ANNUAL REPORT 2005mb.cision.com/Main/2876/9318278/54552.pdfPhoto: BITMAP (side 5, 12, 21, 22, 111),...

120

ANNUAL REPORT 2005

Transcript of ANNUAL REPORT 2005mb.cision.com/Main/2876/9318278/54552.pdfPhoto: BITMAP (side 5, 12, 21, 22, 111),...

ANNUAL REPORT 2005

Photo: BITMAP (side 5, 12, 21, 22, 111), Elisabeth Tønnessen (page 107), Tom Haga (page 112, 115) and Åshild Moen.

The Sparebank 1 SR-Bank Group 4

Highlights 6

Main figures 7

Key figures 7

The CEO's article 8

Annual report 2005 10

Annual accounts, table of contents 23

Auditor's report for 2005 92

The Audit Committee's

statement for 2005 92

Primary capital certificates 93

Key figures during the past years 96

A group willing and able

to contribute 98

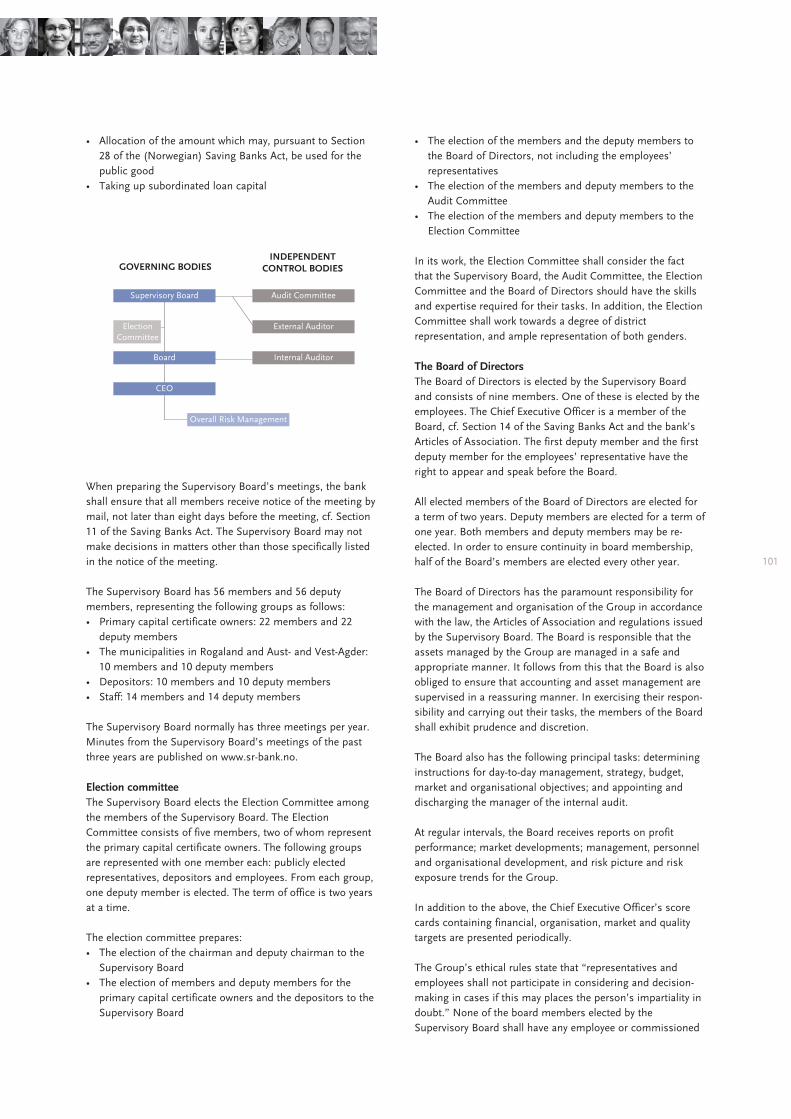

Corporate governance 100

Risk and capital management 105

Corporate market division 110

The Retail market division 113

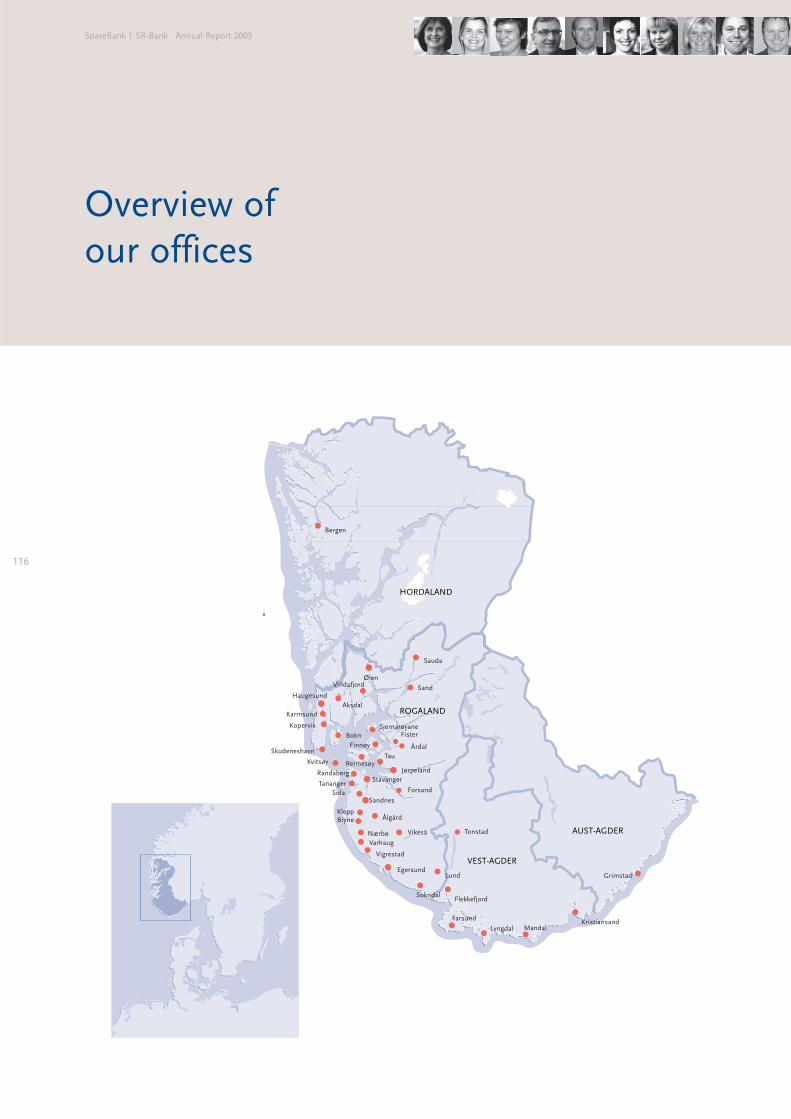

Overview of our offices 116

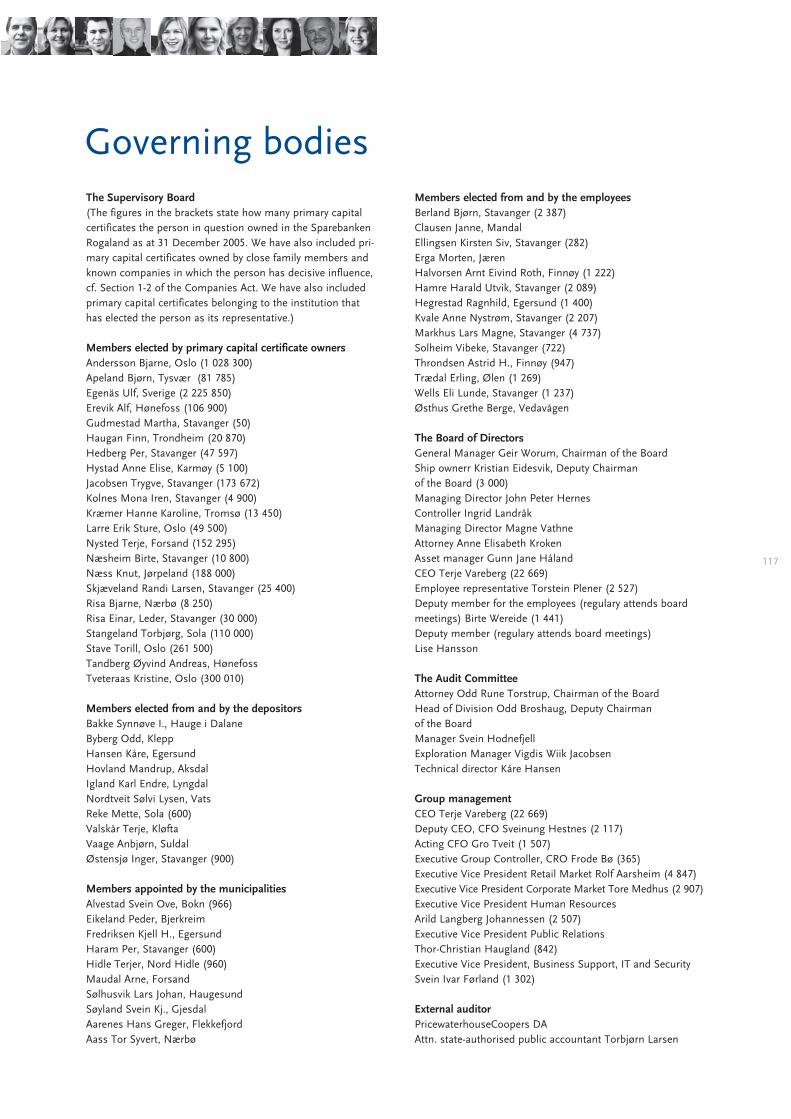

Governing bodies 117

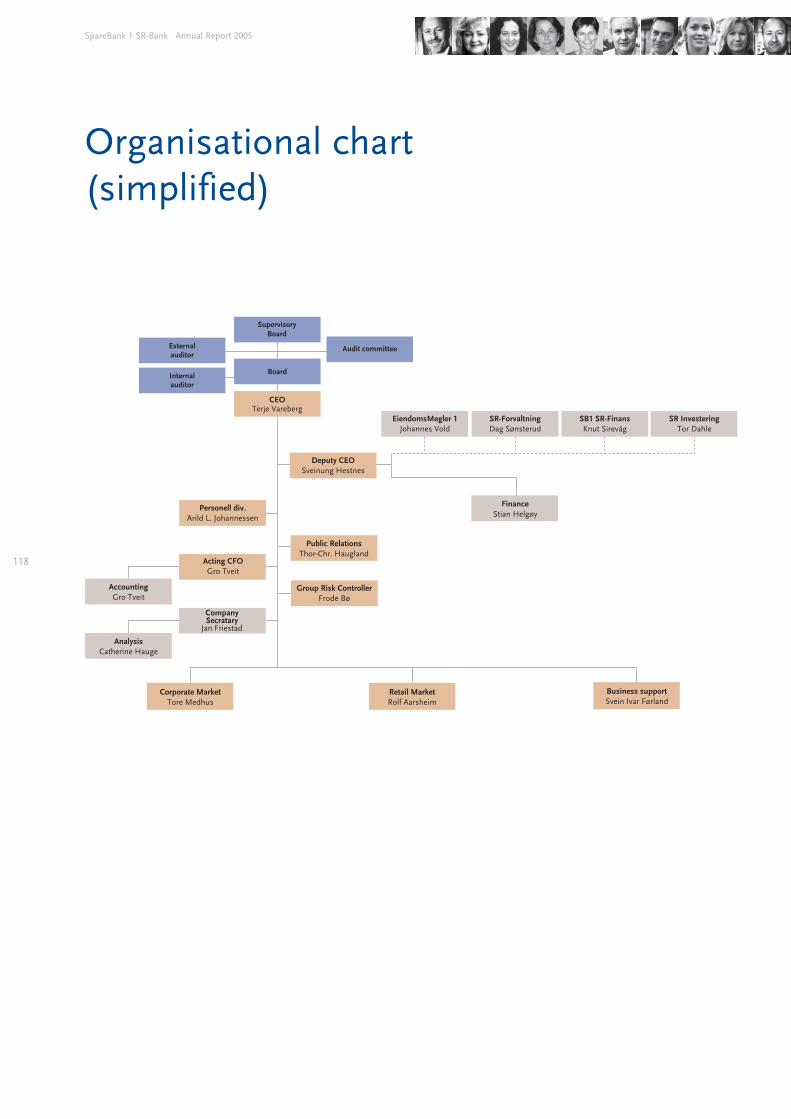

Organisational chart (simplified) 118

TABLE OF CONTENTS

WHAT SEPARATES ONE BANK FROM ANOTHER? INTEREST RATES, FEES AND PRODUCTS ARE OFTEN THE SAME. BUT HAVE YOU ASKED YOUR BANK WHAT THEY WANT?

OR WHAT ROLE THEY WANT TO PLAY? OUR ANSWER IS SIMPLE. THE OBJECTIVE OF SPAREBANK 1 SR-BANK IS TO HELP CREATE VALUES FOR THE REGION WE ARE PART

OF, AND THE ONLY WAY IN WHICH WE CAN DO THIS IS THROUGH THE ACHIEVEMENTS OF OUR 942 EMPLOYEES. IT’S A MATTER OF WILL.

Agathe Høynes, Aina Nordfonn, Alet Due-Olsen, Alf Henning Myklebust, Alf Inge Riska, Alf Sigmund Østreim, Alf Sveinung Lie, Alfhild Vikse, Alv Østerhus, Alvhild Tofterå Berge,

Anders Rundhaug, Andrè Liodden, Anita Christine Gundersen, Anita Hodnefjell, Anita Raustøl, Anita Sørhus, Anita Torjussen, Anlaug Stormo, Ann Helen Mæle, Ann Jeanette

Sunde Olaussen, Ann Kristin Igland, Ann Kristin Rise, Annbjørg Omdahl, Anne-Christine Joys, Anne-Gro Holta, Anne Beate Hope, Anne Beth Høivik, Anne Beth Naustvik Økland,

Anne Brit Idsøe, Anne Brit Myklestad, Anne Brit Watne, Anne Elise Olsen, Anne Grete Gjerde, Anne Grete Skraastad, Anne Grete Svennevig, Anne Haukalid, Anne Havsø Tveit,

Anne Herabakke, Anne Irene Lea, Anne Isaksen, Anne Jelsa, Anne Jorun Hauge, Anne Judith Vik, Anne Karin Undheim, Anne Karin Østerhus, Anne Karine Weibell, Anne Kristin H.

Førland, Anne Krogedal, Anne Lea Hobberstad, Anne Lill Larsen, Anne Lise Aukland, Anne Lise Bjorheim, Anne Lise Krossgått Førre, Anne M Slettebø, Anne Margrethe Karlstad,

Anne Marie Nortveit, Anne Mathiassen Bjørnsen, Anne Nystrøm Kvale, Anne Siri Goa Sandve, Anne Synnøve Håversen, Anne Torhild Anfinsen, Anne Turid Landmark, Anne W

Salbo Hundhammer, Annett Viste Levik, Annette Eide, Annette Skaarstad Hansen, Anny Bergeland, Anny Klingsheim, Ansgar Steffensen, Arild Ask, Arild Engø, Arild Langberg

Johannessen, Arild Lauvsnes, Arild Netteland, Arild Nielsen, Arild Ree, Arlin Opsahl Mæland, Arne Geir Larsen, Arne Gjerde, Arne Kjærstad, Arne L. Lund, Arne Mo, Arne Tjelta,

Arnfinn Høigård, Arnhild Haddeland, Arnlaug Vistnes, Arnt Eivind Roth Halvorsen, Arthur Tengesdal, Arve Austestad, Arve Pedersen, Arvid Ek, Arvid Gjesdal, Arvid Solem, Asgaut

Fiskå, Aslaug Holgersen, Aslaug Irene Frafjord, Asle Ingebrethsen, Astrid Auestad, Astrid Børresen, Astrid Hauge Edland, Astrid Horpestad, Astrid Høyland, Astrid H. Throndsen,

Astrid M. Bolme, Astrid Norheim, Astrid Saurdal, Astrid Skjæveland, Atle Mortensen, Atle Nilsen, Atle Oftedal, Atle Wb Nilsen, Atle Øvestad, Aud Helene Nese, Aud Inger

Haugland, Aud Randi Sivertsen Sletten, Aud S. J. Jåsund, Audny Hellevik, Audun Remesvik, Beate Bjelland Rabben, Bendik Voll, Bent Terje Lie, Bente Due-Olsen, Bente Erevik

Svendsen, Bente Hope, Bente Ilona Grastveit, Bente Stokdal, Bente Øyhovden, Berit Helene Bjerga, Berit Johannessen, Berit Karin Gramstad, Berit Mihle Laugaland, Berit Nygård,

Berit Sandåker Olsen, Berit Sie Eltervåg, Berit Sola, Berit Storhaug Ravndal, Berit Vatnekvam, Berit Vestersjø, Bernt H. Berge, Bernt Ringodd, Bertha Auestad, Bess Grastveit, Beth

Karin Laugaland Sele, Bidun Berge Hansen, Birgitte Nordnes, Birgitte Wendelbo Johansen, Birte Wereide, Bjarte Sivertsen, Bjørg Byberg, Bjørg Espeland, Bjørg Haarr, Bjørg Ravnås

Knutsen, Bjørg Stangenes Nilsen, Bjørg Tordis Lunde, Bjørn Berland, Bjørn Håheim, Bjørn Jan Tesdal, Bjørn Kjetil Hellestræ, Bjørn Rossebø, Bjørn Rune Olsen, Bjørn Sanne, Bjørn

Sivertsen, Bjørn Steinar Surdal, Bjørn Stensland, Bjørn Sørlund, Bjørnar Jacobsen, Bodil Eia Folkvord, Bodil H. Nernes, Bodil Olsen, Bodil Sjøthun, Bodil Sømme Danielsen, Brit

Carlsen, Brit Helen Lie Hagen, Brit Jane Tolås, Brit Røstvik, Brit Thomsen, Brit Tone Harveland, Brith Ladsten Breivik, Britt Fagerland, Børge Espeland, Børge Henriksen, Børge

Severin Furuhaug, Børge Sørensen, Bård-Espen Krabbedal, Bård Birkeland, Bård Ellingsen, Camilla Gram, Carl Fredrik Hjelle, Catherine Hauge, Cathrine Brueland Andersen,

Cathrine Leiros, Cecilie Hjelmervik, Cecilie Lileng, Cecilie Vik, Christian Jacobsen, Christian Krag, Christiane E. Skage, Christina R. Lund, Christine Christiansen, Christine Gjerde

Kvalsund, Christine Wathne Seloter, Christoffer Inge Hovda, Corine Vollen Aulin, Dag Kristian Risa, Dag Strøm, Dag Sønsterud, Dagfinn Pedersen, Dajmi Egenæs Birkedal, Ebba

Marie Breivik, Edda Runarsdottir Hodnefjell, Edna Kallevik, Edvard Jekteberg, Edvard Aarsland, Egil Nygård, Egil Reed, Einar Foss Kvavik, Einar Jøssang, Einar Osmundsen, Eirik

Bjelland, Eirik Fausa, Eirik Thorsen, Eivind Pedersen, Elbjørg Husebø, Eli Fosse Orstad, Eli Lunde Wells, Eli Margrethe Hansen, Eli Nødland Knoph, Eli Øye, Elin Berne, Elin Bie

Egge, Elin Bue, Elin Falck-Jørgensen Gitlesen, Elin Garborg, Elin Klungtveit, Elin Schanche, Elin Sørung, Elisabet Salthe, Elisabeth Falch, Elisabeth Krogedal, Elisabeth Ree-Pedersen,

Elisabeth Østensen, Elisabeth Øvstebø, Elise Oliversen, Ellen Hansen Vestre, Ellen Iversen, Ellen Kristin Westbye, Ellen Marie Jespersen, Ellen Strømme, Elna Olena Ydstebø, Else

Eriksen, Else Juul, Else Karin Rossavik, Else Karin Solvik, Else Marie Jonsson, Else Marie Rønneberg Mcneil, Emmy Holmquist, Endre Mathias Gaard, Erik Hansen, Erik Larsen, Erik

Salte, Erlend Halsne, Erling Titlestad, Erling Trondsen, Erling Trædal, Erna Nilsen, Espen Solum, Eva Eliassen, Eva Wanvik, Eva Aalvik, Evy-Tone Håland, Evy Sagen, Fred

Humborstad, Fredrik Vik Jørgensen, Freidar Sagen, Frode Bø, Frode Gjedrem, Frode Handeland, Frode Kulien, Frode Ollestad, Frode Solheim, Frøydis Spetland, Gabriel Haugen,

Gaute Jacobsen, Gaute Thise Jacobsen, Geir Danielsen, Geir Gundersen, Geir Helge Tjordal, Geir Hoff, Geir Inge Lian, Geir Lie, Geir Olav Måland, Geir Rønhovde, Geir Tjentland,

Geir Aamdal, Gerd Bergum, Gerd Ellinor Eikje, Gerd Karin Snørteland, Gerd Oddny Sørhus, Gerd Soltvedt, Gerd Solveig Sande, Gerd Størkersen, Gerd Watland, Gerd Åsbø,

Gjermund Øren, Glenn Sæther, Greta Tungland, Grete Breisteinslien Olsen, Grete Elisabeth Eide, Grete Frøyland, Grete Oanæs Dahl, Grete Torarin Haga, Grete Ø. Aukland, Grethe

Berge Østhus, Grethe Eriksen, Grethe E. Gjerde, Grethe Iversen, Grethe N. Holm, Grethe S Schreuder, Gro Anita Nøkland, Gro Barka, Gro Berit Haferkamp, Gro Lillian Netland

Hulløen, Gro Tveit, Gry Berit Lundal, Gry L. Paulsen, Gry Soland, Gry Åmot Sjøvoll, Gudbjørg Hetland, Gunlaug Haugland, Gunn Haaland, Gunn Kristi Høgøy, Gunn Merete

Johansen, Gunn Nag Nordanger, Gunn Rygh, Gunn Smithson, Gunnar Eriksen, Gunnar Fatland, Gunnar Førland, Gunnar Kristiansen, Gunnar Nielsen, Gunnar Steinsson, Gunvor

Bergesen, Gunvor Bøe, Guri Aarrestad, Guro Edquist, Guttorm Sirnes, Gyrid Bakka, Gyro Eftestøl Naterstad, Gøran Heggen, Halfdan Meling, Hanne Berit Sunde, Hanne Iren

Sværen, Hanne Joa Jacobsen, Hanne Keth Qvale, Hanne Lise Lindløv, Hanne Synnøve Andreassen, Hanne Tove Østebøvik, Hanne Aanderaa Kristiansen, Hans Jacob Hornseth,

Hans Kristian Torske, Hans Petter Salvesen, Hans P. C. Hansen, Harald Grønnestad, Harald Skarveland, Harald Utvik Hamre, Harald Vorland, Hege Eriksen Nilsen, Hege

Kyllingstad, Hege Lind Tvedt, Hege M. Drarvik Olsnes, Hege O. Larsen, Heidi Høivik, Heidi Nag Flikka, Heinz Goldhahn, Helen Hellesvik, Helene Vaaland Eriksen, Helga

Undheim, Helga Vinje, Helge H. Helgø, Helge Ims, Helge Larsen, Helge Lennart Aarsheim, Helge Lindland, Helge Pollestad, Helge Thorsen, Helge Torjussen, Henning Stålesen,

Henry Bjørkelund, Herbert Lundervold, Hild Marit Torvestad, Hilde Grønhilder Kristiansen, Hilde Marie Djupevik, Hilde Netland, Hilde Sløgedal Stava, Hilde Thoresen Solvoll,

Hilde Tollefsen, Hugo Heitmann Hansen, Håkon Færaas, Håkon Løvslett, Håvard Norberg Bø, Håvard Øvregård, Idun Vagle, Ina Aurtun, Inge Nilson, Inge Reinertsen, Ingebjørg

Feria, Inger Alida Stangeland, Inger Håland Hinna, Inger Johanne Solberg, Inger Lise Ask, Inger Lise Jonassen, Inger Lise Leite, Inger Lise Løland, Inger Lise Tønnessen, Inger

Mathiassen, Inger Reidun Tjordal Underbakke, Inger Årsvoll Tuxen, Ingfrid Warhaug, Inglen Haugland, Ingolf Harkestad, Ingrid Fritzke Andresen, Ingrid N. Stueland, Ingrid

Skjæveland, Ingunn B. Mæland, Ingunn Mæhle, Ingunn Stokdal, Ingunn Sunnevåg, Ingvar Austrått, Ingve Henriksen, Ingve Lerang, Ingvild Fitje Håland, Irene Fjeldheim, Irene Goa,

Irene Nesbø, Ivar Skogen, Iver Tønnessen Mathiesen, Jacob Magne Kvinnsland, Jahn Fredrik Hoff, Jan Arild Sørbø, Jan Arne Puntervoll, Jan Audun Lutro, Jan Audun Pedersen, Jan

Eie, Jan Einar Thesen, Jan Erik Østbø, Jan Friestad, Jan Georg Byberg, Jan Inge Buer, Jan Inge Rasmussen, Jan Jørgen Larsen, Jan Kristian Byberg, Jan Michael Nilsen, Jan

Michaelsen, Jan Ove Wolff-Jakobsen, Jan Petter Mauland, Jan Petter Mikaelsen, Jan Sigve Løvold, Jan Tjelle, Jan Vidar Vestly, Jane Brit Tønnesen Ripland, Jane Cave, Jane Margon

Vølstad, Janne Anette Wold, Janne Bore, Janne Clausen, Janne Erfjord, Janne Eskeland, Janne Fjellvang, Janne Stangeland Rege, Jarl Endre Egeland, Joar Johnsen, Johan Bjørn

Hatleskog, Johan Bull-Njaa, Johannes Høynes, Johannes Vold, John Hov, John Instanes, John Lervik, John Aage Tisløv, Jonas Ytreland, Jone Omland, Jorunn Esther Oliversen,

Jorunn E. Helgøy, Jorunn Finnestad, Jorunn Jøssang, Jorunn Lilledal, Jorunn Nepstad, Jorunn Nordvik, Jorunn Pedersen Lima, Jorunn Reianes Tvedt, Jorunn Risanger, Jorunn

Simonsen, Jorunn Vadla, Jorunn Vestbøstad, Jostein Opsal, Judith Marie Taarland, Julianne Johansen, Julie Klepp, Jørgen Kristiansen, Kalle Naley, Karen Bergesen, Karen Elise

Stølsvik, Karen Strøm Olsen, Kari Ellingsen, Kari Foss, Kari Grødem, Kari Helen Tollefsen, Kari Helgøy, Kari Hoff, Kari Høyvik, Kari Håland, Kari Idsø, Karin Bråtane, Karina

Hobbesland, Karstein Øye, Karsten Helleberg, Kate Elin Gravdal, Kate Pallesen, Ken Bårdvik, Kenneth Dalaker, Ketil B. Askildsen, Kim Ingebretsen, Kirsten Andersen, Kirsten

Ehrhorn Bjerga, Kirsten Knutsen, Kirsten Siv Ellingsen, Kirsti Skoglie, Kirsti Windingstad Løvik, Kjell Birkeland, Kjell Hestvik, Kjell Otto Vikse, Kjell Rek, Kjellaug Håvarstein, Kjetil

Helgesen, Kjetil Helland, Kjetil Kiil Halvorsen, Kjetil Skjæveland, Kjetil Søyland, Kjetil Øygarden, Klara Marie Fiskå, Knut Einar Rovik, Knut Inge Houeland, Knut Jåsund, Knut Nesse,

Knut Sirevåg, Kristian Spanne, Kristian Sørhus, Kristian Ur, Kristin Gundersen Lund, Kristin H. Furuholt, Kristin Skaar Smines, Kristine Ree Espedal, Kåre Gundersen, Kåre Haga,

Kåre Idsøe, Kåre Mæland, Kåre Nils Hallberg, Kåre Aano, Laila Abrahamsen, Laila Berntsen, Laila Rasmussen, Laila Strøm Stange, Laila Vestbø Risa, Lars Arne Bleie, Lars

Enevoldsen, Lars Færevaag, Lars Magne Markhus, Lars Martin Andersen, Lars Meling Hultin, Lars Nærland, Lars Sletten, Lars Varhaug, Leif Bø, Leif E. Bjelland, Leif Inge Løland,

Leif Ole Terøy, Leif Tore Vika, Leiv Helge Kaldheim, Leiv Inge Stokka, Leiv Kåre Asbjørnsen, Leiv Vik, Lena Fidje, Lene Gravdal, Lene Hellestø, Lillian Vestre, Linda Hapnes, Linda

Helen Høie, Linda Lillebø Haugstad, Line Hillestad, Linn Danielsen Hordvik, Linn Vetrhus Lode, Lisbet Tellefsen, Lise Ravndal, Liv Grethe Bergjord, Liv Grethe Obrestad, Liv Helen

Pettersen, Liv Ingjerd Grude, Liv Jorunn Skåland, Liv Mykland, Liv Synnøve Jensen, Liv Tone Tou, Liv Tungland, Livar Dubland, Magnar Hobberstad, Magnar Sandanger, Magne Kr.

Haugland, Magnhild Henden, Magnhild Høiland, Magnus Bjorland, Mai Brit Hanasand, Margaret Sagvåg, Margareth Alfsvaag, Margareth Storesund, Margot Fauskanger, Margot

O. Kristoffersen, Margrete Engeberg, Margrete Nordvik, Margunn Bjørnøy, Margunn Herigstad, Margunn Haaland, Margunn Mikelsen, Mari-Anne Petersen, Marianne Bakke-

Andersen, Marianne Johanson, Marianne Kaada, Marianne Skårdal Austrått, Marianne Skaar, Marianne Thu Salvesen, Marie Brunes, Marie Rosseid Eikeland, Marit Bellesen, Marit

Gryte, Marit Halvorsen, Marit Hvidsten, Marit Idsøe Skarbøvik, Marit Kristin Brekke Fiskaaen, Marit Peggy Eie, Marit Simonsen Ohm, Marit Solberg, Marit Sørbø, Marit Thorsrud,

Marit Veshovde, Marita Fjelde, Marita Olsen, Marita Raaen, Marita Øpstad Naaden, Marius Richard Riise Johnsen, Marlin Furuløkken, Marta Sandvik, Martha H. Botnen, Martin

Henrichsen, Maryanne Skjerve, May Hilde Byberg, May Jorunn Vatnaland, May Kristiansen, May Kristin Enevoldsen, Meheret Dotche, Merete Gustavson, Merete Håland, Merethe

Annaniassen, Merethe Kristensen Jerstad, Merethe Olsen Bygland, Mette Stene, Mindor Jelsa, Mona Malde Pedersen, Monica Bakken, Monica Kristoffersen, Monica Lilleland,

Monica Tjora, Morten Erga, Morten Lange, Morten Roalsø, Møyfrid Mæland, Møyfrid Synnøve Fuglestad, Målfrid Tveit Fredriksen, Målfrid Voll, Nils Eie, Nils Inge Bokn, Nils Mikal

Emberland, Nils Mikal Hegrestad, Nina Christine Henriksen, Nina Elisabeth Mortensen, Nina F. Mydske, Nina Møll, Nina Sjøen, Nina Stange Jakobsen, Nina Werness, Norunn

Marie Nordbø, Odd Abrahamsen, Odd Arild Kvaløy, Odd Breistrand, Odd M. Langvik, Odd Terje Vadla, Oddfrid Warland, Oddny Aven, Oddny Hebnes, Oddny Johnsen, Oddrun

Tjeltveit, Oddvar Rettedal, Oddvar Skretting, Oddveig Lima, Ola Aspen, Olaug Nedrebø, Olav Handeland, Olav Håland, Olav Lande Rossebø, Olav Magne Gard, Olav Strand, Ole

Magnus Bækkelund, Ole Magnus Sirevåg, Ole Petter Dahl, Ole Sigbjørn Langeland, Ole Skjærseth, Ottar Varhaug, Ove Susort, Palma Flølo Ørevik, Peder Skåre, Per-Erik Larsen, Per

Arne Jacobsen, Per Egeland, Per Ingve Leidland, Per Magne Strømstad, Per Skibeli, Petter Linaae, Petter Ølberg, Pål Frøiland, Ragnar Tollisen, Ragnhild Hegrestad, Ragnhild

Røykenes, Ragnhild Åmodt, Randi Dale, Randi Eim, Randi Eim Johansen, Randi Kjær, Randi Lillebø Larsen, Randi Ravndal, Randi Torgersen, Randi Aase, Rasmus Kvassheim, Reidar

Graue, Reidar Haga, Reidar Lieng, Reidun Idland, Reidun Ingjerd Sand, Reidun Nordbø, Reidun Raustein, Reidun Thuestad, Rigmor Bø Austrått, Rita Solum, Roar Bjørnsen, Roar

Haualand, Roar Ullenes Olsen, Roger Abusland, Rolf Birkeland, Rolf Bjarne Lie, Rolf Egeland, Rolf Hansen, Rolf Inge Lura, Rolf Mikkelsen, Rolf Simonsen, Rolf Aarsheim, Roy

Fardal, Roy Helle, Roy Tønnessen, Rudi Vestvik, Runar Skarstein, Runar Aarekol, Rune Andersen, Rune Bertelsen, Rune Bjørlo, Rune Sleveland, Rune Vaage, Sally Lund-Andersen,

Saousen Ludvigsen, Seri Berge, Sigmund Bendiksen, Sigmund Bræk, Sigmund Traa, Signe Halvorsen, Signe Kristiansen, Signe Skeie, Sigrid Riskedal, Sigrunn Austrått, Sigrunn T.U.

Stangeland, Silje Rasmussen, Siri Lindås, Siri S Dalehaug, Siri Tansø, Siril Kristoffersen, Sissel Bolme Hamre, Sissel Fjermestad, Sissel Hagen, Sissel Johnsen, Sissel Rage, Sissel

Roa Hobberstad, Sissel Tønnessen, Siv Birkeland, Siv Hind, Siw Kristin Deisz, Sjur Andre Svihus, Sjur Eftevaag, Solbjørg Lima Skadberg, Solfrid Byberg, Solfrid Sæbø, Solveig

Haugsgjerd, Solveig Olsnes Romsøe, Stein Arne Pallesen, Stein Høiland, Stein Olav Tollaksen, Steinar Borgen, Steinar Stornes, Steinar Vestbø, Stian A. Wathne, Stian Dahl, Stian

Helgøy, Stian Miljeteig, Stian Simonsen, Stig Horsberg Eriksen, Stig Morten Nerheim, Stine Johannessen, Sturla Malde, Ståle Hoff, Ståle Rasmussen, Ståle Thomsen, Sune Svela

Madland, Svein Hauge, Svein Inge Sel, Svein Ivar Førland, Svein Nordbø, Svein Nåden, Svein Rosberg, Svein Rødland, Svein Tysdal, Svein Aarrestad, Sveinung Hestnes, Sverre

Aune, Sverre Bertelsen, Sverre Dahle, Synnøve Wathne, Terje Galta, Terje Gismervik, Terje Johnsen, Terje Krumsvik, Terje Lunde, Terje Torgersen, Terje Vareberg, Therese Håland

Haver, Thor-Christian Haugland, Thora Sæther, Thorbjørn Jacobsen, Thorbjørn Thorkildsen, Thore Lie, Thrine Seglem, Tina Erga, Tjalve Lekvam, Tom Andre Lund, Tom Håland,

Tom Leif Rusdal, Tom Lie, Tom Ove Horpestad, Tom Rune Tjelta, Tom Steinsvåg, Tommy Husebø Ramsvik, Tommy Sletten, Tone Johnsen, Tone Karlsen, Tone Solheim Grøsle,

Tone Tangnæs Schulze, Tone Thorsdalen, Tor Dahle, Tor Ege, Tor Harald Skien, Tor Martin Kristiansen, Tor Reidar Frøystein, Tor Salvesen, Tor Tollefsen, Tor Tveit, Tor Tveit

Aanestad, Tor Undset, Torbjørn Høie, Torbjørn Vasstveit, Tordis Haraldsen, Tordis Pedersen, Tordis Stenberg, Tore Drange, Tore Medhus, Tore Snørteland, Torfrid Baustad,

Torhild Bjørndal, Torhild Dyskeland, Torild Naaden, Torild Sæbø Salvesen, Torill Haaland, Torill Margrethe Bjelland, Tormod Roth, Torodd Varhaug, Torstein Plener, Torunn

Dyskeland, Torunn Synnøve Grude, Torvald Søiland, Tove Bjelland, Tove Christiansen, Tove Haaland, Tove Mette Mikkelsen, Tove Schilling, Trine Lise Mjåland, Trond Anton

Ringøen, Trond Haaverstein, Trond Larsen, Trond Ove Edland, Trond Rannestad, Trond Sandvik, Trond Stave, Trond Støldal, Trygve Jan Gundersen, Turid Frøyland, Turid Hansen,

Turid Holmen, Turid Larsen, Turid Røsdal, Turid T. Krone, Turid Vanvik, Venke Mæland, Veronica Varhaugvik, Vibeke Solheim, Vidar Grastveit, Vidar Høyvik, Vidar Plaszko, Vigleik

Sirnes, Wenche Andreassen, Wenche Endresen, Wenche Netland, Wenche Winge, Wiggo Gilje, Willy Nøstbakken, Willy Skjørestad, Øygunn Nødland Idsøe, Øystein Vestre, Øystein

Viland, Øyvind Bjørgengen, Øyvind Håheim, Øyvind Rege, Øyvind Rønnevik, Øyvind Sjøtrø, Øyvind Vestbø, Ågot Bratteli, Åse Eikesdal, Åse Gry Andreassen, Åse Holm, Åse Linda

Stava, Åse Rygg, Åse Venke Tjørhom, Åse Winnie Skjæveland, Åsmund Sirevåg, Aage Olsen, Aasta Kalstø

The Sparebank 1 SR-Bank

Group

HISTORY

Sparebanken Rogaland, the legal name of SpareBank 1 SR-

Bank, was established on 1 October 1976 by merging 22

savings banks to become the country’s first regional savings

bank. After 29 years of operations and merging of a total of 39

savings banks, the bank has become the region's leading

bank. In November 1996, Sparebanken Rogaland was party to

the formation of the SpareBank 1 alliance, a Nordic banking

and product partnership.

THE GROUP

In addition to the bank, the group consists of the financial

company SpareBank 1 SR-Finans AS, EiendomsMegler 1

Rogaland AS, SR Investering AS and the bank’s company for

active asset management, SR-Forvaltning ASA. The Group has

942 employees, and total assets of NOK 67.2 billion.

THE BANK

SpareBank 1 SR-Bank is the country's second largest savings

bank. The bank's market areas are Rogaland, Agder and

Sunnhordland, and the bank currently has 50 branch offices in

its market area. The head office is located in Stavanger.

The customer-directed activities are organised into a retail

market division and a retail market division.

Retail market

With 186,860 customers, SpareBank 1 SR-Bank is the leading

retail customer bank in Rogaland. In addition to retail

customers, the retail market division serves more than 8,600

small businesses and agricultural customers. The bank supplies

products and services in the fields of financing, placing of

investments, payments facilities, pensions, non-life insurance

and life assurance. At the end of 2005, SpareBank 1 SR-Bank

had 67,700 non-life insurance customers.

Corporate market

SpareBank 1 SR-Bank holds a solid position in the corporate

market. About 40% of all businesspeople in the bank’s traditional

market list SpareBank 1 SR-Bank as their main banking. Since

establishing itself in the Agder counties in the fall of 2002, the

bank has enjoyed a positive market trend. By the end of 2005,

Sparebank 1 SR-Bank had more than 200 corporate main

banking connection customers in Agder, and further healthy

growth is expected. In total, the bank’s corporate market

division serves approx. 4,200 customers in business and

public administration, in addition to the 8,600 small businesses

and agricultural customers served by the retail market division.

EIENDOMSMEGLER 1 ROGALAND AS

The EiendomsMegler 1 chain is the Norwegian market leader

in real estate brokerage. EiendomsMegler 1 Rogaland AS is

the largest firm in this chain, and a regional market leader. In

2005 the company brokered approximately 5,100 homes from

its 20 real estate offices in Rogaland and Agder. The company

has 120 employees. In addition to brokering homes,

EiendomsMegler 1 Rogaland AS has a separate division for

business and project brokering, a separate division for the

sale of new homes in Spain, as well as a division for brokering

homes in housing co-operatives.

SPAREBANK 1 SR-FINANS AS

SpareBank 1 SR-Finans AS is the leading leasing company in

Rogaland, with more than NOK 2.1 billion in total assets, and

23 employees. The company's offfices are located alongside

the bank’s corporate market division for Stavanger and Jæren

at Forus outside of Stavanger. Its main products are leasing

and car loans. The leasing portfolio consists of a wide range

of products, and the customers represent most of the region's

business sectors.

SR-FORVALTNING ASA

SR-Forvaltning ASA manages portfolios for approx. 1,900

external customers, and for SpareBank 1 SR-Bank and

SpareBank 1 SR-Bank’s pension fund. The objective of SR-

Forvaltning is to be a local alternative with a high level of

expertise in financial management. The company has total

assets of NOK 4.3 billion, and nine employees.

SR INVESTERING AS

SR Investering AS is the group's recently established company

4

SpareBank 1 SR-Bank Annual Report 2005

for investment in equity capital instruments. The company’s

objectiveis to invest in companies, ventures, private equity

and seed funds in order to contribute to long term value

creation in the group's market area. SR Investering AS has

initial assets of NOK 200 million.

THE SPAREBANK 1 ALLIANCE

The overall objective of the SpareBank 1 alliance is to develop,

procure, sell and supply financial services and products, as

well as exploiting economies of scale in the form of lower

costs and/or higher quality, giving the customer the best

advice and the best services at competitive terms. The

Norwegian banks in the alliance co-operate through the jointly

owned holding company SpareBank 1 Gruppen AS. In addition

to Sparebank 1 SR-Bank, the other participant banks are

Sparebanken 1 Nord-Norge, Sparebanken 1 Midt-Norge and

Samarbeidende Sparebanker AS (15 local savings banks in

eastern and northwest Norway). Other owners and partners

through the SpareBank 1 Gruppen AS include Förenings-

Sparbanken AB (publ) in Sweden and the Norwegian

Federation of Trade Unions (LO). SpareBank 1 Gruppen AS

owns the companies Bank 1 Oslo AS, SpareBank 1

Livsforsikring AS, SpareBank 1 Fondsforsikring AS, SpareBank

1 Skadeforsikring AS, Odin Forvaltning AS, SpareBank 1

Bilplan AS (19.9%) and First Securities ASA 24.5%).

OBJECTIVE OF SPAREBANK 1 SR-BANK

The objective of Sparebank 1 SR-Bank is the creation of value

for the region which we are part of.

VISION

"SpareBank 1 SR-Bank - the recommended bank"

STRATEGY

SpareBank 1 SR-Bank shall be a profitable and solid bank that

is attractive for customers, capital markets, primary capital

certificate owners and employees alike. This is to be ensured

through:

• A savings bank philosophy with a strong brand identity and

modern operations, in which values are created locally and

channelled back to the community

• A clear set of priorities based on customer needs and

profitability

• A market area consisting primarily of Rogaland, Agder and

Hordaland

• A considerable position in the savings and pension market

• Competent employees who are proud to work for

SpareBank 1 SR-Bank

5

Sparebank 1 SR-Bank group management team: Back row, from the left: Sveinung Hestnes (Deputy CEO), Tore Medhus (Executive Vice President

Corporate Market), Rolf Aarsheim (Executive Vice President Retail Market), Tor-Christian Haugland (Executive Vice President Public Relations).

Front row, from the left: Terje Vareberg (CEO), Frode Bø (Executive Vice President, Head of Risk Management), Svein Ivar Førland (Executive Vice

President, Business Support, IT and Security), Gro Tveit (Acting CFO) and Arild Langberg Johannessen (Executive Vice President, Human Resources).

Highlights

• Historically good results - high recoveries on losses and high return on financial investements

• Group profit before tax. NOK 1.096 mill (NOK 821 mill).

• Return on equity after tax: 24,7% (20,2%)

• Interest rate margin: 1,76% (2,03%)

• Net other operating income: NOK 925 mill (NOK 721 mill)

• Operating costs: NOK 1.012 mill (NOK 948 mill)

• Gross non-performing loans: NOK 130 mill (NOK 203 mill)

• Net recovered losses: NOK 70 million (Net losses NOK 81 million).

• 12 month growth in lending: +13,5% (+11,3%)

• 12 month growth in deposits from customers: 13,5 % (17,0 %)

• Dividend of NOK 14 (NOK 9,2) per PCC

• Allocation of NOK 92 mill (NOK 60 Mill) to the endowment fund

(Figures from corresponding period in 2004 in parenthesis)

6

SpareBank 1 SR-Bank Annual Report 2005

7

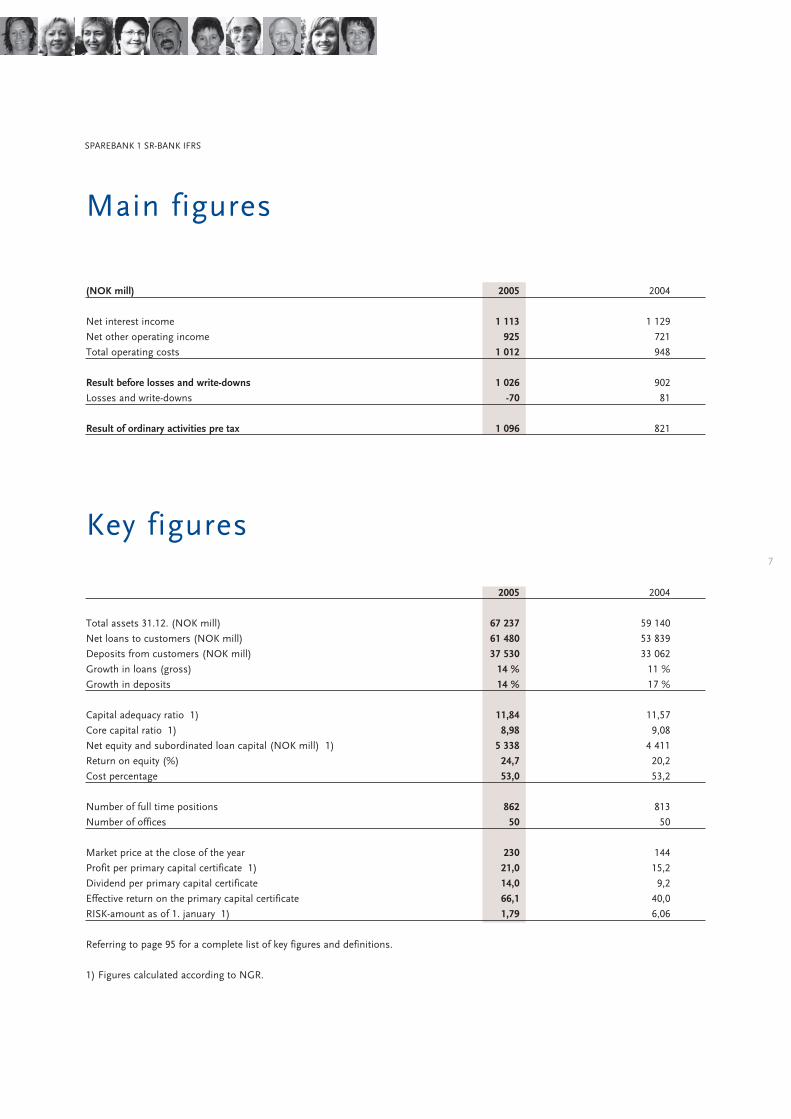

Main figures

(NOK mill) 2005 2004

Net interest income 1 113 1 129

Net other operating income 925 721

Total operating costs 1 012 948

Result before losses and write-downs 1 026 902

Losses and write-downs -70 81

Result of ordinary activities pre tax 1 096 821

Key figures

2005 2004

Total assets 31.12. (NOK mill) 67 237 59 140

Net loans to customers (NOK mill) 61 480 53 839

Deposits from customers (NOK mill) 37 530 33 062

Growth in loans (gross) 14 % 11 %

Growth in deposits 14 % 17 %

Capital adequacy ratio 1) 11,84 11,57

Core capital ratio 1) 8,98 9,08

Net equity and subordinated loan capital (NOK mill) 1) 5 338 4 411

Return on equity (%) 24,7 20,2

Cost percentage 53,0 53,2

Number of full time positions 862 813

Number of offices 50 50

Market price at the close of the year 230 144

Profit per primary capital certificate 1) 21,0 15,2

Dividend per primary capital certificate 14,0 9,2

Effective return on the primary capital certificate 66,1 40,0

RISK-amount as of 1. january 1) 1,79 6,06

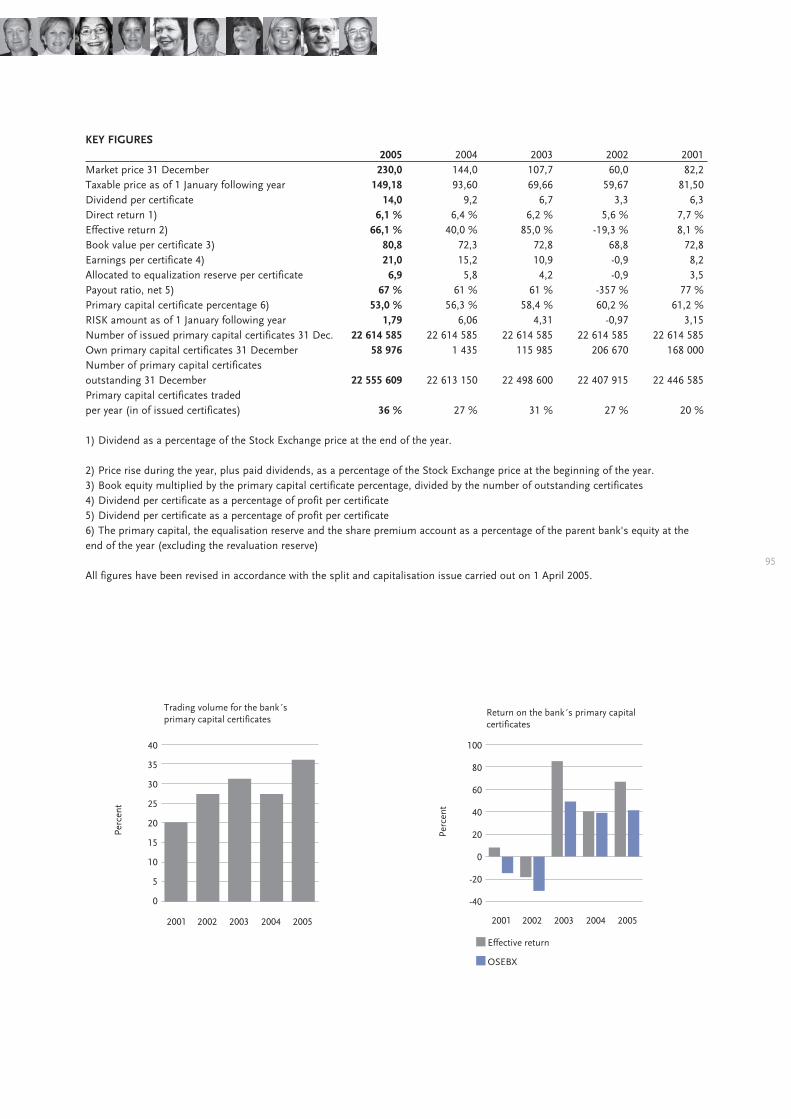

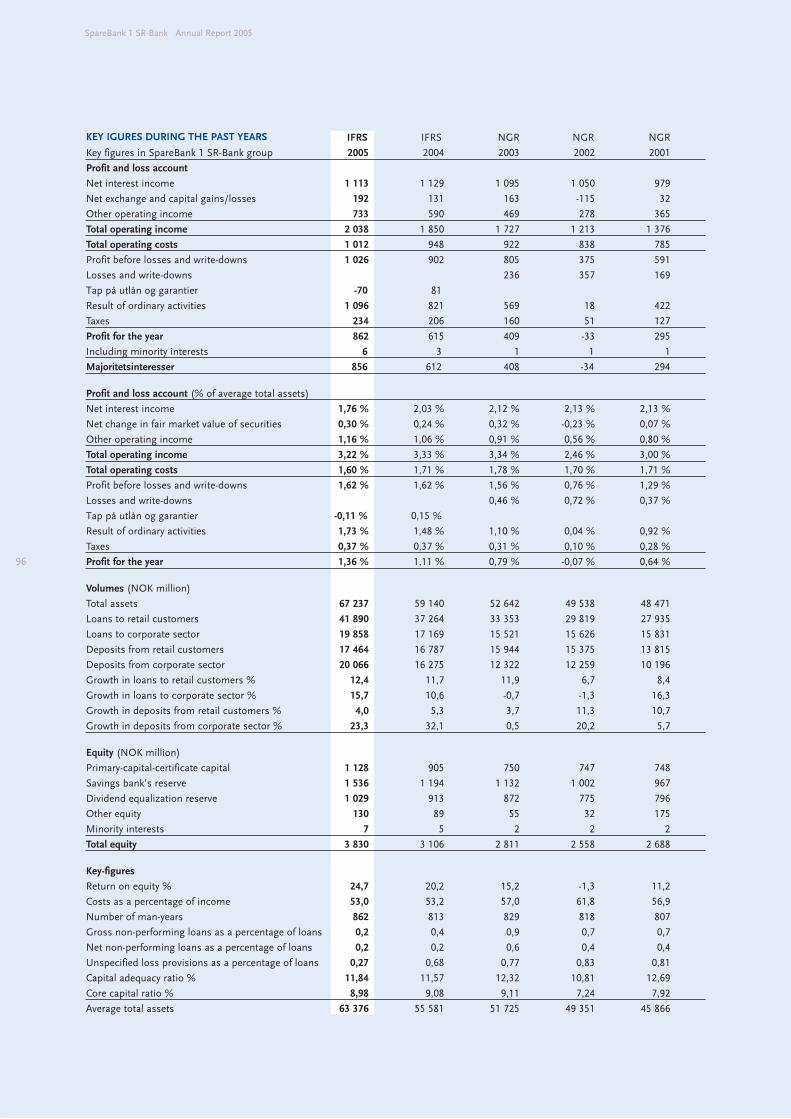

Referring to page 95 for a complete list of key figures and definitions.

1) Figures calculated according to NGR.

SPAREBANK 1 SR-BANK IFRS

8

SpareBank 1 SR-Bank Annual Report 2005

2005 WAS A VERY GOOD YEAR FOR SPAREBANK 1 SR-BANK. Customer satisfaction with our products and

services has been further strengthened. The financial result places the bank among the best banks in Norway

and the Nordic countries and creates a solid foundation for further efforts for the benefit of the region.

What you

is what sets you apart from

the others.

Norway is in a broad-based and probably long-term positive

economic cycle. Good times require strong backs. This is why

it is important to emphasize the need for long-term thinking

and action. The foundation for the development of the region

over the next 10-15 years is being laid now.

In this perspective, one must stress the necessity of careful

attention to the forces which may move or shift the develop-

ment in a positive or negative direction. In 2006, IRIS and

Agder Research will present scenarios for the Rogaland and

Agder counties towards 2020. The objective of this effort is to

create a debate on the long-term forces in play and take

measures to strengthen and exploit positive effects and to

counter negative developments.

In our view, active and diverse ownership with a will to deve-

lop and invest is very important to business development and

the creation of new jobs in the region. SpareBank 1 SR-Bank is

an active partner in the dialogue to create ownership and

equity groups in the region. We were also among the initiators

of Energivekst AS, which has a total equity of NOK 700

million. This company has had a very positive development

and has prepared the foundation for a second phase in which

a further NOK 1.8 billion has been committed. The experien-

ces from Energivekst and the development of other ownership

groups in the region underline the will and importance of

private ownership for positive business development.

Commercialisation of research results is demanding, but we

need to succeed in this respect if we are to supply more

knowledge-based products and services in the future. The

challenge is often not access to capital per se, but combining

competent, industrially oriented capital and commercially

viable ideas.

With the new international division of labour, toll and technical

trade barriers are dismantled. Markets for goods and services

are becoming integrated across national boundaries. A

vigorous and competitive business environment in our region

will have to supply products and services with an even higher

knowledge content than today. This means that the products

must reach markets with a high willingness to pay. As Norway

is a member of the EU inner market, the sections of our

industry which are exposed to competition must have the

same external conditions as the industries in the countries

with which we compete.

As far as long-term measures are concerned, equal external

conditions are by far the most important factor for positive

business development.

There have been significant structural changes in the finance

industry over the last 10 years. As a result of earlier state-

controlled banks Kredittkassen and Fokus Bank being taken

over by foreign banks, SpareBank 1 SR-Bank is now the

country's second largest Norwegian-owned bank. We believe

the nation and the region are best served by a diversity of

players in the finance sector, with Norwegian players also

having a role to play.

In light of this, it is with some concern we note the burgeoning

initiatives from European commercial banks to change the

special arrangement for savings banks as self-owned

foundations. Norwegian savings banks ensure a wide-ranging

ownership across Norway and represent a local and regional

corrective to the national and international financial groups.

Through their chartered purpose to serve the public good, the

savings banks can re-allocate a share of the profits to worthy

causes in the local community. At present, there are 126

savings banks in Norway. The need for structural changes and

adaptation in the Norwegian banking sector will be continuous.

However, a basic principle must be that such changes take

place in accordance with the wishes of the local community

which has contributed to creating the values which are

retained as equity in the savings banks' funds.

This year, SpareBank 1 SR-Bank will celebrate its 30-year

anniversary as the first regional bank in Norway. We believe

that being a savings bank is founded upon a very good

business concept in which a local foundation is combined

with proximity and expertise in all relations with our customers.

SpareBank 1 SR-Bank has always aimed for profitability and

solidity when conducting its business. High profitability is

also a precondition for being able to play an active part as a

regional development partner with considerable civic involve-

ment. The position which the bank has achieved in its market

would have been difficult to attain without the binding co-

operation which has been established with other savings

banks through the SpareBank 1 alliance. It is with satisfaction

we note that more and more savings banks share our view

and we welcome Sparebanken Volda Ørsta into the alliance.

In 2005, the SpareBank 1 banks and SpareBank 1 Gruppen AS

have again achieved financial results which place the banks in

a class of their own, compared to other Norwegian banks. The

results confirm the contribution of our long-term cooperation

strategy in strengthening the individual bank's position in the

respective markets.

SpareBank 1 SR-Bank has, for several years, had a high degree

of operating efficiency, a profitability equal to the best, a high

degree of employee satisfaction and in 2005 a sick leave rate

of 2.8 per cent. Outstanding results are created by proud,

thriving and busy employees.

9

Stavanger, March 2006

Terje Vareberg

CEO

Annual report

2005

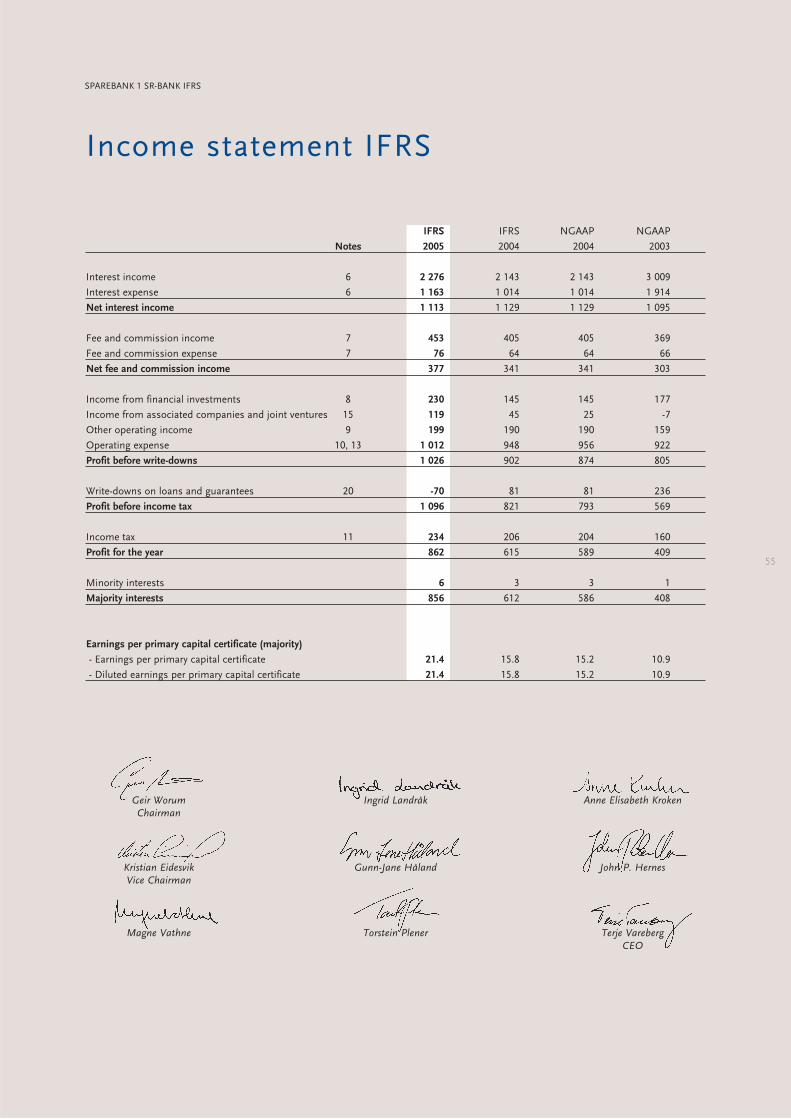

SpareBank 1 SR-Bank achieved a pre-tax group profit of NOK

1,096 million in 2005. This is an improvement of NOK 275

million from 2004. After tax, the profit was NOK 856 million,

an improvement of NOK 244 million from 2004. Return on

equity after tax was 24.7 per cent, compared to 20.2 per cent

in 2004.

The very strong result in 2005 is, in addition to fundamentally

sound banking operations, due to: low losses, payments

connected to the Finance Credit involvement, positive securities

gains and very positive contribution from the stake in

SpareBank 1 Gruppen AS.

The Board is very pleased with the results for 2005.

The 2005 annual accounts for the SpareBank 1 SR-Bank group

have been prepared according to IFRS. All group figures are

stated according to IFRS, while all parent bank figures are

stated according to Norwegian Accounting Standards (NGR).

Comparable figures for 2004 have been converted into IFRS in

the group accounts. For a more detailed description of IFRS

implementation, see the separate section in the annual report,

and the annual accounts.

The groups lendings increased by 13.5 per cent and deposits

increased by 13.5 per cent in 2005.

Deposits as measured in percentage of gross lending were

60.7 per cent by the end of the year.

Net interest received was NOK 1,135 million in 2005, down

NOK 16 million from 2004. The interest margin was 1.76 per

cent in 2005. This is a decline from 2.03 per cent in 2004.

Net commission income was NOK 377 million, up 10.6 per

cent in 2005. Income from financial investments, jointly

controlled businesses and other operating income increased

by NOK 168 million to NOK 548 million in 2005. This increase

was partly due to very strong results from SpareBank 1

Gruppen, as well as solid yield from the group's securities.

Other income (excluding capital gains on securities, dividend

and other income from ownership) amount to 36.5 per cent

of total income, compared to 34.5 per cent in 2004.

Costs increased by 6.8 per cent in 2005. The cost percentage

for the parent bank was 48.4, and 53.0 per cent for the group.

The group had net reverse losses of NOK 70 million,

compared to losses of NOK 81 million in 2004. Corrected for

reverse losses from on the Finance Credit involvement, the

regular loss costs in 2005 were NOK 6 million. Defaults have

been reduced by NOK 73 million in 2005 and were NOK 130

million by the end of the year (0.21 per cent of gross lending).

The Board proposes that of the annual profit of NOK 840

million in the parent bank, NOK 317 million be allocated to

dividend (NOK 14 per primary capital certificate), NOK 156

million be allocated to the equalisation fund, NOK 92 million

be allocated to the endowment fund and NOK 275 million be

allocated to the savings bank's fund.

DEVELOPMENT OF THE GROUP

SpareBank 1 SR-Bank continued making good progress in the

group's business areas in 2005. The group confirmed its

position as the market leader in Rogaland, both in the retail

and corporate markets, as well as in real estate brokering. At

the same time, the group has continued its positive develop-

ment in the Agder counties. In the spring of 2005, SpareBank

1 SR-Bank and EiendomsMegler 1 Rogaland AS opened a new

branch in Grimstad. In the first quarter of 2006, the bank will

open. In 2005, the group decided to expand its geographical

business area to also include Hordaland. In the spring of

2006, the group will open a branch in Bergen where banking,

real estate brokering and leasing will form part of the product

range. Key personnel have been hired and the localisation

decided.

The interaction between the retail market division, the

corporate market division, the subsidiaries and the bank's

special divisions for trading, cash management and insurance

is an important factor behind the strong results in 2005.

A low interest rate level combined with strengthened

10

SpareBank 1 SR-Bank Annual Report 2005

competition in loan products has weakened the interest mar-

gin. The growth in lending shows that there is still a high acti-

vity level in both the group's retail and corporate markets.

The new EU Capital Adequacy Directive Basel II is scheduled

for implementation in Norway from January 1 2007.

SpareBank 1 SR-Bank has high ambitions as regards risk

management in general and for adapting to the new capital

adequacy regime in particular. This is why SpareBank 1 SR-

Bank applied to the Financial Supervisory Authority of Norway

for permission to use internal measuring methods (Internal

Rating-Based Approach - Foundation) for credit risk and the

standard for operational risk management from 1 January

2007. An answer to the application from the Financial

Supervisory Authority of Norway is expected in the autumn of

2006. This is described in greater depth in a separate chapter

in the annual report.

The group reached its targets for 2005 with results well above

the target figure of 15 per cent return on equity after tax, 8 per

cent core capital and almost 12 per cent capital adequacy.

The bank's target of a 50 per cent cost income ratio in the

parent bank has also been reached. The cost income ratio in

the parent bank ended up at 48.4 per cent.

The Board believes it is important to the business community

that SpareBank 1 SR-Bank is a solid financial group with a

local attachment, which can supply necessary capital for

growth and development in the group's market areas,

primarily Rogaland, Agder and Hordaland. In order to

contribute further to the long-term creation of value in the

group's market areas, a new wholly owned investment

company, SR Investering AS, was established in late 2005.

At the same time, SpareBank 1 SR-Bank shows a social

commitment through support of local initiatives in culture,

sports and education. This is done through active use of the

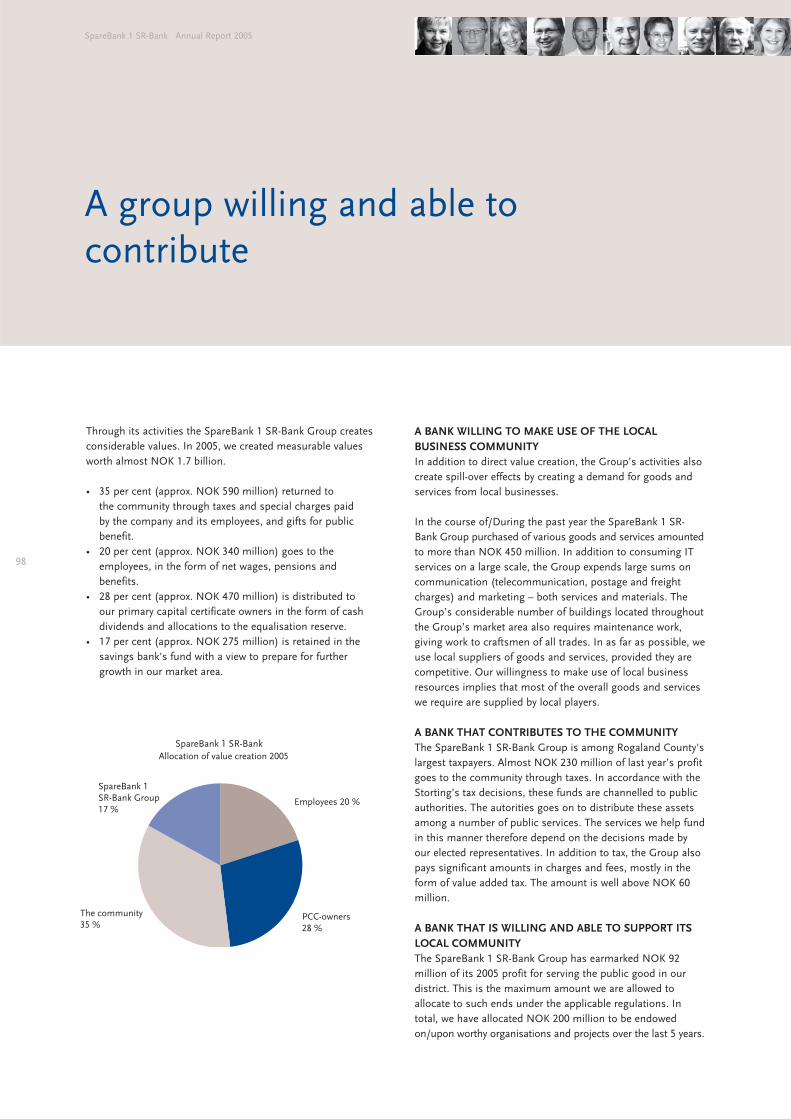

bank's endowment fund. In 2005, a total of NOK 51 million

was granted from the endowment fund.

DEVELOPMENT IN THE GROUP'S MARKET AREAS

The rising economic cycle which has characterised the

Norwegian economy since the latter half of 2003 seems to

continue into 2006, if not as strongly as in 2005. 2005 was

characterised in part by low interest rates and increased

productivity, and in the latter half also by falling unemployment

and a general optimism both in the business community and

households. The export industries are also experiencing

positive development. The growth rate in the Norwegian

economy is high and there is much to indicate that we are

close to full use of capacity. The drop in unemployment rates

has been more marked in Rogaland than in Norway as a

whole. Increased employment in business and industry has

led to a tighter labour market. According to the Economic

Barometer for Rogaland, there is already a lack of qualified

personnel in some industries, and this can lead to increased

pressure on wages and slow growth. This has, among other

things, led to an increase in the use of foreign labour.

The Rogaland business community is experiencing good

times, and according to the Economic Barometer for

Rogaland the prevailing mood for 2006 is one of optimism.

The majority of the businesses expect higher turnover and

profitability in 2006 than in 2005. 40 per cent of the

businesses in the poll expected increased manning needs in

2006. In addition, the municipalities have increased their

hiring in 2005, and increased transfers of state funds are

expected to lead to a continuation of this trend also in 2006.

Oil investments are expected to reach record levels next year,

with a prognosis of almost NOK 93 billion. The increased

level of oil investment is to a large extent due to increased

interest in oil and gas recovery due to the strong rise in the

price of oil. The spillover effects are considerable for the

Norwegian economy in general and for Rogaland in particular.

The development noted in the Agder counties is not dissimilar

from what we see in Rogaland, with falling unemployment

rates, optimism in the business community and an increased

need for labour. Over the last year, unemployment has been

reduced by 30 per cent in Aust-Agder and 13 per cent in Vest-

Agder. The most predominant factors in this development is

growth in orders and new industry enterprises, which are

important in the Agder region.

The same trend is seen in Hordaland, and according to the

NHO (Confederation of Norwegian Enterprise) Economic

Barometer for Hordaland and Sogn og Fjordane, the optimism

in the business community is on the increase. In Hordaland,

an employment increase on the order of 5-6,000 people is

expected in 2006. The highest growth is expected in

construction, retail and business services. Most businesses

expect increased turnover and higher profitability, which will

most likely lead to increased investment.

By the end of December 2005, there were 5,190 completely

unemployed people in Rogaland, according to the Labour

Market Administration. This is 2.5 per cent of the labour

force, a reduction of 1,697 people compared to December

2004. With an unemployment rate of 2.5 per cent, the

unemployment rate in Rogaland is 0.5 percentage points

below the national average. Unemployment in Rogaland is

down 0.8 percentage points since December 2004, while the

corresponding national average is 0.6 percentage points. The

unemployment rate has been reduced in spite of high labour

immigration from the EEA area and a reduction in sick leave.

In the Agder counties, unemployment was reduced by 1,290

people in 2005, to 4,500 people by the end of the year. In

Vest-Agder and Aust-Agder, unemployment rates were 3.6 and

3.2 per cent, respectively. This puts the total unemployment

in the Agder counties somewhat above the national average.

However, unemployment in the Agder counties fell considerably

more than the national average.

According to Statistics Norway, there were 396,490 people

living in Rogaland at the end of the third quarter of 2005. The

population increased by 3,386 people (0.9 per cent) in the

three first quarters of 2005. Only Oslo and Akershus have a

higher population growth rate than Rogaland. It is the Jæren

municipalities, including Stavanger and Sandnes, which have

11

the highest growth rate in the county, measured in per cent.

The number of inhabitants in the Agder counties was 266,268

at the end of the third quarter of 2005. This is an increase of

1,396 (0.5 per cent) in the first three quarters of 2005. The

population growth rate in the Agder counties was somewhat

lower than the national average of 0.6 per cent in the same

period. There are large regional differences in the Agder

counties as well. Kristiansand has the highest growth,

measured in per cent.

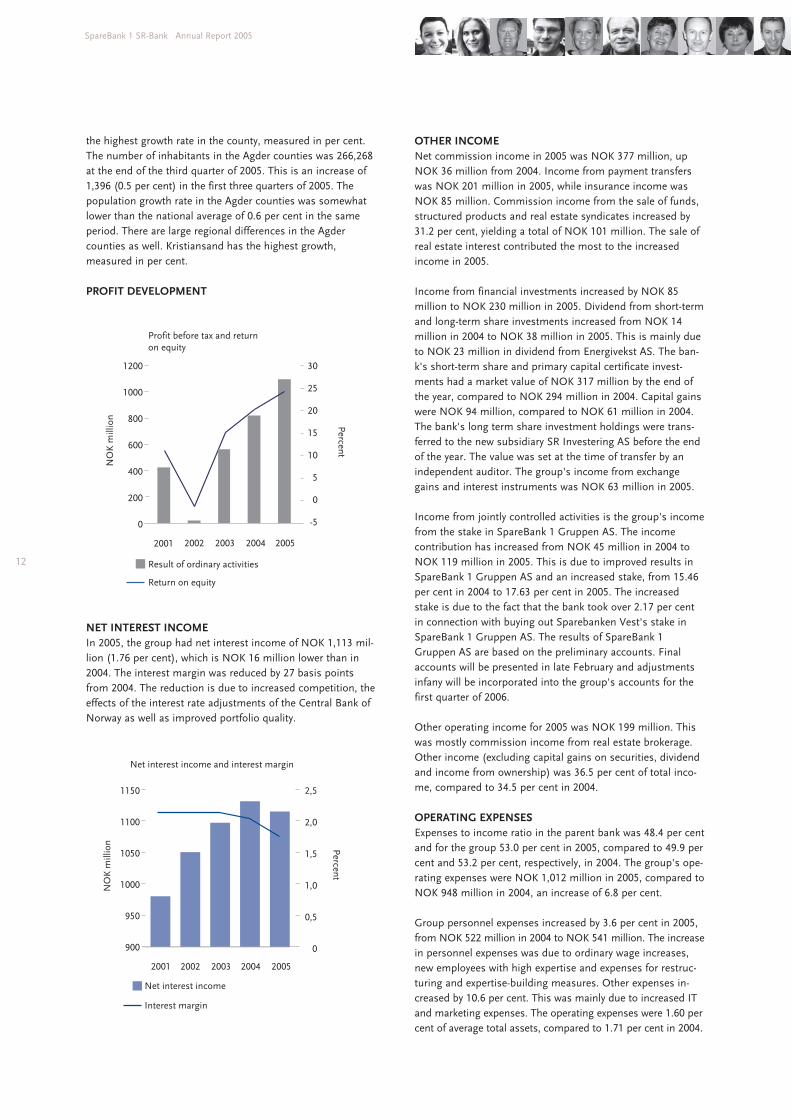

PROFIT DEVELOPMENT

NET INTEREST INCOME

In 2005, the group had net interest income of NOK 1,113 mil-

lion (1.76 per cent), which is NOK 16 million lower than in

2004. The interest margin was reduced by 27 basis points

from 2004. The reduction is due to increased competition, the

effects of the interest rate adjustments of the Central Bank of

Norway as well as improved portfolio quality.

OTHER INCOME

Net commission income in 2005 was NOK 377 million, up

NOK 36 million from 2004. Income from payment transfers

was NOK 201 million in 2005, while insurance income was

NOK 85 million. Commission income from the sale of funds,

structured products and real estate syndicates increased by

31.2 per cent, yielding a total of NOK 101 million. The sale of

real estate interest contributed the most to the increased

income in 2005.

Income from financial investments increased by NOK 85

million to NOK 230 million in 2005. Dividend from short-term

and long-term share investments increased from NOK 14

million in 2004 to NOK 38 million in 2005. This is mainly due

to NOK 23 million in dividend from Energivekst AS. The ban-

k's short-term share and primary capital certificate invest-

ments had a market value of NOK 317 million by the end of

the year, compared to NOK 294 million in 2004. Capital gains

were NOK 94 million, compared to NOK 61 million in 2004.

The bank's long term share investment holdings were trans-

ferred to the new subsidiary SR Investering AS before the end

of the year. The value was set at the time of transfer by an

independent auditor. The group's income from exchange

gains and interest instruments was NOK 63 million in 2005.

Income from jointly controlled activities is the group's income

from the stake in SpareBank 1 Gruppen AS. The income

contribution has increased from NOK 45 million in 2004 to

NOK 119 million in 2005. This is due to improved results in

SpareBank 1 Gruppen AS and an increased stake, from 15.46

per cent in 2004 to 17.63 per cent in 2005. The increased

stake is due to the fact that the bank took over 2.17 per cent

in connection with buying out Sparebanken Vest's stake in

SpareBank 1 Gruppen AS. The results of SpareBank 1

Gruppen AS are based on the preliminary accounts. Final

accounts will be presented in late February and adjustments

infany will be incorporated into the group's accounts for the

first quarter of 2006.

Other operating income for 2005 was NOK 199 million. This

was mostly commission income from real estate brokerage.

Other income (excluding capital gains on securities, dividend

and income from ownership) was 36.5 per cent of total inco-

me, compared to 34.5 per cent in 2004.

OPERATING EXPENSES

Expenses to income ratio in the parent bank was 48.4 per cent

and for the group 53.0 per cent in 2005, compared to 49.9 per

cent and 53.2 per cent, respectively, in 2004. The group's ope-

rating expenses were NOK 1,012 million in 2005, compared to

NOK 948 million in 2004, an increase of 6.8 per cent.

Group personnel expenses increased by 3.6 per cent in 2005,

from NOK 522 million in 2004 to NOK 541 million. The increase

in personnel expenses was due to ordinary wage increases,

new employees with high expertise and expenses for restruc-

turing and expertise-building measures. Other expenses in-

creased by 10.6 per cent. This was mainly due to increased IT

and marketing expenses. The operating expenses were 1.60 per

cent of average total assets, compared to 1.71 per cent in 2004.

12

SpareBank 1 SR-Bank Annual Report 2005

NO

K m

illio

n

Percent

Result of ordinary activities

Profit before tax and returnon equity

Return on equity

2002 2003 2004 20052001

Net interest income and interest margin

2002 2003 2004

NO

K m

illio

n Percent

2005

Net interest income

Interest margin

1150

1100

1050

1000

950

900

2001

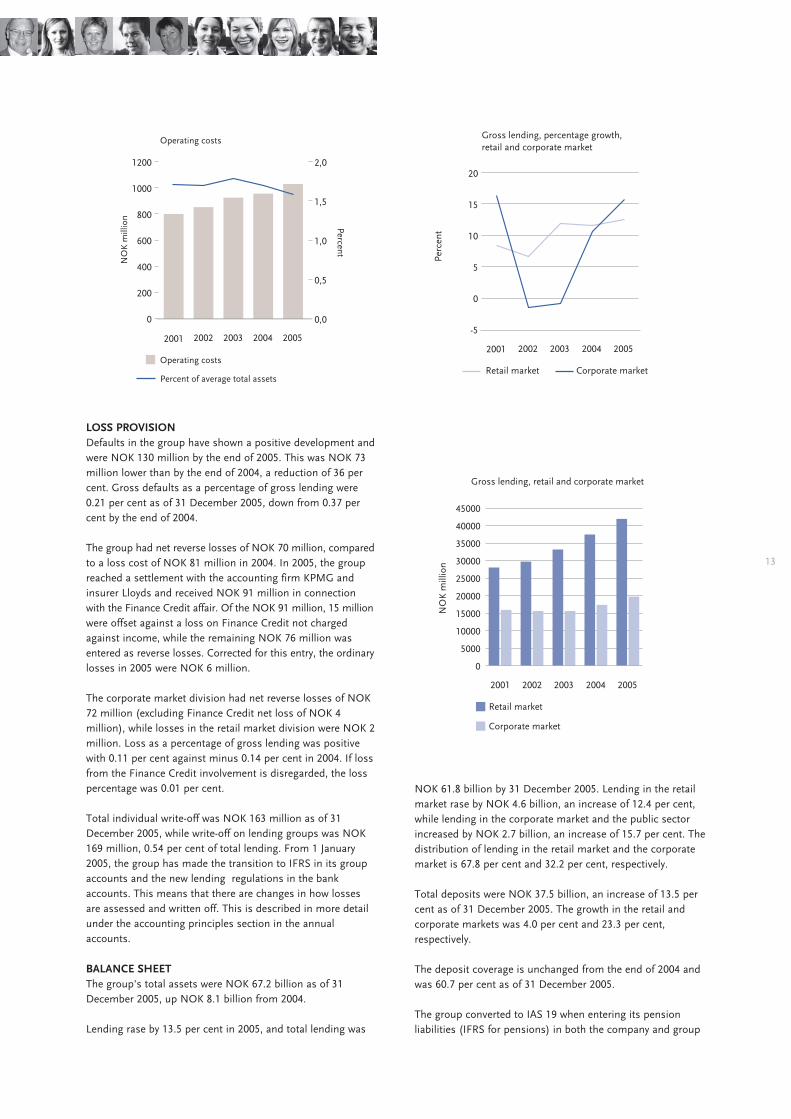

LOSS PROVISION

Defaults in the group have shown a positive development and

were NOK 130 million by the end of 2005. This was NOK 73

million lower than by the end of 2004, a reduction of 36 per

cent. Gross defaults as a percentage of gross lending were

0.21 per cent as of 31 December 2005, down from 0.37 per

cent by the end of 2004.

The group had net reverse losses of NOK 70 million, compared

to a loss cost of NOK 81 million in 2004. In 2005, the group

reached a settlement with the accounting firm KPMG and

insurer Lloyds and received NOK 91 million in connection

with the Finance Credit affair. Of the NOK 91 million, 15 million

were offset against a loss on Finance Credit not charged

against income, while the remaining NOK 76 million was

entered as reverse losses. Corrected for this entry, the ordinary

losses in 2005 were NOK 6 million.

The corporate market division had net reverse losses of NOK

72 million (excluding Finance Credit net loss of NOK 4

million), while losses in the retail market division were NOK 2

million. Loss as a percentage of gross lending was positive

with 0.11 per cent against minus 0.14 per cent in 2004. If loss

from the Finance Credit involvement is disregarded, the loss

percentage was 0.01 per cent.

Total individual write-off was NOK 163 million as of 31

December 2005, while write-off on lending groups was NOK

169 million, 0.54 per cent of total lending. From 1 January

2005, the group has made the transition to IFRS in its group

accounts and the new lending regulations in the bank

accounts. This means that there are changes in how losses

are assessed and written off. This is described in more detail

under the accounting principles section in the annual

accounts.

BALANCE SHEET

The group's total assets were NOK 67.2 billion as of 31

December 2005, up NOK 8.1 billion from 2004.

Lending rase by 13.5 per cent in 2005, and total lending was

NOK 61.8 billion by 31 December 2005. Lending in the retail

market rase by NOK 4.6 billion, an increase of 12.4 per cent,

while lending in the corporate market and the public sector

increased by NOK 2.7 billion, an increase of 15.7 per cent. The

distribution of lending in the retail market and the corporate

market is 67.8 per cent and 32.2 per cent, respectively.

Total deposits were NOK 37.5 billion, an increase of 13.5 per

cent as of 31 December 2005. The growth in the retail and

corporate markets was 4.0 per cent and 23.3 per cent,

respectively.

The deposit coverage is unchanged from the end of 2004 and

was 60.7 per cent as of 31 December 2005.

The group converted to IAS 19 when entering its pension

liabilities (IFRS for pensions) in both the company and group

13

Operating costs

Operating costs

Percent of average total assets

NO

K m

illio

n

Percent

20

15

10

5

0

-5

Gross lending, percentage growth,retail and corporate market

2002 2003 2004

Perc

ent

20052001

Retail market Corporate market

Gross lending, retail and corporate market

NO

K m

illio

n

Retail market

Corporate market

45000

40000

35000

30000

25000

20000

15000

10000

5000

0

2002 2003 2004 20052001

accounts. In the autumn of 2005, the use of this standard in

the company accounts as well was permitted given that the

group accounts are prepared according to IFRS. The group

has chosen to charge current estimate variances on pensions

directly against equity. For the group as a whole, this will

mean charging NOK 130 million after tax against equity.

This is, for all practical purposes, due to lower long-term

government bonds interest rates.

SUBSIDIARIES

Through their products and services, the subsidiaries provide

the group with a wider range of services for its customers.

Through joint activities and marketing, the group appears as

a total supplier of financial services and products.

EiendomsMegler 1 Rogaland AS is the leading real estate

agent in Rogaland with a market share and position paralleled

by that of the bank. In addition, the company has won consi-

derable market shares in Lyngdal, Mandal and Kristiansand in

recent years. In 2005, EiendomsMegler 1 Rogaland AS opened

a new branch in Grimstad, sharing premises with the bank. In

the spring of 2006, a new branch in Bergen will open, sharing

premises with the bank. EiendomsMegler 1 Rogaland AS

operates in the residential, commercial real estate and project

brokerage markets, and sold in excess of 5,100 properties

worth a total of NOK 8.3 billion in 2005. Total income in 2005

was NOK 190 million. The profit before tax was NOK 25.4

million.

SpareBank 1 SR-Finans AS offers expertise and products in

leasing and car financing. In addition to the bank's market

area in Rogaland og Agder, the company has distribution

agreements with 12 banks affiliated with the SpareBank 1

alliance(Samarbeidende Sparebanker AS). Leasing also forms

part of the product range in the group's new effort in Bergen.

In order to strengthen the company's profile and affiliation,

the company changed its name from Westbroker Finans AS to

SpareBank 1 SR-Finans AS in the first quarter of 2005. The

portfolio increased by 25 per cent in 2005, to NOK 2.1 billion.

The profit before tax was NOK 20.5 million.

The management of the investment portfolios of the bank and

its customers is organised in the company SR-Forvaltning

ASA. The company manages securities for consumers,

companies, pension funds and the bank and its pension fund.

The managed assets increased by 47 per cent in 2005, to NOK

4.3 billion. The profit before tax was NOK 24.7 million.

In December 2005, the company SR Investering AS was

founded. The company's aim is to contribute to long-term

value creation through investments in businesses in the

group's market area. The company will be in operation from

the first quarter of 2006. By the end of 2005 the company's

assets consisted of NOK 83 million in long-term share-

holdings and stakes in private equity, venture and seed funds

transferred from SpareBank 1 SR-Bank. SpareBank 1 SR-Bank

has committed a further NOK 100 million to the company to

be used for new investments.

SPAREBANK 1 BOLIGKREDITT AS

In the autumn of 2005, SpareBank 1 SR-Bank and the other

SpareBank 1 banks and Sparebanken Volda Ørsta, established

SpareBank 1 Boligkreditt AS. By the end of 2005, SpareBank 1

SR-Bank had a 26.7 per cent stake in this enterprise. The

enterprise has been established with the aim of being a credit

institution which issues bonds with special guarantees in the

enterprise's portfolio. The enterprise cannot start its operation

before the legislation takes effect. This is expected to happen

around 1 January 2007. In the mean time, the enterprise will

apply for a license as an ordinary credit institution and start

operations in the second quarter of 2006. The enterprise's loss

before tax was NOK 542,000 in 2005.

SPAREBANK 1-ALLIANSEN IN 2005

SpareBank 1 SR-Bank is a member of the SpareBank 1 alliance,

a broad-based cooperation between 19 independent

SpareBank 1 banks with total assets of almost NOK 270 billion.

The cooperation through the alliance is coordinated by the

jointly owned financial group SpareBank 1 Gruppen AS.

SpareBank 1 Gruppen AS is owned through 17.63 per cent

stakes for each of SpareBank 1 SR-Bank, SpareBank 1 Midt-

Norge, SpareBank 1 Nord-Norge and Samarbeidende

Sparebanker AS. Other owners are FöreningsSparbanken AB

(19.5 per cent) and LO (10 per cent).

SpareBank 1 Gruppen AS owns Bank 1 Oslo AS, SpareBank 1

Livsforsikring AS, SpareBank 1 Fondsforsikring AS, SpareBank

1 Skadeforsikring AS and ODIN Forvaltning AS - as well as

24.5 per cent of First Securities ASA and 19.9 per cent of

SpareBank 1 Bilplan AS.

Furthermore, SpareBank 1 Gruppen AS has the administrative

responsibility for cooperation in the SpareBank 1 alliance, in

which IT operations and development, brands, expertise

building, joint processes, use of best practice and purchases

are central. The alliance has, among other things, established

three expertise centres for payments (in Trondheim), credit

models (in Stavanger) and learning (in Tromsø), respectively.

The development in profitability in SpareBank 1 Gruppen AS

in 2005 shows that the objectives of the turnaround operation

which has been carried out have been reached in all business

14

SpareBank 1 SR-Bank Annual Report 2005

Deposit to loan ratio

2002 2003 2004

Perc

ent

20052001

areas, and that the owners' ambitions for a satisfying return

on equity have been fulfilled. SpareBank 1 Gruppen AS managed

to improve its results in all business areas in 2005. In total,

the SpareBank 1 Gruppen achieved a profit before tax of NOK

755 million in 2005, an improvement of NOK 427 million on

2004. Return on equity after tax is 32.9 per cent.

The SpareBank 1 group's different product area companies

supply good and competitive products to the banks in the

areas of savings, pensions and insurance. The development

has been very good in all product areas in 2005. Among the

highlights was SpareBank 1 Skadeforsikring's establishment

of a non-life insurance company in Sweden, in a joint venture

with Trygg-Hansa, which is to distribute non-life insurance

products through FöreningsSparbanken. Furthermore,

SpareBank 1 Livsforsikring has supplied products tailor-made

according to the new law on compulsory service pension,

products which have been well received in the market. ODIN

Forvaltning has in 2005 yet again managed to exceed the

main index with all its funds. Bank 1 Oslo has established

4 new branches in 2005, and has started the rolling out of a

new plan for more branches in Oslo, Akershus and Hedmark.

The SpareBank 1 alliance's strategy for the period up to 2007

is based on the expectation of stronger competition in both

national and regional finance markets. Such a development

calls for a stronger cooperation to exploit further advantages

as regards lower costs, increased expertise and increased

quality in servicing our customers. The ambition level for the

alliance cooperation is in this regard higher than ever.

TRANSITION TO IFRS ACCOUNTING IN THE GROUP

ACCOUNTS FROM 1 JANUARY 2005

Listed companies in the EU/EEA are obliged to report their

group accounts according to IFRS from 1 January 2005. The

purpose of the new regulations is to lead to an increased use

of real values, making the accounts reflect the real book value

per share of companies to a larger degree, as well as making

accounts prepared in different countries easier to compare.

The transition to IFRS had both negative and positive effects

on the accounts of the SpareBank 1 SR-Bank group. According

to the transition regulations, these effects were charged

directly to equity at the implementation date. Some effects

were made effective from 1 January 2004 and some from 1

January 2005. The total effect on equity of the implementation

was positive by NOK 129 million. This includes the moving of

dividend from debt to equity until a final decision is made by

the Supervisory board. If this effect is disregarded, the imple-

mentation had a negative effect of NOK 79 million after tax.

When preparing the quarterly accounts as of 31 March 2005,

these figures were NOK 180 and NOK 28 million, respectively.

The reason for the change is due to corrections to the figures

from SpareBank 1 Gruppen AS, as well as changes in the inter-

pretation of the regulations pertaining to structured products.

So far, using IFRS in the bank's company accounts is not allowed

(with the exception of pensions as described earlier in the

annual report). The Financial Supervisory Authority of Norway

has advised the Ministry of Finance that, for the time being,

banks and financing companies shall not be permitted to

make the transition to IFRS in their company accounts. When

a transition to IFRS will be made effective has not been

clarified. Until such time, SpareBank 1 SR-Bank will present

its company accounts according to Generally Accepted

Norwegian Accounting Practices and the group accounts

according to IFRS.

More detailed information on the implementation of IFRS and

the regulations is found in accounting principles and notes to

the group accounts for 2005. The annual accounts with notes

for 2005 have been prepared according to Norwegian

regulations for the bank accounts and according to IFRS for

the group accounts. Both accounts are included in the annual

report.

CORPORATE GOVERNANCE

Corporate governance in SpareBank 1 SR-Bank comprises the

goals and paramount principles according to which the bank

is managed and controlled in order to ensure that the

interests of the primary capital certificate owners, the

depositors and other groups are safeguarded. Governance of

the group's activities shall ensure prudent asset management

and greater assurance that communicated goals and

strategies are attained and realised.

Consequently, the bank has established the following main

principles for ownership and company management. The

principles rest on the following three main pillars: openness,

predictability and transparency:

• Value creation for the primary capital certificate owners and

other interest groups

• A structure that ensures goal-oriented and independent

management and supervision

• Systems that ensure measurement and accountability

• Effective risk management

• Well set-out, easily understandable and up-to-date

information

• Equal treatment of the primary capital certificate owners

and a well-balanced relationship with other interest groups

• Compliance with laws, regulations and ethical standards

The group's shareholder management and corporate

governance is founded on "Norwegian recommendation for

shareholder management and corporate governance". A more

detailed description of shareholder management and

corporate governance is found in a separate section of the

annual report.

NEW CAPITAL ADEQUACY REGULATIONS (BASEL II)

The EU's new capital adequacy directive is scheduled for

implementation in Norway on 1 January 2007. The new

regulations are based on proposals for a new standard for

capital adequacy estimation from the Bank for International

Settlements (BIS).

SpareBank 1 SR-Bank has high ambitions for risk management

in general, and for adaptation to the new capital adequacy

regulations in particular. As a result, SpareBank 1 SR-Bank

15

has applied to the Financial Supervisory Authority of Norway

for permission to employ internal rating methods (Internal

Rating Based Approach - Foundation) for credit risk from 1

January 2007. For the banks which secure approval and which

can use internal rating methods, the statutory minimum

requirement for capital adequacy for credit risk will be based

on the group's internal risk assessments from 2007. This will

make the statutory minimum requirement for capital adequacy

more risk sensitive, placing the capital adequacy requirement

in closer accordance with the risk in underlying portfolios. In

order to secure approval from the Financial Supervisory

Authority of Norway to use internal rating methods, the banks

must satisfy extensive requirements in relation to organisation,

expertise, risk models and risk management systems. The

Financial Supervisory Authority of Norway expects to complete

the main part of the review of the applications in the autumn

of 2006.

SpareBank 1 SR-Bank has an ambition to use the Standard

method for estimating minimum capital adequacy for

operational risk from 2007.

In accordance with the level of ambition regarding of risk

management mentioned above, SpareBank 1 SR-Bank has for

several years invested considerable means and resources in

the effort to further develop expertise, risk models and risk

management systems.

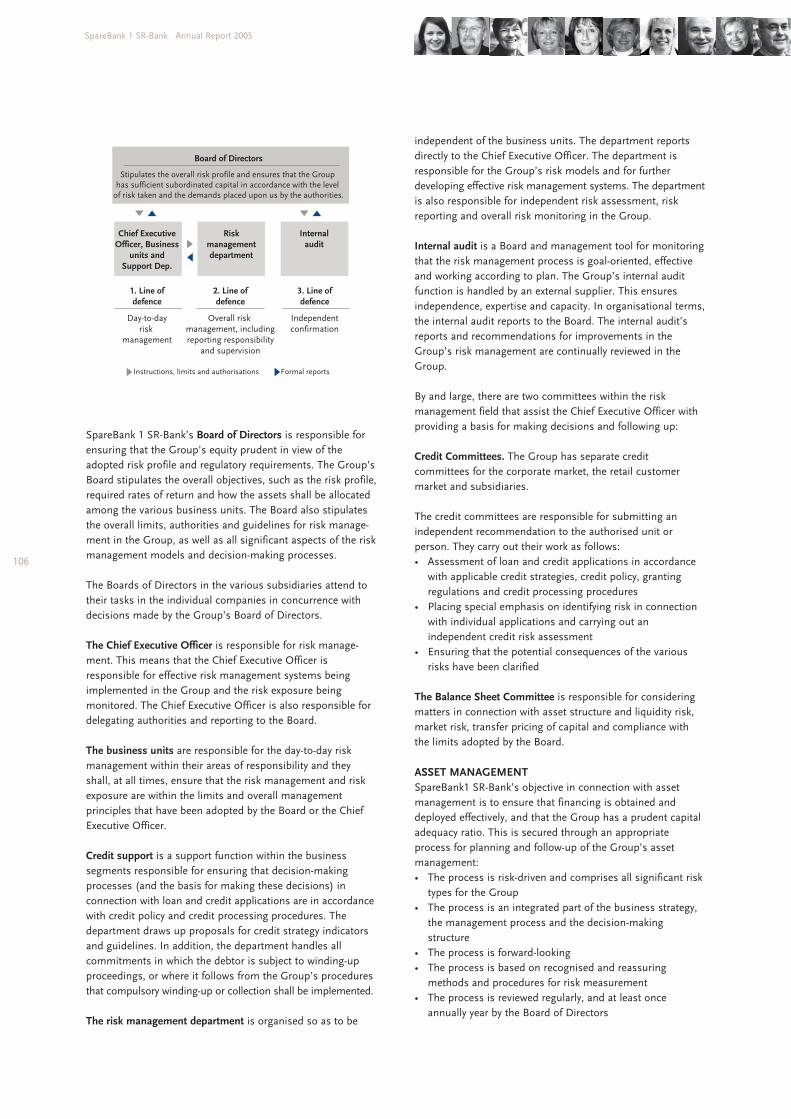

A separate department for risk management, independent of

the business units, has been established. The department

reports directly to the CEO. The department is responsible for

the group's risk models and for the further development of

efficient risk management systems. The department is further-

more responsible for independent risk assessment, risk

reporting and the overall risk monitoring in the group.

To further strengthen the risk area, the SpareBank 1 alliance

has established a separate expertise centre for credit models.

The centre is the alliance's internal specialist group for credit

models, and is responsible for customer rating, pricing, analysis

and portfolio management models. Both the risk management

department and the expertise centre for credit models are

independent of the business units. This ensures independence

in both the following up of risk and reporting.

SpareBank 1 SR-Bank expects long-term gains from the efforts

in the risk management area:

• Reduced volatility in results due to improved risk

management and credit quality

• Increased profitability due to improved profitability

and capital allocation models

• Improved usage of equity through capital minimalisation

corresponding better to the risk in the underlying

operations.

RISK MANAGEMENT IN SPAREBANK 1 SR-BANK

The risk management in SpareBank 1 SR-Bank is to support

the group's strategic development and the fulfilment of its

objectives. Furthermore, the risk management is to ensure

continued financial stability and responsible asset manage-

ment. This is to be achieved through:

• A strong risk culture, characterised by a high level of

consciousness on risk management

• A solid understanding of which risks drive earning and risk

costs, and through this creating a better foundation for

decisions

• Strive towards optimal capital usage within the approved

business strategy

• Avoid unexpected negative events which can damage the

group's operations and reputation in the market

• Exploitation of synergy and diversification effects

The group has a moderate risk profile where no single event

shall be capable of seriously harming the group's financial

position. The risk profile is described in the group's overall

risk strategy, and defined through target figures for:

• Rating: SpareBank 1 SR-Bank is rated by rating firms

Moody's Investors Service and Fitch Ratings

• Return on risk adjusted capital: Yield, adjusted for risk is to

be one of the most important strategic targets in the internal

governance of SpareBank 1 SR-Bank. This entails the

different business areas receiving capital according to the

estimated risk of the activities, and that a running

follow-up of the yield from these is conducted

• Expected loss: Describes the less amount statistically

expected over a 12-month period

• Risk - adjusted capital (financial capital): Describes how

much capital the group believes it needs to cover the actual

risk the group has assumed

• Regulatory capital: Describes the capital requirement based

on set government rates

The overall risk strategy is made operational through separate

risk strategies for credit risk, market risk, liquidity risk and

operational risk. The risk strategies are approved by the Board

16

SpareBank 1 SR-Bank Annual Report 2005

Core capital and capital adequacy ratio

2002 2003 2004 20052001

Core capital

Adequacy ratio

and are reviewed at least annually or when circumstances so

indicate.

The group's risk exposure and risk development are followed

up on the management level through periodical reports to the

administration and the Board.

Credit risk

Credit risk is defined as the danger of loss resulting from

customers or opposite party not being able or willing to fulfil

their obligations to the group.

The group has a low risk profile in the credit area, and the risk

profile is defined through the group's credit strategy. The

credit strategy contains target figures for, inter alia, risk-

adjusted capital, yield, risk adjusted, expected loss and for

concentration risks in connection with industries or the size

of commitments. In connection with the granting of credit

and the following up of credit, separate rating models and

portfolio management systems are used for the different

areas.

The underlying credit risks in the corporate and retail markets

have developed in a positive direction in 2005. This is related

to the fact that the group has a restrictive policy in regard to

high-risk commitments, the positive economic development

in the group's market areas and the low interest rate level.

Market risk

Market risk is the risk of loss due to changes in observable

market variables such as interest rates, currency exchange

rates and securities rates. The risk of changes in securities

rates due to changes in general credit prices is also defined as

market risk. The management of market risk takes place

through defined frameworks for, among other things, share

investments, bonds and for positions in the interest rate and

currency markets, and monthly reports are made to the Board.

The frameworks are reviewed and approved by the Board at

least annually. The group has conservative guidelines for market

risk, well within the maximum limits set by the authorities.

Liquidity risk

Liquidity risk is the risk of the group not being able to refinance

its debt or not being able to finance an increase in its assets

without considerable extra costs. The management of the

group's financing structure is based on an overall liquidity

strategy which is reviewed and approved by the Board at least

annually. The liquidity strategy reflects the group's moderate

risk profile.

The liquidity risk is reduced through spreading deposits over

different markets, deposit sources, instruments and terms.

Customer deposits are the group's most important source

of financing, and the group's deposit coverage remains

unchanged at 60.7 per cent as of 31 December 2004 and 31

December 2005.

The group's liquidity as of 31 December 2005 was satisfactory.

By the end of the year, only 14 per cent of the total deposit

volume is scheduled for refinancing in 2006. There is an even

distribution of international and national sources of funding.

In addition, the group has undrawn committed revolving

credit facility of 270 million euro.

Operational risk

Operational risk is defined as the risk of loss resulting from:

• Human error and lack of expertise

• Failure in ICT systems

• Unclear policy, strategy or routines

• Crime and internal irregularities

• Other internal and external causes

The group's risk management is so efficient that no single

event caused by operational risk is to able to seriously harm

the groups financial position. The risk strategy for operational

risk is approved at least annually by the Board. The risk

strategy focuses on risk sensitive target figures for expected

loss and estimation of risk adjusted capital. The group has a

moderate risk profile for operational risk.

The group has reduced the operational risk in 2005 through

systematic risk analyses and implementation of new

precautionary measures. The group uses a separate system

for reporting and following up on undesirable events, making

the group able to continuously improve processes based on

these reports.

A more detailed description of the risk management and risk

exposure in SpareBank 1 SR-Bank is found in the notes and in

a separate section in the annual report.

CAPITAL MANAGEMENT

The objective of the capital management in Sparebank 1

SR-Bank is to ensure an efficient capital funding and employ-

ment as well as responsible capital coverage. This is to be

ensured through an adequate process for planning and

following up on the group's capital requirements.

• The process is risk driven and includes all significant types

of risk in the group

• The process is an integrated part of the business strategy,

the management process and the decision structure

• The process is future-oriented and stress tests are

conducted

• The process is based on recognised and adequate

methods and procedures for risk measurement

• Processes are reviewed regularly, and at least annually,

by the Board

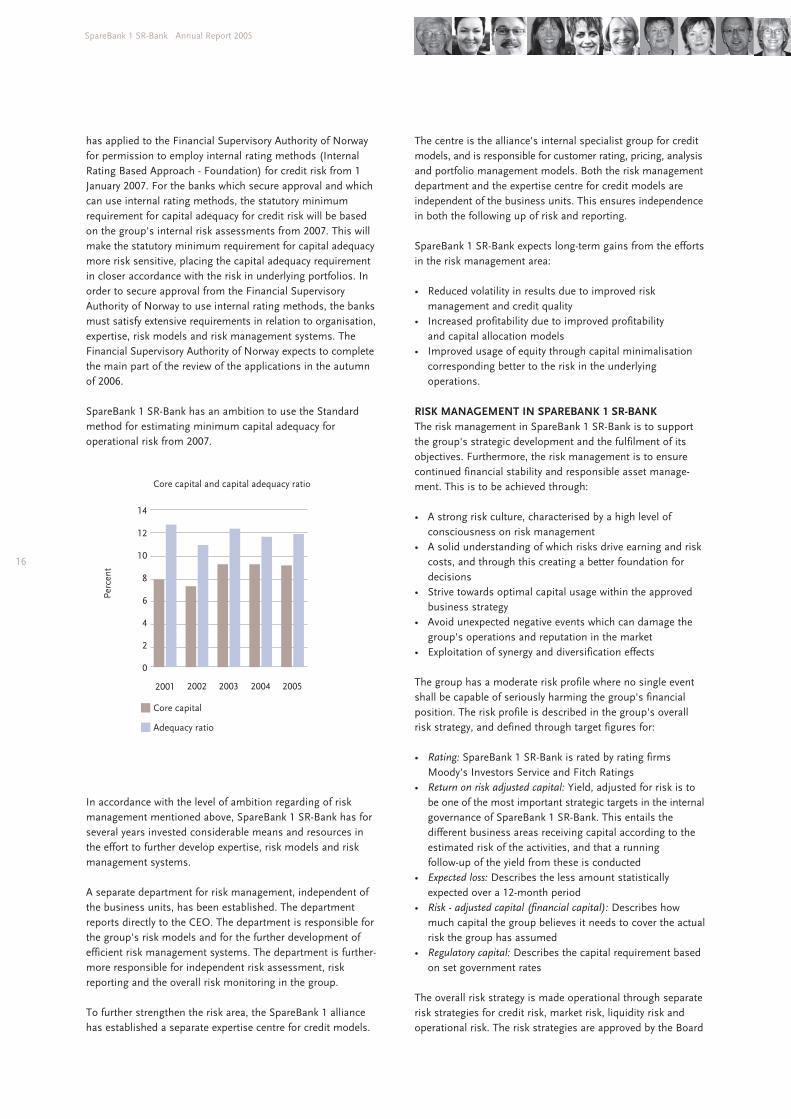

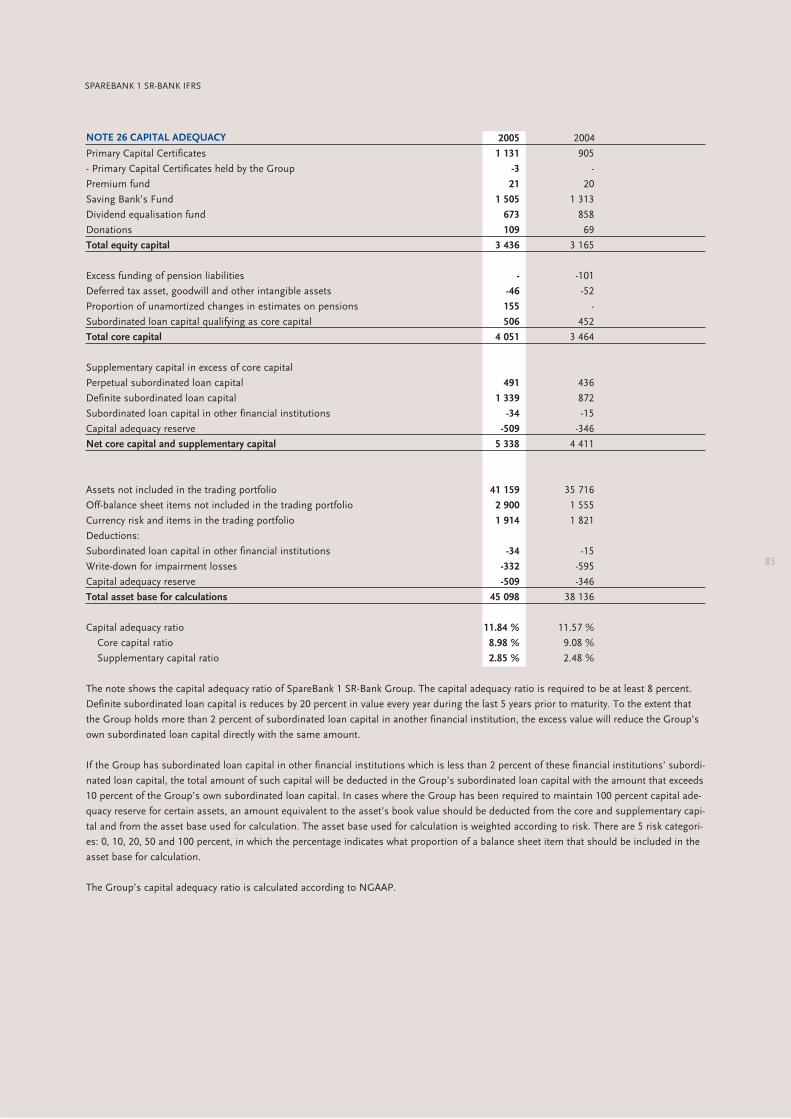

The group's target is a core capital coverage of 8 per cent and

a capital coverage of 12 per cent. By the end of 2005, the group's

capital coverage was 11.84 per cent, of which 8.98 per cent

was core capital. The corresponding key figures for the parent

bank were 12.15 per cent and 9.21 per cent, respectively. In the

first quarter of 2005, a new non-perpetual subordinated loan

of 13 billion yen was raised in the market (NOK 771 million).

This replaced a non-perpetual subordinated loan of NOK 300

million which had a so-called step-up in September 2005.

17

There were not issued any new fund bonds in 2005. On 31

December 2005, the fund bonds contributed 1.12 percentage

points to the group's core capital coverage and capital

coverage. Up to 15 per cent of the core capital can consist of

fund bonds. Any sums beyond this are added to the capital

coverage as subordinated loans.

AUDIT

External audit

The group's external auditor is PricewaterhouseCoopers.

Internal audit

The internal audit has been outsourced to Ernst & Young. The

internal auditor reports to the Board of the group.

EMPLOYEES AND WORKING ENVIRONMENT

By the end of 2005, the group had 942 employees, equalling

862 man-years. Manning has been increased by 49 man-years

in 2005. This is due to a further effort in the customer-

oriented business and a strengthening of the group's risk

management. The largest increase in manning is in the

activities directed towards compulsory service pension, where

10 new employees have been hired. In addition, both the retail

and corporate market divisions have been strengthened.

The group conducted organisation and working environment

surveys in 2005, as in earlier years. The surveys showed that

the employees have a satisfactory relationship with the group.

The group is characterised by employees with a selling

attitude, an ability and a will to adapt and a desire to raise

their level of expertise further. Sickness absence has been

further reduced in 2005, and is still low compared to other

finance institutions. Sickness absence in 2005 was 2.8 per

cent, compared to 3.1 per cent in 2004. Long-term sickness

absence has been further reduced, partly through the

participation in the Inclusive Workplace scheme and solid

follow-up from management.