Anuj & rohit012

52

A Research Report “Investor Perception Towards commodity market for investing’’ Report submitted in partial fulfillment of the requirement of MASTERS OF BUSINESS ADMINISTRATION (Affiliated to Uttar Pradesh Technical University) Academic Session (2011 – 2013) Under Supervision of : Submitted By: Prof. Anjali Mishra Anuj kumar garg – 1129070009 Rohit singh sengar-, 1129070011 MBA 1 st year ABES IT Group of Institutions 1 | Page

-

Upload

rohit-thakur -

Category

Business

-

view

171 -

download

1

Transcript of Anuj & rohit012

A

Research Report“Investor Perception Towards commodity market for investing’’

Report submitted in partial fulfillment of the requirement of

MASTERS OF BUSINESS ADMINISTRATION

(Affiliated to Uttar Pradesh Technical University)

Academic Session

(2011 – 2013)

Under Supervision of: Submitted By:

Prof. Anjali Mishra Anuj kumar garg – 1129070009

Rohit singh sengar-, 1129070011

MBA 1st year

ABES IT Group of Institutions

1 | P a g e

ACKNOWLEDGEMENT

We wish to acknowledge our profound gratitude to all those who assisted us in the completion of this report.

With great pleasure, we extend our deep sense of gratitude towards Anjali Mishra (asst. professor ABES IT college ,Ghaziabad), under whose valuable guidance, constant interest and encouragement, who has devoted her ever-precious time from her busy schedule and helped us in completing the Project.This co-operation is not only useful for this project but will be a constant source of inspiration for us in future life.

We are also thankful to those who helped us intellectually in preparation of this project directly or indirectly.

ANUJ KUMAR GRAG

ROHIT SINGH SENGAR

2 | P a g e

TABLE OF CONTENTS

Acknowledgment

Introduction 4-12

Objective of Project 13

Limitation 14

Literature review 15

Research methodology 16

Data Analysis and interpretation 17-33

Conclusion 34-35

Suggestions and Recommendations 36

Annexure

Bibliography

3 | P a g e

4 | P a g e

INTRODUCTION TO COMMODITY FUTURES

THE HISTORY

The modern commodity markets have their roots in the trading of agricultural products. While wheat and corn, cattle and pigs, were widely traded using standard instruments in the 19th century in the United States, other basic foodstuffs such as soybeans were only added quite recently in most markets. For a commodity market to be established, there must be very broad consensus on the variations in the product that make it acceptable for one purpose or another.

The economic impact of the development of commodity markets is hard to overestimate. Through the 19th century "the exchanges became effective spokesmen for, and innovators of, improvements in transportation, warehousing, and financing, which paved the way to expanded interstate and international trade."

Exchange Name Commodities Traded

Chicago Board of Trade

(CBOT)

Corn, ethanol, gold, oats, rice, silver, soybeans, wheat

Chicago Mercantile

Exchange (CME)

Butter, milk, feeder cattle, frozen pork bellies, lean hogs, live

cattle, lumber

Intercontinental Exchange*

(ICE)

Crude oil, electricity, natural gas

Kansas City Board of Trade

(KCBT)

Wheat, natural gas

Minneapolis Grain

Exchange (MGE)

Corn, soybeans, wheat

New York Board of Trade

(NYBOT)

Cocoa, coffee, cotton, ethanol, frozen concentrated orange

juice, sugar

New York Mercantile

Exchange (NYMEX)

Aluminum, copper, crude oil, electricity, gasoline, gold, heating

oil, natural gas, palladium, platinum, propane, silver

5 | P a g e

Regulatory framework in India

In India, the statutory, basis for regulating commodity futures’ trading is found in the Forward Contracts (Regulation) Act, 1952, which (apart from being an enabling enactment, laying down certain fundamental ground rules) created the permanent regulatory body known as the Forwards Markets Commission. This commission holds overall charge of the regulation of all forward contracts and carries out its functions through recognized association.

GUIDELINES BY THE RBI PERTAINING TO COMMODITY FUTURE TRADING

The guidelines are: -These guidelines cover the Indian entities that are

exposed to commodity price risk.

Name and address of the organization

I. A brief description of the hedging strategy proposed:

Description of business activity and nature of risk. Instruments proposed to be used for hedging. Exchanges and brokers through whom the risk is

proposed to be hedged and credit lines proposed to be available. The name and address of the regulatory authority in the country concerned may also be given.

Size/average tenure of exposure/total turnover in a year expected.

II. Copy of the risk management policy approved by the Board of Directors covering:

Risk identification Risk measurements Guidelines and procedures to be followed with

respect to revaluation/monitoring of positions. Names and designations of the officials authorized to

undertake transactions and limits.

III. Any other relevant information

6 | P a g e

The authorized dealers will forward the application to Reserve Bank along with copy of the Memorandum on the risk management policy placed before the Board of Directors with specific reference to hedging of commodity price exposure. .

i. All standard exchanges traded futures will be permitted.

ii. Tenure of exposure shall be limited to 6 months. Tenure beyond 6 months would require Reserve Bank’s specific approval.

iii. Corporate who wish to hedge commodity price exposure shall have to ensure that there are no restrictions on import/export of the commodity hedged under the Exim policy in force.

After grant of approval by Reserve Bank, the corporate concerned should negotiate with off-shore exchange broker subject, inter alia, to the following:-

Brokers must be clearing members of the exchanges, with good financial track record.

Trading will only be in standard exchange- traded futures contract/options.

SECURITIES AND EXCHANGE BOARD OF INDIA (SEBI)

SEBI was setup in April 12, 1988. To start with, SEBI was set up as a non-statutory body.

.SEBI guidelines for COMMODITY FUTURES TRADING

There are many regulatory authorities, who are monitoring commodity futures trading, one of them is SEBI. The following Report is one of the regulatory frameworks for the commodity futures trading.

Report of the committee appointed by the SEBI on participation by Securities Brokers inCommodity Futures Markets under the chairmanship of Shri K.R. Ramamurthy (February 5, 2003)

7 | P a g e

The following were the recommendations:-

I) Participation of Securities Brokers in Commodity Futures Market

o The committee was of the unanimous view that participation of intermediaries like securities brokers in the commodity futures market is welcome as it could inter-alia increase the number of quality players, infuse healthy competition, boost trading volumes in commodities and in turn provide impetus to the overall growth of the commodity market.

o Since the commodity market falls under the regulatory purview of a separate regulatory authority viz., Forward Market Commission, to ensure effective regulatory oversight by the Forward Market Commission, and to avoid any possible regulatory overlap, the pre-condition for such entry by intending participating securities brokers in the commodity futures market would be through a separate legal entity, either subsidiary or otherwise. Such entity should conform from time to time to the regulatory prescription of Forward Market Commission, with reference to capital adequacy, net worth, membership fee, margins, etc.

o The committee took note of the fact that the existing provisions of the Securities Contracts (Regulation) Rules, 1957 forbid a person to be elected as a member of a recognized stock exchange if he is engaged as principal or employee in any business other than that of securities, except as a broker or agent not involving any personal financial liability. The Committee recommended that the above provisions in the Securities Contract (Regulations) Rules be removed/amended suitably to facilitate securities brokers participation/engagement in commodity futures.

o An important felt need was the necessity to improve market awareness of trading and contracts in commodities. The committee therefore recommended the forward market commission take appropriate initiatives in training the market participants.

II) Risk containment measures

8 | P a g e

In the background of the Forward Market Commission’s report on risk containment measures currently obtaining in commodity markets and the committee’s recommendation to permit security brokers’ participation in commodities markets only through a separate legal entity, the committee considers that ensuring strict compliance of the regulatory prescriptions like net worth, capital adequacy, margins, exposure norms, etc., by the respective market regulators, and due oversight would be an adequate safeguard to ensure that the risks are not transmitted from one market to the other.

III) Utilization of existing infrastructure of stock exchanges

On the issue of convergence/integration of the securities market and commodities market, that is, of allowing stock exchanges to trade in commodity derivatives and vice versa, the committee was of the view that in the current statutory and regulatory framework and existence of two separate and established regulators, the issue of integration of the two markets would require detailed examination, particularly for the purpose of defining clearly the scope of regulatory purview and responsibility.

What is a commodity?

Commodity includes all kinds of goods. FCRA defines “goods” as “every kind of moveable property other than actionable claims, money and securities”.

Futures trading are organized in such goods or commodities as are permitted by the central government. The national commodity exchanges have been recognized by the central government for organizing trading in all permissible commodities which include precious (gold & silver) and non-ferrous metals; cereals and pulses; oil seeds, raw jute and jute goods; sugar; potatoes and onions; coffee and tea; rubber and spices, etc.

Commodity Futures TradingThe commodity futures trading, consists of a futures

contract, which is a legally binding agreement providing for the delivery of the underlying asset or financial entities at specific date in the future.Like all future contracts, commodity futures are agreements to buy or sell something at a later date and at a price that has been fixed earlier by the buyer and seller.So, for example, a cotton farmer may agree to sell his output to a textiles company many months before the crop is ready for actual harvesting.

9 | P a g e

The complicating factor is quality. Commodity futures contracts have to specify the quality of goods being traded. The commodity exchanges guarantee that the buyers and sellers will stick to the terms of the agreement.When one buys or sells a futures contract, he is actually entering into a contractual obligation which can be met in one of two ways.First, is by making or taking delivery of the commodity. This is the exception, not the rule however, as less than 2% of all the futures contracts are met by actual delivery. The other way to meet one’s obligation, the method which everyone most likely will use, is by “offset”.Very simply, offset is making the opposite or offsetting sale or purchase of the same number of contracts sold, sometimes prior to the expiration of the date of the contract. This can be easily done because futures contracts are standardized.

What makes commodity trading attractive?

A good low-risk portfolio diversifierLess volatile, compared with, say, equitiesInvestors can leverage their investments and multiply potential earningsBetter risk- adjusted returnsA good hedge against any downturn in equities or bonds as there is little correlation with equity and bond marketsHigh correlation with changes in inflation

No securities transaction tax levied

Functions of futures markets

The futures market serves the needs of individuals and groups who may be active traders or passive traders, risk averse or profit makers. The above broadly classifies the functions of the futures markets: -

1) Price Discovery2) Speculation3) Hedging

1) Price discovery

“Futures prices might be treated as a consensus forecast by the market regarding trading future price for certain commodities”. This classifies that

10 | P a g e

futures market help market watchers to “discover” prices for the future.

E.g.- A furniture manufacturer, making plywood furniture for printing his catalogue for next year’s needs to estimate price in advance. This task is different as the cost of plywood varies greatly, depending largely on the health of the construction industry. But the problem can be solved by using prices from the plywood futures market.

2) Speculation

Speculation is a spill over of futures trading that can provide comparatively less risk adverse investors with the ability to enhance their percentage returns.Speculators are categorized by the length of time they plan to hold a position.

3) HedgingWhile engaging in a futures contract in order

to reduce risk in the spot position, hedging is undertaken. Therefore the future trader is said to establish a hedge.

Participants

Hedgers

In a commodity market, hedging is done by a miller, processor, stockiest of goods, or the cultivator of the commodity. Sometimes exporters, who have agreed to sell at a particular price, need to be a hedger in a futures and options market. All these persons are exposed to unfavorable price movements and they would like to hedge their cash positions.

11 | P a g e

Speculators

Speculator does not have any position on which they enter in futures options market. They only have a particular view about the future price of a particular commodity. They consider various fundamental factors like demand and supply, market positions, open interests, economic fundamentals internal events, rainfall, crop predictions, government policies etc. and also considering the technical analysis, they are either bullish about the future process or have a bearish outlook.

In the first scenario, they buy futures and wait for rise in price and sell or unwind their position the moment they earn expected profit. If their view changes after taking a long position after taking into consideration the latest developments, they unwind the transaction by selling futures and limiting the losses. Speculators are very essential in all markets. They provide market to the much desired volume and liquidity; these in turn reduce the cost of transactions. They provide hedgers an opportunity to manage their risk by assuming their risk.

Arbitrageur

He is basically risk averse. He enters in to those contracts where he can earn risk less profits. When markets are imperfect, buying in one market and simultaneous selling in another market gives risk less profit. It may be possible between two physical markets, same for 2 different periods or 2 different contracts.

Intermediate Participants

12 | P a g e

Brokers

A broker is a member of any one of the futures exchange, one gets commodity or financial futuresexchange, one gets the right to transact with other members of the same exchange. All persons hedgingtheir transaction exposures or speculation on price movement cannot be members of a futures exchange.Non-member has to deal in futures exchange, through a member only. This provides the member the role ofa “broker”.

Margin

Margin is money deposited in the brokerage account, which serves to guarantee the performance of theclients’ side of the contract. This is generally in the neighborhood of 2-10%

When the client enters a position, he would have deposited, the margin in his account, but the brokeragehouse is required to post the margin with a central exchange arm called the ‘clearing house’. The clearinghouse is a non-profit entity, which in effect is in charge of debiting this money to the accounts of winnersdaily.

13 | P a g e

Objective of the Study

1. To study the perception of investors of commodity market.2. To understand commodity market.

14 | P a g e

Limitations and Constrains

Lack of resources Cost Constraint. Respondents are limited to hapur city.

LITERATURE REVIEW

15 | P a g e

COMMODITY MARKETS: AN ISLAMIC ANALYSIS

Research on derivatives trading is still in its early stages. The general response of Muslim jurists is negative. The first institution to address the issue was the Makkah based Fiqh Academy. It acknowledged some of the benefits of derivativesbut stressed that these benefits are accompanied by transactions forbidden in the shari[ah such as gambling, exploitation, monopoly, price distortion and the selling of what one does not own. Moreover, transactions are settled merely on the basis of price differentials as what happens between gamblers. However, the spot transactions are valid from theshari[ah point of view but when the seller does not own the object he sells, the sale in this case must fulfil the conditions of salam and the buyer is not permitted to sell again prior to taking possession of the underlying assets.

KARVR COMTRADE LTD.

KarvyComtrade Ltd. has established its dedicated research desk at Hyderabad keeping in view of varied requirements of clients in terms of taking informed decision. Initially started with a team of just 2 analysts in early 2005, now the team has 8 analysts tracking different commodity markets.

The Karvy Commodities Research team comprises of Technical Analysts, Fundamental Analysts and Derivatives Analyst who analyze news, events and data in order to arrive at a price outlook both on short term and long term basis for all the commodities. The coverage on different segments of commodities has been increasing over the time and currently generates reports on most of the active commodities which belong to different complexes like precious metals, Base metals, Energy, Oil & Oilseed complex, Pulses, Spices, Softs and Cereals etc.

16 | P a g e

RESEARCH METHODOLOGY

Research Type-Descriptive

Sample DesignIn this study convenient random sampling method is used to select the respondents. The sample size is 30 respondents.

Source of DataThe various sources of data are

1. Primary Sources, which includes questionnaire.2. Secondary data which includes books , internet etc.

Tools for Data CollectionThe questionnaire is the tool used for data collection.

Analyses and InterpretationThe various tools for analysis used are graphs, charts, percentage growth.

17 | P a g e

18 | P a g e

QUESTIONERE ANALYSES

In this section the data obtained through the questionnaire from the investors in commodity futures isanalyzed

SECTION A:

Sex profile

Male Female0%

10%20%30%40%50%60%70%80%90%

Column Chart Showing Sex Profile Of The Respondents

Column1

Sex

Perc

enta

ge

Findings

From the above table and chart, it can be seen that 80% of the respondents were male, and 20% werefemale.

InterpretationIt can be concluded that mainly males invest in commodity futures.

19 | P a g e

Sex No of Respondents Percentage

Male 23 80%

Female 6 20%

Age Profile

Age Group No. of Respondents

Percentage

20-30 years 13 43%30-40 years 9 30%40-50 years 5 17%50 years and above

3 10%

43%

30%

17%

10%

Pie Chart Showing Age Profile Of The Respondents

20-30 Years30-40 Years40-50 Years50 Year and above

Findings

From the above table and chart, it can be seen that 43% of the respondents were in the age group of 20-30 years, 30% were in the age group of 30-40 years, and 17% were in the age group of 40-50 years and 10% inthe age group of 50 years and above.

Interpretation

20 | P a g e

It can be concluded that mainly the young people have invested commodity futures.

Education profile:

EducationalQualification

No. of Respondents

Percentage

Higher Secondary

3 10%

Graduate 15 50%Post Graduate 12 40%

10%

50%

40%

Pie Chart Showing Educational Profile Of The Respondents

Higher SecondaryGraduatePost Graduate

Findings

From the above table and chart, it can be seen that 50% of the respondents were graduates, 40% were post graduates and only 10 percent were studied up to higher secondary.

21 | P a g e

InterpretationIt can be concluded that mainly the young

graduates have invested commodity futures. But in real market this doesn’t stand true.

Occupation ProfileOccupation No. of

RespondentsPercentage

Government Employee

1 3%

Private SectorEmployee

9 30%

Self-Employee 5 17%

Businessmen 10 33%

Commodity FuturesAdvisor

5 17%

Others 0 0%

3%

30%

17%

33%

17%

Pie Chart Showing Occupational Profile Of The Respondents

Government Employee

Private Sector

Self-Employee

Businessmen

Commodity Futures

Others

22 | P a g e

Findings

From the above table and chart, it can be seen that 3% of the respondents were government employees, 30% were private sector employee, 17% were Self-Employed and 33% were businessmen, 17% wereCommodity futures advisors.

InterpretationIt can be concluded that mainly businessmen and

private sector employees invest in commodities.

Income Profile

Income Group No. of Respondents

Percentage

Below Rs. 4 Lakh

11 37%

Rs. 4 – 10 Lakh

18 60%

Rs. 10 – 25 Lakh

1 3%

Above Rs. 25 Lakh

0 0%

37%

60%

3%

No. of Respondents

Below Rs. 4 LakhRs. 4 – 10 LakhRs. 10 – 25 LakhAbove Rs. 25 Lakh

23 | P a g e

Findings

From the above table and chart, it can be seen that 37% of the respondents were in the income group of below Rs. 4 lakh, 60% were in the income group of Rs. 4-10 lakh, and 3% were in the income group of Rs. 10-25 lakh.

Interpretation

It can be concluded that most of the people who have invested commodity futures are in the income groupof Rs.4-10 lakh.

SECTION B

1) Have you invested in commodity futures?

Particulars No. Of Respondents

Percentage

Yes 20 67%

No 10 33%

24 | P a g e

Yes No0%

10%

20%

30%

40%

50%

60%

70%

80%

Column Chart Showing The Percentage of Re-spondents who have Invested In Comodity Future

Column1

Particular

Perc

enta

ge

FindingsFrom the above table and chart, it can be seen that 67% of the

respondents have invested in commodity futures, and 33% have not invested in commodity futures

InterpretationIt can be concluded that most of the respondents

have invested in commodity futures.

2) What is your Experience in your previous Investment ?

Particulars No. Of Respondents

Percentage

Good 15 50%

Bad 9 30%

Reasonable 6 20%

25 | P a g e

Good Bad Reasonable0%

10%

20%

30%

40%

50%

60%

Column Chart Showing The Experience of Respondents in Their Previous Investment

Column1

Particular

Perc

enta

ge

FindingsIt can be seen that 50% of the respondents had a good experience in their previous investment, 30% had a reasonable experience in their previous investment and 20% had a bad experience in their previous investment.

InterpretationIt can be concluded that most of the respondents

had a good experience in their previous investment.

3) What is your objective for trading in commodity futures?

Particulars No. Of Respondents

Percentage

Less Risky Investment

10 33%

Diversification of Portfolio

12 40%

Very Good Returns

6 20%

26 | P a g e

Others 2 7%

Less R

isky I

nvestm

ent

Diversi

fication of P

ortfolio

Very Good Retu

rns

Others0%5%

10%15%20%25%30%35%40%45%

Column chart showing the objective of the investor to invest in commodity futures

Column1

Particular

Perc

enta

ge

FindingsIt can be seen that out of the investors in commodity futures, 33%

of them have invested with the objective a less risky investment, 40% of them invested with the objective of diversifying hid portfolio and 20% of them due to the expectation of very good returns and 7% have invested due to other reasons.

InterpretationIt can be concluded that most of the investors in

commodity futures, have invested with the objective ofdiversifying their portfolio and to reduce risk .

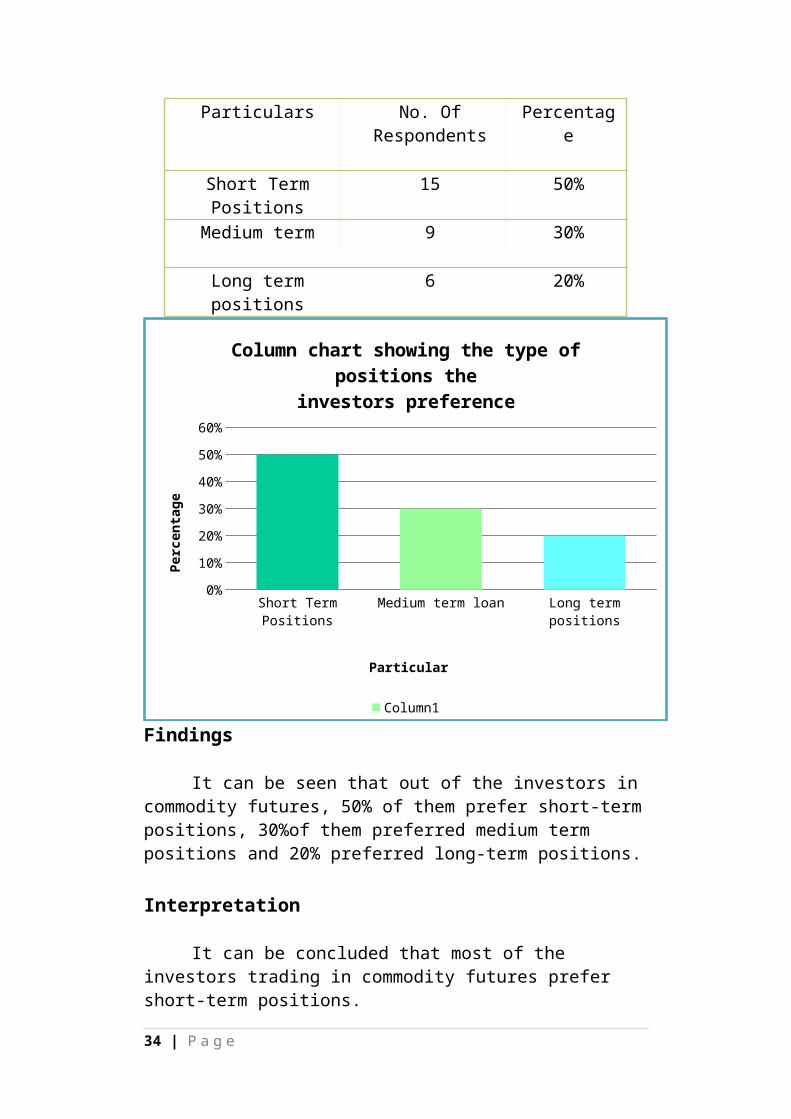

4) What type of trade do you prefer the most?

27 | P a g e

Particulars No. Of Respondents

Percentage

Short Term Positions

15 50%

Medium term 9 30%

Long term positions

6 20%

Findings

It can be seen that out of the investors in commodity futures, 50% of them prefer short-term positions, 30%of them preferred medium term positions and 20% preferred long-term positions.

Interpretation

It can be concluded that most of the investors trading in commodity futures prefer short-term positions.

5) Which commodities have you traded in, the most?

30%

17%20%

13%

10%

10%

No. Of Respondents

WheatCottonGoldSoybeanSilverCopper

FindingsIt can be seen that out of the investors in commodity futures, 30%

of them have traded mostly in wheat, 17% of them traded in cotton, 20% in Gold, 13% in soybean and 10% each in copper and silver, .

28 | P a g e

Commodity No. Of Respondents

Percentage

Wheat 9 30%

Cotton 5 17%

Gold 6 20%Soybean 4 13%

Silver 3 10%Copper 3 10%

InterpretationIt can be concluded that the mostly traded

commodity is wheat, followed by gold and cotton. Copper is the least traded commodity.

6) What percentage of savings have you invested in commodity futures?

Particulars No. Of Respondents Percentage

0-10% 3 10%

10-20% 9 30%

20-30% 12 40%

30-50% 3 10%

50% and above 3 10%

10%

30%

40%

10%

10%

Pie chart showing the percentage of savings the investors has made in commodity futures

0-10%10-20%20-30%30-50%50% and above

Findings

29 | P a g e

It can be seen that, 40% of the investors have invested between 20-30% of their savings in commodity futures, 30% of them have invested between 10-20% of their savings and total 20% of them have invested above 30% of their saving in commodity futures.

InterpretationIt can be concluded that most of the investors have

invested between 20-30% of their savings in commodity futures.

7) What do you think of the return derived from commodity futures?

Particulars No. Of Respondents

Percentage

Good 18 60%

Reasonable 8 27%

Bad 4 13%

30 | P a g e

Good Reasonable Bad0%

10%

20%

30%

40%

50%

60%

70%

Column chart showing the extent of returns derived by the investors from

commodity futures

Column1

Findings

It can be seen that, 60% of the investors feel that they got good returns from commodity futures trading, 27% of them feel that they got reasonable returns commodity futures, 13% of the investors felt they got bad returns from commodity futures.

InterpretationsIt can be concluded that most of the investors got good returns

from commodity futures.

8) Do you think commodity future is a good investment opportunity?

Particulars No. Of Respondents

Percentage

Yes 21 70%

No 9 30%

31 | P a g e

Yes No0%

10%

20%

30%

40%

50%

60%

70%

80%

Column chart showing opinion of the investor of whether commod-

ity futures is a good investmen-topportunity

Column1

FindingsFrom the above table and chart, it can be seen that 70% of the investors feel that commodity futures is a good investment opportunity, and 30% investors feel that commodity futures is not a good investment opportunity

InterpretationIt can be concluded that most of the investors feel

that commodity futures is a “good investmentopportunity”

9) Which type of trader you are?

Particulars No. Of Respondents

Percentage

Hedgers 13 43%

Speculator 6 20%

32 | P a g e

Arbitrager 11 37%

FindingsFrom the above table and chart, it can be seen that most of respondents

are hedger and arbitrager

InterpretationIt can be concluded that most of the respondents are

hedgers

10) In which commodities you would like to invest in future and why?

Particulars No. Of Respondents

Percentage

33 | P a g e

Wheat 15 50%

Cotton 9 30%

Gold 6 20%

FindingsFrom the above table and chart, it can be seen that 50% of the

respondents want to invest in wheat and 30% want to invest in cotton commodity futures

InterpretationIt can be concluded that most of the respondents want

to invest in wheat commodity futures.

11)factors you take into consider while invest in commodities?

Particulars No. Of Respondents

Percentage

Global economy

10 33%

34 | P a g e

Availability 14 47%

others 06 20%

FindingsFrom the above table and chart, it can be seen that 33% of the

respondents consider global economy as a factor before investing commodity future 20% consider inOther factors in commodity futures.

InterpretationIt can be concluded that most of the respondents

consider availability of commodities in commodity futures

FINDINGS

From the analysis made the following findings can be derived:

There is awareness of commodity market in the eyes of investors.

35 | P a g e

Investors consider factor like global economy.

Person between age of 20-40 years are more active player in the commodity trading and 10-30 % of their income are invested in market. Most of them believe that return derived from commodity are good and reasonable.

There has been seen that most of private sector employees and business person invests in commodity marketIt has been that, respondents are investing their income in diversified portfolio and less risky assets and 50% of respondent takes short position in the market.

There has been seen that gold, wheat and cotton are more dealing commodity and investor believe that commodity market have good opportunist market in future and most of investor invest when there is favorable price in market.

CONCLUSION

36 | P a g e

Now a days investor become more careful in investment with considering the factor like global economy, availability of commodity etc..

In the trading system people consider above factor for investment so we can conclude that investor are more moving towards the exchange traded market

It can be concluded that one can use commodity futures for the hedging purposes rather than for the speculative

Thus, commodity futures are a growing market.

from all the above conclusions of it can be concluded,“commodity futures can beused as a risk reduction and a sound investment instrument”

RECOMENDATATIONS

37 | P a g e

Since commodity futures are a new concept, more awareness must be created by marketing this investment instrument appropriately.

As commodity market are growing so one should trade in exchange traded market rather than the OTC market.

As commodity market growing so all groups of people must be asked to invest in commodity futures.

one should take better position with the help of fundamental and technical analysis

It is not a necessity that one must be very educated to invest in commodity futures. So, it is recommended that those who are not so well educated also can invest in commodity futures.

It is recommended that now a days investor should invest in agriculture commodity because within the few days few of agriculture commodity are coming up with huge quantity.

38 | P a g e

QUESTIONNAIRE39 | P a g e

PART – A

1) Name:

2) Sex:

Male Female

3) Age:

20-30 Years 30-40 years

40-50 years Above 50 years

4) Education:

Higher secondary Graduation

Post-graduation

5) Occupation:

Government employee Self-employee

Commodity futures analyst Private sector employee

Businessman Others ____________

6) Income:

Below 4 lakh 4,00,001 – 10,00,000

10,00,001 – 25,00,000 Above 25,00,000

40 | P a g e

PART – B

1) Have you invested in commodity futures?

Yes No

2) What is your experience in your previous investment (excluding commodity futures)?

Good Reasonable Bad

3) What is your objective when trading in commodity futures?

Less risky investment Diversification of portfolio

Very good returns Others ______________

4) What type of trade do you prefer the most?

Short Term Position Medium Term Position

Long Term Position

5) Which commodities have you traded in the most?

a. _________________b. _________________c. __________________

6) What percentage of savings have you invested in commodity futures?

0-10% 10-20%

20-30% 30-50%

50% and above

7) What do you think of the return derived from commodity futures?

41 | P a g e

Good Reasonable Bad

8) Do you think commodity future is a good investment opportunity?

Yes No

9) which type of trader you are?

Hedger speculator arbitrager

10) In which commodities you would like to invest in future and why?

__________________________________________

11 Factors you take into consider while invest in commodities?

__________________________________________

42 | P a g e

BIBLIOGRAPHY

Websites

www.rbi.orgwww.sebi.comwww.mcx.comwww.investopedia.com

43 | P a g e