Annual Report 2019/2020 - Deutsche Industrie REIT-AG

164

Deutsche Industrie REIT-AG 1 October 2019 to 30 September 2020 Annual Report 2019 / 2020

Transcript of Annual Report 2019/2020 - Deutsche Industrie REIT-AG

Deutsche Industrie REIT-AG

1 October 2019 to 30 September 2020

Annual Report 2019/2020

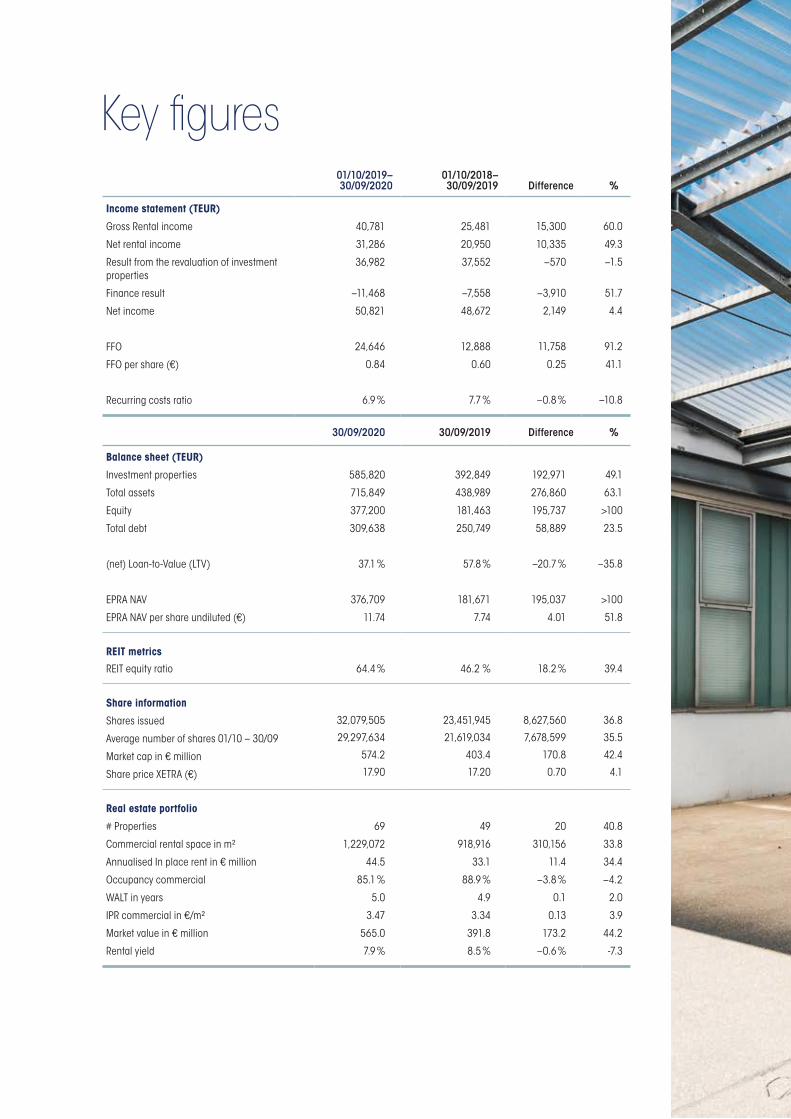

01/10/2019– 30/09/2020

01/10/2018–30/09/2019 Difference %

Income statement (TEUR)

Gross Rental income

Net rental income

Result from the revaluation of investment properties

Finance result

Net income

FFO

FFO per share (€)

Recurring costs ratio

40,781

31,286

36,982

–11,468

50,821

24,646

0.84

6.9 %

25,481

20,950

37,552

–7,558

48,672

12,888

0.60

7.7 %

15,300

10,335

–570

–3,910

2,149

11,758

0.25

–0.8 %

60.0

49.3

–1.5

51.7

4.4

91.2

41.1

–10.8

30/09/2020 30/09/2019 Difference %

Balance sheet (TEUR)

Investment properties

Total assets

Equity

Total debt

(net) Loan-to-Value (LTV)

EPRA NAV

EPRA NAV per share undiluted (€)

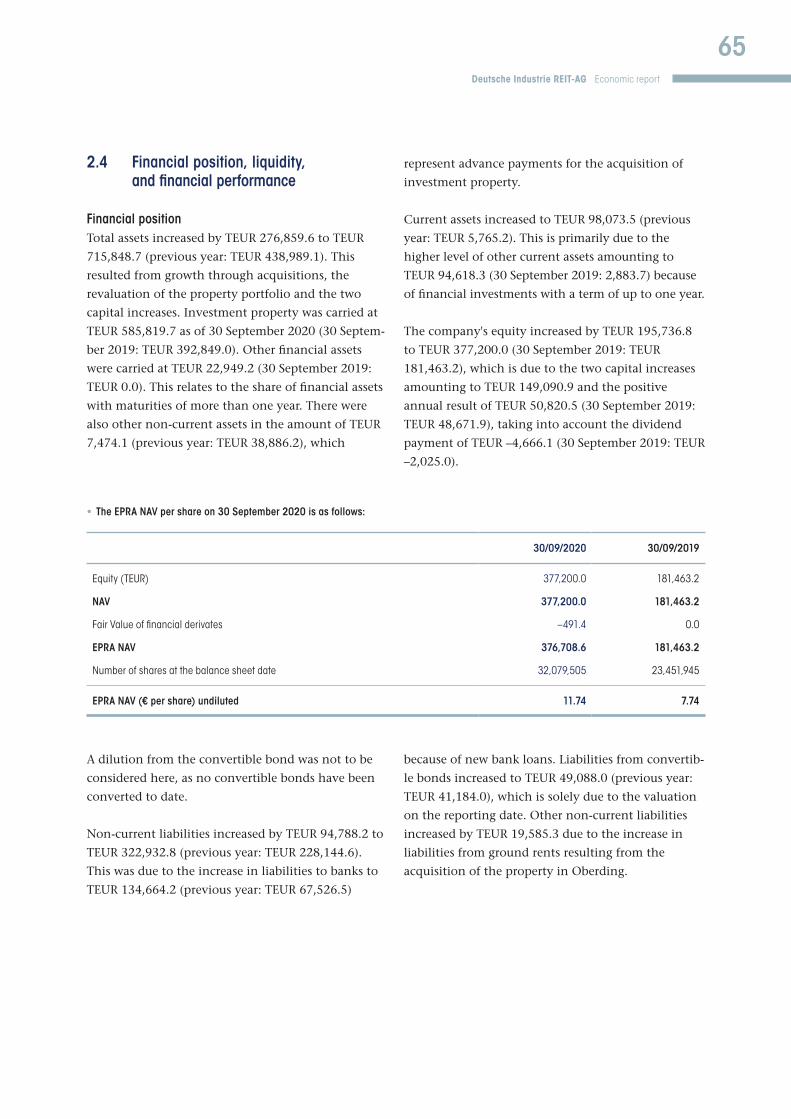

585,820

715,849

377,200

309,638

37.1 %

376,709

11.74

392,849

438,989

181,463

250,749

57.8 %

181,671

7.74

192,971

276,860

195,737

58,889

–20.7 %

195,037

4.01

49.1

63.1

>100

23.5

–35.8

>100

51.8

REIT metrics

REIT equity ratio 64.4 % 46.2 % 18.2 % 39.4

Share information

Shares issued

Average number of shares 01/10 – 30/09

Market cap in € million

Share price XETRA (€)

32,079,505

29,297,634

574.2

17.90

23,451,945

21,619,034

403.4

17.20

8,627,560

7,678,599

170.8

0.70

36.8

35.5

42.4

4.1

Real estate portfolio

# Properties

Commercial rental space in m²

Annualised In place rent in € million

Occupancy commercial

WALT in years

IPR commercial in €/m²

Market value in € million

Rental yield

69

1,229,072

44.5

85.1 %

5.0

3.47

565.0

7.9 %

49

918,916

33.1

88.9 %

4.9

3.34

391.8

8.5 %

20

310,156

11.4

–3.8 %

0.1

0.13

173.2

–0.6 %

40.8

33.8

34.4

–4.2

2.0

3.9

44.2

-7.3

Key figures

1Deutsche Industrie REIT-AG

PICTURE: Westhausen, Dr.-Rudolf-Schieber-Str.

ContentLetter to our shareholders 2

The share 4

Corporate Governance Report 8

Report of the Supervisory Board 20

Composition of the Management Board and Supervisory Board 25

Deutsche Industrie as a REIT 26

The Acquisition Pipeline 28

The Real Estate Portfolio 34

Key figures according to EPRA 52

Table of contents 54

Financial Statement 88

Balance sheet 90

Statement of comprehensive income 91

Cash flow statement 93

Statement of changes in equity 95

Notes 96

Audit Opinion of the independent individual financial statements 152

Statement by the Executive Board regarding compliance with the requirements of the REITG 156

Financial Calendar 158

2Deutsche Industrie REIT-AG Annual report 2019/2020

A difficult year for all of us is coming to an end.

During the preparation of this Annual Report, the

second wave of the Corona pandemic has again

dominated everyday life in Germany. The economic

consequences of this crisis will continue to affect us

in the coming months. However, our business model

has proven to be extremely robust and there have

been no major negative effects for us so far. The past

financial year 2019/2020 was again successful for

Deutsche Industrie REIT-AG. We were able to grow

further this year and improve almost all key figures.

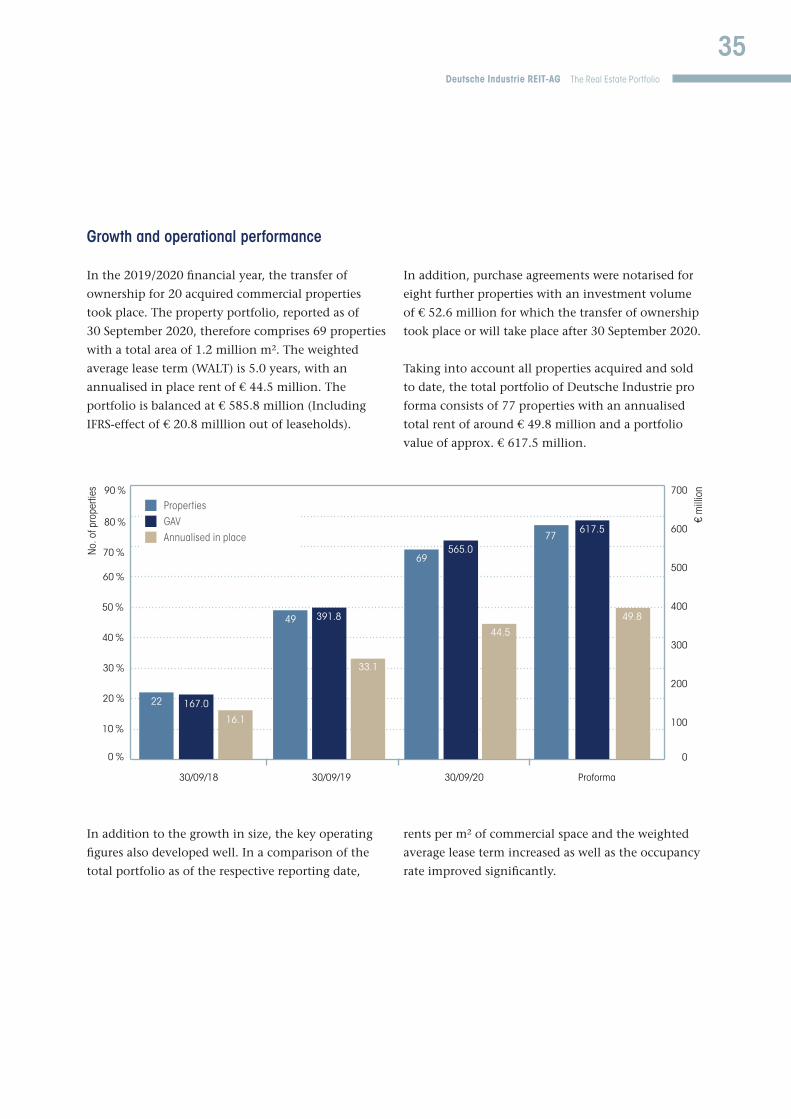

The property portfolio increased again in size and valueAs of 30 September 2020, the portfolio consists of

69 properties and is balanced at almost 568 € million.

This is an increase of nearly 50 %. In addition, there

are already eight further properties with an invest-

ment volume of approximately 53 € million. Con-

sidering all objects purchased so far, the pro forma

portfolio consists of 77 properties with annualised

total rent of around 49 € million and a portfolio

value of around 618 € million.

Our acquisition pipeline continues to be very well

filled and offers us good opportunities for further

significant growth in terms of quantity and quality

in the current financial year.

Capital increases and financing to strengthen liquidity Following the capital increase in November 2019, in

which we raised almost EUR 93 million, we carried

out a further capital measure in June 2020. This took

place mainly in view of the Corona crisis and took

advantage of the optimal time window on the capital

market. On the one hand, this was intended to buffer

possible risks of rent losses and rent deferrals, and on

the other hand, we wanted to be able to act quickly

in the event of further purchase opportunities.

In addition, external financing with a volume of

around 73 million was raised with very attractive

conditions.

Due to the higher value of the investment properties,

the high liquidity reserves and somewhat more

restrained borrowing, our debt-equity ratio (LTV) is

currently only 37.1 %, which is well below our target

level of 50 %. We see potential to take out more loans

in the coming months.

Good annual resultsNet rental income rose by almost 50 % from almost

21 € million in the previous year to just over 31 €

million in the 2019/2020 financial year. FFO (Funds

From Operations) increased by 91 % from just under

13 € million to nearly 25 € million. Despite the sharp

increase in the number of shares due to the two

capital increases, FFO per share rose by 41 % from

0.60 € to 0.84 €.

Equity more than doubled and the undiluted EPRA

NAV per share rose by 52 % from 7.74 € to 11.74 €.

The G-REIT equity ratio now stands at 64 %, which is

significantly above the required 45 % for the second

time in a row.

Dear Shareholders, Ladies and Gentlemen,

Letter to our shareholders

3Deutsche Industrie REIT-AG Letter to our shareholders

Dividend paymentAfter we paid a dividend of 0.09 € per share for the

first time last year, this year shareholders were pleased

to receive a dividend payment of 0.16 € per share.

We intend to continue this positive development

and plan to propose the distribution of a dividend

of EUR 0.24 for the 2019/2020 financial year at the

next Annual General Meeting.

Outlook 2020/2021We want to continue the development of the past

years with steady and sustainable growth in

2020/2021. In addition to manageable risks, the

effects of the corona crisis offer additional oppor-

tunities that we can exploit. For example, we have

actively promoted the issue of sale-and-lease-back

and positioned ourselves as a contact for German

SMEs. We are confident that we will be able to invest

a volume of between 100 € million and 200 € million

again this year. For the 2020/2021 financial year, we

expect to be able to achieve FFO of 32 € million to

34 € million.

We would like to take this opportunity to thank our

shareholders, our tenants, our employees, and service

providers for their great support.

With best regards,

Rolf Elgeti

Chief Executive Officer

Sonja Petersen

Chief Investment Officer

René Bergmann

Chief Financial Officer

Potsdam in December 2020

4Deutsche Industrie REIT-AG Annual report 2019/2020

22.00

15.10

Jan. 20 Feb. 20 Mar. 20Oct. 19 Nov. 19 Dec. 19 Apr. 20 May 20 Jun. 20 Jul. 20 Sep. 20Aug. 2014

15

16

17

18

19

20

21

22

23

September 2019August 2019Juli 2019Juni 2019Mai 2019April 2019März 2019Februar 201903.01.2019Januar 2019Dezember 2018November 2018Oktober 2018

EUR

The Stock Market in view of the Corona Pandemic In 2019, the stock market experienced a massive rally.

Initial success with the negotiations between the USA

and China surrounding the trade dispute boosted the

markets. In 2019, the stock exchanges also benefited

from the central banks furthering their expansive

monetary policy in view of weakening economic.

The DAX closed the 2019 trading year with a plus of

25.5 %. Even both the MDAX and the SDAX rose by

31 %. At the beginning of the year 2020, the global

economy was in a strong position. Following the

worldwide outbreak the Corona Pandemic in Febru-

ary and the widespread national lockdowns put in

place to contain the pandemic, the stock markets

plummeted by over 30 %. The global economy came

under massive pressure and the economy slumped

sharply. After the fall in economic output in the

first half of 2020 a slight initial recovery of economic

activity was recorded. In April 2020 there was an

easing of the restrictions and in many countries some

sense of normality was restored. There is still however

a risk of setbacks as the results of the pandemic con-

tinue to progress. In the summer quarter, despite a

gradual recover, the economy was still far from the

pre-crisis level. A main reason for this, is that the

pandemic has still not been effectively contained

in many countries. After the massive economic

downturn in March and April a V-shaped recovery

took place in May on the stock markets. Nine months

into 2020, the DAX stood at 12,760.70 points,

exceeding the level of the previous year despite

Corona (September 30, 2019: 12,428.10 points).

The share

• Deutsche Industrie REIT-AG - Share price development (XETRA)

5Deutsche Industrie REIT-AG The share

DIR share performs well in the crisisAt the beginning of the 2019/2020 financial year, the

share price (opening price on October 1, 2019) stood

at EUR 17.20. Prior to the effects of the Corona crisis

and the resulting distortions in the stock markets, the

price was always stable above EUR 20.00. The lowest

value of the fiscal year was recorded on 06.04.2020 at

EUR 14.80, the highest share price reached EUR 23.60

on May 5, 2020. After the distortions on the stock

markets at the peak of the Corona crisis in March

and April the DIR share recovered faster and more

strongly than other German real estate stocks and

in May to June was traded at between EUR 19.00

and EUR 22.00.

Capital increases Within the 2019/2020 financial year, two capital

increases resulted in a significant increase in both

the capital stock and the number of shares. The first

cash capital increase took place in November 2019

(+5,711,242 shares) followed by a second increase in

June 2020 of 10 % without subscription rights of the

share capital (+2,916,318 shares), which increased the

number of shares to the current value of 32,079,505.

Shareholder structureThe shareholder structure is characterised by insti-

tutional national and international investors with

a predominantly long-term investment strategy.

The free float (as defined by Deutsche Börse AG

in compliance with the attribution regulations

pursuant to the German Securities Trading Act

(WpHG))amounted to 42.5 % at the reporting date

on September 30, 2020.

• Shareholder structure

The percentages are based on voting rights notifications in accordance with Sections 33 et seq. WpHG of the named shareholders, or notifications of managers transactions pursuant to Art. 19 MAR as well as individual voluntary disclosures by some shareholders. The voting rights in each case relate to the number of total voting rights at the time of the notification. In addition, there is the possibility that the share of voting rights has changed since then without any obligation to notify within the respective thresholds.

7.8 % Obotritia Capital KGaA

7.0 % Obotritia Alpha Invest GmbH4.7 % Obotritia Beta Invest GmbH4.4 % Babelsberger Beteiligungs GmbH3.6 % Försterweg Beteiligungs GmbH2.2 % Obotritia Delta Invest GmbH

29.7 % Total Obotritia-Group

9.8 % VBL

5.2 % Aurelius Growth Investments S.a.r.l.0.2 % Lotus AG0.9 % Olive Tree Invest GmbH

6.3 % attributable to Dirk Markus

6.2 % Parson GmbH5.0 % Massachusetts Financial Services 4.7 % Gert Purkert3.7 % Rocket Internet SE0.5 % Rolf Elgeti34.1 % Remaining free float

6Deutsche Industrie REIT-AG Annual report 2019/2020

Analyst CoverageIn February 2020, Berenberg Bank launched the

coverage on which the DIR shares are valued by three

separate analysts:

• The DIR share at a glance:

As of 30/09/2020

WKN

ISIN

Ticker Symbol

Listing date

Number of shares

Nominal capital in EUR

Stock exchanges

Market segment

Transparency level

A2G9LL

DE000A2G9LL1

JB7

07 December 2017

32,079,505

EUR 32,079,505.00

XETRA, Frankfurt and Berlin

Regulated market

Prime Standard

Date Institute Report Analyst Recommendation Target Price

23/11/2020 Baader Bank Update Andre Remke „Buy“ 24.00 EUR

08/09/2020 Berenberg Bank Update Kai Klose „Buy“ 23.00 EUR

13/08/2020 ODDO BHF Update Manuel Martin „Buy“ 24.50 EUR

Investor RelationsTo ensure a transparent and continuous dialogue

with existing and potential investors the DIR contin-

ued to intensify their investor relation activities in

2019/2020. In doing so, the company managed to

sustain more individual discussions and a greater

representation at various conferences.

Furthermore, in the 2019/2020 financial year, the DIR

often present in major investor media reports and

was thus able to improve its perception of the

company on the capital markets. On the Investor

Relations pages of the website, interested parties can

find information on capital market law mandatory

notices, such as ad-hoc announcements, as well as

financial reports and investor presentations available

for download.

7Deutsche Industrie REIT-AG The sharePICTURE:

Bad Oeynhausen, Unterer Sundern

8Deutsche Industrie REIT-AG Annual report 2019/2020

Declaration on corporate governance and Corporate Governance ReportIn the following, the Supervisory Board and the

Management Board of Deutsche Industrie REIT-AG

(DIR or the “Company”) report on the corporate

governance of the company and on the management

of the company in accordance with Section 289f of

the German Commercial Code (HGB).

The current Declaration of Conformity of the Super-

visory Board and the Management Board of Deutsche

Industrie REIT-AG dated 23 October 2020 is repro-

duced first. This is followed by a description of the

working methods of the Supervisory Board and

Management Board and their composition. In addi-

tion, the corporate governance of the company is

presented, and the diversity concept is discussed.

1. Declaration of Compliance of Deutsche Industrie REIT-AG with the German Corporate Governance Code (DCGK)

The Management Board and Supervisory Board of

Deutsche Industrie REIT-AG welcome and support the

German Corporate Governance Code (GCGC) and

the objectives it pursues.

They hereby declare in accordance with section 161

(1) of the German Stock Corporation Act (Aktienge-

setz) that Deutsche Industrie REIT-AG has complied

with the recommendations of the Government Com-

mission on the German Corporate Governance Code

as amended on 7 February 2017 and published by the

Federal Ministry of Justice in the official section of the

Federal Gazette (Bundesanzeiger) in the version of the

Code dated 7 February 2017, published in the Federal

Gazette on 24 April 2017, with the following excep-

tions, since the submission of the last declaration of

compliance on 25 October 2019:

Section 4.1.3 DCGK - Compliance Management System: The company has not employed more than six em-

ployees since the last declaration of compliance was

issued. The Management Board therefore saw no need

to draw up and disclose systems of measures in a

formalised form for compliance management or a

so-called “whistleblowing”. In view of the size of the

company, the cost of setting up, implementing, and

maintaining formalised systems of measures was and

is disproportionate to the potential benefits.

Section 4.1.5 DCGK - Consideration of women in filling management positions: The Management Board did not follow the recom-

mendation that diversity should be taken into

account when filling management positions in the

company, and in particular that women should be

given appropriate consideration. The company had

and currently has only employees without manage-

ment functions. Apart from the Management Board,

there were no management positions to be filled in

the company, which is why the company could not

follow this recommendation for formal reasons. For

this reason, the company had set 0 % as the target

figure for the participation of women in management

positions for the period until 30 September 2020 and

0 % as the target figure for the period until 30 Sep-

tember 2025. At Deutsche Industrie REIT-AG, how-

ever, the decisive criterion for filling management

positions is qualification and suitability, irrespective

of gender.

Section 4.2.1 Sentence 2 GCGC - Rules of Procedure for the Management Board: There were no rules of procedure for the Management

Board in the past year. The company believed this

instrument would not contribute to the effectiveness

of the Management Board in view of its small size.

9Deutsche Industrie REIT-AG Corporate Governance Report

Section 5.1.2 (1) Sentences 2 and 3; (2) Sentence 3 GCGC – Consideration of diversity, setting targets for the proportion of women on the Management Board and setting an age limit: The Supervisory Board did not follow the recommen-

dation to take diversity into account when appoint-

ing members of the Management Board. The compa-

ny believed professional qualifications and knowledge

of the company were decisive as prerequisites for

appointment. However, the company has set a target

of one-third for the period until 30 September 2020

for the participation of women on the Management

Board, which is currently being met. By 30 September

2025, the company has set one third as the target

figure for the participation of women on the Manag-

ing Board. For the reasons outlined above, an age

limit for members of the Board of Management had

not previously been set. By reso lution of 10 Septem-

ber 2020, the Supervisory Board has now decided on

an age limit for the Board of Management.

Section 5.3 DCGK - Formation of committees: In view of its small number of members, the Supervi-

sory Board had previously refrained from forming

committees. In view of the continued low level of

complexity and the transparent business model of

Deutsche Industrie REIT-AG, it did not consider it

necessary to form committees and devoted its entire

attention to the issues at hand.

Section 5.4.1 (2), (3), (4) DCGK - Specification of objectives for the composition of the Supervisory Board, particularly with regard to diversity, and development of a competence profile as well as an age limit to be specified and a rule limit for membership of the Supervisory Board: The Supervisory Board has not set any concrete

objectives for its composition or developed a compe-

tence profile for the entire body. Nor have rules on

diversity been laid down in the objectives for the

composition of the supervisory board. The company

believed professional qualifications and knowledge

of the company were decisive as prerequisites for

appointment, so that the aforementioned require-

ments were not conducive to achieving the objec-

tives. For this reason, the company has set 0 % for the

period up to 30 September 2020 and 20 % for the

period up to 30 September 2025 as the target figure

for the participation of women on the Supervisory

Board. For these reasons, the company has not yet set

an age limit or a standard limit for membership of

the Supervisory Board. By resolution dated 10 Sep-

tember 2020, the Supervisory Board has now set an

age limit of 80 years. As the GCGC in the version

dated 16 December 2019, does not recommend a rule

limit to be set for the length of service on the Super-

visory Board, the company will not comment on this

point in future.

The Management Board and the Supervisory Board of

Deutsche Industrie REIT-AG further hereby declare in

accordance with section 161 (1) of the German Stock

Corporation Act (Aktiengesetz) that Deutsche Indus-

trie REIT-AG has complied since the announcement

with the recommendations of the Government Com-

mission on the German Corporate Governance Code

in the version dated 16 December 2019, published

in the official section of the Federal Gazette on

20 March 2020, with the following exceptions and

will comply with the recommendations in the future

with the following exceptions:

Recommendation A.1 GCGC – Respect for diversity when filling management positions: The Management Board does not currently follow the

recommendation to take diversity into account when

filling management positions in the company. The

company currently only has employees without

management functions. Apart from the Management

Board, there are no management positions to be filled

in the company, which is why the company cannot

currently follow this recommendation for formal

reasons.

10Deutsche Industrie REIT-AG Annual report 2019/2020

Recommendation A.2 DCGK – Compliance Management System: The company currently employs only six staff. The

Management Board therefore sees no need to develop

and disclose systems of measures in a formalised form

for compliance management or a so-called “whistle-

blowing”. In view of the size of the company, the cost

of setting up, implementing, and maintaining formal-

ised systems of measures has never been and is not in

any reasonable proportion to the potential benefits.

Recommendation B.1 GCGC – Observance of diversity in the composition of the Management Board: The Supervisory Board does not currently follow the

recommendation to observe diversity when appoint-

ing Management Board members in the company.

The company is of the opinion that professional

qualifications and knowledge of the company are

decisive as prerequisites for appointment, so that the

above-mentioned requirements are not conducive to

achieving the objective.

Recommendation B.2 DCGK – Long-term Succession planning by the Supervisory Board and Management Board: In view of the current age of the members of the

Management Board (37 to 50 years), the company

does not consider long-term succession planning to

be necessary at present.

Recommendations C.1 and C.2 GCGC – Specification of objectives for the composition of the Supervisory Board, in particular consideration of diversity and the develop-ment of a competence profile, and specification of an age limit for members of the Supervisory Board: The Supervisory Board has not set any concrete

objectives for its composition or developed a compe-

tence profile for the entire body and does not intend

to set such objectives or develop a competence profile

in the future. Nor have any rules on diversity in the

objectives for the composition of the Supervisory

Board been set or are to be set in the future. The

company is of the opinion that the professional

qualifications and knowledge of the company are

sufficient as prerequisites for the appointment of

members to the Supervisory Board, such that the

aforementioned objectives are not conducive to

achieving the objectives. For this reason, the compa-

ny had set 0 % as the target figure for the participa-

tion of women on the Supervisory Board for the

period up to 30 September 2020, and has dispensed

with setting an age limit for members of the Supervi-

sory Board. By resolution of 10 September 2020, the

Supervisory Board has now set a target of 20 % for

female participation in the Supervisory Board and

an age limit of 80 years for the period up until

30 September 2025.

Recommendation C.5 DCGK – Supervisory Board mandates in non-group listed companies: While the company assumes that Recommendation

C.5 of the GCGC contains guidelines for the mem-

bers of the company’s Supervisory Board (and not for

its Management Board), in view of the ambiguous

wording, it is pointed out that Management Board

member Rolf Elgeti holds more than two Supervisory

Board mandates in non-group listed companies or in

comparable supervisory bodies (also as Chairman of

the Supervisory Board).

Recommendation on section D.II.2 GCGC – Supervisory Board committees: In view of its small number of members, the Supervi-

sory Board has so far refrained from forming commit-

tees and therefore does not follow recommendations

D.2, D.3, D.4 and D.5 GCGC. In view of the contin-

ued low level of complexity and the transparent

business model of Deutsche Industrie REIT-AG, it is

not considered necessary to form committees in the

future either and continues to devote its full atten-

tion to the issues at hand.

Recommendation D.13 GCGC – self-assessment of the Supervisory Board:In view of the low complexity of the company and

its business model, it was assumed that the legally

required interval of Supervisory Board meetings and

the regular meetings held without the Management

Board, were adequate for the effective performance of

its duties. To this extent, a formalised self-assessment

system was dispensed with. By resolution dated

10 September 2020, the Supervisory Board has now

introduced a formalised self-assessment system and

will follow the recommendation in future.

11Deutsche Industrie REIT-AG Corporate Governance Report

Recommendations on Section G.I. of the GCGC – Remuneration of the Management Board: Section G.I. of the GCGC contains new recommen-

dations on the remuneration of the Management

Board, which the current remuneration model of

Deutsche Industrie REIT-AG does not fully comply

with, as it has become outdated and dates back to the

time before the announcement of the Government

Commission on the German Corporate Governance

Code in the version dated 16 December 2019. This

includes the recommendations on the determination

of the remuneration system (G.1), on the determina-

tion of the amount of the variable remuneration

components (G.6, G.7, G.8, G.10 and G.11) and on

benefits upon termination of contract (G.12, G.13

and G.14). The Supervisory Board and Management

Board intend to make the recommendations the focus

of the review of the 2020/2021 compensation system.

Recommendation G.3 GCGC – customary level of specific total remuneration:The Supervisory Board is currently not carrying out

a peer group comparison to assess the customary

level of Management Board remuneration, as there

is currently not a sufficient representation and

therefore a lack of suitable comparable companies/

REITs in Germany. Nevertheless, the Supervisory

Board checks that the remuneration of the Board

of Management is appropriate and customary by

comparing it with national and international listed

real estate companies in the broader sense.

Recommendation G.4 GCGC – Assessment of the customary level of Management Board remuneration within the company:At present, the Supervisory Board does not determine

the customary level of Management Board remune-

ration by establishing a relationship with senior

management and the workforce, since firstly, due to

the small size and low complexity of the company,

there is currently no senior management level and

secondly, the number of employees is too small to be

able to make meaningful deductions.

Recommendation G.16 GCGC – crediting of remuneration when members of the Supervisory Board take on non-group supervisory board mandates: The Supervisory Board does not follow the recom-

mendation that, when members of the Management

Board take on non-group supervisory board man-

dates, it should decide whether and to what extent

remuneration from the respective supervisory board

mandate should be credited. Based on past experience

with the members of the Management Board and

their dealings with non-group Supervisory Board

mandates, it is not expected that non-group Supervi-

sory Board mandates will have a negative impact on

the future activities of the members of the Manage-

ment Board for the company. Given the Supervisory

Board’s ability to exercise control, which also exists

independent of the recommendation, a decision on

the crediting of remuneration from non-group

Supervisory Board mandates is not necessary.

Rostock, 23 October 2020

For the Supervisory Board

Hans-Ulrich Sutter Chairman of the Supervisory Board

For the Management Board

Rolf Elgeti Chairman of the Management Board

12Deutsche Industrie REIT-AG Annual report 2019/2020PICTURE:

Remscheid, Rosentalstraße

13Deutsche Industrie REIT-AG Corporate Governance Report

The current declarations of compliance are published

on our website https://www.deutsche-industrie-reit.

de/, in the “Investor Relations” section under the

menu items “Corporate Governance” and “Declara-

tion of Compliance”.

2. Functioning of the Management Board and Supervisory Board

Management structure with three bodiesThe Management Board and Supervisory Board work

closely together for the benefit of the company to

ensure responsible management and control of the

company through good corporate governance.

An essential element of corporate governance is the

separation of corporate management and corporate

control. This is achieved through a clear division of

tasks and responsibilities between the Management

Board and the Supervisory Board. In addition, the

Annual General Meeting is the third body. Through

it, shareholders participate in fundamental decisions

of the company.

The Management BoardThe Management Board manages the company on its

own responsibility and represents it in transactions

with third parties. In doing so, it is bound to the

interests of the company with the aim of creating

sustainable value. It develops the company’s strategic

orientation, agrees it with the Supervisory Board and

ensures its implementation. The Management Board

also ensures that appropriate risk management and

controlling systems are in place within the company.

The members of the Management Board are responsi-

ble for individual areas of responsibility, irrespective

of their joint responsibility for the company. They

work together as colleagues and keep each other

informed of important events and measures in their

areas of responsibility. The Management Board has

not yet adopted rules of procedure.

The Management Board of Deutsche Industrie

REIT-AG is appointed by the Supervisory Board in

accordance with Article 6 No. 2 of the Articles of

Association. The Supervisory Board also determines

the total number of members on the Management

Board and whether there should be a Chairman or

Spokesman. The members of the Management Board

are appointed for a maximum of five years. Reap-

pointments are permitted.

The Supervisory Board does not currently follow

recommendation B.1 of the German Corporate

Governance Code (DCGK) to take diversity into

account when appointing members of the Manage-

ment Board. The company is of the opinion that

professional qualifications and knowledge of the

company are sufficient as prerequisites for appoint-

ment, with the result that the above-mentioned

requirements are not conducive to achieving the

objectives.

However, the Supervisory Board set a target

of one third for the proportion of women on the

Management Board for the period up to 30 Septem-

ber 2020 and maintains this target, by resolution of

10 September 2020, for the period up to 30 Septem-

ber 2025. This target figure has been achieved in the

past and is currently being achieved. No further rules

on diver sity in the targets for the composition of the

Management Board have been defined to date.

The Management Board of Deutsche Industrie

REIT-AG consists of three persons: Mr Rolf Elgeti

(CEO), Ms Sonja Petersen (née Paffendorf) (CIO)

and Mr René Bergmann (CFO). The Management

Board contract of Mrs. Sonja Petersen (née Paffendorf)

was extended for a further three years until 17 Octo-

ber 2023.

The CEO, Mr Rolf Elgeti, is responsible for Human

Resources, Public Relations and Strategy. The CIO,

Mrs. Sonja Petersen (née Paffendorf), is responsible

for investment and asset management. The CFO,

Mr René Bergmann, is responsible for the areas of

accounting/controlling, financing and investor

relations. All three Management Boards also manage

and control external service providers for their respec-

tive areas.

14Deutsche Industrie REIT-AG Annual report 2019/2020

The CVs of the members of the Management Board

can be found at https://deutsche-industrie-reit.de/en/

company/ceo/

The Supervisory Board and Management Board agree

on annual targets, the achievement of which is

regularly reviewed.

The Management Board is responsible for training

and refresher courses.

In section B.2, the DCGK recommends that long-term

succession planning should be carried out by the

Supervisory Board. The DIR does not comply with

this recommendation, as the company does not

currently consider long-term succession planning to

be necessary in view of the current age of the mem-

bers of the Management Board (37 to 50 years).

The company had previously believed the profession-

al qualifications and knowledge of the company were

decisive as prerequisites for appointments, so that no

age limit had been set for members of the Board of

Management. In a resolution dated 10 September

2020, the Supervisory Board has now decided to set

an age limit of 80 years for members of the Manage-

ment Board.

A D&O insurance policy has been taken out for the

members of the Management Board, considering

Section 93 (2) of the German Stock Corporation Act

(AktG).

The remuneration of the CEO, Rolf Elgeti, is currently

paid in the form of fixed remuneration via a pay-as-

you-go agreement with Obotritia Capital KGaA. The

remuneration system for the Management Board

members Sonja Petersen and René Bergmann is based

on short and long-term remuneration incentives.

Detailed information on the remuneration of the

Management Board is provided in the remuneration

report in the management report 2019/2020.

Section G.I. of the GCGC contains new recommenda-

tions on the remuneration of the Management Board,

which the current remuneration model of Deutsche

Industrie REIT-AG does not fully comply with, as it

was agreed on prior to the announcement of the Gov-

ernment Commission on the German Corporate

Governance Code in the version dated 16 December

2019. This applies to the recommendations on the

determination of the remuneration system (G.1), the

determination of the amount of the variable remu-

neration components (G.6, G.7, G.8, G.10 and G.11)

and benefits upon termination of the contract (G.12

and G.13). Before the next annual shareholders’

meeting, the supervisory board will pass a resolution

in accordance with § 87a (1) of the German Stock

Corporation Act (AktG) on the future remuneration

system for the Management Board and submit it to

the shareholders’ meeting for approval in accordance

with § 120a (1) of the German Stock Corporation Act

(AktG).

Consideration of women when filling management positionsThe Management Board does not currently follow

recommendation A.1 of the German Corporate

Governance Code (DCGK) to pay attention to

diversity when filling management positions in the

company. The company currently only has employees

without management functions. Apart from the

Management Board, there are no management

positions to be filled in the company, which is why

the company cannot currently follow this recommen-

dation for formal reasons. Even if the company was

and is of the opinion that Section 76 (4) AktG has no

practical scope in this particular case due to the lack

of management positions to be filled, the company

had, purely as a precautionary measure for the period

up to 30 September 2020 and currently maintains, by

resolution of 10 September 2020 for the period up to

30 September 2025, 0 % as the target for the participa-

tion of women in management positions. At Deutsche

Industrie REIT-AG, however, the decisive criterion for

filling management positions is qualification and

suitability, irrespective of gender.

The Supervisory BoardThe central tasks of the Supervisory Board are to

advise and monitor the Management Board. The

five-member Supervisory Board of Deutsche Industrie

REIT-AG works based on rules of procedure which it

has given itself. Overall, the members of the Supervi-

15Deutsche Industrie REIT-AG Corporate Governance Report

sory Board have the knowledge, skills and profession-

al experience required to properly perform their

duties.

Proposals for resolutions and information on the

subjects to be discussed are made available to the

members of the Supervisory Board in good time

before the respective meeting. By order of the

Chairman of the Supervisory Board, resolutions may

be passed outside meetings in individual cases. This

option is occasionally used in urgent cases. In the

event of a tied vote on resolutions, the Chairman of

the Supervisory Board has the casting vote.

All members of the Supervisory Board are elected by

the shareholders at the Annual General Meeting.

There are currently no employee representatives on

the Supervisory Board of Deutsche Industrie REIT-AG.

In the opinion of the shareholder representatives on

the Supervisory Board, all shareholder representatives

are to be considered independent.

The Supervisory Board does not intend to set specific

targets for its composition or to draw up a compe-

tence profile for the entire body. Nor is it intended to

lay down rules on diversity in the objectives for the

composition of the supervisory board. The company

is of the opinion that professional qualifications and

knowledge of the company are decisive as prerequi-

sites for appointment, so that the aforementioned

requirements are not conducive to achieving compa-

ny objectives. For this reason, the company set 0 % as

the target for the participation of women on the

Supervisory Board for the period up to 30 September

2020. This target figure was achieved during the

relevant period; since 6 March 2020, the actual level

of female participation has been 40 %. By resolution of

10 September 2020, the Supervisory Board has now set

20% as the target figure for female participation on

the Supervisory Board for the period until 30 Septem-

ber 2025. This target figure is currently also being met.

The Supervisory Board of Deutsche Industrie REIT-AG

currently consists of five persons: Mr Hans-Ulrich

Sutter, Dr Dirk Markus, Mr Achim Betz, Ms Cathy

Bell-Walker and Ms Antje Lubitz.

Hans-Ulrich Sutter is Chairman of the Supervisory

Board, Dr Dirk Markus is the first vice Chairman and

Achim Betz is the second vice Chairman. The term of

office of all members of the Supervisory Board expires

at the end of the Annual General Meeting that

resolves on the discharge of the members of the

Supervisory Board for the financial year ending on

30 September 2024.

The CV‘s of the members of the Supervisory Board are

published at https://www.deutsche-industrie-reit.de/

en/ in the section “Company” under the menu item

“Supervisory Board”.

In view of its small number of members, the Supervi-

sory Board has so far refrained from forming commit-

tees and therefore does not follow recommendations

D.2, D.3, D.4 and D.5 DCKG. In view of the continu-

ing low level of complexity and the transparent

business model of Deutsche Industrie REIT-AG, it

does not consider it necessary to form committees in

the future either and continues to devote its full

attention to the issues at hand.

In the past, no age limit was set. The company was of

the opinion that the specification of an age limit was

not appropriate, as the knowledge and experience of

older persons should also be available to the compa-

ny over a longer period of time in the context of

Management Board and Supervisory Board activities.

In addition, professional qualifications and knowl-

edge of the company should be decisive as pre-

requisites for filling the position. By resolution of

10 September 2020, the Supervisory Board has now

set an age limit of 80 years for the Supervisory Board.

The Chairman of the Supervisory Board explains the

activities of the Supervisory Board in his annual

report and verbally at the Annual General Meeting.

The Supervisory Board regularly assesses the effi-

ciency of its own performance of its duties during

meetings held in person and by telephone. By

resolution dated 10 September 2020, the Supervisory

Board has now introduced a formalised self-assess-

ment system, which will be applied in the current

16Deutsche Industrie REIT-AG Annual report 2019/2020

financial year. It will report on the manner and

results in the next declaration on corporate govern-

ance.

A D&O insurance policy was taken out for the

members of the DIR Supervisory Board in January

2018.

In accordance with the Articles of Association, the

members of the Supervisory Board receive a fixed

remuneration and reimbursement of cash expenses.

Detailed information on the remuneration of the

Supervisory Board is provided in the remuneration

report in the management report 2019/2020.

The members of the Supervisory Board ensure that

they have sufficient time to perform their duties.

They are responsible for providing the necessary basic

and advanced training. The company provides

appropriate support to the members of the Super-

visory Board during their inauguration and training

and further training. All members of the supervisory

board are given access to specialist literature and are

reimbursed for the costs of attending seminars and

webinars in which topics relevant to the work of the

supervisory board are covered.

Further details of the work of the Supervisory Board

can be found in the Report of the Supervisory Board,

which is part of the Annual Report 2019/2020.

Cooperation between Management Board and Supervisory BoardThe Supervisory Board appoints the members of the

Management Board, determines their respective total

remuneration and monitors their management of the

company. It also advises the Management Board on

the management of the company. The Supervisory

Board approves the annual financial statements.

Major decisions made by the Management Board

require the approval of the Supervisory Board.

The Management Board ensures regular, timely and

comprehensive reporting to the Supervisory Board.

In addition, the Chairman of the Supervisory Board

is kept regularly and continuously informed about

business developments. Intensive and continuous

communication between the Management Board

and the Supervisory Board is the basis for efficient

corporate management.

The Management Board of Deutsche Industrie

REIT-AG regularly attends the meetings of the

Supervisory Board. It reports in writing and orally on

the individual agenda items and draft resolutions

and answers the questions of the Supervisory Board

members. If necessary, the Supervisory Board also

meets without the Management Board.

Conflicts of interestConflicts of interest of members of the Management

Board and Supervisory Board must be disclosed to the

Supervisory Board without delay. No conflicts of

interest arose in the 2019/2020 financial year.

17Deutsche Industrie REIT-AG Corporate Governance Report

3. Essential corporate governance practices

Basic principles of complianceDeutsche Industrie REIT-AG is committed to responsi-

ble management of the company with a focus on

sustainable value creation. This includes cooperation

in a spirit of trust between the Management Board

and the Supervisory Board as well as between employ-

ees and a high level of transparency in reporting and

corporate communications.

The main basis of Deutsche Industrie REIT-AG’s

business is to create, maintain and strengthen the

trust of tenants, business partners, shareholders and

other capital market participants and employees.

Thus, compliance at DIR means not only adherence

to legal principles and the Articles of Association, but

also adherence to internal instructions and voluntary

commitments to implement the values, principles,

and rules of responsible corporate governance in

daily operations.

Compliance management SystemCurrently, the DIR has only five employees (exclud-

ing the Management Board). The Management Board

therefore saw and still sees no need to draw up and

disclose systems of measures in a formalised form for

compliance management and a so-called “whistle

blowing”. In view of the size of the company, the cost

of setting up, implementing, and maintaining formal-

ised systems of measures has never been and is not in

any reasonable proportion to the potential benefits.

Organisation and ControllingDeutsche Industrie REIT-AG has its registered office in

Germany and is therefore subject to the provisions of

German stock corporation and capital market law

and the provisions of the Articles of Association.

Deutsche Industrie REIT-AG manages the company

primarily based on the following key figures: EBIT,

FFO, LTV, EPRA NAV and cash flow. Sustainable

economic, social, and ecological aspects are consid-

ered.

Shareholders and Annual General MeetingThe shareholders of Deutsche Industrie REIT-AG

exercise their rights before or during the Annual

General Meetings to the extent permitted by law and

the Articles of Association and exercise their voting

rights. Each share grants one vote.

The Annual General Meeting is chaired by the

Chairman of the Supervisory Board. Every sharehold-

er is entitled to participate in the annual sharehold-

ers’ meeting, to speak on the respective items on the

agenda and to request information on company

matters, insofar as this is necessary for the proper

assessment of an item on the agenda. The sharehold-

ers’ meeting decides on all tasks assigned to it by law.

Deutsche Industrie REIT-AG publishes the agenda of

the annual general meeting and the reports and docu-

ments required for the annual general meeting on its

website at: https://www.deutsche-Industrie.de/en/ in

the section “Investor Relations” under the menu item

“Annual General Meeting”.

PICTURE:Wedemark, Industriestraße

18Deutsche Industrie REIT-AG Annual report 2019/2020

To make it easier for its shareholders to exercise their

rights personally and to be represented by a proxy,

the DIR appoints a representative to exercise voting

rights in accordance with instructions. This represent-

ative can also be contacted during the Annual

General Meeting.

The general meeting of shareholders takes place

within the first eight months of each financial year.

The Annual General Meeting of Deutsche Industrie

REIT-AG, which passed resolutions on the financial

year ended 30 September 2019, was held in Berlin on

6 March 2020. The Annual General Meeting resolved

to expand the Supervisory Board to five members and

re-elected the previous Supervisory Board members

Hans-Ulrich Sutter, Dr Dirk Markus and Achim Betz

and elected Cathy Bell-Walker and Antje Lubitz as

new members of the Supervisory Board.

It was also resolved to pay a dividend of EUR 0.16 per

share for the 2018/2019 financial year.

Furthermore, the Management Board and Supervisory

Board were approved for their term of office in the

2018/19 financial year. DOMUS AG Wirtschaftsprü-

fungsgesellschaft/Steuerberatungsgesellschaft, Berlin,

was elected as auditor for the 2019/20 financial year.

In addition, various minor amendments to the

Articles of Association were approved. New Author-

ised Capital 2020 was created, and a resolution was

passed on the creation of an authorisation to issue

warrant-linked and/or convertible bonds with the

option of excluding subscription rights.

Around 58 percent of the share capital was represent-

ed (share capital of the company at the time the

Annual General Meeting was convened: EUR

29,163,187).

All the items on the agenda were approved by

a large majority.

Stock option plansDeutsche Industrie REIT-AG currently has no stock

option programs or similar incentive systems.

Transparent reportingVia its website, Deutsche Industrie REIT-AG ensures

that shareholders and the interested public receive

uniform, comprehensive, timely and simultaneous

information on the economic situation and new

facts. This information is available on the website at

https://www.deutsche-Industrie-reit.de/en in the

“Investor Relations” section.

Reporting on the financial performance and financial

position is currently carried out in annual reports,

quarterly announcements as well as in the half-yearly

financial reports, which are available for download

on the company’s website. Significant current

information is published via Corporate News and ad

hoc announcements and is also made available on

the company’s website. In addition, transactions

by management personnel and related parties are

publicly disclosed as “Directors’ Dealings” in accord-

ance with Article 19 MAR (Market Abuse Regulation)

and are also available on the company’s website.

In accordance with Art. 18 MAR, prescribed insider

lists are maintained, and the persons included in

insider lists have been and are being informed of

the resulting legal obligations and sanctions.

Significant events and publication dates are main-

tained and published in the financial calendar, which

can be viewed at any time on the company’s website.

19Deutsche Industrie REIT-AG Corporate Governance Report

Accounting and Auditing The annual financial statements of Deutsche Indus-

trie REIT-AG are prepared in accordance with IFRS as

applicable in the European Union. After preparation

by the Management Board, the annual financial state-

ments are examined and approved by the audi tor and

the Supervisory Board. The company aims to publish

the annual financial statements within 90 days of the

end of the financial year in accordance with the

German Corporate Governance Code and to publish

the mandatory financial information during the year

(quarterly reports and the half-yearly financial report)

within 45 days.

The annual general meeting of shareholders which

passed a resolution on the financial year ended

30 September 2019, appointed DOMUS AG

Wirtschaftsprüfungsgesellschaft Steuerberatungs-

gesellschaft as auditor for the 2019/2020 financial

year. DOMUS AG’s audits comply with German

auditing regulations as well as the principles of

proper auditing laid down by the Institut der

Wirtschaftsprüfer (Institute of Auditors) and the

International Standards on Auditing. The chairman

of the supervisory board shall be informed immedi-

ately by the auditor of any reasons for exclusion or

exemption and any inaccuracies in the declaration

of compliance which arise during the audit. The

auditor reports without delay to the Chairman of

the Supervisory Board on all issues and incidents of

importance to the duties of the Supervisory Board

that arise during the audit and is obliged to inform

the Super visory Board immediately of any grounds

for exclusion or impartiality that may arise.

Opportunity and risk managementA key element of corporate management is risk

management to counter the risks to which Deutsche

Industrie REIT-AG is exposed adequately and system-

atically. A comprehensive process has been intro-

duced to enable management to identify, assess and

control risks and opportunities in good time. To this

extent, unfavourable developments and events

become transparent at an early stage and can be

analysed and dealt with in a targeted manner. Further

information on risk management is contained in the

opportunities and risks report in the management

report 2019/2020.

Rostock, December 2020

For the Supervisory Board

Hans-Ulrich Sutter Chairman of the Supervisory

For the Management Board

Rolf Elgeti Chairman of the Management Board

20Deutsche Industrie REIT-AG Annual report 2019/2020

Report of the Supervisory Board

Dear Shareholders,

In the 2019/2020 financial year, the Supervisory

Board of Deutsche Industrie REIT-AG duly performed

the duties incumbent on it under the law, the Articles

of Association and the Rules of Procedure.

Cooperation between Supervisory Board and Management BoardThe Supervisory Board continuously monitored and

advised the Management Board in the management

of the company. The Supervisory Board was directly

involved in all decisions of fundamental importance

to the company. The Board of Management fulfilled

its duties to provide information and informed the

Supervisory Board regularly, promptly and compre-

hensively, both in writing and verbally, about

corporate planning, the course of business, strategic

developments, the current situation of the company

and the current occupancy rates.

The members of the Supervisory Board always had

ample opportunity to critically examine the Manage-

ment Board’s proposed resolutions and to make their

own suggestions. In particular, the members of the

supervisory board discussed in detail and checked the

plausibility of all business transactions of significance

to the company on the basis of written and verbal

reports from the management board. On several

occasions the Supervisory Board dealt in detail with

the risk exposure, liquidity planning and equity of

the company. At the meeting for the balance sheet

approval the Board of Management also reported to

the Supervisory Board on the profitability of the

company, and in particular on the return on equity.

The Supervisory Board gave its approval for individu-

al business transactions as required by law, the articles

of association or the rules of procedure for the Board

of Management.

The Company provides appropriate support to the

members of the Supervisory Board during their inau-

guration and for training and further education meas-

ures. All members of the Supervisory Board are given

access to specialist literature and are reimbursed for

the costs of attending seminars and webinars which

include topics relevant to the work of the Supervisory

Board.

Attendance of the Supervisory Board meetingsA total of nine meetings of the Supervisory Board

were held in the period under review, of which two

were face-to-face meetings, two were internet con-

ferences and five were telephone conferences. In

addition, resolutions were passed by written proce-

dure. Resolution proposals submitted by the Board of

Management were approved following examination

of extensive documentation and intensive discussions

with the Board of Management. No committee meet-

ings of the Supervisory Board took place in the period

under review. If deemed necessary, the Supervisory

Board may meet without the Management Board.

No member of the Supervisory Board attended fewer

than half of the meetings. There were no conflicts of

interest amongst the members of the Management

Board or the Supervisory Board. Any conflicts must be

disclosed to the Supervisory Board without delay.

21Deutsche Industrie REIT-AG Report of the Supervisory Board

• The following overview shows the attendance of the members of the Supervisory Board at meetings in the 2019/2020 financial year:

MeetingHans-Ulrich Sutter

Dr. Dirk Markus

Achim Betz

Cathy Bell-Walker

Antje Lubitz

Date Species

Chairman of the Super-visory Board

First Deputy Chairman of the Supervisory Board

Second Deputy Chairman of the Supervisory Board

Member of the Supervisory Board

Member of the Supervisory Board

since 06.03.2020 since 06.03.2020

30/10/2019 Conference Call x x x

07/11/2019 Conference Call x x x

14/11/2019 Conference Call x x x

17/12/2019Face-to-face meeting, Potsdam

x x x

06/03/2020Face-to-face meeting, Berlin

x x x x (by telephone) x

20/05/2020 Internet Conference x x x x x

16/06/2020 Conference Call x x x x

17/06/2020 Conference Call x x x x

10/09/2020 Internet Conference x x x x x

Key issues discussed by the Supervisory BoardThe Supervisory Board’s discussions at the indivi dual

meetings focused on the following key issues:

On 30 October 2019, the Supervisory Board approved

the resolution put forward by the Board of Manage-

ment on the same date to implement a capital

increase with subscription rights against cash contri-

butions. The subscription price was resolved on 7

November 2019 and the volume of this capital

increase on 14 November 2020.

Meeting on 17 December 2019

• The auditor’s report on the inspection of the

annual financial statements for the 2018/2019

financial year and the audit of the dependency

report

• Resolution on the approval of the audited finan-

cial statements for the 2018/2019 financial year,

the proposal for the distribution of profits and

the audited dependency report

• Resolution on the Report of the Supervisory Board

for the 2018/2019 financial year

• Resolution on the variable remuneration for

the members of the Board of Management Sonja

Petersen and René Bergmann for the financial

year 2018/2019 and the setting of targets for the

variable remuneration for the financial year

2019/2020.

• Discussions on the agenda for the Annual General

Meeting on 6 March 2020

• Management Board report business developments,

the portfolio and successful acquisitions, the

financing and the acquisition pipeline

• Resolution to offer Mrs. Sonja Petersen a contract

extension and appointment to the Management

Board for a further three years.

22Deutsche Industrie REIT-AG Annual report 2019/2020

In accordance with the articles of association, the

term of office of the previous members of the Super-

visory Board ended at the end of the last Annual

General Meeting. In accordance with the resolution

of the Annual General Meeting on 6 March 2020,

the Supervisory Board was expanded from three to

five members. The previous members of the Supervi-

sory Board, Mr. Hans-Ulrich Sutter, Dr. Dirk Markus

and Mr. Achim Betz were re-elected to the Supervisory

Board. Newly elected members are Ms Cathy Bell-

Walker and Ms Antje Lubitz. The Supervisory Board

was constituted on 6 March 2020, immediately after

the Annual General Meeting. At the meeting,

Mr Hans-Ulrich Sutter was re-elected unanimously as

Chairman. Dr. Dirk Markus was unanimously elected

as first vice Chairman. Achim Betz was unanimously

elected as second vice Chairman.

Meeting on 20 May 2020

• Report of the Management Board for the first half

of 2019/2020

• Report of the Management Board on the effects

of the Corona crisis

• Presentation of completed and planned

acquisitions

• Information on the financial situation

of the company

• Consultation on the Declaration of Compliance

2020 with the German Corporate Governance

Codex and other corporate governance issues

On 16 June 2020, the Supervisory Board approved

the resolution of the Board of Management to imple-

ment a capital increase with exclusion of subscription

rights. On 17 June 2020, the Supervisory Board ap-

proved the volume and the Board of Management’s

pricing proposal for this capital increase.

Meeting on 10 September 2020

• Report by the Management Board on business

developments, acquisitions and financing, and

expectations regarding the development of the

results for the financial year

• Resolution on targetting 20 % female represen-

tation on the Supervisory Board

• Resolution on setting a target of a one-third

proportion of women on the Management Board

• Resolution on the setting of a standard age limit

of 80 years for members of the Supervisory Board

and Management Board

• Resolution on the adjustment of the rules of

procedure of the Supervisory Board. The rules

of procedure have since been published on the

website https://www.deutsche-industrie-reit.de/

in the Investor Relations/Corporate Governance

section.

• Presentation of the 2020 draft statement in

compliance with the German Corporate Govern-

ance Codex and agreement to adopt it by circular

resolution in October 2020

In addition, individual transactions requiring approv-

al were approved by the Supervisory Board by circular

resolution.

Corporate governance

The Management Board also reports on corporate

governance at Deutsche Industrie REIT-AG on behalf

of the Supervisory Board in the corporate governance

declaration. This report is published on the compa-

ny’s website at https://www.deutsche-industrie-reit.

de/ in the Investor Relations/Corporate Governance

section and in the 2019/2020 Annual Report. The

Management Board and the Supervisory Board

23Deutsche Industrie REIT-AG Report of the Supervisory Board

repeatedly discussed the recommendations and

proposals from the German Corporate Governance

Code and issued a declaration of compliance in

accordance with section 161 of the German Stock

Corporation Act (AktG) on 23 October 2020.

Annual audit

The annual financial statements for Deutsche Indus-

trie REIT-AG as of 30 September 2020 prepared by

the Management Board, together with the manage-

ment report of the company, were audited by the

auditor appointed at the Annual General Meeting on

6 March 2020 and reviewed by the Supervisory Board,

DOMUS AG Wirtschaftsprüfungsgesellschaft/Steuer-

beratungsgesellschaft, Berlin, and issued with an

unqualified audit certificate.

The annual financial statements for Deutsche Indus-

trie REIT-AG and the management report of the

company as well as the auditor’s reports were made

available to all members of the Supervisory Board in

good time. The auditor attended the Supervisory

Board meeting on the 16 December 2020 for the

approval of the financial statements and reported on

the key findings of their audit at this meeting. This

included his comments on the internal control system

and risk management in relation to the accounting

process. He was also avai lable to the members of the

Supervisory Board for additional questions and

information. After a detailed discussion, the Supervi-

sory Board approved the results of the audit of the

annual financial statements and the management

report of the company.

PICTURE: Hannover, Wiesenauer Straße

24Deutsche Industrie REIT-AG Annual report 2019/2020

The Supervisory Board carefully examined the annual

financial statements and the management report

of the company, the proposal for the appropriation

of net profit and the audit reports of the auditor.

No objections were raised. The Supervisory Board

thereupon approved the annual financial statements

prepared by the Board of Management for the year

ended 30 September 2020. The annual financial

statements were thereby finalised.

Assessment of the report of the

Management Board on relations with

affiliated companies (dependency report)

The Board of Management has prepared a report

on relations with affiliated companies for the period

of control in accordance with Article 312 of the

German Stock Corporation Act and submitted it to

the Supervisory Board. The report of the Board of

Management on relations with affiliated companies

was the subject of the audit by the auditors. The

auditor issued the following opinion on the results

of his audit:

“Based on our audit and assessment in accordance

with professional standards, we confirm that

1. the factual information in the report

is correct

2. consideration paid by the company

for the legal transactions listed in the report

was not inappropriately high.“

The audit report was also submitted to the Superviso-

ry Board. The Supervisory Board examined both the

dependency report of the Board of Management and

the audit report of the auditors, and the auditors

participated in the Supervisory Board’s negotiations

on the dependency report and reported on the main

findings of their audit. Following the final results of

the review by the Supervisory Board, the Supervisory

Board concurs with the dependency report of the

Management Board and the audit report of the

auditors and raises no objections to the final state-

ment by the Management Board contained in the

dependency report.

Personnel changes on the Management

Board and Supervisory Boardt

There were no personnel changes in the Management

Board in the period under review. The manage-

ment contract of Ms. Sonja Petersen (née Paffendorf)

was extended for a further three years until 17 Octo-

ber 2023.

At the Annual General Meeting on 6 March 2020,

the Supervisory Board was expanded to five members.

Ms Cathy Bell-Walker and Ms Antje Lubitz were new-

ly voted onto the Supervisory Board. Furthermore,

the decision was made to allow the election of several

vice chairman to the Supervisory Board.

At the constituent meeting of the Supervisory Board

held after the Annual General Meeting, Mr Hans-

Ulrich Sutter was confirmed as Chairman of the

Supervisory Board. Dr. Dirk Markus was elected as

first vice chairman and Achim Betz as second vice

chairman. The term of office of all members of the

Supervisory Board expires with the conclusion of the

Annual General Meeting that resolves on the dis-

charge of the members of the Supervisory Board for

the financial year ending on 30 September 2024.

The Supervisory Board would like to thank the Board

of Management and the employees for their commit-

ment and hard work in the 2019/2020 financial year.

Rostock, December 2020

For the Supervisory Board

Hans-Ulrich Sutter

Chairman of the Supervisory Board

25Deutsche Industrie REIT-AG Composition of the Management Board and Supervisory Board

Management Board

Sonja Petersen

CIO

Ms. Petersen is responsible for

the areas of acquisition and sales

as well as asset and property

management

Rolf Elgeti

CEO

Mr. Elgeti is responsible for

Human Resources, Public Relations

and Strategy

René Bergmann

CFO

Mr. Bergmann is responsible for

Corporate Finance, Accounting/

Controlling and Investor Relations

Composition of the Management Board and Supervisory Board

Supervisory Board

Hans-Ulrich Sutter

Chairman of the

Supervisory Board

Business diploma, Düsseldorf

Dr. Dirk Markus

First Deputy Chairman of

the Supervisory Board

MBA

CEO, Aurelius Group, London

Achim Betz

Second Deputy Chairman of

the Supervisory Board

Business diploma

Public accountant, Auditor,

Tax advisor, Nürtingen

The CVs of the members of the Management Board and Supervisory Board are published under https://deutsche-industrie-reit.de/en/company/ in the menu items “Management Board” respectively “Supervisory Board”.

Cathy Bell-Walker

Solicitor

Partner, Allen & Overy LLP,

London

Antje Lubitz

Real Estate Economist

Managing Director

3PM Services GmbH, Berlin

26Deutsche Industrie REIT-AG Annual report 2019/2020

REIT is the abbreviation for “Real Estate Investment

Trust”. These are listed real estate corporations whose

business purpose is long-term asset management and

the sustainable achievement of rental income. As a

result of their stock market listing, REITs have direct

access to the capital markets and, therefore, so to

speak, everlasting equity capital compared to real

estate funds. In addition, real estate stocks represent

a fungible investment vehicle for investors, enabling

indirect real estate investments in various asset

classes. Another key feature is the tax transparency

of the REIT company, as no income tax is levied at

company level and taxation at the investor level takes

place downstream of the dividend distribution. In

this respect, a REIT investment is equated to a direct

investment in real estate for tax purposes.

A REIT thus enables a broad spectrum of investors

to participate indirectly in real estate via shares. In

particular, retail investors can thus participate in

various real estate classes for which a direct invest-

ment in a property would not be considered due

to the volume, lump risk and management require-

ments.

For decades, REITs have been characterised by high

stability, profitability, dividend strength, and sus-

tained appreciation, and have long been established

Deutsche Industrie as REIT

PICTURE: Barleben, Im Hasenwinkel

27Deutsche Industrie REIT-AG Deutsche Industrie as REIT

in developed investment markets such as the US,

Canada, UK, France, Belgium, Singapore, Hong Kong

and Japan.

Essential prerequisites for becoming a REIT in

Germany derive from the REIT Law of 2007 and

include the following criteria:

• Minimum equity of the corporation of

EUR 15 million,

• Listing in the regulated market of a German

stock exchange

• At least 15 % free float in the shareholders,

• Limitation of the direct participation of a single

shareholder to 10 % of the share capital

• Minimum equity ratio of 45 %,

• Real estate assets of at least 75 % of total assets,

• Rental income of at least 75 % of total revenues,

• Minimum dividend distribution of 90 % of

the annual financial result according to

commercial law.

In this respect, the founding of a REIT already

requires a certain minimum size and stability of the

company. The German REIT criteria guarantee

shareholders high quality right from the start.

Furthermore, the listing in the “Regulated Market” on

a German stock exchange ensures the highest level of

transparency. For example, there are regular disclo-

sure requirements such as quarterly reporting in

German and English and mandatory participation

in analyst and investor events.

Finally, the tax exemption of a REIT stock company

enables very streamlined and cost-effective manage-

ment structures, as, e. g., no separate tax department

or managing complex tax structures are required.

In this respect, DIR is an interesting, low-risk and

attractive option on the capital market for investing

in German Light Industrial properties.

28Deutsche Industrie REIT-AG Annual report 2019/2020

It is the aim of the company to generate steady,

sustainable and profit-oriented growth. This can be

achieved with a balanced and regionally diversified

real estate portfolio and with a focus on the German

market.

DIR has a strong network and some longstanding

relationships with potential sellers of Light Industrial

real estate. As a result, the company receives a large

number of attractive property offers. Mostly these

assets are not sold through public auctions, but are

only offered to a small audience or even exclusively.

For this reason, the acquisition process and the

associated data management play a central role in the

valuation of the properties as well as the basic market

assessment. For this purpose, the acquisition team

has developed and implemented its own efficient

data collection for processing the offers. This exten-

sive data allows the company to carry out systematic

evaluations of the Light Industrial Real Estate market

in Germany.

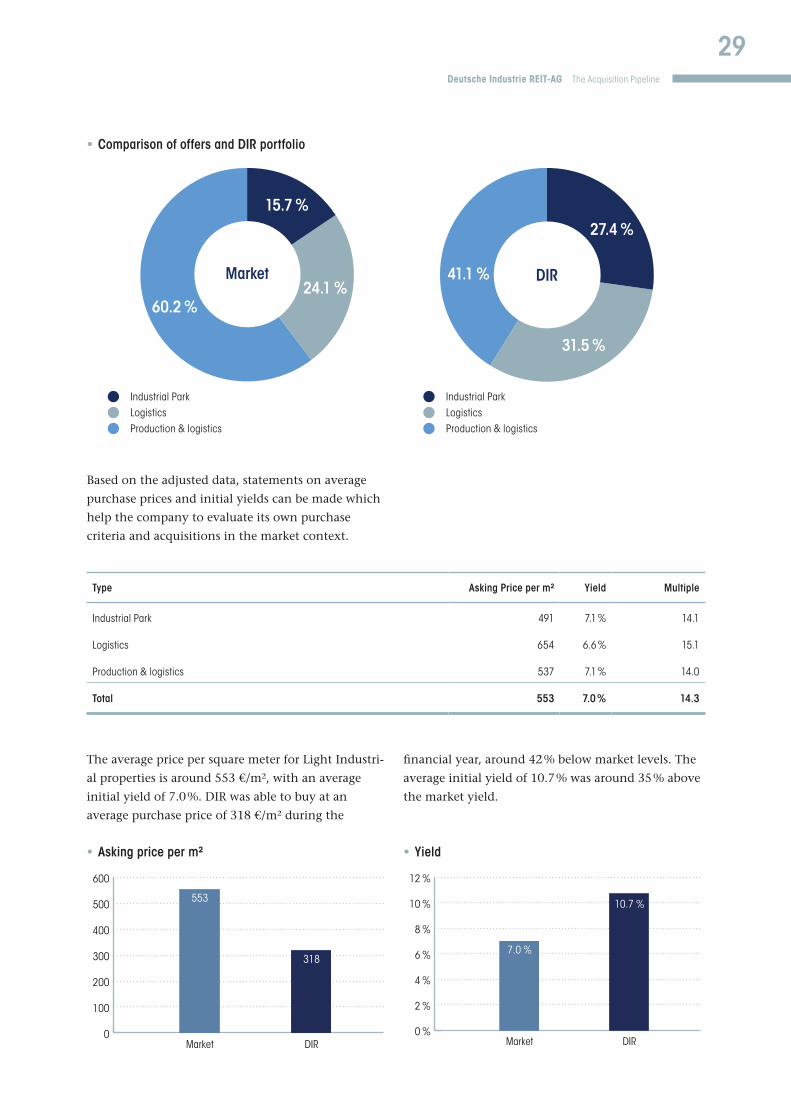

Structure of offers/Evaluation

In the FY 2019/2020, the Company received

525 property offers with a total purchase price

volume of approximately 3,278 € million. To ensure

the validity of the evaluation, duplicates and incom-

plete offers were adjusted for the overall result. Offers

are only considered if they provide, the basic infor-

mation purchase price, rent and total floor space. The

three classifications for the usage of the properties

are: industrial park, logistics and production- &

logistics, which are defined by the DIR as general

categories.

Type Offers Percentage Asking Price vol. in m€ Area in m²

Industrial Park 60 15.7 % 356.3 725,954

Logistics 82 24.1 % 545.5 834,541

Production & logistics 197 60.2 % 1,362.5 2,536,450

Total 339 100.0 % 2,264.3 4,096,945

The analysis shows an excess of offers of production

& logistics real estate (> 60 %), subject to the signifi-

cant market share of German corporate real estate.

Despite the excess in offers for assets in production,