AAPL Forensic Psychiatry Review Course AAPL Forensic Psychiatry ...

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

Market Cap (USD Mil) 483,146

52-Week High (USD) 575.13

52-Week Low (USD) 385.10

52-Week Total Return % 29.1

YTD Total Return % -2.9

Last Fiscal Year End 30 Sep 2013

5-Yr Forward Revenue CAGR % 3.2

5-Yr Forward EPS CAGR % 1.2

Price/Fair Value 0.95

2012 2013 2014(E) 2015(E)

Price/Earnings 15.1 12.0 12.6 12.2EV/EBITDA 10.2 7.3 7.5 7.5EV/EBIT 10.8 8.3 8.7 9.2Free Cash Flow Yield % 6.8 10.6 9.3 8.9Dividend Yield % 0.4 2.5 2.4 2.4

2012 2013 2014(E) 2015(E)

Revenue 156,508 170,910 183,252 190,648

Revenue YoY % 44.6 9.2 7.2 4.0

EBIT 55,241 48,999 52,640 50,112

EBIT YoY % 63.5 -11.3 7.4 -4.8

Net Income, Adjusted 41,733 37,037 38,872 37,193

Net Income YoY % 61.0 -11.3 5.0 -4.3

Diluted EPS 44.15 39.75 43.12 44.45

Diluted EPS YoY % 59.5 -10.0 8.5 3.1

Free Cash Flow 39,323 41,483 39,448 37,512

Free Cash Flow YoY % 37.5 5.5 -4.9 -4.9

Apple will have to fend off increased competition fromAndroid-based competitors in the years ahead.

Brian Colello, CPASenior [email protected]+1 (312) 384-3742

Research as of 10 Mar 2014Estimates as of 31 Jan 2014Pricing data through 01 Apr 2014Rating updated as of 01 Apr 2014

Investment Thesis 28 Jan 2014

We believe Apple's strength lies in its experience and expertise in

integrating hardware, software, services, and third-party

applications into differentiated devices that allow Apple to capture

a premium on hardware sales. Although Apple has a sterling brand,

robust product pipeline, and ample opportunity to gain share in its

various end markets, short product life cycles and intense

competition will prevent the firm from resting on its laurels or

carving out a wide economic moat, in our opinion.

We believe Apple has developed a narrow economic moat, thanks

to switching costs related to a variety of attributes around the iOS

platform that may make current iOS users more reluctant to stray

outside the Apple ecosystem for future purchases. However, much

of Apple's exponential growth in recent years has stemmed not

from the firm's moat, but from the achievement of building the first

truly revolutionary smartphone, the iPhone, that integrated

hardware and software, as well as a robust apps store and

ecosystem that attracted new users to platform. Apple's

first-mover advantage may be diminishing, and "easy growth"

coming from early smartphone adopters may be winding down as

the smartphone market moves up the adoption curve and

competition ramps up from Samsung and others. Yet we still

foresee iPhone growth, coming from both attracting new customers

to iOS (mostly in emerging markets, although we still see U.S.

growth as well) and retaining Apple's existing premium iPhone

customers, where we think the company's moat will play an

increasingly important role. A partnership with China Mobile, the

world’s largest wireless carrier, should also give iPhone growth a

shot in the arm.

Ultimately, we think future smartphone and tablet competition will

stem from software and services, as hardware is already

approaching commoditization. We view Apple as well positioned

to develop and expand enough services to enhance the user

experience, in order to build switching costs that will help the firm

retain customers and generate significant repeat purchases will

be critical for future iPhone growth in the years ahead.

Apple designs consumer electronic devices, including PCs (Mac), tablets(iPad), phones (iPhone), and portable music players (iPod). Apple's productsrun internally developed software, and this integration of hardware andsoftware often allows the firm to maintain premium pricing for its devices.Apple's products are distributed online as well as through company-ownedstores and third-party retailers.

Profile

Vital Statistics

Valuation Summary and Forecasts

Financial Summary and Forecasts

The primary analyst covering this companydoes not own its stock.

Currency amounts expressed with "$" are inU.S. dollars (USD) unless otherwise denoted.

Historical/forecast data sources are Morningstar Estimates and may reflect adjustments.Analyst Note: EPS on a GAAP basis

(USD Mil)

Contents

Investment Thesis

Morningstar Analysis

Analyst Note

Valuation, Growth and Profitability

Scenario Analysis

Economic Moat

Moat Trend

Bulls Say/Bears Say

Credit Analysis

Financial Health

Capital Structure

Enterprise Risk

Management & Ownership

Analyst Note Archive

Additional Information

Morningstar Analyst Forecasts

Comparable Company Analysis

Methodology for Valuing Companies

Fiscal Year:

Fiscal Year:

1

-

2

2

3

4

6

7

7

8

9

11

-

20

24

26

Page 1 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

Morningstar Analysis

Valuation, Growth and Profitability 10 Mar 2014

Our fair value estimate for Apple is $570 per share, whichimplies fiscal 2014 (ending September 2014) price/earningsof 13.5 times, and only 10 times after excluding $157 pershare of net cash on hand as of December 2013. We projectrevenue growth of 6% in fiscal 2014, down from our priorprojection of 13%. Apple profited from successful launchesof new devices such as the iPhone 5s, but follow up salesin the March 2014 quarter were below our expectations,which points to even lower revenue growth through the restof fiscal 2014 as these products age. Longer term, Appleshould still attract late smartphone adopters in developedmarkets and new customers in emerging markets, especiallyas Apple’s partnership with China Mobile, the world’slargest wireless carrier, begins to pay dividends. As moreand more consumers are previous smartphone owners,rather than first-time buyers, we think Apple has a goodchance to retain a sizable portion of its iOS user base today,and perhaps gain further share at the high end of the market.However, although Apple has taken on the strategy ofmaintaining premium pricing, which may support grossmargins in the years ahead, such pricing may weigh onfuture revenue growth. In turn, we model low single-digitiPhone revenue growth in fiscal 2015 and beyond.

We project solid iPad revenue growth in fiscal 2014 and2015, as this device both displaces PCs and is purchased asa third device alongside PCs and phones, but minimal growththereafter as Apple maintains premium pricing on thesedevices but fails to recognize exponential unit growth as inyears past. We assume Apple's line of Mac PCs will seemodest revenue growth, as Macs gain share in the decliningPC industry. We also do not make any profitabilityassumptions for an Apple TV or iWatch but recognize thatfuture innovations may provide upside to our valuation.

We project 37.5% gross margins in fiscal 2014 and mid-30%gross margins in the long term, as Apple maintains its focuson premium pricing that helps to stave off meaningful gross

margin compression, albeit with relatively slower unit salesgrowth. In turn, operating margins should fall to themid-20% range five years out. Our fair value uncertaintyrating for Apple is high.

Scenario Analysis

Our base-case scenario for Apple projects average revenuegrowth of 3% per year from fiscal 2014 to fiscal 2018, aswell as average operating margins of 25% over our five-yearforecast period. Our base scenario projects annual averagerevenue growth of 3% for the iPhone and 6% for the iPad,while unit sales grow at average annual rates of 5% and7%, respectively.

In our bullish scenario, we assume that Apple continues tobuild on its tremendous success with the iPhone, not onlybenefiting from tailwinds surrounding smartphone growth,but maintaining premium pricing for its devices. Similarly,we project 3% higher unit growth for the iPad above ourbase-case assumptions. We also make more optimisticassumptions about all other revenue streams. We maintainour base-case gross margin projections for each productline, but as iPhone becomes a greater portion of overallrevenue, we forecast that Apple's gross margins andoperating margins won't decline as quickly as in ourbase-case assumptions. Under these bullish assumptions,Apple would see average revenue growth of 8% per yearand average operating margins of 28%, and our fair valueestimate would be $730 per share.

In our bearish scenario, we assume Apple's iPhone revenueessentially peaks in fiscal 2014 and falls modestlythereafter. We project average iPhone unit sales declinesof 1% per year, as customers fails to capture new customers.We also model average ASP declines of 3% per year as thefirm sells a higher proportion of older, cheaper models. Wealso model only 3% average iPad unit growth, as Apple’spremium pricing strategy backfires and customers choosecheaper tablets from Android-based competitors. We also

Page 2 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

make more pessimistic assumptions about all other revenuestreams, project modestly sharper gross margin declinesdown to 32% by fiscal 2018, and higher operating expensesthat cause operating margins to dip to 15% by fiscal 2018.Our fair value estimate under our bearish assumptionswould be $400 per share.

Economic Moat

We believe Apple has a narrow economic moat based onmodest, but not insurmountable, customer switching costs.We don't believe these switching costs are critical factorsin attracting new iOS customers, especially in emergingmarkets, but that such switching costs will allow Apple tobuild a loyal iOS user base that may be less likely to flee toother operating systems for future device purchases in thelong term. As the smartphone market matures and a greaterproportion of purchases come from previous smartphoneowners, we foresee these switching costs as extremelyimportant differentiators in favor of Apple. That said, giventhe short product life cycles of two to four years for most ofits devices, we still think competing products will haveplenty of chances to lure iOS customers away from Apple'splatform and overcome these switching costs, especially if

Apple were to stumble in any given product refresh cycle.This prevents us from assigning the company a wideeconomic moat.

Inherently, we believe there are minimal switching costsassociated with smartphones, as all of these devices canperform most necessary functions--place calls, send texts,browse the web, and so on. However, we believe Apple hasdone a much better job at trying to develop switching coststhan its handset predecessors (such as Motorola andBlackBerry) that failed to lock in customers when they wereon top. Apple's speedy initial development of a robustthird-party application ecosystem attracted earlysmartphone buyers and provided a difficult barrier to entryfor other smartphone OS platforms. Although Google’sAndroid was able to develop a similar network andapplications developers focused on building products forboth of these operating systems, Microsoft has been unableto build out a similarly robust developer network thus far,and we think Apple’s early advantage in third-party appswill help fend off many other upstart competitors looking tobuild the next great mobile ecosystem.

In our opinion, Apple's switching costs stem from its iOSoperating system and appear to be increasing, thanks to itsiCloud offering. Apple iOS users who purchase movies, TVshows, and applications from the iTunes store are unableto port these media to Android or other portable devices(music is transferrable). iCloud adds another layer ofswitching costs by synchronizing media, photos, notes, andother items across all Apple devices. We believe an ownerof an iOS device (say, an iPad) is less likely to switch froman iPhone to an Android phone if it means that he or shewill be unable to sync or access a portion of their content.Additional Apple devices, such as the Mac and potentiallyan iWatch, could raise these switching costs even further.By comparison, no other former handset leader (Nokia,Motorola, BlackBerry) offered secondary devices thatpartnered with their phones, giving Apple a unique edge

Page 3 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

that handset makers such as Samsung are only now startingto emulate. Along these lines, the iPad Mini, sold at lowerprice points and, presumably, lower margins, may modestlyeat into Apple's tablet profitability but could be the rightmove if it gains further lock-in from price-consciousconsumers who would otherwise buy Amazon's andGoogle's cheaper tablets. Another encouraging but perhapsfleeting factor is that customers have willingly acceptediCloud and the coinciding switching costs because it offersusers a better product experience, rather than otherinstances of high switching costs where customersbegrudgingly accept these lock-in costs because of existinginfrastructure, a lack of suitable alternatives, or becausetheir businesses dictate such moves.

Looking at other sources of economic moat, Apple holdsintangible assets associated with patents for its hardwareand software designs. However, both the value of suchassets and the sustainable competitive advantagestemming from these assets remain cloudy. RegardingApple’s sterling brand equity, we view brands withintechnology differently than, say, consumer luxury goods. Wedoubt that Apple can charge double the price for a productthat has the exact same hardware and softwarespecifications as an unbranded product. However, we thinkthat Apple benefits from intangible assets, or a brand, interms of the (mostly) positive user experiences thatcustomers capture from the firm’s integrated hardware,software and services. Similarly, Apple might be the world'smost trusted consumer technology firm in terms ofdelivering flawlessly working products in existing, and evennew, product categories. However, we still think tech brandsare relatively fleeting, as technological inferiority cansupersede years of brand equity at any given time. As anexample, Nokia was long considered a top-10 brand, but itsfailure to stay on the technological forefront overtook itsbrand recognition.

Apple is trying to improve the network effects of its deviceswith functions like iMessage and FaceTime. However,BlackBerry's demise proves that even highly popularsmartphone-centric networks like BlackBerry Messengercan be broken if other smartphone features (or lack thereof)drive customers to flee. Network effects may be formingaround Apple’s apps developers, as a more robust apps storeis likely helping Apple attract new customers. However,these same developers likely build for Android as well, sowe think that developers will flock to the ecosystem thatoffers the most attractive return on investment. Finally,Apple may have some cost advantages associated with itssupply chain, such as squeezing suppliers or making massivepurchases of flash memory and other key components.However, we believe these advantages are predicated onthe enormous forecast volume of Apple's products, and wesuspect these advantages would evaporate if Apple'sdevice production were to shrink.

Moat Trend

We believe Apple has a positive moat trend. The company'siCloud offering should raise switching costs associated withiOS devices as more and more customers buy and ownmultiple iOS devices (iPhones plus iPads, for example), aswell as acquire Apple-only media and applications on theiriOS devices and choose to upload this content, along withphotos and other items, to iCloud. We believe theseswitching costs are increasing based on Apple's strong iPadgrowth in recent years, as more and more iPhone users nowown a second device that runs the iOS system and syncsbetween the two devices. Apple has disclosed that it has300 million iCloud subscribers as of June, which representsrapid growth as compared to 250 million just five monthsearlier. In our view, ownership of multiple devices not onlydecreases the likelihood that customers would look foralternative devices that would be incompatible with theseproducts, but perhaps improves the probability thatcustomers buy even more iOS devices including Macs and

Page 4 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

Morningstar Analysis

Apple TVs.

To a lesser extent, we also believe Apple's switching costsare increasing in regard to iPad sales into the enterprise.Gartner estimates that only 13 million iPad businesssubscribers (defined as devices either acquired by abusiness or expensed to it) existed in 2013, but this baseshould rise to 41 million users by 2017. We believe that notonly are a growing number of corporations purchasing iPadstoday, but that these companies are writing nativeapplications for its employees that work solely on iOSproducts, rather than browser-based apps that would runon multiple tablet platforms. We think it would beincreasingly unlikely that such businesses would migrate toAndroid- or Windows-based tablets based purely on costsavings. Although enterprise iPad sales don't move theneedle on our valuation today, we believe Apple's growingpresence in the enterprise is leading to stronger switchingcosts. Switching costs may also arise from the educationmarket, to the extent that schools and universities build iOSapps that work with iPads used by students. In theSeptember quarter, Apple earned $1 billion of revenue fromeducational sales, and further adoption from schools mayallow Apple to have a steadier stream of customers andfuture iOS device buyers in the long term.

In our view, much of Apple's outsized growth in recent yearshas stemmed not from the firm's moat, but rather from afirst-mover advantage as a result of building the first trulyrevolutionary smartphone with a robust apps store andecosystem that attracted new users to platform--all whilefacing little direct competition. Apple's ability to attract newiPhone users to the platform may wane in the years ahead,partially due to greater competition from Samsung, butmostly because Apple's premium pricing strategy mayprevent new customers in emerging markets from switchingto iPhones. However, we don't necessarily see either ofthese factors as a sign that the company's moat is eroding

rather than strengthening. Neither of these factors indicateweakening switching costs, in our view, and we have notyet seen much evidence that iOS users are abandoning theplatform. For example, data from Kantar World Panelsuggest that only a single-digit percentage of Samsung'ssmartphone sales in the U.S. in 2012 came from platformsother than the iPhone, and more recently, data fromComscore indicates that Apple is gaining, rather than losing,smartphone subscribers in the U.S.

Nonetheless, we continue to believe that the short productlife cycles associated with Apple's products will prevent thefirm from gaining a wide economic moat. iOS and iCloudprovide some switching costs, but we don't think these costsare overwhelming. If Apple were to ever launch a completeflop of a product or lose a significant aspect of functionalityin its devices (say, if Facebook were no longer included orif much-maligned Apple Maps was the only mappingsolution allowed on iOS), customers may be annoyed by iOSswitching costs, but less so than the frustration associatedwith buying premium Apple products that provide an inferioruser experience. Another risk to Apple's moat trend, in ourview, is that a variety of platform-agnostic web-basedservices, such as Dropbox, Evernote, Spotify, and Netflixmay make media ownership, switching costs, and iCloudless important differentiators for Apple in the future.

Page 5 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

Bulls Say/Bears Say

Bulls Say Bears Say

3 Gartner expects the smartphone market to more thandouble from 2012 to 2015, providing Apple withavenues for iPhone growth.

3 Apple appears poised to generate strong revenuegrowth from the iPad in the years ahead as tabletscannibalize PCs.

3 For each iOS device purchased, customers may be lesslikely to switch to another provider and more likely tobuy repeat Apple products, which we view as a goodsign for long-term iPhone, iPad, and Mac sales, as wellas an ability to drive revenue from new devices like arevised Apple TV or iWatch.

3 Apple’s recent decisions to maintain a premiumpricing strategy may help fend off gross margincompression but may also limit unit sales and marketshare as the low end of the smartphone space willlikely grow faster than the premium market.

3 Whereas Apple focuses on a handful of key products,Samsung has emerged as a strong rival by offeringhighly competitive devices of all sizes and prices atall times of the year.

3 Apple may have lost much of its vision and creativitywith the passing of cofounder Steve Jobs in October2011.

Page 6 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

2014(E) 2015(E) 2016(E) 2017(E) 2018(E)

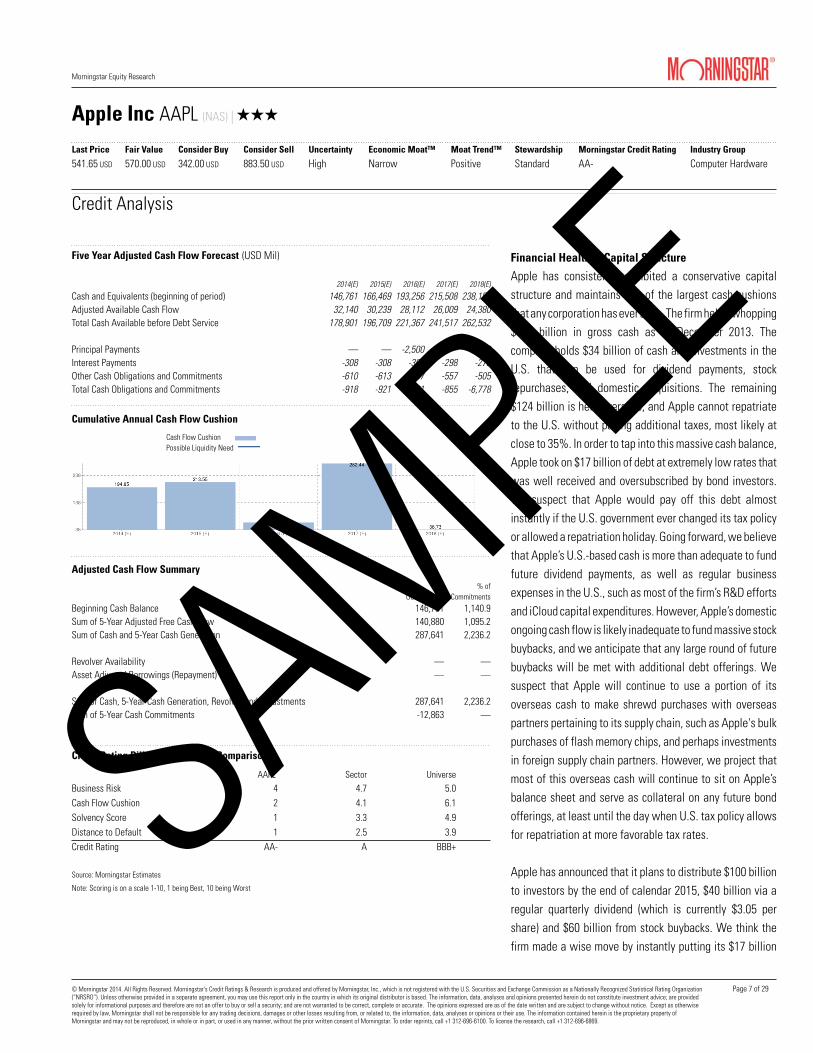

Cash and Equivalents (beginning of period) 146,761 166,469 193,256 215,508 238,152Adjusted Available Cash Flow 32,140 30,239 28,112 26,009 24,380Total Cash Available before Debt Service 178,901 196,709 221,367 241,517 262,532

Principal Payments — — -2,500 — -6,000Interest Payments -308 -308 -304 -298 -273Other Cash Obligations and Commitments -610 -613 -587 -557 -505Total Cash Obligations and Commitments -918 -921 -3,391 -855 -6,778

USD Millions% of

Commitments

Beginning Cash Balance 146,761 1,140.9Sum of 5-Year Adjusted Free Cash Flow 140,880 1,095.2Sum of Cash and 5-Year Cash Generation 287,641 2,236.2

Revolver Availability — —Asset Adjusted Borrowings (Repayment) — —

Sum of Cash, 5-Year Cash Generation, Revolver and Adjustments 287,641 2,236.2Sum of 5-Year Cash Commitments -12,863 —

AAPL Sector UniverseBusiness Risk 4 4.7 5.0Cash Flow Cushion 2 4.1 6.1Solvency Score 1 3.3 4.9Distance to Default 1 2.5 3.9Credit Rating AA- A BBB+

Five Year Adjusted Cash Flow Forecast (USD Mil)

Credit Analysis

Cumulative Annual Cash Flow Cushion

Cash Flow CushionPossible Liquidity Need

Adjusted Cash Flow Summary

Credit Rating Pillars Peer Group Comparison

Source: Morningstar Estimates

Note: Scoring is on a scale 1-10, 1 being Best, 10 being Worst

Financial Health & Capital Structure

Apple has consistently exhibited a conservative capitalstructure and maintains one of the largest cash cushionsthat any corporation has ever seen. The firm held a whopping$159 billion in gross cash as of December 2013. Thecompany holds $34 billion of cash and investments in theU.S. that can be used for dividend payments, stockrepurchases, and domestic acquisitions. The remaining$124 billion is held overseas, and Apple cannot repatriateto the U.S. without paying additional taxes, most likely atclose to 35%. In order to tap into this massive cash balance,Apple took on $17 billion of debt at extremely low rates thatwas well received and oversubscribed by bond investors.We suspect that Apple would pay off this debt almostinstantly if the U.S. government ever changed its tax policyor allowed a repatriation holiday. Going forward, we believethat Apple’s U.S.-based cash is more than adequate to fundfuture dividend payments, as well as regular businessexpenses in the U.S., such as most of the firm’s R&D effortsand iCloud capital expenditures. However, Apple’s domesticongoing cash flow is likely inadequate to fund massive stockbuybacks, and we anticipate that any large round of futurebuybacks will be met with additional debt offerings. Wesuspect that Apple will continue to use a portion of itsoverseas cash to make shrewd purchases with overseaspartners pertaining to its supply chain, such as Apple's bulkpurchases of flash memory chips, and perhaps investmentsin foreign supply chain partners. However, we project thatmost of this overseas cash will continue to sit on Apple’sbalance sheet and serve as collateral on any future bondofferings, at least until the day when U.S. tax policy allowsfor repatriation at more favorable tax rates.

Apple has announced that it plans to distribute $100 billionto investors by the end of calendar 2015, $40 billion via aregular quarterly dividend (which is currently $3.05 pershare) and $60 billion from stock buybacks. We think thefirm made a wise move by instantly putting its $17 billion

Page 7 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

Credit Analysis

of debt proceeds to work by buying back $16 billion of stockin the June 2013 quarter at, in our opinion, attractive prices.Despite calls from some investors for a more aggressivecapital allocation policy, we would be surprised if Applesignificantly expanded its buyback program in the nextcouple of years beyond its $60 billion authorization today.Apple has notoriously been stingy with capital distributionto investors, especially under the Steve Jobs regime, andwe highly doubt that the firm will ever take on a net debtposition, or even more debt than what it could instantly payoff with its overseas cash hoard. We continue to projectthat Apple will make tiny, bolt-on acquisitions of intriguingstartups, in order to capture engineering and developmenttalent that can help improve the firm’s product offeringswhile fitting in seamlessly with Apple’s corporate culture.We see little risk that Apple will make a splashy, high-pricedacquisition that could destroy value for shareholders.

Enterprise Risk

We believe a large, well-diversified company like Applefaces several risks. Smartphone and tablet competition isrising, as Samsung, in particular, has developed compellingiPhone alternatives in the premium smartphone space.Meanwhile, we anticipate that a greater portion ofsmartphone sales come from low-end devices in emergingmarkets where Apple does not participate. If these devicesturn out to offer only a slightly worse user experience thaniOS products, Apple may be unable to capture an adequatepremium on future hardware sales. Apple also has to squareoff against several competitors with much differentstrategies than traditional hardware makers. Apple’sdevices compete against firms like Amazon (with its KindleFire tablet) and Xiaomi, which appear willing to sellhardware at cost, in order to drive other revenuestreams.Despite its intentions to control as much of the userexperience as possible for its products, Apple still relies ona robust app developer base and strong partnerships withthird parties. Its decision to use an in-house mapping

solution (and subsequent apology) may have diminishedApple's reputation and its customers' user experience, andother similar missteps may cause customers to leave theiOS ecosystem altogether. If Apple were to falter and itsexceptional brand be diminished as customers departed iOSin droves, we’re not even sure that Apple’s mighty cashcushion could help the firm buy its way out of any problem.Asa premium phone supplier, Apple also runs the risk thatwireless carriers could reduce or eliminate the subsidiesthat they provide their customers on the iPhone, in turnraising customers' up-front costs and perhaps making othersmartphones appear to be better alternatives. Finally, Applelost cofounder and visionary Steve Jobs in October 2011,and while we believe CEO Tim Cook is a more-than-capableleader, Apple runs the risk that its unique culture and senseof innovation may diminish over time.

Page 8 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

Name Position Shares Held Report Date* InsiderActivity

MR. ARTHUR D.LEVINSON, PHD

Director 162,698 01 Feb 2014 —

MR. TIMOTHY D. COOK CEO/Director,Director 87,371 31 Jan 2014 —MR. ALBERT A. GORE,JR Director 62,523 01 Feb 2014 —CRAIG FEDERIGHI Senior VP, Divisional 41,170 15 Mar 2014 —MR. ROBERT A. IGER Director 5,541 01 Feb 2014 —PETER OPPENHEIMER CFO/Senior VP 4,889 31 Jan 2014 —DANIEL J. RICCIO Senior VP, Divisional 3,064 25 Feb 2014 9,192MR. WILLIAM V.CAMPBELL

Director 2,523 01 Feb 2014 —

Top Owners% of Shares

Held% of Fund

AssetsChange

(k) Portfolio Date

Vanguard Total Stock Mkt Idx 1.54 2.28 105 28 Feb 2014PowerShares QQQ Trust, Series 1 1.09 11.88 -39 31 Mar 2014Vanguard Institutional Index Fund 1.00 2.84 19 28 Feb 2014Vanguard Five Hundred Index Fund 0.98 2.83 47 28 Feb 2014SPDR S&P 500 0.97 2.88 -93 28 Mar 2014

Concentrated Holders

Fidelity® Select Computers Portfolio 0.03 20.56 -6 28 Feb 2014Newmark Risk-Managed Opportunistic — 19.71 0 31 Dec 2013Putnam Global Technology Fund — 18.89 — 31 Dec 2013ProFunds VP Technology — 17.05 1 31 Dec 2013JNL/Mellon Cptl Technology Sector Fund 0.02 16.93 13 31 Dec 2013

Top 5 Buyers% of Shares

Held% of Fund

Assets

SharesBought/Sold (k) Portfolio Date

Heights Capital Management Inc 0.42 42.87 2,066 31 Dec 2013New Jersey Division of Pensions and Benefits 0.21 0.76 1,880 30 Jun 2010Deutsche Bank AG 0.36 2.18 1,650 31 Dec 2013Morgan Stanley & Co Inc 0.22 1.81 1,079 31 Dec 2013Coatue Management LLC 0.17 8.28 1,066 31 Dec 2013

Top 5 Sellers

Susquehanna Financial Group, LLLP 0.35 0.96 -4,140 31 Dec 2013Commerzbank AG 0.16 3.77 -2,430 31 Dec 2013J.P.Morgan Securities Inc. 0.10 1.04 -1,653 31 Dec 2013Citigroup Inc 0.30 1.37 -1,278 31 Dec 2013Bank of New York Mellon Corp 0.54 2.26 -1,093 31 Dec 2013

Management 10 Mar 2014

Management & Ownership

Management Activity

Fund Ownership

Institutional Transactions

*Represents the date on which the owner’s name, position, and common shares held were reported by the holder or issuer.

We view Apple as a good steward of shareholder capital.Arthur Levinson, former chairman and CEO of Genentech, ischairman of Apple's board of directors. Tim Cook becameCEO in August 2011 after cofounder, longtime CEO, andvisionary Steve Jobs stepped down from the CEO role beforepassing away in October 2011. Cook was considered to beJobs' right-hand man and served in various operations roleswith Apple before becoming COO in 2005. We believe Jobs'passing was a blow to the firm, as he was a one-of-a-kindleader and creative mind.

Although Apple maintains sterling brand recognition andhas hundreds of millions of loyal followers, the companyhas made a couple of missteps under Cook that, some wouldargue, would have never happened under Steve Jobs. Appleexecuted poorly when it decided to part ways with GoogleMaps in iOS 6 and launch Apple Maps with a variety of bugsand errors, leading to a formal apology and the ouster of VPScott Forstall. Also, Apple hinted that it believes that a 4" screen is an adequate screen size for a smartphone, yetSamsung has done quite well in the near term with its muchlarger Galaxy smartphones and Galaxy Note phablets(phone/tablets). We fear that Apple may miss out on partof the premium smartphone market if it fails to build alarger-screen iPhone in the near-future, although rumorscontinue to swirl that an iPhone 6 launch in 2014 may includea larger screen version.

On the other hand, while many may have questioned Apple’smanagement team about its decision to price the iPhone 5cat $549, rather than at lower prices that more directlyaddresses emerging market demand, we tend to approve ofApple’s decisions to maintain its premium pricing position.We also applaud Cook’s decision to initiate a dividend andstock buyback plan in early 2012, as well as take on debt inorder to fund a $60 billion stock buyback program in 2013.We recognize that many high-profile investors have calledfor an even larger buyback program, but we think that

Page 9 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

Apple’s current plan is satisfactory as long as buybacks (andthe debt issuances needed to fund these buybacks) are madein a prudent manner. In retrospect, the misstep may havecome from not front loading the buyback program in 2013when both Apple’s share price and interest rates were lowerthan today.

Perhaps more importantly, we think Apple’s frugality is quiteadmirable in terms of acquisitions. Apple's strategy offocusing on smaller tuck-in deals and developing productsin-house, rather than splashy but questionable deals likeMicrosoft's purchase of Skype or Google's foray intohardware by acquiring Motorola Mobility and Nest, appearsto have served investors quite well in recent years. Applehas also done a good job of attracting top-notch talent tothe company in recent months, such as former Burberry CEOAngela Ahrendts to run Apple’s retail and online stores, andPaul Deneve, the former CEO of Yves Saint Laurent. We arecomfortable that these hires have strengthened Apple’sbench in the unlikely event that Cook were to depart thecompany. Both hires not only have experience managingluxury brands that sell aspirational goods, but also fuelspeculation that an iWatch is on the horizon. All the while,Apple’s ongoing operations continue to generate operatingmargins and cash flow well above its peers in varioushardware industries, which bodes well for future free cashflow for investors.

Page 10 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

Analyst Notes

We Expect a Seamless CFO Transition at Apple as

Oppenheimer Retires; Maintaining our FVE 04 Mar 2014

We will maintain our $570 fair value estimate and narrowmoat rating for Apple after the firm announced that CFOPeter Oppenheimer will retire at the end of September. Allin all, we anticipate a seamless transition of the role, andwe don’t foresee any radical changes in capital allocationat Apple as a result of the change. We should note that CEOTim Cook hinted that an update to the firm’s capitalallocation policy, which will presumably include a dividendhike and possibly an expanded stock buyback program, willbe announced in the next 60 days.

Luca Maestri, Apple’s current VP of Finance and corporatecontroller, will take over the CFO position in June, whileOppenheimer will stay on through September to assist withthe transition. Maestri joined Apple in March 2013 and wasformerly CFO of Nokia Siemens Networks and Xerox andalso has 20 years of finance and operations managementexperience at General Motors. Tim Cook was even quotedin the company’s press release that Maestri was consideredto be Oppenheimer’s heir apparent, and we have no reasonto believe that Maestri won’t be up to the challenge ofrunning all of Apple’s financial operations.

Apple's CarPlay May Help Drive Future iOS Device

Sales; Maintaining Our $570 Fair Value Estimate 03 Mar

2014

We will maintain our $570 fair value estimate and narrowmoat rating for Apple as the firm launches CarPlay, itsautomotive software solution that allows for easy iOS usagein the car. We view CarPlay as yet another native applicationdeveloped by Apple that probably won't drive much revenuebut creates another layer of modest switching costs thatwill ultimately allow the firm to maintain premium pricingand sell future high-margin iPhones to current iOScustomers in the long term.

CarPlay will allow drivers to access Siri, directions via Applemaps, phone calls, text messages, music, and podcasts ina hands-free manner in the automobile, either via theinfotainment display panel in the car or with push-and-holdvoice control buttons on the steering wheel. CarPlay willalso support third-party apps like Spotify, and we suspectthat Apple's robust network of iOS app developers will buildnew and modified apps to work with the platform and makeit a stronger car entertainment solution in the future.Perhaps the biggest question is whether Google will supportCarPlay with Google Maps and perhaps search and otherapps down the line. The software solution was introducedthis week in Geneva in partnerships with Ferrari, Mercedes-Benz, and Volvo, but many other original-equipmentmanufacturers are lined up to incorporate CarPlay in futurevehicles. From a geographical perspective, CarPlay issupported in North America and many Western Europeancountries, but mainland China is absent thus far (Hong Kongis supported).

Our initial take on CarPlay is that the platform appearssimilar to what the company hinted at in June during itscomments about "iOS in the car" at its Worldwide DeveloperConference. While CarPlay appears to be optimized tohandle entertainment, mapping, voice, and text functions inthe car, it does not appear to handle other automotive-specific diagnostics functions like tire pressure or fuelgauges. We suspect that Apple will leave this functionalityto current embedded software platforms like QNX, andalthough QNX will still probably offer entertainment appsand features in its software, CarPlay may simply overridethese functions.

Since Apple has consistently relied on vertical integrationand focuses on controlling all of the key technologies in itsproducts, we think it is limited in what it can do in theautomotive market and, similarly, the Internet of Things.

Page 11 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

Analyst Notes

Since Apple won't develop automotive parts like tires orengines anytime soon, we doubt it will want to beresponsible for measuring the diagnostics of such products.Rather, all of CarPlay's functions and features are those thatApple fully controls as part of iOS 7, and CarPlay doesn'tappear to touch any other hardware or software functionsin the rest of the car.

We continue to believe that car OEMs will want to takeownership of the infotainment systems in their cars in orderto better compete with one another in the highly competitiveauto market. Similarly, we don't foresee carmakers simplyinstalling dumb touch screen panels into their cars andallowing smartphones or tablets to control the entireinfotainment experience in the same manner that Apple TVor Google Chromecast allows users to project the contenton their smartphones and tablets onto a larger screen. Thisis why we think CarPlay was launched as simply a softwareinterface, rather than an entire infotainment hardware andsoftware system installed in the car. This dynamic alsoprobably prevents Apple from capturing its normal pricingpremium and above-average gross margins on hardwaredevice sales if it were to build a full infotainment system.

Along these lines, many car OEMs like General Motors,Honda, and Hyundai implicitly intend to be operatingsystem-agnostic in their vehicles, as each not only willsupport CarPlay, but also are founding members of Google'sAndroid-based Open Automotive Alliance. We anticipatethat car OEMs won't want to be locked down to a singleoperating system, as they may lose a potential sale becausethe buyer has a different smartphone OS in his pocket.Similarly, we doubt that each carmaker will want to buildan iOS and an Android version of their automobiles in orderto placate all potential customers. Additionally, given themuch longer lives of automobiles when compared with twoor three years for a smartphone, automakers should wantto protect themselves in the event (albeit unlikely) that iOS

or Android become antiquated technologies. In this vein,CarPlay will probably be accepted by car OEMs exactlybecause it is incremental to, rather than replacing, existingautomotive infotainment operating systems, regardless ofwhether Android, QNX, or something else wins out in thefuture.

In terms of Apple's narrow moat and positive trend rating,we currently view CarPlay in the same manner as iWorks,FaceTime, iMessage, and other native applications providedby Apple. None of these native applications or software willbe major revenue drivers for the firm, but they will eachprobably create modest (but not insurmountable) switchingcosts that will allow Apple to maintain premium pricing andcontinue to sell high-margin iPhones to customers well intothe future. We think the strength of CarPlay's potentialswitching costs will stem from how superior theentertainment system will be when compared with the car'snative infotainment system and, similar to smartphones,how well Apple can cultivate a network of app developersthat can build CarPlay into the most robust and uniqueentertainment system on the market.

Today, if CarPlay is considered to be far superior to theinfotainment options offered by Android or QNX, then it mayin fact lead to solid switching costs for current iOS users.Longer term, however, as Android and QNX improve, CarPlaymay not offer many switching costs or customer lock-in atall, as all infotainment options may be adequate. Butperhaps more important, CarPlay may negate switchingcosts for other operating systems as well, making the cartruly agnostic. Those who buy an automobile with anAndroid operating system may not necessarily be locked into buying Android-based handsets for as long as they ownthe car, as long as CarPlay is an available option within thesame device and is equal to, if not better than, theentertainment options provided within the Android car OS.Similarly, we doubt BlackBerry can leverage any future

Page 12 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

Analyst Notes

improvements in QNX into a sustainable competitiveadvantage that will allow it to sell more BlackBerryhandsets. Thus, we view CarPlay as no worse than neutralbut more likely a modest positive to Apple's narrow moatand sustainable competitive advantage.Apple Serves Up a Disappointing Near-Term Revenue

Forecast; Trimming Our Fair Value Estimate to $570 27

Jan 2014

Apple reported strong fiscal first-quarter earnings, but gaveinvestors a troubling second-quarter forecast that implieslittle iPhone growth despite a new partnership with ChinaMobile, the world’s largest wireless carrier. We will likelytrim our fair value estimate slightly, but will maintain ournarrow economic moat rating. None of the bad news inApple’s earnings report changes our long-term view of itsfundamentals, or its ability to retain customers in the future. Revenue of $57.6 billion for the December quarter wasnear the high end of management's guidance, and withinour range of expectations. Unit sales of its iPhone--51million--was slightly below our projection. However,average selling prices, or ASPs, of $637 held up well. TheiPad was the pleasant surprise, with 26 million units sold,although the iPad's ASPs remained flat despite priceincreases on new models, which suggests a negativeproduct mix. Mac units also grew nicely, up 19%sequentially in a tough PC environment. Gross margins of37.9% also exceeded the firm’s guidance, thanks to afavorable iPhone product mix toward the higher-priced 5s,as well as component cost savings. Our greater concern,however, comes from Apple’s March-quarter revenueprojection of $42 billion to $44 billion. This is well belowStreet expectations of $46 billion. We think the forecastimplies iPhone unit sales in the high 30-million range, andonly modest growth from the 37 million iPhones sold duringthe March 2013 quarter.

In the near term, headwinds persist. These include astronger U.S. dollar, and differences in the timing of iPhone

and iPad launches in China. Still, we would have expectedApple’s new partnership with China Mobile to more thanmask their impact. Apple’s gross margin forecast for Marchis a bright spot, but by maintaining a premium pricingstrategy on hardware, Apple may see less-than-stellarrevenue growth going forward.

We're lowering our fair value estimate for Apple to $570per share following the firm’s gloomy, March-quarterforecast. As revenue typically dives each quarter fromDecember to March and then June (until Apple launchesnew devices again in September, or unless new productsare announced before then), we think a soft March quarterwill lead to fiscal 2014 revenue growth of approximately6%, a bit below our prior projection. Revenue at the high end of Apple's projected range of $44billion would represent a 24% sequential decline, and only1% growth from the year-ago quarter. This would be despitepreviously widespread optimism around new carrier dealswith NTT DoCoMo, and China Mobile. We note that Applealso has not meaningfully exceeded the high end of itsrevenue forecast since it began giving a full revenue rangea year ago, so we’re hesitant to think that there’s much ofa chance of a meaningful upside surprise next quarter. Apple cited four main factors for the soft sales forecastwhich, if absent, would have led to another $2 billion ofrevenue next quarter: currency headwinds, a rapidlydeclining iPod market, greater revenue deferrals on newproduct sales (because Apple now gives more softwareaway for free), and channel inventory adjustments in China.However, we would have anticipated that the China Mobilelaunch alone would have been more than enough toovercome the impact of these collective headwinds.

Additionally, in our view, further growth at China’s othercarriers, China Unicom and China Telecom, would have

Page 13 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

Analyst Notes

masked any dips in sales in China due to changes in thetiming of product launches there. Apple commented thatthe China Mobile launch is off to an "incredible start," butwe believe that investor expectations for such a start wouldhave contributed to more than 1% annual revenue growth,regardless of these other negative factors. Even if sales atChina Mobile turn out to be strong, they may wind up simplymasking other iPhone problems, such as limited growth (atbest) in North America in the near-term, and market sharedeclines, as announced by Kantar World Panel, in WesternEurope. Despite the haircut to our fair value estimate, we still viewApple as having a strong underlying base of loyal customers,where switching costs and the firm’s narrow economic moatwill allow the company to generate repeat purchases overthe long term. We also foresee Apple attracting its fair shareof late smartphone adopters in developed markets, as wellas capturing greater wallet share among customers in bothdeveloped and emerging markets that look to trade up fromlower-priced smartphones to higher-priced iPhones. Wecaution, however, that Apple’s premium pricing strategy willmake it harder for it to capture new customers in the futurethan a few years ago, during the early adoption phase. By our estimates, if we ran a scenario where Apple achievedno iPhone revenue growth beyond fiscal 2014, we’d valuethe company at about $500 per share. Although Apple’s poorforecast for the March quarter suggests that such a scenariomight be closer to reality than what we previously thought,we’re not ready to count out long-term iPhone revenuegrowth just yet. We also anticipate strong iPad growth over the next coupleof years, as tablet adoption hasn’t come close to maturing.Enterprise and educational iPad adoption still remain astickier underlying portion of total iPad growth. We remainencouraged that Apple will be able to retain and make

repeat product sales to these corporations and educationalinstitutions in the long term. Perhaps the brightest piece of news from Apple’s earningsreport was that CEO Tim Cook reiterated that Apple wouldlaunch new products in multiple product categories duringthe 2014 calendar year. We still view Apple’s innovation,and the potential for new products, as possible catalysts forfuture increases to our fair value estimate. We have nospecial insight into Apple’s product pipeline, but continueto suspect that an iWatch may arrive before a TV, simplybecause Apple could likely bring a wearable device tomarket quicker than a TV, which would require a much morecomplex network of support from cable and contentproviders. We also hope that Apple is not lumping its brieflydiscussed "iOS in the car" software platform into thisdiscussion as a new device category. We’re not quiteconvinced that it will become a revolutionary interfacecapable of driving meaningful profitability. For the December quarter, iPhone sales of 51 million unitsreflects a 7% jump from the year-ago quarter. However,given the NTT DoCoMo launch, the initial sales into Chinain the December quarter versus the March quarter a yearago, and the bright data point of nine million units soldduring Apple’s initial weekend launch, this figure is stillmodestly below our expectations. Apple noted that NorthAmerican sales contracted year over year, as some U.S.carriers extended their upgrade terms to full 24 monthcontracts, rather than allowing customers to upgrade early.Sales in Japan did well, thanks to the NTT DoCoMopartnership, although a soft Japanese yen provided somecurrency headwinds. Apple did cite tremendous growth insome emerging market regions like Latin America andEastern Europe, although we suspect such growth is off ofrelatively small bases. Given Kantar World Panel’s recentmarket share data, market share losses in Western Europemay have offset some of this growth.

Page 14 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

Analyst Notes

The iPhone's ASPs of $637 were quite encouraging, but inline with our expectations, and not terribly surprising givenApple’s premium pricing approach. The firm did concedethat its iPhone product mix skewed toward the more-advanced iPhone 5s, which caught the firm a bit by surprisein terms of supply, but is a long-term positive for thecompany’s pricing power and, perhaps, the adoption andpopularity of new iPhone features like Touch ID. The iPad's unit sales of 26 million were up 14% from theyear-ago quarter, although sales were up only 5% whenlooking at iPads sold through to end customers (rather thanto retailers). Flat ASPs of $440 per device were discouraging,given a price increase for the new iPad Mini with Retina to$399. Apple noted that iPad sales in mainland China doubledfrom the year-ago quarter, which we think led to a lessfavorable iPad mix toward older models like the original iPadMini and iPad 2, or perhaps a trade down to the smaller iPadMini with Retina versus the larger iPad Air. Finally, looking at Apple’s financial results, the firmgenerated net income of $13.1 billion, identical with theyear-ago period despite 6% revenue growth year-over-year.Gross margin compression of 70 basis points and a 32%spike in R&D expenses offset the revenue boost. Wecontinue to model relatively flattish EPS ($42 to $44 pershare in each of the next five years, adjusted for sharerepurchases) in the long-term due to a similar dynamic,where modest revenue growth is mostly offset by modestgross margin compression and additional R&D spending.EPS growth in the quarter to $14.50, versus $13.81 a yearago, was driven entirely by stock buybacks, as Apple boughtback another $5 billion worth of its shares in the Decemberquarter, and $28 billion cumulatively in the past fivequarters. We'd like to see Apple continue with its $60 billionstock repurchase plan as-is before considering any otheroutside requests to boost its authorization.

Early China Mobile iPhone Demand Appears In Line With

Our Expectations; Maintain Our FVE 15 Jan 2014

We will maintain our $600 fair value estimate and narrowmoat rating for Apple. A couple of data points emerged frominterviews with Apple CEO Tim Cook and China Mobilechairman Xi Guohua about Apple's official iPhone launchwith the carrier, beginning Friday. Various news reports havehinted that iPhone pre-orders at China Mobile (from Dec.25, 2013 through today) have reached 1.2 million-1.4 million,while Xi commented that pre-orders are in the "millions."These estimates fall within the range of our expectations,as we continue to project that iPhone sales in calendar 2014will double from 2013, mostly because of the China Mobiledeal as well as from ongoing growth with China's other twocarriers. We continue to project that Apple's Decemberrevenue will exceed the firm's previously announcedguidance of $55 billion-$58 billion and that this ChinaMobile partnership will enable the firm to recognize solidyear-over-year revenue growth in the upcoming Marchquarter as well.

Cook also disclosed, ahead of the firm's earningsannouncement on Jan. 27, that the company saw recordiPhone unit sales in Greater China in the December quarter.This comment is also in line with our expectations, givenApple's ongoing momentum in the region and because thefirm launched new iPhones in China at the same time as therest of the world, as opposed to prior years when Chinawould receive Apple's latest phones on a three-month lag.Finally, Xi hinted at "broad" collaboration between the twocompanies that extends beyond handsets, but at this point,we dismiss these comments as we suspect that it hints atthe sale of iPads and other Apple products through ChinaMobile's sales channels.

IPhone Will Finally Arrive at China Mobile on Jan. 17;

Maintaining Our Fair Value Estimate 23 Dec 2013

Page 15 of 29

SAMPLE

Morningstar Equity Research

© Morningstar 2014. All Rights Reserved. Morningstar's Credit Ratings & Research is produced and offered by Morningstar, Inc., which is not registered with the U.S. Securities and Exchange Commission as a Nationally Recognized Statistical Rating Organization(“NRSRO”). Unless otherwise provided in a separate agreement, you may use this report only in the country in which its original distributor is based. The information, data, analyses and opinions presented herein do not constitute investment advice; are providedsolely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. The opinions expressed are as of the date written and are subject to change without notice. Except as otherwiserequired by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property ofMorningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar. To order reprints, call +1 312-696-6100. To license the research, call +1 312-696-6869.

Last Price Fair Value Consider Buy Consider Sell Uncertainty Economic Moat™ Moat Trend™ Stewardship Morningstar Credit Rating Industry Group

541.65 USD 570.00 USD 342.00 USD 883.50 USD High Narrow Positive Standard AA- Computer Hardware

Apple Inc AAPL (NAS) | QQQ

Analyst Notes

We're maintaining our $600 fair value estimate and narroweconomic moat rating for Apple after it formally announcedits long-awaited partnership with China Mobile. The iPhonewill go on sale Jan. 17, 2014, with preorders beginning Dec.25. Specific product pricing and availability has not beenannounced, but we don't anticipate a significant differencein Apple’s product lineup at China Mobile compared withother carriers.

We're encouraged, but not especially surprised, that thepartnership was announced before the critical Chinese NewYear holiday season, and we suspect that the deal couldprovide some upside to Apple’s revenue forecast for theMarch quarter, which should be discussed in late January.We continue to view the greater China region, and a ChinaMobile partnership, as the single most important catalystfor iPhone unit sales growth in fiscal 2014. Between theChina Mobile partnership and growth at China Unicom andChina Telecom, we project that Apple’s iPhone unit sales infiscal 2014 in China will essentially double from fiscal 2013.