ASEAN Financial Integration towards ASEAN 2025 · Source: ASEAN Secretariat (2014) ASEAN Community...

32

ASEAN Financial Integration towards ASEAN 2025: Call for a well-coordinated supervisory and regulatory framework Satoru (Tomo) Yamadera Principal Financial Sector Specialist Asian Development Bank

Transcript of ASEAN Financial Integration towards ASEAN 2025 · Source: ASEAN Secretariat (2014) ASEAN Community...

ASEAN Financial

Integration towards

ASEAN 2025: Call for a well-coordinated supervisory and

regulatory framework

Satoru (Tomo) Yamadera

Principal Financial Sector Specialist

Asian Development Bank

Outline

• ASEAN Community and ASEAN Economic Community

• ASEAN Financial Integration Framework (AFIF) and ASEAN Banking Integration Framework (ABIF)

• Current status of ASEAN Economic and Financial integration

• Future steps: what needs to be done?

– Strategies embedded in the ASEAN Economic Community Blueprint 2025

2

ASEAN Community

ASEAN

Political

Security

Community

ASEAN

Economic

Community

ASEAN

Socio-

Cultural

Community

ASEAN Community

3

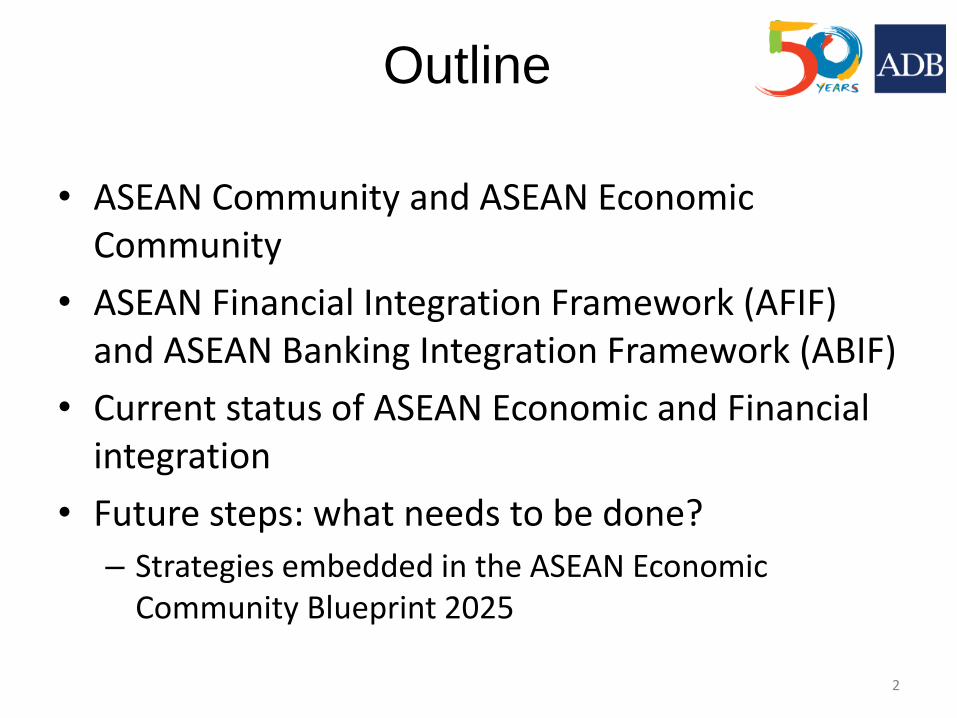

ASEAN: Big potential for

Growth

Source: ASEAN Secretariat (2015) A Blueprint for Growth ASEAN Economic Community 2015: Progress and Key Achievements 4

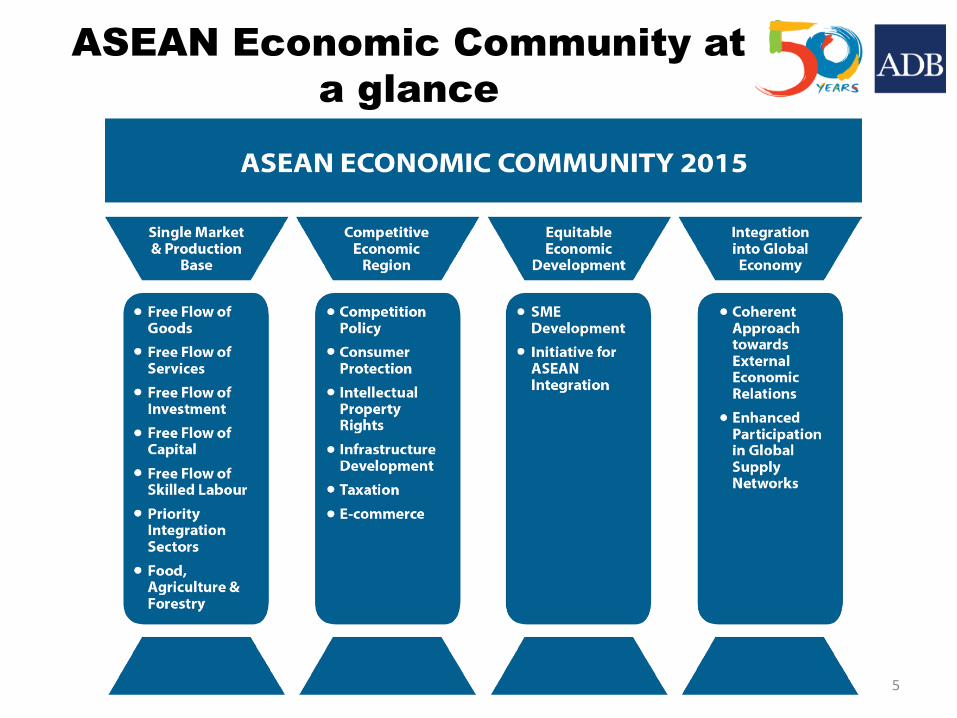

ASEAN Economic Community at

a glance

1.3 The Four Pillars of ASEAN Economic Integration

The AEC Blueprint is built on four interrelated and mutually-reinforcing pillars: (a) a

single market and production base, (b) a highly competitive economic region, (c) a

region of equitable economic development, and (d) a region fully integrated into the

global economy. As broad and multi-faceted as these are, the goals of the AEC have

already been met on many fronts.

The f rst AEC pillar seeks to create a single market and production base through

free f ow of goods, services, investment, skilled labour and freer f ow of capital.

Cumulatively, these aim for a more liberalised market that provides its population

with greater opportunities to trade and do business within the region, with reduced

trade costs and improved investment regimes that make ASEAN a more attractive

investment destination for both international and domestic investors.

The second pillar helps to create a business-friendly and innovation-supporting

regional environment. That is achievable through the adoption of common

4 |A Blueprint for Growth

ASEAN Economic Community 2015: Progress and Key Achievements

| 5 A Blueprint for Growth

ASEAN Economic Community 2015: Progress and Key Achievements

5

AEC 2015 Achievement

Source: ASEAN Secretariat (2015) A Blueprint for Growth ASEAN Economic Community 2015: Progress and Key Achievements

6

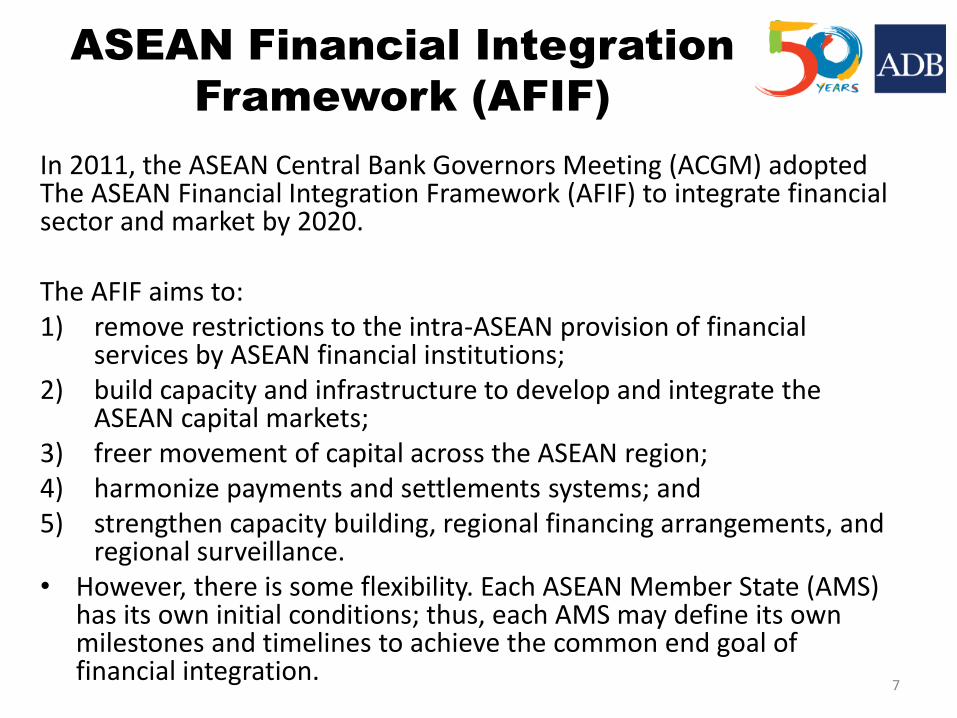

ASEAN Financial Integration

Framework (AFIF)

In 2011, the ASEAN Central Bank Governors Meeting (ACGM) adopted The ASEAN Financial Integration Framework (AFIF) to integrate financial sector and market by 2020. The AFIF aims to: 1) remove restrictions to the intra-ASEAN provision of financial

services by ASEAN financial institutions; 2) build capacity and infrastructure to develop and integrate the

ASEAN capital markets; 3) freer movement of capital across the ASEAN region; 4) harmonize payments and settlements systems; and 5) strengthen capacity building, regional financing arrangements, and

regional surveillance. • However, there is some flexibility. Each ASEAN Member State (AMS)

has its own initial conditions; thus, each AMS may define its own milestones and timelines to achieve the common end goal of financial integration.

7

Governance structure of AFIF

8

In 2014, the ACGM endorsed the ASEAN Banking Integration Framework (ABIF) as a core component of ASEAN Financial Integration Framework (AFIF), and subsequently agreed to the Guidelines for its implementation.

• ABIF allows banks meeting certain criteria to have greater access to other ASEAN markets and more flexibility in operating there.

• ABIF is expected to support ASEAN economic integration by bringing greater competition among ASEAN banks, which would lead to emergence of strong pan-ASEAN regional banks with the scale and the capability to compete against the global banks.

9

ASEAN Banking Integration

Framework (ABIF)

• The Guidelines are kept confidential but focus on the implementation of Qualified ASEAN Banks (QAB). Key points of the Guidelines are following:

a) QAB will be given national treatment in Host country in terms of market access and operational flexibility which is often not enjoyed by a foreign bank (e.g., opening of branches);

b) Financial soundness based on Basel capital accord, sizable market share in Home country and fit-and-proper of bank shareholders and management are key requirements;

c) Granting of QAB status is to be negotiated bilaterally based on a reciprocity principle.

d) In granting QAB status, Indigenous ASEAN banks with existing presence in AMSs are to be given priority.

e) ASEAN central banks aim to have concluded the first set of negotiations among ASEAN 5 by 2018 and among all AMS by 2020.

• Currently MOU or LOI is exchanged between: Malaysia and Thailand; Malaysia and Philippines; Malaysia and Indonesia; Thailand and Indonesia

10

ABIF Guidelines

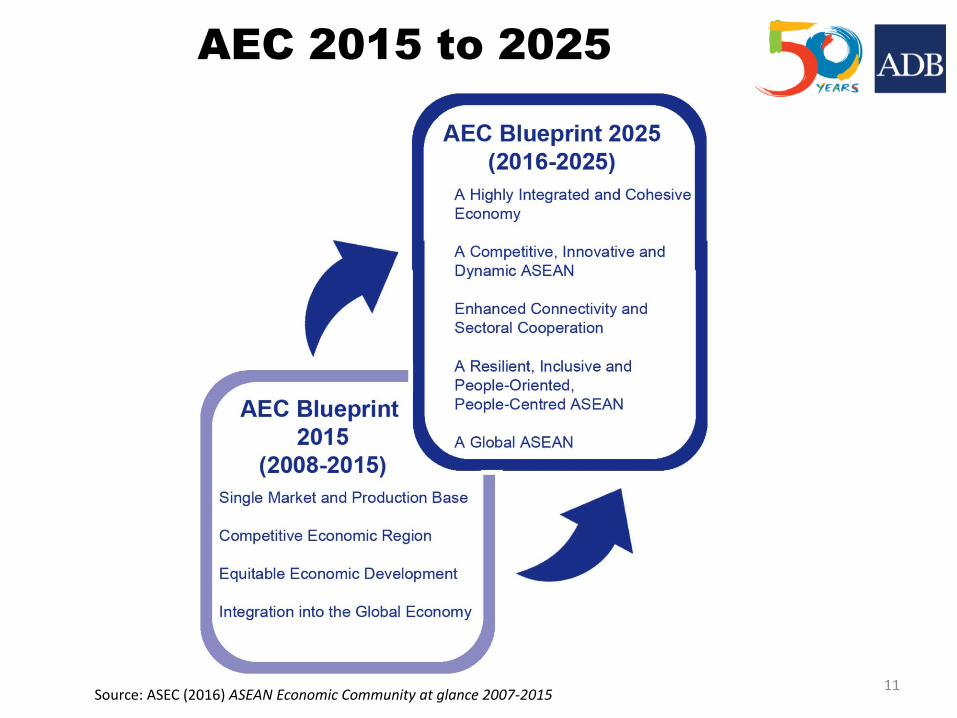

AEC 2015 to 2025

Source: ASEC (2016) ASEAN Economic Community at glance 2007-2015 11

Current state of ASEAN Economic and Financial integration

12

No intra-ASEAN tariff

Source: ASEAN Secretariat (2014) ASEAN Community in Figures – Special Edition 2014

13

Source: ASEC (2016) ASEAN Economic Community at glance 2007-2015 14

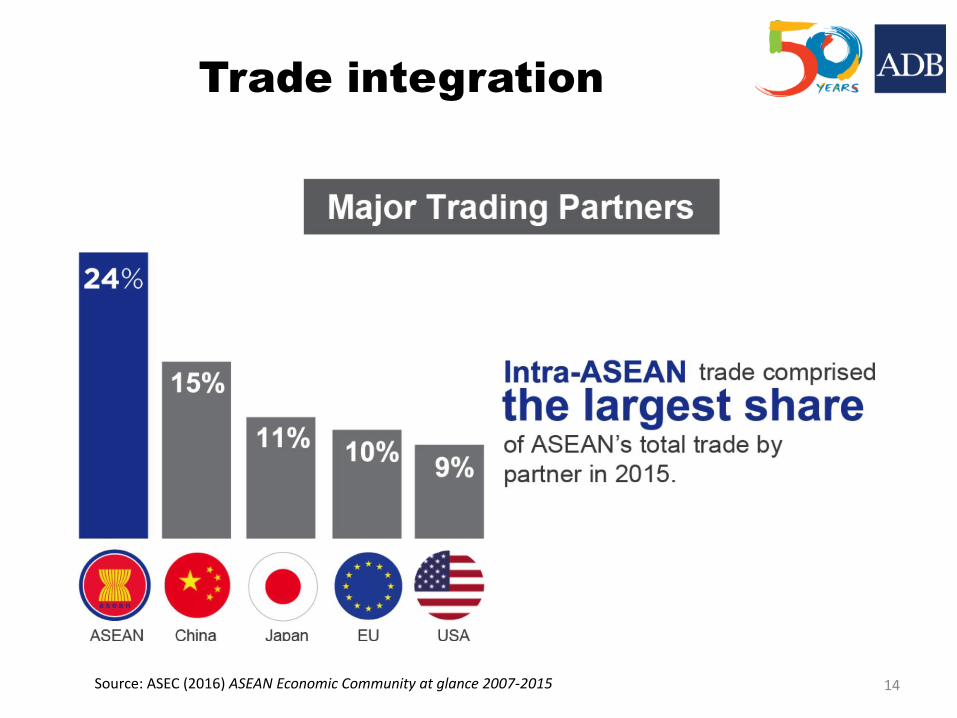

Trade integration

Trend of ASEAN Trade with ASEAN+3,

ASEAN+6 and EAS (in US$ billion),

1993-2013

Source: ASEAN Community in Figures – Special Edition 2014

15

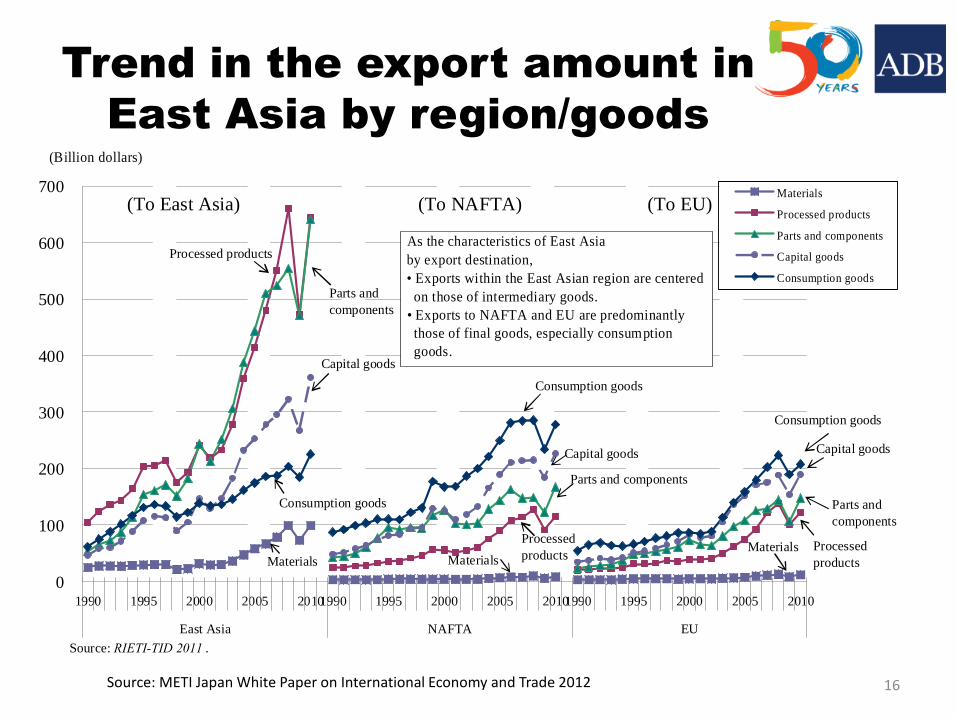

Trend in the export amount in

East Asia by region/goods

298

including Japanese manufacturers. This will be discussed in the next paragraph “2. Division of

production developed in East Asia.”

(B) Differences in inter-regional trades in East Asia, EU and NAFTA

Is this trade structure in East Asia common to other regions (such as EU and NAFTA)? Figure

2-2-1-3 compares the composition by goods in inter-regional trade among three regions. East Asia has

a much higher share of parts and components than NAFTA and EU (East Asia: 32.5%, NAFTA: 17.2%,

EU: 16.2% as of 2010) and conversely has a much lower share of consumption goods than NAFTA

and EU (East Asia: 11.4%, NAFTA: 22.6%, EU: 30.1% as of 2010). This suggest the division of

production has developed more actively in East Asia than in EU and NAFTA, and the entire region

serves as a “factory of the world.”

Figure 2-2-1-3

Composition by goods in inter-regional trade

0

10

20

30

40

50

1990 1995 2000 2005 20101990 1995 2000 2005 20101990 1995 2000 2005 2010

East Asia NAFTA EU

Materials

Processed products

Parts and components

Capital goods

Consumption goods

(%)

(Within East Asia) (Within EU)(Within NAFTA)

Source: RIETI-TID 2011 .

As the characteristics of East Asia,

• The share of trades of parts and components has rapidly increased.

• The share of consumption goods is low and has been declining.

Processed products

Materials

Capital goods

Consumption goods

Parts and components

Consumption goods

11.4

30.1

22.6

16.217.2

32.5

Parts and components

(C) Export destinations of East Asia

Then where are the final consumption goods produced exported to? Figure 2-2-1-4 shows East

Asian exports by region. As was described previously, the share of intermediary goods is high in

exports within the region. Meanwhile, the share of final goods is high, and especially that of

consumption goods is the highest in exports to NAFTA and EU. Exports of consumption goods within

the East Asian region were greater than those to NAFTA as of 2010.

Figure 2-2-1-4

Trend in the export amount in East Asia by region/goods

0

100

200

300

400

500

600

700

1990 1995 2000 2005 20101990 1995 2000 2005 20101990 1995 2000 2005 2010

East Asia NAFTA EU

Materials

Processed products

Parts and components

Capital goods

Consumption goods

(Billion dollars)

(To East Asia) (To EU)(To NAFTA)

Source: RIETI-TID 2011 .

As the characteristics of East Asia

by export destination,

• Exports within the East Asian region are centered

on those of intermediary goods.

• Exports to NAFTA and EU are predominantly

those of final goods, especially consumption

goods.

Processed products

Materials

Capital goods

Consumption goods

Parts and

components

Consumption goods

Consumption goods

Capital goodsCapital goods

Parts and

components

Parts and components

Processed

products

Processed

productsMaterials

Materials

16 Source: METI Japan White Paper on International Economy and Trade 2012

Trend in the export amount of

consumption goods in East Asia by

counterpart country

299

(D) Change of the trade structure before and after the failure of Lehman Brothers

The trade structure described above is susceptible to a demand shock from outside the region

because it has relied on the markets in Europe and the U.S. for final demands such as consumption

goods. In fact, countries highly dependent on exports in particular were greatly affected by the failure

of Lehman Brothers. This led to increasing calls for a departure from dependence on Europe and the

U.S. and growth as self-reliant economic zones based on inter-regional demand within East Asia after

the failure of Lehman Brothers.

Then did such a trade structure actually change? We look at the trend in the amount and share of

final consumption goods in East Asia by export destination as one consideration. First, before the

failure of Lehman Brothers, exports of consumption goods to Europe and the U.S. increased, while

those to East Asia temporarily decreased after the Asian currency crisis in 1997 (Figure 2-2-1-5 (a)). It

is probably because countries affected by the currency crisis in particular expanded exports to Europe

and the U.S. due to the lower exchange rate. After that, although exports to East Asia have been

recovering, their growth is slow. Looking at shares by export destination, exports to East Asia

continued to decrease (Figure 2-2-1-5 (b)). The share of exports to Japan is high among East Asian

economies. Meanwhile, exports to EU have greatly increased in amount and share since 2003 in

exports of consumption goods to Europe and the U.S.

Figure 2-2-1-5 (a)

Trend in the export amount of consumption goods in East Asia by counterpart country

0

50

100

150

200

250

300

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

East Asia

EU27

U.S.

Japan

ASEAN

China

Hong Kong

Taiwan

South Korea

(Billion dollars)

Note: East Asia consists of Japan, China, South Korea, Hong Kong, Taiwan, Brunei, Cambodia, Indonesia, Malaysia, Philippines, Singapore,

Thailand and Vietnam.

Source: RIETI-TID 2011 .

Asian currency crisis

(1997)

Failure of Lehman Brothers

(2008)

U.S.

EU27

East Asia

ChinaASEAN

Japan

Hong Kong

Taiwan

South

Korea

Figure 2-2-1-5 (b)

Trend in the share of East Asian exports of consumption goods by counterpart country

0

10

20

30

40

50

60

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

East Asia

EU27

U.S.

Japan

ASEAN

China

Hong Kong

Taiwan

South Korea

(%)

Note: East Asia consists of Japan, China, South Korea, Hong Kong, Taiwan, Brunei, Cambodia, Indonesia, Malaysia, Philippines, Singapore,

Thailand and Vietnam.

Source: RIETI-TID 2011 .

Asian currency crisis

(1997)

Failure of Lehman Brothers

(2008)

U.S.

EU27

East Asia

China

ASEAN

Japan

South

Korea

Taiwan

Hong

Kong

The share of East Asia has increased, while

the share of the U.S. and EU has decreased.

Source: METI Japan White Paper on International Economy and Trade 2012 17

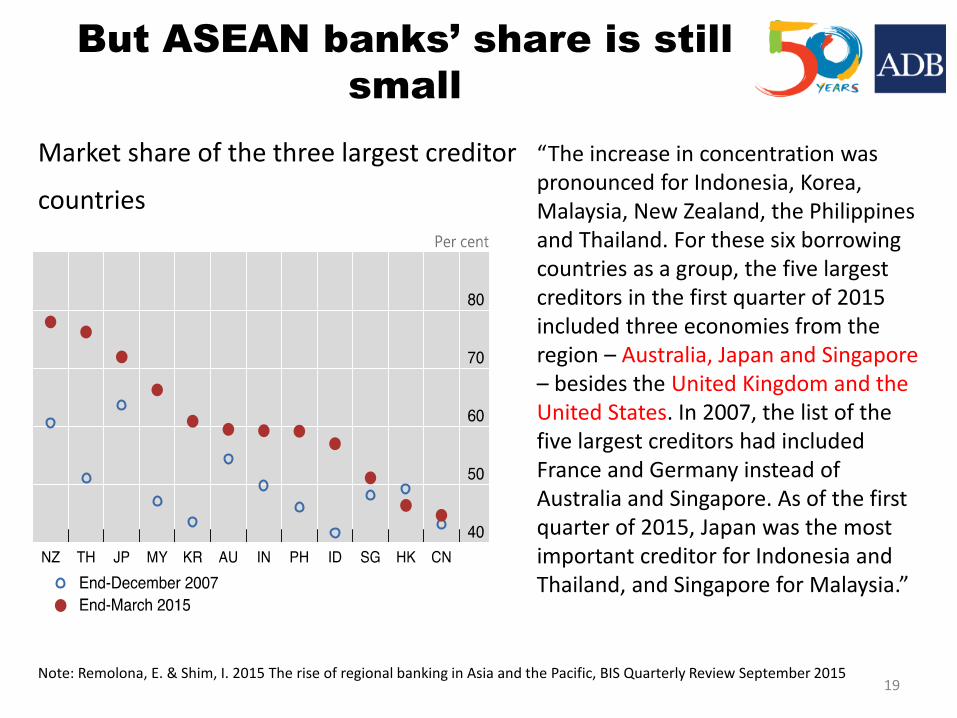

Who is lending to Asia?

Note: Remolona, E. & Shim, I. 2015 The rise of regional banking in Asia and the Pacific, BIS Quarterly Review September 2015

18

But ASEAN banks’ share is still

small

Market share of the three largest creditor

countries

“The increase in concentration was pronounced for Indonesia, Korea, Malaysia, New Zealand, the Philippines and Thailand. For these six borrowing countries as a group, the five largest creditors in the first quarter of 2015 included three economies from the region – Australia, Japan and Singapore – besides the United Kingdom and the United States. In 2007, the list of the five largest creditors had included France and Germany instead of Australia and Singapore. As of the first quarter of 2015, Japan was the most important creditor for Indonesia and Thailand, and Singapore for Malaysia.”

Note: Remolona, E. & Shim, I. 2015 The rise of regional banking in Asia and the Pacific, BIS Quarterly Review September 2015 19

Current state of ASEAN

Integration (in summary)

• Intra-ASEAN trades is still small comparing to EU. • However, Intra-regional trades within ASEAN+3 is comparable to EU.

• Intra-East Asia’s trade is large, but final destination is outside of the

region. higher. • However, East Asia, particularly China and ASEAN, are growing rapidly

and East Asia is become the biggest final destination of trade.

• Banking within ASEAN is rather limited. • However, Asia-Pacific banks are far much more dominant.

• It is better to broaden the scope of regional integration from ASEAN to

ASEAN+3 and ASEAN+6. • ASEAN can leverage its positon by pursuing open regionalism

20

What needs to be done?

21

Is EU a model for ASEAN?

• EU is – Fully integrated market, with

• the single market • under the same regulations and directives • Unified supervisory bodies

– European Banking Authority – European Securities Authority – European Insurance and Pension

• The Single Resolution Mechanism

• ASEAN needs to seek its Financial Integration model – each AMS may define its own milestones and

timelines to achieve the common end goal of financial integration.

• But how? 22

Strategies included in AEC

Blueprint 2025

- 2015ASEAN 2025: Forging Ahead Together-

• Para 17. i: “Strengthen financial integration to facilitate intra-ASEAN trade and investment by increasing the role of ASEAN indigenous banks, having more integrated insurance markets, and having more connected capital markets “

• Para 17.i.b: “Provide greater market access and operational flexibility for Qualified ASEAN Banks (QABs) through the ASEAN Banking Integration Framework (ABIF), based on each country’s readiness and on a reciprocal basis, thereby reducing gaps in market access and operational flexibility across ASEAN”

• Para 17.i.c: “Promote deeper penetration in insurance markets through the ASEAN Insurance Integration Framework (AIIF), with greater risk diversification, deeper underwriting capacity, improved and strengthened insurance sector supervision and regulatory frameworks”

• Para 17.i.d: “Further deepen and interlink capital markets by progressing towards more connectivity in clearing settlement and custody linkages to facilitate investment in the region, and allow investors and issuers to tap cross-border ASEAN capital markets efficiently, in line with the objective of ASEAN Capital Market Infrastructure (ACMI) Blueprint. “

• Para 17.i.e: “Promote the development of sovereign bond markets as well as corporate issuances that will diversify risks from the banking system and provide savers with greater opportunities to invest“ 23

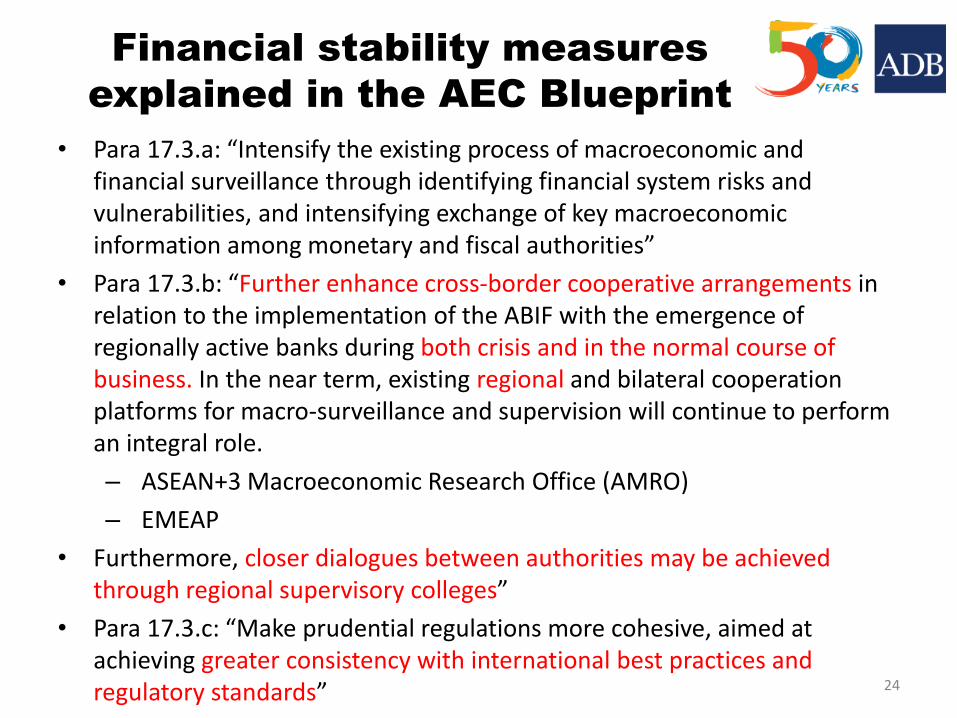

Financial stability measures

explained in the AEC Blueprint

• Para 17.3.a: “Intensify the existing process of macroeconomic and financial surveillance through identifying financial system risks and vulnerabilities, and intensifying exchange of key macroeconomic information among monetary and fiscal authorities”

• Para 17.3.b: “Further enhance cross-border cooperative arrangements in relation to the implementation of the ABIF with the emergence of regionally active banks during both crisis and in the normal course of business. In the near term, existing regional and bilateral cooperation platforms for macro-surveillance and supervision will continue to perform an integral role.

– ASEAN+3 Macroeconomic Research Office (AMRO)

– EMEAP

• Furthermore, closer dialogues between authorities may be achieved through regional supervisory colleges”

• Para 17.3.c: “Make prudential regulations more cohesive, aimed at achieving greater consistency with international best practices and regulatory standards”

24

The measures for the key cross-

cutting areas under the AEC

Blueprint

• Capital account liberalization – . i. a: “Ensure an orderly capital account liberalisation”

• Payment and Settlement Systems – promoting standardisation – developing settlement infrastructure for cross-border trade, remittance,

retail payment systems and capital markets. – This will provide an enabling environment to promote regional linkages

and payment systems that are safe, efficient and competitive. – This will also require a certain level of harmonisation of standards and

market practices based on international best practices (such as ISO 20022) to foster stability and efficiency within as well as outside the region.

• Capacity building – narrow the financial development gap in the region. This can be

achieved through the conduct of learning programmes and exchanges of knowledge and experiences, and best practices in areas relevant to financial integration and development,

25

ASEAN+3 Asian Bond Markets

Initiatives (ABMI)

(Chairman's Press Release on the Asian Bond Markets Initiative, 7 August

2003)

• ABMI aims to develop efficient and liquid bond markets in

Asia, which would enable better utilization of Asian savings

for Asian investments.

• The ABMI would also

contribute to the mitigation of

currency and maturity

mismatches in financing.

- ABMI contributes to

financial stability by

creating multiple channels

of financing

26

• Harmonization and standardization

• ASEAN+3 Multi-currency Bond Issuance Framework (AMBIF)

• CSD-RTGS Linkages as regional safety-net

CGIF

$ 700 million

Asian Bonds Online

ABMF

Public Private platform

CSIF

CBs

CSDs

27

Major outputs of ABMI

CSD

Central Bank RTGS

CSD

Participant

Participant

Participant

Participant

G

W

G

W

CSD

Centr

al

Bank

RTG

S

Participant

Participant

Participant

Participant

G

W

G

W

Centr

al

Bank

RTG

S

CSD

Participant

Participant

Participant

Participant

G

W

Gateway

Participant

Participant

Research on: • Infra bond

finance • Broadening

the investor base

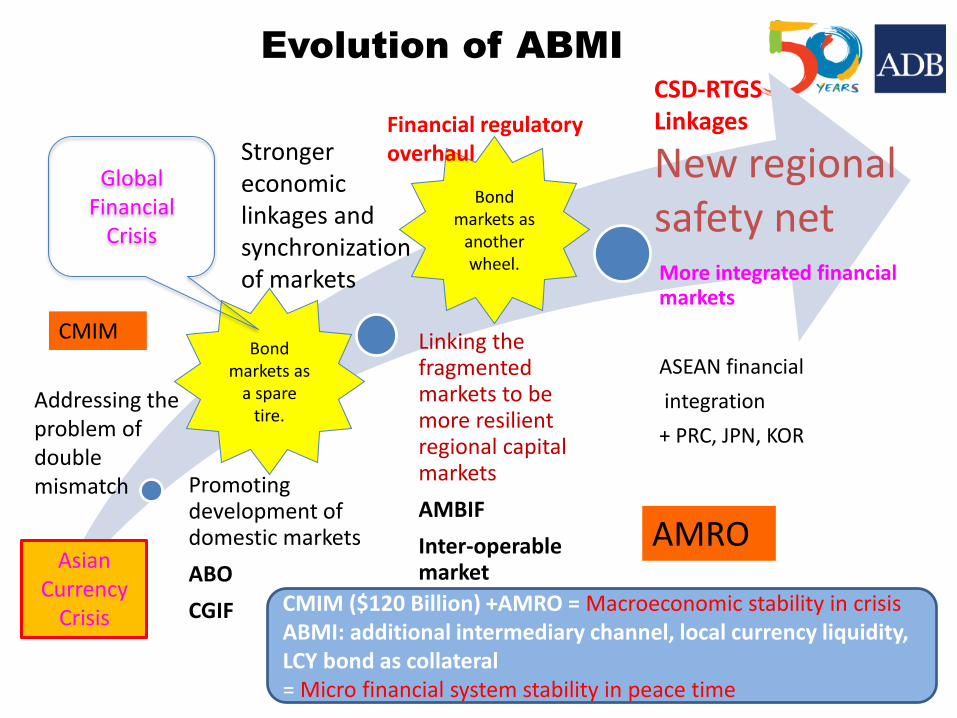

Evolution of ABMI

Promoting development of domestic markets

ABO

CGIF

Linking the fragmented markets to be more resilient regional capital markets

AMBIF

Inter-operable market infrastructures

More integrated financial markets

ASEAN financial

integration

+ PRC, JPN, KOR

28

Addressing the problem of double mismatch

CSD-RTGS Linkages

CMIM ($120 Billion) +AMRO = Macroeconomic stability in crisis ABMI: additional intermediary channel, local currency liquidity, LCY bond as collateral = Micro financial system stability in peace time

Asian Currency

Crisis

Bond markets as

a spare tire.

Global Financial

Crisis

Bond markets as

another wheel.

Stronger economic linkages and synchronization of markets

Financial regulatory overhaul New regional

safety net

CMIM

AMRO

Remaining issues for financial

stability

• Development of institutional safety-net in all ASEAN member states – Deposit Insurance – Insurance policy holders protection – Cross-border collateral and repo

• Coordination among regulators not only among ASEAN but also ASEAN+3 or +6 – Prevention of regulatory arbitrage – Information sharing through supervisory college – Cross-border resolution mechanism

29

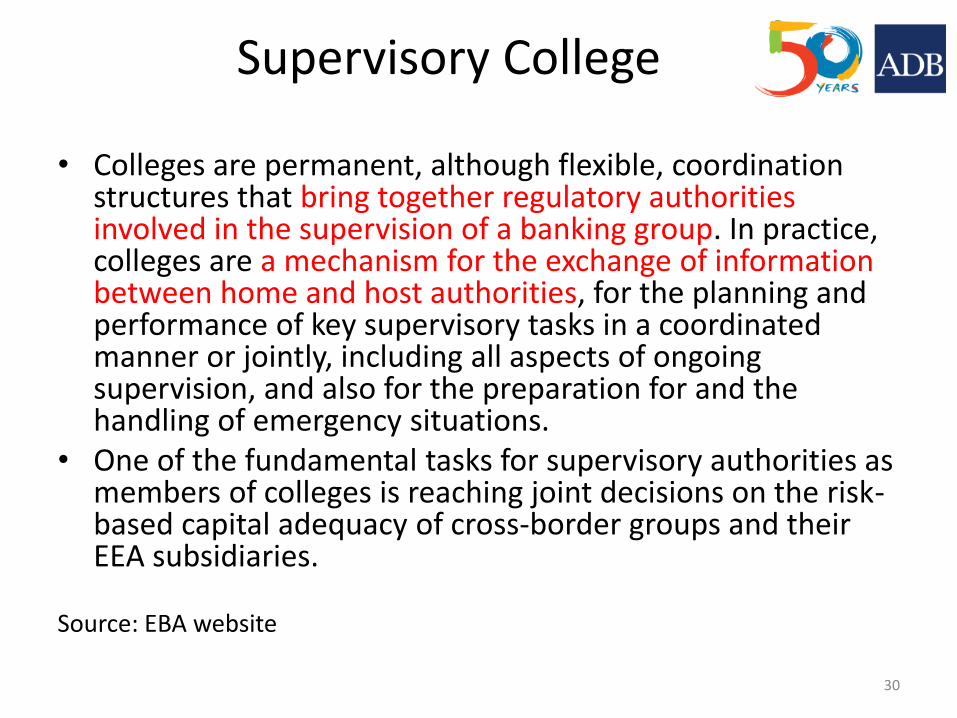

Supervisory College

• Colleges are permanent, although flexible, coordination structures that bring together regulatory authorities involved in the supervision of a banking group. In practice, colleges are a mechanism for the exchange of information between home and host authorities, for the planning and performance of key supervisory tasks in a coordinated manner or jointly, including all aspects of ongoing supervision, and also for the preparation for and the handling of emergency situations.

• One of the fundamental tasks for supervisory authorities as members of colleges is reaching joint decisions on the risk-based capital adequacy of cross-border groups and their EEA subsidiaries.

Source: EBA website

30

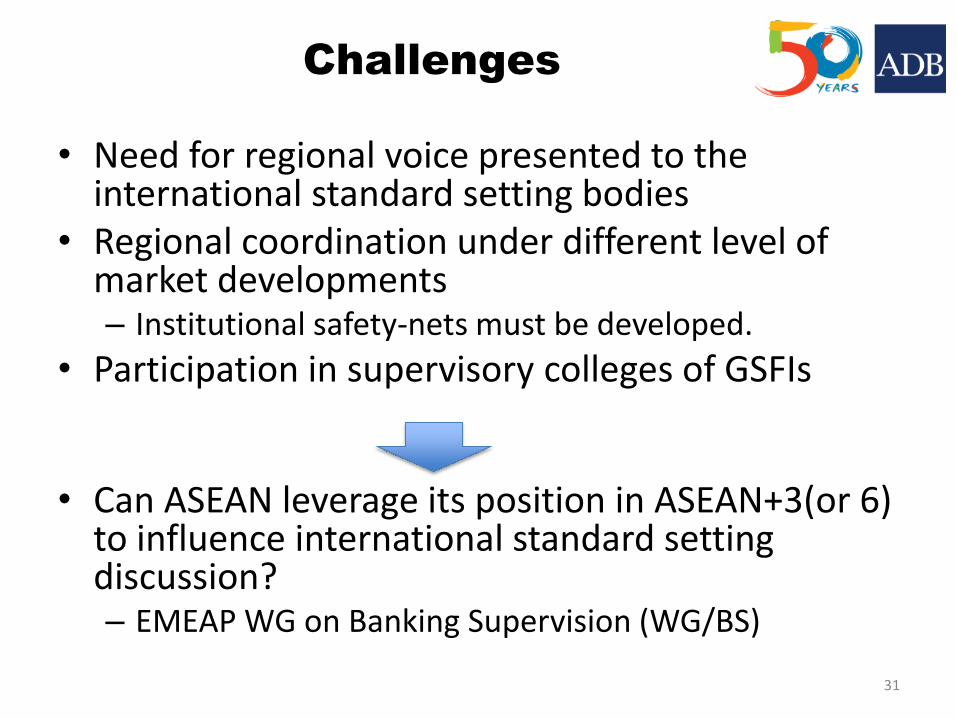

Challenges

• Need for regional voice presented to the international standard setting bodies

• Regional coordination under different level of market developments – Institutional safety-nets must be developed.

• Participation in supervisory colleges of GSFIs

• Can ASEAN leverage its position in ASEAN+3(or 6) to influence international standard setting discussion? – EMEAP WG on Banking Supervision (WG/BS)

31