Arun Reddi VRL 6th Sem

128

VRL LOGISTICS Ltd Varur-Hubli DECLARATION I, Mr. ARUNARADDI.D.TIGARI of BBA 6 TH semester of A.S.S’ College of BBA, Gadag hereby declare that this project titled “Working Capital Management” is based on “VRL Logistics Ltd in Varur-Hubli”. This project has been prepared by me under the guidance of Prof. A. M. Habib. . This project is my original work and has been submitted to A.S.S’ College of BBA, Gadag. Date: A.S.S’S College of Business Administration, Gadag-Betgeri

-

Upload

gopi-krishna -

Category

Documents

-

view

184 -

download

10

Transcript of Arun Reddi VRL 6th Sem

VRL LOGISTICS Ltd Varur-Hubli

DECLARATION

I, Mr. ARUNARADDI.D.TIGARI of BBA 6TH semester of A.S.S’

College of BBA, Gadag hereby declare that this project titled

“Working Capital Management” is based on “VRL Logistics

Ltd in Varur-Hubli”. This project has been prepared by me

under the guidance of Prof. A. M. Habib. . This project is my

original work and has been submitted to A.S.S’ College of

BBA, Gadag.

Date:

Place: Gadag Mr. ARUNARADDI.D.TIGARI

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

ACKNOWLEDGEMENT

Before we get deep into the project, I would like to take

this opportunity to express my profound thanks to people

who have become part of this project.

I would like to express my sincere and profound sense

of gratitude to the Management of “VRL Logistics Ltd in

Varur-Hubli” for Providing me such a great opportunity,

and their support and valuable guidance for “Working

Capital Management in their department”.

I would like to thank the Managing Director of VRL Mr.

Anand Sankeshwar and also to Shri. S.G.Patil General

Manager (HRD), for their support and advice and for giving

me all the valuable information required to fulfill the needs

of this project.

I would also thank the entire Departmental Staff of

VRL who were very kind and supportive enough to spare

their busy schedules, and for giving each and every detail I

needed to complete my project.

I extend my heartfelt and sincere thanks to our

Pri.Prof. Basavaraj A Hiremath, A.S.S’s College of BBA,

Gadag, for her valuable and timely guidance and support,

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

and for his constant motivation throughout my project

period.

I also extend my heart full thanks to my Project guide

Prof. A. M. Habib, A.S.S’s College of BBA, Gadag without

whose support and guidance I would not have been able to

prepare this project.

I want to extend my heartily thanks to my beloved

friend Mr. Basavaraj R Lingashetti, Madan Joshi who

has supported me for finishing the project work.

I would fail in my duty if I can’t remember the

encouragement given by my parents and friends in my

endeavor.

Place: Gadag Mr. Arunaraddi Tigari.

C ONTENTS

1. PROJECT PROFILE 1-3Executive summary

Scope of study

Objectives of the study

Methodology

Limitation

2. INDUSTRY PROFILE 4-9Introduction

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

Out look of the VRL

3. COMPANY PROFILE 10-18

Brief History

Organization profile

Quality Policy

Customers

Organization chart

4. WORKING CAPITAL MANAGEMENT 19-44Introduction

Concept

Importance

Determinates

Analysis

5. CASH MANAGEMENT 45-46

Introduction

Motives

Cash management cycle

Objectives

6. RECEIVABLE MANAGEMENT 47-49Introduction

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

Credit evaluation

Optimum credit policy

Benefits

Company practice

Average collection period

7. DATA ANALYSIS AND INTERPRETATION

8. GENERAL OBSERVATION

Strength

Weakness

Conclusion

BIBLIOGRAPHY

ANNEXURES

A.S.S’S College of Business Administration, Gadag-Betgeri

PROJECTPROFILE

VRL LOGISTICS Ltd Varur-Hubli

EXECUTIVE SUMMARY

I have selected. VRL Vrur-Hubli for the project work “Working capital

management” which I learned at my BBA VIth semester.

VRL Logistics Pvt, Ltd commenced its operation and started in the year 1976.

VRL Logistics is one of the leading road transportation companies in India, with

operations in parcel transportation, passenger transportation, express cargo, aviation and

courier segments.

Management of working capital is an essence of business activity a company should

always maintain good amount of working capital on continuous basis.

So I took this opportunity to study the working capital management of VRL Varur-

Hubli.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

SCOPE OF THE STUDY

The customer Satisfaction Survey activity entails: identification of customer

segments in more details; listing the types of courier interfaces with customers;

categorization of services received by various segment. Intended project activity for 2010

encompasses the design, data collection, analysis and reporting of a statistically reliable

survey of customer segments, perceptions of courier current levels of performance,

service of performance standards expectations, and service improvement opportunities. In

order to be consistent with previous customer satisfaction studies, both the list of

directorates and the “satisfaction criteria” will be consistent. However additional items of

information will be added.

OBJECTIVES OF THE STUDY

To know the attribute of the customer towards the company’s service.

To know the service provided by the VRL Logistics.

To understand the present service system.

To find out the gap between present service and customer expectation.

To know the price level of the VRL Logistics Ltd courier service compared to other

competitors.

To know the safety of documents and time management.

To know the staff behavior with the customer.

To sasses the level of satisfaction of customer towards courier service offered by the

VRL Logistics Ltd.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

METHODOLOGY

The data is collected from both primary and secondary source they are

***Primary Source: Conversation with Mr. S. Sudhakar. Financial Consulter and also

with college guide Mr. Anand Faculty in Finance.

***Secondary Source: Company’s annual reports and the company www.vrllogistics.com

LIMITATIONS

The time is the main limitation to this project. Because “Working capital

management” is a very vast subject and to study it thoroughly one month is a very short

period.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

INDUSTRY PROFILE

VRL LOGISTICS Ltd Varur-Hubli

INDUSTRY PROFILE

Introduction :

Had its start some 15-20 years ago. The courier industry was initially limited to

the four metros –New-Delhi, Mumbai, Kolkatta, and Chennai and to some extent to

Bangalore. The reason was the airport connection these metros were. But, the changing

economy and technical advancement seen on a daily basis, the industry has grown and

extended faster to several cities and even rural areas. And it is still growing.

A courier company anywhere in the world has its primary virtue is its efficiency

to render services. The better the quality of service, the more the satisfied customers,

better the chances of survival. The industry is booming and market is cut-throat

competitive. The advancement of technology and internet has things slight easier and

more competitive as well.

Courier services in India can be segregated in few categories. Basically, it begins

with intra-city services which are about speedy delivery of mails and goods within the

city. Broadening the services, inter-city services are covered. Normally this is termed as

surface cargo services where short distance and bulk loads are handled. Surface mode

service is performed through two ways: firstly, on road (by bus or vehicle) and secondly

on track (by train) services. The products are normally delivered through door to door.

Courier companies work in tandem with the foremost airlines and in sync with their

well tuned, well associated set of connections the timely deliverance and protected

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

service is guaranteed. Few other variant of services could be express services, ocean

freight, industry solutions, logistic solutions, shipping tools. These particular services are

individual of a company's area of specialization and diversification.

Courier :

A courier is a person or a company who delivers message, packages , and mail.

Couriers are distinguished from ordinary mail services by features such as speed,

security, tracking, signature, specialization and individualization of services, and

committed delivery times, which are optional for most everyday mail services. As a

premium service, couriers are usually more expensive than usual mail services, and their

use is typically restricted to packages where one or more of these features are considered

important enough to warrant the cost.

Different courier services operate on all scales, from within specific towns or

cities, to regional, national and global services. The world's largest courier companies are

Velox Express, DHL, FEDEX, OBC Express Ltd., TNT.NV, UPS, and Aramex These

offer services worldwide, typically via a hub and spoke model.

Couriers before the industrial area :

In ancient times runners and homing pigeon and riders on horseback were used to

deliver timely messages. Before there were mechanized courier services foot messengers

physically ran miles to their destinations. To this day there are marathons directly related

to actual historical messenger’s routes.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

Types of couriers :

In cities, there is often bicycle courier or motorcycle courier but for consignments

requiring delivery over greater distance networks, this may often include Lorries,

Railway and Aircraft.

Many companies who operate under a JUST IN TIME or "JIT" inventory method

often utilize on-board couriers. On-board couriers are individuals who can travel at a

moment's notice anywhere in the world, usually via commercial airlines. While this type

of service is the second costliest— GENERAL AVITATION charters are far more

expensive—companies analyze the cost of service to engage an on-board courier versus

the "cost" the company will realize should the product not arrive by a specified time.

Indian Logistics Out look :

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

On the other hand, since year 2000, the Indian industrial sector has also begun to

look up, and in 2006, it registered over 10% growth for the time in decades, primarily

driven by the manufacturing and capital goods segments. In the Indian manufacturing

industry, textile plays a predominant role, while the chemical industry is the second

largest industrial sector (12% of the GDP). However, India’s influence in global trade

remains low and the country represents only 1% of the world export trade. India mainly

exports engineering goods, gems and jewelers (83% of diamond sold in the world are cut

in India), textile and fabrics, and leather goods. The major imports are oil, precious

stones, chemical products and machinery/engineering equipments. India’s main trade

partners (exports and imports) are Belgium, China, Switzerland, UAE, the UK, and US.

With India’s GDP growing at9% and the manufacturing sector enjoying double digit

growth rates the logistics industry is at an inflection point. Strong growth enables exist

today in the forum of $250 billion worth of infrastructure investment phased introduction

of vat, and development of organized retail, telecom, and auto component manufacturing

will lead to increased market opportunities for logistics service providers (LSPs). India

currently spends over 13% of its GDP on logistics, which is very high compared to

Western Europe and north America, where logistics cost as a percentage of GDP is in the

range of 8-10%. With growing global competition, improving operational efficiency has

become imperative and the growth in domestic demand is driven by a number of factors

including the rising income level and easy availability of low-cost finance. The auto

sectors are key to the Indian economy from both the perspective of economic

contribution as well as that of employment generation. The sectors employs 13 million

people and contribution to around 17% of the direct taxes kitty, the growth in the

domestic demand is driven by a number of factors including the rising income levels and

easy availability of low-cost finance. The auto sectors are key to the Indian economy

from both the perspective of economic contribution as well as that of employment

generation. The sectors employs13 million people and contribution to around 17% of the

direct taxes kitty.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

About vRl courier service :

This section was started in the year 1992, which deals with courier services that

play a vital role in modern business. In fact it has been so well accepted by the people

that prefer courier rather than the postal services. Courier is faster than transport because

there is no compulsion for entire lorry to be full. Even a single parcel booked is sent to

destinations through various sources. The company has covered around 350 stations for

courier parcels. Daily circulation of covers is more than 3500 covers there are more than

350 branches only in Karnataka the main office is in Bangalore after the expansion of the

courier service in Karnataka. They are booked at various booking offices and sent to the

main office. The turn over of courier service was 5 crore per annum in the year 2008-09.

it has become famous at national level. But on July 17th 2007 it has reduced to only

Karnataka

Rate charged : For one cover up to 250 grams the rate charged Rs. 10/-

Parcels : Up to one kg 25 plus additional charge on every kg Rs 15 per kg

Brief introduction of working process :

Hubli courier office is the main office. And al collected consignment and

documents which have collected through company employees and company agents are

come to main office. In main office courier are classified according to city name and

keeping that document in separate section. For keeping those classified documents the

section has separate place for every state and city area, after this classified parcels will be

sent to its destinations places.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

Punch line of VRL

courier service

“Any where any

time”

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

VRL EXPRESS CARGO:

Surface, train and cargo mode service

Dedicated company owned vehicle

Door pick up and delivery

On-time delivery

Online track and trace facility

24*7*365 days operation

Dedicated and well-groomed customer care windows

Extensive nation-wide network

COMPETITORS OF VRL COURIER SERVICE :

Dtdc

Professional courier service

Teja

Sharma travels

National travels

Ksrtc

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

COMPANY PROFILE

VRL LOGISTICS Ltd Varur-Hubli

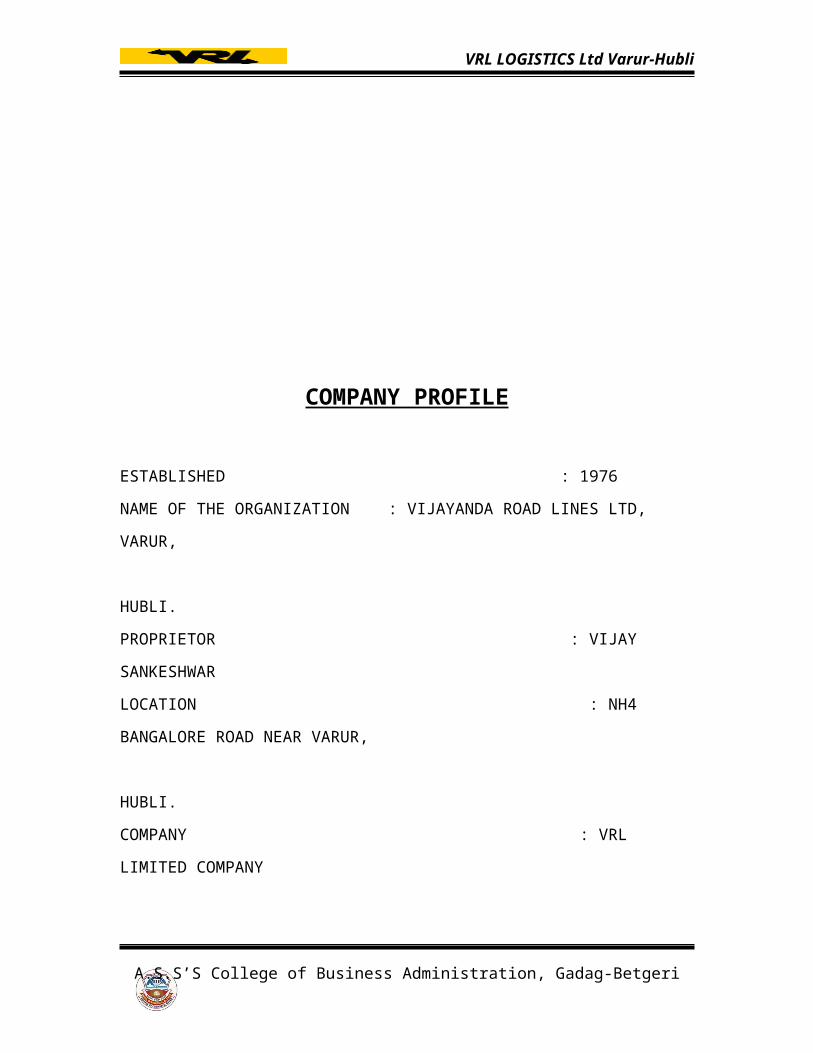

COMPANY PROFILE

BRIEF HISTORY OF THE COMPANY

Vijayanda Road Lines ltd a company registered under the provision of company

act 1956 has with its “symbol of service”. The ‘VRL’ has built and maintained goodwill

in the minds of public at large in the country in general and in Karnataka particular.

The managing director Mr. V.B.sankeshwar started as an individual transport in

January 1976 without any background of experience. Initially for the first two years he

suffered heavy loss. Then by end of 1977 he started as local transporter between in Hubli

and Gadag. Due to effective service, business picked up and purchased one more lorry in

1978. during this work he observed activities of other well know transporter and started

first parcel service from Bangalore to Hubli and Belgaum with only two lorries.

Gradually the business picked up. Later the above proprietorship were converted into

private ltd. The company came into existence in the year march 31st 1983, VRL Company

initially in the transportation of goods and services subsequently it concerned the

business of courier service in the year 1996 it acquired passenger buses, initially

vijayanda travels operating in the state of Karnataka and Maharashtra

Presently VRL existing with largest network in India, the VRL parcel service is

indispensable for large no of corporate houses. This network spans the length and breadth

of the country and is supported by large number transshipment hubs, VRL operates

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

through a network of 2629 Locations 911 branches, franchises and valuable customer,

now VRL expanding its service to reach even the remote location of the country with the

help of 2691 vehicles (including 196 hi-tech buses)

Over the years VRL has pioneered in providing a safe and reliable delivery

network in the field of parcel service. It has spread its operations to courier service

express cargo and Aviation to meet the growing of the customer base

At the core of the groups transport business is its 43 acre transport cum warehouse

complex in Varur, Hubli. This unique facility has all the essential back up service under

one roof. The total built up area of complex is 25000000 sq ft with an additional 1,00,000

sq, ft, of land utilized for sheds and vehicle parking, this complex contain the head office

building, transshipment Godown, Workshop, Canteen, Drivers rest room, Own diesel

bunk.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

COMPANY PROFILE

ESTABLISHED : 1976

NAME OF THE ORGANIZATION : VIJAYANDA ROAD LINES LTD, VARUR,

HUBLI.

PROPRIETOR : VIJAY SANKESHWAR

LOCATION : NH4 BANGALORE ROAD NEAR VARUR,

HUBLI.

COMPANY : VRL LIMITED COMPANY

BOARD OF DIRECTORS

Mr. VIJAY SANKESHWAR : CHAIRMAN AND MANAGING DIRECTOR

Mr. ANAD SANKESHWAR : MANAGING DIRECTOR

Mr. SUDHIR GHATE : DIRECTOR

Mr. J.S. KORLAHALLI : DIRECTOR

Mr. KARUNAKAR SHETTY : DIRECTOR

Mr. SURESH ANGADI : DIRECTOR

REGISTERED OFFICE : 18th km, NH4, Bangalore Road, Varur,

Hubli-581207 Karnataka.

Phone no 0836-2237614,

Email – [email protected],

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

Website – www.vrllogistics.com.

VISION, MISSION, VALUES AND QUALITY POLICY

VISION:

The vision is to inject new ideas in the transportations

Self motivate the employees for a change and there by change the

organizational behavior to achieve company’s goal.

To provide quality and better service to public.

To emerge as one the leading players in the transportation industry in India.

MISSION:

To provide a highest quality service to our customers by continuously increasing

cost efficiency and maintaining delivery deadlines. To encourage our employees

workforce to strive for quality and excellence in everything they do, to promote team

work and create a work environment that takes care of talent and bring out the best in our

employees. Providing a quick and safe delivery of goods service is their motto.

THE VALUES:

“Punctuality, Integrality, Honesty, Loyalty and Credibility”

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

PHILOSOPHY:

They immensely follow: “Time is Gold”

QUALITY POLICY:

The VRL started with the sign of “symbol of service” the VRL are committed to

meet the needs and expectations of our customers by providing quick, prompt, efficient,

reliable, cost effective and safe service. Maintaining transparency in all their truncation

and strive for continual improvement for enhancing customer satisfaction.

In the words of chairman and managing director “we are committed to provide

quality transportation and logistics service consistently at reasonable rate and to

continually improve the same to achieve customer to delight on sustainable basis.

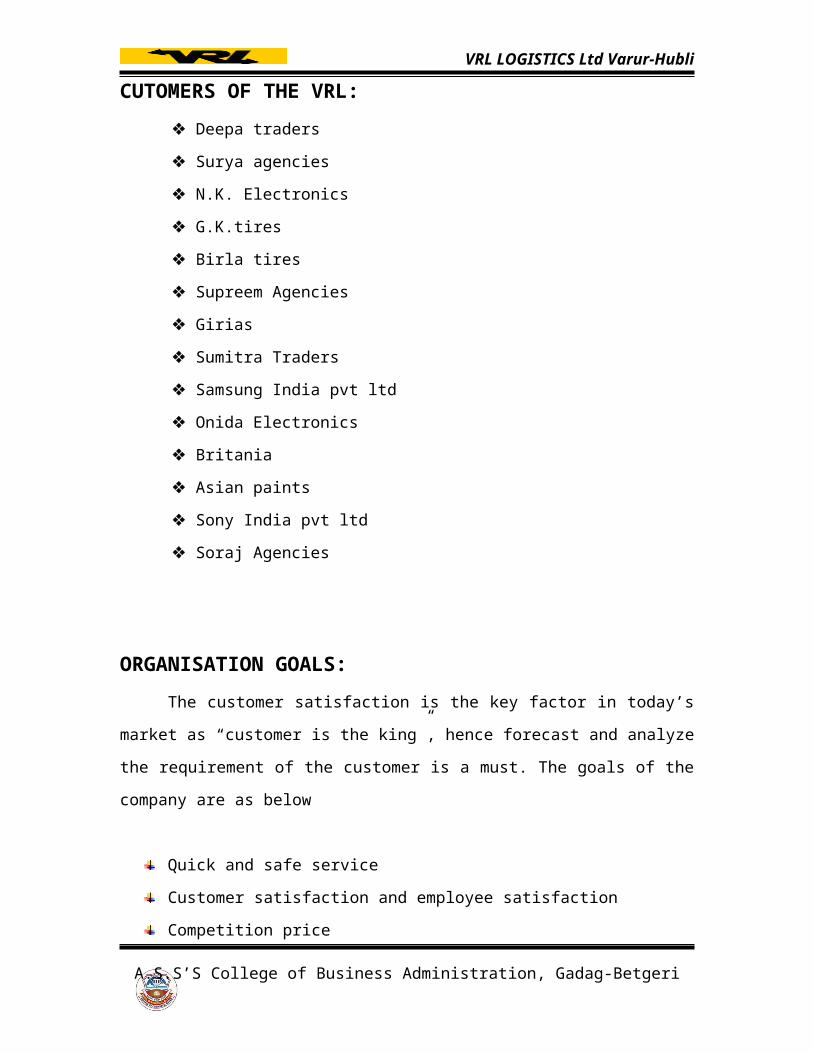

CUTOMERS OF THE VRL:

Deepa traders

Surya agencies

N.K. Electronics

G.K.tires

Birla tires

Supreem Agencies

Girias

Sumitra Traders

Samsung India pvt ltd

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

Onida Electronics

Britania

Asian paints

Sony India pvt ltd

Soraj Agencies

ORGANISATION GOALS:

The customer satisfaction is the key factor in today’s market as “customer is the

king”, hence forecast and analyze the requirement of the customer is a must. The goals of

the company are as below

Quick and safe service

Customer satisfaction and employee satisfaction

Competition price

Attain market leader ship

OBJECTIVES OF THE COMPANY:

The main objective of the company is to provide good service to customer with

the reasonable rate and provide quick prompt and service.

Human resource development

To develop the transportation business in states like Andra pradesh, Tamilunadu

and Kerala

Training for all employees

Customer satisfaction

To have an independent own building with printing machines and computer for

each and every district

Competitive price

Productivity and innovation

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

To build highly motivated and committed team of staff by providing a good

work culture to achieve individual performance

To implement ISO 9002

SERVICES:

The person who are booked for the travels are covered by insurance.

They provide returned journey ticket booking facility

To maintain their good service they go for only selected hotel place for hygienic

food.

Incentives are provided to drives for safe and timely service.

Concession is provide for the school and college going students for their study

trips.

Careful handling of goods consigned

ACHIEVEMENTS AND AWARDS

ACHIEVEMENTS:

The company has 1600 vehicles consisting of cargo and passenger buses and is

claiming as a largest fleet owner in the world entitled for an entry in the business book

record. The “LIMCA BOOK OF RECORD” has already accepted the entry and has been

publishing the updated information in the year after year.

The company has making all affect to have own infrastructure facilities like

transshipment yards etc in all key business by acquiring the immovable properties. It is

the company of certified by ISO 9001 and 2000.

AWARDS:

1) UDOYG RATNA: In the year 1994 “INSTITUTE OF ECONOMICS STUDY”, NEW

DELHI has conferred the MD of the company with “UDOYG RATNA”

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

2) SARIGE RATNA: In the year June 28th 2008 the Bangalore city lorry agent

association has concerned MD of the company.

3) VISHVESWARAYYA NAVARTNA AWARD: In the year 2003

INTERNATIONAL BIOGRAPHIC CENTRE: the international has chosen company

MD to include in the dictionary of “INTER NATIONAL BIOGRAPHICS” for hops

contribution and monitories achievements in cargo transport couriers and tourism sector

WORK FLOW MODE

A.S.S’S College of Business Administration, Gadag-Betgeri

CUSTOMER CARE

CONTRACORY BOOKING

ACCOUNT SECTION

TICKET BOOKING

PARCEL BOOKING

VRL LOGISTICS Ltd Varur-Hubli

ORGANIZATION CHART

A.S.S’S College of Business Administration, Gadag-Betgeri

Vijay sankeshwar Chairman and MD

Anand sankeshwar Managing director

K.N.UmeshCEO

L.R.BhatCTO

V.P.KarmadiVP (operations)

G.S.AyyerVP (Finance)

Anjan RaoVP (Aviation)

G.R.Hatti GM(Administration)

Y.M.Hamali GM(Infrastructure)

C.M.Bulutti GM(MCP)

Prabhu SalegeryGM (Travels)

S.G.Patil GM (HRD)

DEPUTY GM

AREA MANAGER

BRANC MANAGER

TRAVELS

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

CLERKS

WORKING CAPITAL

MANAGEMENT

VRL LOGISTICS Ltd Varur-Hubli

WORKING CAPITAL MANAGEMENT

MEANING:

Working capital is the short-term investment, which is, concerned with the

problems that arise to manage current assets the current liabilities and the relationship

that exists between them.

CONCEPTS:

There are two concepts of working capital

I. Gross Working capital

II. Net Working capital

GROSS WORKING CAPITAL:

The total capital employed in current assets or firms investments in current assets.

Current assets are those assets which can be converted into cash within an

accounting year and include cash short term securities, debtors, bills receivables,

inventory it focuses on two aspects of current assets management.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

1. Optimum investment in current assets- i.e. to avoid two extreme prints excess and

inadequate investments in current assets.

2. Financing of current assets it should make necessary arrangement of working

capital fund whenever a firm due to increase level of business activities or for any

other reasons.

NET WORKING CAPITAL:

It is difference between current assets and current liabilities of the excess current

assets over current liabilities.

Current liabilities are those claims of the outsiders, which are expected to mature

for payment within an accounting year and include creditor’s bills payable etc.

NEED FOR WORKING CAPITAL:

A firm needs working capital for the following reasons.

1. To run the day-to-day business activities.

2. To maximize the wealth of the share holders

3. To deal with the problem arising out of the luck of immediate realization of cash

against goods sold.

4. To match between cash outflow and cash inflow of the firm

5. To smooth, uninterrupted functioning of firm activities.

6. Stock of raw material, work in progress are kept to ensure smooth production and

to guard against non-availability of raw material and there components.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

DETERMINANTS OF WORKING CAPITAL:

There are no set rules or formulas to determine the working capital requirements

of firm a large number of factors each having a different importance affects the working

capital of a firm.

The operating cycle is explained above in detail in also one of the determinant to the

working capital requirement, so these following are some other factors that generally

insurance the working capital requirements of a firm.

1)NATURE OF BUSINESS:

Working capital need is influenced by nature of the business trading and finance

firms have a very small investment in fixed assets, but require a large sum of money to be

invested in working capital.

2)BUSINESS CYCLE:

Working capital requirement is determined by the nature of the business cycle

business fluctuation lead to cyclical and seasonal changed which in turn cause a shift in

the working capital position.

3) PRODUCTION CYCLE:

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

It is another important factor to determine the working capital need of a company.

How much working capital is required for procurements of raw materials is determined

by this factor. The completion of the manufacturing process leads to the production of

finished goods.

4) CREDIT POLICY:

Credit policy relating to the sales and purchases also affects the working capital

used it policy influence the requirement of working capital in 2 ways.

Through credit terms granted by the company to its customers.

Credit terms available to the firm from its creations.

5)PRICE LEVEL CHANGES:

Changes in the price level also affect the requirements of working capital. Rising

prices necessitate the rise of move funds for maintaining an existence level of activity

changing price levels on working capital position vary from company to company

depending on the nature of its operations its stand in the market.

6) RISKS:

The greater the uncertainty of receipt and expenditure, more the need of working

capital, so, risk can also be an influencing factor in determining the working capital

requirement of a firm.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

WORKING CAPITAL MANAGEMENT

TABLE SHOWING NET WORKING CAPITAL CHANGE OF

VRL LOGISTICS PVT, LTD.

SI. No Particulars 2007-08 2008-09 2009-10

1 Current

a) Inventory (Spares, Diesel, etc) 869.50 680.09 633.06

b) Sundry Debtors 1721.25 2260.46 2922.98

c) Cash & Bank 708.15 1515.85 1961.89

d) Loans & Advances (Short-term) 1357.06 3800.13 4497.35

I Gross Working

Capital(a+b+c+d)

4655.96 8256.53 10015.28

2 Current Liabilities

e) Current Liabilities 1792.61 2627.24 3355.96

f) Provisions 362.00 280.43 105.12

II Total Current Liabilities (e+f) 2154.61 2907.67 3461.08

Net Working Capital(I+II) 2501.35 5348.86 6554.20

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

OPERATING CYCLE:

A firm should aim at maximizing the wealth of it’s shareholders, so the firm should earn sufficient return from it is operations. Earning a steady amount of profit requires successful sales activities. The firm has to invest enough funds in current assets for generating sales. Current assets are needed because sales do not convert cash instantaneously. There is always an operating cycle involved in the conversion of sales in to cash.

IT IS EXPLAINED THROUGH THE FLOWING DIAGRAM

A.S.S’S College of Business Administration, Gadag-Betgeri

CASH

SalesA/c Receivables

Inventories

VRL LOGISTICS Ltd Varur-Hubli

Length of Operating Cycle:

The length of the operating cycle can be calculated in two ways:

a) Gross Operating Cycle:

The gross operating cycle of a trading concern in is the sum of Inventory

Conversion period and debtors (Receivable) conversion period. Thus, Gross Operating

Cycle is given as follows:

INVENTORY CONVERSION PERIOD + DEBTORS CONVERSION PERIOD

b) NET Operating cycle:

Net Operating Cycle is the difference between Gross Operating Cycle and

creditors (Payables) Deferral period.

Length of Operating cycle:

The sum of inventory conversion period (ICP), Debtors Conversion period (DCP).

Operating cycle period =ICP+DCP

Inventory Conversion period

1) RML conversion period = RML inventory X 360

RML consumption

2) WIP CP = WIP inventory X 360

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

Cost of production

3) Finished goods CP = Finished goods inventory X 360

Cost of goods sold

4) Debtors conversion period = Debtors X 360

Cr. Sales at cost

5) Payables deferral period = Creditors X 360

Credit sales

INVENTORY CONVERSION PERIOD (ICP):

The total time needed for producing and selling the product and includes raw

material conversion period, work in progress conversion period and finished goods

conversion period.

ICP=RMCP+WIPCP+FGCP

Debtor’s conversion period [DCP]:

The time required to collect the outstanding amount from the customers.

Gross operating cycle [GOC]:

The total of inventory conversion period and debtor’s conversion period.

GOG=ICP+DCP

Net operating cycle [NOC]:

It is the net difference between gross operating cycle and payable deferral period.

Payable deferral period [PDP]:

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

Capacity of firm to postpone the payments. The ability of a firm to acquire

resources on credit and temporarily postpone payment of certain expenses it is length of

time the firm is able to postpone payment on various resources purchases.

NOC=GOC-PDP

Cash conversion cycle [CCP]:

It is the net difference between net operating cycle and depreciation and profit.

CCC=NOC-Depreciation and profit

IMPORTANCE OF OPERATING CYCLE :

Operating cycle concept is a new concept in working capital management, which

has been gaining more and more importance in recent years. This concept emphasis the

importance of time factor in the conversion of raw materials into final product and then

into sales resulting in cash collection right from the acquisition of raw materials.

Normally operating cycles passes through the following stages

a. Acquisition of raw materials

b. Work in process

c. Stock of finished goods

d. Sale and realization of sale proceeds

Operating cycle concept plays an important role in determining the working

capital management of firm. Longer the operating cycle greater will be the amount of

working capital requirement and shortest operating cycle requires limited amount of

working capital. There fore an efficient management should try to reduce the time

elapsed in these consecutive stages of operating cycle.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

Duration of manufacturing process right from the acquisition of raw materials till

they are sold out after being converted into final product and the cash realized determines

the amount of working capital required.

REASONS FOR LENGTHY OPERATING CYCLE:

Pro-longed operating cycles may be due to the following reasons:

1) In effective receivable management.

2) Lack of credit facilities from the suppliers.

3) In effective purchase policies.

A.S.S’S College of Business Administration, Gadag-Betgeri

CASH MANAGEME

NT

VRL LOGISTICS Ltd Varur-Hubli

CASH MANAGEMENT:

MEANING:

Cash is the important current asset for the operations of the business . Cash a basis

input needed to keep the business running on a continuous basis it is also the ultimate

output expected to be realized by selling the service or product manufactured by the

company. The company should keep the sufficient cash neither more or less cash

shortage will descript the firm’s manufacturing operation while excessive cash will

simply remain idle without contributing anything towards the company’s profitability.

Thus, a major function of the financial manager is to maintain a sound cash position.

Cash is the money, which a firm can disburse immediately without any restriction

the term cash included coins currency and cheques held by the firm and balance in its

bank accounts. Sometimes more cash items such as marketable securities or bank time

deposits are also included in cash.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

MOTIVE FOR HOLDING CASH:

1) Transaction Motive:

The transaction motive requires a company to hold to conduct its business in the

ordinary course the company needs cash primary to make payments for purchases.

Wages, salaries, other operating expenses etc.

2) Precautionary Motive:

The precautionary motive is its need to hold cash to meet contingencies in futures.

It provides a cushion to with stand some unexpected emergency. The precautionary

amount of cash defends upon the predictability of cash flows. The precautionary

balance many kept cash and marketable securities.

3) Speculative Motive:

The speculative motive relates to the holding of cash for investing in profit

making opportunities as send when they arise. The opportunity to make profit may arise

when the security prices changes.

CASH PLANNING

Cash inflows and outflows should be planned to project cash surplus or deficit for

cash period of the planning period. Cash budget should be prepared for this purpose.

MANAGING THE CASH FLOW

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

The flow of cash should be properly managed. The cash inflows should be

accelerated as far as possible, decorating the cash outflows.

OPTIMUM CASH LEVEL

The company should decide about appropriate level of cash balances. The cost of

excess cash and danger of cash deficiency should be matched to determine the optimum

level of cash balances.

INVESTING SURPLUS CASH

The surplus cash balances should be properly invested to earn profits. The firm

should decide about the division of cash balance between bank deposits, marketable

securities, and inter corporate lending.

CASH MANAGEMENT AT VRL LOGISTICS PVT,LTD

A well management of cash needs in a company can represents the amount of

money company keeps with a bank on current or deposit account and the money holds in

the company.

To control a company’s cash flows one requires a plan of the company’s

operations for the relevant future period. This plan is based on forecasts of cash receipts.

In patil works and cash disbursements for costs and purchases of equipment’s etc.

COMPANY PRACTICE:

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

Inflows and outflows of cash by the VRL (Varur-Hubli)

CASH INFLOWS OF THE COMPANY:

Advanced payment by the customers.

Sundry debtors / receivable

Export incentives

Other income

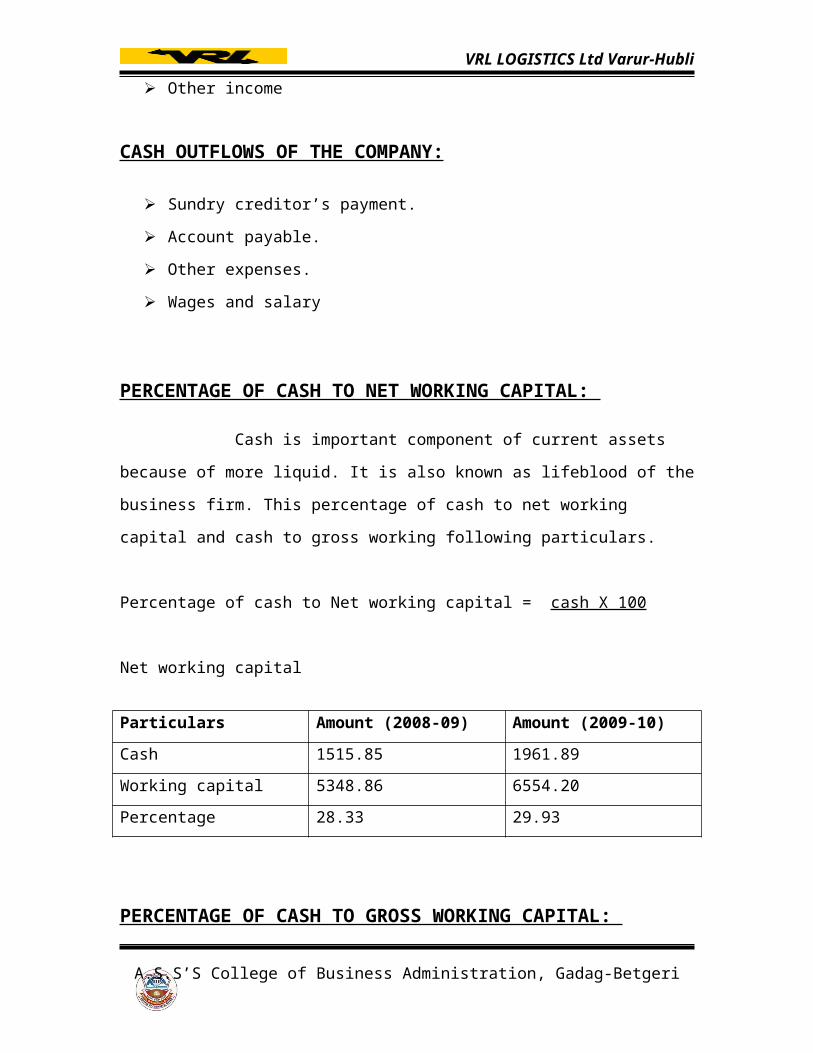

CASH OUTFLOWS OF THE COMPANY:

Sundry creditor’s payment.

Account payable.

Other expenses.

Wages and salary

PERCENTAGE OF CASH TO NET WORKING CAPITAL:

Cash is important component of current assets because of more liquid. It is also

known as lifeblood of the business firm. This percentage of cash to net working capital

and cash to gross working following particulars.

Percentage of cash to Net working capital = cash X 100

Net working capital

Particulars Amount (2008-09) Amount (2009-10)

Cash 1515.85 1961.89

Working capital 5348.86 6554.20

Percentage 28.33 29.93

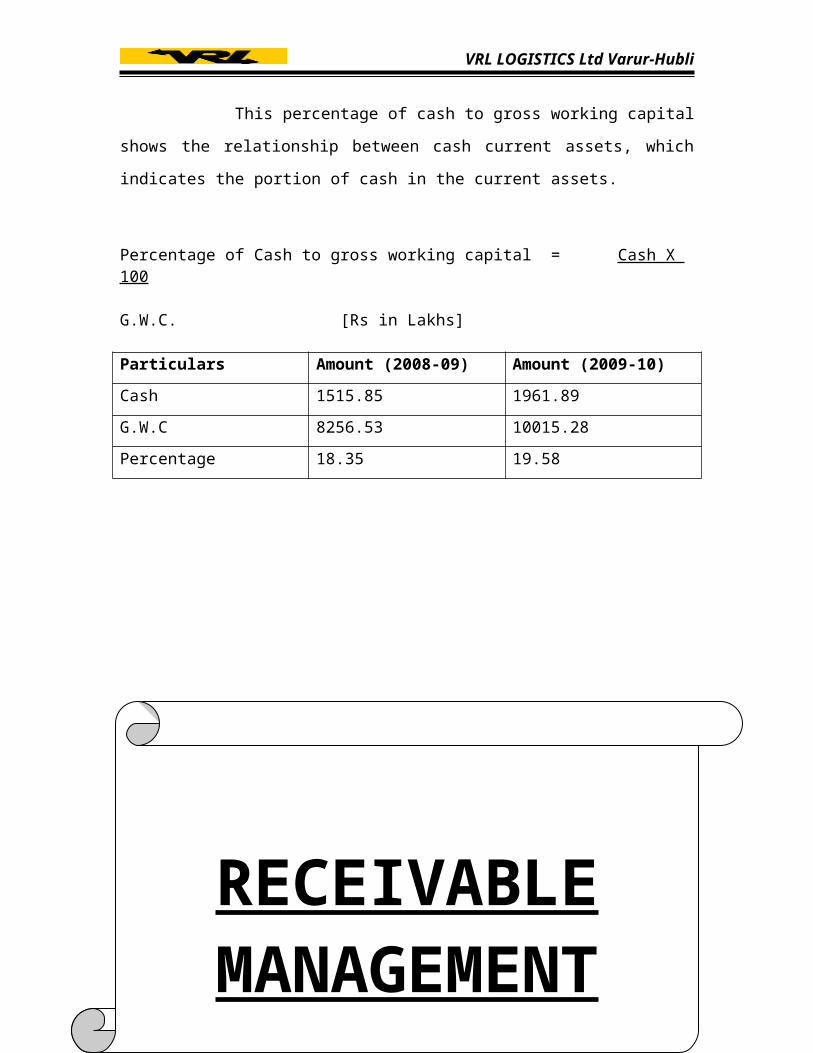

PERCENTAGE OF CASH TO GROSS WORKING CAPITAL:

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

This percentage of cash to gross working capital shows the relationship between

cash current assets, which indicates the portion of cash in the current assets.

Percentage of Cash to gross working capital = Cash X 100 G.W.C. [Rs in Lakhs]

Particulars Amount (2008-09) Amount (2009-10)

Cash 1515.85 1961.89

G.W.C 8256.53 10015.28

Percentage 18.35 19.58

A.S.S’S College of Business Administration, Gadag-Betgeri

RECEIVABLE MANAGEMENT

VRL LOGISTICS Ltd Varur-Hubli

RECEIVABLE MANAGEMENT

MEANING:

Receivables contribute a substantial portion of current assets of several firms e.g.

In INDIA tread debtors, after in ventures one the major components of current assets.

They form about one third of current assets in India granting credit and creating debtors

amount to the blocking of the company’s funds. The interval between the date of sale and

payment has to be financed out of working capital. These necessities the firm to get funds

from banks or other sources. Thus trade debtors represent investment, as substantial

amounts are ties up in trade debtor’s, it needs careful analysis and proper management.

OBJECTIVES:

The following are the objectives of receivables management

a. To maintain the good will of the company in the minds of customers:

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

Good will is an intangible asset clearly specifies the reputation of the company to maintain the good will in the customers mind is essential because good will is only the alternate food for long life of the company there fore providing credit facility to the customers is to maintain the reputation.

b. To have the regular customers

Providing credit facility is to protect its sales from the competitions and to attract the potential customers to buy its products at favorable terms. Regular customers are like KEB etc.

ESTABLISHING OPTIMUM CREDIT POLICY:

A company’s investment in accounts receivable depends on:

a) Volume of credit sales

b) Collection period

The volume of credit sales is a functions of the firm’s total sales and percentage

of credit sales to total sales. Total sales depend on market size firm’s market share

product quality. Intensity of competition economic conditions etc. the financial manager

hardly has any control over these variables. The percentage of credit sales to total sales

are mostly influenced by the native of business and industry norms.

The term credit polity is used to refer to the combination of the decision variables they

are-

i) Credit standard

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

ii) Credit terms

ii) Collections efforts

On which the financial manager has influence.

THE CREDIT STANDARD:

It is the criteria to decide the types of customer’s to whom goods could be sold on

credit. It a company has more slow playing customers its investment in account

receivables. Will increase. The company will also expose to higher risk of default. Credit

terms specify duration of credit and terms of payment by customer’s investment accounts

receivables will be high if the customers are allowed extended time period for making

payments collection efforts. Determine the actual collection period. The lower the

collection period, the lower investment in accounts receivables and vice-versa.

OPTIMUM CREDIT-POLICY: A Cost Benefit- Analysis:

The firms operating Profit is maximized when total cost is minimized for a given

level of revenue. Optimum credit policy is one, which maximizes the company’s value.

The value of the company is maximized when the incremental rate of return on

investment is equal to the incremental cost of funds used to finance the investment. As

the firm looses its credit policy. Its investment in accounts receivable becomes more risky

because of increase in slow paying and defaulting accounts.

Thus we many state that the goal of the firm’s credit policy is to maximize the

value of the company. To achieve this goal the evaluation of investment in accounts

receivable should involve the following steps

Estimation of incremental operating profit

Estimation of incremental investment in accounts receivables

Estimation of the incremental rate of return of investment

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

Comparison of the incremental rate of return with the required rate of return.

CREDIT TERM:

The stipulations under which the firm sells on credit to customers are called credit terms. These stipulations include: a) the credit period b) the cash discount

CREDIT PERIOD:

The length of time for which credit is extended to customers is called the credit

period. It is generally started in terms of a net date. A firm’s credit period may be

governed by the industry norms. However, depending on its objectives, the firm can

lengthen the credit period on the other hand. The company may tighten it credit period if

customers are defaulting too frequently & bad debt looses are building up.

COLLECTION PERIOD:

A collection policy is needed because all customers are slow payers while some

are nonpayers.The collection efforts should there fore aim at accelerating collections

from slow payers and reducing bad debt looses. A collection policy should ensure prompt

collection is need for fast turnover of working capital keeping collection costs and bad

debts within limits and maintaining collection efficiency. Regularity in collections keeps

debtors alert, and they tend to pay their dues promptly.

Receivables management at Patil Electric Works:

a) To achieve growth in sales

b) To increase profit

c) To meet competition

Credit policy variables in Patil electric works

Credit policy has important implication for the company’s production, marketing and

finance functions.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

CREDIT STANDARDS:

Credit standard are the criteria, which a firm follows in selecting customers for

the purpose of extension.

AVERAGE COLLECTION PERIOD :

The average collection period measures the quality of debtors since it

indicates the quality of their collection the average collection period should

be compared the against firms credit terms and collection efficiency.

Average collection period = Debtors X 360 sales

(Amount in lack)Particulars Amount (2009) Amount (2010)

Debtors 2922.98 4459.29

Sales 43737.84 51258.80

ACP 24 Days 31 Days

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

INTERPRETATION:

The average collection period of the VRL in the year 2008-09 is 24

days and in the year 2009-10 is 31 days since the it is in increasing order. It

indicates that the firm has control over credit facility & credit collection.

PERCENTAGE OF DEBTORS TO NET WORKING CAPITAL:

The ratio indicates percentage of debtors in the net working capital.

Percentage of Debtors to Net Working Capital. = Debtors X 100

NWC

(Amount in lack)Particulars Amount (2009) Amount (2010)

Debtors 2922.98 4459.29

NWC 5348.86 6554.20

Percentage 54.64 68.03

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

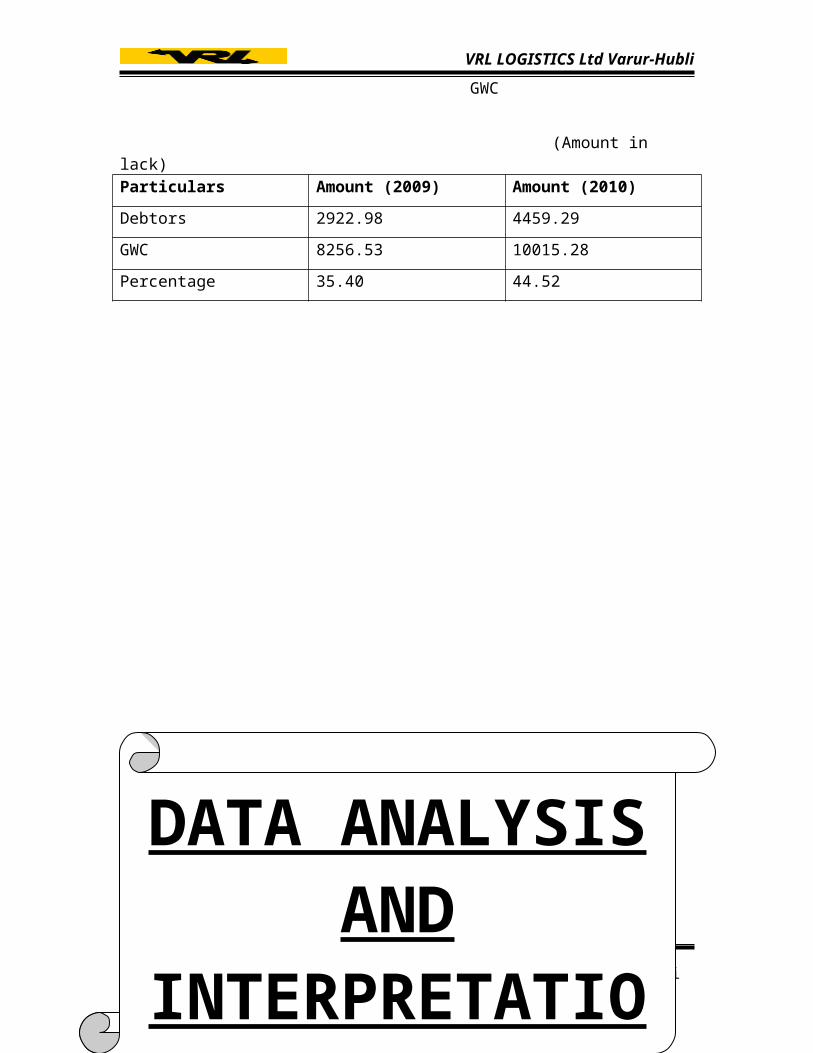

PERCENTAGE OF DEBTORS TO GROSS WORKING CAPITAL:

The percentage of debtors to gross working capital shows the portion of debtors in the current assets.

Percentage of Debtors to Gross Working Capital. = Debtors X 100

GWC

(Amount in lack)Particulars Amount (2009) Amount (2010)

Debtors 2922.98 4459.29

GWC 8256.53 10015.28

Percentage 35.40 44.52

A.S.S’S College of Business Administration, Gadag-Betgeri

DATA ANALYSIS AND INTERPRETATI

ON

VRL LOGISTICS Ltd Varur-Hubli

DATA ANALYSIS AND INTERPRETATION

ASSETS

CURRENT ASSETS

Cash and Bank balance from 2006-07 to 2009-10

YEAR AMOUNT DIFFRENCE

2006-2007 708.15 194.21

2007-2008 1515.85 807.07

2008-2009 1961.89 446.04

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

2009-2010 2391.17 429.28

The Bank balance are the substitutes for cash are most liquid assets for the

company. The more cash and bank balance may be required when there is more operation

to be done. In the last 4 years it has be clear that the highest growth in cash and bank

balance found in the year 2007-08 (807.70).

SUNDRY DEBTORS FROM 2006-07 TO 2009-10

YEAR AMOUNT DIFFRENCE

2006-2007 1721.25 494.00

2007-2008 2371.32 650.07

2008-2009 2922.98 551.66

2009-2010 4459.29 1536.31

A.S.S’S College of Business Administration, Gadag-Betgeri

194.21

807.70

446.04429.28

0

100

200

400

500

600

800

900

2006-07 2007-08 2008-09 2009-10

YEAR

DIFFERENCE

AMOUNT

VRL LOGISTICS Ltd Varur-Hubli

Sundry debtors are debts owned by the customer as goods are sold on credit basis

and are considered to be the most liquid current assets for the firm. As for the calculation,

the highest rate in debtors found in the year 2009-10 at rate of 1536.31.

INVENTORIES FROM 2006-07 TO 2009-10

YEAR AMOUNT DIFFRENCE

2006-2007 869.50 218.03

2007-2008 960.29 90.79

2008-2009 633.06 327.23

2009-2010 686.35 53.29

A.S.S’S College of Business Administration, Gadag-Betgeri

494.00

650.07551.66

1536.31

0

300

600

900

1200

1500

1800

2100

2006-07 2007-08 2008-09 2009-10

YEAR

DIFFERENCE

AMOUNT

VRL LOGISTICS Ltd Varur-Hubli

The inventories constitute that major part of the current assets. The difference

change in growth highest rate over the last 4 years 2008-09 (327.23).

CURRENT LIABILTIES

SUNDRY CREDITORS FROM 2006-07 TO 2009-10

YEAR AMOUNT DIFFRENCE

2006-2007 1596.43 196.97

2007-2008 2794.28 1197.82

A.S.S’S College of Business Administration, Gadag-Betgeri

218.03

90.79

327.23

53.29

0

100

200

300

400

500

600

700

2006-07 2007-08 2008-09 2009-10

YEAR

DIFFERENCE

AMOUNT

VRL LOGISTICS Ltd Varur-Hubli

2008-2009 3355.96 561.68

2009-2010 2944.90 411.06

It may be inferred that the sundry creditors increases to during the year of 2007-

08 (1197.82) As compared to present year 2006-07 (196.97) it will not increase.

OTHER LIABILITIES FROM 2006-07 TO 2009-10

YEAR AMOUNT DIFFRENCE

2006-2007 196.18 129.29

2007-2008 280.43 84.25

2008-2009 105.12 -175.31

2009-2010 109.83 4.71

A.S.S’S College of Business Administration, Gadag-Betgeri

196.97

1197.82

561.68411.06

0

200

400

600

800

1000

1200

1400

2006-07 2007-08 2008-09 2009-10

YEAR

DIFFERENCE

AMOUNT

VRL LOGISTICS Ltd Varur-Hubli

It may be inferred that the other liabilities increased to during the year of 2006-07

(129.29). The present year 2009-10 (4.71). Will be compared with the figure of 2007-08

(-175.31).

Information relating to various current assets

and liabilities includes in the year 2006-07

PARTICULARS AMOUNT PERCENTAGE (%)

Current assets

Cash and Bank balance 708.15 21.47%

Sundry debtors 1721.25 52.17%

Inventories 869.50 26.36%

A.S.S’S College of Business Administration, Gadag-Betgeri

129.2984.25

-175.31

4.71

-200

-150

-100

-50

0

50

100

150

2006-07 2007-08 2008-09 2009-10

YEAR

DIFFERENCE

AMOUNT

VRL LOGISTICS Ltd Varur-Hubli

Total 3298.90 100.00%

Current Liabilities

Sundry Creditors 1596.43 89.06%

Other Liabilities 196.18 10.94%

Total 1792.61 100.00%

Current assets Current Liabilities 21.47% 26.36% 10.94%

26

52.17%

It may be revealed that in the over all composition of sundry creditors are the highest

(89.06%), followed by sundry debtors (52.17%), Inventories (26.36%), cash & bank

balance (21.47%), other liabilities (10.94%).

Information relating to various current assets

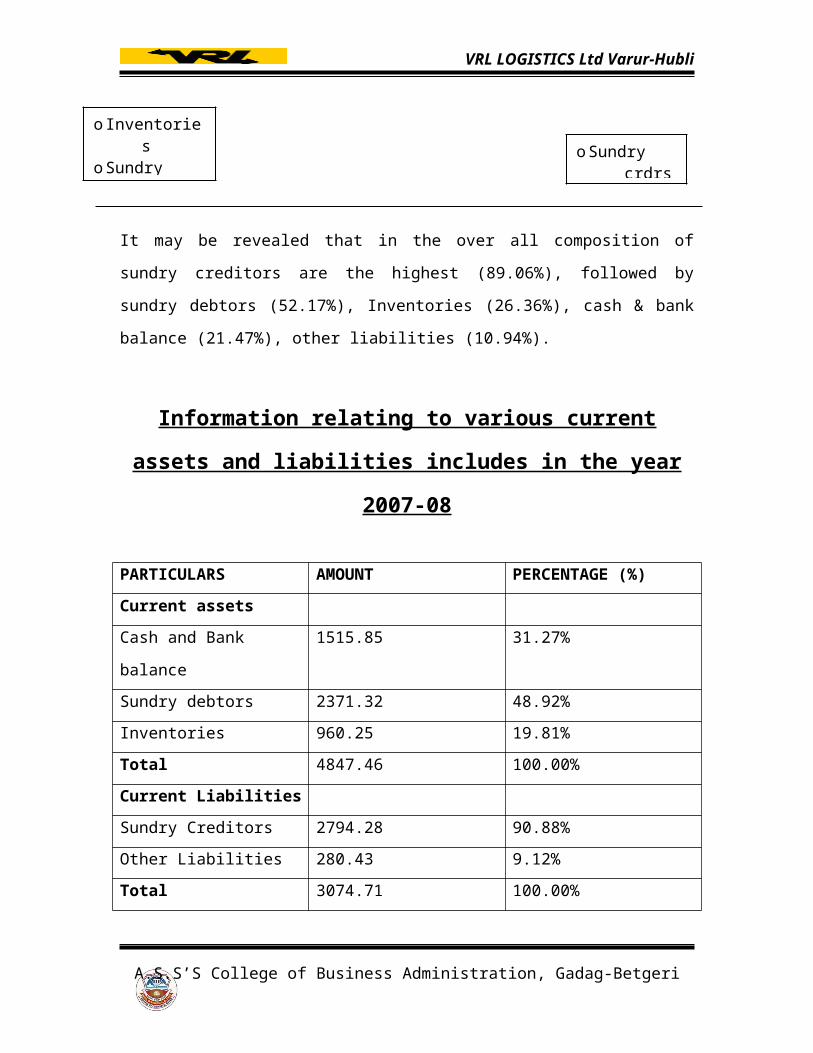

and liabilities includes in the year 2007-08

PARTICULARS AMOUNT PERCENTAGE (%)

Current assets

Cash and Bank balance 1515.85 31.27%

Sundry debtors 2371.32 48.92%

Inventories 960.25 19.81%

A.S.S’S College of Business Administration, Gadag-Betgeri

o InventoriesoSundry DebtoCash & Bank b

oSundry crdrsoOther libet

VRL LOGISTICS Ltd Varur-Hubli

Total 4847.46 100.00%

Current Liabilities

Sundry Creditors 2794.28 90.88%

Other Liabilities 280.43 9.12%

Total 3074.71 100.00%

Current assets Current Liabilities31.27% 9.12%

19.81%

48.92% 90.88%

It may be revealed that in the over all composition of sundry creditors are the

highest (90.88%), followed by sundry debtors (48.92%), cash & bank balance (31.27%),

Inventories (19.81%), other liabilities (9.12%).

Information relating to various current assets

and liabilities includes in the year 2008-09

PARTICULARS AMOUNT PERCENTAGE (%)

Current assets

Cash and Bank balance 1961.89 32.56%

Sundry debtors 2922.98 52.97%

A.S.S’S College of Business Administration, Gadag-Betgeri

o InventoriesoSundry DebtoCash & Bank b

oSundry crdrsoOther libet

VRL LOGISTICS Ltd Varur-Hubli

Inventories 633.06 11.47%

Total 5517.93 100.00%

Current Liabilities

Sundry Creditors 3355.96 96.96%

Other Liabilities 105.12 3.04%

Total 3461.08 100.00

Current assets Current Liabilities32.56% 11.47% 3.04%

96.96%52.97%

It may be revealed that in the over all composition of sundry creditors are the

highest (96.96%), followed by sundry debtors (52.97%), cash & bank balance (35.56%),

Inventories (11.47%), other liabilities (3.04%).

Information relating to various current assets

and liabilities includes in the year 2009-10

PARTICULARS AMOUNT PERCENTAGE (%)

Current assets

Cash and Bank balance 2391.17 31.73%

A.S.S’S College of Business Administration, Gadag-Betgeri

o InventoriesoSundry DebtoCash & Bank b

oSundry crdrsoOther libet

VRL LOGISTICS Ltd Varur-Hubli

Sundry debtors 4459.29 59.17%

Inventories 686.35 9.10%

Total 7536.81 100.00%

Current Liabilities

Sundry Creditors 2977.90 96.40%

Other Liabilities 109.83 3.60%

Total 3054.73 100.00%

Current assets Current Liabilities31.73% 9.10% 3.60%

59.17% 96.40%

It may be revealed that in the over all composition of sundry creditors are the

highest (96.40%), followed by sundry debtors (59.17%), cash & bank balance (31.73%),

Inventories (9.10%), other liabilities (3.60%).

Estimation of Net Working Capital:

Year Current assets Current

Liabilities

Gross Working

Capital

Net Working

Capital

2006-07 3298.90 1792.61 3298.90 1506.29

2007-08 4847.46 3074.71 4847.46 1772.75

A.S.S’S College of Business Administration, Gadag-Betgeri

o InventoriesoSundry DebtoCash & Bank b

oSundry crdrsoOther libet

VRL LOGISTICS Ltd Varur-Hubli

2008-09 5517.93 3461.08 5517.93 2056.85

2009-10 7536.81 3054.73 7536.81 4482.08

A.S.S’S College of Business Administration, Gadag-Betgeri

1506.291772.75

2056.85

4482.08

0

1500

2000

2500

3000

3500

4000

4500

2006-07 2007-08 2008-09 2009-10

YEAR

Net Working Capital (CA-CL)

AMOUNT

VRL LOGISTICS Ltd Varur-Hubli

FINDINGS:

A.S.S’S College of Business Administration, Gadag-Betgeri

GENERAL OBSEREATION

VRL LOGISTICS Ltd Varur-Hubli

There is dedicated workers increase in growth of their turnover

They provide good service that leads to customer satisfaction

The company is recommended by Indian books association Mumbai

They provide training facility

They have good brand image

They provide direct and indirect employment to many people

They did not under go any lockout, strike etc

They have their own in house body building of vehicle

They have new courier service called “CARGO EXPRESS” which refers to the

24 hours of service.

The company is having wide network of branches spread all over Karnataka,

Andhra Pradesh, Madhya Pradesh, Maharashtra, and New Delhi.

SUGGESTIONS:

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

The garage is centralized all the vehicle must have to come Varur for repair and

maintenance

They are highly depend on economic scenario

They only concentrate on rich class of people

There is heavy work load

OPORTUNITIES:

They can enter into hotel business

They can decentralize their garage and office

They can concentrate on remote villages

They can tie up with the government transport service

They can enter into international courier and cargo express service

They can extent their service to north and south station

Another English newspapers to be published out side of the Karnataka

THREATS:

Uncertain policies of changing policy government

Competition can enter into market for leadership

New technology economic slowdown

Maintenance

Competitors

CONCLUSION:

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

The Conclusion of whole the study is that the management of working capital in

the VRL Logistics Pvt. Ltd. Is very good as it is above corporate standard.

The profits of company are also growing with the speed, as the management of

working capital is getting good.

As well as level of working capital liquidity of company is also affected

positively. So the study showing it is true that the working capital is the guiding for the

organization survival growth and profitability.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

BIBLIOGRAPHY:

A.S.S’S College of Business Administration, Gadag-Betgeri

BIBLIOGRAPHY

VRL LOGISTICS Ltd Varur-Hubli

Financial Management : Khan & Jain.

Financial Management : I. M. Panday

Annual Report VRL

www.vrllogistics.com .

www.google.com.

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

ANNEXURES

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri

VRL LOGISTICS Ltd Varur-Hubli

A.S.S’S College of Business Administration, Gadag-Betgeri