Software Engineering 1 N.L. Hsueh, SE-Lab IECS FCU Software Architecture N.L. Hsueh.

Upload

phamkhuongCategory

view

212download

0

Annual Report 20

13

ALFA, S.A.B. DE C.V.Av. Gómez Morín 1111 SurCol. CarrizalejoSan Pedro Garza García, N.L.C.P. 66254, Mexico

www.alfa.com.mx

ANNUAL REPORT

ALFA is the largest independent producer of aluminum

engine components for the automotive industry in

the world, and one of the world’s largest producers of

polyester (PTA, PET and fibers). In addition, it leads the

Mexican market in petrochemicals such as polypropylene,

expandable polystyrene and caprolactam. It is the leading

maker of processed meats in North America, and of cheese

in Mexico, as well as a leading company in information

technology and communications services for the business

segment in this country. Since 2006, it participates in the

hydrocarbon industry in the U.S.

In 2013, ALFA reported revenues of Ps. 203,456 million

(U.S. $15.9 billion), and EBITDA of Ps. 24,534 million

(U.S. $1.9 billion).

Currently, ALFA has manufacturing operations in 18

countries and employs 61,000 people. ALFA’s shares are

quoted on the Mexican Stock Exchange and on Latibex,

the market for Latin American shares of the Madrid Stock

Exchange.

ContentsPage

The Year in Summary 1Global Footprint and Businesses 2Financial Highlights 4Letter to Shareholders 5Alpek 8Nemak 10Sigma 12Alestra 14Newpek 16Board of Directors 18Management Team 20Corporate Governance 20Consolidated Financial Statements 22

NOTE: In this annual report, monetary figures are expressed in nominal Mexican pesos (Ps.), and in nominal dollars (U.S. $) unless otherwise specified. Conversions from pesos to dollars were made using the average rate of the month in which the revenues or disbursements were made. The percentages of variation between 2013 and 2012 are expressed in nominal terms.

The Company

des

ign:s

ign

i.co

m.m

x Independent AuditorPwC

Investor RelationsEnrique FloresVice-President Corporate CommunicationsPhone: +52 (81) 8748 [email protected]

Luis OchoaInvestor Relations DirectorPhone: +52 (81) 8748 [email protected]

Raúl GonzálezInvestor Relations ManagerPhone: +52 (81) 8748 [email protected]

Juan Andrés MartínInvestor RelationsPhone: +52 (81) 8748 [email protected]

Mexican Stock ExchangeALFADate listedAugust 1978

Latibex (Madrid Stock Exchange)ALFA C/I-s/ADate listedDecember 2003

1

• ALFA: revenues and EBITDA continue growing.Investments are made in all business groupsto expand production capacity and improvecompetitiveness.

• A challenging year for Alpek amid pressure onmargins for its main products. However, itsfinancial condition enables it to continue to investin plant capacity and cost-saving programs.

• Unprecedented results for Nemak: revenuesand EBITDA up 13% and 21%, respectively. Aninvestment in Russia is announced. A secondplant starts up in China.

• Sigma: another year of positive results.Ventures into Europe. Strengthens the cheesebusiness in Costa Rica and the foodservicebusiness in Mexico.

• Alestra brings in record results. It invests inthe construction of a fifth Data Center toexpand its market coverage and capacity toprovide services to business clients.

• Newpek continues to grow. It expandsoperations into other regions in the U.S. Startsoffering services to oil & gas companies inMexico. Constitutional amendments enactedin Mexico towards the end of 2013, createpotentially enormous investment opportunitiesin the energy industry in the country.

The Year in Summary

28

31

33

4428 36

24 27 24

39

51 5 2

2

n Alpek n Nemakn Sigman Alestran Newpek

Alpek

Sigma

Nemak

Alestra

Newpek

• The largest petrochemical company in Mexico.

• The leading producer of polyester in North America and one of the most important worldwide.

• Operates the largest expandable polystyrene (EPS) plant in the Americas.

• Sole producer of polypropylene and caprolactam in Mexico.

• The leading maker of processed meats in North America, and of cheese in Mexico.

• The largest producer of hot dogs in the U.S., Mexico and Central America.

• Owns one of the largest refrigerated food distribution networks in Latin America. It serves 440,000 points of sale. Owns a solid portfolio of leading brands.

• The world’s largest independent producer of complex aluminum powertrain components for the automotive industry.

• Leading provider of IT and communications services for corporate customers in Mexico.

• Company engaged in hydrocarbons exploration and production activities.

Revenues(%)

EBITDA(%)

Assets(%)

Global Footprint and Businesses

3

ArgentinaAustriaBrazilCanadaChinaCosta RicaCzech RepublicDominican RepublicEl Salvador GermanyHungaryIndiaMexicoPeruPolandSlovakiaSpainU.S.A.

MAIN PRODUCTS

• Polyester (PTA, PET and fibers)

• Plastics and chemicals (polypropylene, EPS, polyurethanes and caprolactam)

MAIN PRODUCTS

• Processed meats

• Cheese and yogurt

• Prepared meals

MAIN PRODUCTS

• Aluminum heads and blocks for gas and diesel engines

• Transmission parts

MAIN SERVICES

• Data centers

• Cloud applications, information security, managed networks

• Consultancy services, vertical applications for specific industries

MAIN PRODUCTS

• Hydrocarbons

Markets: food & beverages, consumer products, textile, construction and automotive.

Plants: 16, in three countries.

Capacity: 5.3 million tons per year.

Revenues in 2013: U.S. $7.0 billion.

Employees: 4,528.

Markets: food.

Plants: 41 and 134 distribution centers, in ten countries.

Points of sale served: 440,000.

Production volume in 2013: 1.2 million tons.

Revenues in 2013: U.S. $3.8 billion.

Employees: 29,562.

Markets: automotive.

Plants: 34, in 14 countries.

Capacity: 55 million equivalent heads per year.

Revenues in 2013: U.S. $4.4 billion.

Employees: 20,724.

Markets: corporate customers.

Presence: 200 cities in Mexico.

Revenues in 2013: U.S. $395 million.

Employees: 1,860.

Markets: energy, oil and gas.

Revenues in 2013: U.S. $133 million.

Employees: 25.

13

12,6

48

11,8

54

10,8

16

9,0

84

8,27

7

1211100913

1,915

1,854

1,623

1,26

0

1,055

1211100913

15,8

70

15,15

2

14,7

46

10,7

73

8,53

6

12111009

4

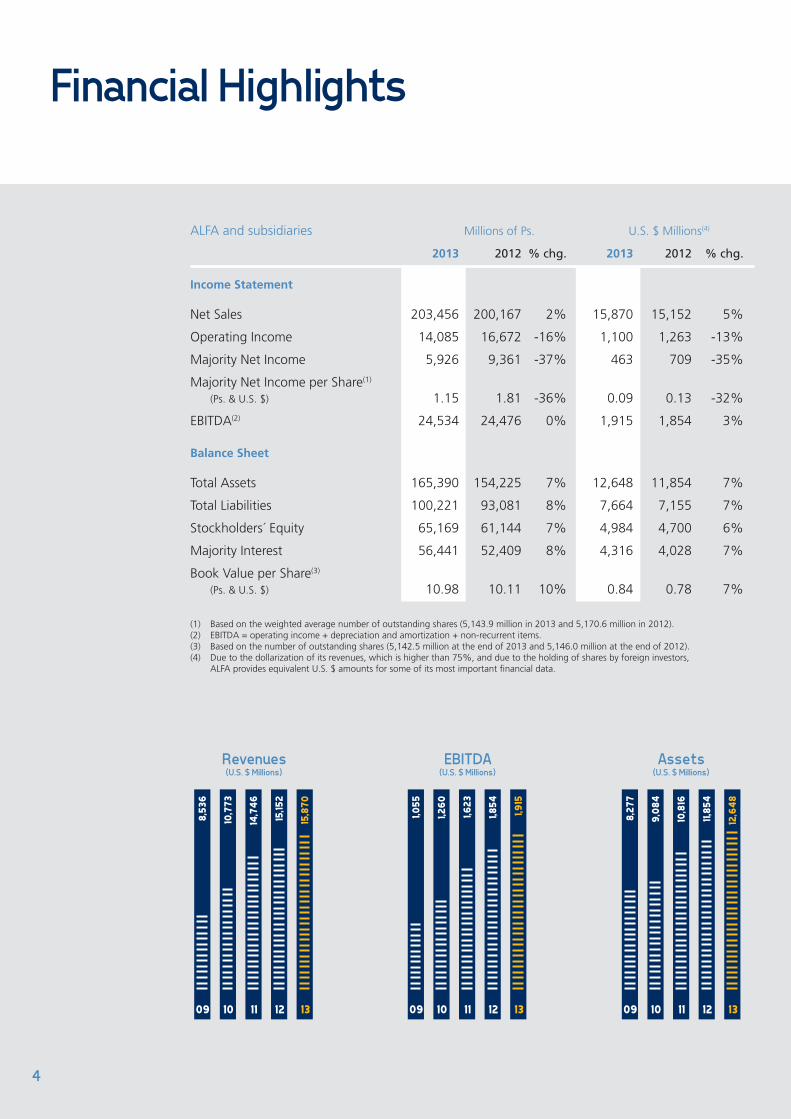

Financial Highlights

Revenues(U.S. $ Millions)

EBITDA(U.S. $ Millions)

Assets(U.S. $ Millions)

ALFA and subsidiaries Millions of Ps. U.S. $ Millions(4)

2013 2012 % chg. 2013 2012 % chg.

Income Statement

Net Sales 203,456 200,167 2% 15,870 15,152 5%

Operating Income 14,085 16,672 -16% 1,100 1,263 -13%

Majority Net Income 5,926 9,361 -37% 463 709 -35%

Majority Net Income per Share(1)

(Ps. & U.S. $) 1.15 1.81 -36% 0.09 0.13 -32%

EBITDA(2) 24,534 24,476 0% 1,915 1,854 3%

Balance Sheet

Total Assets 165,390 154,225 7% 12,648 11,854 7%

Total Liabilities 100,221 93,081 8% 7,664 7,155 7%

Stockholders´ Equity 65,169 61,144 7% 4,984 4,700 6%

Majority Interest 56,441 52,409 8% 4,316 4,028 7%

Book Value per Share(3) (Ps. & U.S. $) 10.98 10.11 10% 0.84 0.78 7%

(1) Based on the weighted average number of outstanding shares (5,143.9 million in 2013 and 5,170.6 million in 2012).(2) EBITDA = operating income + depreciation and amortization + non-recurrent items.(3) Based on the number of outstanding shares (5,142.5 million at the end of 2013 and 5,146.0 million at the end of 2012).(4) Due to the dollarization of its revenues, which is higher than 75%, and due to the holding of shares by foreign investors, ALFA provides equivalent U.S. $ amounts for some of its most important financial data.

1,915

1,854

1312

15,8

70

15,15

2

1312

5

Dear shareholders:

In 2013, ALFA’s results were driven by the performance of

the auto parts and food businesses. Revenues and EBITDA

grew 5% and 3% over 2012. Financial condition remained

strong: Net Debt to EBITDA was 1.8 times, while Interest

Coverage was 6.7 times. Cash flow generation during

the year and the refinancing of debt in the international

financial markets favored the former.

Investments were carried out to expand production

capacity and increase efficiency: Alpek invested in power

cogeneration; Nemak built a second plant in China; Sigma

made acquisitions, highlighting that of 45% of the capital

of Campofrio Food Group, Europe’s leading producer of

processed meats that allows Sigma entry in that region;

Alestra built its fifth Data Center and Newpek continued

drilling for natural gas and oil in Texas.

Letter to Shareholders

EBITDA(U.S. $ Millions)

Revenues(U.S. $ Millions)

6

Performance

Alpek continued to face an oversupply in the global polyester markets, caused by excess production capacity in Asia. It took measures such as the closure of its Cape Fear plant, whose production moved to the Columbia and Pearl River plants. Progress was made in the construction of a cogeneration unit in Mexico and a contract with M&G was signed to have access to 400 thousand tons of PET per year, to be produced at a new plant that this company will build in Corpus Christi, Texas.

Nemak benefitted from the U.S. auto industry’s ongoing recovery to increase its sales volume by 14%. In Europe, the automotive market shrank by 2%. However, Nemak’s biggest clients in that area took advantage of export opportunities to sustain their sales, and this supported Nemak as well. The company continued to build capacity so it can better respond to its customers’ needs. It invested to expand production capacity in North America, Europe and Asia, including a new plant in China.

Sigma’s sales volume rose 4% thanks to a stronger distribution network and new marketing and commercial support campaigns. This despite the fact the Mexican food market decreased by an estimated 1% in the year.

Sigma acquired 45% of the equity of Campofrio, taking a major step forward in its strategy of becoming a leading global player in the refrigerated food market. To this date, the company is awaiting the Spanish Securities Commission’s approval to proceed with a tender offer for the Campofrio shares in the market.

Sigma also bought Monteverde, a Costa Rican cheese producer, and ComNor, a business operating in the Mexican foodservice market.

Alestra reinforced its strategy of focusing on value-added IT and communications services in the Mexican business segment. Revenues from this grew 15% in 2013 and accounted for 84% total sales of these services. Alestra broadened its coverage of the northwestern and southeastern markets of Mexico by acquiring G-Tel Comunicación. It built a new Data Center, the company’s fifth, which gives it the capacity to provide more and better services to its clients. It also built a “Sperto Center” in Mexico City and expanded its fiber optic network and last-mile access.

Newpek continued to drill more wells and connect them to sales in the south of Texas, totaling 411 wells in production at the end of 2013. Also, as part of its strategy of strengthening operating capacity in the U.S., it invested in new conventional and unconventional oil and gas fields in Kansas, Texas, Oklahoma and Colorado. In Mexico, it formalized a strategic alliance with the British company Petrofac, to jointly offer services to companies in the oil and gas industries.

Financial results

ALFA’s revenues for 2013 totaled U.S. $15,870 million, an increase of 5% over the previous year. This was driven by higher sales volume and average prices that reflected a rise in raw material costs in some products.

7

EBITDA rose to U.S. $1,915 million, 3% more than in 2012. Lower margins on petrochemical products in export markets precluded an even stronger growth.

Majority Net Income was U.S. $463 million, a decline of 32% from the previous year. The reduction was due mainly to foreign-exchange losses following the Mexican peso’s depreciation against the U.S. dollar.

ALFA continued to invest in expanding production capacity and strengthening its businesses. In 2013, it invested U.S. $1,550 million, including the abovementioned acquisitions by Sigma and Alestra.

During the year, the ALFA companies refinanced U.S. $1.3 billion at improved terms and conditions. Thus, the average life of debt increased from 4.5 to 5.0 years. As part of this effort, Alpek and Nemak issued bonds for the equivalent of U.S. $800 million on international financial markets. At the end of 2013, 40% of the consolidated debt matures after 2018.

At year’s end, and in order to accelerate the development of Mexico’s energy industry, a constitutional reform was approved that aims to open to private investment areas of the energy industry reserved until now for the Mexican State. As of the date of this letter, the drafting of the laws that will enforce the constitutional amendments is in progress. ALFA has been carrying out activities in the energy industry outside Mexico for seven years. This has allowed it to gain experience so that it is ready to take advantage of business opportunities that may become available in Mexico. Greater clarity on this matter may be in place in the coming months.

The Board of Directors recognizes and is grateful for the support received from shareholders, employees, customers, suppliers, financial institutions and the community at large, during the year reported here.

All of ALFA’s businesses are prepared with valuable human capital, cutting-edge technology, strong cash flow generation and sound financial condition, so that they can better capture emerging opportunities for growth and value generation.

San Pedro Garza García, N.L., Mexico January 29, 2014.

Armando Garza SadaChairman of the Board of Directors

Álvaro Fernández GarzaPresident

8

• The construction of a cogeneration plant in Veracruz is almost complete.

• A contract is signed to sell IntegRex® technology for a new PTA/PET plant.

• Alpek secures the right to 400,000 tons/year of PET out of this plant.

• A joint venture agreement is signed for the construction of a PET plant in Russia.

• U.S. $7.0 billion in revenues in 2013.

Alpek

I n 2013, Alpek undertook projects to improve its operating efficiency and increase the integration of its operations. This in an

environment of declining margins in global polyester and caprolactam markets.

In line with its integration strategy, Alpek invested U.S. $109 million in building a cogeneration plant in Veracruz, Mexico, which will ensure a reliable and efficient supply of energy starting in the first half of 2014.

The consolidation of its polyester operations through the closure of its Cape Fear plant will result in an estimated annual savings of U.S. $30 million. Alpek also finished clearing bottlenecks at its Columbia plant, increasing its annual capacity by 60,000 tons.

In 2013, Alpek signed an IntegRex® licensing agreement and a PTA/PET supply contract with Gruppo M&G, for construction of an integrated PTA/PET plant in Texas.

Besides advantages in conversion costs, the IntegRex® technology has proven to be an efficient vehicle of international expansion, opening an investment opportunity in a PET plant in Russia.

To improve efficiency, Alpek signed a caprolactam technology licensing agreement with DSM Fibers Intermediates and approved construction of a spherical propylene storage tank.

To face the challenging market environment, Alpek is working on a second cogeneration project and has made progress on the integration to monoethylene glycol, under an alliance with Pemex.

9

76

24

8

60

2

30

In terms of financial results, in 2013 the global petrochemical industry continued to face challenges resulting from overcapacity in China and lower demand in export markets, like Europe. Therefore, Alpek’s sales totaled U.S. $7,028 million, while EBITDA came to U.S. $572 million, 3% and 21% lower, respectively, than in 2012.

Mexico’s energy reform, recently passed by Congress, brightens the outlook for the country’s

petrochemical industry by improving the availability of energy and raw materials under more competitive conditions. Access to natural gas and inputs like ethane and propane are fundamental to maximizing Alpek’s integration strategy. •

Revenue breakdown

(%)

End markets (%)

n Food & beveragen Consumer productsn Textilen Construction

n Polyester productsnPlastic & chemicals

10

• Increase in production capacity in North America, Europe and Asia.

• A second plant in China came on stream.

• Investment in Russia is announced.

• U.S. $4.4 billion in revenues in 2013.

Nemak

F or Nemak, 2013 was an unprecedented year, fuelled by the solid performance of the U.S. automotive industry and the company’s

focus on premium clients in Europe. Furthermore, aluminum auto parts are increasingly being used as replacements for cast iron parts, a trend which also favors the company.

Sales volume grew 14%, to 47.6 million equivalent engine heads. In North America, auto sales grew 8% last year to a total of 15.6 million vehicles. Pent-up demand and the availability of consumer credit were the main drivers.

In Europe, the market shrank by 2%, but Nemak’s increased participation on German automakers, which have been successful in finding export opportunities outside of the Eurozone, permitted sales volume growth of 6%.

Nemak also integrated new value-added services, like machining, and made its operations significantly more efficient by optimizing its 34 plants around the world.

The company waged an ambitious capex program over the course of the year, expanding production capacity in North America, Europe and Asia to better serve the incremental demand of its clients.

At the end of the year, Nemak started up a second plant in China, in the city of Chongqing, turning out engine blocks and transmission parts. It also announced its decision to build a plant in

11

51

3314

2

47.

6

42.

0

1312

Russia, where it will produce engine heads and blocks for a German carmaker. This plant will have an annual capacity of 600,000 units and will start up at the end of 2015. Industry analysts expect that Russia will become Europe’s largest market by the end of the decade, surpassing Germany.

As a result of the operating advances, revenues and EBITDA rose to U.S. $4,391 million and

U.S. $611 million, respectively. This represents increases of 13% and 21% over 2012.

Recent investments are part of Nemak’s strategy of increasing participation in regions where auto production is growing fast, like China and Russia, while strengthening its presence in America and Europe. •

Revenue breakdown

(%)

n HeadsnBlocksnTransmissionsnOther

Sales volume

(million equivalent heads)

12

• The Campofrio acquisition will allow Sigma to enter the European market with a leadership position.

• Foodservice business gains relevance.

• 300 new refrigerated vehicles are added to the distribution fleet.

• U.S. $3.8 billion in revenues in 2013.

D espite estimated weak performance in the Mexican food industry in 2013, Sigma posted positive results, selling 1.2

million tons of food, 4% more than in 2012.

The company carried out three strategic acquisitions. The most important one was the purchase of a 45% stake in Campofrio Food Group (Campofrio), which gives Sigma an entry into the European market. Campofrio is the market leader in Europe, where it has presence in eight countries and in the U.S.

Related to this investment, Sigma signed an agreement with the Chinese company WH Group (formerly Shuanghui), a global leader in pork meat production which owns 37% equity of Campofrio, to launch a tender offer which will increase Sigma’s 45% equity position up to 63%.

The Campofrio acquisition represents an opportunity for Sigma to capitalize on the strength of that company’s brands and its robust operating assets, as well as its excellent management and renowned capacity for innovation.

Also in the year, ALFA acquired the companies ComNor and Monteverde. The first of these operates two plants and eight distribution centers, where processes and sells various types of meat for the Mexican foodservice market, while the other is the leader in the mature cheese business in Costa Rica.

Additionally, to expand the coverage of its retail distribution network, Sigma added 300 new vehicles to its fleet, bringing the total to 4,300.

Sigma

13

65

29

6

8

69

23

Regarding financial results, revenues totaled U.S. $3,820 million and EBITDA was U.S. $524 million, 11% more than in 2012 in both cases.

These increases reflect greater sales of processed meats and dairy products in Mexico and other countries; in addition to improvements in productivity and distribution.

Through investments as those explained above, Sigma continues to execute its strategy of

expanding its core businesses while venturing into new segments and regions that are attractive platforms for consolidating its leadership. •

Revenue breakdown

(%)

Revenue breakdown by region

(%)

n MexiconU.S.A.nCentral America, the Caribbean & Peru

n Processed meatsnDairy productsnOther

14

• Alestra builds its fifth Data Center.

• G-Tel Comunicación, a company in Mexico’s northwestern region, is acquired.

• A new Sperto Center is dedicated in Mexico City.

• U.S. $395 million in revenues in 2013.

Alestra

I n 2013, Alestra rolled out a major capex program aimed at expanding its infrastructure and portfolio of solutions. With this, it

strengthened its position as leader in the information technology and communications (ITC) service market for corporate customers in Mexico.

Alestra continued promoting value-added services, like cloud applications, security and managed networks, as well as data, Internet and local services, which accounted for 84% of the company’s revenues in 2013.

To strengthen its infrastructure and portfolio of solutions and keep its clients at the forefront of industry mega-trends, the company invested U.S. $150 million in fixed assets and systems, more than double the 2012 amount. This figure includes the acquisition of G-Tel Comunicación, a leading supplier of integral voice, data and video services in northwest and southeast Mexico.

Alestra also completed construction of a new Data Center located in Querétaro, which is considered the most innovative and sustainable in Latin America.

Additionally, at the end of the year it launched a new Sperto Center, located in Mexico City. This center has the most innovative technological solutions and serves Alestra to demonstrate its capacity to current or potential customers. The Sperto centers have become a powerful tool to attract new clients and encourage them to adopt the latest technologies.

15

50

16

34

170

137

1312

Confirming its commitment to developing and offering the most complete and reliable range of ITC services in Mexico, Alestra established new alliances with Cisco, HP, SAP and other technological partners, who are leaders in their respective fields.

In 2013, revenues were U.S. $395 million, 13% more than in 2012. EBITDA totaled U.S. $170 million, 24% more than the previous year.

Alestra continues to position itself as a leading ITC service supplier by developing cutting edge services and building up its infrastructure to offer its customers the technological options that can generate the best value for them. •

Revenue breakdown

(%)

n Business data, Internet and local services nBusiness IT services nLong distance

EBITDA(U.S. $ Millions)

16

• 125 new wells are connected to sales. 411 in operation at the end of the year.

• Operations expand to other areas within the U.S.

• Services are offered to Oil & Gas companies in Mexico.

• U.S. $133 million in revenues in 2013.

Newpek

I n 2013, Newpek continued to expand operations, turning in positive results. The company continued drilling at the Eagle Ford

Shale, where it connected 125 new wells to sales, bringing the total to 411 currently in operation. Net production to sales was 6,737 equivalent barrels of oil per day, 37% more than in 2012.

In line with its growth strategy, Newpek completed two major acquisitions in the U.S. The first involved 90,000 acres in Kansas, where it will explore and drill shallow oil formations in partnership with a prestigious local company. The second consists of a portfolio of 150,000 acres located in Texas, Oklahoma and Colorado. These acquisitions, along with the recruitment of technical staff with ample experience in the industry, strengthen the operational capabilities of Newpek.

In Mexico, Newpek in association with Monclova Pirineos Gas, took over the operation and development of two mature oil fields of Pemex in

Veracruz, Mexico. This in accordance with service contracts for the exploration, development and production of hydrocarbons won in June 2012. Operations in these fields are proceeding according to plan.

Newpek also formed a partnership with the British company Petrofac Plc in 2013. Together, these two companies created a subsidiary called

17

82

18

6.7

4.9

1312

Petroalfa, which provides comprehensive services to companies operating in the Mexican oil and gas industry.

Revenues and EBITDA totaled U.S. $133 million and U.S. $91 million in 2013, increasing 43% and 37%, respectively, compared to 2012.

Since its foundation, in 2006, Newpek has executed a strategy of growth and learning in the

value chain of the oil and gas industry. Now, with the approval of an energy reform that opens the door to the development of the energy industry in Mexico, its business prospects are more promising than ever. •

Revenue breakdown

(%)

n Oil and condensates nNatural gas

Production volume

(thousand equivalent barrels of oil per day)

18

Board of Directors

José Calderón Rojas (2A)

Chairman of the Board and Chief Executive Officer of Franca Industrias, S.A. de C.V. and FrancaServicios, S.A. de C.V.Board member since April 2005.Member of the Boards of FEMSA and BBVA Bancomer (Regional Board). President of Asociación Amigos del Museo del Obispado, A.C.

Enrique Castillo Sánchez Mejorada (1A)

Managing Partner of Ventura Capital Privado, S.A. de C.V.Board member since March 2010.Member of the Boards of Maxcom Telecomunicaciones, Southern Copper Corporation, Grupo Herdez, Organización Cultiba, Médica Sur and Grupo Aeroportuario del Pacífico. Alternate Board member of Grupo Financiero Banorte and Grupo Gigante.

Francisco Javier Fernández Carbajal (1C)

Chairman of the Board of Primero Fianzas, S.A. de C.V.Board member since March 2010.President of the Planning and Finance Committee.Member of the Boards of Visa Inc., FEMSA, CEMEX and Fresnillo PLC.

Álvaro Fernández Garza (3C)

President of ALFA, S.A.B. de C.V.Board member since April 2005.Member of the Boards of Vitro, Cydsa and Universidad de Monterrey. Currently, he is President of the Chamber of Industry of Nuevo León (CAINTRA).

Armando Garza Sada (3C)

Chairman of the Board of ALFA, S.A.B. de C.V.Board member since April 1991.Member of the Boards of FEMSA, Frisa, Grupo Financiero Banorte, Lamosa, Liverpool, Proeza, ITESM and Stanford University.

Claudio X. González Laporte (1B)

Chairman of the Board of Kimberly Clark de México, S.A.B. de C.V.Board member since December 1987.Member of the Boards of Fondo México, Grupo Carso, Grupo Financiero Inbursa, Grupo México, Grupo Televisa and Bolsa Mexicana de Valores. Consultant for Capital Group and President of Consejo Mexicano de Hombres de Negocio.

Ricardo Guajardo Touché (1B)

Board member since March 2000.Member of the Boards of Liverpool, Grupo Aeroportuario del Sureste, Grupo Bimbo, FEMSA, Coca-Cola FEMSA, Grupo Coppel and ITESM.

David Martínez Guzmán (1C)

Managing Director of Fintech Advisory Limited Board member since March 2010.Member of the Board of Vitro.

19

Adrián Sada González (1B)

Chairman of the Board of Vitro, S.A.B. de C.V.Board member since April 1994. President of the Corporate Practices Committee. Member of the Boards of Gruma, Cydsa and Consejo Mexicano de Hombres de Negocios.

Federico Toussaint Elosúa (1A)

Chairman of the Board and Chief Executive Officer of Grupo Lamosa, S.A.B. de C.V.Board member since April 2008. President of the Audit Committee.Member of the Boards of Xignux, Grupo Iconn, Universidad de Monterrey, Centro Roberto Garza Sada, Fibra Inn, Banco de México (Regional Board), President of Centro de Competitividad de México and Board member of Consejo Mexicano de Hombres de Negocios.

Guillermo F. Vogel Hinojosa (1C)

Chairman of the Board of Grupo Collado, S.A.B. de C.V., Vice Chairman of the Board of Tenaris, S.A. de C.V. and Vice Chairman of the Board of Estilo y Vanidad, S.A. de C.V.Board member since April 2008.Member of the Boards of Corporación Mexicana de Inversiones de Capital, Universidad Panamericana-IPADE, Fondo Nacional de Infraestructura, Corporación San Luis, Innovare and Eximpro.

Carlos Jiménez Barrera

Secretary of the Board

Keys:(1) Independent Board member(2) Independent Proprietary Board member(3) Related Proprietary Board member

(A) Audit Committee(B) Corporate Practices Committee(C) Planning and Finance Committee

20

Corporate Governance

• ALFA adheres to Mexico’s current Code of Best Corporate Practices in force in Mexico since 2000. This Code was developed at the initiative of the securities authorities of Mexico and its purpose is to establish a framework on corporate governance to increase investor confidence in Mexican companies.

• Companies whose stocks trade on the Mexican Stock Exchange must disclose the way they adhere to the Code of Best Corporate Practices. This is done annually by responding to a questionnaire, which is available to the public through the Mexican Stock Exchange’s web site.

• Following is a summary of ALFA’s corporate governance as stated in the June 2013 questionnaire, with any pertinent information updated.

A. The Board of Directors comprises 11 proprietary members who have no alternates. Of this number, 9 are independent. This annual report provides information on all of the Board’s members, identifying those who are independent and the Committees in which they participate.

B. Three Committees assist the Board of Directors in carrying out its duties: Audit, Corporate Practices, and Planning and Finance. Board members participate in at least one committee each. All three committees are headed by an independent board member. The Audit and Corporate Practices Committees are formed by independent members only.

C. The Board of Directors meets every two months. Meetings of the Board can be called by agreement of the Chairman of the Board, the President of the Audit Committees, the President of the Corporate Practices Committee, the Secretary of the Board or of at least 25% of its members. At least one of these meetings is dedicated to defining the company’s medium and long term strategy.

Armando Garza Sada

Chairman of the BoardJoined ALFA in 1978. B.S. from MIT. MBA from Stanford University.

Álvaro Fernández Garza

PresidentJoined ALFA in 1991. Graduated in Economics from Notre Dame University. Master’s degree in Management from ITESM and MBA from Georgetown University.

Mario H. Páez González

President of SigmaJoined ALFA in 1974. Graduated in Accounting and Master’s degree in Management from ITESM. MBA from Tulane University.

Armando Tamez Martínez

President of NemakJoined ALFA in 1984. Graduated in Engineering from ITESM. Master’s degree in Administration and Engineering from George Washington University.

José de Jesús Valdez Simancas

President of AlpekJoined ALFA in 1976. Graduated in Engineering. Master’s degree in Management from ITESM. Master’s degree in Industrial Engineering from Stanford University.

Management Team

21

D. Members must inform the Chairman of any conflicts of interest that may arise, and abstain from participating in the corresponding deliberations. Average attendance at Board meetings was 95% during 2013.

E. The Audit Committee studies and issues recommendations to the Board on matters such as the selection and determination of fees to the external auditor, coordinating with the internal audit area of the company, and studying accounting policies, among others.

F. The company has internal control systems with general guidelines. These are submitted to the Audit Committee for its opinion. In addition, the external auditor validates the effectiveness of the internal control system and issues the corresponding reports.

G. The Planning and Finance Committee evaluates all matters relating to its particular area and issues recommendations to the Board on matters such as feasibility of investments, strategic positioning of the company, alignment of investment and financing policies, and review of investment projects.

H. The Corporate Practices Committee is responsible for issuing recommendations to the Board in such matters as employment terms and severance payments for senior executives, and compensation policies, among others.

I. There is a department dedicated to maintaining an open line of communication between the company and its shareholders and investors. This ensures that investors have the financial and general information they require in order to evaluate the company’s development and progress.

Paulino J. Rodríguez Mendívil

Senior Vice President, Human CapitalJoined ALFA in 2004. Graduated in Engineering and Master’s degree in Energy Technology from the University of the Basque Country, Spain.

Manuel Rivera Garza

Senior Vice President, DevelopmentJoined ALFA in 1976. Graduated in Engineering from ITESM. Master’s degree in Industrial Engineering from Stanford University.

Ramón A. Leal Chapa

Chief Financial OfficerJoined ALFA in 2009. Graduated in Accounting from Universidad de Monterrey. Master’s degree in Operations Management from ITESM. MBA from Harvard University.

Alejandro M. Elizondo Barragán

Senior Vice President, DevelopmentJoined ALFA in 1976. Graduated in Engineering from ITESM. MBA from Harvard University.

Carlos Jiménez Barrera

Senior Vice President, Legal and Corporate AffairsJoined ALFA in 1976. Graduated in Law from Universidad de Monterrey. Master’s degree in Law from New York University.

Rolando Zubirán Shetler

President of AlestraJoined ALFA in 1999. Graduated in Engineering from UNAM. Master’s degree in Operations Research from the University of Southern California. Ph.D. in Philosophy from Universidad Autónoma de Nuevo León, with specialization in Management.

2222

Consolidated Financial Statements

Contents PageManagement’s Analysis 24Report of the Independent Auditors 35

Consolidated Financial StatementsConsolidated Statements of Financial Position 36Consolidated Statements of Income 38Consolidated Statements of Comprehensive Income 39Consolidated Statements of Changes in Stockholders’ Equity 40Consolidated Statements of Cash Flows 42Notes to the Consolidated Financial Statements 43Glossary 104

23

24

ALFA, S. A. B. DE C. V. AND SUBSIDIARIES

Management´s Analysis

2013The following report should be read in conjunction with Letter to Shareholders (pages 5 – 7) and the Audited Financial Statements (pages 35 – 101). Unless otherwise indicated, the figures from 2011 to 2013 are stated in millions of nominal Mexican pesos (Ps). Percentage changes are stated in nominal terms. In addition, some figures are stated in millions of US dollars (US$).

The financial information contained in this Analysis has been expanded in some sections to include three years and adjust it to the General Regulations, applicable to Issuers and Other Securities Market Participants, issued by the National Banking and Securities Commission (CNBV in spanish acronym) up to July 15, 2013.

The financial information contained in this Management Analysis corresponds to the last three years (2011, 2012 and 2013), and has been prepared in accordance with International Financial Reporting Standards (IFRS).

San Pedro Garza García, N. L., January 29, 2014.

ECONOMIC ENVIRONMENTAfter the Mexican economy reported a healthy growth in 2012, the economic environment suffered a slow down during 2013. The performance of the Gross Domestic Product (GDP) and other key variables are described in the following paragraphs:

At the date of the report, it is estimated that the Gross Domestic Product (GDP) in Mexico grew 1.3% in 2013, a lower percentage than in 2012. Consumer price inflation in México was 4.0%(b) in 2013, higher than the 3.6%(b) figure recorded in 2012. During 2013, the Mexican peso had an annual nominal depreciation of 0.5%(c), compared with an appreciation of 6.9%(c) in 2012. In real terms the annual average overvaluation of the Mexican peso vis-á-vis the U.S. dollar amounted to 15.5% (d) in 2013 compared with 14.2%(d) in 2012.

With respect to the interest rate in Mexico, the TIIE was 4.3%(b) in 2013 in nominal terms, compared with 4.8% in 2012. In real terms there was a decrease from an annual accumulated percentage of 1.3% in 2012 to 0.4% in 2013.

The average nominal dollar 3-months LIBOR, for the year 2013 was 0.3%(e) in 2013, similar to 0.4%(e) observed in 2012. Adjusting for the nominal depreciation of the Mexican pesos vis-á-vis the US dollar LIBOR in constant pesos changed from -9.7%(a) in 2012 to -3.1%(a) in 2013.

Sources:(a) Consultores Económicos Especializados, S. A. de C. V. (CEE).(b) Banco de México (Banxico).(c) Banxico. Exchange rate for liquidating liabilities denominated in foreign currency and payable in Mexico.(d) CEE. 1990 basis. Bilateral with the United States, adjusting for consumer prices. (e) British Bankers Association.

25

Revenue indexes(2008=100)

ALFA CONTINUES TO GROWALFA obtained favorable results in 2013. Its revenues and cash flow were increased as compared to 2012, achieving a solid financial position. The generation of cash flow during the year and the refinancing of the debt in international financial markets were favorable.

RESULTS REVENUESThe following table shows ALFA´s revenues for the years 2013, 2012 and 2011 breaking down its components of volume and price (the indexes are calculated on a base of 2008=100):

Change Change Concept 2013 2012 2011 2013-2012 (%) 2012-2011 (%)

Consolidated Revenues 203,456 200,167 182,967 2 9Volume index 147.8 143.8 129.6 3 11Price index pesos 116.1 117.5 120.1 (1) (2)Price index in US dollars 101.3 99.4 107.1 2 (7)

Likewise, the consolidated revenues broken down by ALFA’s principal bussines groups were as follows:

Change Change Concept 2013 2012 2011 2013-2012 2012-2011

Alpek 90,061 96,163 90,667 (6,102) 5,496Sigma 48,989 45,476 41,078 3,513 4,398Nemak 56,299 51,385 44,669 4,914 6,716Alestra 5,067 4,634 4,697 433 (63)Newpek 1,706 1,227 573 479 654Others 1,334 1,282 1,283 52 (1)Consolidated total 203,456 200,167 182,967 3,289 17,200

The behavior of revenues is explained as follows:

13

148

144

130111

98

12111009

VolumesPrices

13

116117

120118

104

12111009

101991079282

Pesos

Dollars

26

2013-2012:Consolidated sales in 2013 amounted to Ps203,456 (US $15,870), 2% over 2012 (5% in US dollars). Following is a discussion of the performance of each of the principal bussines groups:

Alpek’s sales in US dollars during 2013 were 3% lower than those of 2012. An environment of lower prices and margins in global polyester and caprolactam markets translates into a reduction in sales volume. However, the company continues to implement projects to improve efficiency and the integration of its operations.

In 2013, Sigma sold 1.2 million tons of food, 4% more than in 2012. Revenues were increased to US $3,280, 11% more than in 2012. These increases reflect greater sales of cold meats and dairy in Mexico, in addition to an improved productivity and distribution network.

On the other hand, in Nemak, the sales volume grew 11%, adding 47.6 million equivalent pieces. As a result, revenues increased to US $4,391, an increase of 13% vis-à-vis 2012.

In North America, the sales of cars grew 8%, adding 15.6 million vehicles. The decreased demand and consumer credit availability were the main drivers of this increase. In Europe, the market decreased 2%; however, the higher the concentration of Nemak with German warehouses, which have been successful in finding export opportunities outside the Eurozone, favored the Company’s increase of sales volume by 3%.

Furthermore, the use of aluminum auto parts to replace iron auto parts continues to grow, which also favored the company.

Alestra continued to promote added value services, such as cloud applications, security and administrative networks, as well as data services, internet and local for the business segment, which contributed with 84% of the company’s revenues in 2013. Revenues amounted to US $395, 13% over 2012.

Finally, Newpek connected 125 new wells to sales, to add up to 411. Of the above, 371 operate in Eagle Ford Shale and 40 in Edwards Trend. The net production to sales amounted to 6,737 equivalent average oil barrels per day, 37% more than in 2012. From the total volume, 52% corresponded to liquids and oil, with a considerably higher value to that of the dry gas, compared with 50% in 2012.

2012-2011:Consolidated sales in 2012 amounted to Ps200,167 (US $15,152), 9% over 2011 (3% in US dollars). Following is a discussion of the performance of each of the principal bussines gruops:

Alpek’s sales in Mexican pesos during 2012 were 6% higher than those of 2011. Sales were favorably impacted by a higher volume and by the monthly average exchange rate that was lower than during 2011, resulting in an increase in sales expressed in Mexican pesos. On the other hand, they were unfavorably affected by lower raw material prices during the second quarter of the year, which resulted in lower sales prices.

Sigma’s sales increased 11% in Mexican pesos in 2012. The markets serviced by Sigma in Mexico and US showed a healthy demand during most of the year, above all in Mexico. The efforts to win new clients, as well as the organic growth, were the origin of the increase in sales observed specially in yoghurt and cheese.

The sales in pesos of Nemak increased 15% vis-à-vis last year. This increase was based on the sales volume of 42 million heads equivalent heads in the year, 14% more than in 2011. Part of the growth is explained by the acquisition of JL French, company in the business of aluminum pieces for automotive transmission. Also, in continuing with the trend of replacing iron pieces for other aluminum pieces in automotive engines, as well as in the increase in sales of Nemak’s main clients. In Europe in particular, sales remained stable for German assemblers, who demanded new programs and were successful in finding export markets for their vehicles.

Alestra’s revenues decreased 1% as a result of a lower income from traditional long-distance services. The growth in domestic services of added value, fully compensated the decrease in revenues from AGN services, which Alestra ceased to offer after acquiring the shares of AT&T held by ALFA in 2011. Value added services represented 82% of total revenues at 2012 year end.

Finally, Newpek started operations in 135 new wells in 2012. The net sales production of equivalent crude barrels per day during 2012 grew 93% as compared to 2011. Approximately 50% of this volume corresponded to liquid hydrocarbons, including oil, with a substantially higher value than that of dry gas. Total revenues increased 114% in Mexican pesos with respect to 2011.

27

OPERATING PROFITOperating profit in 2013 and 2012, is explained as follows:

2013-2012: Change by group

Operating profit 2013 2012 Change Alpek Sigma Nemak Alestra Newpek Other

Revenues 203,456 200,167 3,289 (6,102) 3,513 4,914 433 479 52Operating profit 14,085 16,672 (2,587) (4,550) 495 961 370 148 (11)Consolidated operating margin (%) 6.9 8.1Alpek (%) 3.2 7.8Sigma (%) 10.8 10.5Nemak (%) 8.0 6.9Alestra (%) 26.2 20.8Newpek (%) 48.4 55.3

The 14% decrease in consolidated operating profit from 2012 to 2013 is explained by the individual performance of ALFA companies, as explained below:

In the case of Alpek, additionally to the lower margin environment in global markets of polyester and caprolactam, an item of Ps2,421 was charged to income, corresponding to the cost of closing facilities and discounting fixed assets of Cape Fear, which had an impact on operating profit.

In Sigma, the increase in sales explained above was shown in an increase in operating profit.

Nemak recorded operating profit in Mexican pesos, which was higher than that of 2012 by 27%. This was a result of an increase in the sales volume, as well as to a greater efficiency in the use of assets and obtaining of synergies among its 34 plants at a global level, as well as the initial integration of some other value-adding services, such as machined parts.

In 2013, Alestra continued strengthening its income mix, increasing its margins and strengthening its infrastructure to reduce costs. Additionally, it obtained a favorable legal resolution in fixed interconnection tariffs. This allowed a 39% increase in operating profit in US dollars vs. 2012. It is important to mention that in 2012, profit included the benefit of an agreement in favor of Alestra regarding fixed-mobile interconnection tariffs.

Operating income in Mexican pesos of Newpek increased 22% in 2013 vs. 2012. This is a consequence of having more operating wells. It is important to mention that the operating profit to sales ratio decreased in 2013 in relation to 2012 due to expenses related to the new projects that the company will start to develop in 2014.

2012-2011: Change by group

Operating profit 2012 2011 Change Alpek Sigma Nemak Alestra Newpek Other

Revenues 200,167 182,967 17,200 5,496 4,398 6,716 (63) 654 (1)Operating profit 16,672 12,672 4,000 (113 ) 1,387 1,568 426 468 264Consolidated operating margin (%) 8.1 7.0Alpek (%) 7.8 8.4Sigma (%) 10.5 8.3Nemak (%) 6.9 4.5Alestra (%) 20.8 11.8Newpek (%) 55.3 36.5

The 29% increase in consolidated operating profit from 2011 to 2012 is explained by the individual performance of ALFA companies, as explained below:

In Alpek’s case, income was reduced by 2% as a consequence of a reduced margin of exports of PTA, PET and Caprolactam, due to a greater competition in Asian markets.

In Sigma, prices of raw materials, such as meat and dairy increased significantly and this put pressure on the markets. However, the company faced this situation effectively and with higher productivity measures and an adequate policy, which allowed it to obtain a higher income that that of 2011. The synergies obtained in BAR-S operations also contributed to the result of the year.

Nemak recorded operating profit in Mexican pesos, which was higher than that of 2011 by 67%. This was the result of an increase in sales volume, combined with operating efficiencies for the advance in the launching curve for new market programs.

28

In 2012, Alestra improved its income mix, it obtained a favorable resolution regarding fixed-mobile interconnection tariffs and increased its operating efficiency. This allowed a 44% increase in operating profit vs. 2011, year in which such profit had shown an extraordinary adjustment from depreciation of assets, to adjust the useful lives of these assets to the new technological conditions.

Operating income of Newpek increased 225% in 2012 vs. 2011. This was a result of having more operating wells, as well as of producing a richer mix of liquid hydrocarbons and dry gas.

COMPOSITION OF REVENUES AND OPERATING PROFITThe percentage structure of revenues and operating profit of ALFA underwent changes between 2013, 2012 and 2011 mainly with a decrease in revenues and operating profit of Alpek and an incremental change in operating profit of Sigma and Nemak, all of which are explained above.

The following table shows these effects;

% of total

Revenues Operating profit

2013 2012 2011 2013 2012 2011Alpek 44 48 50 21 45 60Sigma 24 23 22 37 29 27Nemak 28 26 24 32 21 16Alestra 2 2 3 9 6 4Newpek 1 1 0 6 4 2Others 1 0 1 (5) (5) (9)Total 100 100 100 100 100 100

FINANCE COST, NETThe exchange gain is explained mainly by the macroeconomic environment during the year. As explained in the beginning, the Mexican peso had an annual nominal depreciation of only 0.5% in 2013. Therefore, it was not a determining factor of ALFA’s Finance cost, net during 2013 (even though it is a factor in the variation vs. 2012 as may be seen below). This year, the main component of Finance cost, net were the financial expenses, as explained below:

Finance cost, net determinants 2013 2012

General inflation (Dec. - Dec.) 4.0 3.6Variation % in nominal exchange rate at year end (0.5) 6.9Closing exchange rate, nominal 13.08 13.01Real appreciation (depreciation) Mexican pesos / dollars with respect to the prior year Year end 1.9 8.6 Average of the year 5.1 (4.2)Average interest rate: Nominal LIBOR 0.3 0.4 Nominal implicit, ALFA debt 5.9 6.1 LIBOR in real terms (3.1) (9.7) Real implicit, ALFA debt 2.6 (5.4)Average monthly debt of ALFA in US$ 4,170 4,225

Expressed in US$, the finance cost,net for the year of 2013, 2012 and 2011 were $295, $279 and $283, respectively.

Variation in finance cost, net in US$ 12/11 13/12

Due to a (higher) lower interest rate (34) (21)Due to a (higher) lower net petty cash debt 18 25Net Change (16) 4

Net financial expenses in profit include premiums paid in operations, such as: refinancing, operating interests, in 2013, 2012 and 2011, interest rate swaps and swaps of gas and gasoline and equity swaps in 2011, besides financial bank expenses.

29

Measures in pesos, the finance cost, net was integrated as follows:

Change

Finance cost,net 2013 2012 2011 13/12 12/11

Financial expenses: (3,978) (4,412) (4,120) 434 (292)Financial income 270 719 606 (449) 113Financial expenses, net (3,708) (3,693) (3,514) (15) (179)

Result from exchange fluctuation, net of derivative financial exchange rate operations. (349) 962 (1,244) (1,311) 2,206Total finance cost,net (4,057) (2,731) (4,758) (1,326) 2,027

The depreciation of the Mexican peso during 2013 vs. the appreciation of the peso in 2012 was the main factor to determine the negative finance cost, net variation between 2013 and 2012.

The fair value of ALFA’s derivative financial instruments at December 2013 and 2012 are as follows:

Fair value (Millions of US dollars)

Type of derivative, value or contract Dec. 13 Dec. 12

Exchange rate 0 0Cross currency swaps (29) (24)Interest rate (2) (20)Energy 2 (27)

INCOME TAX Following is an analysis of the principal determinants of income tax in each one of the years in comparison, starting from the concept of the Income Before Tax defined as operating profit less finance cost,net and share of losses of associates recognized by the equity method.

Change

2013 2012 2011 13/12 12/11

Income tax:Profit before income tax 9,987 13,941 7,883 (3,954) 6,058Share of losses of associates recognized by the equity method 41 31 41 (31) 10,028 13,941 7,914 (3,913) 6,027Statutory rate 30% 30% 30%Income tax at statutory rate (3,008) (4,182) (2,375) 1,174 (1,807)

+ / (-) Tax effect of permanent tax accounting differences:Tax vs. accounting basis of finance cost, net 338 652 (364) (314) 1,016

Other permanent differences, net (139) 241 106 (380) 135Total tax effect of permanent differences 199 893 (258) (694) 1,151Total income tax provision based on operations of the year (2,809) (3,289) (2,633) 480 (656)Recalculation of back taxes and other (383) (101) 82 (282) (183)Total income tax provision (charged) credited to profit (3,192) (3,390) (2,551) 198 (839)Effective tax rate 32% 25% 32%

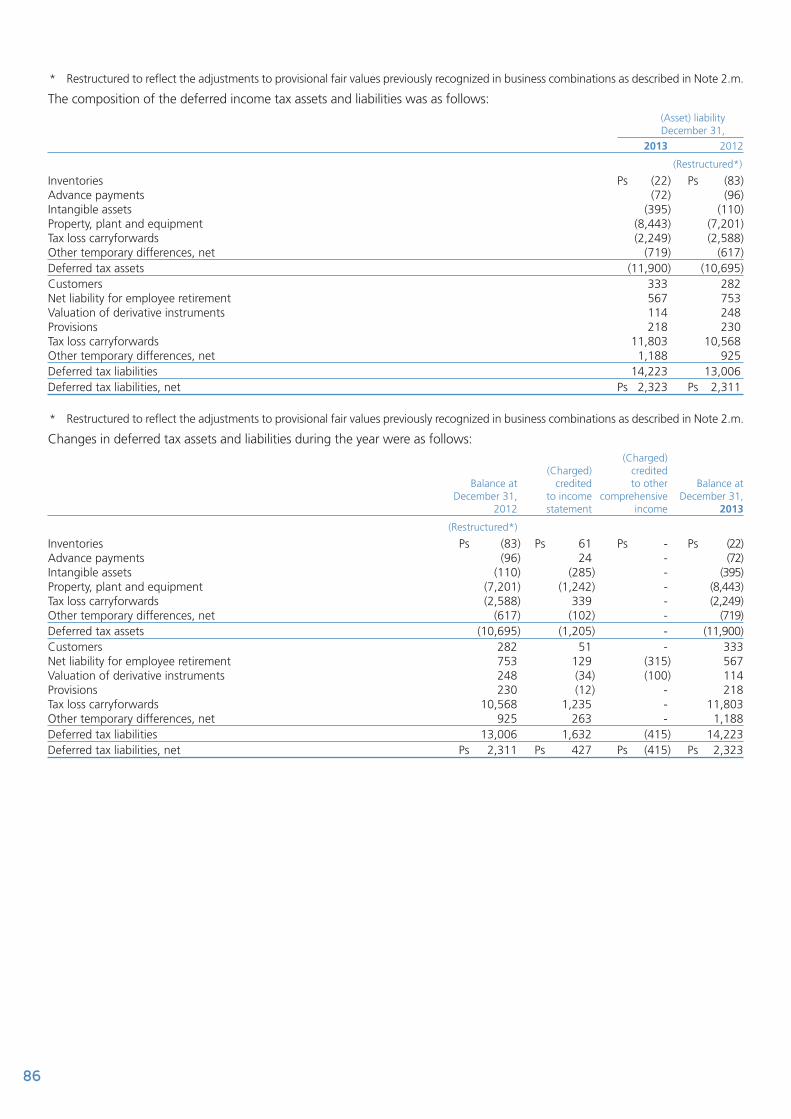

Income tax:Currently payable (3,531) (3,315) (2,017) (216) (1,298)Deferred 339 (75) (534) 414 459Total income tax provision charged to profit (3,192) (3,390) (2,551) 198 (839)

30

2013 NET PROFITDuring the year, ALFA obtained net consolidated profit, as broken down in the table below and it is the result of that explained with regard to the operating profit, finance cost, net and taxes:

Change

Statement of income 2013 2012 2011 13/12 12/11

Operating profit 14,085 16,672 12,672 (2,587) 4,000Finance cost, net (1) (4,057) (2,731) (4,758) (1,326) 2,027Equity in shares of losses of associates (41) (31) (41) 31Taxes (2) (3,192) (3,390) (2,551) 198 (839)Net consolidated income (loss) 6,795 10,551 5,332 (3,756) 5,219Net income (loss) of the controlling interest 5,926 9,361 4,748 (3,435) 4,613

(1) Comprehensive financing result(2) Income tax (payable and deferred)

COMPREHENSIVE INCOMEComprehensive income is shown in the statement of changes in stockholders’ equity and its objective is to show the total effect of all transactions and events which affected earned surplus. Operations between the company and its shareholders are excluded, mainly dividends paid. Comprehensive income in 2013, 2012 and 2011 was as follows:

Consolidated

Comprehensive income 2013 2012 2011

Net profit 6,795 10,551 5,332Effects of translation of foreign entities 456 (2,887) 3,492Effects of derivative financial instruments 234 87 (354)Remeasurement of obligations for the employees’ benefits 734 (306) (248)Consolidated comprehensive income 8,219 7,445 8,222Owners of the controlling company 7,740 6,332 7,176Non-controlling interest 479 1,113 1,046Comprehensive income for the year 8,219 7,445 8,222

A previous section in this report explains the net profit obtained in 2013, 2012 and 2011. The translation effect of subsidiaries abroad, which shows the effect from using different exchange rates between asset and liability accounts, against income and capital accounts, experienced an important change due to the volatility of the exchange rates of the currencies of different countries where ALFA is present. The effect in capital of derivative instruments, represents the effect for energy by-products that, in accordance with International Financial Reporting Standards, is shown in stockholders’ equity. The effect of remeasurement of obligations for employees’ benefits is the gain (loss) in actuarial estimates.

DIVIDENDS DECLARED AND INCREASE IN STOCKHOLDERS’ EQUITY

• ALFA’s Ordinary Stockholders’ Meeting approved the payment of an ordinary dividend of Ps1,513 equal to 0.29 pesos per share, 12% higher to that paid in 2012. Also, in December, an additional dividend was declared in the amount of Ps2,006 equal to 0.39 pesos per share. In 2012, the payment of an ordinary dividend was approved by Ps1,348, equal to 2.60 pesos per share, 19% higher than that paid in 2011. In turn, in 2011 an ordinary dividend was declared by PS1,133, equal to 2.12 pesos per share.

• In 2013, capital was increased by 7%. On the one hand, it was increased by the net income, due to the effect of labor liabilities in actuarial gains or losses and due to the translation effect, explained above, derived mainly from the depreciation of the Mexican peso, and on the other hand, decreasing due to the repurchase of own shares and the payment of dividends.

31

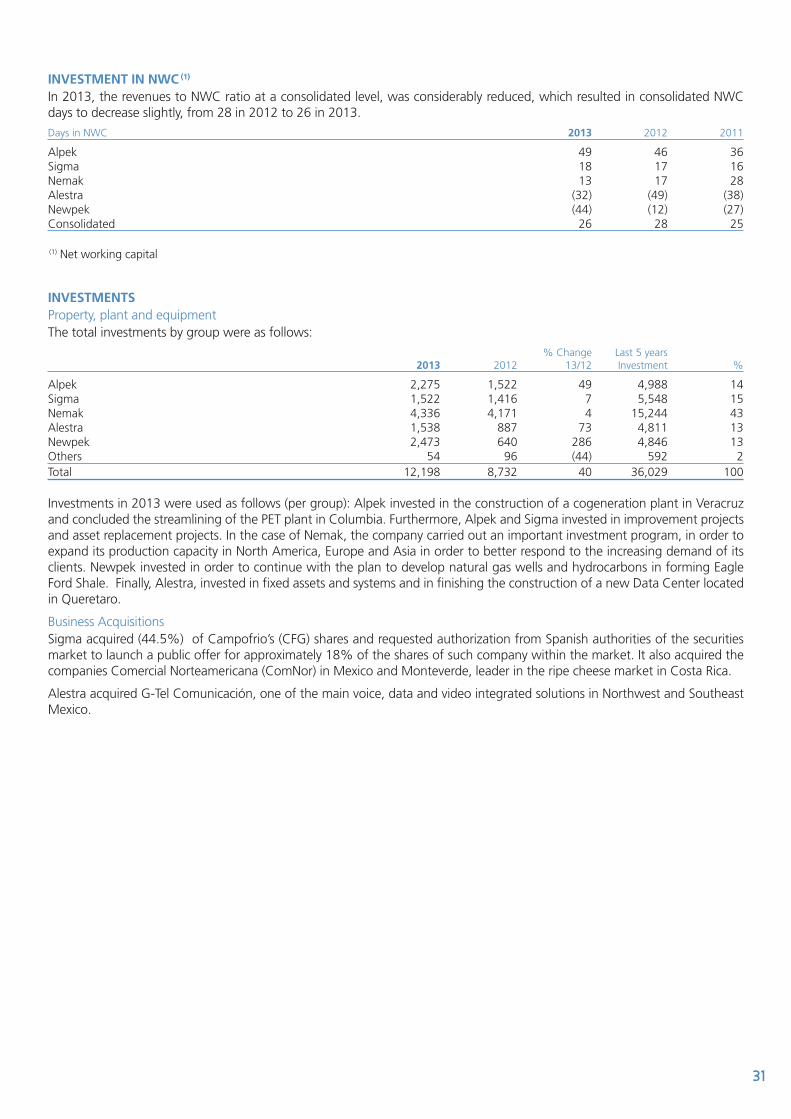

INVESTMENT IN NWC (1) In 2013, the revenues to NWC ratio at a consolidated level, was considerably reduced, which resulted in consolidated NWC days to decrease slightly, from 28 in 2012 to 26 in 2013.

Days in NWC 2013 2012 2011

Alpek 49 46 36Sigma 18 17 16Nemak 13 17 28Alestra (32) (49) (38)Newpek (44) (12) (27)Consolidated 26 28 25

(1) Net working capital

INVESTMENTSProperty, plant and equipmentThe total investments by group were as follows:

% Change Last 5 years 2013 2012 13/12 Investment %

Alpek 2,275 1,522 49 4,988 14Sigma 1,522 1,416 7 5,548 15Nemak 4,336 4,171 4 15,244 43Alestra 1,538 887 73 4,811 13Newpek 2,473 640 286 4,846 13Others 54 96 (44) 592 2Total 12,198 8,732 40 36,029 100

Investments in 2013 were used as follows (per group): Alpek invested in the construction of a cogeneration plant in Veracruz and concluded the streamlining of the PET plant in Columbia. Furthermore, Alpek and Sigma invested in improvement projects and asset replacement projects. In the case of Nemak, the company carried out an important investment program, in order to expand its production capacity in North America, Europe and Asia in order to better respond to the increasing demand of its clients. Newpek invested in order to continue with the plan to develop natural gas wells and hydrocarbons in forming Eagle Ford Shale. Finally, Alestra, invested in fixed assets and systems and in finishing the construction of a new Data Center located in Queretaro.

Business AcquisitionsSigma acquired (44.5%) of Campofrio’s (CFG) shares and requested authorization from Spanish authorities of the securities market to launch a public offer for approximately 18% of the shares of such company within the market. It also acquired the companies Comercial Norteamericana (ComNor) in Mexico and Monteverde, leader in the ripe cheese market in Costa Rica.

Alestra acquired G-Tel Comunicación, one of the main voice, data and video integrated solutions in Northwest and Southeast Mexico.

32

CASH FLOWSBased on the cash flows generated by operations, the following table shows the main transactions in 2013

2013 2012

Cash flows provided by operations 19,758 20,987Property, machinery and equipment and others (12,198) (8,732)Business acquisitions (5,983) (2,401)Increase (Decrease) in Bank Financing 4,918 (4,378)Dividends paid by ALFA SAB (3,510) (1,348)Dividends paid to non-controlling interest (1,612) (790)Repurchase of shares 0 (1,074)Changes in non-controlling interest 0 8,646Net Interest Paid (3,631) (3,796)Other 449 (1,113)(Decrease) increase in cash (1,809) 6,001Adjustment in cash flows from changes in exchange rates 50 (594)Cash and cash equivalents at beginning of year 13,661 8,254Total cash at end of year 11,902 13,661

The principal changes in the net debt of ALFA and its groups were the following:

Changes in net petty cash debt (DNC) US$ Consolidated Alpek Sigma Nemak Alestra Others Newpek

Balance at December 31, 2012 2,878 616 872 1,322 145 (13) (64)Long-term financing, net of payments: Financing 2,094 498 364 1,106 30 93 3 Payments (1,864) (507) (6) (1,214) 0 0 (137) 230 (9) 358 (108) 30 93 (134)

Short term financing, net of payments 144 15 55 (21) (26) 0 121Total financing, net of payments 374 6 413 (129) 4 93 (13)

Translation effect 18 (5) 11 14 (4) 0 2Debt variation in the statement of cash flows. 392 1 424 (115) 0 93 (11)Debt from acquired companies and others 20 0 (9) 0 29 0 0Total debt variation 412 1 415 (115) 29 93 (11)

Decrease (increase) in petty cash and restricted cash 177 149 31 (73) 0 3 67Change in interest payable 6 0 1 6 1 0 (2)Increase (decrease) in debt net of petty cash 595 150 447 (182) 30 96 54Balance at December 31, 2013 3,473 766 1,319 1,140 175 83 (10)

33

Sigma’s debt increases mainly due to the acquisitions made. The rest of the group, except for Nemak, also increased due to investment in fixed assets.

Supported by the different refinancing operations, the average life of ALFA’s total debt was increased as compared to last year. The maturity calendar of ALFA and its groups of companies underwent the following changes.

Short and long term Alpek Sigma Nemak Alestra Othersdebt by group 2013 2012 2013 2012 2013 2012 2013 2012 2013 2012

Debt balances (US$) 1,118 1,116 1,465 1,048 1,293 1,409 230 200 273 195

Debt balance percentageShort-term debt 3 2 4 1 3 4 0 0 37 26Long-term 1 year 2 1 15 1 6 7 87 0 18 32 2 6 15 0 21 8 11 0 100 34 42 3 4 6 4 0 12 33 13 0 0 0 4 0 4 0 0 13 35 0 0 9 0 5 years or more 85 72 77 77 58 10 0 0 2 0Total 100 100 100 100 100 100 100 100 100 100

Average life, long-term debt (years) 8.1 5.7 4.5 4.9 6.0 3.8 2.5 1.5 2.1 1.5Average life, total debt (years) 7.7 5.5 3.7 4.9 5.5 3.5 0.8 1.5 1.2 0.9

US$ % of total

Consolidated short and long term debt: 2013 2012 Change 2013 2012

Short-term debt 243 132 111 6 3Long-term 1 year 561 185 376 13 5 2 271 809 (538) 6 20 3 286 534 (248) 7 13 4 191 538 (347) 4 14 5 years or more 2,826 1,771 1,055 64 45Total 4,378 3,969 409 100 100

Average term of long-term debt (years) 5.9 4.3Average term of total debt (years) 4.9 4.0

34

FINANCIAL RATIOS LIQUIDITYThe ratio of DNC to cash flow increased at a consolidated level in 2013, mainly due to the increase in debt in Sigma and Alpek as shown in the following table:

Debt net of cash / Cash flows (in US dollars, last 12 months) groups 2013 2012

Alpek 1.34 0.83Sigma 2.52 1.83Nemak 1.87 2.58Alestra 1.03 1.05Newpek 0.91 (0.20)Consolidated 1.81 1.53

Interest coverage increased both at a consolidated level as at a group level. This is mainly due to the increase in cash flow.

Due to Change Cash Financial Interest coverage (in US dollars) * 2013 2012 13/12 flow expenses

Alpek 7.1 6.2 0.9 (1.3) 2.2Sigma 6.7 6.9 (0.2) 0.8 (1.0)Nemak 6.1 6.7 (0.6) 1.4 (2.0)Alestra 7.5 5.5 2.0 1.4 0.6Consolidated 6.7 6.4 0.3 0.2 0.1

* Defined as operating profit plus depreciation and amortization, divided by net financial expense.

FINANCIAL STRUCTUREALFA’s financial structure indicators improved during 2013, as observed in the table below:

Financial ratios 2013 2012

Total liabilities / Stockholdres’ equity 1.54 1.51Long-term debt / Total debt (%) 82 92Total currency debt / Total debt (%) 88 87

35

ALFA, S. A. B. DE C. V. AND SUBSIDIARIES

Report of the Independent Auditors

Monterrey, N. L., January 29, 2014

To the Shareholders’ Meeting of Alfa, S. A. B. de C. V.

We have audited the accompanying consolidated financial statements of Alfa, S.A.B. de C.V and subsidiaries, which comprise the consolidated statement of financial position as at December 31, 2013 and 2012, and the consolidated statements of income, comprehensive income, changes in stockholders’ equity and cash flows for the years ended December 31, 2013 and 2012, and a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Consolidated Financial Statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s ResponsibilityOur responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of the accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OpinionIn our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the financial position of Alfa, S. A. B. de C. V. and its subsidiaries as at December 31, 2013 and 2012, and its financial performance and its cash flows for the years ended December 31, 2013 and 2012, in accordance with International Financial Reporting Standards (IFRS).

PricewaterhouseCoopers, S.C.

Alberto Cano CharlesAudit Partner

36

Consolidated Statements of Financial Position

ALFA, S. A. B. DE C. V. AND SUBSIDIARIES

As of December 31, 2013 and 2012(Millions of Mexican pesos) Note 2013 2012 (Restructured *)

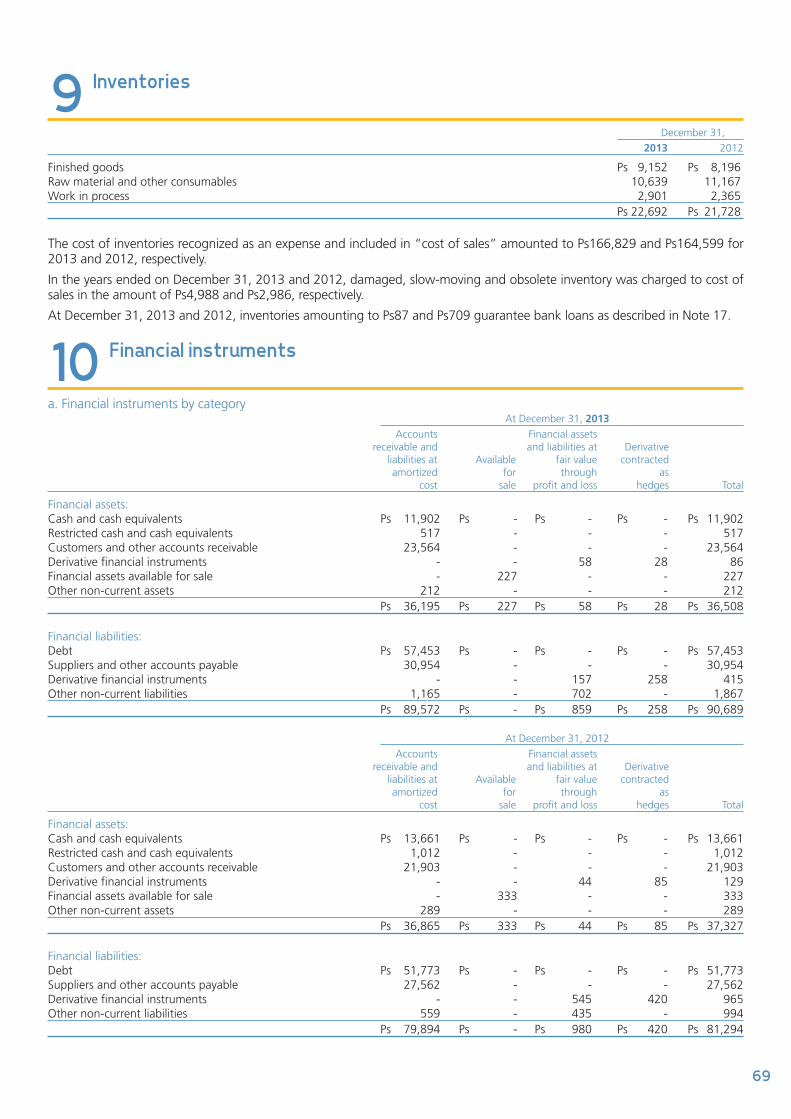

AssetsCURRENT ASSETS:Cash and cash equivalents 6 Ps 11,902 Ps 13,661Restricted cash and cash equivalents 7 364 577Customers and other accounts receivable, net 8 23,564 21,903Inventories 9 22,692 21,728Derivative financial instruments 10 86 129Other assets 11 1,043 976Total current assets 59,651 58,974

NON-CURRENT ASSETS:Property, plant and equipment, net 12 73,974 74,244Goodwill and intangible assets, net 13 23,906 18,732Deferred income tax 18 1,211 1,062Investments accounted using the equity method and others 14 6,648 1,213Total non-current assets 105,739 95,251

Total assets Ps 165,390 Ps 154,225

37

The accompanying notes are an integral part of these consolidated financial statements.

Álvaro Fernández Garza Ramón A. Leal ChapaPresident Chief Financial Officer

Note 2013 2012 (Restructured *)

Liabilities and Stockholders’ equityCURRENT LIABILITIES:Current debt 17 Ps 10,522 Ps 4,598Suppliers and other accounts payable 16 30,252 27,562Income tax payable 3.m 481 535Derivative financial instruments 10 78 378Provisions 19 833 -Other liabilities 20 534 559Total current liabilities 42,700 33,632

NON-CURRENT LIABILITIES:Non-current debt 17 46,932 47,175Derivative financial instruments 10 337 587Provisions 19 543 716Deferred income tax 18 3,534 3,373Deferred income tax from tax consolidation 18 3,785 4,473Employees’ benefits 21 1,891 2,690Other liabilities 20 499 435Total non-current liabilities 57,521 59,449Total liabilities 100,221 93,081

STOCKHOLDERS’ EQUITY:Controlling interest:Capital stock 22 210 211Retained earnings 22 55,643 52,106Other reserves 22 588 92Total controlling interest 56,441 52,409

Non-controlling interest 8,728 8,735Total stockholders’ equity 65,169 61,144Total liabilities and stockholders’ equity Ps 165,390 Ps 154,225

* Restructured to reflect the adjustments to provisional fair values previously recognized in business combinations as described in Note 2.m.

38

Consolidated Statements of Income

ALFA, S. A. B. DE C. V. AND SUBSIDIARIES

For the years ended December 31, 2013 and 2012 (Millions of Mexican pesos) Note 2013 2012 (Restructured *)

Revenue 3.u and 32 Ps 203,456 Ps 200,167Cost of sales 25 (166,829) (164,599)Gross profit 36,627 35,568

Selling expenses 25 (11,142) (10,845)Administrative expenses 25 (9,189) (8,369)Other revenues (expenses), net 26 210 (49)Operating profit before non-recurring items 16,506 16,305

Non-recurring items 27 (2,421) 367Operating profit 14,085 16,672

Financial income, including foreign exchange gain of Ps16 and Ps962 in 2013 and 2012, respectively 28 286 1,681Financial costs, including foreign exchange loss of Ps365 in 2013 28 (4,343) (4,412)Financial costs, net (4,057) (2,731)

Share of losses of investments accounted for using the equity method 14 (41) -Profit before income tax 9,987 13,941

Income tax expense 30 (3,192) (3,390)Net consolidated profit Ps 6,795 Ps 10,551

Profit attributable to:Controlling interest Ps 5,926 Ps 9,361

Non-controlling interest 869 1,190 Ps 6,795 Ps 10,551Earnings per basic and diluted share, in pesos Ps 1.15 Ps 1.81Weighted average of outstanding shares (thousands of shares) 5,143,886 5,170,650

* Restructured to reflect the adjustments to provisional fair values previously recognized in business combinations as described in Note 2.m.

The accompanying notes are an integral part of these consolidated financial statements.

Álvaro Fernández Garza Ramón A. Leal ChapaPresident Chief Financial Officer

39

Consolidated Statements of Comprehensive Income

ALFA, S. A. B. DE C. V. AND SUBSIDIARIES

The accompanying notes are an integral part of these consolidated financial statements.

For the years ended December 31, 2013 and 2012 (Millions of Mexican pesos) Note 2013 2012 (Restructured *)

Net consolidated profit Ps 6,795 Ps 10,551

Other comprehensive income (loss) for the year, net of tax:Items not to be reclassified to income statement Remeasurement of obligations for employees’ benefits 20 734 (306)Items to be reclassified to income statement Effect of derivative financial instruments designated as cash flow hedges 10 234 87 Effect of translation of foreign entities 21 456 (2,887)Total other comprehensive income (loss) for the year 1,424 (3,106)Total comprehensive income for the year Ps 8,219 Ps 7,445

Attributable to:Controlling interest Ps 7,740 Ps 6,332Non-controlling interest 479 1,113Total comprehensive income for the year Ps 8,219 Ps 7,445

* Restructured to reflect the adjustments to provisional fair values previously recognized in business combinations as described in Note 2.m.

Álvaro Fernández Garza Ramón A. Leal ChapaPresident Chief Financial Officer

40

Consolidated Statements of Changes in Stockholders’ Equity

ALFA, S. A. B. DE C. V. AND SUBSIDIARIES

For the years ended December 31, 2013 and 2012(Millions of Mexican pesos) Total Non- Total Capital Retained Other controlling controlling stockholders’ Note Stock earnings reserves interest interest equity

Balances at January 1, 2012 Ps 217 Ps 40,662 Ps 2,815 Ps 43,694 Ps 4,571 Ps 48,265

Transactions with shareholders:

Dividends declared by Alfa 21 - (1,348) - (1,348) - (1,348)

Repurchase of own shares 21 (6) (1,068) - (1,074) - (1,074)

Dividends from subsidiaries to non-controlling interest 3.b - - - - (790) (790)

Changes in the non-controlling interest 3.b - 4,805 - 4,805 3,841 8,646

(6) 2,389 - 2,383 3,051 5,434

Net profit (Restructured*) - 9,361 - 9,361 1,190 10,551

Total other comprehensive income for the year - (306) (2,723) (3,029) (77) (3,106)

Comprehensive income (Restructured*) - 9,055 (2,723) 6,332 1,113 7,445

Balances at December 31, 2012 (Restructured*) 211 52,106 92 52,409 8,735 61,144

Transactions with shareholders:

Dividends declared by Alfa 21 - (3,529) - (3,529) - (3,529)

Repurchase of own shares 21 (1) (98) - (99) - (99)

Dividends from subsidiaries to non-controlling interest 3.b - - - - (1,612) (1,612)

Changes in the non-controlling interest 2.n - - - - 1,133 1,133

(1) (3,627) - (3,628) (479) (4,107)

Net profit - 5,926 5,926 869 6,795

Total other comprehensive income for the year - 1,318 496 1,814 (390) 1,424

Comprehensive income - 7,244 496 7,740 479 8,219

Effects from adoption of new accounting policies 3.x - (80) - (80) (7) (87)

Balances at December 31, 2013 Ps 210 Ps 55,643 Ps 588 Ps 56,441 Ps 8,728 Ps 65,169

The accompanying notes are an integral part of these consolidated financial statements.

* Restructured to reflect the adjustments to provisional fair values previously recognized in business combinations as described in Note 2.m.

Álvaro Fernández Garza Ramón A. Leal ChapaPresident Chief Financial Officer

41

Consolidated Statements of Changes in Stockholders’ Equity

For the years ended December 31, 2013 and 2012(Millions of Mexican pesos) Total Non- Total Capital Retained Other controlling controlling stockholders’ Note Stock earnings reserves interest interest equity

Balances at January 1, 2012 Ps 217 Ps 40,662 Ps 2,815 Ps 43,694 Ps 4,571 Ps 48,265

Transactions with shareholders:

Dividends declared by Alfa 21 - (1,348) - (1,348) - (1,348)

Repurchase of own shares 21 (6) (1,068) - (1,074) - (1,074)

Dividends from subsidiaries to non-controlling interest 3.b - - - - (790) (790)

Changes in the non-controlling interest 3.b - 4,805 - 4,805 3,841 8,646

(6) 2,389 - 2,383 3,051 5,434

Net profit (Restructured*) - 9,361 - 9,361 1,190 10,551

Total other comprehensive income for the year - (306) (2,723) (3,029) (77) (3,106)

Comprehensive income (Restructured*) - 9,055 (2,723) 6,332 1,113 7,445

Balances at December 31, 2012 (Restructured*) 211 52,106 92 52,409 8,735 61,144

Transactions with shareholders:

Dividends declared by Alfa 21 - (3,529) - (3,529) - (3,529)

Repurchase of own shares 21 (1) (98) - (99) - (99)

Dividends from subsidiaries to non-controlling interest 3.b - - - - (1,612) (1,612)

Changes in the non-controlling interest 2.n - - - - 1,133 1,133

(1) (3,627) - (3,628) (479) (4,107)

Net profit - 5,926 5,926 869 6,795

Total other comprehensive income for the year - 1,318 496 1,814 (390) 1,424

Comprehensive income - 7,244 496 7,740 479 8,219

Effects from adoption of new accounting policies 3.x - (80) - (80) (7) (87)

Balances at December 31, 2013 Ps 210 Ps 55,643 Ps 588 Ps 56,441 Ps 8,728 Ps 65,169

42

ALFA, S. A. B. de C. V. Y SUBSIDIARIAS

Consolidated Statements of Cash Flows

The accompanying notes are an integral part of these consolidated financial statements.

For the years ended December 31, 2013 and 2012(Millions of Mexican pesos) Note 2013 2012 (Restructured *)

Cash flows from operating activitiesProfit before income tax Ps 9,987 Ps 13,941Depreciation and amortization 12 7,932 7,962Impairment of long-lived assets 25 2,518 270Costs associated with seniority premiums and pension plan 93 (206)Loss on sale of property, plant and equipment 25 (1) (37)Effect of changes in fair value of derivative financial instruments 50 (497)Foreign exchange, net 365 (739)Other non-operating expenses and finance products, net 2,808 3,799Increase in customers and other accounts receivable (1,131) (103)Increase in inventory (584) (1,419)Increase (decrease) in suppliers and other accounts payable 2,104 (379)Income tax paid (4,383) (1,605)Net cash generated from operating activities 19,758 20,987

Cash flows from investing activitiesInterest received 267 315Acquisition of property, plant and equipment 12 (7,763) (7,318)Purchases of intangible assets 13 (4,435) (1,414)Business acquisitions 2 (7,116) (2,401)Restricted cash 6 474 (278)Dividends received 43 58Other assets (373) (1,063)Net cash used in investing activities (18,903) (12,101)

Cash flows from financing activitiesProceeds from borrowings or debt 16 38,247 22,076Payments of borrowings or debt 16 (33,329) (26,454)Interest paid (3,631) (3,796)Dividends paid by Alfa, S. A .B. de C. V. (3,510) (1,348)Dividends paid to the non-controlling interest 3.b (1,612) (790)Repurchase of shares 22 (99) (1,074)Changes in the non-controlling interest 2.n 1,133 8,646Other 137 (145)

Cash used in financing activities (2,664) (2,885)Net increase in cash and cash equivalents (1,809) 6,001Exchange losses (gains) on cash and cash equivalents 50 (594)Cash and cash equivalents at beginning of year 13,661 8,254Cash and cash equivalents at end of year Ps 11,902 Ps 13,661

* Restructured to reflect the adjustments to provisional fair values previously recognized in business combinations as described in Note 2.m.

ALFA, S. A. B. DE C. V. AND SUBSIDIARIES

Álvaro Fernández Garza Ramón A. Leal ChapaPresident Chief Financial Officer

43

ALFA, S. A. B. de C. V. Y SUBSIDIARIAS

At December 31, 2013 and 2012

1 ALFA companies’ activities

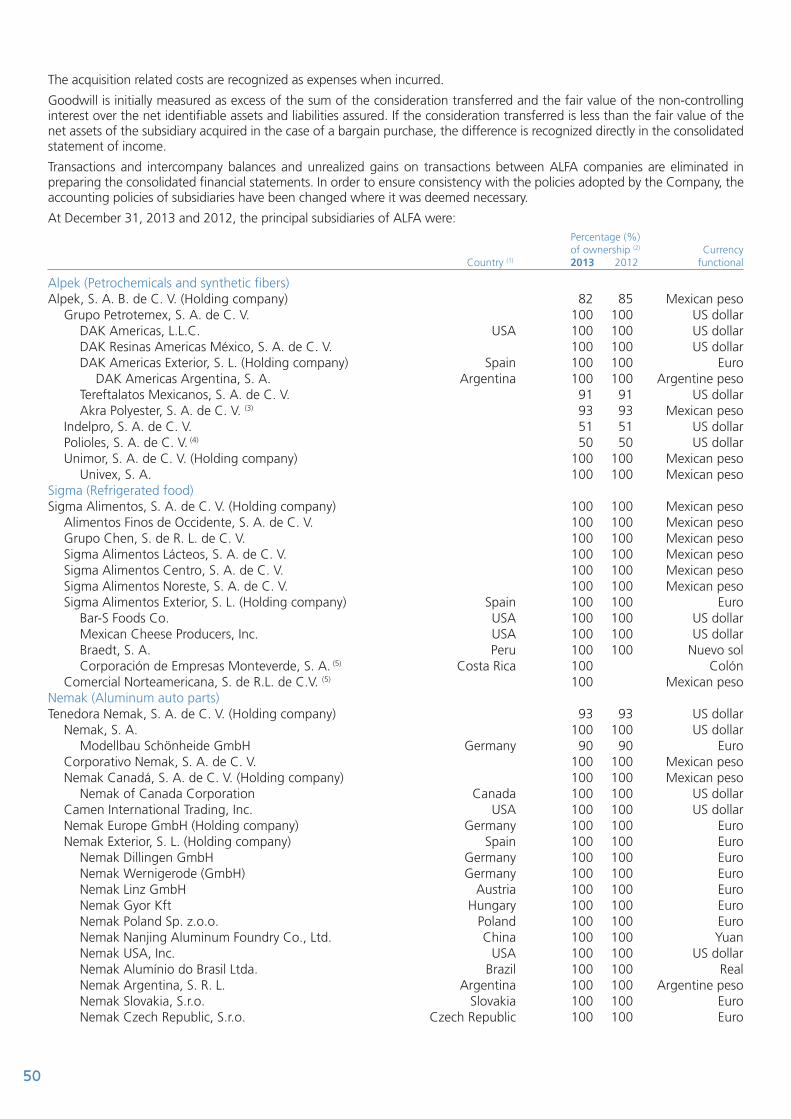

Alfa, S. A. B. de C. V. and subsidiaries (“ALFA” or “the Company”), is a Mexican company controlling five business groups with the following activities: Alpek, engaged in the production of petrochemicals and synthetic fibers; Sigma, a refrigerated food producer; Nemak, engaged in the manufacture of high-tech aluminum auto parts; Alestra, in the telecommunications sector, and Newpek, a natural gas and hydrocarbons company .

ALFA has an outstanding competitive position globally in the auto parts segment as a producer of aluminum engine heads and blocks, as well as in the manufacture of PTA (raw material for the manufacture of polyester), and is a leader in the Mexican market for refrigerated foods. ALFA operates industrial production and distribution centers mainly in Mexico, the United States (U.S.), Canada, Germany, Slovakia, the Czech Republic, Costa Rica, the Dominican Republic, El Salvador, Argentina, Peru, Austria, Brazil, China, Hungary, Spain, India and Poland. The company markets its products in over 40 countries worldwide and employs over 60,000 people.

ALFA’s shares are traded on the Mexican Stock Exchange, S. A. B. de C. V., and Latibex, the Latin American market of the Madrid Stock Exchange.

ALFA is located in Avenida Gómez Morín Sur No. 1111, Col. Carrizalejo, San Pedro Garza García, Nuevo León, Mexico.