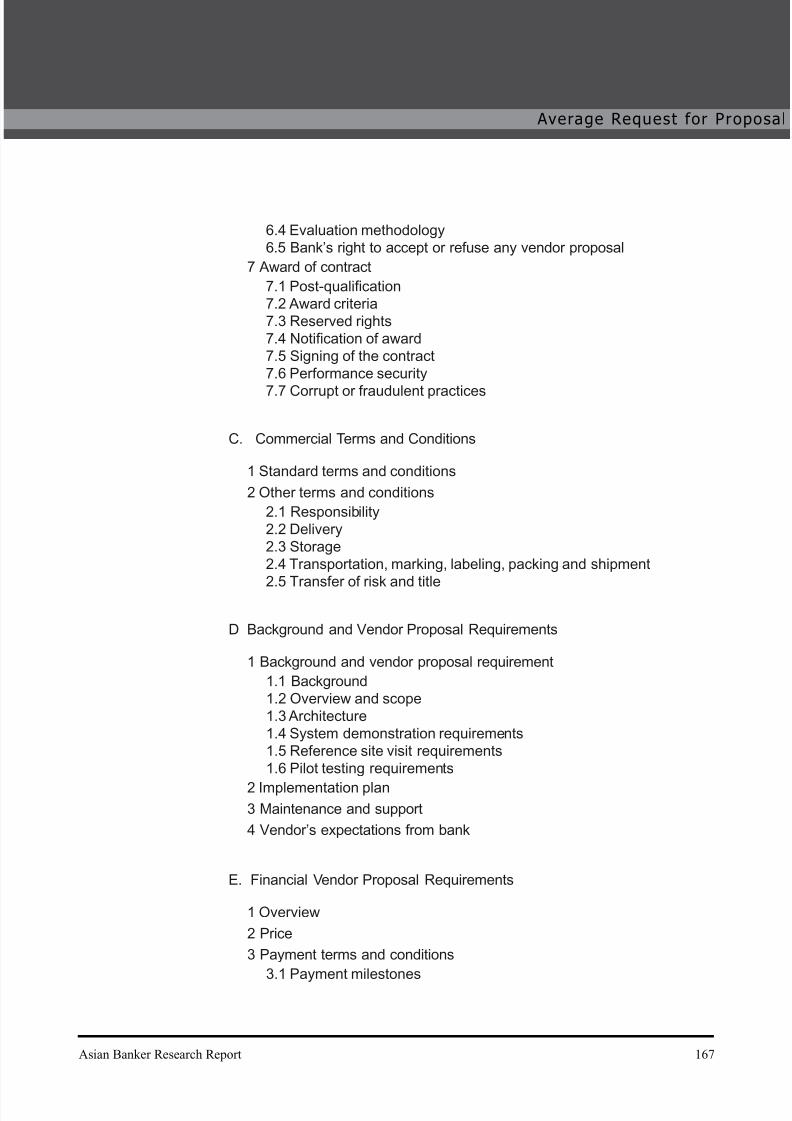

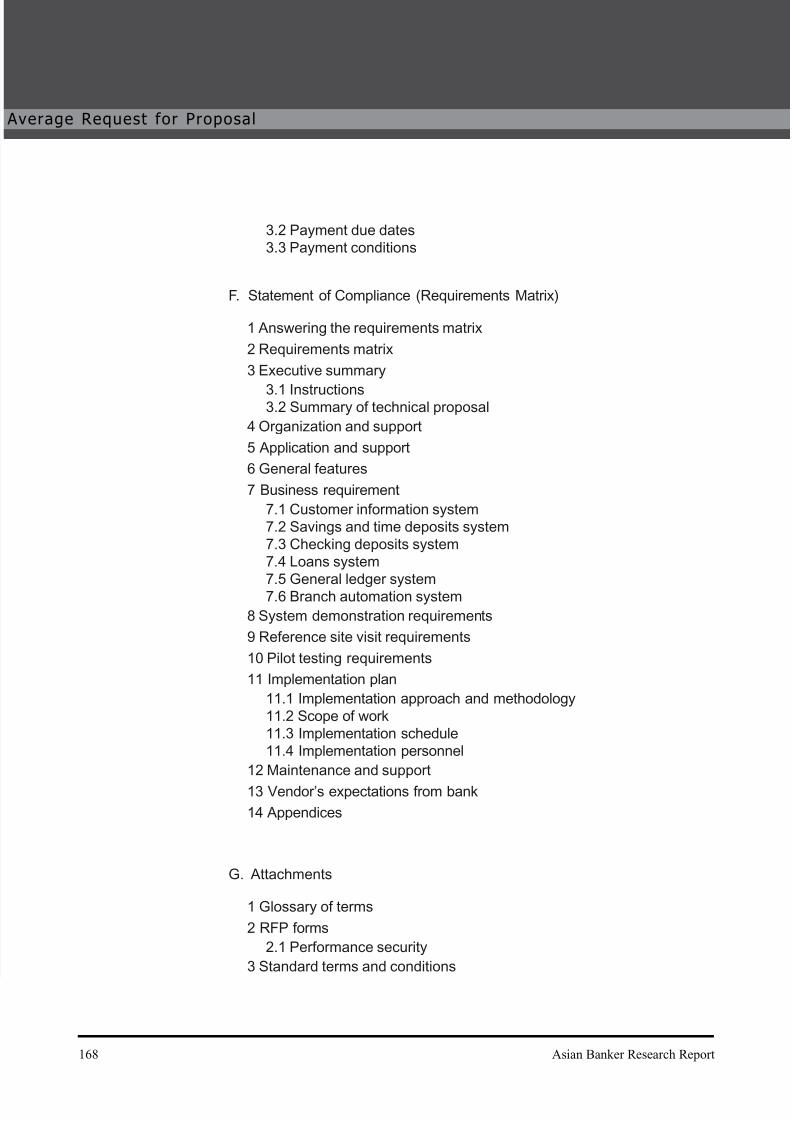

A1. Appendix II – An Average Request for Proposal

4 Asian Banker Research Report

ble of Con tents

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 10/173

Executive Summary

Increasing consumer demands, high costs and widespread dissatisfaction

with ageing systems are making it increasingly dif ficult for Asian bankers

to put off decisions to replace their core banking systems. We feel that the

banking industry worldwide is nearing a time when replacing core banking

systems would be a necessity rather than an option. However the complexity

of the task is such that it is often compared to a heart transplant, involving

huge risks, high costs and substantial time and human resources.

The critical need for replacement stems from rising customer expectations

and existing technical limitations. Banks are finding it imperative to expand

their channels and services while managing operational and technical costs

even as margins are shrinking due to stiff competition. But this is hampered

by technical limitations as many traditional financial institutions are shackled

by a series of heavily siloed non-integrated back-of fice legacy systems in

which customer information resides in multiple and unconnected locations.

Attempts to integrate these through layers of middleware have just made the

structure more complicated in many cases. On the other hand, abandoning the

antiquated structure itself presents a major challenge from the organisation

and financial perspectives. But competitive pressures are forcing banks

to take speedy actions, as can be seen in our analysis of trends in Asian

markets.

Analysing the Asian markets and the recent core banking replacement

decisions, we found that there has been a gradual rise in the number of core

banking deals in the last two years. Interestingly, almost half of the deals

during this period have come from state-owned Indian banks. These banks

had faltered due to competitive pressure from private banks and have found

it imperative to purchase (in most cases for the first time) new core banking

systems and upgrade themselves technically to improve product innovation,

agility in decision making and cost effectiveness. We expect the Asia-widetrend to continue in the year 2006; but as the Indian market nears saturation,

there are likely to be fewer deals from this country in the following years.

Looking at the trend in countries that have first-generation technical

sophistication, we have discovered that core banking replacement is

considered a cyclical industry as banks come to the market about every 15

years to replace an ageing system and improve their ef ficiencies. In the last

two years, many banks in countries like China, Taiwan and Malaysia have

shown initial signs of awakening to the need for technical advancement. We

expect to see increasing activity in China with foreign banks getting full access

to the sector in 2007 under WTO stipulations and with China’s hosting of the

Execut ive Summary

Asian Banker Research Report 5

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 11/173

Olympics in 2008. On the other hand, we have found that banks in countries

like Japan and Indonesia are still mulling over the wisdom of replacing.

Once a bank has decided to replace its system, it embarks on a complex

process involving a series of critical choices. To start with, the bank has

to decide on the most appropriate approach to system replacement. The

choices vary with the availability of technical skills, complexity of the project,

availability of products and costs involved. As banks weigh their options,

they often have to consider the pros and cons of “buying” versus “building”

and “purchasing” versus “outsourcing”. We have discovered that most Asian

banks increasingly prefer to focus on their core business rather than lock

their resources in building a system and there is a distinct trend towards

the purchase of packaged solutions. However for large multinational banks,

a ready packaged solution often does not meet the complex requirements

and hence may require further development (as in the case of HSBC) or

substantial customisation at the minimum.

To better comprehend the complicated process of core banking replacement,

we begin with a definition of the core banking system. We define it as a

highly ef ficient “customer accounting” and transaction processing engine, for

high volumes of back-of fice transactions and customer-level accounting and

reporting of the deposit and loan products processed in the bank. Howeverit does not include the front of fice. Thus we believe that the bank has to

first determine whether it really needs to replace its core system or it can

manage with just front-of fice replacement. In many cases, it is likely that the

bank needs to replace both along with the general ledger – which would be

a project of even bigger magnitude. If the bank has to change both front end

and core banking, we recommend it be done through the same vendor to

avoid integration issues.

Our research shows that banks which go ahead with replacement should

make a clear transition from their legacy system to the new system. Partially

bringing old elements such as codes, process automation and loss-making

legacy products into the new environment will lead to sub-optimal returns.

We have divided the process of core banking replacement into four phases.

The first phase is business justification and identification of business

requirements through delta analysis. We believe that the bank should, first

and foremost, determine its long-term strategic goals as these would guide

the bank towards the critical requirements for its system. With the business

objectives in mind, banks need to analyse the capabilities and deficiencies

of their existing core banking system to determine the new system’s

requirements – yet during our research, we discovered that only 70% of the

banks in our sample do so. In addition to setting the objectives, the bank

should establish the business and financial justification for the project at this

6 Asian Banker Research Report

ecut ive Summary

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 12/173

early stage of the process.

The second phase of the project is selection of the system and the vendor.

Selection of a core banking system will affect not only the growth andfinancials

of the organisation but also its viability and competitiveness. Hence banks

need to critically evaluate all available options and select the system that

provides the right DNA (the architecture) to meet its business and strategic

requirements. We believe that the selection process should involve business

representatives from all functional divisions owing to the pervasive nature

of these systems within the organisation. Viewing the project as just an IT

project would be a recipe for failure.

The selection process begins with the issuance of a Request for Proposal

to various vendors. Each of the bids is assessed on both qualitative and

quantitative terms across a matrix of selection criteria. The critical requirements

from a new system are flexibility and scalability to cater to future growth. We

advise banks to ensure that with the new system, they are not simply shifting

to a bigger box which may become a constraint again in a few years’ time,

as this would defeat the whole purpose of replacing the system. Equally

important is that banks should not be enamoured with “bells” and “whistles”

(which are more often than not the front-end features) and should look for

a system that has the requisite processing power rather than just a userfriendly front-end screen.

We have discovered that one of the challenges is picturing the banking

landscape in years to come due to the rapid pace of change in the banking

business. Thus the right selection would be one with a forward-looking

flexible architecture that has the ability to support the business ambitions of

the bank and allows for future modifications with ease. This can come from

Service Oriented Architecture (SOA). SOA is a relatively recent development

which, in its purest sense, is centred on loosely coupled components which

support generic services and are based on web technology. In a core banking

context, it essentially means reducing barriers in antiquated infrastructure and

creating real-time integration of disparate systems and sharing of databases

on a flexible and easily upgradeable infrastructure. We advise banks to look

for a system that has the flexibility of SOA and to integrate their systems and

components in an SOA-based framework within the bank.

Banks need to select not the “best” system available but the one that is most

appropriate for their particular requirements. Different banks and their unique

requirements are discussed in section 8.

Equally critical is selecting the right vendor. We believe that it is imperative

for banks to consider vendors as long-term partners in growth in today’s

fast-paced environment. The critical vendor assessment criteria include trust

Asian Banker Research Report 7

Execut ive Summary

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 13/173

in the vendor’s ability to meet the business objectives (through optimum

customisation and localisation of the product) as well as the vendor’s

reliability, implementation capabilities and financial strength. Vendors that

have a track record of providing international-quality products while meeting

the local needs of banks are more likely to achieve long-term success. The

mix of product and services coupled with pricing are critical considerations.

We have rated leading vendors in Asian markets based on our assessment

and a survey done among bankers – this is discussed in our section on

vendor assessment.

Platform choice is one other critical factor in selection. While mainframe

remains unbeaten in its robustness and stability, UNIX-based systems are

becoming more popular. We have discovered that banks in Asian countries

are increasingly shifting towards the more agile and flexible UNIX systems,

which are perceived to have lower operational and maintenance costs. While

this is true for banks that have lower transaction volumes, it may not be so

for large retail banks. We believe that mainframes continue to have a distinct

advantage in terms of stability and scalability. Hence for mission critical

projects, mainframes would still be preferred for their reliability. However for

small banks (and those banks that are acquiring a core banking system for

the first time and whose transaction volumes are not very high), a UNIX-

based system could meet their requirements. As more than 50% of the dealsin Asia have come from small banks, UNIX-based systems have become

more common.

The third phase of the project is implementation. The key objective is to

operationalise and pilot the transformed future state, including technology,

process and organisational change. This involves developing detailed

designs, including system designs for configuration and customisation and

designs for interfaces and data conversion. The other critical elements of this

phase are building and testing the system, implementing pilot projects and

conducting business acceptance tests at each stage. We recommend that

banks limit customisation of the core banking system to what is essentialas it may affect the core processing ability of the system. Rather, the banks

should customise the front end which interacts with the users.

At each stage, the bank should undertake delta analysis to determine the

ef ficacy and success of the project; this would determine whether it progresses

to the next stage. Delta analysis and sign-off at each stage are essential to

ensure that deliverables and expectations match, or else the project can

easily digress from its initial plan and increase in scope through incremental

changes which will lead to schedule and cost overruns.

The next and final phase of the project is deployment. This is probably the

most critical and challenging stage, where the bank undertakes the actual

8 Asian Banker Research Report

ecut ive Summary

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 14/173

deployment of the new system. The process involves numerous logistical

issues such as data conversion, interfacing and coexistence.

Banks can approach this transition in two ways – big bang implementation

and gradual deployment. Big bang essentially means all systems go live at

the same time. While this is quicker, it is also riskier. Instead we recommend

phased implementation, where deployment is done in small clusters, though

the bank has to tackle the tricky issue of coexistence. We believe that the

gradual step-by-step approach is appropriate in most cases as it entails lower

risks, facilitates change management and allows changes to be incorporated

in the technical framework as it is being installed (to provide a better fit with

the business).

Data conversion and data mapping are two crucial elements that the bank has

to deal with during deployment. The data migration and conversion process

is often hampered by lack of available information on the old system. Mass

migration requires a large capital investment, takes a few years to implement

and poses a significant risk of service interruptions that can reduce customer

satisfaction. The other critical challenge is to maintain smooth operations

and develop interfaces across delivery channels during transition through

coexistence of two systems.

We believe that banks should predefine the milestones at each stage of the

replacement process and ensure they are adhered to. At any stage, if the

bank finds that it cannot achieve these milestones, it may review its project

and decide whether and how it wants to continue the project.

Our research into change management during replacement shows that the

majority of banks upgrade their system or implement a new one to meet

existing users’ process and work culture requirements. Instead, however,

we recommend that banks align their products, processes and work culture

with the new system. In other words, the replacement should be undertaken

together with product and process rationalisation coupled with work culture

transformation in order to optimise the returns from the new system.

This embracing of new technology requires tremendous effort in change

management, which demands extensive user training and re-engineering

of processes across the organisation. There is often resistance to change

and employee dissatisfaction during the transition. We believe this can be

countered only through effective communication and developing the right

business environment.

We have discovered that just 30% of recent replacement projects had active

CEO involvement. However our research shows that successful projects

require the backing of a strong leader from top management with a strategic

Asian Banker Research Report 9

Execut ive Summary

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 15/173

mindset and the duty to see the project through. Strong leadership support

and a capable steering team (which can harness the bank’s resources, take

quick decisions and motivate staff to see the project through) are critical for

success. Banks need to develop strong internal teams that have effective

communication and technical skills, to share decision-making with the service

provider to overcome problems. The complexity of the process and inevitable

hiccups will demand that banks engage in the process with thorough planning

and programme organisation.

10 Asian Banker Research Report

ecut ive Summary

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 16/173

1Core Banking Trends in Asia Pacifi c

This section examines the trends in core banking transformation

among Asian countries and covers a wide spectrum of issuesranging from pattern in deals, replacement approach, platformselection, implementation and key architectural trends. The aimis to learn from recent decisions and understand the marketdynamics of this region.

Core Banking Trends in Asia Pacifi c

Market Trends1.1 Prominent recent deals in the region1.2 Geographic dispersion of deals in recent years and 2006

estimates1.3 Activity within countries and their vendor preferences1.4 Estimates of system and software spending in Asia Pacific

Technical Trends1.5 Evolution and convergence of core banking systems1.6 Technology integration in Asian countries1.7 Trends in platform usage among Asian countries1.8 Trends in deployment approach

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 17/173

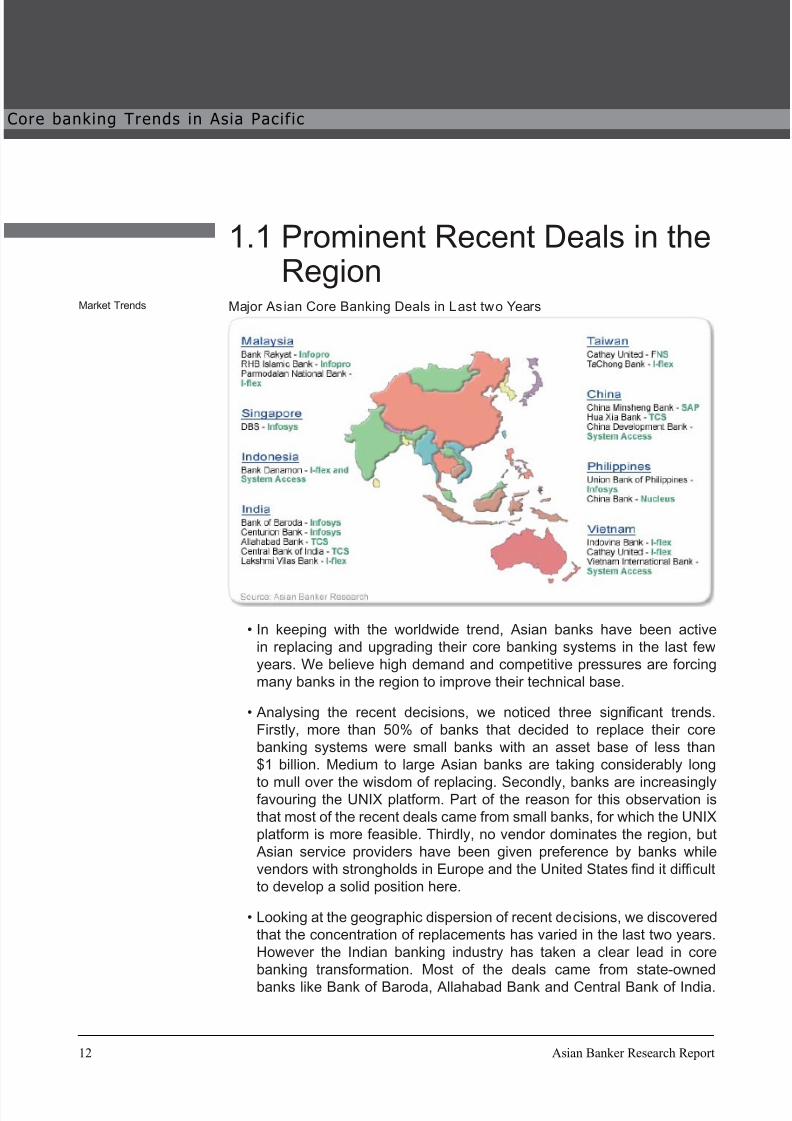

1.1 Prominent Recent Deals in theRegion

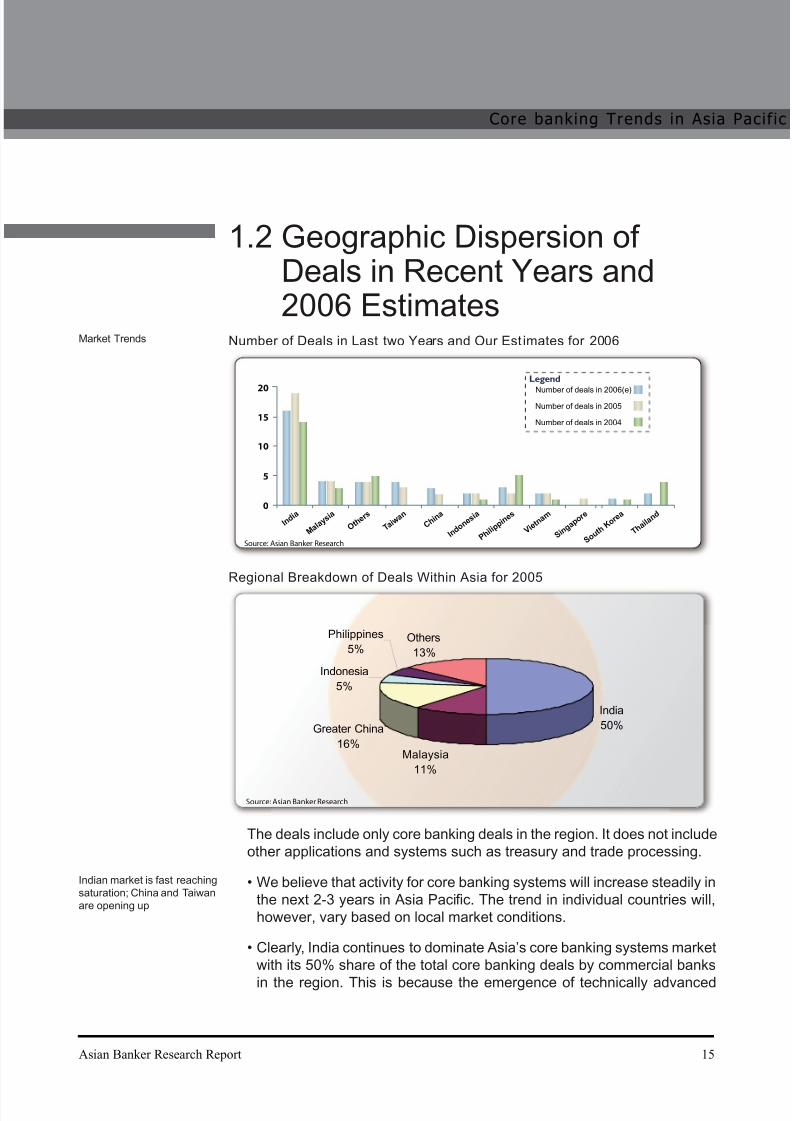

Major Asian Core Banking Deals in Last two Years

In keeping with the worldwide trend, Asian banks have been activein replacing and upgrading their core banking systems in the last fewyears. We believe high demand and competitive pressures are forcingmany banks in the region to improve their technical base.

Analysing the recent decisions, we noticed three significant trends.Firstly, more than 50% of banks that decided to replace their corebanking systems were small banks with an asset base of less than$1 billion. Medium to large Asian banks are taking considerably long

to mull over the wisdom of replacing. Secondly, banks are increasinglyfavouring the UNIX platform. Part of the reason for this observation isthat most of the recent deals came from small banks, for which the UNIXplatform is more feasible. Thirdly, no vendor dominates the region, but Asian service providers have been given preference by banks whilevendors with strongholds in Europe and the United States find it dif ficultto develop a solid position here.

Looking at the geographic dispersion of recent decisions, we discoveredthat the concentration of replacements has varied in the last two years.However the Indian banking industry has taken a clear lead in corebanking transformation. Most of the deals came from state-ownedbanks like Bank of Baroda, Allahabad Bank and Central Bank of India.

•

•

•

Market Trends

12 Asian Banker Research Report

re banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 18/173

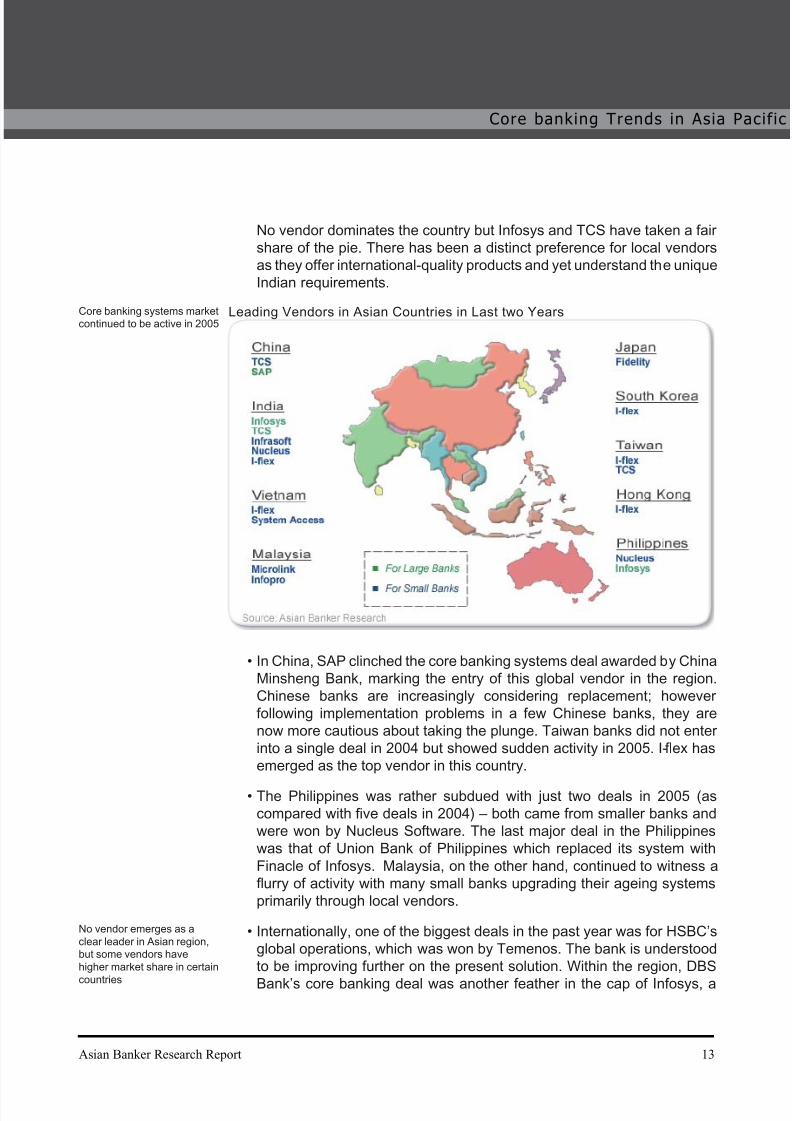

No vendor dominates the country but Infosys and TCS have taken a fairshare of the pie. There has been a distinct preference for local vendorsas they offer international-quality products and yet understand the uniqueIndian requirements.

Leading Vendors in Asian Countries in Last two Years

In China, SAP clinched the core banking systems deal awarded by ChinaMinsheng Bank, marking the entry of this global vendor in the region.Chinese banks are increasingly considering replacement; howeverfollowing implementation problems in a few Chinese banks, they arenow more cautious about taking the plunge. Taiwan banks did not enterinto a single deal in 2004 but showed sudden activity in 2005. I-flex hasemerged as the top vendor in this country.

The Philippines was rather subdued with just two deals in 2005 (ascompared with five deals in 2004) – both came from smaller banks andwere won by Nucleus Software. The last major deal in the Philippineswas that of Union Bank of Philippines which replaced its system withFinacle of Infosys. Malaysia, on the other hand, continued to witness aflurry of activity with many small banks upgrading their ageing systemsprimarily through local vendors.

Internationally, one of the biggest deals in the past year was for HSBC’sglobal operations, which was won by Temenos. The bank is understoodto be improving further on the present solution. Within the region, DBS

Bank’s core banking deal was another feather in the cap of Infosys, a

•

•

•

Core banking systems marketcontinued to be active in 2005

No vendor emerges as aclear leader in Asian region,but some vendors havehigher market share in certain

countries

Asian Banker Research Report 13

Core banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 19/173

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 20/173

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 21/173

private banks in the country has forced most state-owned banks tosubstitute (and in most cases acquire for the first time) a centralised corebanking system to improve their competitiveness and retain their marketshare. However we expect the trend to slow down in the next couple ofyears as most leading banks have already entered into core bankingdeals. A few banks that have not yet upgraded their systems are findingit increasingly dif ficult to compete and are currently evaluating availableproducts and vendors.

Taiwan witnessed a recent surge in core banking deals, though mostlyfrom smaller banks. In China, the number of deals has been rising slowlybut steadily as more and more banks evaluate the need for replacement;however most of these deals have been from smaller banks. We expectthe current trend in both Taiwan and China to continue this year.

Malaysia has also been active with four deals in 2005, though most ofthese were again from smaller banks. However we believe some bigbanks like Maybank are actively considering core banking replacement.We expect to see more core banking deals in Malaysia with Islamic banksfavouring local vendors who can meet Islamic banking requirements.

Most other countries saw just a few small deals with the exception ofSingapore, where DBS has entered into a core banking deal for its retailbusiness. Thailand and Korea were noticeably absent from the scene in2005, but we expect activity in both countries to pick up over the nextcouple of years.

•

•

•

16 Asian Banker Research Report

re banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 22/173

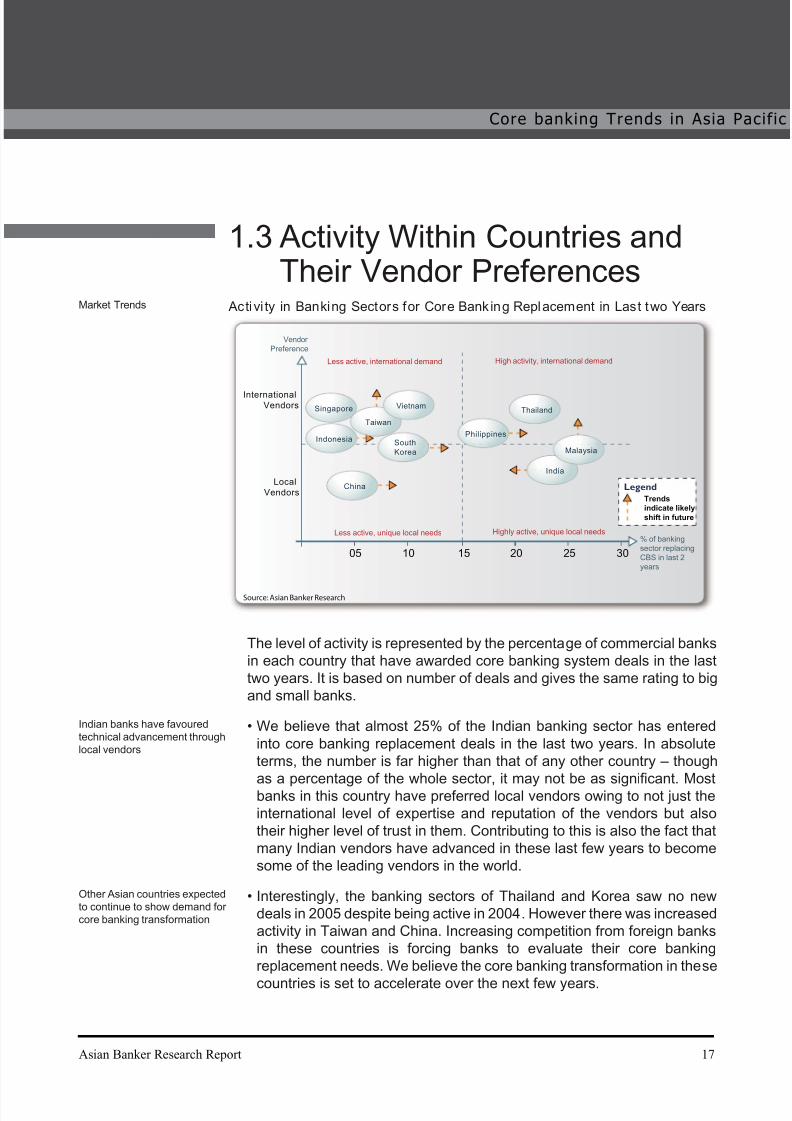

1.3 Activity Within Countries andTheir Vendor Preferences

Activi ty in Banking Sectors for Core Bank ing Replacement in Last two Years

05 10 15 20 25 30

Vendor

Preference

InternationalVendors

Local

Vendors

Less active, international demand High activity, international demand

Less active, unique local needs Highly active, unique local needs

Trends

indicate likely

shift in future

% of banking

sector replacing

CBS in last 2

years

Singapore

South

Korea

Taiwan

Vietnam

Philippines

Thailand

India

Malaysia

Indonesia

China Legend

Source: Asian Banker Research

The level of activity is represented by the percentage of commercial banksin each country that have awarded core banking system deals in the lasttwo years. It is based on number of deals and gives the same rating to bigand small banks.

We believe that almost 25% of the Indian banking sector has enteredinto core banking replacement deals in the last two years. In absoluteterms, the number is far higher than that of any other country – though

as a percentage of the whole sector, it may not be as significant. Mostbanks in this country have preferred local vendors owing to not just the

international level of expertise and reputation of the vendors but alsotheir higher level of trust in them. Contributing to this is also the fact thatmany Indian vendors have advanced in these last few years to becomesome of the leading vendors in the world.

Interestingly, the banking sectors of Thailand and Korea saw no newdeals in 2005 despite being active in 2004. However there was increasedactivity in Taiwan and China. Increasing competition from foreign banksin these countries is forcing banks to evaluate their core bankingreplacement needs. We believe the core banking transformation in these

countries is set to accelerate over the next few years.

•

•

Market Trends

Indian banks have favouredtechnical advancement throughlocal vendors

Other Asian countries expectedto continue to show demand forcore banking transformation

Asian Banker Research Report 17

Core banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 23/173

Most Chinese banks have shown a strong preference for systemsthat are designed to suit their specific and unique requirements. Forthis reason, smaller Chinese banks have preferred domestic vendorswhile larger banks have preferred international vendors that can meettheir local needs. Similarly, many Malaysian banks have preferred localvendors that can meet their Islamic banking requirements.

Banks from developed markets like Singapore and Hong Kong havefirst-generation technical sophistication and are undertaking a cyclicalreplacement of their ageing systems. In contrast, banks in countries likeIndia, Pakistan and Vietnam are purchasing core banking systems forthe first time now. For obvious reasons, activity among the banks thatlack technical sophistication will increase.

We believe that most Asian banks prefer to select vendors that eitherinvolve local people through a setup in their country or partner localvendors. This is because there is a perception among the bankers thata local is more likely to understand and adapt to the unique local needsof a particular country. However in many countries, the availability ofinternational-quality products from local vendors is a limiting factor whichhas forced banks to look for alternatives.

•

•

•

China banks have preferencefor systems that cater to theirunique needs

18 Asian Banker Research Report

re banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 24/173

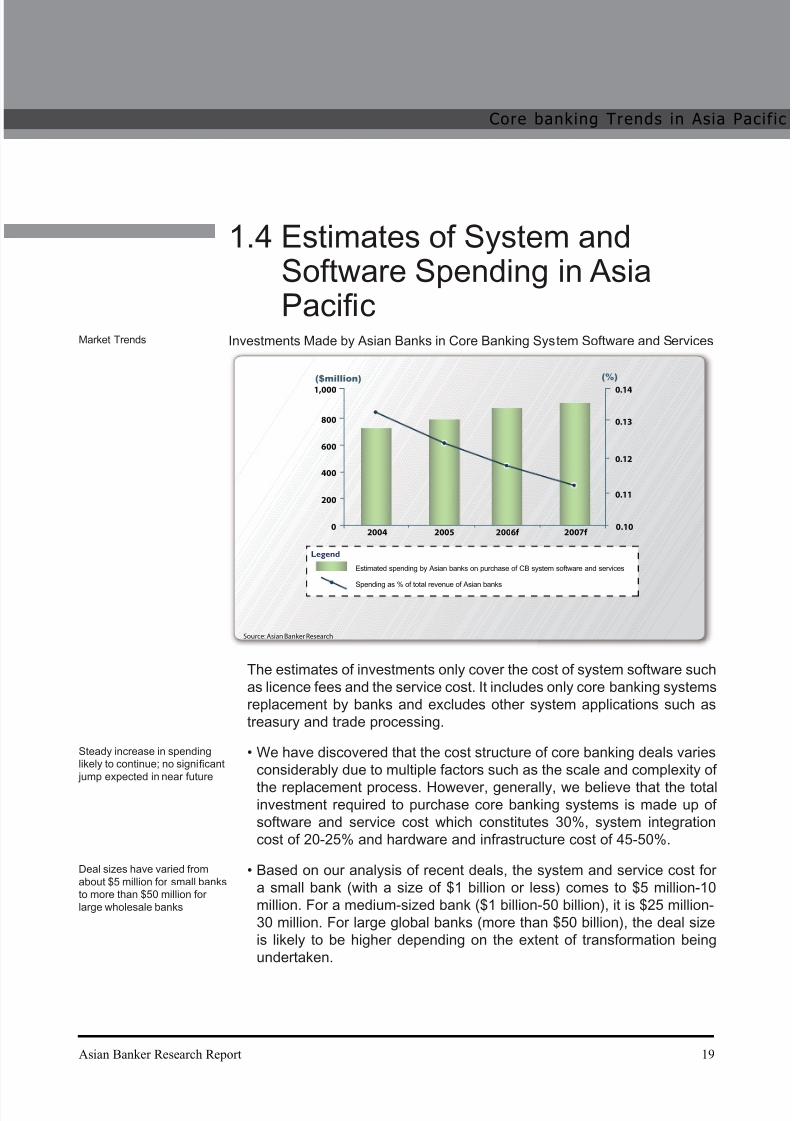

1.4 Estimates of System andSoftware Spending in AsiaPacifi c

Investments Made by Asian Banks in Core Banking System Software and Services

800

600

1,000

400

200

0.14

2004 2005 2006f 2007f 0

(%)($million)

0.10

0.13

0.12

0.11

Estimated spending by Asian banks on purchase of CB system software and services

Legend

Spending as % of total revenue of Asian banks

Source: Asian Banker Research

The estimates of investments only cover the cost of system software suchas licence fees and the service cost. It includes only core banking systemsreplacement by banks and excludes other system applications such astreasury and trade processing.

We have discovered that the cost structure of core banking deals variesconsiderably due to multiple factors such as the scale and complexity of

the replacement process. However, generally, we believe that the totalinvestment required to purchase core banking systems is made up ofsoftware and service cost which constitutes 30%, system integrationcost of 20-25% and hardware and infrastructure cost of 45-50%.

Based on our analysis of recent deals, the system and service cost fora small bank (with a size of $1 billion or less) comes to $5 million-10million. For a medium-sized bank ($1 billion-50 billion), it is $25 million-30 million. For large global banks (more than $50 billion), the deal sizeis likely to be higher depending on the extent of transformation beingundertaken.

•

•

Market Trends

Steady increase in spendinglikely to continue; no significant jump expected in near future

Deal sizes have varied fromabout $5 million for small banksto more than $50 million forlarge wholesale banks

Asian Banker Research Report 19

Core banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 25/173

A critical cost item is system software cost; this includes the cost ofsoftware licences, which varies depending on project. For example, forFNS customers, software licence cost has varied from $1 million to over$7 million, with an average of $1.8 million in 2005.

Overall, we have seen a steady rise in investment made by banks in Asia over recent years. We expect the trend to continue. However, asa percentage of total revenue, we believe the investments are likely toshow a declining trend as the banks have witnessed even higher growthin revenue. We also believe that there is stiff price competition amongvendors and that this will keep the costs in core banking replacementunder control.

•

•

20 Asian Banker Research Report

re banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 26/173

1.5 Evolution and Convergence ofCore Banking Systems

Evolution of Core Banking Systems

Business PlatformJ2EE, .NET

EAI, BPM, WS

Parameterisation

Legacy

systems

1970 1990 2004 2005

Web XML Web services Serv ice-oriented architecture?

China Bank:

Kirchman

ICICI: Finacle

HDFC: I-flex for

retail

KDB: FNS

Banco de Oro:

ICBS

Chinatrust:

FNS

HDFC: I-flex for

corporate

OCBC: Silverlake

StanChart:

testing open

sys

Kasikorn: IBM

Taishin: FNS

Baroda: Finacle

B.Shanghai:

Temenos

HSBC-Temenos DBS -

Infosys Central Bank

of India - TCS

China Minsheng - SAP

Source: Asian Banker Research

Convergence in Core Banking Systems

Parameters

Mainframe

systems

UNIX

systems

J2EE, .NET platforms; EAI, BI, WS integration tools

Towards

core banking

systems today

Source: Asian Banker Research

The first generation of banking technology was represented by the IBMmainframe, which had immense data processing capabilities but was not

as ef ficient in back-of fice accounting functions. Nonetheless its reliability

•

Technical Trends

Evolution of core bankingindustry in Asia showsincreasing convergence of

technologies and focus onarchitecture of systems

Asian Banker Research Report 21

Core banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 27/173

and scalability remain unbeaten today. In the next stage of evolution cameparameterisation of processing rules and enhancement in automationfrom back- to front-of fices. Here, the UNIX platform solutions haveshown high functionality, with some of them using relational databasetechnology to maintain accounting and administrative data.

UNIX systems have borrowed ideas freely from mainframes suchas logical partitioning, the ability for isolation, the ability to shareacross partitions, and common interfaces. Integration tools and othertechnological advancements have brought about a certain level ofstandardisation and convergence of technologies today at the platform,application and architectural layers.

Banks are increasingly looking for solutions that have the technicalcapability to meet their unique functional requirements while improvingtheir competitiveness. There is also increasing demand for component-based modular systems that do not have integration issues.

Trends in Requ irements

• Architecture that supports flexibility, growth and services such asService Oriented Architecture (SOA)

• Systems capable of global deployment – multi-channel, multilingualwith high connectivity

• Customer centric focus with increased connectivity acrossprocesses and functions. Integrated solution increasingly available

• Convergence of old and new technology with increased scalabilityand flexibility

Source: Asian Banker Research

Service Oriented Architecture (SOA) is a relatively new concept thathas gained popularity quickly. Herein, business applications areconstructed from independent reusable interoperable services that canbe reconfigured without a vast amount of technical labour. The conceptis based on web services and components that are brought together toperform specific business tasks. It essentially means reducing barriers inantiquated infrastructure and creating a real-time integration of disparatesystems and a sharing of databases on a flexible and easily upgradeableinfrastructure. We discuss this in more detail in section 5.

On the architectural front, J2EE and .NET are two architectural frameworks

that have evolved in the last few years. These are new-generation flexible

•

•

•

•

Banks need to adopt ServiceOriented Architecture

22 Asian Banker Research Report

re banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 28/173

and interoperable architectures that facilitate the complete meshing ofcore banking solutions with the complex technology fabric of the bank.

The key attributes that banks require from their architecture are flexibility,scalability and agility. With customer expectations increasing, banks havemoved towards centralised systems with customer-centric architecture,where they drive the business through a single view of the customer andthe paramount consideration in all decisions is the consumer.

IT Service Providers in the Region

• Vendor consolidation through mergers and acquisitions.

• Partnership among vendors to mix and match solutions.

• Standard protocols and fierce competition among IT serviceproviders leading to increased product offerings and pricecompetition.

Source: Asian Banker Research

The growth in demand for core banking systems in Asia Pacific hasprompted many international vendors such as SAP, Temenos, Fidelity

and Misys to focus increasingly on the region. At the same time, vendorsthat began their operations in Asian countries have grown to becomerecognised names across the world; these include companies likeInfosys, I-flex and TCS.

Desire to become the leading player in the market has led to mergersand acquisitions among IT service providers. At the global level, Fidelity’sacquisition of Sanchez broadened its reach to a larger collection ofbanks. Among leading vendors in Asia, TCS acquired FNS in a leap fromtheir previous alliance. Another example of consolidation in the industry

is Oracle’s acquisition of a stake in I-flex. These players are developingan increasingly strong foothold in the core banking systems market.

Greater convergence makes it dif ficult for bankers to differentiatebetween vendors’ value propositions. However standard protocols andfierce competition have led to more product offerings and price wars – aboon for the industry as a whole.

•

•

•

•

Asian vendors are increasingtheir global reach

Desire to become leadingplayer has led to consolidationin the industry

Asian Banker Research Report 23

Core banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 29/173

1.6 Technology Integration in Asian Countries

Technology Integration in As ian Countries

‘ A c c o u n t c e n t r i c i t y ’

‘ C u s t o m e r c e n t r i c i t y ’

Thailand

India (State Banks)

Philippines

China

Malaysia

Indonesia

Hong Kong

Taiwan

Singapore

Aus tral ia

India (Private Banks)

Japan

Korea

B r a n

c h

c o m p u

t e r i s

a t i o n

B r a n

c h

n e t w

o r k i n

g

C e n t r a l i s

e d

d a t a

c e n t r e

C o r e

b a n k

i n g s y s t e m s

a d v a n c

e m e n t

R o b u

s t m i d d l e w

a r e

a n d b

a s i c C R

M

W e b s

e r v i c

e s a n d

c u s t o

m e r

c e n t r i c

i t y

Source: Asian Banker Research

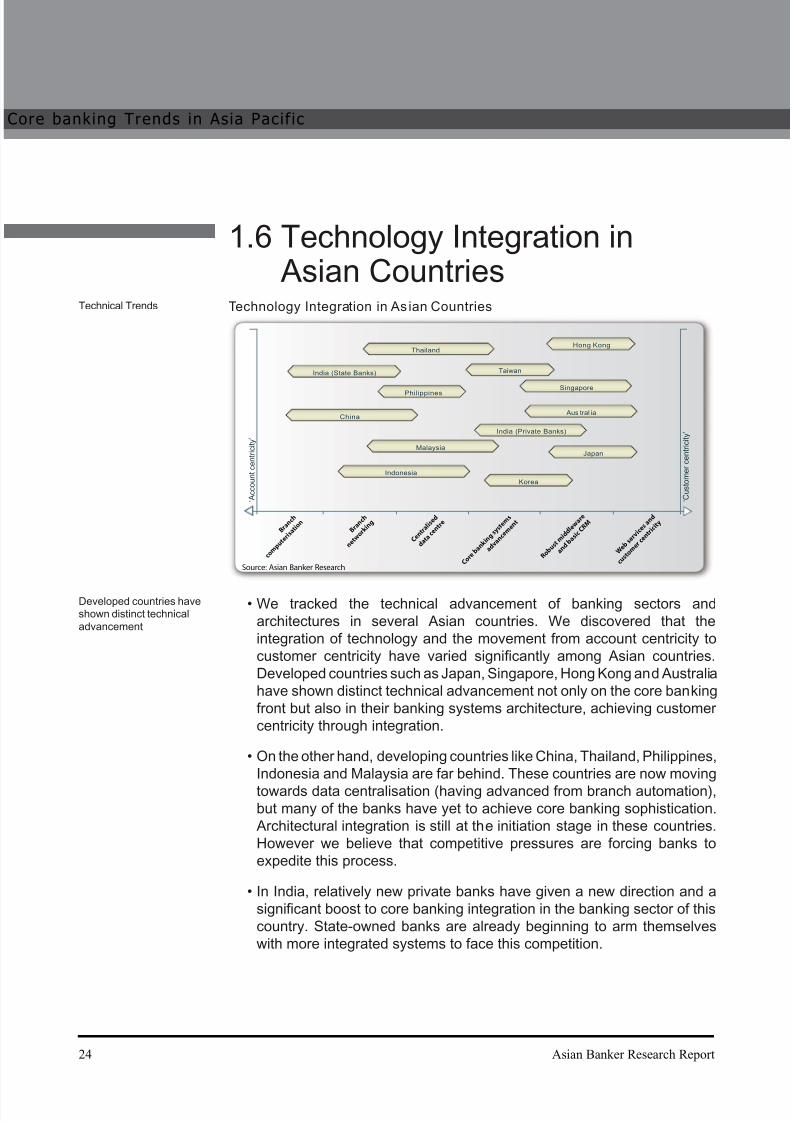

We tracked the technical advancement of banking sectors andarchitectures in several Asian countries. We discovered that theintegration of technology and the movement from account centricity tocustomer centricity have varied significantly among Asian countries.Developed countries such as Japan, Singapore, Hong Kong and Australiahave shown distinct technical advancement not only on the core bankingfront but also in their banking systems architecture, achieving customercentricity through integration.

On the other hand, developing countries like China, Thailand, Philippines,Indonesia and Malaysia are far behind. These countries are now movingtowards data centralisation (having advanced from branch automation),but many of the banks have yet to achieve core banking sophistication. Architectural integration is still at the initiation stage in these countries.However we believe that competitive pressures are forcing banks toexpedite this process.

In India, relatively new private banks have given a new direction and asignificant boost to core banking integration in the banking sector of thiscountry. State-owned banks are already beginning to arm themselveswith more integrated systems to face this competition.

•

•

•

Technical Trends

Developed countries haveshown distinct technicaladvancement

24 Asian Banker Research Report

re banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 30/173

1.7 Trends in Platform Usage Among Asian Countries

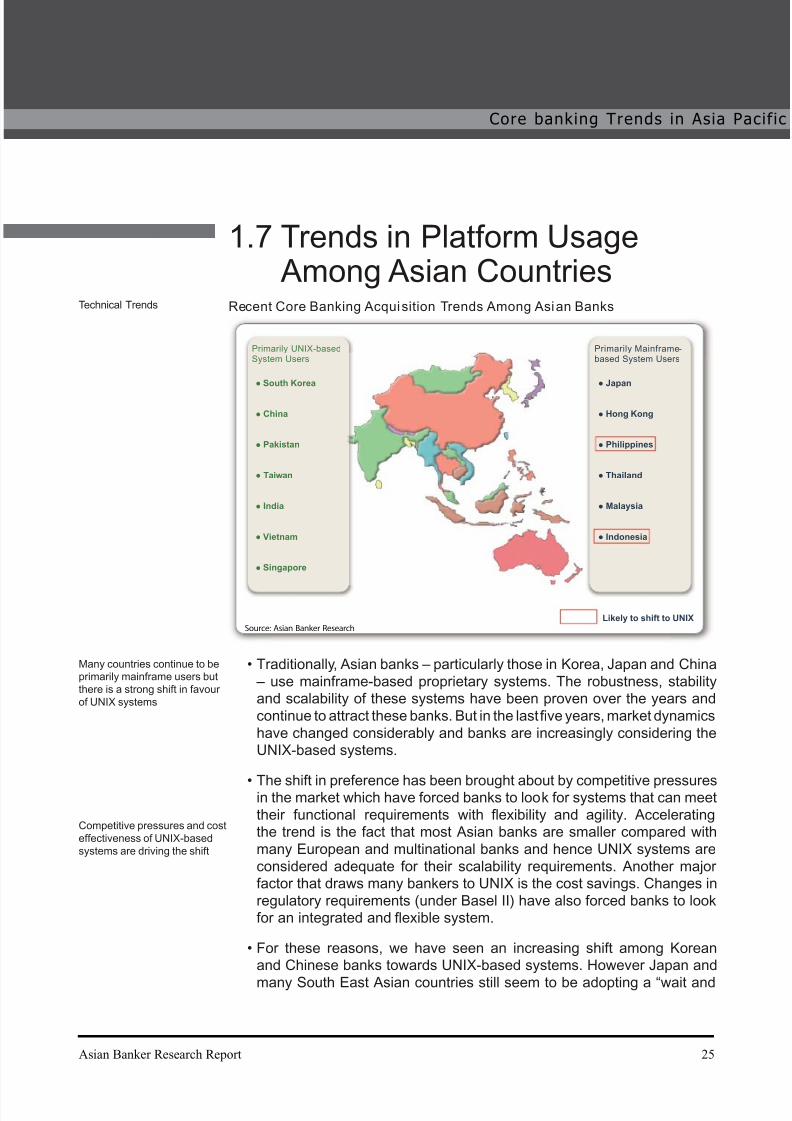

Recent Core Banking Acquisition Trends Among Asian Banks

● South Korea

● China

● Pakistan

● Taiwan

● India

● Vietnam

● Singapore

Primarily UNIX-basedSystem Users

● Japan

● Hong Kong

● Philippines

● Thailand

● Malaysia

● Indonesia

Primarily Mainframe-based System Users

Likely to shift to UNIXSource: Asian Banker Research

Traditionally, Asian banks – particularly those in Korea, Japan and China – use mainframe-based proprietary systems. The robustness, stabilityand scalability of these systems have been proven over the years andcontinue to attract these banks. But in the last five years, market dynamicshave changed considerably and banks are increasingly considering theUNIX-based systems.

The shift in preference has been brought about by competitive pressuresin the market which have forced banks to look for systems that can meettheir functional requirements with flexibility and agility. Acceleratingthe trend is the fact that most Asian banks are smaller compared withmany European and multinational banks and hence UNIX systems areconsidered adequate for their scalability requirements. Another majorfactor that draws many bankers to UNIX is the cost savings. Changes inregulatory requirements (under Basel II) have also forced banks to lookfor an integrated and flexible system.

For these reasons, we have seen an increasing shift among Koreanand Chinese banks towards UNIX-based systems. However Japan and

many South East Asian countries still seem to be adopting a “wait and

•

•

•

Technical Trends

Many countries continue to beprimarily mainframe users butthere is a strong shift in favourof UNIX systems

Competitive pressures and costeffectiveness of UNIX-basedsystems are driving the shift

Asian Banker Research Report 25

Core banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 31/173

see” approach. In mature countries like Singapore, there are very fewdeals as well; but in the country’s most recent deal, DBS opted in favourof a UNIX platform.

In the Indian subcontinent, most commercial banks are adoptingcore banking systems for the first time. Thus most banks have takenadvantage of this new-generation technology. As there is no problemof integrating with the existing system, implementation is cheaper andless complex. Moreover, the traditional preference of Indian banks (andIndian vendors) is for a UNIX environment.

While smaller Asian banks have favoured UNIX-based systems owingto their cost effectiveness, we believe that mainframe has proved to bemore reliable and scalable for a larger size of operations. As transactionvolumes increase, the total cost per user in mainframe decreases,making it more competitive.

•

•

26 Asian Banker Research Report

re banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 32/173

1.8 Trends in Deployment Approach

Deployment Approaches in Recent Core Banking Decision

Long

Duration

Existing

Implementation

Time

Short

Duration

Gradual Implementation Big Bang Implementation

Implementation

App roac h

Singapore

HSBCBank

ChinaMinsheng

Bank

CentralBank of

India

AllahabadBank

MuslimCommercial

Bank

Bank ofPanshin

UnionBank of

Philippines

Bank of East Asia

Hua XiaBank

IndustrialBank ofKorea

CathayUnitedBank

StateBank of India

DBSBank

ChinaDevelopment-

Bank

Bank Asset Size

More than$100 billion

$20-100 billion

Less than$20 billion

Source: Asian Banker Research

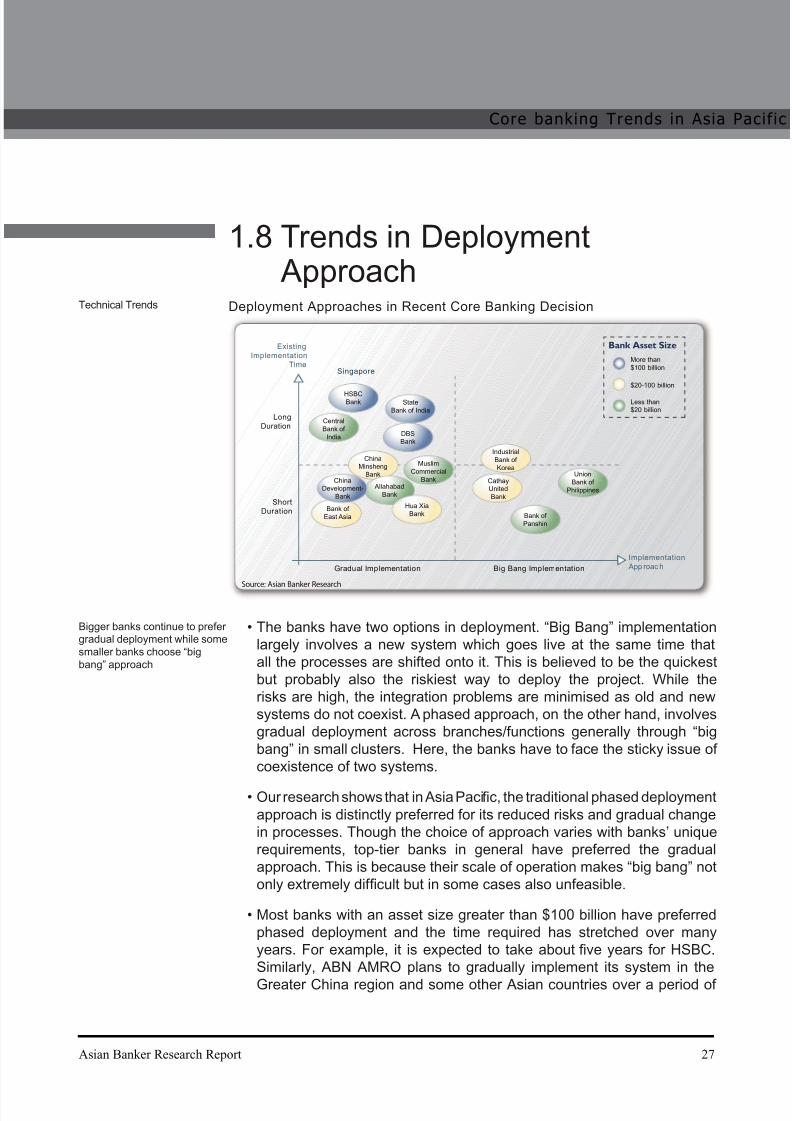

The banks have two options in deployment. “Big Bang” implementationlargely involves a new system which goes live at the same time thatall the processes are shifted onto it. This is believed to be the quickestbut probably also the riskiest way to deploy the project. While therisks are high, the integration problems are minimised as old and newsystems do not coexist. A phased approach, on the other hand, involvesgradual deployment across branches/functions generally through “bigbang” in small clusters. Here, the banks have to face the sticky issue ofcoexistence of two systems.

Our research shows that in Asia Pacific, the traditional phased deploymentapproach is distinctly preferred for its reduced risks and gradual changein processes. Though the choice of approach varies with banks’ uniquerequirements, top-tier banks in general have preferred the gradualapproach. This is because their scale of operation makes “big bang” notonly extremely dif ficult but in some cases also unfeasible.

Most banks with an asset size greater than $100 billion have preferredphased deployment and the time required has stretched over manyyears. For example, it is expected to take about five years for HSBC.Similarly, ABN AMRO plans to gradually implement its system in the

Greater China region and some other Asian countries over a period of

•

•

•

Technical Trends

Bigger banks continue to prefergradual deployment while somesmaller banks choose “bigbang” approach

Asian Banker Research Report 27

Core banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 33/173

five years. For State Bank of India and Central Bank of India, it is likely tobe around four years. We believe that it is critical to keep the rollout timeand the period that two systems coexist as short as possible.

On the other hand, a few smaller banks have taken the quicker approachof “big bang”. These include: Union Bank of Philippines whose systemby Infosys was implemented in just one year; Industrial Bank of Korea byTemenos; and Cathay United Bank, Taiwan by TCS-FNS.

•

28 Asian Banker Research Report

re banking Trends in Asia Pacif ic

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 34/173

2Bankers’ PerceptionSurvey on CoreBanking SystemSelectionWe have conducted a series of surveys in the Asian banking

sector to strengthen our research on various aspects of corebanking transformation. Our surveys have given us an insight

into how bankers assess various vendors in the region, key

considerations in the selection of a new system, and platform

preference among Asian banks. We have discovered that some

of the common perceptions lack sound foundation.

Bankers’ Perception Survey on Core Banking SystemSelection

2.1 Survey results on key reasons for replacement

2.2 Survey results on factors considered in system selection

2.3 UNIX versus mainframe – survey results on considerations in

system selection

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 35/173

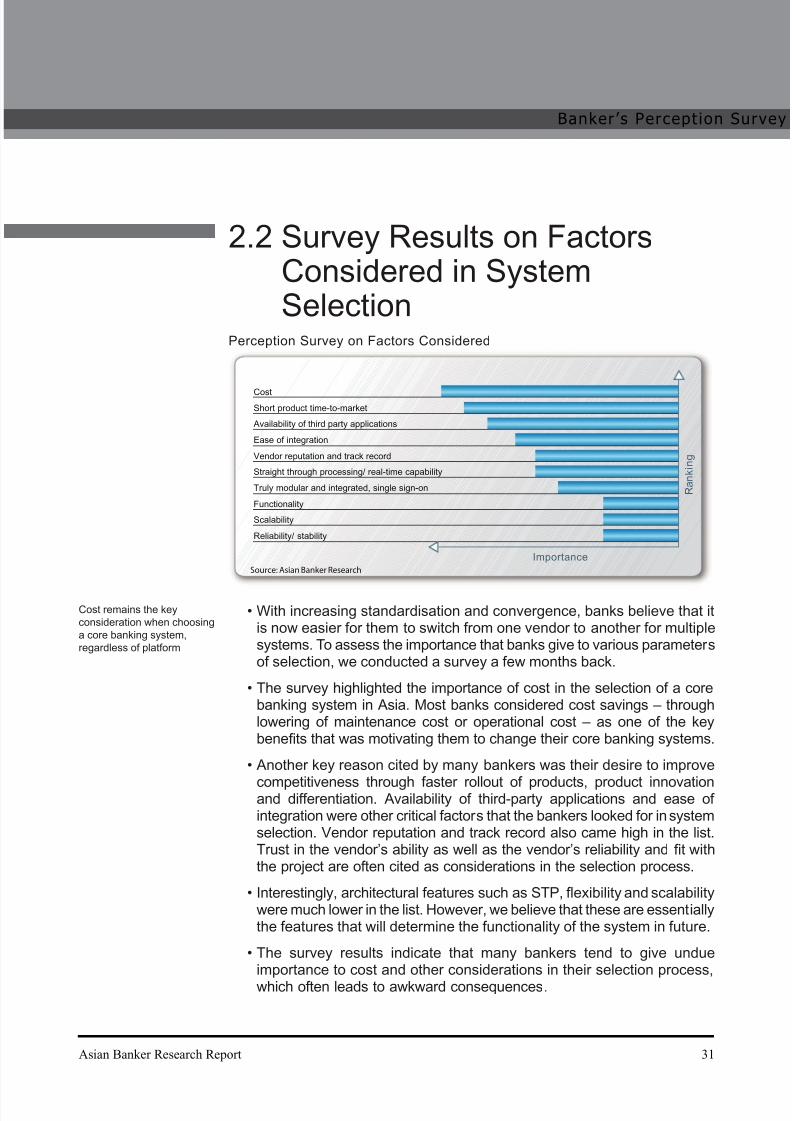

2.1 Survey Results on KeyReasons for Replacement

Perception Survey on Key Reasons for Replacement

% of executives citing area as a problem10 20 30 40 50 60 70 80

Other

Errors in operation

Errors in data

Availability

Errors in processing

Scalability

Timing problems

Technology

Simplification

Integration

Cost

Flexibility

Source: Asian Banker Research

A survey done in Asia Pacific countries last year found that inflexibility,

high cost and dif ficulty of integration were the three main problems that

banks faced in legacy systems.

•

30 Asian Banker Research Report

nker ’s Perception Survey

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 36/173

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 37/173

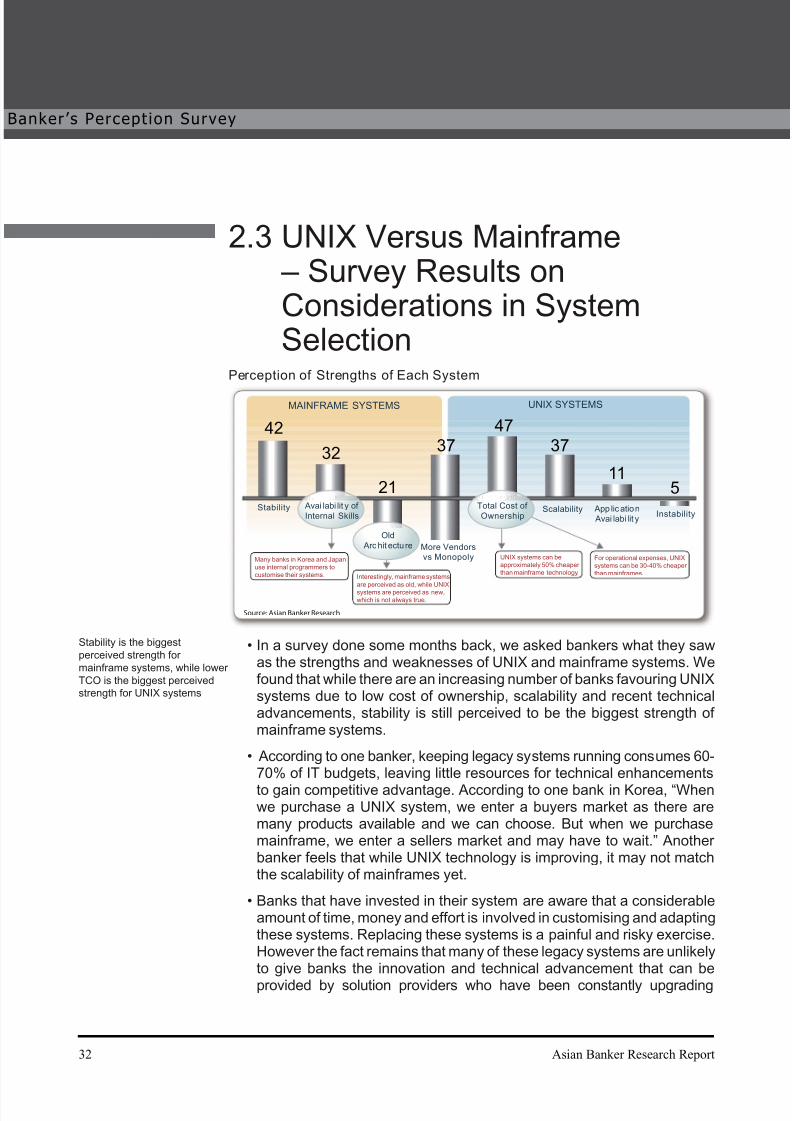

2.3 UNIX Versus Mainframe – Survey Results onConsiderations in SystemSelection

Perception of Strengths of Each System

Interestingly, mainframe systems

are perceived as old, while UNIX

systems are perceived as new,

which is not always true.

Stability

Old

Archit ecture More Vendorsvs Monopoly

Scalability App lication

Avai labi lit yInstability

42

32

21

37

47

37

115

MAINFRAME SYSTEMS UNIX SYSTEMS

Avai labi lit y of

Internal Skills

Many banks in Korea and Japan

use internal programmers to

customise their systems.

Total Cost of

Ownership

UNIX systems can be

approximately 50% cheaper

than mainframe technology.

For operational expenses, UNIX

systems can be 30-40% cheaper

than mainframes.

Source: Asian Banker Research

In a survey done some months back, we asked bankers what they sawas the strengths and weaknesses of UNIX and mainframe systems. Wefound that while there are an increasing number of banks favouring UNIXsystems due to low cost of ownership, scalability and recent technicaladvancements, stability is still perceived to be the biggest strength ofmainframe systems.

According to one banker, keeping legacy systems running consumes 60-70% of IT budgets, leaving little resources for technical enhancements

to gain competitive advantage. According to one bank in Korea, “Whenwe purchase a UNIX system, we enter a buyers market as there aremany products available and we can choose. But when we purchasemainframe, we enter a sellers market and may have to wait.” Anotherbanker feels that while UNIX technology is improving, it may not matchthe scalability of mainframes yet.

Banks that have invested in their system are aware that a considerableamount of time, money and effort is involved in customising and adaptingthese systems. Replacing these systems is a painful and risky exercise.However the fact remains that many of these legacy systems are unlikelyto give banks the innovation and technical advancement that can be

provided by solution providers who have been constantly upgrading

•

•

•

Stability is the biggest

perceived strength for

mainframe systems, while lower

TCO is the biggest perceived

strength for UNIX systems

32 Asian Banker Research Report

nker ’s Perception Survey

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 38/173

their technology. Banks are increasingly realising that their expertise isin banking and not IT development.

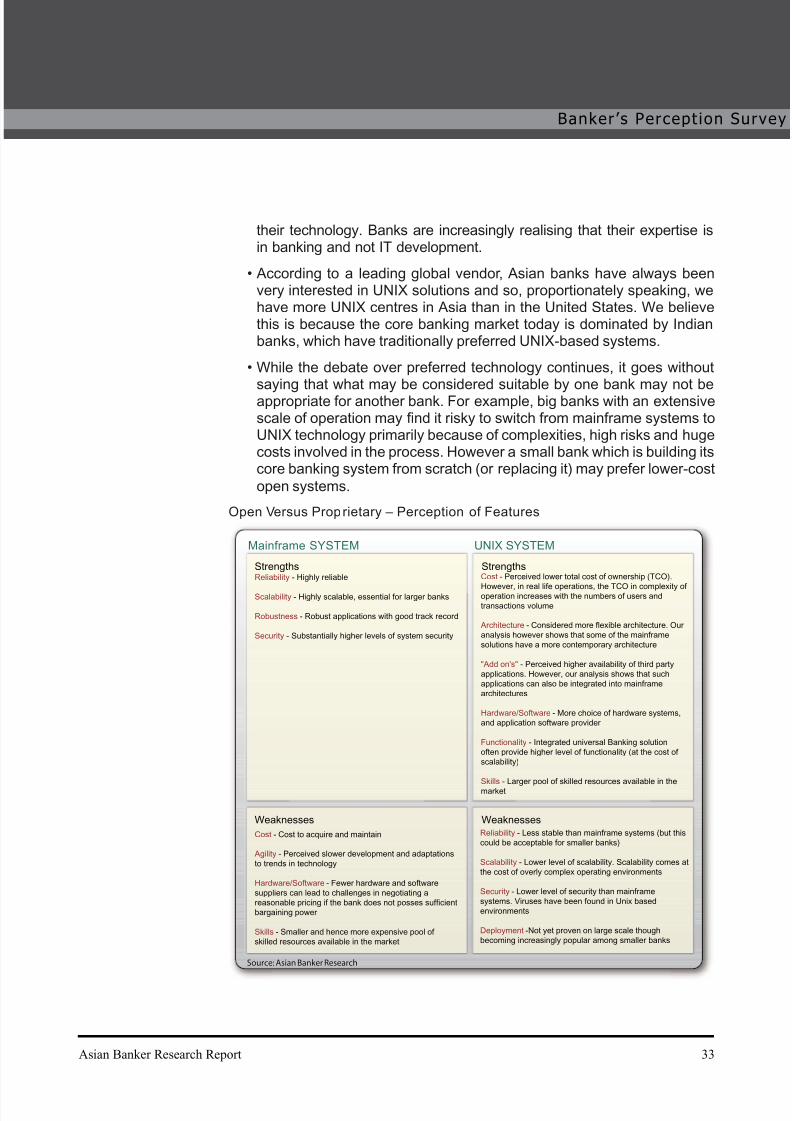

According to a leading global vendor, Asian banks have always beenvery interested in UNIX solutions and so, proportionately speaking, wehave more UNIX centres in Asia than in the United States. We believethis is because the core banking market today is dominated by Indianbanks, which have traditionally preferred UNIX-based systems.

While the debate over preferred technology continues, it goes withoutsaying that what may be considered suitable by one bank may not beappropriate for another bank. For example, big banks with an extensivescale of operation may find it risky to switch from mainframe systems toUNIX technology primarily because of complexities, high risks and hugecosts involved in the process. However a small bank which is building itscore banking system from scratch (or replacing it) may prefer lower-cost

open systems.

Open Versus Proprietary – Perception of Features

Strengths

Weaknesses

Strengths

Weaknesses

Reliability - Highly reliable

Scalability - Highly scalable, essential for larger banks

Robustness - Robust applications with good track record

Security - Substantially higher levels of system security

Cost - Cost to acquire and maintain

Agility - Perceived slower development and adaptations

to trends in technology

Hardware/Software - Fewer hardware and software

suppliers can lead to challenges in negotiating a

reasonable pricing if the bank does not posses sufficient

bargaining power

Skills - Smaller and hence more expensive pool of

skilled resources available in the market

Cost - Perceived lower total cost of ownership (TCO).

However, in real life operations, the TCO in complexity ofoperation increases with the numbers of users and

transactions volume

Architecture - Considered more flexible architecture. Our

analysis however shows that some of the mainframe

solutions have a more contemporary architecture

"Add on's" - Perceived higher availability of third party

applications. However, our analysis shows that such

applications can also be integrated into mainframe

architectures

Hardware/Software - More choice of hardware systems,

and application software provider

Functionality - Integrated universal Banking solution

often provide higher level of functionality (at the cost of

scalability)

Skills - Larger pool of skilled resources available in themarket

Reliability - Less stable than mainframe systems (but this

could be acceptable for smaller banks)

Scalability - Lower level of scalability. Scalability comes at

the cost of overly complex operating environments

Security - Lower level of security than mainframe

systems. Viruses have been found in Unix based

environments

Deployment -Not yet proven on large scale though

becoming increasingly popular among smaller banks

UNIX SYSTEMMainframe SYSTEM

Source: Asian Banker Research

•

•

Asian Banker Research Report 33

Banker ’s Perception Survey

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 39/173

Open systems have proved their ability to perform from the security and

technology points of view. According to one banker, “5-10 years ago a

large bank would go for mainframe, no questions asked. But in the last

5-10 years things have changed. Any bank today, no matter how big,

may consider switching to open system.”

On the other hand, most big banks still favour the reliability and stability

of mainframes. Some bankers are inclined towards proprietary systems

as they are used to working on them. Switching to a new technology

would not only involve a huge amount of cost and high risks but also

require effort to get used to the new processes.

According to one vendor, “Open systems are most appropriate for Asian

banks due to their smaller size compared to many international banks.

They don’t need the scalability of mainframes and the scalability of open

systems has really increased in recent years.” One leading bank in Korea

states that the trend in Korea today is to shift towards UNIX systems

from IBM “due to the availability of small packages that can be easily

integrated in our system [whereas] when we use mainframe we need to

code them which would be a time consuming proposition”.

The right choice varies with banks’ requirements

As can be seen from the survey, platform choice is a dilemma that all

bankers face when they consider replacement. Our in-depth analysis

shows that for smaller Asian banks, a UNIX platform could be more

feasible as they may not need the scalability of the mainframe and UNIX

can be cost effective for a small number of transactions. However our

research shows that for large retail banks, mainframe is likely to still be

the preferred choice because:

It is more reliable and keeps the system running through most upgrades.

Hence the downtime is low.

It has the capability to support a large number of users, supports

multiple applications and allows better resource management. This is

especially important where transaction volumes are high.

It requires less server capacity than UNIX for the same amount of work

and has higher continuous availability (due to less downtime).

On the cost issue, UNIX-based systems are generally believed to have

a lower total cost of ownership (TCO). However the benchmark, we

believe, should not be total cost of ownership but total cost per user. Our

research indicates that when the bank has large volumes of transactions

and users, the operational cost of mainframe could be lower on a per-user

•

•

•

•

-

-

-

•

Strengths and weaknesses of

proprietary and open systems,

as perceived by respondent

banks

Our research and analysis of

the platform features reveal a

different picture

34 Asian Banker Research Report

nker ’s Perception Survey

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 40/173

basis. Also, while making the cost comparison, banks must consider the

switching costs (shifting from existing mainframe to UNIX) and the cost

of the coexistence of two systems during the replacement process.

Please see our section on platform choices in section 4 for more details

Asian Banker Research Report 35

Banker ’s Perception Survey

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 41/173

This page has been left intentionallly blank

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 42/173

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 43/173

3.1 Core Banking System – AnIntroduction and Defi nition

Core banking replacement is becoming a hot topic in banking. We

have discovered that many banks are considering core banking system

replacement because of the following perceived needs:

Ageing Technology Infrastructure – Ageing technology that is

increasingly dif ficult and expensive to maintain and support

No Common Customer View – Multiple customer views and complex

processes are not easily integrated with the existing technology

infrastructure

No Product Factory – Innovative, highly interdependent product bundles

are not supported by the existing core banking system; it is laborious to

launch new products and services

Long Deployment Cycle – Technological inflexibility demands lengthy

development cycles

No/Limited Basel II Support – New and more complex Basel II-drivenrisk frameworks are not supported

Due to such perceptions, the business users demand an immediate

replacement of the core banking systems. Here are some examples of

the justification given for this investment to address all of these issues:

“We are losing market share. We need to replace our core banking

system now to increase our competitiveness and regain lost markets.”

“We need to replace our core banking system to have a better

understanding of our customer.”

“We need to replace our core banking system to be able to bring new

products to the market faster.”

“We need a core banking-enabled product factory.”

These and similar statements are what we hear when talking to leading

bankers throughout the region.

The software vendors of course are responding to these needs, by

claiming:

•

-

-

-

-

-

•

-

-

-

-

•

Perceived needs justifying

replacement of core banking

system

38 Asian Banker Research Report

ore Banking System Overview

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 44/173

Core Banking System Overview

“Our system will transform your organisation and make your bank more

competitive.”

“With our system, you will be able to significantly enhance your CRM

capabilities and gain market share.”

“Our solution will automate your lending process, improve your collateral

management capabilities and make you Basel II compliant.”

The key questions which now arise are:

Are the bankers’ perceptions about the outcome of a core banking

replacement correct?

Does a “traditional” core banking replacement project address all of

these issues?

Do the statements made by software vendors truly reflect what their

clients can expect from a core banking replacement project?

To answer these questions, it is necessary to clearly define what a core

banking replacement really is

3.1.1 Definition of a core banking system

We have discovered that there are multiple definitions of core banking

systems today. However based on our discussions with industry experts,

we can define core banking, in simple terms, as a highly ef ficient “customer

accounting” and transaction processing engine for high volumes of back-

of fice transactions. The purpose of a core banking system is thus to

give banks the ability to process large transaction volumes in a fast and

ef ficient way; clearing, transfers and interest/fee calculation are all the

fortes of core banking. But let us explore this in more detail and look atsome of the myths regarding core banking replacement projects.

What Core Banking Systems Do

A core banking system is a transaction processing engine with customer-

level accounting and reporting of the deposit and loan products processed

in the bank.

Core banking also deals with transactions such as interest and fee

calculation, pre-processing for statement printing, end-of-day processing,

and consolidation of daily individual transactions as

-

-

-

•

-

-

-

•

•

•

Core banking system is simply

the core processing power of

the bank

Asian Banker Research Report 39

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 45/173

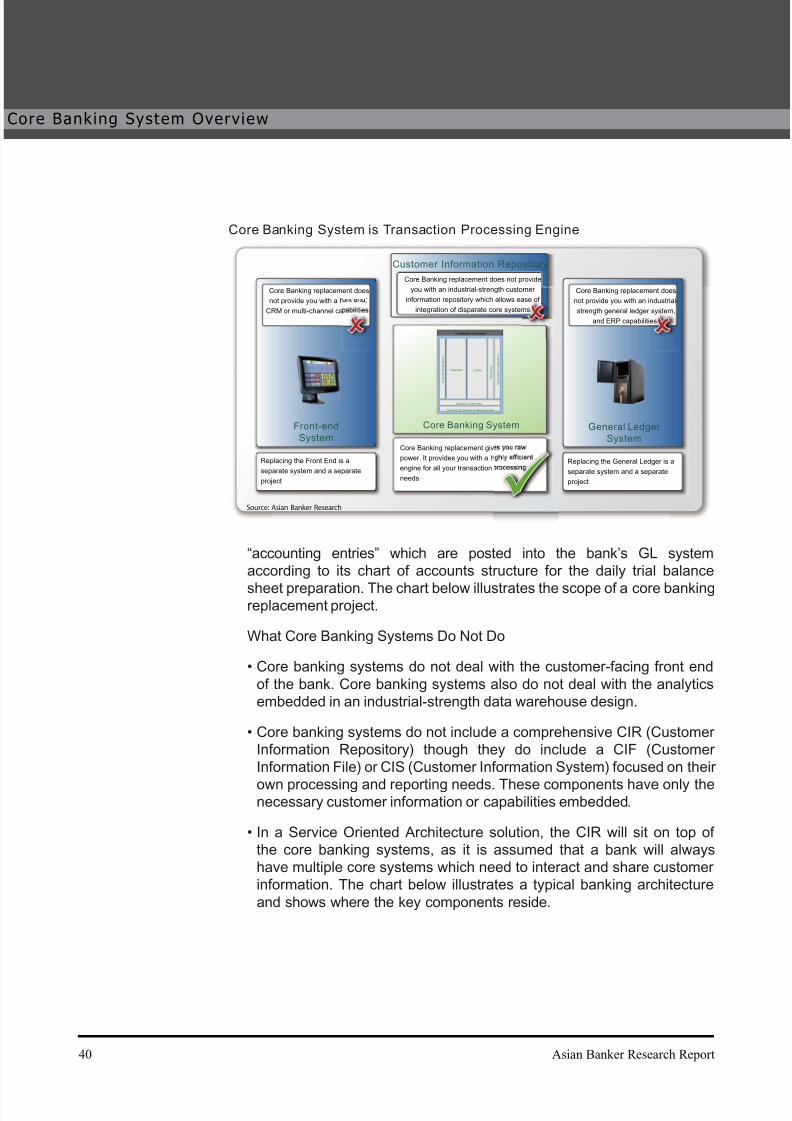

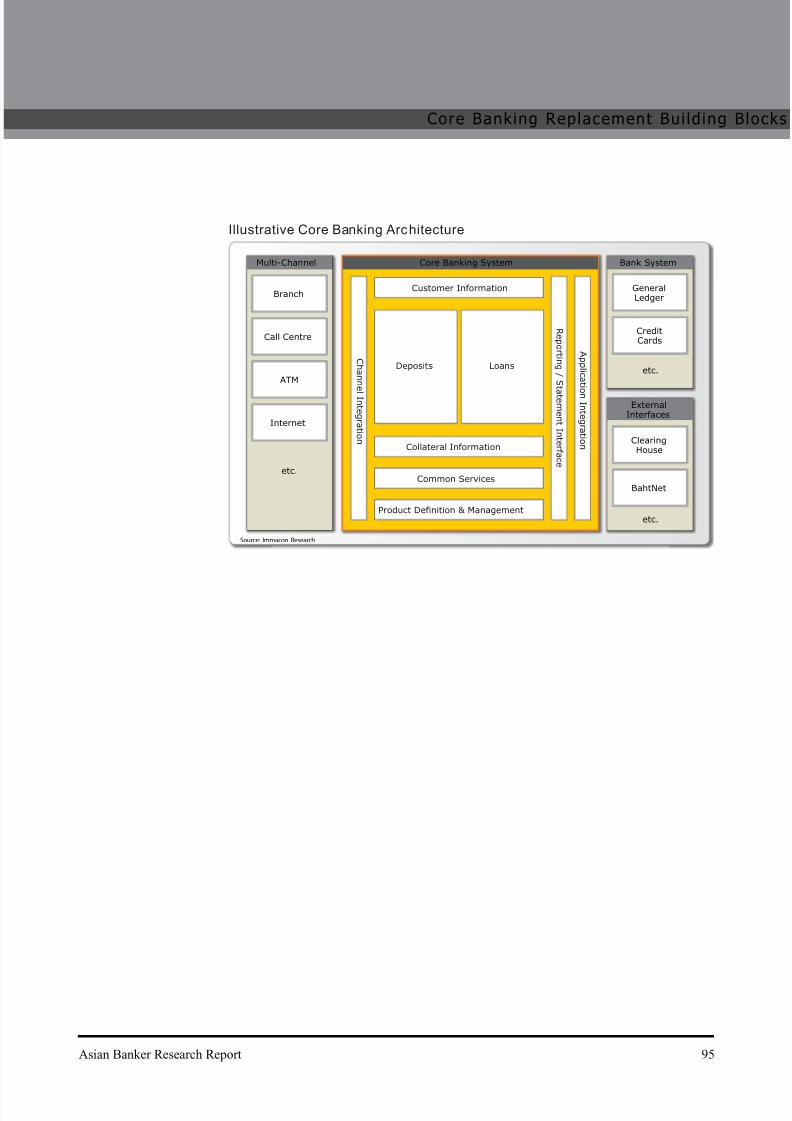

Core Banking System is Transaction Processing Engine

Deposits Loans

Common Services

Product Definition & Management

CoreBanki ng System

C h a n n e l I n t e g r a t i o n

A p p l i c a t i o n

I n t e g r a t i o n

R e p o r t i n g

Core Banking replacement does

not provide you with a front end,

CRM or multi-channel capabilities.

Core Banking replacement does

not provide you with an industrial-

strength general ledger system,

and ERP capabilities.

Replacing the Front End is a

separate system and a separate

project

Replacing the General Ledger is a

separate system and a separate

project

Core Banking replacement does not provide

you with an industrial-strength customer

information repository which allows ease of

integration of disparate core systems

Core Banking replacement gives you raw

power. It provides you with a highly efficient

engine for all your transaction processing

needs

General Ledger

System

Front-end

System

Core Banking System

Customer Information Repository

Source: Asian Banker Research

“accounting entries” which are posted into the bank’s GL system

according to its chart of accounts structure for the daily trial balance

sheet preparation. The chart below illustrates the scope of a core bankingreplacement project.

What Core Banking Systems Do Not Do

Core banking systems do not deal with the customer-facing front end

of the bank. Core banking systems also do not deal with the analytics

embedded in an industrial-strength data warehouse design.

Core banking systems do not include a comprehensive CIR (Customer

Information Repository) though they do include a CIF (Customer

Information File) or CIS (Customer Information System) focused on their

own processing and reporting needs. These components have only thenecessary customer information or capabilities embedded.

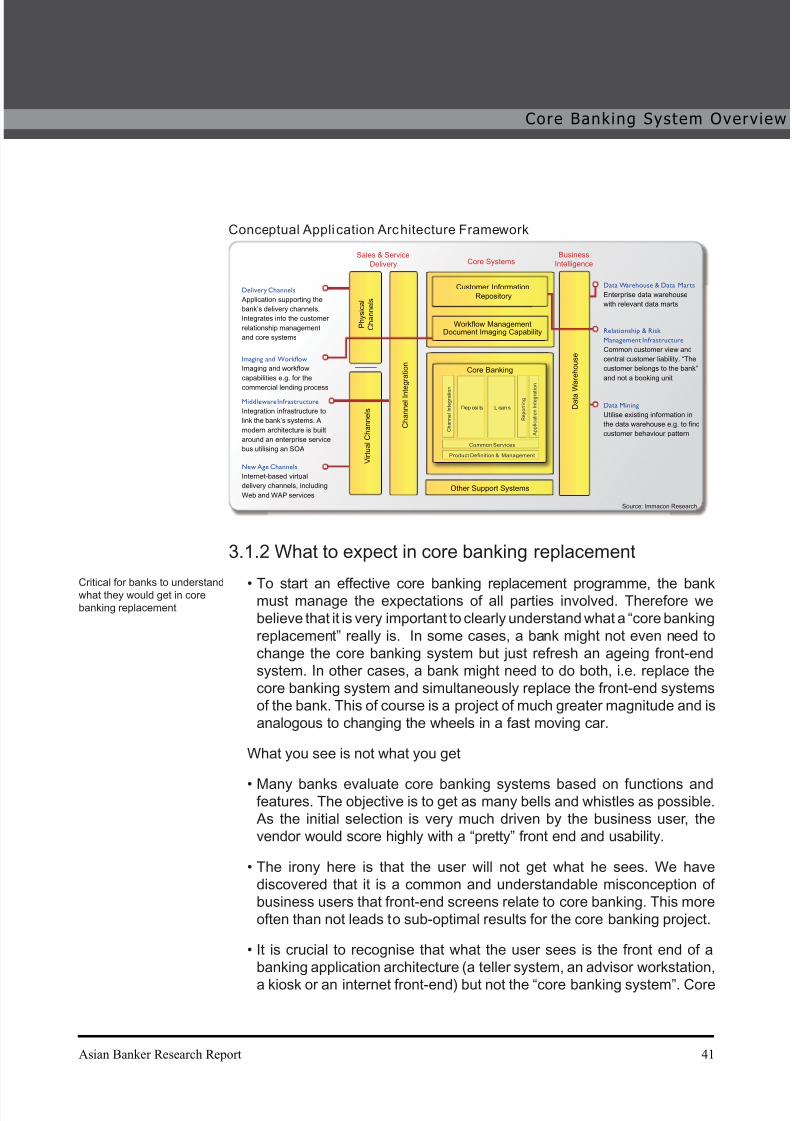

In a Service Oriented Architecture solution, the CIR will sit on top of

the core banking systems, as it is assumed that a bank will always

have multiple core systems which need to interact and share customer

information. The chart below illustrates a typical banking architecture

and shows where the key components reside.

•

•

•

40 Asian Banker Research Report

ore Banking System Overview

8/10/2019 Asian Banker - Core Banking Replacement

http://slidepdf.com/reader/full/asian-banker-core-banking-replacement 46/173

Conceptual Application Architecture Framework

Sales & Service

Delivery

Business

IntelligenceCore Systems

Delivery Channels

Application supporting the

bank’s delivery channels.

Integrates into the customer

relationship management

and core systems

Data Warehouse & Data Marts

Enterprise data warehouse

with relevant data marts

Relationship & Risk

Management Infrastructure

Common customer view and

central customer liability. “The

customer belongs to the bank”

and not a booking unit

Data Mining

Utilise existing information in

the data warehouse e.g. to find

customer behaviour pattern

Imaging and Workflow

Imaging and workflow

capabilities e.g. for the

commercial lending process

Middleware Infrastructure

Integration infrastructure to

link the bank’s systems. A

modern architecture is built

around an enterprise service

bus utilising an SOA

New Age Channels

Internet-based virtual

delivery channels, including

Web and WAP services

Customer Information

Repository

D a t a W a r e h o u s e

C h a n n e l I n t e g r a t i o n

P h y s i c a l

C h a n n e l s

V i r t u a l C h a n n e l s

Other Support Systems

Workflow ManagementDocument Imaging Capability

Core Banking

Dep osi ts L oan s

A p p l i c a t i o n I n t e g r a t i o n

C h a n n e l I n t e g r a t i o

n

R e p o r t i n g

Common Services

Product Definition & Management

Source: Immacon Research

3.1.2 What to expect in core banking replacement

To start an effective core banking replacement programme, the bankmust manage the expectations of all parties involved. Therefore we

believe that it is very important to clearly understand what a “core banking

replacement” really is. In some cases, a bank might not even need to

change the core banking system but just refresh an ageing front-end

system. In other cases, a bank might need to do both, i.e. replace the

core banking system and simultaneously replace the front-end systems

of the bank. This of course is a project of much greater magnitude and is

analogous to changing the wheels in a fast moving car.

What you see is not what you get

Many banks evaluate core banking systems based on functions andfeatures. The objective is to get as many bells and whistles as possible.

As the initial selection is very much driven by the business user, the

vendor would score highly with a “pretty” front end and usability.

The irony here is that the user will not get what he sees. We have

discovered that it is a common and understandable misconception of

business users that front-end screens relate to core banking. This more