“LNG: A fast track solution to meet South Africa’s Energy ... · CCGT: gas-fired power compared...

18

“LNG: A fast track solution to meet South Africa’s Energy needs” 1 Port Elizabeth Mosselbay Western Cape Eastern Cape Kwazulu-Natal Limpopo Gauteng Northern Cape North West Free State Mpumalanga Lesotho Richards Bay Durban East London Johannesburg Fossil Fuel Foundation Gas Conference Johannesburg , May 21 2014

Transcript of “LNG: A fast track solution to meet South Africa’s Energy ... · CCGT: gas-fired power compared...

“LNG: A fast track solution to meet South Africa’s Energy needs”

1

Port ElizabethMosselbay

Western Cape

Eastern Cape

Kwazulu-Natal

Limpopo

Gauteng

Northern Cape

North West

Free State

Mpumalanga

LesothoRichards Bay

Durban

East London

Johannesburg

Fossil Fuel Foundation Gas ConferenceJohannesburg , May 21 2014

CAUTIONARY NOTE

The companies in which Royal Dutch Shell plc directly and indirectly owns investments are separate entities. In this presentation“Shell”, “Shell group” and “Royal DutchShell” are sometimes used for convenience where references are made to Royal Dutch Shell plc and its subsidiaries in general. Likewise, the words “we”, “us” and “our”are also used to refer to subsidiaries in general or to those who work for them. These expressions are also used where no useful purpose is served by identifying theparticular company or companies. ‘‘Subsidiaries’’, “Shell subsidiaries” and “Shell companies” as used in this [report] refer to companies over which Royal Dutch Shell plceither directly or indirectly has control. Companies over which Shell has joint control are generally referred to “joint ventures” and companies over which Shell hassignificant influence but neither control nor joint control are referred to as “associates”. In this presentation, joint ventures and associates may also be referred to as “equity-accounted investments”. The term “Shell interest” is used for convenience to indicate the direct and/or indirect (for example, through our 23% shareholding in WoodsidePetroleum Ltd.) ownership interest held by Shell in a venture, partnership or company, after exclusion of all third-party interest.

This presentation contains forward-looking statements concerning the financial condition, results of operations and businesses of Royal Dutch Shell. All statements otherthan statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements are statements of future expectations that arebased on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance orevents to differ materially from those expressed or implied in these statements. Forward-looking statements include, among other things, statements concerning thepotential exposure of Royal Dutch Shell to market risks and statements expressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions.These forward-looking statements are identified by their use of terms and phrases such as ‘‘anticipate’’, ‘‘believe’’, ‘‘could’’, ‘‘estimate’’, ‘‘expect’’, ‘‘goals’’, ‘‘intend’’, ‘‘may’’,‘‘objectives’’, ‘‘outlook’’, ‘‘plan’’, ‘‘probably’’, ‘‘project’’, ‘‘risks’’, “schedule”, ‘‘seek’’, ‘‘should’’, ‘‘target’’, ‘‘will’’ and similar terms and phrases. There are a number of factorsthat could affect the future operations of Royal Dutch Shell and could cause those results to differ materially from those expressed in the forward-looking statementsincluded in this [report], including (without limitation): (a) price fluctuations in crude oil and natural gas; (b) changes in demand for Shell’s products; (c) currencyfluctuations; (d) drilling and production results; (e) reserves estimates; (f) loss of market share and industry competition; (g) environmental and physical risks; (h) risksassociated with the identification of suitable potential acquisition properties and targets, and successful negotiation and completion of such transactions; (i) the risk of doingbusiness in developing countries and countries subject to international sanctions; (j) legislative, fiscal and regulatory developments including regulatory measuresaddressing climate change; (k) economic and financial market conditions in various countries and regions; (l) political risks, including the risks of expropriation andrenegotiation of the terms of contracts with governmental entities, delays or advancements in the approval of projects and delays in the reimbursement for shared costs;and (m) changes in trading conditions. All forward-looking statements contained in this [report] are expressly qualified in their entirety by the cautionary statementscontained or referred to in this section. Readers should not place undue reliance on forward-looking statements. Additional risk factors that may affect future results arecontained in Royal Dutch Shell’s 20-F for the year ended December 31, 2013 (available at www.shell.com/investor and www.sec.gov ). These risk factors also expresslyqualify all forward looking statements contained in this presenation and should be considered by the reader. Each forward-looking statement speaks only as of the date ofthis presentation, May 21 2014. Neither Royal Dutch Shell plc nor any of its subsidiaries undertake any obligation to publicly update or revise any forward-lookingstatement as a result of new information, future events or other information. In light of these risks, results could differ materially from those stated, implied or inferred fromthe forward-looking statements contained in this presentation.

We may have used certain terms, such as resources, in this [report] that United States Securities and Exchange Commission (SEC) strictly prohibits us from including inour filings with the SEC. U.S. Investors are urged to consider closely the disclosure in our Form 20-F, File No 1-32575, available on the SEC website www.sec.gov. Youcan also obtain this form from the SEC by calling 1-800-SEC-0330.

THE CASE FOR GAS

Abundant global gas resources, growing and geographically diverse Conventional and unconventional recoverable gas resources can supply >250 years of current global gas production

CCGT: gas-fired power compared to coal:n 30% more energy

efficientn Emit around half the CO2

n CCS retrofit at similar cost per MWh

n Better complement to wind power

Replacing coal with gas for electricity generation is the cheapest and fastest way to meet CO2 reduction targets

CCGT cheapest to build

Similar total cost to coal and nuclear

ABUNDANT ACCEPTABLE AFFORDABLE

CCGT: Combined Cycle Gas TurbineTotal Cost = Capital + Fuel + Operating

Source: DECC (Mott MacDonald) June 2010

CCS: Carbon Capture & Storage

CAPITAL COST TOTAL COSTS

Source: IEA World Energy Outlook, WoodMackenzie, Shell Interpretation

North America

South America

Europe Eurasia

Middle East

Africa Asia Pacific

Conventional Gas ResourcesUnconventional Gas Resources

0 100 200 300

CCGT

Coal

Nuclear

Wind Onshore

Wind Offshore (25km)

Wind Offshore (75 km)

USD/MWh

SHARE OF GAS IN PRIMARY ENERGY MIX

THE SHARE OF NATURAL GAS IN THE PRIMARY ENERGY MIX IS EXPECTED TO INCREASE IN THE 3 LARGEST GAS MARKETS (MODERATE INCREASE IN OECD)

Source: WoodMac for USA and Europe, WoodMac and Shell analysis for China

USA EUROPE CHINA

OthersCoalNatural Gas Oil

2010 2030 2010 2030 2010 2030

~16,000~19,500

~14,000~16,000 ~17,000

~31,000Total primary energy (mln boe)

16%

38%

24%

22%

20%

33%

23%

24%

23%

36%16%25%

28%

31%

13%

28%

13%17%

66%

4%

14%

25%

51%

10%

LNG A FAST TRACK SOLUTION FOR SOUTH

AFRICA

WHAT IS LNG?

WORLD LNG PRODUCTION IN 2013 = ~242 MILLION TONNES

n Natural Gas production and separation from oil and water (when present)

n Natural Gas cooled to liquid state at -160oC and atm. pressure(volume reduced 600 fold)

n LNG transported over long distances in purpose built carriers

n LNG returned to gas state and injected into the transport pipeline network for distribution and sales

Source: Gas Matters

PRODUCTION LIQUEFACTION SHIPPING REGASIFICATION

COST EFFECTIVE ALTERNATIVE TO PIPELINE FOR DISTANCE > ~3000 KM

Copyright of Royal Dutch Shell plc

LNG DEMAND AND SUPPLY GROWTH

LNG DEMAND (mtpa) LNG SUPPLY (mtpa)

§ LNG demand will grow at ~5% pa doubling in size in the period 2010 to 2020

Source: Shell Analysis

0

100

200

300

400

500

600

2000 2005 2010 2015 2020 20250

100

200

300

400

500

600

2000 2005 2010 2015 2020 2025

India

Japan/ Korea/ Taiwan SE AsiaChina Europe

AfricaAustraliaAsia

MENACIS / Europe

Other AmericasQatar

GLOBAL LNG MARKET DEVELOPMENTS

LNG IMPORTERSLNG EXPORTERS

2010 2020

NUMBERS OF COUNTRIES IMPORTING LNG EXPECTED TO ALMOST DOUBLE BETWEEN 2010 AND 2020

#COUNTRIES 1990 2000 2010 2011* 2020 EST

EXPORTERS 8 12 18 18 ~25

IMPORTERS 9 11 24 25 ~40

Source: Wood Mackenzie LNG (April 2010)

* Source: PFC Energy (2011 Actuals)

SHELL’S GLOBAL LNG LEADERSHIP

Shell Global LNG Growth

Shell LNG Leadership

2013 ~2020+2007

Under constructionOptions

On streamRepsol LNG acquisition

2014

2013

2017Repsol acquisition (Jan 2014)

Copyright of Royal Dutch Shell plc

PLUTO (WOODSIDE)*

SAKHALIN II

MALAYSIA LNGBRUNEI LNG

NORTH WEST SHELF

* Indirect interest

QATARGAS 4 OMAN LNGQALHAT*NIGERIA LNG GORGON LNGPRELUDEWHEATSTONE

SHELL’S GLOBAL LNG PORTFOLIO

LNG - OPERATION

LNG - CONSTRUCTION

REGAS POSITION - OPERATION

EXPORT

SPAINHAZIRABAJA DUBAIELBA ISLANDALTAMIRA COVE POINTACC

ESS

TO K

EY

STR

ATEG

IC

M

ARKE

TS

ARKAT

SHIPPING

GREEN CORRIDOR

LNG FOR TRANSPORT

Copyright of Royal Dutch Shell plc

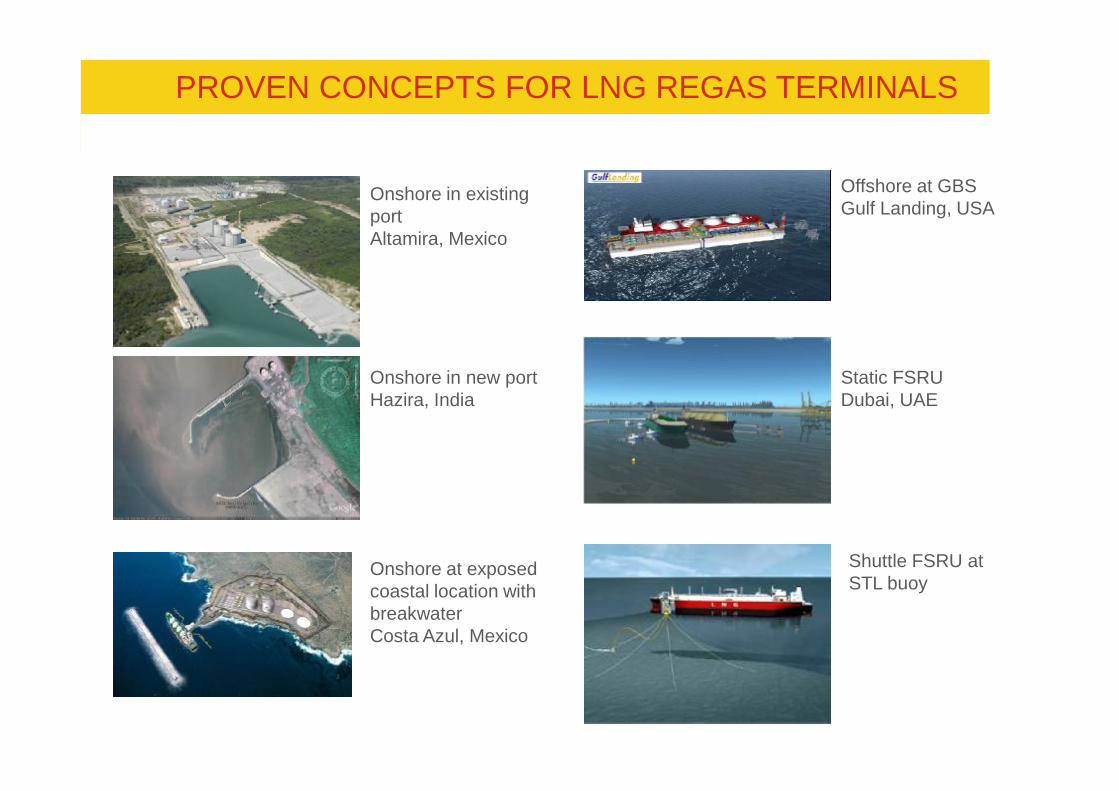

PROVEN CONCEPTS FOR LNG REGAS TERMINALS

Onshore in existing portAltamira, Mexico

Shuttle FSRU at STL buoy

Offshore at GBSGulf Landing, USA

Static FSRU Dubai, UAE

Onshore in new portHazira, India

Onshore at exposed coastal location with breakwaterCosta Azul, Mexico

Copyright of Royal Dutch Shell plc

DUBAI LNG – CAN RSA REPLICATE THIS MODEL?

Fully funded and owned by DUSUP (government company owning the gas pipeline grid)Offshore floating terminal – capacity 3 mtpa (400 mmscfd). LNG supplied on an ex-ship basisEnd gas consumers are Dubai government owned power generation and industrial customersShell provides critical value through:

— Fixed supply terms: 15 years (take or pay) and all of the contracted volume and rights to supply spot volumes

— Independent Technical Advisory Role— Initial design— Master Service Agreement from Shell to cover project

management, construction and execution — Operational support for first year (Golar operates the FSRU

and DUSUP operates the marine facilities)— Logistics support for future cargos purchases— Cost estimates for site/ port development and FSRU leased at

a day charter rate

TIMELINE

First engagements: Feb 2006

Selection of technical solution: Aug 2006

FSRU tendering start: Jun 2007

Comm. agreements: Jun 2007 to Apr 2008

SPA negotiations: Nov 2007 to Apr 2008

Investment decision: May 2008

Marine Const. Start: Jun 2009 – Oct 2010

FSRU conversion: Aug 2009 – Apr 2010

Commercial Start Up: Q4 2010

Copyright of Royal Dutch Shell plc

OVERVIEW FSRU GLOBAL MARKET

*Source IHS Report April 2014

Copyright of Royal Dutch Shell plc

POTENTIAL LNG DEMAND NODES

ANKERLIG OCGTCapacity: 1350 MWDate Commissioned: 2009Fuel type: Diesel Alt: KeroseneLocation: Atlatntis Industrial

Park, Western Cape

Mossel Bay

New CCGT IPP @ Richards Bay??

ACACIA OCGTCapacity: 171 MWDate Commissioned: 1976Fuel Type: Distillate Alt: NoneLocation: Goodwood, Western

Cape

GOURIKWA OGCTCapacity: 740 MWDate Commissioned: 2007Fuel Type: Kerosene Alt: Location: Mossel Bay, Western Cape

Cape Town

Saldanha

New CCGT IPP @ COEGA??Port Elizabeth

Western Cape

Eastern Cape

Kwazulu-Natal

Limpopo

Gauteng

Northern Cape

North West

Free State

Mpumalanga

Lesotho Richards Bay

Durban

East London

Johannesburg

GTL PlantCapacity: ca 1.5 Mtpa LNGFuel Type: Indigenous

condensateLocation: Mossel Bay, Western

Cape

Saldanha Bay

New CCGT IPP 2.0 GW @ SALDANHA?

CHALLENGES TO DEVELOP A LNG PROJECT IN SOUTH AFRICA

Lack of natural gas and LNG infrastructureRSA needs a coordinated approach to gas developments and gas strategy is required: GUMP a key elementDecision Making Process: Fast track decision making required for Fast Track LNG implementation Fine tuning of current regulatory legislation underwayProject Structuring: Integrated vs Segregated LNG to Power Value Chain

WHY PARTNER WITH AN EXPERIENCED LNG PLAYER

Proven track record of delivering LNG import projectsDeep understanding of the technical and commercial requirements are needed to develop a LNG importation project. Financial strength will be required to help finance the LNG projectWill enable local state/private companies to benefit from the transfer of technical/operations expertise Provides security of supply by having a diverse LNG supply portfolio

Copyright of Royal Dutch Shell plc

BENEFITS OF LNG IMPORTS FOR RSA

n Robust LNG supply market provides security of supplynFast track implementation (36 to 48 months) to produce powernProvides competitive base load Power GenerationnReplaces expensive diesel power generation and meets industrial

demandnComplements existing and future renewable power generationnCheapest power technology to meet RSA’s CO2 reduction targetsnDevelops the natural gas infrastructure and industrial markets ahead of

domestic natural gas production (offshore/shale gas)