Arbeitspapiere der FOM · Arbeitspapiere der FOM, Nr. 57: Residential trade and industry PREFACE...

152

Arbeitspapiere der FOM Nr. 57 Residential trade and industry European market analysis, future trends and influencing factors ~ Roberto Cervelló-Royo / Francisco Guijarro Martínez / Thomas Pfahler / Marion Preuss

Transcript of Arbeitspapiere der FOM · Arbeitspapiere der FOM, Nr. 57: Residential trade and industry PREFACE...

Arb

eits

papi

ere

der

FOM

Nr. 57

Residential trade and industry

European market analysis, future trends and influencing factors

~Roberto Cervelló-Royo / Francisco Guijarro Martínez /

Thomas Pfahler / Marion Preuss

Roberto Cervelló-Royo / Francisco Guijarro Martínez /

Thomas Pfahler / Marion Preuss

Residential trade and industry European market analysis, future trends and influencing factors

Arbeitspapiere der FOM, Nr. 57 Essen 2015

ISSN 1865-5610

© 2015 by

MA Akademie Verlags- und Druck-Gesellschaft mbH Leimkugelstraße 6, 45141 Essen Tel. 0201 81004-351 Fax 0201 81004-610

Das Werk einschließlich seiner Teile ist urheberrechtlich geschützt. Jede Verwertung außerhalb der engen Grenzen des Urhebergeset-zes ist ohne Zustimmung der MA Akademie Verlags- und Druck-Gesellschaft mbH unzulässig und strafbar. Das gilt insbesondere für Vervielfältigungen, Übersetzungen, Mikroverfilmungen und die Ein- speicherung und Verarbeitung in elektronischen Systemen.

Die Wiedergabe von Gebrauchs-namen, Handelsnamen, Warenbe-zeichnungen usw. in diesem Werk berechtigt auch ohne besondere Kennzeichnung nicht zu der Annah-me, dass solche Namen im Sinne der Warenzeichen- und Marken-schutz-Gesetzgebung als frei zu betrachten wären und daher von jedermann benutzt werden dürfen. Oft handelt es sich um gesetzlich geschützte eingetragene Waren- zeichen, auch wenn sie nicht als solche gekennzeichnet sind.

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

PREFACE

Residential trade and industry assets are a basic need of individuals with the

result of assessing housing as a right in several nations all over the world. Though

there is a strong focus on the relationship between populations and housing

demands, there is no direct interaction between them for two reasons: it is mainly

households and not individuals that require real estate and, secondly, the needs

of households change over time.

Therefore, various correlations can be identified in order to clarify the movements

detected in housing asset stock on a foundation of household characteristics as

well as population and society performance structures. The analysis of housing

stock in terms of demographic development is important for gaining an in-depth

understanding of housing tendencies, general characteristics and underlying

economic factors.1

In the present volume of the FOM Arbeitspapiere the authors2 establish a market

and trend analysis of the European member countries on the basis of specified

criteria. Thus they identify numerous streams as well as analogical tendencies.

1 Cp. Leal, J. (2007), p. 22 ff. 2 Corresponding author: Marion Preuss

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

II

The identified results could be on the one hand useful for the corresponding

decision-makers to minimise risks, uncertainties and tilts in the medium-term. On

the other hand the latter could support the long-term development of real estate

markets in order to manage public and private investments in this sector with the

target of stabilising and advancing future real estate assets.

Hamburg, August 2015

Dr. Sabine Quirrenbach

Geschäftsleitung FOM Hochschulzentrum Hamburg

University of Applied Sciences

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

III

INDEX

LIST OF ABBREVIATIONS ................................................................................ IV

LIST OF FIGURES .............................................................................................. V

1 Introduction.................................................................................................... 1

2 Market analysis of the residential trade and industry in the European Union ............................................................................................................. 3

2.1 The progress in the European Union 27 ............................................. 3

2.2 Demographic progress ........................................................................ 8

2.3 Space progress ................................................................................. 46

2.4 Environmental social progress .......................................................... 57

3 Trends of the different European Union countries ...................................... 81

4 Conclusion and outlook ............................................................................... 95

LIST OF LITERATURE ....................................................................................... 97

APPENDIX........................................................................................................ 101

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

IV

LIST OF ABBREVIATIONS

A.D. Anno Domini

B.C. Before Christ

EEC European Economic Community

FOM Hochschule für Oekonomie &

Management

USA United States of America

USD United States Dollar

USSR Union of Soviet Socialist Republics

UVP Universidad Politécnica de Valencia

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

V

LIST OF FIGURES

Figure 1: Development of the population in Bulgaria .......................................... 8

Figure 2: Formation of the ageing indicators in Bulgaria ................................... 10

Figure 3: Trend of the number of households in Bulgaria ................................. 11

Figure 4: Development of the population in Estonia ......................................... 12

Figure 5: Formation of the ageing indicators in Estonia .................................... 13

Figure 6: Trend of the number of households in Estonia .................................. 15

Figure 7: Development of the population in Germany ....................................... 16

Figure 8: Formation of the ageing indicators in Germany ................................. 17

Figure 9: Trend of the number of households in Germany ............................... 19

Figure 10: Development of the population in Hungary ...................................... 20

Figure 11: Formation of the ageing indicators in Hungary ................................ 21

Figure 12: Trend of the number of households in Hungary ............................... 23

Figure 13: Development of the population in Latvia .......................................... 24

Figure 14: Formation of the ageing indicators in Latvia .................................... 25

Figure 15: Trend of the number of households in Latvia ................................... 26

Figure 16: Development of the population in Lithuania ..................................... 27

Figure 17: Formation of the ageing indicators in Lithuania ............................... 29

Figure 18: Average number of people per household in Lithuania ................... 30

Figure 19: Development of the population in Poland ........................................ 31

Figure 20: Formation of the ageing indicators in Poland ................................... 33

Figure 21: Clusters of households in Poland..................................................... 34

Figure 22: Development of the population in Romania ..................................... 35

Figure 23: Formation of the ageing indicators in Romania ............................... 37

Figure 24: Trend of the number of households in Romania .............................. 38

Figure 25: Development of the population in Slovakia ...................................... 39

Figure 26: Formation of the ageing indicators in Slovakia ................................ 40

Figure 27: Trend of the number of households in Slovakia ............................... 42

Figure 28: Development of the population in Spain .......................................... 43

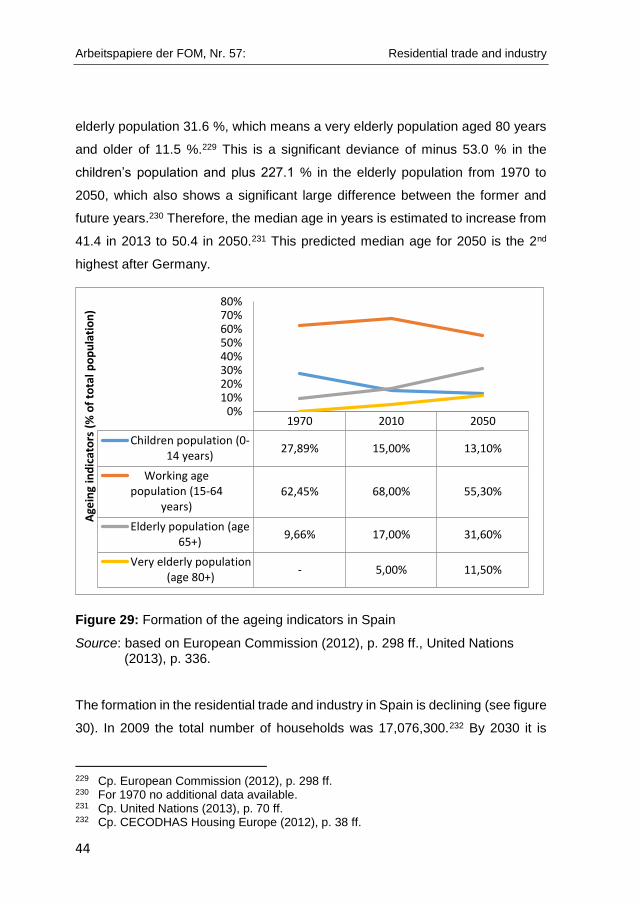

Figure 29: Formation of the ageing indicators in Spain ..................................... 44

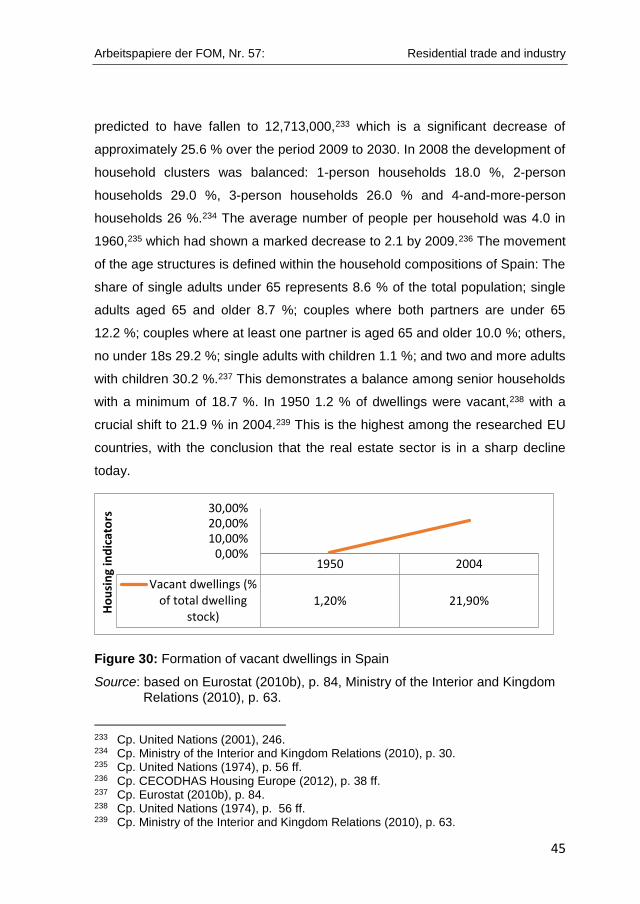

Figure 30: Formation of vacant dwellings in Spain ........................................... 45

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

VI

Figure 31: Build quality inside the housing in Bulgaria ...................................... 46

Figure 32: Trend of the age distribution of housing stock in Estonia ................ 47

Figure 33: Trend of the age distribution of housing stock in Germany .............. 48

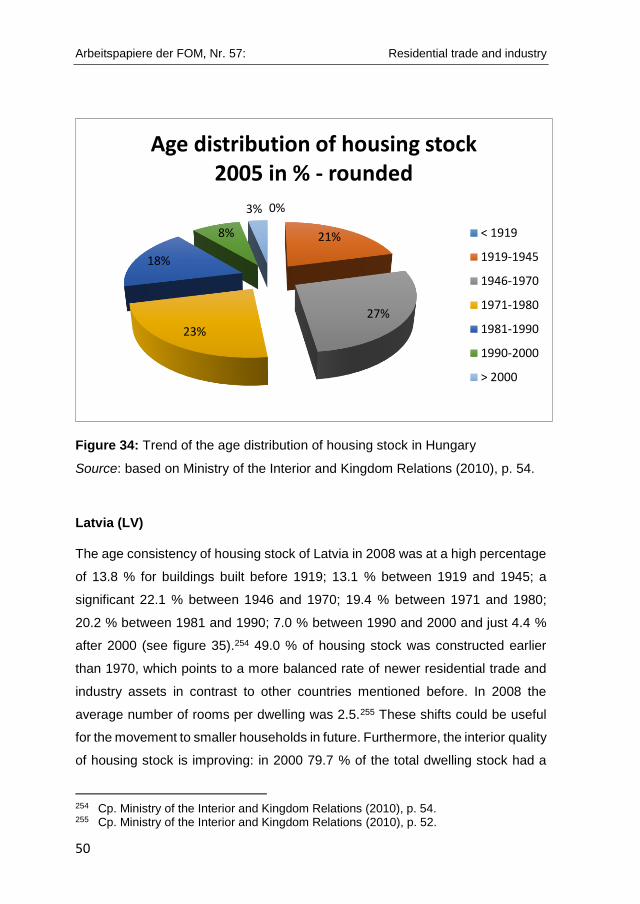

Figure 34: Trend of the age distribution of housing stock in Hungary ............... 50

Figure 35: Trend of the age distribution of housing stock in Latvia ................... 51

Figure 36: Trend of the age distribution of housing stock in Lithuania .............. 52

Figure 37: Trend of the age distribution of housing stock in Poland ................. 53

Figure 38: Trend of the age distribution of housing stock in Romania .............. 54

Figure 39: Trend of the age distribution of housing stock in Slovakia ............... 55

Figure 40: Trend of the age distribution of housing stock in Spain ................... 56

Figure 41: The movement of the income level in Bulgaria ................................ 58

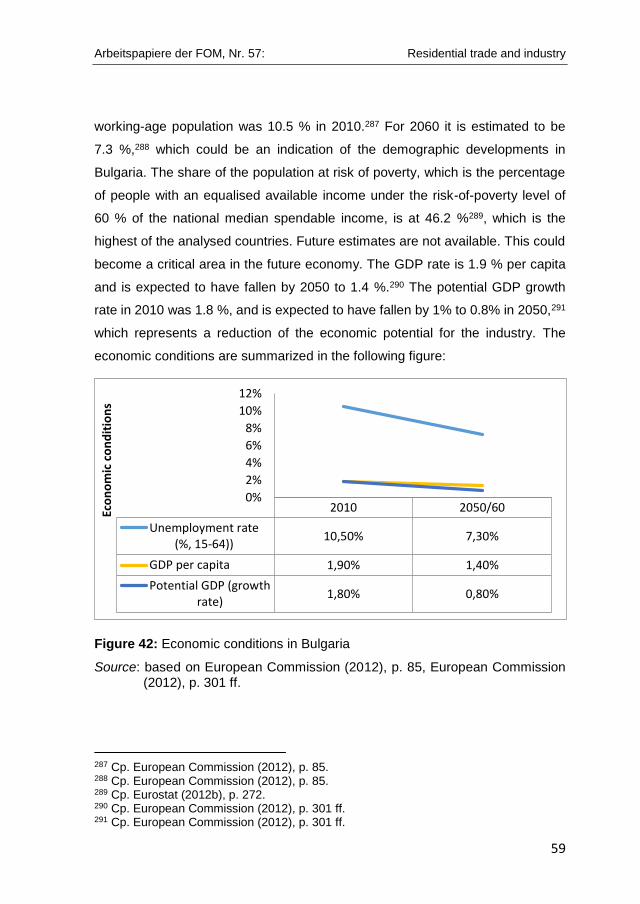

Figure 42: Economic conditions in Bulgaria ...................................................... 59

Figure 43: Economic conditions in Estonia........................................................ 61

Figure 44: Economic conditions in Germany ..................................................... 64

Figure 45: Economic conditions in Hungary ...................................................... 66

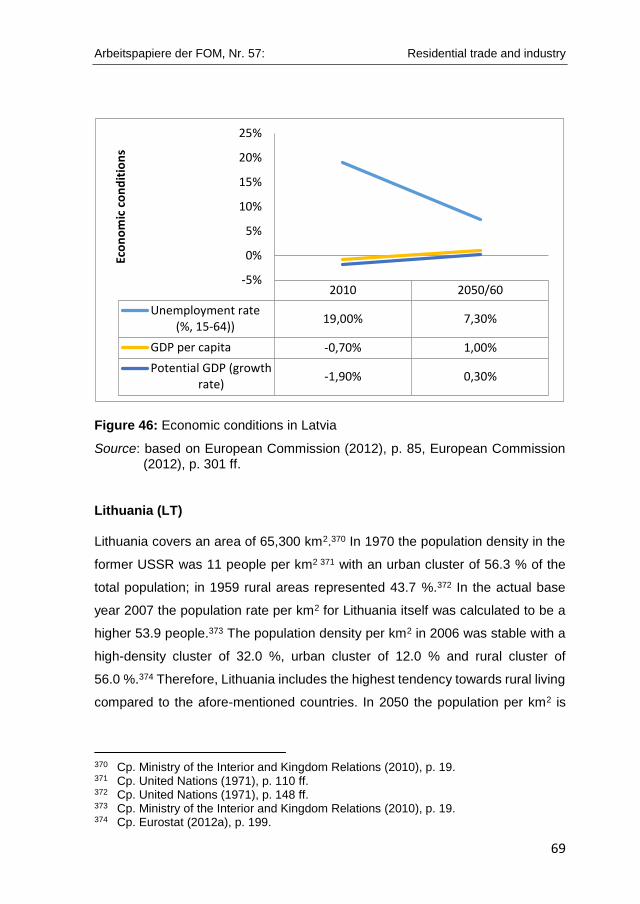

Figure 46: Economic conditions in Latvia .......................................................... 69

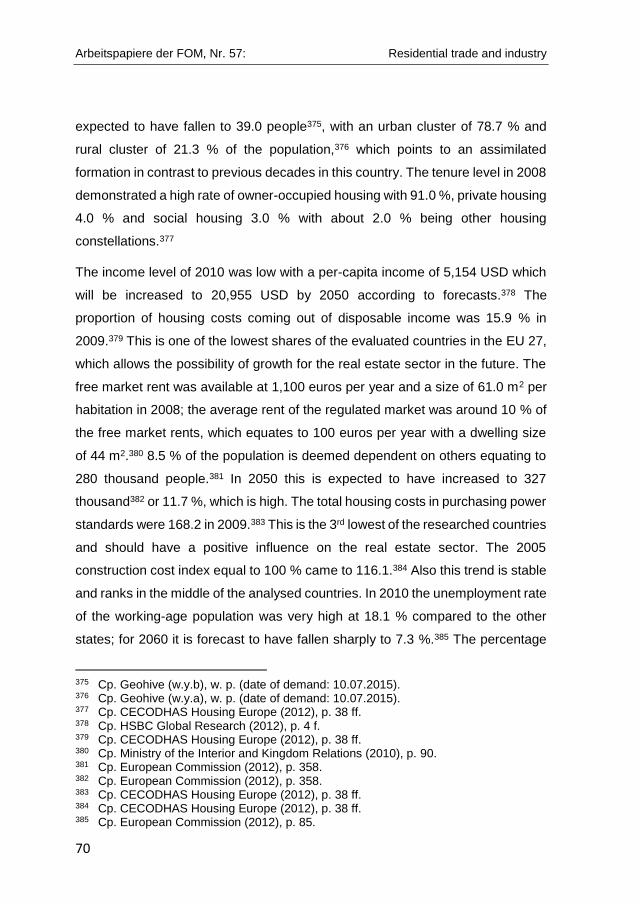

Figure 47: Economic conditions in Lithuania ..................................................... 71

Figure 48: Economic conditions in Poland ........................................................ 73

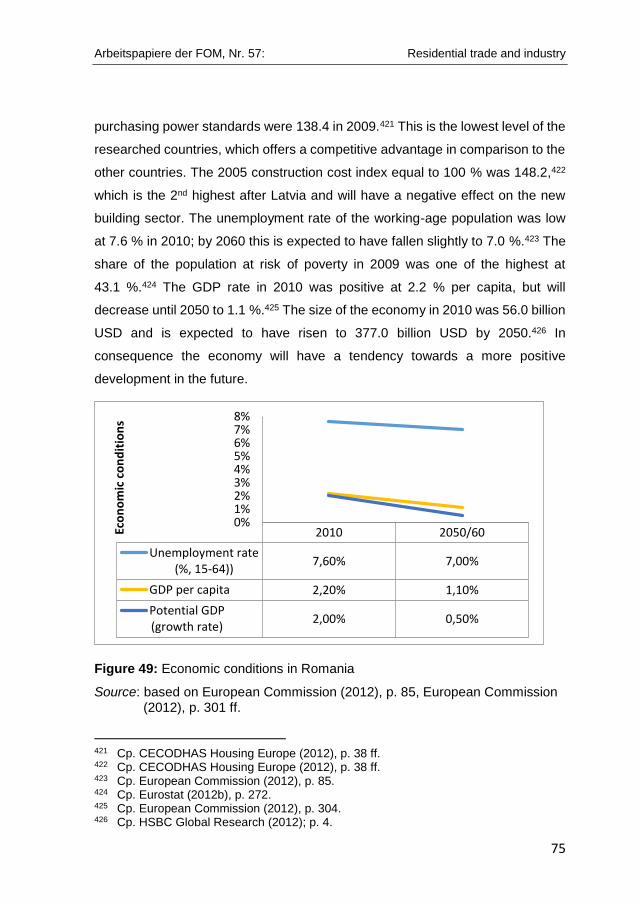

Figure 49: Economic conditions in Romania ..................................................... 75

Figure 50: Economic conditions in Slovakia ...................................................... 78

Figure 51: Economic conditions in Spain .......................................................... 80

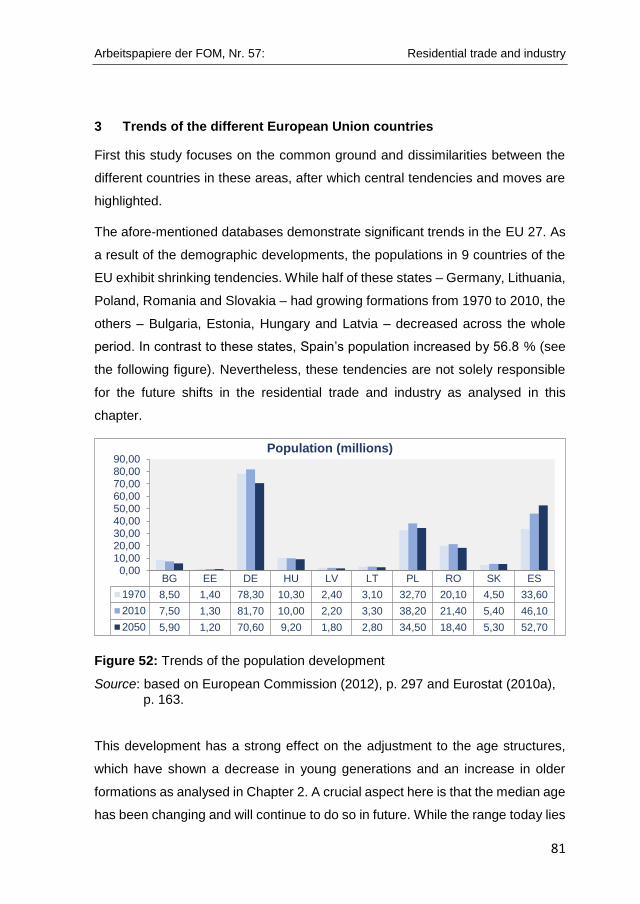

Figure 52: Trends of the population development ............................................. 81

Figure 53: Tendencies of the median age of the populations ........................... 82

Figure 54: Development of the formation of the number of household ............. 83

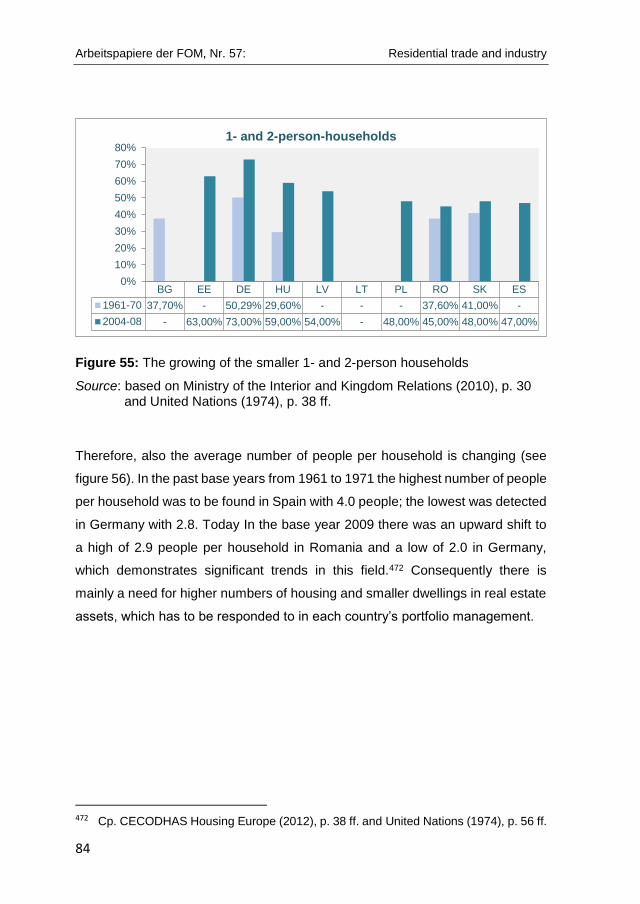

Figure 55: The growing of the smaller 1- and 2-person households ................. 84

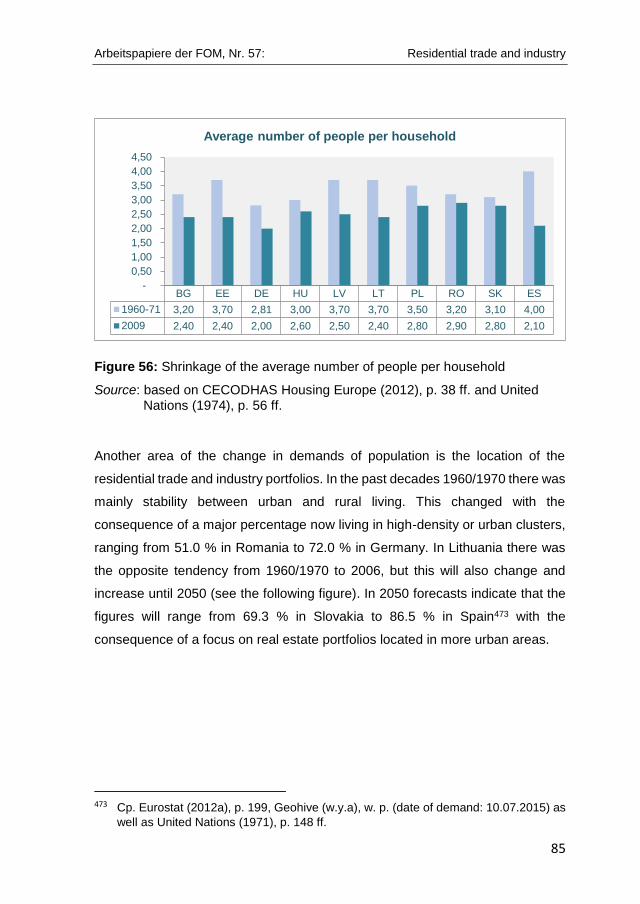

Figure 56: Shrinkage of the average number of people per household ............ 85

Figure 57: Movement to high-density and urban clusters ................................. 86

Figure 58: Formation of owner-occupied tenure status ..................................... 87

Figure 59: Exposure of total housing costs in purchasing power standards ..... 88

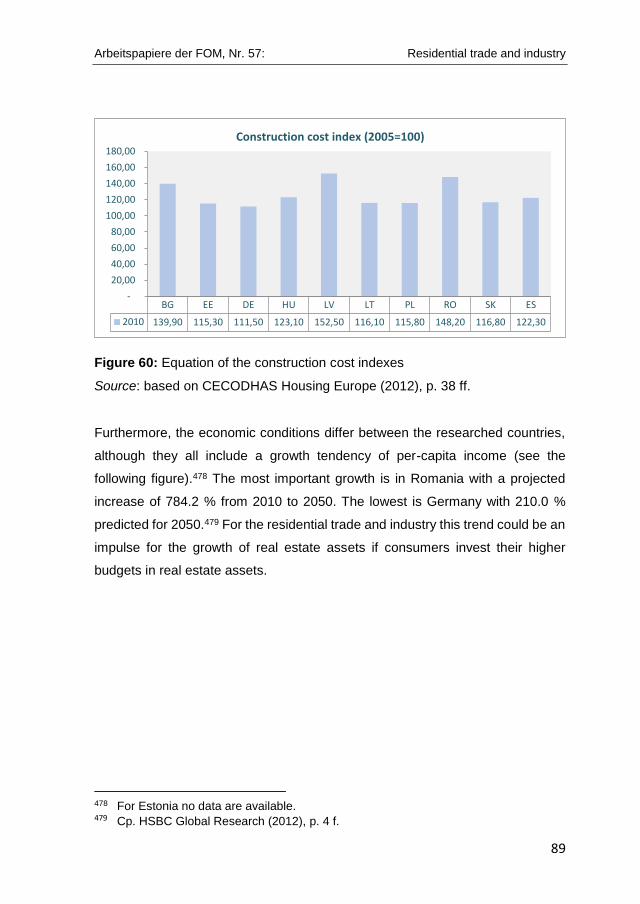

Figure 60: Equation of the construction cost indexes ........................................ 89

Figure 61: Trend of the income per capita ......................................................... 90

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

VII

Figure 62: Tendency of the GDP per capita ...................................................... 90

Figure 63: Formation of the population at risk of poverty .................................. 91

Figure 64: The tendencies of vacant conventional dwellings ............................ 92

Figure 65: Trends of the age distribution of housing stock ............................... 93

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

1

1 Introduction

Major demographic developments in recent decades have caused economies to

fluctuate, effecting supply and demand in the residential trade and industry. The

industry has had to react in order to stabilise, expand and avert shrinkage of its

assets. Rational decision-making is a must when dealing with this situation. There

is a high necessity for sense making of managerial decisions and strategies to

protect asset values. To successfully manage the situation, it is necessary to

focus on various fields such as demographic, space and environmental social

areas in order to gain an overview of the diverse movements and developments

in the different countries of the EU (European Union).

The aim of this paper is to realise a market analysis and identify the different

variables in order to differentiate between several streams and analogical

tendencies. In the focus of the present market analyses are the 27 countries of

the EU3 with decreasing populations, especially Bulgaria, Estonia, Germany,

Hungary, Latvia, Lithuania, Poland, Romania and Slovakia. Furthermore, there

will be a comparison with Spain whose population is expected to increase.

In Chapter 2, this paper begins with a brief description of the EU and following

the 10 in this study analysed countries, listing major historic developments and

also substantial data pertaining to them in order to gain an impression of the

protagonists at play. Then various variables relating to demographics, space and

environmental social progress are mentioned and analysed to identify the areas

of concern for the residential trade and industry.

To focus on the common ground and dissimilarities of the different countries in

these areas, important trends and shifts are highlighted in Chapter 3 to carving

out possible decision-making strategies. In Chapter 4, the paper ends with a

summary.

3 Although Croatia has been the 28th member state of the EU since July 2013, it is not

part of this analysis as a result of missing data.

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

3

2 Market analysis of the residential trade and industry in the European Union

A market analysis is essential for detecting different movements in the residential

trade and industry of Europe. Therefore, this chapter begins with a short

explanation of the afore-mentioned ten EU countries including their basic historic

progresses. Then several data of demographics, space and environmental social

developments are declared and analysed in order to detect the significant fields

of interest for the real estate segment. Consequently various base years of

databases from, e.g., The European Commission, The EU, Eurostat (European

Statistical Office), The United Nations and many more are explained in this

chapter with base years from around 1950 until 2050.4 Nevertheless, some data

are not available and therefore not mentioned in the analyses of this market

research.

2.1 The progress in the European Union 27

The EU is an economic and political alliance established in 1992 after ratification

of the Maastricht Treaty by members of the European Community. This alliance

includes 27 member states and expanded the political coverage of the European

Economic Community, mainly in the field of foreign and security affairs. The EU

advocated the establishment of an European bank and the implementation of a

common valuta, named the euro.5

In 2012 the GDP (Gross Domestic Product) of the EU economy amounted to

12,945,402 million euros. With around 7.0 % of the world’s population, the EU

trades about 20.0 % of all global exports and imports. Approximately 67.0 % of

the EU states trade with other EU countries. The EU was the largest importer with

a share of 16.4 % in 2011, followed by the United States with 15.5 % and China

with 11.9 %. The EU was also the most important exporter with 15.4 % of all

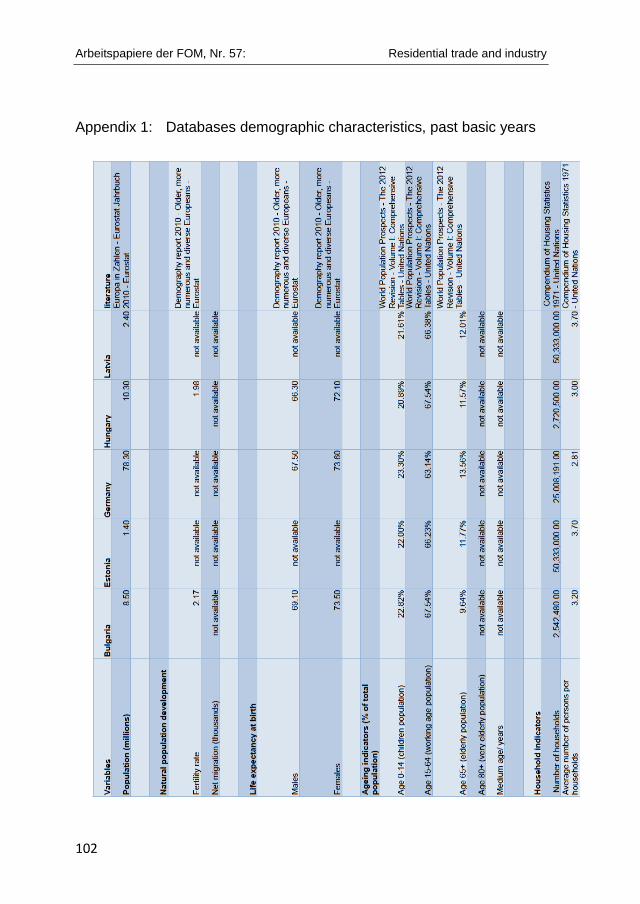

4 Cp. Appendix 1-8 of this analysis, pp. 78-102. 5 Cp. European Union (w.y.a), w. p., (date of demand: 15.07.2015) and European

Union (w.y.b), w. p., (date of demand: 15.07.2015).

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

4

exports, followed by China with 13.4 % and the United States with 10.5 %.6

Therefore, this alliance has strong macro- and micro-economic power with a high

potential for the EU member states.

There now brief descriptions of the analysed EU states will follow covering their

historical and economic developments of the last few decades:

Bulgaria is a country located in the southeast of Europe. It was first populated in

the 6th century A.D. From the 14th century it was occupied by the Ottoman Empire,

referred to sometimes as the Turkish Empire, and became independent in 1908.

After invading Bulgaria in 1944, the Soviet Union founded the People’s Republic

of Bulgaria, after which the country was under a communist government until

1989. The state established a demographic constitution in 1991. Bulgaria’s

capital is Sofia.7 It gained admission to the EU in 2007.8

Estonia is a state located in Northern Central Europe west of Russia. The country

was settled before the 1st century A.D. In the period between the 13th and 18th

centuries Estonia was occupied by the states Denmark, Germany, Sweden and

Russia. It became independent in 1918. In 1940 it was annexed by the USSR. In

1941 it was occupied by Germany, but in 1944 it reverted to being a Soviet state

named the Estonian Soviet Socialist Republic. Complete independence was

established in 1991. The capital of Estonia is Tallinn.9 Its EU entry was in 2004.10

Germany is a state in Northern Central Europe. In 500 B.C. it was annexed by

Germanic tribes. In the 6th century A.D. Germany became part of the Frankish

empire. Afterwards it became a federation of different princedoms and the core

of the Holy Roman Empire. In 1806 this imperial state was finished by Napoleon.

After 1815 Germany became an alliance and from 1871 to 1918 it was an empire

located around Prussia. After defeat in the First World War, it was restructured

6 Cp. European Union (w.y.c), w. p., (date of demand: 20.07.2015). 7 Cp. The American Heritage (2013a), w. p., (date of demand: 17.08.2015). 8 Cp. European Union (2014w.y.b), w. p., (date of demand: 20.07.2015). 9 Cp. The American Heritage (2013b), w. p., (date of demand: 17.08.2015). 10 Cp. European Union (w.y.c), w. p., (date of demand: 20.07.2015).

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

5

as the Weimar Republic, which came to an end when Adolf Hitler formed the

Third Reich. With Germany's defeat in 1945 at the end of the Second World War

the country was divided into four occupation zones controlled by the Allied

powers. In 1949 the zones of the allies USA, France and Britain formed West

Germany, while the Soviet zone became East Germany. These two parts of

Germany were reunified in 1990 after the collapse of the East German

Communist regime. The capital of Germany is Berlin.11 Germany was one of the

founding members of the EU and prior to this it was a member of the European

Economic Community from 1952.12

Hungary is a state in central Europe. Before the late 9th century Hungary was

under the authority of the Roman, Hunnish, Gothic and Slavic federations.

Foreign control ended when the country was captured by Magyars. In 997 St.

Stephen founded the first Hungarian state. After 1526, Hungary was ruled by the

Ottoman Turks. It later fell under Habsburg control, during which time in 1867 it

became part of Austria-Hungary. In 1918 Hungary became independent again. A

communist regime was installed in 1949, which lasted until 1989 when the

country became democratic. Budapest is the capital of Hungary.13 It entered the

EU in 2004.14

Latvia is a state in northern central Europe. In the 1200s the ancestral inhabitants,

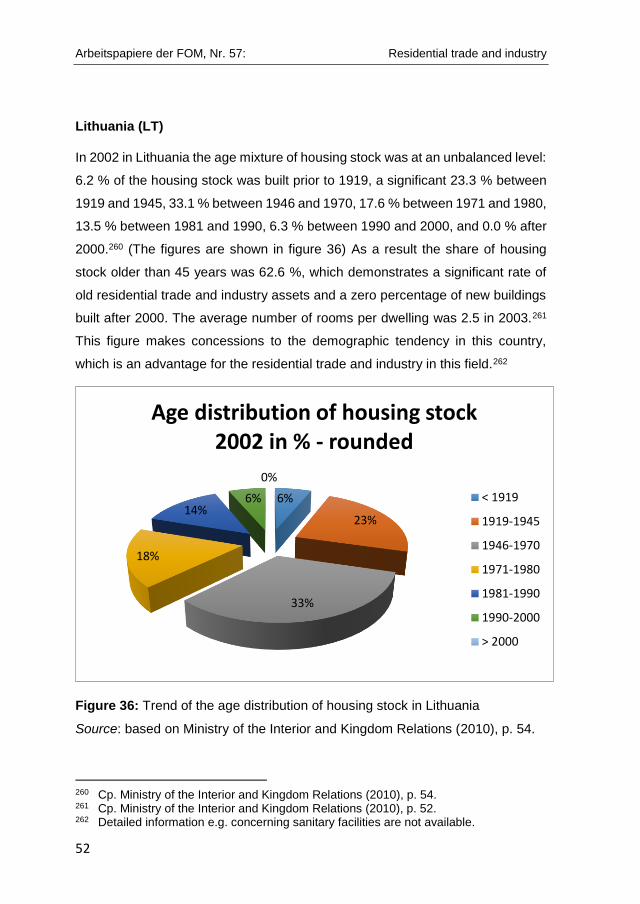

the Letts, were captured and Christianised by German knights, named the

Livonian Brothers of the Sword, who controlled the area until 1561 when Latvia

was passed to Poland. From the 18th century, the country was under Russian

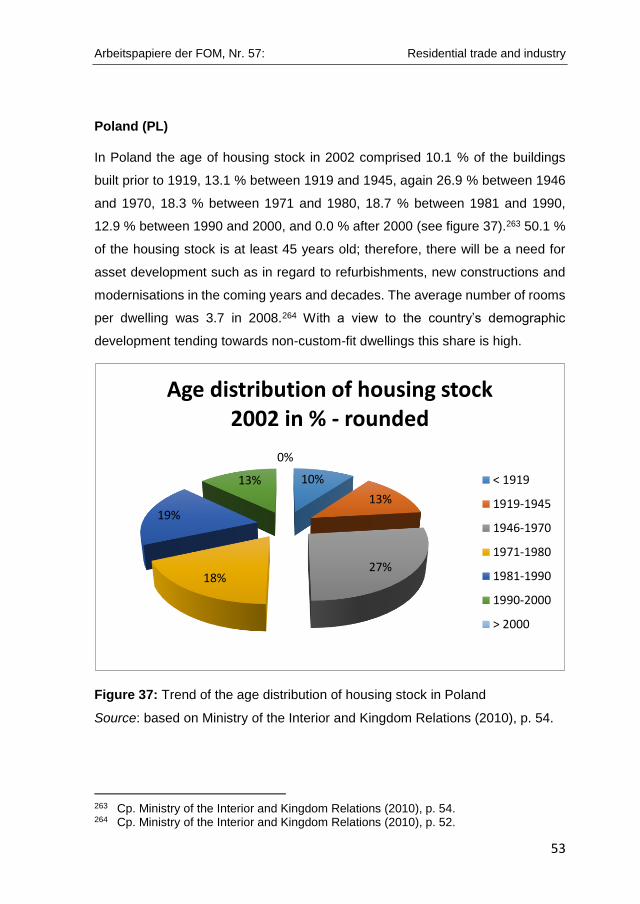

control. After the First World War, Latvia became independent. In 1940 the state

was annexed by the USSR and named the Latvian Soviet Socialist Republic. In

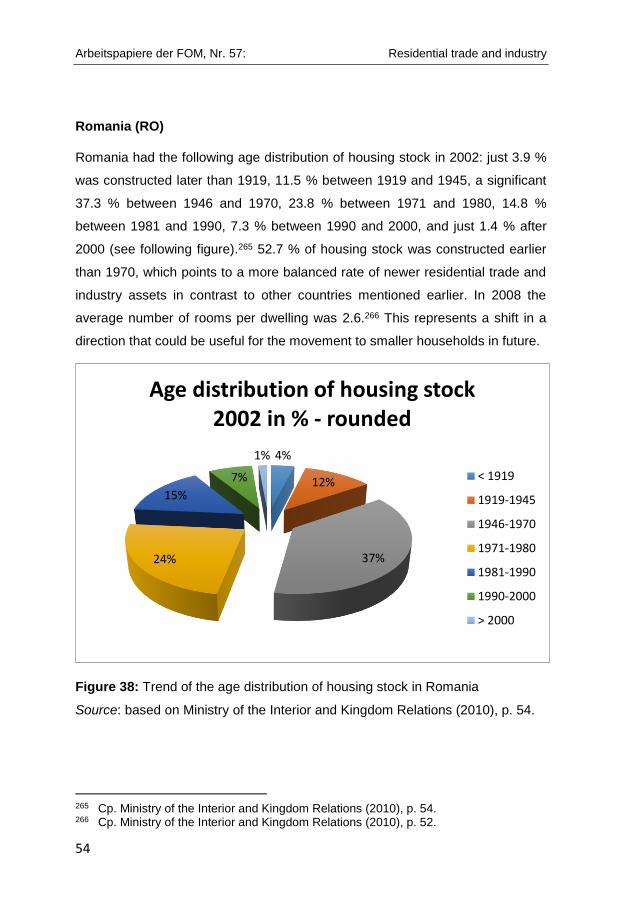

11 Cp. The American Heritage (2013c), w. p., (date of demand: 17.08.2015). 12 Cp. European Union (w.y.c), w. p., (date of demand: 20.07.2015). 13 Cp. The American Heritage (2013d), w. p., (date of demand: 17.08.2015). 14 Cp. European Union (w.y.c), w. p., (date of demand: 20.07.2015).

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

6

1990 Latvia declared its independence. Riga is its capital city.15 It entered the EU

in 2004.16

Lithuania is a state in northern central Europe. In the 1200s its different regions

were first brought together, whereby it became one of the largest countries in

medieval Europe. In 1569 Lithuania merged with Poland, but was annexed into

three Russian parts of Poland in 1772, 1793 and 1795. Lithuania was an

independent country from 1918 to 1940 when it became a constituent regime of

the USSR. From 1941 until 1944 it was occupied by Germany, but after the

Second World War it reverted to Soviet rule as the Lithuanian Soviet Socialist

Republic. In 1991 Lithuania again achieved independence. Vilnius is its capital.17

The country has belonged to the EU since 2004.18

Poland is a state in central Europe. In the 10th century it was unified as a kingdom,

and was established under the Jagiello Dynasty in the period from 1386 until

1572. It was a major power in the 15th and 16th centuries. In 1697 Poland lost its

independence and became fragmented into three parts in 1772, 1793 and 1795.

In 1918 Poland was reconstituted as a republic. Its current borders were fixed at

the end of the Second World War. Warsaw is the capital of Poland.19 Its EU entry

was in 2004.20

Romania is a country in southeast Europe. From the 3rd to the 12th century, the

state was annexed by a succession of invaders including the Goths, Huns,

Magyars and Mongols. In the 13th century the princedoms Moldavia and

Wallachia emerged within the Ottoman Empire and the Russian protectorates. In

1862 the princedoms were united then became an independent state in 1878. As

a result of a growing fascist system in the 1930s the monarchy regime changed

to a dictatorship in 1940. During the Second World War, Romania surrendered to

15 Cp. The American Heritage (2013e), w. p., (date of demand: 17.08.2015). 16 Cp. European Union (w.y.c), w. p., (date of demand: 20.07.2015). 17 Cp. The American Heritage (2013f), w. p., (date of demand: 17.08.2015). 18 Cp. European Union (w.y.c), w. p., (date of demand: 20.07.2015). 19 Cp. The American Heritage (2013g), w. p., (date of demand: 17.08.2015). 20 Cp. European Union (w.y.c), w. p., (date of demand: 20.07.2015).

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

7

the USSR and the state was declared a communist regime in 1947. In 1989 the

regime was overthrown with military-backed revolts. The capital of Romania is

Bucharest.21 Its entry to the EU was in 2007.22

Slovakia is a landlocked state in central Europe. In the 6th century A.D. it was

settled by Slavic peoples. In the early 10th century the area was conquered by the

Magyars. It later became part of the Hungarian regime, which lasted until 1918.

Afterwards it became part of the state of Czechoslovakia. In 1945, Slovakia was

annexed by the Soviets as a result of the Second World War and was again made

part of Czechoslovakia, which became a communist regime in 1948. With the end

of the communist regime in 1989, the country was split into two independent

republics. On 1st January 1993, the Republic of Slovakia came into its existence.

Bratislava is the capital.23 Slovakia has been a member of the EU since 2004.24

Spain is a country in southwest Europe. The area was colonised by the

Phoenicians and the Greeks and ruled after 201 B.C. by Carthage and Rome. In

409 A.D. the Barbarians penetrated Spain and were eliminated by the Moors from

North Africa during the period from 711 until 719. The Moors were displaced by

Christian countries and ousted from their last fortress in Granada in 1492.

Ferdinand of Aragon and Isabella of Castile then became lords of Spain. In the

18th and 19th centuries the empire was lost and Spain experienced social and

economic turbulence as a result of the Spanish Civil War from 1936 until 1939

and the reign of Francisco Franco. After the death of Franco, the monarchy was

rebuilt in 1975 under King Juan Carlos, who created a parliamentary democracy.

Madrid is the capital of Spain.25 Prior to the advent of the EU Spain had been a

member of the EEC (European Economic Community) from 1986.26

21 Cp. The American Heritage (2013h), w. p., (date of demand: 17.08.2015). 22 Cp. European Union (w.y.c), w. p., (date of demand: 20.07.2015). 23 Cp. The American Heritage (2013i), w. p., (date of demand: 17.08.2015). 24 Cp. European Union (w.y.c), w. p., (date of demand: 20.07.2015). 25 Cp. The American Heritage (2013j), w. p., (date of demand: 17.08.2015). 26 Cp. European Union (w.y.c), w. p., (date of demand: 20.07.2015).

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

8

2.2 Demographic progress

Bulgaria (BG)

Bulgaria has a population of around 7.5 million,27 which is in decline. In 1970 it

was 8.5 million28 representing an 11.8 % reduction compared to the recorded

figure for 2010. In 2050 the population is predicted to be 5.9 million,29 which will

mean a fall of 21.5 % (see figure 1). This reduction would be much greater without

the increase of the net migration ratio from minus 9.9 thousand in 2010 to plus

3.8 thousand people predicted for 2050,30 which would balance the population

shrinkage in a positive manner. The reason for the population fall is a low fertility

rate, which fell from 2.2 in 197031 to 1.6 in 2010.32 Nevertheless, the fertility rate

is one of the highest for the analysed countries. Forecasts indicate that this rate

will stabilise at this low insufficient level.33

Figure 1: Development of the population in Bulgaria

Source: based on European Commission (2012), p. 297, Eurostat (2010a), p. 163.

27 Cp. European Commission (2012), p. 297. 28 Cp. Eurostat (2010a), p. 163. 29 Cp. European Commission (2012), p. 297. 30 Cp. European Commission (2012), p. 296. 31 Cp. Eurostat (2011), p. 112 ff. 32 Cp. European Commission (2012), p. 294. 33 Cp. European Commission (2012), p. 294.

1970 2010 2050

Population (millions) 8,50 7,50 5,90

0,0

2,0

4,0

6,0

8,0

10,0

Po

pu

lati

on

(m

illio

ns)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

9

The age structures have shown a significant shift in Bulgaria. As mentioned

before, the fertility rate is low with the consequence of a decline of younger

generations. On the other hand, life expectancy is increasing. From a male life

expectancy of 69.1 and female of 73.5 in the base year 1970,34 the figures had

risen to 70.3 and 77.5, respectively, by 2010.35 In 2050 it is predicted that the

figures will be 79.7 and 85.0, respectively.36 This shows a growth trend of around

15.4 % for males and 15.7 % for females from 1970 to 2050. As a result, the

ageing indicators are changing rapidly. In 1970 children aged 0 to 14 represented

22.8 % of the population.37 The working-age population aged 15 to 64

represented 67.5 % and the elderly population aged 65 years and older 9.6%.38

Today with the latest base year 2010 children have shown a shift of nearly minus

40 %, while for the elderly population it is plus 83 %. The working population is

on the whole stable at 68.7 %.39 In 2050 a marginal difference of the children’s

population of 13.5 % in total is expected, a significant shift of minus 19.5 % in the

working population, and one of 177.5 % in the elderly population,40 which

demonstrates the demographic trends in a clear manner (see figure 2). The

median age will rise from 43.0 currently to 48.1 in 2050.41 The current median

age is the second highest after Germany; nevertheless, it will stabilise by 2050 to

a mid-table position among the researched states.

34 Cp. Eurostat (2011), p. 112 ff. 35 Cp. European Commission (2012), p. 294 f. 36 Cp. European Commission (2012), p. 294 f. 37 Cp. United Nations (2013), p. 336. 38 Cp. United Nations (2013), p. 336. 39 Cp. European Commission (2012), p. 298 ff. 40 Cp. European Commission (2012), p. 298 ff. 41 Cp. United Nations (2013), p. 70 ff.

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

10

Figure 2: Formation of the ageing indicators in Bulgaria

Source: based on European Commission (2012), p. 298 ff., United Nations (2013), p. 336.

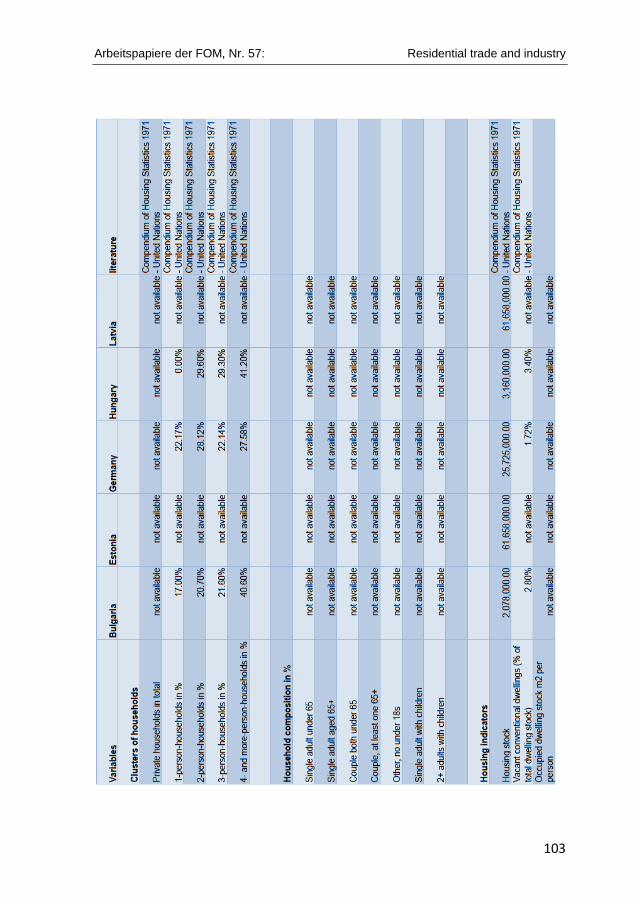

The trend in the residential trade and industry has been the opposite. The number

of households in 1965 was 2,542,48042 compared to 2,900,80043 in 2009; by 2030

it is predicted to be 3,236,000 after a period of continuous growth (see figure 3).44

This tendency demonstrates an increase of 27.3 % compared to 1965. The

reason is the development of the household clusters: In 1965 the approximate

share of 1-person households was 17.0 %, 2-person households 20.7 %, 3-

42 Cp. United Nations (1974), p. 38 ff. 43 Cp. CECODHAS (2012), p. 38 ff. 44 Cp. United Nations (2001), p. 246.

1970 2010 2050

Children population (0-14 years)

22,82% 13,70% 13,50%

Working agepopulation (15-64

years)67,54% 68,70% 55,30%

Elderly population (age65+)

9,64% 17,60% 31,20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Age

ing

ind

icat

ors

(%

of

tota

l po

pu

lati

on

)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

11

person households 21.6 % and 4-and-more-person households 40.6 %45 with an

average number of people per household of 3.2.46 In 2009 the average number

of households was 2.4.47 Although the percentage of clusters of households is

not available for this base year, it represents a change from 3-and-more-person

households to smaller 1- and 2-person households with the result of an increase

of households in total.

Figure 3: Trend of the number of households in Bulgaria

Source: based on CECODHAS Housing Europe (2012), p. 38 ff., United Nations (1974), p. 38 ff., United Nations (2001), p. 246.

Estonia (EE)

In 2010 the population of Estonia was around 1.3 million,48 which is also in

decline; in 1970 it was 1.449. In 2050 population is predicted to be 1.2 million50,

which is also a decrease of around 15 % from 1970 to 2050 (see figure 4). Like

Bulgaria this trend would be more significant without the development of the net

migration from minus 0.5 thousand in 2010 to plus 0.8 thousand people predicted

45 Cp. United Nations (1974), p. 38 ff. 46 Cp. United Nations (1974), p. 56 ff. 47 Cp. CECODHAS (2012), p. 38 ff. 48 Cp. European Commission (2012), p. 297. 49 Cp. Eurostat (2010a), p. 163. 50 Cp. European Commission (2012), p. 297.

1965 2009 2030

Number of households(millions)

2,54 2,90 3,24

- 0,50 1,00 1,50 2,00 2,50 3,00 3,50

Ho

use

ho

ld in

dic

ato

rs

(mill

ion

s)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

12

for 2050.51 Again like Bulgaria, this population fall is a result of a low fertility rate,

which was 1.6 in 2010,52 representing the highest fertility level of the researched

countries together with Bulgaria. By 2050 it is predicted to have risen to 1.7

children per woman,53 which will also be among the highest of the analysed

states.

Figure 4: Development of the population in Estonia

Source: based on European Commission (2012), p. 297, Eurostat (2010a), p. 163.

Furthermore, there is movement in the age indicators in Estonia. The age clusters

for the base year 1970 are not available54; nevertheless, in 2010 the life

expectancies were 69.8 for males and 80.1 for females.55 In 2050 the forecast is

79.6 and 86.6, respectively.56 This trend represents a development of plus 9.8

years for males and plus 6.5 years for females from 2010 to 2050. Consequently

the ageing indicators will change. In 1970 the cluster of the children’s population

aged 0 to 14 represented 22.0 % of the total population.57 The working-age

51 Cp. European Commission (2012), p. 296. 52 Cp. European Commission (2012), p. 294. 53 Cp. European Commission (2012), p. 294. 54 Cp. Eurostat (2011), p. 112 ff. 55 Cp. European Commission (2012), p. 294 f. 56 Cp. European Commission (2012), p. 294 f. 57 Cp. United Nations (2013), p. 336.

1970 2010 2050

Population (millions) 1,40 1,30 1,20

1,10

1,15

1,20

1,25

1,30

1,35

1,40

1,45

Po

pu

lati

on

(m

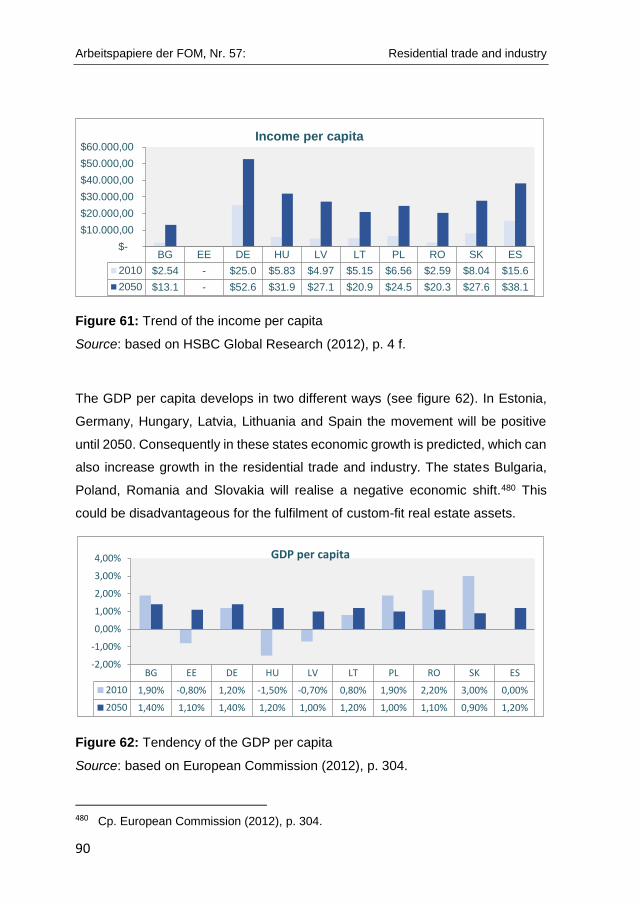

illio

ns)

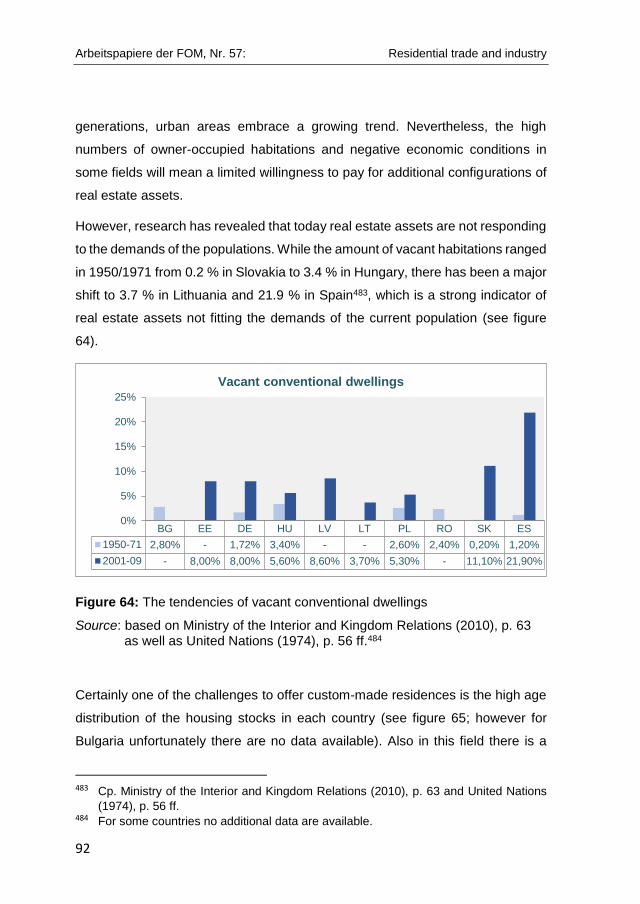

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

13

population aged 15 to 64 represented 66.2 % and the elderly population aged 65

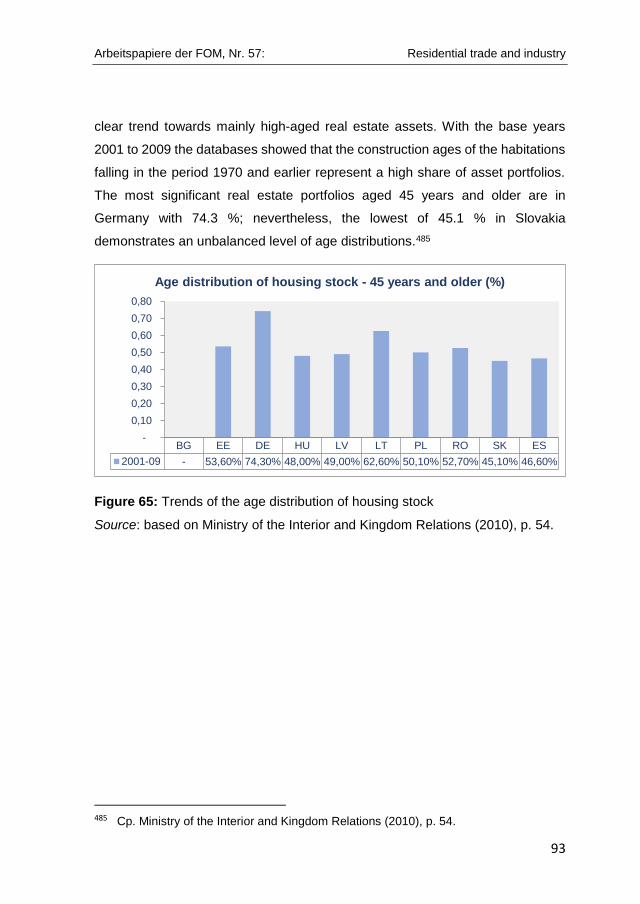

and older nearly 12 %.58

Today the children’s population has fallen to 15.2 % and the elderly population

raised to 17.0 %.59 The working population has increased to 67.7 %.60 In 2050

forecasts indicate that the children’s population will represent 15.0 % of the total,

the working-age population 57.1 % and the elderly population 27.9 % (see figure

5).61 This is a significant shift of minus 31.8 % for children, minus 13.7 % for the

working population and a higher one of plus 132.5 % for the elderly from 1970 to

2050. The result is an increase of the median age in years from 40.9 in 2013 to

44.4 in 2050,62 which falls in the middle of the analysed states today, but will

develop to become one of the youngest median ages in the future.

Figure 5: Formation of the ageing indicators in Estonia

Source: based on European Commission (2012), p. 298 ff., United Nations (2013), p. 336.

58 Cp. United Nations (2013), p. 336. 59 Cp. European Commission (2012), p. 298 ff. 60 Cp. European Commission (2012), p. 298 ff. 61 Cp. European Commission (2012), p. 298 ff. 62 Cp. United Nations (2013), p. 70 ff.

1970 2010 2050

Children population(0-14 years)

22,00% 15,20% 15,00%

Working agepopulation (15-64

years)66,23% 67,70% 57,10%

Elderly population(age 65+)

11,77% 17,00% 27,90%

0%10%20%30%40%50%60%70%80%

Age

ing

ind

icat

ors

(%

of

tota

l p

op

ula

tio

n)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

14

The tendency in the residential trade and industry is the opposite. As a result of

the annexation by the USSR for the base year 1965 there is just the total number

of USSR households available, 50,333,000; the number for Estonia is not

available.63 In 2009 the number for Estonia was 548,500.64 An increasing trend

is forecast until 2030 when the number of households will reach 607,000,65 which

is a development of approximately 10.6 % over a period of 21 years (see figure

6). In 2008 1-person households represented 33.0 % of the total, 2-person

households 30.0 %, 3-person households 20.0 % and 4-and-more-person

households 17.0 %.66 Despite the lack of available base-year data, it can still be

determined that Estonia has experienced an increase in smaller 1- and 2-person

households, because the average number of people per household was 3.7 in

196567 compared to 2.4 in 2009.68 The shift in age structures is clearly visible in

the context of the household compositions: The share of the single adults under

65 is 18.3 %; single adults aged 65 and over 15.4 %; couples both under 65

11.1 %; couples with at least one aged 65 and older 7.8 %; others, no under 18s

19.1 %; single adults with children 4.2 %; and two and more adults with children

24.2 %.69 This demonstrates that senior households represent a minimum of

23.2 % of the total, which is a significant share held by senior households. 8 % of

dwellings were vacant in 2009,70 which is high in comparison to the other

analysed EU states.

63 Cp. United Nations (1974), p. 38 ff. 64 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 65 Cp. United Nations (2001), p. 246. 66 Cp. Ministry of the Interior and Kingdom Relations et al. (2010), p. 30. 67 Cp. United Nations (1974), p. 56 ff. 68 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 69 Cp. Eurostat (2010b), p. 84. 70 Cp. Ministry of the Interior and Kingdom Relations (2010), p. 63.

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

15

Figure 6: Trend of the number of households in Estonia

Source: based on CECODHAS Housing Europe (2012), p. 38 ff., United Nations (2001), p. 246.

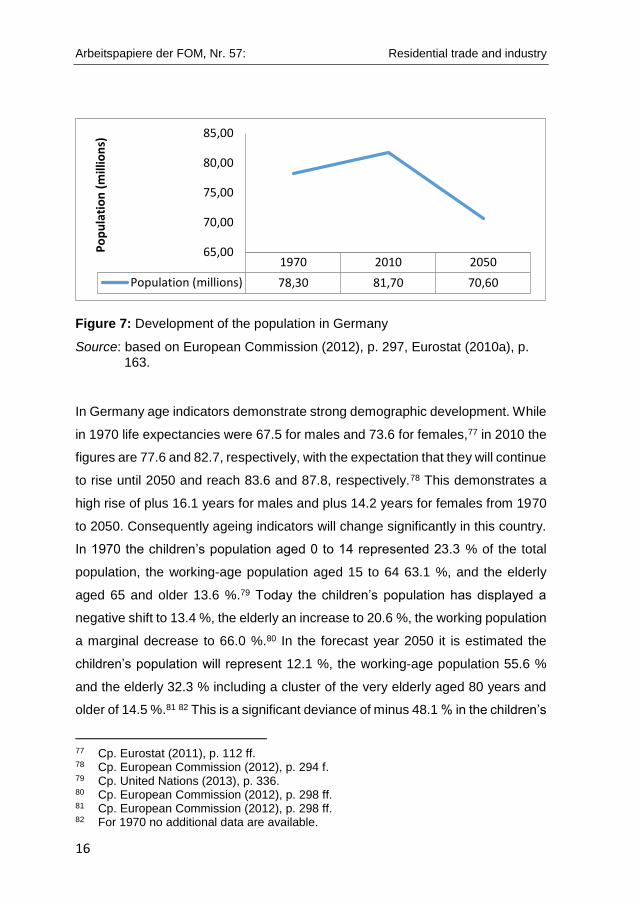

Germany (DE)

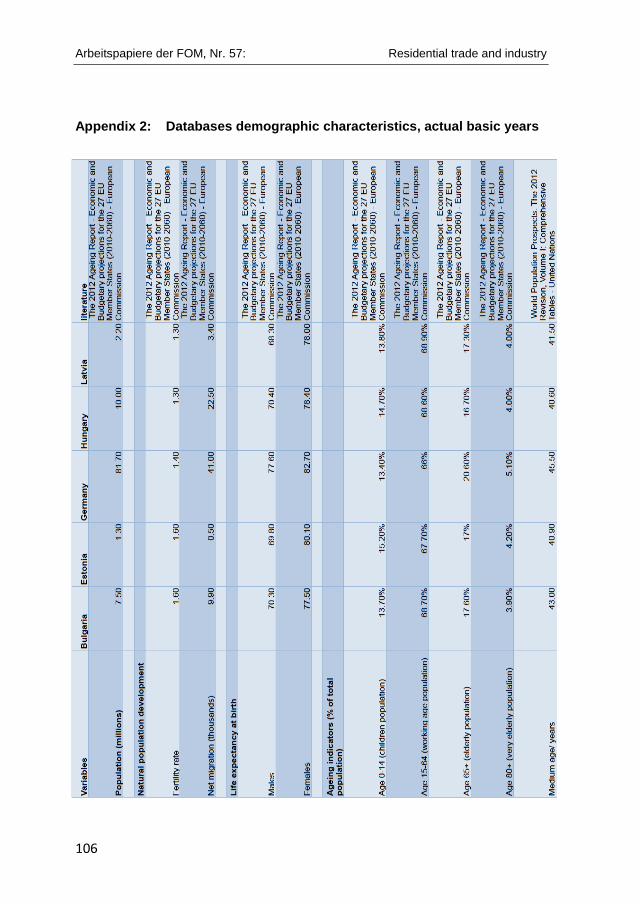

In 2010 Germany’s population was 81.7 million people,71 an increase of 4.3 %

from 78.3 million in 1970.72 Nevertheless, it is predicted that the population will

have fallen to 70.6 million people by 2050,73 which is again a negative trend of

around minus 9.8 % from 1970 to 2050 (see figure 7). Also, in Germany net

migration will prevent a higher decline; from 41.0 thousand migrants coming to

Germany in 2010, the figure is predicted to have risen to 87.7 thousand by 2050.74

Like in the afore-mentioned countries, Germany’s fertility rate was quite low at

1.4 children per woman in 2010.75 This figure is predicted to have risen to 1.5 by

2050,76 which is also low and the average for the EU.

71 Cp. European Commission (2012), p. 297. 72 Cp. Eurostat (2010a), p. 163. 73 Cp. European Commission (2012), p. 297. 74 Cp. European Commission (2012), p. 296. 75 Cp. European Commission (2012), p. 294. 76 Cp. European Commission (2012), p. 294.

2009 2030

Number ofhouseholds (millions)

0,55 0,61

0,50

0,52

0,54

0,56

0,58

0,60

0,62

Ho

use

ho

ld in

dic

ato

rs

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

16

Figure 7: Development of the population in Germany

Source: based on European Commission (2012), p. 297, Eurostat (2010a), p. 163.

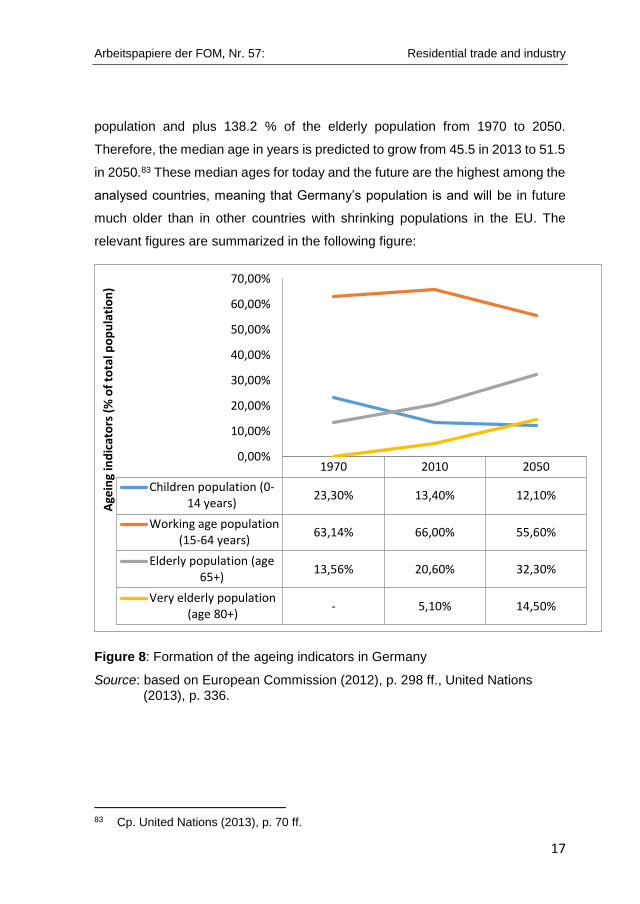

In Germany age indicators demonstrate strong demographic development. While

in 1970 life expectancies were 67.5 for males and 73.6 for females,77 in 2010 the

figures are 77.6 and 82.7, respectively, with the expectation that they will continue

to rise until 2050 and reach 83.6 and 87.8, respectively.78 This demonstrates a

high rise of plus 16.1 years for males and plus 14.2 years for females from 1970

to 2050. Consequently ageing indicators will change significantly in this country.

In 1970 the children’s population aged 0 to 14 represented 23.3 % of the total

population, the working-age population aged 15 to 64 63.1 %, and the elderly

aged 65 and older 13.6 %.79 Today the children’s population has displayed a

negative shift to 13.4 %, the elderly an increase to 20.6 %, the working population

a marginal decrease to 66.0 %.80 In the forecast year 2050 it is estimated the

children’s population will represent 12.1 %, the working-age population 55.6 %

and the elderly 32.3 % including a cluster of the very elderly aged 80 years and

older of 14.5 %.81 82 This is a significant deviance of minus 48.1 % in the children’s

77 Cp. Eurostat (2011), p. 112 ff. 78 Cp. European Commission (2012), p. 294 f. 79 Cp. United Nations (2013), p. 336. 80 Cp. European Commission (2012), p. 298 ff. 81 Cp. European Commission (2012), p. 298 ff. 82 For 1970 no additional data are available.

1970 2010 2050

Population (millions) 78,30 81,70 70,60

65,00

70,00

75,00

80,00

85,00

Po

pu

lati

on

(m

illio

ns)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

17

population and plus 138.2 % of the elderly population from 1970 to 2050.

Therefore, the median age in years is predicted to grow from 45.5 in 2013 to 51.5

in 2050.83 These median ages for today and the future are the highest among the

analysed countries, meaning that Germany’s population is and will be in future

much older than in other countries with shrinking populations in the EU. The

relevant figures are summarized in the following figure:

Figure 8: Formation of the ageing indicators in Germany

Source: based on European Commission (2012), p. 298 ff., United Nations (2013), p. 336.

83 Cp. United Nations (2013), p. 70 ff.

1970 2010 2050

Children population (0-14 years)

23,30% 13,40% 12,10%

Working age population(15-64 years)

63,14% 66,00% 55,60%

Elderly population (age65+)

13,56% 20,60% 32,30%

Very elderly population(age 80+)

- 5,10% 14,50%

0,00%

10,00%

20,00%

30,00%

40,00%

50,00%

60,00%

70,00%

Age

ing

ind

icat

ors

(%

of

tota

l po

pu

lati

on

)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

18

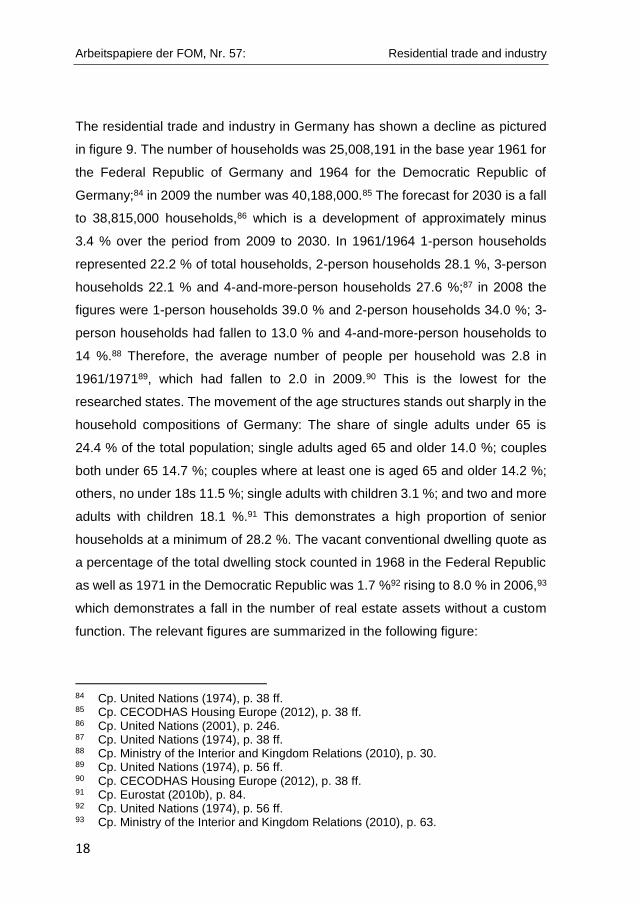

The residential trade and industry in Germany has shown a decline as pictured

in figure 9. The number of households was 25,008,191 in the base year 1961 for

the Federal Republic of Germany and 1964 for the Democratic Republic of

Germany;84 in 2009 the number was 40,188,000.85 The forecast for 2030 is a fall

to 38,815,000 households,86 which is a development of approximately minus

3.4 % over the period from 2009 to 2030. In 1961/1964 1-person households

represented 22.2 % of total households, 2-person households 28.1 %, 3-person

households 22.1 % and 4-and-more-person households 27.6 %;87 in 2008 the

figures were 1-person households 39.0 % and 2-person households 34.0 %; 3-

person households had fallen to 13.0 % and 4-and-more-person households to

14 %.88 Therefore, the average number of people per household was 2.8 in

1961/197189, which had fallen to 2.0 in 2009.90 This is the lowest for the

researched states. The movement of the age structures stands out sharply in the

household compositions of Germany: The share of single adults under 65 is

24.4 % of the total population; single adults aged 65 and older 14.0 %; couples

both under 65 14.7 %; couples where at least one is aged 65 and older 14.2 %;

others, no under 18s 11.5 %; single adults with children 3.1 %; and two and more

adults with children 18.1 %.91 This demonstrates a high proportion of senior

households at a minimum of 28.2 %. The vacant conventional dwelling quote as

a percentage of the total dwelling stock counted in 1968 in the Federal Republic

as well as 1971 in the Democratic Republic was 1.7 %92 rising to 8.0 % in 2006,93

which demonstrates a fall in the number of real estate assets without a custom

function. The relevant figures are summarized in the following figure:

84 Cp. United Nations (1974), p. 38 ff. 85 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 86 Cp. United Nations (2001), p. 246. 87 Cp. United Nations (1974), p. 38 ff. 88 Cp. Ministry of the Interior and Kingdom Relations (2010), p. 30. 89 Cp. United Nations (1974), p. 56 ff. 90 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 91 Cp. Eurostat (2010b), p. 84. 92 Cp. United Nations (1974), p. 56 ff. 93 Cp. Ministry of the Interior and Kingdom Relations (2010), p. 63.

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

19

Figure 9: Trend of the number of households in Germany

Source: based on CECODHAS Housing Europe (2012), p. 38 ff., United Nations (1974), p. 38 ff. as well as United Nations (2001), p. 246.

Hungary (HU)

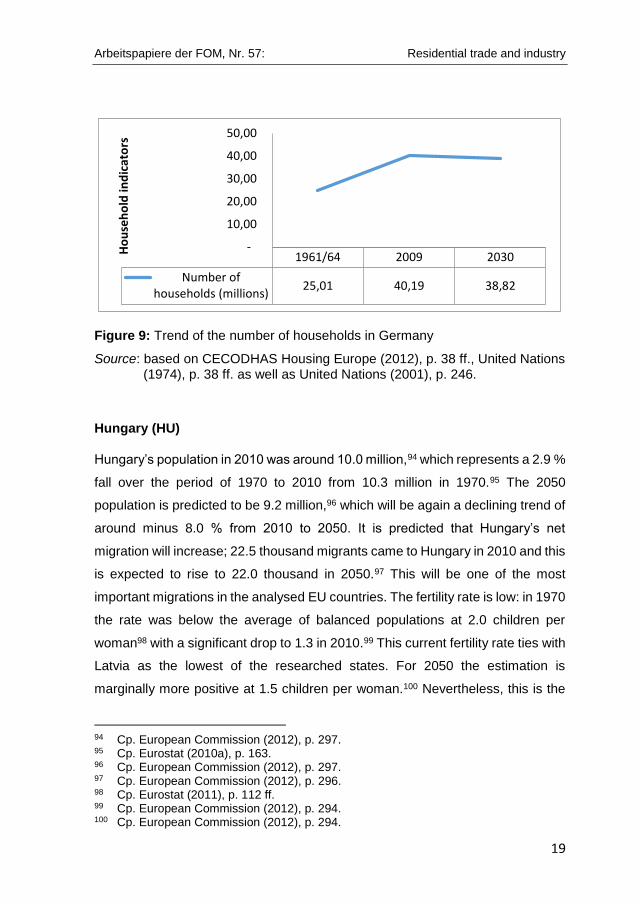

Hungary’s population in 2010 was around 10.0 million,94 which represents a 2.9 %

fall over the period of 1970 to 2010 from 10.3 million in 1970.95 The 2050

population is predicted to be 9.2 million,96 which will be again a declining trend of

around minus 8.0 % from 2010 to 2050. It is predicted that Hungary’s net

migration will increase; 22.5 thousand migrants came to Hungary in 2010 and this

is expected to rise to 22.0 thousand in 2050.97 This will be one of the most

important migrations in the analysed EU countries. The fertility rate is low: in 1970

the rate was below the average of balanced populations at 2.0 children per

woman98 with a significant drop to 1.3 in 2010.99 This current fertility rate ties with

Latvia as the lowest of the researched states. For 2050 the estimation is

marginally more positive at 1.5 children per woman.100 Nevertheless, this is the

94 Cp. European Commission (2012), p. 297. 95 Cp. Eurostat (2010a), p. 163. 96 Cp. European Commission (2012), p. 297. 97 Cp. European Commission (2012), p. 296. 98 Cp. Eurostat (2011), p. 112 ff. 99 Cp. European Commission (2012), p. 294. 100 Cp. European Commission (2012), p. 294.

1961/64 2009 2030

Number ofhouseholds (millions)

25,01 40,19 38,82

-

10,00

20,00

30,00

40,00

50,00H

ou

seh

old

ind

icat

ors

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

20

lowest rate across the decreasing populations of the EU 27. The relevant figures

are summarized in the following figure:

Figure 10: Development of the population in Hungary

Source: based on European Commission (2012), p. 297, Eurostat (2010a), p. 163.

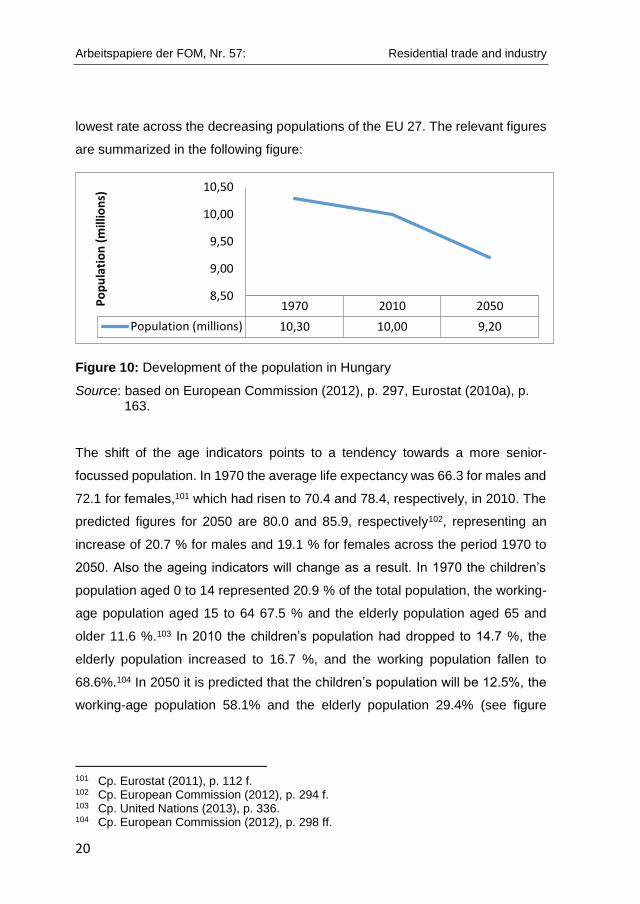

The shift of the age indicators points to a tendency towards a more senior-

focussed population. In 1970 the average life expectancy was 66.3 for males and

72.1 for females,101 which had risen to 70.4 and 78.4, respectively, in 2010. The

predicted figures for 2050 are 80.0 and 85.9, respectively102, representing an

increase of 20.7 % for males and 19.1 % for females across the period 1970 to

2050. Also the ageing indicators will change as a result. In 1970 the children’s

population aged 0 to 14 represented 20.9 % of the total population, the working-

age population aged 15 to 64 67.5 % and the elderly population aged 65 and

older 11.6 %.103 In 2010 the children’s population had dropped to 14.7 %, the

elderly population increased to 16.7 %, and the working population fallen to

68.6%.104 In 2050 it is predicted that the children’s population will be 12.5%, the

working-age population 58.1% and the elderly population 29.4% (see figure

101 Cp. Eurostat (2011), p. 112 f. 102 Cp. European Commission (2012), p. 294 f. 103 Cp. United Nations (2013), p. 336. 104 Cp. European Commission (2012), p. 298 ff.

1970 2010 2050

Population (millions) 10,30 10,00 9,20

8,50

9,00

9,50

10,00

10,50

Po

pu

lati

on

(m

illio

ns)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

21

11).105 This is a deviance of minus 40.5% in the children’s population and plus

145.0 % in the elderly population from 1970 to 2050. The median age in years

will change from the current 40.6 to 46.1 in 2050.106 These ages fall in the mid

range of the analysed countries.

Figure 11: Formation of the ageing indicators in Hungary

Source: based on European Commission (2012), p. 298, cp. United Nations (2013), p. 336.

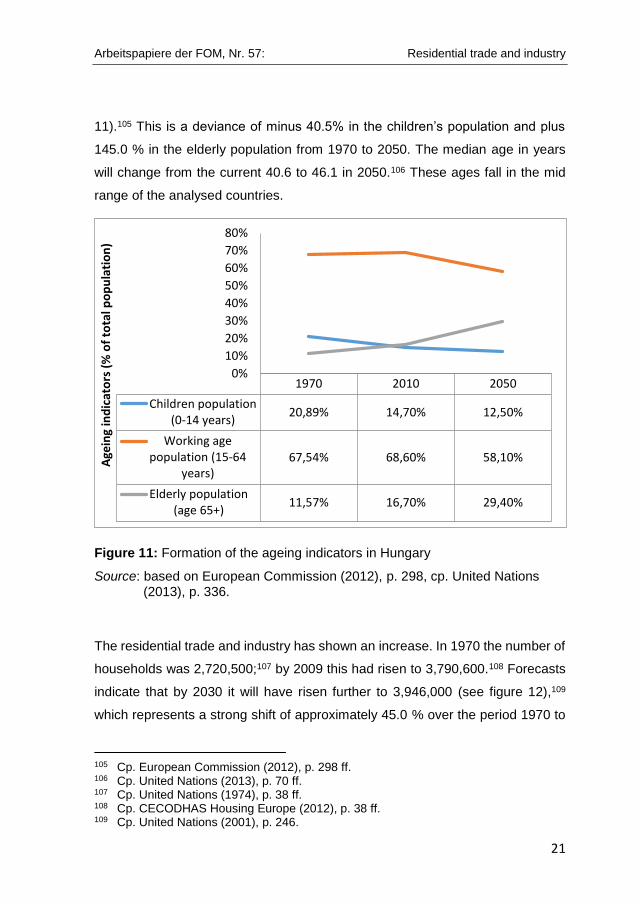

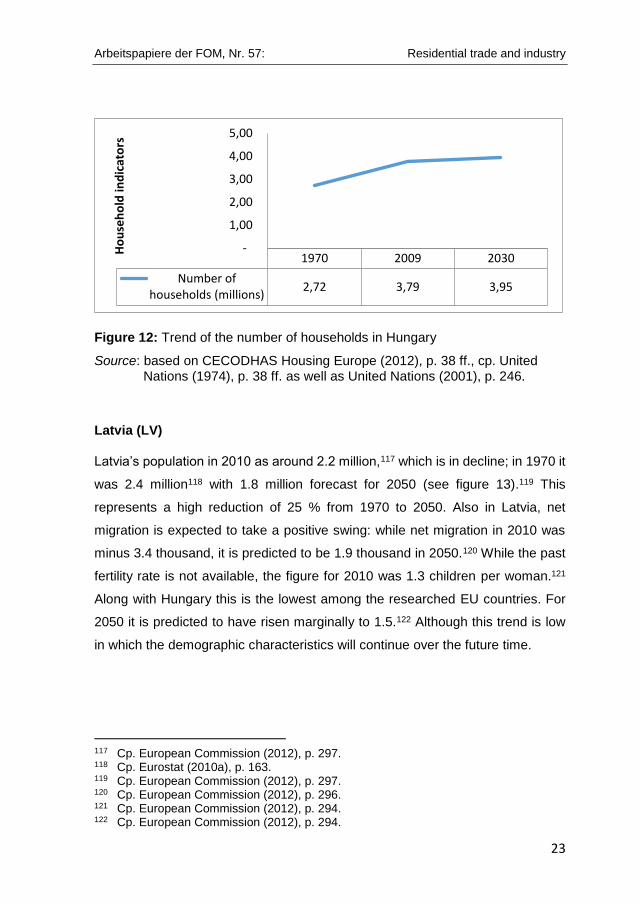

The residential trade and industry has shown an increase. In 1970 the number of

households was 2,720,500;107 by 2009 this had risen to 3,790,600.108 Forecasts

indicate that by 2030 it will have risen further to 3,946,000 (see figure 12),109

which represents a strong shift of approximately 45.0 % over the period 1970 to

105 Cp. European Commission (2012), p. 298 ff. 106 Cp. United Nations (2013), p. 70 ff. 107 Cp. United Nations (1974), p. 38 ff. 108 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 109 Cp. United Nations (2001), p. 246.

1970 2010 2050

Children population(0-14 years)

20,89% 14,70% 12,50%

Working agepopulation (15-64

years)67,54% 68,60% 58,10%

Elderly population(age 65+)

11,57% 16,70% 29,40%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Age

ing

ind

icat

ors

(%

of

tota

l po

pu

lati

on

)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

22

2030. The household clusters have shifted accordingly. In 1970 1-person

households represented 0.0 % of the total, 2-person households 29.6 %, 3-

person households 29.3 % and 4-and-more-person households 41.2 %.110 2004

saw a tendency towards smaller households: 1-person households 29.0 %, 2-

person households 30.0 %, 3-person households 19.0 % and 4-and-more-person

households 23.0 %.111 The average number of people per household of 3.0 in

1970112 had fallen to 2.6 by 2009.113 The movement of the age structures is

apparent from Hungary’s household compositions: In 2007 single adults under

65 represented 11.5 % of the total population; single adults aged 65 and older

12.8 %; couples both under 65 12.8 %; couples where at least one is aged 65

and older 8.6 %; others, no under 18s 22.6 %; single adults with children 3.2 %;

and two and more adults with children 28.6.114 This means senior households

represent a minimum of 21.4 % of the total; nevertheless, this is relatively low in

comparison to the other countries. In 1970 3.4 % of dwellings were vacant,115

which had risen to 5.6 % by 2005.116 This is more balanced and lower than for

the other analysed countries.

110 Cp. United Nations (1974), p. 38 ff. 111 Cp. Ministry of the Interior and Kingdom Relations (2010), p. 30. 112 Cp. United Nations (1974), p. 56 ff. 113 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 114 Cp. Eurostat (2010), p. 84. 115 Cp. United Nations (1974), p. 56 ff. 116 Cp. Ministry of the Interior and Kingdom Relations (2010), p. 63.

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

23

Figure 12: Trend of the number of households in Hungary

Source: based on CECODHAS Housing Europe (2012), p. 38 ff., cp. United Nations (1974), p. 38 ff. as well as United Nations (2001), p. 246.

Latvia (LV)

Latvia’s population in 2010 as around 2.2 million,117 which is in decline; in 1970 it

was 2.4 million118 with 1.8 million forecast for 2050 (see figure 13).119 This

represents a high reduction of 25 % from 1970 to 2050. Also in Latvia, net

migration is expected to take a positive swing: while net migration in 2010 was

minus 3.4 thousand, it is predicted to be 1.9 thousand in 2050.120 While the past

fertility rate is not available, the figure for 2010 was 1.3 children per woman.121

Along with Hungary this is the lowest among the researched EU countries. For

2050 it is predicted to have risen marginally to 1.5.122 Although this trend is low

in which the demographic characteristics will continue over the future time.

117 Cp. European Commission (2012), p. 297. 118 Cp. Eurostat (2010a), p. 163. 119 Cp. European Commission (2012), p. 297. 120 Cp. European Commission (2012), p. 296. 121 Cp. European Commission (2012), p. 294. 122 Cp. European Commission (2012), p. 294.

1970 2009 2030

Number ofhouseholds (millions)

2,72 3,79 3,95

-

1,00

2,00

3,00

4,00

5,00H

ou

seh

old

ind

icat

ors

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

24

Figure 13: Development of the population in Latvia

Source: based on European Commission (2012), p. 297 and Eurostat (2010a), p. 163.

The life expectancies are developing in a mostly analogical manner compared to

the afore-mentioned countries: While the figures for 1970 are not available, in

2010 they were 68.3 for males and 78.0 for females.123 In 2050 they are predicted

to have risen to 78.9 and 85.6, respectively124, representing a significant increase

of 15.5 % for males and 9.7 % for females from the base year 1970 to 2050. In

1970 the children’s population aged 0 to 14 represented 21.6 % of the total

population, the working-age population aged 15 to 64 66.4 % and the elderly

population aged 65 and older 12.0 %.125

Today with an actual base year of 2010 the children’s population has a negative

development with a quotation of 13.8 %, the elderly population increases to a

share of 17.3 %; the working population will marginally increase to 68.9 %.126 In

2050 it is estimated that the children’s population be 12.3 % in total, the working-

age population will be 56.6 % and the elderly 31.2 % (summarized in the following

figure). The figure for the very elderly generation aged a minimum of 80 years will

123 Cp. European Commission (2012), p. 294 f. 124 Cp. European Commission (2012), p. 294 f. 125 Cp. United Nations (2013), p. 336. 126 Cp. European Commission (2012), p. 298 ff.

1970 2010 2050

Population (millions) 2,40 2,20 1,80

0,00

0,50

1,00

1,50

2,00

2,50

3,00

Po

pu

lati

on

(m

illio

ns)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

25

be 10.7 %,127 which is the 3rd highest of the population. This is a crucial difference

of minus 43.1 % in the children’s population and plus 160.0 % in the elderly

population between 1970 and 2050. The median age in years will also increase

from 41.5 per person to 42.7 in 2050.128

Figure 14: Formation of the ageing indicators in Latvia

Source: based on European Commission (2012), p. 298 ff. and United Nations (2013), p. 336.

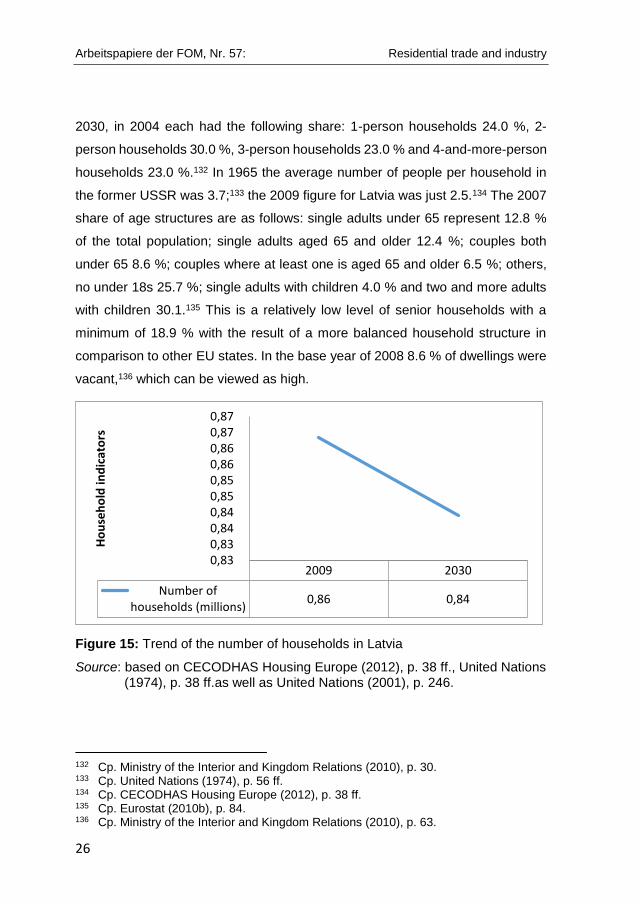

The residential trade and industry of Latvia is on a downward trend in contrast to

most of the afore-mentioned countries (see figure 15). In 1970 the total number

of households was only analysed for the whole of the USSR.129 Nevertheless, in

2009 the figure was 863,400.130 In 2030 it is forecast to have fallen to 839,000,131

which demonstrates a negative trend of minus 2.8 % over the period 2009 to

2030. While the data for clusters of households are not available for 1970 and

127 Cp. European Commission (2012), p. 298 ff. 128 Cp. United Nations (2013), p. 70 ff. 129 Cp. United Nations (1974), p. 38 ff. 130 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 131 Cp. United Nations (2001), 246.

1970 2010 2050

Children population (0-14 years)

21,61% 13,80% 12,30%

Working agepopulation (15-64

years)66,38% 68,90% 56,60%

Elderly population (age65+)

12,01% 17,30% 31,20%

0,00%10,00%20,00%30,00%40,00%50,00%60,00%70,00%80,00%

Age

ing

ind

icat

ors

(%

of

tota

l p

op

ula

tio

n)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

26

2030, in 2004 each had the following share: 1-person households 24.0 %, 2-

person households 30.0 %, 3-person households 23.0 % and 4-and-more-person

households 23.0 %.132 In 1965 the average number of people per household in

the former USSR was 3.7;133 the 2009 figure for Latvia was just 2.5.134 The 2007

share of age structures are as follows: single adults under 65 represent 12.8 %

of the total population; single adults aged 65 and older 12.4 %; couples both

under 65 8.6 %; couples where at least one is aged 65 and older 6.5 %; others,

no under 18s 25.7 %; single adults with children 4.0 % and two and more adults

with children 30.1.135 This is a relatively low level of senior households with a

minimum of 18.9 % with the result of a more balanced household structure in

comparison to other EU states. In the base year of 2008 8.6 % of dwellings were

vacant,136 which can be viewed as high.

Figure 15: Trend of the number of households in Latvia

Source: based on CECODHAS Housing Europe (2012), p. 38 ff., United Nations (1974), p. 38 ff.as well as United Nations (2001), p. 246.

132 Cp. Ministry of the Interior and Kingdom Relations (2010), p. 30. 133 Cp. United Nations (1974), p. 56 ff. 134 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 135 Cp. Eurostat (2010b), p. 84. 136 Cp. Ministry of the Interior and Kingdom Relations (2010), p. 63.

2009 2030

Number ofhouseholds (millions)

0,86 0,84

0,83 0,83 0,84 0,84 0,85 0,85 0,86 0,86 0,87 0,87

Ho

use

ho

ld in

dic

ato

rs

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

27

Lithuania (LT)

Lithuania’s population in the base year 1970 was 3.1 million,137 and had grown to

around 3.3 million by 2010.138 Nevertheless, in 2050 the population is predicted

to have fallen to 2.8 million139 (see figure 16), which represents a shift of minus

9.7% across this whole timeframe from 1970 to 2050. The high net migration in

2010 caused a negative change of minus 13.0 thousand people, but it is predicted

to have risen to plus 2.2 thousand by 2050.140 This positive trend will prevent

greater population shrinkage. Lithuania had a positive fertility rate in 1970 of 2.4

children per woman,141 but this had fallen to a low of 1.5 in 2010.142

Forecasts indicate that it will remain more or less stable until 2050 when it will be

1.6 children, which is also low.143

Figure 16: Development of the population in Lithuania

Source: based on European Commission (2012), p. 297 and Eurostat (2010a), p. 163.

137 Cp. Eurostat (2010a), p. 163. 138 Cp. European Commission (2012), p. 297. 139 Cp. European Commission (2012), p. 297. 140 Cp. European Commission (2012), p. 296. 141 Cp. Eurostat (2011), p. 112 ff. 142 Cp. European Commission (2012), p. 294. 143 Cp. European Commission (2012), p. 294.

1970 2010 2050

Population (millions) 3,10 3,30 2,80

2,40

2,60

2,80

3,00

3,20

3,40

Po

pu

lati

on

(m

illio

ns)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

28

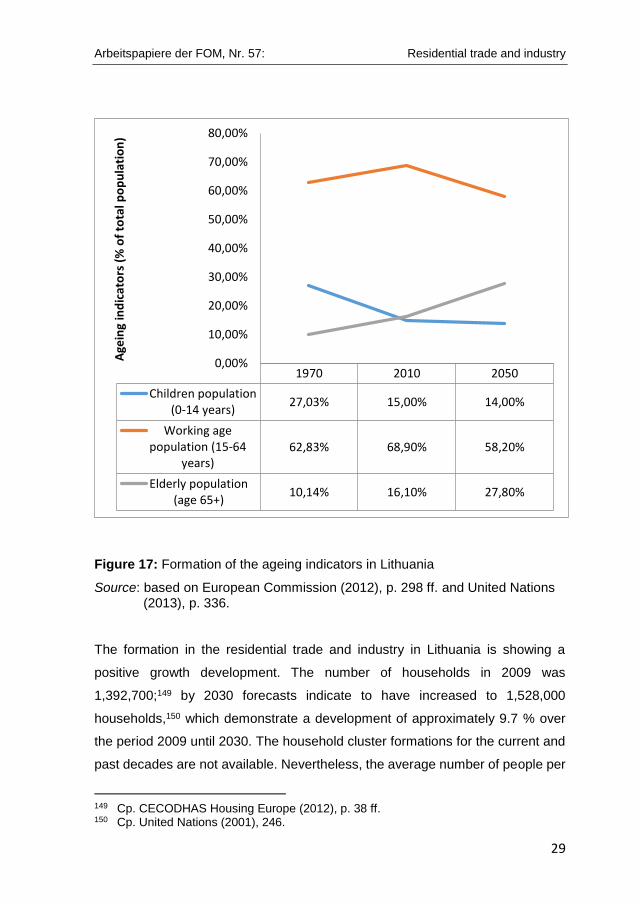

In Lithuania the age indicators demonstrate a demographic shift. While in 2010

the average life expectancy was 67.7 years for males and 78.7 for females, it is

expected to have risen by 2050 to 78.5 and 85.6, respectively.144 This

demonstrates an increase of 10.8 years for males and 6.9 years for females from

2010 to 2050. As a consequence the ageing indicators will rapidly change. In

1970 the cluster of the children’s population aged 0 to 14 represented 27.0 % of

the total population, the working-age population aged 15 to 64 had a percentage

of 62.8 % and the elderly population aged 65 and older had a share of nearly

10.1 %.145 Today the children’s population has shown a negative shift to a

quotation of 15.0 %, the elderly population has risen to a share of 16.1%; and the

working population increased to 68.9 %.146 In the forecast year 2050 it is

estimated that the children’s population will represent 14.0% of the total, the

working-age population 58.2 % and the elderly population 27.8 %, which includes

a cluster of a very elderly population aged 80 years and older of 10.2 % (see

figure 17).147 This is a significant deviance of minus 48.1% in the children’s

population and plus 175.2 % of the elderly population between 1970 and 2050.

Therefore, the median age in years is estimated with a growing shift from an

average age of 39.3 per person in 2013 to a median age of 44.2 in 2050.148 This

medium age is one of the lowest ages in the analysed countries.

144 Cp. European Commission (2012), p. 294 f. 145 Cp. United Nations (2013), p. 336. 146 Cp. European Commission (2012), p. 298 ff. 147 Cp. European Commission (2012), p. 298 ff. 148 Cp. United Nations (2013), p. 70 ff.

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

29

Figure 17: Formation of the ageing indicators in Lithuania

Source: based on European Commission (2012), p. 298 ff. and United Nations (2013), p. 336.

The formation in the residential trade and industry in Lithuania is showing a

positive growth development. The number of households in 2009 was

1,392,700;149 by 2030 forecasts indicate to have increased to 1,528,000

households,150 which demonstrate a development of approximately 9.7 % over

the period 2009 until 2030. The household cluster formations for the current and

past decades are not available. Nevertheless, the average number of people per

149 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 150 Cp. United Nations (2001), 246.

1970 2010 2050

Children population(0-14 years)

27,03% 15,00% 14,00%

Working agepopulation (15-64

years)62,83% 68,90% 58,20%

Elderly population(age 65+)

10,14% 16,10% 27,80%

0,00%

10,00%

20,00%

30,00%

40,00%

50,00%

60,00%

70,00%

80,00%A

gein

g in

dic

ato

rs (

% o

f to

tal p

op

ula

tio

n)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

30

household of 3.7 in 1965151 and 2.4 in 2009152 demonstrates a trend towards

smaller households (see figure 18). In 2007 a shift in age structures is visible from

the household compositions in Lithuania: The share of the single adults under 65

number 12.1 % of the total population; single adults aged 65 and older 14.9 %;

couples both under 65 9.6 %, couples where at least one is aged 65 and older

7.9 %; others, no under 18s 21.9 %; single adults with children 3.8 % and two

and more adults with children 29.8 %.153 This demonstrates senior households

with a proportion of a minimum of 22.8 % in total, which is a relatively balanced

composition level. Total vacant dwelling stock amounted to 3.7 % in 2001,154

which is the lowest level of the analysed countries. Therefore, it is estimated that

there is a basic realisation of custom-made dwellings.

Figure 18: Average number of people per household in Lithuania

Source: based on CECODHAS Housing Europe (2012), p. 38 ff., United Nations (1974); p. 56 ff.

151 Cp. United Nations (1974), p. 56 ff. 152 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 153 Cp. Eurostat (2010b), p. 84. 154 Cp. Ministry of the Interior and Kingdom Relations (2010), p. 63.

1965 2009

Average number ofpersons perhouseholds

3,70 2,40

- 0,50 1,00 1,50 2,00 2,50 3,00 3,50 4,00

Ho

use

ho

ld in

dic

ato

rs

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

31

Poland (PL)

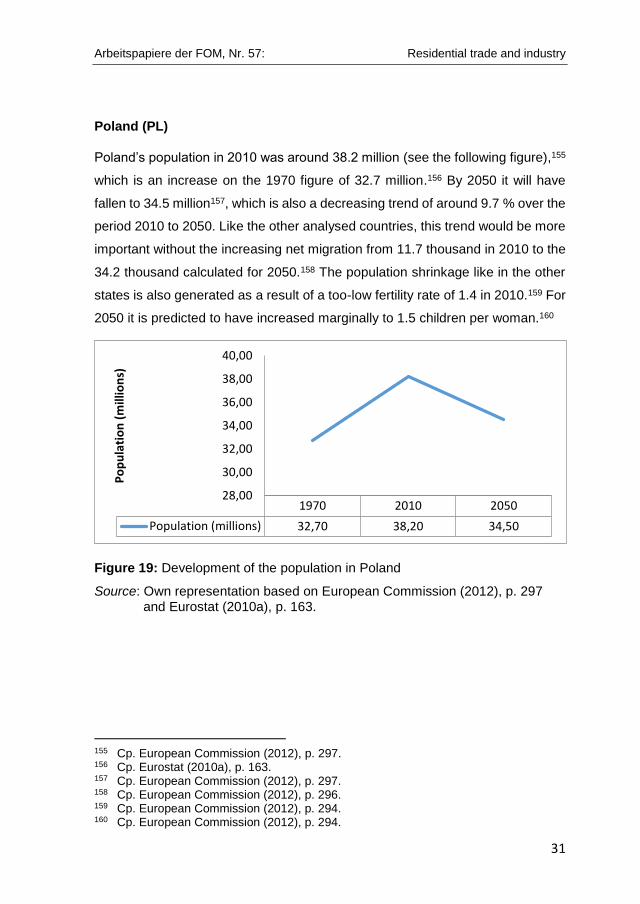

Poland’s population in 2010 was around 38.2 million (see the following figure),155

which is an increase on the 1970 figure of 32.7 million.156 By 2050 it will have

fallen to 34.5 million157, which is also a decreasing trend of around 9.7 % over the

period 2010 to 2050. Like the other analysed countries, this trend would be more

important without the increasing net migration from 11.7 thousand in 2010 to the

34.2 thousand calculated for 2050.158 The population shrinkage like in the other

states is also generated as a result of a too-low fertility rate of 1.4 in 2010.159 For

2050 it is predicted to have increased marginally to 1.5 children per woman.160

Figure 19: Development of the population in Poland

Source: Own representation based on European Commission (2012), p. 297 and Eurostat (2010a), p. 163.

155 Cp. European Commission (2012), p. 297. 156 Cp. Eurostat (2010a), p. 163. 157 Cp. European Commission (2012), p. 297. 158 Cp. European Commission (2012), p. 296. 159 Cp. European Commission (2012), p. 294. 160 Cp. European Commission (2012), p. 294.

1970 2010 2050

Population (millions) 32,70 38,20 34,50

28,00

30,00

32,00

34,00

36,00

38,00

40,00

Po

pu

lati

on

(m

illio

ns)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

32

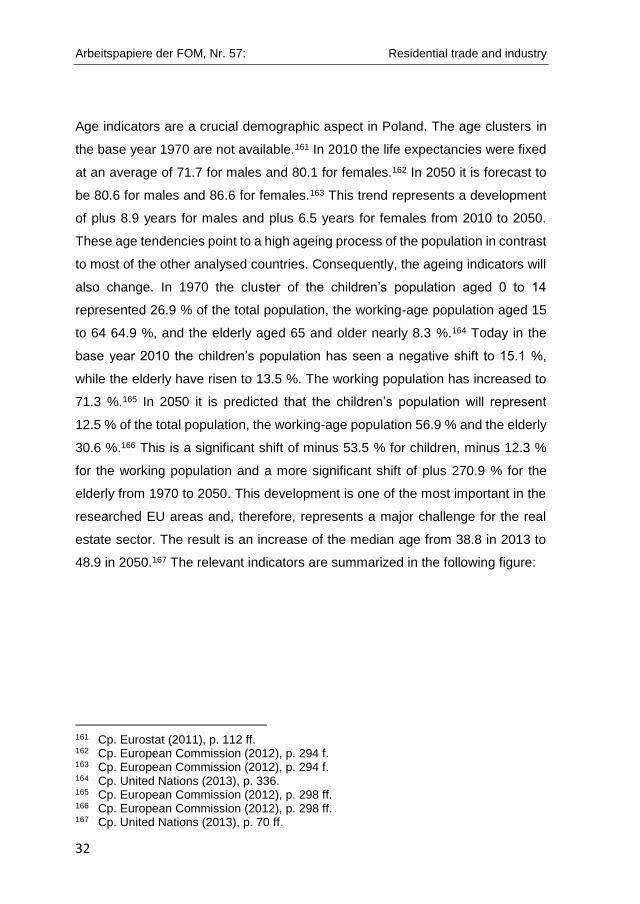

Age indicators are a crucial demographic aspect in Poland. The age clusters in

the base year 1970 are not available.161 In 2010 the life expectancies were fixed

at an average of 71.7 for males and 80.1 for females.162 In 2050 it is forecast to

be 80.6 for males and 86.6 for females.163 This trend represents a development

of plus 8.9 years for males and plus 6.5 years for females from 2010 to 2050.

These age tendencies point to a high ageing process of the population in contrast

to most of the other analysed countries. Consequently, the ageing indicators will

also change. In 1970 the cluster of the children’s population aged 0 to 14

represented 26.9 % of the total population, the working-age population aged 15

to 64 64.9 %, and the elderly aged 65 and older nearly 8.3 %.164 Today in the

base year 2010 the children’s population has seen a negative shift to 15.1 %,

while the elderly have risen to 13.5 %. The working population has increased to

71.3 %.165 In 2050 it is predicted that the children’s population will represent

12.5 % of the total population, the working-age population 56.9 % and the elderly

30.6 %.166 This is a significant shift of minus 53.5 % for children, minus 12.3 %

for the working population and a more significant shift of plus 270.9 % for the

elderly from 1970 to 2050. This development is one of the most important in the

researched EU areas and, therefore, represents a major challenge for the real

estate sector. The result is an increase of the median age from 38.8 in 2013 to

48.9 in 2050.167 The relevant indicators are summarized in the following figure:

161 Cp. Eurostat (2011), p. 112 ff. 162 Cp. European Commission (2012), p. 294 f. 163 Cp. European Commission (2012), p. 294 f. 164 Cp. United Nations (2013), p. 336. 165 Cp. European Commission (2012), p. 298 ff. 166 Cp. European Commission (2012), p. 298 ff. 167 Cp. United Nations (2013), p. 70 ff.

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

33

Figure 20: Formation of the ageing indicators in Poland

Source: based on European Commission (2012), p. 298 ff. and United Nations (2013), p. 336.

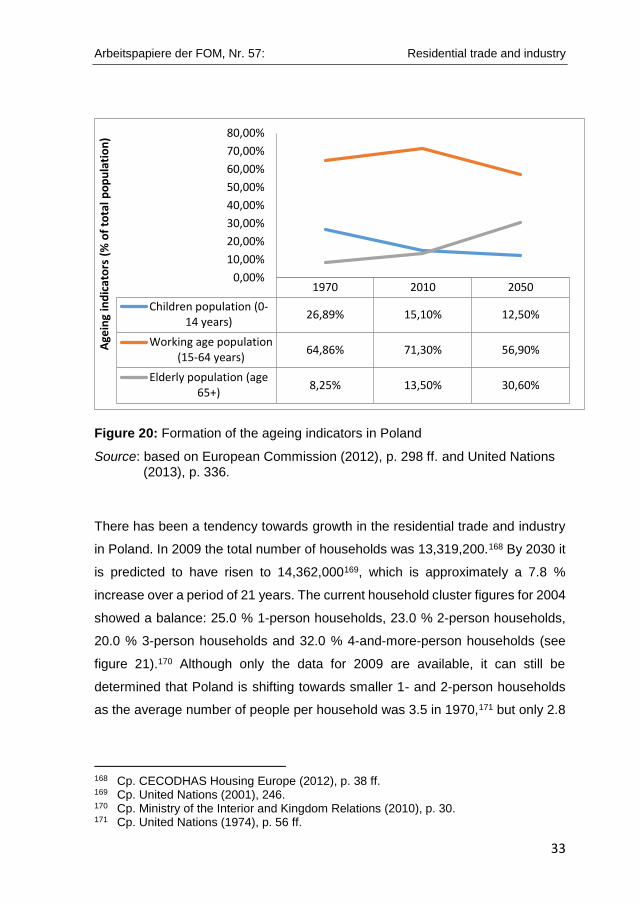

There has been a tendency towards growth in the residential trade and industry

in Poland. In 2009 the total number of households was 13,319,200.168 By 2030 it

is predicted to have risen to 14,362,000169, which is approximately a 7.8 %

increase over a period of 21 years. The current household cluster figures for 2004

showed a balance: 25.0 % 1-person households, 23.0 % 2-person households,

20.0 % 3-person households and 32.0 % 4-and-more-person households (see

figure 21).170 Although only the data for 2009 are available, it can still be

determined that Poland is shifting towards smaller 1- and 2-person households

as the average number of people per household was 3.5 in 1970,171 but only 2.8

168 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 169 Cp. United Nations (2001), 246. 170 Cp. Ministry of the Interior and Kingdom Relations (2010), p. 30. 171 Cp. United Nations (1974), p. 56 ff.

1970 2010 2050

Children population (0-14 years)

26,89% 15,10% 12,50%

Working age population(15-64 years)

64,86% 71,30% 56,90%

Elderly population (age65+)

8,25% 13,50% 30,60%

0,00%

10,00%

20,00%

30,00%

40,00%

50,00%

60,00%

70,00%

80,00%

Age

ing

ind

icat

ors

(%

of

tota

l po

pu

lati

on

)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

34

in 2009.172 The movement of the age structures is apparent from the household

compositions: In 2007 the share of single adults under 65 amounted to 11.3 % of

the total population; single adults aged 65 and older 13.4 %; couples both under

65 10.0 %; couples with at least one partner aged 65 and older 6.6 %; others, no

under 18s 24.6 %; single adults with children 1.8 %; and two and more adults

with children 32.4 %.173 This demonstrates that senior households represent a

minimum of 20.0% of the total, which today points strongly to a balanced age

structure. The amount of vacant conventional dwellings has changed over the

years: in 1970 the figure was 2.6 %174 and in 2002 5.3 %.175 Nevertheless, this

represents the 2nd smallest growth after Lithuania among the countries analysed,

and it can be concluded that the country consists mainly of stable residential trade

and industry portfolio assets because most are in use by the population.

Figure 21: Clusters of households in Poland

Source: based on Ministry of the Interior and Kingdom Relations (2010), p. 30.

172 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 173 Cp. Eurostat (2010b), p. 84. 174 Cp. United Nations (1974), p. 56 ff. 175 Cp. Ministry of the Interior and Kingdom Relations (2010), p. 63.

25%

23%20%

32%

Clusters of households 2004

1-person-households in %

2-person-households in %

3-person-households in %

4-person-households in %and more

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

35

Romania (RO)

Romania’s population in 2010 was around 21.4 million176, which represents a

decline; in 1970 it was 20.1 million177 with 18.4 million forecast for 2050 (see

figure 22).178 This points to an 8.5 % drop between 1970 and 2050. Also in

Romania the net migration has shown a positive development: while the current

net migration figures for 2010 showed a negative trend of about minus 0.2

thousand, migration for 2050 is predicted to be plus 16.8 thousand.179 While the

past fertility rate is not available, the 2010 figure of 1.4 children per woman in

2010 is one of the lowest among the analysed countries.180 For 2050 the forecast

is marginally more positive at 1.5,181 but remains low.

Figure 22: Development of the population in Romania

Source: European Commission (2012), p. 297, Eurostat (2010a), p. 163.

176 Cp. European Commission (2012), p. 297. 177 Cp. Eurostat (2010a), p. 163. 178 Cp. European Commission (2012), p. 297. 179 Cp. European Commission (2012), p. 296. 180 Cp. European Commission (2012), p. 294. 181 Cp. European Commission (2012), p. 294.

1970 2010 2050

Population (millions) 20,10 21,40 18,40

16,00

17,00

18,00

19,00

20,00

21,00

22,00

Po

pu

lati

on

(m

illio

ns)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

36

Life expectancy develops in an analogical way to the afore-mentioned

demographic characteristics of the country.182 While in 1970 the average life

expectancy was 65.8 for males and 70.4 for females,183 in 2010 the figures had

risen to 70.0 and 77.5, respectively.184 By 2050 they are expected to have risen

further to 79.8 and 85.1, respectively.185 This demonstrates the significant

increase of 21.3 % for males and 20.9 % for females from the base year 1970 to

2050. In 1970 the children’s population aged 0 to 14 represented 25.9 % of the

total population, the working-age population aged 15 to 64 66.6 % and the elderly

aged 65 and older nearly 8.4 %.186 Today with the current base year of 2010 the

children’s population has fallen to 15.2 %, the elderly population increased to 14.9

% and the working population increased to 69.9 %.187 In 2050 it is estimated that

the children’s population will have fallen further to 11.9 %, the working-age

population to 57.0 % and the elderly population increased to 31.1 %. The very

elderly aged at least 80 years will represent 9.6 %,188 which is high for this

population (see figure 23). This is a crucial difference of minus 54.1 % in the

children’s population and plus 267.6 % of the elderly population from 1970 to

2050, which is one of the most crucial shifts in the EU with shrinking populations.

The median age in years will also increase from 39.4 in 2013 to a much higher

48.8 in 2050.189

182 No additional data available. 183 Cp. Eurostat (2011), p. 112 ff. 184 Cp. European Commission (2012), p. 294 f. 185 Cp. European Commission (2012), p. 294 f. 186 Cp. United Nations (2013), p. 336. 187 Cp. European Commission (2012), p. 298 ff. 188 Cp. European Commission (2012), p. 298 ff. 189 Cp. United Nations (2013), p. 70 ff.

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

37

Figure 23: Formation of the ageing indicators in Romania

Source: based on European Commission (2012), p. 298 ff., United Nations (2013), p. 336.

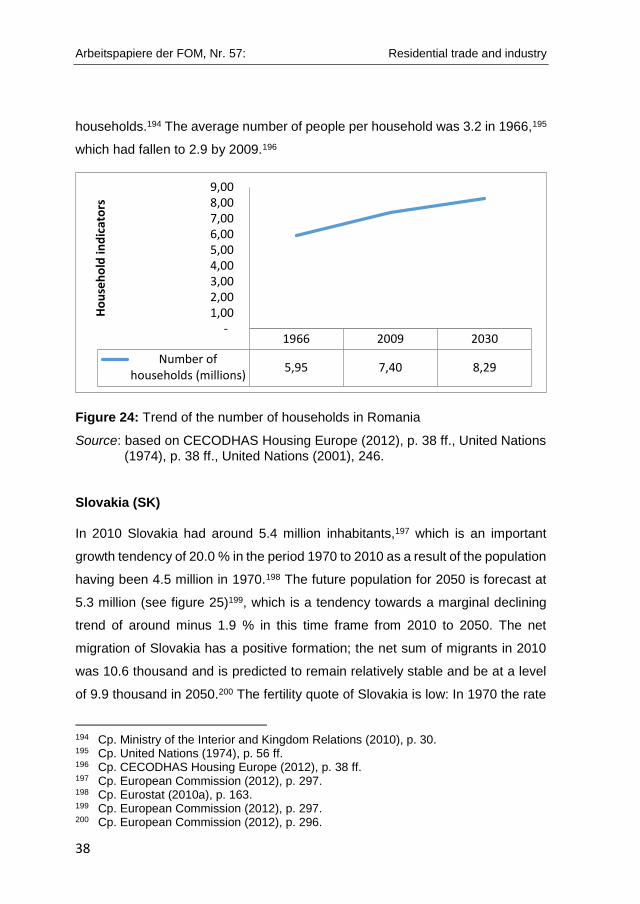

The residential trade and industry of Romania has growing structures (see figure

24). In 1966 the sum of households was analysed with 5,954,555.190 In 2009 the

number was 7,395,700.191 In 2030 the formation will increase with a total number

of 8,288,000 households,192 which demonstrates a significant growth trend of

about 39.2 % over the period 1966 to 2030. In 1966, 1-person households

represented 14.2 % of the household share, for 2-person households 23.4 %, 3-

person households 23.4 % and 4-and-more-person households 39.1 %;193 in

2008 the figures were 18.0 % for 1-person households, 27.0 % 2-person

households, 23.0 % 3-person households and 33.0 % 4-and-more-person

190 Cp. United Nations (1974), p. 38 ff. 191 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 192 Cp. United Nations (2001), 246. 193 Cp. United Nations (1974), p. 38 ff.

1970 2010 2050

Children population (0-14 years)

25,91% 15,20% 11,90%

Working age population(15-64 years)

65,62% 69,90% 57,00%

Elderly population (age65+)

8,46% 14,90% 31,10%

Very elderly population(age 80+)

- 3,20% 9,60%

0%10%20%30%40%50%60%70%80%

Age

ing

ind

icat

ors

(%

of

tota

l po

pu

lati

on

)

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

38

households.194 The average number of people per household was 3.2 in 1966,195

which had fallen to 2.9 by 2009.196

Figure 24: Trend of the number of households in Romania

Source: based on CECODHAS Housing Europe (2012), p. 38 ff., United Nations (1974), p. 38 ff., United Nations (2001), 246.

Slovakia (SK)

In 2010 Slovakia had around 5.4 million inhabitants,197 which is an important

growth tendency of 20.0 % in the period 1970 to 2010 as a result of the population

having been 4.5 million in 1970.198 The future population for 2050 is forecast at

5.3 million (see figure 25)199, which is a tendency towards a marginal declining

trend of around minus 1.9 % in this time frame from 2010 to 2050. The net

migration of Slovakia has a positive formation; the net sum of migrants in 2010

was 10.6 thousand and is predicted to remain relatively stable and be at a level

of 9.9 thousand in 2050.200 The fertility quote of Slovakia is low: In 1970 the rate

194 Cp. Ministry of the Interior and Kingdom Relations (2010), p. 30. 195 Cp. United Nations (1974), p. 56 ff. 196 Cp. CECODHAS Housing Europe (2012), p. 38 ff. 197 Cp. European Commission (2012), p. 297. 198 Cp. Eurostat (2010a), p. 163. 199 Cp. European Commission (2012), p. 297. 200 Cp. European Commission (2012), p. 296.

1966 2009 2030

Number ofhouseholds (millions)

5,95 7,40 8,29

- 1,00 2,00 3,00 4,00 5,00 6,00 7,00 8,00 9,00

Ho

use

ho

ld in

dic

ato

rs

Arbeitspapiere der FOM, Nr. 57: Residential trade and industry

39

was a balanced growth level with 2.4 children per woman201 with the result of an

increasing population structure. This fell sharply to 1.4 children per woman in

2010.202 For 2050 the estimated rate is marginally more positive at 1.5 children

per woman.203

Figure 25: Development of the population in Slovakia

Source: based on European Commission (2012), p. 297, Eurostat (2010a), p. 163.

The shift of the age indicators shows a strong demographic tendency (see the

following figure). In 1970 the average life expectancies were 66.8 for males and