Anti dumping duty

32

ANTI DUMPING DUTY

-

Upload

manish-sachdeva -

Category

Economy & Finance

-

view

133 -

download

0

Transcript of Anti dumping duty

ANTI DUMPING

DUTY

DUMPINGDisposing off the goods at a value lower than

its prevailing price in the origin country by the origin country so as to decrease the price of

goods cheaper to the price prevailing in destination country is called DUMPING.

Margin of Dumping

Landing Charges

Export Price

Normal Price in Exporting Market

Injury caused

Normal Value• Comparable price of the like article when

meant for home consumption in the exporting State

• Representative Export Price to another country

• Cost of Production including allowance for admin and selling cost and profitsExporting Price

• Export Price to other countries• Price at which the imported articles are first

resold to an independent buyer• On a reasonable basis

FEATURES OF DUMPING Disrupting the domestic market of

destination country Dumping is not illegal or immoral, it is

only threatening There is no fair motive behind doing such

practice as a rational man wont sell his product lower than his manufacturing cost.

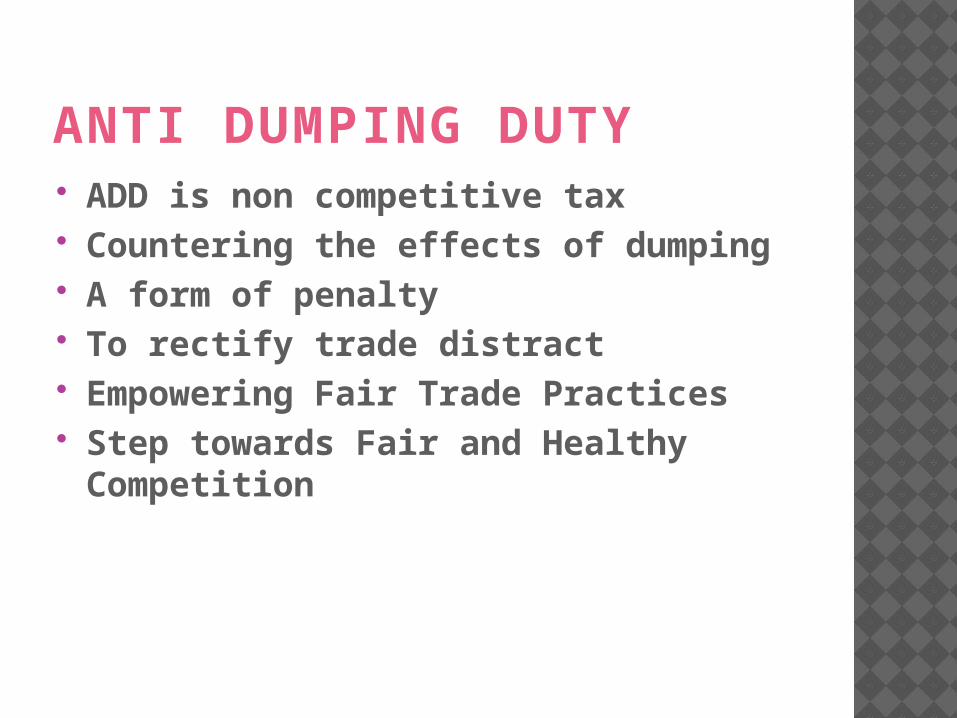

ANTI DUMPING DUTY ADD is non competitive tax Countering the effects of dumping A form of penalty To rectify trade distract Empowering Fair Trade Practices Step towards Fair and Healthy

Competition

LEGAL FRAMEWORK OF ADD

ADD

Investigations of DA

Customs

Tariff Act and

Rules

Article VI of GATT

GENERAL AGREEMENT ON TARIFF AND TRADE OF WTO Agreement based on Harmonious

System of Taxation Came into force on 1 January 1948

and amended in 1994 The General Agreement is applied

"provisionally" by all contracting parties

India has framed Anti Dumping Duty Rules in consonance with the provision of the Article VI of GATT

Section 9BArticle VI

Either ADD or CVD can be levied for countervailing a particular dumping or export subsidies and not both the duties

Determination that import of such article causes or threatens material injury to any established industry in India or

materially retards the establishment of any industry in IndiaADD cannot be levied to counter effect the beneficial exemption available to exporter in the exporting country given to him in the

course of home consumption

ADD can be imposed to secure the domestic interest of any other Exporting Country

ADD wont be imposed if exporter revise prices or

cease exporting and injury is eliminated

With prior consultation with the exporting country, for the

stabilizing domestic prices in exporting nation Dumping

provision wont apply

GENERAL AGREEMENT ON TARIFF AND TRADE OF WTO

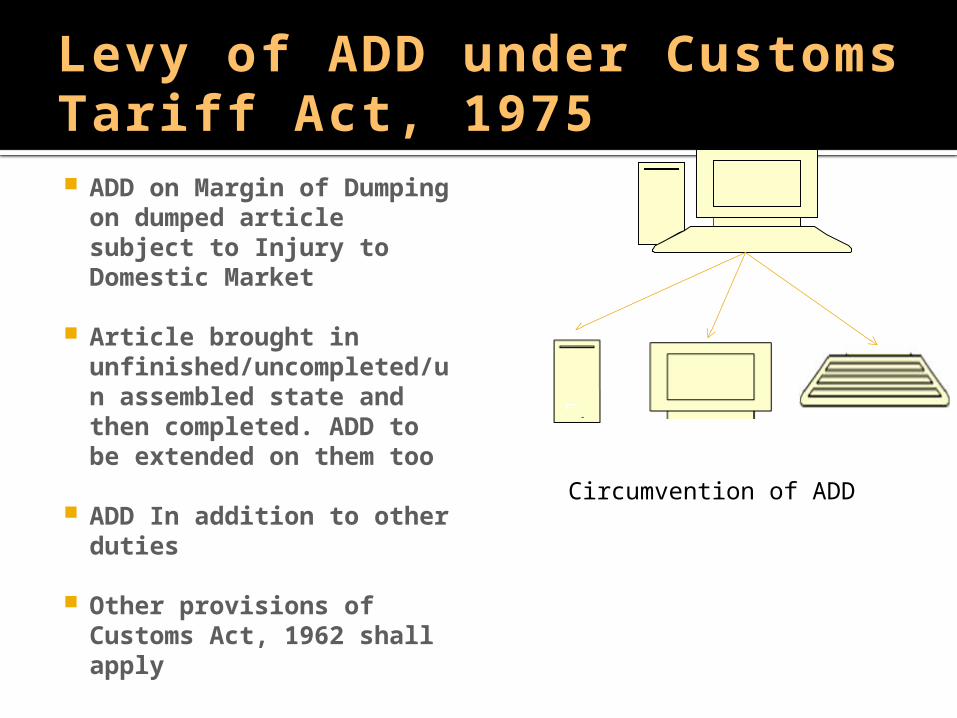

Levy of ADD under Customs Tariff Act, 1975 ADD on Margin of

Dumping on dumped article subject to Injury to Domestic Market

Article brought in unfinished/uncompleted/un assembled state and then completed. ADD to be extended on them too

ADD In addition to other duties

Other provisions of Customs Act, 1962 shall apply

Circumvention of ADD

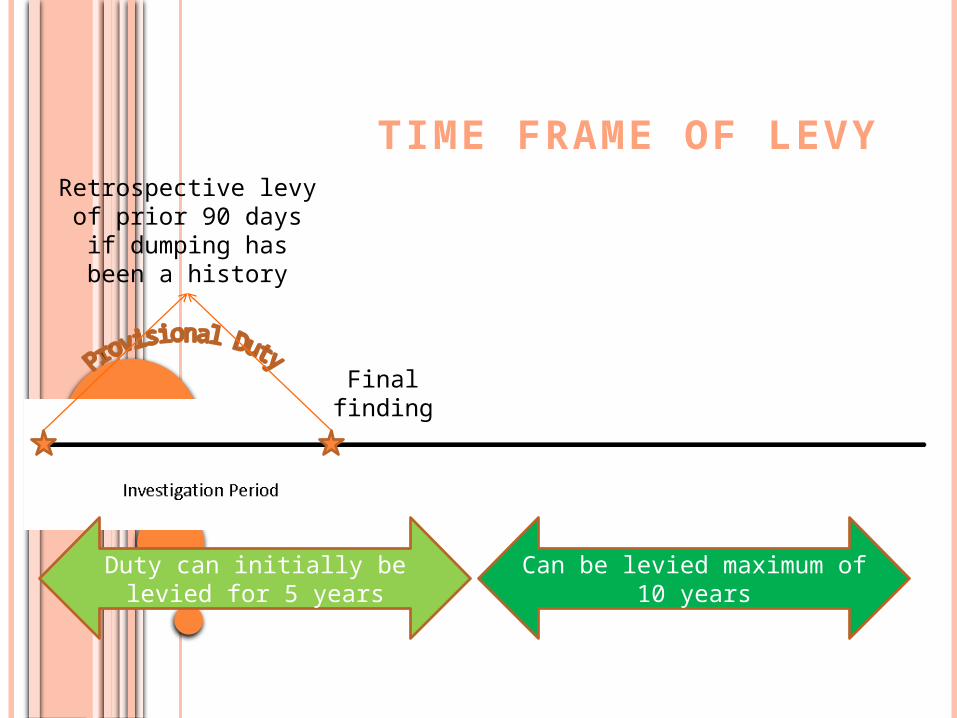

Final finding

Duty can initially be levied for 5 years

Can be levied maximum of 10 years

Retrospective levy of prior 90 days if

dumping has been a history

TIME FRAME OF LEVY

RELAXATIONS UNDER FTP SCHEMES ADD shall not be applicable on 100

% EOU unlessSpecifically applicable orClearance after processing or as such

to DTA

ADD is covered under Advance Authorization exemption Scheme

ADD Litigations can be funded under MAI Scheme

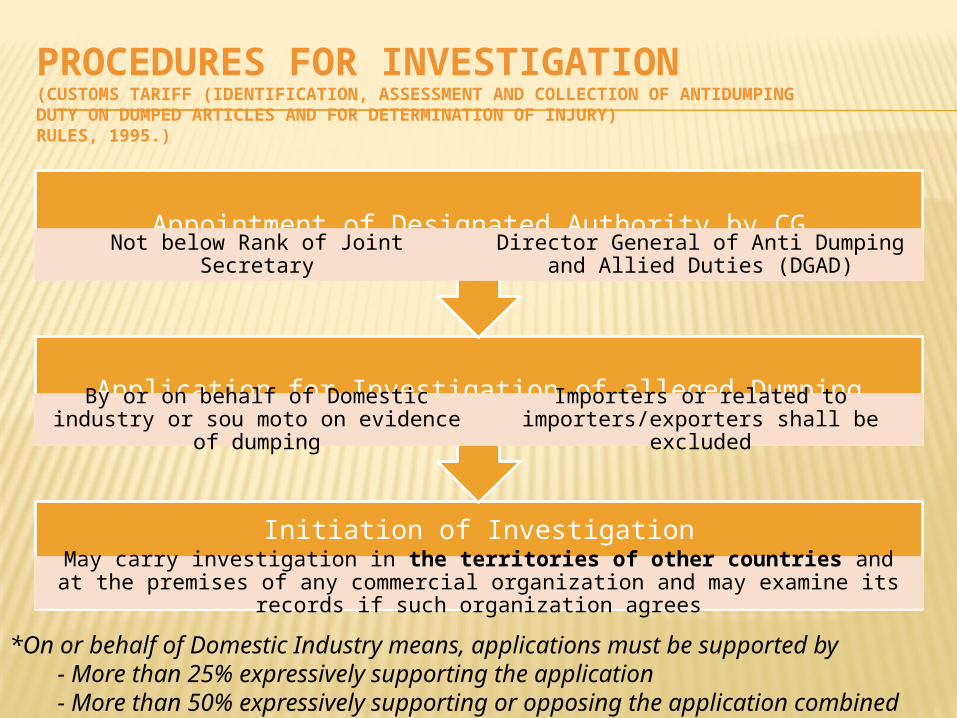

PROCEDURES FOR INVESTIGATION(CUSTOMS TARIFF (IDENTIFICATION, ASSESSMENT AND COLLECTION OF ANTIDUMPINGDUTY ON DUMPED ARTICLES AND FOR DETERMINATION OF INJURY)RULES, 1995.)

Initiation of InvestigationMay carry investigation in the territories of other countries and at the

premises of any commercial organization and may examine its records if such organization agrees

Application for Investigation of alleged DumpingBy or on behalf of Domestic industry or

sou moto on evidence of dumpingImporters or related to

importers/exporters shall be excluded

Appointment of Designated Authority by CGNot below Rank of Joint Secretary Director General of Anti Dumping and

Allied Duties (DGAD)

*On or behalf of Domestic Industry means, applications must be supported by- More than 25% expressively supporting the application- More than 50% expressively supporting or opposing the application combined

INVESTIGATION PROCEDURE

Export Price Normal Value

•At ex-factory level

•Transaction-to-transaction

•Weighted Avg. Comparison in case affecting factors

Based on Records of exporter prepared on GAAP

S.P. of domestic market or to export

price to 3rd country

Counting for all the

costs, amortizations , and

Profits

Allowance for

costs and duties

incurred between importation and

reselling including

profits

S.P. in case of

Non Market

Economy

Comparison on the basis of

prices of a comparable Market Economy

Margin of

Dumping

Comparison:

FACTORS AFFECTING INJURY AND LINK WITH MARGIN OF DUMPING

Injury to Domesti

c Market

Volume of dumped Imports

Affect on prices of domestic market

Impact on producers

of domestic market

End effect is to depress prices or prevent

increase in prices of domestic industry

Cumulative Assessment

of two exporting dumping countries

Evaluation of

Economic Factors

Factors affecting increase

in dumping

Margin of Dumping

Casual

Link

DETERMINATION OF ADD

Injurious Price to Domestic Industry

Injury Non Injurious to Domestic Country

Not acceptable to Domestic Industry

Acceptable to Domestic Industry

ADD

DETERMINATION OF INJURY AMOUNT Fair Selling Price = Notional Price

Margin of Dumping to be considered

Information relating to Cost of Production to be considered based on Best use of raw materials, constituents and capacity

utilization by Domestic Market Propriety (Grouping) of expenses, their non-recurring

nature, Allocations and Amortization Reasonable Pre Tax Return on Capital Employed based on

Appropriate Working Capital and Fixed Assets Non includible amount such as non related R & D, post

manufacturing expenses, levies on sale, trading activity expenses, non cost items e.g. bad debts, loss on sale of assets, donations etc.

Reasonableness of Interest Cost to examine no abnoraml expenditure

W. Avg. of non injurious price of individual Domestic producers to be considered

INVESTIGATION PROCEDURE

• Public notices containing adequate information shall be issued notifying decision of authority to initiate investigation

Public Notice

• A copy of the public notice along with APPLICATION filed by domestic industry producers shall be forwarded by the designated authority to the known exporters of the article alleged to have been subsidized, the government of the exporting country concerned and other interested parties.

Notice to Exporters

• The designated authority may calling for any information in such form the exporters, foreign producers and governments of interested countries

• Such information shall be furnished by such persons in writing within 30 from the date of receipt of the notice or within such extended period as the designated authority may allow on sufficient cause being shown.

Information form

Exporters, Exporting Country

INVESTIGATION PROCEDURE

• The designated authority shall also provide opportunity to the industrial users of the article under investigation, and to representative consumer organizations in cases where the article is commonly sold at retail level, to furnish information which is relevant to the investigation

Opportunity to

Importers

• Oral information shall be taken into consideration only when it is subsequently reproduced in writing.Oral

Information

• In a case where an interested party refuses access to, or otherwise does not provide necessary information within a reasonable period, or significantly impedes the investigation, the designated authority may record its findings on the basis of facts available to it and make such recommendations to the Central Government as it deems fit under such circumstances.

Information not

provided

Terminati on/Suspension of Investi gati on

Dumping not so prevailing• Request in writing for doing so from or

on behalf of the domestic industry affected

• Lack of suffi cient evidence of dumping or injury to justify

• Margin of dumping is less than 2 per cent of the export price

• Volume of the dumped imports, actual or potential, from a particular country accounts for less than 3 per cent of the imports

• However if collectively contribution from these countries accounts for more than 7 per cent of the import of the like product, it shall not terminate

• injury where applicable, is negligible.

Price Undertaking• If exporter

(i) furnishes an undertaking in writing to revise the prices so that no exports of the said article are made to India at dumped prices or

(ii) undertake to revise the prices so that injurious effect of dumping is eliminated and the designated authority is satisfied about this

• Designated authority shall intimate the acceptance of an undertaking and suspension or termination of investigation to the Central Government and also issue a public notice in this regard

• Designated Authority shall from time to time review the need for continuance of any undertaking

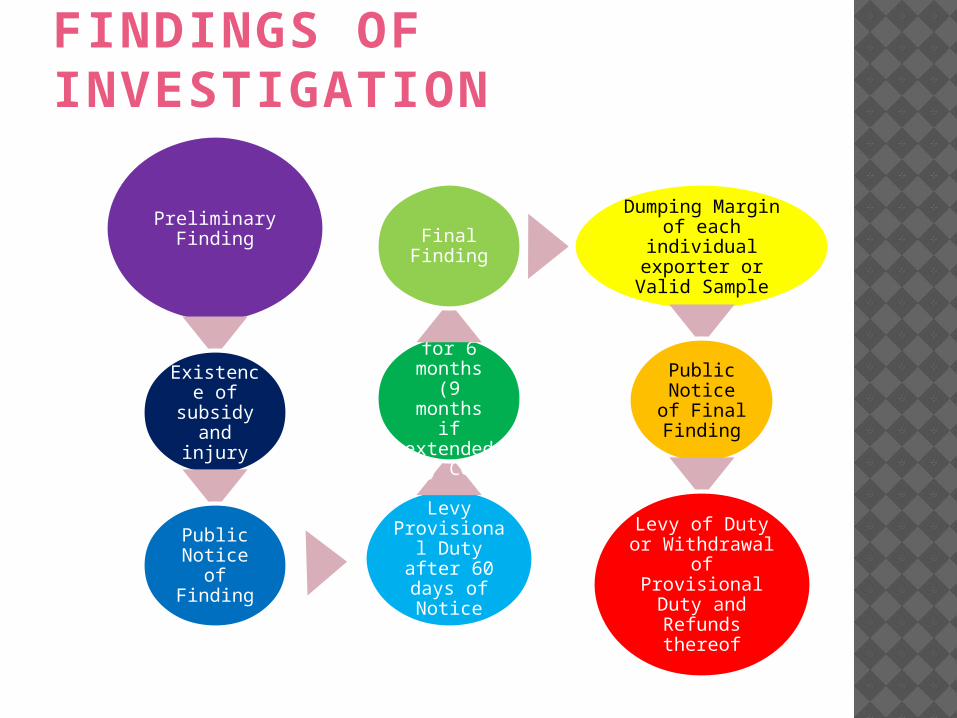

FINDINGS OF INVESTIGATION

Preliminary Finding

Existence of subsidy and injury

Public Notice of Finding

Levy Provisional Duty after 60 days of

Notice

Valid for 6 months (9 months if extended

by CG)

Final Finding

Dumping Margin of each individual exporter or Valid

Sample

Public Notice of

Final Finding

Levy of Duty or Withdrawal of

Provisional Duty and

Refunds thereof

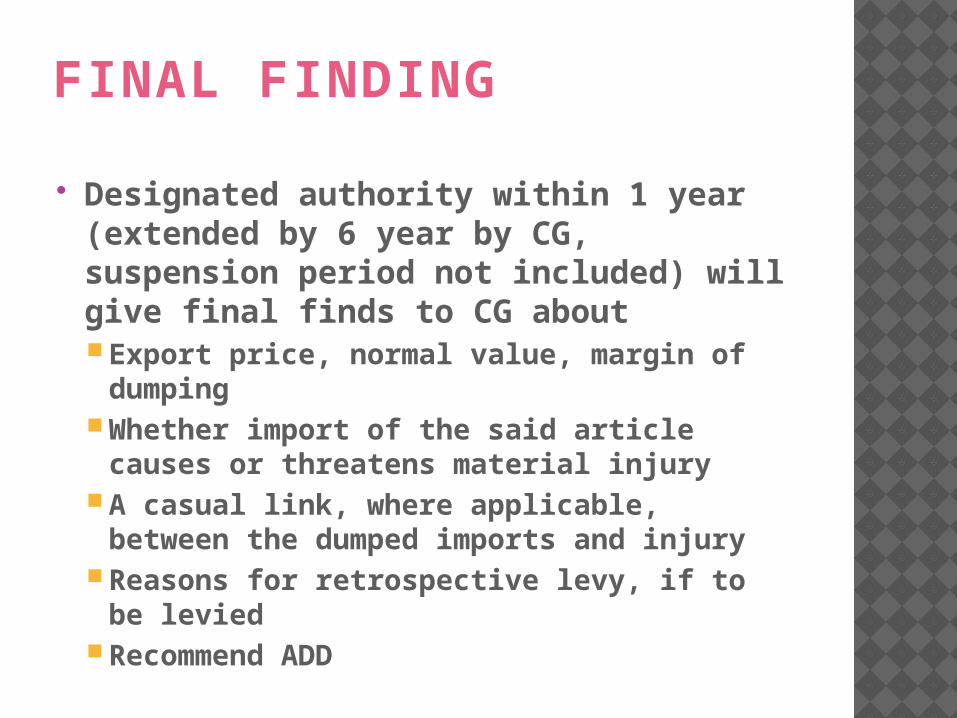

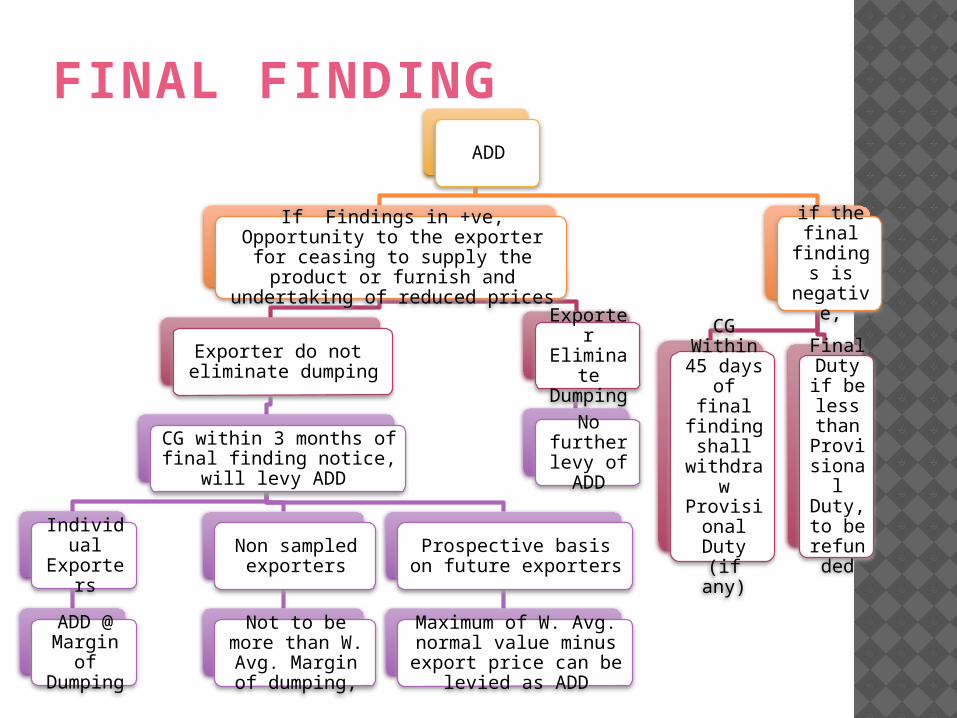

FINAL FINDING

Designated authority within 1 year (extended by 6 year by CG, suspension period not included) will give final finds to CG aboutExport price, normal value, margin of

dumpingWhether import of the said article causes

or threatens material injuryA casual link, where applicable, between

the dumped imports and injuryReasons for retrospective levy, if to be

leviedRecommend ADD

ADD

If Findings in +ve, Opportunity to the exporter for ceasing to supply

the product or furnish and undertaking of reduced prices

Exporter do not eliminate dumping

CG within 3 months of final finding notice, will

levy ADD

Individual

Exporters

ADD @ Margin of Dumping

Non sampled exporters

Not to be more than W. Avg.

Margin of dumping,

Prospective basis on future exporters

Maximum of W. Avg. normal value minus export price can be

levied as ADD

Exporter Eliminate Dumping

No further levy of ADD

if the final

findings is

negative,

CG Within

45 days of final finding shall

withdraw Provisional Duty (if any)

Final Duty if be less than

Provisional Duty, to be refunded

FINAL FINDING

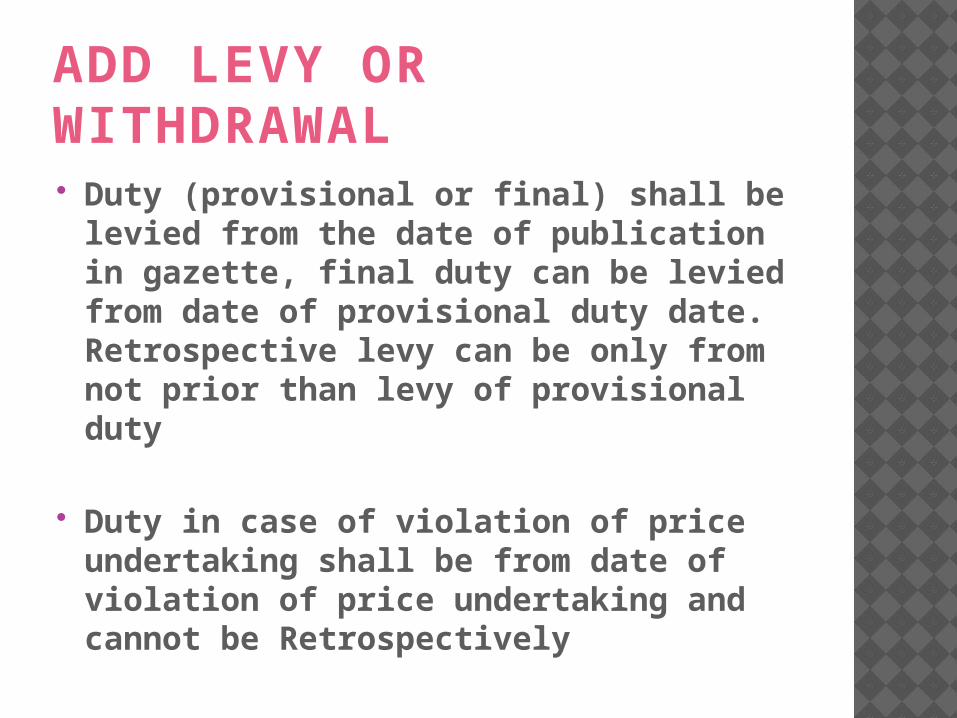

ADD LEVY OR WITHDRAWAL Duty (provisional or final) shall be

levied from the date of publication in gazette, final duty can be levied from date of provisional duty date. Retrospective levy can be only from not prior than levy of provisional duty

Duty in case of violation of price undertaking shall be from date of violation of price undertaking and cannot be Retrospectively

REFUND OF ADDCUSTOMS TARIFF (IDENTIFICATION, ASSESSMENT AND COLLECTION OF ANTI-DUMPING DUTY ON DUMPED ARTICLES AND FOR DETERMINATION OF INJURY) RULES, 1995

Importer may file application with designated authority in such form and such documents if he is of the opinion that he has paid any anti-dumping duty imposed in excess of the margin of dumping

Designated authority shall initiate investigation

The designated authority shall, after investigation, determine the actual margin of dumping for the goods and if the anti-dumping paid on the goods is in excess of the margin of dumping so determined, the authority shall make recommendation to the Central Government within nine months and in no case more than 12 months, from the date of receipt of the application, complete in all respects, to refund the difference of Excess of ADD.

REFUND OF ADDREFUND OF ANTI-DUMPING DUTY (PAID IN EXCESS OF ACTUAL MARGIN OF DUMPING) RULES 2012

The importer shall file refund application within 3 months from date of notification of reduction of ADD or consequence to a judgment, decree or order with AC/DC of Customs at the port of importation

Deficiencies if any to be corrected and re submit the refund application

AC/DC after his satisfaction shall refund the excess ADD to importer subject to doctrine of Unjust Enrichment

REVIEW OF FUTURE DUMPING EXPORTERS The designated authority shall carry out a periodical review

for the purpose of determining individual margins of dumping for any exporters or producers in the exporting country in question who have not exported the product to India during the period of investigation

Provided that these exporters or producers show that they are not related to any of the exporters or producers in the exporting country who are subject to the anti-dumping duties on the product.

During the review period no duty shall be levied on them.

CG may resort to provisional assessment and may ask a guarantee from the importer if the designated authority so recommends and if such a review results in a determination of dumping in respect of such products or exporters

REVIEW OF ADD

ADD levied

5 years

Investigation after

reasonable time12

months

ADD will remain effective so long as and to the extent necessary

Sou Moto

Request by

Interested Party

After investigation, recommend to CG to withdraw

duty if found satisfactory

CIRCUMVENTION OF ADD

ABC Ltd. Computers

LED Monitor PC LED TV set

XYZ Ltd. Computers

INDIA

ABC Ltd. Computers

LED Monitor PC

CIRCUMVENTION OF ADD

•Designated either sou moto or receipt of written application of domestic industry, shall initiate proceedings of Circumvention of duty

•Procedure of original investigation will apply mutatis mutandis.

•Investigation to be concluded within 12 month (extended by 6 months by CG on its satisafaction).

•After investigation authority may recommend imposition of anti dumping duty to imports of articles found to be circumventing an existing anti dumping duty or to imports of article originating in or exported from countries other than those which are already notified for the purpose of levy of the antidumping duty

CIRCUMVENTION OF ADD

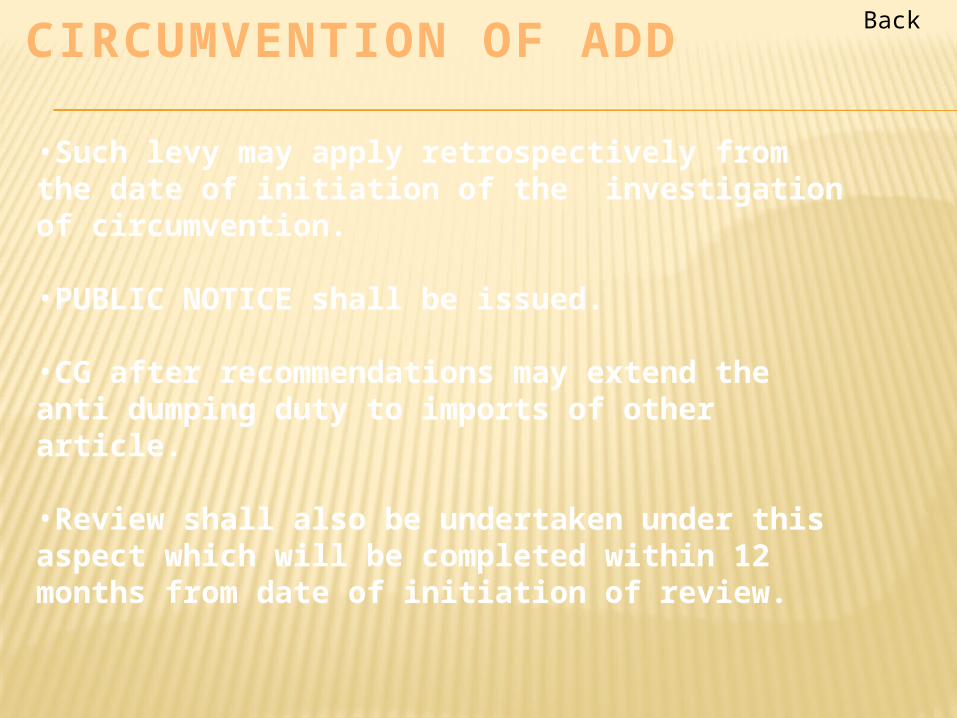

•Such levy may apply retrospectively from the date of initiation of the investigation of circumvention.

•PUBLIC NOTICE shall be issued.

•CG after recommendations may extend the anti dumping duty to imports of other article.

•Review shall also be undertaken under this aspect which will be completed within 12 months from date of initiation of review.

Back

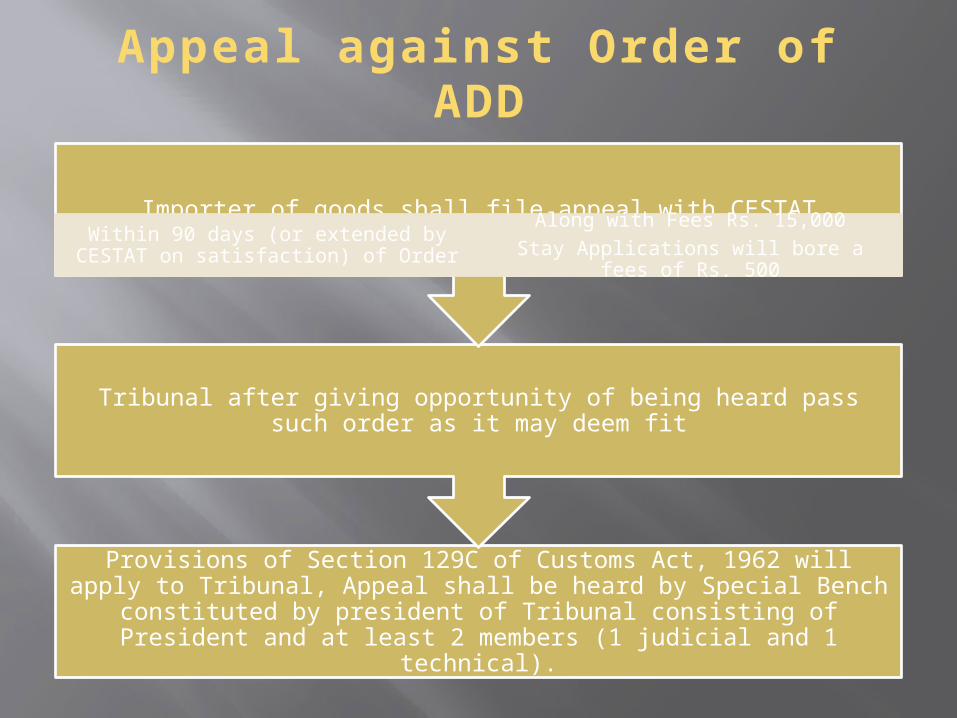

Appeal against Order of ADD

Provisions of Section 129C of Customs Act, 1962 will apply to Tribunal, Appeal shall be heard by Special Bench constituted by

president of Tribunal consisting of President and at least 2 members (1 judicial and 1 technical).

Tribunal after giving opportunity of being heard pass such order as it may deem fit

Importer of goods shall file appeal with CESTATWithin 90 days (or extended by CESTAT

on satisfaction) of Order

Along with Fees Rs. 15,000Stay Applications will bore a fees of Rs.

500