Annual Report final - United Nations Office on Drugs … · MNSL Maldives National Shipping Limited...

72

s d s a c ANNUAL REPORT 2002 Maldives Monetary Authority Maldives Monetary Authority Maldives Monetary Authority Maldives Monetary Authority Maldives Monetary Authority

Transcript of Annual Report final - United Nations Office on Drugs … · MNSL Maldives National Shipping Limited...

1

MMA ANNUAL REPORT 2002

s d s ac

ANNUAL REPORT

2002

Maldives Monetary AuthorityMaldives Monetary AuthorityMaldives Monetary AuthorityMaldives Monetary AuthorityMaldives Monetary Authority

2

3

MMA ANNUAL REPORT 2002

MALDIVES MONETMALDIVES MONETMALDIVES MONETMALDIVES MONETMALDIVES MONETARARARARARY AUTHORITYY AUTHORITYY AUTHORITYY AUTHORITYY AUTHORITYMalé, Republic of Maldives

Dear Sir,

In accordance with Article 35 (2) of Maldives Monetary Authority Act (1981), I have the honour to submit theAnnual Report of the Maldives Monetary Authority for 2002, which includes a copy of the Financial State-ments for the year ended 31 December 2002, audited by the Government Auditors.

Yours sincerely

Mohamed JaleelVice Governor

H.E. Maumoon Abdul Gayoom,President of the Republic of Maldives,Office of the President,Malé.

Letter of Transmittal

4

Letter of TransmittalLetter of TransmittalLetter of TransmittalLetter of TransmittalLetter of Transmittal ............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 33333

List of AcronymsList of AcronymsList of AcronymsList of AcronymsList of Acronyms ............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................. 66666

An Overview of the Maldives Monetary AuthorityAn Overview of the Maldives Monetary AuthorityAn Overview of the Maldives Monetary AuthorityAn Overview of the Maldives Monetary AuthorityAn Overview of the Maldives Monetary Authority .......................................................................................................................................................................................................................................................................................................................................... 77777

Organisational Chart of Maldives Monetary Authority............................................................... 8Organisational Chart of Maldives Monetary Authority............................................................... 8Organisational Chart of Maldives Monetary Authority............................................................... 8Organisational Chart of Maldives Monetary Authority............................................................... 8Organisational Chart of Maldives Monetary Authority............................................................... 8

Directors and Senior OfficialsDirectors and Senior OfficialsDirectors and Senior OfficialsDirectors and Senior OfficialsDirectors and Senior Officials ............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 99999

PrefacePrefacePrefacePrefacePreface .................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................. 1 01 01 01 01 0

Economic ReviewEconomic ReviewEconomic ReviewEconomic ReviewEconomic Review ........................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................ 1 11 11 11 11 1

Domestic Economic ReviewDomestic Economic ReviewDomestic Economic ReviewDomestic Economic ReviewDomestic Economic Review ................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................ 1 31 31 31 31 3

1. Overview1. Overview1. Overview1. Overview1. Overview ................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................ 1 31 31 31 31 3

2. Production, Prices and Employment2. Production, Prices and Employment2. Production, Prices and Employment2. Production, Prices and Employment2. Production, Prices and Employment ..................................................................................................................................................................................................................................................................................................................................... 1 51 51 51 51 5

2.1 Tourism ................................................................................................................. 15

2.2 Fisheries ................................................................................................................ 17

2.3 Agriculture ............................................................................................................ 18

2.4 Distribution .......................................................................................................... 18

2.5 Construction. ........................................................................................................ 19

2.6 Inflation ................................................................................................................ 19

2.7 Employment ......................................................................................................... 19

3. Public Finance3. Public Finance3. Public Finance3. Public Finance3. Public Finance ................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 2 02 02 02 02 0

4. Financial Sector4. Financial Sector4. Financial Sector4. Financial Sector4. Financial Sector ......................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 2 12 12 12 12 1

4.1 Banking System and Monetary Policy ................................................................ 21

4.2 Money and Credit Developments in the Banking Sector .................................. 22

4.2.1 Operations of the Commercial Banks ..................................................... 23

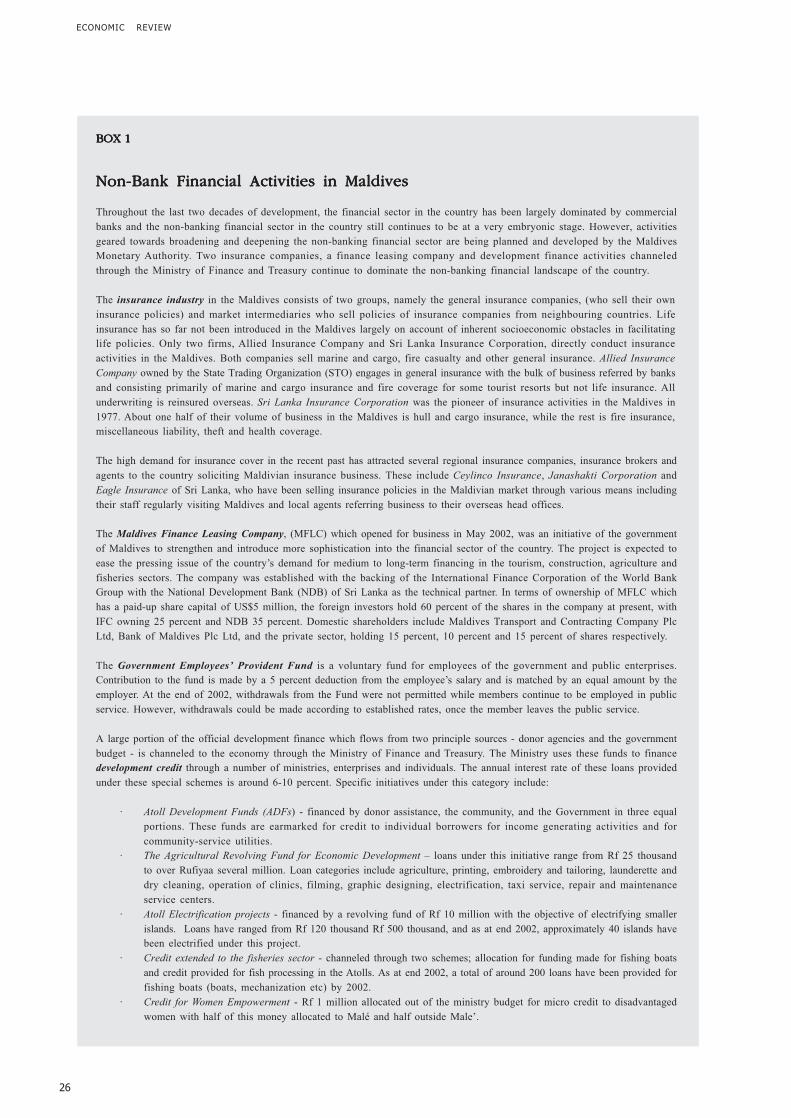

4.3 Non-Bank Financial Activities .............................................................................. 25

4.4 Capital Market. ....................................................................................................... 25

5. Balance of Payments5. Balance of Payments5. Balance of Payments5. Balance of Payments5. Balance of Payments ................................................................................................................................................................................................................................................................................................................................................................................................................................................................................. 2 72 72 72 72 7

5.1 Current Account ................................................................................................... 27

5.2 Merchandise Trade .............................................................................................. 27

5.3 Services and Transfers ........................................................................................ 28

5.4 Capital Account ................................................................................................... 29

5.5 Overall Balance of Payments and International Reserves ................................ 29

6. Interest Rate and Exchange Rate Developments6. Interest Rate and Exchange Rate Developments6. Interest Rate and Exchange Rate Developments6. Interest Rate and Exchange Rate Developments6. Interest Rate and Exchange Rate Developments ........................................................................................................................................................................................................................................... 3 03 03 03 03 0

7. External Debt7. External Debt7. External Debt7. External Debt7. External Debt ............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................. 3 03 03 03 03 0

International Economic ReviewInternational Economic ReviewInternational Economic ReviewInternational Economic ReviewInternational Economic Review ............................................................................................................................................................................................................................................................................................................................................................................................................................................................. 3 23 23 23 23 2

Page

COContentsContentsContentsContentsContents

5

MMA ANNUAL REPORT 2002

Administration and OperationsAdministration and OperationsAdministration and OperationsAdministration and OperationsAdministration and Operations ................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................ 3 53 53 53 53 5

Board Meetings ................................................................................................................ 37

Key Operational Developments .............................................................................................. 37

Human Resource Management and Development ............................................................... 38

Technical Assistance ............................................................................................................... 41

Visitors ................................................................................................................ 42

Financial StatementsFinancial StatementsFinancial StatementsFinancial StatementsFinancial Statements ............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 4 34 34 34 34 3

Audit Report ............................................................................................................................. 45

Income Statement .................................................................................................................... 46

Balance Sheet. ......................................................................................................................... 47

Notes to the Financial Statements ........................................................................................... 49

AppendicesAppendicesAppendicesAppendicesAppendices .......................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 5 15 15 15 15 1

Appendix 1Appendix 1Appendix 1Appendix 1Appendix 1 List of Statistical Tables ..................................................................................... 53

Statistical Tables ................................................................................................. 54

Appendix 2Appendix 2Appendix 2Appendix 2Appendix 2 Commercial Banks Operating in the Maldives ................................................ 71

Monetary Measures and Prudential Regulations in Effect During 2002 ........ 71

Char t sChar t sChar t sChar t sChar t s

Chart 1 GDP by major sectors, 1996 - 2002 ...................................................... 13

Chart 2 Tourist Bednights, 1996 - 2002. ............................................................. 15

Chart 3 Tourist Arrivals by Nationality, 1996 - 2002 ......................................... 16

Chart 4 Fish Landings and Exports, 1996 - 2002 ............................................... 17

Chart 5 Inflation, 1996 - 2002 ............................................................................. 19

Chart 6 Expatriate Employment by Industry, 2002. .......................................... 20

Chart 7 Government Revenue and Grants, 1996 - 2002 ................................... 21

Chart 8 Government Expenditure, 1996 - 2002 ................................................. 21

Chart 9 Monetary Indicators, 1996 - 2002 .......................................................... 22

Chart 10 Domestic Credit, 1996 - 2002 ................................................................. 22

Chart 11 Net Foreign Assets, 1996 - 2002 ............................................................ 23

Chart 12 Credit by Major Economic Sectors, 2002 ............................................. 24

Chart 13 Commercial Banks’ Deposits by Type, 1996 - 2002 ............................ 24

Chart 14 Total Value of Shares Traded by Companies, Apr - Dec 2002. .......... 25

Chart 15 International Trade, 1996 - 2002 ........................................................... 27

Chart 16 Composition of Imports, 2000 - 2002. .................................................. 28

Chart 17 Balance of Payments as a Percentage of GDP, 1996 - 2002............... 29

Chart 18 Change in Rufiyaa Exchange Rate against Major Foreign

Currencies 1996 - 2002. .......................................................................... 30

Chart 19 External Debt, 1996 - 2002 .................................................................... 31

Text TablesText TablesText TablesText TablesText Tables

Table 1 Key Economic Indicators, 1999 - 2002 ................................................. 14

Table 2 Fish Landings and Exports, 1999 - 2002 ............................................... 17

Table 3 Summary of Government Finance, 1999 - 2002 .................................. 20

Table 4 Monetary Aggregates, 2001 - 2002 ........................................................ 23

Table 5 International Economic Indicators, 1999 - 2002. ................................. 32

BoxesBoxesBoxesBoxesBoxes

Box 1 Non-Bank Financial Activities in the Maldives ...................................... 26

Page

6

C.I.F Cost, Insurance and Freight

CBSS Credit and Bank Supervision Section

CD Certificate of Deposit

CPI Consumer Price Index

DER Department of External Resources

EEZ Exclusive Economic Zone (75-200 miles from the coast)

ERSD Economic Research and Statistics Division

F.O.B Free On Board

FES Foreign Exchange Section

GDP Gross Domestic Product

HSBC Hongkong and Shanghai Banking Corporation

IMF International Monetary Fund

LIBOR London Interbank Overnight Rate

M1 Narrow Money Supply

M2 Broad Money Supply (Total Liquidity)

MCS Maldives Customs Service

MIFCO Maldives Industrial Fisheries Company Ltd.

MMA Maldives Monetary Authority

MNSL Maldives National Shipping Limited

MOFAMR Ministry of Fisheries, Agriculture and Marine Resources

MOFT Ministry of Finance and Treasury

MOT Ministry of Tourism

MPND Ministry of Planning and National Development

MRR Minimum Reserve Requirement

MT Metric Tonne

NYPR New York Prime Rate

PLC Public Limited Company

PNFE Public Non-Financial Enterprises

PPR Personnel and Public Relations

Rf Rufiyaa

SAARC South Asian Association for Regional Cooperation

SDR Special Drawing Rights

STO State Trading Organisation plc.

TDC Total Domestic Credit

TDS Total Debt Service

XGS Exports of Goods and Services

List of AcronymsList of AcronymsList of AcronymsList of AcronymsList of Acronyms

7

MMA ANNUAL REPORT 2002

The Maldives Monetary Authority (MMA) was

established on 1st July 1981 under the Maldives

Monetary Authority Act (1981) to act as the central

bank of the Maldives. The principal purposes of the

Authority as stipulated in the 1981 Act are: to issue

currency and regulate the availability and international

value of the Maldivian rufiyaa; to provide advisory

services to the Government on banking and monetary

matters; to supervise and regulate banking so as to

promote a sound financial structure; and to promote

in the country and outside the country the stability of

Maldivian currency, and foster financial conditions

conducive to the orderly and balanced economic

development of the Maldives.

Board of DirectorsBoard of DirectorsBoard of DirectorsBoard of DirectorsBoard of Directors

The highest policy making body of the MMA is the

Board of Directors. The Board consists of the Minister

of Finance as ex-officio Governor, the senior most

official of the Ministry of Finance as ex-officio Vice

Governor, three members from amongst the cabinet,

and two members representing the private sector

appointed by the President of the Republic.

The OrganisationThe OrganisationThe OrganisationThe OrganisationThe Organisation

The Maldives Monetary Authority is structured in three

Divisions: the Operations Division, the Economic

Research and Statistics Division and the General

Division.

The Operations DivisionOperations DivisionOperations DivisionOperations DivisionOperations Division consists of the Foreign

Exchange, Banking, Currency, Credit and Bank

Supervision, Capital Market Development, Accounts,

Non-Bank Financial Institutions Supervision and Public

Debt Sections. The Foreign Exchange Section deals

with all matters relating to foreign currency transactions

by the MMA and the management of the country's

foreign reserves. The Banking Section, in addition to

maintaining the accounts of government offices and

commercial banks, acts as a clearinghouse for the

commercial banks operating in the Maldives. The

Currency Section is responsible for printing and minting

of currency notes and coins, issuing commemorative

coins, maintaining the records of currency in

circulation and in stock and releasing new notes and

coins into circulation. The Accounts Section maintains

the General Ledger and prepares management and

financial accounts of the Maldives Monetary Authority.

A An Overview of the Maldives Monetary AuthorityAn Overview of the Maldives Monetary AuthorityAn Overview of the Maldives Monetary AuthorityAn Overview of the Maldives Monetary AuthorityAn Overview of the Maldives Monetary Authority

The duties of the Credit and Bank Supervision Section

include issuing licences for commercial banks to

operate in the Maldives, monitoring activities of

commercial banks to ensure their compliance to the

rules and regulations of the MMA, and assessing the

financial performance of commercial banks. The

Capital Market Development Section is responsible

for establishing and developing a capital market in

the Maldives, including licensing and supervising

capital market institutions to protect the interests of

investors. The Non-Bank Financial Institutions

Supervision Section is responsible for licensing,

regulating and supervising insurance companies,

leasing companies and other non-bank financial

institutions to ensure their smooth functioning. The

Public Debt Section, when it becomes operational,

would be responsible for securitising, monitoring and

managing government debt.

The Economic Research and Statistics DivisionEconomic Research and Statistics DivisionEconomic Research and Statistics DivisionEconomic Research and Statistics DivisionEconomic Research and Statistics Division

(ERSD)(ERSD)(ERSD)(ERSD)(ERSD), consists of the Statistics Section and the

Research Section. The Statistics Section gathers

economic and financial data from relevant sources

within the MMA and outside, and maintains a database

of such information. The Research section undertakes

research and analysis broadly on the areas of

production, prices and labour force, money and

banking, government budget and the balance of

payments. ERSD also undertakes the publication of

MMA's Annual Report and the Quarterly Economic

Bulletin, and in addition, operates as the focal point

for the Maldives' interactions with the International

Monetary Fund.

The General DivisionGeneral DivisionGeneral DivisionGeneral DivisionGeneral Division consists of the Personnel and

Public Relations Section, the Information Technology

Section and the Expenditure Section. The Personnel

and Public Relations Section deals with matters relating

to employment and training, the affairs of the Board

of Directors, official meetings, conferences, travel, and

various administrative reports. In addition, this section

is responsible for co-ordinating all aspects related to

the media. The Information Technology (IT) Section

is responsible for the management of the computer

network and databases, maintenance of the MMA

website and other IT needs of the Authority. The

Expenditure Section deals with the MMA budget,

finance, and all aspects of general maintenance of

assets and premises.

8

Organisational Chart

BOARD OF DIRECTORS

Governor

Vice Governor

General Manager

Executive Director

Assistant General Manager

Operations Division Economic Research &

Statistics Division

General Division

Banking Section Accounts Section

Currency Section

Capital Market

Development Section

Credit & Bank

Supervision Section

Personnel & Public

Relations Section

Expenditure Section

Research Section

Statistics Section

Non-bank FinancialInstitutionsSupervision Section

InformationTechnology Section

Foreign Exchange

Section

Public Debt Section

Publications and LibraryPublications and LibraryPublications and LibraryPublications and LibraryPublications and Library

With a view to highlighting the major issues relating

to the development of the country and the affairs of

the organisation, the MMA regularly publishes this

Annual Report, and a Quarterly Economic Bulletin,

which covers the macroeconomic developments

during the quarter. The MMA has a small library, which

contains a collection of reports, periodicals, annual

reports and statistical publications including those of

international organisations such as the International

Monetary Fund and foreign central banks. The library

also has foreign and local newspapers, and books

related to economics, finance and development.

PP

9

MMA ANNUAL REPORT 2002

Board of DirectorsBoard of DirectorsBoard of DirectorsBoard of DirectorsBoard of Directors

H.E. Maumoon Abdul Gayoom ............................... Governor, Minister of Finance and Treasury

(Board Chairman)

Hon. Mohamed Jaleel .............................................. Vice Governor, Minister of State for Finance and Treasury

Hon. Fathulla Jameel ................................................ Minister of Foreign Affairs

Hon. Ismail Shafeeu ................................................ Minister of Education

Hon. Hassan Sobir ................................................... Minister of Tourism

Mr. Mohamed Umar Maniku ................................... Chairman, Universal Enterprises Pvt. Ltd.

(Private Sector member)

Mr. Mohamed Solih ................................................. Chairman, DAMAS Company Pvt. Ltd.

(Private Sector member)

Board Secretary

Ms. Khadeeja Hassan ............................................... Executive Director of MMA

Senior OfficialsSenior OfficialsSenior OfficialsSenior OfficialsSenior Officials

H.E. Maumoon Abdul Gayoom ............................... Governor

Hon. Mohamed Jaleel .............................................. Vice Governor

Ms. Khadeeja Hassan ............................................... Executive Director

Mr. Abdul Ghafoor Abdul Latheef ........................... General Manager

Mr. Ibrahim Naeem .................................................. Assistant General Manager

Directors and Senior Officials as at 31 December 2002

10

This report covers developments in the domestic economy during 2002 and a brief overview of events in theglobal economy during the year. It also presents the financial statements of the MMA as at 31 December 2002 asrequired by the MMA Act (1981), and the key administrative and operational developments in MMA during theyear. All domestic analyses are based on information relating to the year 2002, received from relevant governmentauthorities, public enterprises, commercial banks operating in the country and other private sector sources, as at30th June 2003. The section on international developments is based on information obtained from publicationsof the International Monetary Fund (IMF), and other international sources as at 31 October 2003. The viewsexpressed in this Report, however, are those of this Authority and do not necessarily represent those of thesource of data. We thank all those who have contributed to the publication of this report including the provisionof the information contained here in.

Preface

11

MMA ANNUAL REPORT 2002

T h e

Th e

s d f s d f d s f s a f

EECONOMIC REVIEW

2002

12

13

MMA ANNUAL REPORT 2002

1. Overview1. Overview1. Overview1. Overview1. Overview

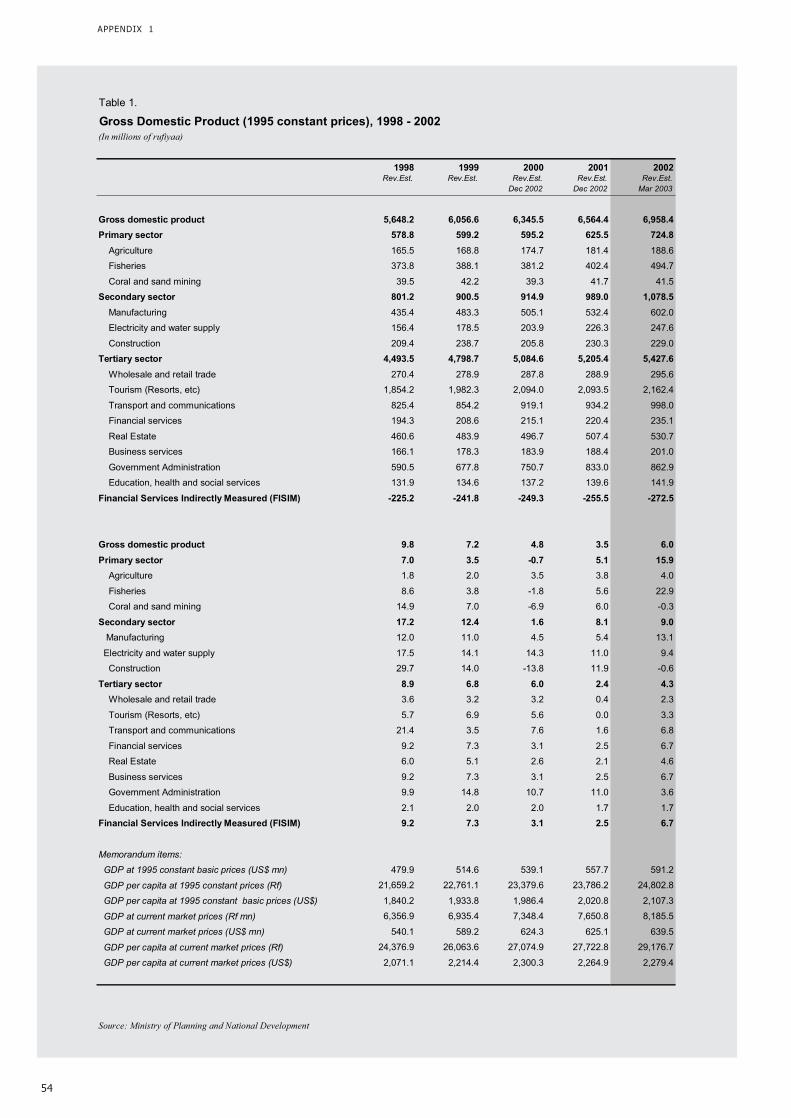

According to GDP estimates released by the MPND

in March 2003, real economic growtheconomic growtheconomic growtheconomic growtheconomic growth accelerated to

6.0 percent in 2002 from 3.5 percent in 2001. Post

‘September 11' recovery in tourism commenced

around mid-2002, which together with the strong

pickup witnessed in the fisheries sector during the

year resulted in the higher growth for 2002.

The tourism sectortourism sectortourism sectortourism sectortourism sector, which contributed around 31

percent to the country's GDP in 2002, witnessed

continued decline in tourist arrivals through the first

half of 2002. However, the sector recovered in the

latter half of the year, and strong growth was registered

in the last few months, resulting in an annual growth

of 5 percent in tourist arrivals and 3 percent in

bednights. In 2001 both arrivals and bednights

recorded annual declines. Meanwhile, average

duration of stay once again fell slightly in 2002, while

the average occupancy rate increased to 69 percent,

from 66 percent in 2001. Average occupancy rate

registered over 74 percent in the period 1996-1999,

but had fallen to 68 percent in 2000 following the

large increase in bed capacity between 1996-2000.

Average number of beds in operation was less in

2002 than in the previous year, mainly as a result of

renovation work undertaken in quite a number of

resorts, at various times during the year.

The fisheries sectorfisheries sectorfisheries sectorfisheries sectorfisheries sector was buoyant during the year,

accounting for 7 percent of total GDP and witnessing

an annual growth of 23 percent. This followed a 6

percent growth in 2001 and a decline of 2 percent in

2000. During the year, fish landings (excluding EEZ)

increased notably over 2001 while total fish exports

(excluding live tropical fish) increased as well.

According to MIFCO data, unit prices received on

exports of canned and frozen tuna were better during

the year than in the previous year. Liberalisation of

the tuna industry began in 2001 with the awarding of

licences in the first zone to two private sector parties,

which provided them with rights to process and export

tuna bought from domestic fisherman. These two

parties commenced their operations in 2002, and the

first exports resulting from the liberalisation were

recorded in December of the year, when each party

shipped two consignments of frozen tuna.

As for domestic prices, the annual inflation rateinflation rateinflation rateinflation rateinflation rate, as

measured by the percentage change in the Consumer

Price Index, continued to remain below 1 percent for

the third consecutive year, registering 0.9 percent

during 2002.

In terms of employmentemploymentemploymentemploymentemployment, at the end of 2002, total

public sector employment stood at 26,363 which was

about 1 percent lower than 2001. In the private sector,

demand continued to be high in the labour market.

While detailed employment statistics are not available

on an annual basis, expatriate employment data

indicated that the average number of foreign workers

in the country during the year increased by about 1

percent.

According to provisional estimates for the year

published in December 2002, the overall fiscalfiscalfiscalfiscalfiscal

positionpositionpositionpositionposition was less favourable in 2002 than the actual

outcome of 2001. The overall deficit showed a 64

percent increase during the year, from the 2001 actual

outcome, depicting the recent trend of higher growth

in expenditure (including net lending) compared to

the expansion in revenue (including grants). In

particular, the large overall deficit in 2002 was the

result of large investment expenditure and lower

than anticipated revenue due to the general weakness

in the economy. Financing of the deficit was largely

from foreign sources; as a result of which domestic

financing declined quite significantly.

Domestic Economic ReviewDomestic Economic ReviewDomestic Economic ReviewDomestic Economic ReviewDomestic Economic Review

0

1000

2000

3000

4000

5000

6000

7000

1996 1997 1998 1999 2000 2001 2002

Tourism Transport and communicat ions

Fisheries M anufacturing & elect ricityGovernment Administration Others

In m illions of ruf iy aa

Chart 1.

GD P B Y M A JOR SEC T OR S, 1996-2002

Sour ce: Ministry of Planning and National Development

14

ECONOMIC REVIEW

Money and credit Money and credit Money and credit Money and credit Money and credit developments during 2002 featured

accelerated growth in net foreign assets, a slight

deceleration in growth of domestic credit, which

resulted in a sharp rise in the rate of growth of broad

money. After falling for the past three years, net foreign

assets of the banking system grew strongly in 2002

mainly due to strong growth in the net foreign assets

of MMA. Meanwhile, total domestic credit growth

decelerated with growth in credit extended to the

private sector slowing significantly. In 2001, a steep

rise was seen in this variable following the removal

(in July 2001) of the credit ceiling that was previously

imposed on banks by the MMA. In terms of sectoral

allocation of private sector credit, the tourism sector

accounted for over half of the credit outstanding at

the end of the year, while the commerce sector

accounted for almost a quarter. Growth in net credit

to the government also continued to decelerate, while

credit to public enterprises grew during the year, after

remaining at around the same level in 2001. As a

result, total liquidity (broad money, M2) increased by

19 percent at the end of the year. Quasi money

comprising of mainly foreign currency deposits rose

more steeply than narrow money (consisting mainly

of demand deposits and currency in circulation)

resulting in an increase in the dollarisation ratio (ratio

of foreign currency deposits to broad money) from

45 percent in 2001 to 47 percent in 2002.

According to estimates of May 2003, the Maldives'

balance of paymentsbalance of paymentsbalance of paymentsbalance of paymentsbalance of payments improved significantly during

2002. The merchandise trade deficit improved by

around 11 percent, while on the services account,

receipts were lower than 2001 by around 0.4 percent,

largely owing to the decline in receipts from tourism.

The transfers account also deteriorated during the

year, with a sharp decline in inflow of official grant

aid together with a slight increase in the remittances

made by expatriate workers. The financing of the

current account was largely through official medium

and long-term flows, which were almost five times

more than the flows recorded during 2001, while

private capital inflows also increased. Consequently,

the overall balance of payments strengthened

significantly during the year, recording an inflow of

around US$39.8 million, as opposed to the net outflow

of US$21.4 million registered in 2001. This contributed

to the positive developments witnessed in the grossgrossgrossgrossgross

international reservesinternational reservesinternational reservesinternational reservesinternational reserves which grew by US$40.2

million during the year to reach a total of US$134.5

million by the end of the year. In terms of past 12

months' merchandise import cover, this was equivalent

to 4.1 months of imports at the end of December

2002, as opposed to 2.9 months at the end of

December 2001 and 3.8 months at the end of

December 2000. The exchange rateexchange rateexchange rateexchange rateexchange rate of the Rufiyaa

vis-à-vis the US dollar remained at the mid rate of

Rf12.80 per US dollar through out the year, with a

spread of 10 laaris between the buying and selling

rates.

Statistics on the external indebtednessexternal indebtednessexternal indebtednessexternal indebtednessexternal indebtedness of the

economy are limited to medium and long-term

government and government guaranteed borrowings

Table 1.

KEY ECONOMIC INDICATORS, 1999 - 2002

1999 2000 2001 2002

Gross Domestic Product

GDP (1995 constant prices) Rf mn 1/ 6,056.6 6,345.5 6,564.4 6,958.4

% change in GDP 7.2 4.8 3.5 6.0

Consumer Price Index

% change in CPI 3.0 (1.2) 0.7 0.9

Tourism

Tourist arrivals ('000) 429.7 467.2 461.0 484.7

Bed night capacity ('000) 2/ 5,348.5 5,787.8 6,015.1 5,886.9

Capacity utilization (%) 69.7 68.2 65.6 69.0

Fish Production

Landings('000 MTs) excl. EEZ 123.3 115.4 125.0 160.2

Total fish exports ('000 MTs) 3/ 37.6 28.3 29.7 44.6

Total fish exports (US$ mn) 3/ 34.4 34.0 35.8 49.2

Government Finance (Rf mn) 4/

Total revenue and grants 2,225.3 2,372.7 2,522.6 2,720.4

Expenditure and net lending 2,506.4 2,694.2 2,885.9 3,316.0

Overall balance (+/-) (281.1) (321.5) (363.3) (595.6)

Money and Banking (Rf mn)

Net foreign assets 1,405.4 1,312.2 1,153.0 1,662.9

Domestic credit 2,259.3 2,586.8 3,089.9 3,445.7

Net credit to govt. 760.2 995.0 1,078.6 1,133.9

Net credit to public enterprises 196.3 184.7 184.0 211.0

Net credit to private sector 1,302.8 1,407.1 1,827.2 2,100.8

Narow Money (M1) 1,585.2 1,760.4 1,655.9 1,886.7

Total liquidity (M2) 2,929.8 3,049.8 3,324.7 3,966.4

Quasi money 1,344.6 1,289.4 1,668.8 2,079.7

Balance of Payments 5/

Exports (f.o.b) 91.5 108.7 110.2 133.6

Imports (f.o.b) (353.9) (342.0) (346.3) (344.7)

Services (net) 203.6 208.8 206.4 207.7

Non-monetary capital (net) 71.7 43.5 35.9 83.8

Overall balance (7.2) (7.9) (21.4) 39.8

Gross International Reserves (US$ mn) 6/ 128.5 124.1 94.3 134.5

External Reserves

in months of Imports 3.8 3.8 2.9 4.1

Exchange Rate

Rufiyaa / Euro (End of Period) 11.69 10.35 11.03 12.66

Rufiyaa / US$ (End of Period) 11.77 11.77 12.80 12.80

1/ Figures for 1999 -2000 are revised estimates of 10th November 2002, figures for 2001 are revised

estimates of 16th December 2002 and figure for 2002 are revised estimate of March 2003

2/ Bed capacity x number of days per month.

3/ Excluding live tropical fish.

4/ Figures for 2002 are provisional estimates.

5/ Figures for 2001 and 2002 are revised estimates.

6/ Foreign Assets of MMA

Source: MPND, MOT, MOFAMR, MOFT, Maldives Customs Service & MMA.

15

MMA ANNUAL REPORT 2002

and the external debt of the banking sector. Total

recorded external debt stockexternal debt stockexternal debt stockexternal debt stockexternal debt stock stood at US$257.1

million at the end of 2002, with medium and long-

term public debt stock constituting 86 percent, and

foreign liabilities of the commercial banks the rest.

The public sector external debt stock comprises of

loans received from bilateral and multilateral sources

(largely on concessional terms), loans taken from

financial markets, as well as of suppliers' credits. At

the end of 2002, multilateral loans accounted for 63

percent of total medium and long-term external debt

stock, while suppliers' credits accounted for 21

percent, bilateral loans for 11 percent and loans from

financial markets for 4 percent. During 2002,

disbursements of medium and long-term foreign debt

to the public sector stood at US$43.5 million, while

debt service totalled US$23.5 million, which is the

equivalent of around 5 percent of Maldives' exports

of goods and non-factor services.

2. Production, Prices and2. Production, Prices and2. Production, Prices and2. Production, Prices and2. Production, Prices and Employment Employment Employment Employment Employment

2.1 Tourism2.1 Tourism2.1 Tourism2.1 Tourism2.1 Tourism

Tourism activities, which were started very modestly

in the 1970s by a couple of small local entrepreneurs,

have grown rapidly during the years. At present the

tourism sector is very dynamic and plays a vital role

in the economic development of the country. The

sectoral contribution of tourism has averaged at

around 32 percent of GDP in the past 5 years in

addition to directly accounting for about 30 percent

of the government's total revenue and approximately

66 percent of foreign exchange earnings of the

country. Tourism developments have also stimulated

growth in various other sectors of the economy such

as transport, commerce, construction and

communication.

At the end of 2002 there were 87 tourist resortstourist resortstourist resortstourist resortstourist resorts in

operation in the county with 16,400 beds. Of these,

43 resorts were located in Kaafu Atoll and 26 in Alifu

Atoll, and these two atolls together had 77 percent of

the total beds in operation. The remaining 18 resorts

were in Vaavu, Lhaviyani, Baa, Dhaalu, Meemu, Faafu

and Raa atoll. In terms of ownership, except for one

resort all the resorts were on lease holdings at the

end of 2002, with Maldivians holding leases on 67

resorts, foreign companies 10 resorts, and joint venture

lease-ownership of 9 resorts. However, in the recent

past, there has been an increasing trend towards the

use of various types of management contracts, and

at the end of 2002, Maldivian management was existent

in only 46 resorts, while 32 resorts were in the hands

of foreign management, and the rest were being

managed as joint ventures.

Due to the nature of tourism, the sector remains highly

vulnerable to international developments and this was

very clear in the aftermath of the September 11th

incident in 2001. Tourism activities started to contract

immediately afterwards and for the first time, touristtouristtouristtouristtourist

arrivalsarrivalsarrivalsarrivalsarrivals registered a negative annual growth rate of

1 percent. This trend continued in the first half of

2002, with the growth in tourist arrivals witnessing a 9

percent decline during the period compared to the

same period of 2001. However, the sector bounced

back strongly in the latter months of the year,

culminating in an annual growth of 5 percent in tourist

arrivals. In absolute terms the number of tourists that

visited the country during 2002 stood at 484.7

thousand, compared to 461.0 thousand in 2001 and

467.2 thousand in 2000.

Total tourist bednightstourist bednightstourist bednightstourist bednightstourist bednights during the year 2002 grew

by about 3 percent, a little lower than the growth in

tourist arrivals, indicating a slight reduction in the

T OUR IST B ED N IGH T S, 1996-2002

0

1000

2000

3000

4000

5000

6000

7000

1996 1997 1998 1999 2000 2001 2002

Sour ce: Ministry of T our ism

In t housands

Bednights Unut ilised Bednight Capacity

Chart 2.

16

ECONOMIC REVIEW

average length of a tourist visit. Average length oflength oflength oflength oflength of

staystaystaystaystay was shorter from 8.6 days in 2001 to 8.4 days in

2002. While the number of tourist resorts during 2002

stood at the same level as 2001 at 87 resorts, the

average number of beds that were in operation during

the year was lower than 2001 by around 350 beds.

This was largely on account of the renovation work

that was undertaken in some of these resorts during

the year. However, most of the beds that were under

construction during the year were in operation at the

end of the year and the total bed capacitybed capacitybed capacitybed capacitybed capacity of the

industry stood at 17,070, about 462 more beds than

at the end of 2001. The average utilisationutilisationutilisationutilisationutilisation of bed

capacity, which fell from 68 percent in 2000 to 66

percent in 2001 rose to 69 percent in 2002. However,

it must be noted that there was considerable variation

in the utlisation rate throughout the year, with the rate

as high as 82 percent and as low as 42 percent in

some months.

The major tourism generating marketsmarketsmarketsmarketsmarkets during the

year 2002 were Europe and Asia, as in the past years,

with European tourists accounting for 77 percent of

the market and Asian tourists accounting for 20

percent. The number of tourists from Europe totalled

373.4 thousand in 2002 with an annual growth of 3

percent. The majority of tourists arrived from Italy

(24 percent of the total tourist arrivals) during the

year, but reflected a slight negative growth of 1 percent

on annual terms in 2002 following a growth of 9

percent in 2001. Tourist arrivals from United Kingdom,

accounting for about 17 percent of total tourists, grew

by a further 4 percent in 2002 after an 8 percent

increase in 2001. Although German tourists accounted

for about 13 percent of the total number of tourists

from this country has been steadily declining in the

past few years. Hence, arrivals from Germany after

declining by 10 percent in 2000 and 15 percent in

2001, further declined by 4 percent in 2002.

Meanwhile, strong growth was witnessed in the Swiss

market registering an annual growth of 12 percent in

2002 following a 15 percent growth in 2001. Tourists

from France after increasing by 11 percent in 2001

showed a modest increase of 2 percent in 2002.

Tourists from these two countries each accounted

for about 7 percent of the total tourist arrivals.

Following a 7 percent decline in tourist arrivals from

the Asian region in 2001, such arrivals grew strongly

by 18 percent in 2002. This mainly reflected the

developments in the Japanese market, as tourists from

Japan accounted for about 46 percent of the Asian

tourists and 9 percent of the total tourists into the

country. The number of Japanese tourists who visited

the country after declining by 11 percent in 2001,

registered a 4 percent increase in 2002. The Chinese

market has also been steadily growing in recent years,

with the share of Chinese among Asian tourists

increasing from 5 percent in 1999 to 13 percent in

2002. Hence, the number of Chinese tourists who

visited the country increased by 65 percent in 2002.

Tourist arrivals from India, accounting for about 12

percent of Asian tourists, had been on a declining

trend in recent years with arrivals declining by 20

percent in 2001. However, in 2002 the trend reversed

and grew by 34 percent. In terms of the share of

arrivals from China and India in total tourists, each

held a 2 percent share in 2002.

0

100

200

300

400

1996 1997 1998 1999 2000 2001 2002

Germany Italy UK Japan France Switzerland Other

In t housands

Sour ce: Minis try of T ourism

Chart 3.

TOUR IST A R R IVA LS B Y N A T ION A LIT Y, 1996-2002

17

MMA ANNUAL REPORT 2002

2.2 Fisheries2.2 Fisheries2.2 Fisheries2.2 Fisheries2.2 Fisheries

Although the tourism sector is more dominant in the

economic development of the country, the fisheries

sector is much more inter-linked with the lives of the

vast majority of the population. According to the 2000

census, about 11 percent of the working population

were engaged in fishing.

Fisheries sector developments during the year 2002

were exceptionally good, with the sectoral contribution

to GDP edging up from 6 percent in 2001 to 7 percent

in 2002. In terms of growth rates, the value added to

GDP of the fisheries sector grew by 23 percent in

2002, following a 6 percent growth in 2001 and a

negative 2 percent growth in 2000. This was on account

of the high fish landingsfish landingsfish landingsfish landingsfish landings recorded during the year

2002, which (excluding EEZ) totalled 160 thousand

metric tons compared with 125 thousand metric tons

in 2001, registering an increase of 28 percent during

the period. The Maldivian fishery continued to be

dominated by tuna varieties, especially skipjack tuna,

which accounted for about 72 percent of total fish

catch in 2002. According to fisheries statistics, of the

total fish catch, about 48 percent were used for local

consumption and 49 percent were exported during

2002. Despite higher fish catch, the number of fishingfishingfishingfishingfishing

vesselsvesselsvesselsvesselsvessels that were engaged in fishing during a month

on average was a little lower in 2002 at 1,102 compared

to 1,128 in 2001. Hence, fish catch per unit of effort

expended per trip increased from 600 kg in 2001 to

748 kg in 2002.

MIFCO, largest company operating in the fisheries

sector, bought about 32 percent of the coastal fish

catch or 51.4 thousand metric tonnes, for production.

This was 64 percent higher than the amount bought

in 2002. Meanwhile, fish procurement prices procurement prices procurement prices procurement prices procurement prices of

MIFCO declined in 2002 with prices of skipjack over

2 kilograms falling by 4 percent to Rf3,150.0 per metric

tonne, while those weighing between 1.5 and 2

kilogram declined by 22 percent to Rf2,175.0 and those

under 1.5 kilogram declined by 44 percent to Rf1,000.0.

The total production of MIFCO, mainly in the form of

canned and frozen tuna and fishmeal, totalled 58.3

thousand metric tonnes during 2002 compared to 39.6

thousand metric tonnes in 2001, registering an increase

of 47 percent. The two private parties that were

awarded licences to process and export tuna bought

from domestic fishermen in Zone 11, under the

fisheries sector liberalisation program, commenced

their operations in 2002. They started purchasing fish

for production in October 2002 and bought 1.8

thousand metric tonnes during the year, exporting

their first consignments of frozen tuna in December

2002.

1 For coastal fisheries purposes the country has been divided into four

zones. Zone 1 encompasses the northern most atolls of Haa Alifu, Haa

Dhaalu, Shaviyani and Noonu, whilst Zone 2 comprises of Raa, Baa,

Lhaviyani and Kaafu Atoll. Zone 3 comprises of Alifu Alifu, Alifu Dhaalu,

Vaavu, Meemu, Faafu, Dhaalu, Thaa, and Laamu Atoll and Zone 4 com-

prises of Gaafu Alifu, Gaafu Dhaalu, Gnaviyani and Seenu Atoll. While

two private sector parties have been given the license to operate in Zone

1 under the fisheries sector liberalisation program, MIFCO continues

to operate in Zone 2 and Zone 4.

0

20

40

60

80

100

120

140

160

180

1996 1997 1998 1999 2000 2001 2002

Landings Exports

In t housands of m et ric t onnes

Chart 4.

F ISH LA N DIN GS A N D EXP OR T S, 1996-2002

Source: Landings ; Minis try of Fis her ies, Agriculture and Mar ine Resources

Exports; Maldives Customs Ser vice

Table 2.

FISH LANDINGS AND EXPORTS, 1999 - 2002

In thousands of metric tonnes

1999 2000 2001 2002

Coastal Catch 123.3 115.4 125.0 160.2

Skipjack 92.9 79.7 88.0 115.3

Yellow fin 14.3 12.2 14.6 21.7

Other tuna 5.5 6.3 6.8 7.2

Reef and bottom fish 10.6 17.2 15.6 16.0

Fish Exports 1/ 37.6 28.3 29.7 44.6

Frozen/Chilled 25.9 14.5 15.8 31.8

Canned 4.6 7.3 7.0 5.7

Dried 5.3 5.8 6.0 5.8

Salted 1.9 0.7 0.8 1.2

Source: Ministry of Fisheries, Agriculture and Marine Resources/ Maldives Customs Service

18

The volume of total fish exports fish exports fish exports fish exports fish exports (excluding live

tropical fish) increased significantly by 50 percent from

29.7 thousand metric tonnes in 2001 to 44.6 thousand

metric tonnes in 2002. This was mainly on account

of considerably higher exports of frozen tuna in 2002,

which accounted for 70 percent of fish export volume

and increased by over 100 percent during the year.

Meanwhile, the volume of dried fish and canned fish

exported declined by 4 percent and 18 percent

respectively in 2002. Earnings from fish exports

increased from US$35.8 million in 2001 to US$49.2

million in 2002, reflecting a considerable increase

albeit smaller than the increase in volume. This was

largely due to the lower unit value received for dried

fish as the unit values of other major export categories

registered annual increases in 2002. (Please see section

5.2 for a more detailed analysis of fish exports)

2.3 Agriculture2.3 Agriculture2.3 Agriculture2.3 Agriculture2.3 Agriculture

Agricultural activities in the country are constrained

by the lack of arable and fertile land, coupled with

the shortage of human and physical resources

necessary for the development of the sector. The value

added of the sector has remained at around 3 percent

of GDP and registered an annual growth rate of 4

percent during the year. According to the Census 2000,

less than 3 percent of the country's working

population were engaged in the agricultural sector.

Agricultural activities in the country have been primarily

a subsistence activity and backyard or homestead

cropping continue to be the major suppliers of the

produce. However, commercial production of some

varieties such as banana, papaya, watermelon and

chilli are increasing, with a few islands becoming

specialised in certain crops. Moreover, in 2002 there

were 16 uninhabited islands where relatively larger-

scale production of different fruits and vegetables

were being undertaken. These islands have been

leased by the Government to private individuals for

long-term use, with the objective of promoting

agricultural activities in the country.

A two year hydroponics agriculture pilot project,

which was launched by the Ministry of Fisheries,

Agriculture and Marine Resources in March 2000 with

the assistance of UNDP, was extended for a further

year in 2002. The major activities of this project were

carried out at the Ministry's agricultural centre in Haa

Dhaalu Hanimaadhoo, where there are three green

houses for this purpose. Products from this centre,

which included rockmelon, cucumber and chillies,

have been sold in Male' as well as in the Haa Alifu

and Haa Dhaalu atolls. While the first two years of

the project focussed on the technical feasibility of

hydroponics agriculture in the country, in the third

and final year the project aims to further disseminate

information and train more personnel in the area in

different atolls.

2.4 Distribution2.4 Distribution2.4 Distribution2.4 Distribution2.4 Distribution

Distribution activities (mainly wholesale and retail

trade) have increased rapidly in recent years and play

an important role in the domestic economy. While

the developments in the sector are closely linked to

the fisheries and construction sector activities, it is

the activities in the tourism sector that provides the

major impetus to the sector. As such, developments

in the tourism sector have direct and spill over effects

to distribution activities. In terms of the sector's

contribution to GDP, the sector accounted for about

4 percent of GDP in 2002 and grew by 2 percent in

the year following a growth rate of close to zero

percent in 2001. Apart from value added to GDP, the

leading indicators of the sector are private sector

imports and commercial banks’ credit to commerce.

Imports by the private sectorImports by the private sectorImports by the private sectorImports by the private sectorImports by the private sector (excluding tourism

sector imports2) increased by 4 percent in 2002 after

a 2 percent decline in 2001, mainly reflecting the

developments in the tourism sector. While the crcrcrcrcrediteditediteditedit

extended to the sector by the commercial banks

showed a significant annual decline of 20 percent at

the end of 2002, this was following a large increase

of 68 percent at the end of 2001. This increase in

2001 was mainly due to the removal of the credit

ceiling in July 2001, which led to a rapid increase in

credit up until June 2002.

2 Sectoral breakdowns are made on the basis of Customs records, which

are based on the sector an importer is from. As such, the sectoral analy-

sis will not strictly reflect the total imports consumed by each of these

sectors

ECONOMIC REVIEW

19

MMA ANNUAL REPORT 2002

2.5 Construction2.5 Construction2.5 Construction2.5 Construction2.5 Construction

The construction sector contributing about 3 percent

of GDP in 2002, registered a marginal decline of 0.6

percent in the year after a positive growth of 12 percent

in 2001. The activities in the sector have been broadly

based on public sector projects, private sector activity

in tourism, and housing and commercial property

development. Despite the overall decline in the

construction sector as reflected in the GDP, some of

the individual indicators of the sector showed positive

growth. As such, according to Customs statistics

import of construction materialsimport of construction materialsimport of construction materialsimport of construction materialsimport of construction materials showed a 4

percent increase in 2002 following an 8 percent

increase in the previous year. The stock of bank loansloansloansloansloans

and advancesand advancesand advancesand advancesand advances to the sector trended upwards by about

1 percent on a year-on-year basis. However,

commercial bank credit extended to housing

development showed a 12 percent decline in 2002,

which corroborates the decline in the number of

buildings completed during the year, which fell from

279 in 2001 to 264 in 2002. Moreover, buildings

authorised for construction also decreased from 588

in 2001 to 452 in 2002.

2.6 Inflation2.6 Inflation2.6 Inflation2.6 Inflation2.6 Inflation

Inflation, as measured by the changes in the Consumer

Price Index (12 month moving average) is largely

influenced by changes in the prices of fish and

imported goods since a large proportion of the

consumption basket comprises of these items. The

annual inflation rateinflation rateinflation rateinflation rateinflation rate registered 0.9 percent at the

end of 2002. This is 0.3 percent less compared to

2001. When individual price indices are looked into,

the food indexfood indexfood indexfood indexfood index (excluding fish) after growing by 10

percent in the year 2001 slowed to 6 percent growth

in the year 2002. The fish indexfish indexfish indexfish indexfish index declined by 5 percent

compared to a 21 percent decline in the previous

year. The recreation entertainment and cultural services

improved by 2 percent after declining by the same

level in 2001, while the clothing and footwear index

declined further by 4 percent in 2002. When the fish

index is excluded from the total index, annual inflation

was 1.5 percent.

2.7 Employment2.7 Employment2.7 Employment2.7 Employment2.7 Employment

Total employment data for the year are not available.

However, according to 2000 Census 3, the total labour

force of the country was estimated at 87,070, of which

85,356 were employed and 1,714 were unemployed,

indicating an unemployment rate of 2 percent at the

time. The labour force participation rate, as estimated

by the MPND based on 2000 Census data, stood at 55

percent edging up from 51 percent in the 1995 Census.

This low level of labour force participation was largely

due to the low female participation, which stood at

37 percent in 2000. Of the total employed, 66 percent

were males and 34 percent females. The highest

numbers of people were employed in community,

social and personal services (21 percent) followed

by manufacturing activities (13 percent) and fishing

activities (11 percent).

According to 2000 Census data, public sectorpublic sectorpublic sectorpublic sectorpublic sector

employmentemploymentemploymentemploymentemployment accounted for about 31 percent of the

total employment. The number of employees in the

public sector totalled 26,363 in 2002 and showed a

slight decline of 1 percent during the year 2002, mainly

on account of the 57 percent decline in temporary

workers. Meanwhile, the number of permanent

employees increased by 12 percent in 2002 following

a 7 percent increase in 2001. Of the total public sector

employees, the largest number of people are

3 The figures used in this analysis are based on the Analytical Report of

the Population and Housing Census of Maldives, 2000. The difference in

figures with the Statistical Year Book of Maldives 2003 is due to the

difference in working age group that was used in the analytical report in

which, the working age group was considered as those above 15 years.

-2

0

2

4

6

8

1996 1997 1998 1999 2000 2001 2002

Annual perce nt age change in CPI

Chart 5.

IN F LAT ION, 1996-2002

Source: Minis try of Planning and National Development

20

ECONOMIC REVIEW

employed as service providers (43 percent) followed

by the education sector (30 percent) and health sector

(15 percent).

In spite of increases in the labour force, the relatively

low domestic labour force participation rate as well

as the buoyant economic performance has resulted

in the continuation of a tight labour market situation.

As a result, the expatriate labour forceexpatriate labour forceexpatriate labour forceexpatriate labour forceexpatriate labour force has

continued to expand during 2002 as well, producing

negative effects on the balance of payments, with the

transfers made by the expatriates estimated at around

US$ 50 million. The average number of expatriate

workers in the country during 2002 was 29,680,

compared to 29,385 in 2001, reflecting a 1 percent

growth during the period. The largest number of

expatriate workers continued to be employed in the

tourism sector, accounting for about 29 percent of

the total. While the construction sector employed about

17 percent of the expatriates, 13 percent were

employed in business related activities and 11 percent

in community, social and personal services. At the

end of 2002, the largest group within the expatriate

workforce (41 percent of total expatriate labour) were

classified as labourers, who were employed in various

industries such as maintenance, construction/building,

fisheries and as odd-jobbers.

3. Public Finance3. Public Finance3. Public Finance3. Public Finance3. Public Finance

According to provisional estimates for the year

published in December 2002, the overall fiscal

position was less favourable in 2002 than the actual

outcome of 2001. The overall deficit overall deficit overall deficit overall deficit overall deficit increased by

64 percent during the year from the 2001 actual

outcome, depicting the recent trend of higher growth

in expenditure (including net lending) compared to

the expansion in revenue (including grants). In

particular, the large overall deficit in 2002 was the

result of an increase in expenditure related to large

investment projects and lower than anticipated revenue

due to general weakness in the economy.

For 2002, total revenuetotal revenuetotal revenuetotal revenuetotal revenue including grants was estimated

at Rf2,720.4 million after registering Rf2,522.6 million

in 2001. This reflected a growth of 8 percent after

witnessing a 6 percent growth in 2001. Total taxtaxtaxtaxtax

revenuerevenuerevenuerevenuerevenue registered Rf1,046.6 in 2001 and was expected

to increase to Rf1,071.2 million in 2002. In terms of

growth, this was a deceleration from 3 percent growth

in 2001 to 2 percent growth in 2002. Import duty

increased from Rf661.7 million in 2001 to Rf669.5

million in 2002 with the growth rate remaining the

same (1 percent) in both years. Meanwhile, tourism

tax earnings increased by Rf12.5 million to Rf 305.2

million in 2002. However, in terms of growth rates,

this reflected a deceleration from a 6 percent growth

in 2001 to a 4 percent growth in 2002. Receipts from

Table 3.

SUMMARY OF GOVERNMENT FINANCE, 1999 - 2002

Annual percentage change

1999 2000 2001 2002

(Prv.Est.)

Total revenue and grants 15.3 6.6 6.3 7.8

Total revenue 16.8 7.0 4.7 11.4

Tax 8.3 3.7 3.2 2.4

Nontax 25.6 9.9 5.0 20.1

Grants1/

-1.1 2.0 27.6 -30.5

Expenditure and net lending 22.1 7.5 7.1 14.9

Current expenditure 19.1 21.4 5.1 8.4

Capital expenditure 16.3 -9.0 8.9 27.4

Net lending 2/

-119.0 -497.4 -42.7 -30.5

Overall deficit 128.4 14.4 13.0 63.9

Foreign financing -56.1 -93.7 3950.0 247.6

Domestic financing -3719.4 41.7 -31.6 -59.2

1/ Includes grants-in-kind and cash but excludes direct expenditure by donors.

2/ Comprises development expenditure financed from domestic sources

and by foreign grants.

Source: Ministry of Finance and TreasuryEducation

(8%)

Hotels &

Restaur ants

(7%)

Manuf actur ing

(8%)

Constr ucti on

(17%)

Tour i sm

(28%)

Other

(8%)

Financi ng, Business

and Real estate

(13%)

Communi ty, Social

and Per sonal

Ser vices

(11%)

Source: Ministry of Planning and National Development

Chart 6.

EXP A T R IA T E EM P LOYM ENT BY IN D UST R Y, 2002

21

MMA ANNUAL REPORT 2002

non-tax revenuenon-tax revenuenon-tax revenuenon-tax revenuenon-tax revenue increased from Rf1,247.7 million in

2001 to Rf1,498.4 million in 2002, accelerating from a

5 percent growth to a 20 percent growth, mainly due

to the increase in profit transfers from public

enterprises and income from resort lease rent.

Meanwhile, grantsgrantsgrantsgrantsgrants inflow was estimated to have

declined by 30 percent to Rf147.2 million in 2002

after recording a 28 percent growth in 2001.

Total expenditure and net lending expenditure and net lending expenditure and net lending expenditure and net lending expenditure and net lending grew by 15

percent to Rf3,316.0 million in 2002, with 47 percent

of total expenditure and net lending being spent on

social services, 33 percent on public services and 16

percent on economic services. Current expenditureCurrent expenditureCurrent expenditureCurrent expenditureCurrent expenditure

increased from Rf1,971.4 million in 2001 to Rf2,136.1

million in 2002, accounting for 64 percent of total

expenditure and net lending, and recording an 8

percent growth in 2002 after registering a 5 percent

growth in 2001. Capital expenditure increased by 27

percent in 2002 following a 9 percent increase in 2001.

Reflecting these changes in revenue and expenditure,

the overall deficit deteriorated from Rf363.3 million

in 2001 to Rf595.6 million in 2002. FinancingFinancingFinancingFinancingFinancing of the

deficit was largely from foreign sources; the major

project financed by foreign loans was the Hulhumalé

Housing and Infrastructure project, which accounted

for around 39 percent of total loan disbursements

during the year. Consequently, domestic financingdomestic financingdomestic financingdomestic financingdomestic financing

declined from 60 percent of the deficit in 2001 to 15

percent in 2002.

4. Financial Sector4. Financial Sector4. Financial Sector4. Financial Sector4. Financial Sector

4.1 Banking System and Monetary Policy4.1 Banking System and Monetary Policy4.1 Banking System and Monetary Policy4.1 Banking System and Monetary Policy4.1 Banking System and Monetary Policy

The banking system consists of the Maldives Monetary

Authority (MMA) and five commercial banks. The

role of central banking is undertaken by the MMA

which was established in 1981, with the principal

functions of issuing currency, licensing, supervising

and regulating commercial bank operations,

undertaking banking activities on behalf of the

Government, providing domestic financing for

Government operations and the management of

international reserves and the exchange rate.

Of the commercial banks, only one is a domestic

bank, Bank of Maldives Plc. (BML), jointly owned by

the government (51 percent), general public (25

percent), Government Employees' Provident Fund (9

percent), State Trading Organisation Plc., Maldives

Transport and Contracting Company Plc. and Island

Communities (5 percent each). At the end of 2002,

BML had fourteen branches and five mobile banking

units (dhonis), with three out of the fourteen branches

located in Male', one at Male' International Airport

and the rest distributed amongst the atolls, each with

a designated command area. The Bank of Maldives

also undertakes development banking activities

whereby credit is extended to private parties for

various income generating activities. Of the foreign

0

500

1000

1500

2000

2500

1996 1997 1998 1999 2000 2001 2002

Others

Profit remittance by PNFE

Grants

Tourism Tax

Import Duty

In m illions of ruf iy aa

Chart 7.

GOVER N M ENT R EVEN UE A N D GR A N T S, 1996-2002

Sour ce: Ministry of Finance and Tr eas ury

0

500

1000

1500

2000

1996 1997 1998 1999 2000 2001 2002

Current Expenditure

Capital Expenditure and Net Lending

Chart 8.

GOVERNM ENT EXP ENDITURE, 1996-2002In millions of ruf iyaa

Source: Minis try of Finance and Treasury

22

ECONOMIC REVIEW

commercial banks, all of which are located in Malé,

three are branches of South Asian banks, namely State

Bank of India, Habib Bank Ltd. of Pakistan and Bank

of Ceylon and one is a branch of the Hong Kong

Shanghai Banking Corporation, HSBC. The latter

obtained license to operate in December 2001 and

commenced its operations in March 2002. These banks

play an important role in providing short and medium-

term loans to the private sector especially to the tourism

sector. They continue to be the principal institutions

for mobilising savings and for providing foreign

exchange to the private sector.

As in past years, monetary policy during 2002 has

been aimed at ensuring macroeconomic stability in

the country by supporting a low inflationary growth

and maintaining an adequate level of external reserves.

In order to achieve these objectives MMA uses an

exchange rate peg with the US dollar as the

intermediate target and is gradually moving towards

more market-based instruments of monetary policy.

The main policy instrumentspolicy instrumentspolicy instrumentspolicy instrumentspolicy instruments currently in use are

the 35 percent minimum reserve requirement on all

commercial banks; a Lombard facility providing short-

term rufiyaa liquidity to commercial banks; a 20

percent ceiling on rufiyaa lending rate; and MMA

Certificates of Deposits (CDs), which are used to

manage liquidity in the system.

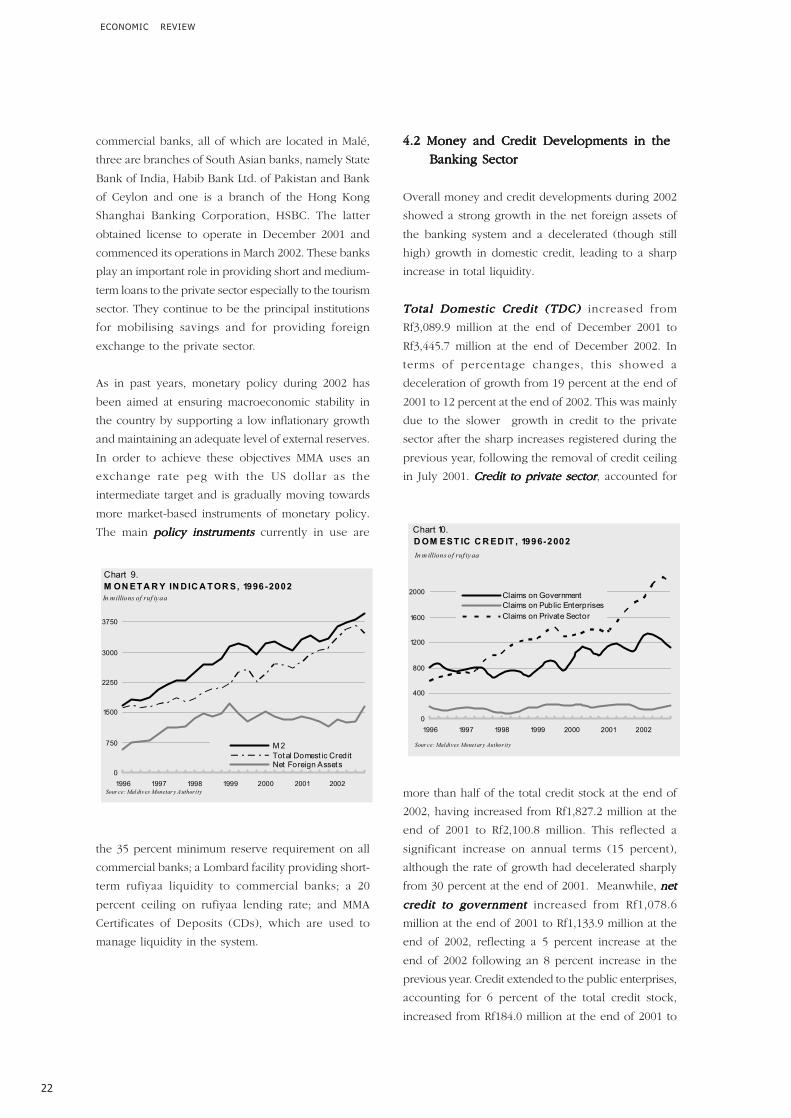

4.2 Money and Credit Developments in the4.2 Money and Credit Developments in the4.2 Money and Credit Developments in the4.2 Money and Credit Developments in the4.2 Money and Credit Developments in the

Banking Sector Banking Sector Banking Sector Banking Sector Banking Sector

Overall money and credit developments during 2002

showed a strong growth in the net foreign assets of

the banking system and a decelerated (though still

high) growth in domestic credit, leading to a sharp

increase in total liquidity.

Total Domestic Credit (TDC)Total Domestic Credit (TDC)Total Domestic Credit (TDC)Total Domestic Credit (TDC)Total Domestic Credit (TDC) increased from

Rf3,089.9 million at the end of December 2001 to

Rf3,445.7 million at the end of December 2002. In

terms of percentage changes, this showed a

deceleration of growth from 19 percent at the end of

2001 to 12 percent at the end of 2002. This was mainly

due to the slower growth in credit to the private

sector after the sharp increases registered during the

previous year, following the removal of credit ceiling

in July 2001. CrCrCrCrCredit to private sectoredit to private sectoredit to private sectoredit to private sectoredit to private sector, accounted for

more than half of the total credit stock at the end of

2002, having increased from Rf1,827.2 million at the

end of 2001 to Rf2,100.8 million. This reflected a

significant increase on annual terms (15 percent),

although the rate of growth had decelerated sharply

from 30 percent at the end of 2001. Meanwhile, netnetnetnetnet

credit to governmentcredit to governmentcredit to governmentcredit to governmentcredit to government increased from Rf1,078.6