ASGARD SUPER AND PENSION ACCOUNT Annual Report · ASGARD SUPER AND PENSION ACCOUNT. ... This Annual...

28

YEAR ENDING: 30 JUNE 2012 ASGARD SUPER AND PENSION Managed Profiles and Separately Managed Accounts Funds – Super/Pension Elements – Super/Pension eWRAP – Super/Pension Infinity eWRAP Super/Pension ASGARD BUSINESS SUPER Asgard Employee Super Account Asgard Corporate Superannuation Service APPROVED DEPOSIT FUND Rollover Service Annual Report ASGARD SUPER AND PENSION ACCOUNT

Transcript of ASGARD SUPER AND PENSION ACCOUNT Annual Report · ASGARD SUPER AND PENSION ACCOUNT. ... This Annual...

YEAR ENDING: 30 JUNE 2012

ASGARD SUPER AND PENSIONManaged Profiles and Separately Managed Accounts Funds – Super/Pension

Elements – Super/Pension

eWRAP – Super/Pension

Infinity eWRAP Super/Pension

ASGARD BUSINESS SUPERAsgard Employee Super Account

Asgard Corporate Superannuation Service

APPROVED DEPOSIT FUNDRollover Service

Annual Report

ASGARD SUPER AND PENSION ACCOUNT

ii | Annual Report

IMPORTANT INFORMATIONThis Annual Report is issued by Asgard Capital Management Limited (Asgard, we, us, our) ABN 92 009 279 592 AFSL 240695, as the Trustee of:• Asgard Independence Plan – Division 1 (which comprises the Asgard Corporate Superannuation Service Fund)

ABN 69 099 508 025;• Asgard Independence Plan – Division 2 (which includes Managed Profiles and Separately Managed Accounts – Funds

Super/Pension, Elements – Super/Pension, eWRAP – Super/Pension, Infinity eWRAP Super/Pension and Employee Super Account) Fund ABN 90 194 410 365; and

• Asgard Independence Plan – Division 4 (which comprises the Asgard Rollover Service) Fund ABN 47 948 096 909.The Trustee has not received any notices or penalties for non-compliance during the reporting period and has formally resolved that the accounts will at all times be administered in strict compliance with all applicable acts and regulations.The investment information or general advice provided in this publication does not take into account your personal objectives, financial situation or needs and because of that you should consider the appropriateness of the information or advice having regard to these factors. Before deciding whether to open or to continue to hold an Asgard product or service, you should obtain and consider the relevant Product Disclosure Statement (PDS) for that product, available from your financial adviser or our Contact Centre.Asgard is a subsidiary the Westpac Banking Corporation (Westpac) ABN 33 007 457 141. Unless otherwise disclosed in the offer document for the relevant financial product, a financial product or service issued or offered by Asgard or through an Asgard product or service is not a deposit with, investment in, or other liability of, Westpac, nor any other company within the Westpac Group. They are subject to investment risk, including possible delays in repayment and loss of income and principal invested. Neither Westpac nor any other company within the Westpac Group stands behind or otherwise guarantees the capital value or investment performance of any such financial product or service issued or offered by or through Asgard.

CONTACT CENTRE1800 998 185 CORRESPONDENCEPO Box 7490Cloisters Square WA 6850

e: [email protected]: www.asgard.com.au

www.investoronline.info

ISSUED BYAsgard Capital Management LtdABN 92 009 279 592AFSL 240695

Annual Report What's inside | 1

hat’s inside

Asgard Super and Pension Account 2 The year in review from Kelly Power

3 Recent legislative change

7 Upcoming legislative change

9 Asgard Super and Pension enhancements

11 Asgard Super and Pension products

14 Investment information

16 Other important information

22 Financial reports

2 | Annual Report The year in review

he year in reviewDear Investor,

In 2012 we continued to invest in our platform and looked at how we could further improve your day-to-day experience with us.

Investor Online (our Internet-based account information service you can access via www.investoronline.info) received a facelift with a new messaging system highlighting actions or outstanding information for your attention, the ability to instantly reset your PIN online and more. The new option to inspecie transfer managed investments and shares from another complying superannuation fund via rollover into new eWRAP/Infinity eWRAP Super/Pensions or existing eWRAP/Infinity eWRAP Super means no need to sell down your assets to move them, no time out of the market and greater opportunity to combine your accounts. We also expanded the Asgard Super/Pension share menus to include a number of hybrid and income securities which you can discuss with your financial adviser in developing your investment strategy.

You’ll find more information about recent and upcoming legislative change, our products and enhancements in this 2012 Annual Report. As always, we encourage you to talk to your financial adviser who can give you any guidance you may need.

If you have any questions about this Annual Report or your account, please talk to your financial adviser or give us a call on 1800 998 185.

I thank you for your continued support and wish you all the very best for a happy festive season and a healthy year ahead.

Yours sincerely

Kelly PowerHead of Platforms

Annual Report Recent legislative change | 3

ecent legislative change

1. 2012/13 superannuation thresholds The superannuation contributions caps and various other superannuation thresholds that apply for the 2012/13 financial year are as follows.

Low rate cap: $175,000Concessional contributions cap (all ages): $25,000Non-concessional contributions cap: $150,0001

Capital Gains Tax (CGT) cap (lifetime limit): $1,255,000 Proposed Government co-contributions2:

• Maximum co-contribution3

• Lower threshold• Upper threshold (cut off)

$500$31,920$46,920

1. If you were under age 65 on 1 July 2012 you may be able to make up to $450,000 of non-concessional contributions over three financial years.

2. The Government propose to reduce the matching rate from $1 to 50 cents and the maximum Government co-contribution available to $500 from 1 July 2012. This proposal is not yet law.

3. The maximum co-contribution payable is phased out by 3.333 cents for every dollar of total income over the lower threshold, until it reaches zero at the upper threshold.

2. Minimum pension payments The Government has extended relief from the minimum pension payment requirements to the 2012/13 financial year.

Allocated PensionThe minimum pension payment specified by Government regulations is reduced by 25% for the year ended 30 June 2013. This means if your minimum payment requirement for the 2012/13 financial year is $10,000, you can choose to take a payment of only $7,500 for the financial year.

Term Allocated PensionFor the 2012/13 financial year only you may elect to reduce your annual income payment specified by Government regulations by up to 25%. This means if your annual payment amount for the 2012/13 financial year is $10,000 +/- 10%, you can choose to reduce your payment to $6,750 or increase your payment to $11,000.

4 | Annual Report Recent legislative change

3. Refund of excess concessional contributions for breaches less than $10,000

If you breach your concessional contributions cap by $10,000 or less in 2011/12 or a later financial year you may be able to choose to have the excess contributions refunded from your superannuation fund and taxed at your marginal tax rate rather than incurring excess contributions tax.

If you breach your concessional contributions cap you may be eligible for a refund offer if:

• it’s the first time you’ve breached your concessional contributions cap in respect of 2011/12 or a subsequent financial year

• your excess concessional contributions are $10,000 or less

• you’ve lodged a tax return for the financial year in which the excess concessional contributions were made within 12 months of the end of that financial year.

Any excess concessional contributions for a financial year prior to 2011/12 will not affect your eligibility for a refund offer.

If the first time you breach your concessional contributions cap in relation to 2011/12 or a later financial year your excess contributions are over $10,000, you will not be eligible for a refund offer for that breach or any future breaches of the cap (even if a future breach is less than $10,000).

The ATO will issue refund offers to eligible individuals. If you receive a refund offer from the ATO you will have 28 days to accept the refund offer. If you decide not to accept the refund offer you will be assessed for excess contributions tax and you will not be entitled to the refund offer in the future.

For further details about this one-off refund offer go to www.ato.gov.au.

4. Low Income Super ContributionFrom 2012/13 low income earners may receive a government super payment of up to $500 per financial year to help save for their retirement. This payment is called the low income super contribution (LISC).

The amount of LISC payable is calculated as 15% of your total concessional contributions for the financial year, up to a maximum of $500. Where the amount of LISC calculated is less than $20, no payment will be made.

You will be eligible for a LISC from 2012/13 if:

• concessional contributions have been made to a complying super fund for you during the financial year

• your adjusted taxable income1 for the financial year is not more than $37,000

• you are not a holder of a temporary resident visa (New Zealand citizens are eligible for the payment)

Annual Report Recent legislative change | 5

• 10% or more of your total income2 for the financial year is sourced from business or employment, and

• the LISC payable is $20 or more.

If you’re eligible for the LISC the ATO will automatically make the payment into your super account.

If you make personal contributions to super you may also be eligible to receive the Government co-contribution.

For more information on LISC or Government co-contributions go to www.ato.gov.au.1. Adjusted taxable income is the sum of taxable income, adjusted fringe

benefits, target foreign income, total net investment loss, tax-free pension or benefits and reportable superannuation contributions less deductible child maintenance expenditure.

2. Total income is the sum of assessable income, reportable fringe benefits and reportable employer superannuation contributions.

5. Indexation of concessional contributions cap paused until 30 June 2014

Each year the concessional contributions cap is usually indexed to Average Weekly Ordinary Time Earnings, rounded down to the nearest $5,000. The Government has paused this indexation for the next two years until 30 June 2014.

This means the concessional contributions cap will remain at $25,000 for 2012/13 and 2013/14.

6. Concessional contributions cap for those aged 50 or over

The transitional $50,000 concessional contributions cap for individuals who are aged 50 or over ended on 30 June 2012.

For the 2012/13 and 2013/14 financial years, the general $25,000 concessional contributions cap will apply to all individuals.

From 1 July 2014, the Government has proposed allowing individuals aged 50 and over with superannuation balances below $500,000 to make up to $25,000 more in concessional contributions than allowed under the general concessional contributions cap. This proposal is not yet law.

Contributions counted against your concessional contributions cap include:

• employer contributions including Superannuation Guarantee, Award, employer voluntary, and salary sacrifice contributions

• personal contributions for which you claim a personal tax deduction.

6 | Annual Report Recent legislative change

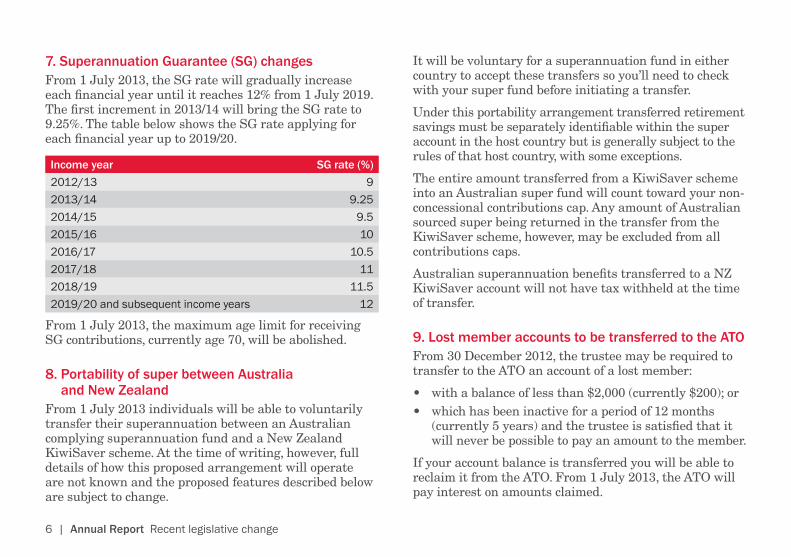

7. Superannuation Guarantee (SG) changes From 1 July 2013, the SG rate will gradually increase each financial year until it reaches 12% from 1 July 2019. The first increment in 2013/14 will bring the SG rate to 9.25%. The table below shows the SG rate applying for each financial year up to 2019/20.

Income year SG rate (%)2012/13 92013/14 9.252014/15 9.52015/16 102016/17 10.52017/18 112018/19 11.52019/20 and subsequent income years 12

From 1 July 2013, the maximum age limit for receiving SG contributions, currently age 70, will be abolished.

8. Portability of super between Australia and New Zealand

From 1 July 2013 individuals will be able to voluntarily transfer their superannuation between an Australian complying superannuation fund and a New Zealand KiwiSaver scheme. At the time of writing, however, full details of how this proposed arrangement will operate are not known and the proposed features described below are subject to change.

It will be voluntary for a superannuation fund in either country to accept these transfers so you’ll need to check with your super fund before initiating a transfer.

Under this portability arrangement transferred retirement savings must be separately identifiable within the super account in the host country but is generally subject to the rules of that host country, with some exceptions.

The entire amount transferred from a KiwiSaver scheme into an Australian super fund will count toward your non-concessional contributions cap. Any amount of Australian sourced super being returned in the transfer from the KiwiSaver scheme, however, may be excluded from all contributions caps.

Australian superannuation benefits transferred to a NZ KiwiSaver account will not have tax withheld at the time of transfer.

9. Lost member accounts to be transferred to the ATOFrom 30 December 2012, the trustee may be required to transfer to the ATO an account of a lost member:

• with a balance of less than $2,000 (currently $200); or • which has been inactive for a period of 12 months

(currently 5 years) and the trustee is satisfied that it will never be possible to pay an amount to the member.

If your account balance is transferred you will be able to reclaim it from the ATO. From 1 July 2013, the ATO will pay interest on amounts claimed.

Annual Report Upcoming legislative change | 7

The following items are Government announcements only and are not yet law. Legislation would need to be passed by parliament to make these proposals law.

1. Government co-contributions The Government intend to reduce the maximum Government co-contribution available to $500 from 1 July 2012.

If this proposal becomes law, if your total income1 is more than $46,920, you won’t be entitled to a Government co-contribution. Further, to attract the maximum co-contribution of $500, you’ll still be required to make a personal after-tax contribution of $1,000 as the matching rate will reduce to 50% (currently 100%).1. Total income is the sum of assessable income, reportable fringe benefits and

reportable employer contributions less business deductions.

2. Consolidating multiple superannuation accounts within the same fund

The Government has proposed that from 1 January 2013, on an annual basis, superannuation funds will be required to identify whether a member of the fund holds multiple accounts. If multiple accounts are identified, the super fund will be required to consolidate these accounts if this is in the member’s best interest. The consolidation process must be completed at least once by 30 June 2013.

When determining whether it is in a member’s best interest to merge their super accounts, super fund trustees must consider the possible savings in fees, charges and insurance premiums which will result if they merge accounts as well as any other relevant factors.

This requirement will only apply to accumulation accounts, and not to pension accounts.

pcoming legislative change

8 | Annual Report Upcoming legislative change

3. Additional 15% tax on super contributions for high income earners

The Government propose to introduce an additional 15% tax on concessional contributions made to superannuation for those earning income1 of more than $300,000 per year.

For the purpose of this additional tax, concessional contributions include Superannuation Guarantee contributions, voluntary employer contributions, salary sacrifice contributions and personal deductible contributions. For defined benefit members, concessional contributions also include notional employer contributions to (funded and unfunded) defined benefit schemes.

If your income exceeds $300,000 only due to your concessional contributions, the additional 15% tax will only apply to that portion of your contributions in excess of $300,000. For example, if your income excluding concessional contributions was $285,000, and your concessional contributions were $20,000 taking your total income to $305,000, the additional tax would only apply on $5,000 of your concessional contributions.

The additional tax will not apply to excess concessional contributions (ie the value of any concessional contributions over your concessional contributions cap).1. Income is the sum of taxable income, concessional contributions, adjusted

fringe benefits, total net investment loss, target foreign income and tax-free Government pension and benefits less child support payments.

Annual Report Asgard Super and Pension enhancements | 9

sgard Super and Pension enhancements

Transferring managed investments and shares into your Asgard eWRAP/Infinity eWRAP Super/Pension AccountEffective 20 August 2012, you can in-specie transfer managed investments and/or shares (investments) into your new Asgard eWRAP/Infinity eWRAP Super/Pension account or existing Asgard eWRAP/Infinity eWRAP Super account, provided those investments:

• appear on our list of available investment options, and• are transferred from another complying

superannuation fund or Self Managed Super Fund (SMSF) in a form of a rollover.

In-specie transfer involves the direct transfer of investments without selling the underlying assets which is done in place of a cash rollover. The benefits of in-specie transfers include:

• No time out of the market, no buy and sell costs – when you transfer assets via in-specie you remove the buy and sell costs associated with transacting and eliminate time out of the market, which means you’re not exposed to market movement and you can maximise on-market opportunities.

• One place to manage all your investments – in-specie transfers allow you to combine your accounts onto the one platform, so you have complete visibility of your accounts in the one place.

For more information, please speak to your financial adviser or call us on 1800 998 185.

10 | Annual Report Asgard Super and Pension enhancements

Asgard Employee Super Account developments

Personal membershipFrom 20 August 2012, Asgard Employee Super Account (AESA) members who leave their employer will become Personal members instead of being transferred to the Asgard Super Account:

• AESA members and any linked spouse and family members will automatically become Personal members once we’re notified the employee member has left their employer.

• Members will retain their adviser, client number, Investor Online PIN and investment profile, and their insurance cover will become fixed on transfer.

• Personal members will benefit from accessing group life insurance terms and conditions and premium rates.

• Most Personal members will no longer have access to employer-related discounts on fees and insurance premiums.

InsuranceWe introduced a number of enhancements to our AESA insurance offering such as:

• A discount of 5% off premium rates for Life Protection and Total and Permanent Disablement (TPD) premium rates from 20 August 2012. This discount excludes members with an employer who has negotiated different premium rates.

• A new definition for Total and Permanent Disablement to cover ‘cognitive loss’.

• Rehabilitation expenses can now be covered under Salary Continuance Insurance (SCI).

• Improved eligibility terms for the ‘partial disability’ definition under SCI.

• Introduced eligibility for automatic cover for members who join after 120 days.

• Extended eligibility for cover during unpaid leave.

Investor Online transformationWe’ve changed the look and feel of the Investor Online homepage to make it more user-friendly. Articles are now organised into separate categories so it’s easier for you to select the ones you’re interested in reading, a ‘New messages’ box at the top of the page brings any account alerts to your attention and a new advertising carousel highlights information on our products and services.

You can view these changes by logging into Investor Online any time at www.investoronline.info.

And if you’ve lost or forgotten your Investor Online PIN you can now click the ‘Forgotten PIN?’ link on the Investor Online login screen to re-set it yourself, or call our Contact Centre 1800 998 185.

Annual Report Asgard Super and Pension products | 11

Asgard Managed Profiles and Separately Managed Accounts – FundsManaged Profiles offer you and your financial adviser the ability to construct an investment profile from more than 400 managed investments and to purchase shares from a broad range of securities listed on the Australian Securities Exchange (ASX). To see the full range of investment options available to you, contact your financial adviser.

Separately Managed Accounts – Funds (SMA – Funds) offers you a selection of five pre-set portfolios of managed investments. The five portfolios are tailored to meet specific risk tolerance levels, depending on whether you’re a cautious investor or whether you’re willing to take greater risks for a higher return on your money. Your investments in the SMA – Funds are directly invested into the equivalent Advance Diversified Multi-blend fund.

A range of well known investment managers have been selected. The ‘sector specialist’ approach blends the best combinations of funds within each market sector where there’s benefit in doing so, for example, Australian and international shares. Where the benefit is minimal, one indexed/active fund is selected to represent each sector, for example, fixed interest and cash.

The investment objectives and strategies of the SMA – Funds portfolios are summarised on the next page.

sgard Super and Pension products

12 | Annual Report Asgard Super and Pension products

SMA – Funds objectives and strategy

Asgard SMA – Funds portfolio Investment objectives Strategy

Defensive To provide secure income with a low risk of capital loss over the short to medium term with some capital growth over the long term.

To gain exposure to a diverse mix of assets with a majority in defensive assets of cash and fixed income and a modest investment in growth assets such as shares.

Moderate To provide relatively stable total returns over the short to medium term, with some capital growth over the long term through a diversified mix of growth and defensive assets.

To gain exposure to a diverse mix of assets with an emphasis on secure income producing assets.

Balanced To provide moderate to high total returns (before fees and taxes) over the medium term from a combination of capital growth and income through a diversified mix of growth and defensive assets.

To gain exposure to a diverse mix of assets with both income-producing assets of cash and fixed interest, and growth assets including shares and property.

Growth To provide moderate to high total returns (before fees and taxes) over the medium to long term largely through capital growth by investing in a mix of growth and defensive assets.

To gain exposure to a diverse mix of assets with an emphasis on growth oriented assets of Australian and international shares, and an investment in the defensive assets of cash and fixed interest providing some income and stability of returns.

High Growth To provide superior total returns (before fees and taxes) over the long term through capital growth by investing in growth assets.

To gain exposure primarily to Australian and international shares with some exposure to property.

Annual Report Asgard Super and Pension products | 13

Asgard ElementsAsgard Elements offers you the opportunity to invest with some of the most recognised investment brands in the industry at a low cost. The Elements investment menu provides investors with a smaller, concentrated menu of diversified and sector specific multi-blend options (known as multi-manager funds) and a range of discretionary investments (known as single-manager funds) that have been selected against rigorous criteria to ensure they’re of the highest quality.

Asgard eWRAPAsgard eWRAP enables you to wrap all your superannuation investments into the one simple superannuation or pension account. You get access to our extensive range of wholesale managed investments, term deposits, a wide range of shares listed on the ASX and a competitive cash account with no account-keeping or transaction fees.

Asgard Infinity eWRAPAsgard Infinity eWRAP is an online wrap account that allows you to wrap all of your superannuation investments (managed investments, shares, term deposits and cash) and insurance into one simple superannuation or pension account. You have the flexibility to add (or remove) optional features to your

Core account as your needs change, and you only pay for the features you need. Infinity eWRAP Super/Pension consolidates all transaction reporting to provide you with continuous, online access to account information via Investor Online 24 hours a day, 7 days a week.

Business Super

Asgard Employee Super AccountThe Asgard Employee Super Account provides comprehensive superannuation and insurance solutions as your employer’s chosen plan. Employees, their spouses and families can access a broad investment menu, including the Asgard SMA – Funds, over 400 managed investments and a range of securities listed on the ASX.

Asgard Corporate Superannuation ServiceThe Asgard Corporate Superannuation Service is closed to new members and employer groups; however, existing members can still have their contributions paid into their accounts.

Asgard Rollover ServiceThe Asgard Rollover Service is closed to new members. However, existing members can still have their contributions paid into their accounts.

14 | Annual Report Investment information

Investment choiceThrough Asgard, you have access to an extensive range of investment options, such as managed investments, shares and a competitive cash offering. For the list of investment choice available to you, refer to the latest PDS which is accessible through Investor Online.

If you would like to update your investments or obtain a free copy of the latest PDS, speak to your financial adviser or call our Contact Centre on 1800 998 185.

Investment strategy and objectivesThe Trustee selects and monitors investments for the accounts by taking into consideration the quality of the investment managers’ business, stability of their investment team, past performance and their management process before selecting investment options. For a full list of investment managers, go to the ‘Important information — your Asgard Super and Pension Account Annual Report’ link on the Investor Online homepage.

You may direct the Trustee to invest in one or more investment options on your behalf. You should ask your financial adviser if you have any questions about the relevant managed investments in terms of whether they suit your financial objectives, situation and needs before deciding to invest.

For more information on a specific investment option including its investment strategy and objectives, refer to the relevant disclosure document for that investment option which is accessible through Investor Online. You may also obtain a copy of these disclosure documents free of charge from your financial adviser or us.

Asset allocationsThe Trustee provides you with detailed information on the asset allocations of the investments in the accounts. You can access the Investment Monthly asset allocation tables as at 30 June 2012 via Investor Online at www.investoronline.info. For a full list of investments with a holding greater than 5% of the accounts’ assets

nvestment information

Annual Report Investment information | 15

at 30 June 2012, go to the ‘Important information — your Asgard Super and Pension Account Annual Report’ link on the Investor Online homepage.

Earnings paid to your accountEarnings, in the form of capital growth, income distributions or dividends, received from your investments are credited to your account. Your investment earnings will depend on the performance of the investments you choose and the amount of money invested in each.

All gains and losses are reflected through changes in the value of your investments. With the exception of investments in the Asgard Corporate Superannuation Service, we credit all dividend or distribution payments from your investments to your cash balance when they’re received.

Earnings on investments through the Asgard Corporate Superannuation Service are credited to each employer’s account, from which a distribution is made to each employee account at the end of each month after fees have been deducted. Each employee account receives a share of earnings at a rate calculated by dividing the sum of the amounts held in the employee’s account for each day of the month, by the sum of the amounts held in the employer’s account for each day of the month.

If an employee’s membership in the Asgard Corporate Superannuation Service is terminated for any reason, in accordance with superannuation law any non-vested benefits are generally redistributed to the remaining employees.

Use of derivative financial instrumentsOur superannuation accounts are not directly exposed to, or involved in, the use of derivative financial instruments. However, some of the accounts’ underlying investments are in externally managed investments. These may, as part of that fund manager’s investment strategy, be involved in derivative financial instruments to hedge or partially hedge specific exposures. The investment strategy of our superannuation accounts is not to enter, hold or issue derivative financial instruments for trading purposes.

16 | Annual Report Other important information

Always speak to your financial adviserBefore you make any investment decisions, we recommend you speak with your financial adviser.

Your financial adviser will help you make an assessment of your financial goals and attitude to risk in order to determine which investment strategy best suits your individual needs.

Providing information to you electronicallyWe’re progressively increasing the range of reporting, transaction and product information you can access electronically through Investor Online.

Through Investor Online, you can currently access PDSs for the managed investments in your portfolio electronically. We may also provide you with the following information electronically:

• Notifications of any adverse changes and significant adverse events affecting your managed investments.

• Notice of any proposal by Asgard to introduce new fees and/or other costs, or to increase current fees or costs, affecting your account. This includes notice of our intention to receive and retain, as an additional fee for its services, any rebate, fee, commission or other payment in relation to an investment in your account.

• This Annual Report.

We may also use Investor Online in the future to provide you with any information (including Investor Reports), which may be required to be sent, given or made available to you under the trust deed or superannuation law.

You can access the following information on Investor Online anytime:

• Your account balance and transaction history• A list and value of investments held at any point

in time• Your pension details and Centrelink Schedule

(if applicable)

ther important information

Annual Report Other important information | 17

• Your insurance details (if applicable)• Account actions

You can also:

• change your address, contact and email details• change your PIN• submit your tax file number (TFN)• download Product Disclosure Statements• access all your Investor Reports and Axis

Superannuation Magazine• download a range of forms and• view tax and distribution information.

You’ll continue to have access to all of this information through your financial adviser and we may still choose to send some or all of this information directly to you. Unless you’ve previously agreed to receive this information and other notifications electronically1, you can ask us to send the required information to you in paper form, free of charge, by contacting us in advance.1. All Infinity eWRAP Super/Pension, eWRAP Super/Pension and Elements Super/

Pension investors and most other investors who joined since 1 April 2003 have agreed to this.

Contributing to your super via the Bpay® payment facilityBpay® is a quick and easy way for you to make deposits directly into your Asgard account. All you need is your customer reference number and the relevant Biller Code.

Depending on what type of contribution you’re making, there are different Biller Codes that apply when using Bpay®.

Contribution type Biller code

Personal deducted 66043 Personal undeducted 66050 Salary sacrifice 66027 Super guarantee 66019 Employer 66035 Spouse 66068

® Registered to Bpay® Pty Ltd ABN 69 079 137 518

Note: by using a Biller Code to make a Bpay® deposit, you acknowledge that you’ve received PDSs for the managed investments and cash products in your account (including information about significant events or matters affecting them) electronically on Investor Online. You can access these documents via the ‘PDS’ menu option on the Investor Online homepage.

18 | Annual Report Other important information

Do we have your tax file number (TFN)? If your TFN hasn’t been provided to us by 30 June of a financial year, we may be required to deduct an additional 31.5% tax from any employer contributions made to your account during that financial year. This additional tax, commonly referred to as ‘No-TFN tax’, may have been deducted from employer contributions made to your account since 1 July 2007.

You’re not required to supply your TFN to us, however if you do provide your TFN to us before 30 June 2013:

• you won’t have additional tax deducted from employer contributions made to your account during the 2012/13 financial year, and

• you may be eligible for a refund of any additional tax that may have been paid on employer contributions made to your account in the last three financial years (2009/10, 2010/11 and 2011/12).

Refund of contributions tax as an anti-detriment paymentAsgard’s Super and Pension products (excluding the Corporate Superannuation Service and the Rollover Service) take advantage of provisions within tax law that enable super funds to calculate an increased amount, known as an ‘anti-detriment’ payment, to be paid when a death benefit payment is made to an eligible beneficiary.

An anti-detriment payment represents a refund of contributions tax paid on all contributions made to the fund by the investor since joining the fund.

Eligible beneficiaries include a person who is a spouse, former spouse or child of the member. A beneficiary who was a financial dependant of the member but not a spouse, former spouse or child of the member is not eligible to receive an anti-detriment payment. In addition, an ‘anti-detriment’ payment cannot be paid if the death benefit is paid as a pension.

We’ve established a reserve to facilitate these refunds. At 30 June 2012, the amount held in this reserve was $929,952 (2011: $1,251,649, 2010: $1,430,910). We manage the reserve by holding it in cash as the liquidity is needed to ensure refunds can readily be made on an ongoing basis. Asgard will generally manage any applicable refunds/anti-detriment payments automatically at claim time.

Annual Report Other important information | 19

Remuneration

Service fee and/or commission – cash productsWe may receive a service fee and/or commission of up to 1.1% pa (including GST) from St.George, Westpac or other providers of cash products. The service fee is for the introduction of your banking business and/or performing client service activities and transaction reporting on any of your cash accounts. The service fee is calculated as a percentage of the daily balance of the relevant cash product and is not an additional charge to you.

Closed accountsIf you close your Super or Pension account and amounts less than $50 are subsequently credited to your closed account, we’ll apply this money for the general benefit of all current investors of the fund rather than your closed account.

Eligible Rollover Fund – Superannuation accounts onlyThe Advance Retirement Savings Account (Advance RSA) is our nominated Eligible Rollover Fund. We may transfer your benefits to this fund if:

• the value of your account is less than $2,000,• we’ve written to you twice and both times the mail has

been returned unclaimed,

• you’re a member of the Asgard Corporate Superannuation Service or Asgard Employee Superannuation Account, and:

– no contributions or rollovers have been paid to your account in two years,

– you’ve left your employer and no instructions have been received from you regarding where to transfer your benefits, or

– the value of all accounts held by members of the same employer group is less than $10,000,

• it is otherwise permitted by superannuation law.

We’re also the trustee of the Advance RSA. Both Asgard and Advance are wholly owned subsidiaries of Westpac Banking Corporation.

On transferring to the Advance RSA, your rights in your Asgard account will cease and you’ll no longer be able to make contributions to your account. Instead, you become a member of the Advance RSA and are subject to its governing rules. You’ll receive a PDS for the Advance RSA setting out relevant information shortly after the time your benefits are transferred. This PDS is also available online.

20 | Annual Report Other important information

It’s important to note the following are some of the conditions that will be different to the Asgard account you previously held.

• You’ll no longer receive regular reports from Asgard about your Asgard account.

• Any insurance cover you may have held through your Asgard account will cease.

• A different fee structure will apply.• Holding an interest in the Advance RSA may result in

different risks and returns to those applicable to your current investments.

For further information speak to your financial adviser or contact:

The Advance Retirement Savings Account GPO Box B87, Perth WA 6838 Telephone: 1800 819 935

Policy committees (only applicable to Asgard Employee Super Account and Asgard Corporate Superannuation Service)Employers with 50 or more employer sponsored members in a superannuation plan have an obligation to establish a policy committee. Employers with fewer employees may establish a committee but are not obliged to do so.

The policy committee serves as an avenue for sponsored members to enquire about the operation or management of their plan. While there’s an obligation to establish the committee, if the committee decides that it serves no purpose, then it may resolve to dissolve itself at its convenience. It may be re-established in the future if requested by at least five employees.

If you’re interested in finding out more about your policy committee, you should ask your employer for details. Your employer should be able to advise you of the committee members and how each member was appointed.

Professional indemnity insuranceWe’re currently covered by a professional indemnity insurance policy issued by American Home Assurance Company and other insurers.

Annual Report Other important information | 21

Enquiries and complaintsIf you’d like further financial information that’s not included in this Annual Report, including information about fees and charges and other effects arising from a rollover or transfer of your benefit entitlements, we’re happy to provide it on request.

If you have any enquiries or complaints about the operation or management of one of our super accounts, please contact us on:

Telephone: 1800 998 185 Email: [email protected]

Or write to:

Asgard Investor Services PO Box 7490 Cloisters Square WA 6850

If you’ve made a complaint to us about a decision which affects you, and your complaint has not been resolved to your satisfaction, you have a right to lodge a complaint about the decision with the Superannuation Complaints Tribunal.

The Tribunal is a body established by the Commonwealth Government to review trustee decisions relating to members (as opposed to trustee decisions relating to the management of the fund as a whole). You can contact the Superannuation Complaints Tribunal on 1300 884 114.

22 | Annual Report Financial reports

Asgard Super and Pension AccountsIn accordance with superannuation law, we provide you with abridged financial information for the:

• Asgard Corporate Superannuation Service• Asgard Superannuation Accounts• Asgard Pension Accounts• Asgard Rollover Service.

A copy of the full audited financial statements for these accounts and services for the financial year ended 30 June 2012 is available from us on request.

inancial reports

Annual Report Financial reports | 23

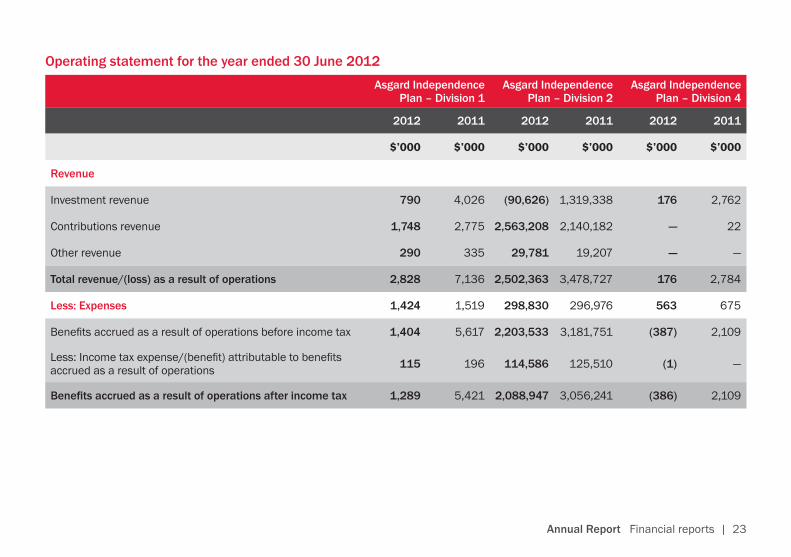

Operating statement for the year ended 30 June 2012Asgard Independence

Plan – Division 1Asgard Independence

Plan – Division 2Asgard Independence

Plan – Division 4

2012 2011 2012 2011 2012 2011

$’000 $’000 $’000 $’000 $’000 $’000

Revenue

Investment revenue 790 4,026 (90,626) 1,319,338 176 2,762

Contributions revenue 1,748 2,775 2,563,208 2,140,182 — 22

Other revenue 290 335 29,781 19,207 — —

Total revenue/(loss) as a result of operations 2,828 7,136 2,502,363 3,478,727 176 2,784

Less: Expenses 1,424 1,519 298,830 296,976 563 675

Benefits accrued as a result of operations before income tax 1,404 5,617 2,203,533 3,181,751 (387) 2,109

Less: Income tax expense/(benefit) attributable to benefits accrued as a result of operations 115 196 114,586 125,510 (1) —

Benefits accrued as a result of operations after income tax 1,289 5,421 2,088,947 3,056,241 (386) 2,109

24 | Annual Report Financial reports

Statement of financial position as at 30 June 2012Asgard Independence

Plan – Division 1Asgard Independence

Plan – Division 2Asgard Independence

Plan – Division 4

2012 2011 2012 2011 2012 2011

$’000 $’000 $’000 $’000 $’000 $’000

Assets

Cash and cash equivalents 15,044 15,041 2,048,530 1,918,947 3,412 3,177

Receivables 74 134 50,126 80,573 96 325

Current tax receivables — — — — — —

Deferred tax assets — — 74,981 150,756 — —

Investments 33,543 41,780 13,588,372 13,894,887 25,501 30,419

Total assets 48,661 56,955 15,762,009 16,045,163 29,009 33,921

Less: Liabilities

Payables 703 758 32,318 33,832 59 69

Current tax liabilities 27 90 8,019 47,944 — —

Deferred tax liabilities 1 3 — — — —

Total liabilities 731 851 40,337 81,776 59 69

Net assets available to pay benefits 47,930 56,104 15,721,672 15,963,387 28,950 33,852

Annual Report Financial reports | 25

Asgard Independence Plan – Division 1

Asgard Independence Plan – Division 2

Asgard Independence Plan – Division 4

2012 2011 2012 2011 2012 2011

$’000 $’000 $’000 $’000 $’000 $’000

Represented by:

Liability for accrued benefits

– allocated to members’ accounts 47,930 56,104 15,646,691 15,812,631 28,950 33,852

– unallocated to members’ accounts — — 74,981 150,756 — —

Total liabilities for accrued benefits 47,930 56,104 15,721,672 15,963,387 28,950 33,852

ASx1666-1112gd