ANNUAL REPORT - investor.ascottresidencetrust.com · The Ascott Reit story began in 2006, when it...

202

ANNUAL REPORT 2012

Transcript of ANNUAL REPORT - investor.ascottresidencetrust.com · The Ascott Reit story began in 2006, when it...

ANNUALREPORT 2012

Over the years, Ascott Reit has strengthened its portfolio and achieved greater success through an excellent track record. Staying committed to our goals has propelled us to grow from strength to strength to become who we are today – a trusted company recognised for quality assets and sound management strategies, and an award winning Reit manager that delivers stable returns to Unitholders.

About Ascott Reit

Ascott Residence Trust (Ascott Reit) was established with the objective of investing primarily in real estate and real estate-related assets which are income-producing and which are used or predominantly used as serviced residences or rental housing properties and other hospitality assets.

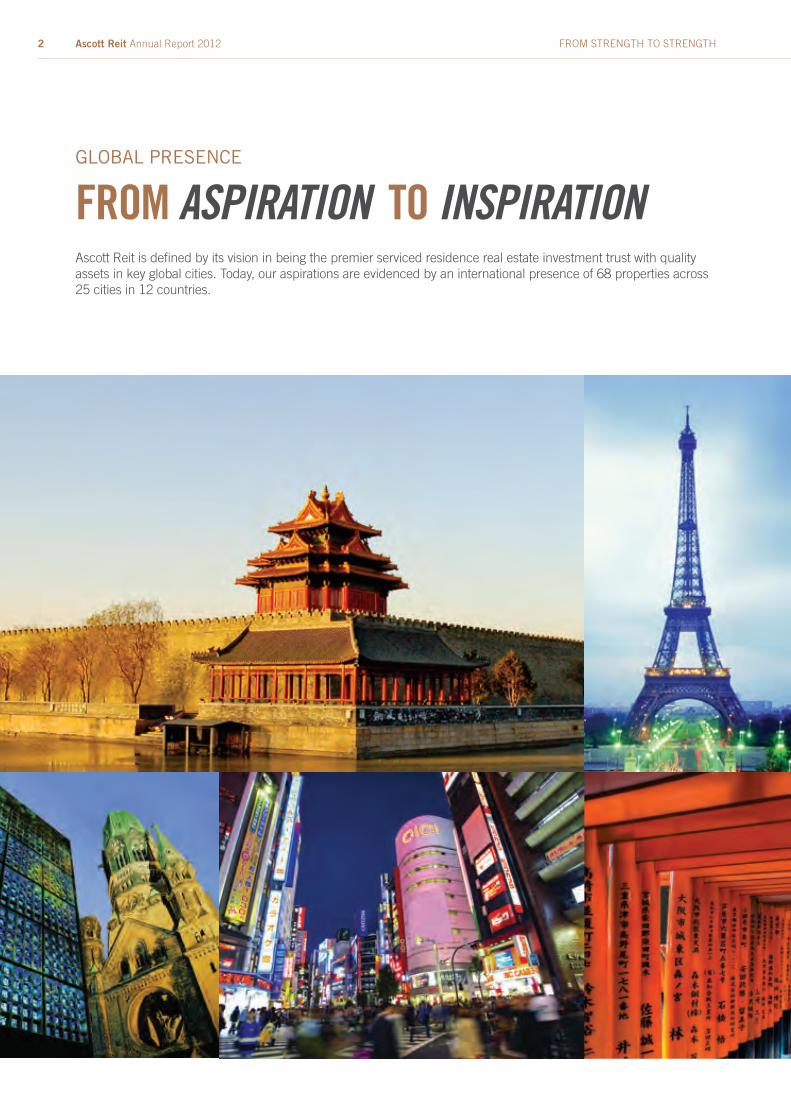

Ascott Reit’s asset size has more than tripled to about S$2.8 billion as at 31 December 2012 since it was listed on the Singapore Exchange Securities Trading Limited (SGX-ST) in March 2006. When the acquisition of the new Cairnhill serviced residence in Singapore is completed, Ascott Reit’s international portfolio will expand to S$3.2 billion comprising 68 properties with 7,427 units in 25 cities across 12 countries in Asia Pacific and Europe. Ascott Reit’s serviced residences are operated under the Ascott, Citadines and Somerset brands, and are mainly located in key gateway cities such as Singapore, Beijing, Shanghai, Guangzhou, Tokyo, London, Paris, Berlin, Brussels, Barcelona, Munich, Hanoi, Ho Chi Minh City, Jakarta, Manila and Perth.

Ascott Reit is managed by Ascott Residence Trust Management Limited (ARTML), a wholly owned subsidiary of The Ascott Limited (Ascott) and an indirect wholly owned subsidiary of CapitaLand Limited, one of Asia’s largest real estate companies.

Our Vision

We believe in being the premier serviced residence real estate investment trust with quality assets in key global cities.

Our Mission

We believe in delivering stable and sustainable returns to Unitholders.

FROM STRENGTH TO STRENGTHANNUAL REPORT 2012

CONTENTSGlobal Presence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2Milestones . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Letter to Unitholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Financial Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14Trust Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16The Manager . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22Value Creation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

- Active Asset Management . . . . . . . . . . . . . . . . . . . . . 26 - Growth by Acquisition . . . . . . . . . . . . . . . . . . . . . . . . . . 28 - Capital and Risk Management . . . . . . . . . . . . . . . . . 30

Corporate Governance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32Our People and the Community . . . . . . . . . . . . . . . . . . . . 46

- Caring for Our Communities . . . . . . . . . . . . . . . . . . . 48 - Creating a Sustainable Environment . . . . . . . . . . . 50 - Nurturing Our Human Capital . . . . . . . . . . . . . . . . . . 52

Investor Relations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54Portfolio Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56Operations Review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62Financial Review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88Directory Listing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97Additional Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 191Notice of Annual General Meeting . . . . . . . . . . . . . . . . . 194Proxy Form . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 197Corporate Information

Ascott Reit Annual Report 2012 1FROM STRENGTH TO STRENGTH

Ascott Reit is defined by its vision in being the premier serviced residence real estate investment trust with quality assets in key global cities. Today, our aspirations are evidenced by an international presence of 68 properties across 25 cities in 12 countries.

GLOBAL PRESENCE

FROM ASPIRATION TO INSPIRATION

Ascott Reit Annual Report 20122 FROM STRENGTH TO STRENGTH

Ascott Reit Annual Report 2012 3FROM STRENGTH TO STRENGTH

ASCOTT REIT’S SHAREOF ASSET VALUES

As at 31 December 2012

Ascott Reit enjoys balance in income stability and growth in view of our extended-stay business model and geographic spread.

25 cities 12 countries7,427 apartment unitsS$3.2 billion1 share of asset values

GLOBAL PRESENCE

1. Includes new Cairnhill serviced residence.

United Kingdom

London

Belgium

Brussels

ParisCannesGrenobleLilleLyonMarseilleMontpellier

France

Germany

BerlinMunichHamburg

Barcelona

Spain

Ascott Reit Annual Report 20124 FROM STRENGTH TO STRENGTH

25 cities 12 countries7,427 apartment unitsS$3.2 billion1 share of asset values

China

BeijingTianjinShanghaiGuangzhou

HanoiHo Chi Minh City

Vietnam

Jakarta

Indonesia

Perth

Australia

Singapore

Philippines

Manila

Japan

TokyoKyoto

Ascott Reit Annual Report 2012 5FROM STRENGTH TO STRENGTH

MILESTONES

FROM THEN TO NOW

2007 Acquired Somerset Azabu East Tokyo S$79.8 million Acquired 60% stake in Somerset Roppongi Tokyo S$36.4 million

Acquired 40.2% stake in Somerset Chancellor Court Ho Chi Minh City S$27.9 million Acquired 18 Rental Housing Properties in Tokyo S$158.6 million

2006 Ascott Reit goes public with an initial portfolio of 12 properties in 5 countries. Acquired SomersetOlympic TowerProperty TianjinS$75.6 million Acquired 40% stake in SomersetRoppongi TokyoS$20.7 million

Acquired Ascott MakatiS$84.4 million

Acquired Somerset Gordon Heights Melbourne S$13.9 million Acquired 26.8% stake in Somerset Chancellor Court Ho Chi Minh City S$8 million

2008 Acquired Somerset St Georges Terrace Perth S$36.1 million Acquired 70% stake in Somerset West Lake Hanoi S$22.9 million

The Ascott Reit story began in 2006, when it became the world’s first Pan-Asian serviced residence real estate investment trust. While the initial asset size of S$856 million has grown to S$3.2 billion, our fundamentals for stability and diversity have remained unchanged. From then to now, they continue to underscore our objectives of steady growth and sustainable returns.

Ascott Reit Annual Report 20126 FROM STRENGTH TO STRENGTH

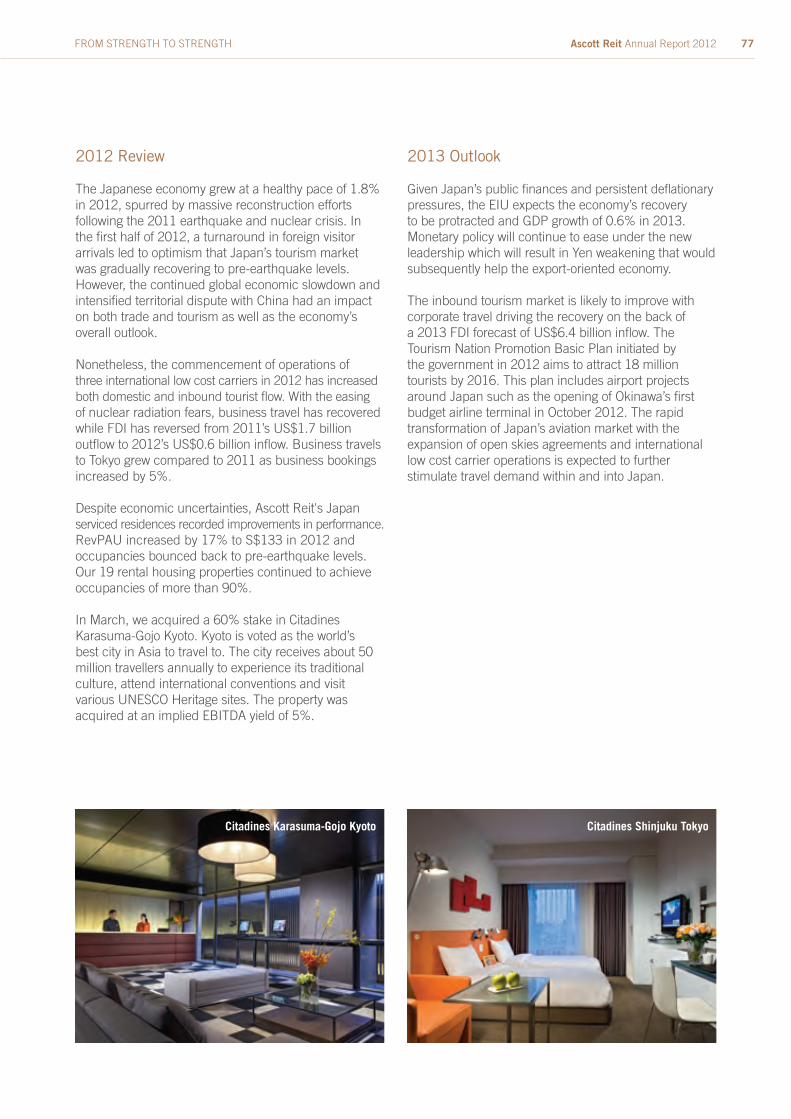

2012 Acquired 60% stake in Citadines Karasuma-Gojo Kyoto S$18.3 million Acquired Ascott Raffles Place SingaporeS$220 million

Acquired Ascott GuangzhouS$63.5 million

Acquired New Cairnhill Serviced Residence S$405 million

Acquired Madison Hamburg S$59.4 million Divested Somerset Gordon Heights Melbourne S$15.3 million Divested Somerset Grand Cairnhill Singapore S$359 million

2011 Acquired 60% stake in Citadines Shinjuku Tokyo S$45.7 million

2010Acquired 2 Asian and 26 European properties S$1.4 billion Divested Ascott Beijing S$301.8 million Divested Country Woods Jakarta S$33.9 million

Ascott Reit Annual Report 2012 7FROM STRENGTH TO STRENGTH

LETTER TO UNITHOLDERS

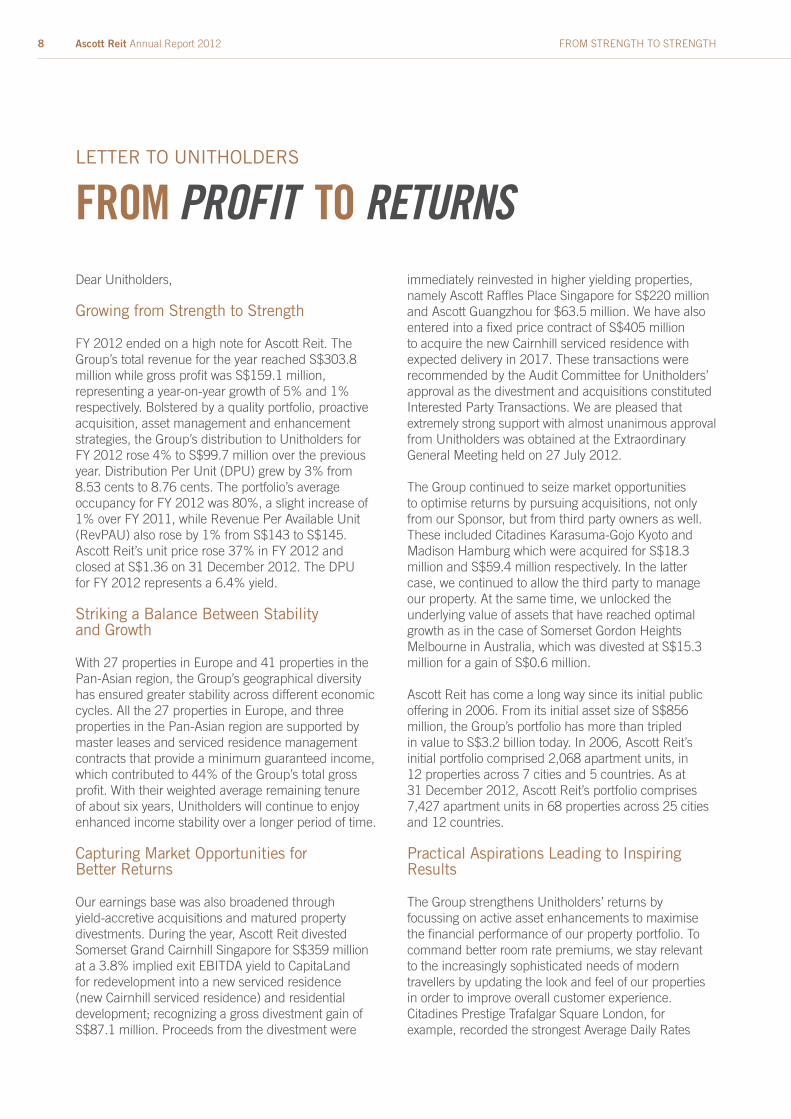

FROM PROFIT TO RETURNSDear Unitholders,

Growing from Strength to Strength

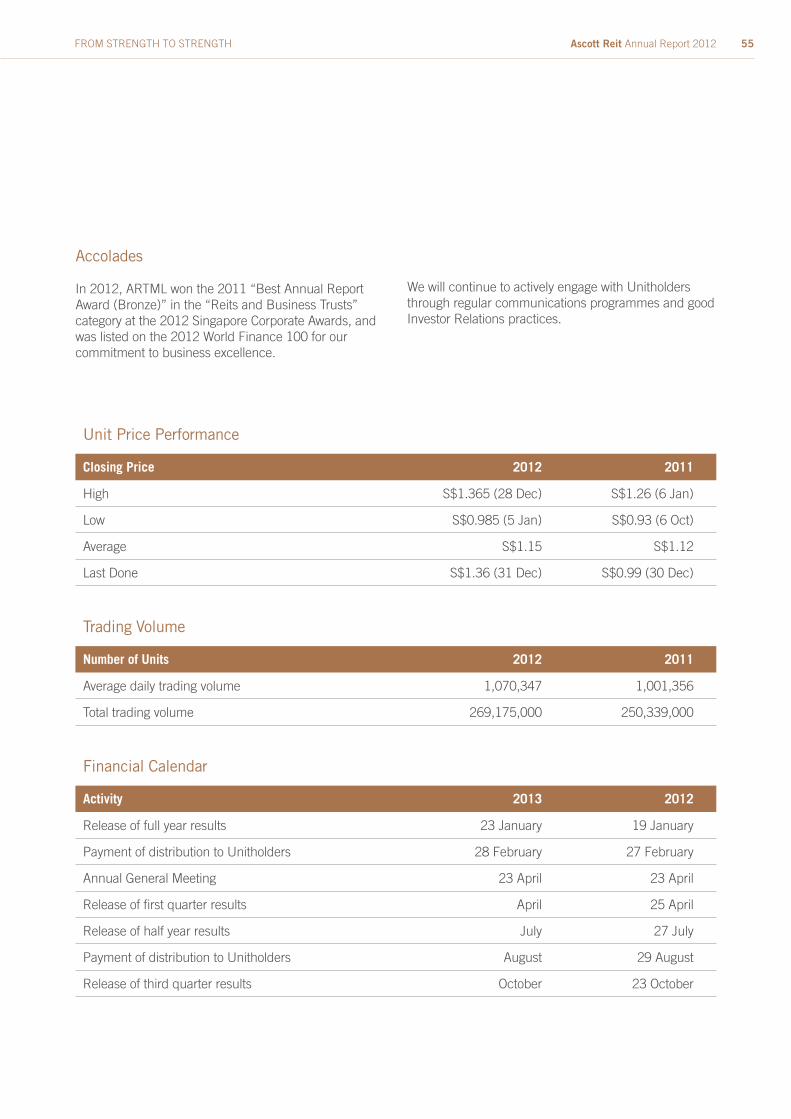

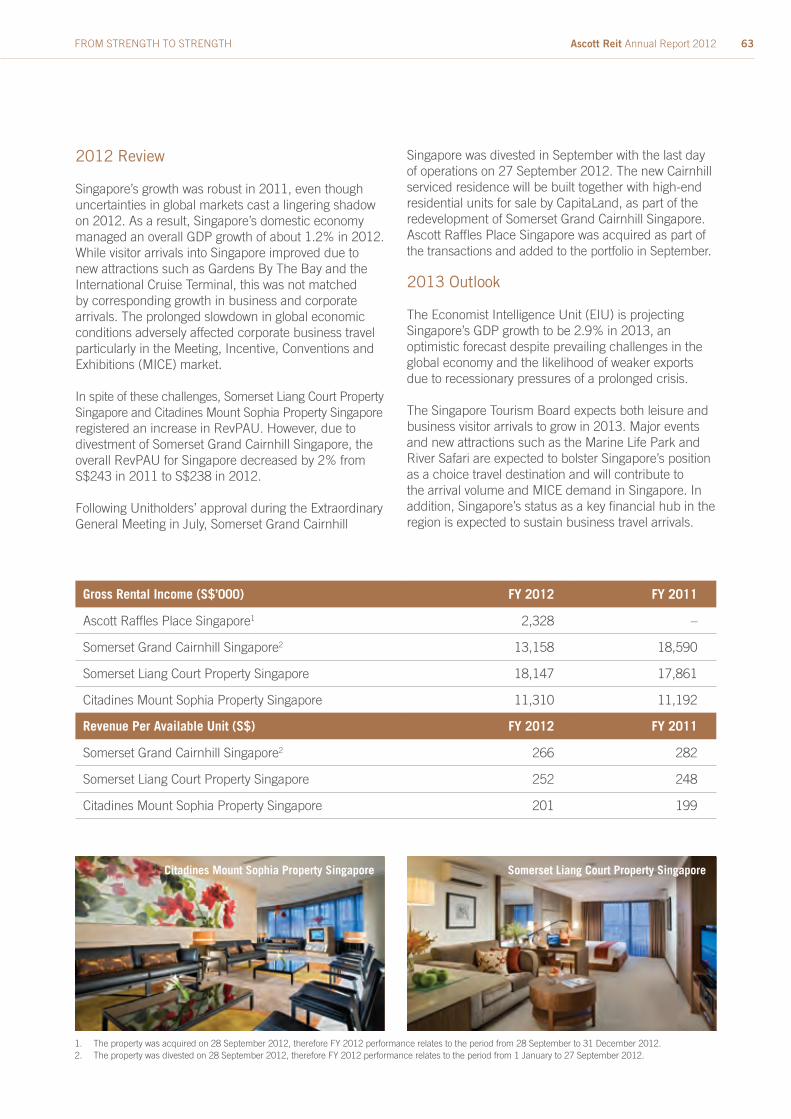

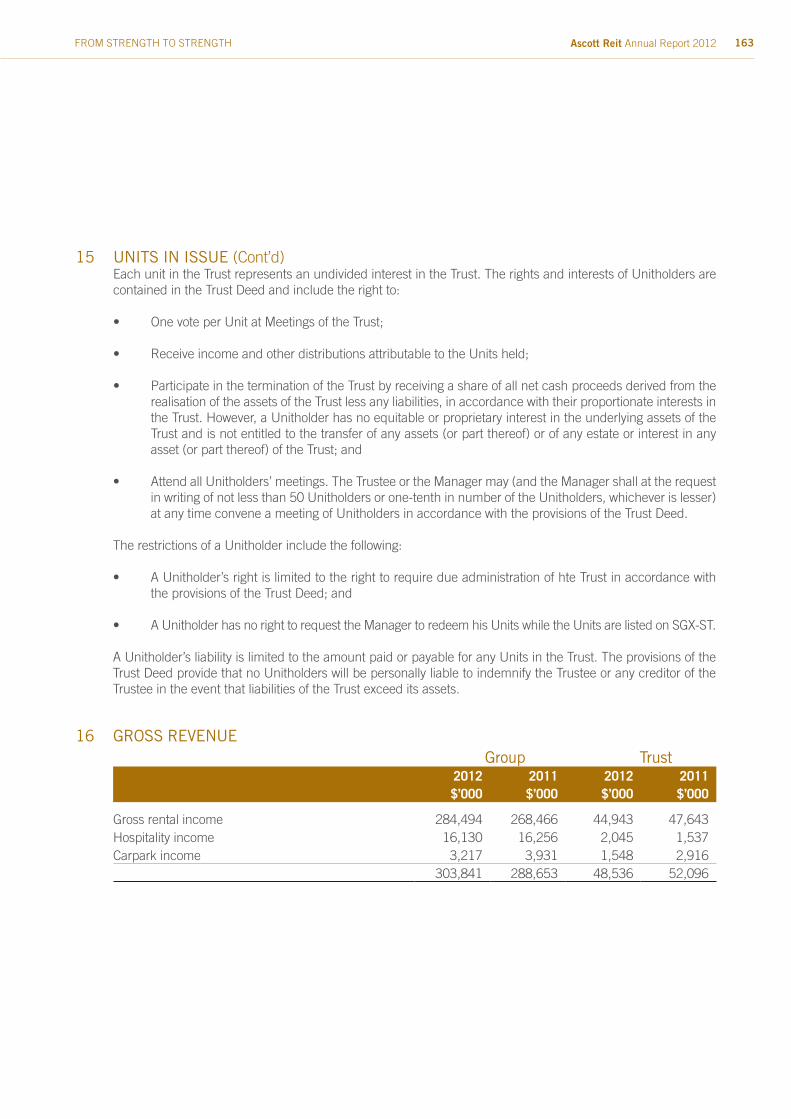

FY 2012 ended on a high note for Ascott Reit. The Group’s total revenue for the year reached S$303.8 million while gross profit was S$159.1 million, representing a year-on-year growth of 5% and 1% respectively. Bolstered by a quality portfolio, proactive acquisition, asset management and enhancement strategies, the Group’s distribution to Unitholders for FY 2012 rose 4% to S$99.7 million over the previous year. Distribution Per Unit (DPU) grew by 3% from 8.53 cents to 8.76 cents. The portfolio’s average occupancy for FY 2012 was 80%, a slight increase of 1% over FY 2011, while Revenue Per Available Unit (RevPAU) also rose by 1% from S$143 to S$145. Ascott Reit’s unit price rose 37% in FY 2012 and closed at S$1.36 on 31 December 2012. The DPU for FY 2012 represents a 6.4% yield.

Striking a Balance Between Stability and Growth

With 27 properties in Europe and 41 properties in the Pan-Asian region, the Group’s geographical diversity has ensured greater stability across different economic cycles. All the 27 properties in Europe, and three properties in the Pan-Asian region are supported by master leases and serviced residence management contracts that provide a minimum guaranteed income, which contributed to 44% of the Group’s total gross profit. With their weighted average remaining tenure of about six years, Unitholders will continue to enjoy enhanced income stability over a longer period of time.

Capturing Market Opportunities for Better Returns

Our earnings base was also broadened through yield-accretive acquisitions and matured property divestments. During the year, Ascott Reit divested Somerset Grand Cairnhill Singapore for S$359 million at a 3.8% implied exit EBITDA yield to CapitaLand for redevelopment into a new serviced residence (new Cairnhill serviced residence) and residential development; recognizing a gross divestment gain of S$87.1 million. Proceeds from the divestment were

immediately reinvested in higher yielding properties, namely Ascott Raffles Place Singapore for S$220 million and Ascott Guangzhou for $63.5 million. We have also entered into a fixed price contract of S$405 million to acquire the new Cairnhill serviced residence with expected delivery in 2017. These transactions were recommended by the Audit Committee for Unitholders’ approval as the divestment and acquisitions constituted Interested Party Transactions. We are pleased that extremely strong support with almost unanimous approval from Unitholders was obtained at the Extraordinary General Meeting held on 27 July 2012.

The Group continued to seize market opportunities to optimise returns by pursuing acquisitions, not only from our Sponsor, but from third party owners as well. These included Citadines Karasuma-Gojo Kyoto and Madison Hamburg which were acquired for S$18.3 million and S$59.4 million respectively. In the latter case, we continued to allow the third party to manage our property. At the same time, we unlocked the underlying value of assets that have reached optimal growth as in the case of Somerset Gordon Heights Melbourne in Australia, which was divested at S$15.3 million for a gain of S$0.6 million.

Ascott Reit has come a long way since its initial public offering in 2006. From its initial asset size of S$856 million, the Group’s portfolio has more than tripled in value to S$3.2 billion today. In 2006, Ascott Reit’s initial portfolio comprised 2,068 apartment units, in 12 properties across 7 cities and 5 countries. As at 31 December 2012, Ascott Reit’s portfolio comprises 7,427 apartment units in 68 properties across 25 cities and 12 countries.

Practical Aspirations Leading to Inspiring Results

The Group strengthens Unitholders’ returns by focussing on active asset enhancements to maximise the financial performance of our property portfolio. To command better room rate premiums, we stay relevant to the increasingly sophisticated needs of modern travellers by updating the look and feel of our properties in order to improve overall customer experience.Citadines Prestige Trafalgar Square London, for example, recorded the strongest Average Daily Rates

Ascott Reit Annual Report 20128 FROM STRENGTH TO STRENGTH

LIM JIT POHChairman

Independent Non-Executive Director

TAY BOON HWEE, RONALDChief Executive Officer and

Executive Director

Ascott Reit Annual Report 2012 9FROM STRENGTH TO STRENGTH

LETTER TO UNITHOLDERS

(ADR) since acquisition in 2010 upon completion of refurbishment works of the 187 apartment units in 2012. In Belgium, the 169-unit Citadines Sainte-Catherine Brussels reported higher ADR in Euro terms after the first phase of renovation in February. The second phase was completed in the fourth quarter of 2012. Separately, Somerset Olympic Tower Property Tianjin has been commanding higher rental rates following the completion of renovation of all the 185 apartment units at the end of 2011. In Vietnam, a lobby enhancement initiative in July 2012, following the renovation of all the 185 apartment units at Somerset Grand Hanoi, has improved guest arrival experiences. Overall, rental rates of the above properties have increased by as much as 50% post renovations.

In Indonesia, the refurbishment of the 198-unit Ascott Jakarta, which commenced in July 2012, is scheduled to complete by the fourth quarter of 2013. The renovation of the 154-unit Citadines Toison d’Or Brussels is due for completion in the first quarter of 2014.

To enhance overall brand value and asset yield across Europe, asset enhancements were also carried out by Ascott, our Sponsor cum master lessee in five of our properties across France. Citadines Suites Lourve Paris commenced renovation in July 2012 and will re-open in the first quarter of 2013. This was followed by the phase-two renovation of Citadines City Centre Grenoble, which was completed in the fourth quarter of 2012. Citadines Croisette Cannes underwent refurbishment in October 2012 and completion is expected in the first quarter of 2013. Similarly, the refurbishment of 49 units out of the 101-unit Citadines City Centre Lille in December will be completed in the first quarter of 2013. We also expect enhancement works at Citadines Place d’Italie Paris, which commenced in November 2012, to be completed by the first quarter of 2014.

Our award winning properties continue to enjoy worldwide recognition as preferred accommodation for business travellers. Some of the awards include “Best Serviced Residence in Asia-Pacific” for Ascott Raffles Place Singapore (Ranked 1st) and Ascott Jakarta (Ranked 2nd) by Business Traveller Asia-Pacific Awards 2012; “Best Serviced Apartment Company” for all Citadines branded properties in UK (Ranked 2nd); and TripAdvisor Certificate of Excellence for 18 of our properties in key gateway cities including London, Singapore, Paris and Berlin.

Exercising Prudent Capital Management

Our discipline in capital and risk management has supported our growth by ensuring a strong balance sheet and a financial flexibility to seize market opportunities. As a result, we are able to tap into financial markets and acquire yield-accretive properties when opportunities arise.

As at 31 December 2012, Ascott Reit’s gearing of 40.1% is well within the Monetary Authority of Singapore’s Property Fund Appendix’s gearing limit of 60%. Our interest cover ratio remains healthy at 3.9 times and average borrowing cost is 3.3% per annum with 62% of the debts secured at fixed interest rates. In October 2012, Ascott Reit redeemed in full S$50 million 4.11% Fixed Rate Notes under the S$1 billion Multicurrency Medium Term Note Programme.

On 29 January 2013, Ascott Reit successfully raised S$150 million through a private placement exercise of 114.9 million new units at S$1.305 per new unit. The equity placement will allow us to increase our financial capacity to fund potential future acquisitions. This will in return enable us to further grow and enhance Ascott Reit’s portfolio to boost Unitholders’ returns. We remain confident in the markets that we operate in as we continue to grow the business and enhance value for Unitholders.

Supporting Social Causes

Corporate social responsibility remains an integral part of our business. Over the years, the plight of underprivileged children has remained close to our hearts, and we continue to support them through their subsistence and educational needs. Across our properties, we encourage sustainable and environmentally friendly practices such as water and electricity conservation, waste reduction and recycling efforts by staff and guests alike.

From Then to Now, and Beyond

Global economic outlook is cautious in the year ahead and the European economic situation continues to be fragile. Ascott Reit will actively monitor cash flows generated from our European assets and manage currency risks. We will continue to adopt a natural

FROM PROFIT TO RETURNS

Ascott Reit Annual Report 201210 FROM STRENGTH TO STRENGTH

hedge strategy by borrowing in the same currency as the underlying asset. We also aim to maintain a strong balance sheet and financial flexibility. Apart from managing risks in uncertain times, we will continue to drive and optimise returns through yield-accretive acquisitions and asset enhancement initiatives to create greater value for Unitholders. The Group’s income stability remains supported by a strong stable of assets across 25 cities in 12 countries; while its extended-stay business model focussed on corporate travellers, properties on master leases, and serviced residence contracts with minimum guaranteed income, will continue to provide a strong foundation for stability and growth.

Acknowledgement and Board Appointments

With effect from 1 January 2013, Mr Liew Mun Leong resigned as Non-Independent Non-Executive Director, Deputy Chairman of the Board and Chairman of the Executive Committee of the Company following his retirement as President and Chief Executive Officer of CapitaLand Group. Mr Liew had been a Director and Deputy Chairman of the Board since inception. The Group has benefitted immensely from his extensive experience and expertise and would like to express our sincere thanks and appreciation for his significant contributions to Ascott Reit.

On the same day, Mr Lim Ming Yan assumed the position of Deputy Chairman of the Board and Chairman of Executive Committee of the Company upon his promotion to President and Chief Executive Officer of CapitaLand. We wish to congratulate Mr Lim on his new appointment.

Ascott Reit is also pleased to welcome the following two new appointments to the Board on 1 January 2013: Mr Zulkifli Bin Baharudin is appointed as an Independent Non-Executive Director of the Company. Mr Tay Boon Hwee, Ronald, is appointed as an Executive Director of the Company. He continues as its Chief Executive Officer.

With effect from 24 January 2013, Mr Wen Khai Meng has resigned as Non-Independent Non-Executive Director of the Company to focus on his other areas of responsibilities within the CapitaLand Group. We would like to express our thanks and appreciation to him for his valuable contributions to Ascott Reit.

To our serviced residence guests, Unitholders and business partners, we thank you for your continued support. To our staff and Board of Directors, our gratitude for yet another year of hard work, dedication and results.

Lim Jit PohChairman

Tay Boon Hwee, RonaldChief Executive Officer

26 February 2013

Ascott Reit Annual Report 2012 11FROM STRENGTH TO STRENGTH

致单位持有人

尊敬的单位持有人,

发展不断壮大

2012 财年,雅诗阁公寓信托 (Ascott Reit) 取得骄人的业绩。集团总营业收入达 3 亿零 380 万新元,毛利润则达 1 亿 5910 万新元,分别实现 5% 和 1% 的年比增长。受益于高质量的资产组合,积极的收购、资产管理和物业提升策略,集团可派发分红较上一年增长了 4%,达 9970 万新元。每单位可派发红利从 8.53 分,上涨 3% 至 8.76 分。物业平均入住率达 80%,较前一年略微增长 1%。每间可供出租公寓单位收入也从 143 新元增长 1%,达 145 新元。雅诗阁公寓信托的单位价格全年增长了 37%,年尾闭市收于 1.36 新 元,收益率为 6.4%。

在稳定和增长中取得平衡 集团拥有 27 个欧洲物业和 41 个泛亚洲区域物业,多元化地区布局确保集团能稳定地渡过不同的经济周期。雅诗阁公寓信托在欧洲的 27 间物业和泛亚洲区的 3 间物业为主租约 (master lease) 出租或拥有最低收入保证的管理合约。2012 财年,这些合约收入占集团总毛利的 44%。这些物业的平均剩余租期约 6 年,单位持有人将在较长一段时间持续享有非常稳定的收入。

捕捉市场契机,争取更高回报 通过收购能增进收益率的资产和脱售成熟资产,我们扩大了收入来源。在 2012 年,雅诗阁公寓信托以 3 亿 5900 万新元,相等于 3.8% 的收益率,向凯德集团出售了 Somerset Grand Cairnhill Singapore,实现了 8710 万新元的脱售收益。凯德集团计划将其建成一个全新的服务公寓 (new Cairnhill serviced residence) 及住宅项目。我们将脱售所得投资于更高收益的资产,分别以 2 亿 2000 万新元收购 Ascott Raffles Place Singapore, 以及以 6350 万元收购 Ascott Guangzhou。我们也以 4 亿零 500 万新元的固定价格收购预期在 2017 年建成的 new Cairnhill serviced residence。由于上述买卖交易属于利害关系人交易,因此需在审计委员会推荐下获单位持有人批准。我们很高兴于 2012 年 7 月 27 日召开的临时股东大会上,获得单位持有人的强力支持,取得几乎全体通过的结果。 我们不仅向保荐机构雅诗阁有限公司 (The Ascott Limited) 购买资产,也继续把握市场契机从第三方业主收购资产, 来优化收益,包括以 1830 万新元收购 Citadines Karasuma-Gojo Kyoto, 以及以 5940 万新元收购 Madison Hamburg。我们还允许第三方业主继续经营 Madison Hamburg。此外,我们也以 1530 万新元脱售 Somerset Gordon Heights Melbourne, 从中获益 60 万新元。

雅诗阁公寓信托自 2006 年上市以来取得长足的发展和进步。集团的资产从 8 亿 5600 万新元的初始规模,增长 三倍多,达 32 亿新元。从 2006 年的 5 个国家,7 个城市,12 个物业,共 2068 间公寓单位,到 2012 年年底,雅诗阁公寓信托的足迹已扩展至12个国家的 25 个城市, 拥有 68 个物业,共 7427 间公寓单位。

经营实际目标,收获骄人成绩

集团通过专注于积极的资产优化来最大限度地提高物业的 业绩,以增加单位持有人的收益。为争取更高的日均房价,我们不断提升物业的外观和质感,改善客户体验,以满足现代旅客越来越多样化的需求。

Citadines Prestige Trafalgar Square London 为例,这家 187 间单位的物业在 2012 年完成翻新工程后,取得自收购以来最高的日均房价。在比利时,拥有 169 间单位的 Citadines Sainte-Catherine Brussels 于 2 月份完成第一期翻新工程后也取得更高的日均房价。其第二期翻新工程已在 2012 年第四季度完工。此外,拥有 185 间单位的 Somerset Olympic Tower Tianjin 在 2011 年底完成翻新工程后,也取得了更高房价。在越南, Somerset Grand Hanoi 的 185 间单位翻新工程和 2012 年 7 月进行的大堂翻新计划,大大提升了到访客人的入住体验。总而言之,以上翻新后的物业房价都取得极大增长,最高达 50%。

在印度尼西亚,拥有 198 间单位的 Ascott Jakarta 在 2012 年 7 月开始翻新工程,预计在 2013 年第四季度完工。拥有 154 间单位的 Citadines Toison d’Or Brussels 的翻新工程预计在2014年第一季度竣工。

为加强我们在欧洲的品牌价值和资产收益,身为我们的保荐机构和法国五个资产的主要承租人,雅诗阁有限公司也对资产进行了优化。Citadines Suites Louvre Paris 于 2012 年 7 月展开翻新工程,预计在2013年第一季度重新开业。Citadines City Centre Grenoble 的第二期翻新工程已在 2012 年第四季度完工。同时,在十月开始翻新的 Citadines Croisette Cannes 与十二月开始翻新的 Citadines City Centre Lille (101 间其中 49 间单位)预计于 2013 年第一季度完成。我们也预计于 2012 年 11 月启动翻新的 Citadines Place d’Italie Paris 将在 2014 年第一季度竣工。

我们的物业继续获全球认可,为商务旅客的住宿首选。我们获得的奖项包括 2012 年商旅亚太评选的“亚太区最佳服务公寓”(第一名: Ascott Raffles Place Singapore; 第二名: Ascott Jakarta), 以及“最佳服务公寓公司”(第二名:英国的所有馨乐庭物业)。全球最大旅游网站 TripAdvisor 也给我们位于主要枢纽城市,包括伦敦、新加坡、巴黎和柏林的 18 个物业颁发年度卓越奖 (Certificate of Excellence)。

从物业收益到投资回报

Ascott Reit Annual Report 201212 FROM STRENGTH TO STRENGTH

谨慎的资金管理 谨慎的资金和风险管理支持了我们的增长,确保我们拥有强劲的资产负债表和灵活的融资能力以把握市场契机。正因为如此,我们才能把握机会,通过金融市场融资,收购能增加收益的物业。

截至 2012 年 12 月 31 日,雅诗阁公寓信托的负债与资产值比率为 40.1%, 低于新加坡金融管理局房地产基金指导原则下所规定的 60% 顶限。我们的利息覆盖率也保持在健康的 3.9 倍,平均贷款成本为 3.3% 年利率,其中有 62% 是固定利率贷款。2012 年 10 月,雅诗阁公寓信托完全兑现了 10 亿新元的多货币中期票据计划中的 5000 万新元的 4.11% 固定收益票据。

2013 年 1 月 29 日,雅诗阁公寓信托以每新单位 1.305 新元的价格发行了 1 亿 1490 万个新单位,成功筹集了 1 亿 5000 万新元。这项私募行动加强了我们的财务承受能力,以把握未来市场契机,购买有潜力的资产。这让我们能继续扩张和发展,从而增加单位持有人的收益。我们对目前的业务和市场深具信心,将继续稳健的发展,为单位持有人创造更大的价值。

取诸社会,用诸社会

企业社会责任一直是我们业务中的关键部分。多年来,我们关注弱势孩童的成长,并且将继续资助他们的生活和教育需要。此外,我们也鼓励旗下物业的员工和住户实践可持续发展及环保的生活方式,包括水电节能、减少浪费和再循环等。

从过去到现在,以至未来

未来一年,我们对全球经济展望持谨慎态度,欧洲经济形势仍然脆弱。雅诗阁公寓信托将积极监管欧洲资产的流动资金,以及管理货币风险。我们也将继续采取一个自然对冲政策,为关联资产进行同货币贷款。我们的目标是保持强劲的资产负债表和灵活的融资能力。除了在市场不稳定时期管理风险,我们也将继续通过增进收益率的收购和资产优化计划,增加和优化收益,为单位持有人创造更大价值。12 个国家 25 个城市的资产运营强有力的支持集团的收入稳定。而针对商务客的长住商业模式、以主租约的模式出租物业,以及拥有最低收入保证的服务公寓合约,这三个主轴将继续为集团的稳定和发展提供扎实的基础。

致谢与董事会任命

原凯德集团总裁兼首席执行官廖文良先生在荣休后,辞去了雅诗阁公寓信托的非独立非执行董事、董事局副主席和公司常务委员主席的职务,于 2013 年 1 月 1 日生效。廖文良先生自雅诗阁公寓信托创办以来担任董事兼董事局副主席的职务。他的丰富经验和专长让集团受益匪浅。在此我们献上最诚挚的谢意,感谢他对雅诗阁公寓信托所作出的显著贡献。

在同一天,林明彦先生接任凯德集团总裁兼首席执行官的职务,也接任雅诗阁公寓信托董事局的副主席和公司常务委员主席。我们在此祝贺林明彦先生的擢升。

2013 年 1 月 1 日,雅诗阁公寓信托欢迎两名新董事局成员的加入。Zulkifli Bin Baharudin 先生受委为公司独立非执行董事。我们的首席执行官郑文辉先生受委为公司执行董事。

2013 年 1 月 24 日,温启明先生辞去了公司非独立非执行董事的职务,以专注于凯德集团的其他职责上。我们感谢温先生对雅诗阁公寓信托所作出的贡献。

借此,我们由衷感谢我们的住户、单位持有人和商业伙伴对我们长久以来的支持,同时对各位员工和董事局成员的辛勤付出、贡献以及所取得的成绩,表达诚挚的谢意。

Lim Jit Poh林日波主席

Tay Boon Hwee, Ronald郑文辉总裁

2013 年 2 月 26 日

Ascott Reit Annual Report 2012 13FROM STRENGTH TO STRENGTH

2008 2009 2010 2011 2012

Gross Revenue S$192.4m S$175.5m S$207.2m S$288.7m S$303.8m

Gross Profit S$95.5m S$84.6m S$101.3m S$157.5m S$159.1m

Unitholders’ Distribution S$53.7m S$45.2m S$57.7m S$96.2m S$99.7m

Distribution Per Unit (DPU) 8.78¢ 7.32¢ 7.54¢ 8.53¢ 8.76¢

Distribution Yield1 15.14% 6.10% 6.18% 8.62% 6.4%

Balance Sheet as at 31 December

Total Assets S$1,687.6m S$1,652.0m S$2,803.8m S$3,023.0m S$3,002.5m

Unitholders’ Funds S$899.0m S$825.1m S$1,417.5m S$1,537.0m S$1,547.4m

Total Borrowings S$624.4m S$651.1m S$1,099.5m S$1,204.6m S$1,170.8m

Financial Ratios as at 31 December

Net Asset Value (NAV) Per Unit S$1.47 S$1.34 S$1.28 S$1.36 S$1.35

Aggrerate Leverage 38.3% 41.2% 40.3% 40.8% 40.1%

Interest Cover Ratio2 4.5 times 3.5 times 3.7 times 3.8 times 3.9 times

Management Expense Ratio3 1.3% 1.3% 1.0% 1.3% 1.1%

Derivative Financial Liabilities as a Percentage of NAV4

1.7% 2.3% 0.8% 1.2% 1.3%

Others as at 31 December

Market Capitalisation1 S$354.3m S$740.7m S$1,351.6m S$1,118.6m S$1,554.2m

Number of Units in Issue 610.8m 617.2m 1,107.9m 1,129.9m 1,142.8m

1. Based on the closing unit price of S$0.58 on 31 December 2008, S$1.20 on 31 December 2009, S$1.22 on 31 December 2010, S$0.99 on 31 December 2011 and S$1.36 on 31 December 2012.

2. Refers to EBITDA (earnings before net interest expense, tax, depreciation and amortisation) before changes in fair value of financial derivatives and serviced residence properties, and unrealised foreign exchange differences over net interest expense.

3. Refers to the expenses of Ascott Residence Trust (excluding direct expenses, unrealised foreign exchange differences, net interest expense, change in fair value of financial derivatives and serviced residence properties, assets written off and income tax expense).

4. Derivative financial liabilities refer to the interest rate swaps and interest rate caps which the Group has entered into.

FINANCIAL HIGHLIGHTS

Ascott Reit Annual Report 201214 FROM STRENGTH TO STRENGTH

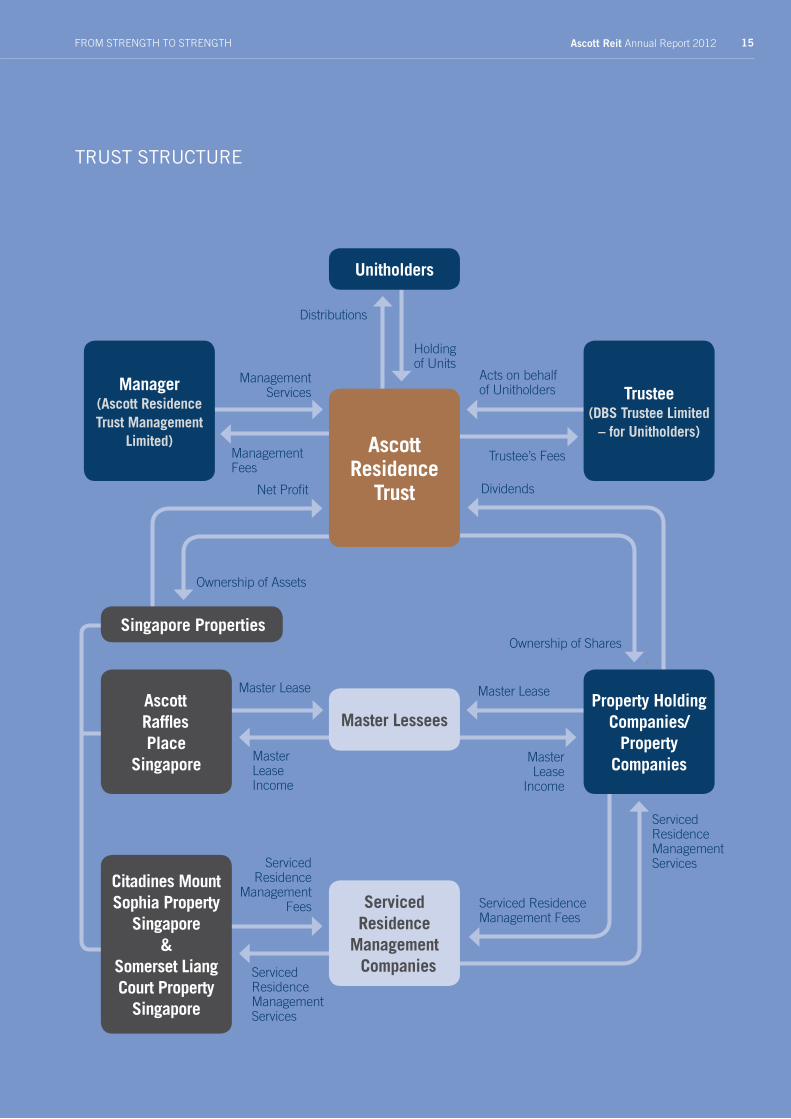

Distributions

Management Services

Management Fees

Net Profit Dividends

Ownership of Assets

Ownership of Shares

Holding of Units

Acts on behalf of Unitholders

Trustee’s Fees

Master LeaseMaster Lease

Serviced Residence

Management Fees

Serviced Residence Management Services

Serviced Residence Management Fees

Master Lease

Income

Master Lease Income

Serviced Residence Management Services

Unitholders

Ascott Residence

Trust

Manager (Ascott Residence Trust Management

Limited)

Trustee (DBS Trustee Limited

– for Unitholders)

Property Holding Companies/

Property Companies

Ascott Raffles Place

Singapore

Citadines Mount Sophia Property

Singapore&

Somerset Liang Court Property

Singapore

Master Lessees

Serviced Residence

Management Companies

Singapore Properties

TRUST STRUCTURE

Ascott Reit Annual Report 2012 15FROM STRENGTH TO STRENGTH

BOARD OF DIRECTORS

LIM JIT POH, 73CHAIRMAN INDEPENDENT NON-EXECUTIVE DIRECTOR

BACHELOR OF SCIENCE IN PHYSICS (HONOURS), UNIVERSITY OF SINGAPORE

MASTER OF EDUCATION, UNIVERSITY OF OREGON, USA

Date of first appointment as a director and Chairman 20 January 2006Length of service as a director (as at 31 December 2012) 6 years 11 months

Board committee(s) served on• Corporate Disclosure Committee (Chairman)

Present Directorships in other listed companies • ComfortDelGro Corporation Limited (Chairman)

• SBS Transit Ltd (Chairman)

• VICOM Ltd (Chairman)

Present Principal Commitments (other than Directorships in listed companies)• ComfortDelGro Corporation Limited (Group Chairman)

• Maybank Kim Eng Holdings Limited (Director)

• Surbana Corporation Pte. Ltd. (Chairman)

Directorships in other listed companies held over the preceding three years• Eng Kong Holdings Limited

Background and Working Experience• Independent Non-Executive Director of The Ascott

Group Limited (1999 to 2008)

Award(s)• Distinguished Science Alumni Award 2006 from the

National University of Singapore• National Trades Union Congress - Distinguished Service Award in 2000 - Meritorious Service Award in 1990 - Friend of Labour Award in 1986• Government of Singapore - Public Administration

Medal in 1972

LIM MING YAN, 50DEPUTY CHAIRMAN NON-INDEPENDENT NON-EXECUTIVE DIRECTOR

BACHELOR OF SCIENCE (MECHANICAL ENGINEERING AND ECONOMICS) (FIRST CLASS HONOURS), UNIVERSITY OF BIRMINGHAM, UK

Date of first appointment as a director 23 July 2009Date of appointment as Deputy Chairman 1 January 2013Length of service as a director (as at 31 December 2012) 3 years 5 months

Board committee(s) served on• Executive Committee (Chairman)

Present Directorships in other listed companies • CapitaCommercial Trust Management Limited

(manager of CapitaCommercial Trust) (Deputy Chairman)

• CapitaLand Limited• CapitaMall Trust Management Limited

(manager of CapitaMall Trust) (Deputy Chairman)

• CapitaMalls Asia Limited• CapitaRetail China Trust Management Limited

(manager of CapitaRetail China Trust) (Deputy Chairman)

• Central China Real Estate Limited

Present Principal Commitments (other than Directorships in listed companies)• CapitaLand Limited (President & Group Chief Executive Officer)

• Business China (Director)

• CapitaLand China Holdings Pte Ltd (Chairman)

• CapitaLand Hope Foundation (Director)

• CapitaLand Malaysia Pte. Ltd. (Chairman)

• CapitaLand Singapore Limited (formerly known as CapitaLand Commercial Limited prior to 15 March 2013) (Chairman)

• CTM Property Trust, Steering Committee (Chairman)

• LFIE Holding Limited (Co-Chairman)

• Shanghai YiDian Holding (Group) Company (Director)

• The Ascott Limited (Chairman)

Ascott Reit Annual Report 201216 FROM STRENGTH TO STRENGTH

Directorships in other listed companies held over the preceding three years• Lai Fung Holdings Limited

Background and Working Experience• Chief Operating Officer of CapitaLand Limited

(May 2011 to December 2012)

• Chief Executive Officer of The Ascott Limited (July 2009 to February 2012)

• Chief Executive Officer of CapitaLand China Holdings Pte Ltd (July 2000 to June 2009)

Award(s)• Outstanding CEO (Overseas) in the Singapore Business

Awards 2006• Magnolia Award, Shanghai Municipal Government in

2003 and 2005

TAY BOON HWEE, RONALD, 44CHIEF EXECUTIVE OFFICEREXECUTIVE DIRECTOR

BACHELOR OF BUSINESS (HONOURS), NANYANG TECHNOLOGICAL UNIVERSITY

Date of first appointment as a director 1 January 2013

Board committee(s) served on• Corporate Disclosure Committee (Member)

• Executive Committee (Member)

Present Principal Commitments (other than Directorships in listed companies)• Ascott Residence Trust Management Limited

(manager of Ascott Residence Trust) (Chief Executive Officer)

Background and Working Experience• Chief Investment Officer and Managing Director of

India and GCC sector of The Ascott Limited (January 2007 to February 2012)

• Head of Business Development and Asset Management of Ascott Residence Trust Management Limited (manager of Ascott Residence Trust) (January 2007 to February 2012)

• Head and Senior Vice President, Investment of CapitaLand Residential Limited (July 2001 to December 2006)

Ascott Reit Annual Report 2012 17FROM STRENGTH TO STRENGTH

BOARD OF DIRECTORS

KU MOON LUN, 62INDEPENDENT NON-EXECUTIVE DIRECTOR

GRADUATED FROM THE HONG KONG TECHNICAL COLLEGE (NOW KNOWN AS THE HONG KONG POLYTECHNIC UNIVERSITY)

REGISTERED PROFESSIONAL SURVEYOR

Date of first appointment as a director 20 January 2006Length of service as a director (as at 31 December 2012) 6 years 11 months

Board committee(s) served on• Audit Committee (Chairman)

Present Directorships in other listed companies• Kerry Properties Limited• Lai Fung Holdings Limited

Present Principal Commitments (other than Directorships in listed companies)• Hospital Governing Committee of Tuen Mun

Hospital, Hong Kong Hospital Authority (Member)

Background and Working Experience• Executive Director of Davis Langdon and Seah

International (1995 to 2005)

• Chairman of Davis Langdon and Seah Hong Kong Limited (1995 to 2004)

• Chairman of icFox International (2000 to 2003)

• Chairman of Premas Hong Kong Limited (2000 to 2002)

• Hong Kong Institute of Surveyors (Fellow Member)

S. CHANDRA DAS, 73INDEPENDENT NON-EXECUTIVE DIRECTOR

BACHELOR OF ARTS (HONOURS), UNIVERSITY OF SINGAPORE

Date of first appointment as a director 20 January 2006Length of service as a director (as at 31 December 2012) 6 years 11 months

Board committee(s) served on• Audit Committee (Member)

Present Directorships in other listed companies• Super Group Ltd• Yeo Hiap Seng Ltd (Deputy Chairman)

• Yeo Hiap Seng (Malaysia) Berhad

Present Principal Commitments (other than Directorships in listed companies)• NUR Investment & Trading Pte Ltd (Managing Director)

• Alliance Select Foods International Inc (Director)

• Goodhope Asia Holdings Ltd (Chariman)

• Nanyang Technological University (Pro-Chancellor)

• Non-Resident Ambassador to Turkey• Tamil Murasu Limited (Chairman)

• YHS (Singapore) Pte Ltd (Chairman)

Directorships in other listed companies held over the preceding three years• CapitaMall Trust Management Limited (manager of

CapitaMall Trust)• Nera Telecommunications Ltd• S i2i Limited• Sincere Watch Limited

Ascott Reit Annual Report 201218 FROM STRENGTH TO STRENGTH

Background and Working Experience• Independent Non-Executive Director of The Ascott

Group Limited (1999 to 2008)

• Chairman of NTUC Fairprice Co-operative Ltd (1993 to 2005)

Award(s)• Distinguished Service (Star) Award by National

Trades Union Congress in 2005• President’s Medal by the Singapore Australian

Business Council in 2000

GIAM CHIN TOON @ JEREMY GIAM, 70INDEPENDENT NON-EXECUTIVE DIRECTOR

BACHELOR OF LAW (HONOURS), UNIVERSITY OF SINGAPORE

MASTERS OF LAW, UNIVERSITY OF SINGAPORE

ADVOCATE & SOLICITOR

Date of first appointment as a director 23 March 2007Length of service as a director (as at 31 December 2012) 5 years 9 months

Board committee(s) served on• Audit Committee (Member)

Present Directorships in other listed companies• Mewah International Inc.

Present Principal Commitments (other than Directorships in listed companies)• Wee Swee Teow & Co (Senior Partner)

• Inland Revenue Authority of Singapore (Member)

• Non-Resident Ambassador to Peru • Non-Resident High Commissioner to Ghana • Singapore Mediation Centre (Director)

Directorships in other listed companies held over the preceding three years• Guthrie GTS Ltd

Background and Working Experience• Senior Counsel (1997)

• President of the Law Society of Singapore (1987 to 1989)

• Magistrate of the Subordinate Courts of Singapore (1967 to 1970)

Award(s)• PBM, Public Service Medal Award in 2012

Ascott Reit Annual Report 2012 19FROM STRENGTH TO STRENGTH

BOARD OF DIRECTORS

ZULKIFLI BIN BAHARUDIN, 53INDEPENDENT NON-EXECUTIVE DIRECTOR

BACHELOR OF SCIENCE IN ESTATE MANAGEMENT, NATIONAL UNIVERSITY OF SINGAPORE

Date of first appointment as a director 1 January 2013

Board committee(s) served on• Corporate Disclosure Committee (Member)

Present Directorships in other listed companies• Hup Soon Global Corporation Limited• Singapore Post Limited

Present Principal Commitments (other than Directorships in listed companies)• ITL Corporation (Chairman)

• Global Business Integrators Pte. Ltd. (Managing Director)

• Ang Mo Kio - Thye Hua Kwan Hospital Ltd. (Director)

• Civil Aviation Authority of Singapore (Authority Member)

• Mentor Media Ltd (Director)

• Non-Resident Ambassador to the People’s Democratic Republic of Algeria

• Non-Resident Ambassador to the Republic of Uzbekistan

• Singapore Management University (Director – Board of Trustees)

• Thye Hua Kwan Moral Charities Limited (Director)

Background and Working Experience• Nominated Member of Parliament

(October 1997 to September 2001)

Award(s)• BBM, Public Service Star Award in 2011• Public Service Award (Meritorious) in 2005

JENNIE CHUA, 68NON-INDEPENDENT NON-EXECUTIVE DIRECTOR

BACHELOR OF SCIENCE, CORNELL UNIVERSITY, NEW YORK, USA

Date of first appointment as a director 2 July 2007Length of service as a director (as at 31 December 2012) 5 years 6 months

Present Directorships in other listed companies• CapitaMalls Asia Limited• GuocoLeisure Limited

Present Principal Commitments (other than Directorships in listed companies)• Alexandra Health Pte Ltd (Chairperson)

• CapitaLand Hope Foundation (Director)

• Community Chest of Singapore (Chairperson)

• Governing Council of the Institute of Service Excellence (Co-Chairperson)

• ISS A/S & ISS World Services A/S (Director)

• MOH Holdings Pte Ltd (Director)

• Nanyang Technological University (Director/Trustee)

• Non-Resident Ambassador to The Slovak Republic• Prime Minister’s Office (Justice of Peace)

• Sentosa Cove Pte Ltd (Chairperson)

• Sentosa Development Corporation (Board Member)

• Singapore Film Commission (Chairperson)

• Singapore Government (Member of Pro-Enterprise Panel)

• Singapore International Chamber of Commerce (Board Member)

• Temasek Foundation CLG Limited (Deputy Chairperson)

• The Old Parliament House Limited (Chairperson)

• The Singapore Chinese Girls’ School (Board Member)

Ascott Reit Annual Report 201220 FROM STRENGTH TO STRENGTH

Background and Working Experience• Chief Corporate Officer of CapitaLand Limited

(July 2009 to July 2012)

• Chief Executive Officer of The Ascott Group Limited (August 2007 to June 2009)

• Chief Strategic Relations Officer of CapitaLand Limited (February 2007 to July 2007)

• President & Chief Executive Officer of Raffles Holdings Limited (April 2003 to January 2007)

• Chairman of Raffles International Ltd (October 2004 to September 2007)

• Chairman & Chief Executive Officer of Raffles International Ltd (April 2003 to September 2004)

• President & Chief Operating Officer of Raffles International Ltd (1999 to March 2003)

Award(s)• Three Singapore National Day Awards

(1984, 2004 & 2008)• Outstanding Contribution to Tourism Award 2006• Women’s World Excellence Awards 2006• Travel Personality of the Year Award 2005• National Trades Union Congress (NTUC) Medal of

Commendation 2005• Bloomberg Business Week Magazine 25 Stars of Asia

Award 2003• Person of the Year – Asia Pacific (Hotel) 2002• National Productivity Award 2002• Pacific Area Travel Writers Association Hall of Fame

2000• Hotelier of the Year 1999• Woman of the Year 1999• Champion of the Arts 1999• Independent Hotelier of the World 1997

CHONG KEE HIONG, 46NON-INDEPENDENT NON-EXECUTIVE DIRECTOR

BACHELOR OF ACCOUNTANCY, NATIONAL UNIVERSITY OF SINGAPORE

CERTIFIED PUBLIC ACCOUNTANT

Date of first appointment as a director 15 March 2010Length of service as a director (as at 31 December 2012) 2 years 9 months

Board committee(s) served on• Corporate Disclosure Committee (Member)

• Executive Committee (Member)

Present Principal Commitments (other than Directorships in listed companies)• The Ascott Limited (Chief Executive Officer & Director)

• Ascott International Management (2001) Pte Ltd (Director)

• Ascott Serviced Residence (China) Fund (Chairman)

• The Ascott Capital Pte Ltd (Director)

Background and Working Experience• Chief Executive Officer of Ascott Residence Trust

Management Limited (manager of Ascott Residence Trust) (November 2005 to January 2012)

• Deputy Chief Executive Officer, Finance & Investment, The Ascott Limited (September 2004 to March 2010)

• Chief Financial Officer of Raffles Holdings Limited (May 2001 to August 2004)

• Member of Institute of Certified Public Accountants of Singapore

• Completed Harvard Business School’s Advanced Management Program in 2008

Ascott Reit Annual Report 2012 21FROM STRENGTH TO STRENGTH

THE MANAGER

TAY BOON HWEE, RONALDChief Executive Officer and

Executive Director

KANG SIEW FONGVice President, Finance

Mr Tay Boon Hwee, Ronald is the Chief Executive Officer of ARTML. He is responsible for spearheading the overall strategic planning and leading the implementation of the business, investment and operational strategies for Ascott Reit.

Prior to this, Mr Tay was concurrently Chief Investment Officer of Ascott and Head of Business Development and Asset Management of ARTML until February 2012.

Mr Tay has been with the CapitaLand Group for more than 10 years. Prior to joining Ascott, Mr Tay was with CapitaLand Residential Singapore as Senior Vice President (Finance and Investment). Mr Tay began his career in the banking industry, where he spent nine years in various senior positions in corporate and investment banking.

Mr Tay holds a Bachelor of Business (Honours) from the NanyangTechnological University.

Ms Kang Siew Fong heads the finance team and is responsible for financial management and compliance matters for Ascott Reit. Ms Kang has more than 20 years’ experience in the finance profession.

Prior to joining ARTML, Ms Kang was with Ascott for more than 12 years, holding various positions including Vice President, Finance and Vice President, Business Development and Planning.

While at Ascott, Ms Kang was responsible for all aspects of Ascott’s financial management and accounting. She was involved in mergers and acquisitions activities at Ascott, and the formulation and implementation of its financial policies and practices, budgeting and internal controls. She was also a member of the team responsible for the listing of Ascott Reit.

Ms Kang graduated from the National University of Singapore with a Bachelor of Accountancy degree.

Ascott Reit Annual Report 201222 FROM STRENGTH TO STRENGTH

VINCENT WEEDeputy Chief Executive Officer

ELAINE SOHAssistant Vice President, Investor

Relations & Communications

Mr Vincent Wee assists the CEO, Mr Tay Boon Hwee, Ronald, in enhancing Ascott Reit’s portfolio performance, supporting business development activities and strategic capital and risk management for Ascott Reit. He is concurrently Ascott’s Managing Director, India & Gulf Cooperation Council (from 6 February 2012), where he has overall responsibility for the development and operations of Ascott’s business in the region.

Mr Wee has over 19 years of experience in the real estate industry and has been with CapitaLand since 1997. Prior to joining the ARTML in July 2011, he was with Australand Property Group (Australand), the Australian Stock Exchange listed subsidiary of CapitaLand Limited for 10 years where he held various senior executive positions.

Mr Wee holds an MBA from Cranfield School of Management, UK and a Bachelor of Economics from Monash University, Australia.

Ms Elaine Soh heads the Investor Relations function in ARTML and is responsible for conducting effective communication, as well as building and maintaining relations with Unitholders, potential investors and analysts.

Prior to joining ARTML, she was the head of Investor Relations for Indofood Agri Resources Limited. Ms Soh began her career in banking and finance and held various functions from trading to investment banking.

Ms Soh holds a Bachelor of Economics and Finance from Royal Melbourne Institute of Technology.

Ascott Reit Annual Report 2012 23FROM STRENGTH TO STRENGTH

VALUE CREATION

FROM STRATEGY TO OPPORTUNITY

Ascott Reit Annual Report 201224 FROM STRENGTH TO STRENGTH

At Ascott Reit, value creation is the result of active asset management, sustainable growth and prudent capital and risk management strategies. Year after year, we continue to deliver consistent and positive financial results by leveraging the right strategies to seize market opportunities and to optimise the potential of our portfolio.

Ascott Reit Annual Report 2012 25FROM STRENGTH TO STRENGTH

VALUE CREATION

Active Asset Management

Ascott Reit creates value for its stakeholders by maximising the financial yield of its property portfolio and by focussing on the operational performance of each property.

As part of our focussed and profit-oriented approach, we benchmark the operating results of each property against market performance and against its previous year’s results and planned budgets. We also conduct detailed reviews of properties that are not achieving their targets, and work closely with the Serviced Residence Management Companies (SRMCs) to develop action plans to improve the operating performance of each of these properties.

We have in place robust asset management programmes that enable us to actively manage each of our properties to generate organic growth and strengthen existing relationships with key customers. Through the SRMCs, we seek to optimise occupancy levels and average daily rates, and maximise RevPAU.

We closely monitor the growth potential of each property, and divest properties that have reached their maximum potential or whose growth prospects are limited by changes in the operating environment. The proceeds from our divestments are then redeployed into acquiring properties with potential for higher-yielding returns.

DEVELOP YIELD MANAGEMENT AND MARKETING STRATEGIES TO MAXIMISE REVPAU

The profitability of Ascott Reit’s portfolio depends primarily on the maximisation of RevPAU. Therefore, our yield management and marketing strategies are focussed on:

• assessing and adjusting apartment rental rates based on occupancy levels and demand; and

• determining the appropriate balance between higher yielding short-stay guests and stability of revenue from long-stay guests.

We work closely with the SRMCs to establish and develop relationships with global key accounts, and leverage on Ascott’s wider networks to improve Ascott Reit’s revenue and profitability.

Ascott enjoys strong brand equity through a series of marketing initiatives across different platforms. Following the enhancements to the Ascott, Citadines and Somerset brand portals, Ascott has introduced mobile versions of these websites with faster access and smarter navigation through touchscreen-friendly icons and webpages optimised for smaller screens.

Searching for information, viewing promotions, enquiries and making reservations for Ascott’s properties worldwide have never been easier. Guests simply log in to their profiles for quick access, while a GPS-enabled feature recommends the nearest Ascott serviced residence based on user locations. Interactive maps are now available on demand, displaying the attractions and amenities around each serviced residence.

Besides the mobile application, Ascott has launched an online chat facility to provide guests with real-time support. Guests can communicate with an Ascott representative in five languages – English, Mandarin Chinese, French, German and Spanish. These initiatives are part of Ascott’s ongoing efforts to enhance and enrich guests’ experience at different touch-points, including their interactions prior to their stay at Ascott.

The Facebook pages for Ascott The Residence, Citadines Apart’hotel and Somerset Serviced Residence have drawn over 60,000 fans. In addition to that, Ascott has garnered more than 125,000 fans on Weibo – a Chinese microblogging site. Guests can also connect with Ascott through Twitter, YouTube and Flickr to stay updated on the latest news, promotions and opening specials.

Ascott’s Global Distribution System (GDS) chain code “AZ” continues to help travel management companies and travel agents access rates and room availability more efficiently. As the first serviced residence company to offer a “Best Rate Guarantee”, Ascott assures its guests of the lowest publicly available online rate each time a guest makes a booking through Ascott’s website. If a cheaper online rate for the same apartment is found, Ascott will honour its promise and offer 50% off the cheaper rate for the first night of stay, while guests pay the cheaper rate for subsequent nights’ stay under the same booking.

Ascott Reit Annual Report 201226 FROM STRENGTH TO STRENGTH

Ascott also has global promotional partnerships with Citibank in the form of discounts and special benefits for cardholders. Separately, residents who are Asia Miles and Singapore Airlines’ KrisFlyer members can earn mileage for their stays at participating residences.

IMPROVE OPERATING EFFICIENCIES AND ECONOMIES OF SCALE

To minimise direct expenses and increase gross profit margin without compromising our quality of services, Ascott Reit, together with the SRMCs, have identified several areas for cost management. These include: direct marketing to tenants to reduce commission expenses; centralisation of key functions such as finance and procurement for properties located within the same city or region; and bulk purchases by leveraging on Ascott’s global portfolio to achieve economies of scale.

MAINTAIN QUALITY OF PORTFOLIO

We continuously strive to enhance our assets through planned periodic upgrading, refurbishment and reconfiguration in order to achieve a higher level of guest satisfaction, as well as to improve our properties’ performance and competitiveness.

Citadines Place d’Italie Paris

Ascott Reit Annual Report 2012 27FROM STRENGTH TO STRENGTH

Growth by Acquisition

As part of its value creation strategy, Ascott Reit explores investment and acquisition opportunities globally to enhance the quality of its portfolio.

Our primary investment focus is on serviced residences, particularly in countries where we have an established presence. Rental housing is also an integral part of our extended stay accommodation market, particularly in more stable economies.

To expand our portfolio and maintain our geographical diversification across growth markets as well as stable economies, our acquisition strategies are as follows:

ACQUISITION OF ASSETS OWNED WHOLLY OR IN PART BY ASCOTT

Ascott Reit is granted the right of first refusal over the future sale of properties by any Ascott entity that are used or predominantly used as serviced residences or rental housing properties in the Pan-Asian region and Europe.

As our Sponsor, Ascott supports Ascott Reit’s acquisition strategy by acquiring, retaining and enhancing assets with good income and growth potential, with the view of subsequently divesting the assets to Ascott Reit at the appropriate time.

ACQUISITION OF ASCOTT’S PROPERTIES UNDER DEVELOPMENT

A number of Ascott properties are currently under development. Upon completion, they offer a pipeline of potential targets for acquisition by Ascott Reit as serviced residences or rental housing properties.

ACQUISITION OF ASSETS CURRENTLY MANAGED AND/OR LEASED BUT NOT OWNED BY ASCOTT

In addition to managing Ascott Reit’s portfolio, Ascott also operates and/or manages serviced residences and rental housing properties owned by third parties. These assets are complementary to Ascott Reit’s current portfolio. We will leverage on Ascott’s knowledge and relationships with the owners of these properties to acquire these assets should such opportunities become available.

ACQUISITION OF SUITABLE ASSETS FROM THIRD PARTY OWNERS

Ascott Reit also acquires quality, yield-accretive assets from third party owners. Such opportunities arise from:

• divestment of income producing assets by third party owners in need of capital for new business expansion or investments;

• divestment of assets by owners under financial stress; and

• acquisition of well-located but underperforming assets with the potential for rebranding or asset enhancements for higher returns.

Furthermore, we leverage on our strategic relationship with CapitaLand, one of Asia’s largest listed real estate companies, by tapping into their expertise, experience and knowledge in real estate investments to identify potential acquisitions for Ascott Reit.

ACQUISITION CRITERIA

In evaluating acquisition opportunities, Ascott Reit adopts the following criteria:

Yield thresholdsWe acquire properties or make investments with yields that are currently, or have the potential to be, above their cost of capital. Our acquisitions are expected to maintain or enhance returns to Unitholders.

LocationWe assess properties in terms of their micromarket locations as well as their accessibility to major roads, public transportation and proximity to amenities such as entertainment and food and beverage outlets.

Local market characteristicsWe acquire properties in markets with positive macro-economic indicators such as strong economic growth and expanding cross border business investments and trade. Key considerations are the levels of Foreign Direct Investment (FDI), business travel (including intracountry business travel), expatriate population and the resulting demand for serviced residences or rental housing properties.

VALUE CREATION

Ascott Reit Annual Report 201228 FROM STRENGTH TO STRENGTH

Value-creation opportunitiesWe acquire properties with potential for increase in occupancy rates and/or ADR. The potential for value creation through asset enhancement initiatives such as upgrading, refurbishment and reconfiguration is also assessed.

Building and facilities specifications including the operator of the serviced residencesWe acquire properties that comply with approved building specifications and legal and zoning regulations, with due consideration to the size and age of the buildings.

Before a serviced residence or rental housing property is considered for acquisition, the operator must possess a track record in delivering stable cash flow and operations, or demonstrate the potential for achieving stable cash flows.

Ascott Raffles Place Singapore

Ascott Reit Annual Report 2012 29FROM STRENGTH TO STRENGTH

VALUE CREATION

Capital and Risk Management

Ascott Reit optimises its capital structure and cost of capital within the borrowing limits set out in the Property Fund Appendix. A combination of debt and equity is used to fund future acquisitions and asset enhancement projects.

Additionally, we optimise asset yields and provide stable and sustainable Unitholders’ returns while maintaining flexibility for future capital expenditure or yield-accretive acquisitions. Our objectives for capital and risk management are as follows:

MAINTAIN STRONG BALANCE SHEET BY ADOPTING AND MAINTAINING A TARGET GEARING RANGE

We maintain our gearing at a comfortable range, well within the borrowing limits allowed under the Property Fund Appendix. We balance our cost of capital and returns to Unitholders by achieving the right combination of debt and equity.

SECURE DIVERSIFIED FUNDING SOURCES FROM BOTH FINANCIAL INSTITUTIONS AND CAPITAL MARKETS TO SEIZE MARKET OPPORTUNITIES

To finance future acquisitions and refurbishment of properties, we tap into diversified funding sources. This includes bank borrowings and access to debt capital markets through the issuance of bonds and notes.

We also seize opportunities to raise additional equity capital through the issuance of units, if there is an appropriate use for such proceeds.

ADOPT PROACTIVE INTEREST RATE MANAGEMENT STRATEGY

We adopt a proactive interest rate management policy by maintaining a target percentage of fixed versus floating interest rates. We also manage risks associated with changes in interest rates on loan facilities while keeping Ascott Reit’s ongoing cost of debt competitive.

Our interest rate exposure is managed through the use of interest rate swaps, interest rate caps and fixed rate borrowings.

MANAGE EXPOSURE TO FOREIGN EXCHANGE

Due to the geographical diversity of our portfolio, cash flow generated by our assets as well as their capital values are subject to foreign exchange movements.

In managing the currency risks associated with cash flow generated by our assets, we actively monitor foreign exchange rates and enter into hedges, if appropriate.

In managing the currency risks associated with the capital values of the overseas assets, our borrowings are made in the same currency as the underlying asset as a natural hedging strategy, to the extent possible.

PERFORM RIGOROUS CREDIT RISK MANAGEMENT We establish credit limits for customers and monitor their balances on an ongoing basis. For bookings by individuals, payments are usually made upfront and arrears are checked against lease deposits to minimise losses. Corporate bookings are generally given more credit days and we adopt a strict policy of withdrawing credit terms when payments are outstanding to minimize bad debts.

ENSURE SUFFICIENT CASH FLOW TO MINIMISE LIQUIDITY RISK

Our approach to managing liquidity is to ensure, as far as possible, that we have sufficient liquidity to meet our liabilities when they mature, under both normal and stressed conditions.

In addition to credit facilities, we have a $1 billion MTN Programme, which was established in 2009. We have also established a US$2 billion Euro-Medium Term Note Programme in 2011.

PREPARE FOR MARKET UNCERTAINTIES

The objective of market risk management is to manage and control market risk exposures while optimising returns. Market risk is managed through established investment policies and guidelines. These policies and guidelines are reviewed regularly taking into consideration changes in the overall market environment.

Ascott Reit Annual Report 201230 FROM STRENGTH TO STRENGTH

Somerset Xu Hui Shanghai

Ascott Reit Annual Report 2012 31FROM STRENGTH TO STRENGTH

CORPORATE GOVERNANCE

Our Role

Ascott Residence Trust (Ascott Reit) is externally managed by Ascott Residence Trust Management Limited (Manager), an indirect wholly-owned subsidiary of CapitaLand Limited (CL). The Manager is appointed in accordance with the terms of the trust deed entered into by and between DBS Trustee Limited, as trustee of Ascott Reit (the Trustee) and the Manager on 19 January 2006 (as amended) (Trust Deed). The Manager appoints experienced and well-qualified personnel to run its day-to-day operations.

Our primary role as the Manager is to set the strategic direction of Ascott Reit and give recommendations to the Trustee on acquisition, divestment or enhancement of the assets of Ascott Reit in accordance with its stated investment strategy.

As the Manager, we have general powers of management over the assets of Ascott Reit. Our main responsibility is to manage the assets and liabilities of Ascott Reit for the benefit of the Unitholders. We do this with a focus on generating income and, where appropriate, increasing Ascott Reit’s assets over time so as to enhance the returns from the investments, and ultimately the distributions and total return to the Unitholders.

Our other functions and responsibilities as the Manager include:

• Using our best endeavours to carry on and conduct business in a proper and efficient manner and to conduct all transactions with or for Ascott Reit at arm’s length.

• Preparing property plans on an annual basis for review by the Board of Directors of the Manager (Board), including proposals and forecasts on net income, capital expenditure, sales and valuations, explanation of major variances to previous forecasts, written commentary on key issues and relevant assumptions. These plans explain the performance of Ascott Reit’s assets.

• Preparing the accounts of Ascott Reit.• Ensuring compliance with relevant laws and regulations, including the applicable provisions of the Securities and

Futures Act (SFA), the Listing Manual (the Listing Manual) of Singapore Exchange Securities Trading Limited (SGX-ST), the Code on Collective Investment Schemes issued by the Monetary Authority of Singapore (MAS) (including Appendix 6 on property funds thereto (Property Fund Appendix)), and the Trust Deed.

• Attending to all regular communications with the Unitholders.

The Manager can be removed, under certain circumstances outlined in the Trust Deed, by notice in writing given by the Trustee, in favour of a corporation appointed by the Trustee upon the occurrence of certain events, including by a resolution passed by a simple majority of the Unitholders present and voting at a meeting of the Unitholders duly convened and held in accordance with the provision of the Trust Deed.

Our Corporate Governance Culture

We are committed to the highest standard of corporate governance and transparency in our management of Ascott Reit, and operate in keeping with the spirit of the Code of Corporate Governance in the discharge of our responsibilities as the Manager. We believe that strong and effective corporate governance is essential for the success of Ascott Reit and to protect the best interests of the Unitholders.

The current Code of Corporate Governance was revised by MAS in May 2012 and takes effect in respect of annual reports relating to financial years commencing 1 November 2012. Notwithstanding that the 2012 Code of Corporate Governance (2012 Code) is not yet applicable to us, we are taking the progressive step of voluntarily describing our corporate governance policies and practices in 2012, as the Manager, against the principles and guidelines of the 2012 Code, to the extent that we are able to do so.

We have in place clear internal control systems, reporting and responsibility lines, and procedures in line with the current Code of Corporate Governance. The following paragraphs describe our corporate governance policies and practices in 2012 as the Manager, with specific references to the 2012 Code to the extent the 2012 Code is relevant and applicable to real estate investment trusts (REIT).

Ascott Reit Annual Report 201232 FROM STRENGTH TO STRENGTH

(A) BOARD MATTERS

Principle 1: The Board’s Conduct of Affairs

The Board is responsible for the overall management, corporate governance and long-term success of the Manager and Ascott Reit. It provides leadership to the Manager, sets strategic directions and oversees competent management of Ascott Reit. The Board has established a framework for the management team of the Manager (Management), which includes a system of internal controls and a business risk management process. The Board also sets the disclosure and transparency standards for Ascott Reit and ensures that obligations to the Unitholders and other stakeholders are understood and met.

Each Director must act honestly, with due care and diligence, and in the best interests of Ascott Reit. This obligation ties in with the Manager’s prime responsibility in managing the assets and liabilities of Ascott Reit for the benefit of the Unitholders. Decisions are taken objectively in the interests of Ascott Reit. The Manager has adopted guidelines for related party transactions and dealing with conflicts of interests, details of which are set out on pages 43–45 of this Annual Report. The Board meets regularly and as and when warranted by particular circumstances as deemed appropriate by the relevant Directors. Board meetings may also be held by way of teleconference and video conference, in accordance with the Articles of Association of the Manager. Board meetings are scheduled in advance and are held at least on a quarterly basis, inter alia, to review and deliberate on strategic policies, significant acquisitions and disposals, financial performance and budget, and announcements of results. The Board also reviews the risks to the assets of Ascott Reit with a view to safeguarding Unitholders' interest, and acts upon recommendations from both the internal auditors (Internal Auditors) and the external auditing firm appointed for Ascott Reit (External Auditors). Six Board meetings were held in 2012. In addition to the foregoing, in its deliberations, the Board remains fully conscious of the views and concerns of all Ascott Reit's stakeholders, as well as Ascott Reit's wider corporate social and ethical responsibilities.

In the discharge of its functions, the Board is supported by special Board Committees that provide independent oversight of Management, and which also serve to ensure that there are appropriate checks and balances. These Board Committees are the Audit Committee, the Corporate Disclosure Committee and the Executive Committee. Each of these Board Committees operates under delegated authority from the Board, however, the Board retains overall responsibility for any decisions made by the Board Committees. Other Board Committees may be formed as dictated by business imperatives and/or to promote operational efficiency.

Information on the Audit Committee can be found in the section “Audit Committee” on pages 39 and 40 of this Annual Report.

The Corporate Disclosure Committee’s main role in relation to Ascott Reit is to review corporate disclosure issues and announcements made to the SGX-ST and the public, as well as to ensure good corporate governance and the adoption of best practices in providing transparency to the Unitholders, the investing community and other stakeholders of Ascott Reit. It also ensures that the Manager complies with all applicable legal and regulatory disclosure requirements in relation to Ascott Reit and releases information in a timely and appropriate manner.

The Executive Committee has adopted terms of reference to define its scope of authority and responsibilities in relation to Ascott Reit, which include (i) overseeing the day-to-day activities and affairs of the Manager and Ascott Reit for and on behalf of the Board (except in relation to such matters that specifically require action or decision by the Board pursuant to applicable law or regulations); (ii) reviewing, endorsing and recommending to the Board strategic directions and management policies of the Manager in respect of Ascott Reit; (iii) overseeing operational, investment and divestment matters within approved financial limits; and (iv) performing such other functions as authorised or delegated by the Board. Management seeks the guidance and views of the Executive Committee regularly both within and outside the formal environment of Executive Committee meetings. Decisions taken and resolutions passed are circulated to the Board for information. The Board has adopted a set of internal controls which specifies approval requirements for, inter alia, capital expenditure, new investments and divestments, and borrowings. Apart from matters that specifically require the Board’s approval, such as the issue of units in Ascott Reit (Units) and any distributions and other returns to the Unitholders, the Board has also set approval limits and thresholds for transactions, and has authorised the Executive Committee

Ascott Reit Annual Report 2012 33FROM STRENGTH TO STRENGTH

CORPORATE GOVERNANCE

to approve transactions which fall below the specified limits and thresholds; transactions in excess of said limits and thresholds remain subject to approval by the Board. Appropriate delegation of authority and approval sub-limits is also provided at the management level to facilitate operational efficiency.

Information on the meeting attendance are set out on page 37 of this Annual Report.

The Board takes the induction, orientation and training of new Directors seriously. Newly-appointed Directors are given management briefings on the business activities and strategic direction of Ascott Reit, the corporate governance policies and practices of the Manager, and are also provided with formal letters apprising them of their statutory and other duties and responsibilities as Directors. The new Directors are required to attend training conducted at the Singapore Institute of Directors on compliance, regulatory and corporate governance matters and a broad understanding of their roles and responsibilities under the Companies Act, the SFA, the Listing Manual and the Code of Corporate Governance.

The Board is also mindful of the need for all Directors to undergo continual relevant training as may be appropriate in the circumstances and to equip them to properly serve in their respective roles. To this end, the Directors are encouraged to participate in industry conferences, seminars or any training programme which may assist them in connection with their duties as Directors. Apart from external training, Directors are also provided with legal and regulatory updates from time to time (arranged by the company secretary of the Manager (Company Secretary)) to keep them apprised of relevant changes.

The induction, orientation and training of the Directors was arranged by the Company Secretary under the supervision of the Board, and fully funded by the Manager.

Principle 2: Board Composition and Guidance

As at 26 February 2013, the Board consists of nine Directors, eight of whom are non-executive Directors, and out of whom five, that is, more than half of the Board are independent Directors. A Director is considered independent if he has no relationship with the Manager, its related companies or its officers, any 10% Unitholder1 or its officers that could interfere, or be reasonably perceived to interfere, with the exercise of the Director’s independent business judgement with a view to the best interests of Ascott Reit. Mr Lim Jit Poh, Mr Ku Moon Lun, Mr S. Chandra Das, Mr Giam Chin Toon @ Jeremy Giam and Mr Zulkifli Bin Baharudin (who was appointed as independent non-executive Director with effect from 1 January 2013) are considered to be independent Directors. The Board has reviewed each one of the independent Directors and found him to be independent both in character and judgement, and that there are no relationships or circumstances which are likely to affect, or could appear to affect, the director's independent business judgement.

The non-executive Directors actively participate in setting and developing strategies and goals for Management, and reviewing and assessing Management’s performance. This enables Management to benefit from the non-executive Directors' external and objective perspective on issues that are brought before the Board. This also enables the Board to interact and work with Management through a healthy exchange of ideas and views to help shape the strategy for Ascott Reit.

The Board is of the view that its current composition comprises persons who, as a group, provides the necessary core competencies, and demonstrates an appropriate balance and diversity of skills, experience, gender and knowledge.

The Board is also of the view that the current size of the Board is appropriate and effective, taking into consideration the nature and scope of Ascott Reit’s operations.

The profiles of the Directors are set out on pages 16–21 of this Annual Report.

1. The term "10% Unitholder" shall refer to a person who has an interest or interests in one or more voting units in Ascott Reit and the total votes attached to that unit, or those units, is not less than 10% of the total votes attached to all the voting units in Ascott Reit.

Ascott Reit Annual Report 201234 FROM STRENGTH TO STRENGTH

Principle 3: Chairman and Chief Executive Officer

The roles of the chairman of the Board (Chairman) and the Chief Executive Officer (CEO) of the Manager are separate and the positions are held by two individuals, to maintain effective oversight and to ensure a clear division of responsibilities and duties between them. This is also to ensure an appropriate balance of power, increased accountability and greater capacity of the Board for independent decision-making. The Chairman and the CEO are not related to each other.

The Chairman leads the Board to ensure its effectiveness on all aspects of its role and sets its agenda. He ensures that the Directors receive accurate, clear and timely information, ensures adequate discussion of all agenda items at Board meetings, facilitates the contribution of the non-executive Directors, encourages constructive relations between non-executive Directors and Management, ensures effective communication with the Unitholders and promotes a high standard of corporate governance. The Chairman is also responsible for promoting a culture of openness and debate at the Board and for upholding high corporate governance standards.

The Chairman also ensures that the Board works together with Management with integrity, competency and moral authority, and engages Management in constructive debate on strategy, business operations and enterprise risks.

On 27 February 2012, Mr Tay Boon Hwee, Ronald, was appointed to the position of CEO of the Manager, and was subsequently also appointed as an Executive Director of the Manager with effect from 1 January 2013. Mr Tay currently has full executive responsibilities over the business direction and operational and management decisions of Ascott Reit.

Principle 4: Board MembershipPrinciple 5: Board Performance

As the Manager is not itself a listed entity, the Manager does not consider it necessary for the Board to establish a nominating committee. The Board itself performs the functions that may have been delegated to such a committee, namely, it administers nominations to the Board, reviews the structure, size and composition of the Board, and reviews the independence of Directors. Directors are not subject to periodic retirement by rotation. However, Directors who are above the age of 70 are statutorily required to seek re-appointment at each annual general meeting of the Manager.

The composition of the Board is reviewed regularly to ensure that the Board has the appropriate size and mix of expertise and experience to properly discharge its duties, having a view to the need for succession planning and board refreshment. In particular, the Manager strives to ensure that the Board as a whole has the requisite blend of background, experience and knowledge in business, finance and management skills critical to Ascott Reit’s businesses, and that each non-executive Director brings to the Board an independent and objective perspective to enable balanced and well-considered decisions to be made by the Board as a whole. The Board requires each Director to dedicate sufficient time and attention to the affairs of the Manager and Ascott Reit, and a Director with multiple board representations or other substantial commitments is held to the same expectation. The Board is of the view that the current commitments of each of its Directors are reasonable and each of the Directors is able to and has been adequately carrying out his duties.

The composition of the Board, including the selection of candidates for new appointments to the Board as part of the Board’s renewal process, is determined in line with, inter alia, the following principles:

• the Chairman should be an independent Director; • the Board should comprise Directors with a broad range of commercial experience, including expertise in funds

management, the property industry and in the legal field; and• independent Directors should constitute at least half of the Board.

The independence of each Director is reviewed by the Board upon appointment, and thereafter at least annually, by the Board.

Ascott Reit Annual Report 2012 35FROM STRENGTH TO STRENGTH

CORPORATE GOVERNANCE

The Manager believes that Board performance and that of each individual Director is reflected in, and evidenced by, its or his proper guidance, diligent oversight and able leadership, and the level of support it or he has lent to Management in steering Ascott Reit in the appropriate direction, as well as the long term performance of Ascott Reit through both favourable and challenging market conditions. This is ultimately reflected in safeguarding the interests of Ascott Reit and maximising Unitholders' value.

Contributions by an individual Director may also take other forms, including providing objective perspectives on issues, facilitating business opportunities and strategic relationships with external parties, and being accessible to Management outside of formal Board and/or Board Committee meetings. For example, the Directors make significant contributions to the management of Ascott Reit and give guidance to Management regularly via e-mail and telephone discussions outside of Board and Board Committee meetings.

The Board assesses its and each board committee’s effectiveness as a whole, as well as the contribution by each individual Director to the effectiveness of the Board and each board committee.

The matrix of the Directors’ appointment in the respective various Board Committees as at 26 February 2013 and their attendance at meetings of the Board and the Audit Committee during the financial year ended 31 December 2012 are set out below:

Board & Board Committees(as at 26 February 2013)

Board Members Audit CommitteeCorporate Disclosure Committee Executive Committee

Lim Jit Poh (Chairman) – Chairman –

Lim Ming Yan1 (Deputy Chairman) – – Chairman

Tay Boon Hwee, Ronald2 – Member Member

Ku Moon Lun Chairman – –

S. Chandra Das3 Member – –

Giam Chin Toon @ Jeremy Giam4 Member – –

Zulkifli Bin Baharudin5 – Member –

Jennie Chua6 – – –

Chong Kee Hiong7 – Member Member

Notes:1. Lim Ming Yan was appointed as Deputy Chairman of the Board and Chairman of Executive Committee on 1 January 2013. For FY2012, he was Member of

Corporate Disclosure Committee up to 5 February 2012.2. Tay Boon Hwee, Ronald, was appointed as Executive Director on 1 January 2013. He was also appointed as Member of Corporate Disclosure Committee and

Executive Committee on 24 January 2013.3. S. Chandra Das was Member of Corporate Disclosure Committee and Executive Committee up to 23 January 2013.4. Giam Chin Toon @ Jeremy Giam was Member of Executive Committee up to 23 January 2013.5. Zulkifli Bin Baharudin was appointed as Independent Non-Executive Director on 1 January 2013. He was also appointed as Member of Corporate Disclosure

Committee on 24 January 2013. 6. Jennie Chua was Member of Executive Committee up to 23 January 2013.7. Chong Kee Hiong stepped down as CEO of the Manager and became Non-Independent Non-Executive Director on 6 February 2012. He was appointed as

Member of Corporate Disclosure Committee on 6 February 2012.