Antipodes LIC roadshow - long (web) · This presentation is not, ... LIC background First LIC...

48

Confidential / 1

Transcript of Antipodes LIC roadshow - long (web) · This presentation is not, ... LIC background First LIC...

Confidential / 1

Confidential / 2

Disclaimer

This presentation has been prepared by Antipodes Global Investment Company Limited (APL). The information contained in this presentation is for information purposes only and has been

prepared for use in conjunction with a verbal presentation and should be read in that context.

The information contained in this presentation is not investment or financial product advice and is not intended to be used as the basis for making an investment decision. Please note that, in

providing this presentation, APL has not considered the objectives, financial position or needs of any particular recipient. APL strongly suggests that investors consult a financial advisor prior to

making an investment decision.

This presentation is strictly confidential and is intended for the exclusive benefit of the institution to which it is presented. It may not be reproduced, disseminated, quoted or referred to, in whole

or in part, without the express consent of APL.

No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information, opinions and conclusions contained in this presentation.

To the maximum extent permitted by law, none of APL, its related bodies corporate, shareholders or respective directors, officers, employees, agents or advisors, nor any other person accepts

any liability, including, without limitation, any liability arising out of fault or negligence for any loss arising from the use of information contained in this presentation.

This presentation includes “forward looking statements”. Such forward-looking statements are not guarantees of future performance and involve known and unknown risks, uncertainties and

other factors, many of which are beyond the control of APL and its officers, employees, agents or associates that may cause actual results to differ materially from those expressed or implied in

such statement. Actual results, performance or achievements may vary materially from any projections and forward looking statements and the assumptions on which those statements are

based. APL assumes no obligation to update such information.

This presentation is not, and does not constitute, an offer to sell or the solicitation, invitation or recommendation to purchase any securities and neither this presentation nor anything contained in

it forms the basis of any contract or commitment. APL’s offer of securities is made pursuant to a replacement prospectus issued by APL and dated 4 August 2016, which describes the terms of

the offer (Offer Document). This Offer Document is available http://antipodespartners.com/. Prospective investors should consider the Offer Document in deciding whether to acquire securities

in APL under the offer. Prospective investors who want to acquire securities under the offer will need to complete an application form that is in or accompanies the Offer Document.

This presentation does not constitute an offer to sell, or a solicitation of an offer to buy, any securities in the United States. The securities of APL have not been, and will not be, registered under

the U.S. Securities Act of 1933, as amended (Securities Act) or the securities laws of any state or other jurisdiction of the United States, and may not be offered or sold in the United States except

in compliance with the registration requirements of the Securities Act and any other applicable securities laws or pursuant to an exemption from, or in a transaction not subject to, the registration

requirements of the Securities Act and any other applicable securities laws.

NOT FOR DISTRIBUTION IN THE UNITED STATES

Confidential / 3

• Why Listed Investment Companies?

• Why Global Equities

• Introducing Antipodes Global Investment Company

• Antipodes Partners

Agenda

Confidential / 4

Why Listed Investment Companies?

Confidential / 5

LIC background

First LIC launched in 1923

Currently 78 LICs trading on ASX managing $28.5bn FUM

Market capitalisation of the sector has grown at 10.4% over 15 years and 11.4% over 5 years

Inflow of new capital has been well supported with the LIC sector trading at a 1.0% premium to its net tangible assets (NTA)

Strong growth has been underpinned by FoFA and SMSFs

The ASX LIC composition is 85% Australian equities and only 9% global equities

Source: ASX Data

Confidential / 6

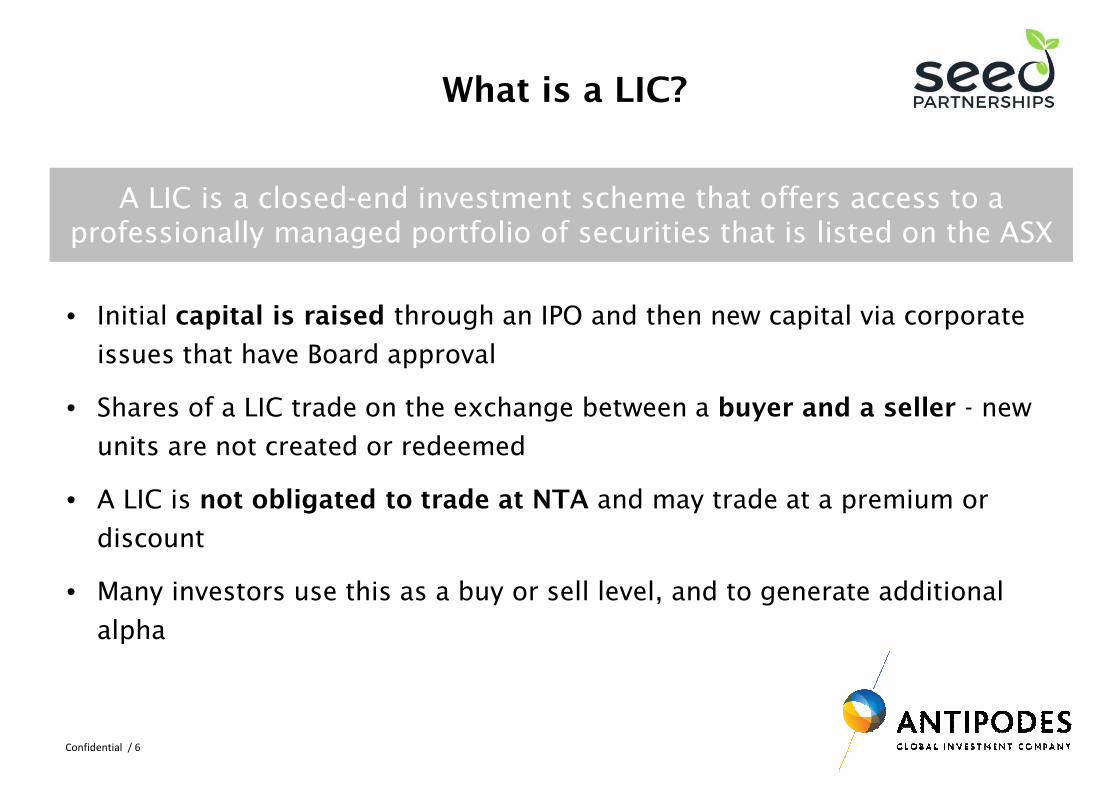

• Initial capital is raised through an IPO and then new capital via corporate

issues that have Board approval

• Shares of a LIC trade on the exchange between a buyer and a seller - new

units are not created or redeemed

• A LIC is not obligated to trade at NTA and may trade at a premium or

discount

• Many investors use this as a buy or sell level, and to generate additional

alpha

What is a LIC?

A LIC is a closed-end investment scheme that offers access to a professionally managed portfolio of securities that is listed on the ASX

Confidential / 7

A LIC portfolio manager is able to focus on maximising long-term investment

performance and consistent fully franked income.

• Stable capital base: Not exposed to inflows and outflows, and able to earn a

compound return from retained earnings

• Tax aware vehicle: Tax paying entity that is incentivised to maximise post

tax performance including franking credits

• Supports consistent fully franked income: Dividends are announced at the

discretion of the board, and can be smoothed through the investment cycle

Performance and income

A Unit Trust must distribute all capital gains and income annually, which often make distributions variable and complicate tax planning

for investors

Confidential / 8

Why Global Equities?

Confidential / 9

The global opportunity set is vast

• Across the globe there are ~8,000 companies over US$1b, compared with ~150 in Australia

Australia2%

Rest of the World98%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Olympic Medals

Consumer Discretionary

Consumer Staples

Energy

Financials

Healthcare

Industrials

Technology

Materials

Telecom

Utilities

Australia World

Source: Bloomberg, Antipodes

Global investment universe – Australia % of World

Australia represents just 2% of the investible universe

Confidential / 10

Global investing opens a world of opportunities

Socio-Macro Sector

European restructuring &reflation

Telecom, aerospace, financials

Korean governance reform Hardware, autos, financials

Indian macro/political reform

Infrastructure, property, financials

Donald Trump … ‘nuff said

Sector Thematic

Technology Cloud, big data/internet of things, cyber-security

Industrials/durables Nanotechnology, 3D printing, electric vehicles/autonomous driving

Healthcare Biologics, oncology, rare disease

Consumer/content Emerging middle class, social media, augmented reality

Financials Online disruption, blockchain, peer-to-peer lending

Energy Alternatives, storage, smart-grid

Confidential / 11

Opportunity to diversify Australian risk

Are Aussie investors crowding?

0x

5x

10x

15x

20x

All stocks > $1b (excluding resources & financials)

20

17

PE

Australia US ROW

Global equity returns (10Y annualised)

-10%

-5%

0%

5%

10%

15%

20%

19

97

19

98

19

99

20

00

20

00

20

01

20

02

20

03

20

03

20

04

20

05

20

06

20

06

20

07

20

08

20

09

20

09

20

10

20

11

20

12

20

12

20

13

20

14

20

15

20

15

10

Y R

OLLIN

G R

ET

URN

(P.A

.)

Contribution from AUD Contribution from MSCI ACWI (USD)

But hardly the longer term pattern...

Source: Factset, Antipodes

Commodities boomabnormally strong AUD detracted

from global equity returns

Confidential / 12

Global as a risk reducer

• An allocation to global equities can offer significant diversification benefits, not available in the

local market

Source: Bloomberg, Antipodes

4%

9%

14%

19%

24%

199

3

199

4

199

5

199

6

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

VO

LA

TIL

ITY

Rolling 1Y Volatility

World Australia

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

CO

RRELA

TIO

N

Australia's correlation to global markets1991 - 2016

“Don’t confuse lack of volatility with stability, ever” – Nassim Taleb

Confidential / 13

Blending reduces overall volatility

Source: Bloomberg, Antipodes

100% Australia

100% Global

11%

11%

12%

12%

13%

13%

14%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

VO

LA

TIL

ITY

ALLOCATION TO AUSTRALIAN SHARES

An allocation to global equities can reduce risk ☺

Confidential / 14

Introducing

Antipodes Global Investment Company

Confidential / 15

Terms of the Offer

Company name Antipodes Global Investment Company LimitedInvestment Manager Antipodes Partners LimitedASX Codes Shares APL

Options APLO

Offer Price $1.10 per ordinary share

Issue Size Min $100m

Max $220m

Overs $330mOffer Close (exp) Broker Firm 23 Sep 16

General Offer 30 Sep 16

Shares Trading 18 Oct 16Options Conditions 1 option per ordinary share

Strike Price, Expiry $1.10, 15 Oct 18

Investment Fees Management Fee 1.1% (plus GST) per annum

Performance Fee 15% (plus GST) out-performance v MSCI ACWISyndicate Corporate Advisor Seed Partnerships

Lead Arranger National Australia BankJoint Lead Managers Morgans CIMB

Morgan Stanley

Ord Minnett

Taylor Collison

Co-Managers Bell Potter Securities

JB Were

Wilsons

Confidential / 16

Jonathan Trollip Jonathan is an experienced Director with over 30 years experience. He is presently non-executive chairman of Future Generation Investment Company Limited and Global Value Fund Limited, and a non-executive director of Elemental Minerals. Jonathan has worked as a principal of Meridian and prior to that was a Partner with law firm Herbert Smith Freehills.

Independent Chairman

Chris Cuffe Chris has more than 25 years of experience in building successful wealth management practices. He is presently Chairman of UniSuper and Fitzpatrick Private Wealth and founder/producer of Cuffelinks. Chris has worked extensively in the wealth management industry and was the CEO of Challenger Financial Services Group, and Colonial First State.

Independent Director

Lorraine Berends Lorraine has worked for over 30 years in the superannuation and funds management industry. She presently serves on the BT Financial Group Superannuation Board and MDC Foundations, and is a member of the investment committee at QSuper. She served on the Board of the Association of Superannuation Funds of Australia for 12 years and the Board of the Investment Management Consultants Association for 13 years.

Independent Director

Alex Ihlenfeldt Alex has 25 years commercial experience in financial services. Alex is currently COO and CFO of Pinnacle Investment Management Limited with whom he has been associated with since its inception in 2006. Prior to joining Pinnacle in 2011, he spent 10 years with the Wilson HTM Investment Group as COO, CFO and Head of Wealth Management.

Non-Independent Director

Andrew Findlay Andrew joined Pinnacle as an equity partner in 2009. He is a Director of Antipodes Partners Limited and Pinnacle Fund Services Limited which acts as responsible entity or trustee for pooled funds managed by Pinnacle’s affiliated managers. Before joining Pinnacle, Andrew worked in a variety of financial marketing roles with Macquarie Bank, Deutsche Bank and UBS across Australia, Hong Kong, Zurich and London.

Non-Independent Director

Board comprises a majority of Independent Directors

Confidential / 17

Roadshow presentation series

Auckland Euro Bar 7:30-9:30

Shed 22, Princes WharfAuckland

25 August 2016

Wellington Rydges Wellington 7:30-9:30

75 Featherstone StPipitea, Wellington

26 August 2016

Perth Parmelia Hilton 10:00-11:00

14 Mill StreetPerth

31 August 2016

Melbourne Morgans at 401 10:00-11:00

401 Collins StreetMelbourne

1 September 2016

Sydney Wesley Conference Centre 10:00-11:00

220 Pitt StreetSydney

6 September 2016

Brisbane The Novotel Brisbane 10:00-11:00

200 Creek Street Brisbane

8 September 2016

Adelaide The Hilton Adelaide 10:00-11:00

233 Victoria SquareAdelaide

12 September 2016

Meetings are also being hosted in Albury, Canberra, Gold Coast, Hobart, Newcastle, Norwest, Sunshine Coast, Toowoomba, Townsville and Wollongong

Confidential / 18

• Pragmatic value manager of global equities (typically 30-50 long holdings)

• Founded March 2015 by Jacob Mitchell (formerly Deputy CIO of Platinum), team

includes five former colleagues

• Jacob Mitchell track-record: Platinum (2000 to 2014), at time of resignation over

$3.5bn under direct portfolio management and responsible with CIO for firm-wide

process implementation

Introducing Antipodes PartnersHigh conviction, capital preservation focus

Fund Period Alpha

Platinum International Fund 3.5 years (to Nov 14) Sub-portfolio, track record not publicly disclosed

Platinum Unhedged Fund 7 years (to May 14) +5.7% p.a. (after retail fees)

Platinum Japan Fund 6.5 years (to Nov 14) +9.9% p.a. (after retail fees)

Confidential / 19

Antipodes Partners’ track-record

*Source: Morningstar Direct

Alpha generation at below market levels of risk

Confidential / 21

Andrew Baud

Deputy Portfolio Manager

Graham Hay

Deputy Portfolio Manager

Christine Ong

Investment Analyst

James Rodda

Investment Analyst

Rameez Sadikot

Head of Quant/Macro

Cleo Somers

Investment Analyst

Jacob Mitchell

CIO and Portfolio Manager

Sunny Bangia

Head of Execution

Chris Connolly

Investment Analyst

Consumer, healthcare

Technology,content,

communications

Property, durables,

Asia

Service,Asia

Global socio-macroeconomic

currency

Consumer, healthcare

GlobalFinancials,

infrastructure, currency

Industrials, commodities

Plus Associate Quantitative Analyst and Associate Investment Analyst

Firm overviewOver 100 years of experience with significant shared history of investing

• Non-investment functions outsourced to minority owner Pinnacle Investment Management ($21Bn FUM across seven boutique managers)

• Structured to reinforce strong alignment between investors and the investment team

• FUM has grown from ~$200m at inception to ~$1Bn*

* As at 5 September 2016

Confidential / 22

Our philosophyTake advantage of markets’ tendency for irrational extrapolation

around change (cyclical, structural, socio/macro)

Business

Resilience

Starting valuation

Investment returns

Margin of Safety Multiple ways of winning

Confidential / 23

Sources of alpha

Example: Cisco Systems

Product cycle

Cyclical/structural growth insoftware defined networking,security, collaboration and IoT

Management

New CEO commitment to returnhalf of FCF to shareholders

Competitive dynamics

Incumbent with customer lock, captures 67% of global profit pool

Responding to threats, sells solutions not hardware

Regulation

Cybersecurity a keyaddressable market

Style

Rare “inexpensive defensive”

Macro

Sensitivity to corporatecapex

Multiple ways of winning

Confidential / 24

Portfolio levelSeek clusters of non-correlated alpha, some examples …

Korea - neglected market, generational change

US software incumbents - disruption fears overstated

Banks - neglected sector, select for cost leadership and

growth

US natural gas - cyclical recovery opportunity

China/India consumer - macro fears overstated

Short - beneficiaries of high yield debt bubble

Confidential / 25

Longs Shorts Currency

Multiple levers

• Typically 30–50 holdings

• Incumbents entering

recovery phase

• Disruptors at the

inflection point of

mainstream adoption

• Opposite logic to longs

• Take advantage of self-

reinforcing cycles

• Manage timing risk via

position sizing

• Identification of

significant over/under

valuation

• Sovereign risk assessment

• Requires higher margin

of safety than for longs

A high conviction, capital preservation outcome

Confidential / 26

-3

-2

-1

0

1

2

3

19

87

19

87

19

88

19

89

19

89

19

90

19

90

19

91

19

91

19

92

19

93

19

93

19

94

19

94

19

95

19

96

19

96

19

97

19

97

19

98

19

98

19

99

20

00

20

00

20

01

20

01

20

02

20

03

20

03

20

04

20

04

20

05

20

05

20

06

20

07

20

07

20

08

20

08

20

09

20

10

20

10

20

11

20

11

20

12

20

12

20

13

20

14

20

14

20

15

20

15

20

16

Z S

CO

RE

Investors are over-paying for Profitability and Growth

Profitability, Growth and Value are composite factors

Source: Antipodes Partners

Z Score (median EV/CE of upper quintile relative to lower quintile)

Look for cheaper, more eclectic expressions of profitability and growth

Profitability

Growth

Value

Confidential / 27

Global valuation clusteringPrice to Book relative to World vs. 21 year trend (z-score)

Region and sector defined by Antipodes Partners

Software, a cheaper global defensive

China/HK staples, cheap versus an expensive global peer group

Confidential / 28

China Resources Beer (CRB) – world’s largest beer brand

Beer sold(bL)

Valuation(US$b)

China Resources Beer 12.8 6

Fosters 0.7 121

Multiple of Fosters 18x 0.5x

Summary

• 22% volume share, over 50% more than second and third players

• Premiumisation opportunity - Average selling price of beer in China is 75% lower than Australia

Multiple ways of winning

• Premiumisation and consolidation drives higher prices and lower costs

• Great long-term opportunity for margins to normalise to global peers

Margin of safety

CRB sells 18x as much beer as Fosters at half the valuation!

1 SABMiller 2011 takeover

Long

Confidential / 29

Global valuation clusteringPrice to Book relative to World vs. 21 year trend (z-score)

Region and sector defined by Antipodes Partners

Financials, commodities –value or value trap?

Confidential / 30

0%

1%

2%

3%

4%

Germany Spain Italy France Australia Poland Turkey Romania

CO

STS /

TO

TA

L A

SSETS ING Market

ING Groep – a leader in digital distributionBuy the EU’s fastest growing bank at a discount!

Summary

• Dominant Northern European retail banking

franchise

• Like Australia, Netherlands is an

oligopolistic banking market

Multiple ways of winning

• Low cost disruptive internet banking model

e.g. Australia’s 6th largest mortgage player

• Asset reflation in Northern Europe

Margin of safety

• 0.8x book for 10.5% RoE (vs. EU bank avg.

of 1.0x and 8.0% RoE)

• Attractive 6.5% yield that can grow

Source: ING

A structural cost advantage over peers...

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

200

1

200

2

200

2

200

3

200

3

200

4

200

4

200

5

200

5

200

6

200

6

200

7

200

7

200

8

200

8

200

9

200

9

201

0

201

0

201

1

201

1

201

2

201

2

201

3

201

3

201

4

201

4

201

5

201

5

201

6

Price to book: CBA v. ING Groep

CBA

ING

Long

Confidential / 31

US high yield debt, a growing risk

18%

19%

20%

21%

22%

23%

24%

25%

26%

27%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.01

98

6

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

$ t

rnUS high yield issuance

HY market size + bank loans (L)HY issuance as a % of corporate debt outstanding (R)

Short the expensive equity beneficiaries of this bubble:

• Leveraged cyclical businesses approaching the shake-out phase, e.g. Equipment rental, Auto

dealerships

• Over-hyped disruptors with deteriorating fundamentals, e.g. Biotechs, Cloud and Social

• Low volatility, bond proxies favoured by passive strategies that confuse momentum with value and low

volatility with quality, e.g. Tower companies priced for the illusion of duration

Source: Deutsche Bank, Antipodes Partners

Subprime mortgage market peaked at $1.3trn, HY market is 2.5x the size!

Short

Confidential / 32

Currency - Risk to be managed AND profit opportunity

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

RUB BRL NOK IDR EUR AUD MYR CAD KRW JPY HKD THB GBP INR USD SGD CNY

Devia

tion f

rom

20Y t

rend

fundam

enta

ls

Antipodes currency valuation

Cheap

Expensive

• Renminbi (CNY) has appreciated by 50% against trading partners on a real basis over 10yrs

• Norwegian Kroner (NOK) oil exposed, but cheap, saved the commodity dividend - strong “balance

sheet”

Source: Antipodes Partners

Why hedge to AUD if there are cheaper alternatives?

Currency

Confidential / 33

Investment performance: Antipodes Global Fund1

Absolute performance

Antipodes Global Fund (after fees2

) 7.4%

MSCI AC World Net Index -0.6%

Outperformance after fees 8.0%

Up-market capture 91

Down-market capture 48

Past performance is not a reliable indicator of future performance.1 12 months to 30 June 20162 1.20% plus 15% of outperformance (net of the base fee)3 Based on gross returns to 30 June 2016

Contribution to absolute performance3

Longs 4.0%

Shorts 4.0%

Currency/Liquidity 0.5%

Confidential / 35

Summarising our competitive advantage

High conviction, pragmatic value approach

Track record of alpha generation at below market levels of risk

Ability to profit from three levers -> longs, shorts and currency

Confidential / 36

Why Antipodes Global Investment Company?

• Portfolio -> high conviction, capital preservation focus

• Independent and qualified board -> rational capital management

• Liquidity -> $100m minimum offer to improve market depth and cover fixed

costs

• Clear communication -> bi-annual roadshow, monthly commentary, quarterly

reports, webinars, blogs etc.

• Competitive fee structure -> compared to Antipodes Global Fund unit trust

and competitors

• Option value for IPO subscribers -> 2 years to exercise

Confidential / 37

Portfolio positioning1

1 Antipodes Global Fund holdings as at 30 June 2016

Broad Sector Exposure Investment Rationale Examples Long Net Bench.

Global Cyclical 33.0 25.2 28.1

Hardware Next generation of foldable devices, AMOLED, 3D NAND Samsung Electronics 10.1 9.5 7.2

CommoditiesCheap, low cost oil and gas producers and services;Short expensive high cost oil producers and services

Consol. Energy 16.9 12.6 11.1

Industrials Product cycle and capital management optionality Hyundai Motors 6.0 3.1 9.9

Global Defensive 27.3 19.0 29.2

Software/ContentEvolving incumbents that are cheap due to fears regarding disruption

Cisco Systems, Baidu 16.9 14.4 8.1

Staples – DevelopedShort as downtrading, online/private label competition not discounted

Various 0.5 -2.2 9.1

Staples – EmergingChinese beer/liquor premiumisation opportunity, deep recession discounted

China Resources Beer 5.9 3.9 0.3

Healthcare Select exposures in an otherwise expensive sector 4.0 3.3 11.6

Domestic Cyclical 8.0 0.8 14.4

Developed Cheap growers with limited exposure to structural head-winds of down trading and increased online competition

Amerco, Japan housing 5.1 -1.1 13.1

Emerging Online retail/services 2.9 2.0 1.3

Domestic Defensive 8.0 6.2 10.9

DevelopedThirst for yield ongoing; net short high yield debt beneficiaries

Tower companies 3.3 1.5 9.7

Emerging Cheap defensive growth with yield support China Mobile 4.7 4.7 1.2

Financials 12.8 9.8 16.8

Developed Cheap, well capitalised banks with pricing powerKB Financial, ING Groep, Capital One Financial

10.4 8.0 14.5

EmergingCheap Indian structural financial services growth; no exposure to Chinese "national service" value traps

ICICI Bank 2.4 1.8 2.3

PreciousOperational recovery progressing, now more dependent on gold price outcome

1.9 1.9 0.6

Total - Sector 90.9 62.9 100.0

Confidential / 39

Appendix

Confidential / 40

Mandate information

• Typical net equity exposure: 50-100%

• Max gross exposure: 150%

• Stock shorting: permitted

• Derivatives: permitted

• Currency management: permitted

• Benchmark: MSCI AC World Net Index in AUD

Confidential / 41

Cisco Systems – a pillar of global networking

Summary

• Cisco won’t be disrupted -> Sells solutions

not devices

• Captures 67% of global networking profits

Multiple ways of winning

• Cyclical upgrade cycle

• Structural growth in software defined

networking, security and collaboration

• Internet of Things

• Commitment to return half of FCF to

shareholders

Margin of safety

• Incumbent with strong customer lock

• 11x PE (vs 20x for comparable companies)

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

4.5x

5.0x

8

13

18

23

28

33

200

4

200

4

200

5

200

5

200

6

200

6

200

7

200

7

200

8

200

8

200

9

200

9

201

0

201

0

201

1

201

1

201

2

201

2

201

3

201

3

201

4

201

4

201

5

201

5

201

6

EV/ Sales vs. World (Right)

Source: Antipodes Partners, Factset

“Nobody ever got fired for buying IBM Cisco”

Price (left)

Long

Confidential / 42

0

250

500

750

1000

1250

1500

1750

2000

45

50

55

60

65

70

75

80

85

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

Rig

Count

Gas P

roducti

on (Bcf/

d)

US gas production and rig count

Production

Rig Count (R)

US natural gas – A forgotten commodity

Source: EIA, Antipodes Estimates

Summary

• Current state of over supply has seen gas

prices fall by ~50% since 2013

Multiple ways of winning

• High decline rate (~22% p.a.)

• Material reduction in new investment

• Robust demand growth underpinned by

price sensitive electricity utilities

switching from coal to cheaper gas and

LNG exports

Margin of safety

• Current gas price ($2.8/mmBtu) well

below marginal cost of new production

(est. $4.50/mmBtu)

Confidential / 43

The Chinese credit hangover

• Since 2008 debt has expanded by 80% of GDP, underwritten by thinly capitalised, smaller banks in the

riskiest projects

• Corporates/SOEs have borrowed the most

• Household and government balance sheets are relatively healthy

• On our estimate of the credit gap, a 35% NPL cycle (the level reached in 2000) could be absorbed by the

national balance sheet

100

150

200

250

300

199

5

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

201

0

201

1

201

2

201

3

201

4

201

5

% o

f G

DP

China non-financial debt to GDP

0

100

200

300

400

500

China US Korea UK Eurozone Japan

% o

f G

DP

Govt. Corporate Household

Domestic non-financial debt to GDP

Source: 2014, UBSSource: BIS

Beware the impact of national service and building internal pressure

Confidential / 44

*Source: Morningstar Direct

Confidential / 45

More information

Arranger and Joint Lead ManagerNicholas Chaplin Matthew JohnsonNational Australia Bank National Australia Bank

Tel: +61 401 194 448 Tel: +61 459 800 [email protected] [email protected]

Other Joint Lead ManagersPhillip Lee Hamish Head Ross Baildon Hamish NairnMorgan CIMB Morgan Stanley Ord Minnett Taylor Collison

Tel: +61 411 130 514 Tel: +61 422 621 888 Tel: +61 7 3214 5509 Tel: +61 8 8217 [email protected] [email protected] [email protected] [email protected]

Co-Lead ManagersTim Griffin Steve Zilioli John Lockton

Bell Potter JBWere Wilsons

Tel: +61 2 8224 2841 Tel: +61 414 588 953 Tel: +61 488 089 [email protected] [email protected] [email protected]

Investment ManagerJacob Mitchell Graham Hay Andrew Baud Sunny BangiaAntipodes Partners Antipodes Partners Antipodes Partners Antipodes Partners

CIO / Lead Portfolio Manager Deputy Portfolio Manager Deputy Portfolio Manager Head of Execution

Tel: 02 8059 7600 Tel: 02 8059 7603 Tel: 02 8059 7608 Tel: 02 8059 [email protected] [email protected] [email protected] [email protected]

Corporate Adviser Chris Donohoe Will Spraggett Mary-Ann BaldockSeed Partnerships Seed Partnerships Seed Partnerships

Tel: +61 413 315 631 Tel: + 61 400 535 577 Tel: +61 412 579 [email protected] [email protected] [email protected]

Confidential / 46

Disclaimer

Interests in the Antipodes Global Fund ARSN 087 719 515 (‘Fund’) are issued by Pinnacle Fund Services Limited, ABN 29 082 494 362, AFSL 238371. Antipodes Partners Limited

ABN 29 602 042 035 AFSL 481580 (‘Antipodes Partners’) is the investment manager of the Fund. The Product Disclosure Statement (PDS) for the Fund is available at

www.antipodespartners.com/funds. Pinnacle Fund Services Limited is not licensed to provide financial product advice. Any potential investor should consider the current PDS in

its entirely and consult their financial adviser before making an investment decision in relation to the Fund.

Antipodes Partners and Pinnacle Fund Services Limited believe the information contained in this presentation is reliable, however no warranty is given as to its accuracy and

persons relying on this information do so at their own risk. Any opinions or forecasts reflect the judgment and assumptions of Antipodes Partners and its representatives on the

basis of information at the date of publication and may later change without notice. The information is not intended as a securities recommendation or statement of opinion

intended to influence a person or persons in making a decision in relation to investment. This presentation is for general information only. It has been prepared without taking

account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is

not a reliable indicator of future performance.

To the extent permitted by law, Antipodes Partners and Pinnacle Fund Services Limited disclaim all liability to any person relying on the information in respect of any loss or

damage (including consequential loss or damage) however caused, which may be suffered or arise directly or indirectly in respect of such information contained in this

presentation. The information contained in this presentation is not to be disclosed in whole or part or used by any other party without the prior written consent of Antipodes

Partners. Antipodes Partners and their associates may have interests in financial products mentioned in this presentation.

*Morningstar

© 2016 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete

or timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665

544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs. Refer to our Financial

Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product

Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest. Our publications, ratings and products should

be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance.

To obtain advice tailored to your situation, contact a professional financial adviser. Some material is copyright and published under licence from ASX Operations Pty Ltd ACN 004

523 782 ("ASXO").

Confidential / 47

Disclaimer

Zenith

The Zenith Investment Partners (“Zenith”) Australian Financial Services License No. 226872 rating (ASX:APL rating issued 15 Aug 2016) referred to in this document is limited to

“General Advice” (as defined by the Corporations Act 2001) for Wholesale clients only. This advice has been prepared without taking into account the objectives, financial

situation or needs of any individual. It is not a specific recommendation to purchase, sell or hold the relevant product(s). Investors should seek independent financial advice

before making an investment decision and should consider the appropriateness of this advice in light of their own objectives, financial situation and needs. Investors should

obtain a copy of, and consider the PDS or offer document before making any decision and refer to the full Zenith Product Assessment available on the Zenith website. Zenith

usually charges the product issuer, fund manager or a related party to conduct Product Assessments. Full details regarding Zenith’s methodology, ratings definitions and

regulatory compliance are available on our Product Assessment’s and at http://www.zenithpartners.com.au/RegulatoryGuidelines