ASEAN Coal Trends: Challenges and Oppor tuni ties on Facing ASEAN Economi c Communi ty (AEC)

26

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) i ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) Asra Virgianita, Ph.D Santi Hapsari Paramitham, S.Sos Meliana Lumbantoruan, M.A

-

Upload

meliana-lumbantoruan -

Category

Environment

-

view

309 -

download

3

Transcript of ASEAN Coal Trends: Challenges and Oppor tuni ties on Facing ASEAN Economi c Communi ty (AEC)

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) i

ASEAN Coal Trend Challenges and Opportunities on Facing

ASEAN Economic Community (AEC)

Asra Virgianita, Ph.D

Santi Hapsari Paramitham, S.Sos

Meliana Lumbantoruan, M.A

ii

ASEAN Coal Trend :

Challenges and Oppor tuni ties on Facing ASEAN Economi c Communi ty (AEC)

ISBN : 978-602-72039-2-1

Writer

Asra Virgianita,Ph.D.

Lecturer, Department of International Relations,

Faculty of Social and Poli tical Sciences, University of Indonesia

Santi Hapsari Paramitham,S.Sos.

Paperer, ASEAN Study Centre,

Faculty of Social and Poli tical Sciences, University of Indonesia

Meliana Lumbantoruan,M.A.

Research and Knowledge Manager, Publish What You Pay Indonesia

Reviewer

Maryati Abdullah

National Coordin ator, Publish What You Pay Indonesia

Jensi Sartin

Program Development Manager, Publish What You Pay Indonesia

All Right Reserved

First Edition, 2015

This paper was publi shed by Yayasan Transparasi Sumberdaya Ekstraktif-Publish What You Pay

Indonesia, with suppor ted by Natural Resources Governance Institute and United State Agency

for International Development (USAID). The contents are the responsibili ty of Publish What

You Pay (PWYP) Indonesia and do not necessarily reflect the views of USAID, the United States

Government, or the Natural Resource Governance Institute (NRGI).

Publish What You Pay Indonesia

Jl. Tebet Utara 2C No.22B, Jakarta Selatan 12810, Indonesia

Telp/Fax :+62-21-8355560 | E: sekretariat@pwyp-indon esia.org

Contents

Abstract ............................................................................................................. 3

Introduction ................................................................................................... 4

Coal Trade Pattern and Global Value Chain: An Overview ....................................... 6

ASEAN Economi c Communi ty: The Way towards Integration ............................. 10

Coal Trends and the Readines of ASEAN Coun tries on Facing the AEC ................ 12

Coal Prospects in ASEAN Region .................................................................... 12

ASEAN Energy Policy ...................................................................................... 14

ASEAN Coun tries Strategy ........................................................................... 16

Clean and Eff icient Coal use in ASEAN: The Economi c Benefit ....................... 17

Challenges and Oppor tuni ties of Coal Sector on Facing AEC ................................ 19

Closing ............................................................................................................ 22

Bibliogr aphy ........................................................................................................ 23

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) iii

iv

A

Abstract

SEAN energy consump tion is forecasted to rise because of the

signi ficant gro wt h of economy and popul ation in the region. Coal

use continuou sly increase as a replacement for oil and natural gas.

ASEAN plays signi ficant roles in coal consump tion and produ ction in Asia

Pacific. Using the value chain approach, it is projected that coal produ cer

coun tries in ASEAN will have the chance to maximize the market through

bilateral trade or AEC framework. The AEC can foster market integration

in ASEAN, build s awareness of ASEAN coun tries to develop their

infrastructure in energy suff iciency, as well as develops clean coal

technolog y. Coal produ ction in ASEAN will still leant on Indonesia as the

main expor ter in ASEAN. Energy policy of each coun try in ASEAN has a lot

of things in common , which provides the space of building further regional

coooperation in managing energy features. The future of coal sector in

ASEAN will highl y depends on advancement of technolog y, impro vement

of governance, effeciency of transpor tation, and connectivity between

the coun tries. Strengthening cooperation and coordin ation must be a key

strategy for ASEAN coun tries to ensure readiness in facing AEC.

Keywords: Coal, ASEAN, AEC, energy, value chain, governance

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) 1

E

Introduction

conomi c gro wt h and industrial activity

are the tw o strongl y related aspects. In

the era of global and regional market,

coun tries are expected to be competitive to

survive the flow of foreign commodi ties, as

well as compete their domestic commodi ties

into foreign market. This condi tion requires

high quality of infrastructure, including the

technolog y, transpor tation, electricity, and

energy suppli es. Adequate energy suppli es

ensure sustainabili ty of energy consump tion

for transpor tation, electricity, and

technolog y.

Use of coal is continualy rising for produ cing

electricity. Even, coal is forcasted to replace

the use of oil and natural gas due to its

abundance and aff ordabili ty. With its

cheaper price, coal comes out as a ― new

favourable option of energy source‖ in

fulfilling energy demands. This is suppor ted

by volatili ty of oil price, scarcity of world’ s oil

reserves which upli ft s necessity to seek

alternative energy resources such as coal.

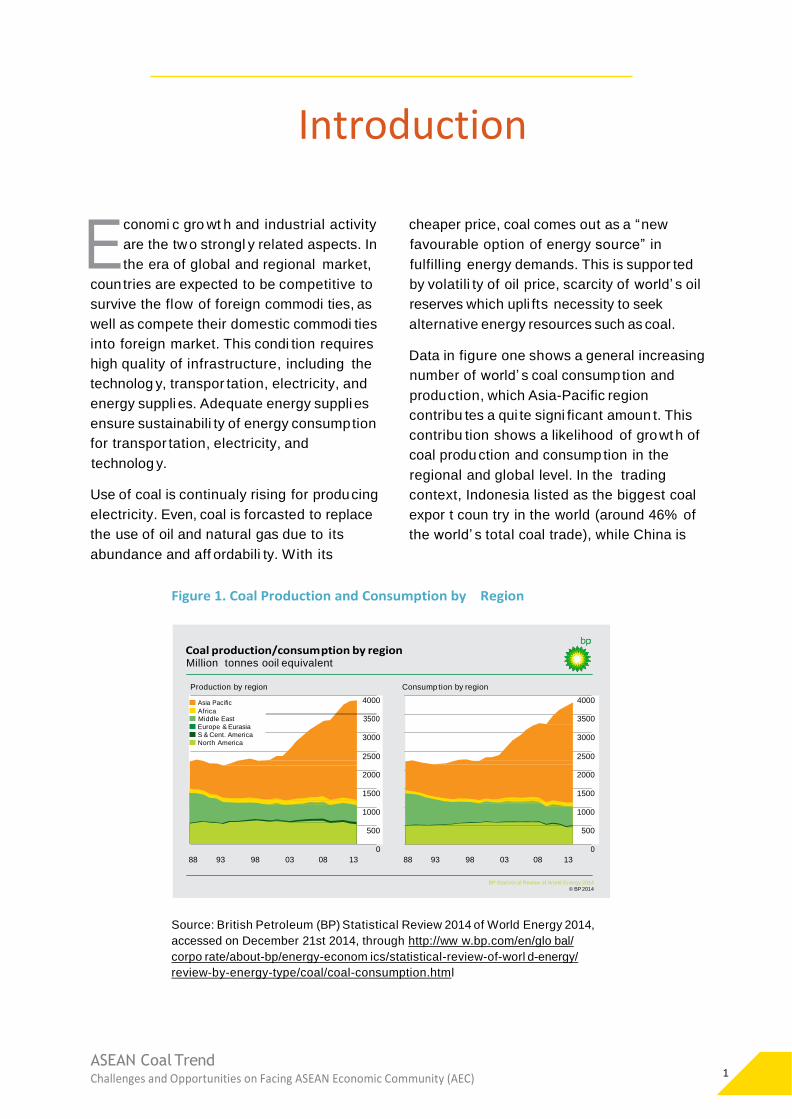

Data in figure one shows a general increasing

number of world’ s coal consump tion and

produ ction, which Asia-Pacific region

contribu tes a qui te signi ficant amoun t. This

contribu tion shows a likelihood of gro wt h of

coal produ ction and consump tion in the

regional and global level. In the trading

context, Indonesia listed as the biggest coal

expor t coun try in the world (around 46% of

the world’ s total coal trade), while China is

Figure 1. Coal Production and Consumption by Region

Source: British Petroleum (BP) Statistical Review 2014 of World Energy 2014,

accessed on December 21st 2014, through http://ww w.bp.com/en/glo bal/

corpo rate/about-bp/energy-econom ics/statistical-review-of-worl d-energy/

review-by-energy-type/coal/coal-consumption.html

Coal production/consum ption by region Million tonnes ooil equivalent

Production by region Consump tion by region

Asia Pacific 4000 4000

Africa Middle East

Europe & Eurasia

S & Cent. America

North America

3500 3500

3000 3000

2500 2500

2000 2000

1500 1500

1000 1000

500 500

0 0

88 93 98 03 08 13 88 93 98 03 08 13

BP Statistical Review of World Energy 2014

© BP 2014

6

the coun try with the highest consump tion of

coal in the world.1

According to figure 1, coal has an abundant

resource and has the securi ty aspects in its

supply. World Energy Outlook predicts that

the global coal demand will gro w by 15% in

2040. The coal main produ cers are China,

India, Indonesia, and Australia. In Asia Pacific,

ASEAN plays signi ficant roles in coal

consump tion and produ ction. Nowadays, in

ASEAN coun tries, with the implementation of

AEC-which will be in place in 2015-, the

economi c gro wt h will stimulates industrial

activities. Then this stimulu s will affects

ASEAN energy consump tion. Furthermore,

ASEAN energy consump tion is forecasted to

rise continously because of the signi ficant

gro wt h of economy and popul ation. These

trajectory will place ASEAN as a key player in

global energy system for now and the

future.2 Although , ASEAN has plenty of

natural resources, ASEAN coun tries are still

relying on energy impor ts. Also, each coun try

individually have different pattern of energy

use.

This paper aims to look on challenges and

oppor tuni ties of coal sector on facing AEC.

This paper will use value chain approach,

good governance, ASEAN framework and

cooperation which is strengh tened through

each coun tries member strategies.

1 BP Statictical Review of World Energy 2014, accessed on

December 21st, 2014 through http://ww w.bp.com/en/

glo bal/corpo rate/about-bp/energy-econom ics/statistical-

review-of- worl d-energy/review-by-energy-type/coal/

coal-consumption.html

2 Maria van der Hoeven, Southeast Asia Energy Outlook,

accessed on December 20th 2014 through htt p://www .

iea. org / publi cat ion s/ f reepubli cat ion s/ publi cat ion /

southeastasiaenergyoutlook_weo2013specialrepor t.pdf

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) 3

V

Coal Trade Pattern and Global Value Chain:

An Overview

alue chain explains set of activities of different produ ction

phases, including the combin ation of physical

transformation and service inpu t from produ cers, the

process of delivering the produ ct to the consumers, and the waste

of using.3 Value chain puts attention to the dynamics of inter-

linkages between produ ction activities which takes further to the

traditional modes of economi cs and social analysis. Moreover, the

full value of a produ ct is regulated in this value chain.

In the case of coal, value chain can be illu strated through the set of

activities of preparation, exploration, management and logistic,

marketing, upgrading and investment. From this set of activities,

exploration, produ ction, management (including governance) and

logistic are the key elements in assuring the value of coal. Next are

marketing, investment, and guarantee towards the sustainable

development of coal and mining usage. This process describes that

investment for the infrastructure impro vement, including rail and

por ts are crucial to deliver and distribu te the end-produ cts. The

simple value chain is shown at Figure 2.

Thus, it is impor tant to determine pattern of current coal trade in

regard to the value chain. It is found that there is no signi ficant

change in the pattern of trade, both in expor ts and impor ts. The

steam coal expor ts is more favourable, compared to cooking and

ligni te. However, the coun tries which produ ce steam coal are still

limi ted.

Figure 2. Value Chain of Coal

Source: Modi fied from various sources

3 Raphael Kaplinsky and Mike Morris, A Handbook for Value Chain Paper, 4.

• Host Coun try:

ASEAN Coun

tries

Preparation: Infrastructure,

Policy,

technolog y

Exploration and

Development

of Product

• Direct Use

• Conversion

• High Quality of

Coal and Mining

(Upgrading)

Management/ Governance

and Logistic

Marketing Investing

• Ensuring Revenue

Transparancy

• Energy Securi ty

• Transpor tation/

delivery/distribu tion

• Intra Trade

ASEAN (based on

AEC)

• Outside ASEAN/

Global Market

• CCTs

• Energy Eff iciency

• Sustainable

development

4

Furthermore, the global steam coal trade

value in 2013, was abou t 1028 Mt, which

pattern of trade is led by the expor ts of coal

steam produ ct from Indonesia (432 Mt),

Australia (182 Mt) and Russia (118 Mt).4 At

the same time, the biggest impor ters come

from China, Japan, India, South Korea,

Chinese Taipei, and Germany. This proves

that the coal trade center is currently heading

to Asia. In 2013, China produ ced 3034 Mt of

coal which assembled it to the 1st position of

coal produ cer coun try, above US (756 Mt),

India (486 Mt), and Indonesia (486 Mt). This

condi tion puts an interesting fact that China

takes both roles as the biggest coal impor ter

Indonesia leads the pattern of coal trade.

Indonesian coal is mostly expor ted to

Philippin es, Myanmar, and Singapore. The

detail of coal and mining trade intra ASEAN is

described in the table 2

The data in the table 2, shows that coal and

mining trade intra ASEAN is potential to be

explored. Producer coun tries will have the

chance to maximize the intra ASEAN market

through bilateral trade or AEC framework.

For instance, Thailand is repor ted to produ ce

approximately 1,372 Million Ton coal per year

(2009). However, the produ ced coal is

categorized as ligni te to sub bituminou s coal,

as well as the biggest coal produ cer. which is a low quality coal.5 This situation

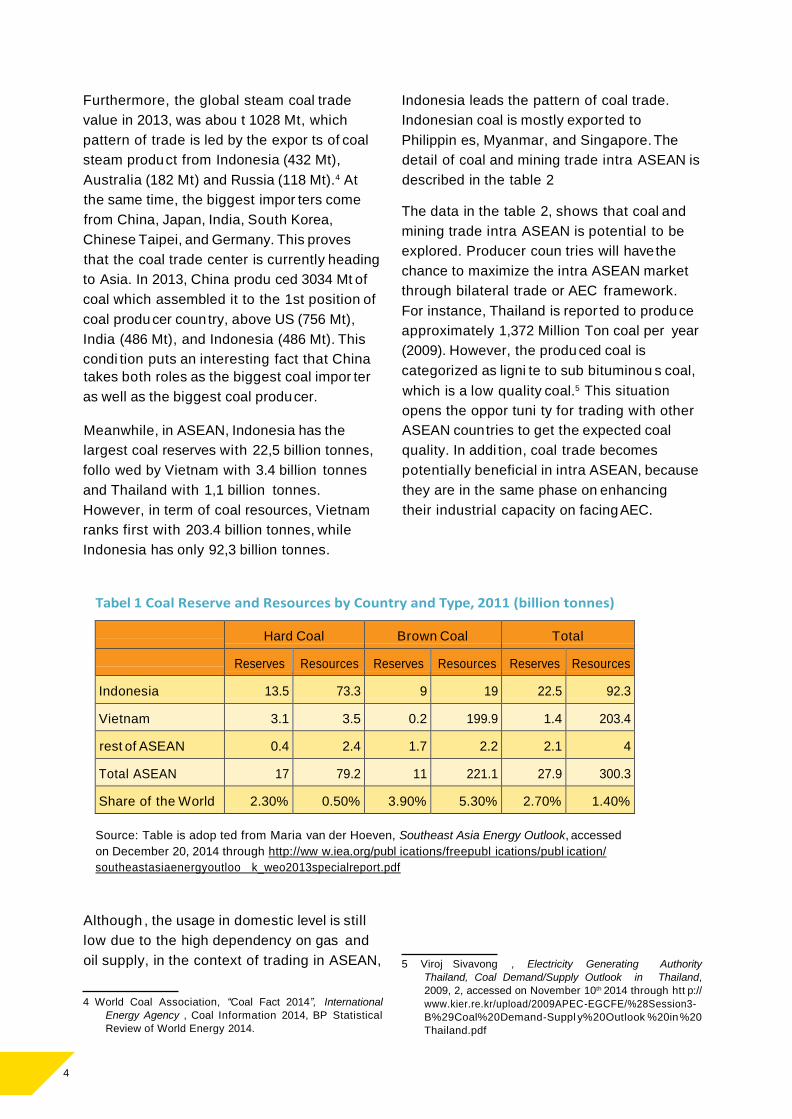

Meanwhile, in ASEAN, Indonesia has the

largest coal reserves with 22,5 billion tonnes,

follo wed by Vietnam with 3.4 billion tonnes

and Thailand with 1,1 billion tonnes.

However, in term of coal resources, Vietnam

ranks first with 203.4 billion tonnes, while

Indonesia has only 92,3 billion tonnes.

opens the oppor tuni ty for trading with other

ASEAN coun tries to get the expected coal

quality. In addi tion, coal trade becomes

potentially beneficial in intra ASEAN, because

they are in the same phase on enhancing

their industrial capacity on facing AEC.

Tabel 1 Coal Reserve and Resources by Country and Type, 2011 (billion tonnes)

Hard Coal Brown Coal Total

Reserves Resources Reserves Resources Reserves Resources

Indonesia 13.5 73.3 9 19 22.5 92.3

Vietnam 3.1 3.5 0.2 199.9 1.4 203.4

rest of ASEAN 0.4 2.4 1.7 2.2 2.1 4

Total ASEAN 17 79.2 11 221.1 27.9 300.3

Share of the World 2.30% 0.50% 3.90% 5.30% 2.70% 1.40%

Source: Table is adop ted from Maria van der Hoeven, Southeast Asia Energy Outlook, accessed

on December 20, 2014 through http://ww w.iea.org/publ ications/freepubl ications/publ ication/

southeastasiaenergyoutloo k_weo2013specialreport.pdf

Although , the usage in domestic level is still

low due to the high dependency on gas and

oil supply, in the context of trading in ASEAN,

4 World Coal Association, “Coal Fact 2014”, International

Energy Agency , Coal Information 2014, BP Statistical

Review of World Energy 2014.

5 Viroj Sivavong , Electricity Generating Authority

Thailand, Coal Demand/Supply Outlook in Thailand,

2009, 2, accessed on November 10th 2014 through htt p://

www.kier.re.kr/upload/2009APEC-EGCFE/%28Session3-

B%29Coal%20Demand-Suppl y%20Outlook %20in %20

Thailand.pdf

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) 5

Table 2 Export-Import on Mine & Coal Intra ASEAN 2013 (in USD)

Country Brunei

Darussalam

Cambodi a

Indonesia

Lao PDR

Malaysia

Myanmar

Phillippin es

Singapore

Thailand

Vietnam

Brunei Mining 531.195.045 370.727.641 - 73.860.279 378.122.631 466.747.623 593.266.643

Coal Cambodia Mining 522.537 1.184 16 1.004 749.477 2.673.466 42.336.525

Coal 19.006.068 1.246.633.530 - 802.148.711 28.934.970 962.556.934 117.701.068

Indonesia Mining 10.946.750 22.177.064 15.434 5.279.104.587 84.376.438 1.609.142.244 6.788.530.765 2.303.483.460 368.384.679

Coal 21.511.813 1.136.928.627 1.546.249 1.007.207.109 19.608.561.066 834.864.654 130.606.674 755.000

Lao PDR Mining 3.122.743 733.697 - - 704.231.954 102.806.500

Coal - - - 497.580 16.497.799 876.926 Malaysia Mining 249.025.497 10.399.660 4.837.167.607 153.689 226.842.937 461.976.182 10.650.869.362 2.800.851.009 751.037.765

Coal 173.109 504.999 - 25.945.558 5.518.537 Myanmar Mining 15.136.482 - 733.482 727.253 117.896.275 3.765.764.484 49.120

Coal - - 799.200 Philippin es Mining 1.412.272 183.223 189.796.451 5.141 303.945.904 1.521.561 444.319.340 178.005.850 32.408.726

Coal 2.362 13.201.200 66.278.084 31.747 361.236 2.262.000 16.794.594 263.395.991 89.653.832

Singapore Mining 103.048.201 580.590.615 15.955.904.738 104.223 20.418.909.369 780.488.527 1.140.933.034 1.086.288.936 2.559.611.766

Coal 3.506 264.704 206.286 112.869 32.933 Thailand Mining 21.037.629 997.766.847 979.352.633 1.345.661.415 2.702.160.901 740.171.772 671.166.580 3.856.884.031 973.621.382

Coal 1.742 81.497 6.684 474.358 232.001 14.062 21.961 Vietnam Mining 621.687 1.363.956.350 464.294.156 244.760.576 1.231.615.244 66.125.090 239.662.441 383.614.651 460.642.517 Coal 750 4.147.504 10.963.990 23.836.954 12.326.804 835.221.845 16.160.492

Source : ASEAN Stats Database based on the ASEAN coun tries’ repor t, accessed by request to the ASEAN

Stats Database Off icer in 2014

Nevertheless, several ASEAN coun tries only place coal as minor

commodi ty on their whole intra ASEAN expor t. Reserving the coal

for their own purpo se is the essential factor of their acts, because

they already have high domestic energy demands for industries and

electricity, such as Laos and Vietnam. That’s why then some other

coun tries with limi ted coal resource needs to impor t from other

coun tries, while based on its proximi ty, neighbouring impor ter

from ASEAN is an att ractive option. Malaysia is one sample of coal

produ cer in ASEAN which produ ces coal, but still needs coal supply

from impor ts. It happens since Malaysia can only produ ce 1 million

tons per year, while its coal demand is abou t 30 million tons per

year.6 Thus, Malaysia should impor ts coal from ASEAN coun tries,

especially from Indonesia which is now recognized as reliable

source of Malaysian primary energy.7

6 IEA Clean Coal Centre, htt p://www .iea-coal.org/documents/82373/7605/Prospects-for-

coal-and-clean-coal-technologi es-in-Malaysia-%28CCC/171%29

7 Ibid.

6

Table 3. ASEAN Mine and Coal Trade 2010 – 2013 (USD)8

Year 2010 2011 2012 2013

Coun try E I E I E I E I

Brunei Darussalam 818.450.727 287.302.215 1.429.178.511 413.557.339 1.248.681.128 551.270.625 2.413.919.861 407.612.209

Cambodi a 6.477.649 1.736.181.566 1.272.968 2.532.482.403 4.999.898 2.747.191.945 3.223.265.489 2.992.941.773

Indonesia 15.622.651.672 18.544.618.722 15.317.893.317 20.552.598.175 21.621.354.440 21.328.473.993 39.208.142.614 23.073.252.218

Lao PDR 889.808.661 863.559.029 712.239.553 1.129.360.367 620.958.285 1.445.296.146 8.282.767.199 2.752.178.450

Malaysia 12.729.699.087 22.158.194.175 14.535.309.602 28.935.047.677 17.728.160.664 31.122.993.454 20.020.465.911 31.556.817.894

Myanmar 2.963.400.096 2.008.252.380 2.945.464.591 1.001.307.797 2.268.839.598 1.358.840.844 3.901.106.297 2.921.336.316

Phillippin es 972.203.554 5.476.287.895 1.298.606.006 5.276.410.303 828.685.216 5.082.631.287 1.796.276.353 25.662.595.508

Singapore 36.900.984.567 15.162.277.865 44.605.001.469 16.814.626.185 44.769.653.129 23.887.909.044 42.626.499.706 23.535.038.241

Thailand 7.804.496.361 10.465.497.274 11.307.853.909 11.973.504.100 12.299.508.276 11.849.134.052 12.288.800.705 13.131.789.570

Vietnam 3.662.483.628 5.668.484.811 4.279.796.783 7.696.818.404 4.686.403.623 6.703.502.867 5.357.951.051 5.631.633.006

Source : ASEAN Stats Database based on the ASEAN

coun tries’ repor t, accessed by request to the ASEAN

Stats Database Off icer in 2014

The table 3 above explains that since 2010

until 2013, during the period when 3rd APAEC

Plan is implemented, the expor ts of coal and

mining rise signi ficantly on some ASEAN

coun tries. It further provides the evidence

that the impor t also faces some gains. This

phenomena suggest that the upcoming

ASEAN Economi c Communi ty fosters the

integrated market of ASEAN, as well as

building awareness of ASEAN coun tries to

develop their infrastructure in energy

suff iciency for electricity and industrial

activities.

The impact of ASEAN market integration

opens the door for foreign companies to

invest and conduct the coal and mining

exploration in ASEAN coun tries. In 2013, the

Government of Cambodi a repor ted that the

company which has licensed to do the

exploration activities was 91, consisted of

domestic and foreign companies.9 The

companies contribu ted in exploration in

Cambodi a were from Australia, China,

Thailand, and Vietnam.

Nevertheless, it should be noted that foreign

investment is one of impor tant factors not

only for the development of coal and mining

industry, but also for the development of

eco-friendly coal and mining industry. It

corresponds with the usage of clean coal

technolog y which also needs the investment

for the technolog y installation and other

related process. Thus, the international

cooperation has to be realized equally in

investment, technolog y, and human

resources.

8 This data is measured on follo wing kinds of resource :

Mining (iron and steel; articles of iron and steel; ores,

slag, and ash; copper and articles thereof; alumunium

and articles thereof; lead and articles thereof; zinc

and articles thereof; tin and articles thereof) and Coal

(anthracite coal not agglom erated; bituminou s coal not

agglom erated; other coal not agglom erated; briqu ettes,

ovoids, similar solid fuels from coal).

9 Chrea Vichett, Current Situation of Mining Industry in

Cambodia, General Department of Mineral Resources of

Cambodi a, 2013.

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) 7

A

ASEAN Economic Community:

The Way towards Integration

SEAN Economi c Communi ty (AEC) is one of three pillars

that designed to implement the establishment of ASEAN

Communi ty by 2015. The idea of ASEAN Communi ty 2015

formation was made through the Summi t in Kuala Lumpur ,

Malaysia, in 1997 which agreed upon the ASEAN Vision 2020,

aimed to create a stable and competitive region, and balanced

economi c development. Nevertheless, during the Summi t in 2003,

ASEAN Vision 2020 was accelerated to 2015. There are tw o main

reasons why the establishment of ASEAN Communi ty is fast-

tracked. 10 First, the increasing influence and competition of China

towards the region. Second, the rise of economi c integration in

various regions in the world withou t ASEAN participation.

AEC is expected to work in cooperation with ASEAN Socio-Cultural

Communi ty and ASEAN Poli tical Securi ty Communi ty in succeeding

the ASEAN Communi ty.11 The aims of AEC itself is to achieve higher

level of economi c dynamism, sustained prosperity, inclusive

gro wt h, and integrated development of ASEAN by realizing the

increasing interdependence amidst ASEAN coun tries. Three key

characteristics of AEC are as follo w, (1) Single Market and

Production Base; (2) Competitive Economi c Region; and (3)

Equi table Economi c Development. These poin ts, highligh t the

implementation of agreement in which the signatories will be able

to trade and invest optimally with the intra region partner.

However, there are pros and cons toward the AEC. The pros often

view that AEC can stimulate the intra ASEAN trade, in which

provide the strengthening integrated market of ASEAN. On the

other hand, like every classic cons toward market integration, the

concern revolves around , the ― wide-opened door ‖ of market

which may result the tigh t competition and put the domestic

commodi ties into danger.

Despite debates on postitive and negative view towards AEC, the

suppor ts for AEC can be indicated using the AEC Scorecard

achievements. Based on AEC Scorecard data in 2011, from 277 sizes

10 Justyna Szczudlik -Tatar, ― Regionalism in East Asia: A Bumpy Road to Asia Integration,‖

Policy Paper No. 16, (2013), 3.

11 ASEAN Economi c Communi ty Blueprin t, (ASEAN Secretariat, 2008), 5, accessed on

November 20th 2014 through http://ww w.asean.org/archive/5187-10.pdf

8

of expected liberalisation, ASEAN has done

187 or abou t 67,9% of them. In 2014, that

percentage gro ws to 82,1%.12 Clearly, it

describes the common eff orts of ASEAN

coun tries in realizing ASEAN liberalization

and integration through AEC.13

The AEC implementation not only elimin ates

tariffs on trade and free flow of investment,

but also discusses the agremeent upon the

energy and mining . Exclusively in poin t B4,

the energy aspect is mentioned, as part of

AEC to-do list to promo te the infastructure

development, involving the completion of

energy and mining cooperation.14 The energy

cooperation, including the coal and mining is

regulated in AEC Blueprin t Article 53-56

which explicitly put the energy securi ty and

strengthening trade and investment in

energy as the common goals.15 Meanwhile,

the framework of trade coal and mining

trade cooperation appeares on the formation

of ASEAN Forum on Coal (AFOC) in 1999

which is a transformation of Coal Sub-Sector

Netw ork, previously buil t under the ASEAN

Energy Cooperation Program.

It is agreed that the regional energy policy

which enables the fulfillment of those goals,

is required. This is to ensure implementation

of the AEC goals as a single market and

produ ction base, a highl y competitive

economi c region, a region of equi table

economi c development, and a region fully

integrated into the global economy by 2015.

APAEC 2010-2015 mentions that the energy

policy agenda of the AEC is targeted to

acquire these follo wing ultimate objectives:16

1) to ensure a secure and reliable supply of

energy including , bio-fuel, which is crucial to

suppor t and sustain economi c and industrial

activities; 2) to expedite the development of

ASEAN Power Grid (APG) and the Trans-

ASEAN Gas Pipeline (TAGP) which allo w the

optimization of the region’ s energy resources

for greater securi ty and provide oppor tuni ties

for private sector involvement in terms of

investment, including financing and

technolog y transfer. Integrated netw orks of

electricity and gas pipelines offer signi ficant

benefits both in terms of securi ty, flexibili ty,

and quality of energy supply; 3) to ensure

sustainable energy development, through

mitigating greenhouse gas emission by means

of effective policies and measures, among

others; and 4) to strengthen renewable

energy development, such as, bio-fuels, as

well as to promo te open trade, facili tation

and cooperation in the renewable energy

sector and related industries as well as

investment in the requisite infrastructure for

renewable energy development.

12 The 12th AEC Council Meeting, August 26, 2014 accessed

on December 28th , 2014, through http://ditjenkp i.

kemendag.go.id/website_kpi/index.php?modu le=news_

detail& news_content_id=1501&detail=true

13 ASEAN Economi c Communi ty Scorecard: Charting

Progress Toward Regional Economi c Integration Phase

1 (2008-2009) and Phase II (2010-2011) accessed on

November 23rd 2014, through http://ww w10.iadb.org/

intal/intalcdi/PE/2012/10132.pdf

14 Ibid., 20

15 ASEAN Economi c Commnui ty Blueprin t, ASEAN

Secretariat, 2008. Accessed on November 23rd 2014,

through http://ww w.asean.org/archive/5187-10.pdf

16 ASEAN Plan of Action for Energy Cooperation, 2, accessed

on November 10th 2014, through http://aseanenergy.

org/media/filemanager/2012/10/11/f/i/file_1.pdf

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) 9

Coal Trends and the Readines of ASEAN Countries on Facing the AEC

Coal Prospects in ASEAN Region

ASEAN can be recognized as a region with adequate energy

sources, especially in coal produ ction. Geographically, ASEAN

coun tries remains in the land inherited with coal and mining

resources. This is proven by the latest repor t which shows that

almost every coun try in ASEAN has the self-capacity to supply its

energy demands, where the government of each coun try takes the

biggest part. Like what Vietnam does by optimizing the role of

Vinacom, the state-owned enterprise, to operate the coal

extraction 100%.17 Vinacom also responsibles to control the coal

produ ction, with the aims to secure the coal reserve. In 2001-2005,

Vietnam faced a fast gro wing coal produ ction which was

considerable as a threat to domestic reserve. However, this fast

gro wt h were sucessfully managed by the authori ty of the

government for the domestic reserve reason.18

Chart 1. Percentage of Growth Averages of Primary Energy Demand in

Selected ASEAN Countries by fuel (Mtoe) 2011-2035

Source: Data are based on Maria van der Hoeven, Southeast Asia Energy Outlook,

accessed on December 20th 2014 through http://ww w.iea.org/publ ications/

freepubl ications/publ ication/southeastasiaenergyoutloo k_weo2013specialreport.pdf

17 Global Methane Ini tiative accessed on December 12, 2014 through htt ps://www .

globalmethane.org/documents/toolsres_coal_overview_ch37.pdf

18 Ibid.

60

50

40

30

20

10

Coal

Oil

Gas

Hydro

Bio Energy

Other RE 0

Indonesia Thailand Phillipin es Malaysia -10

10

In the case of Indonesia, the coal prospect is

high and predicted to sustain until 2035.19

Indonesian coal produ ction takes 85% of

produ ction in ASEAN which places Indonesia

as the biggest coal expor ter in the world. The

value of Indonesian coal resource is 120,53

Billion Ton and the reserve is 31,36 Billion

Ton, contribu tes only 6% of the world’ s total

coal reserve.20

Indonesia is also repor ted as the largest

energy consumer in ASEAN, follo wed by

Thailand and Malaysia on the second and

third place. Nonetheless, its domestic

consump tion is lower than Indonesian coal

expor t. This situation leads to the

dependency and the mul tiply oil impor t value

of Indonesia, even the whole ASEAN.

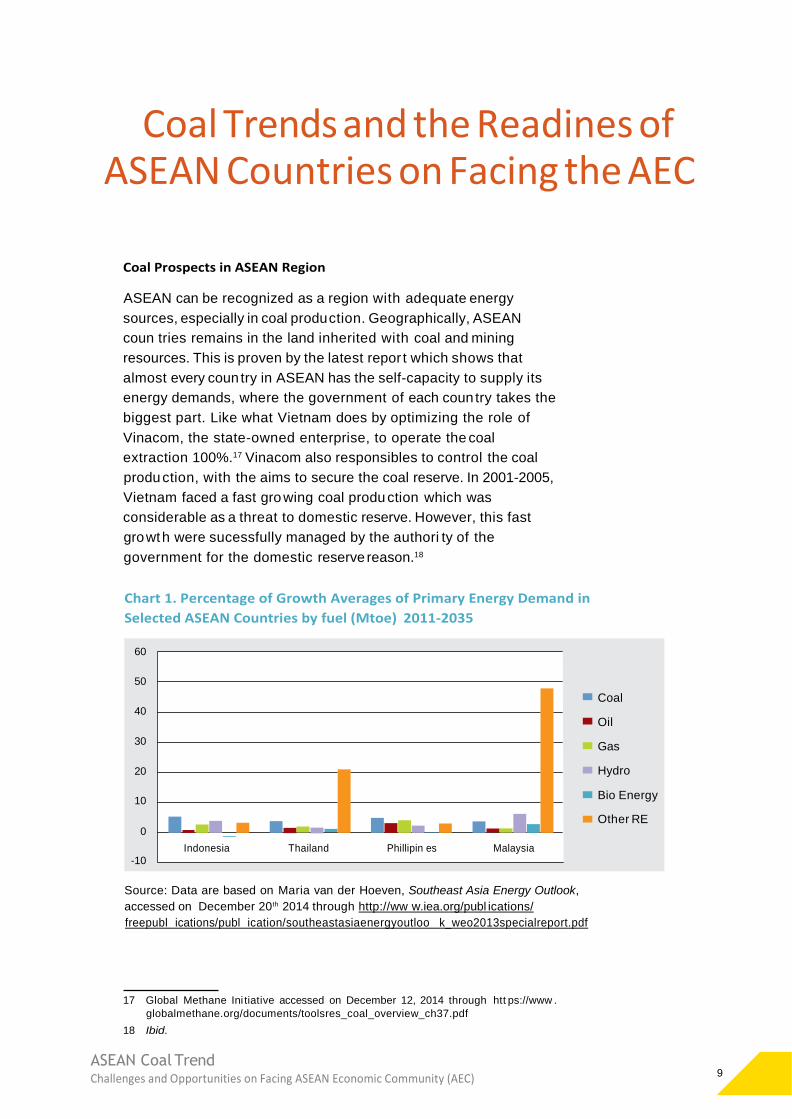

In other hand, the gro wt h averages of energy

demand including coal of four of the larger

ASEAN coun tries in 2011-2035 are very

diversified. The gro wt h of demand for coal

will occur in each coun try with percentage

around 5.5% to 3.9% (Chart 1).21 In

meantime, the highest gro wt h of demand for

oil and gas will occur in Philipin es , while for

hydro, bio-energy and other renewable

energy, Malaysia will positioned as the

coun try with the highest gro wt h of demand

for these kind of energy.

Coal prospects in ASEAN seems to be qui te

high, as electricity in ASEAN still uses coal as

the source, and electricity plays an impor tant

role not only in daily uses but also in

succeeding the industrial activities. It’s

suppor ted by the fact that though some

coun tries have the abundant resources of

coal and mining , the quality of the

commodi ties are somehow distinct from one

place to another.

The current condi tions above indicates tw o

impor tant things. First, the coal produ ction in

ASEAN will still be leant on Indonesia as the

main expor ter in ASEAN. Second, the

alternative way to use coal as the fuel of

choice gives the prospect upon the coal trade

value both intra ASEAN, and outside the

region.

19 Maria van der Hoeven, Op.Cit.

20 BP Statistical Review of Energy 2013.

21 Maria van der Hoeven, Op.Cit.

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) 11

T

ASEAN Energy Policy

Strategy Action

1. Development of Energy Eff iciency

Policy and Build Capacity

1. Develop a clear policy and plan to promo te energy eff iciency.

2. Sett ing national energy eff iciency target and develop a plan to moni tor the

results.

3. Strengthen human capacity and enhance infrastructure to facili tate the EE

policy and plan.

2. Awareness raising and

dissemination of information

1. Develop and run EE&C campaigns to raise awareness, emphasizing on global

environm ental issues

2. Disseminate information using all appropri ate medias (including energy

labels) to help energy consumers make a righ t decision

3. Demonstrate best energy practices and successful cases, e.g, publi c-private

sector collaboration on EE&C

3. Promo ting good energy

management practices, especially

for industrial and commercial

sectors

1. Develop regulation and / or provide incentives to encourage good energy

management practices in facili ties

2. Build up capacity for all stakeholders to implement good energy

management

4. Facili tation of Energy Eff iciency

Financing

1. Develop mechanism (s) to enhance financing for energy eff iciency and

conservation project implementation

2. Increase involvement of banking sector and financial institutes both domestic

and international agencies in financing energy eff iciency projects

he upcoming AEC cause the economi c

gro wt h of ASEAN coun tries as the intra

ASEAN trade opens the oppor tuni ty of

all commodi ties to pass through the other

coun tries in region with no bound aries. This

economi c gro wt h is follo wed by the massive

industrial activities in ASEAN coun tries which

is undeniably increasing. In purpo se to fulfil

the market demand, the suff icient energy

sources (such as oil, coal, and gas) are

needed, so that the industrial activities are

conducted properly.

Regarding the huge energy needs, ASEAN

creates the common ini tiation for energy,

called ASEAN Centre for Energy (ACE) to

deepen the energy cooperation among

ASEAN coun tries. A factual plan of ACE is

ASEAN Plan of Action for Energy Cooperation

(APAEC). APAEC aims to achieve the energy

securi ty and the sustainable of ASEAN in

health and environm ent through the further

utilization of Clean Coal Technolog y. Not

limi ted to that, APAEC also poin ts to facili tate

the coal trade in ASEAN within the advance

regional energy securi ty. APAEC has been

done in 3 periods, which is 1999-2004, 2005-

2009, 2010-2015. The tw o latest plans are

made to accompli sh the ASEAN’s energy

needs which is forecasted to doubl e from

2005 to 2030 along with the implementation

of AEC.22

In terms of coal, the existence of APAEC is

expected to promo te coal and clean coal

technolog y, also foster the intra-ASEAN coal

trade an investment for the regional energy

securi ty. These plans are implemented

through the ownership of AFOC under the

ACE supervision as the secretariat, which

involves the off icials of Ministry of Energy

from ASEAN coun tries. Each year, AFOC holds

a meeting to receive each ASEAN coun try’s

repor t on the mining and coal reserve and

22 Ibid.

12

trade. This kind of meeting is advantageous

to picture the challenges of mining and coal

trade intra ASEAN, share abou t the energy

needs, and suspect the potential partner for

trade.

On this stage, the existence of ACE

acommod ate the grand framework for the

ASEAN coun tries, related to the aspects that

are impor tant to be done, such us the use of

clean coal technolog y and building of coal

power plant. The cooperation made under

the ACE gives the guidance for each coun try

to formul ate the national energy policy

which is harmoni zed with the regional goal.

The policy in regional level agreed in 2009 for

example, elaborates tw o impor tant aspects:

the pursue of reducing regional intensity of

at least 8% by 2015, based on 2005 level

(under Program Area No. 4 Energy Eff iciency

and Cooperation); and the eff ort to achieve a

collective target of 15% for regional

renewable energy in total power installed

capacity by 2015 (under Program Area No.6

Renewable Energy).23

The ultimate progr ams in regional level are :

buiding of an ASEAN coal image,

development of ASEAN Coal Price Index,

sett ing up coal laboratory and standards,

promo te intra ASEAN coal trade by

facili tating bilateral and mul tilateral long

term coal supply agreement, formul ater an

MOU similar to ASEAN Petroleum Securi ty

Agreement to enhance regional and securi ty

of coal supply, and developemnt of strategy/

action towards harmoni zation of local

practices to encourage coal trading and

sharing of resources and facili ties.24 These

progr ams aff irms the ASEAN attempt to build

a commi tment in undertaking energy

probl em.

23 Energy Management Policy in Indonesia and ASEAN,

presentation for Workshop for ASEAN Coal Database

and Information System 9-12 July 2012, accessed on

December 10th 2014 through http://ww w.aseanenergy.

org/media/documents/2012/08/03/f/i/file_2.pdf

24 ASEAN Plan of Action for Energy Cooperation (APAEC

2010-2015), Op.Cit.

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) 13

A

ASEAN Countries Strategy

SEAN coun tries highligh t aseveral

impor tant things related to energy,

such as suff icient domestic energy

fulfillment, fair and stable energy pricing, the

exploration of sources within the terri tory,

energy eff iciency and conservation, and the

environm ental impacts. In general, it can be

said that the energy policy of each coun try in

ASEAN has a lot of things in common , which

provides the space of building further

regional coooperation in managing energy

features.

Specifically in coal aspects, intra trade coal

has been regulated in the Programme Area

No.3 through the establishment of AFOC.

Along with AEC, AFOC works to create the

guidelines of coal specifications, produ cers,

and consumers in ASEAN, as well as organise

a netw ork of coal laboratories in ASEAN to

harmoni se standards of coal analysis, to

enhance the intra trade coal.25 Nevertheless,

with regard to different capacity of coal

produ ction, each coun try in ASEAN

implements different kind of policy related to

its domestic needs and goals. The different

kind of policy is sometimes also affected by

the resource reserve and resource capacity

constraint. Coun tries with the abundant

resources of coal and mining , such as

Indonesia and Malaysia relatively trade their

coal resource with other coun tries in the

region more than coun tries which resource is

less. In addi tion, the different energy policy is

reflected on the energy trade decision. For

example, the energy policy of Laos to not

expor t its coal produ ction and reserve all

types of coal for supplying its high domestic

consump tion.

On the other hand, Singapore as the coun try

with insuff icient energi resources, is highl y

dependent to the impor t of energy. It puts

Singapore in the fragile position under the

dynamic of energy suppli es. In purpo se to

face this condi tion, one of the implemented

policy is by enhancing the enegy eff iciency

within Energy Conservation Act 2013.26 This

agenda meets the energy policy in ASEAN

which considers the eff icient and clean

energy as a crucial issue to ensure the energy

reserve and sustainabili ty in ASEAN. On the

other hand, similar with Singapore,

Philippin es also concerns abou t impro ving the

energy eff iciency consump tion. Although it’s

recorder as the second biggest geothermal

produ cer in the world, Philippin es is still

dependent on the impor t of energy. This

makes a ground for Philippin es to focus in

eff iciency energy and domestic energy access

assurance.

The different natural resources ownership

which causes to the various policies, becomes

the justification to maximize the energy

policy in ASEAN. This accompli shment foster

the energy supply and sustainabili ty, as well

the domestic energy policy of each ASEAN

coun try.

25 ― Programme Area No.3 ‖ , accessed on December 10th

2014 through ASEAN Secretariat Website http://ww w.

asean.org/news/item/prog ramme-area-no-3-coal

26 ― Singapore: Energy Eff iciency in the Industry‖, accessed

on accessed on December 23rd, 2014 through http://ww w.

sgc.org.sg/f ileadmi n/ahk_singapur/DEinternational/IR/

diffIR/Energy_Efficiency_in_the_Industry_June_2014.pdf

14

T

Clean and Efficient Coal use in ASEAN:

The Economic Benefit

he abundant resource and competitive

price of coal, put coal as the

considerable energy option. It’s

forecasted that the use of coal will steadily

rise and reach to 58% in 2035, in business as

usual scheme. On the other hand, coal is one

of the primary environm ental pollu ters. Large

number of coal requires a good arrangement

as the environm ental responsibili ty and the

eff ort in maximizing sustainable economi c

benefit. ASEAN needs to create clean and

eff icient coal technolog y which costs much

and capable human resources to operate the

technolog y optimally. With regard to coal as

a future energy alternative, it demands not

only the ASEAN coun tries interests to secure

the coal reserve, development, and

sustainabili ty, but also the contribu tion of

developed coun tries to assist the funding and

impro ving ASEAN human resources which

orientation is up to clean and coal technolog y

development.

A technolog y which is introduced to be the

solu tion upon the environ tmetal effect of

coal usage is Clean Coal Technologi es (CCTs).

According to Shi and Jacobs,

― CCTs cover technologi es ranging from the

perspectives of coal through combustion

and the clean up of waste gases to carbon

capture and storage (CCS), will reduce the

pollu tion emission intensity of coal and

make coal cleaner.‖ 27

27 Xunpeng Shi and Brett Jacobs, Clean Coal Technologies in

Developing Countries, accessed on December 23rd 2014,

through http://ww w.eastasiaforu m.org/2012/09/25/

clean-coal-technolog ies-in-developin g-countries/ Details

see also, Xunpeng Shi,China’s Attempts to Minimize non-

CO2 Emissions from Coal: Evidence of Declining

Emission Intensity, Environment and Development

Economics 16. (2011): 573-590.

They also argue that the development and

application of clean coal technologi es (CCTs)

are believed not only as the key to reconciling

the tensions between coal use and the

environm ent, but also the economi c benefit,

as they noted,

― While CCTs typically incur addi tional costs,

they can also pr ovide econom ic benefits in

addi tion to environm ental ones. For

example, Integrated coal Gasification

Combin ed Cycle power plant technolog y

can increase eff iciencies by 20–30 per cent

compared with conventional coal-fired

power plants; the captured carbon dioxide

from CCS power plants can be injected into

oil fields to increase the oil recovery rate by

4–18 per cent; and carbon storage

technologi es, such as the creation of bio-

charcoal, can impro ve soil fertili ty,

agricultural produ ctivity and water quality.

CCTs can also bring new expor t

oppor tuni ties for developing coun tries.

Upgraded low-rank coal — such as bro wn

coal in Indonesia, which has had no

previous market — may develop expor t

oppor tuni ties clean and eff icient coal

technolog y. ‖ 28

In addi tion, the World Energy Repor t 2013

explains that energy eff iciency through the

oil impor t reduction and the alternative to

coal and natural gas will provide economi c

gains to ASEAN. This will increase the ASEAN

coun tries’ impor t cost savings that eventually

contribu te to the rise of Regional GDP of

abou t 2% (chart 2). 29 The same

argumentation will also justify the necessity

of coal usage eff iciency to give the

sustainable economi c gains in the future.

28 Ibid.

29 Maria van der Hoeven, Op.Cit

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) 15

Chart 2 Economic Gains on Energy Efficiency

Source: Chart is adop ted from Xunpeng Shi and Brett Jacobs, Clean Coal Technologies

in Developing Countries, accessed on December 23rd 2014, through http://ww w.

eastasiaforu m.org/2012/09/25/clean-coal-technolog ies-in-developin g-countries/

In ASEAN, the implementation of CCTs was

arranged during the Ministerial Statement

(JMS) at the 32nd ASEAN Energy Meeting

(AMEM) on September 23rd, 2014 in

Vientiane, Lao People’s Democratic Republi c.

In the attempt of CCTs implementation, the

cooperation with dialogue partners (Japan,

China, and Korea) is fostered, especially in

the technolog y development and funding .

The implementation of APAEC shows its

contribu tion to coun try’s awareness abou t

the energy reserve, like what Indonesia

experienced in 2010 to 2013. Indonesia

gained its coal reserve from 21,13 in 2010 to

31,36 Billion Ton in 2013.30 Indonesia is also

affected by the APAEC plan in realizing the

clean coal technolog y as Indonesia’s coal long

term strategy.

30 ― Coun try Repor ts Updates of Indonesia‖, Ministry of

Energy and Mineral Resources, delivered in 12th AFOC

Meeting, Thailand, 21-22 May 2014.

Gains in fossil-fuel trade balances Increase in GDP

35 200 2.5%

30 160 2.0%

25

20 120 1.5%

15 80 1.0%

10

40 0.5% 5

Coal Gas Oil

Addi tional Impor t cost expor trevenue savings

2020

Change

in GDP

2025 2030 2035

Percentage change in GDP (righ t axis)

Billio

n d

oll

ars

(20

12)

Billio

n d

oll

ars

(20

12)

16

A

Challenges and Opportunities of Coal Sector on Facing AEC

ccording to the value chain and

overview explanation above, to arrive

at the answer of prospect of coal

value chain of mining and coal trade in

ASEAN, the paper should be determined to

several factors which affected the flow of

produ ction and trade, such as the trend of

trade, the technolog y, governance,

transpor tation and connectivity, and

defini tely the ASEAN energy policy. These

factors are examined with the consideration

of upcoming ASEAN Economi c Communi ty.

First, the trend of trade. Oil used to be the

major resource consumed by the ASEAN

coun tries. However, as the reserve of oil in

ASEAN is being depleted, coal appears as

another possible resource to explore. Based

on the data of ASEAN energy outlook during

the 1999 to 2007, the coal is an energy source

that has the fastest gro wt h. The high demand

of coal is the result of the larger number of

coal-fired power plant installation all over

ASEAN coun tries. The consump tion of coal is

projected to increase approximately 7.7% per

year from 2007 to 2030, due to the power

plant installment and industries. The trend of

coal and mining is further explained by the

increasing amoun t of intra ASEAN Trade31 on

coal and mining sector in 2010 that doubl ed

in 2013 and reached more than 11 billion US

Dollar in balance.

This situation proves that the energy

consump tion in ASEAN is gett ing higher as

well as the demand of coal in the region,

when the time is gett ing closer to the AEC

implementation. It also guarantees the

continuation of value chain in terms of supply

31 Both in expor t and impor t

and demand, because while the coal and

mining are continuou sly produ ced, the

demand is coming again and again.

Second, the technolog y, governance,

transpor tation, and connectivity. This four

aspects are interlink ed to the success of

produ ction, since the value chain stresses on

the flow of produ ction, which involves the

easy access of modern technolog y and

distribu tion. The modern technolog y

development is needed by the coun tries to

cultivate the energy produ ction. The more

sophisticated the technolog y, the produ ction

will be more eff icient and resulting the high

quality. However it’s buil t widely vary across

the coun tries, as Myanmar and Cambodi a still

has limi ted access to modern technolog y

while Singapore has reached 100 percent of

access.32 This triggers some coun tries in

ASEAN, which Government and state-owned

company unable to build high-technolog y to

manufacture the coal and mining materials,

to open the oppor tuni ty for foreign

companies to explore the mining and coal

within their land under specific regulations

and permission.

Since coal is claimed as the preferable energy

source than oil for its cheaper price and

flexibili ty to be distribu ted, the probl em no

longer spins around the coal as a material.

The challenge occurs on how fast and how

easy the coal is carried from the produ cer to

the consumer, for example from Indonesia to

Cambodi a. According to the nature of market

integration, the border restraint gradually

32 Hanan Nugroho , ― ASEAN Energy Cooperation: Facts and

Challenges‖, Jakarta Post May 19th 2011, accessed on

December 11th 2014 through http://ww w.thejakartapost.

com/news/2011/05/19/asean-energy-cooperation-facts-

and-challenges.html

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) 17

perishes as the AEC is appro aching , which

means the less cost for coal trade intra region.

Governance is the inseparable key element of

value chain. Regarding the attempt to build a

global and regional value chain, domestic

policy (including the added-value of coal and

mining process) becomes so essential. The

governance issue is also related to the

revenue transpor tation which is collected

from the coal and mining industry. Resources

Governance Index (RGI) which measures the

quality of governance in the oil, gas and

mining sector of 58 coun tries by looking at

four key areas of transparency and

accoun tabili ty such as institutional and legal

sett ing, repor ting practices of government

disclosure of information, the presence and

quality of checks and oversigh t mechanisms

that encourage integri ty and guard against

conflicts of interest, the broader governance

environm ent, based on more than 30 external

measures of accoun tabili ty, government

effectiveness, rule of law, corrup tion and

democracy. Chart of RGI below, showing that

most ASEAN coun tries still perforrm poorl y

on the index.33

Main finding of RGI repor t showing that

ASEAN coun tries still lack laws and

institutions that encourage integri ty and

openness, leading to poor performance, lack

effective moni toring of licensing decisions,

and poor government effectiveness, control

of corrup tion and the rule of law, and

Cambodi a, Myanmar and Vietnam publi sh

very li tt le information on resource revenues.34

From this condi tions, impor tant to push

coun tries on ensuring revenue from oil, gas

and mining sector used for society welfare.

For the future value chain, integrated

connection between each coun tries in ASEAN

needs to be realized. The realization of

integrated connection in ASEAN enhances

Chart 3: East Asia and Pacific Index scores and ranking

Source:Resources Governance index, 2013, Asia Pacific Index Revenue

Watch Institute (Coun try by coun try repor t : http://ww w.

resourcegovernance.org/rgi)

33 Resources Governance Index: A measure of transparency

and accoun tabili ty in the oil, gas and mine sector,

Revenue Watch Institute: 2013

34 Ibid

18

the eff iciency of distribu tion in ASEAN.

Singapore, with its strategic location and

modern technolog y is ideal to be placed as a

hub to connect the coal and mining trade of

the entire coun tries in region. Singapore has

been well-kno wn as a key hub for oil and

maritime commerce for a long time, as it

covers the activities of the entire valuechain

from exploration management, refinery, and

marketing and trading for energy produ cts.35

Consequently the plan will also work for the

coal and mining trade.

Third, ASEAN energy policy. The continuation

of ASEAN Centre for Energy, especially the

APAEC Plan, gives the guidance for each

coun try in ASEAN to compose the national

energy policy that meets the standard of

regional purpo se, for example the power

plant building , the agreement to reduce the

carbon emissions, and the use of clean coal

technolog y. An agenda to foster the intra-

ASEAN coal and mining trade also signs that

ASEAN is moving forward to achieve the

regional self-suff iciency. The reason why it is

impor tant, as explained previously, because

the energy self-suff iciency leads to the

gro wt h of economy and industrial activity,

which is crucial in facing the ASEAN Economi c

Communi ty. In precise, harmoni zed policy

will make unprobl ematic produ ction and

distribu tion in the region, so that each

coun try has the abili ty to expor t and impor t

the commodi ty thoroughl y, which directly

affects the fulfillment of national demand of

energy.

Closing

Besides, the proli feration of modern

technolog y is also necessary to cultivated for

the coun tries with limi ted access. It helps the

coun tries to manage and conduct the coal

and mining produ ction properly and produ ce

the high quality produ cts. With the abili ty to

reach the demand and standard of good coal

and mining those coun tries will then actively

suppor t the intra ASEAN coal and mining

trade. Addi tionally, to tackle the challenge of

coal as energy source which contribu tes to

the environm ental pollu tant, an advanced

technolog y is also required. In this context,

strengthening regional cooperation on both

intra ASEAN and ASEAN with its dialogue

partners will be an alternative to acquire a

coal and mining trade which economi cally

and environm entally advantageous.

Moreover, the readiness of ASEAN coun tries

in the face of the AEC , especially in coal and

mining trade, not only rely on domestic

strategy of each coun try , but cooperation

and coordin ation on energy issues Including

coal and mining sectors in ASEAN level should

be maximized. Potential cooperation for

development and trade of mining and coal

must also be a key strategy of ASEAN

coun tries. The good common framework in

the management, development, and trade

should be buil t, as withou t it, the AEC will

become merely an ASEAN’s rhetoric.

35 Mark Hong, ― Overview of Singapore’s Energy Situation ‖ ,

Energy Perspectives on Singapore and the Region,

(Singapore: ISEAS, 2007), 2-3.

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) 19

Bibliography

― Coun try Repor ts Updates of Indonesia‖ . Ministry of Energy and Mineral Resources. delivered in

12th AFOC Meeting, Thailand, 21-22 May 2014.

― Energy Management Policy in Indonesia and ASEAN‖. Presentation for Workshop for ASEAN Coal

Database and Information System. 9-12 July 2012. ht tp://ww w.aseanenergy.or g/media/

documents/2012/08/03/f/i/file_2.pdf

― Programme Area No.3 ‖ . ASEAN Secretariat Website. ht tp://ww w.asean.or g/news/item/prog ramme-

area-no-3-coal

― Singapore Energy Eff iciency in the Industry‖ 2014. ht tp://ww w.sgc.or g.sg/fileadmi n/ahk_singapu r/

DEinternational/IR/diffIR/Energy_Ef ficiency_in_the_Industry_June_2014.pdf

ASEAN Economi c Communi ty Blueprin t. ASEAN Secretariat Website. 2008. ht tp://ww w.asean.or g/

archive/5187-10.pdf

ASEAN Economi c Communi ty Scorecard: Charting Progress Toward Regional Economi c Integration

Phase 1 (2008-2009) and Phase II (2010-2011). 2012. ht tp://ww w10.iadb.or g/intal/intalcdi/

PE/2012/10132.pdf

ASEAN Plan of Action for Energy Cooperation. 2012. ht tp://aseanenergy.or g/media/

filemanager/2012/10/11/f/i/file_1.pdf

BP Statictical Review of World Energy 2014, accessed on December 21st 2014, through ht tp://ww w.

bp.com/en/glo bal/corpo rate/abo ut-bp/energy-econom ics/statistical-review-of-worl d-energy/

review-by-energy-type/coal/coal-consum ption.html

Global Methane Ini tiative, ht tps://ww w.glo balmethane.or g/documents/too lsres_coal_overview_

ch37.pdf

Hoeven, Maria van der. Southeast Asia Energy Outlook. 2013. ht tp://ww w.iea.or g/publ ications/

freepubl ications/publ ication/southeastasiaenergyoutloo k_weo2013specialrepo rt.pdf

Hong, Mark. ― Overview of Singapore’s Energy Situation ‖ in Energy Perspectives on Singapore and

the Region. (Singapore: ISEAS, 2007): 2-3.

IEA Clean Coal Centre, ht tp://ww w.iea-coal.or g/documents/82373/7605/Prospects-for-coal-and-

clean-coal-technolog ies-in-Malaysia-%28CCC/171%29

Kaplinsky, Raphael and Mike Morris. A Handbook for Value Chain Paper.

Nugroho , Hanan. ― ASEAN Energy Cooperation: Facts and Challenges‖. Jakarta Post May 19th 2011.

ht tp://ww w.thejakartapost.com/news/2011/05/19/asean-energy-cooperation-facts-and-

challenges.html

Resources Governance Index: A measure of transparency and accoun tabili ty in the oil, gas and mine

sector, Revenue Watch Institute: 2013

Szczudlik -Tatar, Justyna. ― Regionalism in East Asia: A Bumpy Road to Asia Integration,‖ Policy

Paper No. 16, (2013): 3.

20

Shi, Xunpeng and Brett Jacobs. ― Clean Coal Technologi es in Developing Coun tries‖ East Asia

Forum. 2012. ht tp://ww w.eastasiaforu m.or g/2012/09/25/clean-coal-technolog ies-in-developin g-

cou ntries/

Shi, Xunpeng. China’s Attempts to Minimize non-CO2 Emissions from Coal: Evidence of Declining

Emission Intensity, Environment and Development Economics 16. (2011): 573-590.

Sivavong, Viroj. Electricity Generating Authority Thailand, Coal Demand/Supply Outlook in

Thailand. 2009. ht tp://ww w.kier.re.kr/upl oad/2009APEC-EGCFE/%28Session3-B%29Coal%20

Demand-Supp ly%20Outloo k%20in%20Thailand.pdf

World Coal Association. “Coal Fact 2014”. International Energy Agency. Coal Information 2014. BP

Statistical Review of World Energy 2014.

Vichett, Chrea. Current Situation of Mining Industry in Cambodia. (Cambodi a: General Department

of Mineral Resources of Cambodi a, 2013).

ASEAN Coal Trend Challenges and Opportunities on Facing ASEAN Economic Community (AEC) 21

Short Biography of Authors

Asra Virginianita, lecturer at Depertment of International Relations at Faculty of

Social and Poli tical Sciences, University Indonesia. Got her Ph.d. from Meiji

gakuin University, Japan in 2014. She is research manager at Japan study

centre University of Indonesia, lead researcher in DIKTI on ― Perception and

Local Government Policy on facing ASEAN Economi c Communi ty (AEC)‖.

She ever become speaker in some seminars abou t AEC in Makasar, Jambi,

International Seminar that held by Centre for International Relations

Studies (CIRes)- FISIP UI. She also active writing opinion in Media and journ al

such as Jakarta Post, Global and Strategies Journal Airlangga University.

Santi H Paramitha was born on March, 11st, 1992 in Surabaya,

East Java. She graduated from Department of International

Relations - University of Indonesia in 2014. She actively

engage as contribu tor and research assistant in ASEAN Study

Centre, Faculty of Social and Poli tical Sciences, University of

Indonesia. She concern in ASEAN China free trade agreement

and Asean Economi c Communi ty (AEC) issues.

Meliana Lumbantoruan was born on July, 5th, 1987 in Indrapura-North

Sumatera. She got her Master degree from Department of International

Relations - Gadjah Mada University in 2013. She manage research and

kno wledge management division and also manage progr amme of Southeast

Partnership for Extractive Reform in Publish What You Pay. She interested

on Value chain, Asean Economi c Communi ty, extractive industry

governance, communi ty advocacy and sustainable development issues.

ASEAN energy consump tion is forecasted to rise because of the signi ficant

gro wt h of economy and popul ation in the region. Coal use continuou sly increase

as a replacement for oil and natural gas. ASEAN plays signi ficant roles in coal

consump tion and produ ction in Asia Pacific. Using the value chain approach, it

is projected that coal produ cer coun tries in ASEAN will have the chance to

maximize the market through bilateral trade or AEC framework. The AEC can

foster market integration in ASEAN, build s awareness of ASEAN coun tries to

develop their infrastructure in energy suff iciency, as well as develops clean coal

technolog y. Coal produ ction in ASEAN will still leant on Indonesia as the main

expor ter in ASEAN. Energy policy of each coun try in ASEAN has a lot of things in

common , which provides the space of building further regional coooperation in

managing energy features. The future of coal sector in ASEAN will highl y

depends on advancement of technolog y, impro vement of governance, effeciency

of transpor tation, and connectivity between the coun tries. Strengthening

cooperation and coordin ation must be a key strategy for ASEAN coun tries to

ensure readiness in facing AEC.

PWYP Indonesia is a coalition of civil societies for transparency and accountability

of extractive resources governance in Indonesia. PWYP Indonesia was established in

2007, legalised under Indonesia’s law in 2012 as Yayasan Transparansi Sumberdaya

Ekstraktif , and affiliates to the network of PWYP global campaign. PWYP Indonesia

works in transparency and accountability along the chain of extractive resource, from

development phase of contract and mining operation (publish why you pay and how

you extract), production phase and revenue from industries (publish what you pay), to

the spending phase of revenue for sustainable development and social welfare (publish

what you earn and how you spent).

Website: www.pwyp-indonesia.org Email: [email protected] Facebook Fanpage: Publish What You Pay Indonesia Twitter: @PWYP_Indonesia