Annual Report - NabtescoAnnual Report Year ended March 31,2003 2003 Profile Teijin Seiki Co., Ltd....

40

Annual Report 2003 Year ended March 31,2003

Transcript of Annual Report - NabtescoAnnual Report Year ended March 31,2003 2003 Profile Teijin Seiki Co., Ltd....

Annual Report2003Year ended March 31,2003

ProfileTeijin Seiki Co., Ltd. was originally established as TeijinKoku Kogyo Co., Ltd., in 1944, as a spin-off from TeikokuRayon Co., Ltd. (presently TEIJIN Limited). The Companyassumed its current name in 1945.

Since our establishment, we have continued to respond to awide range of industry needs by developing highlyinnovative technologies. Beginning our operations with thedevelopment and manufacture of textile machinery, wehave steadily increased the depth and breadth of ourtechnology and product lines. In 1955, we startedmanufacturing aircraft equipment. In 1959, we addedindustrial machinery. Manufacturing of oil hydraulicequipment began in 1961. In response to the growingsophistication of “mechatronics” technology, wecommenced developing precision reduction gears forindustrial robots and began manufacturing them in 1985. Attheir introduction, the precision movement and non-backlash characteristics of these gears reached levels notpreviously achieved in the market.

Moreover, with the aim of developing our business in Japanand overseas, we have continued to strengthen TEIJINSEIKI Group by establishing additional new companies withhighly specialized technologies and by investing in andacquiring companies with original technologies. Today, inaddition to TEIJIN SEIKI as the parent company, the Groupcurrently comprises 22 companies: 12 domesticsubsidiaries, 8 overseas subsidiaries, and 2 domesticaffiliates accounted for using the equity method.

Currently, TEIJIN SEIKI Group organizes its globaloperations in three major segments - Precision Equipmentand New Business, Aircraft and Oil Hydraulic Equipment,and Textile and Industrial Machinery. With a view tomaximizing its corporate value and ensuring ever-continuinggrowth, the Group has agreed to combine operations withNABCO Ltd., a long established and highly respectedmanufacturer of braking and other motion control systemsfor transportation, building and other applications. Aholding company is being established jointly with NABCOLtd. The holding company will assume ownership ofequity stock in the two groups and bring them, as equals,under its single management (presently scheduled forSeptember, 2003). To mark the special nature of thisoccasion in our company’s history, Teijin Seiki Co., Ltd. willrename itself TS Corporation (presently scheduled forOctober 1, 2003) as part of an overall program of morestrongly projecting the company’s image into worldmarkets.

TEIJIN SEIKI Group is aggressively implementing itsManagement Strategy aiming at generating consistent futuregrowth. Integration with NABCO Ltd. is the most importantaction taken as a part of this growth strategy. As it hasdone throughout its history, TEIJIN SEIKI Group, and now inits new combination with NABCO, will continue to focusever more closely on the shifting requirements of itscustomers worldwide and stay in the vanguard oftechnological innovation as the Group and its customersevolve in the 21st century.

Contents

CONSOLIDATED FINANCIAL HIGHLIGHTS.............................................................. 01

TO OUR SHAREHOLDERS.............................................................. 02

MANAGEMENT STRATEGY.............................................................. 03

INTRODUCTION OF NABTESCO CORPORATION.............................................................. 07

TEIJIN SEIKI AT A GLANCE.............................................................. 08

REVIEW OF OPERATIONS.............................................................. 10

CONSOLIDATED FINANCIAL REVIEW.............................................................. 12

CORPORATE DATA.............................................................. 37

01

For the Year:

Net sales ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・

Operating income ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・

Net income (loss) ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・

Net income (loss) per share (Yen) ・・・・・・・・・・・・・・・・・・・・・・

Overseas net sales ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・

Share of overseas net sales ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・

At Year-end:

Total shareholders’ equity ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・

Total assets ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・

Equity ratio ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・

Return on equity (ROE) ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・

¥ 66,707

2,134

96

1.22

30,953

46.4%

22,015

79,822

27.6%

0.4%

¥ 54,708

504

(4,252)

(54.10)

18,041

33.0%

16,654

74,020

22.5%

(22.0%)

¥ 67,865

2,509

687

9.74

26,992

39.8%

17,689

66,301

26.7%

4.0%

¥ 62,168

1,706

(307)

(3.90)

25,214

40.6%

17,627

57,120

30.9%

(1.7%)

¥ 66,222

3,842

1,570

19.56

26,551

40.1%

18,346

60,433

30.4%

8.7%

Millions of yen

1999 2000 2001 2002 2003

Net sales

90

80

70

60

50

40

30

20

10

0

¥ Billion

■ Precision Equipment and New Business

■ Aircraft and Oil Hydraulic Equipment

■ Textile and Industrial Machinery

Net income (loss) ROE

66.7

54.7

62.266.2

1999 2000 2001 2002 2003

¥ Billion

3.0

2.0

1.0

0.0

-1.0

-2.0

-3.0

-4.0

-5.01999 2000 2001 2002 2003

0.1

-0.3

0.7

1.6

%

15.0

10.0

5.0

0.0

-5.0

-10.0

-15.0

-20.0

-25.01999 2000 2001 2002 2003

-22.0

4.0

8.7

-1.7

CONSOLIDATED FINANCIAL HIGHLIGHTSYears ended March 31

0.4

-4.3

67.9

02

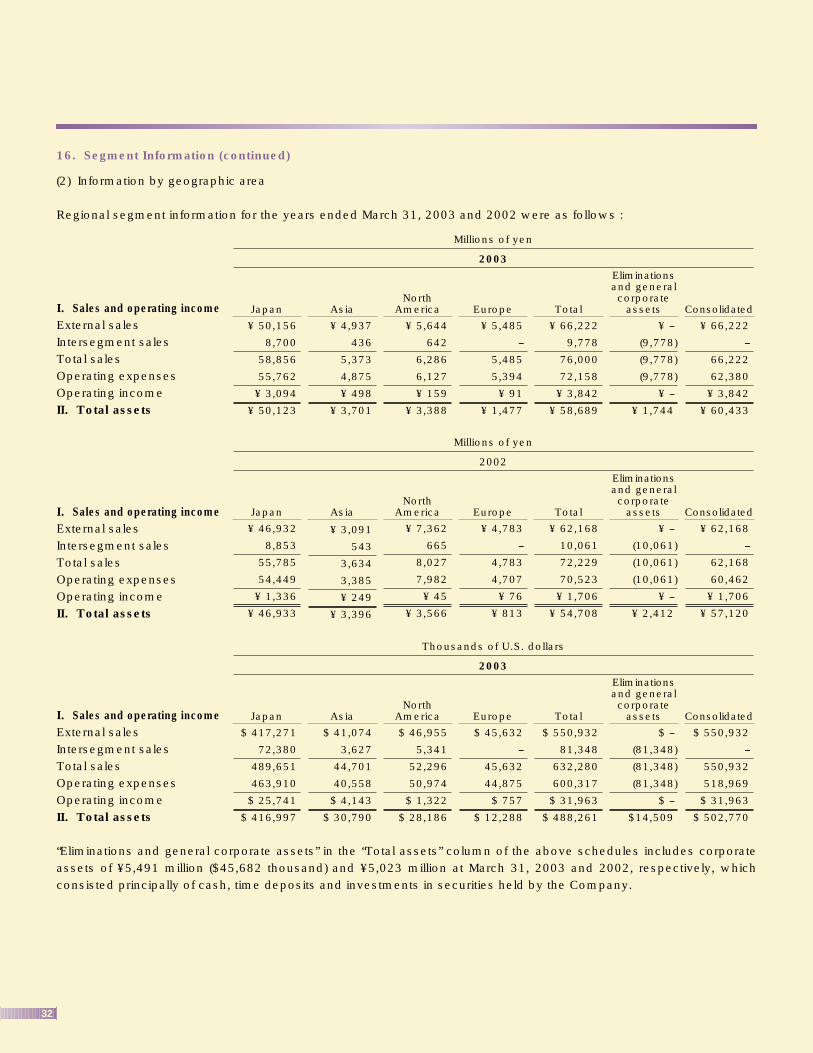

During FY2002, TEIJIN SEIKI Group increased its revenues over the previous year, chiefly due to continuedstrong demand for precision equipment and growth in China’s markets for hydraulic equipment and textilemachinery. Also because the Group’s ongoing efforts, initiated during the preceding year, to streamline itsoperations and to optimize its earning structure became fruitful, the Group increased its earningssignificantly, with all business segments maintaining or returning to profitability. TEIJIN SEIKI Group’s netsales in FY2002 were up by 6.5%, compared with the preceding year, to ¥66,222 million, and its operatingincome was up 125.3% to ¥3,842 million. Accordingly, the Group posted net income of ¥1,570 million andsucceeded in returning to overall profitability.

If we review our group operations segment by segment, the “Precision Equipment and New Business”segment was again profitable, thanks primarily to strong business in domestic and overseas robotics-manufacturing industries. The “Aircraft and Oil Hydraulic Equipment” segment experienced some reducedrevenues and earnings, mainly due to weaker Aircraft Equipment business following the aftereffects of the9.11 terrorist attacks in the United States which depressed the commercial airline industry’s business. Inthe “Textile and Industrial Machinery” segment, sales were lower in Industrial Machinery business, whereasTextile Machinery business enjoyed stronger sales, reflecting textile manufacturers’ continued enthusiasmespecially in China for investing in equipment and machinery. Overall, the Group achieved positive netincome across all of our business segments.

In line with our Corporate Philosophy – “We will make unceasing efforts to win the trust of the public bycontributing to world progress through our technology and by respecting people and nature” – TEIJIN SEIKIGroup has established the following Fundamental Management Policies:

・Pursuit of Profitable Growth・Enhancement of Group-Oriented Management・Investing in Technological Progress and Innovation・Pursuing and Strengthening Globalization

Driven by these policies, the Group is reforming its management structure, improving its profitability andincreasing its asset utilization efficiency, while pursuing growth opportunities. Our ultimate goal is toperpetuate growth in the “Corporate Value” of the Group as a whole as existing business grows and newbusinesses are undertaken.

In November 2002, TEIJIN SEIKI agreed with NABCO Ltd. (President Shigeo Iwatare, headquartered in Kobe,Hyogo Prefecture) to jointly establish a holding company and to come together as equals under the holdingcompany’s single management. Nabtesco Corporation, the new holding company scheduled to be formallyorganized in September 2003, will inherit all equity stock in these two groups, and make them its whollyowned subsidiaries.

TEIJIN SEIKI and NABCO are both manufacturers of complex and technologically advanced motion controlsystems. Our companies are of approximately equal size. They have maintained their leadership positionsin a number of specialized fields both in Japan and overseas. Finding themselves facing ever increasingglobal competition, the two groups have concluded that teaming up under integrated management is the mosteffective way of maximizing their combined corporate value and guaranteeing their long-term growth. Weare going to work tirelessly to maximize the synergies of corporate integration, and ensure that theintegration process proceeds as smoothly as possible.

Together with NABCO senior management in the new holding company, TEIJIN SEIKI Group is now quiteready to steer itself towards a new period of consistent growth. Our efforts are being dedicated in thatdirection and as we enter this new era in the history of TEIJIN SEIKI, we are working hard to earn the fulltrust and satisfaction of our customers, employees and shareholders.

June 2003

Makoto OkitsuPresident & CEO

To Our Shareholders

03

Management Strategy

Firmly based upon the TEIJIN SEIKI Group Vision to “Become a Leading and Highly ProfitableCorporate Group that Actively Performs Business on a Global Basis”, our Group continues to pursuethe Management Strategy developed in recent years aiming specifically at increasing overallcorporate value for our shareholders –– today and into the future.

As a major step toward increasing corporate value, TEIJIN SEIKI has concluded an agreement withNABCO Ltd., to join forces under a business integration agreement. Through this new combination,the Group is working to maximize synergies within the two companies and pursuing long-termdevelopment programs aiming at further increasing the combined companies’ value.

At this time TEIJIN SEIKI Group is focusing on“enhancing the stable revenue base” and “promotingdevelopment of new products and businesses.” TheGroup is promoting a process of “selectivity andconcentration” whereby resources are allocatedpreferentially to business areas that enjoy the

strongest competitive positions or offer the greatestpromise for the future. Within this element of ourStrategy, the Group is moving to improve theefficiency and production capabilities of theseselected areas so that their dominance in themarketplace can be increased. Through these and

TEIJIN SEIKI Group consists of three main businesssegments: “Precision Equipment and New Business”,“Aircraft and Oil Hydraulic Equipment” and “Textileand Industrial Machinery”. Conditions vary in the markets for each of thesebusiness segments but in overall terms, weakness inthe Japanese economy continued impactingoperations in each segment. Weaknesscharacterized important segments of the internationalmarket served by the Group. The worldwide slumpin semiconductors and more importantly for us,semiconductor capital equipment continued.Uncertain outlook for air travel (due to the effects ofthe 9.11 terrorist attacks, the war in Iraq, and SARS)extended the impact of the overall economic slumpon orders for aircraft, aircraft parts and supportservices.

We are very proud that in this difficult businessenvironment, all of the Group’s business segmentswere profitable and a significant increase in overallprofits was generated. Even the PrecisionEquipment business (specifically industrial robotsales), which struggled in the previous period,recovered strongly because of the increase in capitalinvestments by domestic and internationalautomakers. The Oil Hydraulic Equipment businessenjoyed the effects of a construction boom in Chinawhile sales of textile machinery especially in Chinagrew as business owners increased capitalinvestments. Furthermore, the Group’s efforts tooptimize operations and improve profit structure,which began in the previous period, contributed tothe profitability achieved by all of the businesssegments.

Under this severe business environment, the Group’s ManagementStrategy has led to a significant increase in profits in which allsegments participated

A Major Element of the Strategy is to Aggressively Develop the MostPromising Areas in Each Business Segment

04

other actions we look to achieve the desired overallstrengthening of our stable revenue base.Within “Precision Equipment and New Business”, theCompany is steadily expanding applications for itscore precision reduction gears into new areas for ussuch as semiconductor manufacturing and elevatorhoisting machines. In addition, new products arebeing developed to broaden our penetration in ourmain application areas which are industrial robotsand machine tools. The Group is pursuingdevelopment of a new series of reduction gears withhigher levels of precision and stiffness. A projectteam has also been formed to determine ways inwhich to minimize lead times and to reduce costs forthis product. Furthermore, the Group is planning tointroduce new products, such as wafer transfer unitsand dry vacuum pumps for semiconductormanufacturing and improved reduction gears forelevator hoisting machines so that its domestic andinternational customer base can be expanded.Finally, in 1999 and 2000, the Group establishedthree new business areas (heat control devices,digital logging systems and optical molding systems)with the hope that they will become major newcompanies within the Group. Significant progresshas already been made in digital logging systemsbusiness which has achieved profitability. Within “Aircraft and Oil Hydraulic Equipment”, therapid succession of negative news such as the 9.11terrorist attacks, the war in Iraq, and the SARSoutbreak took a toll on the Aircraft Equipmentbusiness. However, it is thought that the medium tolong-term outlook for this field remains stable andpositive. The world is shrinking and air travel has avery strong long-term growth trend. With this in mind,TEIJIN SEIKI Group is working hard to secure orderson new aircraft projects currently under developmentboth in Japan and overseas. Success in these effortswill generate stable profits for many years into thefuture. The Oil Hydraulic Equipment business wasalso hampered by the continued slump in thedomestic construction machinery market. However,this business area was buoyed by the steady growthof the hydraulic excavator market in China. Thistrend is expected to continue as the need increasefor construction machinery with preparations for the

2008 Olympics in Beijing. TEIJIN SEIKI Group hadthe foresight to establish a production base in Chinain 1996 and since then the strong local reputationand sales network that we have nurtured hasincreased sales in the region. The Group is workingto further strengthen its production base in China.Steps are being taken to further rationalize thedivision of production between the Group’s plants inJapan and China. An important new productcategory is TEIJIN SEIKI’s actuation units for windturbines where sales are increasing. We plan to enterboth the European and US markets where the use ofwind power is more prevalent. Plans are underwayto develop initial sales organizations in thesemarkets. In April 2003, the Group transferred its synthetic fibermachinery business to TMT Machinery, Inc. As aresult, reported revenues for “Textile and IndustrialMachinery” will decrease by approximately ¥8 billionin the coming period. In order to cover this drop inrevenues, TEIJIN SEIKI Group is aggressivelydeveloping new strategies for the industrialmachinery side of the business. The Group’sautomatic packaging machines have seen anincrease in overseas sales and in particular, the newhigh-speed pouch filler/sealer machines have beenhighly successful in the European pet food industry.In order to build on this success, the Group plans toexpand its overseas sales organization. In addition,the Group is working to develop new packagingmachines that incorporate greater functionality (suchas sterilization) and introduce new higher-speedmodels. The shift from cans and bottles to pouchesis a major trend in food and beverage packaging inmany parts of the world. TEIJIN SEIKI is focusingsignificant efforts on exploiting this trend. In the fieldof multi-forming machines, the Group has an ongoingprogram of cost reductions and is exploring a rangeof alternative strategies to grow the business andimprove its profitability. In a related product area, theGroup plans to supply Teijin Ltd.’s Home CareDivision with the principal components for its oxygenconcentrators.

05

Management Strategy

In November 2002, TEIJIN SEIKI Group executed aletter of intent for a business integration agreementwith NABCO Ltd. (Head Office: Kobe, HyogoPrefecture, Japan; President & CEO: Shigeo Iwatare).This agreement called for formation of a holdingcompany with both companies agreeing to integrateon an equal footing.TEIJIN SEIKI Group and NABCO Ltd. are bothmachinery system and component makers withsimilar business portfolios. In addition, bothcompanies are leaders in multiple domestic and/orinternational markets with long established and well-respected product lines. However, both companiesrecognized that fierce competition in the globalmarketplace will only intensify in the future. For thisreason, the companies determined that the mosteffective way to increase corporate value and toachieve long-term growth is to integrate.In order to ensure that integration goes smoothly andpositive effects of the integration are maximized, atwo-phase approach is being taken. First, a purelyshare-holding company named NabtescoCorporation will be established in September, 2003.Under this agreement, TEIJIN SEIKI and NABCO willbecome wholly owned subsidiaries operating directlyunder the holding company. In approximately oneyear, Phase II will begin and actual restructuring willoccur with the objective of transitioning to a“ business holding company.” This step will includesignificant integration activities. The reason for thistwo-phased approach is so that during Phase I, eachcompany’s strengths, strategies and corporate culture

can be understood mutually. In this way, overallinvestment efficiency within the group can beoptimized and positive effects of the integration canbe maximized during the second stage.The management structure in Phase I is comprised ofthe holding company owning all the shares of bothcompanies and functioning as the strategicheadquarters for both the NABTESCO Group and itssubsidiaries. In addition, the holding company willbe responsible for overall risk management, investor,government and other external relations andresponsibilities of the Group. At the same time, theholding company will have responsibility forprograms to create new businesses and productsthat take advantage of existing technologicalsynergies. The board of directors of the holdingcompany will appoint corporate officers to holdboard of director posts at the separate businessentities, including TEIJIN SEIKI, NABCO and theirsubsidiaries. These corporate officers will beresponsible for carrying out the day-to-day operationsof the subsidiary entities. Ultimate decision-makingauthority will be maintained by the board of directorsof the holding company on important issues but anappropriate level of authority will be delegated tosuch corporate officers. Through this, amanagement style that ensures both efficientdecision-making and necessary independence willbe implemented.

Efforts are already underway to identify and pursueprofit opportunities even before the integration takesplace.

For example in the Oil Hydraulic Equipmentbusiness, various efforts relating to procurement,mutual product supply and sales cooperation have

Carefully Planned Integration with NABCO is a Major Element ofManagement Strategy Aimed at Long-Term Development andIncreased Corporate Value

Management Strategy for Integration Calls for Immediate Pursuit ofProfit Opportunities and Identification of Technological Synergies

06

Management Strategy

The Oil Hydraulic Equipment’s joint development withNABCO has been mentioned. Pursuing “technologicalsynergies” will be a major element in the success ofTEIJIN SEIKI’s combination with NABCO. We mustquickly establish a management system that canfuse together each company’s core technologies andfacilitate development of highly competitive newproducts for new markets and business areas usingthis expanded technological base.To accomplish this, during Phase I, NABTESCOGroup will consolidate the technological oversightfunctions now present in both companies in order topromote maximum potential technological synergies.

There is a close fit between the technologies of thetwo companies. TEIJIN SEIKI supplies high-performance components that are borne out of ourcore “motion control technologies” including precisionreduction gears, aircraft equipment and oil hydraulicequipment. At NABCO, “control systemtechnologies” is one of their core technologies.These two core technologies are mutuallycomplementary and when combined correctly, willachieve accelerated development of next-generationproducts and entry into both new business areas andmarkets.

been carried out as a result of the businesscooperation agreement that was finalized in April2002 between TEIJIN SEIKI and NABCO. Already,several million yen worth of cost savings have beenachieved because of joint procurement activitiesperformed during the current period. The Grouphopes to achieve this sort of success throughoutother business segments as integration proceeds.

In the area of identifying technological synergies, theOil Hydraulic Equipment business plans to introducea new model, jointly developed with NABCO, ontothe market ahead of other divisions and optimize theglobal division-of-labor structure (including productionbases in China). Through these and other efforts, thedivision hopes to maximize positive benefits from theintegration.

As described above, tight integration with NABCOwill be a cornerstone of our future ManagementStrategy. Combining our two companies creates amuch larger entity with greater resources, broaderproduct lines and technological capabilities and alarger customer base. Taking maximum advantageof this unique opportunity is the challenge for ourcombined management teams. As part of thisimportant step in TEIJIN SEIKI’s history, we will bechanging our company name to “TS Corporation” onOctober 1, 2003. New logo designs and otherelements of a revitalized corporate image program

will be undertaken as part of the introduction ofNABTESCO. This new beginning will allow theCompany as a whole to aggressively implement theStrategy described above including focusing on ourmost promising opportunities whether they bemarkets such as China or products/technologiessuch as our packaging machines and continuing topursue promising new business areas. We believethat you can look forward with positive anticipationas TEIJIN SEIKI soon to be TS Corporation joins withNABCO and together as NABTESCO responds tonew challenges and opportunities.

Combining the Core Technologies of Both Companies is a MajorElement of Management Strategy in Order to Accelerate New ProductDevelopment and Entry into New Business Areas

Management Strategy for the Future

07

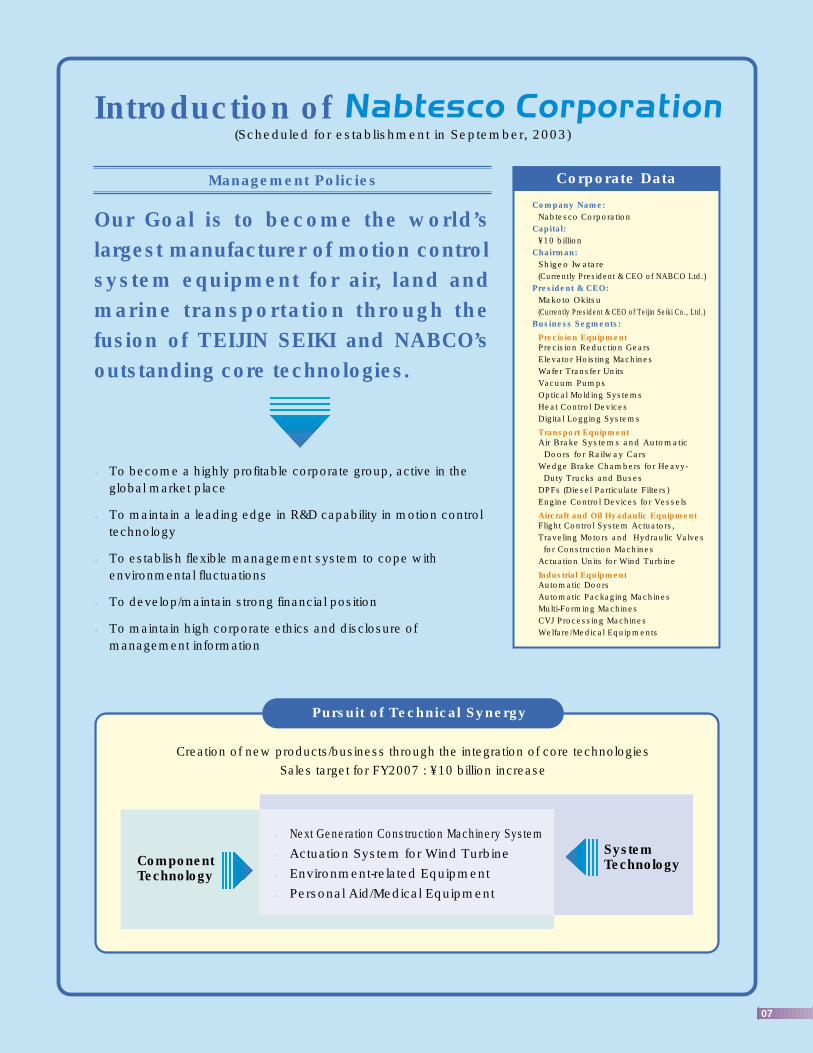

Our Goal is to become the world’slargest manufacturer of motion controlsystem equipment for air, land andmarine transportation through thefusion of TEIJIN SEIKI and NABCO’soutstanding core technologies.

●To become a highly profitable corporate group, active in the global market place

●To maintain a leading edge in R&D capability in motion control technology

●To establish flexible management system to cope with environmental fluctuations

●To develop/maintain strong financial position

●To maintain high corporate ethics and disclosure of management information

Creation of new products/business through the integration of core technologies

Sales target for FY2007 : ¥10 billion increase

Introduction of (Scheduled for establishment in September, 2003)

Management Policies

■Company Name:Nabtesco Corporation

■Capital:¥10 billion

■Chairman:Shigeo Iwatare (Currently President & CEO of NABCO Ltd.)

■President & CEO:Makoto Okitsu (Currently President & CEO of Teijin Seiki Co., Ltd.)

■Business Segments:

Precision EquipmentPrecision Reduction GearsElevator Hoisting MachinesWafer Transfer UnitsVacuum PumpsOptical Molding SystemsHeat Control DevicesDigital Logging Systems

Transport EquipmentAir Brake Systems and Automatic

Doors for Railway CarsWedge Brake Chambers for Heavy-Duty Trucks and Buses

DPFs (Diesel Particulate Filters)Engine Control Devices for Vessels

Aircraft and Oil Hyadaulic EquipmentFlight Control System Actuators,Traveling Motors and Hydraulic Valves for Construction Machines

Actuation Units for Wind Turbine

Industrial EquipmentAutomatic DoorsAutomatic Packaging MachinesMulti-Forming MachinesCVJ Processing MachinesWelfare/Medical Equipments

Corporate Data

Pursuit of Technical Synergy

ComponentTechnology

● Next Generation Construction Machinery System

●Actuation System for Wind Turbine

●Environment-related Equipment

●Personal Aid/Medical Equipment

SystemTechnology

08

Teijin Seiki at a GlanceOutline of BusinessPrecision Equipment and New Business

1999~Actuator for Semiconductor

Heat Lane

Logging System

1994~ Rapid Prototyping System

1971~ Vacuum Pump and Equipment

1985~ Precision Reduction Gear / Servo Actuator

2002~ Actuation Unit for Wind Turbine

1976~ Hydraulic Motor with Reduction Gear

1944~ Aircraft Equipment

1975~ Automotive Parts

1966~ Automatic Packaging Equipment

1959~ Forming Machine / Machine Tool

1945~ Textile Machinery

Precision Equipment and New Business

Aircraft and Oil Hydraulic EquipmentAircraft and Oil Hydraulic Equipment

Textile and Industrial MachineryTextile and Industrial Machinery

●Precision Equipment and New Business

In this business segment, our most important products are precision reduction gearsand servo actuators which integrate servomotors and precision reduction gears.TEIJIN SEIKI’s highly regarded reduction gears and servo actuators feature smallsize, light weight, high precision, high stiffness and achieve high levels of efficiency.They are used by some of the world’s leading manufacturers of industrial robotics,machine tools and general industrial machinery.

New Business activities are concentrated in three companies originally organized bythe corporation’s New Business Development Department. The business areas ofthese three companies are: optical molding systems which can form complex shapeswithout the use of metal dies, high-performance heat control devices equipped withmeandering capillary tube heat pipes which possess unique heat transfertechnology, and digital logging systems that are finding broad applications such ascall centers in financial institutions.

●Aircraft and Oil Hydraulic Equipment

In the Aircraft Equipment sector, TEIJIN SEIKI supplies major aircraft manufacturerssuch as Boeing and Cessna with a range of high precision products especially oilhydraulic actuators for flight control systems. Through long established technicalassistance and joint venture agreements with leading American companies in thefield of aerospace systems and components, TEIJIN SEIKI has become an importantsupplier of aircraft and aerospace electrical power generating systems, fuel pumps,valves and other critical components. TEIJIN SEIKI is an important supplier toJapanese aircraft and aerospace companies and a key partner in internationalaircraft development projects.

In the Oil Hydraulic Equipment sector, traveling motors powering the drive sprocketsof crawler mounted hydraulic excavators and other construction equipment are theprincipal products of this business sector. TEIJIN SEIKI maintains a high marketshare earned through superior compact design and the high evaluation and solidtrust it has earned from the market.

Recently TEIJIN SEIKI began supplying actuation units for wind turbines. We areexpanding our business in this important energy saving and environmentally friendlyapplication. Wind turbine use is expected to grow significantly as technologyimproves and the need for clean energy increases.

●Textile and Industrial Machinery

TEIJIN SEIKI supplies an integrated line of high performance equipment andsystems for the production of man made filament yarns including: spinningmachines, high speed take up winders and draw texturing machines. In thisbusiness sector, TEIJIN SEIKI is established as one of the world’s leadingcompanies. Long a major supplier in both Japan and throughout Asia, we havebroadened our markets to include Oceania, Europe and North America. In April2003, TEIJIN SEIKI transferred its Synthetic-Fiber Machinery Business to TMTMachinery, a new company jointly established with two of Japan’s leading textilemachinery manufacturers.

In the Industrial Machinery sector, TEIJIN SEIKI has developed and supplies highlyoriginal industrial machinery designed to address automation, labor-savings, andmechanization for a variety of production lines in different industries. We have beenenjoying an extremely large share of the market for certain types automatic foodindustry filling/packaging machines. This product line is being broadened with thedevelopment of machinery for the detergent and the pharmaceutical industries.

09

Market Condition and Key-Stratesies Major Companies

●Domestic

Teijin Seiki Co., Ltd.Diavac LimitedTS Heatronics Co., Ltd.LogIT CorporationCMET INC.

●Overseas

TEIJIN SEIKI BOSTON, INC.TEIJIN SEIKI EUROPE GmbHTeijin Seiki Advanced Technologies, Inc.

●Domestic

Teijin Seiki Co., Ltd.

STS Corporation

●Overseas

TEIJIN SEIKI AMERICA, INC.

Shanghai Teijin Seiki Co., Ltd.

●Domestic

Toyo Jidoki Co., Ltd.

Teijin Seiki Precision Co., Ltd.

TSTM Co., Ltd.

TMT MACHINERY, INC.

●Overseas

P.T.PAMINDO TIGA T

Shanghai Teijin Seiki Textile machinery Co., Ltd.

●Precision Equipment and New Business

The Group has long supplied precision reduction gears to many of the world’s leading industrial-robotics manufacturers. In order to maintain and strengthen its competitive position, the Group hasaccelerated the introduction of next-generation models. Broadly based efforts to improve cost-competitiveness are continuing. The Group is investing further in developing markets forsemiconductor-manufacturing and elevator-hoisting applications both based on its proprietarytechnologies.

The Group is working to improve the market position of its optical molding systems (CMET Inc.) bydeveloping and marketing new products with ever higher levels of performance. The uniqueness of theGroup’s high-performance "meandering capillary heat pipe" thermal-control devices (TS HeatronicsCo., Ltd.) is gaining greater customer recognition in target markets. Greater investments are beingmade to realize the full commercial potential of this unique and proprietary technology. The Group willexpand its digital logging systems (LogIT Corporation) business by vigorously offering a greater rangeof integrated solutions combining enhanced technological capabilities and related products offeringgreater functionality.

●Aircraft and Oil Hydraulic Equipment

The aftereffects of the 9.11 terrorist attacks in the United States have depressed business in thecommercial airline industry and aircraft manufacturers’ production is not expected to begin recoveringbefore 2005. New programs for aircraft development have been initiated both domestically andinternationally. The Group is working hard to secure contracts from these new aircraft developmentprograms. Long lead times characterize the development of major new aircraft. Success in havingGroup components and systems specified on these new aircraft will prepare a strong foundation for thisbusiness to continue operating briskly over the next ten years and beyond. Flight control actuators areexpected to continue as the group’s most important product but today’s product line is much broaderthan in earlier years giving the Group greater future potential.

In the Oil Hydraulic Equipment sector, the Group’s most important market, construction-machinery,remains weak in Japan but is growing overseas, particularly in China where very large infrastructureinvestments are being made. TEIJIN SEIKI’s combination with NABCO Ltd. will provide significantsynergies for the Group in product development, manufacturing and sales. These synergies will beenhanced further using the Group’s China based manufacturing facility and its supplier network. Next-generation construction-machinery applications are currently being designed to provide a strongfoundation for the Group’s future market position.

As the global market for wind turbines is expected to grow at an annual rate of roughly 20%, the Groupis focusing considerable attention on this area with particular emphasis on actuator units for windturbines.

●Textile and Industrial Machinery

In April 2003 the Group completed the transfer of all functions related to its synthetic-fiber machinerybusiness, into TMT Machinery Inc., a joint venture with two of Japan’s leading textile machinerymanufacturers. Because of weak conditions in its industry, TMT Machinery will focus primarily onimproving the profitability of its combined operations. However, work is already underway to developits first machine incorporating the combined technical strengths of its three equity partners. Togetherthe three partners possess a world-leading base of textile machinery technology and TMT Machineryshould become a powerful force in world markets.

The Group projects growing demand for its automatic filling/packaging machines for food and chemicalproducts (Toyo Jidoki Co., Ltd.). The Japanese food industry’s increased awareness of the need forconserving resources, food safety and improved sanitation are major drivers for this expected growth.Overseas, too, applications using Group filling/packaging machines for pet food, retorted foods,beverages, and other products, are expected to become increasingly popular.

In the highlypromising area of home medical care, the Group is working with Teijin Limited tomanufacture key components for oxygen concentrators (Teijin Seiki Precision Co., Ltd.) utilizing itsextensive design, production, and processing/manufacturing skills.

10

Review of Operations(consolidated)

Textile and IndustrialMachinery

Aircraft and Oil HydraulicEquipment

Precision Equipment and New Business

Net Sales

¥ 66,222 million(2003)

32.7%

38.0%

29.3%

Precision Equipment and New Business

【Principal Products】

Operating income (loss)

¥ Billion

2.5

2.0

1.5

1.0

0.5

0

-0.51999 2000 2001 2002 2003

Net sales

¥ Billion

30

25

20

15

10

5

01999 2000 2001 2002 2003

12.8

18.5

21.621.8

15.40.9

1.2

2.4

1.4

-0.2

Note:External sales only

In Precision Equipment and New Business, sales increased by¥3.1 billion or by 16.8%, compared with the preceding year, to¥21.6 billion, and operating income was ¥1.4 billion, improvingby ¥1.6 billion and regaining profitability.

Sales of precision reduction gears for robotics and forsemiconductor-manufacturing equipment benefited from thevery strong markets in both domestic and overseas robotics-manufacturing industries.

"New Business" generally had difficulties increasing sales, asthe decline in IT industries.

Precision Equipment and New Business

Vigo Drive Vigo Servo Rapid Meister 6000

CMET INC.

11

Aircraft and Oil Hydraulic Equipment Textile and Industrial Machinery

In Aircraft and Oil Hydraulic Equipment, sales decreased by¥0.2 billion or by 0.9%, compared with the preceding year, to¥25.2 billion, and operating income decreased by ¥0.5 billion orby 24.6%, to ¥1.5 billion.

The aftereffects of the 9.11 terrorist attacks in the U.S.depressed business in the commercial airline industry, slowedaircraft manufacturers’ production, and dampened demand forafter-market supplies and services.

Demand for oi l hydraulic equipment among domesticconstruction-machinery manufacturers seems to havestabilized after a period of decline while overseas demand,particularly in China to assemble hydraulic excavators,continued to be strong.

In Textile and Industrial Machinery, sales increased by ¥1.2billion or by 6.5%, compared with the preceding year, to ¥19.4billion, and operating income was ¥0.9 billion, improving by¥1.0 billion and regaining profitability.

Sales of textile machinery increased because customers inChina continued to invest heavily in automated equipment toimprove quality and reduce costs even as the market forsynthetic fibers, especially for polyester filament yarns,remained oversupplied. This line’s profitability improvedsubstantially, the result of streamlined operations leading toreduced costs as well as higher sales.

A succession of irregularities exposed in the domestic foodindustry dampened demand for automatic food-filling/packagingmachines. Sales of forming machines and machine tools failedto recover, since domestic and overseas manufacturingindustries remained stagnant. Overall sales of industrialmachinery decreased.

Aircraft and Oil Hydraulic EquipmentOperating income

¥ Billion

3.0

2.5

2.0

1.5

1.0

0.5

01999 2000 2001 2002 2003

1.1

1.9

1.2

2.0

Net sales

¥ Billion

30

25

20

15

10

5

01999 2000 2001 2002 2003

24.9 24.725.6 25.4 25.2

1.5

Note:External sales only

Textile and Industrial MachineryOperating income (loss)

¥ Billion

3

2

1

0

-1

-2

-3

-4

-51999 2000 2001 2002 2003

0.1

-2.5

-1.1

-0.1

0.9

Net sales

¥ Billion

40

35

30

25

20

15

10

5

01999 2000 2001 2002 2003

29.0

13.7

21.418.2 19.4

Note:External sales only

TL-AX1High Speed Pouch Filler/Sealer Machine Forming MachineB777 FLAPERON

Power Control UnitGM GMm-SERIESTravelling Motor

Toyo Jidoki Co., Ltd. Teijin Seiki Precision Co., Ltd.

12

Consolidated Financial Review

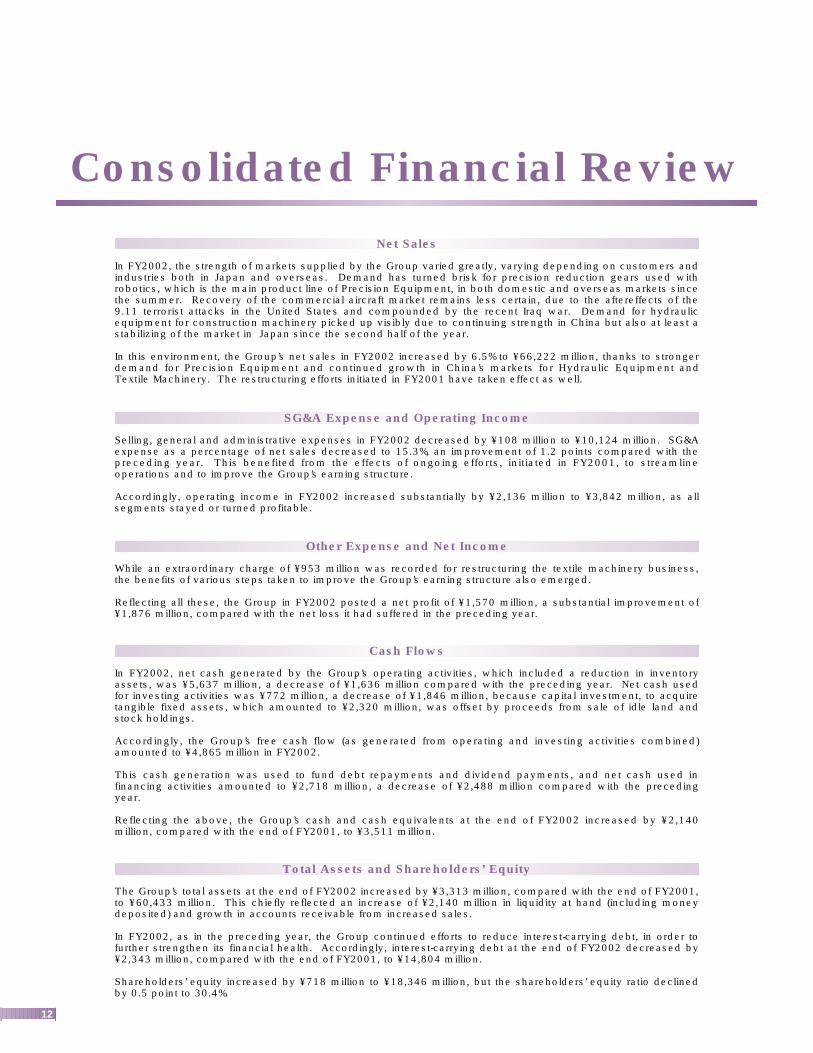

In FY2002, the strength of markets supplied by the Group varied greatly, varying depending on customers andindustries both in Japan and overseas. Demand has turned brisk for precision reduction gears used withrobotics, which is the main product line of Precision Equipment, in both domestic and overseas markets sincethe summer. Recovery of the commercial aircraft market remains less certain, due to the aftereffects of the9.11 terrorist attacks in the United States and compounded by the recent Iraq war. Demand for hydraulicequipment for construction machinery picked up visibly due to continuing strength in China but also at least astabilizing of the market in Japan since the second half of the year.

In this environment, the Group’s net sales in FY2002 increased by 6.5% to ¥66,222 million, thanks to strongerdemand for Precision Equipment and continued growth in China’s markets for Hydraulic Equipment andTextile Machinery. The restructuring efforts initiated in FY2001 have taken effect as well.

Net Sales

Selling, general and administrative expenses in FY2002 decreased by ¥108 million to ¥10,124 million. SG&Aexpense as a percentage of net sales decreased to 15.3%, an improvement of 1.2 points compared with thepreceding year. This benefited from the effects of ongoing efforts, initiated in FY2001, to streamlineoperations and to improve the Group’s earning structure.

Accordingly, operating income in FY2002 increased substantially by ¥2,136 million to ¥3,842 million, as allsegments stayed or turned profitable.

SG&A Expense and Operating Income

While an extraordinary charge of ¥953 million was recorded for restructuring the textile machinery business,the benefits of various steps taken to improve the Group’s earning structure also emerged.

Reflecting all these, the Group in FY2002 posted a net profit of ¥1,570 million, a substantial improvement of¥1,876 million, compared with the net loss it had suffered in the preceding year.

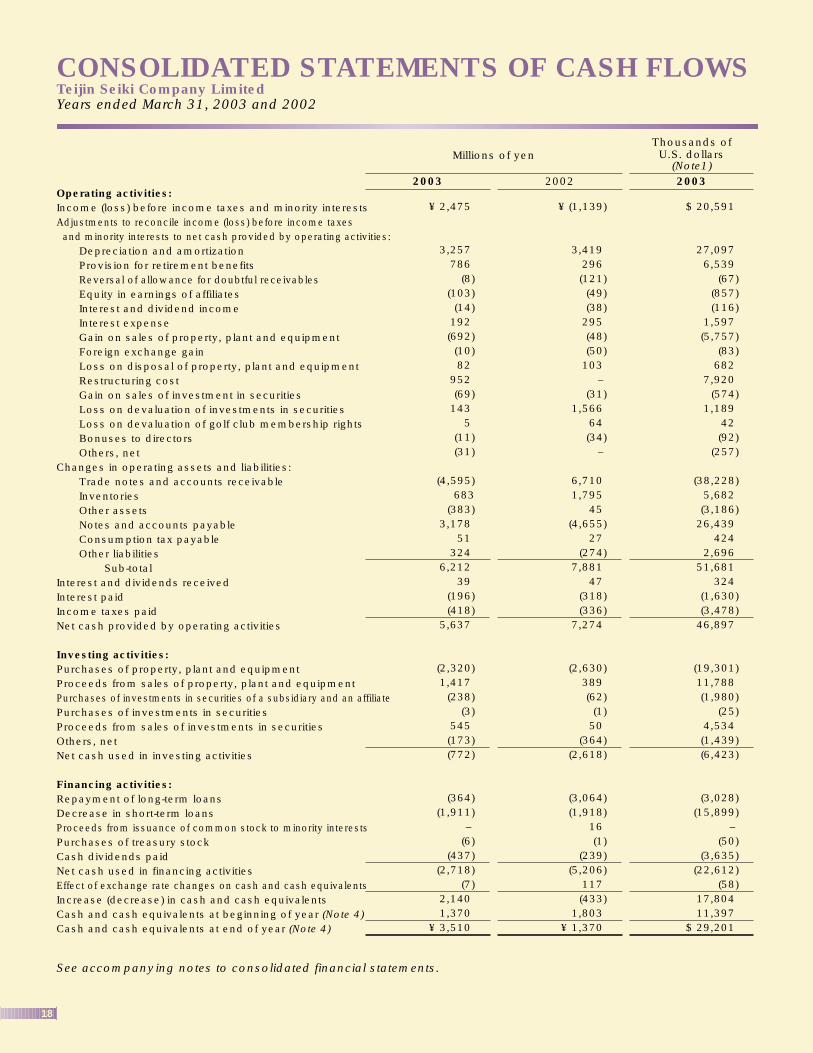

Other Expense and Net Income

In FY2002, net cash generated by the Group’s operating activities, which included a reduction in inventoryassets, was ¥5,637 million, a decrease of ¥1,636 million compared with the preceding year. Net cash usedfor investing activities was ¥772 million, a decrease of ¥1,846 million, because capital investment, to acquiretangible fixed assets, which amounted to ¥2,320 million, was offset by proceeds from sale of idle land andstock holdings.

Accordingly, the Group’s free cash flow (as generated from operating and investing activities combined)amounted to ¥4,865 million in FY2002.

This cash generation was used to fund debt repayments and dividend payments, and net cash used infinancing activities amounted to ¥2,718 million, a decrease of ¥2,488 million compared with the precedingyear.

Reflecting the above, the Group’s cash and cash equivalents at the end of FY2002 increased by ¥2,140million, compared with the end of FY2001, to ¥3,511 million.

Cash Flows

The Group’s total assets at the end of FY2002 increased by ¥3,313 million, compared with the end of FY2001,to ¥60,433 million. This chiefly reflected an increase of ¥2,140 million in liquidity at hand (including moneydeposited) and growth in accounts receivable from increased sales.

In FY2002, as in the preceding year, the Group continued efforts to reduce interest-carrying debt, in order tofurther strengthen its financial health. Accordingly, interest-carrying debt at the end of FY2002 decreased by¥2,343 million, compared with the end of FY2001, to ¥14,804 million.

Shareholders’ equity increased by ¥718 million to ¥18,346 million, but the shareholders’ equity ratio declinedby 0.5 point to 30.4%.

Total Assets and Shareholders’ Equity

13

Consolidated Financial StatementsTeijin Seiki Company Limited

Years ended March 31, 2003 and 2002

Contents

Consolidated Balance Sheets.............................................................. 14

Consolidated Statements of Operations.............................................................. 16

Consolidated Statements of Shareholders’ Equity.............................................................. 17

Consolidated Statements of Cash Flows.............................................................. 18

Notes to Consolidated Financial Statements.............................................................. 19

Report of Independent Public Accountants.............................................................. 35

14

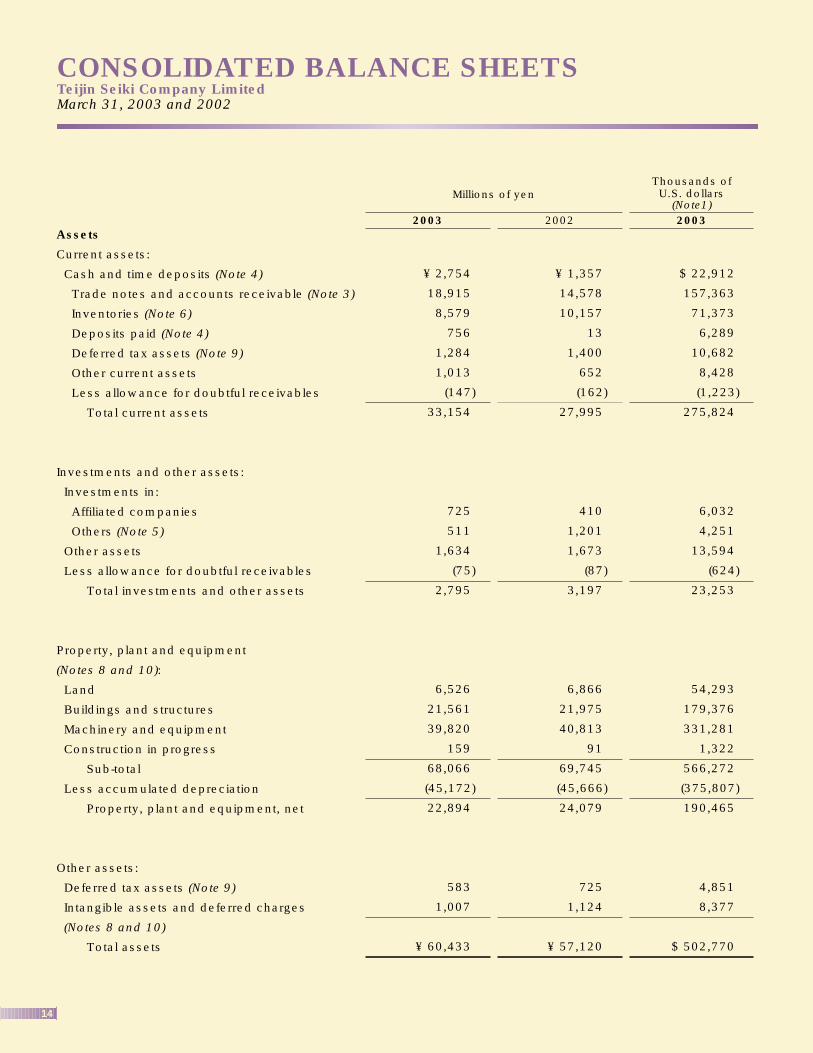

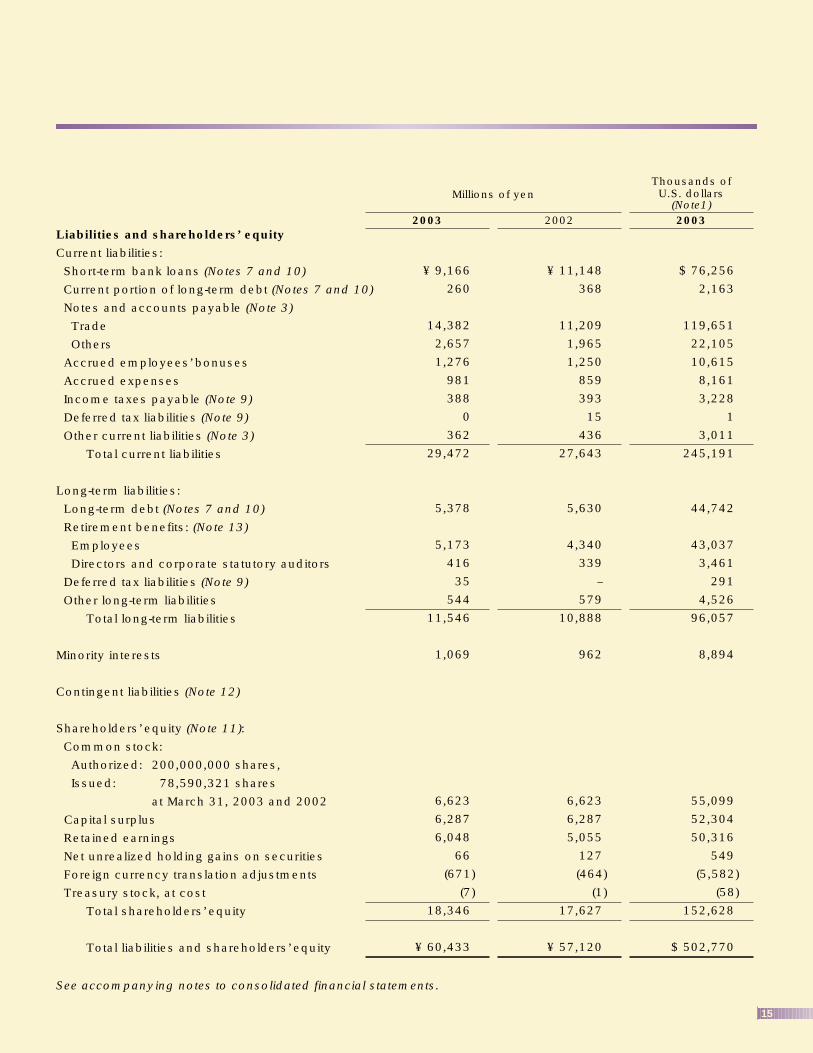

CONSOLIDATED BALANCE SHEETSTeijin Seiki Company Limited March 31, 2003 and 2002

Millions of yen

2003

Thousands ofU.S. dollars

(Note1)2002 2003

¥ 2,754

18,915

8,579

756

1,284

1,013

(147)

33,154

725

511

1,634

(75)

2,795

6,526

21,561

39,820

159

68,066

(45,172)

22,894

583

1,007

¥ 60,433

¥ 1,357

14,578

10,157

13

1,400

652

(162)

27,995

410

1,201

1,673

(87)

3,197

6,866

21,975

40,813

91

69,745

(45,666)

24,079

725

1,124

¥ 57,120

$ 22,912

157,363

71,373

6,289

10,682

8,428

(1,223)

275,824

6,032

4,251

13,594

(624)

23,253

54,293

179,376

331,281

1,322

566,272

(375,807)

190,465

4,851

8,377

$ 502,770

Assets

Current assets:

Cash and time deposits (Note 4)

Trade notes and accounts receivable (Note 3)

Inventories (Note 6)

Deposits paid (Note 4)

Deferred tax assets (Note 9)

Other current assets

Less allowance for doubtful receivables

Total current assets

Investments and other assets:

Investments in:

Affiliated companies

Others (Note 5)

Other assets

Less allowance for doubtful receivables

Total investments and other assets

Property, plant and equipment

(Notes 8 and 10):

Land

Buildings and structures

Machinery and equipment

Construction in progress

Sub-total

Less accumulated depreciation

Property, plant and equipment, net

Other assets:

Deferred tax assets (Note 9)

Intangible assets and deferred charges

(Notes 8 and 10)

Total assets

15

Liabilities and shareholders’ equity

Current liabilities:

Short-term bank loans (Notes 7 and 10)

Current portion of long-term debt (Notes 7 and 10)

Notes and accounts payable (Note 3)

Trade

Others

Accrued employees’ bonuses

Accrued expenses

Income taxes payable (Note 9)

Deferred tax liabilities (Note 9)

Other current liabilities (Note 3)

Total current liabilities

Long-term liabilities:

Long-term debt (Notes 7 and 10)

Retirement benefits: (Note 13)

Employees

Directors and corporate statutory auditors

Deferred tax liabilities (Note 9)

Other long-term liabilities

Total long-term liabilities

Minority interests

Contingent liabilities (Note 12)

Shareholders’ equity (Note 11):

Common stock:

Authorized: 200,000,000 shares,

Issued: 78,590,321 shares

at March 31, 2003 and 2002

Capital surplus

Retained earnings

Net unrealized holding gains on securities

Foreign currency translation adjustments

Treasury stock, at cost

Total shareholders’ equity

Total liabilities and shareholders’ equity

See accompanying notes to consolidated financial statements.

¥ 9,166

260

14,382

2,657

1,276

981

388

0

362

29,472

5,378

5,173

416

35

544

11,546

1,069

6,623

6,287

6,048

66

(671)

(7)

18,346

¥ 60,433

Millions of yen

2003

Thousands ofU.S. dollars

(Note1)2002 2003

¥ 11,148

368

11,209

1,965

1,250

859

393

15

436

27,643

5,630

4,340

339

–

579

10,888

962

6,623

6,287

5,055

127

(464)

(1)

17,627

¥ 57,120

$ 76,256

2,163

119,651

22,105

10,615

8,161

3,228

1

3,011

245,191

44,742

43,037

3,461

291

4,526

96,057

8,894

55,099

52,304

50,316

549

(5,582)

(58)

152,628

$ 502,770

16

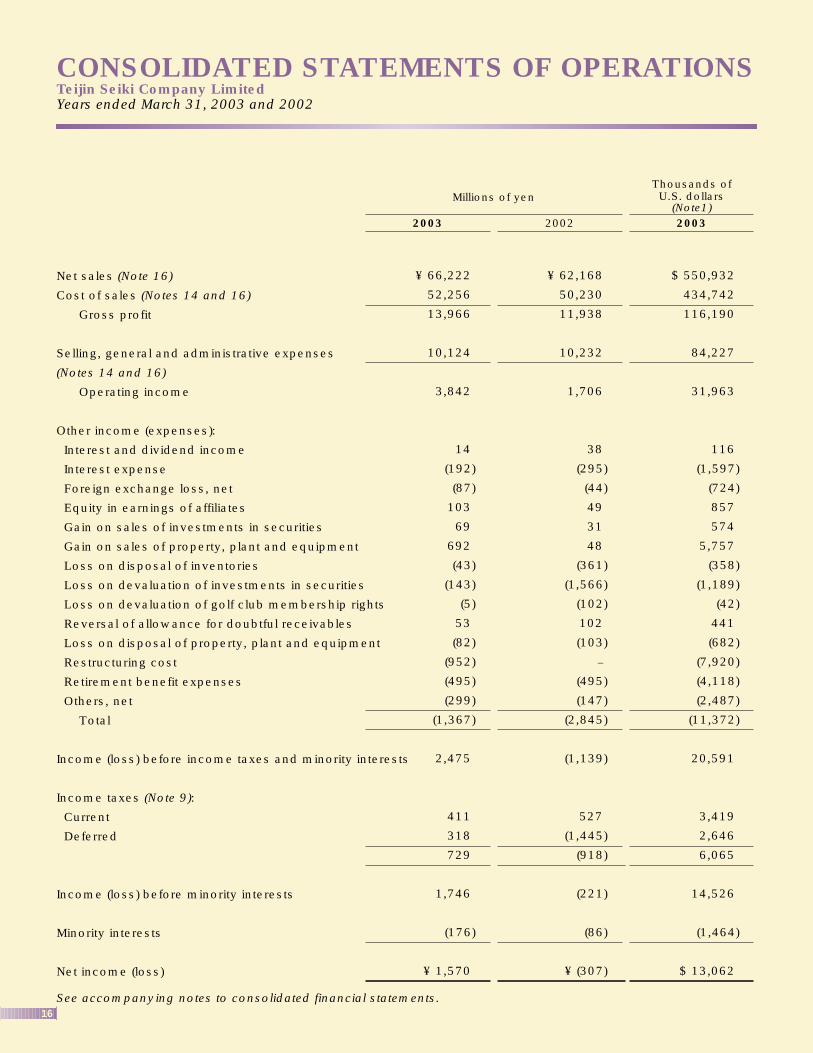

CONSOLIDATED STATEMENTS OF OPERATIONSTeijin Seiki Company LimitedYears ended March 31, 2003 and 2002

Net sales (Note 16)

Cost of sales (Notes 14 and 16)

Gross profit

Selling, general and administrative expenses

(Notes 14 and 16)

Operating income

Other income (expenses):

Interest and dividend income

Interest expense

Foreign exchange loss, net

Equity in earnings of affiliates

Gain on sales of investments in securities

Gain on sales of property, plant and equipment

Loss on disposal of inventories

Loss on devaluation of investments in securities

Loss on devaluation of golf club membership rights

Reversal of allowance for doubtful receivables

Loss on disposal of property, plant and equipment

Restructuring cost

Retirement benefit expenses

Others, net

Total

Income (loss) before income taxes and minority interests

Income taxes (Note 9):

Current

Deferred

Income (loss) before minority interests

Minority interests

Net income (loss)

See accompanying notes to consolidated financial statements.

Millions of yen

2003

Thousands ofU.S. dollars

(Note1)2002 2003

¥ 62,168

50,230

11,938

10,232

1,706

38

(295)

(44)

49

31

48

(361)

(1,566)

(102)

102

(103)

–

(495)

(147)

(2,845)

(1,139)

527

(1,445)

(918)

(221)

(86)

¥ (307)

$ 550,932

434,742

116,190

84,227

31,963

116

(1,597)

(724)

857

574

5,757

(358)

(1,189)

(42)

441

(682)

(7,920)

(4,118)

(2,487)

(11,372)

20,591

3,419

2,646

6,065

14,526

(1,464)

$ 13,062

¥ 66,222

52,256

13,966

10,124

3,842

14

(192)

(87)

103

69

692

(43)

(143)

(5)

53

(82)

(952)

(495)

(299)

(1,367)

2,475

411

318

729

1,746

(176)

¥ 1,570

17

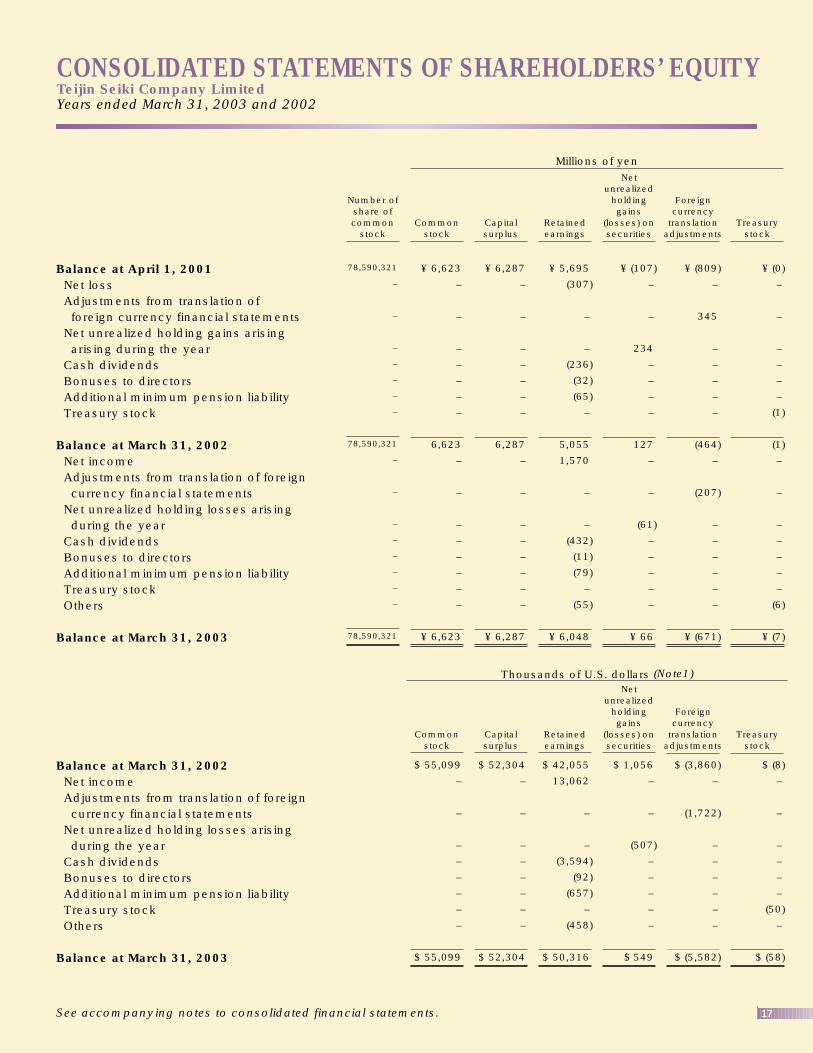

CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITYTeijin Seiki Company LimitedYears ended March 31, 2003 and 2002

Balance at April 1, 2001Net lossAdjustments from translation offoreign currency financial statements

Net unrealized holding gains arising arising during the year

Cash dividendsBonuses to directorsAdditional minimum pension liabilityTreasury stock

Balance at March 31, 2002Net incomeAdjustments from translation of foreign currency financial statements

Net unrealized holding losses arising during the year

Cash dividendsBonuses to directorsAdditional minimum pension liabilityTreasury stockOthers

Balance at March 31, 2003

Balance at March 31, 2002Net incomeAdjustments from translation of foreigncurrency financial statements

Net unrealized holding losses arising during the year

Cash dividendsBonuses to directorsAdditional minimum pension liabilityTreasury stockOthers

Balance at March 31, 2003

See accompanying notes to consolidated financial statements.

Millions of yen

Number ofshare ofcommon

stock

78,590,321

–

–

–

–

–

–

–

78,590,321

–

–

–

–

–

–

–

–

78,590,321

Commonstock

¥ 6,623

–

–

–

–

–

–

–

6,623

–

–

–

–

–

–

–

–

¥ 6,623

$ 55,099

–

–

–

–

–

–

–

–

$ 55,099

Capitalsurplus

¥ 6,287

–

–

–

–

–

–

–

6,287

–

–

–

–

–

–

–

–

¥ 6,287

$ 52,304

–

–

–

–

–

–

–

–

$ 52,304

Retainedearnings

¥ 5,695

(307)

–

–

(236)

(32)

(65)

–

5,055

1,570

–

–

(432)

(11)

(79)

–

(55)

¥ 6,048

$ 42,055

13,062

–

–

(3,594)

(92)

(657)

–

(458)

$ 50,316

Netunrealized

holdinggains

(losses) onsecurities

¥ (107)

–

–

234

–

–

–

–

127

–

–

(61)

–

–

–

–

–

¥ 66

$ 1,056

–

–

(507)

–

–

–

–

–

$ 549

Foreigncurrency

translationadjustments

¥ (809)

–

345

–

–

–

–

–

(464)

–

(207)

–

–

–

–

–

–

¥ (671)

$ (3,860)

–

(1,722)

–

–

–

–

–

–

$ (5,582)

Treasurystock

¥ (0)

–

–

–

–

–

–

(1)

(1)

–

–

–

–

–

–

–

(6)

¥ (7)

$ (8)

–

–

–

–

–

–

(50)

–

$ (58)

Thousands of U.S. dollars (Note1)

Commonstock

Capitalsurplus

Retainedearnings

Netunrealized

holdinggains

(losses) onsecurities

Foreigncurrency

translationadjustments

Treasurystock

18

Operating activities:Income (loss) before income taxes and minority interestsAdjustments to reconcile income (loss) before income taxes and minority interests to net cash provided by operating activities:

Depreciation and amortizationProvision for retirement benefitsReversal of allowance for doubtful receivablesEquity in earnings of affiliatesInterest and dividend incomeInterest expenseGain on sales of property, plant and equipmentForeign exchange gainLoss on disposal of property, plant and equipmentRestructuring costGain on sales of investment in securitiesLoss on devaluation of investments in securitiesLoss on devaluation of golf club membership rightsBonuses to directorsOthers, net

Changes in operating assets and liabilities:Trade notes and accounts receivableInventoriesOther assetsNotes and accounts payableConsumption tax payableOther liabilities

Sub-totalInterest and dividends receivedInterest paidIncome taxes paidNet cash provided by operating activities

Investing activities:Purchases of property, plant and equipmentProceeds from sales of property, plant and equipmentPurchases of investments in securities of a subsidiary and an affiliatePurchases of investments in securitiesProceeds from sales of investments in securitiesOthers, netNet cash used in investing activities

Financing activities:Repayment of long-term loansDecrease in short-term loansProceeds from issuance of common stock to minority interestsPurchases of treasury stockCash dividends paidNet cash used in financing activitiesEffect of exchange rate changes on cash and cash equivalentsIncrease (decrease) in cash and cash equivalentsCash and cash equivalents at beginning of year (Note 4)Cash and cash equivalents at end of year (Note 4)

See accompanying notes to consolidated financial statements.

¥ 2,475

3,257786

(8)(103)(14)

192(692)(10)82

952(69)

1435

(11)(31)

(4,595)683

(383)3,178

51324

6,21239

(196)(418)

5,637

(2,320)1,417

(238)(3)

545(173)(772)

(364)(1,911)

–(6)

(437)(2,718)

(7)2,1401,370

¥ 3,510

Millions of yen

2003

Thousands ofU.S. dollars

(Note1)2002 2003

¥ (1,139)

3,419296(121)(49)(38)

295(48)(50)

103–

(31)1,566

64(34)

–

6,7101,795

45(4,655)

27(274)

7,88147

(318)(336)

7,274

(2,630)389(62)(1)

50(364)

(2,618)

(3,064)(1,918)

16(1)

(239)(5,206)

117(433)

1,803¥ 1,370

$ 20,591

27,0976,539

(67)(857)(116)

1,597(5,757)

(83)682

7,920(574)

1,18942(92)

(257)

(38,228)5,682(3,186)

26,439424

2,69651,681

324(1,630)(3,478)

46,897

(19,301)11,788(1,980)

(25)4,534(1,439)(6,423)

(3,028)(15,899)

–(50)

(3,635) (22,612)

(58)17,80411,397

$ 29,201

CONSOLIDATED STATEMENTS OF CASH FLOWSTeijin Seiki Company LimitedYears ended March 31, 2003 and 2002

19

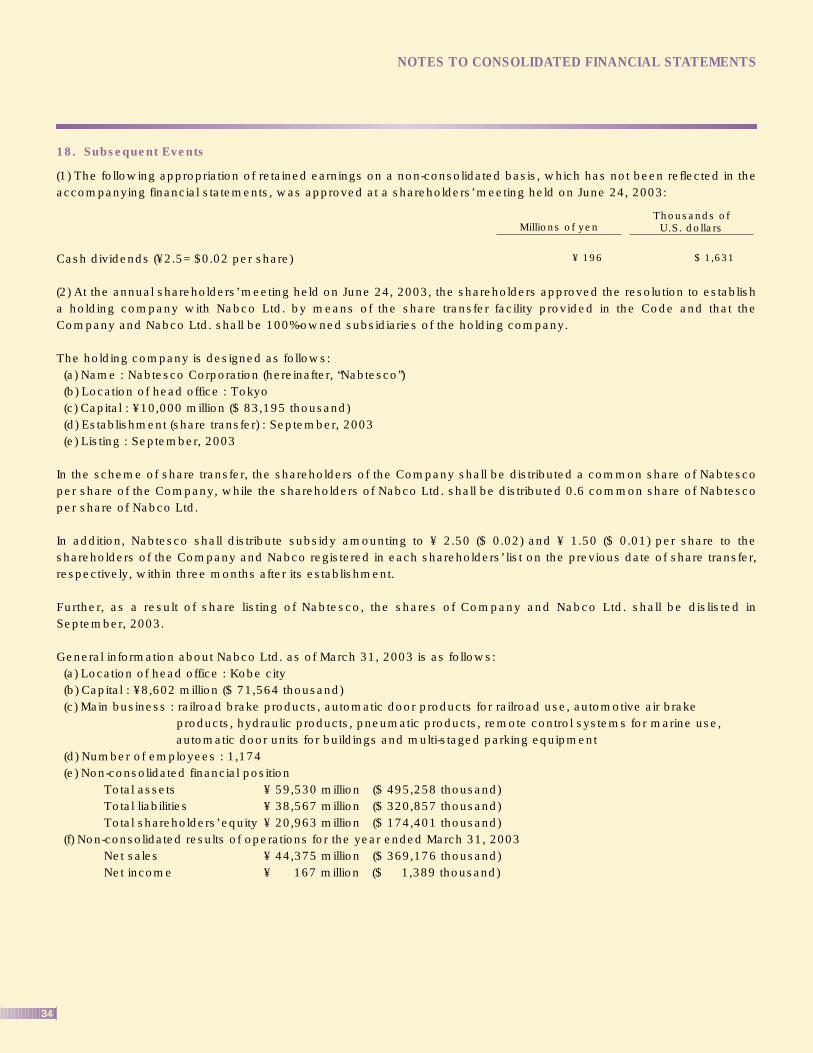

NOTES TO CONSOLIDATED FINANCIAL STATEMENTSTeijin Seiki Company LimitedYears ended March 31, 2003 and 2002

1. Description of Business and Basis of Presenting Consolidated Financial Statements

(1) Description of business

Teijin Seiki Company Limited (the “Company”), a Japanese

corporation, is a majority-owned subsidiary of Teijin Limited.

The main products of the Company and its consolidated

subsidiaries (the “Companies”) include precision equipment,

aircraft and oil hydraulic equipment, and textile and industrial

machinery.

The Company will change its name to “TS Corporation” on

October 1, 2003, based on approval of general shareholders’

meeting held on June 24, 2003.

(2) Basis of presenting consolidated financial statements

The Company and its consolidated domestic subsidiaries

maintain their official accounting records in Japanese yen in

accordance with the provisions set forth in the Japanese

Commercial Code and accounting principles and practices

generally accepted in Japan (“Japanese GAAP”). The accounts

of consolidated foreign subsidiaries are based on their

accounting records maintained in conformity with generally

accepted accounting principles and practices prevailing in the

respective countries of domicile. Certain accounting

principles and practices generally accepted in Japan are

different from International Accounting Standards and

standards in other countries in certain respects as to

application and disclosure requirements. Accordingly, the

accompanying financial statements are intended for use by

those who are informed about Japanese accounting

principles and practices.

The accompanying consolidated financial statements have

been restructured and translated into English (with some

expanded descriptions and the inclusion of statements of

shareholders’ equity) from the consolidated financial

statements of the Company prepared in accordance with

Japanese GAAP and filed with the appropriate Local Finance

Bureau of the Ministry of Finance as required by the

Securities and Exchange Law. Some supplementary

information included in the statutory Japanese language

consolidated financial statements, but not required for fair

presentation is not presented in the accompanying financial

statements.

The translation of the Japanese yen amounts into U.S. dollars

are included solely for the convenience of readers, using the

prevailing exchange rate at March 31, 2003, which was

¥120.20 to U.S.$1. The convenience translations should not

be construed as representations that the Japanese yen

amounts have been, could have been, or could in the future

be, converted into U.S. dollars at this or any other rate of

exchange.

2. Summary of Significant Accounting Policies

(1) Principles of consolidation

The accompanying consolidated financial statements include

the accounts of the Company and all subsidiaries which are

controlled through substantial ownership of majority voting

rights or existence of certain conditions. All significant inter-

company transactions, account balances and unrealized

profits are eliminated in consolidation.

In the elimination of investments in subsidiaries, the assets

and liabilities of the subsidiaries, including the portion

attributable to minority shareholders, are evaluated using the

fair value at the time the Company acquired control of the

respective subsidiaries.

The difference between the cost of investments in

subsidiaries and the equity in their net assets at the date of

acquisition is amortized over a period of five years on a

straight-line basis.

(2) Equity method

Investments in two affiliated companies, which include all of

20% to 50% owned companies are accounted for by the

equity method. The Company has no unconsolidated

subsidiary, nor affiliated company which is not accounted for

by the equity method.

(3) Cash and cash equivalents

For the purpose of the consolidated statements of cash

flows, cash and cash equivalents consist of cash on hand,

deposits with banks drawable on demand and short-term

investments which are readily convertible to cash subject to

an insignificant risk of changes in value and which were

purchased with an original maturity of three months or less.

See Note 4 as to reconciliation to cash and time deposits on

the balance sheets.

(4) Allowance for doubtful receivables

The allowance for doubtful receivables is provided in

amounts management considers sufficient to cover possible

losses on collection. The allowance is based on past

collection experience and management estimate of the

collectibility of individual receivables.

20

2. Summary of Significant Accounting Policies(continued)

(5) Securities

The companies are required to examine the intent of holding

each security and classify those securities as (a) securities

held for trading purposes (hereafter, “trading securities”), (b)

debt securities intended to be held to maturity (hereafter,

“held-to-maturity debt securities”), (c) equity securities issued

by subsidiaries and affiliated companies, and (d) for all other

securities that are not classified in any of the above

categories (hereafter, “available-for-sale securities”) The

Company had no trading securities and held-to-maturity debt

securities at March 31, 2003 and 2002.

As mentioned in (1) and (2), all equity securities issued by

subsidiaries and affiliated companies are consolidated or

accounted for using the equity method. Available-for-sale

securities with available fair market values are stated at fair

market value. Unrealized gains and losses on these securities

are reported, net of applicable income taxes, as a separate

component of shareholders’ equity. Realized gains and

losses on sale of such securities are computed using

moving-average cost method. Other securities with no

available fair market value are stated at moving-average cost.

If the market value of available-for-sale securities declines

significantly, such securities are stated at fair market value

and the difference between fair market value and the carrying

amount is recognized as loss in the period of the decline. For

equity securities with no available fair market value, if the net

asset value of the investee declines significantly, such

securities should be written down to net asset value with a

corresponding charge in the income statement in the period

of decline. In these cases, such fair market value or the net

asset value will be the carrying amount of the securities at the

beginning of the next year.

(6) Inventories

Inventories of the Company and its consolidated domestic

subsidiaries are stated at cost. The cost of finished goods

and work in process are principally determined by the

specific identification method and the cost of raw materials is

determined by either the moving average method or the

periodic weighted average method. Inventories of

consolidated foreign subsidiaries are principally stated at the

lower of cost, which is determined by the first-in, first-out

method, or market.

(7) Property, plant and equipment

Property, plant and equipment are stated at cost. The

Company and its consolidated domestic subsidiaries

calculate depreciation principally by the declining-balance

method over the estimated useful lives of the respective

assets, except for buildings acquired on or after April 1, 1998,

which are depreciated by the straight-line method over the

estimated useful lives of the respective assets. Machinery

and equipment, whose acquisition cost is ¥100 thousand or

more but less than ¥200 thousand, are depreciated over a

period of three years on a straight-line basis. The

consolidated foreign subsidiaries calculate depreciation

principally by the straight-line method over the estimated

useful lives of the respective assets.

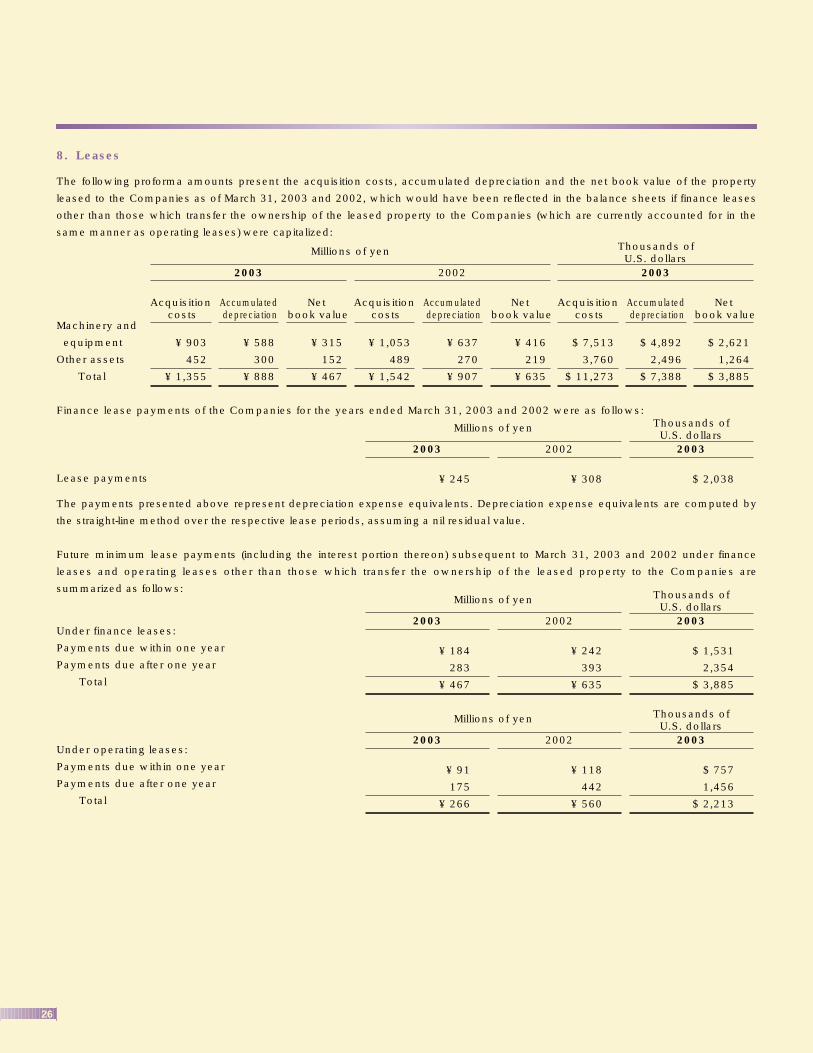

(8) Leases

Non-cancelable leases are accounted for in the same manner

as operating leases (whether such leases are classified as

operating or finance leases) except that lease agreements

which stipulate the transfer of ownership of the leased assets

to the lessee are accounted for as finance leases. Certain

consolidated foreign subsidiaries capitalize their assets

leased under finance lease contracts in accordance with local

accounting principles.

(9) Derivative financial instruments and hedging transactions

The Companies use forward foreign exchange contracts and

forward foreign currency options as derivative financial

instruments only for the purpose of mitigating future risks of

fluctuation of foreign currency exchange rates with respect to

foreign currency receivables and payables.

The basic policies for executing the derivative transactions

are managed by the Board of Directors of the Company.

Based on such policies, the finance departments of each

company establish the internal regulations which prescribe

the specified limits and procedures on the derivative

transactions. After execution, each finance department has

to report the certain information on derivative transactions to

the Board of Directors of the Company.

The following summarizes hedging derivative financial

instruments used by the Companies and items hedged:

Hedging instruments: Hedged items:

Forward foreign Foreign currency trade

exchange contracts receivables and trade payables

Forward foreign currency Foreign currency trade

option contracts receivables and trade payables

21

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

The Companies evaluate hedge effectiveness semi-annually

by comparing the cumulative changes in cash flows from or

the changes in fair value of hedged items and the

corresponding changes in the hedging derivative

instruments.

The companies are required to state derivative financial

instruments at fair value and to recognize changes in the fair

value as gains or losses unless derivative financial

instruments are used for hedging purposes.

If derivative financial instruments are used as hedges and

meet certain hedging criteria, the companies defer

recognition of gains or losses resulting from changes in fair

value of derivative financial instruments until the related

losses or gains on the hedged items are recognized.

However, in cases where forward foreign exchange

contracts or forward foreign currency option contracts are

used as hedges and meet certain hedging criteria, hedging

instruments and hedged items are accounted for in the

following manner:

1. If a forward foreign exchange contract or a forward foreign

currency option contract is executed to hedge an existing

foreign currency receivable or payable,

(a) the difference, if any, between the Japanese yen amount

of the hedged foreign currency receivable or payable

translated using the spot rate at the inception date of the

contract and the book value of the receivable or payable is

recognized in the income statement in the period which

includes the inception date, and

(b) the discount or premium on the contract (that is, the

difference between the Japanese yen amount of the contract

translated using the contracted forward rate and that

translated using the spot rate at the inception date of the

contract) is recognized over the term of the contract

2. If a forward foreign exchange contract or a forward foreign

currency option contract is executed to hedge a future

transaction denominated in a foreign currency, the future

transaction will be recorded using the contracted forward

rate, and no gains or losses on the forward foreign exchange

contract or the forward foreign currency options are

recognized.

(10) Amortization

Amortization of intangible assets is computed using the

straight-line method, principally over five years. Software is

included in intangible assets and amortized using the straight-

line method over the estimated useful lives (five years).

(11) Research and development costs

Research and development costs are charged to income

when incurred.

(12) Income taxes

The Companies recognize tax effects of timing differences

between the carrying amounts of assets and liabilities for

financial reporting purposes and the amounts for tax

reporting purpose. Income taxes comprise of corporation

tax, enterprise tax and prefectural and municipal inhabitants

taxes.

(13) Accrued employees’ bonuses

Accrued employees’ bonuses are accounted for at the

amount of the estimated bonuses to be paid and allocated to

the current fiscal year.

(14) Translation of foreign currencies

Monetary assets and liabilities denominated in foreign

currencies are translated into Japanese yen at the year-end

rates.

Financial statements of consolidated foreign subsidiaries are

translated into Japanese yen at the year-end rates, except

that shareholders’ equity accounts are translated at historical

rates and income statement items resulting from transactions

with the Company at the rates used by the Company. The

Company and its domestic subsidiaries report foreign

currency translation adjustments in the shareholders’ equity

and minority interests.

(15) Appropriation of retained earnings

Under the Commercial Code of Japan, the appropriation of

retained earnings with respect to a given financial period is

made by resolution of the shareholders at a general meeting

held subsequent to the close of such financial period. The

accounts for that period do not, therefore, reflect such

appropriations. (See Note 18).

(16) Employees’ severance and retirement benefits

The Company and its certain consolidated subsidiaries

provide two types of post-employment benefit plans,

unfunded lump-sum payment plans and funded non-

contributory pension plans, under which all eligible

employees are entitled to benefits based on the level of

wages and salaries at the time of retirement or termination,

length of service and certain other factors.

22

2. Summary of Significant Accounting Policies (continued)

(16) Employees’ severance and retirement benefits

(continued)

The Companies provided allowance for employees’

severance and retirement benefits at the end of years based

on the estimated amounts of projected benefit obligation,

actuarially calculated using certain assumptions and the fair

value of the plan assets at that dates.

The net transition obligation of ¥2,474 million (the excess of

the projected benefit obligation over the total of the fair value

of pension assets and the liabilities for severance and

retirement benefits) has been recognized in expenses in

equal amounts primarily over five years commencing with

the year ended March 31, 2001. Prior service costs are

recognized in expenses when incurred, and actuarial gains

and losses are recognized in expenses using the straight-line

method over the average of the estimated remaining service

lives commencing with the following period.

In addition, subject to the shareholders’ approval, directors

and corporate statutory auditors of the Company and its

consolidated domestic subsidiaries are customarily entitled

to lump-sum payments under unfunded retirement benefits

plans. The provision for retirement allowances for these

officers has been made at estimated amounts based on each

company’s internal rule.

(17) Treasury stock and statutory reserves

Effective April 1, 2002, the Company and consolidated

domestic subsidiaries adopted the new accounting standard

for treasury stock and reversal of statutory reserves

(Accounting Standards Board Statement No. 1, "Accounting

Standard for Treasury Stock and Reduction of Statutory

Reserves", issued by the Accounting Standards Board of

Japan on February 21, 2002).

The adoption of the new accounting standard had no impact

on the financial statements.

(18) Earning per share

Effective April 1, 2002, the Company adopted the new

accounting standard for earnings per share and related

guidance (Accounting Standards Board Statement No. 2,

"Accounting Standard for Earnings Per Share" and Financial

Standards Implementation Guidance No. 4, "Implementation

Guidance for Accounting Standard for Earnings Per Share",

issued by the Accounting Standards Board of Japan on

September 25, 2002).

The effect of adopting of the new standard and guidance is

disclosed in the Note 17.

(19) Reclassifications

Certain prior year amounts have been reclassified to conform

to the year 2003 presentation. These changes had no impact

on previously reported results of operations or shareholders’

equity.

5. Securities

The information on securities for the Companies at March 31, 2003 and 2002 is shown below.

The following tables summarize acquisition costs, book values and fair values of securities with available fair values as of March

31, 2003 and 2002:

(Available-for-sale securities)

(1) Securities with book values exceeding acquisition costs:

Equity securities

Bonds

Others

Total

Millions of yen

2003

Thousands ofU.S. dollars

2002 2003

$ 965

–

–

$ 965

DifferenceBook valueAcquisition

costDifferenceBook valueAcquisition

costDifferenceBook valueAcquisition

costType

$ 3,062

–

–

$ 3,062

$ 2,097

–

–

$ 2,097

¥ 220

–

–

¥ 220

¥ 1,149

–

–

¥ 1,149

¥ 929

–

–

¥ 929

¥ 116

–

–

¥ 116

¥ 368

–

–

¥ 368

¥ 252

–

–

¥ 252

23

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

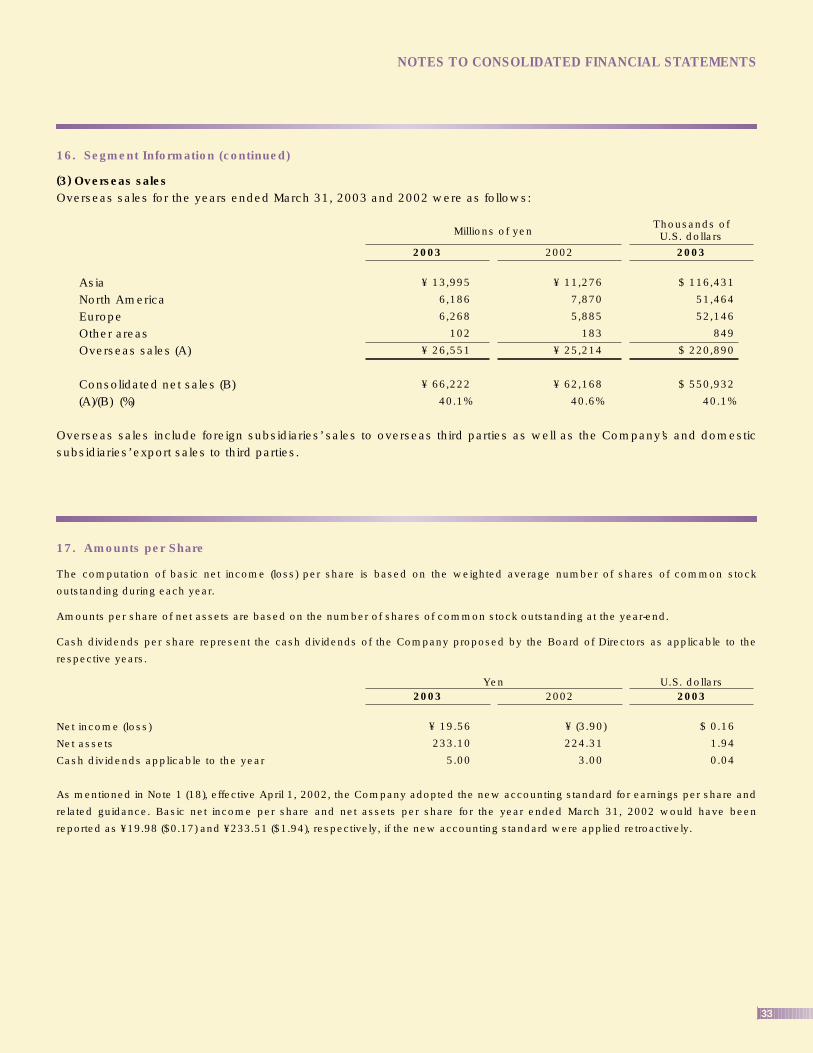

3. Effect of Bank Holiday

As financial institutions in Japan were closed on March 31, 2002, amounts that would normally be settled on March 31 were

collected or paid on the following business day, April 1. The effect of the settlements on April 1 and April 2 instead of March 31,

2002 included the following:

Trade notes receivable

Notes payable - trade

Note payable - other

4. Cash and Cash Equivalents

Reconciliation of cash and time deposits shown in the consolidated balance sheets and cash and cash equivalents shown in the

consolidated statements of cash flows as of March 31, 2003 and 2002 are as follows:

Cash and time deposits

Deposits paid

Total

¥ 2,754

756

¥ 3,510

Millions of yen

2003

Thousands ofU.S. dollars

2002 2003

¥ 1,357

13

¥ 1,370

$ 22,912

6,289

$ 29,201

¥ 151

110

1

Millions of yen

2002

5. Securities (continued)

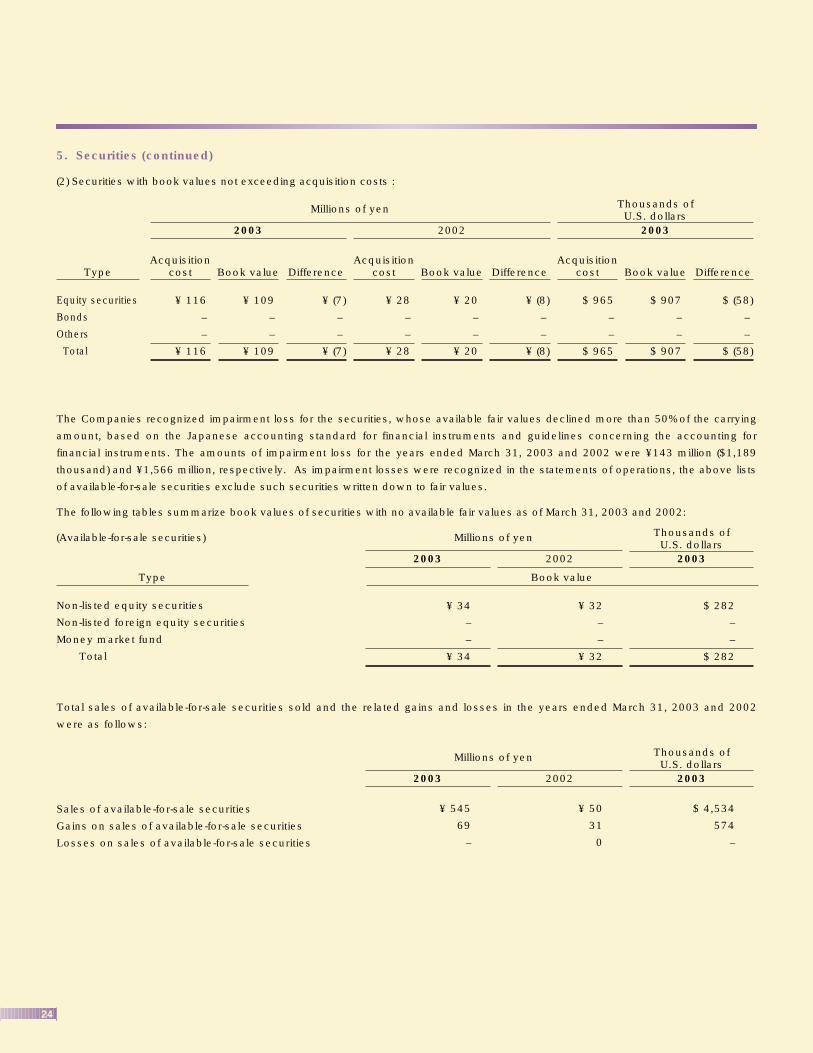

(2) Securities with book values not exceeding acquisition costs :

Equity securities

Bonds

Others

Total

The Companies recognized impairment loss for the securities, whose available fair values declined more than 50% of the carrying

amount, based on the Japanese accounting standard for financial instruments and guidelines concerning the accounting for

financial instruments. The amounts of impairment loss for the years ended March 31, 2003 and 2002 were ¥143 million ($1,189

thousand) and ¥1,566 million, respectively. As impairment losses were recognized in the statements of operations, the above lists

of available-for-sale securities exclude such securities written down to fair values.

The following tables summarize book values of securities with no available fair values as of March 31, 2003 and 2002:

(Available-for-sale securities)

Non-listed equity securities

Non-listed foreign equity securities

Money market fund

Total

Total sales of available-for-sale securities sold and the related gains and losses in the years ended March 31, 2003 and 2002

were as follows:

Sales of available-for-sale securities

Gains on sales of available-for-sale securities

Losses on sales of available-for-sale securities

24

¥ 545

69

–

Millions of yen

2003

Thousands ofU.S. dollars

2002 2003

¥ 50

31

0

$ 4,534

574

–

¥ 34

–

–

¥ 34

Millions of yen