Asia Pacific Healthcare Outlook 2012-2015

19

Asia Pacific Healthcare Outlook 2012- 2015 What comes next…. Rhenu Bhuller Vice President, HC

-

Upload

frost-sullivan -

Category

Business

-

view

2.609 -

download

4

Transcript of Asia Pacific Healthcare Outlook 2012-2015

Asia Pacific Healthcare Outlook 2012- 2015

What comes next….

Rhenu BhullerVice President, HC

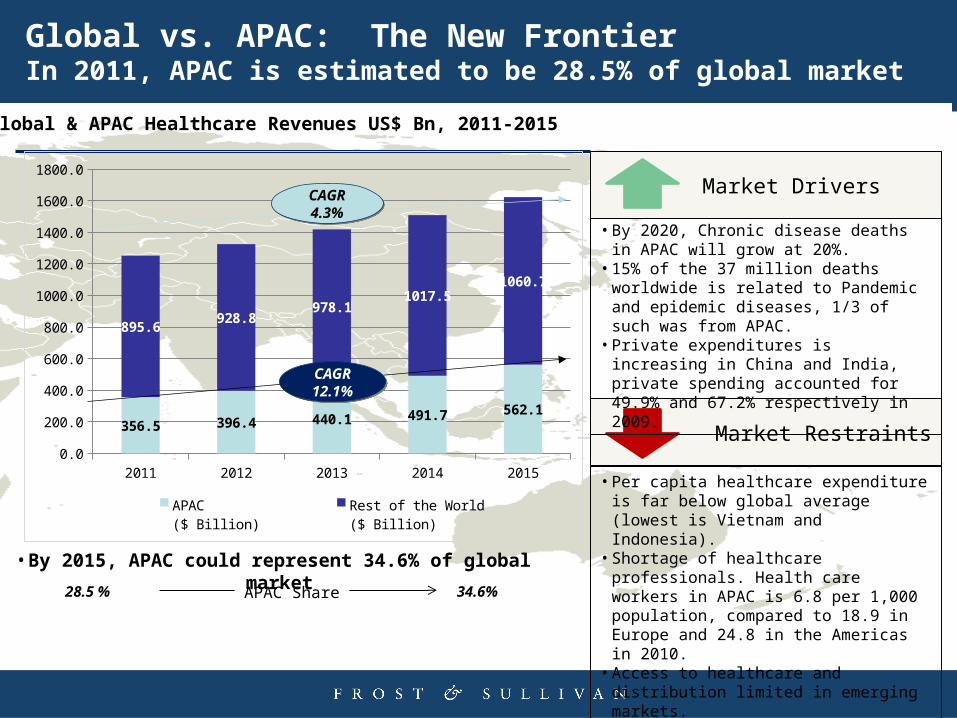

• Per capita healthcare expenditure is far below global average (lowest is Vietnam and Indonesia).

• Shortage of healthcare professionals. Health care workers in APAC is 6.8 per 1,000 population, compared to 18.9 in Europe and 24.8 in the Americas in 2010.

• Access to healthcare and distribution limited in emerging markets.

Market Restraints

• By 2020, Chronic disease deaths in APAC will grow at 20%.

• 15% of the 37 million deaths worldwide is related to Pandemic and epidemic diseases, 1/3 of such was from APAC.

• Private expenditures is increasing in China and India, private spending accounted for 49.9% and 67.2% respectively in 2009.

Market Drivers

APAC Share

Global vs. APAC: The New FrontierIn 2011, APAC is estimated to be 28.5% of global market

28.5 % 34.6%

Global & APAC Healthcare Revenues US$ Bn, 2011-2015

• By 2015, APAC could represent 34.6% of global market

2011 2012 2013 2014 20150.0

200.0

400.0

600.0

800.0

1000.0

1200.0

1400.0

1600.0

1800.0

356.5 396.4 440.1 491.7 562.1

895.6928.8

978.11017.5

1060.7

APAC($ Billion)

Rest of the World($ Billion)

CAGR12.1%CAGR12.1%

CAGR4.3%

CAGR4.3%

2011 2012 2013 2014 20150.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

252.1 278.4 309.4 346.1 389.4

636.0 649.0677.6

707.4738.5

APAC($ Billion)

Rest of the World($ Billion)

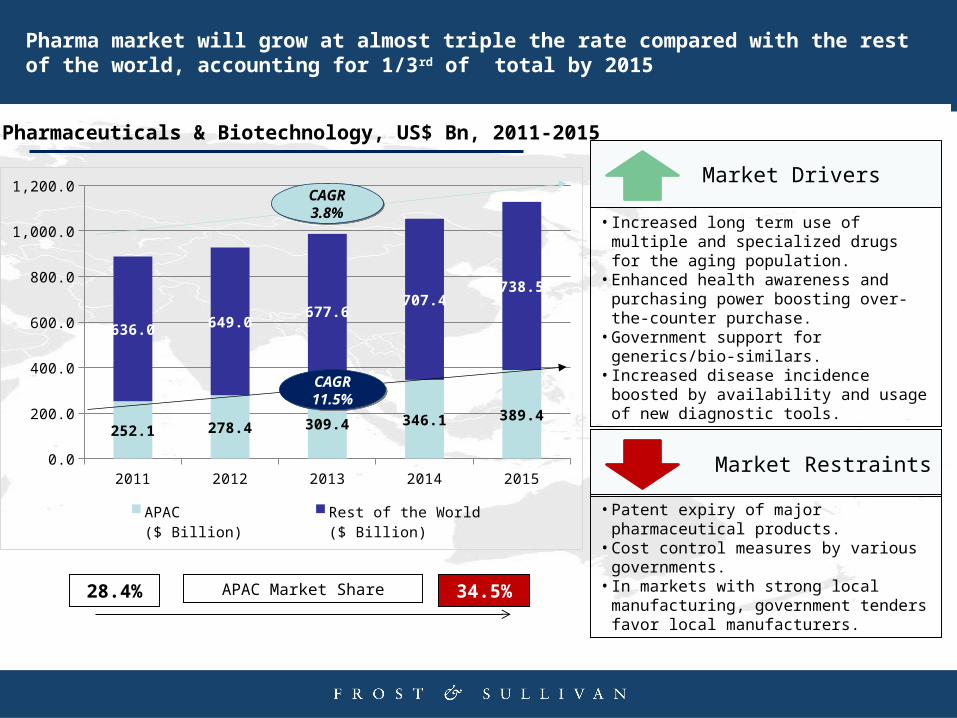

Pharmaceuticals & Biotechnology, US$ Bn, 2011-2015

Market Drivers

• Increased long term use of multiple and specialized drugs for the aging population.

• Enhanced health awareness and purchasing power boosting over-the-counter purchase.

• Government support for generics/bio-similars.

• Increased disease incidence boosted by availability and usage of new diagnostic tools.

Market Restraints

• Patent expiry of major pharmaceutical products.

• Cost control measures by various governments.

• In markets with strong local manufacturing, government tenders favor local manufacturers.

Pharma market will grow at almost triple the rate compared with the rest of the world, accounting for 1/3rd of total by 2015

CAGR11.5%CAGR11.5%

CAGR3.8%

CAGR3.8%

28.4% 34.5%APAC Market Share

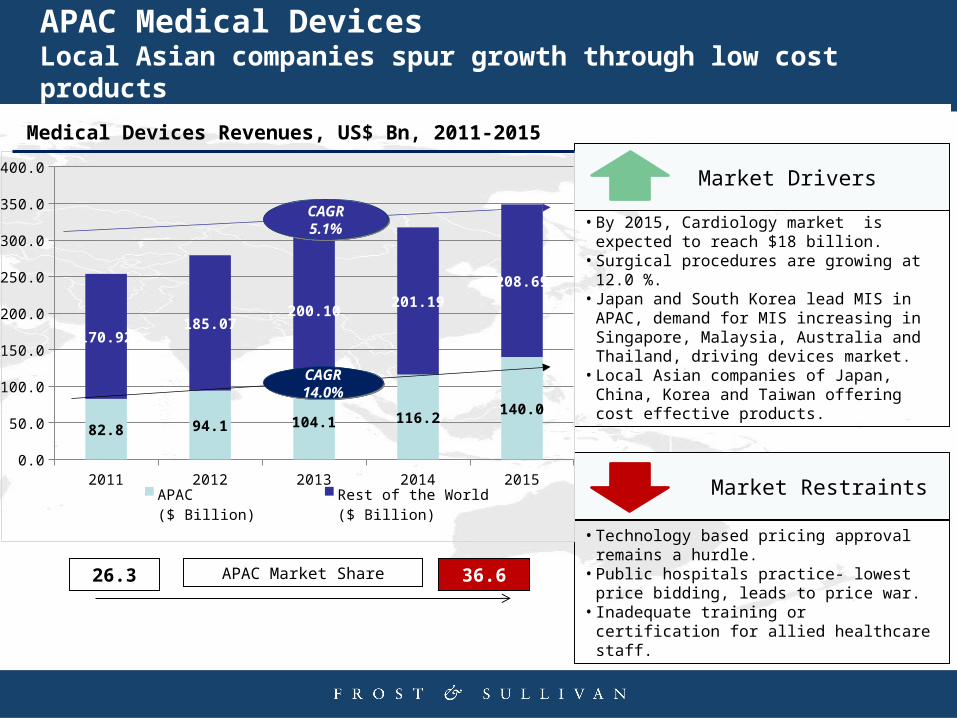

• Technology based pricing approval remains a hurdle.

• Public hospitals practice- lowest price bidding, leads to price war.

• Inadequate training or certification for allied healthcare staff.

Market Restraints

• By 2015, Cardiology market is expected to reach $18 billion.

• Surgical procedures are growing at 12.0 %.• Japan and South Korea lead MIS in APAC,

demand for MIS increasing in Singapore, Malaysia, Australia and Thailand, driving devices market.

• Local Asian companies of Japan, China, Korea and Taiwan offering cost effective products.

Market Drivers

2011 2012 2013 2014 20150.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

82.8 94.1 104.1 116.2140.0

170.92185.07

200.10201.19

208.69

APAC($ Billion)

Rest of the World($ Billion)

APAC Medical DevicesLocal Asian companies spur growth through low cost products

Medical Devices Revenues, US$ Bn, 2011-2015

CAGR14.0%CAGR14.0%

CAGR5.1%

CAGR5.1%

26.3 36.6APAC Market Share

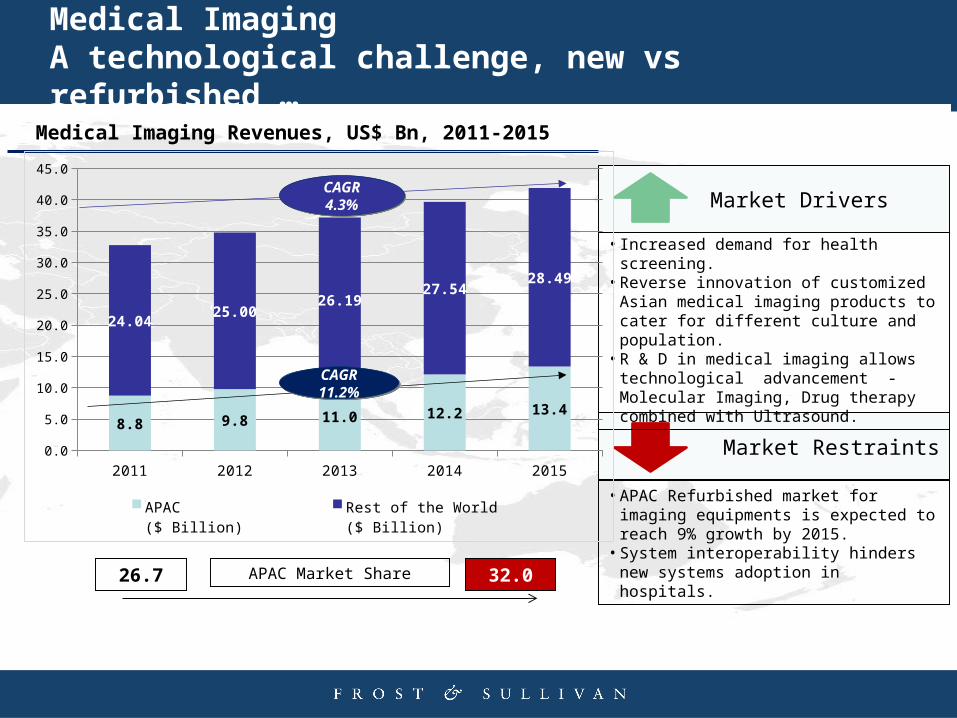

• APAC Refurbished market for imaging equipments is expected to reach 9% growth by 2015.

• System interoperability hinders new systems adoption in hospitals.

Market Restraints

• Increased demand for health screening.• Reverse innovation of customized Asian

medical imaging products to cater for different culture and population.

• R & D in medical imaging allows technological advancement - Molecular Imaging, Drug therapy combined with Ultrasound.

Market Drivers

Medical ImagingA technological challenge, new vs refurbished …

Medical Imaging Revenues, US$ Bn, 2011-2015

26.7 32.0APAC Market Share

2011 2012 2013 2014 20150.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

8.8 9.8 11.0 12.2 13.4

24.0425.00

26.1927.54

28.49

APAC($ Billion)

Rest of the World($ Billion)

CAGR11.2%CAGR11.2%

CAGR4.3%

CAGR4.3%

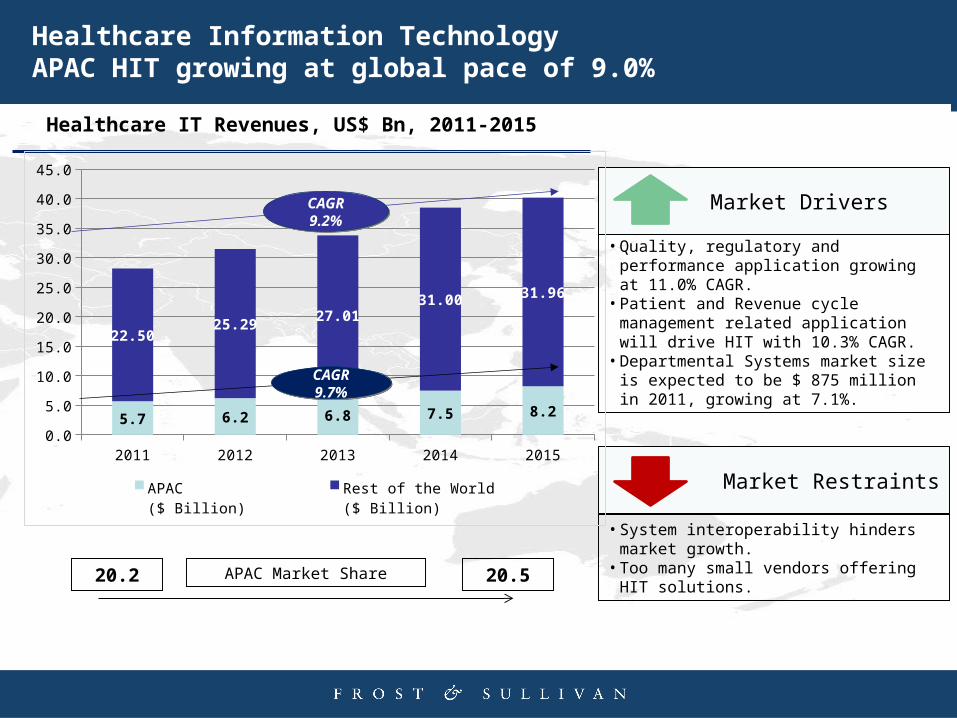

• System interoperability hinders market growth.

• Too many small vendors offering HIT solutions.

Market Restraints

• Quality, regulatory and performance application growing at 11.0% CAGR.

• Patient and Revenue cycle management related application will drive HIT with 10.3% CAGR.

• Departmental Systems market size is expected to be $ 875 million in 2011, growing at 7.1%.

Market Drivers

Healthcare Information TechnologyAPAC HIT growing at global pace of 9.0%

Healthcare IT Revenues, US$ Bn, 2011-2015

20.2 20.5APAC Market Share

2011 2012 2013 2014 20150.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

5.7 6.2 6.8 7.5 8.2

22.5025.29

27.0131.00 31.96

APAC($ Billion)

Rest of the World($ Billion)

CAGR9.7%

CAGR9.7%

CAGR9.2%

CAGR9.2%

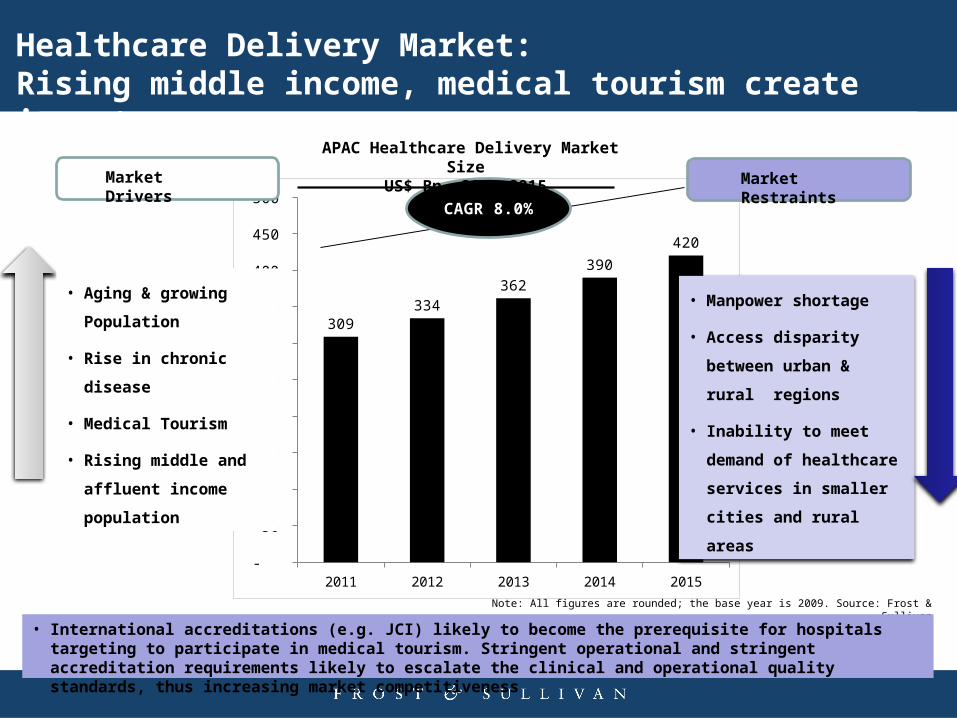

Healthcare Delivery Market:Rising middle income, medical tourism create impact

2011 2012 2013 2014 2015 -

50

100

150

200

250

300

350

400

450

500

309334

362

390

420

CAGR 8.0%

APAC Healthcare Delivery Market Size US$ Bn, 2011-2015

Note: All figures are rounded; the base year is 2009. Source: Frost & Sullivan

Market Drivers

• Aging & growing

Population

• Rise in chronic disease

• Medical Tourism

• Rising middle and

affluent income

population

• Manpower shortage

• Access disparity between

urban & rural regions

• Inability to meet demand of

healthcare services in smaller

cities and rural areas

Market Restraints

• International accreditations (e.g. JCI) likely to become the prerequisite for hospitals targeting to participate in medical tourism. Stringent operational and stringent accreditation requirements likely to escalate the clinical and operational quality standards, thus increasing market competitiveness

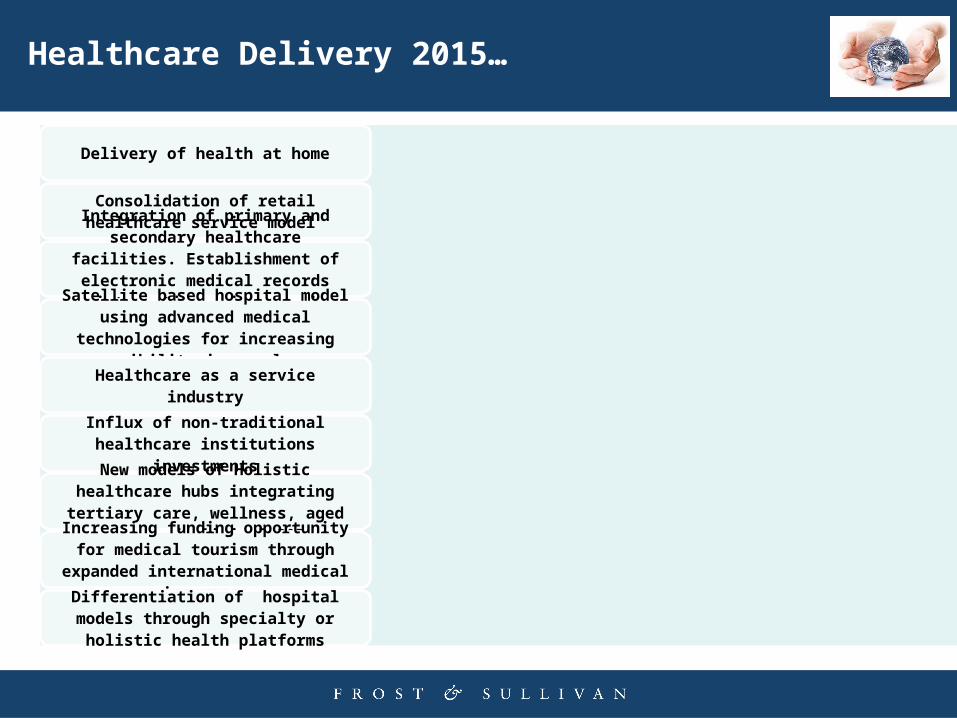

Healthcare Delivery 2015…

Delivery of health at home

Consolidation of retail healthcare service model

Integration of primary and secondary healthcare facilities. Establishment of electronic medical records integrating

primary and secondary healthcareSatellite based hospital model using advanced medical technologies for

increasing accessibility in rural areas

Healthcare as a service industry

Influx of non-traditional healthcare institutions investments

New models of Holistic healthcare hubs integrating tertiary care, wellness, aged

care and clinical R&D

Increasing funding opportunity for medical tourism through expanded

international medical insurance

Differentiation of hospital models through specialty or holistic health

platforms

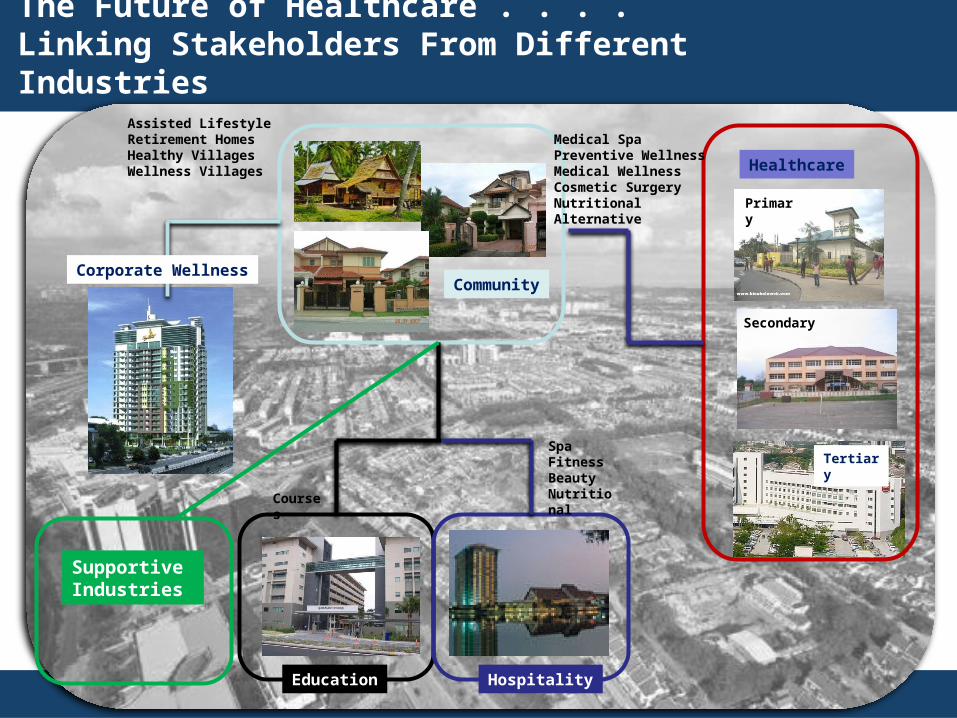

The Future of Healthcare . . . .Linking Stakeholders From Different Industries

Community

Education Hospitality

Healthcare

Corporate Wellness

Medical SpaPreventive WellnessMedical WellnessCosmetic SurgeryNutritionalAlternative

SpaFitnessBeautyNutritional

Assisted LifestyleRetirement HomesHealthy VillagesWellness Villages

Primary

Courses

Secondary

Tertiary

Supportive Industries

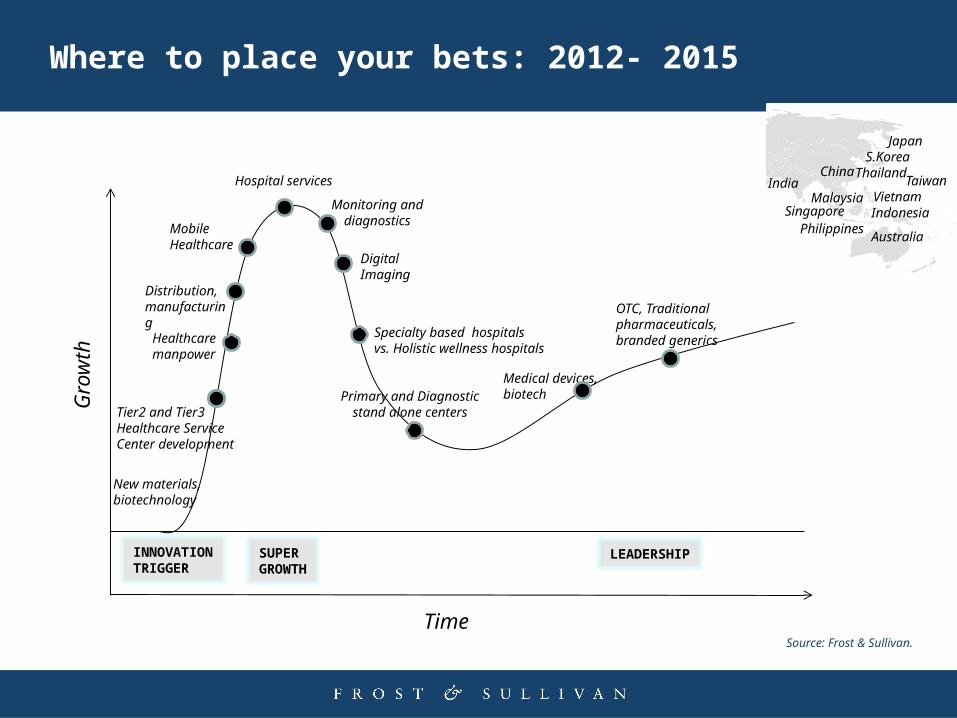

Where to place your bets: 2012- 2015

Time

Gro

wth

Healthcare manpower

Mobile Healthcare

Hospital services

OTC, Traditional pharmaceuticals, branded generics

INNOVATIONTRIGGER

SUPERGROWTH

LEADERSHIP

IndiaChina

S.Korea

SingaporeMalaysia Vietnam

Source: Frost & Sullivan.

Medical devices, biotech

Digital Imaging

Taiwan

Distribution, manufacturing

Australia

Japan

Monitoring and diagnostics

PhilippinesIndonesia

Thailand

Tier2 and Tier3Healthcare ServiceCenter development

New materials, biotechnology

Specialty based hospitalsvs. Holistic wellness hospitals

Primary and Diagnosticstand alone centers

Frost & Sullivan

An Active Contributor to Global HC Market Development

12

The Frost & Sullivan Story

Pioneered Emerging Market & Technology Research

• Global Footprint Begins

• Country Economic Research

• Market & Technical Research

• Best Practice Career Training

• MindXChange Events

Partnership Relationship with Clients

• Growth Partnership Services

• GIL Global Events

• GIL University

• Growth Team Membership™

• Growth Consulting

Visionary Innovation

• Mega Trends Research

• CEO 360 Visionary Perspective

• GIL Think Tanks

• GIL Global Community

• Communities of Practice

13

What Makes Us Unique

All services aligned on growth to help clients develop and implement innovative growth strategies

Continuous monitoring of industries and their convergence, giving clients first mover advantage in emerging opportunities

More than 40 global offices ensure that clients gain global perspective to mitigate risk and sustain long term growth

Proprietary Team Methodology integrates 7 critical research perspectives to optimize growth investments

Career research and case studies for the CEOs’ Growth Team to ensure growth strategy implementation at best practice levels

Close collaboration with clients in developing their research based visionary perspective to drive GIL

Focused on Growth

IndustryCoverage

Global Footprint

Career Best Practices

360 Degree Perspective

Visionary Innovation Partner

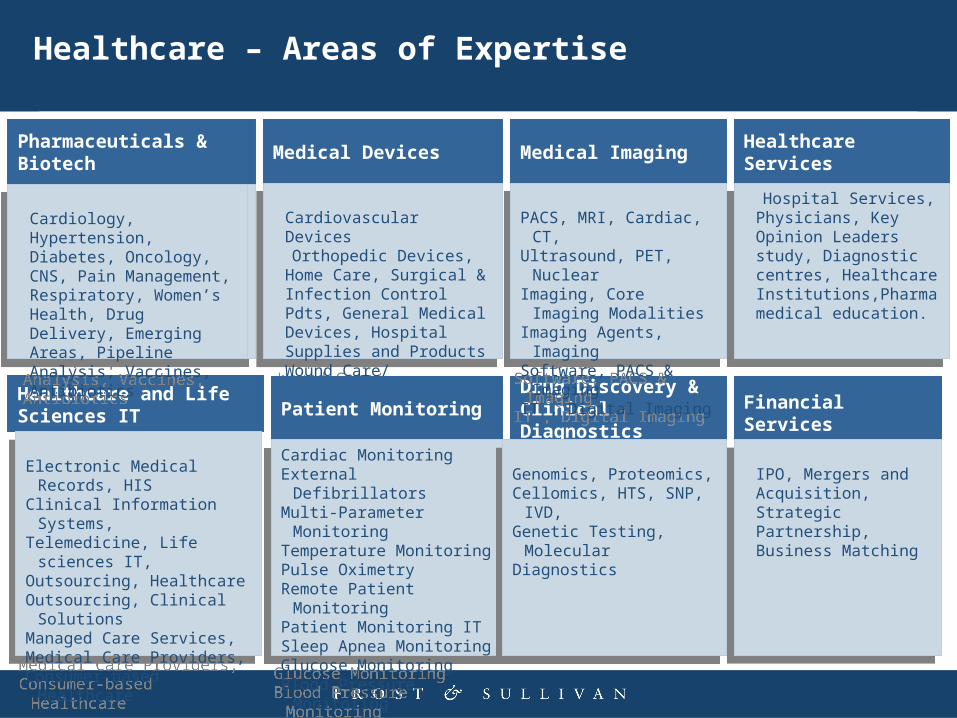

Healthcare – Areas of Expertise

Pharmaceuticals & Biotech

CNS, Oncology, Diabetes, Cardiology, Drug Delivery, Emerging Areas, Pipeline analysis, Biotech Oncology, Drug Delivery Biotechnology, Contract Manufacturing, Contract Research, Ophthalmic, Chronic Diseases

CNS, Oncology, Diabetes, Cardiology, Drug Delivery, Emerging Areas, Pipeline analysis, Biotech Oncology, Drug Delivery Biotechnology, Contract Manufacturing, Contract Research, Ophthalmic, Chronic Diseases

Medical Devices

Cardiovascular Devices Orthopedic Devices, Home Care,

Surgical & Infection Control Pdts, General Medical Devices, Hospital Supplies and ProductsWound Care/ Management Products

Cardiovascular Devices Orthopedic Devices, Home Care,

Surgical & Infection Control Pdts, General Medical Devices, Hospital Supplies and ProductsWound Care/ Management Products

Healthcare and Life Sciences IT

Electronic Medical Records, HISClinical Information Systems,Telemedicine, Life sciences IT,Outsourcing, HealthcareOutsourcing, Clinical SolutionsManaged Care Services,Medical Care Providers,Consumer-based Healthcare

Electronic Medical Records, HISClinical Information Systems,Telemedicine, Life sciences IT,Outsourcing, HealthcareOutsourcing, Clinical SolutionsManaged Care Services,Medical Care Providers,Consumer-based Healthcare

Patient Monitoring

Cardiac MonitoringExternal DefibrillatorsMulti-Parameter MonitoringTemperature MonitoringPulse OximetryRemote Patient MonitoringPatient Monitoring ITSleep Apnea MonitoringGlucose MonitoringBlood Pressure Monitoring

Cardiac MonitoringExternal DefibrillatorsMulti-Parameter MonitoringTemperature MonitoringPulse OximetryRemote Patient MonitoringPatient Monitoring ITSleep Apnea MonitoringGlucose MonitoringBlood Pressure Monitoring

Drug Discovery & Clinical Diagnostics

Genomics, Proteomics,Cellomics, HTS, SNP, IVD,Genetic Testing, MolecularDiagnostics

Genomics, Proteomics,Cellomics, HTS, SNP, IVD,Genetic Testing, MolecularDiagnostics

Medical Imaging

PACS, MRI, Cardiac, CT,Ultrasound, PET, NuclearImaging, Core Imaging

ModalitiesImaging Agents, ImagingSoftware, PACS & ImagingIT , Digital Imaging

PACS, MRI, Cardiac, CT,Ultrasound, PET, NuclearImaging, Core Imaging

ModalitiesImaging Agents, ImagingSoftware, PACS & ImagingIT , Digital Imaging

Pharmaceuticals & Biotech

Cardiology, Hypertension, Diabetes, Oncology, CNS, Pain Management, Respiratory, Women’s Health, Drug Delivery, Emerging Areas, Pipeline Analysis, Vaccines, Antibiotics

Cardiology, Hypertension, Diabetes, Oncology, CNS, Pain Management, Respiratory, Women’s Health, Drug Delivery, Emerging Areas, Pipeline Analysis, Vaccines, Antibiotics

Healthcare Services

Hospital Services, Physicians, Key Opinion Leaders study, Diagnostic centres, Healthcare Institutions,Pharma medical education.

Hospital Services, Physicians, Key Opinion Leaders study, Diagnostic centres, Healthcare Institutions,Pharma medical education.

Financial Services

IPO, Mergers and Acquisition, Strategic Partnership, Business Matching

IPO, Mergers and Acquisition, Strategic Partnership, Business Matching

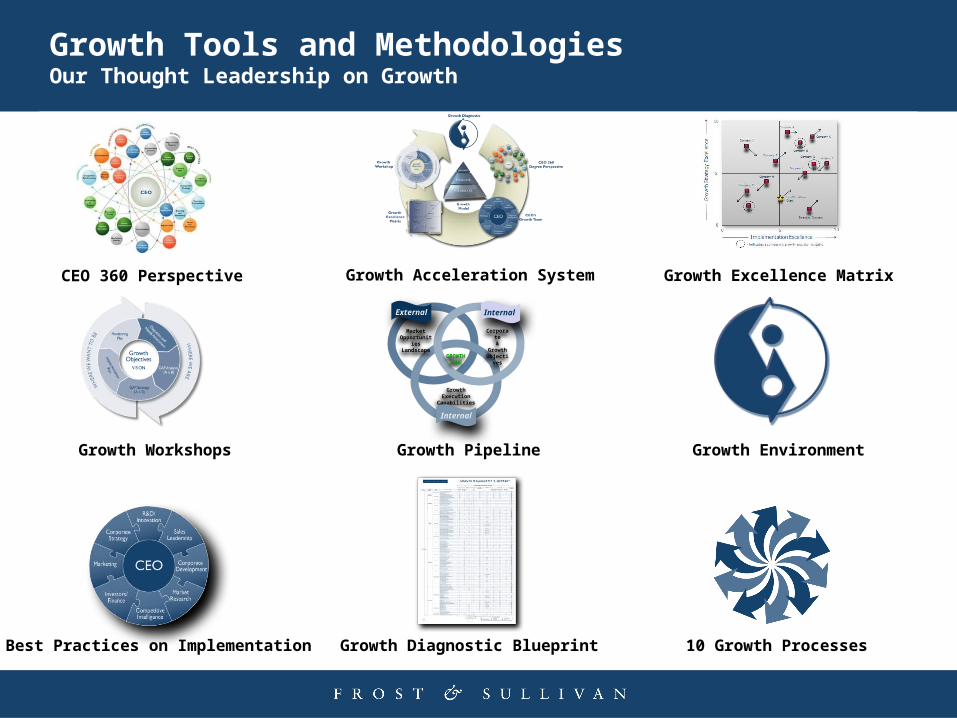

Growth Tools and MethodologiesOur Thought Leadership on Growth

CEO 360 Perspective

MarketOpportunities

Landscape

Corporate& GrowthObjectives

Growth ExecutionCapabilities

External Internal

Internal

GROWTHZONE

Growth Acceleration System Growth Excellence Matrix

Growth Workshops Growth Pipeline Growth Environment

10 Growth ProcessesBest Practices on Implementation Growth Diagnostic Blueprint

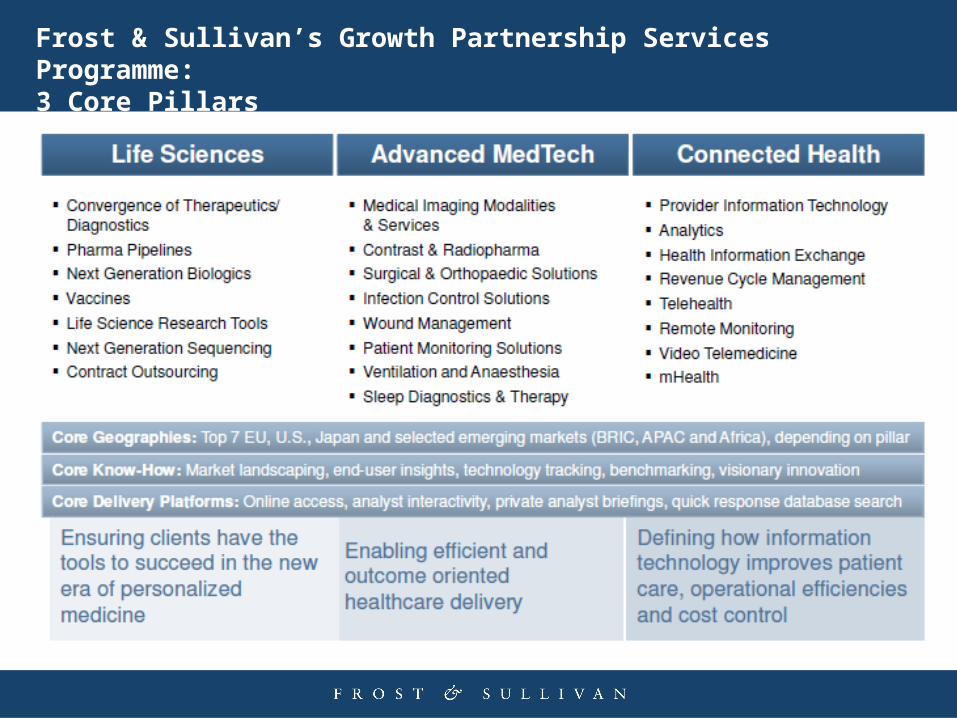

Frost & Sullivan’s Growth Partnership Services Programme:3 Core Pillars

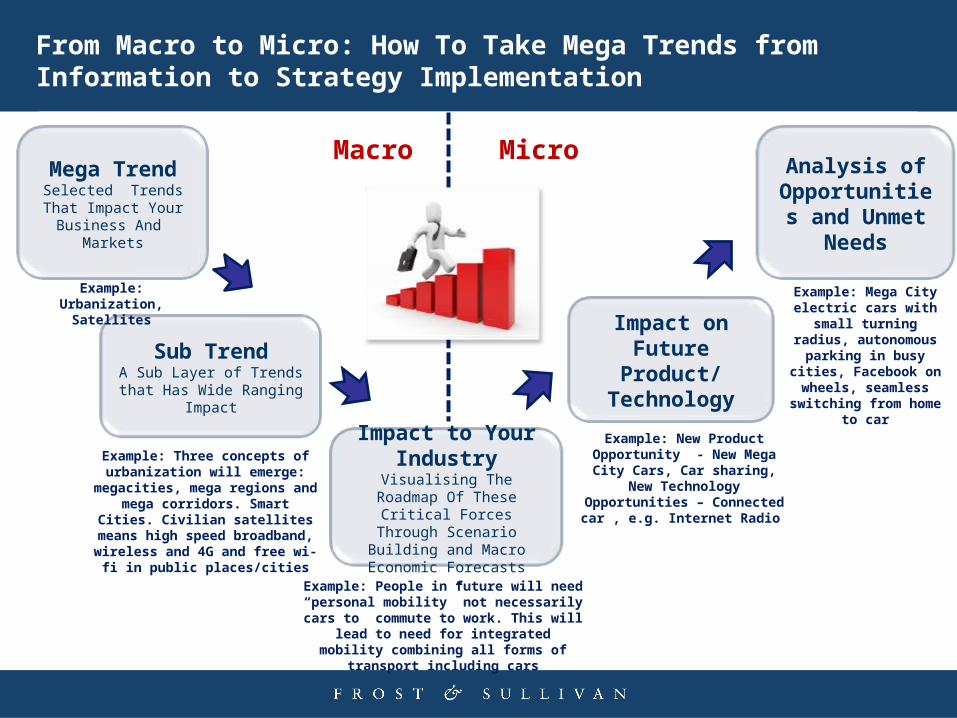

From Macro to Micro: How To Take Mega Trends from Information to Strategy Implementation

Sub TrendA Sub Layer of Trends that Has Wide Ranging Impact

Mega TrendSelected Trends That Impact Your Business

And Markets

Analysis of Opportunities

and Unmet Needs

Impact on Future Product/

Technology

Impact to Your Industry

Visualising The Roadmap Of These Critical Forces Through Scenario Building and Macro

Economic Forecasts

Example: Urbanization, Satellites

Example: Three concepts of urbanization will emerge:

megacities, mega regions and mega corridors. Smart Cities. Civilian satellites means high

speed broadband, wireless and 4G and free wi-fi in public places/cities

Example: New Product Opportunity - New Mega City

Cars, Car sharing,New Technology Opportunities –

Connected car , e.g. Internet Radio

Example: Mega City electric cars with small

turning radius, autonomous parking in

busy cities, Facebook on wheels, seamless

switching from home to car

Example: People in future will need “personal mobility” not necessarily cars to commute to work. This will lead to need for integrated mobility combining all forms of

transport including cars

Macro Micro

http://twitter.com/frost_sullivan

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

For Additional Information

Donna JeremiahCorporate CommunicationsAsia Pacific+61 (0) 8247 8927 [email protected]

Carrie LowCorporate CommunicationsAsia Pacific+603 6204 [email protected]

Sasikarn Watthanachan Corporate CommunicationsThailand+66 2 637 7414 [email protected]

Jessie LohCorporate CommunicationsAsia Pacific+65 6890 [email protected]