Articles Cima Maximizing Shareholder Value

29

Maximising Shareholder Value Achieving clarity in decision-making Technical Report

-

Upload

carlos-farfan-calderon -

Category

Documents

-

view

86 -

download

0

Transcript of Articles Cima Maximizing Shareholder Value

Maximising Shareholder ValueAchieving clarity in decision-making

Technical Report

Maximising Shareholder Value 1

Contents

Preface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

1 Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31.1 Context – conformance and performance . . . . . . . . . . . . . . . . 31.2 What is value-based management (VBM)? . . . . . . . . . . . . . . . 31.3 Shareholder value and the cost of capital. . . . . . . . . . . . . . . . . 5

Sir Brian Pitman . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

2 Creating Shareholder Value – Strategy . . . . . . . . . . . . . . . . . . . . . . 7David Kappler . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

3 Measuring Shareholder Value – The Metrics . . . . . . . . . . . . . . . . . . 103.1 Shareholder value analysis (SVA) . . . . . . . . . . . . . . . . . . . . . . . . 103.2 Economic profit (EP). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 113.3 Cash flow return on investment (CFROI) . . . . . . . . . . . . . . . . . 133.4 Total business returns (TBR) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 143.5 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Steve Marshall . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

4 Managing For Shareholder Value . . . . . . . . . . . . . . . . . . . . . . . . . . . . 164.1 Governance and ownership. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 164.2 Remuneration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Jeremy Roche. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16John Barbour . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

4.3 Culture . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 194.4 Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Charles Tilley . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 214.5 Stakeholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

5 Drawbacks of Value-Based Management (VBM) . . . . . . . . . . . . . . 22

6 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

7 Bibliography. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Since then, all kinds of companies havebeen publicly proclaiming theircommitment to increasing long-termvalue for their shareholders. One lookat the statements of directors or chiefexecutives in annual reports canconfirm this.

To a certain extent this is old news. Wehave heard such pronouncementsbefore. The aim of publicly listedcompanies has always been to increasethe value of shareholders’ investment.

But headlines such as, “Value is the acidtest of good governance”, “Is goodgovernance good value?” or “Returningvalue by governance”, all taken fromthe Financial Times in the last fewmonths, show the influence thataccounting scandals and the marketdownturn of the early 2000’s have hadon corporate discourse.

The debate is now focused on theinterplay between corporategovernance and company success. Theycross at a point where what matters iswhether – and how – a company hascreated value for its owners. Corporategovernance, defined as “the system bywhich the owners of the corporationensure that it pursues, does not deviatefrom and only allocates resources to itsdefined purpose” (LSE and RSM RobsonRhodes, 2004), has become anubiquitous topic here in Europe andeven more so in the US.

Although CIMA believes this ispraiseworthy, there is a danger thatcompanies will assume that, oncecorporate governance has been sortedout, they will know how to manage forshareholder value. The truth is, many donot. These companies will carry onmuch like before, only under increasedscrutiny from both investors and thepublic. In fact, many executives seevalue creation as more of “a corporaterallying cry rather than the goal ofserious strategic planning” (Armour andMankins, 2001).

This briefing is an attempt to drawattention to the context, tools,techniques and philosophy of managingfor shareholder value, or value-basedmanagement (VBM) as it is sometimesknown. It is not meant to beprescriptive. Like other managementconcepts, managing for value has beenadapted by companies to suit theircircumstances. There can be no “one-size fits all” model.

In CIMA’s Official Terminology, VBM isdefined as “a managerial process whicheffectively links strategy, measurementand operational processes to the end ofcreating shareholder value”.

It is generally understood to consist ofthree key elements:● creating value, ie, ways to actually

increase or generate maximum futurevalue;

● measuring value; and● managing for value, ie, governance,

management, organisation, culture,communication.(www.valuebasedmanagement.net)

We aim to outline the main features ofstrategic planning and decision-making,as well as how the chosen strategiescan be delivered via integratedperformance management systems andchanges to organisational culture andstructure.

The briefing is divided into threesections corresponding to the mainVBM components:● strategy – for value creation;● metrics – for value measurement;

and ● management – encompassing

governance, remuneration, culture,structure and stakeholderrelationships.

It also provides insights from seniorfinance professionals with directexperience of managing for value and abrief discussion of some of the keybarriers and drawbacks of attemptingto implement VBM programmes.

As this is a briefing from CIMA, it isprimarily aimed at those working infinance. Finance professionals andaccountants in business should play akey role in VBM implementation. Fewother professionals will have the samecommercial awareness coupled with abroad understanding of both thefinancial issues and the business as awhole.

However, the overview of VBM shouldalso prove a useful introduction foranyone keen to gain a basicunderstanding of the subject.

Maximising Shareholder Value2

Preface

After the market exuberance of the dot com bubble inthe late 1990’s, the sobering up period that followed thebust brought with it a renewed interest in the concept ofshareholder value.

1.1 Context –conformance and performanceWhen corporate scandals started to hitthe headlines in the US and, morerecently Europe, the legislators’response was swift and efficient. Amid aflurry of reviews, consultations anddebates about business ethics, a wholenew raft of legislation was introducedin an attempt to restore faith in capitalmarkets.

On both sides of the Atlantic, much ofthis effort was focused on regulatoryand corporate governance issues. Thiswas hardly surprising, considering thenature and magnitude of the problems.What’s more, it is unlikely that thefocus on corporate governance andregulation is going to wane in comingmonths, despite the inevitable industrybacklash. The reforms continue and, formany, the effects of Sarbanes-Oxley inthe US and the new Combined Code inthe UK are starting to be felt.

There is a danger, however, that thisadmittedly laudable attempt toimprove the way in which companiesare regulated and governed will detractfrom the basics of value creation. Goodcorporate governance may be anecessary prerequisite but will not byitself lead to superior performance –which is, after all, what investors wantand expect in return for their money.

At the beginning of 2004, theInternational Federation of Accountants(IFAC), in partnership with CIMA,published a report entitled, “Enterprisegovernance – getting the balanceright”. It argued for a more holistic wayof looking at companies.

Enterprise governance is defined as:

“the set of responsibilities and practicesexercised by the board and effectivemanagement with the goal of providingstrategic direction, ensuring thatobjectives are achieved, ascertainingthat the risks are managedappropriately and verifying that theorganisation’s resources are usedresponsibly”.(Information Systems Audit and ControlFoundation, 2001).

It has two dimensions – conformanceand performance – which need to bekept in balance. Too much emphasis onone, as the current focus on governancerisks doing, may detract from valuecreation.

This briefing complements the“Enterprise governance” report byacting as a reminder not to overlookthe performance side of the enterprisegovernance framework. It covers thephilosophy and practice of managingfor long-term value.

1.2 What is value-basedmanagement (VBM)?Defining VBM is not easy. There is, onthe one hand, a broad context ofgenerating value for shareholders thatis at the heart of the market economy.But there is also a more specificconcept that narrows VBM into amanagement approach, or even aphilosophy, characterised mainly by themetrics used to measure performance.

In terms of the former- in the Anglo-Saxon context, the maximisation ofshareholder value has been widelyaccepted as a principal, if not the only,bona fide corporate aim.The concept of“enlightened shareholder value” hasbeen enshrined in the recent UKCompany Law Review. The Reviewexplicitly rejected the notion ofpluralism – where a company isrequired to serve a range of interestswider than just those of itsshareholders – as being “unlikely tocommand wide support”.

The Company Law Steering Group citedthe generation of maximum value forshareholders as the ultimate objectivefor companies and in principle the bestmeans of also securing overallprosperity and welfare (StrategicFramework, 1999). It was a simplemessage that emphasised the need tofine-tune the current system, ratherthan radically change it.

Most UK companies would describethemselves as being in the business ofmaximising value for their shareholders.But how that value is defined,measured and pursued is somewhatmore contentious. The rhetoric ofcorporate mission statements may bedivorced from the reality of firms’ day-to-day operations.

We have all witnessed, in the recentaccounting scandals, the extremes ofhow companies can be run forseemingly everything else except theirowners’ best interests. The collapse ofEnron and Parmalat destroyed value forboth their shareholders and theirstakeholders, such as the thousands ofemployees who lost their jobs andpensions. There are also companies,such as Marconi, that failed as a resultof strategic errors, not fraud.

It is not hard to find less spectacularexamples of decisions that do not takelong-term value into account. In manycases, value-destroying decisions arenot driven by greed or dishonesty.Instead, they are the result of pursuinglegitimate business objectives, such asgrowth or increasing market share. Theproblem is that managers often lackunderstanding of the differencebetween decisions that lead to higherprofits and those that create value.

Maximising Shareholder Value 3

1. Introduction

It is interesting to note that 78 per centof companies interviewed for aUniversity of Washington study(Graham, 2004) admitted to artificiallysmoothing earnings and sacrificingshareholder value in order to meet, orbeat, Wall Street expectations. Fifty-fiveper cent also said they would avoidinitiating a project with a very positivenet present value (NPV) if it meantfalling short of the current quarter’sconsensus on earnings.

The picture may not be that dissimilaron this side of the Atlantic. In anattempt to maintain steady earningstreams believed to be preferred byequity analysts and investors, somecompanies seem to forget that theirreason for being is to maximise valuefor investors.

And, because an increasing number ofcompanies are bowing to this pressure,accounting itself can become“unhinged” from value – it is seen as nolonger counting what counts (Stewart,2003). Measures of accounting profit,such as earnings per share, may obscurethe true state of the business. Value-based management is a reminder thatthe way to gauge whether or not acompany is generating value for itsshareholders is to measure thedifference between a return on equityand the cost of capital.

The narrower definition of shareholdervalue management starts with thesame governing objective but addsdifferent ways of measuring andmanaging value. Sections 3 and 4 ofthis briefing describe these in moredetail.

The basic concept of value can betraced back to 19th century economictheory, which pioneered the idea ofresidual income. However, the termvalue-based management andacronyms such as VBM or MSV(managing for shareholder value) werenot used until the mid-1990s byauthors such as Copeland andMcTaggart.

McTaggart defines VBM as:

“…a formal, systematic approach tomanaging companies to achieve theobjective of maximising value creationand shareholder value over time”.(McTaggart et al, 1994)

Copeland sees value-basedmanagement as:

“… an approach to managementwhereby the company’s overallaspirations, analytical techniques andmanagement processes are all alignedto help the company maximise its valueby focusing management decision-making on the key drivers of value”.(Copeland et al, 2000)

Value-based management becamepopular in the mid-1980s whenRappaport published his seminal text,Creating shareholder value: the newstandard for business performance(1986). Companies such as Boots,Lloyds TSB and Cadbury Schweppeswere soon making explicit publiccommitments to increasing value fortheir shareholders. (For a morecomprehensive history of VBM, seewww.valuebasedmanagement.net)

Thanks to the good track record ofthose companies, the ability of VBM togenerate superior returns was, for awhile, unquestioned. During the latestmarket boom and bust, however, itsimage was somewhat tarnished. Asearly as 1998, an article in the FinancialTimes (14 May 1998) questionedwhether VBM was not simply a productof a 16-year bull market.

Predictably, generating value became alot more difficult in times of marketdownturn (although 2002 researchfrom PA Consulting claims that onlycompanies with an explicit VBM agendamanage to create value during bearmarkets). In addition, recent accountingscandals have led some to regardanything related to making money assomehow suspicious. Most importantly,the early and very successful VBMpioneers have not been immune tostrategic and operational problems.

With an improved market outlook, it iseasy to see why shareholder value goesback in favour. Also, pledging allegianceto shareholders can be a good antidotefor being chastised – often unfairly –for abusing managerial positions forpersonal gain. After the collapse ofEnron, the risk of such accusations hasbecome only too real.

It is perhaps time to investigatewhether managing for shareholdervalue can be a part of the solution torestoring faith in capital markets. Someclaim that the performance metrics andthe strong emphasis on accountabilitytypical of VBM programmes canreinforce the focus on performance,while enhancing the checks andbalances of corporate governance.

According to Ken Favaro, cheifexecutive of Marakon Consulting,companies that have “gone to the wallin the last few years never had – or hadtotally relaxed – their standards forgrowing value over time” (Marakon,2003). It was not their corporategovernance arrangements that were atfault, so fixing those would notnecessarily solve the problem.According to Favaro, “making topmanagement more accountable forgrowing the company’s intrinsic value”is the key to protecting shareholderinterests.

Maximising Shareholder Value Introduction4

1.3 Shareholder value andthe cost of capitalDespite the lack of universal definitions,all VBM programmes have in commonthe basic premise that profit needs tobe measured in a way that takes intoaccount the cost of the capitalemployed to generate it.

UK plc has a low debt to equity ratiowhich effectively means that most ofthe capital invested in publiccompanies has come from share issuesor earnings retained. The investors whopurchase shares will only part withtheir cash on a promise of a higherreturn. They would certainly expect thatreturn to be higher than what theycould get from depositing their moneyin a bank almost risk-free. They arewilling to tolerate the higher risk ofequity ownership because of thepotentially higher returns.

This fundamental premise at the heartof Anglo-Saxon capitalism containswithin it a simple, yet frequentlyforgotten, notion: that there is aminimum acceptable return oninvestment. In other words, it is notonly the debt capital which is costly –although it is more obviously sobecause of the interest rate applied bythe lender – but the equity capital too.

The cost of equity capital is anopportunity cost and it is this thatmakes it more difficult to express insimple terms. Unfortunately, thiscomplexity makes it easier to ignorewhen making profit calculations. But itis no less ‘real’ for that: if theshareholders fail to get the desiredreturn on their investment, they willeventually invest their moneyelsewhere.

The basic tenet of managing forshareholder value is that the cost ofequity capital must be taken intoaccount when calculating value. That is,a company only makes a real oreconomic profit after it has repaid the

cost of capital that was used togenerate it:

“The most egregious error accountantsare now making is to treat equitycapital as a free resource. Although theysubtract the interest expenseassociated with debt financing, they donot place any value of the fund thatshareholders have put, or left, in abusiness. This means that companiesoften report accounting profits whenthey are in fact destroying shareholdervalue.”(Stewart, 2003)

This happens in some companies today,not just in terms of headline figuresreported to markets but at all levels.Managers charged with makingdecisions about strategic planning orresource allocation may never considerthe cost of equity capital.

Instead, their actions will be governedby any number of received businesswisdoms about growth, innovation,customer satisfaction, market share,etc. These are the common – andfrequently conflicting – choicesavailable. Most managers will struggleto prioritise them (and the differentgroups of stakeholders they represent)or understand the causal relationshipsbetween these objectives and asustained growth in profits.

Value-based management is anattempt to get back to the basics ofvalue creation and focus on whatmatters to those who own thecompanies: an acceptable return ontheir capital.

CIMA’s Official Terminology defines thecost of capital as:

“The minimum acceptable return on aninvestment, generally computed as ahurdle rate for use in investmentappraisal exercises. The computation ofthe optimal cost of capital can becomplex and many ways ofdetermining this opportunity cost havebeen suggested.”

The cost of capital depends on theriskiness of projects being evaluated.Davies et al (1999) define it as “theweighted average of the costs of thevarious investments of which thecompany is made up”, determined bythe risk of the firm’s investmentopportunities. It consists of thecombined costs of equity and debt.

Measuring the cost of capital relates toreturns on new investments rather thanwhat happened in the past. The equitypart of it will be determined by the riskto which equity holders are exposed(Davies, 1999). Because of this, therecan be no exact way of calculating it,especially on the level of company as awhole (see Gregory et al, 1999 andDavies et al, 1999).

Companies should think hard about aprecise number for the cost of capital,although the “correct” answer does notexist. Also, an approximate figureapplied consistently is better thanassuming that shareholder capital hasno cost at all.

Maximising Shareholder Value Introduction 5

Sir Brian Pitman, former chief executive and chairman of Lloyds TSB

The ability to generate consistently superior total shareholder returns overtime is the best single measurement of corporate management performance,claims Sir Brian Pitman, former chief executive and chairman of Lloyds TSB.

But it is also the most challenging objective that a company can set itself. “Itrequires delivering outstanding levels of current performance while building alegacy for the future,” he says. “Those few companies that achieve it are hailedfor their ability, year after year, to generate wealth for their owners in excess oftheir competitors.”

One of the great advantages of shareholder value as a governing objective isthat it demands continual improvement, according to Pitman. “There is no timewhen you can sit back and admire your achievements. The measurement isobvious to all, both inside and outside of the company. There is no hidingplace.”

It also allows chief executives to raise management performance and creategreater involvement and excitement within the company.

“Setting ambitious goals forces the organisation to dig deeper for creativesolutions and to rethink how the business should be run. It doesn’t permitincremental thinking. The objective is to win, not just improve.”

Differentiating the business from the competition is the key to generatinggreater shareholder returns, PItman says. He cites his time as chairman atclothing retail group Next. “Retail businesses, such as Next, can differentiatethemselves through service and the quality of garments. If you are selling askirt that is different from the competition and the customers like it, then youwill win more business.”

Price is often a key differentiator, such as with the low-cost airlines. The cleverbusinesses create a product that they sell for a premium, however.

“The retro radio made by Roberts is a good example. People don’t buy it justfor the sound quality but for what it looks like. And Bang and Olufsen hasmanaged to create a lifestyle around its equipment. People pay money forwhat is says about them.”

By creating this difference, a firm will be more successful and create bettervalue for its shareholders.

Organisations that adopt shareholder value management must revise their paypolicies to support the new focus. The aim is for employee and shareholderinterests to become inherently similar. Increasing employee ownership of thecompany’s shares, through profit-sharing schemes, share saving schemes andshare option schemes, is a key way of achieving this, according to Pitman.

Maximising Shareholder Value Introduction6

It is one thing to say that companiesought to be managed for shareholdervalue but quite another to try toprovide guidance on the best way ofachieving this. Creating value is notabout applying a prescribed set of toolsor processes but about creatingcompetitive advantage in themarketplace. Strategy lies at the heartof enterprise success: “Managing forvalue begins with strategy and endswith financial results.” (Knight, 1998)

The focus on strategic planning hasbeen one of the hallmarks of managingfor value. In VBM, successful strategiesdon’t just happen. They are not theresult of good fortune, individual geniusor a having a “lucky run”. Instead, theyare the end product of a structured anddisciplined decision-making process.

It is surprising how casual strategicdecision-making can be in manycompanies. Mankins (2004) claims thattop management spend less than threehours a month discussing strategyissues (including mergers andacquisitions) or making strategicdecisions. Instead, his researchconfirmed that “80 per cent of topmanagement’s time is devoted toissues that account for less than 20 percent of a company’s long term value”.

Admittedly, strategy is not somethingthat can easily be taught, despite theproliferation of MBA courses. There willalways be room for intuition and “gutfeeling”. But there are also ways ofmaking the actual process of decision-making – rather then just the outcomes– more structured and explicit. Theresulting transparency should helpcompanies understand where value iscreated and destroyed and pinpoint thereal drivers of value.

Understanding value drivers and theirinteractions is, without doubt, thehardest part of developing strategy. ThePwC Management Barometer Surveyfound that 69 per cent of executives intheir sample reported that they hadattempted to demonstrate empiricalcause-and-effect relationships betweenthe different categories of value driversand value creation and future financialresults. However, less than one third ofthese felt they had truly completed thetask. Sixty one per cent had made atleast a modest attempt to combine thenumerous cause-and-effectrelationships into an overall businessmodel but only 10 per cent felt theyhad really nailed it.(DiPiazza et al, 2002)

Instead of having confidence in what isundoubtedly the determining factor oftheir market success or failure,companies’ strategic planning is doggedby uncertainty. One executive involvedin McKinsey research about strategicplanning called it “a primitive tribalritual”, adding that “there is a lot ofdancing, waving of feathers and beatingof drums. No one is exactly sure whywe do it, but there is an almostmystical hope that something good willcome out of it.” (McKinsey Quarterly,2002)

In VBM, the presence of a single,governing objective makes the processboth easier and harder.

It is easier because there is no need forthe trade-offs between differentobjectives that encumber traditionalstrategic planning.

But it is also harder, as the choice thatadds the most value may go against theaccepted wisdom of what constitutessuccess. For example, a path thatmaximises shareholder value may, infact, depress market share. Manymanagers would intuitively regard thisas a negative outcome.

When Lloyds TSB started managing forvalue, its board decided to divest someof its overseas businesses. The decisionwas widely regarded as strategic suicidebecause the US banks it owned wereseen as a springboard into Americanmarket. But Lloyds realised that thecontinuing US presence was a route tothe destruction of shareholder valueand little else.

It is not only the priorities dictated bythe governing objective that makestrategic planning more disciplined inVBM companies. It is also theunrelenting focus on good qualityperformance information and on thecreation of alternative strategies andthe means of implementing them.

Good quality information is necessaryfor both strategic and operationaldecisions. In many companies, time iswasted trying to obtain and reconcilenumbers from different systems. Thismeans that there is no integrated,single view about where the value isbeing created or destroyed in thebusiness. This, in turn, makes theallocation of resources more akin tospeculation, rather than strategicchoice.

“Most organisations are rich in data andcluttered with incomparable systems.Some are succeeding in extracting thedata that they need to make rapiddecisions by, for example, building datawarehouses. However, the majority arestruggling. The information they receiveis incomplete, defective or too out-of-date to be useful in making rapid, well-informed decisions about the future.Often, they are unable to interpret thedata or its implications. At the sametime, the pace of change isaccelerating. The environment in whichfirms must operate, and its impact ontheir organisation, is becoming lesspredictable and more threatening. Lackof correct information, combined withrapid change, makes effective decision-making even more critical.”(Fahy, 2001)

Maximising Shareholder Value 7

2. Creating Shareholder Value – Strategy

For some companies, improvinginformation quality will require a largeone-off investment in informationtechnology infrastructure. However,managers should be warned againstspending large amounts of money in aquest for 100 per cent accuratereporting in real time. In many cases,having the right technology is nowherenear as important as building asupportive culture or fostering effectivecommunication that will facilitate themore informal sharing of knowledge.

In addition, some research shows thathigh-performing companies do notnecessarily have better informationthan their competitors – they just domore with it. In his managementblockbuster “Good to Great”, JimCollins (2001) claims that the key liesin installing “red flag” mechanisms thattransform available, although imperfect,data into relevant information thatcannot be ignored.

Generating the relevant information fordecision-making is only the first,relatively simple, step in the process ofstrategic planning. The most difficultpart is devising successful strategiesthat are going to give a company itscompetitive edge in the marketplace.

In VBM companies, managers arefrequently expected to come up withseveral strategic options, rather thanone “answer”. These are then discussedbefore the option with the beststrategic fit is chosen. Importantly, thechoices presented have to beconsidered and realistic, not chosen fortheir ability to make the preferredoption look better. Mankins (2004)argues that “they must be realalternatives, not just minor variationson a single theme”.

While at Lloyds TSB, Sir Brian Pitmanused to tell his managers that “there isalways a better strategy than the onethat you have; you just haven’t thoughtof it yet”. He required them to produceat least three different strategicoptions.

His view is echoed by John Barbourwho, during his presentation at theCIMA 2003 conference on shareholdervalue, reminded the delegates thatstrategy is never a simple matter ofchoosing from a yes/no proposition.

Barbour also pointed out thatcompanies need to come up with notonly different strategic solutions but

also different approaches toimplementation. There is rarely only oneindisputably and absolutely superiorway of doing things. Most of the time,there are different (and sometimescompeting) choices, including decisionsabout when and where different optionsought to be pursued and what theresource requirements of decisions arelikely to be.

Maximising Shareholder Value Creating Shareholder Value – Strategy8

The case of SmithKline Beecham, as described by the Harvard Business Review(March/April 1998), illustrates the potential benefits of a structured approachto strategic planning and resource allocation.

Any large company with many different projects can struggle to establish clearpriorities for funding. The problem can be particularly acute in pharmaceuticalcompanies with different drugs in the pipeline. It is practically impossible forone person to have a complete overview of every project or drug beingdeveloped, especially considering the scientifically complex nature of theindustry.

In SmithKIine Beecham, each project champion used to present his or her owncase for funding. Inevitably, decision-making became heavily politicised as thefinal choices about resource allocation owed more to the advocacy andpolitical skills of project champions than to the project’s inherent worth to thecompany. Even when there was an attempt to evaluate individual projects,there was no real transparency to the process. No one could be sure that theassumptions and the quality of thinking that went into the evaluations were atleast consistent, if not always good.

SmithKline Beecham’s approach was to get project teams to create watertightalternatives to current plans. They had to consider what their strategy wouldbe if they had less, more or the same amount of funding, as well as if theproject was abandoned but they had to preserve the value earned so far.

Once this was done, the alternatives were presented to a peer review board,which tested the fundamental assumptions of each scenario. The teams thenrevised them, as appropriate, before they were reviewed again, this time bysenior managers.

The strategic options were created and reviewed before any evaluation tookplace. SmithKline Beecham maintained that premature evaluation had adetrimental effect on creativity – which is crucial in R&D. The evaluation wasconducted later, using consistent methodology throughout the process. Projectteams were also asked to provide sets of clearly documented and comparableinformation, originating from a reliable source. The assessments thenunderwent further peer review before a portfolio was finally created andresources allocated.

Such a structured, phased and documented approach facilitates a sharedunderstanding of all of the factors that drive value. Importantly, it also createsan audit trail for each project pursued or abandoned. The consistency ofinformation collected along the way allows anyone to examine the data andthe assumptions that went into choosing a portfolio.

There is a danger, however, thatapproaching strategic planning in suchan analytical way runs the risks of “overintellectualising” decision-making. Theexercise of strategic planning mayeventually get in the way of runningthe company. This is precisely whatBoots – one of the VBM pioneers – hadbeen accused of doing by its new chiefexecutive (Financial Times, 26 October2003). Shortly after his appointment,Richard Barker was reported to bedismayed at finding very few realretailers within the company’s staff,while analysts were questioning theneed for 7,000 staff at its Nottinghamheadquarters.

Finally, strategic plans can never beaccurate predictions of the future,despite the rigour of VBM. Perfectforecasts remain impossible and VBM isno guarantee of success. All it can do isto make the various assumptions thatnormally go into decision-making alittle more explicit. And this, in turn,means that decisions aboutinvestments or resource allocation canbe better explained and justified, bothwithin the company and externally toinvestors.

What investors want to know is notjust how the company performed in thepast but how it is likely to perform inthe future. They can glean this from thequality of its management and itsstrategic capability. After all, this iswhat separates the excellent from themerely good.

To conclude, VBM does give “greaterrealism to otherwise vague strategies”(Johnson, 2002) even if it does notremove all of the inherent uncertaintiesof strategic planning.

David Kappler, former chief financial officer, Cadbury Schweppes

Shareholder value is technically reinvested dividends and share priceappreciation but how this links into a business is rather judgmental, says DavidKappler, Cadbury Schweppes’ former chief financial officer.

Cadbury Schweppes considered growth in economic profit as the key driver tocreating shareholder value.

Some firms regard free cash flow as the driver and this is broadly similar toeconomic profit. However, economic profit is more useful, argues Kappler.

“It’s transferable to individual businesses and unit levels, whereas cash flow is acorporate number. But in choosing a measurement you can’t be over academic.You have to be pragmatic, with a basis of science underpinning the method.”

Kappler argues that a shareholder value measurement must allow the firm todrill down and translate that measurement to individual business units.

“Growth in economic profit is a metric that individual managers can see andmeasure. For example, if the board decides it wants to increase economic profitby 15 per cent, then they can pass that figure down to individual businessesand get them to increase economic profit in their businesses or divisions.”

Economic profit can also be easily linked to incentive and remuneration plans.At Cadbury Schweppes, for example, economic profit is the major element inthe annual incentive plan at group and business level.

But growth in economic profit is not going to increase the share price on itsown, as the share price is based on more subjective things than that.

“You need an investor relations programme to explain strategy, long-terminvestment decisions, and mergers and acquisitions activity, as all these arelinked to the growth of economic profit and it all builds shareholder value,” heasserts.

Maximising Shareholder Value Creating Shareholder Value – Strategy 9

Written by Stuart Cooper,lecturer in finance and accounting,Aston Business School andMatt Davies, senior consultant ofThe Financial Training Company

Throughout the late 1980s and 1990sthere have been a growing number ofconcerns raised about traditionalaccounting measures. These criticismsare primarily concerned with the scopefor subjectivity that even the mostcomprehensive accounting standardsallow. A number of consultants, such asRappaport (1986) and Stewart (1991),recognised these problems. As a result,they turned to the concept ofshareholder value and how this can becreated and sustained. This has, in turn,led to the development of a number of“value metrics”, the most significant ofwhich are:

● shareholder value analysis (SVA)● economic profit (EP) and economic

value added (EVA®)● cash flow return on investment

(CFROI)● total business returns (TBR)

Each of these types of metrics isadvocated by a number of consultantsand has been adopted by companies inthe UK and elsewhere. It is argued thatthese metrics can be used for numerouspurposes, including valuation, strategy,evaluation and the monitoring ofperformance. There are significantdifferences between the different valuemetrics but in each case it is agreedthat the primary objective of acompany should be to maximiseshareholder wealth. Therefore, each ofthe metrics attempts to measure valuecreation for shareholders.

We will consider how each metric iscalculated and identify some of the keydifficulties in using them in practice.

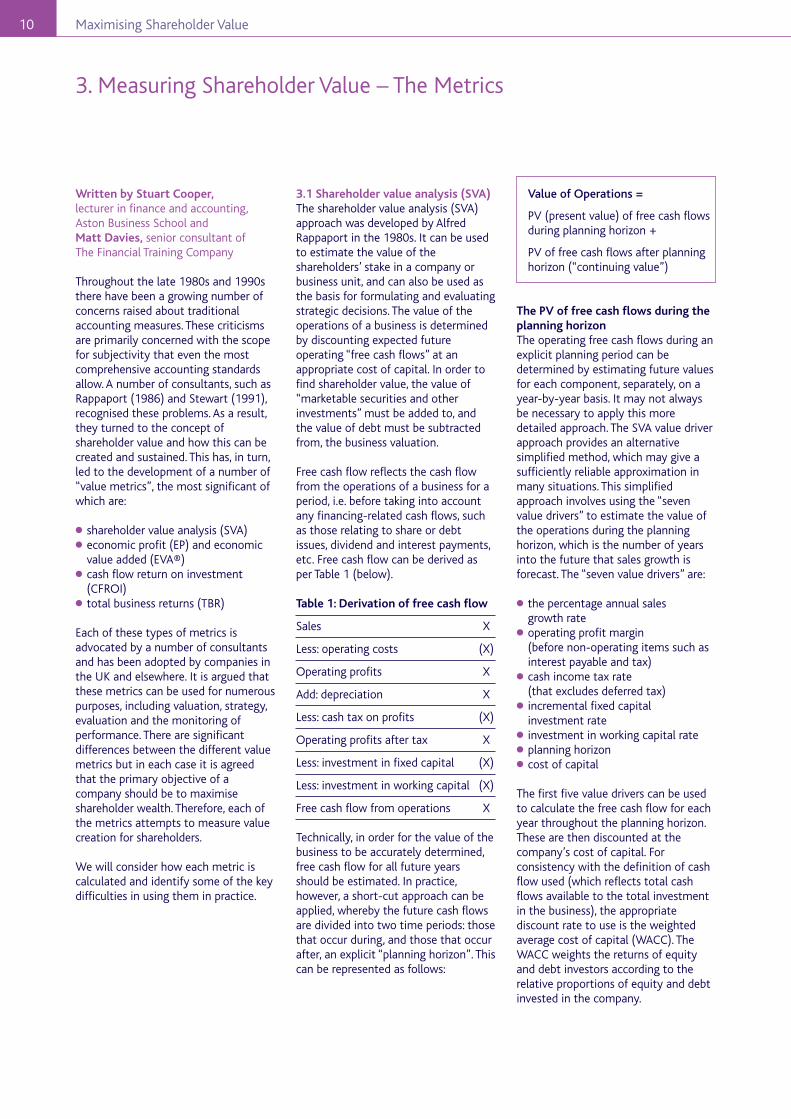

3.1 Shareholder value analysis (SVA)The shareholder value analysis (SVA)approach was developed by AlfredRappaport in the 1980s. It can be usedto estimate the value of theshareholders’ stake in a company orbusiness unit, and can also be used asthe basis for formulating and evaluatingstrategic decisions. The value of theoperations of a business is determinedby discounting expected futureoperating “free cash flows” at anappropriate cost of capital. In order tofind shareholder value, the value of“marketable securities and otherinvestments” must be added to, andthe value of debt must be subtractedfrom, the business valuation.

Free cash flow reflects the cash flowfrom the operations of a business for aperiod, i.e. before taking into accountany financing-related cash flows, suchas those relating to share or debtissues, dividend and interest payments,etc. Free cash flow can be derived asper Table 1 (below).

Table 1: Derivation of free cash flow

Sales X

Less: operating costs (X)

Operating profits X

Add: depreciation X

Less: cash tax on profits (X)

Operating profits after tax X

Less: investment in fixed capital (X)

Less: investment in working capital (X)

Free cash flow from operations X

Technically, in order for the value of thebusiness to be accurately determined,free cash flow for all future yearsshould be estimated. In practice,however, a short-cut approach can beapplied, whereby the future cash flowsare divided into two time periods: thosethat occur during, and those that occurafter, an explicit “planning horizon”. Thiscan be represented as follows:

Value of Operations =

PV (present value) of free cash flowsduring planning horizon +

PV of free cash flows after planninghorizon (“continuing value”)

The PV of free cash flows during theplanning horizonThe operating free cash flows during anexplicit planning period can bedetermined by estimating future valuesfor each component, separately, on ayear-by-year basis. It may not alwaysbe necessary to apply this moredetailed approach. The SVA value driverapproach provides an alternativesimplified method, which may give asufficiently reliable approximation inmany situations. This simplifiedapproach involves using the “sevenvalue drivers” to estimate the value ofthe operations during the planninghorizon, which is the number of yearsinto the future that sales growth isforecast. The “seven value drivers” are:

● the percentage annual salesgrowth rate

● operating profit margin(before non-operating items such asinterest payable and tax)

● cash income tax rate(that excludes deferred tax)

● incremental fixed capitalinvestment rate

● investment in working capital rate● planning horizon● cost of capital

The first five value drivers can be usedto calculate the free cash flow for eachyear throughout the planning horizon.These are then discounted at thecompany’s cost of capital. Forconsistency with the definition of cashflow used (which reflects total cashflows available to the total investmentin the business), the appropriatediscount rate to use is the weightedaverage cost of capital (WACC). TheWACC weights the returns of equityand debt investors according to therelative proportions of equity and debtinvested in the company.

Maximising Shareholder Value10

3. Measuring Shareholder Value – The Metrics

The PV of free cash flows beyond theplanning horizon The second component of the valuationof the operations of a business is thepresent value of operating free cashflows that arise beyond the planninghorizon. This value is often referred toas the “continuing” or “terminal value”.For most companies operating incompetitive industries, it is unlikely thata business that is generating excessreturns on capital will be able to sustainthis for an extended period of time. Apoint will be reached when returnshave been driven down to the cost ofcapital, and a “steady-state” situation isreached. An assumption is usually madethat in the post-planning period, thebusiness will earn, on average, its costof capital. In other words, additionalinvestment would neither create, nordestroy, value and so the effect of newinvestment beyond the planninghorizon can be ignored. As a result, anassumption often made with SVA isthat the cash flow arising in the finalyear of the planning period willcontinue to arise into the future, toinfinity.

The advantages and disadvantages ofSVAAs seen above, SVA can be used tovalue a business. It can also be used toevaluate alternative strategic decisions,by comparing the pre- and post-strategy value of the business.Furthermore, the simplified approach,which emphasises the seven key valuedrivers, lends itself to “sensitivityanalysis”. (Sensitivity analysis involvesassessing the effect of changes inassumptions on the value of a businessor strategy. It can be a particularlyuseful way of identifying the criticalvariables that affect shareholder value.)

Shareholder value analysis can alsohave relevance in an operationalcontext. The seven key value drivers canbe broken down into more detailed andpractical performance measures andtargets, so that managers areencouraged to act in ways that areconsistent with the ultimate objectiveof creating shareholder wealth. Themost significant problem with thistechnique is predicting the variablesrequired in the analysis.

3.2 Economic profit (EP)Another method for determiningshareholder value is by using theeconomic profit (EP) approach.Economic profit has been used, usuallyunder the name “residual income”, as ameans of measuring divisionalperformance for more than 30 years(see Solomons, 1965).

The basic EP approach, however, can betraced back to the work of theeconomist Alfred Marshall (1890).

This section first considers the basic EPapproach. It then examines how thishas been refined by the US consultants,Stern Stewart, to produce EconomicValue Added or EVA®.

Economic profit describes the surplusearned by a business in a period afterthe deduction of all expenses, includingthe cost of using investors’ capital inthe business. The accounting measureof net profit does not gauge this, sincealthough there is a deduction for theinterest charged on debt capital, thecost associated with using equity fundsis ignored. Advocates of the EPapproach argue that net profit ismisleading and that some companiesthat are apparently profitable, based onaccounting profit, can be shown to beeconomically unprofitable using the EPmeasure. Economic profit is thedifference between the return oncapital and the cost of capital and canbe calculated in two ways, as shownbelow:

1 EP = Invested capital x(return on capital – WACC)

2 EP = Operating profits aftertax less capital charge

The first approach clearly demonstratesthat EP represents the amount ofcapital invested in a business multipliedby the “performance spread”, whichrepresents the difference between thereturn achieved on the invested capitaland the weighted average cost ofcapital. The second approach deducts acapital charge (calculated as investedcapital x WACC), from operating profitsafter tax. Operating profits refer to theprofits of a business before deductingnon-operating items, such as interestreceivable, investment income andinterest payable.

It is tempting to think that operatingprofits after tax are simply profits,before interest, less the taxation charge.This, however, ignores the effect of theabove non-operating items on the taxcharge for the business. Under the UKtaxation system, interest payable is atax-deductible expense, whereas as ageneral rule, interest receivable andinvestment income is taxable income.In other words, for a company with anet interest expense, the tax charge inthe profit and loss account has beenreduced by the tax shield effect ofinterest.

To arrive at the true after-tax profitsfrom operations, the tax charge mustfirst be adjusted to reverse this effect.This can be estimated by multiplyingthe net interest payable figure in theprofit and loss account by the marginalrate of corporation tax.

The adjusted tax charge effectivelyrepresents the tax payable by thecompany if it had been entirely equity-financed, and had no non-operatingincome. If this adjustment is not made,the way in which a company has beenfinanced will distort the calculatedreturn.

Maximising Shareholder Value Measuring Shareholder Value – The Metrics 11

EP as a valuation toolAlthough economic profit may appearto be a short-term, single-periodmeasure, an important feature of thisapproach is that it has a direct link withlong-term value based on the free cashflow approach.

In mathematical terms, long-term value(the present value of expected futurefree cash flow) equals the sum of thepresent value of all expected futureeconomic profits, plus the initial capitalinvestment. In other words, theeconomic profit approach can be usedas the basis for corporate or businessunit valuations. This property ofeconomic profit was recognised byO’Hanlon and Peasnell (1996), whostate that:

“... even if accounting book values andprofits bear little resemblance toeconomic reality, EP numbers can beused within a valuation model that hasjust as strong a theoretical basis as thestandard dividend capitalisationmodel”.

The advantages and disadvantagesof EPAs shown above, EP can be used tovalue businesses. It can also be used tomeasure and evaluate performance andto fulfil a more strategic role. Theintroduction of EP would also berelatively straightforward, as it requirestwo adjustments to reported operatingprofit, to adjust the tax charge and todeduct a charge for the cost of capital.At the business level, EP can be used toset the performance targets for thebusiness, and providing that thebalance sheet information exists,performance against these targets canbe tracked via the establishedaccounting system.

The use of traditional accountingnumbers, based on the same rules,conventions and policies that governthe production of published accounts is,however, a significant drawback of thisapproach. For example, the distortingeffects of inflation and depreciationcould well undermine the validity ofthe calculations.

As with the SVA approach, it is possibleto identify a number of value-driversthat can be used to develop moredetailed specific performance targetsand indicators. There are three keyfactors that influence economic profit:

● the return on capital achieved;● the cost of capital; and● the growth of new capital.

It is useful to recognise that the returnon capital generated by a businessdepends upon the combination ofprofit margins achieved relative toturnover (“margin”) and the ability ofthe business to generate turnover fromcapital invested (“efficiency’”). In otherwords, an improvement in the return oncapital requires an improvement in thecombination of “margin” and“efficiency” for the business. (Return oncapital can be further analysed into itsconstituent elements via what is knownas the ‘ROCE tree’, or DuPont chart.)

Economic value added (EVA®)Economic value added (EVA), asexplained by Stewart (1991), iseffectively a refined version of the basicEP approach discussed above and isdemonstrated by the formulae below.

EVA = Adjusted invested capital x(adjusted return on capital –WACC)

EVA = Adjusted operating profitsafter tax less capital charge

EVA = Adjusted operating profitsafter tax less(adjusted invested capital xWACC)

Generally speaking, Stern Stewartsuggests that the basic EP calculation isundermined by three distorting factors.These are the effect of:

● non-cash, accruals-basedbookkeeping entries, which tend toconceal the true “cash” profitabilityof a business;

● the fundamental accounting conceptof prudence, which tends to lead to asystematic conservative biasaffecting the relevance of reportedaccounting numbers;

● ”successful efforts accounting”whereby companies write-off costsassociated with unsuccessfulinvestments, which tends tounderstate the ‘”true capital” of abusiness, and also potentiallysubjects the profit and loss accountto one-off, non-recurring gains orlosses.

To overcome these distortions, SternStewart advocate that up to 164adjustments be made to the measureof operating profits and capital, onwhich EVA is based. These adjustmentsare applied, where appropriate, to bothoperating profits and capital to ensureconsistency in the calculation of EVA.Perhaps the two most commonadjustments are to add cumulativegoodwill written off and the presentvalue of capitalised operating leases tothe value of capital.

Advantages and disadvantagesof EVAThe EVA approach possesses all of thekey advantages of the basic EPapproach. In addition, the adjustmentsrequired for EVA described above seemto address some of the accounting-related weaknesses with the basicapproach.

Maximising Shareholder Value Measuring Shareholder Value – The Metrics12

Making all of the recommendedadjustments, however, could be a time-consuming and costly exercise involvingsome rather arbitrary judgements. To befair, Stern Stewart do not recommendthat all 164 adjustments are needed forevery company.

“In most cases, we find it necessary toaddress only some 20 to 25 issues indetail – and as few as 5 to 10 keyadjustments are actually made inpractice. We recommend thatadjustments to the definition of EVA bemade only in those cases that pass fourtests below.– Is it likely to have a material impact

on EVA?– Can the managers influence the

outcome?– Can the operating people readily

grasp it?– Is the required information relatively

easy to track or derive?”(Source: Stewart, 1994)

3.3 Cash flow return on investment(CFROI)In essence, CFROI is a “real” (i.e.,adjusted for the effect of inflation) rateof return measure, which identifies therelationship between the cashgenerated by a business relative to thecash invested in it. It is argued thatCFROI provides an accurate measure ofthe economic performance of abusiness, free from potentialaccounting distortions relating to issuessuch as inflation and variations in assetages. As well as providing a “superior”measure of current performance, it isalso promoted as “the performancemeasure which best predicts futurecash generation” (Braxton, 1991).

In its more sophisticated form, CRFOIincorporates the principles of theinternal rate of return (IRR) concept,which is more often associated withthe appraisal of capital investmentopportunities. Specifically, CFROIrepresents the “discount rate” that“discounts” the future annual cashflows that are expected to arise overthe average life of a firm’s assets, backto current cash value (i.e. adjusted forinflation) of the firm’s net operatingassets.

The calculation requires threeimportant stages:

● First, accounting profit is convertedinto “real cash flow” for the period.This involves adjusting for non-cashprofit and loss account items andnon-operating items.

● Secondly, the balance sheet value ofthe capital invested in the business isconverted into an inflation-adjustedmeasure of investment in thebusiness, described as “gross assets atcurrent cost”. Gross assets includeoff-balance sheet assets, but excludegoodwill. The inflation adjustmentreturns assets to their full historicalcost. This is then adjusted for theeffects of general price inflation.

● Finally, the annual cash performanceis converted into a measure ofeconomic performance over theaverage life of the firm’s assets, usingthe principles of IRR. This requires theaverage life of the firm’s assets to beknown and, in addition, the value ofnon-depreciating assets (such as landand working capital, which areassumed to be released at the end ofthe firm’s life) to be estimated. Oncethis information has been obtained,an IRR calculation is performed todetermine the discount rate (“r”)that solves the following equation.

Gross operating assets(current prices) =

CF1 CF2 CFt NDA+ + ... + +

(1+r) (1+r)2 (1+r)t (1+r)t

Where:CFn represents the real cash flow ineach year for the average life of thefirm’s assets.NDA represents non-depreciatingassets.

With this approach, CFROI measuresthe cash profitability of a business for aspecific year, and represents theaverage projected rate of return fromall of a business’ existing projects at aparticular point in time. It can becalculated separately for each yearusing the above approach, enabling thetrend in CFROI performance to beanalysed. Furthermore, CFROI can becompared to the company’s “real” costof capital to identify the CFROIperformance spread. As we saw with EP,investing at a positive performancespread will create value forshareholders.

CFROI and valuationCash flow return on investment is aperformance measure and no more orless a valuation technique than EP orSVA. Advocates argue that CFROIprovides a superior basis for predictingfuture cash flows that can then beinput into conventional cash-basedvaluation methods, thereby producingmore accurate valuations.

There are two key features of theCFROI approach to valuations.

1 The valuation process is separatedinto two component elements:

● the value of cash flows arising fromexisting assets; and

● the value of cash flows arising fromfuture investments.

The cash flows from existing assets canbe expected to “wind down” over theremaining life of these assets and, atthe end of this period, cash flowsrelating to the release of non-depreciating assets will also arise.

Maximising Shareholder Value Measuring Shareholder Value – The Metrics 13

For future investments it is assumedthat the rate of return on newinvestments and the rate of growth ofnew investment will, as a result ofcompetitive forces, regress towards thelong-term “economy wide” averagelevels. Or, in other words, cash flowsarising from new investments aredetermined by “fading” future CFROIsand capital growth rates so that theyapproach long-term market averages.

2 A company-specific cost of capital isapplied to discount future cash flows.However, here the most popularapproach for defining the cost ofcapital – the capital asset pricingmodel (CAPM) – is rejected and analternative approach is advocated.

“We derive investors’ required returnsfrom the observed relationship overtime between stock prices andexpected cash returns. Put simply, theinvestors’ required return is thediscount rate which, when applied to acompany’s forecast cash flows, best fitsits stock price history. For most firms,the company-specific discount rate lieswithin a percentage or two of themarket’s required rate of return.”(Braxton Associates, 1991)

Advantages and disadvantagesof CFROIAdvocates claim that CFROI is asuperior measure of performance thatprovides the basis for more accuratebusiness valuations. The keyjustification for using this approach isthe argument that of each of themetrics available, it most accuratelyreflects the way in which the stockmarket judges a company’sperformance. One of the keyadvantages of CFROI as a measure ofperformance is that, unlike theEP/EVA®‚ models, it is neither distortedby the effect of inflation nordepreciation.

There are, however, some practicaldifficulties with the CFROI calculation.

Arguably, the calculations required aretime consuming and costly to apply.Determining the appropriate inflationadjustment to apply to fixed assets, forexample, requires an estimate to bemade of the average age of assets andan appropriate inflation factor.Furthermore, the time period referredto as the “normal life of assets” for thebusiness, which represents the timeperiod over which CFROI is calculated,is very subjective.

The assumption that current cash flowis sustainable over this time period is,again, open to question. In addition, thecost of capital and “fade rate”assumptions that are made whenCFROI is used as a valuation techniqueare also subjective.

3.4 Total business returns (TBR)Total business returns (TBR) is theinternal equivalent of the external totalshareholder returns (TSR) measure,which considers capital gains anddividends received by shareholders. Thisapproach is advocated by BostonConsulting Group, who explain theapproach as follows:

“It measures the capital gain anddividend yield of a business unit orcompany plan as if the plan wereknown by the market or the businessunit were publicly traded.”(Boston Consulting Group, 1996)

The approach is claimed to overcomethe principal weakness with any short-term performance measure (includingcash flow, EP/EVA®‚ and CFROI), as itincorporates the long-term effect onthe value of the business of decisionsand actions taken in a particular period.This is because TBR combines the cashflow performance of a business withthe change in value that occurredduring the period.

Effectively, TBR represents an internalrate of return measure that equates thebeginning value of a business with netfree cash flows arising in the period,plus the value of the business at theend of the period. The accuracy of TBRtherefore depends upon the accuracy ofthe valuation of the business at thestart and end of the relevant period.

It is often used in conjunction withCFROI, in which case valuations can bebased on the application of the CFROIvaluation methodology referred toabove. Sometimes, however, asimplified valuation approach isapplied, using a formula thatincorporates the “CFROI spread”currently generated by the business andan appropriate multiple that reflectsexpected market growth. Although TBRis often used alongside CFROI, there isno reason why TBR cannot be usedwith other value metrics. (In fact,Unilever has used TBR as a key strategicmeasure with an EP-type measure asthe key measure for monitoring short-term performance.)

Advantages and disadvantagesof TBRThe key justification for TBR is that, byincorporating the effect of changes invalue as well as “delivered”performance in a period, it representsthe closest measure of the trueeconomic performance of a business.

The main problem with TBR relates tothe difficulty in accurately measuringopening and closing business valuationsfor a particular period. These can bebased on managers’ forecasts, whichare inevitably subjective. Alternatively,some form of pre-determined formulacan be used, which may improveobjectivity but potentially at theexpense of accuracy.

Maximising Shareholder Value Measuring Shareholder Value – The Metrics14

Steve Marshall, former chief executive of Railtrack

Many company boards are fixated by short-term financial results and ignorelong-term issues. This is detrimental to shareholder value, argues SteveMarshall, former chief executive of Railtrack.

“They concentrate on short-term financials, what the market expects, whatdividends are expected and other short-term issues. These are a proxy measureof shareholder value and not the whole picture.”

By looking at short-term issues, however, Marshall claims that firms are notintentionally neglecting shareholder value. “This sort of behaviour is not a lackof intent to create value for shareholders,” he says. “Rather, it is a blurredattitude to what actually generates shareholder value.”

When businesses get into trouble, he adds, it is rarely down to a failure ofcorporate governance or a breach of financial controls. “Instead, boards tend tosleepwalk into unwise decisions. Often a decision is made by default becauseno-one realised that a decision had to be made to get out of a certainsituation.”

Marshall argues that the recent changes to corporate governance are helpfulbut will only solve around 10 per cent of problems – the remaining 90 per centwould be solved by boards “upping their game”.

“Many non-executive directors are at fault for failing to put enough time intounderstanding the business and what are the firm’s key value drivers,” he says.“Boards must ensure that they have the skills to tackle each issue they areconfronted with and this may mean that the board composition has to changeas the company tackles new challenges.”

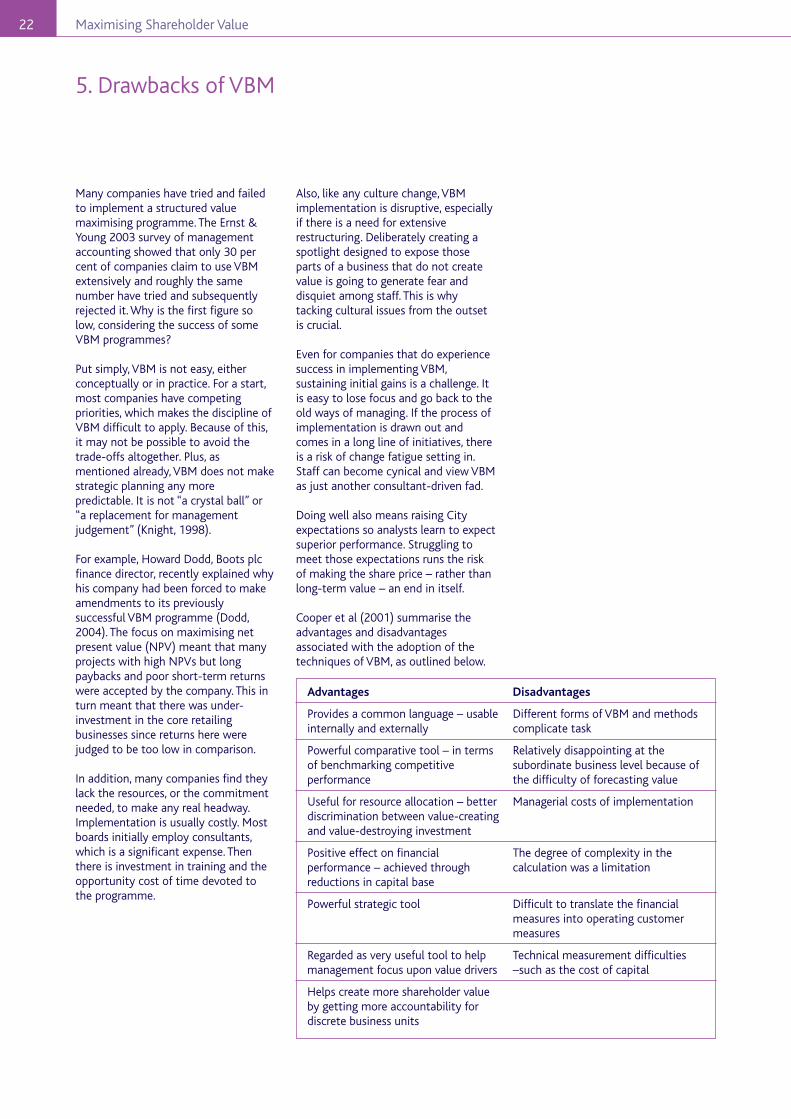

3.5 ConclusionsThere is a great deal of consistencybetween the measures but alsosignificant differences that have beenidentified above. One of the commonarguments in favour of each metric ison the grounds of its superior power toexplain the way the stock marketactually measures shareholder wealth.

The empirical evidence is, however,inconclusive with independent studiesgenerally showing lower levels ofcorrelation than those suggested by theconsultants.

Furthermore, each of the metricssuffers from a potential lack ofobjectivity in calculating the cost ofcapital and other key value drivers.Another potential problem for each ofthe metrics is whether managers findthem to be understandable. In thisrespect, perhaps it could be argued thatEP/EVA® is relatively easily understood,but even here the level ofunderstanding will depend upon thecomplexity of the adjustments andvaluations performed.

Finally, potentially significantmeasurement costs will be incurred inimplementing the metrics, whichshould be considered to ensure thatany benefits are not outweighed by therelated costs.

Maximising Shareholder Value Measuring Shareholder Value – The Metrics 15

4.1 Governance and ownershipAt the heart of managing for value liesa problem common to many large –and particularly listed – companies. Thisis the so-called “agency problem”created by the separation of ownershipand management. Owners effectivelydelegate the day-to-day running of thecompany to paid managers who act astheir agents. The result can be a lack ofalignment between the interests of thetwo groups.

The people likely to have the biggestimpact on value creation are managersin charge of running the company. Yet,there is a risk that they may not alwaysmake decisions that have shareholders’best interests at heart. They – like allother market participants – can begoverned by self-interest.

As executive tenures get shorter andexecutive pay packets get bigger, it ishardly surprising that some try to maketheir spell at the top as profitable aspossible. In extreme cases this can go asfar as aggressive earnings management.But there are other, more benign, waysof temporarily boosting the share priceand thus the size of the reward linkedto it. Most of those are designed towork in the short-term and could endup destroying shareholder value.

There are, of course, barriers in place toprevent managers from abusing theirpositions. One of these is the threat ofreputational damage to their futureemployment prospects. There are alsoother safeguards, in the form ofcorporate governance codes andpractice.

Making sure the owners’ and managers’interests are aligned entails fosteringopen and honest communication andactive interest from shareholders.Commentators have been complainingfor a while now that fewer and fewershareholders are committed to thecompanies they own. Instead, “giantmutual funds buy and sell millions ofshares every day to mirror impersonalmarket indexes” (Mintzberg, 2002).Some critics go as far as to say that therecent accounting scandals in the USare a direct product of a lack ofownership. They lay the blame squarelyon investors’ lack of involvement in thecompanies they own.

But this apparent apathy is not new. Asfar back as 1990, an article in theEconomist remarked that there werefew real owners left and most of thosewho buy and sell shares are in effect“punters, not proprietors”.

Although there is some truth in this,large funds do not usually trade withsuch haste or impulsiveness. Recentevents have shown that shareholdersare making their views known and arewilling to get involved in companiesthey own. Some examples ofshareholder activism include ITV –where the disgruntled shareholdersprevented the appointment of Carlton’sMichael Green as the chairman of anew, merged business – and J Sainsbury– where shareholders successfullyblocked the appointment of Ian Prosseras the new chairman. Share ownershipis now effectively concentrated in thehands of relatively few institutionalinvestors who can wield a significantamount of power in the boardrooms,should they choose to do so.

In addition, many funds – eitherbecause they track an index or becausethey feel they need to be invested incertain major stocks – are obliged tohave significant holdings in manyquoted companies. In other words, theyhave no real “choice” about whether ornot to hold. In the absence of theoption to buy or sell, they must insteaduse their holding to influence companystrategy and performance.

Few would contest the investors’ rightto have a say in issues of boardroomconstitution or governancearrangements. However, the force andextent of recent shareholder activismseem to have caught many by surprise.So vocal have shareholders become inrecent months that their efforts havebeen labelled “megaphone diplomacy”by some of the largest UK companies.Executives complain of having toomany corporate governance codesforced onto them and accuse theinvestors of micro-managing andmeddling in the day-to-day affairs ofthe company. Some have even hintedat exiting equity markets and goingprivate.

Whether this “new City”, as one of theinstitutional investors called the trendduring the Carlton/Granada merger,really is a taste of things to comeremains to be seen. What is clear is thatcorporate governance has come a longway, and only partly because thegovernment has threatened legislationshould investors choose to remainpassive. Companies that ignore thisnew reality may risk negative publicity,as well as shareholder hostility.

4.2 Remuneration

Jeremy Roche,CEO, financial software firm,Coda

“Remuneration policy must beperformance-related and linked toother parts of the business andalso to the goal of managing forshareholder value. Otherwise, youend up with the situation that anew, big order might be good forthe sales team’s objectives butcreates problems for other parts ofthe organisation, which causesshareholder value to fall.”

Maximising Shareholder Value16

4. Managing for Shareholder Value

● The bonus system rewardsimprovement at any level ofperformance – there is no cap on thebonus payable.

● Staff are in a shareholder value-basedbonus system.

● The business defers part of the bonuspay out over several years.

● Many staff have built upshareholdings in the business,through purchases or bonuses, whichare a significant part of their totalwealth.

They found the most significantpositive correlation with the last twopoints, which seem to deliver additionaltotal shareholder returns of 2 and 4 percent per annum, respectively.

The link between reward andmotivation is far from straightforward,despite the widespread recognition thatpay is one of the main influences onhow people behave at work. The sheernumber of motivational theories isenough of a testament to this, as is thecomplexity and sometimes opaquenessof remuneration packages awarded (todirectors and executives in particular).It is hardly surprising that a wholeindustry has mushroomed aroundremuneration consulting and that thesubject continues to provoke anemotive response from companies,investors and the general public alike.

Remuneration can take many forms.Employees can be paid in cash,including basic salary, bonus andpension, or through various forms ofequity-linked compensation, such asshares or share options. All can beawarded in different proportions andcan be either fixed or variable. They canalso be subject to different timingrestrictions in terms of when they canbe exercised.

As the table above shows, over a fiveyear period, incentives such as shares orshare options represented the bulk ofoverall executive pay, while the basicsalary formed a relatively smallproportion.

The paradox of agency, describedabove, can be a major stumbling blockfor companies committed to value-based management.

“Shareholder value (…) drives a wedgebetween those who create theeconomic performance and those whoharvest its benefits. (…) Those whocreate the benefits are disengaged fromthe ownership of their efforts, andtreated as dispensable, while those whoown the enterprise treat that ownershipas dispensable and so disengagethemselves from its activities.”(Mintzberg, 2002)

It has even been suggested that whatreally matters in companies today isnot the financial capital provided bythe shareholders but the intellectualcapital of employees. In other words, itis the knowledge and the creativity ofpeople working for the company thatare the real assets in the so-calledknowledge economy.

Value-based management agenda mustinclude an attempt to align – or at leastreconcile – the interests of the twoparties. The most obvious way in whichthis can be done is by allowingemployees to share directly in thebenefits they helped create. Thiseffectively means paying them in a waythat makes them behave more likeowners, by linking their rewards to along-term growth in value. In practice,this equates to remuneration structuresthat include some form of equity-linked compensation.

This is why remuneration policiesfrequently form a central plank of VBMprogrammes. In fact, some believe theyrepresent the biggest missedopportunity. PA Consulting examinedthe correlation between totalshareholder returns and theremuneration practices commonlyassociated with VBM. They examinedthe following practices:

CEO Pay Mix

Long-Term

Year Salary Bonus Incentives

1998 20% 18% 62%

1999 20% 17% 63%

2000 18% 17% 65%

2001 16% 13% 71%

2002 16% 16% 68%

(Mercer consulting, from Institute ofManagement and Administration Pay forPerformance report, 2003)

Although the idea of paying employeesin equity sounds straightforward, it hasnot been without problems in practice.This was partly due to the dot combubble; employees who chose to cashin their share options benefited from aphenomenal rise in global equity prices.This effectively severed the linkbetween pay and performance and ledsome commentators to brand optionsas “legalised looting at shareholders’expense” (Plender, 2003).

This was exacerbated by the fact thataccounting standards did not requireoptions to be treated as an expense.However many options a companyawarded, the cost to the company – i.e.shareholders – went unrecorded. Atbest, share options may have featuredin notes to the accounts but there hasgenerally been very little transparencyabout their use. Some argue that,despite this, the stock market hasalready factored the disclosed cost ofoptions into today’s value (WatsonWyatt, 2003) but others estimate thatreported profits may be as much as 30per cent lower if the options areexpensed.

Recently, more and more companieshave chosen to stop issuing shareoptions altogether. J D Wetherspoons,for example, announced it wouldabandon the practice because it lackedtransparency. Microsoft, a companywhose success was undoubtedly, inpart, based on incentivising people withequity, also decided to stop issuingoptions.

Maximising Shareholder Value Managing for Shareholder Value 17

Others are beginning to expenseoptions through their profit and lossaccounts to reflect their true cost. From2005, all European listed companieswill be forced to do so in any case,following the introduction ofinternational accounting standards.

In February, the InternationalAccounting Standards Board (IASB)published a reporting standard entitledShare-based Payments (IFRS2). Theobjective of IFRS2, according to theIASB, was

“to specify the financial reporting by anentity when it undertakes a share-based payment transaction. Inparticular, the IFRS requires an entity toreflect in its profit or loss and financialposition the effects of share-basedpayment transactions, includingexpenses associated with transactionsin which share options are granted toemployees.”(www.iasb.org)

The IASB acknowledged that the lack oftransparency in share-based paymentshas attracted criticisms from investorsand raised corporate governanceconcerns. The new standard, it hopes,will go some way in addressing theseand preventing any possible “economicdistortions”.

Despite the pitfalls, the basic conceptof tying remuneration to an increase incompany value seems a sensible way ofaligning owners’ and managers’interests. This is especially true in thecase of small companies, where the linkbetween individual performance andcompany success is visible andrelatively straightforward.

In any case, it is important to install theprocesses and structures whichsafeguard owners’ interests againstpossible abuses of power. In thiscontext, the importance of strongremuneration committees cannot bestressed enough. For those below theboard and senior management level,there need to be clear and documentedremuneration policies and procedures.

Professor John Barbour,founder of consultancy Corporate Value Improvement

Managing for shareholder value is as much a frame of mind as a technicalissue, says John Barbour, founder of Corporate Value Improvement, aconsultancy which helps top businesses deliver superior returns toshareholders.

“When companies start thinking about what shareholder value entails, theyneed to start thinking beyond financial measurement”, he says. “A business islike a horse. The head is the board, setting the objectives and deciding the bestway to go. The four legs are the company’s strategy, finances, organisation andits people. The horse will go as quickly as the slowest leg allows. So if youconcentrate everything on financial metrics and ignore your people, then thehorse will lag behind in the shareholder value stakes.”

Barbour argues that shareholder value has to be led from the top. “If the topteam does not change the way it does things, then the drive for shareholdervalue will fail. People do what their bosses do and the board has to lead bywhat they are doing, not what they’re saying.”

The CEO may become the spokesperson on the issue but it is often the financedirector who, by doing lots behind the scenes, can end up making a lot happen.Financial visibility and performance are a key part of managing for shareholdervalue and often the strategy side of the business fits in well with the financedirector’s role.

Many firms bring in large teams of consultants to set up a programme tomanage for shareholder value. But Barbour argues that there are pros and consto getting in consultants.

The advantage is that you engage professionals whose focus is to change theorganisation and gear it towards managing for shareholder value. However, itcan be hard to keep that change sustained after the consultants have left.

Barbour recommends hiring a small number of consultants who show the staffhow to change the organisation rather than do the work for them. “You learnby doing and that way the company is experienced at doing it once theconsultants leave,” he says.

The finance department has a key role to play in helping a firm manage forshareholder value, according to Barbour. Firstly, the function has to find a wayof delivering the department’s outputs – the financial transaction processes,for example – at a lower economic cost. This can be either throughstreamlining and making the internal service more effective and efficient, oroutsourcing it to expert operators.

Once this has been achieved, the finance department needs to develop as an“internal consultant” for the organisation, looking at areas such as the impactof mergers and acquisitions, long-term strategy and investments.

“Becoming an efficient information machine, while acting as a business partnerto the board, will be a major challenge for many finance departments,”acknowledges Barbour. “But if they are successful, then their survival isguaranteed.”

The business itself will be more successful, as a result. An integrated financedepartment, acting as an internal consultant, can help a firm improve its valueto shareholders.

Maximising Shareholder Value Managing for Shareholder Value18

Companies implementing VBM shouldbe cautious about giving their financedepartment full ownership of thechange programme. The rest of theorganisation may dismiss theprogramme as having no relevanceoutside of the finance function. Awidespread buy-in will be difficult toobtain.

In their seminal article for the HarvardBusiness Review, researchers from theINSEAD business school concluded thatthe key to successful implementationof VBM is a focus on culture rather thanfinance.

Culture encompasses all of the implicitnorms and ways of behaving that directemployee actions. These tend to havemore influence on what happens day-to-day than official edicts from seniormanagement, which may not get past aread and forgotten all-staff memo. Thatis why change, particularly culturalchange, is so difficult to get right.