Annual Report - 2020 CD - gestetnersl.com

83

Transcript of Annual Report - 2020 CD - gestetnersl.com

ANNUAL REPORT

19/20

G E S T E T N E R O F C E Y L O N P L CP A G E

01

02 | GROUP HIGHLIGHTS

03 | CHAIRMAN’S REVIEW

04 | BOARD OF DIRECTORS

07 | CORPORATE GOVERNANCE

11 | REPORT OF THE BOARD AUDIT COMMITTEE

12 | ANNUAL REPORT OF THE BOARD OF DIRECTORS

16 | STATEMENT OF DIRECTORS’ RESPONSIBILITIES

17 | RELATED PARTY TRANSACTIONS REVIEW COMMITTEE REPORT

19 | INDEPENDENT AUDITOR’S REPORT

25 | STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

26 | STATEMENT OF FINANCIAL POSITION

27 | STATEMENT OF CHANGES IN EQUITY

28 | STATEMENT OF CASH FLOWS

30 | NOTES TO THE FINANCIAL STATEMENTS

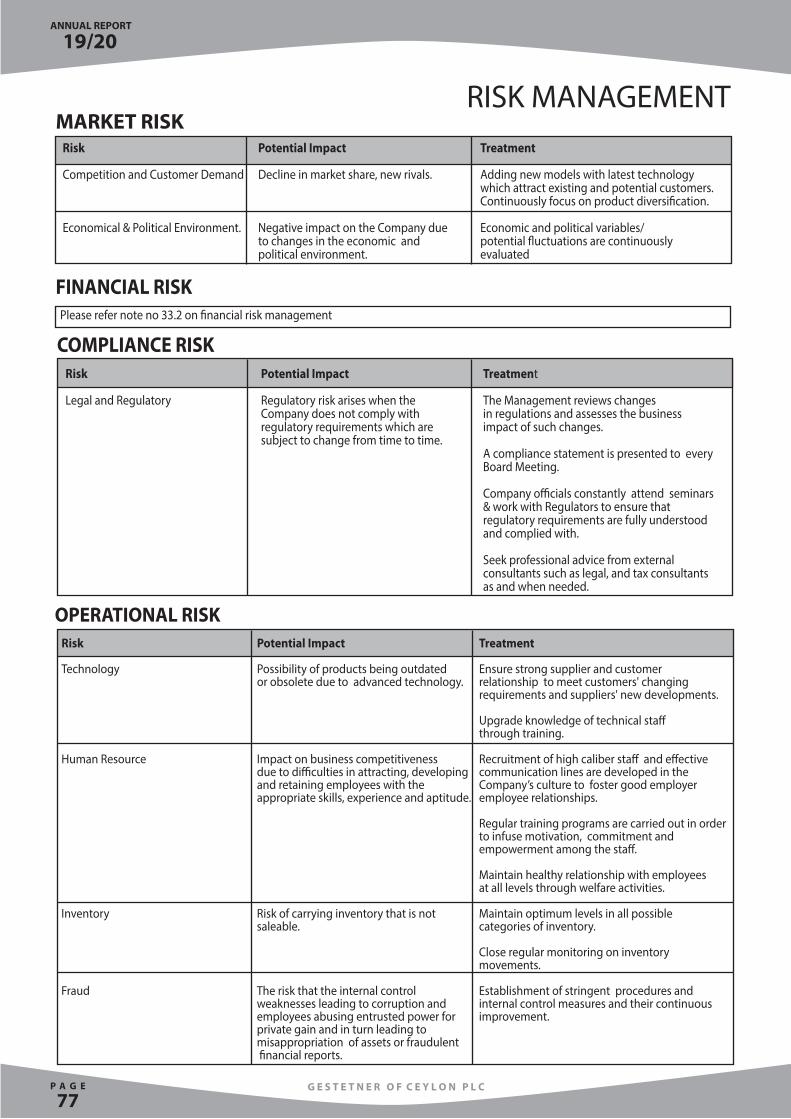

77 | RISK MANAGEMENT

78 | TEN YEAR SUMMERY

79 | INVESTOR INFORMATION

80 | NOTICE OF MEETING

C O N T E N T S

ANNUAL REPORT

19/20

G E S T E T N E R O F C E Y L O N P L C P A G E

02

2019/2020 2018/2019

Results for the year (Rs.Mn)

Group revenue 1,035 909

Pro�t from operations 15 64

Pro�t / (Loss) before tax (13) 56 As at 31st March

Total Assets (Rs Mn) 740 558

Total Liabilities (Rs Mn) 429 245

Current Ratio (times) 1.16 1.91

Per share (Rs.)

Earnings Per share (1.75) 16.14

Dividend per share - 1.25

Net asset value per share as at 31st March 116.83 117.82

Market price per share as at 31st March 91.00 88.00

GROUP HIGHLIGHTS

ANNUAL REPORT

19/20

G E S T E T N E R O F C E Y L O N P L CP A G E

03

CHAIRMAN’SREVIEW

I have pleasure, on behalf of the Board of

Directors, to present you the Annual Report and

Accounts of Gestetner of Ceylon PLC for the year

ended 31st March 2020.

An Overview

The Group’s turnover for the year under review

was Rs. 1,035 million. However, the Group had a

loss of Rs.4.6 million due to increase in other

operating expenses, early stage of operations in

new subsidiary, Fintek Managed Solutions (Pvt)

Ltd as well as the impacts of Covid 19 including

the virtual close down of operations in March

2020 and the impairment adjustments that

were based on the impacted performances over

the post year-end periods.

Dividends

The Directors are not proposing the payment of

any dividends for the year under review.

Conclusion

My sincere thanks are due to the other Directors

for support and assistance and to all the

employees at all levels for their dedicated and

committed service. I also wish to express my

appreciation for the continued support from

our shareholders, overseas principals, bankers,

suppliers and other stakeholders.

S J M Anzsar FCA Chairman

ANNUAL REPORT

19/20

G E S T E T N E R O F C E Y L O N P L C P A G E

04

L R WATAWALANon - Executive Director

S J M ANZSARChairman / Non - Executive Director

Mr. S J M Anzsar was appointed to the Board of Gestetner of Ceylon PLC on 7th January 1997 and as the Chairman on 12th December 1997.

He is a Chartered Accountant with a career span of over thirty-�ve years that included Partnership at an international professional �rm; senior management roles at a UK based conglomerate specializing in Africa. Since the mid nineties he has been engaged in the private equity sector focusing in Africa and Sri Lanka.

Prof. L R Watawala was appointed to the Board of Gestetner of Ceylon PLC on 07th November 1996.

Prof. Watawala is a Fellow Member of the Institute of Chartered Accountants of Sri Lanka (FCA), Fellow of the Institute of Certi�ed Management Accountants of Sri Lanka (FCMA), Fellow of the Chartered Institute of Management Accountants of UK (FCMA UK), Chartered Global Management Accountant (CGMA) and Fellow of the Institute of Chartered Professional Managers of Sri Lanka (FCPM).

He served his articles and as a Quali�ed Assistant at Turquand Youngs & Co.(Ernst & Young), Chairman and Managing Director of the Ceylon Leather Products Corporation, Chairman and Managing Director of the State Mining & Mineral Development Corporation, Chairman of the People’s Bank, Chairman of the People's Merchant Bank, Chairman and Director General of the Board of Investment of Sri Lanka (1991-1993) and (2005-2007), Advisor to the Ministry of Finance, Chairman of Pan Asia Bank Ltd, Director South Asia Informatics Computer Institute Ltd (Singapore), Director Richard Peiris PLC, Abans Electricals PLC and Chairman of the National Insurance Trust Fund.

He currently serves on the Company Directorates of, Lanka IOC PLC, Lake House Printers & Publishers PLC and Sri Lanka Technological Campus (SLTC).

He is the President of the Institute of Certi�ed Management Accountants of Sri Lanka (CMA), President Institute of Chartered Professional Managers of Sri Lanka (CPM), Past President of the Association of Management Development Institutes of South Asia (AMDISA), Past President of the Institute of Chartered Accountants of Sri Lanka and South Asian Federation of Accountants (SAFA), Founder President of the Association of Accounting Technicians of Sri Lanka (AAT) and Past President of the Organization of Professionals Association of Sri Lanka (OPA).

He was installed in the Hall of Fame of the Institute of Chartered Accountants of Sri Lanka.

BOARD OF DIRECTORS

Mr. D M R Phillips, President’s Counsel, was appointed to the Board of Gestetner of Ceylon PLC on 07th November 1996.

He is a Attorney-At-Law and a Solicitor (England & Wales) and holds a Diploma in Intellectual Property (University of London- Queen Mary & West Field College). He currently serves as the Chairman of Intellectual Property Advisory Board and presently serves on the company Directorates of NDB Bank PLC.

D M R PHILLIPSNon - Executive Director

ANNUAL REPORT

19/20

G E S T E T N E R O F C E Y L O N P L CP A G E

05

S A J GOONETILLEKENon - Executive Director

Ms. S A J Goonetilleke was appointed to the Board of Gestetner of Ceylon PLC on 01st October 1997.

Ms. Goonetilleke is a Fellow Member of Chartered Accountants of Sri Lanka, Fellow Member of Chartered Institute of Management Accountants (UK) and holds a MBA from Postgraduate Institute of Management - Sri Jayewardenapura.

She started her career at Ernst & Young and then served in several companies such as Chemanex Ltd, GTE Directories (Pvt) Ltd and presently serves as a Director in Reditune Ceylon (Pvt) Ltd.

B C U PERERANon - Executive Director

Mr. B C U Perera was appointed to the Board of Gestetner of Ceylon PLC on 01st January 2014.

Mr. B C U Perera has over twenty-�ve years of commercial experience in senior management capacity. He Joined the John Keells Group in 1992 seconded to John Keells O�ce Automation (Pvt) Limited and held the positions of Sales & Marketing Manager, Director Sales & Marketing, Director / General Manager and became the CEO / Vice President – John Keells Holdings in the year 2000.

In 2010 he moved from IT to take up a challenging career in the F & B Sector within the same group. Mr. B C U Perera was in-charge of the beverage business where he held the position of Vice President John Keells Holdings / Head of Beverages until he resigned John Keels Group in December 2013. Ceylon Cold Stores a public quoted company which had operated for over one hundred forty years. After joining Gestetner of Ceylon PLC as its Managing Director in January 2014 he served until 5th January 2019 and stepped down from an operational role to continue serving the board as a non-executive Director.

M HAMZA Executive Director / Group Chief Executive

Mr. Muhammed Hamza was appointed to the Board of Gestetner of Ceylon PLC on 9th August 2018. He was appointed as the Group Chief Executive of Gestetner of Ceylon PLC with e�ect from 2nd September 2020.

Mr. Hamza hold a Bachelor of Commerce Degree (B.Com) from University of Peradeniya, Sri Lanka and MBA with a Major in Marketing from the American University, Washington DC. He joined Nestle Lanka as a Management Trainee in 1983 and was with the group till July 2013. During his career spanning 30 years with Nestle, he had held senior Marketing, Sales and General Management positions within Nestle, across Sri Lanka, India, Pakistan and Indonesia.

He Worked as the CEO/Director for Ceylon Pencil Co Ltd (ATLAS) from 2013 to 2018, the market leader for school and o�ce stationery products in Sri Lanka. He has been a Non-Executive Independent Director at Ceylon Cold Stores (Including the JKH Supermarkets) and a member of the Audit Committee from 2015. From July 2018 he has been appointed the Chairman of the Sri Lanka Handicrafts Board.- LAKSALA.

ANNUAL REPORT

19/20

G E S T E T N E R O F C E Y L O N P L C P A G E

06

KEKI WADIA Non - Executive Director

Keki Wadia (commonly known as Kris Wadia) was appointed as a Non-Executive Director with e�ect from 13th August 2019.

Kris has held senior executive roles with Pearson plc in Hong Kong, OCBC Bank in Singapore and global roles with Accenture, the world’s leading technology consultancy and Quintiles, the world’s largest clinical trials outsourcer.

Kris currently serves as a Senior Advisor to CEOs and Boards in Financial Services, BioPharma and Cyber Security. He has lived in 8 countries and travelled to over 70 countries, building a proven track record of successful launches, rapid growth, and transformation of businesses at scale globally.

As an Entrepreneur, he has orchestrated the turnaround of loss-making, mid-size businesses by leveraging his academic training as a UK Chartered Certi�ed Accountant (FCCA).

He is a regular keynote speaker at global conferences on subjects ranging from Leadership, In�uencing Skills, Process Optimization and Technology Innovation.

Kris has been quoted in Bloomberg Businessweek, the Financial Times, CNN, and life sciences journals as a thought leader. He has authored �ve books on technology, marketing and �nance, and is writing his sixth on ‘Humanized Leadership in Virtualized World’ speci�cally for managers in emerging economies.

A R RASIAH Alternate Director to S J M Anzsar

Mr. A R Rasiah was appointed as an alternate Director to Chairman, Mr. S J M Anzsar of Gestetner of Ceylon PLC e�ective from 13th August 2019.

Mr. Rasiah is a Fellow Member of the Institute of Chartered Accountants of Sri Lanka with an illustrious career span of over thirty �ve years. He holds a Bachelor of Science Degree from University of Ceylon.

He started his career with Ernst and Young and later on served Mercantile Group of Companies and Almulla Group of Companies respectively. Finally, he joined Nestle Lanka PLC as Director Finance in 1994 and was with the Group till his retirement 2005. He was the Chairman of Atlas Axillia (Pvt) Ltd till 2017.

At present Mr. Rasiah functions as the Chairman of the Hela Clothing (Pvt) Ltd and Chairman of the Sri Lanka Institute of Directors. He is also a Non Executive Director of EB Creasy Group of Companies, Marawila, Sigiriya and Beruwala Hotels Ltd, Fintek Managed Solutions (Pvt) Ltd, Clindata Lanka (Pvt) Ltd and Sunshine Tea Co (Pvt) Ltd.

ANNUAL REPORT

19/20

G E S T E T N E R O F C E Y L O N P L CP A G E

07

CORPORATE GOVERNANCE

The policy of the Company is to manage its

a�airs in accordance with appropriate

standards for good Corporate Governance.

Implementation of policy and strategy is done

in a framework that requires compliance with

existing laws and regulations as well as

establishing best practices in dealing with

employees, customers, suppliers and the

community.

The Company currently complies with the

requirements set out in the Code of Best

Practices for Corporate Governance issued by

the Institute of Chartered Accountants of Sri

Lanka and the Rules on Corporate Governance

contained in the Listing Rules of the Colombo

Stock Exchange.

Name Of Director 28th May, 2019 13th August, 2019 13th November, 2019 02nd January, 2020 13th February, 2020

Mr S J M Anzsar - Chairman √ - √ √ √

Mr L R Watawala - Deputy Chairman _ √ _ √ √

Mr D M R Phillips _ _ _ √ _

Ms S A J Goonetilleke √ _ _ _ _

Mr B C U Perera √ _ √ √ √

Mr S T P Kahawela (Resigned with e�ect from 31st August 2020) √ √ √ √ √

Mr M Hamza - Group Chief Executive √ √ √ _ √

Mr K M Wadia _ _ √ √ _(Appointed with e�ectfrom 13th August, 2019)

Mr A M G Gomez √ _ _ _ _(Resigned with e�ect from 29th May, 2019)

BOARD OF DIRECTORS

The Board consists of Six Non-Executive Directors including the Chairman, Mr S J M Anzsar. The other Non-Executive Directors are Messrs. L R Watawala (Deputy Chairman), Dinal Phillips, Ms S A J Goonetilleka, B C U Perera, and Keki Wadia. Mr. M Hamza who is a Director is also the Group Chief Executive. Mr A R Rasiah who is the Alternate Director to the Chairman is a Non-Executive Director.

A brief description of each of the Directors is set out from pages 04 to 06.

The Board meets regularly to take decisions e�ectively and ensure that the operations of the Group are satisfactorily carried out and special Board Meetings are also held whenever necessary. In the year under review �ve (05) meetings were held and Directors’ attendance thereat was as follows :

ANNUAL REPORT

19/20

G E S T E T N E R O F C E Y L O N P L C P A G E

08

Compliance with Rules on Corporate Governance contained in the Listing Rules of the Colombo Stock Exchange:

Subject Requirement Extent of Compliance

Non – Executive At least one third of the Other than Mr. M Hamza, all Directors are Directors total number of Directors Non-Executive Directors. should be Non- Executive Directors

Independent Directors One third of the Mr. Keki Wadia is a Non-Executive Non-Executive Directors Independent Director. All the other Non should be independent Executive Directors except Mr B C U

Perera should be Independent have served on the Board continuously for over nine years and, the Board having taken into consideration all relevant circumstances, is of the opinion that the said Directors are independent since all other criteria for de�ning “independence” set out in the Listing Rules of the Colombo Stock Exchange have been satis�ed.

Mr. B C U Perera who is a Non-Executive Director is not independent as he was employed by the Company during the past two years.

The Non - Executive Directors of the Company have submitted declarations pertaining to their independence/non- independence as required by Listing Rules of the Colombo Stock Exchange.

APPOINTMENTS

At each Annual General Meeting one third of the Directors for the time being, except the Group Chief Executive retire from o�ce. The Directors to retire at each Annual General Meeting are those who being subject to retirement by rotation, have been longest in o�ce since their last election. A retiring Director is eligible for re – election.

RESPONSIBILITY OF THE BOARD

The Company’s business and Group operations are managed under the supervision of the Board and include :

Providing entrepreneurial leadership to the Company.

Evaluating, reviewing and approving corporate strategy and Performance.

Approving and monitoring �nancial reporting of the Company.

Recommending the appointments and fee of the External Auditor.

Ensuring compliance with all relevant laws, regulations and codes of business practice.

ANNUAL REPORT

19/20

G E S T E T N E R O F C E Y L O N P L CP A G E

09

Compliance with Rules of Corporate Governance

Subject Requirement Extent of Compliance

Composition Should comprise of All Members are Non-Executive Directors, Non- Executive Directors except Mr M Hamza. Other members are not majority of whom shall be independent however the Board is of the Independent opinion that such Directors are “ independent”

having taken into consideration all the circumstances relating thereto.

Chairman One Non- Executive Director This requirement has been complied with. should be appointed as the Chairman Membership in The Chairman or one Member Two Members of the Committee are Members a recognized should be a Member of a of the Institute of Chartered Accountants ofAccounting Body recognized Accounting Body Sri Lanka.

FINANCIAL REPORTING

The Company makes available all the �nancial reports to shareholders in a timely manner, providing information as per the Colombo Stock Exchange requirements and prepares the Financial Statements as per Sri Lanka Accounting Standards (LKASs/SLFRSs) and guidelines issued by the Sri Lanka Institute of Chartered Accountants.

Adequate internal control systems are in place to ensure compliance with regulatory requirements.

BOARD AUDIT COMMITTEE

The Board Audit Committee consists of one Executive Director who is Mr M Hamza and two Non - Executive Directors, namely Prof L R Watawala (Chairman) and Ms S A J Goonetilleke.

Mr A M G Gomez ceased to be a member of the Board Audit Committee pursuant his resignation

as a Director of the company with e�ect from 29th May 2019 and he was replaced by Mr. M Hamza.

The Committee examines any matters relating to the �nancial a�airs of the Company, compliance with accounting standards and laws as well as internal control policies and procedures. The Committee is also responsible for the consideration and appointment of External Auditor, the maintenance of a professional relationship with them and reviewing Accounting Principles, Policies and Practices adopted in the preparation of public �nancial information.

The Audit Committee held two (02) meetings during the �nancial year ended 31st March 2020. The detailed Report of the Audit Committee is given on page 11 of the Annual Report.

G E S T E T N E R O F C E Y L O N P L C

ANNUAL REPORT

19/20

P A G E

10

NAME OF THE DIRECTOR CATEGORY 28TH MAY 2019

L R Watawala (Chairman) Deputy Chairman √

S A J Goonetilleke Director √

A M G Gomez Director √

M Hamza Director Not Applicable as he was appointed on 29th May 2019

Compliance with Rule of Corporate Governance

SUBJECT REQUIREMENT EXTENT OF COMPLIANCE

Composition Should comprise of All Members are Non-Executive Directors, except Non- Executive Directors Mr M Hamza. Other members are not independent majority of whom shall be however the Board is of the opinion that such Independent. Directors are “ independent” having taken into

consideration all the circumstances relating thereto.

RREMUNERATION COMMITTEE

The Committee is headed by Prof L R Watawala and the other members are Ms S A J Goonetilleke and Mr M Hamza .

Mr A M G Gomez ceased to be a member of the Remuneration Committee pursuant his resignation as a Director of the Company with e�ect from 29th May 2019 who was replaced by Mr. M Hamza.

The Remuneration Committee reviews the performance of the Group Chief Executive and recommends appropriate remuneration bene�ts and other payments based on the remuneration policy of the Company, which has been formulated on market and industry factors and performance of the Group Chief Executive.

The Committee also approves the remuneration of the members of the Senior Management Committee on the recommendations made by the Group Chief Executive.

The proceedings of the Committee are reported to the Board of Directors who will in turn make the �nal determination based on the recommendations of the Committee.

All Non-Executive Directors receive a fee for serving on the Board and serving on sub-committees. They do not receive any performance related incentive payments. The Directors’ emoluments are disclosed in note 08 on page 52.

The Committee meets as and when the need arises. The Remuneration Committee met once during the year ended 31st March 2020 and Directors’ attendance thereat was as follows :

SENIOR MANAGEMENT

Senior Management meets regularly with Departmental Heads to review progress, discuss and resolve issues concerning the operations of the Company as well as to compare performance with budget and management information that contains explanations for any variances and recommendations.

To the Shareholders of Gestetner of Ceylon PLC Report on the Audit of the Financial Statements

Opinion

We have audited the �nancial statements of Gestetner of Ceylon PLC, (“the Company”), and the consolidated �nancial statements of the Company and its Subsidiaries (“the Group”), which comprise the statement of �nancial position as at 31 March 2020, and the statement of pro�t or loss and other comprehensive income, statement of changes in equity and statement of cash �ows for the year then ended, and notes to the �nancial statements, including a summary of signi�cant accounting policies and other explanatory information set out on pages 25 to 76 of the annual report.

In our opinion, the accompanying �nancial statements give a true and fair view of the �nancial position of the Company and the Group as at 31 March 2020, and of their �nancial performance and cash �ows for the year then ended in accordance with Sri Lanka Accounting Standards.

Basis for Opinion

We conducted our audit in accordance with Sri Lanka Auditing Standards (SLAuSs). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Group in accordance with the Code of Ethics issued by CA Sri Lanka (Code of Ethics), and we have ful�lled our other ethical responsibilities in accordance with the

Code of Ethics. We believe that the audit evidence we have obtained is su�cient and appropriate to provide a basis for our opinion.

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most signi�cance in our audit of the Company �nancial statements and the consolidated �nancial statements of the current period. These matters were addressed in the context of our audit of the Company �nancial statements and the consolidated �nancial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

01. Impairment assessment of goodwill and investment in subsidiaries

Refer to signi�cant accounting policies in Note 3.2.5 and 3.2.7 and explanatory notes 17 and 17.1(c) of the �nancial statements.

Risk Description

On 28th May 2019, the Company acquired 100% ownership in Fintek Managed Solutions (Private) Limited (“the acquiree”) for a consideration of 100Mn and recognized goodwill on acquisition amounting to Rs. 37,977,635 in the consolidated �nancial statements. Management allocated goodwill to the respective cash-generating unit (CGU) as described in note 17.1(c) to the �nancial statements. The recoverability of the identi�ed CGU has been determined based on the value-in-use calculation.

As at 31st March 2020, the carrying amount of the investment in subsidiaries amounted to Rs. 90,260,525 and the goodwill was carried at Rs. 37,647,802. The Management performed impairment assessment for the subsidiaries with indications of impairment and determined their recoverable amounts based on value-in-use calculation.

The assessment of the existence of any indicators of impairment of the carrying amount of investment in subsidiaries is judgmental. In the event that indicators of impairment are identi�ed, the assessment of the recoverable amounts is also judgmental and requires estimation and the use of subjective assumptions.

The primary risks are identifying impairment indicators, inaccurate models being used for the impairment assessment, and that the assumptions to support the value of the investments are inappropriate. The principal consideration for our determination that the impairment assessment of goodwill and investments in subsidiaries is a key audit matter is the subjectivity in the assessment of the recoverable amounts which requires estimation and the use of assumptions.

Our Audit Procedures Included,

1. Assessing based on the market outlook, performance during the year and net assets from the audited �nancial statements of the subsidiaries, the existence of any indicators of impairment.

2. Obtaining an understanding of management’s impairment assessment process.

3. Assessing the reasonableness of cash�ow projection in calculation of the value-in -use, challenging the reasonableness of the key assumptions such as the revenue growth rate, gross pro�t margin percentage and discount rate based on our knowledge of the business and industry by comparing the assumptions to historical results and published risk free rate and comparing the subsequent period’s actual results with the forecast, and other relevant information.

4. On a sample basis, testing the accuracy and relevance of the input data to supporting evidence, such as approved budgets and considering the reasonableness of these budgets to the historic results and subsequent period actuals.

5. Performing sensitivity analysis in consideration of the potential impact of reasonably possible downside changes in these key assumptions.

6. Assessing the accuracy of the disclosures relating to investments in subsidiaries and goodwill included in notes 17 and 17.1(c) to the �nancial statements.

02. Carrying Value Of Inventories

Refer to signi�cant accounting policies in Note 3.9, and explanatory note in Note 18 of the �nancial statements.

Risk Description

The Group held inventories with an aggregate carrying value of Rs. 192,756,472 as at 31 March 2020.

Changes in economic sentiment or consumer preferences and the introduction

of newer machines with the latest design and technologies could result in inventories on hand no longer being sought after or being sold at a discount below their cost.

Estimating future demand for and the related selling prices of printing machines, air conditioners and spare parts are inherently subjective and uncertain because it involves management estimating the extent of markdown of selling prices necessary to sell the older or slow moving models in the period subsequent to the reporting date.

We identi�ed the carrying value of inventories as a key audit matter because of the exercise of signi�cant judgment by management in determining appropriate carrying value of inventories.

Our Audit Procedures Included,

• Assessing whether the inventory provisions at the end of the reporting period were determined in a manner consistent with the Group’s inventory provision policy by recalculating the inventory provisions based on the percentages and other parameters in the Group’s inventory provision policy.

• Assessing, on a sample basis, whether items in the inventory ageing report were classi�ed within the appropriate ageing category by comparing individual items with the underlying goods receipt notes.

• Enquiring of management about any expected changes in plans for markdowns or disposals of slow moving or obsolete inventories and comparing their representations with actual transactions

subsequent to the reporting date and assumptions adopted in determining the inventory provisions.

• Comparing, on a sample basis, the carrying value of inventories with sales prices subsequent to the end of the reporting period.

• Inspecting documentation of management’s full inventory count conducted (which we were unable to attend due to impracticability) and performing a roll back procedure in order to ensure the existence and condition of inventories as at the reporting date.

• Carrying out an independent inventory count for a sample of items on an alternative date subsequent to easing of lockdown restrictions and performing a roll back procedure in order to ensure the existence and condition of inventories as at the reporting date.

03. Recoverability of Trade Receivables

Refer to signi�cant accounting policies in Note 3.4 and explanatory note in Note 19 of the �nancial statements.

Risk Description

The carrying value of trade receivables of the Group was Rs. 204,882,171 as at 31 March 2020.

Assessing the allowance for impairment of trade receivables requires management to make subjective judgements over both the timing of recognition and estimation of the amount required of such impairment.

We identi�ed assessing the recoverability of trade receivables as a key audit matter because of the signi�cance of trade debtors to the �nancial statements as a whole and the assessment of the recoverability of trade receivables is inherently subjective and requires signi�cant management judgement in accordance with SLFRS 09, which increases the risk of error or potential management bias.

The Group measures loss allowances using Simpli�ed Expected Credit Loss (ECL). For this purpose, the Group has established a provision matrix that is based on the historical loss experience. The Group considers reasonable and supportable information that is relevant and available without undue cost or e�ort.

Our Audit Procedures Included,

• Reviewing the appropriateness of the provisioning methodology used by management in determining the impairment allowances against the requirements of SLFRS 09.

• Assessing the reasonableness of the assumptions used in the provisioning methodology by comparing them with historical data adjusted for current market conditions.

• Recomputing management’s calculation for the impairment allowance determined based on simpli�ed expected credit loss method.

• Assessing the accuracy of the disclosures and evaluating the appropriateness of the

accounting policies based on the requirements of the accounting standard.

• Assessing, on a sample basis, whether items in the debtors ageing report were classi�ed within the appropriate ageing category by comparing individual items with the underlying invoices.

• Calling for confirmations from major debtors and / or verifying subsequent settlements as an alternative procedure.

Other Information

Management is responsible for the other information. The other information comprises the information included in the annual report but does not include the �nancial statements and our auditor’s report thereon.

Our opinion on the �nancial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the �nancial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the �nancial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of Management and Those Charged with Governance for the Consolidated Financial Statements

Management is responsible for the preparation of �nancial statements that give a true and fair view in accordance with Sri Lanka Accounting Standards, and for such internal control as management determines is necessary to enable the preparation of �nancial statements that are free from material misstatement, whether due to fraud or error.

In preparing the �nancial statements, management is responsible for assessing the Group’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Group or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s and the Group’s �nancial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the �nancial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with SLAuSs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the

aggregate, they could reasonably be expected to in�uence the economic decisions of users taken on the basis of these �nancial statements.

As part of an audit in accordance with SLAuSs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the �nancial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is su�cient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the e�ectiveness of the Company and the Group’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

• Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast signi�cant doubt

on the Group’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the �nancial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Group to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the �nancial statements, including the disclosures, and whether the �nancial statements represent the underlying transactions and events in a manner that achieves fair presentation.

• Obtain sufficient appropriate audit evidence regarding the �nancial information of the entities or business activities within the Group to express an opinion on the consolidated �nancial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and signi�cant audit �ndings, including any signi�cant de�ciencies in internal control that we identify during our audit.

We also provide those charged with governance with a statement that we have complied with ethical requirements in accordance with the Code of Ethics regarding independence, and to communicate with them all relationships and

other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with those charged with governance, we determine those matters that were of most signi�cance in the audit of the �nancial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest bene�ts of such communication.

Report on Other Legal and Regulatory Requirements

As required by section 163 (2) of the Companies Act No. 07 of 2007, we have obtained all the information and explanations that were required for the audit and, as far as appears from our examination, proper accounting records have been kept by the Company.

CA Sri Lanka membership number of the engagement partner responsible for signing this independent auditor’s report is 1798.

Chartered AccountantsColombo, Sri Lanka23rd December 2020

ANNUAL REPORT

19/20

G E S T E T N E R O F C E Y L O N P L CP A G E

11

The Audit Committee is responsible to the Shareholders and other stakeholders regarding the integrity of the Company’s Financial Reporting Process in accordance with Sri Lanka Accounting Standards and other legislations. The Audit Committee also ensures the Company’s internal control and procedures and compliance with legal regulatory requirements.

COMPOSITION OF AUDIT COMMITTEE

The Board Audit Committee comprises of one Executive Director and two Non Executive Directors. The Members of the Committee are Prof. L R Watawala (Chairman), Ms S A J Goonetilleke who are Non Executive Directors and Mr. M Hamza, who is an Executive Director. All Directors are individuals with extensive experience and expertise in the �elds of Finance, Corporate Management and Marketing. The quali�cations of the Directors are given from pages 04 to 06 of the Annual Report.

Mr A M G Gomez ceased to be a member of the Board Audit Committee pursuant his resignation as a Director of the Company with e�ect from 29th May 2019 who was replaced by Mr. M Hamza. MEETINGS OF THE AUDIT COMMITTEE

During the year there were two Meetings and attendance of the Members were as follows :

NAME OF THE DIRECTOR CATEGORY 28TH MAY 2019 13TH AUGUST 2019

L R Watawala (Chairman) Deputy Chairman √ √

S A J Goonetilleke Director √ -

A M G Gomez Director √ -

M Hamza Director Not Applicable √ as he was appointed on 29th May 2019

SUMMARY OF ACTIVITIES DURING THE FINANCIAL YEAR

The main responsibilities of the Audit Committee.

• Reviewing and monitoring the integrity of the Financial Statements

• Reviewing the Management Letter of External Auditor and Management Response

• Reviewing the progress of management actions to resolve highlighted signi�cant internal controls issued by External Auditors

• Reviewing Interim Financial Statements for purpose of quarterly announcement of �nancial results

• Reviewing of Business Risk and Mitigation Plans

• Reviewing and monitoring compliance with Companies Act No 07 of 2007

• Reviewing and monitoring the e�ectiveness of the Internal Controls

• Reviewing and monitoring Statutory and Regulatory Compliance Processes.

EXTERNAL AUDITOR

The Audit Committee evaluates the external audit functions and establishes the independence and objectivity of the external audit functions. The Audit Committee has recommended to the Board that Messrs KPMG, Chartered Accountants, be reappointed as External Auditors of Gestetner of Ceylon PLC for the �nancial year ending 31st March 2021, subject to approval by the Shareholders at the Annual General Meeting.

L R Watawala Chairman - Audit Committee

The Group DGM-Finance, attends these meetings by invitation.

REPORT OF THE BOARD AUDIT COMMITTEE

TERMS OF REFERENCE

The terms of reference clearly de�ne the role, responsibilities and powers of the Audit Committee and ensures that the composition and the activities of the Audit Committee are in line with International Best Practices and Corporate Governance Rules applicable to listed companies.

To the Shareholders of Gestetner of Ceylon PLC Report on the Audit of the Financial Statements

Opinion

We have audited the �nancial statements of Gestetner of Ceylon PLC, (“the Company”), and the consolidated �nancial statements of the Company and its Subsidiaries (“the Group”), which comprise the statement of �nancial position as at 31 March 2020, and the statement of pro�t or loss and other comprehensive income, statement of changes in equity and statement of cash �ows for the year then ended, and notes to the �nancial statements, including a summary of signi�cant accounting policies and other explanatory information set out on pages 25 to 76 of the annual report.

In our opinion, the accompanying �nancial statements give a true and fair view of the �nancial position of the Company and the Group as at 31 March 2020, and of their �nancial performance and cash �ows for the year then ended in accordance with Sri Lanka Accounting Standards.

Basis for Opinion

We conducted our audit in accordance with Sri Lanka Auditing Standards (SLAuSs). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Group in accordance with the Code of Ethics issued by CA Sri Lanka (Code of Ethics), and we have ful�lled our other ethical responsibilities in accordance with the

Code of Ethics. We believe that the audit evidence we have obtained is su�cient and appropriate to provide a basis for our opinion.

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most signi�cance in our audit of the Company �nancial statements and the consolidated �nancial statements of the current period. These matters were addressed in the context of our audit of the Company �nancial statements and the consolidated �nancial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

01. Impairment assessment of goodwill and investment in subsidiaries

Refer to signi�cant accounting policies in Note 3.2.5 and 3.2.7 and explanatory notes 17 and 17.1(c) of the �nancial statements.

Risk Description

On 28th May 2019, the Company acquired 100% ownership in Fintek Managed Solutions (Private) Limited (“the acquiree”) for a consideration of 100Mn and recognized goodwill on acquisition amounting to Rs. 37,977,635 in the consolidated �nancial statements. Management allocated goodwill to the respective cash-generating unit (CGU) as described in note 17.1(c) to the �nancial statements. The recoverability of the identi�ed CGU has been determined based on the value-in-use calculation.

As at 31st March 2020, the carrying amount of the investment in subsidiaries amounted to Rs. 90,260,525 and the goodwill was carried at Rs. 37,647,802. The Management performed impairment assessment for the subsidiaries with indications of impairment and determined their recoverable amounts based on value-in-use calculation.

The assessment of the existence of any indicators of impairment of the carrying amount of investment in subsidiaries is judgmental. In the event that indicators of impairment are identi�ed, the assessment of the recoverable amounts is also judgmental and requires estimation and the use of subjective assumptions.

The primary risks are identifying impairment indicators, inaccurate models being used for the impairment assessment, and that the assumptions to support the value of the investments are inappropriate. The principal consideration for our determination that the impairment assessment of goodwill and investments in subsidiaries is a key audit matter is the subjectivity in the assessment of the recoverable amounts which requires estimation and the use of assumptions.

Our Audit Procedures Included,

1. Assessing based on the market outlook, performance during the year and net assets from the audited �nancial statements of the subsidiaries, the existence of any indicators of impairment.

2. Obtaining an understanding of management’s impairment assessment process.

3. Assessing the reasonableness of cash�ow projection in calculation of the value-in -use, challenging the reasonableness of the key assumptions such as the revenue growth rate, gross pro�t margin percentage and discount rate based on our knowledge of the business and industry by comparing the assumptions to historical results and published risk free rate and comparing the subsequent period’s actual results with the forecast, and other relevant information.

4. On a sample basis, testing the accuracy and relevance of the input data to supporting evidence, such as approved budgets and considering the reasonableness of these budgets to the historic results and subsequent period actuals.

5. Performing sensitivity analysis in consideration of the potential impact of reasonably possible downside changes in these key assumptions.

6. Assessing the accuracy of the disclosures relating to investments in subsidiaries and goodwill included in notes 17 and 17.1(c) to the �nancial statements.

02. Carrying Value Of Inventories

Refer to signi�cant accounting policies in Note 3.9, and explanatory note in Note 18 of the �nancial statements.

Risk Description

The Group held inventories with an aggregate carrying value of Rs. 192,756,472 as at 31 March 2020.

Changes in economic sentiment or consumer preferences and the introduction

of newer machines with the latest design and technologies could result in inventories on hand no longer being sought after or being sold at a discount below their cost.

Estimating future demand for and the related selling prices of printing machines, air conditioners and spare parts are inherently subjective and uncertain because it involves management estimating the extent of markdown of selling prices necessary to sell the older or slow moving models in the period subsequent to the reporting date.

We identi�ed the carrying value of inventories as a key audit matter because of the exercise of signi�cant judgment by management in determining appropriate carrying value of inventories.

Our Audit Procedures Included,

• Assessing whether the inventory provisions at the end of the reporting period were determined in a manner consistent with the Group’s inventory provision policy by recalculating the inventory provisions based on the percentages and other parameters in the Group’s inventory provision policy.

• Assessing, on a sample basis, whether items in the inventory ageing report were classi�ed within the appropriate ageing category by comparing individual items with the underlying goods receipt notes.

• Enquiring of management about any expected changes in plans for markdowns or disposals of slow moving or obsolete inventories and comparing their representations with actual transactions

subsequent to the reporting date and assumptions adopted in determining the inventory provisions.

• Comparing, on a sample basis, the carrying value of inventories with sales prices subsequent to the end of the reporting period.

• Inspecting documentation of management’s full inventory count conducted (which we were unable to attend due to impracticability) and performing a roll back procedure in order to ensure the existence and condition of inventories as at the reporting date.

• Carrying out an independent inventory count for a sample of items on an alternative date subsequent to easing of lockdown restrictions and performing a roll back procedure in order to ensure the existence and condition of inventories as at the reporting date.

03. Recoverability of Trade Receivables

Refer to signi�cant accounting policies in Note 3.4 and explanatory note in Note 19 of the �nancial statements.

Risk Description

The carrying value of trade receivables of the Group was Rs. 204,882,171 as at 31 March 2020.

Assessing the allowance for impairment of trade receivables requires management to make subjective judgements over both the timing of recognition and estimation of the amount required of such impairment.

We identi�ed assessing the recoverability of trade receivables as a key audit matter because of the signi�cance of trade debtors to the �nancial statements as a whole and the assessment of the recoverability of trade receivables is inherently subjective and requires signi�cant management judgement in accordance with SLFRS 09, which increases the risk of error or potential management bias.

The Group measures loss allowances using Simpli�ed Expected Credit Loss (ECL). For this purpose, the Group has established a provision matrix that is based on the historical loss experience. The Group considers reasonable and supportable information that is relevant and available without undue cost or e�ort.

Our Audit Procedures Included,

• Reviewing the appropriateness of the provisioning methodology used by management in determining the impairment allowances against the requirements of SLFRS 09.

• Assessing the reasonableness of the assumptions used in the provisioning methodology by comparing them with historical data adjusted for current market conditions.

• Recomputing management’s calculation for the impairment allowance determined based on simpli�ed expected credit loss method.

• Assessing the accuracy of the disclosures and evaluating the appropriateness of the

accounting policies based on the requirements of the accounting standard.

• Assessing, on a sample basis, whether items in the debtors ageing report were classi�ed within the appropriate ageing category by comparing individual items with the underlying invoices.

• Calling for confirmations from major debtors and / or verifying subsequent settlements as an alternative procedure.

Other Information

Management is responsible for the other information. The other information comprises the information included in the annual report but does not include the �nancial statements and our auditor’s report thereon.

Our opinion on the �nancial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the �nancial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the �nancial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of Management and Those Charged with Governance for the Consolidated Financial Statements

Management is responsible for the preparation of �nancial statements that give a true and fair view in accordance with Sri Lanka Accounting Standards, and for such internal control as management determines is necessary to enable the preparation of �nancial statements that are free from material misstatement, whether due to fraud or error.

In preparing the �nancial statements, management is responsible for assessing the Group’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Group or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s and the Group’s �nancial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the �nancial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with SLAuSs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the

aggregate, they could reasonably be expected to in�uence the economic decisions of users taken on the basis of these �nancial statements.

As part of an audit in accordance with SLAuSs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the �nancial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is su�cient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the e�ectiveness of the Company and the Group’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

• Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast signi�cant doubt

on the Group’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the �nancial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Group to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the �nancial statements, including the disclosures, and whether the �nancial statements represent the underlying transactions and events in a manner that achieves fair presentation.

• Obtain sufficient appropriate audit evidence regarding the �nancial information of the entities or business activities within the Group to express an opinion on the consolidated �nancial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and signi�cant audit �ndings, including any signi�cant de�ciencies in internal control that we identify during our audit.

We also provide those charged with governance with a statement that we have complied with ethical requirements in accordance with the Code of Ethics regarding independence, and to communicate with them all relationships and

other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with those charged with governance, we determine those matters that were of most signi�cance in the audit of the �nancial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest bene�ts of such communication.

Report on Other Legal and Regulatory Requirements

As required by section 163 (2) of the Companies Act No. 07 of 2007, we have obtained all the information and explanations that were required for the audit and, as far as appears from our examination, proper accounting records have been kept by the Company.

CA Sri Lanka membership number of the engagement partner responsible for signing this independent auditor’s report is 1798.

Chartered AccountantsColombo, Sri Lanka23rd December 2020

ANNUAL REPORT

19/20

G E S T E T N E R O F C E Y L O N P L C P A G E

12

The Board of Directors of Gestetner of Ceylon PLC is pleased to present the Annual Report together with the Audited Financial Statements of Gestetner of Ceylon PLC and the Audited Consolidated Financial Statements of the Group for the year ended 31st March 2020.

This report contains information required by Section 168 of the Companies Act No.07 of 2007 and other necessary information required by the Listing Rules of Colombo Stock Exchange.

PRINCIPAL ACTIVITIES OF THE GROUP The core business of the Company is the import and sale of Digital Copiers, Digital Duplicators, Laser Printers, Projectors and Laptops.

Nashua Lanka (Pvt) Limited, which is a fully owned subsidiary of the Company, imports and markets Copiers, Consumables and manages a Copy Bureau.

Gestetner Printing Services (Pvt) Limited, which is also a fully owned subsidiary of the Company is engaged in the provision of Outsourced Photocopying / Printing Services and also IT Solutions.

Fintek managed Solutions (Pvt) Limited, which is a fully owned subsidiary of the Company is engaged in Importing and selling of Digital Copiers, laser printers, Air conditioners, provision of Outsourced Photocopying and providing after sales services including services for G&D machines.

Gestetner Manufacturers (Pvt) Limited, the other fully owned subsidiary of the Company was engaged in manufacturing ink and currently it is not operating.

CHANGES TO THE NATURE OF THE BUSINESS There were no changes to the principal activities of the Company during the �nancial year ended 31st March 2020.

ANNUAL REPORT OF THE BOARD OF DIRECTORS

2019/2020 2018/2019 Rs. Rs.

Gestetner of Ceylon PLC 828,411,061 886,399,502

Subsidiaries 224,083,512 43,846,673

1,052,494,573 930,246,175

Less: Intra Group Sales (17,513,040) (20,818,919)

1,034,981,533 909,427,256

RESULTS AND APPROPRIATIONS

Gross Pro�t 337,171,189 285,584,921

Other Income 10,493,918 12,353,199

Administrative Expenses (209,047,930) (177,233,831)

Selling & Distribution Expenses (96,615,227) (54,066,456)

Impairment (Charge) / Reversal of Trade Receivables (5,345,596) 813,199

Impairment of Goodwill (329,833) -

Other Operating Expenses (21,308,068) (3,176,349)

Net Finance Cost (27,814,391) (7,995,076)

Pro�t / (Loss) Before Tax (12,795,938) 56,279,607

Income Tax Reversal / (Expense) 8,143,372 (13,393,452)

Pro�t / (Loss) for the Year (4,652,566) 42,886,155Other Comprehensive Income for the Year, net of Tax 5,343,773 (1,859,249)

Accumulated Pro�t B/F 216,189,721 175,162,815

Dividend Paid (3,322,265) -

Pro�t Available for Appropriation 213,558,663 216,189,721

Earnings Per Share (1.75) 16.14

FINANCIAL STATEMENTSThe Financial Statements of the Group and the Company are set out from pages 25 to 76 of the Annual Report.

DIRECTORATE The Board of Directors of the Company as at date is set out in “ Corporate Information”. The Directors of the Company who held o�ce during the year under review and changes thereto are indicated below.

TURNOVER ANALYSIS The turnover of the Group for the year Rs.1,034,981,533/- (2018/19 - Rs. 909,427,256/-) analyzed among the group is as follows.

To the Shareholders of Gestetner of Ceylon PLC Report on the Audit of the Financial Statements

Opinion

We have audited the �nancial statements of Gestetner of Ceylon PLC, (“the Company”), and the consolidated �nancial statements of the Company and its Subsidiaries (“the Group”), which comprise the statement of �nancial position as at 31 March 2020, and the statement of pro�t or loss and other comprehensive income, statement of changes in equity and statement of cash �ows for the year then ended, and notes to the �nancial statements, including a summary of signi�cant accounting policies and other explanatory information set out on pages 25 to 76 of the annual report.

In our opinion, the accompanying �nancial statements give a true and fair view of the �nancial position of the Company and the Group as at 31 March 2020, and of their �nancial performance and cash �ows for the year then ended in accordance with Sri Lanka Accounting Standards.

Basis for Opinion

We conducted our audit in accordance with Sri Lanka Auditing Standards (SLAuSs). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Group in accordance with the Code of Ethics issued by CA Sri Lanka (Code of Ethics), and we have ful�lled our other ethical responsibilities in accordance with the

Code of Ethics. We believe that the audit evidence we have obtained is su�cient and appropriate to provide a basis for our opinion.

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most signi�cance in our audit of the Company �nancial statements and the consolidated �nancial statements of the current period. These matters were addressed in the context of our audit of the Company �nancial statements and the consolidated �nancial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

01. Impairment assessment of goodwill and investment in subsidiaries

Refer to signi�cant accounting policies in Note 3.2.5 and 3.2.7 and explanatory notes 17 and 17.1(c) of the �nancial statements.

Risk Description

On 28th May 2019, the Company acquired 100% ownership in Fintek Managed Solutions (Private) Limited (“the acquiree”) for a consideration of 100Mn and recognized goodwill on acquisition amounting to Rs. 37,977,635 in the consolidated �nancial statements. Management allocated goodwill to the respective cash-generating unit (CGU) as described in note 17.1(c) to the �nancial statements. The recoverability of the identi�ed CGU has been determined based on the value-in-use calculation.

As at 31st March 2020, the carrying amount of the investment in subsidiaries amounted to Rs. 90,260,525 and the goodwill was carried at Rs. 37,647,802. The Management performed impairment assessment for the subsidiaries with indications of impairment and determined their recoverable amounts based on value-in-use calculation.

The assessment of the existence of any indicators of impairment of the carrying amount of investment in subsidiaries is judgmental. In the event that indicators of impairment are identi�ed, the assessment of the recoverable amounts is also judgmental and requires estimation and the use of subjective assumptions.

The primary risks are identifying impairment indicators, inaccurate models being used for the impairment assessment, and that the assumptions to support the value of the investments are inappropriate. The principal consideration for our determination that the impairment assessment of goodwill and investments in subsidiaries is a key audit matter is the subjectivity in the assessment of the recoverable amounts which requires estimation and the use of assumptions.

Our Audit Procedures Included,

1. Assessing based on the market outlook, performance during the year and net assets from the audited �nancial statements of the subsidiaries, the existence of any indicators of impairment.

2. Obtaining an understanding of management’s impairment assessment process.

3. Assessing the reasonableness of cash�ow projection in calculation of the value-in -use, challenging the reasonableness of the key assumptions such as the revenue growth rate, gross pro�t margin percentage and discount rate based on our knowledge of the business and industry by comparing the assumptions to historical results and published risk free rate and comparing the subsequent period’s actual results with the forecast, and other relevant information.

4. On a sample basis, testing the accuracy and relevance of the input data to supporting evidence, such as approved budgets and considering the reasonableness of these budgets to the historic results and subsequent period actuals.

5. Performing sensitivity analysis in consideration of the potential impact of reasonably possible downside changes in these key assumptions.

6. Assessing the accuracy of the disclosures relating to investments in subsidiaries and goodwill included in notes 17 and 17.1(c) to the �nancial statements.

02. Carrying Value Of Inventories

Refer to signi�cant accounting policies in Note 3.9, and explanatory note in Note 18 of the �nancial statements.

Risk Description

The Group held inventories with an aggregate carrying value of Rs. 192,756,472 as at 31 March 2020.

Changes in economic sentiment or consumer preferences and the introduction

of newer machines with the latest design and technologies could result in inventories on hand no longer being sought after or being sold at a discount below their cost.

Estimating future demand for and the related selling prices of printing machines, air conditioners and spare parts are inherently subjective and uncertain because it involves management estimating the extent of markdown of selling prices necessary to sell the older or slow moving models in the period subsequent to the reporting date.

We identi�ed the carrying value of inventories as a key audit matter because of the exercise of signi�cant judgment by management in determining appropriate carrying value of inventories.

Our Audit Procedures Included,

• Assessing whether the inventory provisions at the end of the reporting period were determined in a manner consistent with the Group’s inventory provision policy by recalculating the inventory provisions based on the percentages and other parameters in the Group’s inventory provision policy.

• Assessing, on a sample basis, whether items in the inventory ageing report were classi�ed within the appropriate ageing category by comparing individual items with the underlying goods receipt notes.

• Enquiring of management about any expected changes in plans for markdowns or disposals of slow moving or obsolete inventories and comparing their representations with actual transactions

subsequent to the reporting date and assumptions adopted in determining the inventory provisions.

• Comparing, on a sample basis, the carrying value of inventories with sales prices subsequent to the end of the reporting period.

• Inspecting documentation of management’s full inventory count conducted (which we were unable to attend due to impracticability) and performing a roll back procedure in order to ensure the existence and condition of inventories as at the reporting date.

• Carrying out an independent inventory count for a sample of items on an alternative date subsequent to easing of lockdown restrictions and performing a roll back procedure in order to ensure the existence and condition of inventories as at the reporting date.

03. Recoverability of Trade Receivables

Refer to signi�cant accounting policies in Note 3.4 and explanatory note in Note 19 of the �nancial statements.

Risk Description

The carrying value of trade receivables of the Group was Rs. 204,882,171 as at 31 March 2020.

Assessing the allowance for impairment of trade receivables requires management to make subjective judgements over both the timing of recognition and estimation of the amount required of such impairment.

We identi�ed assessing the recoverability of trade receivables as a key audit matter because of the signi�cance of trade debtors to the �nancial statements as a whole and the assessment of the recoverability of trade receivables is inherently subjective and requires signi�cant management judgement in accordance with SLFRS 09, which increases the risk of error or potential management bias.

The Group measures loss allowances using Simpli�ed Expected Credit Loss (ECL). For this purpose, the Group has established a provision matrix that is based on the historical loss experience. The Group considers reasonable and supportable information that is relevant and available without undue cost or e�ort.

Our Audit Procedures Included,

• Reviewing the appropriateness of the provisioning methodology used by management in determining the impairment allowances against the requirements of SLFRS 09.

• Assessing the reasonableness of the assumptions used in the provisioning methodology by comparing them with historical data adjusted for current market conditions.

• Recomputing management’s calculation for the impairment allowance determined based on simpli�ed expected credit loss method.

• Assessing the accuracy of the disclosures and evaluating the appropriateness of the

accounting policies based on the requirements of the accounting standard.

• Assessing, on a sample basis, whether items in the debtors ageing report were classi�ed within the appropriate ageing category by comparing individual items with the underlying invoices.

• Calling for confirmations from major debtors and / or verifying subsequent settlements as an alternative procedure.

Other Information

Management is responsible for the other information. The other information comprises the information included in the annual report but does not include the �nancial statements and our auditor’s report thereon.

Our opinion on the �nancial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the �nancial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the �nancial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of Management and Those Charged with Governance for the Consolidated Financial Statements

Management is responsible for the preparation of �nancial statements that give a true and fair view in accordance with Sri Lanka Accounting Standards, and for such internal control as management determines is necessary to enable the preparation of �nancial statements that are free from material misstatement, whether due to fraud or error.

In preparing the �nancial statements, management is responsible for assessing the Group’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Group or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s and the Group’s �nancial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the �nancial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with SLAuSs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the

aggregate, they could reasonably be expected to in�uence the economic decisions of users taken on the basis of these �nancial statements.

As part of an audit in accordance with SLAuSs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the �nancial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is su�cient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the e�ectiveness of the Company and the Group’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

• Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast signi�cant doubt

on the Group’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the �nancial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Group to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the �nancial statements, including the disclosures, and whether the �nancial statements represent the underlying transactions and events in a manner that achieves fair presentation.

• Obtain sufficient appropriate audit evidence regarding the �nancial information of the entities or business activities within the Group to express an opinion on the consolidated �nancial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and signi�cant audit �ndings, including any signi�cant de�ciencies in internal control that we identify during our audit.

We also provide those charged with governance with a statement that we have complied with ethical requirements in accordance with the Code of Ethics regarding independence, and to communicate with them all relationships and

other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with those charged with governance, we determine those matters that were of most signi�cance in the audit of the �nancial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest bene�ts of such communication.

Report on Other Legal and Regulatory Requirements

As required by section 163 (2) of the Companies Act No. 07 of 2007, we have obtained all the information and explanations that were required for the audit and, as far as appears from our examination, proper accounting records have been kept by the Company.

CA Sri Lanka membership number of the engagement partner responsible for signing this independent auditor’s report is 1798.

Chartered AccountantsColombo, Sri Lanka23rd December 2020

ANNUAL REPORT

19/20

G E S T E T N E R O F C E Y L O N P L CP A G E

13

In terms of Article 85 of the Articles of Association Messrs

Seyed Jemaldeen Muhammed Anzsar and Dinal Mario Rex

Phillips retire by rotation and being eligible are

recommended by the Board for re-election.

Mr Lakshman Ravendra Watawala who is 72 years of age ,

vacates his o�ce in terms of the provisions of Section 210

of the Companies Act, No. 7 of 2007.

Notice is given by the Company to its Shareholders of the

intention to move an Ordinary Resolution for the

re-appointment of Mr Watawala as a Director of the

Company, in terms of the provisions of Section 211 of the

Companies Act, No. 7 of 2007 and is referred to in the

Notice convening the Annual General Meeting.

Mr Albert Rasakantha Rasiah, Alternate Director to Mr S J M

Anzsar, Chairman, who is 74 years, vacates his o�ce in

terms of the provisions of Section 210 of the Companies

Act, No. 7 of 2007.

Seyed Jemaldeen Muhammed Anzsar Chairman

Lakshman Ravendra Watawala Deputy Chairman

Muhammed Hamza Muhammed Appointed as Group Chief Executive On 02nd September, 2020

Sita Anne Juliana Goonetilleke

Dinal Mario Rex Phillips

Bulathsinghalage Chandima Upul Perera

Shivantha Tissa Perera Kahawela Resigned as Director and Chief Operating O�cer with e�ect from 31st August, 2020

Keki Wadia Appointed with e�ect from 13th August, 2019

Albert Rasakantha Rasiah Appointed as Alternate Director to SJM Anzsar with e�ect from 13th August, 2019

Notice is given by the Company to its

Shareholders of the intention to move an

Ordinary Resolution for the

re-appointment of Mr Rasiah as a

Director of the Company, in terms of the

provisions of Section 211 of the

Companies Act, No. 7 of 2007 and is

referred to in the Notice convening the

Annual General Meeting.

The quali�cations and experience of the

Directors are given from pages 04 to 06

of the Annual Report.

DIRECTORS’ INTEREST IN CONTRACTS

The Company maintains an Interest

Register in compliance with the

requirements of the Companies Act No 7