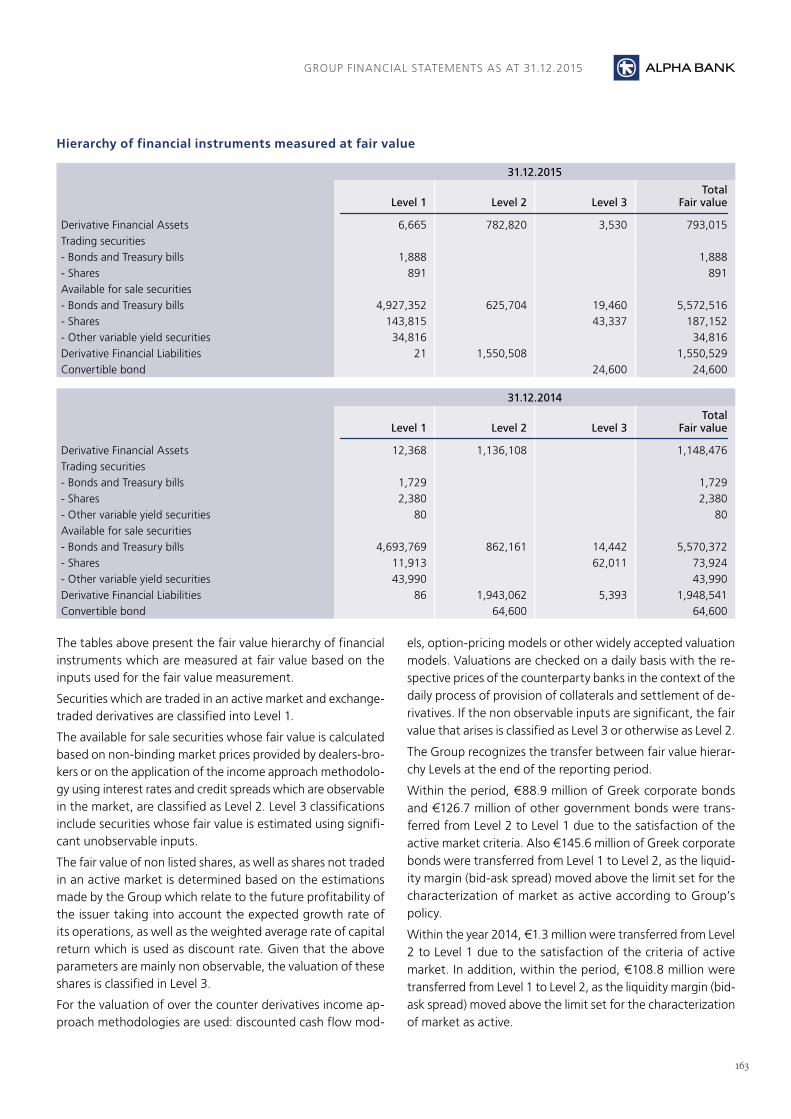

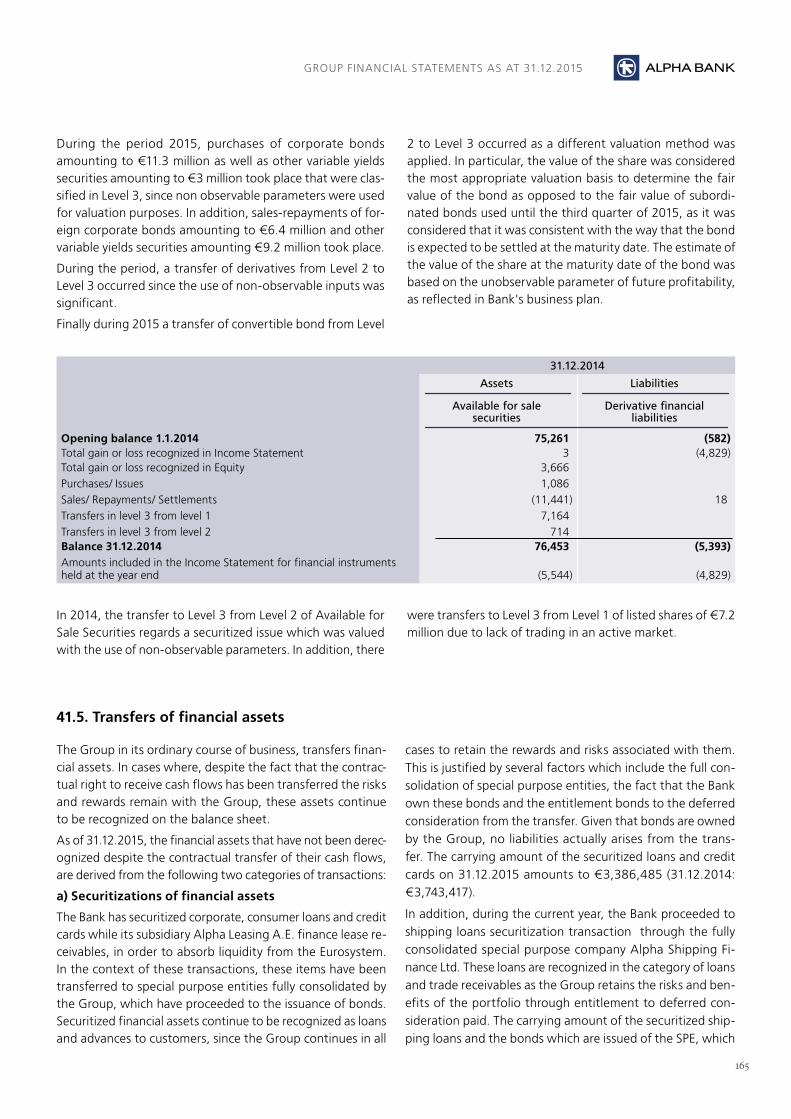

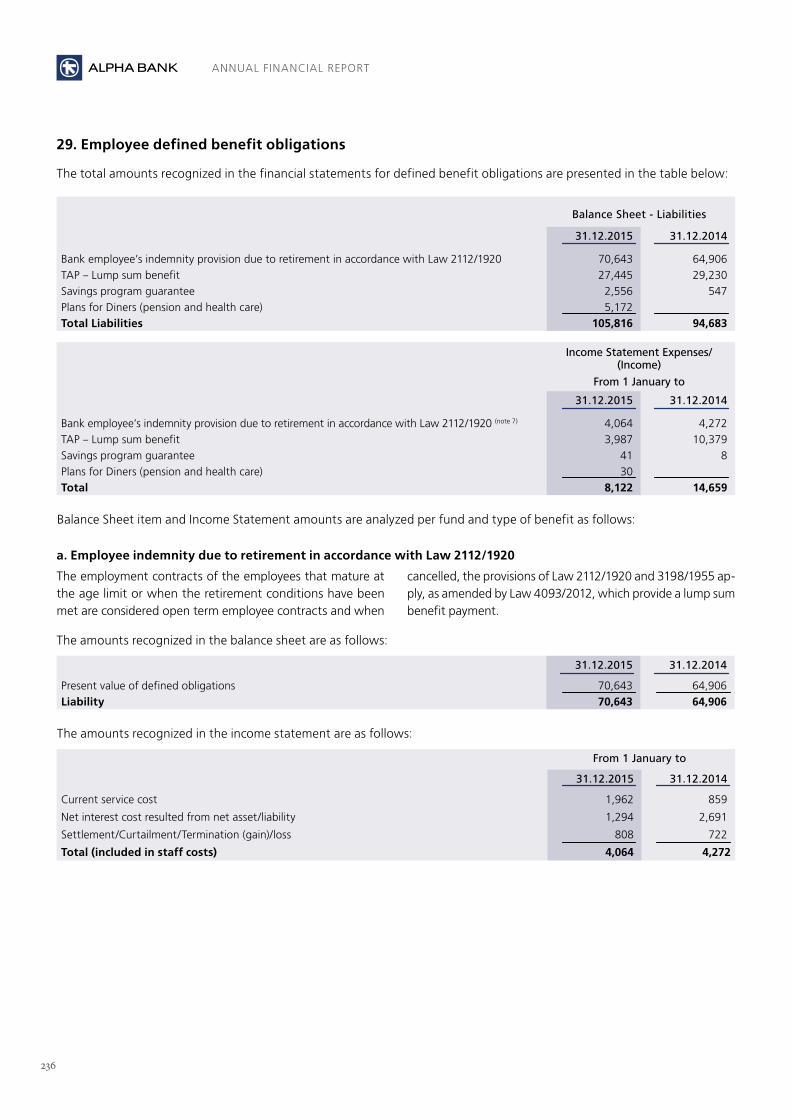

ANNUAL REPORT - Alpha Bank · 41.6 166Offsetting financial assets-liabilities ... Restructuring...

319

Athens, 3 March 2016 ANNUAL REPORT For the period from 1 January to 31 December 2015 (In accordance with Law 3556/2007)

Transcript of ANNUAL REPORT - Alpha Bank · 41.6 166Offsetting financial assets-liabilities ... Restructuring...

Athens,3 March 2016

ANNUAL REPORTFor the period from 1 January to 31 December 2015

(In accordance with Law 3556/2007)

Statement by the Members of the Board of Directors .................................................................. 7

Board of Directors’ Annual Management Report as at 31.12.2015 .............................................. 9

Explanatory Report of the Board of Directors for the year 2015 ................................................ 21

Corporate Governance Report for the year 2015 .......................................................................... 23

Independent Auditors’ Report (on Group Financial Statements) ......................................................................................................... 35

Group Financial Statements as at 31.12.2015

Consolidated Income Statement ..................................................................................................... 37

Consolidated Balance Sheet ............................................................................................................ 38

Consolidated Statement of Comprehensive Income ....................................................................... 39

Consolidated Statement of Changes in Equity ............................................................................... 40

Consolidated Statement of Cash Flows ...........................................................................................42

Notes to the Group Financial Statements

General Information .................................................................................................................... 43

Accounting policies applied

1.1 Basis of presentation ..................................................................................................... 45 1.2 Basis of consolidation ....................................................................................................49 1.3 Operating segments ....................................................................................................... 51 1.4 Transactions in foreign currency and translation of foreign operations ................................. 51 1.5 Cash and cash equivalents .............................................................................................. 52 1.6 Classification and measurement of financial instruments ................................................... 52 1.7 Derivative financial instruments and hedge accounting ..................................................... 54 1.8 Fair value measurement .................................................................................................. 56 1.9 Property, plant and equipment ........................................................................................ 57 1.10 Investment property ...................................................................................................... 58 1.11 Goodwill and other intangible assets ................................................................................ 58 1.12 Leases ........................................................................................................................... 58 1.13 Insurance activities ........................................................................................................ 59 1.14 Impairment losses on loans and advances ....................................................................... 60 1.15 Impairment losses on non-financial assets ....................................................................... 60 1.16 Income tax .................................................................................................................... 61 1.17 Non-current assets held for sale ...................................................................................... 61 1.18 Employee benefits .......................................................................................................... 62 1.19 Share options granted to employees ................................................................................62 1.20 Provisions and contingent liabilities.................................................................................. 63 1.21 Sale and repurchase agreements and securities lending ..................................................... 63 1.22 Securitization................................................................................................................. 63 1.23 Equity ........................................................................................................................... 63 1.24 Interest income and expense ...........................................................................................64 1.25 Fee and commission income ............................................................................................64 1.26 Dividend income ............................................................................................................64 1.27 Gains less losses on financial transactions .........................................................................64

T A B L E O F C O N T E N T S

1.28 Discontinued operations .................................................................................................64 1.29 Related parties definition ................................................................................................ 65 1.30 Comparatives ................................................................................................................. 65 1.31 Estimates, decision making criteria and significant sources of uncertainty ............................ 65

Income Statement

2 Net interest income .......................................................................................................69 3 Net fee and commission income ......................................................................................69 4 Dividend income ............................................................................................................70 5 Gains less losses on financial transactions .........................................................................70 6 Other income ................................................................................................................70 7 Staff costs ..................................................................................................................... 71 8 General administrative expenses ..................................................................................... 73 9 Other expenses .............................................................................................................. 73 10 Impairment losses and provisions to cover credit risk ......................................................... 74 11 Income tax .................................................................................................................... 74 12 Earnings /(losses) per share ............................................................................................. 77

Assets

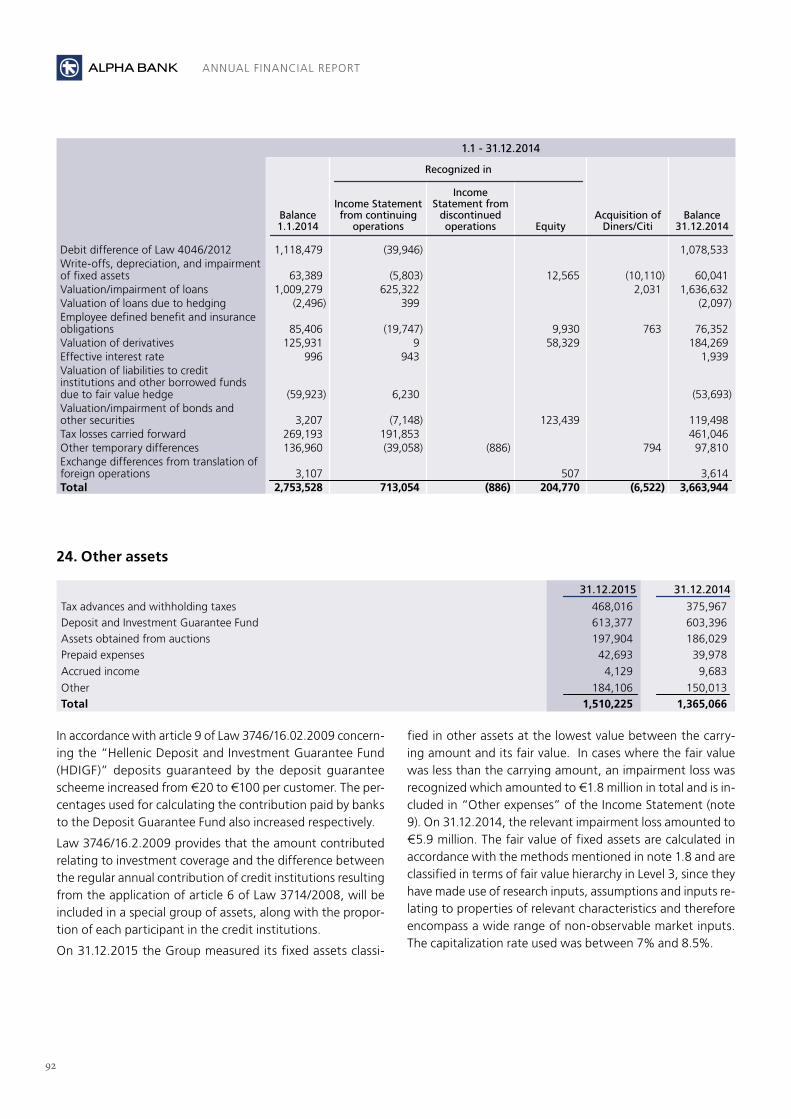

13 Cash and balances with Central Banks ............................................................................. 79 14 Due from banks ............................................................................................................. 79 15 Trading securities .......................................................................................................... 79 16 Derivative financial instruments (assets and liabilities) .......................................................80 17 Loans and advances to customers ................................................................................... 82 18 Investment securities .....................................................................................................84 19 Investments in associates and joint ventures .................................................................... 85 20 Investment property ...................................................................................................... 88 21 Property, plant and equipment ........................................................................................89 22 Goodwill and other intangible assets ............................................................................... 90 23 Deferred tax assets and liabilities .................................................................................... 91 24 Other assets .................................................................................................................. 92

Liabilities

25 Due to banks ................................................................................................................ 93 26 Due to customers (including debt securities in issue) .......................................................... 93 27 Debt securities in issue and other borrowed funds ............................................................ 93 28 Liabilities for current income tax and other taxes .............................................................. 95 29 Employee defined benefit obligations ...............................................................................96 30 Other liabilities ............................................................................................................102 31 Provisions ....................................................................................................................102

Equity

32 Share capital ............................................................................................................... 104 33 Share premium ............................................................................................................. 105 34 Reserves ...................................................................................................................... 105 35 Retained earnings ........................................................................................................ 106 36 Hybrid securities .......................................................................................................... 106

Additional information

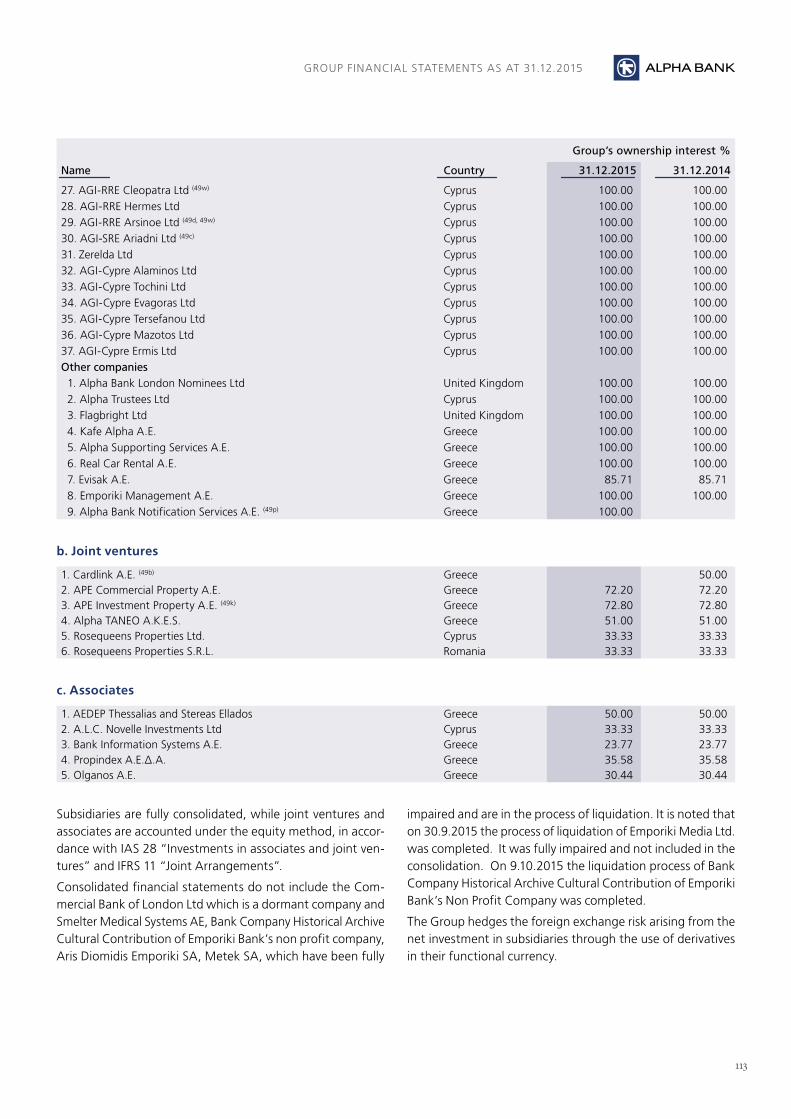

37 Contingent liabilities and commitments ......................................................................... 107 38 Group consolidated companies ...................................................................................... 111

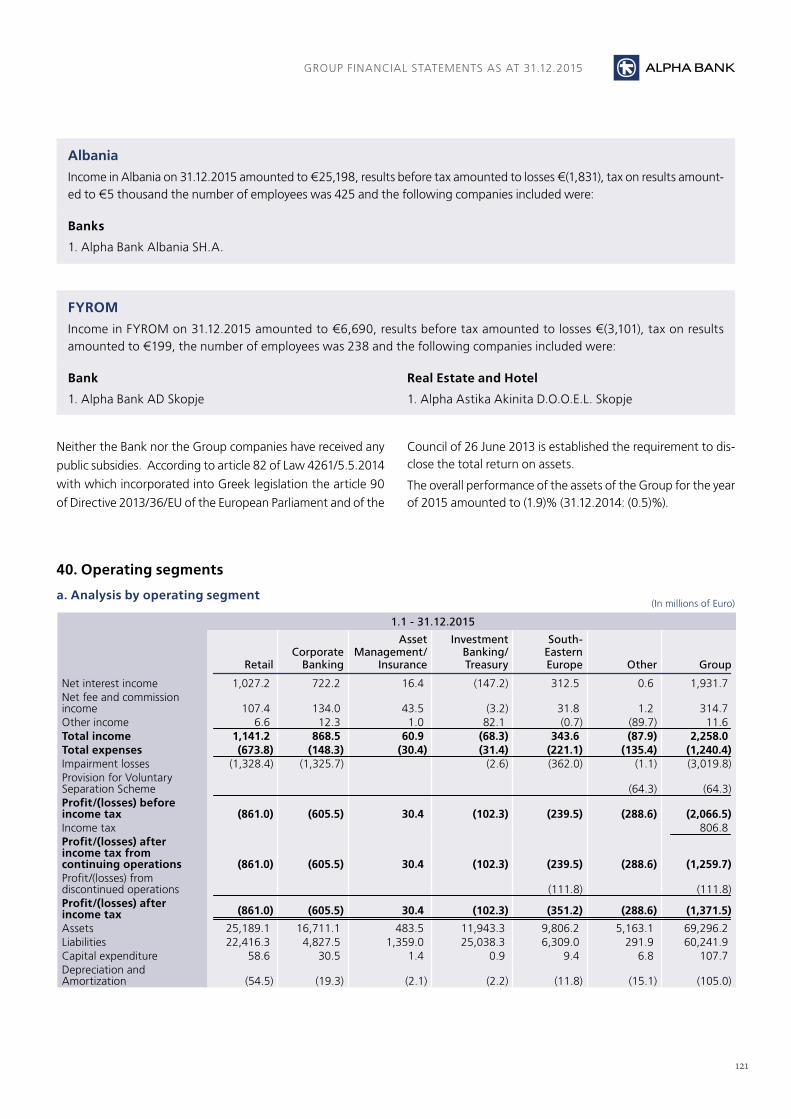

39 Disclosures of Law 4261/5.5.2014 .................................................................................. 118 40 Operating segments ..................................................................................................... 121 41 Risk management ......................................................................................................... 123 41.1 Credit risk management ................................................................................................. 123 41.2 Market risk .................................................................................................................. 151 Foreign currency risk ..................................................................................................... 151 Interest rate risk ........................................................................................................... 154 41.3 Liquidity risk ................................................................................................................. 157 41.4 Fair value of financial assets and liabilities ......................................................................162 41.5 Transfers of financial assets ............................................................................................ 165 41.6 Offsetting financial assets-liabilities ............................................................................... 166 42 Recapitalization framework – Restructuring Plan ............................................................. 168 43 Capital adequacy ......................................................................................................... 170 44 Related party transactions ............................................................................................. 171 45 Auditors’ fees .............................................................................................................. 172 46 Acquisitions of companies. ............................................................................................. 172 47 Disclosures of Law 4151/2013 …..……..……..……..……..……..……..……..……..……..…… 174 48 Assets held for sale and discontinued operations ……..……..……..…… ............................. 174 49 Corporate events .......................................................................................................... 178 50 Restatement of financial statements ...............................................................................179 51 Events after the balance sheet date................................................................................. 182

Independent Auditors’ Report (on Bank Financial Statements) ........................................................................................................... 183

Bank Financial Statements as at 31.12.2015

Income Statement .......................................................................................................................... 185

Balance Sheet ................................................................................................................................ 186

Statement of Comprehensive Income ............................................................................................. 187

Statement of Changes in Equity ..................................................................................................... 188

Statement of Cash Flows ................................................................................................................189

Notes to the Financial Statements

General Information .................................................................................................................. 190

Accounting policies applied

1.1 Basis of presentation ..................................................................................................... 192 1.2 Operating segments ..................................................................................................... 196 1.3 Transactions in foreign currency and translation of foreign operations .............................. 196 1.4 Cash and cash equivalents.............................................................................................. 197 1.5 Classification and measurement of financial instruments .................................................. 197 1.6 Derivative financial instruments and hedge accounting .................................................... 199 1.7 Fair value measurement ............................................................................................... 201 1.8 Investments in subsidiaries, associates and joint ventures ................................................. 202 1.9 Property, plant and equipment ...................................................................................... 202 1.10 Investment property .................................................................................................... 203 1.11 Goodwill and other intangible assets .............................................................................. 203

1.12 Leases ........................................................................................................................ 203

1.13 Impairment losses on loans and advances ...................................................................... 204

1.14 Impairment losses on non-financial assets ...................................................................... 205

1.15 Income tax .................................................................................................................. 205

1.16 Non-current assets held for sale .................................................................................... 205

1.17 Employee benefits ........................................................................................................ 206

1.18 Share options granted to employees .............................................................................. 207

1.19 Provisions and contingent liabilities................................................................................ 207

1.20 Sale and repurchase agreements and securities lending .................................................... 207

1.21 Securitization .............................................................................................................. 208

1.22 Equity ......................................................................................................................... 208

1.23 Interest income and expense ......................................................................................... 208

1.24 Fee and commission income .......................................................................................... 208

1.25 Gains less losses on financial transactions ...................................................................... 208

1.26 Discontinued operations ............................................................................................... 208

1.27 Related parties definition .............................................................................................. 209

1.28 Comparatives ............................................................................................................... 209

1.29 Estimates, decision making criteria and significant sources of uncertainty .......................... 209

Income Statement

2 Net interest income ...................................................................................................... 213

3 Net fee and commission income ..................................................................................... 213

4 Dividend income ...........................................................................................................214

5 Gains less losses on financial transactions ........................................................................214

6 Other income ...............................................................................................................214

7 Staff costs ................................................................................................................... 215

8 General administrative expenses ....................................................................................216

9 Other expenses ............................................................................................................. 217

10 Impairment losses and provisions to cover credit risk ........................................................217

11 Income tax ................................................................................................................... 217

12 Earnings /(losses) per share ........................................................................................... 220

Assets

13 Cash and balances with Central Banks ............................................................................221

14 Due from banks ............................................................................................................ 221

15 Trading securities .........................................................................................................221

16 Derivative financial instruments (assets and liabilities) ..................................................... 222

17 Loans and advances to customers ................................................................................. 224

18 Investment securities ....................................................................................................225

19 Investments in subsidiaries, associates and joint ventures ................................................ 226

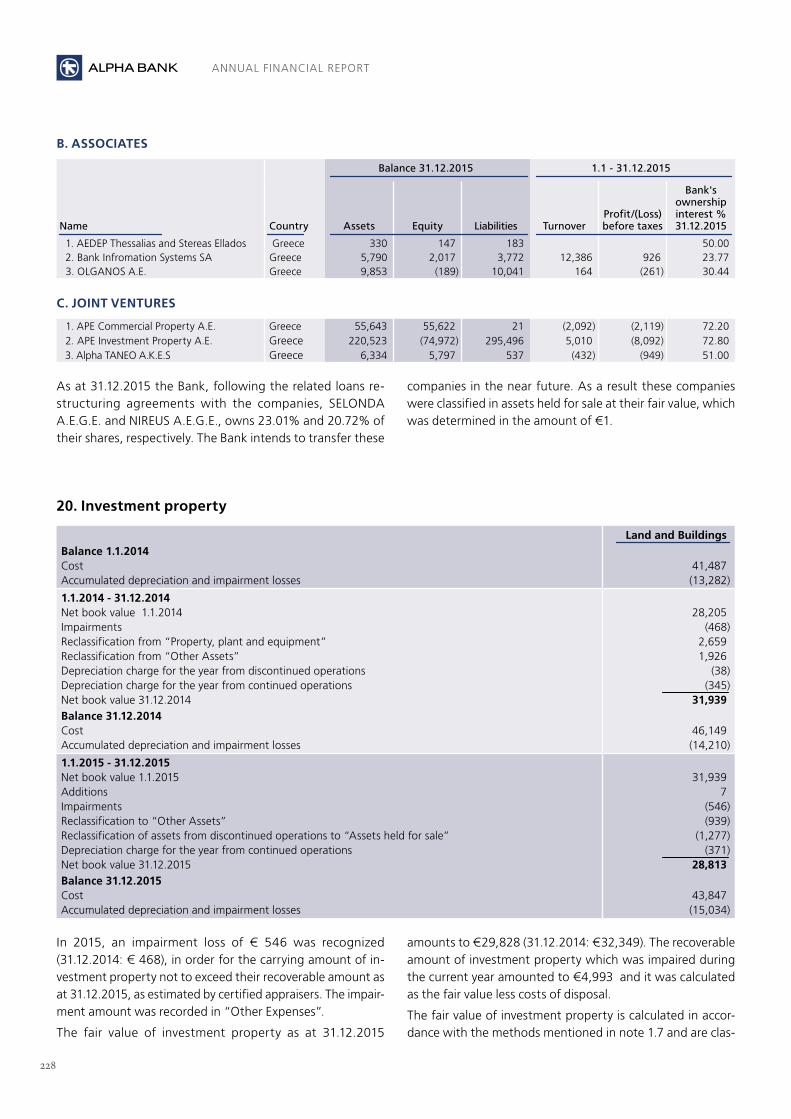

20 Investment property .................................................................................................... 228

21 Property, plant and equipment ...................................................................................... 229

22 Goodwill and other intangible assets ............................................................................. 230

23 Deferred tax assets ........................................................................................................ 231

24 Other assets .................................................................................................................232

Liabilities

25 Due to banks ...............................................................................................................233

26 Due to customers .........................................................................................................233

27 Debt securities in issue and other borrowed funds ...........................................................233

28 Liabilities for current income tax and other taxes .............................................................235 29 Employee defined benefit obligations ............................................................................ 236 30 Other liabilities ........................................................................................................... 242 31 Provisions ................................................................................................................... 242

Equity

32 Share capital ............................................................................................................... 243 33 Share premium ............................................................................................................ 244 34 Reserves ..................................................................................................................... 244 35 Retained earnings ........................................................................................................ 245

Additional information

36 Contingent liabilities and commitments ......................................................................... 246 37 Operating segments .................................................................................................... 249 38 Risk management ......................................................................................................... 251 38.1 Credit risk management ................................................................................................. 251 38.2 Market risk ................................................................................................................. 277 Foreign currency risk .................................................................................................... 277 Interest rate risk .......................................................................................................... 280 38.3 Liquidity risk ............................................................................................................... 283 38.4 Fair value of financial assets and liabilities ..................................................................... 288 38.5 Transfers of financial assets ...........................................................................................291 38.6 Offsetting financial assets-liabilities ............................................................................... 292 39 Recapitalization framework – Restructuring Plan ............................................................. 293 40 Capital adequacy ......................................................................................................... 295 41 Related party transactions ............................................................................................ 296 42 Auditors’ fees ............................................................................................................. 299 43 Acquisition of the Retail Banking operations of Citibank and Diners Club Greece A.E.P.P. .... 299 44 Current assets held for sale and discontinued operations ................................................. 302 45 Disclosures of Law 4151/2013 ....................................................................................... 304 46 Corporate events ......................................................................................................... 304 47 Restatement of financial statements ............................................................................. 305 48 Events after the balance sheet date ............................................................................... 307

Financial Information of Alpha Bank A.E. and the Group for the period from 1 January 2015 to 31 December 2015 (in accordance with Codified Law 2190/20, article 135 concerning businesses that prepare annual financial statements, consolidated or not, in accordance with IFRS) ................................................................................................................... 308

Report on the Use of Funds raised from the Share Capital Increase of ALPHA BANK AE ........ 311

Report of factual findings ............................................................................................................... 313

Information pursuant to article 10 of Law 3401/2005 ................................................................ 315

Availability of Annual Financial Report ....................................................................................... 317

7

Statement by the Members of the Board of Directors(in accordance with article 4 paragraph 2 of Law 3556/2007)

To the best of our knowledge, the annual financial state-ments that have been prepared in accordance with the ap-plicable accounting standards, give a true view of the assets, liabilities, equity and financial performance of Alpha Bank A.E. and of the group of companies included in the consolidated financial statements taken as a whole, as provided in article

4 paragraphs 3 and 4 of Law 3556/2007, and the Board of Directors' annual report presents fairly the evolution, perfor-mance and financial position of Bank, and group of companies included in the consolidated financial statements taken as a whole, including the analysis of the main risks and uncertain-ties that they face.

Athens, 3 March 2016

THE CHAIRMAN OF THE BOARD OF DIRECTORS THE CHIEF EXECUTIVE OFFICER THE EXECUTIVE DIRECTOR

VASILEIOS T. RAPANOSID. No ΑΙ 666242

DEMETRIOS P. MANTZOUNISID. No Ι 166670

ARTEMIS CH. THEODORIDISID. No ΑΒ 281969

9

Board of Directors’ Annual Management Report as at 31.12.2015

GREEK ECONOMy

The Greek economy, despite the strong headwinds of the last months, showed resilience that appears to mitigate the initially expected negative consequences, due to the pro-longed negotiations with the partners, the bank holiday and the imposition of capital controls. That was the result of the milder than expected consequences in the economy from the restrictions in capital movements, the significant increase of tourism activity and the big decline in oil prices.

The adjustment programmes implemented in our country since 2010, managed to address the main macroeconomic and fiscal imbalances, despite delays and divergences. Spe-cifically, the large general government deficit narrowed while the ¾ of total adjustment required was accomplished (final target for a primary surplus of 3.5% of GDP from 2018, as compared to a deficit of 10.1% of GDP in 2009).

Moreover, the current account deficit narrowed, losses in competitiveness recouped and the rigidities in labor market eased. Additionally, it was observed a notable restructuring in production in favor of tradable goods and services and generaly in favor of the more productive enterprises in each economic sector.The new Loan Agreement with the partners, contributed significantly to the decline in uncertainty and the restoration of confidence.

The main developments of the Greek economy are described below:

A. The real GDP recorded during the first half of 2015 a posi-tive rate of change of 0.6% which declined to -1.9% in the second half, due to the capital controls and the increase in tax rates. In 2015 as a whole, GDP fell by 0.7%, against an increase by 0.7% in 2014.

The economic activity was supported by the strong tourism performance and the rise of export of goods. Conversely, investment, revenues from shipping and imports were neg-atively affected by the capital controls and financing con-straints. Private consumption had a positive contribution to GDP growth in H1 2015, while in H2 of 2015 was negatively affected by the increase in tax burden which took a toll on households’ disposable income.

B. Concerning inflation developments, the national index of consumer prices decreased by 1.7% on average in 2015, com-pared to a fall of 1.3% in 2014, while the inflation rate based on the harmonized index registered a positive sign (+0.4%) in December 2015, for the first time since February 2013.

There is a notable deceleration of the deflationary process mainly from October 2015 until the end of the year. This development was triggered mostly by the increase in the

standard VAT rate from 13% to 23% for a large number of food products and services in August 2015. The impact of VAT hikes outweighed the deflationary pressures caused by the fall in oil prices and sluggish demand. In 2016 inflation is expected to increase in line with the expected economic recovery in the second half of the year.

C. Concerning the labor market, the employment rate grew by 1.8%, in January-November 2015 (Jan.-Nov. 2014: +0.5 %) on average, according to the seasonally adjusted data of ELSTAT (population of 15-74 age group). Moreover the num-ber of unemployed decreased significantly by 6.0% (Jan.-Nov. 2014: -4.0%). As a result, the average unemployment rate declined to 25.1% in January-November 2015, from 26.6% in January-November 2014.

Moreover, the employment population ratio increased to 44.4% in January-November 2015, compared to 43.3% in January-November 2014. Also, according to the ERGANI in-formation system data, the net flows of salaried employment were positive in 2015; a development which is the second best performance since 2001. In particular, in 2015, the bal-ance of net employment flows was positive to 99,700 per-sons, as compared to 99,100 in 2014.

D. Manufacturing production increased by 1.2% in 2015, while in the first half of 2015 increased by 1.9% yoy, sug-gesting that it managed to gain momentum quite rapidly, after the plunge the index registered during the summer, due to capital controls’ imposition. The industrial production in-creased by 0.6% in 2015, against a fall by 1.9% in 2014. The improving performance of Greek industry stemmed from the decline in oil prices as well as raw material and the deprecia-tion of the euro. The upsurge in tourist arrivals in 2015 had a significant contribution to the industrial production growth, mainly to the food and beverages sub-sector. It is noted that key sectors of Greek industry continue to increase their pro-duction, as they managed to redirect a significant part of their production to foreign markets as well.

It is encouraging that the purchasing managers’ index in manufacturing (PMI) rebounded relatively quickly in October 2015, and in December 2015 exceeded the threshold of 50 points at 50.2 (indicating a marginal increase of manufactur-ing output), for the first time since August 2014. The business confidence and in particular the Business Sentiment Indicator in industry rebounded sharply after its large decline registered last summer, as it started recovering since September 2015 and continued its upward trend until January 2016.

E. In external transactions, according to the Bank of Greece, the current account surplus amounted to €1.1 billion In Jan-uary-November 2015, against a significant deficit of €1.9

ANNUAL FINANCIAL REPORT

10

billion in the same period of 2014. This significant improve-ment in the balance of payments reflects the narrowing of the trade balance deficit (as imports registered a bigger fall than exports), which offset the decrease of the surplus of the services balance. Consequently, the 11month 2015 current ac-count balance recorded a surplus of 0.6% of GDP, against a deficit of 1.1% of GDP observed in the same period of 2014.

In particular, the balance of goods and services, which repre-sents the largest share of the current account balance (86.5% in Jan.-Nov. 2015), registered a surplus of €0.9 billion in Jan-uary-November 2015, compared to a deficit of €2.5 billion in the same period of 2014.The surplus of the services balance shrank by €1.1 billion. (Jan.-Nov. 2015: €16.7 billion, Jan.-Nov. 2014: €17.8 billion), as net transport receipts registered a de-cline, which was partly offset by a rise in net travel and other services receipts. Specifically, the travel surplus increased, al-beit at a decelerated pace, by 7.0% (Jan.- Nov. 2014: +10.1%). In 2016, tourism is expected to support the Greek economy for another year, benefiting from the relatively weak euro.

F. Regarding the fiscal adjustment in 2015 (cash based public data) a primary surplus of €4.1 billion or 2.4% of GDP was re-corded, compared to a primary surplus of €2.1 billion in 2014 (1.1% of GDP). Therefore, the target set for primary deficit of 0.25% of GDP, according to the new programme, seems achievable. This development was due to the better-than-ex-pected performance of government revenues during the last months of 2015 and the-larger-than-anticipated decrease of primary expenditure. The downward revision of the primary fiscal surplus targets in the following years, improves liquid-ity conditions in real economy. According to the Programme, a primary surplus target of 0.5% of GDP is set in 2016.

G. In 2015, the domestic banking system faced unprecedent-ed challenges.

The significant deposit outflow and the increase in non-per-forming loans (NPLs) ratio, caused turbulences at the Greek banking system and necessitated another comprehensive as-sessment and recapitalisation for the Greek banks.

In fall 2015, the European Central Bank conducted the com-prehensive assessment of the four significant Greek banks and the stress test identified, under the baseline scenario, an ag-gregate capital shortfall of €4.4 billion and under the adverse scenario, an aggregate capital shortfall of €14.4 billion. The recapitalisation of the Greek banking system was completed successfully in December 2015. The interest of foreign inves-tors was substantial as they placed around €5.3 billion in the four significant banks. Furthermore, an additional €2.7 billion was covered through liability management exercises (volun-tary bond swap offers to bank bondholders). Finally, the Hel-lenic Financial Stability Fund covered the necessary additional

funds for the two banks, i.e circa €5.4 billion, that was not covered by private investors.

The rate of contraction of bank credit to the private sector, which started since the second quarter of 2012, continued in 2015 mainly due to the feeble demand, albeit at a significant slower pace (December 2015: -2.0%1, December 2014: -3.1%). On end-December, 2015 the private sector loan outstanding amounted to €204.3 billion compared to €212 billion on end-December, 2014. In particular, the rate of contraction of bank credit to non-financial corporations sloweddown in Decem-ber 2015 to an annual rate of 0.9%, compared to a decline of 3.7% in December 2014. The respective rate of decline of bank credit to households, accelerated to 3.1% in December 2015, compared to - 2.9% in December 2014.

The reduced uncertainty combined with the imposition of capi-tal controls, resulted in the increase of private sector deposits by €2.5 billion, from end-July 2015 until the end-December 2015. However, the outstanding amount of private sector de-posits stood at €123.4 billion in December 2015, from €160.3 billion in December 2014, registering a fall by 23.0%. Concern-ing the structure of deposits, in 2015 compared to 2014, there was a fall in time deposits by 48.8% and an increase of savings deposits (+15.5%) and sight deposits (+10.3%). The substitu-tion of time deposits with savings deposits was more intense since July 2015, after the imposition of capital controls.

The expected improvement of the Greek economy from H2 2016 onwards will facilitate financial conditions.

Non-performing loans portfolio management and the return of deposits, remain the main challenges for the Greek banking system. The new framework for the management of the non-performing loans, improves the non-judicial remedies, deter-mines the terms for the protection of the main residence and enhances the bankruptcy law, thus restoring payment morale.

The front-loaded design of the new programme, which con-stitutes a structural element of the new agreement with the partners, enables the swift restoration of the business confi-dence and investment attraction, as the implementation of a large number of reforms are required before the first review of the programme.

INTERNATIONAL ECONOMy

The first weeks of 2016, reminded investors of last August, when the sudden devaluation of the Chinese currency by 2% caused strong turbulence to international markets. The sharp decline in stock prices in China and the depreciation of the yuan, reinforced investors’ concerns about a noteworthy slow-down in China's economic growth in 2016, accompanied this time by a significant decline in oil prices (lowest price for the last 12 years).

1 The rates of change are calculated taking into account the reclassification of loans , write-offs , disposals and exchange rate fluctuations.

BOARD OF DIRECTORS’ ANNUAL MANAGEMENT REPORT AS AT 31.12.2015

11

The prevalent position in the Organization of Petroleum Ex-porting Countries (OPEC) to maintain current production lev-els in order that members with lower production cost protect their market shares, as well as, the anticipated increase of pro-duction by Iran and Indonesia, lead to the expectation that the oil price will decline further. However, the price of oil and basic metals is likely to remain low for a long period. Already, copper price are at the lowest level since May 2009.

High volatility of stock markets recorded since the beginning of the year, which negatively affects economic activity, is not expected to disappear soon. In 2016, global economic growth will mainly depend on the stabilization of commodity prices and whether China's economy will succeed in avoiding major shocks, while moving from an economic growth model based on external demand, to one which is based on consumption and services. China aims to produce competitive goods and turn Chinese consumers to domestically produced goods, in-stead of imported ones. The ultimate purpose is both to sup-port economic growth and to offset the diminishing income.

However, it should not be forgotten that the heightening of geopolitical tensions is simmering and any time may disturb the international economic activity.

According to the most recent estimates by the International Monetary Fund (January 2016), world GDP is expected to grow by 3.1% in 2015, compared with 3.4% in 2014 and by 3.4% in 2016. As for the developed economies, they will reach a growth rate of 1.9% in 2015 and 2.1% in 2016 from 1.8% in 2014. International trade in goods and services is expected to record a rise in the current year (3.4%) and accelerate further in the next year (4.1%).

In the US, domestic demand was affected by adverse weather conditions in the first quarter of 2015, exports fell significantly and economic activity contracted. However, the dynamics of economic growth returned to higher levels for the rest of the year, as the effect of temporary factors started fading. Within a fragile global economic environment, better than expected positive employment figures in December, helped stabilizing the investment climate to some extent. Although, the US economy continues improving, it is not clear that it will register a notable rate of economic growth during 2016. In particular, the GDP growth rate in the US is expected to reach 2.5% in 2015 and 2.6% in 2016 from 2.4% in 2014.

In 2015, Japan’s growth rate is estimated to reach a positive level (0.6%) and further increase by 1.0% in 2016, compared to a negative growth rate (-0.1%) posted in 2014. Positive growth is attributed to fiscal stance, lower oil prices, favour-able economic conditions and rising household income.

In the Eurozone, GDP growth is expected to be 1.5% in 2015, compared with 0.9% in 2014, while during 2016 it is estimated to increase further by 1.7%. The recovery is based mainly on domestic demand, though it is still weak. The accommoda-

tive monetary policy pursued by the European Central Bank and the weakness of euro have positively contributed to eco-nomic growth.

Developing economies’ GDP is estimated to fall by 4.0% in 2015 from 4.6% in 2014 and increase by 4.3% in 2016.

China’s growth rate, after slowing down in 2015 to 6.9% from 7.3% in 2014, is expected to decelerate further in 2016 to 6.3% due to reduction in investment and the effort to render domestic consumption as the growth driver.

In the third quarter of 2015, according to most recent data, the SEE countries recorded an increase in economic activity. The highest growth rates were registered in Romania (3.6%) and FYROM (3.5%). The economy of Cyprus for the third con-secutive quarter posted a positive growth rate (2.2%) after fourteen consecutive quarters of recession, caused by the shrinking of the secondary sector and the difficulties in the financial industry. Moreover, the Serbian economy registered GDP growth (2.2%) for the second consecutive quarter, af-ter five consecutive quarters of negative performance as a result of the natural disasters in May 2014. Overall, the av-erage growth rate in Southeast Europe (excluding Turkey) is estimated to reach approximately 2.2% in 2015 and 2.5% in 2016, from 1.0% in 2014.

A key feature of the global economy is the prevalence of low inflationary pressures, particularly in developed economies, mainly due to the decline in energy and commodity prices.

In advanced economies, low inflation allows the continua-tion of expansionary monetary policy in order to strengthen recovery and improve the financial conditions of the private sector which indirectly will positively affect the public as well. The major Central Banks aim to increase inflation to a level close to 2%, with a combination of conventional and uncon-ventional measures of expansionary monetary policies such as very low, even negative, official interest rates, quantitative easing (QE) and forward guidance.

Analysis of financial statements

On 31.12.2015 the total assets amounted to €69.3 billion. This amount was reduced by €3.6 billion or 5% compared to 31.12.2014. At the end of December 2015, the total Group loans, before impairment, amounted to €58.2 billion, remain-ing stable compared to 2014 (€58.4 billion). The increase of accumulated impairments by €3.2 billion, resulted in the ad-justment of loans’ balance after impairment to €46.2 billion compared to €49.6 billion in 31.12.2014 .

The total deposits of the Group amounted to €31.4 billion, showing a decrease compared to 31.12.2014 by 26.7%, result-ing to a loan deposit ratio of 185%. This indicator was deterio-rated compared to 31.12.2014, when reached to 136%, as a result of the unstable economic and political environmentand the significant deposit ouflow during the year. The reduction

ANNUAL FINANCIAL REPORT

12

of the deposits led to the increase of the Group's funding from credit institutions (mainly the Eurosystem), which amounted to €25.1 billion, increasing by 45.2% compared to 31.12.2014.

In Assets held for Sale and Liabilities related to Assets held for sale, have been included the figures of the Bank’s Branch in Bulgaria and of its subsidiaries Alpha Bank A.D. Skopje and Ioniki Hotel Enterprises S.A., following the relevant decisions for the commencement of the sale procedure.

Regarding the sizes of the equity, the increase from €7.7 bil-lion on 31.12.2014 to €9.1 billion on 31.12.2015, reflects the successful share capital increase wholly from private sources during 2015. Particularly, the increase of the share capital by €2.6 billion was a result of the capitalization of money claims of 1 billion through the liability management exer-cise and of €1.5 billion paid in cash. Following the above in-crease, the share capital amounts to €0.46 billion, divided into 1,536,881,200 common, registered, voting shares, and the share premium amounts to €10.8 billion.

Analyzing the financial performance of the year, the net inter-est income amounted to €1,932 million and it was positively affected by the decrease of the deposits’ interest rates, but it was partially offset by an increased cost of capital due to the participation in the Emergency mechanism Liquidity As-sistance (ELA).

Net fee and commission income amounted to €314.7 million decreasing by 5.8% compared to the previous year, when amounted to €334.2 million. This reduction was a result of the bank holiday and the imposition of restrictions on capital movements.

Gains less losses on financial transactions recorded a loss of €45 million, having mainly affected negatively by the liabil-ity management exercise which was completed in November 2015. Group's total revenue amounted to €2,268 million, re-duced by 3.9% compared to 2014 when amounted to €2,360 million.

Group’s total expenses, amounted to €1,305 million, reduced by 16% compared to 2014 when amounted to €1,554 million mainly due to the decrease of the personnel cost. This was a result of the successful completion of the voluntary retirement program in the last year.

The impairment losses and provisions to cover credit risk amounted to €3,020 million compared to €1,847 million in 2014. This increase was a result of specific macroeconomic conditions during the year.

In a Group level the income tax is credit and it amounts to €806.8 million. The income tax has been affected by €398 million due to the change in the tax rate from 26% to 29%. Profit/(loss) after income tax from continuing operations amounted to losses of €1,260 million. and the profit/(loss) after income tax from discontinued operations amounted to losses of €111.8 million, including the negative fair valuation

of Bulgaria Branch which amounted to €89 million, and of Alpha Bank AD Skopje which amounted to €14 million.

Participation in the program for the enhancement of liquidity of the Greek economy

In the context of the program for the enhancement of the Greek economy’s liquidity, according to Law 3723/2008, the Bank proceeded with:

• TheissuanceofseniordebtsecuritiesguaranteedbytheGreek State amounting to €9.2 billion.

These securities are pledged to the European Central Bank to obtain liquidity.

Other information

The Bank’s Ordinary General Meeting of the Shareholders on 26.6.2015 decided the following:

i) The non distribution of dividend to the common sharehold-ers.

ii) The non payment to the Greek State of the return of 2014 as defined by Article 1 paragraph 3 of Law 3723/2008 of the preference shares owned by the Greek State until 17.4.2014.

Risk management

Alpha Bank Group has established a framework of thorough and discreet management of all kinds of risks facing on the best supervisory practices and which is based on the common European legislation and the current system of common bank-ing rules, principles and standards is improving continuously over the time in order to be applied in a coherent and effec-tive way in a daily conduct of the Bank's activities within and across the borders.

The main objective of the Group was to maintain the high quality internal corporate governance and compliance within the regulatory and supervisory provisions risk management. This will have as a result to ensure the confidence in the busi-ness field based on suitable financial services.

Since November 2014, the Group falls within the Single Super-visory Mechanism (SSM) - the new financial supervision sys-tem which involves the European Central Bank (ECB) and the Bank of Greece - and as a major banking institution is directly supervised by the European Central Bank (ECB). The Single Su-pervisory Mechanism is working with the European Banking Authority (EBA), the European Parliament, the Eurogroup, the European Commission and the European Systemic Risk Board (ESRB) within their respective competences.

Moreover, since January 1, 2014, EU Directive 2013/36/EU of the European Parliament and of the Council dated June 26, 2013 along with the EU Regulation 575/2013/EU dated June 26, 2013 (“CRD IV”) are effective. The Directive and the Reg-ulation gradually introduce the new capital adequacy frame-work (Basel III) of credit institutions.

BOARD OF DIRECTORS’ ANNUAL MANAGEMENT REPORT AS AT 31.12.2015

13

In this new regulatory and supervisory risk management frame-work, Alpha Bank Group strengths its internal governance and its risk management strategy and redefining its business model in order to achieve full compliance within the increased regula-tory requirements and the extensive guidelines. The latest ones are related to the governance of data risks, the collection of such data and their integration in the required reports of the management and supervisory authorities.

The Group’s new approach constitutes of a solid foundation for the continuous redefinition of Risk Management strategy through (a) the determination of the extent to which the Bank is willing to undertake risks (risk appetite), (b) the assessment of potential impacts of activities in the development strat-egy by defining the risk management limits, so that the rel-evant decisions to combine the anticipated profitability with the potential losses and (c) the development of appropriate monitoring procedures for the implementation of this strategy through a mechanism which allocates the risk management responsibilities between the Bank units.

More specifically, the Group taking into account the nature, the scale and the complexity of its activities and risk profile, develops a risk management strategy based on the follow-ing three lines of defense, which are the key factors for its efficient operation:

• DevelopmentUnitsofbankingandtradingarrangements{host functions and handling customer requests, promotion and marketing of banking products to the public (credits, deposit products and investment facilities), and generally conduct transactions (front line)}, which are functionally separated from the requests approval units, confirmation, accounting and settlement. They constitute the first line of defense and 'ownership' of risk, which recognizes and man-ages risks that will arise in the course of banking business.

• ManagementandcontrolriskandregulatorycomplianceUnits, which are separated between themselves and also from the first line of defense. They constitute the second line of defense and their function is complementary in con-ducting banking business of the first line of defense in or-der to ensure the objectivity in decision-making process, to measure the effectiveness of these decisions in terms of risk conditions and to comply with the existing legisla-tive and institutional framework, by involving the internal regulations and ethical standards as well as the total view and evaluation of the total exposure of the Bank and the Group to risk.

• InternalauditUnits,whichareseparatedfromthefirstandsecond line of defense.

They constitute the third line of defense, which through the audit mechanisms and procedures cover an ongoing basis of all operation of the Bank and the Group. They ensure the consistent implementation of the business strategy, by in-

volving the risk management strategy through the true and fair implementation of the internal policies and procedures and they contribute to the efficient and secure operation.

Credit Risk

Credit risk arises from the potential weakness of borrowers’ or counterparties’ to repay their debts as they arise from their loan obligations to the Group.

The primary objective of the Group's strategy for the credit risk management is to achieve the maximization of the ad-justed relative to the performance risk, by ensuring at the same time the conduct of daily business within a clearly de-fined framework of granting credit. This framework has been supported by strict credit criteria and it is the continuous, timely and systematic monitoring of the loan portfolio and the maintenance of the credit risks within the framework of acceptable overall risk limits.

The framework of the Group’s credit risk management is de-veloped based on a series of credit policy procedures, systems and measurement models by monitoring and auditing models of credit risk which are subject to an ongoing review process. This happens in order to ensure ful compliance with the new institutional and regulatory framework as well as the inter-national best practices and their adaptation to the require-ments of respective economic conditions and to the nature and extent of the Group's business.

The indicative actions below represent the development and improvement that occurred in 2015 with respect to the afore-mentioned framework:

• OngoingupgradeofWholesaleandRetailBankingCreditPolicies in Greece and on abroad in order to be adapted in the given macroeconomic and financial conditions of the Group's risk profile as well as in the acceptable maximum risk appetite limits totally for each kind of risk.

• Ongoingupdateofthecreditratingmodelsforcorporateand retail banking in Greece and on abroad in order to en-sure their proper and effective operation.

• UpdateoftheimpairmentpolicyforWholesaleandRetailBanking.

• Centralizedandautomatedapprovalprocessforretailbanking applications in Greece and abroad.

• Completecentralizationofthecollectionspolicymecha-nisms for retail banking (mortgage loans, consumer loans, credit cards, retail banking corporate loans) in Greece and abroad.

• Systematicestimationandassessmentofcreditriskpercounterparty and per sector of economic activity.

• Periodicstresstestsasatoolofassessmentofconsequenc-es of various macroeconomic scenarios to establish the business strategy, the business decisions and the capital

ANNUAL FINANCIAL REPORT

14

position of the Group. The stress tests are performed ac-cording to the requirements of the regulatory framework and they are fundamental parameters of the Group’s credit risk management Policy.

Additionally, the following actions are in progress in order to enhance and develop the internal system of credit risk management:

• Continuationofthepreparationforthetransitionprocessfor the Bank and the Group companies, including the port-folios of the former Emporiki Bank and Citibank in Greece, to the Advanced Method for the Calculation of Capital Requirements against Credit Risk. For the purpose of this transition, the Advanced Internal Ratings-Based Approach method will be used with regards to the corporate loan portfolios, retail banking, leasing and factoring.

• Determiningaspecificframeworkforthemanagementof overdue and non-performing loans, in addition to the existing obligations, which arise from the Executive Com-mittee Act 2015/227 of January 9, 2015 of the European Committee for amending Executive Committee Act (EU) No. 680/2014 of the Committee for establishing execu-tive technical standards regarding the submission of su-pervisory reports by institutions in accordance with the regulation (EU) No. 575/2013 of the European Parliament and the Council and Executive Committee Act of Bank of Greece, P.E.E. 42/30.5.2014 and the amendment of this with the Executive Committee Act of Bank of Greece, P.E.E. 47/9.2.2015, which define the framework of super-visory commitments for the management of overdue and non-performing loans from credit institutions.

This framework develops based on the following pillars:

a. The establishment of an independent operation man-agement for the “Troubled assets” (Troubled Asset Com-mittee). This is achieved by the representation of the Ad-ministrative Bodies in the Evaluation and Monitoring of Denounced Customers Committee as well as in the Ar-rears Councils,

b. The establishment of a separate management strategy for these loans, and

c. The improvement of IT systems and processes in order to comply with the required periodic reporting to manage-ment and supervisory mechanisms.

• Continuousupgradeofdatabasesforperformingstatis-tical tests in the Group’s credit risk rating models. Up-grade and automatisation of the aforementioned process in relation to the Wholesale and Retail banking by using specialized statistical software. Gradual implementation of an automatic interface of the credit risk rating systems with the central systems (core banking systems I-flex) for all Group companies abroad.

Reinforcing the completeness and quality control mechanism of crucial fields of Wholesale and Retail Credit for monitoring, measuring and controlling of the credit risk.

Liquidity, interest rate and foreign exchange risk of banking portfolio

2015 was a crucial year for the Greek economy and the Greek banking system. The political uncertainty created by the an-nouncement of the national elections, the fear of non-com-pliance with the debt repayment program and non-agree-ment with their partners for the expansion, as well as the prolonged period of negotiations led to the imposition of the capital controls in banking system. This had as an effect the reduction of the capital sources from the banking system. In the first half of 2015, due to the uncertainty the deposits dropped significantly both at a Bank and Group level. Thus, on 30.06.2015 the deposits of the Bank decreased by 29% compared to 31.12.2014 and the deposits of the Group’s subsidiaries decreased 9.4%, respectively. The result from these developments was that on 30.06.2015 Bank's financ-ing from the Eurosystem raised to €27.8 billion, from which €23 billion came from the emergency funding mechanism of Bank of Greece (ELA).

In the second half of 2015, after the announcement of the the stress tests results, the Bank successfully completed on 25.11.2015 the share capital increase of € 2.563 billion.

More specifically, the share capital increase was a result of both the deposit in cash of €1.552 billion via private investors and the capitalization of the financial receivables amounting to €1.011 billion through voluntary exchange of existing secu-rities from holders who participated in the Liability Manage-ment Exercise. The successful capital increase in conjunction with the restriction of uncertainty and the reinstatement of confidence with the new loan agreement with the partners and stabilization of the political climate after the elections of September, led to a slight increase in deposits during the last quarter of 2015 and also to the conduction of repo transac-tions with third parties. At the end of 2015, our lending by the Eurosystem amounted to EUR 24.4 billion, from which €19.6 billion came from the ELA.

Under the new requirements of the Regulatory Environment (Basel III) for liquidity, the stability, cost and the diversifica-tion of liquidity sources are systematically monitored. During 2015, the new Liquidity Coverage Ratio has been submitted on a monthly basis with a limit of 60%,along with the sub-mission of the Net Stable Funding Ratio on a monthly basis as well. The detailed conditions for both the liquidity and the analysis of financing sources and the effects of regula-tory interest rate crisis scenarios on Group’s profitability are given on a quarterly basis in the Single Supervisory Mecha-nism (SSM).

During 2015, Bank has renewed and updated the policies

BOARD OF DIRECTORS’ ANNUAL MANAGEMENT REPORT AS AT 31.12.2015

15

and procedures of the Recovery Plan. Given the compromised situation of the Greek economy, the Bank’s subsidiaries have been asked by their local supervisors, to renew and update, apart from the Contingency Funding Plans, the Recovery Plans as well.

The continuous update of the ALM system, in which all Bank's reports are based, is essential for the evolution and the de-velopment of the product mix of the Bank, by taking into ac-count the current structure of competition and the economic conditions. In particular, the audit and the finalization of the conventions of repricing and of movement of non-maturing assets-liabilities are parts of the efficient and the effective management of asset liability risk. It has to be noted that at the end of 2015, in accordance with the new directions of the European Banking Authority, a review of all applicable assumptions has been completed as a part of the annual up-date of the applied assumptions.

The interbank financing (short, medium to long-term) and the Early Warning Indicators of the Bank and of Group’s sub-sidiaries and foreign branches are monitored on a daily basis with reports and checks in order to capture daily variations.

In a monthly basis, stress tests are incurred for liquidity pur-poses in order to assess potential outflows (contractual or contingent). The purpose of this process is to determine the level of the immediate liquidity which is available in order to cover the Bank's needs. These exercises are carried out in ac-cordance with the approved, in 2015, Liquidity Buffer and Liquidity Stress Scenario of Group’s policy.

Moreover, the stress tests are implemented for interest rate risk purposes of the Banking Portfolio in order to estimate the volatility of the net interest income of the banking portfolio and the value of the customer loans and deposits.

Market and Counterparty Risk

The Group has developed a strong environmental control policies and procedures in accordance with the regulatory framework and the international best practices. This policies and procedures meet the business needs, which involve mar-ket risk and counterparty limiting adverse impact on results and equity. The framework of methodologies and systems for the effective management of those risks is evolving on a con-tinuous basis in accordance with the changing circumstances in the markets and in order to meet customer requirements.

The valuation of bonds and derivative positions are monitored on an ongoing basis. Each new position is examined for its characteristics and an appropriate valuation methodology is developed, in case it is required. On a regular basis stress tests are conducted in order to assess the impact on the results and the equity, in the markets where the Group operates.

A detailed structure for transaction limits, counterparty in-vestment positions and country limits have been adopted and

implemented. This structure involves regular monitoring of trigger events in order to perform extra revisions. The control limits are monitored on an ongoing basis and any violations are reported officially.

For the mitigation of the market risk of the banking portfo-lio, hedging relationships are applied to the derivatives and hedge effectiveness is tested on a regular basis.

In 2015, there were problems in conducting operations in foreign currency financing due to the restrictions on capital movements and the reduction or withdrawal of interbank credit lines. This had as a result the increase in the open currency position of the Group. As market conditions are improved, the Group gradually reduces these positions. Fur-thermore, on a continuous basis the valuation parameters for Greek market bonds and derivatives were monitored. The purpose of this exercise is their update in the event of illiquidity for valuation purposes and risk monitoring. New negotiation and investment limits, counterparties and coun-tries for various Group companies have been reviewed and implemented according to the ordinary and extraordinary re-visions. Moreover, the monitoring of the report of the Group’s exposure in market and counterparty risks has been enriched.

Additionally, the model to calculate Credit Valuation Adjust-ment was evaluated under Greek Comprehensive Assessment and it was carried out by the European Central Bank result-ing in a minimal impact on equity. The Bank participated in the exercise in order to assess the impacts (QIS) of exempted positions from the calculation of own funds requirements for counterparty risk in credit valuation adjustment (CVA), which were organized by the European Banking Authority in cooperation with the National Supervisory Authorities and the European Central Bank (ECB).

Operational Risk

In the context of the continuous improvement in the imple-mentation of the operational risk management framework, the Bank proceeded intensively to the expansion of preventive measures in order to identify and evaluate risk as well as, to the enhancement of the process of collecting and analyzing operational risk events.

More specifically, the RCSA method of operational risk self-assessment has been implemented during the year in accor-dance to the general plan for selected divisions as well as, for domestic and foreign Bank subsidiaries. It is noted that this method provides the recognition and assessment of po-tential operational risks through the implementation of au-dits (residual risks). Further to the above, the respective divi-sions proceed with the appropriate actions in order to hedge against negative results.

An Advance Measurement Approach for the Bank has been prepared in order to be implemented.

ANNUAL FINANCIAL REPORT

16

The events of operational risk, the self-assessment results as well as, other current issues of operational risk are sys-tematically monitored both in Bank and Group level by the competent Operational Risk Management Committees with increased responsibilities which are related to the review of relevant information as well as to the adoption of Operational Risk mitigation measures.

Management Non Performing Loans (NPLs)

The quality of the Bank's loan portfolio deteriorated in the fourth quarter of 2008 till the fourth quarter of 2014 as a re-sult of the prolonged recession of the Greek economy where GDP fell by 24.3%2. This had as a consequence an increase of the non-performing loans (NPL) in all individual portfolios. In response to these challenges, the Bank focused on three key prevention and strategies of NPLs:

• Focusonrecoveryrequirementsattempts,particularlyinrelation to the borrowers in early delays

• Improvementofcollateralsthroughextraunderwritings

• Offerforbearanceproductstoborrowersinanefforttoal-leviate short-term financial difficulties. This ensures that the Bank could complete these products, if necessary, since a more stable macroeconomic environment will allow a bet-ter assessment of the financial capacity for the borrowers.

However, in a very challenging economic environment, the Bank constantly reviews and adjusts its strategy for the man-agement of NPLs. During 2014 and 2015, the Bank has imple-mented a major change in the infrastructure management and NPLs strategy, using Bank of Greece recommendations of for non-performing loans (Troubled Asset Review) and the Act 47 of the Executive Committee.

The development and launch of targeted long-term arrange-ments represents a significant shift from the past, where the focus was short-term arrangements. In addition, efforts for the increased collectability and collateral improved levels re-main a key aspect of the Bank's strategy.

At the same time key operating indicators were adapted and updated accordingly:

• Organizationalrestructuring:Majorredesignwhilecreat-ing and developing appropriate and independent man-agement structures. The latest ones, in addition to the improvements in the overall governance structure, provide increased control over governance as well as the implemen-tation of evidence-based practices and policies regarding the management of past due portfolio.

• SegmentationandPortfolioAnalysis:clearlydefinedanddetailed strategies are in progress, including a strict frame of segmentation.

• Flexibleandupgradedforborneproductsaswellasdefini-tive settlement process (for example court settlements).

• Humanresourcesmanagementwithspecificgroupsandtargeted training.

• Significantinvestmentintechnologicalequipmentandauto-mated decision-making tools (for example NPV calculators)

These functional changes are related to major strategic move-ments, and more specifically:

• JointVenturewithAktua(whichisaspecializedproviderof loan services, group member of Centerbridge). This joint venture, which is based on the current negotiations, is ex-pected to start its operations in the first quarter of 2016. This action will allow the Bank to manage more effectively the portfolio of the non-performing loans as well as the real estate which is under its ownership (REO).

• Budgetandlossesallocationframework:theBankelabo-rates with an international consultant in order to facilitate the implementation of its strategy for the restructuring of the portfolio of non-performing loans. This framework provides:

i. Loss distribution into sub-portfolios in order to achieve better non-performing loans management objectives.

ii. Key performance indicators control of the Bank's NPLs management strategy

iii. Find proper strategies per groups / classes

• RepossessionPropertyStrategy(REO):Evaluationoftheex-isting Repossession Property strategy in order to determine the best way and maximize at the same time their value for the Bank in the current economic environment.

Some of the above initiatives are already in place (e.g, organi-zation, systems), while others have been already developed and implemented over the past months.

In addition, it is expected that the above initiatives will be ben-efited from the changes in the Greek legislative framework and the improvement in the economic climate.

More specifically:

• StructuralReforms:Theimplementationoftheplannedstructural reforms, as they are stated in the third loan agreement, is expected to create the necessary conditions for the banks in order to implement the best possible way for their strategy. Particularly, the expanded reform of Jus-tice, the new civil procedure code, the changes regarding the residential property either the auction suspension re-moval of the principal residence or the private creditors al-leviation are some of them.

• Improvedmacroeconomicenvironmentforecast:Theesti-

2 ELSTAT http://www.statistics.gr/portal/page/portal/ESYE/PAGE-themes?p_param=A0704&r_param=SEL84&y_param=TS&mytabs=0, table 13

BOARD OF DIRECTORS’ ANNUAL MANAGEMENT REPORT AS AT 31.12.2015

17

mated improvement of the Greek economy, in accordance with the increase of capital controls (capital controls), is ex-pected to improve the ability of borrowers who have made debt restructuring in order to follow repayment schedules. It is also expected that they will enhance the reliability of the planned business projects, by enhancing the value of the existing collaterals.

Administrative Structure Division - Arrears Management:

The Bank realised the need to invest in the NPLs manage-ment and made an effort to streamline the monitoring func-tions and past due exposure management. Specialized teams have been established within the Bank in order to monitor the evolution of those apertures, achieving at the same time targeted settings which are in line with Bank’s strategy.

Organizational Structure and Corporate Governance

Since 2009 discrete units for Retail and Wholesale past due loans monitoring have been established and they are the key pillars of the Bank. These independent Units report directly to the Bank CEO through the Directors of each division. More-over, they are responsible for all the areas which are related to the loan management – such as monitoring the portfolio and the first line services. Through those Units, the Bank has achieved the distinction of arrears management, from the Relationship Management and the Approval Authorities, by combining automated and massive procedures for portfolio’s low-risk segments of and case by case management of port-folio’s complex or high-risk segments.

Furthermore, the Exposure in arrears Monitoring Commit-tee contributed to the strategic alignment of the Retail & Wholesale strategy.

Exposure management of arrears strategy

Investing in the organizational structure of arrears units,the Bank has developed a strategic framework for the troubled assets in line with the Act 47 / 02.09.2015 of the Executive Committee of the Bank of Greece and the banks' Code of Conduct.

The procedures are defined based on the delinquency bucket and / or whether the borrower is viable or not (Going Concern vs. Gone Concern) status. In this way, the fragmentation of the non-performing portfolio by using financial indicators and techniques analyzes have been achieved. The policies and procedures of sophisticated control mechanisms on the front line processes, such as daily monitoring of tax collec-tion companies and by strengthening the control mechanisms for collection agencies and law firms (including the frequent on-site visits) are key pillars of the management of the non-performing loans for the Bank's management.

The Exposure in arrears Monitoring Committee has an im-portant role in the overall exposures in arrears management.

Prospects for the future

With the exception of USA where the contractionary mon-etary policy is expected to be maintained in 2016, the cen-tral banks of other developed economies follow a relaxed monetary policy. In January 2016, the Bank of Japan fol-lowed the example of the central banks in Sweden, Denmark, Switzerland and the European Central Bank and completed the quantitative easing measures by imposing a -0.1% nega-tive interest rate on deposits of financial institutions held in the BoJ.

In Europe, the negative deposit facility rate is the benchmark for the money and loan markets. Thus, yields of the Ger-man government bonds have been negative for the shorter maturities (16 February 2016). Negative interest rates are about to squeeze the European banks’ profitability as de-posit rates are expected to exhibit a higher degree of rigidity, compared to the lending rates, given that depositors could switch to cash.

Concerns about global economy weakening due to sluggish demand from China and the risks for further deceleration of growth rates, affected negatively the international capital markets in 2016. At the same time there are concerns, about the low commodity prices reflected in share prices and cor-porate bonds in both the US and European markets, that increased even further in January and February 2016 due to new turmoil that hit emerging markets.

These developments, as expected, affected significantly stock prices in the Athens Stock Exchange after the recapitaliza-tion of Greek banks and deteriorated the investment climate in our country, in a period where the first review of the new program is expected to be completed. Thus, since the begin-ning of 2016 the stock prices at the Athens Stock Exchange declined significantly (until 26.02.2016, Athex Composite Index: -19.68%, Banks Index: -47.40%).

At the beginning of 2016, the Greek economy is in a critical situation. The course of the economic activity in 2016 is re-lated to the successful completion of the first evaluation of the program and the implementation of the reformulations. The completion of the first evaluation is crucial since it will impact positively the confidence and it will create discussions with partners in order to take actions (such as the debt re-lief) with a favorable effect on the financing as well as in the development of the Greek economy.

The growth rate of the real GDP is expected to remain nega-tive in 2016, at least in the first half of the year, due to the negative carry-over effect of 2015 and the impact of the increased tax burden on households' disposable income. The confidence needs to be restored and the liquidity in the banking system needs to be strengthened in order to achieve a gradually recovery of the economy, in the second half of 2016.

ANNUAL FINANCIAL REPORT

18

Related parties

According to the corresponding regulatory framework, this report must include the main transactions with related par-ties. All the transactions between related parties, the Bank and the Group companies, are performed in the ordinary course of business, conducted according to market conditions and are authorized by corresponding management person-nel. There are no other material transactions between related parties beyond those described in the following paragraph.

a. The outstanding balances of the Group transactions with key management personnel which is composed by members of the Board of Directors and the Executive Committee of the Bank, as well as their close family members and the com-

panies relating to them, as well as the corresponding results

from those transactions are as follows:

Loans and advances to customers 11,460

Due to customers 26,200

Employee defined benefit obligations 453

Letters of guarantee and approved limits 11,689

Interest and similar income 242

Fee and commission income 147

Interest expense and similar charges 166

Fees paid to key management and close family members 3,469

(Amounts in thousand of Euro)

b. The outstanding balances and the corresponding results of the most significant transactions of the Bank with Group com-panies are as follows:

Name Assets Liabilities Income Expenses

Letters of guarantee and

other guarantees