Armstrong World Industries -...

54

Armstrong World Industries Analysts’ Meeting, NYC September 29, 2008

Transcript of Armstrong World Industries -...

Armstrong World Industries

Analysts’ Meeting, NYC September 29, 2008

2

Safe Harbor Statement

This presentation contains “forward-looking statements”

related to Armstrong World Industries, Inc.’s future financial performance. Our results could differ materially from the results discussed in these forward-looking statements due to known and unknown risks and uncertainties. A more detailed discussion of the risks and uncertainties that may affect our ability to achieve the projected performance

is included in the “Risk Factors”

and “Management’s Discussion and Analysis”

sections of our recent reports on Forms 10-K and 10-Q filed with the SEC. We undertake no obligation to update any forward-looking statement.

In addition, we will be referring to non-GAAP financial measures within the meaning of SEC Regulation G. A reconciliation of the differences between these measures with the most directly comparable financial measures calculated in accordance with GAAP is available on the Investor Relations page of our website at www.armstrong.com.

3

Mike LockhartChairman & Chief Executive Officer

Company Overview

4

Armstrong at a Glance

Leading global manufacturer of floors and ceilings for use in renovation and new construction. Significant U.S. cabinets business.

$3.5 billion in salesServing global customers from 10 countries40 manufacturing locationsApproximately 12,700 employees

$2 billion market capitalization57 million diluted shares outstanding

250k average daily trading volume 66% owned by Armstrong Asbestos Trust

‘AWI’ on the NYSESince October 2006 emergence from asbestos-related bankruptcy

Company Overview

5

History

In 1998: Residential sales 65% of total

By 2008: Residential sales 40% of total

Significant geographic and product line expansion with the purchase of Triangle Pacific (Hardwood floors & Cabinets) and DLW (European flooring)

Asbestos-related bankruptcyManufacturing and overhead restructuringSignificant growth in Commercial products

Strategic review process, Commercial volume growth, improved product mix and manufacturing productivity contribute to earnings growth despite difficult domestic residential markets

Strategic focus on profitable growth and managing the domestic market downturn

Thomas Armstrong’s cork-

making business evolves into linoleum flooring, acoustic ceiling tiles, then vinyl flooring

Armstrong’s Evolution

1900-1997 1998 2001-2006 2007 2008

Company Overview

6

Business Segment Profile

Building Products$1,292

36%

Wood Flooring$79222%

Resilient Flooring$1,23135%

Cabinets$2357%

Building Products$21866%

Wood Flooring

$6520%

Resilient Flooring

$4112%

Cabinets$62%

(Ceilings)

#1 in businesses representing 80% of sales

2007 Sales 2007 Operating Income Adjusted – see website for reconciliation

– Excludes unallocated corporate expense

Company Overview

(Ceilings)

7

Business Segment and End-Use Profile: 2007 Sales

Diversified End Markets Reduce Impact of Cycles

Cabinets Resilient Flooring(Europe)

Resilient Flooring(U.S.)

HardwoodFlooring

BuildingProducts(Ceilings)

Consolidated

Residential new Residential renovation Commercial new Commercial renovation

75%25% 60%

25%

45%

50%

5%38%

42%

12%

60%

30%

10%

25%

20%

20%

35%$1,300

$800$800

$350$250

$3,500

15%

8%

Company Overview

8

Industry Structure/Competitive Position

U.S. ResilientEuropean Resilient Hardwood

Building Products Cabinets

Market Leadership

Competitor Concentration

Barriers to Entry

Industry Capacity Utilization

AWI is Low-Cost Manufacturer

Armstrong is positioned to capitalize on positive AND negative competitive dynamics

Key Favorable Neutral Unfavorable

Company Overview

9

Key Investment Catalysts

Market Leadership: #1 in businesses representing 80% of sales

Diversified end markets, product portfolios and geographies

Sales and margin growth potential

Well-positioned for recoveries in domestic markets

Low-cost manufacturing and advantageous footprint

Strong cash flow sufficient to capture all expected opportunities

Company Overview

10

Steve SenkowskiExecutive Vice President

Building Products

11

ABP 2007 Sales by Geography (Ceilings & Grid)

0

200

400

600

800

1000

1200

Americas W. Europe E. Europe/MiddleEast

Asia

($-Billions)

Operating Profit 22% 13% 2% 14%

Asia and Eastern European growth opportunities

Building Products

Sales Are >90% Commercial

$1.6B in sales is a full consolidation of WAVE and the Building Products segment (ABP) and is, therefore, greater than reported ABP sales

12

ABP Product Categories – Core Ceilings

Key CharacteristicsMineral fiber – wet felt/soft fiber (fiberglass)●

Acoustics●

Durability●

Surface Pattern

GridLoad ratingFace width/design

Installed (NYC) cost:$5.50 - $8.50/sq. ft.

Armstrong selling price:$0.78 - $2.75/sq. ft.

Building Products

13

Installed (NYC) cost:$11 - $120/sq. ft.

Armstrong selling price:$8 - $100/sq. ft.

Architectural Specialties42% annual growth since 20032007 ●$32M sales●$9M operating profit

ABP Product Categories – Specialties

Design Accents Acoustical Accents

Expanded product portfolio

Building Products

14

Commercial Construction Selling Process

ArchitectExperience levelEase of doing businessAcoustical design expertise

Ceilings-only sales force focused on specific customer groups

Ceiling SubcontractorEase of doing businessExperience levelCompetitive prices

DistributorPricing processPlant serviceArmstrong sales rep

Owner Architect General Contractor

Ceiling Subcontractor Distributor Manufacturer

U.S. Key Drivers of Loyalty/Satisfaction

Building Products

15

Mineral Fiber Ceilings Manufacturing Locations

ABP has broadest presence

* Low-end Chinese manufacturers not included (≈60)

Americas Europe Asia*Wet Felt Mineral Fiber

ABPCompetition●

Number of plants●

Number of competitors

6

52

3

22

1

22

Soft FiberABPCompetition●

Number of plants●

Number of competitors

1

1–

–

92

N/A

N/A–

Building Products

16

Commercial Ceiling Coverage by Material Category

Size of Market (B sq. ft.) 2.3 2.0 0.7 6.0

% Market

75

32

69

9

4

18

5

9

1018

30

13

77

11 7

1

7

2 3

0

20

40

60

80

100

Americas W. Europe Russia ChinaWet Felt Soft Fiber Metal Drywall Other

Exposed structure (no ceiling) is 12% of U.S. total ceiling areaRussia is second largest mineral fiber ceiling market

Mineral fiber ceilings the top choice in most markets

Building Products

17

0

20

40

60

Armstrong USG CertainTeed

Mineral Fiber Commercial Ceilings Market Shares

North America

*Russia market share is 23%*China market share is 20%Low-end Chinese share in Russia is 60% and China is 50%

ABP is global leader in mineral fiber category

Western Europe

*Armstrong is No. 1

0

10

20

30

40

Armstrong Rockfon OWA AMF Ecophon

Building Products

Wet Felt Only Soft Fiber Only

18

Commercial Market Segments

U.S. office construction downturn will have limited effect on volume

36 4063

18 16

710 14

825 14

11 16 202

0

20

40

60

80

100

Americas W. Europe ChinaOffice Education Healthcare Retail Other

Renovation is the majority of the opportunity in the U.S. and Western Europe

%

Building Products

30% 43% >90%% New Construction

19

WAVE

2000 2004 2007

Sales ($) 208 277 380

Operating Profit (%) 19 22 30

2000to

2004

2000to

2004

2004to

2007

2004to

2007

Product innovation to improve usability, reduce cost, increase market share and enhance margins

Product innovation - cost reduction and share gainSteel/product pricing

Manufacturing consolidationShare gainSteel/product pricing

Building Products

20

U.S. Commercial Ceilings Downturn

Disciplined pricing and new product initiatives produce solid margins in commercial downturn

2000 - 2003

15%

100%

50%

3%

2%

19%

14%

What’s Changed

Pricing discipline

Market share gain

Architectural Specialties growth

2008 First Half

5%

100+%

4%

25%Operating Profit

VolumeDecline

Price vs. Inflation

Mix

Building Products

21

Key Strengths and Growth Strategies

Continued new product development plus manufacturing investments in developing markets

1 Best Product Portfolio

European soft fiberLocal Asian productsSpecialties – new materialsCore ceilings and grid – new product leadership

2 Complete Market Coverage

Expand distribution in RussiaGrow use of acoustical ceilings in China

3 Low-Cost Manufacturing

Build manufacturing plant in RussiaExpand manufacturing capacity in China

4 Best-In-Class Service/Quality

Build manufacturing plant in RussiaExpand manufacturing capacity in China

5 Disciplined “Premium”’ Pricing

Building Products

22

Frank J. ReadyExecutive Vice President - AWI &

CEO North American Floor Products

North American Floor Products and Cabinets

23

Business Overview

Vinyl/Laminate Sales Mix

Hardwood Residential – 95%

Commercial 46%

Residential 54%

Tile9%

Tile37%

Sheet Vinyl9%

Sheet Vinyl30%

Laminate15%

Other9%

Engineered30%

Solids61%

2007 Actual ($ Millions)

Net Sales $826 $792Operating Income $50 $65ROC % 16.4% 9.2%

North American Floor Products

24

2007 Segment/Channel Overview

Resilient Net Sales = $826M

Hardwood Net Sales = $792M

Channel Breakdown% of 2007 Sales

Resilient HardwoodDistribution 71 65Big Box 29 35

Res'l - Remodel

42%

Comm'l - Renovation

38%

Comm'l - New8%

Res'l - New12%

Res'l - Remodel

45%

Comm'l - 5%

Res'l - New50%

North American Floor Products

25

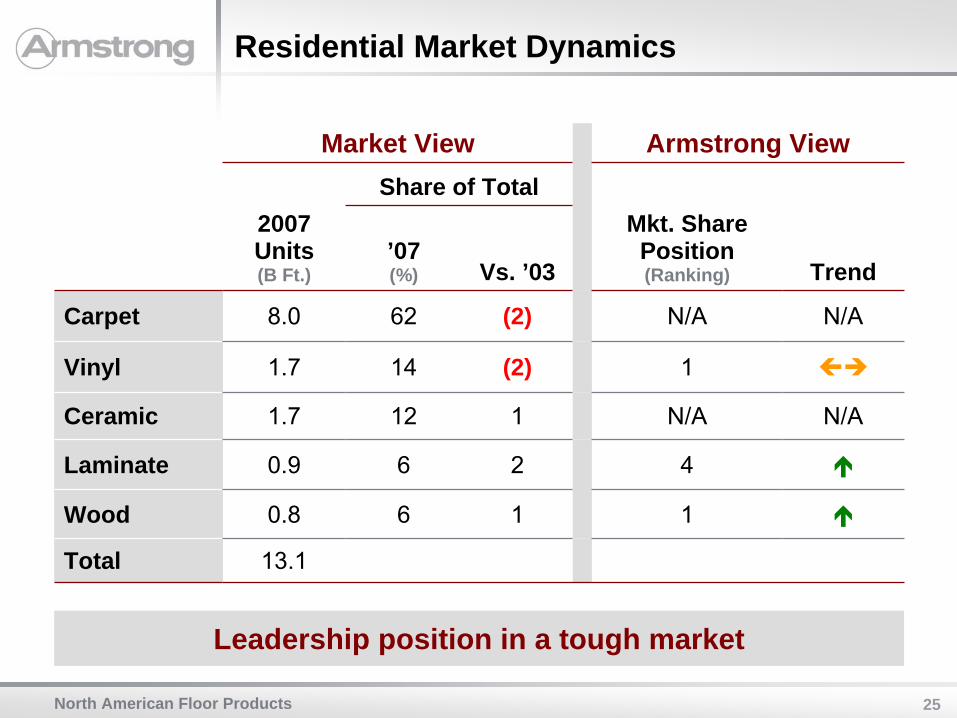

Residential Market Dynamics

Market View Armstrong ViewShare of Total

2007 Units(B Ft.)

’07(%) Vs. ’03

Mkt. Share Position(Ranking) Trend

Carpet 8.0 62 (2) N/A N/A

Vinyl 1.7 14 (2) 1

Ceramic 1.7 12 1 N/A N/A

Laminate 0.9 6 2 4

Wood 0.8 6 1 1

Total 13.1

Leadership position in a tough market

North American Floor Products

26

Commercial Market Dynamics

Market View Armstrong ViewShare of Total

2007 Units (B Ft.)

’07 (%) Vs. ’03

Mkt. Share Position (Ranking) Trend

Carpet 4.4 70 1 N/A N/A

Vinyl 1.2 19 (1) 1

Wood 0.1 2 – 2

Ceramic 0.5 7 – N/A N/A

Other 0.1 2 – N/A N/A

Total 6.3

Armstrong has #1 position in Commercial Vinyl segment

North American Floor Products

27

Industry Structure/Competitive Position

Resilient Hardwood

Residential Commercial

Tile Sheet Tile Sheet

Industry Capacity Utilization

Number of Competitors

Barriers to Entry

Armstrong Cost vs. Competition

Opportunity is industry consolidation in Residential Sheet Vinyl

Key Favorable Neutral Unfavorable

North American Floor Products

28

Production System

Armstrong produces 90% of what it sells… Laminate and LVT are the exception

% of VolumeArmstrong Third Party

# of Domestic Plants Domestic Global

CommercialVCTLVTSheetLinoleum

4–1–

100–10–

––55100

–10035–

ResidentialSheet VinylVinyl TileEngineered WoodSolid WoodLaminate

2346–

85909097–

15–5––

–1053

100

North American Floor Products

29

What We Have Done

Improved design capability

New products

Better commercial portfolio

Reduced footprintLancaster

This is a better business…

Expanded product line

Improved quality/service

AcquisitionsCapella

HomerWood

Reduced footprintClosed 3 plants

Added China plant

Resilient Hardwood

North American Floor Products

30

Financial Trends

Improved financial performance despite tough market conditions

2003 2005 2007Resilient

Op. Margin % 8.0 3.1 6.0

ROC % 15.2 7.6 16.4

Hardwood

Op. Margin % 5.1 10.5 8.2

ROC % 6.7 14.2 9.2

North American Floor Products

31

Competitive Dynamics

Resilient Hardwood

Residential Commercial

Market

Raw Material Inflation

Price

Productivity

Challenging markets and Vinyl raw material inflation partially offset by price and productivity

Key Favorable Neutral Unfavorable

North American Floor Products

32

Resilient Strategy

VinylOffer broadest assortmentReduce manufacturing costRationalize industry capacity

LaminateLeverage design leadership positionLower-cost sourcing

Residential Resilient Sales

Expand product range in higher margin categoriesEnvironmental/Non-PVCSheet Vinyl…lower product costs

Commercial

Comm'l Vinyl46%

Res'l Vinyl39%

Laminate 15%

North American Floor Products

33

Hardwood Strategy

Offer the broadest assortment of species/colors

Improve mix…Wide widthExotics

Lower manufacturing costsOn-going productivityFootprint changes

Reduce working capitalYard productivity

Focus on Improving ROC…

North American Floor Products

34

Cabinets

Small player…<5% shareFocus on small/medium size builderGo-to-Market

Current Situation 2007 Sales = $235M

Product/service executionImprove Service Center productivityReduce manufacturing costs

Strategy

Remodel25%

New75%

% of SalesCompany-Owned Service Centers 55%

Distribution 25%Multi-Family 20%

Cabinets

35

Mike LockhartChairman & Chief Executive Officer

European Floor Products

36

European Resilient

Vinyl30%

Other17%

Linoleum38%

Vinyl15%

Commercial 85%

Residential 15%

Linoleum is the most desirable business

2007Sales $330M

Operating Loss $ 20M

European Floor Products

37

Situation Overview

ChallengesAcquired #4 market competitor in 1998Greatest exposure is to the German commercial market

Declined an average 5% per year for 7 years following acquisition

Scale disadvantage in manufacturing and SG&AOutdated manufacturing processes in all but Linoleum

OpportunitiesSG&A: reduced spending, outsourcing to India plus consolidation in Eastern EuropeClosing unprofitable plants; investing to make plants competitive

Independently or through combination with a competitor

Selling assets

Have a credible plan by the end of the year

European Floor Products

38

F. Nicholas GrasbergerSenior VP & CFO

Financial Review

39

($-Millions) 2005 2006 2007 2008E

Net Sales 3,427 3,532 3,579 3,500% Change 3% 1% (2%)

Operating Income 183 272 307 275% Change 49% 13% (10%)% Margin 5% 8% 9% 8%

Cash Flow 98 117 511 175

Net Debt/EBITDA NM 1.7 0.3 0.6

Return on Capital 4% 6% 7% 6%

* Figures are normalized for unusual gains and expenses, foreign

currency and fresh start accounting.

Key Metrics* (2005-2008E)

Financial Review

40

185 (125)

70200

(195)

120 20 275

2005 Price Volume Mix Inflation Mfg +SG&A

WAVE 2008E

($-Millions)

Operating Income Bridge (2005-2008E)

Financial Review

41

Key Assumptions (2009-2011)

End Markets

US Residential recovers mid-2010

US Commercial recovers late-2010

Europe weak through 2010

European Floor Loss eliminated in 2010

Price vs. Inflation Neutral

Manufacturing Productivity $50-75 million cost reduction

SG&A 16-17% of sales

Capital SpendingCeilings plants in Russia and China

US/Europe vinyl footprint changes

Domestic NOL Utilized by end of 2011

Financial Review

42

Financial Outlook (2008E-2011)

2008E 2011

Net Sales $3.5 billion $3.7-3.8 billion

Operating Margin 8% 10-11%

Free Operating Cash Flow $500-600 million

Return on Capital 6% 11-12%

Financial Review

43

Operating income up 50% since 2005 despite weak markets

Operating margins up 300 bps due to better sales mix and improved productivity

Strong cash flow produced very modest financial leverage

Operating margins should improve further despite weak outlook due to mix gains and manufacturing improvements

Investment opportunities can be funded without raising new capital

Financial Summary

Financial Review

44

Price/Volume/Mix (2006-2008E)

2%

(1)%

2% 2%

(2)%

2% 2%

(6)%

2%

2006 2007 2008E

Price Volume Mix

Financial Review

45

Sales Change by Segment (2006-2008E)

9% 9%

1%

(2)%

2%

9%

(6)%

(1)%

(19)%

5%

(15)%

2%

2006 2007 2008E

Resilient Flooring

Wood Flooring

Building Products Cabinets

Financial Review

46

25

(15)

40

1515

(10)

40

(15)

(30)

15

(10)

2006 2007 2008E

Resilient Flooring

Wood Flooring

Building Products Cabinets

($-Millions)

Profit Change by Segment (2006-2008E)

Financial Review

47

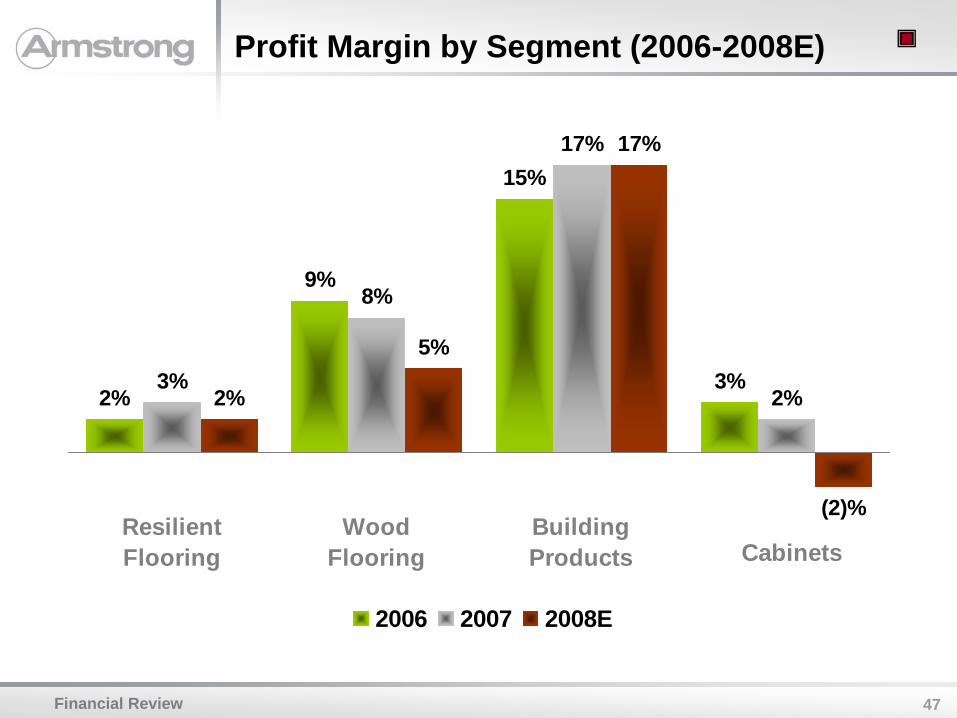

Profit Margin by Segment (2006-2008E)

3%

15%

9%

2% 2%

17%

8%

3%

(2)%

17%

5%

2%

2006 2007 2008E

Resilient Flooring

Wood Flooring

Building Products Cabinets

Financial Review

48

Cash Flow (2006-2008E)

($-Millions)

Cash Earnings (Pre-Tax) 800

Tax Refunds/(Payments) 100

Working Capital (50)

WAVE Dividends 200

Cash Flow from Operations 1,050

Capital Spending (net) (250)

Free Operating Cash Flow 800

Dividends Paid (250)

Debt Reduction (400)

Change in Cash 150

Financial Review

49

Balance Sheet (2008E)

($-Millions)Cash 400Working Capital 500PP&E 950Pension Asset 400Intangibles 700WAVE Investment 250Deferred Tax Asset 400Retiree Medical (300)Tax Liabilities (600)Net Assets 2,700Debt 500Equity 2,200Total Capital 2,700

Financial Review

50

Volume/Mix by Segment (2006-2008E)

(45)(55)

(10)(15)

25

40

5

Volume Mix

Resilient Flooring

Wood Flooring

Building Products Cabinets

($-Millions)

Financial Review

51

Productivity by Segment (2006-2008E)

($-Millions)50

3530

(5)

(20)

5

25

Manufacturing SG&A

Resilient Flooring

Wood Flooring

Building Products Cabinets Corporate

Financial Review

52

Mike LockhartChairman & Chief Executive Officer

Conclusion

53

Strengths

Market leadership: #1 in businesses representing 80% of sales

Renowned brands

Diversified end markets, product portfolios and geographies

Low-cost manufacturing and advantageous footprint

Customer service

Product quality and design

Conclusion

54

Opportunities

We are strongly positioned to benefit from opportunities created by weak markets and their eventual recovery

Portfolio Opportunities

Execution Experience

Plant consolidation

Product mix improvement

Price realization

Outperform the market

Strong Balance Sheet

European Resilient

Emerging markets

US Resilient consolidation

Residential market recovery

Tuck-in acquisitions

Low leverage

Strong cash flow

No new capital required+ +

=Increased Shareholder Returns

Conclusion