Apex Capital, LLC - Why Netflix Will Be The Next $100 Billion Internet Company

10

Why Netflix Will Be The Next $100 Billion Internet Company Gil Simon │ May 7, 2015

-

Upload

aj9432 -

Category

Economy & Finance

-

view

4.330 -

download

1

Transcript of Apex Capital, LLC - Why Netflix Will Be The Next $100 Billion Internet Company

Why Netflix Will Be The Next $100 Billion

Internet Company

Gil Simon │ May 7, 2015

2

This presentation is being furnished to you on a confidential basis to provide information and analysis. The material presented is for general discussion, illustration and informational purposes only. The opinions expressed herein are based on the current judgment and opinions of Apex Capital, LLC as of 05/05/2015 and are subject to change without notice. References herein to future revenues, earnings or share prices of Netflix, Inc. are included for discussion purposes only and should not be construed as predictions. Actual revenues, earnings or share prices could differ materially from those shown herein. Although the information shown was prepared using sources, models and data believed to be reasonably reliable, its accuracy and completeness cannot be guaranteed, and Apex assumes no responsibility or liability for any of the information herein.

Apex Capital, LLC is an investment advisory firm that serves as the investment manager of investment funds. As of the date of this presentation, those funds currently own common shares of Netflix, Inc. The material presented is not to be construed as investment advice or as a solicitation to invest in any security, or, directly or indirectly, as a solicitation (on behalf of Apex Capital, LLC or another party) to act as proxy for a security holder or any form of consent or authorization. This Presentation does not constitute an offer to sell or a solicitation of an offer to buy any interests in any Apex Capital, LLC funds. Any offer or solicitation may be made only by the confidential offering memorandum of each fund which may be obtained from the funds’ administrator Citco.

Additional information about Apex Capital, LLC is available from the firm and in its disclosure documents that are available on the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

This presentation may not be excerpted from, summarized, distributed, reproduced or used for any purpose without the written consent of Apex Capital, LLC.

Disclaimer

Netflix: Proving the Naysayers WrongWhy NFLX could be a $2,000 stock

Bears Say…

NFLX is a niche service facing significant competition

Already one of the world’s largest media subscription services, NFLX is watched 10-20x more than its closest competitors

Content producers have all the leverage while NFLX is just a distributor ripe to be squeezed

International growth will disappoint due to entrenched competition and differing media consumption habits

NFLX is a great service, but its financial results will never justify its current price

NFLX’s global scale and growing checkbook positions it as the buyer of choice for premium licensed and original content

The desire to consume Hollywood content is universal, and strong adoption in its early international markets has given NFLX the confidence to accelerate its global rollout

The company’s global subscription model along with eventual pricing power will translate into profitability well beyond consensus expectations

Says…

NFLX is an overvalued content distributor with too many competitors to meet lofty expectations

NFLX is quickly becoming one of the most powerful media companies in the world

We expect global subscribers to approach 150m by 2020

NFLX Has Tripled Its Subscriber Base in 3 Yrs.

Streaming Subscribers (millions)

2012 2013 2014 2015 2016 2017 2018 2019 2020

0

25

50

75

100

125

150 Projected International

Projected Domestic

Already watched by ~45% of U.S. broadband households! Source: Company filings and Apex projections

Global Rollout Continues to RampManagement expects international to eventually represent 2/3 of total subscribers

Canada

2010

Latin America

2011

Australia New ZealandJapan (Q3)

20152013

Netherlands Germany France Austria Belgium Switzerland Luxembourg

2014

UKIrelandFinlandDenmarkSwedenNorway

2012

International expansion expected to be largely complete by YE2016

2016

ROW

6

Netflix is Already The Scaled OTT Provider

Viewed 14x more than closest OTT competitor…

…and 10x more than HBO at a fraction of the price

Share of U.S.

downstream traffic in

peak evening hours1

Minutes watched

per household

per day2

1. Sandvine 2H 2014 Global Internet Phenomena; 2. Rentrak Q1 2015 data; 3. Amazon Prime annual rate on a monthly basis; 4. HBOGo free with linear subscription

Price/Mo: $8.99 $8.253 $7.99 $14.994

2.6%1.4% 1.0%

34.9%

Price/Mo: $8.99 $14.99

111

12

14x 10x

7

2015+

2014

2013

Content is King And Netflix has become the new kingmaker

2012

8

Consumers Already Love Netflix…

57% of the nearly 800 Netflix users queried said that, if forced to choose, they would keep Netflix over traditional pay TV; 49% reported spending more time watching Netflix than traditional pay TV.

- From ClearVoice/FBR Survey Says Consumes Love It More Than TV by Barton Crockett, FBR 4/16/2015

Netflix is the 5th most popular network … [and] is now considered a must have channel right behind most broadcast channels and ESPN.

- From A Proprietary Service of “Must See” TV by Marci Ryvicker, Wells Fargo 3/11/2015

And the service is only getting better

9

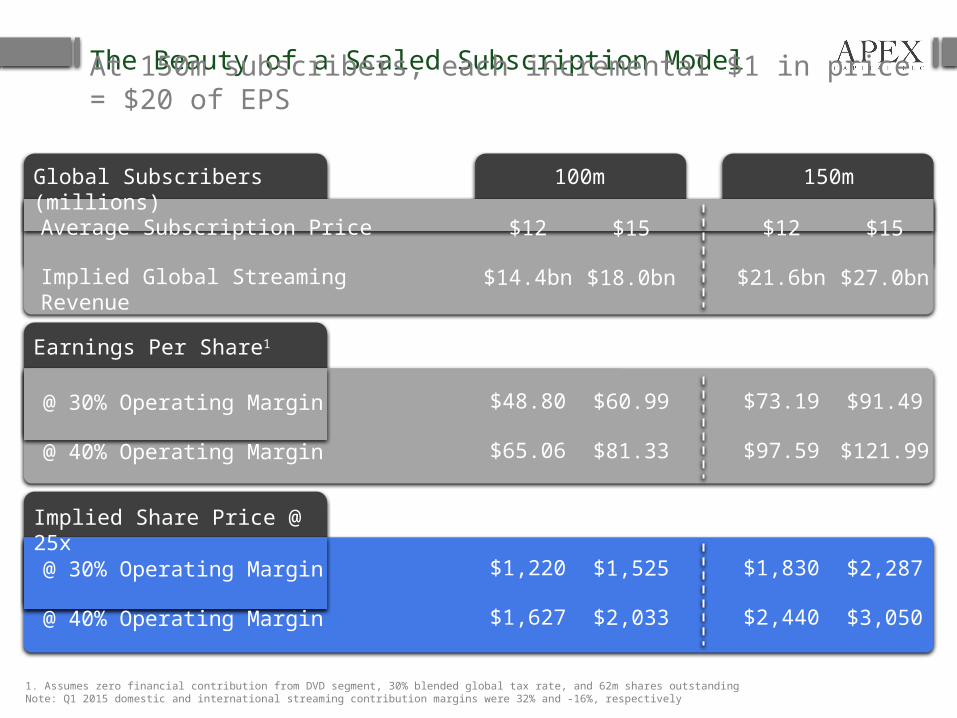

The Beauty of a Scaled Subscription Model

Global Subscribers (millions) 100m 150m

Average Subscription Price

Implied Global Streaming Revenue

$12

$14.4bn

$15

$18.0bn

$12

$21.6bn

$15

$27.0bn

Earnings Per Share1

$48.80

$65.06

$60.99

$81.33

$73.19

$97.59

$91.49

$121.99

@ 30% Operating Margin

@ 40% Operating Margin

$1,220

$1,627

$1,525

$2,033

$1,830

$2,440

$2,287

$3,050

@ 30% Operating Margin

@ 40% Operating Margin

Implied Share Price @ 25x

1. Assumes zero financial contribution from DVD segment, 30% blended global tax rate, and 62m shares outstandingNote: Q1 2015 domestic and international streaming contribution margins were 32% and -16%, respectively

At 150m subscribers, each incremental $1 in price = $20 of EPS

3-Year NFLX Price Target: $2,000

“PAY ATTENTION TO THE FINE

PRINT, IT’S FAR MORE

IMPORTANT THAN THE

SELLING PRICE”- Frank Underwood

PAY ATTENTION TO THE FUNDAMENTALS, THEY SHOW FAR MORE OPPORTUNITY THAN THE CURRENT SHARE

PRICE