Arbitrage and Its Physical Limits -...

53

Arbitrage and Its Physical Limits Louis H. Ederington Price College of Business, University of Oklahoma Chitru S. Fernando Price College of Business, University of Oklahoma Kateryna V. Holland Krannert School of Management, Purdue University Scott C. Linn Price College of Business, University of Oklahoma January 15, 2017 Abstract We examine how physical constraints limit arbitrage by studying the effect of crude oil storage constraints on arbitrage activity in the U.S. crude oil market. We document both temporary and long-term violations of the no-arbitrage conditions that are robustly attributable to storage capacity constraints. When crude oil storage levels are well below available storage capacity, temporary violations of the upper no-arbitrage bound occur but tend to be eliminated within a few days. However, as the amount of oil in storage approaches the capacity limit, the price adjustment process slows and violations of the upper no-arbitrage limit persist. We find evidence of temporary, but not long-term, violations of the lower no-arbitrage futures pricing bound, with the latter being consistent with our observation that there were no periods of stock- out conditions during our sample period. We also find that arbitrage was limited by financial constraints over our 2004-2015 sample period. However, the evidence in support of physical constraints impeding arbitrage is independently strong and remains robust when we control for the effect of financial constraints. Our results are also robust to the use of different measures of physical constraints. Our evidence further indicates that arbitrage normally impacts the spot price more than the futures price. Our findings highlight the importance of accounting for physical arbitrage limits in the pricing of commodity futures. We also contribute to the Theory of Storage literature by highlighting the consequences for prices when inventories approach storage capacity limits. JEL Classifications: law of one price, limits to arbitrage, commodity markets, oil futures markets, oil storage, physical constraints, cash-and-carry arbitrage. Keywords: G13, G18, Q41. Author contact information: Ederington: [email protected], (405)325-5697; Fernando: [email protected], (405)325-2906; Holland: [email protected]; (765)496-2194; Linn: [email protected] (405)325-3444. We thank Bruce Bawks, John Conti, Thomas Lee, Yongjia Li, Anthony May, Glen Sweetnam, John Zyren, and seminar participants at the U.S. Energy Information Administration, and the Second IEA IEF OPEC Workshop on the interactions between physical and financial energy markets for valuable discussions and comments. We gratefully acknowledge financial support from the U.S. Department of Energy -- Energy Information Administration and the University of Oklahoma Office of the Vice President for Research. We also thank Moody’s Analytics for making the company’s EDF (Expected Default Frequency) data available to us and to Sue Zhang and Robert Tran for their gracious help in assembling the data. The views expressed in this paper reflect the opinions of the authors only, and do not necessarily reflect the views of the Energy Information Administration or the U.S. Department of Energy. The authors are solely responsible for all errors and omissions.

Transcript of Arbitrage and Its Physical Limits -...

Arbitrage and Its Physical Limits

Louis H. Ederington

Price College of Business, University of Oklahoma

Chitru S. Fernando

Price College of Business, University of Oklahoma

Kateryna V. Holland

Krannert School of Management, Purdue University

Scott C. Linn

Price College of Business, University of Oklahoma

January 15, 2017

Abstract

We examine how physical constraints limit arbitrage by studying the effect of crude oil storage

constraints on arbitrage activity in the U.S. crude oil market. We document both temporary

and long-term violations of the no-arbitrage conditions that are robustly attributable to storage

capacity constraints. When crude oil storage levels are well below available storage capacity,

temporary violations of the upper no-arbitrage bound occur but tend to be eliminated within a

few days. However, as the amount of oil in storage approaches the capacity limit, the price

adjustment process slows and violations of the upper no-arbitrage limit persist. We find

evidence of temporary, but not long-term, violations of the lower no-arbitrage futures pricing

bound, with the latter being consistent with our observation that there were no periods of stock-

out conditions during our sample period. We also find that arbitrage was limited by financial

constraints over our 2004-2015 sample period. However, the evidence in support of physical

constraints impeding arbitrage is independently strong and remains robust when we control for

the effect of financial constraints. Our results are also robust to the use of different measures

of physical constraints. Our evidence further indicates that arbitrage normally impacts the spot

price more than the futures price. Our findings highlight the importance of accounting for

physical arbitrage limits in the pricing of commodity futures. We also contribute to the Theory

of Storage literature by highlighting the consequences for prices when inventories approach

storage capacity limits.

JEL Classifications: law of one price, limits to arbitrage, commodity markets, oil futures

markets, oil storage, physical constraints, cash-and-carry arbitrage.

Keywords: G13, G18, Q41.

Author contact information: Ederington: [email protected], (405)325-5697; Fernando: [email protected],

(405)325-2906; Holland: [email protected]; (765)496-2194; Linn: [email protected] (405)325-3444.

We thank Bruce Bawks, John Conti, Thomas Lee, Yongjia Li, Anthony May, Glen Sweetnam, John Zyren, and

seminar participants at the U.S. Energy Information Administration, and the Second IEA IEF OPEC Workshop

on the interactions between physical and financial energy markets for valuable discussions and comments. We

gratefully acknowledge financial support from the U.S. Department of Energy -- Energy Information

Administration and the University of Oklahoma Office of the Vice President for Research. We also thank

Moody’s Analytics for making the company’s EDF (Expected Default Frequency) data available to us and to Sue

Zhang and Robert Tran for their gracious help in assembling the data. The views expressed in this paper reflect

the opinions of the authors only, and do not necessarily reflect the views of the Energy Information Administration

or the U.S. Department of Energy. The authors are solely responsible for all errors and omissions.

2

Arbitrage and Its Physical Limits

Abstract

We examine how physical constraints limit arbitrage by studying the effect of crude oil

storage constraints on arbitrage activity in the U.S. crude oil market. We document both

temporary and long-term violations of the no-arbitrage conditions that are robustly

attributable to storage capacity constraints. When crude oil storage levels are well below

available storage capacity, temporary violations of the upper no-arbitrage bound occur but

tend to be eliminated within a few days. However, as the amount of oil in storage approaches

the capacity limit, the price adjustment process slows and violations of the upper no-arbitrage

limit persist. We find evidence of temporary, but not long-term, violations of the lower no-

arbitrage futures pricing bound, with the latter being consistent with our observation that

there were no periods of stock-out conditions during our sample period. We also find that

arbitrage was limited by financial constraints over our 2004-2015 sample period. However,

the evidence in support of physical constraints impeding arbitrage is independently strong

and remains robust when we control for the effect of financial constraints. Our results are

also robust to the use of different measures of physical constraints. Our evidence further

indicates that arbitrage normally impacts the spot price more than the futures price. Our

findings highlight the importance of accounting for physical arbitrage limits in the pricing of

commodity futures. We also contribute to the Theory of Storage literature by highlighting the

consequences for prices when inventories approach storage capacity limits.

JEL Classifications: law of one price, limits to arbitrage, commodity markets, oil futures

markets, oil storage, physical constraints, cash-and-carry arbitrage.

Keywords: G13, G18, Q41.

3

Arbitrage and Its Physical Limits

“…contango would have to widen much more to signal real storage distress.”

Spencer Jakab, Wall Street Journal, December 2, 2015

1. Introduction

While the Law of One Price (LOP) is one of the most powerful concepts in the

financial economics tool chest, a number of recent papers explore the financial limits to the

arbitrage that enforces LOP, and the implications of these limits for asset pricing.1 Physical

limits, specifically limits on the availability of either inventory or storage capacity, are

potentially equally important in the arbitrage pricing relationship for financial assets whose

value is derived from the value of commodities.2 While several recent studies have examined

the role of financial limits to arbitrage in the pricing of commodity derivatives,3 the potential

effect of physical limits has not been empirically studied. In this paper, we address this gap

in the literature by studying the effect of physical storage limits on arbitrage activity in the

U.S. crude oil market. We specifically focus on the futures physical delivery hub at

Cushing, Oklahoma, which is also the major storage center in the U.S. for crude oil. We draw

inferences through an examination of the behavior of the spread between futures and spot

prices for West Texas Intermediate (WTI) crude oil.

In commodity markets, if the price of a commodity for future delivery exceeds the

price for near-term delivery by more than the carrying (including storage) and transaction

costs, arbitrageurs should be able to make a riskless profit by simultaneously executing

contracts to buy in the spot market and sell in the forward market, while storing the

commodity over the interim period. Exploitation of such an arbitrage opportunity, commonly

referred to as “cash-and-carry arbitrage,” results in the now familiar relation between futures

and spot prices derived from the Theory of Storage.4 More precisely, cash-and-carry

1 See, for example, Shleifer and Vishny (1997), Gromb and Vayanos (2002), Mitchell, Pulvino and Stafford

(2002), Hong and Stein (2003), Gabaix, Krishnamurthy, and Vigneron (2007), Brunnermeier and Pedersen

(2009), Etula (2013), and Acharya, Lochstoer, and Ramadorai (2013). 2 See Routledge, Seppi, and Spatt (2000) and Gorton, Hayashi, and Rouwenhorst (2013). 3 See, for example, Mou (2010), Hong and Yogo (2012), Etula (2013), Acharya, Lochstoer, and Ramadorai

(2013), and Cheng, Kirilenko, and Xiong (2015). 4 Kaldor (1939), Working (1949), Brennan (1958), Deaton and Laroque (1992), and Routledge, Seppi, and Spatt

(2000).

4

arbitrage should place an upper limit on the spread between the price for near-term delivery,

the “spot price,”5 and the price for longer-term delivery, henceforth the “futures price.”

Likewise, the possibility of reverse cash-and-carry arbitrage, which involves a short sale in

the spot market covered by a purchase in the forward market, should set a lower limit on the

futures-spot spread. In many commodity markets, however, storage capacity is limited --

especially at the delivery location for the futures contract. Once all available storage

facilities are full (or, in the case of reverse cash-and-carry arbitrage, the available inventory is

depleted), the corresponding arbitrage described above is no longer possible and the no-

arbitrage limits on the futures-spot spread should no longer hold.

In a classical cash-and-carry arbitrage transaction involving a physical commodity at

a spot-futures market hub like the WTI Cushing hub, the arbitrageur will execute three

simultaneous transactions: (1) purchase the commodity in the spot market; (2) sell a

corresponding quantity of the commodity in the futures market; and (3) contract to store the

commodity at the hub until the futures transaction is closed out or settled. The ability to

execute this trade depends on the availability of storage space at the hub.6 If storage capacity

or inventory is not immediately available, violations of the no-arbitrage condition may persist

until storage becomes available. Storage contracts are typically over-the-counter agreements

and thus may require some time to arrange. Moreover, they have elements of counterparty

risk, such as force majeure and physical delivery default that are not present in purely

financial arbitrage trades. These elements may discourage or delay the actions necessary to

implement the arbitrage trades. If delayed, spreads above the no-arbitrage limit may persist

until storage can be arranged. Consequently, the physical limits to executing an arbitrage

may contribute to the persistence of futures-spot spread no-arbitrage violations above and

beyond the limits imposed by financial constraints.

5 As discussed below, contracts in the crude-oil market are normally for delivery over a month since (unlike for

commodities like gold) immediate spot delivery of large quantities of oil is very difficult and expensive. For

futures contracts held to physical delivery, the CME group allows one calendar month for the oil to be delivered

to the Cushing hub. Hence the quoted “spot” prices are normally forward or futures prices for delivery over the

nearest calendar month. Contracts for immediate delivery are rare and typically for small quantities that can be

moved by tanker truck. Despite the absence of immediate spot delivery in this market, we keep with convention

by using the term “spot price” to refer to the settlement price for near-term-delivery contracts. 6 In a reverse cash-and-carry arbitrage transaction, the arbitrageur will simultaneously (1) borrow and sell the

commodity in the spot market; and (2) purchase a corresponding quantity of the commodity in the futures

market. The ability to execute this contract depends on the availability of inventory at the hub that can be

borrowed.

5

We find evidence of both short- and long-term violations of the no-arbitrage

conditions in the U.S. crude oil futures market at the WTI Cushing hub. Consistent with the

argument that often storage cannot be arranged immediately, we find evidence of numerous

temporary violations of the no-arbitrage upper bound. When storage levels are well below

capacity, these temporary violations tend to be eliminated quickly, i.e., within a couple of

days. However, as the amount of oil stored approaches the available capacity, the adjustment

process takes longer and violations of the upper no-arbitrage limit persist for longer than a

few days. In contrast, we observe only temporary violations of the no-arbitrage lower bound

indicating the absence of persistent physical limits on reverse cash-and-carry arbitrage. Our

finding for reverse cash-and-carry arbitrage is consistent with the absence of any periods of

inventory stock-out conditions during our sample period, with crude oil inventory in storage

never dropping below 30% of available storage capacity. Our evidence further indicates that

the spot price adjusts more than the futures price in bringing the spread back within the no-

arbitrage bounds, which again points to physical arbitrage limits being a major factor

determining the mispricing of the futures-spot spread.

Testing for violations of the no-arbitrage conditions is complicated because we are

unable to exactly identify the no-arbitrage limits at each point in time since (as discussed

below) historical data on storage and transaction costs are not available. Hence, we test for

evidence of cash-and-carry and reverse cash-and-carry arbitrage by examining the behavior

of the futures-spot spread. We find evidence of both cash-and-carry arbitrage and reverse

cash-and-carry arbitrage normally operating to return the futures-spot spread to within no-

arbitrage bounds. When the futures-spot spread is positive on day t-2 and rises further on day

t-1 (and storage capacity is not exhausted), there is a strong tendency for the spread to fall on

day t which is what we would expect if the further rise in the spread on day t-1 sets off cash-

and-carry arbitrage. This reversal tendency is stronger when the spread on day t-2 is high

than when it is positive but low. This is again what we would expect since the further rise on

day t-1 is more likely to raise the spread above the upper no-arbitrage bound if the spread is

already very high. Likewise, if the spread on day t-2 is negative and the spread declines

further on day t-1, there is a strong tendency for the spread to rise or reverse on day t. Again,

this is what one would expect if the further decline in the spread on day t-1 triggers reverse

6

cash-and-carry arbitrage and this reversal tendency is stronger the more negative is the

spread on day t-2. Both of these spread reversal tendencies are stronger when spread

volatility is high. In contrast, if the level of the spread on day t-2 and the change on day t-1

are of opposite sign, making it less likely that the change in the spread on day t-1 carried it

outside the no-arbitrage bound, the spread changes on days t-1 and t are basically

uncorrelated.

While normally a further rise in the spread on day t-1 from an already high level on

day t-2 tends to be reversed on day t, this is not the case when oil inventories are close to

capacity, which indicates that the lack of available storage space hinders the cash-and-carry

arbitrage which would normally operate to pull the spread back down on day t. On the other

hand, as alluded to previously, we find no evidence that reverse cash-and-carry arbitrage is

impeded by low inventories.

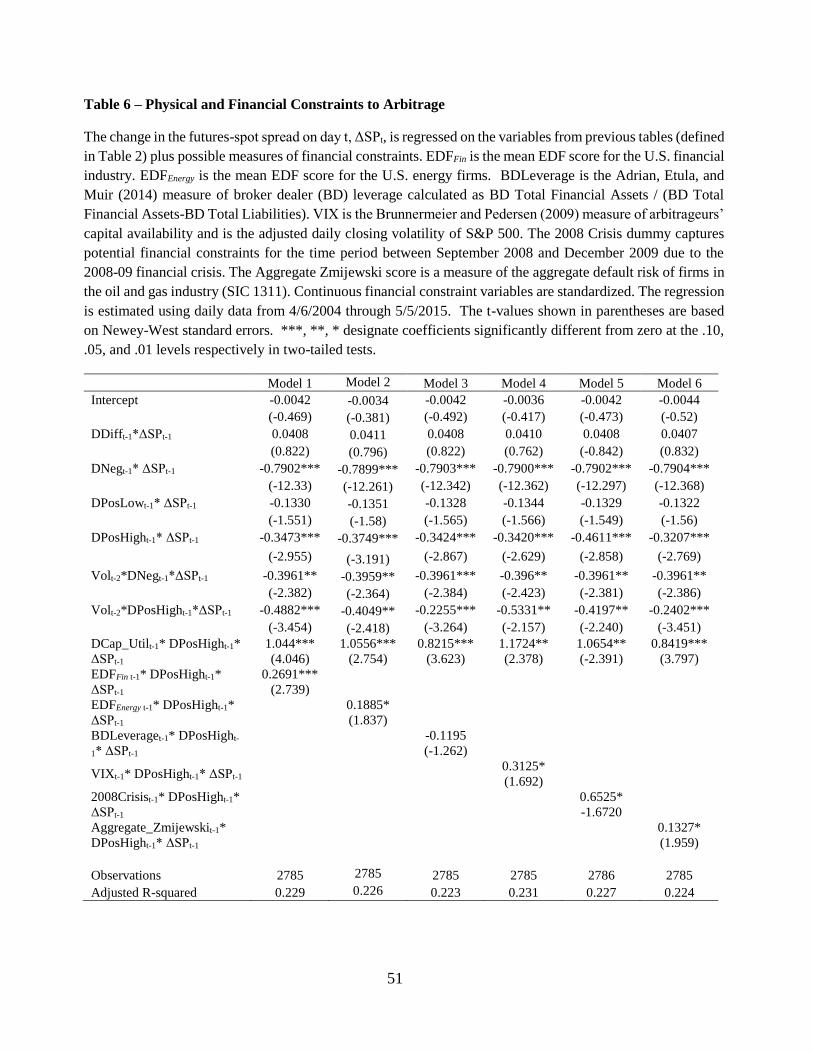

We also examine possible financial limits to arbitrage in the WTI crude oil market

concurrently with measures of physical limits to arbitrage. The importance of financial limits

to arbitrage in the oil market is highlighted by Acharya, Lochstoer, and Ramadorai (2013).7

Those authors document the effect on futures and spot prices when producers’ hedging

demand in the futures market is not fully met due to broker-dealer capital constraints. We

also present evidence that arbitrage was restricted by financial constraints over our 2004-

2015 sample period. However, the evidence in support of physical constraints impeding

arbitrage is considerably stronger and remains robust when we control for the effect of the

financial constraint measures we examine. While Acharya, Lochstoer, and Ramadorai (2013)

emphasize the importance of an inventory stock-out in giving rise to commodity sector

default risk, there is no significant oil inventory stock-out that occurs in the 2004-2015

period of our study. In contrast, our study highlights the role played by the unavailability of

storage capacity due to high inventory levels as the cause of a decoupling between the futures

and spot market in oil, an event that occurs several times during our sample period.

Therefore, our study builds on the existing literature on the financial limits to arbitrage in

commodity markets by also establishing the importance of the physical limits to arbitrage in

these markets. We therefore provide a more complete picture of the role that limits to

7 Birge, Hortacsu, and Mercadal (2016) show that financial constraints impede arbitrage in electricity markets.

7

arbitrage, both physical limits as well as financial limits, play in the pricing of commodity

futures.

We contribute to the literature on the Theory of Storage by examining the effect of

inventory storage capacity limits. The existing literature has focused on the effect of stock-

outs when inventories are very low with little or no attention to the possible pricing effects

when inventories are very high and storage capacity becomes limited or is exhausted. For

instance, Routledge, Seppi, and Spatt (2000), who explore the consequences of the non-

negativity inventory constraint for forward and futures prices, write, “Inventory can always

be added to keep current spot prices from being too low relative to expected future spot

prices.” We contribute to this literature by exploring the price consequences when

inventories approach storage capacity limits so that additional inventory cannot be added.

Modeling inventories as buffers to supply and demand shocks, Deaton and Laroque

(1992) show that the increase in the risk of an inventory stock-out when inventories are low

carries through to an increase in expected future spot price volatility. Routledge, Seppi, and

Spatt (2000) extend the Deaton and Laroque (1992) model by including a forward market

and show that inventory stock-outs can break the arbitrage link between the spot and forward

markets. Similarly, we show that when storage capacity is limited or exhausted, the

commodity’s spot price will also be decoupled from the forward price. Therefore, in the case

of both inventory stockouts and full storage situations, the arbitrage pricing relation between

forward and spot prices will break down. Additionally, consistent with the Theory of Storage,

we find that when inventories are neither very high nor very low, arbitrage restores the

futures-spot spread to its no-arbitrage bounds following temporary violations.

The rest of the paper is structured as follows. In the next section, we discuss arbitrage

and storage in the crude oil market and develop our primary hypotheses. The data is

described and basic results are presented in section 3, where we test for how the market

responds to temporary violations of the no-arbitrage limits and present evidence that

violations of the upper limit persist as storage approaches full capacity. In section 4, we

explore how reverse cash-and-carry arbitrage enforces the lower no-arbitrage limit on the

spread and whether this spread enforcing arbitrage is hindered when available oil inventories

are low. In section 5, we expand the analysis to consider financial as well as physical limits

8

to arbitrage. In section 6, we examine how spot and futures prices change due to arbitrage

and ask whether arbitrage impacts primarily the spot price, primarily the futures price, or

both. Various robustness checks are presented in section 7, and section 8 concludes.

2. Oil market arbitrage and storage

2.1. No arbitrage spread conditions in the oil market

Consider the limits that arbitrage places on the futures-spot and futures-futures

spreads at the crude oil futures contract delivery/pricing hub assuming that storage is

available for lease at the hub location.8 Let Pt,t+v designate the price at time t for delivery at

time t+v and Pt,t+s represent the time t price for delivery at time t+s where s>v. If t+v is the

first available delivery time, Pt,t+v may be referred to as the spot price and Pt,t+s-Pt,t+v as the

futures-spot spread. We will follow that convention here. Since large quantities of crude oil

cannot be delivered instantaneously, virtually all physical delivery contracts in the crude oil

market, including spot contracts, are contracts for delivery over a future period of time –

generally one month (Kaminski, 2012). For futures contracts held to physical delivery, the

CME group allows one calendar month for the oil to be delivered to the Cushing hub. For

example, suppose the current month is June. The three-month futures contract will be the

contract that, if held to expiration, will result in physical delivery of crude oil commencing

September 1 and ending on or before September 30. Similarly, delivery on the two-month

futures contract will occur from August 1-31. In the case of the “spot” contract traded in the

month of June, physical delivery of crude oil will commence July 1 and end on or before July

31. Hence by convention the quoted “spot” prices in the crude oil market are typically prices

for delivery over the nearest forward calendar month.9 Contracts that stipulate physical

delivery over shorter periods, including immediate physical delivery, are rare and typically

for small quantities that can be moved by tanker truck.

8 More generally, storage may also be available at remote locations, in which case the availability of such

remote storage will be determined by both storage and transportation constraints. 9 The CME group stipulates several methods by which the buyer can opt to receive physical delivery. At the

buyer's option, delivery can be made by: (1) by inter-facility transfer ("pumpover") into a designated pipeline or

storage facility with access to seller's incoming pipeline or storage facility; (2) by in-line (or in-system) transfer,

or book-out of title to the buyer; or (3) if the seller agrees to such transfer and if the facility used by the seller

allows for such transfer, without physical movement of product, by in-tank transfer of title to the buyer.

Especially with the third option, physical delivery will effectively be instantaneous and subject only to the

provision that the buyer has acquired the right to store oil in the tank/s used previously by the seller.

9

Let SCt,t+v,t+s represent the present value as of time t of the cost of storing one unit of

the commodity from time t+v to t+s including transaction costs on the futures trades.10 Let

CVt,t+v,t+s designate the (assumed known) present value as of time t of the convenience yield

from holding physical units of the commodity from time t+v to t+s. If Pt,t+s > [Pt,t+v +

SCt,t+v.t+s – CVt,t+v,t+s](1+rt,t+v,t+s) where rt,t+v,t+s is the interest rate from t+v to t+s, arbitrageurs

can earn a “riskless” profit by simultaneously: (1) buying the near-term contract Pt,t+v, (2)

shorting the longer term contract Pt,t+s, and (3) assuming storage capacity is available,

arranging for storage from t+v to t+s.11 An implicit assumption is that funding of the

transaction is not constrained, which we will relax in the analysis presented in section 5. As

arbitrageurs transact to capture the riskless profit, Pt,t+v should rise and Pt,t+s fall until Pt,t+s ≤

[Pt,t+v + SCt,t+v.t+s – CVt,t+v,t+s](1+rt,t+v,t+s). Hence this arbitrage should ensure that:

[Pt,t+s -Pt,t+v] ≤ [Pt,t+vrt,t+v,t+s + (SCt,t+v.t+s – CVt,t+v,t+s)(1+rt,t+v,t+s)] (1)

Ederington, Fernando, Holland, Lee, and Linn (2016) provide strong evidence in support of

this arbitrage relationship for U.S. crude oil futures at the Cushing delivery point.

Assuming trades and storage can be contracted the instant violations of equation 1 are

observed, violations of equation 1 should be fleeting and only observable in high frequency

data. However, if storage takes time to arrange (as explored in section 2.2 below), violations

of equation 1 could arise but be temporary. If storage cannot be arranged immediately, a

trader pursuing riskless arbitrage would need to wait to arbitrage the mispricing between the

spot and futures contracts until storage becomes available.12 In the latter case, the spread may

continue to exceed the no-arbitrage upper bound in equation 1 until sufficient storage

capacity becomes available. Assuming storage can be arranged, any temporary violation of

10 For ease of exposition, we disregard the possibility of storage at a location away from the hub, in which case

any transportation costs between the delivery points for the t+v and t+s contracts need to be added to the

transaction costs. 11 This trade is not completely riskless if the convenience yield is uncertain. For pedagogical simplicity we

allow future storage costs to be uncertain but treat the convenience yield as uncertain but effect of uncertainty

regarding either is basically the same. Nonetheless, risk cannot be completely eliminated due to physical and

financial performance risk. 12 Speculators could execute a naked speculative transaction involving only the spot and futures trades, hoping

that storage can be arranged in the future on terms that would not eliminate arbitrage profit. However, such

transactions are not riskless. Ederington et al. (2016) show that most cash-and-carry arbitrage transactions in

this market tend to be riskless.

10

equation 1 should be followed by a fall in the spread as arbitrage trades take place.13

However if storage is at capacity, violations of equation 1 can persist.

Our treatment of SCt,t+v.t+s in equation 1 warrants clarification. We recognize that

both SCt,t+v.t+s and CVt,t+v,t+s are endogenous. In particular, as discussed below, SCt,t+v.t+s will

tend to rise and CVt,t+v,t+s will tend to fall as inventories increase. Thus, it could be argued

that if storage cannot be arranged immediately, the cost of storage is effectively infinite so

that equation 1 always holds but this is void of any predictive content. To obtain predictive

hypotheses, when we refer to equation 1 being violated, we are treating SCt,t+v.t+s as the cost

of storage when it can be arranged.

We next examine the no-arbitrage lower bound. Consider a trader who holds the

commodity in inventory. If Pt,t+s < [Pt,t+v + SCSt,t+v.t+s – CVt,t+v,t+s](1+rt,t+v,t+s) where SCSt,t+v,t+s

is the saving on storage costs by not storing oil from t+v to t+s minus transaction costs, the

trader can profit by simultaneously: (1) selling the oil for delivery at time t+v at Pt,t+v and (2)

purchasing for delivery at time t+s for Pt,t+s. This frees up storage from time t+v to t+s. If

alternative uses for the storage can be arranged immediately or SCSt,t+v,t+s is known, this

arbitrage is riskless and arbitrage should ensure that:

[Pt,t+s -Pt,t+v] ≥ [Pt,t+vrt,t+v,t+s + (SCSt,t+v.t+s – CVt,t+v,t+s)(1+rt,t+v,t+s)] (2)

Note that this lower bound on the spread may be either positive or negative.14 If alternative

storage uses cannot be arranged immediately and SCSt,t+v,t+s is uncertain, this trade is risky

unless the trades are delayed until alternative uses for the storage have been arranged.

Therefore, it is possible that inequality (2) is violated temporarily. If inventories are depleted

so that there is no oil to sell for delivery at time t+v, then the violation of equation 2 may

persist longer.

13 Additionally, temporary violations of arbitrage bounds could occur because of inattentive traders (Duffie,

2010) or lack of sufficient financial traders in the market, which is also inhabited by physical traders who have

traditionally dominated the market. 14 In commodity futures market analyses, it is sometimes assumed that (1) transaction costs are negligible, and

(2) any storage costs can be completely recaptured if the storage is not used so that SCSt,t+v,t+s = SCt,t+v,t+s and

hence [Pt,t+s -Pt,t+v] = [Pt,t+vrt,t+v,t+s + (SCt,t+v.t+s – CVt,t+v,t+s)(1+rt,t+v,t+s)]. However we argue in section 2.2 below

that in commodity markets, and crude oil in particular, SCSt,t+v,t+s is generally less than SCt,t+v,t+s either because

transaction costs are not negligible or because storage costs cannot be totally recouped if the storage is unused.

Hence there is normally a gap between the upper and lower spread limits in equations 1 and 2.

11

2.2. Storage and storage costs

If oil is purchased for delivery at time t+s and sold for delivery at time t+v in a cash-

and-carry arbitrage, storage must be arranged for the time period between t+s and t+v. Since

the availability and cost of storage are important to our analysis, it is helpful to summarize

relevant characteristics of crude oil storage. Once produced, crude oil may be stored in tank

farms, underground caverns, refineries, and pipelines, or off-shore in tankers. Particularly

important for our purpose are storage levels and costs at the pricing point and delivery hub

for the WTI futures contract, which is in Cushing, Oklahoma. Ederington et al. (2016) find

that most arbitrage in the WTI crude oil market entails Cushing oil inventories. The U.S.

Energy Information Administration (EIA) estimates the working capacity of tank farms in the

U.S. at 399.7 million barrels as of September 2015 of which 73 million barrels, or 18.0%, are

at Cushing, making it the largest oil storage facility in the world (EIA, 2015,

http://www.eia.gov/petroleum/storagecapacity/table1.pdf ). Cushing, labeled the “pipeline

capital of the world,” is connected to crude oil production facilities and oil refineries

throughout the United States through an extensive pipeline network. Oil is stored in Cushing

for operational, arbitrage, and speculative purposes. While anecdotal and media reports

appear from time to time about investment banks and other oil traders leasing storage at

Cushing for arbitrage and speculative purposes (see, for example, Leff, 2015), hard data is

unavailable. However according to the EIA, in spring 2015 approximately 80% of the storage

at Cushing was leased by the owner-operators to others while the percentage leased to others

at other tank farms in the U.S. was only about 29%. Storage away from Cushing entails

additional transportation costs or additional risk to arbitrage using crude oil futures since the

delivery point for the NYMEX oil futures contract is Cushing.15 This suggests that much of

the storage at Cushing is leased for arbitrage or speculative purposes. Storage capacity at

Cushing has grown considerably over the last decade. The EIA reports that working capacity

increased from 46.0 million barrels in September 2010 to 71.4 million in March 2015.

Capacity figures prior to 2010 are unavailable but the maximum held in storage prior to

January 2006 was only 22.8 million barrels. The business media commonly attribute at least

15 Nonetheless, the press has published articles describing crude oil being stored on floating tankers in

conjunction with arbitrage trades (See, for example, Kent and Kantchev, 2015). However, a precise time series

of tanker storage data is not available.

12

some of this storage construction to demand for storage by WTI futures traders (see, for

example, Blas, 2015, and Kaufman, 2015).

Storage contracts at Cushing and elsewhere are typically over-the-counter and thus

may require some time to arrange.16 Moreover, they have counterparty risk, force majeure

and physical delivery risk elements that are not present in purely financial arbitrage trades,

which may discourage or delay the actions necessary to implement the arbitrage trades. If

delayed, spreads above the no-arbitrage limit may persist until storage can be arranged.17

Unfortunately, historical figures for the storage cost measures SCt,t+v,t+s and SCSt,t+v,t+s

are unavailable so we cannot directly test for violations of equations 1 and 2. Instead, as

explained below, we test for indirect evidence of violations and consequent market

corrections by examining changes in the futures-spot spread. Average crude oil storage costs

at Cushing are commonly estimated around $0.40 to $0.50 per barrel per month but

reportedly vary considerably depending on capacity utilization.18 If a trader wants to execute

an arbitrage transaction but has not yet leased storage capacity, the cost to him is the storage

cost per barrel stated in the new lease. If a trader has already leased storage, what matters to

him in considering a particular arbitrage possibility is the storage unit’s opportunity cost,

which will vary with capacity utilization and quite possibly across individual traders.

Consider, for instance, a trader who has leased storage capacity for a year at $0.50 a

barrel/month. After the lease is signed, the $0.50 becomes a sunk cost and what then matters

is the marginal opportunity cost of using the storage capacity. Depending on whether it is

possible to re-lease the unused storage capacity, this marginal opportunity cost may vary

from zero to the re-lease rate. Moreover the unused storage has an option value. If the trader

institutes a cash and carry arbitrage as soon as the spread widens sufficiently to make the

arbitrage profitable and hence fills his storage units to capacity, he loses the option to

conduct the arbitrage on even more favorable terms in the future if spreads should widen

16 The CME has recently launched an oil storage futures contract at the Louisiana Offshore Port but not as yet

for storage at Cushing. 17 Faced with an apparently profitable futures-spot spread that exceeds expected storage costs, some traders may

trade the futures and spot immediately. In doing so, they accept the risk that storage cannot be arranged or will

be more expensive than anticipated and the trade will remain a speculation unless and until the exposure is

covered in the physical market. 18 Private communication with a company specializing in oil and petroleum product storage confirms that the

typical price has been about $.50/barrel per month but that the cost increases whenever the market is in

contango, suggesting those are periods in which demand for storage capacity is high.

13

further. Thus, in this case, SCt,t+v,t+s is hard to measure and may vary across traders but

undoubtedly varies positively with capacity utilization.

While storage costs likely vary positively with capacity utilization, the convenience

yield likely varies inversely as Einloth (2009), Gorton, Hayashi, and Rouwenhorst (2013)

and others point out, reinforcing the tendency for the upper no-arbitrage bound in equation 1

to vary positively with capacity utilization levels. Gorton, Hayashi, and Rouwenhorst (2013)

argue that the convenience yield in commodity futures should vary inversely with inventory

levels since low inventory levels increase price volatility. Consistent with this, using data for

33 commodity markets, they find that: 1) the cash-futures basis is an inverse function of

inventory levels, and 2) returns to a strategy of holding long futures positions are positive and

inversely correlated with inventory levels. Turning to reverse-cash-and-carry arbitrage, the

storage cost savings if the trader draws down his inventory, SCSt,t+v,t+s, depend on whether

the storage tank can be re-leased or used for other purposes since he will pay the storage cost

per barrel of leased capacity whether he has oil stored or not. If it cannot be re-leased,

SCSt,t+v,t+s is zero.

Since we hypothesize that arbitrage possibilities are limited by available storage

capacity and that storage costs vary directly with capacity utilization, we need measures of

both actual storage levels and storage capacity at Cushing. Since the EIA began reporting

actual weekly Cushing storage levels in April 2004, our data period begins April 5, 2004.19

The EIA began surveying and reporting storage capacity figures semi-annually in September

2010.20 Since the EIA’s capacity figures cover only the latter third of our data period and

only estimate shell and working capacity, not effective capacity, we use as our primary proxy

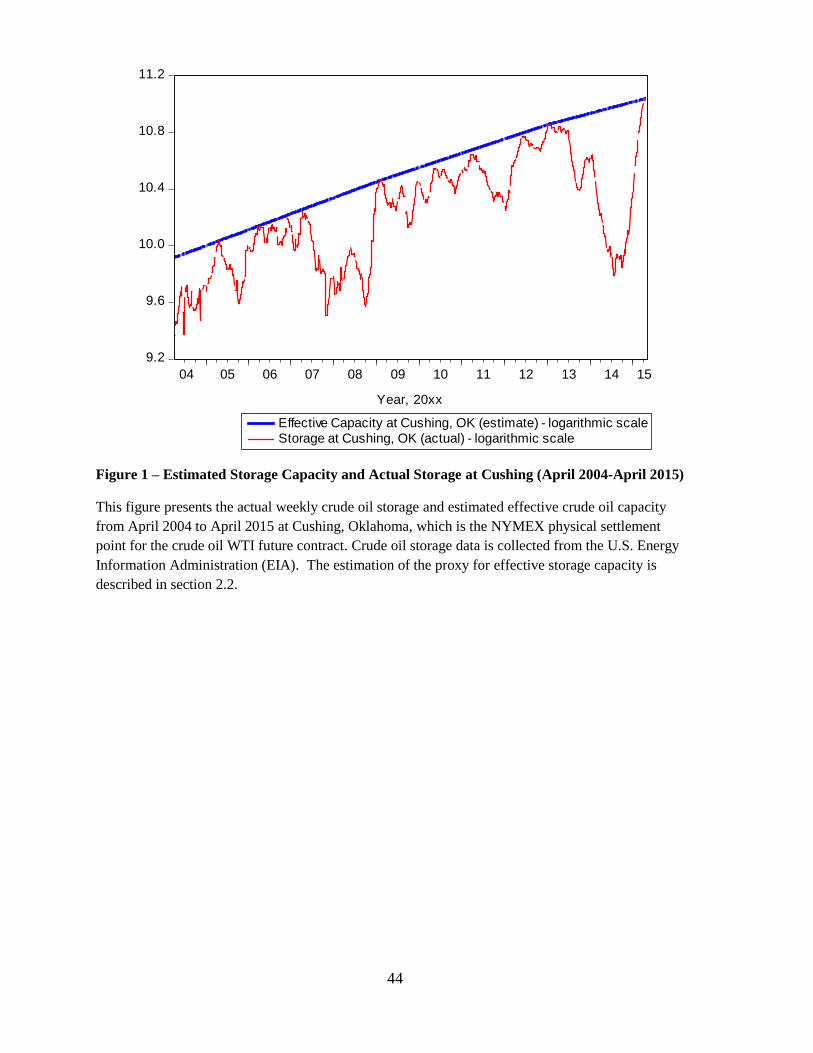

for effective capacity a measure based on historical peaks in actual storage. In Figure 1, we

chart Cushing estimated working storage capacity levels and actual storage levels from April

2004 to April 2015 on a logarithmic scale.

***Insert Figure 1 about here***

Searching for the lowest number of peaks or inflection points for a linear spline

19 Prior to that time the Cushing figures were lumped into those for the Midwest region. 20 The EIA reports both shell capacity and working capacity where the latter lower figure adjusts for the fact

that oil at the bottom of the tank is not obtainable and that the tanks cannot be filled to the very top. Both the

EIA and others stress that the unknown effective capacity is less than either figure since some space is required

for effective operation.

14

function, which bounds all observed storage levels with inflection points at the chosen peaks,

yields the linear spline with peaks at 4/18/2005, 2/2/2009, 1/4/2013, and 4/3/2015 shown as

the solid blue line in Figure 1 where we also graph actual storage levels. We use this log

linear function as our initial and primary proxy for computing effective storage capacity. In

section 7, we also use the EIA measures of working capacity for the October 2010 – April

2015 sub-period for which these figures are available.

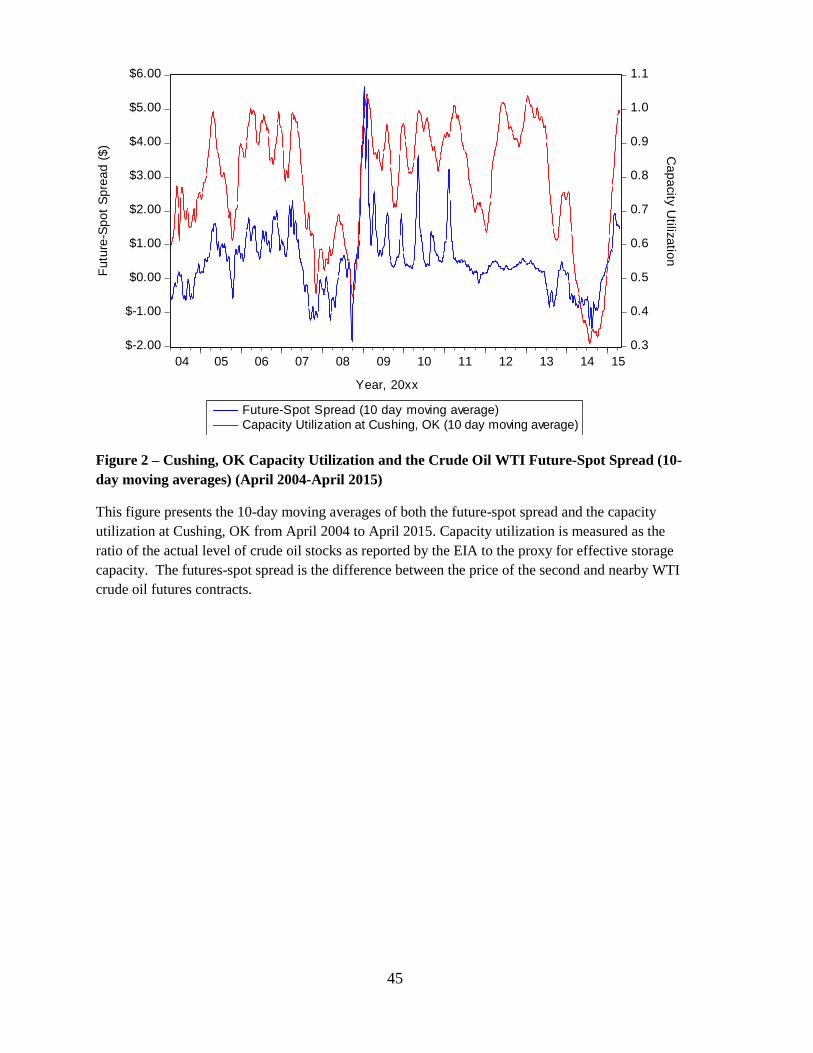

2.3. Storage and spreads – Initial evidence

According to the analysis in section 2.l, large positive spreads between the prices of

contracts for longer-term and near-term delivery should only persist when storage levels

approach capacity so that arbitrageurs find it difficult or impossible to arrange storage.

Initial evidence on this is presented in Figure 2 where we chart 10-day moving averages of

both capacity utilization and the futures-spot spread.

***Insert Figure 2 about here***

Capacity utilization is measured as the ratio of the actual level of crude oil stocks as

reported by the EIA to the proxy for effective storage capacity described in section 2.2. The

futures-spot spread in Figure 2 is measured as the difference between the price of the second

and nearby futures contracts. As predicted, Figure 2 shows that large positive futures-spot

spreads are generally associated with high levels of capacity utilization.

2.4. Hypotheses

While Figure 2 indicates that high futures-spot spreads are generally associated with

high levels of capacity utilization, this does not necessarily indicate that physical limits to

arbitrage were a constraint since other factors could account for the correlation in Figure 2.

For instance, an unexpected short-term decline in the demand for crude oil which is not

expected to persist could lead to both an increase in crude oil inventories and a

disproportionate decline in the spot price, and therefore an increase in the spread.

For further evidence on the effect of arbitrage and its limits, we analyze the behavior

of the futures-spot spread across time. Ideally, if we could observe the storage cost and

convenience yield terms, SCt,t+v,t+s, SCSt,t+v,t+s, and CVt,t+v,t+s, in equations 1 and 2, we could

15

explore how they change as storage levels approach capacity and test for violations of

equations 1 and 2. However, as explained in section 2.2 those data are unobservable.

Consequently, we test for arbitrage and its limits based on the behavior of the futures-spot

spread.

Consider the implications of the analysis in section 2.1 for the behavior of the futures-

spot spread. As long as the futures-spot spread is between the upper bound defined by

equation 1 and the lower bound defined by equation 2, arbitrage should not occur. In this

case, if markets are weak form efficient and news arrives randomly, the change in the spread

one day should be independent of previous spread changes. However, if a change in the

spread in period t-1 carries the spread above the no-arbitrage bound, this should set off

arbitrage in which arbitrageurs buy for delivery in the near-term and sell for delivery in the

longer-term resulting in a decline in the spread in period t. Likewise, a fall in the spread

below the no-arbitrage upper bound in period t-1 should set off arbitrage that raises the

spread in period t. Thus, we expect successive changes in the spread to be uncorrelated

within the upper and lower no-arbitrage bounds and negatively correlated outside the no-

arbitrage bounds.

Testing for evidence of arbitrage based on spread autocorrelations is complicated by

the fact that we cannot observe storage costs, transaction costs, the convenience yield, or the

storage cost savings when storage levels are reduced, and so we cannot compute the upper

and lower no-arbitrage bounds. However, we expect storage costs to vary directly and the

convenience yield to vary inversely with storage capacity utilization and thus, the upper

bound should rise as capacity utilization rises. In addition, for given values of the no-

arbitrage bounds, the likelihood that a change in the spread leads to a violation of the upper

or lower bounds should depend on the sign and size of both the change in the spread and its

16

prior level.21 For instance, suppose the period t-1 change in the spread is positive. In this

case, it is more likely that it crosses the upper bound and thus leads to a fall in the spread in

period t if the spread level at the beginning of period t-1 is positive and high than if the

spread at the beginning of period t-1 is negative or low. Likewise, a given decline in the

spread in period t-1 is more likely to cross the lower bound, and thus lead to a rise in period t,

if the spread at the beginning of period t is already negative or low. This leads to our first

hypothesis:

H1: If there are no limits to arbitrage, an increase (decrease) in the futures-spot spread should

be more likely to lead to arbitrage and a subsequent fall (rise) in the spread if the spread is

already high (low).

It is not clear a priori whether we should observe this predicted autocorrelation

pattern in weekly, daily, hourly, or higher frequency data. If the arbitrage can be arranged

almost instantaneously, then we should observe these patterns only in high frequency data if

at all. However, we have argued above in sections 2.1 and 2.2 that, when the spread rises

above the upper bound, risk or the inability to arrange storage may lead arbitrageurs to delay

going long in the near-term contract and shorting the longer-term contract until they can

contract for storage. Thus it may take hours or days until the spread change reverses. We test

for arbitrage patterns in daily data.

We have argued above that there are likely physical limits to arbitrage. When storage

is near capacity, both storage costs and the lead time required to contract storage will likely

increase. Given these difficulties in storage contracting when storage is near capacity, a

21 To see this, suppose the upper bound is fixed and equal to U. Suppose also that at t-1 the actual spread equals

A. The distance to U therefore equals U-A. The narrower the gap the smaller is the required change in the

spread before the upper bound is breached. Assume arbitrage opportunities arrive randomly (that is the change

in the spread arrives randomly each period) and that the size of the change is a drawing from a stationary

distribution with mean 0 and constant variance. The probability that U will be breached given U and A equals

the probability that the change will exceed U-A. To illustrate, suppose the change in the spread is a drawing

from a 2(0, )N distribution. Therefore, the probability that the change will breach U equals PrU A

z

,

which is increasing in A since U is fixed. Conditional on the change equaling an arbitrary value P, the

probability evaluated at t-1 equals PrU A P

z

which is increasing in P given U and A.

17

spread change reversing arbitrage is less likely, implying lower first-order autocorrelation.

This leads to our second hypothesis:

H2: When storage levels are at or near capacity, cash-and-carry arbitrage is more costly or

difficult, thus if the futures-spot spread is positive and high, a further increase in the spread is

less likely to be followed by arbitrage and a reversal in the spread.

Similarly, if there is an inventory stockout or if inventories are at the minimum required for

operational purposes, reverse cash-and-carry arbitrage, in which arbitrageurs sell from

inventory in the spot market, cannot occur, leading to our third hypothesis:

H3: When tradeable inventory levels are at or near zero, reverse cash-and-carry arbitrage is

more costly or difficult, thus if the futures-spot spread is negative and low, a further decrease

in the spread is less likely to be followed by arbitrage and a reversal in the spread.

3. Results

3.1. Data description and initial evidence.

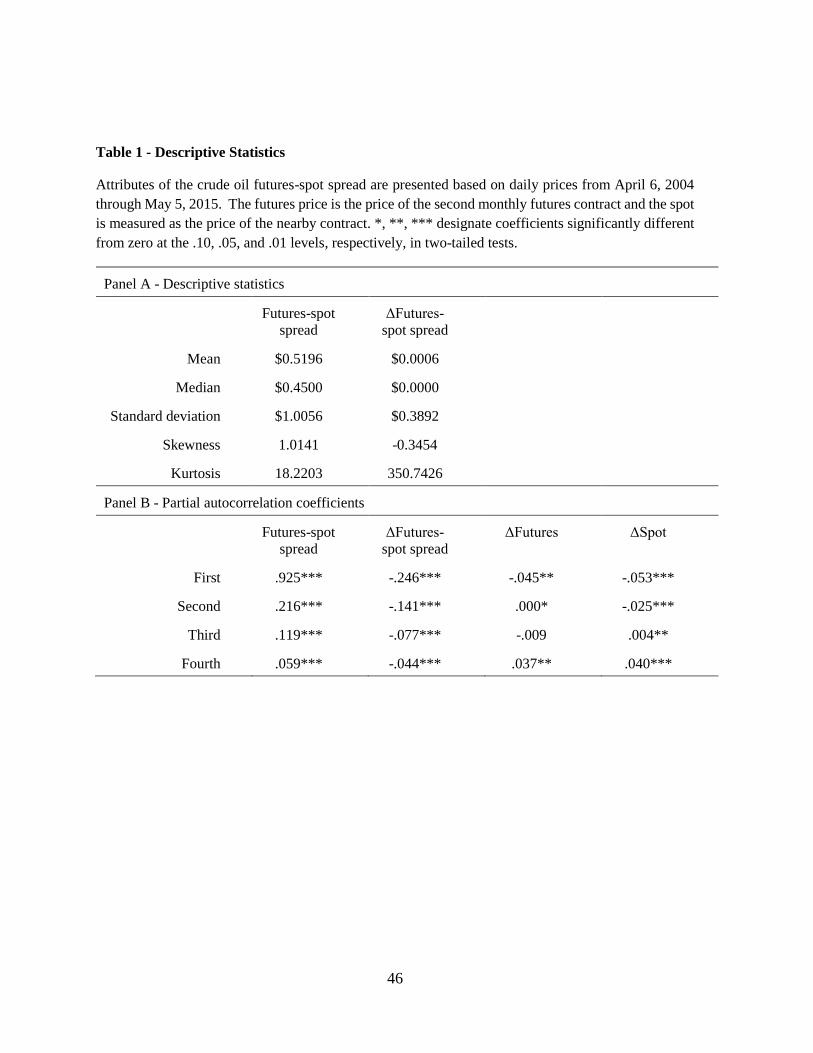

While futures and spot price data are available from 1983, our data period begins in

April 2004 when the EIA began reporting crude oil stock levels at Cushing. We examine

daily prices of NYMEX WTI crude oil futures contracts from April 6 2004 through May 6,

2015 obtained from the website of the Energy Information Administration. Descriptive

statistics for the futures-spot spread measured as the difference between the prices of the

second and nearby contracts are presented in Table 1 for both the level and daily changes in

the spread.

***Insert Table 1 about here***

Interestingly, while Schwartz (1997) and Routledge, Seppi, and Spatt (2000) argue

that in this market backwardation should be more common than contango, the market

actually tended to be in contango over much of this period with the spread averaging $0.52,

as shown in Panel A. The spread was positive on 76.5% of the observed days. With a

standard deviation of $0.39, daily changes in the spread were fairly large.

18

Partial autocorrelations out to a four-day lag are reported in Panel B for both the

spread and its components. Several patterns are worth noting. First, consistent with our

arbitrage argument, there is evidence of fairly strong mean reversion with a first order

autocorrelation of -0.246 between changes on successive days. Clearly, there is a tendency

for increases and decreases in the spread to be partially reversed on subsequent days. In the

absence of arbitrage, this would seem to violate weak-form efficiency. Second, the spread

displays considerably more mean reversion than either of its two components. The first order

autocorrelation for the futures and spot price changes are only -0.045 and -0.053 respectively.

This indicates that the mean reversion of the spread is not simply a reflection of mean

reversion in the spot and futures prices due to some other cause such as bid-ask bounce.

Third, while the first-order autocorrelation in spread changes is clearly the largest, there is

also evidence of negative partial correlation at lags of two and three days. As we discussed

above, it is unclear a priori how long it would take arbitrageurs to contract storage and thus

how quickly arbitrage should reverse violations of the no-arbitrage bounds. If indeed the

mean reversion observed in the spread is due to arbitrage, this indicates that most of the

reversal takes place in one day but that full reversal may take several days.

3.2. Testing for evidence of arbitrage activity and physical limits to arbitrage

According to the arbitrage hypothesis, mean reversion in the spread should be

observed only when the change in the spread crosses the no-arbitrage bounds – and then only

if arranging the arbitrage transactions occurs with a lag. As long as the spread is fluctuating

within the no-arbitrage bounds, weak form efficiency implies that there should be little, if

any, autocorrelation. As discussed above, testing is complicated by the difficulty in

measuring the no-arbitrage bounds. However, as we argued in section 2.4 and H1, an

increase in the spread in period t-1 is more likely to cross the no-arbitrage upper bound, and

thus lead to mean reversion in period t, if the spread is already positive and high than if it is

negative or low. Likewise, a negative change in the spread is more likely to cross the no-

arbitrage lower bound leading to mean reversion if the spread is already low.

To test this, we examine variations of a simple regression ΔSPt = β0 + β1ΔSPt-1+et, 22

22 The estimated β1 = -0.246 which is significant at the 1% level based on Newey-West standard errors.

19

where ΔSPt = SPt – SPt-1 and SPt = Ft – St with Ft being the futures price on day t and St

being the spot price. We consider several variations. First, we divide the sample into (1)

cases when the change in the spread and the beginning spread have the same sign and (2)

cases when they have different signs. We define DSamet-1 =1 if ΔSPt-1*SPt-2 >0 and =0

otherwise. Thus DSamet-1 =1 if a positive spread at time t-2 is followed by a further increase

in the spread at time t-1 or if a negative spread at time t-2 is followed by a further decrease at

time t-1, i.e. if the spread at time t-2 and the change in day t-1 have the same sign. We define

DDifft-1 =1-DSamet-1. Thus DDifft-1=1 if ΔSPt-1*SPt-2 <=0, i.e., if the spread change on day t-

1 is opposite in sign to the spread on day t-2. As reported in Table 2 DDifft-1=1 is slightly

more common than DSamet-1=1 since it includes the cases when ΔSPt-1 or SPt-2 are zero.

***Insert Table 2 about here***

Second, we separate those cases when the change in the spread (at time t-1) and the

beginning spread (at time t-2) have the same sign into two groups: contango, where both

signs are positive (so that the upper bound might be violated) and backwardations, where

both signs are negative (or zero) (so that the lower bound might be violated). DPost-1=1 if

SPt-2>0 and ΔSPt-1>0 and zero otherwise and DNegt-1=1 if SPt-2<0 and ΔSPt-1<0 and zero

otherwise. Table 2 shows that during our sample period DPos is more common than DNeg.

Third, given that the spread is positive and in contango for 76.5% of the observations

in our sample, we further divide the set when a positive spread is followed by a further

increase in the spread into: (1) those cases when the time t-2 spread is positive but less than

$0.50 and (2) those cases when the time t-2 spread is positive and greater than $0.50. We

choose $0.50 since this is a common estimate of storage costs and since the median spread is

$0.45. Specifically, we take cases where the spread is positive (SPt-2>0) and the change in

spread is positive (ΔSPt-1>0) and define DPosLowt-1=1 if the spread is between 0 and $0.50,

0<SPt-2<=0.50, and zero otherwise and DPosHight-1=1 if the spread is above $0.5 (SPt-2>0.5)

and zero otherwise.

Fourth, we consider instances of contango where the spread is more likely to provide

opportunities for arbitrage (positive, increasing and above $0.50) but storage capacity is

exhausted. To test this, we define the dummy variable DCap_Utilt=1 if the ratio of actual

Cushing storage levels announced by the EIA for that week divided by our estimate of

20

effective capacity based on historical production peaks as described in section 2.2 is in the

top 20% of observed levels of capacity utilization. This translates to capacity utilization rates

exceeding approximately 92%.23 Since storage levels should only affect the likelihood of

arbitrage when the spread increases from already high levels, we interact this variable with

DPosHigh t-1. As reported in Table 2, DCap_Utilt-1*DPosHight-1=1 for approximately 7.4%

of our observations.

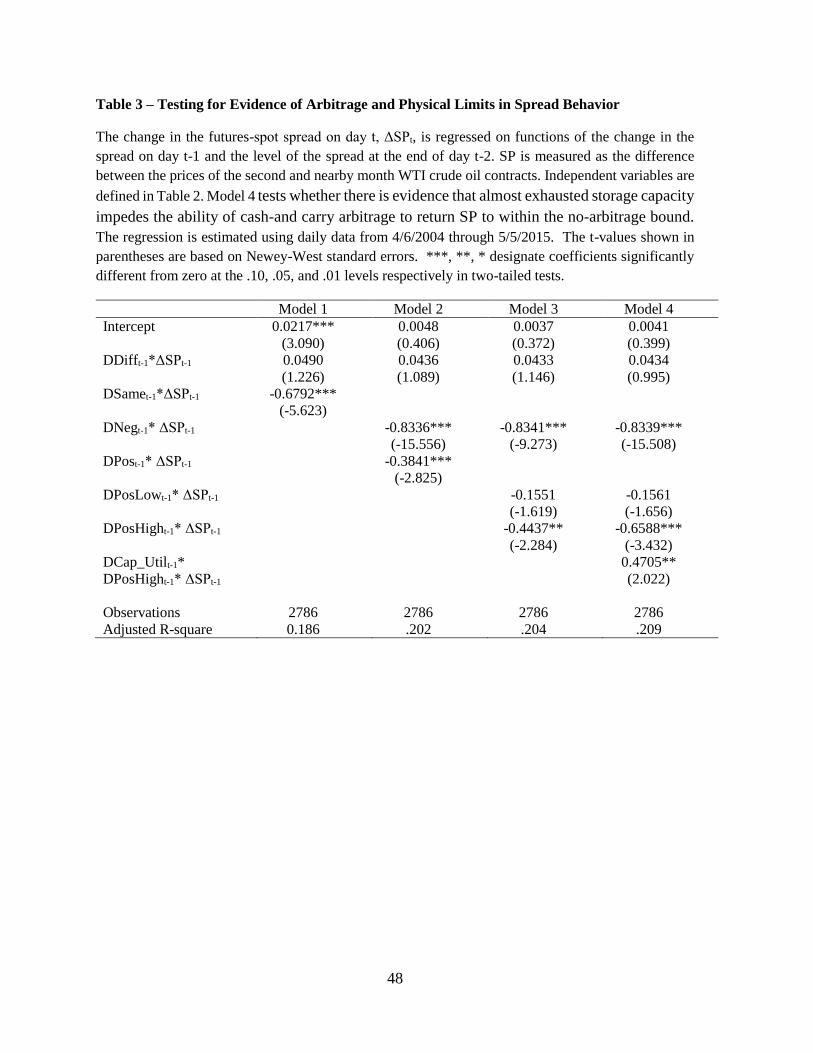

Table 3 presents results of the four variations of the simple regression ΔSPt = β0 +

β1ΔSPt-1+et described above. Model 1 examines periods where change in the spread and the

beginning spread have the same sign and those with the opposite sign by modifying the

above mentioned simple regression in the following manner: ΔSPt = β0 + β1DDifft-1*ΔSPt-1

+β2 DSamet-1*ΔSPt-1+ et. According to our hypothesis H1, the likelihood of setting off

arbitrage by crossing either no-arbitrage bounds is greater if DSamet-1=1; thus H1 implies β2-

β1<0. Model 2 examines periods where change in the spread and the beginning spread have

the same sign and further separates those into periods of backwardation (negative spreads)

and contango (positive spreads). We expect that the coefficient of DNegt-1*ΔSPt-1 will be

more negative than that of DPost-1*ΔSPt-1.24

***Insert Table 3 about here***

Model 3 further divides contango cases into those where spreads are above and below

$0.50 We expect more instances of spread movements above the $0.50 level to set off cash-

and-carry arbitrage (given that the approximate cost of storage is $0.5), and thus more mean

reversion, when DPosHight-1=1. Model 4 adds a physical storage capacity limit. In

hypothesis H2 in section 2.4., we hypothesized that as crude oil storage tanks approach

capacity, storage costs rise, thereby elevating the no-arbitrage upper bound for cash-and-

carry arbitrage. This implies that, for a given level of SPt-2, a further increase in the spread is

less likely to cross the no-arbitrage bound setting off cash-and-carry arbitrage and mean

reversion when capacity utilization is high. We also hypothesized that arbitrage and mean

23 We consider alternative measures of storage capacity utilization in section 7. 24 We have argued that SCSt,t+v,t+s is generally less than SCt,t+v,t+s and therefore, expect the likelihood that

the lower bound is crossed when Dnegt-1=1 to be greater than the likelihood that the upper bound is crossed

when Dpost-1=1. This depends on the relative sizes of storage costs, SC, storage cost savings, SCS and the

convenience yield, CV, in equations 1 and 2. But, the fact that mean and median spreads are strongly positive

and that negative spreads are observed only 23.3% of the time suggests that storage costs and savings normally

exceed the convenience yield in this market so that the absolute value of the upper bound exceeds the absolute

value of the lower bound (which may even be positive).

21

reversion might be delayed because more time may be required to contract storage when

capacity is tight. This implies that even when other conditions for cash-and-carry arbitrage

are met, i.e. a further increase in the spread from already high spread levels, arbitrage and

mean reversion are less likely when storage levels are already high. Therefore, we expect less

mean reversion when DCap_Utilt-1*DPosHight-1=1.

Results for Model 1 in Table 3 are striking. 𝛽1̂ is insignificant and even positive in

sign, indicating that there is no evidence of mean reversion on day t when a positive spread at

time t-2 is followed by a negative change at time t-1 or a negative spread at time t-2 is

followed by a positive change on day t-1. This is consistent with our argument that in these

cases, the change on day t-1 is unlikely to cross the no-arbitrage bounds and set off arbitrage.

In summary, when the change in the spread in period t-1 has the opposite sign to the level of

the spread at the beginning of period t-1, making it unlikely that the change in period t-1

carried the spread outside the no-arbitrage bounds, there is no evidence of mean reversion or

arbitrage and weak form efficiency holds.

On the other hand, 𝛽2̂ = -.679 which is significant at the .0001 level based on Newey-

West standard errors. This implies that when a positive spread on day t-2 is followed by a

further increase in the spread on day t-1 or when a negative spread is followed by a further

decrease, approximately two-thirds of the day t-1 change is reversed on day t. This is

consistent with our argument that in these cases, the change on day t-1 is more likely to cross

one of the no-arbitrage bounds leading to arbitrage which partially reverses the day t change.

Needless to say 𝛽2̂ - 𝛽1̂ <0 and the difference is significant at the .0001 level confirming

hypothesis H1. This evidence also indicates that arranging arbitrage trades takes some time,

likely because storage takes time to arrange, so that temporary violations of the no-arbitrage

limits are observed.

Model 2 in Table 3 examines cases where the spread on day t-2 and change in spread

on day t-1 have the same sign, which are further separated into cases where the spread is

increasing or decreasing. While significantly negative in both cases, as expected, the

coefficient of DNegt-1*ΔSPt-1 is considerably larger in absolute terms than the coefficient of

DPost-1*ΔSPt-1. The difference between the two is significant at the .01 level. This pattern is

consistent with our argument that the no-arbitrage lower bound is smaller in absolute terms

22

than the upper bound, and may even be positive in some periods so that arbitrage is more

likely when the t-2 spread and the t-1 change are both negative than when both are positive.

Model 3 shows that, as hypothesized, when the time t-2 spread is positive, the

tendency for the spread to mean revert is much stronger when the beginning spread exceeds

$0.50 than when it is positive but less than $0.50. Thus, it appears that increases in the spread

are more likely to cross the no-arbitrage upper bound thus leading to cash-and-carry arbitrage

if the t-2 spread is more than approximately $0.50. This further confirms our hypothesis H1.

Model 4 confirms our hypothesis H2. The coefficient of DCap_Utilt-1* DPosHight-1*

ΔSPt-1 is positive and significant at the .05 level. Moreover, the coefficient of DPosHight-1*

ΔSPt-1 is a highly significant -0.6588. The latter result implies that when the spread increases

from a level exceeding $0.50, approximately 65.88% of the increase in the spread tends to be

reversed the next day if capacity utilization levels are below the top 20%. However, when

capacity utilization levels are in the top 20% of observed utilization levels, the estimated

reversal is only 0.6588-0.4705 = 18.83% which is insignificant at the 10% level. In other

words, when the spread already exceeds $0.50, a further increase in the spread tends to be

mostly reversed if capacity utilization is low but not reversed significantly if capacity

utilization is already high. This is consistent with our argument that available storage

capacity imposes a physical limit on cash-and-carry arbitrage.

Note that when capacity utilization is high and storage approaches its capacity limits,

the cost of storage increases causing the spread to increase. However, this effect works

against our finding evidence supporting H2. Specifically, when DPosHight- 1=1 and

DCap_Utilt-1=1, the mean of SPt-1 is $1.891 while when DPosHight- 1=1 and DCap_Utilt-1=0,

the mean of SPt-1 is $1.219. Thus, in the absence of storage limits, the incentive to undertake

cash and carry arbitrage that would reverse the spread increase would be even greater when

DCap_Utilt-1=1 implying a negative coefficient for DCap_Utilt- 1* DPosHight-1* ΔSPt-1.

Despite this, we find a positive coefficient, indicating that cash-and-carry arbitrage is less

likely to occur when actual oil in storage is close to capacity.

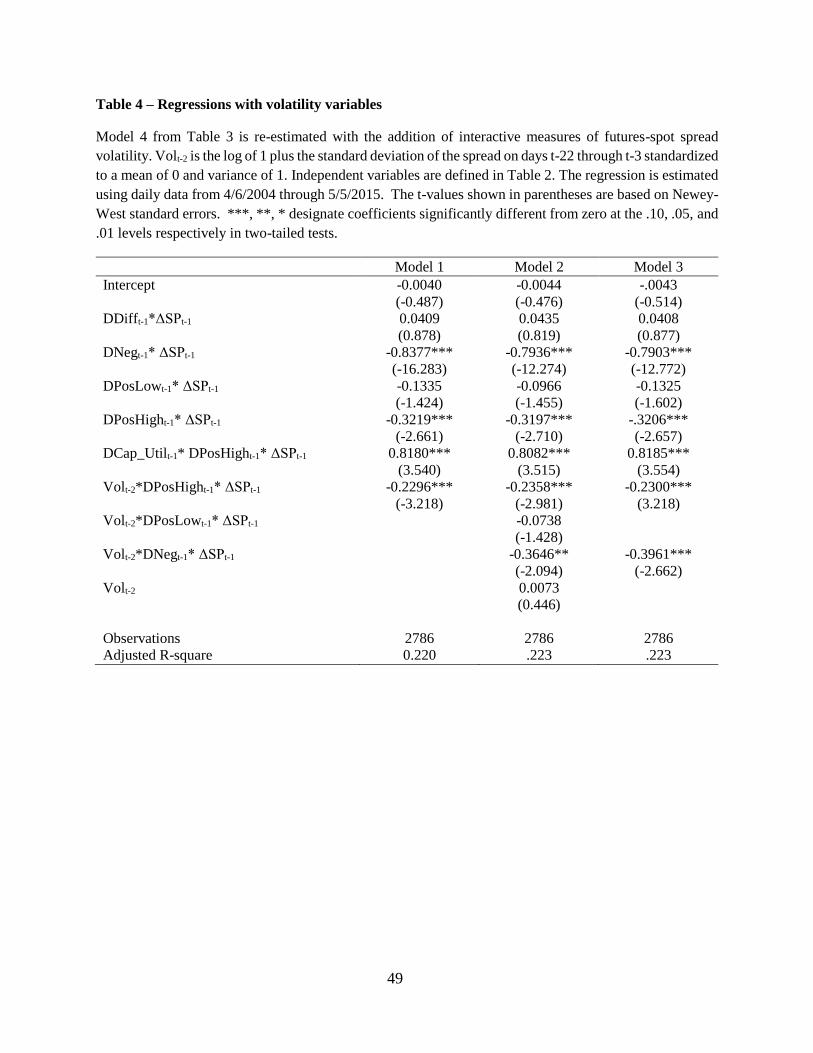

3.3 Volatility

In Table 4, we add measures of spread volatility to the regression. Movements of the

23

futures-spot spread are more likely to cross the no-arbitrage bounds and thus trigger C&C

arbitrage when spread volatility is high. In our regressions, we relate the spread change at

time t to the change in the spread at time t-1, but profitable arbitrage may also be more likely

if the changes in the spread at times t-2, t-3, t-4 etc. were large. Also, our measure of the

change based on settlement prices, misses intraday spread changes which might set off

arbitrage and these are likely larger when volatility is high. Finally, spread volatility tends to

be higher when Cushing storage tanks are almost full. Hence it is important to control for

volatility when testing for evidence of physical limits to arbitrage.

Our measure of spread volatility is the log of one plus the standard deviation of the

futures-spot spread over the 20 days prior to t-2. With the exception of ΔSPt-1, all our

independent variables in Table 3 are zero-one dummies. To facilitate interpretation of the

coefficient of the continuous volatility variable and comparison with the other coefficients,

we standardize this log volatility measure to a mean of zero and variance of one.25 We label

this variable: Volt-2. As explained and confirmed above, in the absence of physical limts,

violation of the upper no-arbitrage limit should be most likely when the spread increases at

time t-1 after already exceeding $0.50 at time t-2. To test whether violation of the no-

arbitrage limit and thus a reversal of the spread increase at time t-1 under these conditions is

more likely when spread volatility is high, we interact Volt-2 with DPosHight-1* ΔSPt-1 and

add this variable to Model 4 of Table 3. The hypothesis that C&C arbitrage is more likely

when volatility is high implies a negative coefficient on the new interaction variable.

*** Insert Table 4 about here ***

Results with this variable added are reported as Model 1 in Table 4. As expected the

coefficient of the interactive volatility variable is negative and significant at the 1% level

implying C&C arbitrage is more likely when volatility is high. The coefficients in Table 4

imply that when spread volatility is at its mean level, i.e. Volt-2=0, and storage is not

constrained, approximately 32.2% of the increase in the spread at time t-1 (from an already

high level a time t-2) tends to be reversed at time t. However, when volatility is one standard

deviation above its mean, approximately 55.2% (-0.3219-0.2296) of the increase in the

spread at time t-1 tends to be reversed.

25 Prior to standardization, the mean was .23213 and standard deviation .1955.

24

Importantly, controlling for volatility leads to a substantial increase in the coefficient

of the capacity utilization variable which rises from .4705 in Table 3 to .8180 and is now

significant at the .1% level. The implication is that C&C arbitrage is impeded when oil

storage approaches capacity.

Our evidence in Table 3 indicates that, consistent with reverse C&C arbitrage, a

further decline in the futures spot spread at time t-1 from an already negative level at time t-

2, tends to be partially reversed at time t. To test whether this tendency is even stronger

when volatility is high (as we would expect), in Model 2, we add a variable in which we

interact Volt-2 with DNegt-1* ΔSPt-1. The hypothesis that reverse C&C arbitrage is more likely

when volatility is high implies a negative coefficient.

We found no significant evidence in Table 3 that increase in the spread at time t-1

from a positive but low level at time t-2 (specifically < $0.50) sets off C&C arbitrage. To

test whether spread volatility impacts the probability of a spread reversal in this case, we

interact Volt-2 with DPosLowt-1*ΔSPt-1. We have no strong prior for this coefficient sign. It

is possible that while the conditions for C&C arbitrage are not normally met in this case, they

might be when volatility is high implying a negative coefficient. On the other hand, it may

be that volatility has little impact when the other conditions for arbitrage are not met

implying a coefficient insignificantly different from zero.

Finally, in Model 2 in Table 4 we include Volt-2 un-interacted. We do not expect a

significant coefficient for this variable since our theory implies that the impact of volatility

on the change in the spread at time t should be conditional on the prior level and change in

the spread. Nonetheless, it seems prudent to put this expectation to the test and to determine

if our interacted volatility variables are actually just proxying for an un-interacted effect.

The results in Model 2 confirm our expectations. Consistent with our reverse C&C

arbitrage hypothesis, the coefficient of Volt-2*DNegt-1* ΔSPt-1is negative and significant

implying that when the spread at time t-1 declines further from an already negative level, the

spread reversal tendency at time t is stronger when volatility is high. As expected the

coefficient of the un-interacted volatility measure is insignificant and the coefficient of

Volt-2*DPosLowt-1* ΔSPt-1 is also insignificant. In Model 3, we drop Volt-2 and

Volt-2*DPosLowt-1* ΔSPt-1 since these variables both lack theoretical justification and are

25

insignificant. Model 3 is used as our base model for a number of subsequent estimations

3.4 Summary

In summary, the behavior of the futures-spot spread in the crude oil market shows

evidence of considerable arbitrage activity that is sometimes limited by significant physical

constraints. We argued that an increase (decrease) in the spread is unlikely to set off

arbitrage if the spread is negative (positive) prior to the increase (decrease) and there is no

evidence of mean reversion in the spread when this is the case. Likewise, when the spread is

positive and storage costs are substantial, minimal arbitrage and mean reversion are expected

when the beginning spread is positive but small. Consistent with this expectation, we find

evidence of only a slight mean reversion when the beginning spread is positive but below

$0.50. In other words, when the past spread pattern makes it unlikely that the no-arbitrage

bounds are crossed, there is little evidence of mean reversion or arbitrage, and weak form

efficiency holds.

However, as hypothesized, we find evidence of strong mean reversion when an

already negative spread declines further. Likewise, in the absence of capacity constraints, we

find evidence of strong mean reversion when the spread increases after it already exceeds

$0.50. These mean reversion tendencies are especially strong when futures-spot spread

volatility is high. However, when capacity utilization rates are relatively high, the mean

reversion tendency is non-existent or much weaker, indicating that due to unavailability or

high cost of storage, arbitrage to reverse the spread is limited.

The spread’s mean reversion tendency could be due to other factors such as

inefficient markets. However, the fact that it is not observed (or is much weaker) when the

spread and the change in the spread are of different signs or when the beginning spread is

positive but small, and is substantial when the spread falls from a negative level or increases

from an already high level seem most consistent with arbitrage. In short, strong mean

reversion is observed when the arbitrage hypothesis implies it should be observed and not

observed when arbitrage is not expected. Moreover, the fact that this is observed in daily

data indicates that storage cannot normally be contracted immediately but takes some time to

arrange.

26

This evidence of physical limits to arbitrage has serious economic efficiency

implications. Cash-and-carry arbitrage tends to allocate assets across time in an efficient

manner. If traders foresee a future crude oil shortage and thus bid up the futures price

relative to the spot price, the resulting arbitrage leads to oil being taken off the market in the

current time of relative plenty and coming back on the market during the foreseen period of

relative scarcity. If storage capacity is limited, this reallocation cannot take place.

4. Minimum Inventories and Reverse Cash-and-Carry Arbitrage

In section 3, we examined the possible effects of storage limits on cash-and-carry

arbitrage, finding that when the market is in contango, the futures-spot spread is already high,

and there is excess storage capacity, further increases in the spread tend to be reversed

consistent with cash-and-carry arbitrage. However, when the futures-spot spread is already

high but there is little or no excess storage capacity, further increases in the spread are not

reversed (or the reverse is much smaller) indicating that cash-and-carry arbitrage is limited

by the lack of storage.

As discussed above, the existing theory of storage has focused more on the

consequences of inventory depletions than storage limits. If inventories are quite low, the

risk of a stockout is high, leading to a convenience yield for physical holdings of the

commodity. In addition, if there are no inventories, reverse cash-and-carry arbitrage in which

the arbitrageur simultaneously sells from inventory in the spot market and buys (or goes

long) in the futures market cannot take place. Accordingly, the arbitrage enforcing a lower

limit on the futures-spot spread cannot occur. This suggests that just as we find evidence of a

lack of available storage capacity inhibiting the ability of cash-and-carry arbitrage to return

the futures-spot spread to below the no-arbitrage upper bound when oil inventories approach

capacity, we might find evidence that an inventory shortage inhibits the ability of reverse

cash-and-carry arbitrage to enforce the no-arbitrage lower spread bound.

Determining the level at which inventories might be so low as to limit reverse cash-

and-carry arbitrage is difficult. Oil is an economically essential commodity and inventories

are never zero. Indeed, over our 2004-2015 period, actual oil storage levels at Cushing never

fall below 30.5% of our capacity proxy. Still, it is possible that inventories could fall below

27

the minimum level required for operational purposes, leaving no inventories for reverse C&C

arbitrage, but it is hard to determine what this minimum level might be.26 Testing for possible

inventory limits on reverse C&C arbitrage is also complicated by the relative scarcity of days

in our sample (10.3% of all days) when the spread declines from an already negative level so

that reverse C&C arbitrage might be profitable.

Despite these limitations, we nonetheless explore the possibility of lower inventory

limits on reverse C&C arbitrage. Analogous to our definition of DCap_Utilt, we first define

DLow_Inv_10t =1 when the ratio of actual inventories to our capacity proxy is in the lower

10% of observed capacity utilization ratios.27 This translates to capacity utilization rates

below 52%. Since this inventory cutoff level is high relative to the minimum observed of

30.5%, we also define DLow_Inv_5t =1, and DLow_Inv_3t =1 when the ratio of actual

inventories to our capacity proxy is in the lower 5% and 3% of observed capacity utilization

ratios, i.e., below 40% and 35%, respectively.

In the previous section, we made a distinction between cases when the spread at time

t-2 was positive but less than $0.50 and cases when it was more than $0.50, since cash-and-

carry arbitrage should be more profitable when the spread is larger (as our evidence

confirmed). Likewise, we would expect reverse cash-and-carry arbitrage to be more

profitable when the spread is negative and large in absolute terms than when negative but

small. However, we do not split these observations into spreads above and below -$0.50 due

to several reasons. First, the number of backwardation observations (DNegt-1) is quite low in

our sample. 28 Second, while +$0.50 is an often-quoted storage cost, there is no such guide as

to where to draw the lower bound and it might not even be negative. Also, while $0.50 is

quite important in the case of C&C arbitrage as storage will need to be secured, in the case of

reverse C&C there are may be many instances where the $0.50 storage cost is sunk.

26 While we refer to a minimum operational level for ease of exposition, it should be made clear that this is

likely a continuum since the risk of a stock-out increases as the level of operational inventories is lowered. Thus

it is more accurate to say that as inventories decline, obtaining oil for reverse cash and carry arbitrage becomes

more difficult. 27While we use the upper 20% of observed levels of capacity utilization to define the upper bound, it is

equivalent to storage being 92% full, which is a likely physical capacity constraint. However, the smallest 20%

of observations happen when storage is over 63% full, which is hardly a shortage. We therefore consider the

bottom 10% of observations when defining the lower bound. 28 Unfortunately, as noted above, cases when the spread is negative make up only 23.5% of our sample so the