Any activity that creates present or future economic value ...

21

Production Any activity that creates present or future economic value (utility). The transformation of inputs into outputs Inputs can include categories such as: labour, capital, energy, land, entrepreneurship etc...

Transcript of Any activity that creates present or future economic value ...

Production

Any activity that creates present or future economic value (utility).

The transformation of inputs into outputs

Inputs can include categories such as: labour, capital, energy, land, entrepreneurship etc...

Production Function

Q = F(.)

The form of the production function F(.) depends on the technology available. It can be thought of as the blueprint for production.

Technology: All knowledge that creates economic value

Eg: Dual Input Production Function Q = F(K,L)=2KL

Labour(person-hours/wk)

1 2 3 4 5

1 2 4 6 8 10

Capital 2 4 8 12 16 20

(equipment-hours/wk 3 6 12 18 24 30

4 8 16 24 32 40

5 10 20 30 40 50

Fixed and Variable Inputs

The minimum time it takes to change an input varies with the type of input. For this reason we differentiate:

Long Run: The shortest period of time required to alter the amounts of all inputs used in a production process.

Short Run: The longest period of time during which at least one of the inputs cannot be altered

Note that this definition has nothing to do with months, years etc... for some industries (semiconductors) the short run may be years, while for others (hot dog

vending) the long run may be hours.

Production in the Short Run

Say we hold one of the inputs constant, in this case capital.

Total Product Curve

Diminishing Returns: If other inputs are fixed, the increase in output from an increase in the variable input must eventually decline

Most production processes can be described by the following function.

Marginal Product

The Total Product curve relates the total amount of production to the variable input.The Marginal Product curve relates the change in total production due to a unit change in the variable input (ie: it is the slope of the TP curve).

Are there any levels of L a producer would not choose?

MPL =∆Q

∆L=

δQ

δL

Average Product

The average product is the total output divided by the quantity of the variable input, the line joining the origin to the corresponding point on the total product curve. In a sense, it reflects productivity.

APL = LQ

MP, AP Relationships

When the marignal product curve lies above the average product curve, the average product curve must be rising; and when the marginal product curve lies below the average product curve, the average product curve must be falling. The two curves intersect at the maximum value of the

average product curve.

Example Using MP, AP

Say you are the owner of 4 fishing boats, and you must decide how to divide your fleet between two locations. If you currently have 2 boats at the west end and 2 boats at the east end, will you

change this ratio?

General Rule for Indivisible Resources: Allocate each unit of resources to the production activity where the MP is the highest.

When goods are divisible, this rule becomes:Allocate each unit of resources to the production activity until the MPs are equal

Production in the Long RunAll inputs are now variable

Q(K,L)=2KL

Isoquant: The set of all technically efficient input combinations that yield a given level of output.Note: The labels of the isoquants are now output quantities. They can not be arbitrarily relabeled

as can be done with indifference maps.

The Long Run Production Function

Q = F(K,L)Isoquant: The locus through all combinations of K and L which yield the same amount of output

Marginal Rate of Technical SubstitutionThe rate at which one input can be exchanged for another at the same level of output.

MRTS = |slope of isoquant| = MPLMPK

Elasticity of SubstitutionMeasures the degree of substitution of a production function. If it is close to zero, there is little

opportunity to substitute. If it is large, then significant substitution.

σ =%∆K

L

%∆MRTS

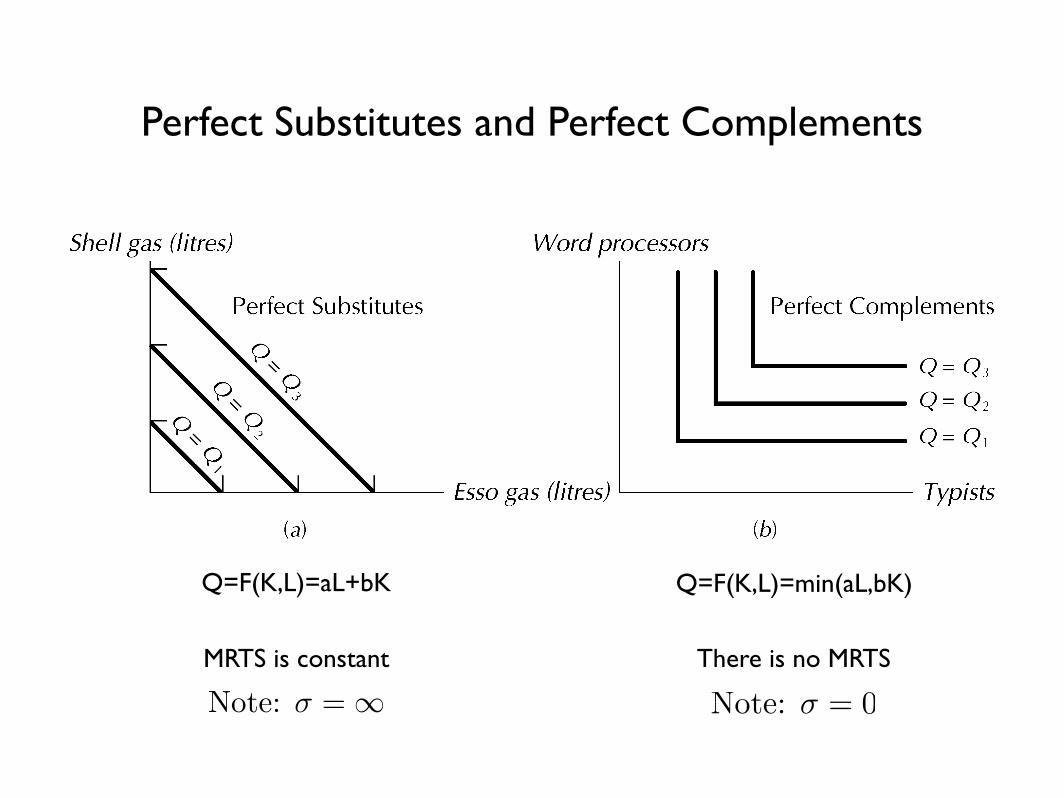

Perfect Substitutes and Perfect Complements

Q=F(K,L)=aL+bK

MRTS is constant

Q=F(K,L)=min(aL,bK)

There is no MRTS

Note: σ =∞ Note: σ = 0

Cobb-Douglas Production Function

Q = AKaLb where A, a, b > 0 and b = 1− a Note: σ = 1

Returns to ScaleOnly applies to the Long Run

What happens to output when all inputs are increased in proportion?Does production take place more efficiently in small scale or large scale?The answer will dictate whether an industry is served by many small firms or a few large ones.

Increasing Returns to Scale: A proportional increase in every input yields a more than proportional increase in outputConstant Returns to Scale: A proportional increase in every input yields an equal increase in outputDecreasing Returns to Scale: A proportional increase in every input yields a less than proportional increase in output

αQ = F (λK, λL)

Returns to Scale

A production function may have different returns to scale over its domain....

.... or it may have the same returns to scale over its domain. Eg: Cobb-Douglas

Technological Change

Technological improvements are represented graphically by a shifting of the production function

Note that even though both production functions exhibit

diminishing returns, the growth in output outpaces the growth in labour,

and productivity per worker rises.

Can be thought of as:1) Produce same Q with less inputs2) Produce more Q with same inputs3) Something in between

Neutral Technological ChangeTechnological change can be classified by its impact on MRTS at a given K/L ratio

MRTSpre = MRTSpost

Labour Saving Technological Change

MRTSpre > MRTSpost

Now marginal product of capital rises faster than that of labour, which in effect causes firms to use more capital in their choices than labour.

Capital Saving Technological Change

Now marginal product of capital rises faster than that of labour, which in effect causes firms to use more capital in their choices than labour.

MRTSpre < MRTSpost