“Leistungshonorierung in der Financial Services Industry” Tangible actual results Expectations /...

44

1 © finval 2010 Universität St. Gallen IC – 06.05.2010 Thomas Wähling finval Mühlebachstrasse 64, CH-8008 Zürich www.finval.ch “Performance Management in der Financial Services Industry” Vorlesung an der Universität St. Gallen, 2010 “Leistungshonorierung in der Financial Services Industry” 06. Mai 2010

Transcript of “Leistungshonorierung in der Financial Services Industry” Tangible actual results Expectations /...

1

© finval 2010

Universität St. GallenIC – 06.05.2010

Thomas Wähling

finvalMühlebachstrasse 64, CH-8008 Zürich

www.finval.ch

“Performance Management in der Financial Services Industry”Vorlesung an der Universität St. Gallen, 2010

“Leistungshonorierung in der Financial Services Industry”

06. Mai 2010

2

© finval 2010

Universität St. GallenIC – 06.05.2010

Agenda

Getting started Basics of Incentive Compensation Design

– Components & Focus– Function & Scope– Funding– Allocation– Instruments– Vesting / Blocking– Payout

Wrap-up: Topics to be considered in Incentive Compensation design

3

© finval 2010

Universität St. GallenIC – 06.05.2010

What they should focus on …(highly simplified - illustrative only)

Sell-side analystsInvestors:

get TSR in line with risk profile of investment

Competitors

Shareholders’ Assembly:represent investors’ interests

Board of Directors:define & monitor strategy, protect

investors’ assets

Front units:advise & sell, according to clients’ best

interests

Product units:generate and manage performing

products

Non-Front units: Control & enable

ClientsMarkets

Executive Board:ensure sustainable value creation (EP),

manage operations

Provide meaningful financial analysis Compete for markets, resources & clients

Risk-return-oriented advice / products & services, based on

client needs & profile

Develop profitable markets & use scarce resources

appropriately

4

© finval 2010

Universität St. GallenIC – 06.05.2010

What they are usually interested in …(highly simplified - illustrative only)

Sell-side analysts Investors:maximize TSR Competitors

Shareholders’ Assembly:maximize TSR

Board of Directors:maximize TSR & compensation, while

minimizing own liability risks

Front units:maximize revenue-driven compensation

Product units:maximize product-driven compensation

Non-Front units: maximize profit-driven compensation

ClientsMarkets

Executive Board:maximize profit-driven compensation,

while maintaining control

Generate transactions Outperform competitors

Maximize revenuesMaximize volumes in order to justify business cases

5

© finval 2010

Universität St. GallenIC – 06.05.2010

What they focus on in practice “from time to time” …(highly simplified - illustrative only)

Sell-side analysts Competitors

Shareholders’ Assembly:Short-term (backward) focus,

“political game”

Board of Directors:Personal liability / do not lose reputation / represent individual investors’ interests

Front units:Maximize volumes & revenues

Product units:Maximize product range & focus on

(relative) performance

Non-Front units: “Enable” ExB priorities & do not get

penalized vs. Front units

ClientsMarkets

Executive Board:Maximize profits in the short run

(expectations, management turnover, …)

“Grey” does not sell …

Product Push & Churn, inappropriate consideration of

risks, etc.

Inappropriate consideration of risks – “size first!”

Relative outperformance (only …)

Investors:Short-term profits

6

© finval 2010

Universität St. GallenIC – 06.05.2010

Potential conflict areas & Incentive Compensation Design (illustrative examples)

Shareholders / Owners

Corporate interests

Use of invested capital Risk taking & relevant time horizon Gambling for resurrection “Cook the Books” Asymmetric compensation Diverging interests among shareholder “categories”!

“Business Areas” / Employees

Growth through doubtful NNA / volumes Churn / “product push” (inducements) Anti-tying Best execution, mispricing, … Dual roles, etc.

Tangible actual results Expectations / “vested rights” / competitive pay Long-term focus Mostly short-term focus Top-down funding (corporate perspective) Bottom-up funding (individual / team / area perspective) Allocation according to tangible results / contribution Allocation according to contribution / perceived value Sound mix of compensation instruments (depending on roles) “Cash is king …”, unless there is additional leverage Payout if results confirmed in the longer run (sustainability) “Once in the pocket …” Hire & retain by forward-looking components “Sign-in-bonus” / “Pay me to retain me …” Honor agreements, but do not invest in leaving people “Golden parachutes”

ClientsMarkets

Investment priorities “Hockey stick” business cases vs. “don’t

reduce the bottom line” Expectations management &

risk taking

7

© finval 2010

Universität St. GallenIC – 06.05.2010

Empiric research used for illustration purposes:Incentive Compensation Survey 2010 - Ukrainian Banks

Survey Responses2010

8

© finval 2010

Universität St. GallenIC – 06.05.2010

Agenda

Getting started Basics of Incentive Compensation Design

– Components & Focus– Function & Scope– Funding– Allocation– Instruments– Vesting / Blocking– Payout

Wrap-up: Topics to be considered in Incentive Compensation design

9

© finval 2010

Universität St. GallenIC – 06.05.2010

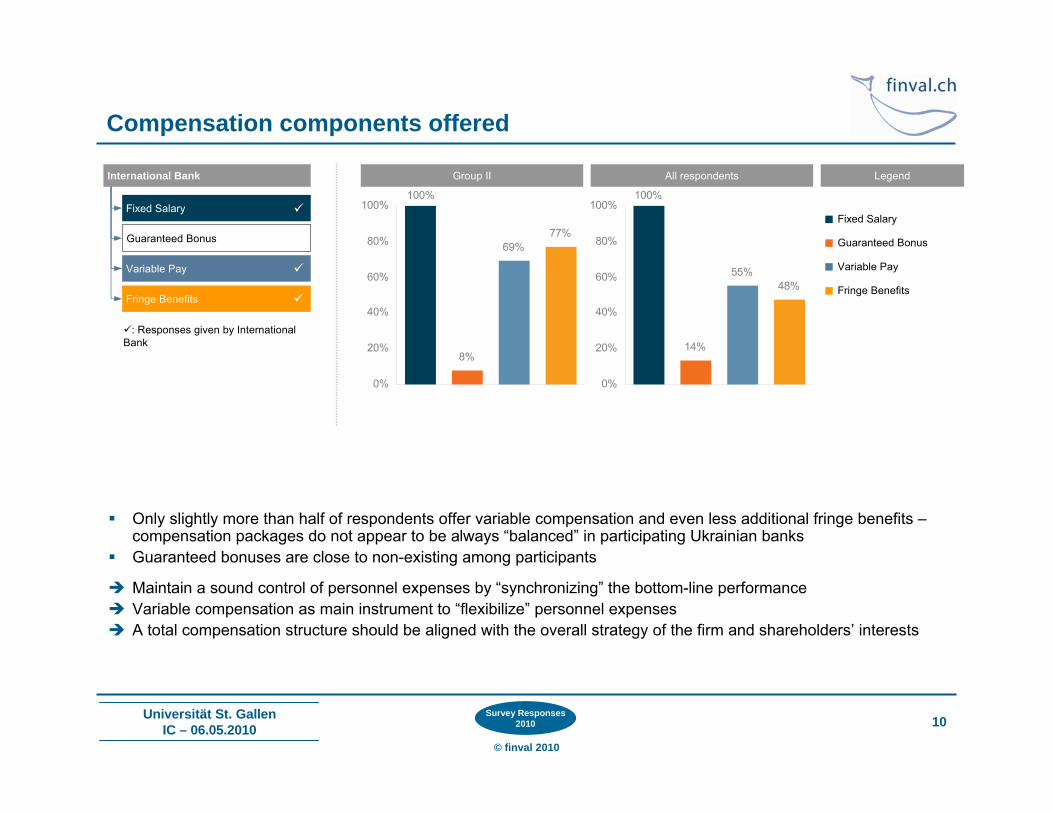

Total Compensation – Components

Base Salary

Critical issues:1. Optimal mix between Fixed (Base Salary) & Variable Pay per eligible person, depending on role & function?2. “Competitive Pay” is usually based on a “Total Compensation” perspective, thus including “variable pay” and

converting the latter into an “expected component”, instead of a purely performance-based variable!

Variable Pay

Fringe Benefits

Focus is on Function, Position, Responsibility:− Pay for generally expected contribution to firm− Compensate in line with market & firms’ compensation structure

Focus is on „Pay for Performance“:− Compensate overall company performance− Consider contribution of business unit / individual (business

model)− Basis: key performance indicators, in line with company interests

Offer additional incentives for employees to consider company „employer of choice“: e.g., additional insurance, transportation, training, ...

In designing Incentive Compensation

programs, „Total Compensation“ is a

key parameter („package“ view)

10

© finval 2010

Universität St. GallenIC – 06.05.2010

69%77%

100%

8%

0%

20%

40%

60%

80%

100%

55%48%

100%

14%

0%

20%

40%

60%

80%

100%

Compensation components offered

Only slightly more than half of respondents offer variable compensation and even less additional fringe benefits –compensation packages do not appear to be always “balanced” in participating Ukrainian banks

Guaranteed bonuses are close to non-existing among participants

Maintain a sound control of personnel expenses by “synchronizing” the bottom-line performance Variable compensation as main instrument to “flexibilize” personnel expenses A total compensation structure should be aligned with the overall strategy of the firm and shareholders’ interests

Fixed Salary

Guaranteed Bonus

Variable Pay

Fringe Benefits

International Bank Group II All respondents

Fixed Salary

Guaranteed Bonus

Variable Pay

Fringe Benefits

Legend

: Responses given by International Bank

Survey Responses2010

11

© finval 2010

Universität St. GallenIC – 06.05.2010

Focus of Incentive Compensation Design

Shareholders / Owners

IC design in Financial Institutions should exclusively focus on long-term and sustainability oriented investors’ interests!

The IC design determines the amount – focus on design!

IC design should not conflict with “sound business” rules nor create incentives to increase business-intrinsic risks!

Function & scope of program Funding Allocation Instruments Vesting / Blocking Payout Entry / Exit / Forfeiting rules

Incentive Compensation design parameters need to be considered as a system

– focusing on individual components only will lead

to inconsistencies!

Simplicity Motivation Alignment Retention Transparency … and Cost!

ClientsMarkets

IC design should set the right incentives to promote sound investment decisions and “unpopular” decision making, if required!

IC Design parameters IC Design valuation criteria

12

© finval 2010

Universität St. GallenIC – 06.05.2010

Agenda

Getting started Basics of Incentive Compensation Design

– Components & Focus– Function & Scope– Funding– Allocation– Instruments– Vesting / Blocking– Payout

Wrap-up: Topics to be considered in Incentive Compensation design

13

© finval 2010

Universität St. GallenIC – 06.05.2010

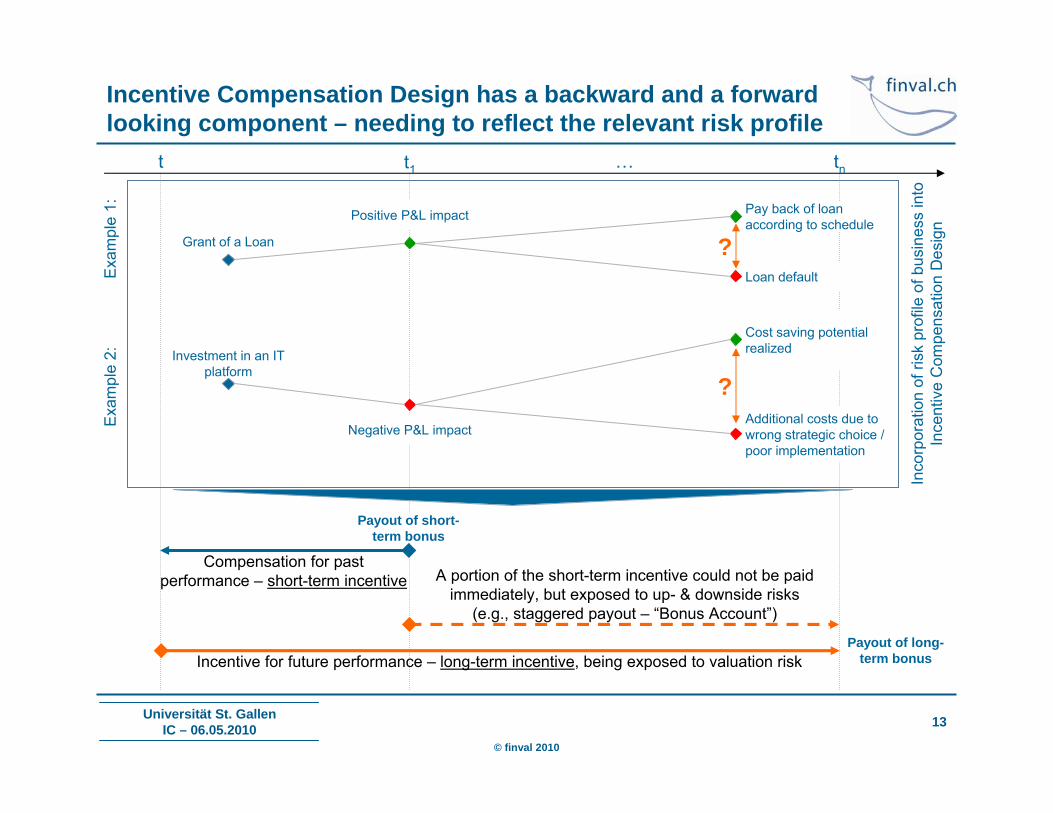

Incentive Compensation Design has a backward and a forward looking component – needing to reflect the relevant risk profile

t t1 tn

Compensation for past performance – short-term incentive

Payout of short-term bonus

Payout of long-term bonus

A portion of the short-term incentive could not be paid immediately, but exposed to up- & downside risks

(e.g., staggered payout – “Bonus Account”)

Exa

mpl

e 1:

Grant of a Loan

Positive P&L impact Pay back of loan according to schedule

Loan default

Exa

mpl

e 2: Investment in an IT

platform

Negative P&L impact

Cost saving potential realized

Additional costs due to wrong strategic choice / poor implementation

?

?

Inco

rpor

atio

n of

risk

pro

file

of b

usin

ess

into

In

cent

ive

Com

pens

atio

n D

esig

n

Incentive for future performance – long-term incentive, being exposed to valuation risk

…

14

© finval 2010

Universität St. GallenIC – 06.05.2010

Incentive Compensation Design & Risk

Risk profile of current business

Materialized risk Non-anticipated risk

Incurred losses

Economic profit

Risk weighted assets

Allocated capital

Cost of equity (%) applied to capital

Anticipated risk

Provisions and impairments (fair value adjustments)

Risk-adjustments reflect only realized / anticipated risk in the

short run

How Do you integrate a long-term perspective in

your incentive compensation design?

Backward looking Forward looking

Business exposure ValuationPricing / Valuation Business exposure

P&L P&L

Extension of time horizon needed in order to cope with shortcomings of performance measurement – incentive for sustainable performance in the long run (reflection of

long-term consequences of short-term decision making, e.g. loans business, trading,

investments, etc.)RORAC

Focus on allocated capital and RORAC does not take

into account the investment risk of the shareholder

(required return)!

?

!

15

© finval 2010

Universität St. GallenIC – 06.05.2010

Function & Scope of IC Design (illustrative example)

Equity bonus Cash bonus

Equity plans for ExB

Equity plans for middle management

Stock Purchase Plans for employees

Profit Sharing @ Group level

Profit Sharing @ divisional level

Mix of bonus plans & profit sharing

Important to retain:1. Even if “Equity Programs” are often linked to forward looking and “Cash Programs” to past performance, this is

generically not correct: Cash, Quasi-Equity and Equity are only instruments that can serve different purposes!2. Just stating that “an equity program is positive, as it aligns management & shareholders’ interests” would

completely ignore the mechanics of funding, allocation, vesting etc. – focusing on share price maximization (in incentive setting) can be very critical, as the main focus is put on creating expectations (= “sell-side”analysts), instead of the intrinsic operational value of the company (= long-term investor)!

16

© finval 2010

Universität St. GallenIC – 06.05.2010

Basic parameters of bonus design (examples)

Top down

Bottom up

Annual basis

Multi-year-basis

Volumes / revenues

Cost efficiency

Economic profit

Capital efficiency

Funding

Performance metrics

Target Setting

Performance logic

Financial performance

Qualitative objectives

Financial & qualitative objectives

Discretionary

Formula-based & discretionary

Allocation

Formula-based

Cap / Floor

Payout

Payout range

Unlimited payout range

Annual basis

Every x years

Payout frequency

Instant payout

Payout mode

Payout @ risk

Staggered @ risk: Bonus Account

Deferred payout

Restricted shares

Performance shares

Stock options

Cash bonus

Instruments

Equity bonus

Quasi-equity bonus

Performance units

Stock Appreciation Rights (SARs)

Vesting / Blocking

Vesting

Entry / Exit / Forfeiting rules

Entry / Exit / Forfeiting rules

Immediate Vesting

Time Vesting

Performance Vesting

Blocking

Entry / Exit / Forfeiting rules

17

© finval 2010

Universität St. GallenIC – 06.05.2010

Agenda

Getting started Basics of Incentive Compensation Design

– Components & Focus– Function & Scope– Funding– Allocation– Instruments– Vesting / Blocking– Payout

Wrap-up: Topics to be considered in Incentive Compensation design

18

© finval 2010

Universität St. GallenIC – 06.05.2010

The choice of Performance Metrics is a key component of an Incentive Compensation design (examples)

High-level assessment:

Funding Options: Economic Profit(EP)

Basis: Profit after Taxes, as published

Adjustment for e.o. items („normalization“)

Deduction of shareholder‘s required return from normalized profit (cost of capital)

Fully aligned with shareholder´ interests

Full cost considered, incl. cost of capital

If highly divergent business areas, possible acceptance issues of “Group” EP (contribution, risk profile, ...)

Profit after Taxes (Corporate level)

Profit after Taxes, as published

No further adjustments No consideration of cost

of capital / shareholder‘s required return

Only partially aligned, as required return not considered

No consideration of cost of capital

If highly divergent business areas, possible acceptance issues (contribution, risk profile, ...)

Profit Contribution (Business Area)

Profit Contribution of each business area

Direct costing only includes relevant costs of business area

Overhead costs not allocated / allocated through transfer pricing

Only limited alignment Only direct costing, or

complex transfers Potentially higher degree

of acceptance by business areas; transfers have negative impact

Funding Allocation PayoutInstruments Vesting / Blocking

19

© finval 2010

Universität St. GallenIC – 06.05.2010

Funding mechanisms

Only 55% of all participants responded to define an explicit “funding pool” at all None of the respondents takes the expected return of the shareholder, i.e., the “Economic Profit”, systematically

into account when defining a bonus “pool” – thus not reflecting the “investment risk” of the company’s owner

In order to control variable personnel expenses, the relevant governance body of a bank should define a “funding pool” for variable compensation purposes

A funding level defined on the basis of “Economic Profit” not only considers revenues, expenses and any risk-based P&L bookings, but also reflects the expected return of the shareholder

% Total Operating Income

% Pre–tax Profit

% Net Profit

% Economic Profit

At discretion of management/shareholders

The bank doesn’t define a maximum amount for total variable compensation

The bank doesn’t define a maximum amount for total variable compensation

% Total Operating Income

% Pre–tax Profit

% Net Profit

% Economic Profit

At discretion of manage-ment / shareholders

International Bank Group II All respondents Legend

22%

22%

0%

0%

0%

56% 28%

15%

45%

4%

0%

8%

: Responses given by International Bank

Survey Responses2010

20

© finval 2010

Universität St. GallenIC – 06.05.2010

Conflicts if funding not consistent with shareholders’ interests (illustrative example)

Funding Allocation PayoutInstruments Vesting / Blocking

GroupEconomic Profit: -10

Incentive Compensation: 13

PBEP: +5IC: 4

AMEP: +12

IC: 2

CRBEP: 0IC: 2

IBEP: -27

IC: 5Area AEP: +10

IC: 3

Area BEP: -5IC: 1

EquitiesEP: +5IC: 1

FIEP: +7IC: 1

RetailEP: +4IC: 1

Corp.EP: -4IC: 1

IBDEP: +3IC: 2

FIEP: -30

IC: 3

Share price: -30% No dividends

Shareholder?

Perf. Basis for IC:NNA / Revenues

Perf. Basis for IC:Inv. Performance

Perf. Basis for IC: Volumes / PC

Perf. Basis for IC: Deals /Sales Credits/Trading P&L

Alignment of IC performance basis with shareholders’ interests? But these isolated value drivers still serve as a basis to grant variable pay in practice!

21

© finval 2010

Universität St. GallenIC – 06.05.2010

Target setting & bonus curve design are decisive when reflecting the overall governance and shareholders‘ interests (examples)

High-level assessment:

Design Options: Target Setting Basis

Actual results Plan / Budget

Linking bonus payments to actual results represents a truly “pay-for-performance”-based Incentive Compensation

Budget or plan focus leads to (lengthy) annual renegotiations of desired results, bonus gambling –and „hockey stick“business cases

Target Setting Perspective

Annual targets Multi-year targets: annual

targets established for a predefined period (e.g., 3 years)

Annual targets: focus on one year only, “bonus gambling”

Multi-year targets: increased transparency and long-term orientation, in line with shareholders’long-term interests

Bonus Curve

Caps & floors No caps & floors

Caps & floors: performance incentive limited by Cap – Floor range

Caps & floors can provoke „window dressing“ behavior

No caps / floors : increased „wealth leverage“ for employees, while aligning performance interests

Funding Allocation PayoutInstruments Vesting / Blocking

22

© finval 2010

Universität St. GallenIC – 06.05.2010

Budget / short-term plan: incentive for long-term orientation?

Linking bonus levels to budget achievement leads to inconsistent incentives by

a) penalizing superior performanceb) rewarding poor performance

as next year’s goal is often based on prior year’s results

Encouragement for income and expense shifting at the end of the relevant performance period

Lengthy negotiations of budget / short-term plan Budget / short-term plans do not reflect long-

term shareholders’ interests

Multi-year and value-based targets (derived from shareholders‘ expectations) take into account earnings variability

Stronger incentives due to “clear deal” Budgeting process has no impact on bonus,

which is based on economic considerations Avoidance of “year-end behavior” (i.e., “bonus

gambling” / “budget gaming”) Significant reduction of management time used

for budget negotiation process Requires more careful target setting and risk

analysis

t2

t3

t…

t1

a)

b)

t2

t3

t…

t1

No bonus, as demanding budget not reached?

Bonus, as low budget clearly exceeded

Bonus

No bonus

Bon

us b

ased

on

budg

et /

shor

t-ter

m p

lan

Bon

us b

ased

on

long

-term

goa

ls

Budget / Short-term plan Actual performance

Long-term value-based

goal

Funding Allocation PayoutInstruments Vesting / Blocking

23

© finval 2010

Universität St. GallenIC – 06.05.2010

Target setting time horizon implemented for bonus purposes

The target setting procedures applied by Ukrainian banks indicate a highly short-term oriented focus Among all respondents, there is only one respondent that uses a target setting timeframe that exceeds one year

A multi-year target setting (eventually only applied to Incentive Compensation programs that focus on Top Management) would help to align long-term shareholder‘s interests with those of relevant employees

Monthly

Quarterly

Semiannually

Annually

For every 3–5 years

At discretion of management

Combination of different periods

Monthly

Quarterly

Annually

For every 3 – 5 years

Semiannually

At discretion of management

Combination of different periods*

International Bank Group II All respondents Legend

0%

0%

38%

0%

38%

63%

50%

0% 20% 40% 60% 80% 100%

7%

2%

21%

2%

39%

39%

52%

0% 20% 40% 60% 80% 100%

: Responses given by International Bank

*: “Combination of different periods” includes respondents with multiple payout frequencies (multiple responses have been allocated to individual time horizons; overall response rates might exceed 100%)

Survey Responses2010

24

© finval 2010

Universität St. GallenIC – 06.05.2010

Traditional vs. value-based funding limits (Bonus Account – payout options also reflected here)

Bonus

Economic ProfitValue creation target

TargetBonus

Bonus Account (+)

Bonus Account (-)

Long-term oriented entrepreneurial incentivesBonus

Multiple perf. metrics

Budget

Incentive to perform

Promotes below-average

performance

Avoids above-average

performance

Short-term oriented budget focus

One-year focus Focus on budget High „complexity“ „Bonus Gambling“ Only (limited) upside considered

Long-term oriented entrepreneurial incentives

Multi-year focus Focus on actual results Generally improved simplicity of program Increased transparency of variable pay Both up- & downside considered

TargetBonus

Funding Allocation PayoutInstruments Vesting / Blocking

25

© finval 2010

Universität St. GallenIC – 06.05.2010

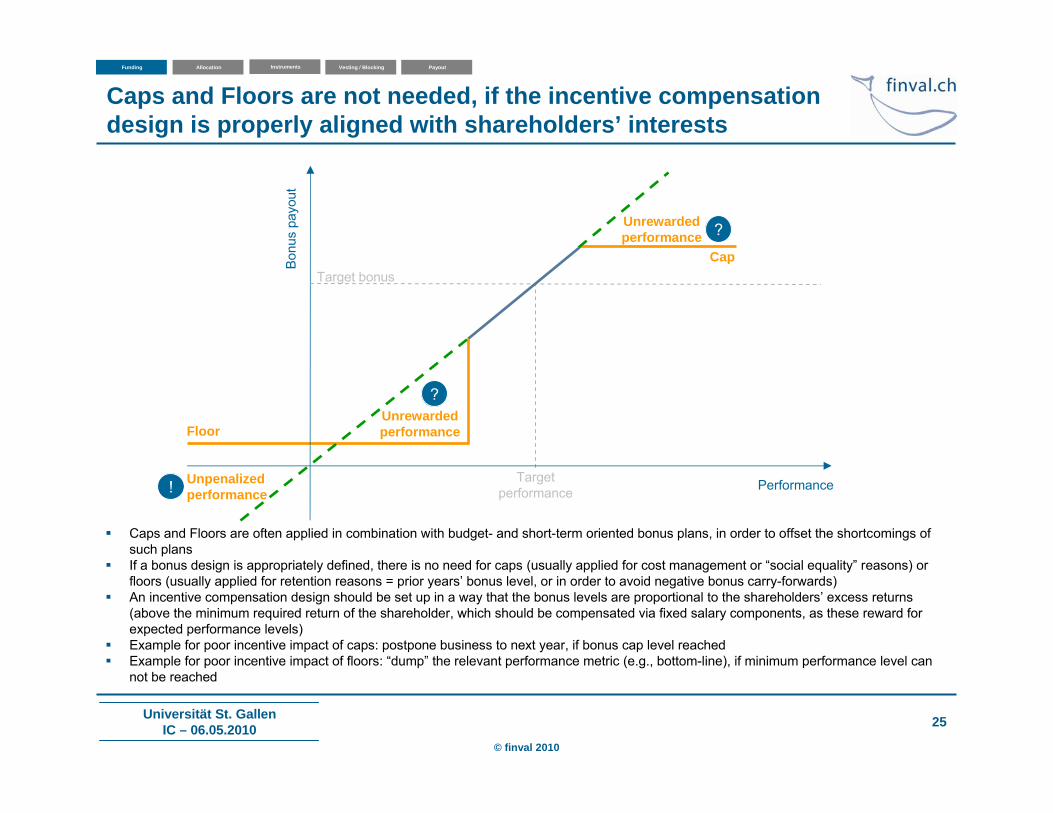

Caps and Floors are not needed, if the incentive compensation design is properly aligned with shareholders’ interests

Unrewardedperformance

Unrewardedperformance

Target bonusBo

nus

payo

ut

Target performance

Floor

Cap

Caps and Floors are often applied in combination with budget- and short-term oriented bonus plans, in order to offset the shortcomings of such plans

If a bonus design is appropriately defined, there is no need for caps (usually applied for cost management or “social equality” reasons) or floors (usually applied for retention reasons = prior years’ bonus level, or in order to avoid negative bonus carry-forwards)

An incentive compensation design should be set up in a way that the bonus levels are proportional to the shareholders’ excess returns (above the minimum required return of the shareholder, which should be compensated via fixed salary components, as these reward for expected performance levels)

Example for poor incentive impact of caps: postpone business to next year, if bonus cap level reached Example for poor incentive impact of floors: “dump” the relevant performance metric (e.g., bottom-line), if minimum performance level can

not be reached

Unpenalizedperformance

Performance

?

!

?

Funding Allocation PayoutInstruments Vesting / Blocking

26

© finval 2010

Universität St. GallenIC – 06.05.2010

Usage of caps and/or floors when defining the bonus per eligible employee

Caps (and floors) are widespread in Ukrainian banks – 57% of respondents indicated that they employ floors and/or caps

In Group II, 44% of participants claimed to use these instruments

Caps and floors are often applied in combination with budget- and short-term oriented bonus plans, in order to offset the shortcomings of such plans

If a bonus design is appropriately defined, there is no need for caps or floors

Yes

No

International Bank Group II All respondents Legend

Yes

No

57%

43%44%

56%: Responses given by International Bank

Survey Responses2010

27

© finval 2010

Universität St. GallenIC – 06.05.2010

Agenda

Getting started Basics of Incentive Compensation Design

– Components & Focus– Function & Scope– Funding– Allocation– Instruments– Vesting / Blocking– Payout

Wrap-up: Topics to be considered in Incentive Compensation design

28

© finval 2010

Universität St. GallenIC – 06.05.2010

The way bonuses are allocated to areas/individuals is decisive for the acceptance by key employees & the perceived attractiveness

High-level assessment:

Allocation Options: Fully formula-based allocation

Allocation depends fully on an allocation formula

Allocation formula can (and should) be made transparent to key employees

Fully objective & transparent

Highest retention & motivation impact for performing employees

Formula should be fully aligned with shareholder‘s interests (linear relationship)

Partially formula-based allocation

Front Areas and Top Management with a formula-based allocation

Other areas with discretionary allocation, according to management appraisal

Only partially objective & transparent

Non-Front areas with far lower retention & motivation impact

Alignment is not necessarily given, as management‘s discretion can diverge from shareholder‘s interests

Discretionary allocation

Allocation fully dependent on manager‘s discretion

No transparency for employees on how bonus levels have been determined

No objectivity & transparency

No positive motivation or retention impact embedded in design

Alignment is not necessarily given, as management‘s discretion can diverge from shareholder‘s interests

But: still needed for specific situations

Funding Allocation PayoutInstruments Vesting / Blocking

29

© finval 2010

Universität St. GallenIC – 06.05.2010

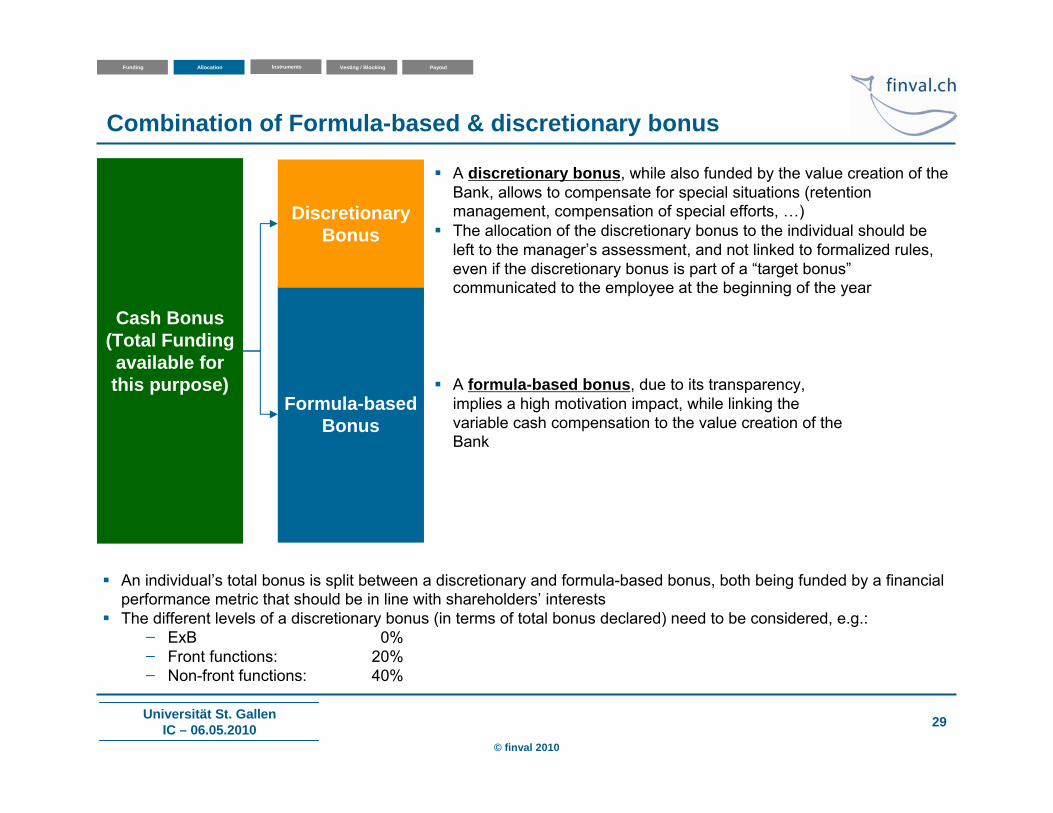

A formula-based bonus, due to its transparency, implies a high motivation impact, while linking the variable cash compensation to the value creation of the Bank

A discretionary bonus, while also funded by the value creation of the Bank, allows to compensate for special situations (retention management, compensation of special efforts, …)

The allocation of the discretionary bonus to the individual should be left to the manager’s assessment, and not linked to formalized rules, even if the discretionary bonus is part of a “target bonus”communicated to the employee at the beginning of the year

Cash Bonus (Total Funding available for this purpose)

Formula-based Bonus

Discretionary Bonus

An individual’s total bonus is split between a discretionary and formula-based bonus, both being funded by a financial performance metric that should be in line with shareholders’ interests

The different levels of a discretionary bonus (in terms of total bonus declared) need to be considered, e.g.:̶ ExB 0%̶ Front functions: 20%̶ Non-front functions: 40%

Combination of Formula-based & discretionary bonus

Funding Allocation PayoutInstruments Vesting / Blocking

30

© finval 2010

Universität St. GallenIC – 06.05.2010

Ways of allocating variable compensation to employees

Slightly more than a third of all respondents indicated using a mixed approach, including both formula-driven and discretionary allocation processes – in Group II, this portion represented slightly more than half of respondents

The understanding of a certain bonus logic, determined by a formula (if correctly set up), can further motivate an employee to reach his/her targets

A bonus, allocated on a discretionary basis, allows compensation for special situations (retention management, compensation of special efforts, etc.) – however, such a determination of an individual bonus should be left to the manager’s assessment and not linked to formalized rules

Calculated based on a certain formula

Defined on a discretionary basis

Partly formula–based and partly defined on a discretionary basis

International Bank Group II All respondents Legend

Based on a certain formula

Defined on a discretionary basis

Partly formula–based and partly defined on a discretionary basis

56%22%

22%

39% 35%

26%

: Responses given by International Bank

Survey Responses2010

31

© finval 2010

Universität St. GallenIC – 06.05.2010

Agenda

Getting started Basics of Incentive Compensation Design

– Components & Focus– Function & Scope– Funding– Allocation– Instruments– Vesting / Blocking– Payout

Wrap-up: Topics to be considered in Incentive Compensation design

32

© finval 2010

Universität St. GallenIC – 06.05.2010

Incentive Compensation instruments translate the desired objectives into tangible tools (examples – Cash alternatives)

High-level assessment:

Instrument Options: Target Bonus & Multiple (Cash)

Each eligible employee receives a „target bonus“

The level of the actual bonus depends on a bonus multiple applied to the target bonus, reflecting value creation

High objectivity, as multiple reflects value creation

Enhanced motivation & retention, as target Bonus is a point of reference for employees

Bonus multiple reflects development of underlying result – if linear relationship, no negative impact on alignment

Performance Units(Cash)

Profit Sharing, not capital participation

Same principle as „Target Bonus“, but translated into „Performance Units“

Each employee receives a number of units; price reflects value creation

High objectivity, as unit price reflects value creation

As target bonus, but with additional „unit“ impact

Price of Performance Units with same consequences as „Bonus Multiple“

Amount only

No use of target bonus Generally, prior year‘s

bonus taken as a reference

No objectivity & transparency

No positive motivation or retention impact embedded in design

Alignment not necessarily given, as far as bonus amounts depend on prior year‘s levels

Risk of „compensating measures“

Funding Allocation PayoutInstruments Vesting / Blocking

33

© finval 2010

Universität St. GallenIC – 06.05.2010

Incentive Compensation instruments translate the desired objectives into tangible tools (examples – Equity alternatives)

High-level assessment:

Instrument Options: Performance Shares

Each eligible employee receives shares with ownership transfer in a certain period of time, depending on a performance condition (e.g., # of shares at vesting multiplied by a performance multiple)

Restricted shares

Each eligible employee receives company shares with ownership transfer in a certain period of time

Aligned with shareholder´interests due to incorporation of future performance (even if only indirect by share price development)

High objectivity and motivation impact, if grant value is derived from current company performance

Stock Options

Each eligible employee receives options with the possibility to get company’s shares in a certain period of time

Asymmetric risk exposure (as compared to shareholder leverage)

Funding Allocation PayoutInstruments Vesting / Blocking

Aligned with shareholder´interests due to incorporation of future internal (operational, as multiple reflects value creation during vesting period) and external (share price development) performance

High objectivity and motivation impact, if grant value is derived from current company performance

34

© finval 2010

Universität St. GallenIC – 06.05.2010

69%

15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Forms of compensation currently used

Equity incentives (or the like) are almost never used by Ukrainian banks – in line with the quasi-absence of long-term orientation

With equity instruments (or hybrid forms, e.g., performance units), a firm usually intends to link incentives provided to employees to the overall value of the firm, thus aligning employees’ with shareholders’ interests – additional insight would nevertheless be required to assess whether the instruments used really provide for such an effect

Cash bonus

Equity

Top Management

Front

Trading/Sales

Risk Management & Controlling

Back Office

Other employees groups

Top Management

Front

Trading/Sales

Risk Management & Controlling

Back Office

Other employees groups

International Bank Group II Legend

Cash Bonus

Equity BonusTop Management

Front

Trading/Sales

Risk Management & Controlling

Back Office

Other employees groups

67%

89%

56%

56%

56%

44%

22%

11%

11%

0%

0%

0%

0% 20% 40% 60% 80% 100%

: Responses given by International Bank

Survey Responses2010

35

© finval 2010

Universität St. GallenIC – 06.05.2010

Agenda

Getting started Basics of Incentive Compensation Design

– Components & Focus– Function & Scope– Funding– Allocation– Instruments– Vesting / Blocking– Payout

Wrap-up: Topics to be considered in Incentive Compensation design

36

© finval 2010

Universität St. GallenIC – 06.05.2010

Vesting / Blocking

Funding Allocation PayoutInstruments Vesting / Blocking

High-level assessment:

Options: Vesting

Immediate vesting Time vesting Performance vesting

Immediate vesting has no additional retention / motivation impact

Time vesting exposes ownership transfer to pure time factors (no additional incentive)

Performance vesting usually combines time vesting with a performance condition (additional incentive)

Blocking

Blocking No blocking

Blocking provides for additional retention and could also be used to increase long-term orientation

Nevertheless, once vested, blocking rules usually forfeit in case of departure of the employee during the blocking period

37

© finval 2010

Universität St. GallenIC – 06.05.2010

Agenda

Getting started Basics of Incentive Compensation Design

– Components & Focus– Function & Scope– Funding– Allocation– Instruments– Vesting / Blocking– Payout

Wrap-up: Topics to be considered in Incentive Compensation design

38

© finval 2010

Universität St. GallenIC – 06.05.2010

The way bonuses are paid out contribute to achieve the overall objectives of an Incentive Compensation design

High-level assessment:

Payout Options: Immediate Cash

Immediate payout at the end of the underlying „performance period“

No impact on retention & motivation per se

Nevertheless, payout frequency (combined with „exit rules“) should be thoroughly assessed

Not fully aligned with shareholders, as payout does not necessarily reflect long-term interests

Bonus @ risk(partial amount)

A portion of bonus is retained and paid out after some time (e.g., 3-5 years)

Value of retained bonus portion changes with ongoing performance (during the „@risk-period)

High retention impact, if appropriate level of “@ risk” portion

High motivation impact, as incentive for continuous value creation

Improved alignment, as value of „bonus @ risk“portion changes with ongoing performance –long-term interests of shareholders reflected

Deferred payment(partial amount)

A portion of bonus is deferred and paid out after some time (e.g., 3-5 years)

Value of deferred bonus portion does not change with ongoing performance – pure timing issue

High retention impact, if appropriate level of deferred portion

No motivation impact - no incentive for continuous value creation

No positive impact per se, except for retention of key employees

Ongoing performance is not considered

Funding Allocation PayoutInstruments Vesting / Blocking

39

© finval 2010

Universität St. GallenIC – 06.05.2010

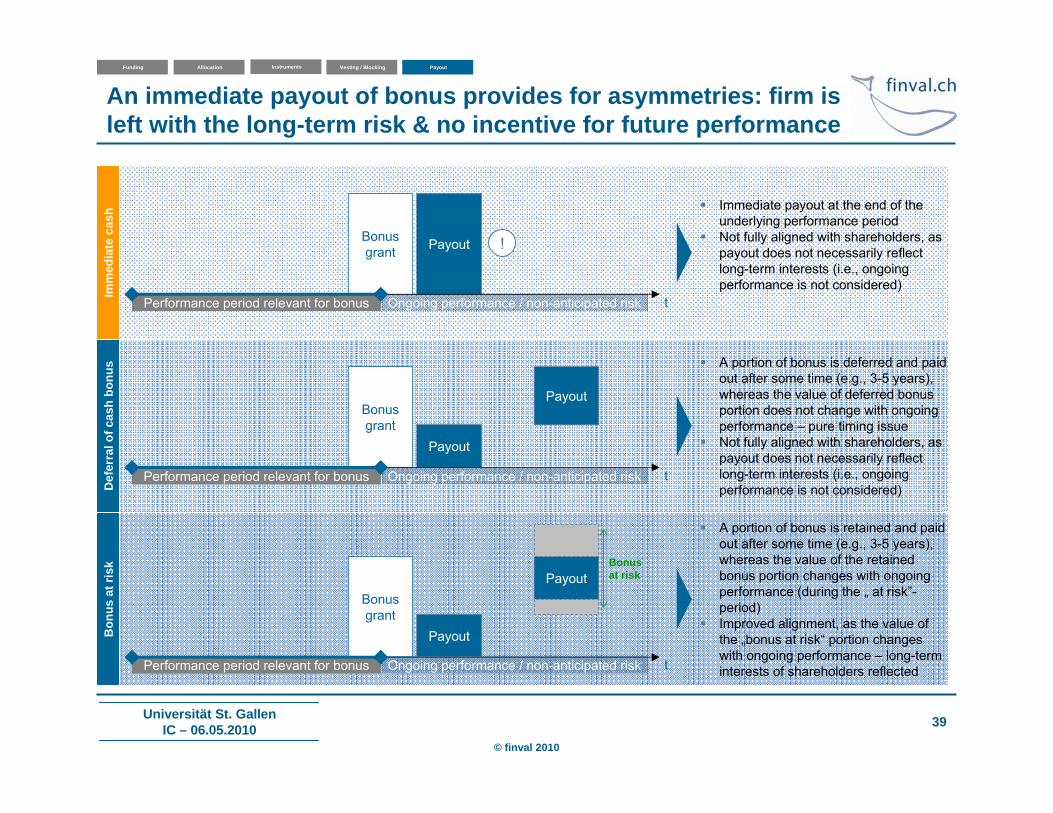

An immediate payout of bonus provides for asymmetries: firm is left with the long-term risk & no incentive for future performance

Ongoing performance / non-anticipated riskPerformance period relevant for bonus

Bonus grant

Payout

Payout

Performance period relevant for bonus

Bonus grant

Payout

Payout

Ongoing performance / non-anticipated risk

Performance period relevant for bonus

Bonus grant Payout

Ongoing performance / non-anticipated risk

Immediate payout at the end of the underlying performance period

Not fully aligned with shareholders, as payout does not necessarily reflect long-term interests (i.e., ongoing performance is not considered)

A portion of bonus is deferred and paid out after some time (e.g., 3-5 years), whereas the value of deferred bonus portion does not change with ongoing performance – pure timing issue

Not fully aligned with shareholders, as payout does not necessarily reflect long-term interests (i.e., ongoing performance is not considered)

A portion of bonus is retained and paid out after some time (e.g., 3-5 years), whereas the value of the retained bonus portion changes with ongoing performance (during the „ at risk”-period)

Improved alignment, as the value of the „bonus at risk“ portion changes with ongoing performance – long-term interests of shareholders reflected

Imm

edia

te c

ash

Bon

us a

t ris

kD

efer

ral o

f cas

h bo

nus

Bonus at risk

!

t

t

t

Funding Allocation PayoutInstruments Vesting / Blocking

40

© finval 2010

Universität St. GallenIC – 06.05.2010

An approach to capture the long-term perspective within an annual cash bonus plan (“Bonus Reserve”)

Advantages of a bonus reserve: Smoothes bonus in case of volatile

business performance Retains productive employees

throughout business cycle Lengthens decision horizons for

managers Holds managers accountable for

delivering sustainable long-term performance

Serves as an “insurance” for investors regarding sustainable improvements of company performance

Bonu

s

Performance

Performance

Bonu

s

Payout of specified percentage of balance each

year

Bank is paid out up to a defined threshold (e.g.

target bonus) and only part of excess bonus is paid out (e.g. 1/3); remaining part

(e.g. 2/3) is “banked”(remains in the account)

Bon

us re

serv

e “a

ll-In

”ap

proa

chB

onus

rese

rve

“thr

esho

ld”

appr

oach

Funding Allocation PayoutInstruments Vesting / Blocking

41

© finval 2010

Universität St. GallenIC – 06.05.2010

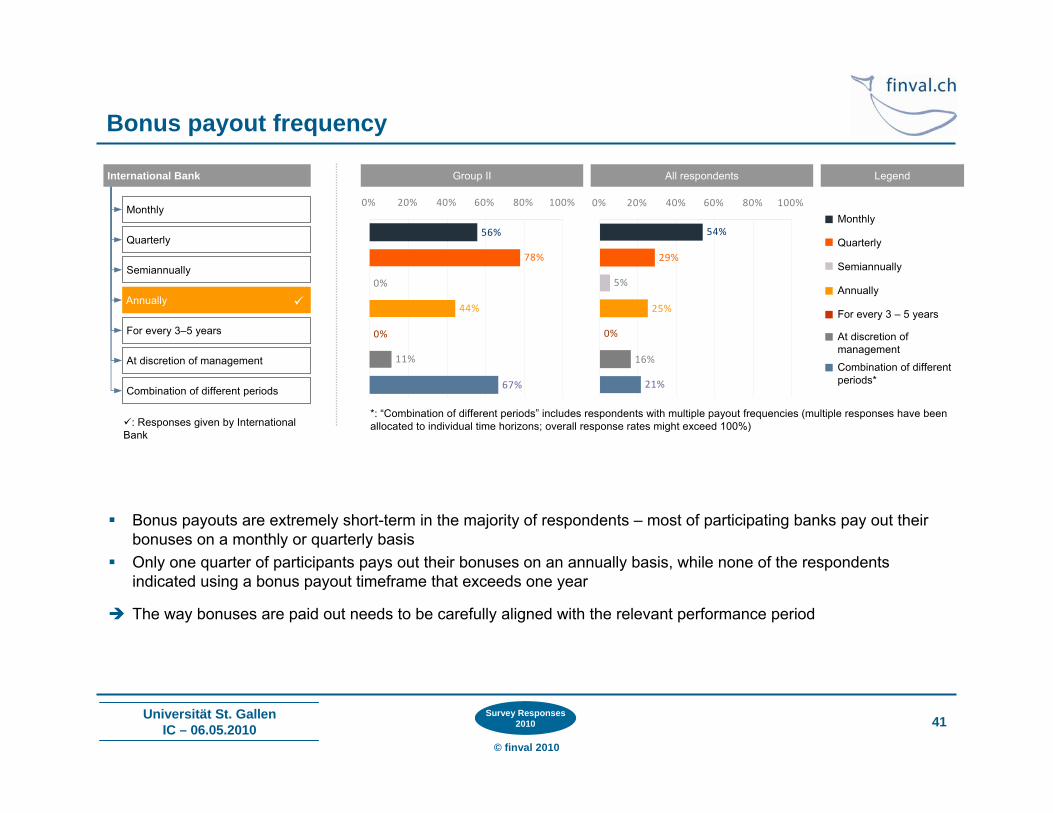

Bonus payout frequency

Bonus payouts are extremely short-term in the majority of respondents – most of participating banks pay out their bonuses on a monthly or quarterly basis

Only one quarter of participants pays out their bonuses on an annually basis, while none of the respondents indicated using a bonus payout timeframe that exceeds one year

The way bonuses are paid out needs to be carefully aligned with the relevant performance period

Monthly

Quarterly

Semiannually

Annually

For every 3–5 years

At discretion of management

Combination of different periods

International Bank Group II All respondents Legend

0%

11%

56%

78%

44%

0%

67%

0% 20% 40% 60% 80% 100%

5%

16%

21%

0%

25%

29%

54%

0% 20% 40% 60% 80% 100%

Monthly

Quarterly

Semiannually

Annually

For every 3 – 5 years

At discretion of management

Combination of different periods*

*: “Combination of different periods” includes respondents with multiple payout frequencies (multiple responses have been allocated to individual time horizons; overall response rates might exceed 100%): Responses given by International

Bank

Survey Responses2010

42

© finval 2010

Universität St. GallenIC – 06.05.2010

Agenda

Getting started Basics of Incentive Compensation Design

– Components & Focus– Function & Scope– Funding– Allocation– Instruments– Vesting / Blocking– Payout

Wrap-up: Topics to be considered in Incentive Compensation design

43

© finval 2010

Universität St. GallenIC – 06.05.2010

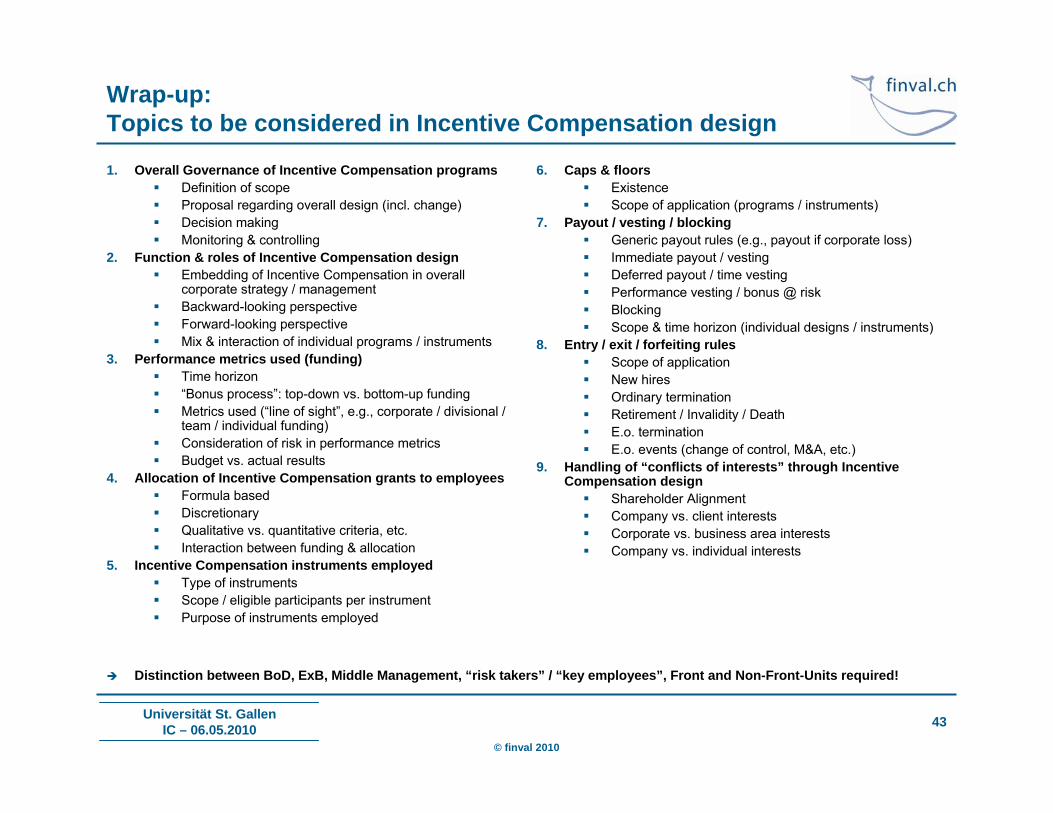

Wrap-up: Topics to be considered in Incentive Compensation design

1. Overall Governance of Incentive Compensation programs Definition of scope Proposal regarding overall design (incl. change) Decision making Monitoring & controlling

2. Function & roles of Incentive Compensation design Embedding of Incentive Compensation in overall

corporate strategy / management Backward-looking perspective Forward-looking perspective Mix & interaction of individual programs / instruments

3. Performance metrics used (funding) Time horizon “Bonus process”: top-down vs. bottom-up funding Metrics used (“line of sight”, e.g., corporate / divisional /

team / individual funding) Consideration of risk in performance metrics Budget vs. actual results

4. Allocation of Incentive Compensation grants to employees Formula based Discretionary Qualitative vs. quantitative criteria, etc. Interaction between funding & allocation

5. Incentive Compensation instruments employed Type of instruments Scope / eligible participants per instrument Purpose of instruments employed

6. Caps & floors Existence Scope of application (programs / instruments)

7. Payout / vesting / blocking Generic payout rules (e.g., payout if corporate loss) Immediate payout / vesting Deferred payout / time vesting Performance vesting / bonus @ risk Blocking Scope & time horizon (individual designs / instruments)

8. Entry / exit / forfeiting rules Scope of application New hires Ordinary termination Retirement / Invalidity / Death E.o. termination E.o. events (change of control, M&A, etc.)

9. Handling of “conflicts of interests” through Incentive Compensation design Shareholder Alignment Company vs. client interests Corporate vs. business area interests Company vs. individual interests

Distinction between BoD, ExB, Middle Management, “risk takers” / “key employees”, Front and Non-Front-Units required!

44

© finval 2010

Universität St. GallenIC – 06.05.2010

Contact Details

finval – Finance & ValueAttn. Thomas Wä[email protected]ühlebachstr. 64CH – 8008 Zurich (Switzerland)Phone: +41 (79) 500.78.03www.finval.ch